Omitted variable bias of Lasso-based inference methods: A finite sample analysis††thanks: This version: . First version: March 20, 2019. Alphabetical ordering; both authors contributed equally to this work. This paper was previously circulated as “Behavior of Lasso and Lasso-based inference under limited variability” and “Omitted variable bias of Lasso-based inference methods under limited variability: A finite sample analysis”. We would like to thank the editor (Xiaoxia Shi), anonymous referees, Stéphane Bonhomme, Gordon Dahl, Graham Elliott, Michael Jansson, Michal Kolesar, Ulrich Müller, Andres Santos, Azeem Shaikh, Aman Ullah and seminar participants for their comments. We are especially grateful to Yixiao Sun and Jeffrey Wooldridge for providing extensive feedback. Wüthrich is also affiliated with CESifo and the ifo Institute. Zhu acknowledges a start-up fund from the Department of Economics at UCSD and the Department of Statistics and the Department of Computer Science at Purdue University, West Lafayette.

Abstract

We study the finite sample behavior of Lasso-based inference methods such as post double Lasso and debiased Lasso. We show that these methods can exhibit substantial omitted variable biases (OVBs) due to Lasso not selecting relevant controls. This phenomenon can occur even when the coefficients are sparse and the sample size is large and larger than the number of controls. Therefore, relying on the existing asymptotic inference theory can be problematic in empirical applications. We compare the Lasso-based inference methods to modern high-dimensional OLS-based methods and provide practical guidance.

Keywords: Lasso, post double Lasso, debiased Lasso, OLS, omitted variable bias, size distortions, finite sample analysis

JEL codes: C21, C52, C55

1 Introduction

Since their introduction, post double Lasso (Belloni et al., 2014) and debiased Lasso (Javanmard and Montanari, 2014; van de Geer et al., 2014; Zhang and Zhang, 2014) have quickly become the most popular inference methods for problems with many control variables. Given the rapidly growing theoretical111 See, for example, Farrell (2015), Belloni et al. (2017b), Zhang and Cheng (2017), Chernozhukov et al. (2018), Caner and Kock (2018) among others. and applied222See, for example, Chen (2015), Decker and Schmitz (2016), Schmitz and Westphal (2017), Breza and Chandrasekhar (2019), Jones et al. (2019), Cole and Fernando (2020), and Enke (2020) among others. literature on these methods, it is crucial to take a step back and examine the performance of these procedures in empirically relevant settings and to better understand their merits and limitations relative to other alternatives.

In this paper, we study the performance of post double Lasso and debiased Lasso from two different angles. First, we develop a theory of the finite sample behavior of post double Lasso and debiased Lasso. We show that under-selection of the Lasso can lead to substantial omitted variable biases (OVBs) in finite samples. Our theoretical results on the OVBs are non-asymptotic; they complement but do not contradict the existing asymptotic theory. Second, we conduct extensive simulations and two empirical studies to investigate the performance of Lasso-based inference methods in practically relevant settings. We find that the OVBs can render the existing asymptotic approximations inaccurate and lead to size distortions.

Following the literature, we consider the following standard linear model

| (1) | |||||

| (2) |

Here is the outcome, is the scalar treatment variable of interest, and is a -dimensional vector of control variables. In the main text, we focus on the performance of post double Lasso for estimating and making inferences (e.g., constructing confidence intervals) on the treatment effect in settings where can be larger than or comparable to . We present results for debiased Lasso in Appendix B.

Post double Lasso consists of two Lasso selection steps: a Lasso regression of on and a Lasso regression of on . In the third step, the estimator of , , is the OLS regression of on and the union of controls selected in the two Lasso steps. OVB arises in post double Lasso whenever the relevant controls (i.e., the controls with non-zero coefficients) are selected in neither Lasso steps, a situation we refer to as double under-selection. Results that can explain when and why double under-selection occurs are scarce in the existing literature. This paper shows theoretically that this phenomenon can even occur in simple examples with classical assumptions (e.g., normal homoscedastic errors, orthogonal designs for the relevant controls), which are often viewed as favorable to the performance of the Lasso. We prove that if the products of the absolute values of the non-zero coefficients and the variances of the controls are no greater than half the regularization parameters derived based on standard Lasso theory333Note that the existing Lasso theory requires the regularization parameter to exceed a certain threshold, which depends on the standard deviations of the noise and the covariates., Lasso fails to select these controls in both steps with high probability.444The “half the regularization parameters” type of condition on the magnitude of non-zero coefficients was independently discovered in Lahiri (2021). We are grateful to an anonymous referee for making us aware of this paper. Our proof strategies differ from the asymptotic ones in Lahiri (2021) and allow us to derive an explicit lower bound with meaningful constants for the probability of under-selection for fixed , which is needed for deriving an explicit formula for the OVB lower bound. While some of the arguments in Lahiri (2021) can be made non-asymptotic, one of their core arguments for showing necessary conditions for variable selection consistency of the Lasso relies on tending to infinity. It is not clear that such an argument can lead to an explicit lower bound with meaningful constants for the probability of under-selection. On the other hand, our non-asympototic argument can easily lead to asymptotic conclusions. This result allows us to derive the first non-asymptotic lower bound formula in the literature for the OVB of the post double Lasso estimator . Our lower bound provides explicit universal constants, which are essential for understanding the finite sample behavior of post double Lasso and its limitations.

