Approximate spectral gaps for Markov chains mixing times in high dimensions

Abstract

This paper introduces a concept of approximate spectral gap to analyze the mixing time of Markov Chain Monte Carlo (MCMC) algorithms for which the usual spectral gap is degenerate or almost degenerate. We use the idea to analyze a class of MCMC algorithms to sample from mixtures of densities. As an application we study the mixing time of a Gibbs sampler for variable selection in linear regression models. Under some regularity conditions on the signal and the design matrix of the regression problem, we show that for well-chosen initial distributions the mixing time of the Gibbs sampler is polynomial in the dimension of the space.

keywords:

[class=MSC]keywords:

propositiontheorem \aliascntresettheproposition \newaliascntlemmatheorem \aliascntresetthelemma \newaliascntcorollarytheorem \aliascntresetthecorollary \newaliascntdefinitiontheorem \aliascntresetthedefinition \newaliascntremarktheorem \aliascntresettheremark \newaliascntexampletheorem \aliascntresettheexample \startlocaldefs \endlocaldefs

T1This work is partially supported by the NSF grant DMS1513040.

1 Introduction

Understanding the type of problems for which fast Markov Chain Monte Carlo (MCMC) sampling is possible is a question of fundamental interest. The study of the size of the spectral gap is a widely used approach to gain insight into the behavior of MCMC algorithms. However this technique may be inapropriate when dealing with distributions with small isolated local modes. To be more precise, let be some probability measure of interest on some measure space , and let be a Markov kernel with invariant distribution . For the purpose of sampling from using , one can represent an isolated local mode (to which is sensitive) as a subset such that is small compared to for all . In this case, will have a small conductance (see (2.2) for definition), and hence a small spectral gap. Note however that if is also small (that is we are dealing with a small isolated mode ), then, since

we see that the set will be typically hard to reach in the first place. Hence, any finite Markov chain say, with transition kernel and initialized in is unlikely to visit . Yet, for large, may still be a good approximate sample from , since is small. This implies that the mixing time predicted by the standard spectral gap may markly differ from the practical behavior of these finite chains. Motivated by this problem, and building on the -conductance of L. Lovasz and M. Simonovits ([16, 17]), we develop an idea of approximate spectral gap (that we call -spectral gap, for some ) which allows us to measure the mixing time of a Markov chain while discounting the ill-effect of overly small (and potentially problematic) sets.

Mixtures are good examples of probability distributions with isolated local modes. We use the idea to analyze a class of MCMC algorithms to sample from mixtures of densities. Much is known on the computational complexity of various MCMC algorithms for log-concave densities (see e.g. [16, 17, 7, 15, 18, 6] and the references therein). However these results cannot be directly applied to mixtures, since a mixture of log-concave densities is not log-concave in general. By augmenting the variable of interest to include the mixing variable, a Gibbs sampler can be used to sample from a mixture. A very nice lower bound on the spectral gap of such Gibbs samplers (and generalizations thereof) is developed in [19]. However the analysis of [19] typically leads to mixing times that grow exponentially fast with the dimension of the space. We re-examine [19]’s argument using the concept of -spectral gap, leading to Theorem 1 that gives potentially better dependence on the dimension.

Our initial motivation into this work is in large-scale Bayesian variable selection problems. The Bayesian posterior distributions that arise from these problems are typically mixtures of log-concave densities with very large numbers of components, and the aforementioned Gibbs sampler is commonly used for sampling (see e.g. [9, 22]). We show that the proposed concept of -spectral gap and Theorem 1 can be combined with Bayesian posterior contraction principles to show that the algorithm – with a good initialization – has a mixing time that is polynomial in the number of regressors in the model (see Theorem 2).

The paper is organized as follows. We develop the concept of -spectral gap in Section 2. The main result there is Lemma 2. In Section 3 we study the mixing time of mixtures of Markov kernels, and derive (Theorem 1) a generalization of Theorem 1.2 of [19]. We put these two results together to analysis the linear regression model in Section 4, leading to Theorem 2. Some numerical simulations are detailed in Section 4.2.

