Optimal Reinsurance and Investment in a Diffusion Model

Abstract

We consider a diffusion approximation to an insurance risk model where an external driver models a stochastic environment. The insurer can buy reinsurance. Moreover, investment in a financial market is possible. The financial market is also driven by the environmental process. Our goal is to maximise terminal expected utility. In particular, we consider the case of SAHARA utility functions. In the case of proportional and excess-of-loss reinsurance, we obtain explicit results.

Keywords: Optimal reinsurance; optimal investment; Hamilton–Jacobi–Bellman equation; SAHARA utility; proportional reinsurance; excess-of-loss reinsurance

Classification: Primary 91B30; secondary 60G44; 60J60; 93E20.

1 Introduction

The optimal reinsurance-investment problem is of large interest in the actuarial literature. A reinsurance is a contract whereby a reinsurance company agrees to indemnify the cedent (i.e. the primary insurer) against all or part of the future losses that the latter sustains under the policies that she has issued. For this service the insurer is asked to pay a premium. It is well known that such a risk-sharing agreement allows the insurer to reduce the risk, to increase the business capacity, to stabilise the operating results and so on. In the existing literature there are a lot of works dealing with the optimal reinsurance strategy, starting from the seminal papers [4], [2] and [6]. During the last decades two different approaches were used to study the problem: some authors model the insurer’s surplus as a jump process, others as a diffusion approximation (see e.g. [16] and references therein for details about risk models). In addition, only two reinsurance agreements were considered: the proportional and the excess-of-loss contracts (or both, as a mixed contract). Among the optimization criteria, we recall the expected utility maximization (see [9], [8] and [11]), ruin probability minimization (see [12], [13] and [14]), dividend policy optimization (see [2] and [15]) and others. In particular, the former was developed only for CRRA and CARA utility functions.

Our aim is to investigate the optimal reinsurance problem in a diffusion risk model when the insurer subscribes a general reinsurance agreement, with a retention level . The insurer’s objective is to maximise the expected utility of the terminal wealth for a general utility function , satisfying the classical assumptions (monotonicity and concavity). That is, we do not assume any explicit expression neither for the reinsurance policy nor for . However, we also investigate how our general results apply to specific utility functions, including CRRA and CARA classes, and to the most popular reinsurance agreements such as proportional and excess-of-loss.

One additional feature of our paper is that the insurer’s surplus is affected by an environmental factor , which allows our framework to take into account size and risk fluctuations (see [7, Chapter 2]). We recall two main attempts of introducing a stochastic factor in the risk model dynamic: in [10] the authors considered a Markov chain with a finite state space, while in [1] is a diffusion process, as in our case. However, they considered jump processes and the rest of the model formulation is very different (for instance, they restricted the maximization to the exponential utility function and the proportional reinsurance). Moreover, in those papers only affects the insurance market.

Indeed, another important peculiarity of our model is the dependence between the insurance and the financial markets. We allow the insurer to invest her money in a risky asset, modelled as a diffusion process with both the drift and the volatility influenced by the stochastic factor . From the practical point of view, this characteristic reflects any connection between the two markets. From the theoretical point of view, we remove the standard assumption of the independence, which is constantly present in all the previous works, especially because it simplifies the mathematical framework.

The paper is organized as follows: in the following section we formulate our optimal stochastic control problem; next, in Section 3 we analyse the main properties of the value function, while in Section 4 we characterize the value function as a viscosity solution to the Hamilton-Jacobi-Bellman (HJB) equation associated with our problem; in Section 5 we apply our general results to the class of SAHARA utility functions, which includes CRRA and CARA utility functions as limiting cases. In addition, we characterize the optimal reinsurance strategy under the proportional and the excess-of-loss contracts, also providing explicit formulae. Finally, in Section 6 we give some numerical examples.

