11email: v.mavroudis@cs.ucl.ac.uk

Market Manipulation as a Security Problem

Abstract

Order matching systems form the backbone of modern equity exchanges, used by millions of investors daily. Thus, their operation is strictly controlled through numerous regulatory directives to ensure that markets are fair and transparent. Despite these efforts, market manipulation remains an open problem.

In this work, we focus on a class of market manipulation techniques that exploit technical details and glitches in the operation of the exchanges (i.e., mechanical arbitrage). Such techniques are used by predatory traders with deep knowledge of the exchange’s structure to gain an advantage over the other market participants. We argue that technical solutions to the problem of mechanical arbitrage have the potential to significantly thwart these practices. Our work provides the first overview of the threat landscape, models fair markets and their security assumptions, and discusses various mitigation measures.

1 Introduction

From outcry pits to electronic exchanges, trading has always been a very competitive field, where even the slightest “edge” could be used to gain an advantage over the rest of the market participants. However, electronic trading gave rise to a previously unseen type of arbitrage that exploits minor technical details and glitches in the exchange’s infrastructure [18].

These techniques are employed by traders with a very good understanding of the exchange’s operations (e.g., matching system’s processes, order handling rules) and usually with low-latency access to the exchange’s engine (on the order of milliseconds or less). For example, traders have been found to exploit corner cases of the order-handling rules to unfairly receive execution priority over other market participants [14]. Moreover, predatory traders use minuscule orders to uncover investors who submit hidden instructions for large blocks of equity [18, 17].

While in retrospect this development was to be expected, the prevalence of such techniques caught markets off-guard, and led to various analyses and proposals by both researchers and regulatory bodies [11]. Our work complements these (legal and finance) research efforts and argues that these phenomena cannot be sufficiently studied without examining their technical component. We decouple the study of manipulation techniques from their legal standing, and model fair exchanges based on security properties and assumptions derived from EU and US market regulations. On this basis, we examine six known mechanical manipulation techniques and investigate how they violate one or more of the aforementioned properties. The insights of this analysis are useful for the development of efficient countermeasures with minimum impact to the operation of the markets.

To better understand the existing mitigation options and their effectiveness, we also discuss and compare various technical and regulatory proposals. We conclude that technical countermeasures cannot fully replace regulators but can significantly reduce the opportunities for manipulation. This is also indicated by the small body of works introducing alternative market designs that are less prone to certain forms of mechanical arbitrage [36, 20, 18].

Contributions. To summarize, this paper makes the following contributions:

-

•

We define the security properties that fair exchanges should satisfy and introduce the adversarial model assumed by the majority of modern equity exchanges.

-

•

We study six known manipulation techniques, introduce their technical details, and investigate how they violate the exchange’s security properties. To our knowledge, this is the first time that market manipulation techniques are studied in the “systems security” context.

-

•

We survey existing countermeasures and discuss their effectiveness in tackling manipulation techniques based on mechanical arbitrage.

The rest of the paper is organized as follows: Initially, we detail the operation of order matching systems and discuss the different order types (Section 2). Subsequently, we list the basic security properties that a fair exchange should provide, and introduce a realistic model of an intelligent adversary (Section 3). Section 4 studies the technical details of mechanical arbitrage techniques, while Section 5 discusses both technical and regulatory countermeasures. Section 6 concludes the paper.