2 Approximate spectral gaps for Markov chains

Let be a probability measure on some Polish space (where is its Borel sigma-algebra), equipped with a reference sigma-finite measure denoted . In the applications that we have in mind, is the Euclidean space equipped with its Lebesgue measure. We assume that is absolutely continuous with respect to , and we will abuse notation and use to denote both and its density: . We let denote the Hilbert space of all real-valued square-integrable (wrt ) functions on , equipped with the inner with associated norm . More generally, for , we set . For , is defined as the essential supremum of with respect to . If is a Markov kernel on , and an integer, denotes the -th iterate of , defined recursively as , , measurable. If is a measurable function, then is the function defined as , , assuming that the integral is well defined. And if is a probability measure on , then is the probability on defined as , . The total variation distance between two probability measures is defined as

Let be a Markov kernel on that is reversible with respect to . That is for all ,

We will also assume throughout that is lazy in the sense that . The concept of spectral gap and the related Poincare’s inequalities are commonly used to quantify Markov chains mixing times. For , we set , , and . The spectral gap of is then defined as

It is well-known and easy to establish (see for instance [21] Corollary 2.15) that if , and , then

| (2.1) |

Therefore, lower-bounds on the spectral gap can be used to derive upper-bounds on the mixing time of . We refer the reader to ([26, 25, 5, 21]) for more details, and for various strategies to lower-bound . In many examples, the conductance of , defined as

| (2.2) |

is easier to control than the spectral gap. Cheeger’s inequality for Markov chains ([13, 26]) can then be used to translate a lower-bound on into a lower-bound on the spectral gap:

| (2.3) |

The concept of -conductance introduced by L. Lovacz and M. Simonivits ([16, 17], see also [18]) as a generalization of the conductance has proven very useful. For – using a definition slightly different from [16, 17] – we define the -conductance of the Markov kernel as

where the infimum above is taken over measurable subsets of . Note that . Plainly put, captures the same concept as , except that in we disregard sets that are either too small or too large under . It turns out that still controls the mixing time of up to an additive constant that depends on (see [17] Corollary 1.5). One important drawback of the -conductance is that the arguments that relate to the mixing time of (Theorem 1.4 of [17]) is rather involved, and this has limited the scope and the usefulness of the concept. Furthermore there are many problems where direct bound on the spectral gap instead of the conductance is easier, and yields better results. This is for instance the case in discrete problems where canonical path arguments yields much sharper bounds on the Poincare constant ([5]).

Motivated by the -conductance, we introduce a similar concept of -spectral gap that directly approximates the spectral gap. And we show that the proposed -spectral gap still controls the mixing time of the Markov chains.

Let denote a norm-like function on with the following properties: , if then , and

For , we define the -spectral gap of as

| (2.4) |

We note that depends on the choice of , although we will not make that dependence explicit. We note also that if and , then we recover . Furthermore, given , and writing , we have

By the lazyness of the chain, , and we deduce that is a quantity that always belongs to the interval .

This idea of -spectral gap is somewhat similar to the concept of weak Poincare inequality developed for continuous-time Markov semigroups with zero spectral gap ([14, 24, 4]). One key difference is that weak Poincare inequalities lead to sub-geometric rates of convergence of the semi-group, whereas the idea of -spectral gap as introduced here leads to a geometric convergence rate, plus an additive remainder that depends on . More precisely, we have the following analog of (2.1). The proof is similar to the proof of (2.1), and is based on an argument from [20].

Lemma \thelemma.

Fix . Suppose that for a function such that . Then for all integer , we have

Proof.

See Section 5.1. ∎

We now highlight an approach to lower bound and use Lemma 2. This is the same approach used in the proof of Theorem 2. Hence the following discussion can also be viewed as a rough sketch of the proof of Theorem 2. To proceed we first introduce a related concept of restricted spectral gap. If is a non-empty measurable subset such that , the -restricted spectral gap of is defined as

where the infimum is taken over all measurable functions such that

. The next result shows that these restricted spectral gaps can be used to lower bound .

Lemma \thelemma.

Given , and taking , for some real number , let be a measurable subset of such that . Then we have

Proof.

See Section 5.2. ∎

We combine the above two lemmas as follows. Fix . Suppose that we can choose the initial distribution such that , for some constant (warm start). In that case Lemma 2 with , and gives for all ,

Therefore, for this given choice , if we can find a set such that , then Lemma 2 asserts that . Hence it holds that

If is a posterior distribution from some Bayesian analysis, posterior contraction results can be used to find the sets . Furthermore, standard techniques used to establish Poincare inequalities can be similarly applied to lower bound . We illustrate these ideas in Theorem 2.