2 The Model

The surplus process of an insurer is modelled as the solution to the stochastic differential equation

where is an environmental process, satisfying

and is the reinsurance retention level of the insurer at time . We assume that is a cadlag process and can take all the values in an interval , where and that the functions , , and are continuously differentiable bounded functions satisfying a Lipschitz condition uniformly in . Further, the insurer has the possibility to invest into a risky asset modelled as the solution to

Also the functions , and are assumed to be bounded continuous positive functions satisfying a Lipschitz condition. We further assume that is bounded away from zero. Here, , , are independent Brownian motions on a reference probability space . Thus, the reinsurance strategy does not influence the behaviour of the risky asset. But, the surplus process and the risky asset are dependent. Choosing an investment strategy , the surplus of the insurer fulfils

In order that a strong solution exists we assume that . Our goal is to maximise the terminal expected utility at time

and, if it exists, to find the optimal strategy . That is,

where the supremum is taken over all measurable adapted processes such that the conditions above are fulfilled. is a utility function. That is, is strictly increasing and strictly concave. We make the additional assumption that is continuous. The filtration is the smallest complete right-continuous filtration such that the Brownian motions are adapted. In particular, we suppose that is observable.

We will also need the value functions if we do start at time instead. Thus we define

where we only consider strategies on the time interval and, analogously, . The boundary condition is then . Because our underlying processes are Markovian, depends on via only.

3 Properties of the value function

Lemma 1.

-

i)

The value function is increasing in .

-

ii)

The value function is continuous.

Proof.

That the value function is increasing in is clear. By Itô’s formula

Because the stochastic integrals are martingales by our assumptions

Taking the supremum over the strategies we get the continuity by the Lipschitz assumptions. ∎

Lemma 2.

The value function is concave in .

Proof.

If the value function was not concave, we would find and a test function with , and for all , , and . By the proof of Theorem 1 below,

But it is possible to choose such that the above inequality does not hold. ∎

4 The HJB equation

We expect the value function to solve

| (1) | |||||

A (classical) solution is only possible if . In this case,

| (2) |

Thus, we need to solve

| (3) | |||||

By our assumption that and are continuous functions on a closed interval of the compact set , there is a value at which that supremum is taken.

Theorem 1.

The value function is a viscosity solution to (1).

Proof.

Without loss of generality we only show the assertion for . Choose and . Let and . Consider the following strategy. for , and for some strategy , such that . Note that the strategy can be chosen in a measurable way since is continuous. Let be a test function, such that with . Then by Itô’s formula

Note that the integrals with respect to the Brownian motions are true martingales since the derivatives of are continuous and thus bounded on the (closed) area, and therefore the integrands are bounded. Taking expected values gives

The right hand side does not depend on . We thus can let . This yields

It is well known that tends to zero as . Thus, letting gives

Since is arbitrary,

Let now be a test function such that and . Then there is a strategy , such that . Choose a localisation sequence , such that

| and | ||||

are martingales, where as above, . We have

Because we consider a compact interval, we can let and obtain by bounded convergence

This gives by dividing by and letting

This proves the assertion. ∎

Let now and be the maximiser in (1). By [17, Sec. 7] we can choose these maximisers in a measurable way. We further denote by and the feedback strategy.

Theorem 2.

Suppose that is a classical solution to the HJB equation (1). Suppose further that the strategy admits a unique strong solution for and that is uniformly integrable. Then the strategy is optimal.

Proof.

By Itô’s formula we get for

Thus, is a local martingale. From and the uniform integrability we get that is a martingale. We therefore have

This shows that the strategy is optimal. ∎

Corollary 1.

Suppose that is a classical solution to the HJB equation (1). Suppose further that the strategy admits a unique strong solution for and that . Then the strategy is optimal.

Proof.

Since the parameters are bounded, the condition implies uniform integrability of . The result follows from Theorem 2. ∎

5 SAHARA utility functions

In this section we study the optimal reinsurance-investment problem when the insurer’s preferences are described by SAHARA utility functions. This class of utility functions was first introduced by [3] and it includes the well known exponential and power utility functions as limiting cases. The main feature is that SAHARA utility functions are well defined on the whole real line and, in general, the risk aversion is non monotone.

More formally, we recall that a utility function is of the SAHARA class if its absolute risk aversion (ARA) function admits the following representation:

| (4) |

where is the risk aversion parameter, the scale parameter and the threshold wealth.

Let us try the ansatz

| (5) |

Remark 1.

By (2) and (5), the optimal investment strategy admits a simpler expression:

| (6) |

In particular, is bounded by a linear function in and therefore our assumption is fulfilled. Under our hypotheses, if the HJB equation admits a classical solution, the assumptions in Corollary 1 are satisfied. Let us note that is influenced by the reinsurance strategy .

In this case (3) reads as follows:

where

| (7) |

By our assumptions, is continuous in , hence it admits a maximum in the compact set . However, we need additional requirements to guarantee the uniqueness.