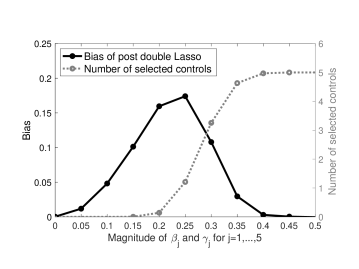

The OVB lower bound is characterized by the interplay between the probability of double under-selection and the magnitude of the coefficients corresponding to the relevant controls in (1)–(2). In particular, there are three regimes: (i) the omitted controls have coefficients whose magnitudes are large enough to cause substantial bias; (ii) the omitted controls have coefficients whose magnitudes are too small to cause substantial bias; (iii) the magnitude of the relevant coefficients is large enough such that the corresponding controls are selected with high-probability. We illustrate these three regimes in Figure 1, which plots the bias of post double Lasso and the number of selected control variables as a function of the magnitude of the non-zero coefficients. [FIGURE 1 HERE.]

Our theoretical analysis of the OVB has important implications for inference procedures based on the post double Lasso. Belloni et al. (2014) show that is asymptotically normal with zero mean. We show that in finite samples, the OVB lower bound can be more than twice as large as the standard deviation obtained from the asymptotic distribution in Belloni et al. (2014). This is true even when is much larger than and and are sparse. To illustrate, assume that (1) and (2) share the same set of non-zero coefficients and set as in Angrist and Frandsen (2019, Section 3), who use post double Lasso to estimate the effect of elite colleges. The ratio of our OVB lower bound to the standard deviation in Belloni et al. (2014) is if and if . This example shows that the requirement on the sparsity parameter for the OVBs to be negligible is quite stringent. We emphasize that our findings do not contradict the existing results on the asymptotic distribution of post double Lasso in Belloni et al. (2014). Rather, our results suggest that the OVBs can make the asymptotic zero-mean approximation of inaccurate in finite samples.

To better understand the practical implications of the OVB of post double Lasso, we perform extensive simulations. Our simulation results can be summarized as follows. (i) Large OVBs are persistent across a range of empirically relevant settings and can occur even when is large and larger than , and the sparsity parameter is small. (ii) The OVBs can lead to invalid inferences and under-coverage of confidence intervals. (iii) The performance of post double Lasso varies substantially across different popular choices of regularization parameters, and no single choice outperforms the others across all designs. While it may be tempting to choose a smaller regularization parameter than the standard recommendation in the literature to mitigate under-selection, we find that this idea does not work in general and can lead to rather poor performance.

In addition to the simulations, we consider two empirical applications: the analysis of the effect of 401(k) plans on savings by Belloni et al. (2017b) and Chernozhukov et al. (2018) and the study of the racial test score gap by Fryer and Levitt (2013b). We draw samples of different sizes from the large original data and compare the subsample estimates to the estimates based on the original data.555For example, Kolesár and Rothe (2018) use a similar of exercise to illustrate the issues with discrete running variables in regression discontinuity designs. In both applications, we find substantial biases even when is considerably larger than , and we document that the magnitude of the biases varies substantially depending on the regularization choice.

Given our theoretical results, simulations, and empirical evidence, a natural question is how to make statistical inferences in a reliable manner if one is concerned about OVBs. In many economic applications, is comparable to but still smaller than . This motivates the recent development of high-dimensional OLS-based inference procedures (e.g., Cattaneo et al., 2018; D’Adamo, 2018; Jochmans, 2020; Kline et al., 2020). These methods are based on OLS regressions with all controls and rely on novel variance estimators that are robust to the inclusion of many controls (unlike conventional variance estimators). Based on extensive simulations, we find that OLS with standard errors proposed by Cattaneo et al. (2018) demonstrates excellent coverage accuracy across all our simulation designs. Another advantage of OLS-based methods over Lasso-based inference methods is that the former do not rely on any sparsity assumptions. This is important because sparsity assumptions may not be satisfied in applications and, as this paper shows, the OVBs of Lasso-based inference procedures can be substantial even when is small and is large and larger than . However, OLS yields somewhat wider confidence intervals than the Lasso-based inference methods, suggesting a trade-off between coverage accuracy and the length of the confidence intervals.

Our analyses suggest two main recommendations concerning the use of post double Lasso in empirical studies. First, if the estimates of are robust to increasing the recommended regularization parameters in both Lasso steps, this suggests that either the OVBs are negligible (Regime (ii)) or under-selection is unlikely (Regime (iii)). In either case, post double Lasso is a reliable and efficient method. Otherwise, modern high-dimensional OLS-based inference methods constitute a possible alternative when is smaller than . Second, our findings highlight the importance of augmenting the final OLS regression in post double Lasso with control variables motivated by economic theory and prior knowledge, as suggested by Belloni et al. (2014).

2 Lasso and post double Lasso

2.1 The Lasso

Consider the following linear regression model

| (3) |

where is an -dimensional response vector, is an matrix of covariates with denoting the th row of , is a zero-mean error vector, and is a -dimensional vector of unknown coefficients.