2 Background

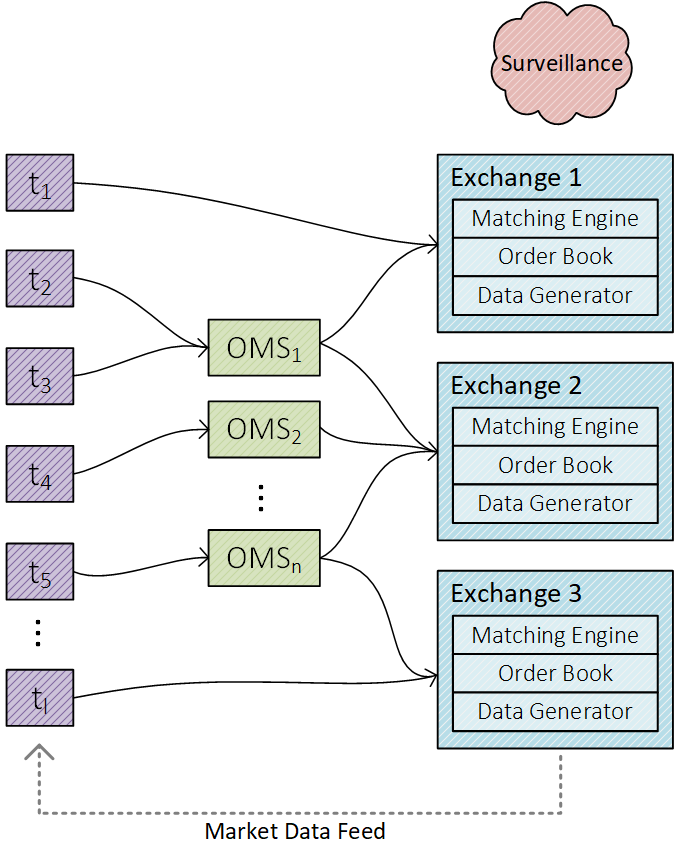

We now outline the basic subsystems of electronic exchanges and their operation. Figure 1 illustrates the interactions between the different components and actors of an electronic trading system. Initially, traders () submit their instructions (i.e., send, cancel, modify) to the order management system (OMS) of their broker. The OMS captures the details of each incoming instruction, identifies the best execution venue, and routes it to that exchange111In practice, order routing is more complex, and optimal execution in a volatile market is non-trivial [25].. The received orders are then placed in the exchange’s order book, where the matching engine ranks, pairs and fills them with other sell or buy orders. An order is fully matched and cleared from the book if its entire open quantity is executed, while partially matched orders are updated to list only the remaining open quantity. Most equity and cryptocurrency exchanges operate continuous markets, where orders are matched on a continuous basis and the price is determined by the highest bid and the lowest ask quotes.

Traders remain up to date with these prices either through the Stock Information Provider (SIP)222The Stock Information Provider is a central, consolidated stream and aggregator displaying the best priced bid and ask quotes, and the trading activity of each exchange. or by subscribing to the trading data feeds offered by the exchanges. There are two types of such feeds: Layer 1 that provide only basic information such as real-time best bid/ask prices for securities trading in the exchange, and Layer 2 that offer quotes for all the orders resting in the order book (or up to a certain depth). In terms of latency, SIP averages at 0.09 milliseconds, while proprietary data feeds are several times faster [30].

Finally, to ensure that traders, brokers and exchanges operate within the legal boundaries, regulators (e.g., the U.S. Securities and Exchange Commission) constantly surveil the market and investigate cases of abuse such as market manipulation and insider trading. Moreover, exchanges often monitor and review trader positions and transactions (i.e., self-regulate) to avoid facilitating illegal activities [5, 6, 7].

Dark pools are trading venues that protect the traders’ privacy by not advertising the open orders in their book. Pre-trade privacy is of great importance to institutional investors, as it enables them to submit large orders without adversely influencing the market price. Beside that, their operation is similar to that of standard exchanges (i.e., lit markets). Dark pools were initially used for equity trading, but the recent cryptocurrency burst gave rise to various new dark coin-trading venues [40].

2.1 Orders Types

Trade orders are instructions sent by traders/investors to buy or sell on a venue, and are either routed through a broker or sent directly to the exchange (when participants have direct market access). We now outline a few of the hundred order types (and variants) that modern exchanges support.

Market Orders. This order type specifies the quantity to be sold or bought, but not the price. The exchange is responsible for filling the order at the best available price. While market orders are commonly used to quickly unload a “position”, traders prefer other types that give them better control over the execution price.

Limit Orders. A limit order specifies a maximum or minimum price for buying or selling a number of shares. Unlike market orders, limit orders may not be executed if the price set cannot be met. Some variants allow investors to place time-limits for order execution after which the order is canceled.

Reserve Orders. Such orders are comprised of a displayed and a reserved (i.e., non-displayed) component (also called Iceberg orders). Once the displayed quantity is depleted to less than a round lot (i.e., the smallest order size allowed) the reserved component is used to replenish it. There are several variants realizing different replenishment strategies (e.g., fixed amount, random replenishment).