Lemma 3.

If is concave in and is non negative and convex in , then there exists a unique maximiser for .

Proof.

We prove that is the sum of two concave functions, hence it is concave itself. As a consequence, there exists only one maximiser in . Now, since is strictly concave by hypothesis, we only need to show that

is convex in . We know that this quadratic form is convex and increasing when the argument is non negative. Recalling that by hypothesis, we can conclude that the function above is convex, because it is the composition of a non decreasing and convex function with a convex function ( is so, by assumption). The proof is complete. ∎

Remark 2.

Uniqueness is not necessary. If is not unique, we have to choose a measurable version in order to determine an optimal strategy.

5.1 Proportional reinsurance

Let us consider the diffusion approximation to the classical risk model with non-cheap proportional reinsurance, see e.g. [15, Chapter 2]. More formally,

| (8) |

with and . Here . From the economic point of view, the insurer transfers a proportion of her risks to the reinsurer (that is corresponds to full reinsurance). In this case, by (7) our optimization problem reduces to

| (9) |

The optimal strategy is characterized by the following proposition.

Proposition 1.

Under the model (8), the optimal reinsurance-investment strategy is given by , with

| (10) |

where

and

| (11) |

Proof.

The expression for can be readily obtained by (6). By Lemma 3, there exists a unique maximiser for , where is defined in (7) replacing and . Now we notice that

therefore full reinsurance is optimal. On the other hand,

hence in this case null reinsurance is optimal. Now let us observe that

which implies . Finally, when , the optimal strategy is given by the unique stationary point of . By solving , we obtain the expression in (10). ∎

Remark 3.

The previous result holds true under the slight generalization of , , dependent on time and on the environmental process. In this case, there will be an additional effect of the exogenous factor .

Proposition 1 also holds in the case of an exponential utility function.

Corollary 2.

For with , the optimal strategy is given by , with

| (12) |

where

and

| (13) |

Proof.

By definition of the ARA function, the exponential utility function corresponds to the special case . Hence, we can apply Proposition 1, by replacing the ARA function. All the calculations remain the same, but the optimal strategy will be independent on the current wealth level . ∎

5.2 Excess-of-loss reinsurance

Now we consider the optimal excess-of-loss reinsurance problem. The retention level is chosen in the interval and for any future claim the reinsurer is responsible for all the amount which exceeds that threshold . For instance, corresponds to no reinsurance. The surplus process without investment is given by, see also [5]

| (14) |

where are the reinsurer’s and the insurer’s safety loadings, respectively, and is the tail of the claim size distribution function. In the sequel we require and, for the sake of the simplicity of the presentation, that . Notice also that it is usually assumed . However, we do not exclude the so called cheap reinsurance, that is .

By (7), we obtain the following maximization problem:

| (15) | |||||

Proposition 2.

Proof.

We first note that, using L’Hospital’s rule,

The derivative with respect to of the function in (15) is

Consider the expression between brackets

| (18) |

Since , we see that for any the function in (15) is strictly decreasing. Thus in this case. For we obtain by L’Hospital’s rule,

This implies that the function to be maximised increases close to zero. In particular, the maximum is not taken at zero. Further, if , then (18) tends to as . If , then

Thus also in this case, (18) tends to as . Thus the maximum is taken in , and uniqueness of is guaranteed by the concavity. Now the proof is complete. ∎

Corollary 3.

The main assumption of Proposition 2, that is the concavity of the function in (15), may be not easy to verify. In the next result we relax that hypothesis, only requiring the uniqueness of a solution to equation (17).

Proposition 3.

Proof.

In the proof of Proposition 2 we only used the concavity to verify uniqueness of the maximiser. Therefore, the same proof applies. ∎

5.3 Independent markets

Suppose that the insurance and the financial markets are conditionally independent given . That is, let . Then by (6) we get

Remark 4.

Suppose that as usual. The insurer invests a larger amount of its surplus in the risky asset when the financial market is independent on the insurance market. Indeed, the reader can easily compare the formula above with (6).

Regarding the reinsurance problem, by (7) we have to maximise this quantity:

Proposition 4.

Suppose that is strictly concave in . Then the optimal reinsurance strategy admits the following expression:

| (19) |

where

and is the unique solution to

Proof.