The Lasso estimator of , which was first proposed by Tibshirani (1996), is given by

| (4) |

where is the regularization parameter. Let and be a fixed design matrix with normalized columns (i.e., for all ). In this example, Bickel et al. (2009) set (where ) to establish upper bounds on with a high probability guarantee. To establish perfect selection, Wainwright (2009) sets proportional to , where is a measure of correlation between the covariates with nonzero coefficients and those with zero coefficients.

Besides the classical choices in Bickel et al. (2009) and Wainwright (2009), other choices of are available in the literature. For instance, Belloni et al. (2012) and Belloni et al. (2016) propose choices that accommodate heteroscedastic and clustered errors. The regularization choice of Belloni et al. (2012), which is recommended by Belloni et al. (2014) for post double Lasso, is based on the following Lasso program:

| (5) |

where are penalty loadings obtained using the iterative algorithm developed in Belloni et al. (2012).

2.2 Post double Lasso

The post double Lasso, introduced by Belloni et al. (2014), essentially exploits the Frisch-Waugh theorem, where the regressions of on and on are implemented with the Lasso:

| (7) | |||||

| (8) |

The final estimator of is then obtained from an OLS regression of on and the union of selected controls

| (9) |

where and .

3 Numerical example

This section presents a simple numerical example illustrating the OVB of post double Lasso. All computations were performed in Matlab (MATLAB, 2020). The Lasso is implemented using the built-in function lasso. We consider a simple but classical setting that is often considered favorable to the performance of the Lasso. The data are simulated according to the structural model (1)–(2), where , , and are independent of each other. Our object of interest is . We set , , , and consider a sparse setting where for and . Following the simulation exercise in Belloni et al. (2014), we vary the population s in (2) and (6) by varying the magnitude of the non-zero coefficients . We employ the regularization parameter choice by Bickel et al. (2009).

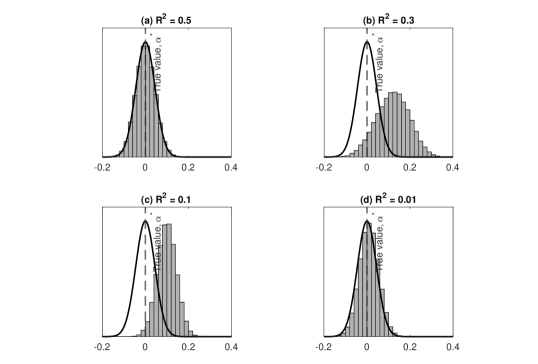

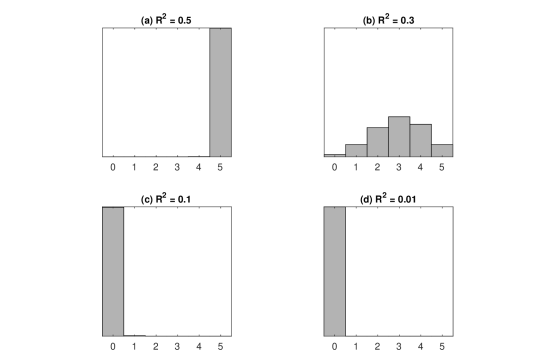

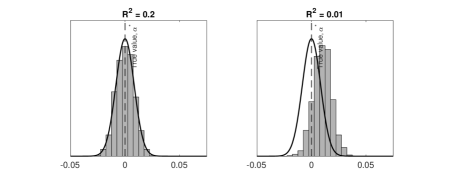

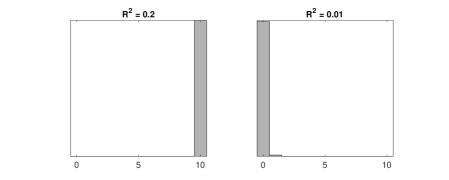

Figure 2 displays the finite sample distribution of post double Lasso for different values of . For comparison, we plot the distribution of the “oracle estimator” of , a regression of on . The finite sample behavior of post double Lasso depends on how many of the relevant controls get selected in both Lasso steps. Figure 3 shows histograms of the number of selected relevant controls. [FIGURES 2 AND 3 HERE.]

When , post double Lasso exhibits an excellent performance. The finite sample distribution is well-approximated by the normal distribution of the oracle estimator and centered at . The reason for the excellent performance is that all controls are selected with high probability such that post double Lasso essentially coincides with an OLS regression of on and the five relevant controls.

Let us now consider what happens if we decrease the magnitude of the coefficients and the implied . For , post double Lasso exhibits a large finite sample bias. Moreover, the distribution of post double Lasso differs substantially from the distribution of the oracle estimator: it has a larger standard deviation and is slightly skewed. This distribution is a mixture of the distributions of OLS conditional on the two Lasso steps selecting different combinations of relevant controls (Panel (b) in Figure 3). For , post double Lasso again exhibits a significant bias. At the same time, the shape of the distribution is similar to that of the oracle estimator. This is because, with high probability, none of the controls gets selected, while the coefficients are large enough to cause an OVB. Decreasing the to reduces the bias. However, it does not change the shape of the finite sample distribution because the selection performance remains unchanged.

The simple numerical example in this section shows that post double Lasso can suffer from OVBs when the two Lasso steps do not select all relevant controls. The magnitude of the coefficients corresponding to the omitted controls can be large enough such that the OVB shifts the location of the finite sample distribution far away from the true value . The issue documented here is not a “small sample” phenomenon but persists even in large sample settings; see Appendix C.1.