3 Mixing times of mixtures of Markov kernels

We consider here the case where is a discrete mixture of log-concave densities of the form

| (3.1) |

for nonnegative measurable functions , where I is a nonempty finite set. Sampling from mixtures is more challenging than sampling from log-concave densities. For instance it is shown in [8] that no polynomial-time MCMC algorithm exists to sample from mixtures of densities with inequal covariance matrix, if the algorithm uses only the marginal density of the mixture and its derivative. One major shortcoming of [8] is that their algorithm is impractical when the number of mixture components is very large. In such settings, a Gibbs sampler is commonly employed (based on conditional distributions). We show below that this Gibbs sampler is fast mixing in some cases.

To avoid confusion we will write to denote the joint distribution on defined as

Let (resp. ) denote the implied conditional (resp. marginal) distribution on I, and let be the implied conditional distribution on . For each , let be a transition kernel on with invariant distribution . We assume that is reversible with respect to , and ergodic (phi-irreducible and aperiodic). We then consider the Markov kernel defined as

| (3.2) |

that is reversible with respect to as in (3.1). In [19] the authors developed a very nice lower bound on the spectral gap of knowing the spectral gaps of the ’s. Fix , and construct a graph on I such that there is an edge between if and only if

If denotes the diameter of the graph thus defined111The diameter of a graph is the length (the number of edges) of the longest among all the shortest paths between all pairs of vertices., Theorem 1.2 of [19] says that

| (3.3) |

The lower bound in (3.3) can be extremely small, particularly when I is large. Indeed, the ratio would then be small: taking large makes large. Furthermore, in problems where I is large, is typically exponentially small for many components . We have the following analog of Lemma 2.

Theorem 1.

Proof.

See Section 5.3. ∎

Note the similarity with (3.3). However Theorem 1 allows us to restrict the analysis of the chain to the set . Theorem 1 is basically a mixture analog of Lemma 2. In the important special case where , and one chooses , Theorem 1 shows that

As we show with the next example these two lower bounds can have very different dependence on the dimension of .

4 Analysis of a Gibbs sampler

We consider the Bayesian treatment of a linear regression problem with response variable , and covariate matrix . The regression parameter is denoted . In settings where the number of regressors is very large, and one is interested in selecting the most significant regressors and the corresponding coefficients, it is common practice to introduce an additional variable selection parameter , and to use a spike-and-slab prior distribution on . More precisely, given we assume that the prior distribution of is given by

and given , we assume that the components of are conditionally independent given , and we assume that has density if , and density otherwise, where denotes the univariate Gaussian distribution with mean and variance . The resulting posterior distribution on is

| (4.1) |

where is a diagonal matrix with -th diagonal element equal to if , and if . The regression error is assumed known. This model is very popular in the application ([9, 11, 22]), mainly because it is straightforward to sample from (4.1). Indeed, the posterior conditional distribution is a product of independent Bernoulli distributions, with closed form probabilities:

| (4.2) |

Given , the conditional distribution of given is , with and given by

| (4.3) |

Put together these two conditional distributions yield a simple Gibbs sampling algorithm for (4.1). We consider the following version that is modified so that the resulting Markov chain is lazy as required by our theory.

Algorithm 1.

We analyze the mixing time of the marginal chain from Algorithm 1. As easily seen, is a Markov chain with invariant distribution

| (4.4) |

which is of the form (3.1), and with transition kernel

| (4.5) |

which is of the form (3.2). In order to bring in the discussion the idea of posterior contraction toward a true value of the parameter, we need to assume a model for the data.

H 1.

-

1.

The data is the realization of a random variable , for some unknown parameter , and a known absolute constant .

-

2.

The matrix is non-random and normalized such that

(4.6) where denotes the -th column of .

-

3.

The prior parameter q is chosen such that

(4.7) for some absolute constant .

-

4.

The prior parameters and are taken such that

(4.8)

We will write (resp. ) to denote the probability distribution (resp. expectation operator) of the random variable assumed in H1.

Remark \theremark.

Overall these are very basic assumptions. We assume in H1-(1) that the statistical model is well specified, and there is a true value of the parameter denoted . The assumption that the regression errors are Gaussian is imposed mostly for simplicity, and can be replaced by a sub-Gaussian assumption, with minimal change to what follows. The prior assumption in H1-(3) is fairly standard, and follows [3, 22, 2]. H1-(4) simply says that the variance of the slab prior density should be sufficiently larger than the variance of the spike prior density.