Since is continuous in , it admits a unique maximiser in the compact set . The derivative is

If , then and is decreasing in , because it is concave; hence is optimal . Now notice that , because of the concavity of . If , then and is increasing in , therefore it reaches the maximum in . Finally, if , the maximiser coincides with the unique stationary point . ∎

The main consequence of the preceding result is that the reinsurance and the investment decisions depend on each other only via the surplus process and not via the parameters.

Corollary 4.

Suppose that and consider the case of proportional reinsurance (8). The optimal retention level is given by

Proof.

As expected, the optimal retention level is proportional to the reinsurance cost and inversely proportional to the risk aversion. Moreover, reinsurance is only bought for wealth not too far from (recall equation (4)). Note that the optimal strategy is independent on and , i.e. it is only affected by the current wealth. Finally, full reinsurance is never optimal.

Corollary 5.

Suppose that and consider excess-of-loss reinsurance (14). The optimal retention level is given by

Proof.

Again, the retention level turns out to increase with the reinsurance safety loading and decrease with the risk aversion parameter. In addition, it increases with the distance between the current wealth and the threshold .

6 Numerical results

In this section we provide some numerical examples based on Proposition 1. All the simulations are performed according to the parameters in Table 1 below, unless indicated otherwise.

| Parameter | Value |

|---|---|

The choice of constant parameters may be considered as fixing . Note that the strategy depends on via the parameters only. Now we illustrate how the strategy depends on the different parameters. In the following figures, the solid line shows the reinsurance strategy, the dashed line the investment strategy.

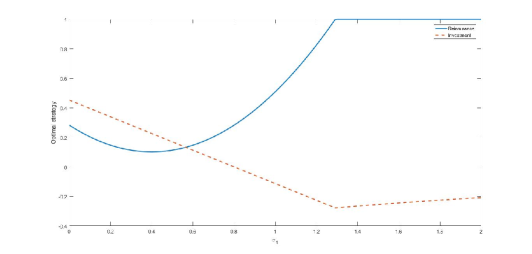

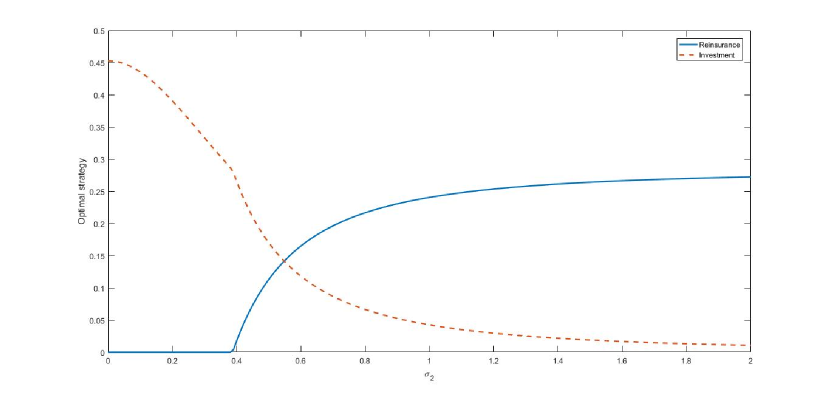

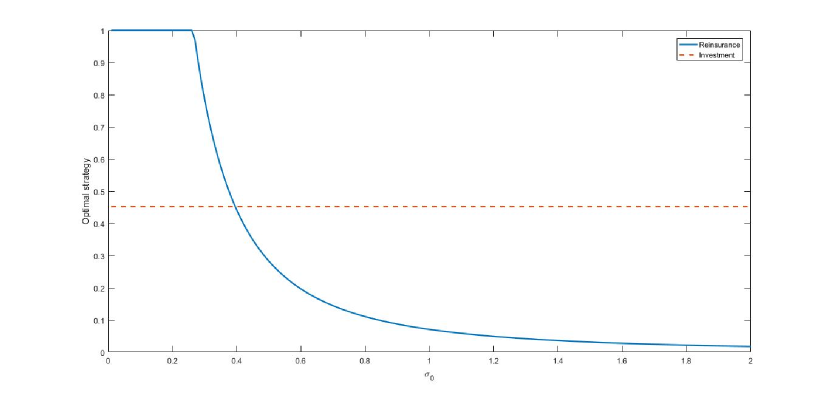

First, we analyse how the volatility coefficients of the risky asset influence the optimal strategies. In Figures 1 and 2 we notice very different behaviour. On the one hand, the retention level is convex with respect to up to a certain threshold, above which null reinsurance is optimal. On the other, when (see Figure 2(a)) is null up to a given point and concave with respect to from that point on. Finally, for (see Figure 2(b)) the retention level is constant (see Corollary 4). Let us observe that the regularity of the optimal investment in Figure 2(b) is due to the absence of influence from (which remains constant).