4 Theoretical analysis

This section provides a theoretical analysis of the OVB of post double Lasso. Our goal here is to demonstrate that, even in simple examples with classical assumptions (e.g., normal homoscedastic errors, orthogonal designs for the relevant controls), which are often viewed favorable to the performance of Lasso, the finite sample OVBs of post double Lasso can be substantial relative to the standard deviation provided in the existing literature. We first establish a new necessary result for the Lasso’s inclusion and then derive lower and upper bounds on the OVBs of post double Lasso. These results are derived for fixed and are also valid when or . As it will become clear in the following, needs to be large enough for our results to be informative. Without loss of generality, we normalize the matrix such that for all . We focus on fixed designs (of ) to highlight the essence of the problem; see Appendix D for an extension to random designs.

For the convenience of the reader, here we collect the notation to be used in the theoretical analysis. Let denote the dimensional (column) vector of “1”s and is defined similarly. The norm of a vector is denoted by and the norm of a vector is denoted by . The matrix norm (maximum absolute row sum) of a matrix is denoted by . For a vector and a set of indices , let denote the sub-vector (with indices in ) of . For a matrix , let denote the submatrix consisting of the columns with indices in . For a vector , let denote the sign vector such that if , if , and if . Given a set , let denote the cardinality of . We denote by and by .

4.1 Stronger necessary results on the Lasso’s inclusion

Post double Lasso exhibits OVBs whenever the relevant controls are selected in neither (7) nor (8). To the best of our knowledge, there are no formal results strong enough to show that, with high probability, Lasso can fail to select the relevant controls in both steps. Therefore, we first establish a new necessary result for the single Lasso’s inclusion in Lemma 1. To derive this result, we consider the following classical assumptions, which are often viewed favorable to the performance of the Lasso.

Assumption 1.

In terms of model (3), suppose: (i) and ; (ii) is a diagonal matrix; (iii) for some , where is the complement of .

Known as the incoherence condition due to Wainwright (2009), part (iii) in Assumption 1 is needed for the exclusion of the irrelevant controls. Note that if the columns in are orthogonal to the columns in (but within , the columns need not be orthogonal to each other), then . Obviously a special case of this is when the entire consists of mutually orthogonal columns (which is possible if ). To provide some intuition for Assumption 1(iii), let us consider the simple case where and , is centered (such that ), and the columns in are normalized such that the standard deviations of and (for any ) are identical. Then, is simply the maximum of the absolute (sample) correlations between and each of the s with .

Lemma 1 (Necessary result on the Lasso’s inclusion).

In model (3), suppose the s are independent over and , where . Let Assumption 1 hold. We solve the Lasso (4) with

| (10) |

where . Let denote the event that for at least one , and denote the event that for at least one with

| (11) |

Then, we have

| (12) |

where and .

If (11) holds for all , we have

| (13) |

Lemma 1 shows that for large enough , Lasso fails to select any of the relevant covariates with high probability if (11) holds for all . If such conditions hold with respect to both (1) and (2), then Lemma 1 implies that the relevant controls are selected in neither (7) nor (8) with probability at least ; see Panels (c) and (d) of Figure 3 for an illustration.

Let us rewrite (11) as with . Assume that is bounded from above and away from zero; moreover, satisfies (10) and scales as . These conditions imply that in the classical asymptotic framework where and is fixed. This regime of is exactly where classical model selection procedures struggle to distinguish a coefficient from zero in low-dimensional settings.

In the introduction, we have discussed the relationship of our result to that in Lahiri (2021). It is also interesting to compare Lemma 1 with the results in Wainwright (2009). Note that (12) implies for any subject to (11). In comparison, Wainwright (2009) shows that whenever or for some ,

| (14) |

Constant bounds in the form of (14) cannot explain that, with high probability, Lasso fails to select the relevant covariates in both (7) and (8) when is sufficiently large.

Remark 1.

As the choices of regularization parameters used in the vast majority of literature (e.g., Bickel et al., 2009; Wainwright, 2009; Belloni et al., 2012; Belloni and Chernozhukov, 2013; Belloni et al., 2014), the choice of in Lemma 1 is derived from the principle that should be no smaller than with high probability. In particular, our choice for takes the form of that in Wainwright (2009), but ours involves a sharper universal constant. Choosing regularization parameters in this form ensures the exclusion of irrelevant controls. In addition, our choice for has a scaling that can be achieved by the regularization parameters in Belloni et al. (2012), Belloni and Chernozhukov (2013), Belloni et al. (2014), and coincides with that in Bickel et al. (2009) when the columns in are orthogonal to the columns in (but within , the columns need not be orthogonal to each other).

4.2 Lower bounds on the OVBs

In this section, we apply Lemma 1 to derive lower bounds on the OVB of post double Lasso. We consider the structural model (1)–(2), which can be written in matrix notation as

| (15) | |||||

| (16) |

In matrix notation, the reduced form (6) becomes

| (17) |

where and . We make the following assumptions about model (15)–(16).

Assumption 2.

(i) The error terms and consist of independent entries drawn from and , respectively, where and are independent of each other; (ii) the data are centered: , , and ; (iii) and .

Proposition 1 derives a lower bound formula for the OVB of post double Lasso concerning the case where .

Proposition 1 (OVB lower bound).

Remark 2.