Discretionary Orders. This type of orders have both a displayed price and a non-displayed discretionary execution range. The exchange first tries to fill the order at the displayed price, but if this is not possible it looks for fills within the hidden discretionary range.

Anonymous Orders. These orders are used by investors who elect not to reveal their identity in a particular trade. Anonymous orders display a generic id in place of the unique participant’s id. Regulators and authorities monitoring the market retain access to the full details of the order.

Dark/Hidden Orders. This class of orders provides varying degrees of pre-trade privacy, concealing parts of or all the details of an order before it is executed. They are available in both dark and lit markets and are used by investors wishing to buy or sell large volumes of stocks, options, or cryptocurrencies without influencing the market direction or sentiment. It should be noted that they do not provide any post-trade privacy, as this is prohibited by EU and US market regulations.

2.2 Order Matching Algorithms

Order matching is the process by which exchanges pair compatible buy and sell instructions. For this purpose, each matching system uses an algorithm that considers several precedence criteria to determine which orders must be filled at any given time. This ranking process becomes of particular importance, when there are several open orders for the same security (or cryptocurrency) at the same price. Here, we outline the two most common categories of matching algorithms, while a more thorough analysis can be found in [29].

Price-Time Priority. Most equity and cryptocurrency markets use Time-based FIFO ranking. FIFO is an intuitive ranking strategy, where orders are first prioritized based on their offered price (i.e., a buyer that is willing to pay more is served first) and then based on their relative submission time (in cases of orders with the same price). For instance, given a buy order A for shares at a price that arrives before an order B for shares at the same price, the system will seek to fully fill A first, and then move on to find matches for B. Conditional order types further complicate the ranking process, as ranking algorithms need to also consider several other order precedence rules. For example, displayed orders (e.g., limit orders) have priority over all hidden order types (e.g., dark orders). Similarly, other ranking criteria are used to rank the different hidden order variants.

Pro-Rata. As with price-time priority, Pro-Rata algorithms prioritize first the orders that offer the best price, but do not consider their relative submission time. Instead, they split the quantity sold between the buy orders at the same price level i.e., The volume of the shares allocated to each buy order is proportional to the number of available shares currently available at that price. In our previous scenario, with two buy orders A (for 200 shares) and B (50 shares) at the same price, an incoming sell order for 200 shares will be matched with 160 shares from A and 40 shares from B (i.e., 80% of each). In other words, if the offer does not suffice to cover the demand, all orders will be filled partially[12, 27]. Besides this basic version of the pro-rata algorithm, there are several other variants with additional constraints such as maximum volume caps and minimum volume thresholds.

3 Security Considerations

We now examine market regulations to derive the security properties of modern exchanges and the threat model they operate under. We base our analysis primarily on literature for the US and EU markets, but our modeling remains relevant to exchanges worldwide.

3.1 Security Properties

In 2005, the U.S. Securities and Exchange Commission (SEC) consolidated all pre-existing equity market regulations into the Regulation National Market System [1], aiming to simplify market surveillance and increase investor protection. In the European Union, the “Markets in Financial Instruments Directive” (MiFID II) provides a regulatory framework for investment services [2]. Based on these two regulations, we introduce a list of properties that, we believe, provide a well-rounded definition of fair and transparent markets. Comprehensive overviews of the U.S. Regulatory Landscape can be found in [36, 14].

-

•

Trading Integrity. All the orders entered by market participants should express honest trading intent, and should not be used to artificially influence the volume of trades, the prices or any other market activity index.

-

•

Operational Transparency. All the details and rules governing the operation of an exchange should be accessible by all market participants.

-

•

Fair Market Access. All market participants should have equal access to the exchange when sending, modifying and canceling orders.

-

•

Symmetric Information Access. All market participants should have equal access to up-to-date data on exchange’s order book activity.

-

•

Order Queue Integrity. Orders should be always ranked and executed according to the public order-matching rules of the exchange.

-

•

Participant Anonymity. Non-authorized parties should not have access to the identity of traders using anonymous orders.