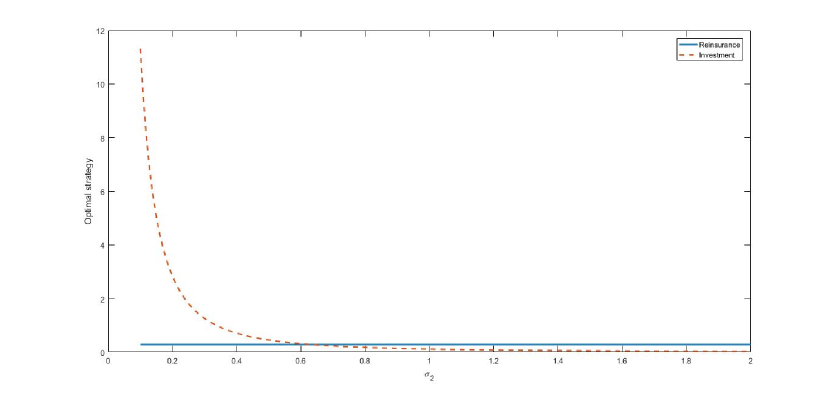

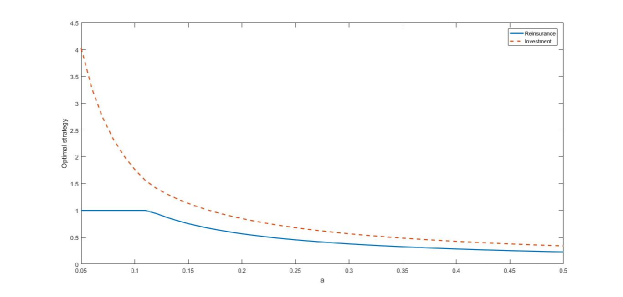

Now let us focus on Figure 3. When increases the insurer rapidly goes from null reinsurance to full reinsurance, while the investment strongly depends on the retention level . Under (see Figure 3(a)), as long as , decreases with ; when starts decreasing, increases; finally, when stabilises at , then stabilises at the starting level. On the contrary, when the investment remains constant and asymptotically goes to .