In our theoretical results, we implicitly assume is sufficiently large such that . Indeed, probabilities in such a form are often referred to as the “high-probability” guarantees in the literature of (non-asymptotic) high-dimensional statistics concerning large and small enough . Recalling the definitions of and in Section 2.2, the event is the intersection of and an additional event . The event occurs with probability at least , and the event occurs with probability at least . The additional event is needed for us to derive a non-trivial lower bound. In particular, with probability at most , we have , and on this event, the lower bound in Proposition 1 can be negative, which is uninformative for the absolute value of OVBs.

Let us compare the non-asymptotic lower bound in Proposition 1 to the implications of the existing asymptotic results for the bias of post double Lasso. If is bounded away from zero and is bounded from above, the existing theory would imply that the biases of post double Lasso are bounded from above by , irrespective of whether Lasso fails to select the relevant controls or not, and how small and are. The (positive) constant does not depend on , and bears little meaning in the asymptotic framework which simply assumes among other sufficient conditions. [The existing theoretical framework makes it difficult to derive an informative constant, and to our knowledge, the literature provides no such derivation.] The asymptotic upper bound does not distinguish cases that vary in . By contrast, our lower bound analyses are informative about whether the upper bound can be attained by the magnitude of the OVBs and provide explicit constants. These features of our analysis are crucial for understanding the finite sample limitations of post double Lasso. In view of Proposition 1, is not a simple linear function of in general, but roughly linear in when and .

4.3 Key takeaways of our theoretical results

The finite sample behavior of post double Lasso can be characterized by three regimes: (i) non-negligible OVBs, (ii) negligible OVBs, and (iii) absence of OVBs.

Regime (i) (non-negligible OVB). When double under-selection occurs with high probability and is not small enough, according to Proposition 1, the OVB lower bound can be substantial compared to the standard deviation obtained from the asymptotic distribution in Belloni et al. (2014). To gauge the magnitude of the OVB and explain why the confidence intervals proposed in the literature can exhibit under-coverage, it is instructive to compare with , the standard deviation (of ) obtained from the asymptotic distribution in Belloni et al. (2014).666We thank Ulrich Müller for suggesting this comparison. Let us consider an example with , (as in Angrist and Frandsen, 2019), , , , and . If and for all , then when and when ; see Panel (c) of Figures 2 and 3 for an illustration of Regime (i). The OVBs can also be non-negligible when some but not all relevant controls are selected; see Panel (b) of Figures 2 and 3. These results suggest that, non-asymptotically, post double Lasso cannot avoid the “post-selection inference issues” raised in a series of papers by Leeb and Pötscher (e.g., Leeb and Pötscher, 2005, 2008, 2017).

Regime (ii) (negligible OVB). By Lemma 1 and (18), and with probability at least . If is bounded away from zero, is bounded from above, and , by a similar argument as in Belloni et al. (2014), we can show that is approximately normal and centered at zero, even if is bounded away from zero and scales as a constant. Holding other factors constant, the magnitude of OVBs decreases as and decrease (i.e., as and decrease). As and become very small, the relevant controls become essentially irrelevant. Panel (d) of Figures 2 and 3 provides an illustration of Regime (ii).

Regime (iii) (absence of OVB). All relevant controls will be selected when the magnitude of their coefficients is large enough. Specifically, for all , if

| (19) |

then or by standard arguments (e.g., Wainwright, 2019). As a result, (where and are defined in Section 2.2); i.e., the final OLS step (9) includes all the relevant controls with high probability. By similar argument as in Appendix A.2, on the high probability event , the OVB of is zero. Panel (a) of Figures 2 and 3 provides an illustration of Regime (iii).

This “triple-regime” characterization suggests that one may assess the robustness of post double Lasso by increasing the penalty level. If increasing and yields similar estimates , then the underlying model could be in the regime where either the OVBs are negligible (Regime (ii)) or under-selection in both Lasso steps is unlikely (Regime (iii)). By contrast, under Regime (i), the performance of post double Lasso can be quite sensitive to an increase of and . The rationale behind this heuristic lies in that the final step of post double Lasso, (9), is simply an OLS regression of on and the union of selected controls from (7)–(8). A natural question is by how much and should be increased for the robustness checks. For the regularization choice proposed in Belloni et al. (2014), we will show in the simulations of Section 5 that an increase by works well in practice.

Finally, our theoretical results have interesting implications for the comparison between post double Lasso and post single Lasso, where the latter only relies on one Lasso step to select the relevant controls. Note that the magnitude of the OVB of the post single Lasso estimator of also falls into three regimes: (i) non-negligible OVB, (ii) negligible OVB, and (iii) absence of OVB. Thus, qualitatively, the OVBs of post single Lasso and post double Lasso have a similar behavior in finite samples. However, quantitatively, the magnitude of the OVBs can be much larger for the post single Lasso than for the post double Lasso, as illustrated by the following example. If with , and , then the argument for showing Proposition 1 in Appendix A.2 implies that the OVB lower bound scales roughly as for the post single Lasso estimator of (and note that ).