-

•

Data Confidentiality. Non-authorized parties should not have access to the pre-trade data of dark orders. In the case of dark pools, other traders should not have access to any information related to a transaction (apart from the buyer and the seller).

The US and European market regulations assume that the majority of traders and exchange operators abide by the regulations, but may occasionally violate one or more of the above properties even if it is explicitly prohibited by the law. Additionally, investors assume that other traders and exchange operators may operate in a legal but unethical manner (e.g., predatory trading).

3.2 Adversarial Model

While in theory all traders have the same access to the market, the complexity of modern exchanges provides various opportunities for gaining competitive edges. We now outline the main characteristics of intelligent traders that make optimal use of their resources without overstepping any legal boundaries [18, 10, 34, 28, 31, 35]:

-

•

High Computational Power. They heavily and continuously invest in computer hardware and software, so as to process market data and execute orders as fast as possible.

- •

-

•

Knowledgeable & Strategic. They have a very good understanding of the exchange’s internal processes and systems, and make optimal use of order types to leverage every (intended and unintended) feature they provide.

4 Manipulation Techniques

We now describe several market manipulation techniques that exploit the underlying infrastructure of exchanges and violate one or more of the properties listed in Section 3.1.

As part of a complex exploitation strategy, predatory traders often use attacks to: 1) deanonymize investors entering anonymous orders, and 2) uncover large hidden orders.

Latency Fingerprinting. This class of deanonymization techniques uses the order-transmission latency as a side-channel to uncover the identity of investors that use anonymous orders (i.e., violates the Participant Anonymity property). The adversary maintains a latency table that maps the different brokers/funds to the time it takes for a message to reach the exchange from their network [8, 37]. Upon observing an anonymous order and calculating its inter-arrival time, the adversary uses the latency table to identify the broker that submitted it. From a technical perspective, the transmission latency of an anonymous order is retrieved by subtracting the “submission” timestamp (found in each Financial Information eXchange Protocol message333http://www.fixprotocol.org/) from the time the order was listed in the order book of the exchange.

Pinging. As outlined in Section 2.1, investors placing large orders often elect to use hidden order types to avoid influencing the market price and falling prey to predatory practices. These orders are not displayed in the order book and are matched only if another order at the same price is submitted. Alternatively, investors often break up large buy orders into much smaller ones and enter them gradually into the market [10]. Pinging is one of the techniques used by predatory traders to uncover such investors, and is particularly effective in exchanges that send order execution notifications immediately and market activity updates at regular downsampled intervals. The trader enters several sell orders of the smaller marketable size for the stocks they are interested in monitoring. Once one or more of those orders are matched, the trader is alerted (i.e., pinged) about the presence of a potentially large hidden buy-side order. This technique violates the Data Confidentiality property and is usually combined with other techniques that exploit large buy orders (e.g., scalping).

Quote stuffing. This technique is used only by sophisticated traders with direct access to the market (i.e., not through a broker), and involves placing and canceling high volumes of orders. Its objective is to disrupt trading and create arbitrage opportunities by flooding the data feeds of other participants, who are now unable to follow the market (Symmetric Information Access property) [24]. Thus, it exploits bottlenecks in the data processing pipeline of regular investors. In some cases, these attacks may also affect the responsiveness of the matching engine to market participants [33, 39].

Sniping. Sniping [18] is a form of mechanical arbitrage that relies on high-speed transmission lines and co-location to gain an edge over slower investors. Let a cryptocurrency or security traded on an exchange at price and a public signal y that is strongly correlated to . Consequently, when increases, traders immediately update their open sell quotes for that security from to a new increased price . However, this process is not instantaneous and hence momentarily (i.e., a few milliseconds) there are open sell quotes at the stale price . Predatory traders with high-speed connections exploit this delay, and submit buy orders at that old price. With non-trivial probability [31], some of their buy orders get filled at , thus allowing them to immediately sell the security back for , risk-free [18]. This practice breaches the Fair Market Access property and has been also observed in dark pools [8].