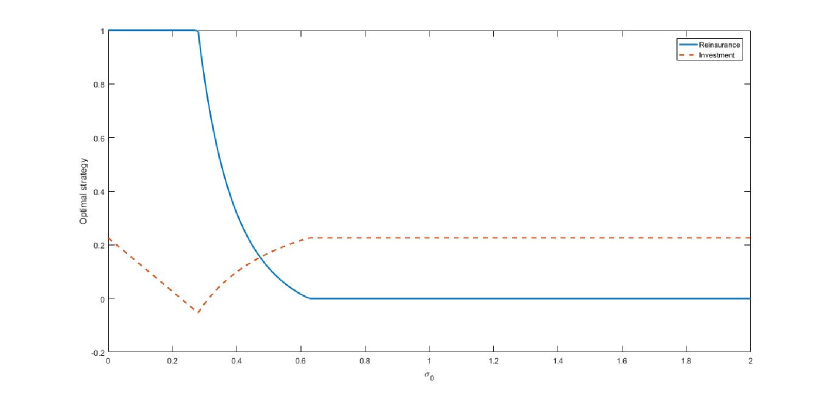

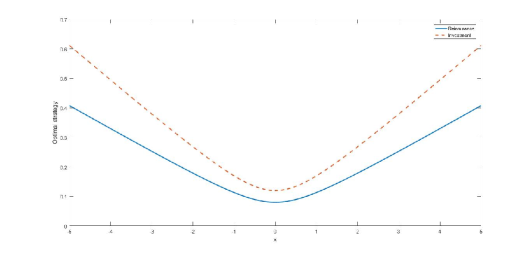

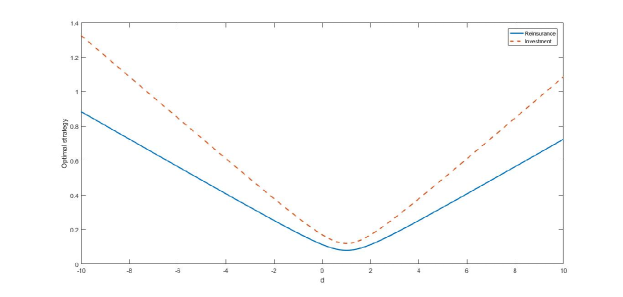

As pointed out in the previous section, the current wealth level plays an important role in the evaluation of the optimal strategy and this is still true under the special case . In Figure 4 below we illustrate the optimal strategy as a function of . Both the reinsurance and the investment strategy are symmetric with respect to . Moreover, they both increase when moves away from the threshold wealth . This is not surprising because the risk aversion decreases with the distance to .

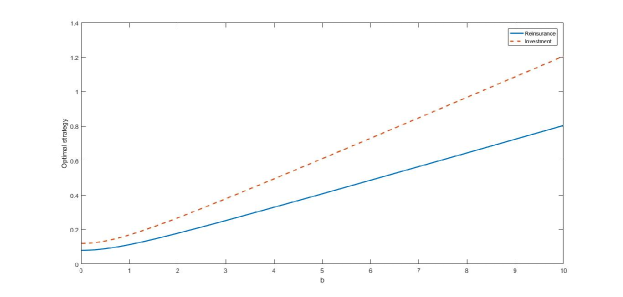

In the next Figure 5 we investigate the optimal strategy reaction to modifications of the utility function. As expected, the higher is the risk aversion, the larger is the optimal protection level and the lower is the investment in the risky asset (see Figure 5(a)). When increases, both the investment and the retention level monotonically increase (see Figure 5(b)). Let us recall that corresponds to HARA utility functions. Finally, by Figure 5(c) we notice that any change of produces the same result of a variation in current wealth (see Figure 4).

References

- [1] M. Brachetta and C. Ceci. Optimal proportional reinsurance and investment for stochastic factor models. Insurance: Mathematics and Economics (in press), 2019.

- [2] H. Bühlmann. Mathematical Methods in Risk Theory. Springer-Verlag, 1970.

- [3] A. Chen, A. Pelsser, and M. Vellekoop. Modeling non-monotone risk aversion using sahara utility functions. Journal of Economic Theory, 146(5):2075–2092, 2011.

- [4] B. de Finetti. Il problema dei “pieni”. G. Ist. Ital. Attuari, 11:1–88, 1940.

- [5] J. Eisenberg and H. Schmidli. Optimal control of capital injections by reinsurance in a diffusion approximation. Bl tter DGVFM, 30:1–13, 2009.

- [6] H. U. Gerber. An Introduction to Mathematical Risk Theory. Huebner Foundation Monographs, 1979.

- [7] J. Grandell. Aspects of risk theory. Springer-Verlag, 1991.

- [8] M. Guerra and M. Centeno. Optimal reinsurance policy: The adjustment coefficient and the expected utility criteria. Insurance: Mathematics and Economics, 42(2):529 – 539, 2008.

- [9] C. Irgens and J. Paulsen. Optimal control of risk exposure, reinsurance and investments for insurance portfolios. Insurance: Mathematics and Economics, 35:21–51, 2004.

- [10] Z. Liang and E. Bayraktar. Optimal reinsurance and investment with unobservable claim size and intensity. Insurance: Mathematics and Economics, 55:156–166, 2014.

- [11] M. Mania and M. Santacroce. Exponential utility maximization under partial information. Finance and Stochastics, 14(3):419–448, Sep 2010.

- [12] S. D. Promislow and V. R. Young. Minimizing the probability of ruin when claims follow brownian motion with drift. North American Actuarial Journal, 9(3):109, 2005.

- [13] H. Schmidli. Optimal proportional reinsurance policies in a dynamic setting. Scandinavian Actuarial Journal, 2001(1):55–68, 2001.

- [14] H. Schmidli. On minimizing the ruin probability by investment and reinsurance. Ann. Appl. Probab., 12(3):890–907, 08 2002.

- [15] H. Schmidli. Stochastic Control in Insurance. Springer-Verlag, 2008.

- [16] H. Schmidli. Risk Theory. Springer Actuarial. Springer International Publishing, 2018.

- [17] D. Wagner. Survey of measurable selection theorems. SIAM J. Control and Optimization, pages 859–903, 1977.