4.4 Additional theoretical results

In this section, we briefly summarize the additional theoretical results that are provided in the appendix. First, we also consider cases where . The conditions required to derive the explicit formula are difficult to interpret when . However, it is possible to provide easy-to-interpret scaling results (without explicit constants) for cases where . Roughly, the scaling of our OVB lower bound can be as large as

and

| (20) |

These results reveal an interesting feature of the post double Lasso. The scaling of the OVB lower bound depends on when the relevant controls are not selected. This is because the error in the reduced form equation (17) involves such that the choice of in (7) depends on via the variance of . By contrast, it is well-known that the OVB of OLS does not depend on when relevant controls are omitted. Interested readers are referred to Propositions 2 and 3 in Appendix A.3 for details.

Second, we also provide upper bounds on the OVB. We have seen in equation (20) that the lower bound on the OVBs scales as when . Interestingly enough, we can also show that the upper bound on the OVB scales as in equation (20) despite and the Lasso being inconsistent in the sense , with high probability. Interested readers are referred to Propositions 4 and 5 in Appendix A.6 for details.

5 Simulations and empirical evidence

To better understand the practical implications of the OVB of post double Lasso, in this section, we present the results from simulations and two empirical applications with widely-used regularization choices available in standard software packages. The analyses were carried out using Matlab (MATLAB, 2020), R (R Core Team, 2021), and Stata (StataCorp., 2021).

5.1 Simulations

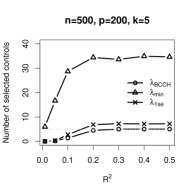

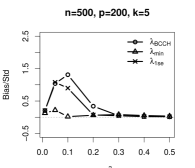

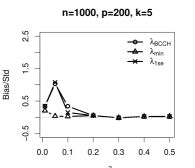

In this section, we present simulation evidence on the performance of post double Lasso with three choices of the regularization parameter: (i) the heteroscedasticity-robust proposal of Belloni et al. (2012, 2014) () implemented using the R-package hdm with the double selection option (Chernozhukov et al., 2016), (ii) the regularization parameter with the minimum cross-validated error () implemented using the R-package glmnet (Friedman et al., 2010), and (iii) the regularization parameter corresponding to the minimum plus one standard deviation cross-validated error () also implemented using glmnet. We use the same type of regularization parameter choice in both Lasso steps.

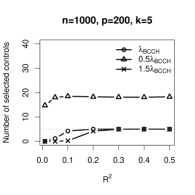

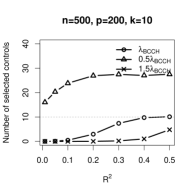

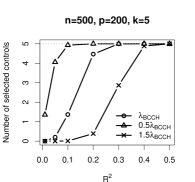

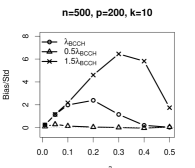

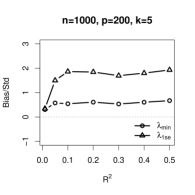

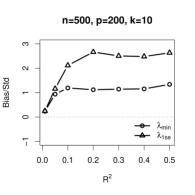

We simulate data according to the DGP of Section 3. To illustrate the role of the sample size and the sparsity parameter , we consider (i) , (ii) , and (iii) . We show results for based on 1,000 simulation repetitions. Appendix C presents additional simulation evidence, where we vary , the distribution of , the true value , and also consider a heteroscedastic DGP.

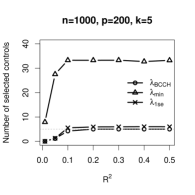

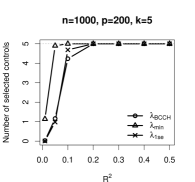

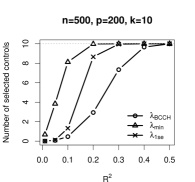

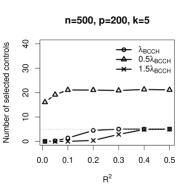

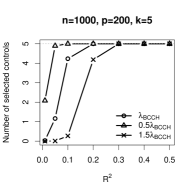

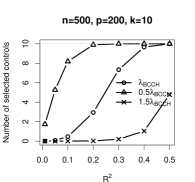

We start by investigating the selection performance of the two Lasso steps of post double Lasso. Panel (a) of Figure 4(b) displays the average number of selected controls (i.e., the cardinality of in (9)) as a function of . Lasso with selects the lowest number of controls. Choosing leads to a somewhat higher number of selected controls and results in moderate over-selection for larger values of . Lasso with selects the highest number of controls and exhibits substantial over-selection. Panel (b) shows the corresponding average numbers of selected relevant controls. [FIGURE 4(b) HERE.]