Scalping. This technique relies on very low-latency network links, violates Fair Market Access property, and is usually combined with market snooping techniques (e.g., pinging to identify large buy orders). Let a broker handling a large buy order for 100,000 shares of company Z. Upon examining the order books of all exchanges, the broker finds 60,000 in exchange and 40,000 shares in exchange , both at price x. The broker submits a buy order for 100,000 shares to and gets a partial fill for 60,000 at x. This also triggers a “ping” order set by a predatory trader, informing them that a large order for Z is in the market (see also “Pinging”). Following the order protection rule444The Order Protection Rule of Regulation NMS (Rule 611) introduced the National Best Bid and Offer requirement that protects investors from receiving sub-optimal prices for their quotes. In particular, Rule 611 mandates that exchanges should either reject marketable orders or route them to the exchange with the best price., now routes the order to exchange to buy the remaining 40,000 shares at price x. However, the predatory trader utilizing its lower network latency, has already executed a buy order in for all available shares of Z at price x. When the broker’s buy order for 40,000 share arrives to (a few milliseconds after), the trader matches it with a sell order at a slightly inflated price [8].

Queue Jumping. While initially speed was sufficient for predatory traders to place their orders ahead of other market participants, the influx of technically advanced investors caused this practice to lose its effectiveness. To maintain their edge, predatory traders started using more sophisticated techniques that rely on special (i.e., “exotic”) order types, allowing them to jump at the top of the queue555Orders that are closer to the top of the order book have access to more liquidity and better prices [23]., even if their order was not the first to enter the market.

In theory, these order types were accessible to all market participants and thus everyone could bump up the priority of their orders. However, in many cases exchange operators selectively disclosed them only to a subset of their clients and failed to inform everyone else about their existence and operation (Operational Transparency property) [4, 19, 14, 3]. Nevertheless, these order types were exploitable only by sophisticated traders with knowledge of the precedence rules, very low-latency links and high processing power.

Hide & Light Orders is one of the most controversial order types. It was introduced as a workaround to Rule 610(d) of Regulation NMS [1], which prohibits orders that lock666A buy order at price in an exchange locks the market, if there is another sell order for the same price in another exchange [33]. or cross777A market is crossed if a buy order is posted at a price that is higher than the best (lowest) existing sell order, or inversely if a sell order is posted at a price lower than the best (highest) bid [33] the National Best Bid and Offer888The NBBO index is updated throughout the day with the lowest selling price and the highest buying bid (from all US exchanges) in order to ensure that investors receive the best possible price. To abide by this rule, exchanges temporarily adjust the price of the locking/crossing orders to be a tick (i.e., the minimum price movement) lower/higher than the NBBO, for as long as the market remains locked. Once the market unlocks, the prices are slid back to their original values. However, this does not apply to Hide & Light orders, which retain their original price and are instead switched to being hidden (i.e., non-displayed). Once the market unlocks, they are automatically lighten up again. This seemingly subtle difference corrupted the price-time priority of the queue, as lighten-up orders where placed in front of price-adjusted orders regardless of their relative ranking before the lock.

Day Intermarket Sweep Orders is another controversial order type, which is prioritized over all other types, including Hide & Light orders999This prioritization rule concerns only the first Day ISO to enter the market and every subsequent Day ISO receives standard arrival time priority [14].. Day ISOs are based on a special exception in the Regulation NMS and are executed immediately without verifying if they lock or cross the market (the trader assumes all the regulation compliance liability). While their original motivation was to help institutional investors place large orders without chasing liquidity throughout the market, Day ISOs were quickly proven exploitable by predatory traders. In particular, ISOs were used by sophisticated traders with high-speed market activity feeds to rapidly react to market events, and place themselves ahead of regular investors that: 1) did not use Day ISOs, and 2) relied on the slow Stock Information Provider\footrefsip to find the NBBO.

5 Countermeasures

Market regulation is an obvious measure of protection against predatory traders and manipulation practices. Until now, there have been several incidents where market operators and traders were accused of wrongdoing and settled to pay penalties [4, 3, 36, 20]. However, keeping up with the latest manipulation practices, trading styles, market mechanisms, and distinguishing malicious-intent from irrational behavior is far from trivial [13, 38]. For this reason, a small body of work has proposed and, in some cases, deployed technical countermeasures that aim to prevent all or some of these practices. These countermeasures do not seek to replace regulators, but aim to alleviate or at least reduce the opportunities for mechanical arbitrage.