To proceed we introduce some notations. For , we write to represent the component-wise product of and . For , and , we write as a short for , and we define , that is , . For a matrix , (resp. ) denotes the matrix of (resp. ) obtained by keeping only the columns of for which (resp. ). For two elements of , we write to mean that whenever . The support of a vector is the vector such that if and only if .

An important role is played in the analysis by the matrices

and the coherence of the matrix defined for an integer as

We will also need the following important assumption.

H 2.

There exist and an integer , such that

Remark \theremark.

For small enough and , we show in the appendix that the matrix can be loosely interpreted as the projector on the orthogonal of the space spanned by the columns of . Therefore, H2 rules out settings where a small number of columns of have the same linear span as all the columns of . Indeed signal recovery becomes nearly impossible in such settings. We show in Lemma A in the appendix that if is a random matrix with i.i.d. standard normal entries (Gaussian ensemble) and is taken small enough, then H2 holds with high probability, and

for some universal constant , provided that .

We need few more quantities in order to state the theorem. We define

| (4.9) |

that we view as the signal detectability threshold. Let be the element of that indicates which components of are greater than in absolute value (detectable components): if and only if . Components of that are below are too small to be detected. This implies that the element of toward which we can expect to contract is (here refers to the -marginal of the joint posterior). We formalize this contraction as follows. Given , we define

which collects models that contain the true model (that is ) and have at most false-positives, and we say that posterior contraction holds if

| (4.10) |

We will not directly establish (4.10). However several existing work suggest that this description of the posterior contraction of holds. For instance under similar assumptions as above, [22] show that with high-probability for positive constants . And when , [1] shows that (4.10) holds for a slightly modified version of the posterior distribution (4.1). We introduce the event

Note that Gaussian tail bounds easily implies that under H1, the last part of holds true with high probability. Hence the key condition in is the posterior contraction assertion that . Here is our main result in this section.

Theorem 2.

Proof.

See Section 5.5. ∎

4.1 Discussion

Since we impose , the condition (4.11) basically says that the number of false-positives of cannot be too large. Hence the main conclusion of Theorem 2 is that Algorithm 1 has a polynomial mixing time if posterior contraction holds (), and the number of initial false-positives FP is not too large – the idea of warm-start. In contrast, the mixing time predicted by the standard spectral gap scales with as . This follows simply by plugging the lower bound (5.16) in (3.3).

One of the first paper that analyzes the mixing times of MCMC algorithm in high-dimensional linear regression models and highlights fast/slow mixing behaviors is [27]. These authors takes a worst-case scenario approach222they look at the worst mixing time achievable by changing the initial distribution, and show that in general their Gibbs sampler has a mixing time that is exponential in unless the state space is restricted to only models for which for some threshold . We note however that correctly choosing such threshold in practice may be complicated. In contrast Theorem 2 shows that without restricting the state space one can still achieve polynomial mixing time by warm-starting the algorithm. The idea of warm-start is a well-known strategy to accelerate mixing times in MCMC computation (see e.g. [18]).

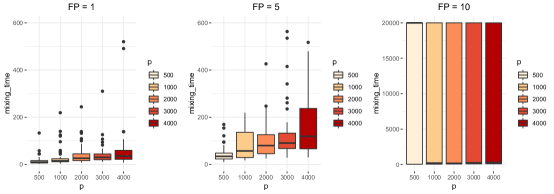

We note from (4.11) that the power that appears in (4.12) grows with FP. This suggests that the mixing time of the algorithm can rapidly deteriorate as FP grows. It is unclear whether the precise dependence on thus expressed in (4.12) is tight. In any case, we did observe in the simulations a sharp increase in the mixing time of the algorithm as FP increases, which seems consistent with (4.12).

With respect to the initialization, the natural question is how the mixing time behaves if admits false-negatives. Our method is not adapted to provide an answer to this question. Nonetheless to gain some intuition, we perform some numerical simulations which seem to suggest that the polynomial mixing time obtained in Theorem 2 no longer hold if has false-negatives.

The bound in (4.12) highlights the effect of the coherence of the matrix . In general grows with as , which cancels with the same term in the denominator. However if there are strong correlations among some of the columns of , then typically grows with faster than , which can significantly impacts the mixing time. For instance if as assumed above, and , then the resulting mixing time grows with faster than exponential.