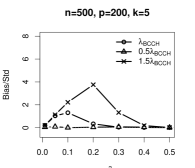

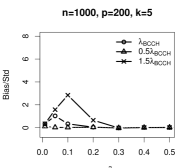

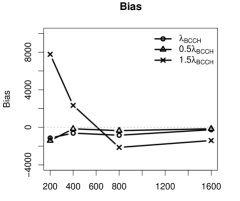

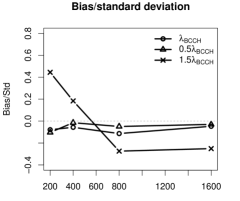

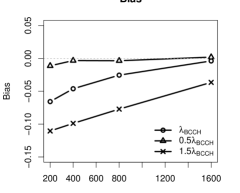

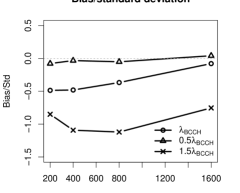

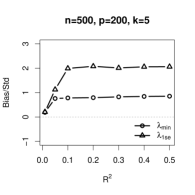

Figure 5 presents evidence on the bias of post double Lasso. To make the results easier to interpret, we report the ratio of the bias to the empirical standard deviation. Post double Lasso with can exhibit biases that are more than two times larger than the standard deviation when . The bias can still be comparable to the standard deviation when . Consistent with our theoretical discussions in Sections 4.2 and 4.3, the relationship between and the ratio of bias to standard deviation is non-monotonic: it is increasing for small and decreasing for larger . The bias is somewhat smaller for . Setting yields the smallest ratio of bias to standard deviation. Finally, we note that when is large enough such that there is no under-selection, post double Lasso performs well and is approximately unbiased for all regularization parameters. [FIGURE 5 HERE.]

The additional simulation evidence reported in Appendix C confirms these results but further shows that is an important determinant of the performance of post double Lasso because of its direct effect on the magnitude of the coefficients and the error variance in the reduced form equation (6). Moreover, we show that, while choosing works well when , this choice can yield poor performances when (see Figure 14). A similar phenomenon arises when using instead of : this choice works well when (see Figure 7 below), but yields biases when . We found that, under our DGPs, this is related to the fact that when , (2) and (6) differ with respect to the underlying coefficients and noise variances, which leads to differences in the (over-)selection behavior of the Lasso. Thus, there is no simple recommendation for how to choose the regularization parameters in practice.

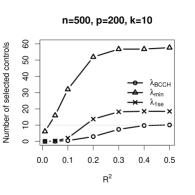

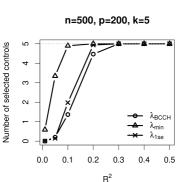

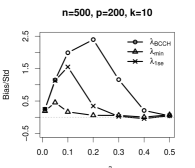

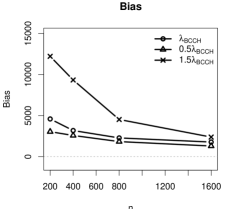

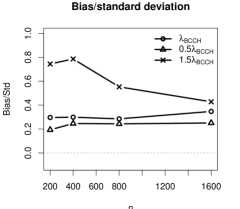

The substantive performance differences between the three regularization choices suggest that post double Lasso is sensitive to the penalty levels in the intermediate case where is small enough so that under-selection occurs but large enough to cause substantial OVBs. To further investigate this issue, we compare the results for , , and . Figure 6(b) displays the average numbers of all selected controls (relevant or not) and selected relevant controls in both Lasso steps. The differences in the selection performance are substantial. Lasso with over-selects for all and , while Lasso with under-selects unless and are large and . The differences get smaller as increases and larger as increases. [FIGURE 6(b) HERE.]

Figure 7 displays the ratio of bias to standard deviation. Choosing yields small biases relative to the standard deviations for all . By contrast, choosing yields biases that can be more than six times larger than the standard deviations when and still substantial when . For very small and large values of , post double Lasso is less sensitive to the penalty level. In Section 7, we discuss how to interpret and use robustness checks with respect to the regularization parameters in empirical applications. [FIGURE 7 HERE.]

In sum, our simulation evidence shows that (i) under-selection can lead to large biases relative to the standard deviations, (ii) the performance of post double Lasso can be very sensitive to the choice of regularization parameters, and (iii) there is no simple recommendation for how to choose the regularization parameters in practice.

5.2 Empirical evidence

5.2.1 The effect of 401k plans on total wealth

We revisit the analysis of the causal effect of eligibility for 401(k) plans () on total wealth ().777 The effect of 401(k) plans is well-studied. We estimate intention to treat effect of 401(k) eligibility on assets as, e.g., in Poterba et al. (1994, 1995, 1998) and Benjamin (2003). Other studies have used 401(k) eligibility to instrument for the actual 401(k) participation status (e.g., Abadie, 2003; Chernozhukov and Hansen, 2004; Belloni et al., 2017b; Wüthrich, 2019). We use the data on households from the 1991 SIPP (Belloni et al., 2017a) analyzed by Belloni et al. (2017b) and Chernozhukov et al. (2018) with high-dimensional methods. We consider two different specifications of the control variables ().

-

1.

Two-way interactions (TWI) specification. We use the same set of low-dimensional control variables as in Benjamin (2003) and Chernozhukov and Hansen (2004): seven income dummies, five age dummies, family size, four education dummies, and dummies for marital status, two-earner status, defined benefit pension status, individual retirement account (IRA) participation status, and homeownership. Following common empirical practice, we augment this baseline specification with all two-way interactions. After removing collinear columns there are control variables.

-

2.

Quadratic spline & interactions (QSI) specification. This is the “Quadratic Spline Plus Interactions specification” of Belloni et al. (2017b, p.265). It contains dummies for marital status, two-earner status, defined benefit pension status, IRA participation status, and homeownership, second-order polynomials in family size and education, a third-order polynomial in age, a quadratic spline in income with six breakpoints, as well as interactions of all the non-income variables with each term in the income spline. After removing collinear columns there are control variables.