As discussed in Section 4, many of the manipulation techniques require that the trader can submit, alter and cancel orders within a few milliseconds. For this reason, several exchanges introduced “speed-bumps” that delay the incoming orders and outgoing messages by a predefined amount of time. For example, the Investors Exchange (IEX) and the Toronto Stock Exchange (TSX) use “speed-bumps” that introduce delay of 350 microseconds [16] and 1–3 milliseconds respectively [21, 15]. So far, “speed-bumps” have shown promising results in thwarting manipulation techniques that rely on low latency. However, studies are not yet conclusive regarding their effects on the market [21]. Similarly, [18] introduces an alternative market design that uses discrete time instead of continuous. The authors argue that this design stops the arms race for speed and eliminates the risk-less latency-based arbitrage opportunities. While most of the countermeasures require changes to the market design, there are certain steps that investors can take to protect themselves from specific attacks. For example, “latency tables” (Section 4) can be mitigated by adding noise on the timestamp of the submitted instructions.

Due to the above efforts, the rising infrastructure costs and the diminishing returns, high frequency (i.e., very low-latency) trading activity has been steadily declining in the past few years [26]. Simultaneously, markets for other financial assets (e.g., currencies) have seen an increase in low-latency activity [9, 26].

6 Conclusions & Future Work

This work aims to shed light on the technical aspects of market manipulation and to highlight the relevance of security analysis techniques and secure engineering principles to that problem. Toward this goal, we introduced a set of basic fairness properties, and used them to examine different market manipulation techniques and their mitigation counterparts. It is our hope that this new research direction will complement the legislative efforts for fair and transparent markets. While we focused on stock exchanges, future research could also investigate the risks that the average investor faces in unregulated cryptocurrency exchanges and decentralized trading platforms.

References

- [1] Regulation NMS, Release No. 34-51808. Securities and Exchange Commission (2005), https://www.sec.gov/rules/final/34-51808.pdf

- [2] Directive 2004/39/ec on markets in financial instruments. The European Parliament and the Council of the European Union, https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:02004L0039-20060428 (2006)

- [3] Report 331: Dark liquidity and high-frequency trading. Australian Securities and Investments Commission (2013), https://download.asic.gov.au/media/1338878/info178-published-15-January-2014.pdf

- [4] In the Matter of UBS Securities LLC, Exchange Act Release No. 74060. United States of America before the Securities and Exchange Commission (2015), https://www.sec.gov/litigation/admin/2015/33-9697.pdf

- [5] Disciplinary actions. IEX Group Inc, https://iextrading.com/regulation/disciplinary-actions (2018)

- [6] Disciplinary actions. NASDAQ Trader (2018), https://www.nasdaqtrader.com/Trader.aspx?id=NDisciplinaryActions

- [7] Disciplinary actions. New York Stock Exchange, Intercontinental Exchange, Inc (2018), https://www.nyse.com/regulation/disciplinary-actions

- [8] Adrian, J.: Informational inequality: How high frequency traders use premier access to information to prey on institutional investors. Duke L. & Tech. Rev. 14, 256 (2016)

- [9] Aggarwal, R.K., Wu, G.: Stock market manipulation-theory and evidence. In: AFA 2004 San Diego Meetings (2003)

- [10] Aldridge, I.: High-frequency trading: a practical guide to algorithmic strategies and trading systems, vol. 604. John Wiley & Sons (2013)

- [11] Angel, J.J., McCabe, D.: Fairness in financial markets: The case of high frequency trading. Journal of Business Ethics 112(4), 585–595 (2013)

- [12] Aspris, A., Foley, S., Harris, D., O’Neill, P.: Time pro-rata matching: Evidence of a change in liffe stir futures. Journal of Futures Markets 35(6), 522–541 (2015)

- [13] Banks, E.: Dark pools: The structure and future of off-exchange trading and liquidity. Springer (2010)