Theorem 2 has also some obvious implications on how to initialize the chain. It suggests that the initialization strategy sometimes used in practice where is taken as the zero vector is sub-optimal, and might result in Markov chain with exponential mixing times. Instead, our result suggests a warm-start initialization where is taken for instance as the support of the lasso estimate – or some other similarly-behaved frequentist estimate.

4.2 Numerical illustrations

We illustrate some of the conclusions with the following simulation study. We consider a linear regression model with Gaussian noise , where is set to . We experiment with sample size , and dimension . We take as a random matrix with i.i.d. standard Gaussian entries. We fix the number of non-zero coefficients to , and is given by

The non-zero coefficients of are uniformly drawn from , where

We use the following prior parameters values:

We use an initial distribution , where we vary the number of false-positives of . To monitor the mixing, we compute the sensitivity and the precision at iteration as

We empirically measure the mixing time of the algorithm as the first time where both and reach , truncated to – that is we stop any run that has not mixed after iterations. The average empirical mixing time thus obtained (based on on independent MCMC replications) are presented in Table 1 and Figure 1. These estimates are consistent with our results. They show only a modest increase in mixing time as increases, but a sharp increase in mixing time as the number of false-positives increases. We also explore the behavior of the sampler in the presence of false-negatives in the initialization. More specifically we consider the case where has 2 false-negatives, but no false-positive. In this setting, and for all 50 replications, the sampler fails to recover all significant components within iterations.

| 15.7 (21.1) | 71.6 (280.3) | 43.5 (45.6) | 42.8 (47.5) | 65.4 (100.6) | |

| 93.8 (247.8) | 93.5 (102.3) | 130.8 (164.9) | 186.9 (303.9) | 225.9 (239.5) | |

| 11325.6 | 7916.3 | 8955.0 | 10648.0 | 12113.4 | |

| 20000 | 20000 | 20000 | 20000 | 20000 | |

| , | 20000 | 20000 | 20000 | 20000 | 20000 |

5 Proofs

5.1 Proof Lemma 2

We first note that if a probability measure is absolutely continuous with respect to with Radon-Nikodym derivative , then for any ,

where the third equality uses the reversibility of . This calculation says that is also absolutely continuous with respect to with Radon-Nikodym derivative . More generally , and

| (5.1) | |||||

Take . Since , we have

| (5.2) |

where the last equality exploits the reversibility of . For any function ,

By the lazyness of the chain, the first term on the right hand side of the last display is bounded from below by

whereas the second term is bounded from below by

Hence, for all ,

Using the last display together with (5.2), and the definition of , we conclude that for all ,

| (5.3) |

Fix , and take . If , then, by (5.3),

But if , then by (5.3),

Clearly the last display (which is derived assuming that ) continues to hold if . We conclude that for all ,

Since , it follows that for all

| (5.4) |

We can iterate the above inequality to deduce that for all , such that , and for all ,

Now, if , the last display combined with (5.1) implies that

This ends the proof.

5.2 Proof Lemma 2

Take such that , and . We have

Using the convexity inequality , and Holder’s inequality,

With similar calculation,

Using , we get

Hence

This ends the proof.

5.3 Proof Theorem 1

The proof of the theorem is similar to the proof of Lemma 2. But first, we need the following lemma.

Lemma \thelemma.

Let , be two probability measures on some measurable space with reference measure , such that for some . Then for any measurable function such that and , we have

Proof.

This result is established as part of the proof of Theorem 1.2 of [19] (see inequality (47)). ∎

Choose such that . Given , we set

By the definition of , we have

| (5.5) |

By Fubini’s theorem, and using (5.5), we have

| (5.6) | |||||

Using , and , we write

by using similar calculations as in Lemma 2. And since is such that , we conclude that

For , let us write to denote the path from to , and given an edge , let us write as where and denote the incident nodes of . By the Cauchy-Schwarz inequality,

By Lemma 5.3, integral on the right-hand side of the last display is upper bounded by

Therefore the last inequality becomes

5.4 Some preliminary remarks on the proof of Theorem 2

We collect here some basic calculations on that we rely on repeatedly in the proofs. For any subset of , and , we have

| (5.8) | |||||

By the determinant lemma ( valid for any invertible matrix , and ) we have

By the Woodbury identity ([10] Section 0.7.4) which states that for any set of matrices with matching dimensions, , we have