- [14] Bodek, H.: The Problem of HFT: Collected Writings on High Frequency Trading & Stock Market Structure Reform. Decimus Capital Markets LLC, Norwalk, CT (2013)

- [15] Brown, A., Yang, F., et al.: Adverse selection, speed bumps and asset market quality. Tech. rep. (2015)

- [16] Buchanan, M.: Physics in finance: Trading at the speed of light. Nature News 518(7538), 161 (2015)

- [17] Budish, E., Cramton, P., Shim, J.: Implementation details for frequent batch auctions: Slowing down markets to the blink of an eye. American Economic Review 104(5), 418–24 (2014)

- [18] Budish, E., Cramton, P., Shim, J.: The high-frequency trading arms race: Frequent batch auctions as a market design response. The Quarterly Journal of Economics 130(4), 1547–1621 (2015)

- [19] Buti, S., Consonni, F., Rindi, B., Werner, I.M.: Sub-penny and queue-jumping (2013)

- [20] Cartlidge, J., Smart, N.P., Alaoui, Y.T.: MPC joins the dark side. IACR Cryptology ePrint Archive 2018, 1045 (2018), https://eprint.iacr.org/2018/1045

- [21] Chakrabarty, B., Huang, J., Jain, P.K.: Exchange competition with levelled speed (2018)

- [22] Clarke, T.: High-frequency trading and dark pools: sharks never sleep. Law and Financial Markets Review 8(4), 342–351 (2014)

- [23] Cont, R., Kukanov, A., Stoikov, S.: The price impact of order book events. Journal of financial econometrics 12(1), 47–88 (2014)

- [24] Egginton, J.F., Van Ness, B.F., Van Ness, R.A.: Quote stuffing. Financial Management 45(3), 583–608 (2016)

- [25] Foucault, T., Menkveld, A.J.: Competition for order flow and smart order routing systems. The Journal of Finance 63(1), 119–158 (2008)

- [26] Goldstein, M.A., Kumar, P., Graves, F.C.: Computerized and high-frequency trading. Financial Review 49(2), 177–202 (2014)

- [27] Guilbaud, F., Pham, H.: Optimal high-frequency trading in a pro rata microstructure with predictive information. Mathematical Finance 25(3), 545–575 (2015)

- [28] Hasbrouck, J., Saar, G.: Low-latency trading. Journal of Financial Markets 16(4), 646–679 (2013)

- [29] Janecek, K., Kabrhel, M.: Matching algorithms of international exchanges. Tech. rep., Citeseer (2007)

- [30] Jones, C.M.: Understanding the market for us equity market data. Tech. rep. (2018)

- [31] Kirilenko, A., Kyle, A.S., Samadi, M., Tuzun, T.: The flash crash: High-frequency trading in an electronic market. The Journal of Finance 72(3), 967–998 (2017)

- [32] Laughlin, G., Aguirre, A., Grundfest, J.: Information transmission between financial markets in chicago and new york. Financial Review 49(2), 283–312 (2014)

- [33] McNamara, S.: The law and ethics of high-frequency trading. Minn. JL Sci. & Tech. 17, 71 (2016)

- [34] Menkveld, A.J.: High frequency trading and the new market makers. Journal of Financial Markets 16(4), 712–740 (2013)

- [35] Pagnotta, E.S., Philippon, T.: Competing on speed. Econometrica 86(3), 1067–1115 (2018)

- [36] Parkes, D.C., Thorpe, C., Li, W.: Achieving trust without disclosure: Dark pools and a role for secrecy-preserving verification (2015)

- [37] Sannikov, Y., Skrzypacz, A., et al.: Dynamic trading: Price inertia and front-running (2016)

- [38] Söderström, R.: Regulating Market Manipulation: An Approach to designing Regulatory Principles. Juridiska fakulteten, Uppsala universitet (2011)

- [39] Xie, J.: Criminal regulation of high frequency trading on China’s capital markets. International Journal of Law, Crime and Justice 47, 106–120 (2016)

- [40] Zhang, T., Wang, L.: Republic protocol: A decentralized dark pool exchange providing atomic swaps for ethereum-based assets and bitcoin (2017), https://github.com/republicprotocol/whitepaper/raw/master/republic-whitepaper.pdf