Hence,

It follows from the above and (5.8) that for all , and ,

| (5.9) |

where, for , we recall the definition . We will use the following to deal with the terms involved in (5.9). Suppose that we have such that . Setting , it is easily seen that

| (5.10) |

Therefore by the determinant lemma,

| (5.11) |

And by the Woodbury identity,

| (5.12) |

5.5 Proof Theorem 2

Throughout, we fix , and for some that satisfies (4.11). We recall that the initial distribution is taken as , for some initial choice . Let

be the density of with respect to . Since , we have

Using we can write,

Using (5.9) with and , and using (5.11) and (5.12), we deduce that

where the second inequality uses the fact the eigenvalues of are all at least , and (4.6). In view of the above, we set

| (5.13) |

which gives . Therefore, by Lemma 2 (applied with ), for all integer , we have

| (5.14) |

Lower bound on . To proceed with (5.14) we need a lower bound on the approximate spectral gap. We apply Theorem 1 with the obvious choices , , and , and . For , and as in (5.13) we have

provided (4.11) holds. In other words we have as required by Theorem 1. It remains only to find . To do so, we consider the follow graph on : we link and if , or , and . We need to find such that for all , such that if , or , and we have

| (5.15) |

Suppose that . Then

Using (5.8), and (5.9) we have

We combine these inequalities with (5.11) and (5.12) to get

For such that , and , we must have , since both and contain . Therefore, since , where , we have for ,

It follows that

Hence we can apply Theorem 1 with

The diameter of the graph thus constructed is . We conclude from the above and Theorem 1 that for ,

Furthermore, for , using (5.9) with and , together with (5.11) and (5.12), we have

| (5.16) |

Hence

It follows from (5.14) and the lower bound on above that for

| (5.17) |

we have

where is an absolute constant that does not depend on nor . This completes the proof.

Appendix A Some technical results

We make use of the following standard Gaussian deviation bound.

Lemma \thelemma.

Let , and be vectors of . Then for all ,

The next result gives a bound on , and shows that H2 holds with high probability in the case of a Gaussian ensemble.

Lemma \thelemma.

Suppose that is a random matrix with i.i.d. standard Normal entries. Given an integer , and positive constants and , set

Then there exist some universal finite constants such that for , the following two statements hold with probability at least : for taken small enough and

| (A.1) |

it holds that

| (A.2) |

Proof.

For a matrix we set

and for and , we define

By Theorem 1 of [23], Lemma 1-(4.2) of [12], and standard Gaussian deviation bounds, we can find universal constants , such that for , we have . So to obtained the statement of the lemma, it suffices to consider some arbitrary element and show that (A.2) holds.

Fix such that . We set , so that . The Woodbury identity gives

| (A.3) |

Hence, for any ,

| (A.4) |

If , and , then we deduce easily from (A.4) that for all such that ,

| (A.5) |

In order to proceed, we need to bound the term . Easily, for , we have

Another application of the Woodbury identity gives

| (A.6) |

If is the singular value decomposition of , with positive singular values , and if denotes the projector on the space orthogonal to the span of , we have

We note that for , . Therefore,for , and using the above,

provided that as assumed in (A.1). We combine this with (A.5) to obtain that for such that ,

| (A.7) |

for small enough. (A.7) says that , for , as claimed.

For such that , (A.6) gives

| (A.8) | |||||

since , and by taking large enough (. Equation (A.3) then yields

For , it follows that

which together with (A.7) and (A.1) implies that for any such that , and , we have

as claimed.

∎

Acknowledgements

I’m grateful to Joonha Park for pointing out an error in an initial draft of the manuscript.

References

- Atchade and Bhattacharyya [2018] Atchade, Y. and Bhattacharyya, A. (2018). An approach to large-scale Quasi-Bayesian inference with spike-and-slab priors. arXiv e-prints arXiv:1803.10282.

- Atchade [2017] Atchade, Y. A. (2017). On the contraction properties of some high-dimensional quasi-posterior distributions. Ann. Statist. 45 2248–2273.

- Castillo et al. [2015] Castillo, I., Schmidt-Hieber, J. and van der Vaart, A. (2015). Bayesian linear regression with sparse priors. Ann. Statist. 43 1986–2018.

- Cattiaux and Guillin [2009] Cattiaux, P. and Guillin, A. (2009). Trends to equilibrium in total variation distance. Ann. Inst. H. Poincaré Probab. Statist. 45 117–145.

- Diaconis and Stroock [1991] Diaconis, P. and Stroock, D. (1991). Geometric bounds for eigenvalues of markov chains. The Annals of Applied Probability 1 36–61.

- Dwivedi et al. [2018] Dwivedi, R., Chen, Y., Wainwright, M. J. and Yu, B. (2018). Log-concave sampling: Metropolis-Hastings algorithms are fast! arXiv e-prints arXiv:1801.02309.

- Frieze et al. [1994] Frieze, A., Kannan, R. and Polson, N. (1994). Sampling from log-concave distributions. Ann. Appl. Probab. 4 812–837.

- Ge et al. [2018] Ge, R., Lee, H. and Risteski, A. (2018). Simulated Tempering Langevin Monte Carlo II: An Improved Proof using Soft Markov Chain Decomposition. arXiv e-prints arXiv:1812.00793.

- George and McCulloch [1997] George, E. I. and McCulloch, R. E. (1997). Approaches to bayesian variable selection. Statist. Sinica 7 339–373.

- Horn and Johnson [2012] Horn, R. A. and Johnson, C. R. (2012). Matrix Analysis. 2nd ed. Cambridge University Press, New York, NY, USA.

- Ishwaran and Rao [2005] Ishwaran, H. and Rao, J. S. (2005). Spike and slab variable selection: Frequentist and bayesian strategies. Ann. Statist. 33 730–773.

- Laurent and Massart [2000] Laurent, B. and Massart, P. (2000). Adaptive estimation of a quadratic functional by model selection. Ann. Statist. 28 1302–1338.

- Lawler and Sokal [1988] Lawler, G. and Sokal, A. (1988). Bounds on the l2spectrum for markov chains and markov processes: A generalization of cheeger’s inequality. Transactions of the American Mathematical Society 309 557–580.

- Liggett [1991] Liggett, T. M. (1991). rates of convergence for attractive reversible nearest particle systems: The critical case. Ann. Probab. 19 935–959.

- Lovász [1999] Lovász, L. (1999). Hit-and-run mixes fast. Math. Program. 86 443–461.

- Lovasz and Simonovits [1990] Lovasz, L. and Simonovits, M. (1990). The mixing rate of markov chains, an isoperimetric inequality, and computing the volume. In Proceedings of the 31st Annual Symposium on Foundations of Computer Science. SFCS ’90, IEEE Computer Society, Washington, DC, USA.

- Lovász and Simonovits [1993] Lovász, L. and Simonovits, M. (1993). Random walks in a convex body and an improved volume algorithm. Random Structures Algorithms 4 359–412.

- Lovász and Vempala [2007] Lovász, L. and Vempala, S. (2007). The geometry of logconcave functions and sampling algorithms. Random Structures Algorithms 30 307–358.

- Madras and Randall [2002] Madras, N. and Randall, D. (2002). Markov chain decomposition for convergence rate analysis. Ann. Appl. Probab. 12 581–606.

- Mihail [1989] Mihail, M. (1989). Conductance and convergence of markov chains-a combinatorial treatment of expanders. In 30th Annual Symposium on Foundations of Computer Science.

- Montenegro and Tetali [2006] Montenegro, R. and Tetali, P. (2006). Mathematical aspects of mixing times in markov chains. Found. Trends Theor. Comput. Sci. 1 237–354.

- Narisetty and He [2014] Narisetty, N. and He, X. (2014). Bayesian variable selection with shrinking and diffusing priors. Ann. Statist. 42 789–817.

- Raskutti et al. [2010] Raskutti, G., Wainwright, M. J. and Yu, B. (2010). Restricted eigenvalue properties for correlated gaussian designs. J. Mach. Learn. Res. 11 2241–2259.

- Rockner and Wang [2001] Rockner, M. and Wang, F.-Y. (2001). Weak poincaré inequalities and l2-convergence rates of markov semigroups. Journal of Functional Analysis 185 564–603.

- Sinclair [1992] Sinclair, A. (1992). Improved bounds for mixing rates of markov chains and multicommodity flow. Combinatorics, Probability and Computing 1 351–370.

- Sinclair and Jerrum [1989] Sinclair, A. and Jerrum, M. (1989). Approximate counting, uniform generation and rapidly mixing Markov chains. Inform. and Comput. 82 93–133.

- Yang et al. [2016] Yang, Y., Wainwright, M. J. and Jordan, M. I. (2016). On the computational complexity of high-dimensional bayesian variable selection. Ann. Statist. 44 2497–2532.