Table LABEL:tab:results_401k presents post double Lasso estimates based on the whole sample with , , and . For comparison, we also report OLS estimates with and without controls. For both specifications, the results are qualitatively similar across the different regularization choices and similar to OLS with all controls. This is possible as is much larger than . Nevertheless, there are some non-negligible quantitative differences between the point estimates. A comparison to OLS without control variables shows that omitting controls can yield substantial OVBs in this application.[TABLE LABEL:tab:results_401k HERE.]

To investigate the impact of under-selection, we perform the following exercise. We draw random subsamples of size with replacement from the original dataset. Based on each subsample, we estimate using post double Lasso with , , and and compute the bias as the difference between the average subsample estimate and the point estimate based on the original data with the same type of regularization choice in Table LABEL:tab:results_401k. The results are based on 1,000 simulation repetitions.

Figures 8(b) displays the bias and the ratio of bias to standard deviation for both specifications. We find that post double Lasso can exhibit large finite sample biases. The biases under the QSI specification tend to be smaller (in absolute value) than the biases under the TWI specification. Interestingly, the ratio of bias to standard deviation may not be monotonically decreasing in (in absolute value) due to the standard deviation decaying faster than the bias. Finally, we find that post double Lasso can be very sensitive to the penalty level. [FIGURE 8(b) HERE.]

5.2.2 Racial differences in the mental ability of children

We revisit Fryer and Levitt (2013b)’s analysis of the racial differences in the mental ability of young children based on data from the US Collaborative Perinatal Project (Fryer and Levitt, 2013a). As in the reanalysis of Chernozhukov et al. (2020), we restrict the sample to Black and White children so that our final sample includes observations. We focus on the standardized test score in the Wechsler Intelligence Test at the age of seven as our outcome variable (). The variable of interest () is an indicator for Black children. We use the same specification as in Fryer and Levitt (2013b), excluding interviewer fixed effects. The control variables () include extensive information on socio-demographic characteristics, the home environment, and the prenatal environment; see their Table 1B for descriptive statistics. After removing collinear terms there are controls.

Table LABEL:tab:results_testscores shows the results for post double Lasso with , , and , as well as OLS with and without controls based on the whole sample. Since is much larger than , all methods except for OLS without controls yield similar results. [TABLE LABEL:tab:results_testscores HERE.]

To investigate the impact of under-selection, we draw random subsamples of size with replacement from the original dataset. In each sample, we estimate using post double Lasso with , , and and compute the bias as the difference between the average estimate based on the subsamples and the estimate based on the original data with the same type of regularization choice. The results are based on 1,000 simulation repetitions.

Figure 9 displays the bias and the ratio of bias to standard deviation. While the magnitude of the bias is decreasing in , it can be substantial and larger than the standard deviation when is small. Moreover, the performance of post double Lasso is very sensitive to the choice of the regularization parameters. With , post double Lasso is approximately unbiased for all , whereas, with , the bias is comparable to the standard deviation even when . [FIGURE 9 HERE.]

6 Implications for inference and comparison to high-dimensional OLS-based methods

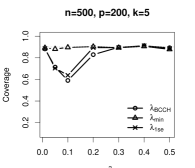

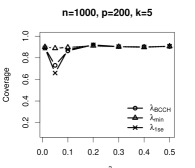

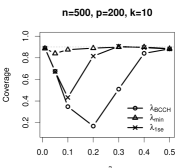

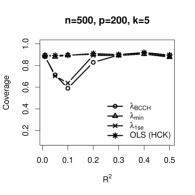

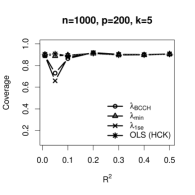

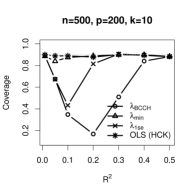

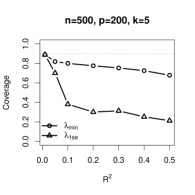

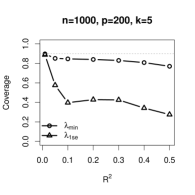

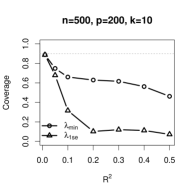

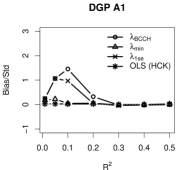

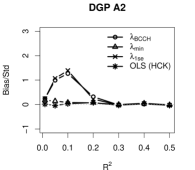

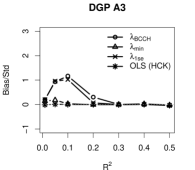

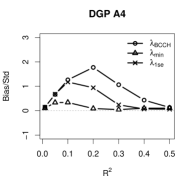

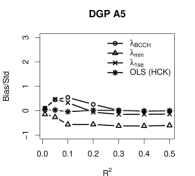

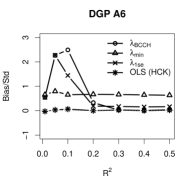

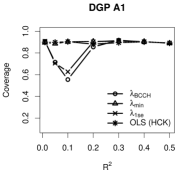

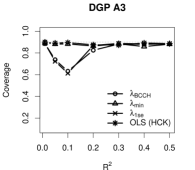

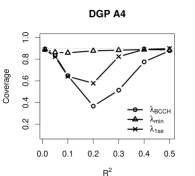

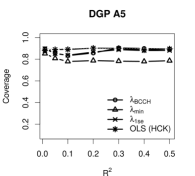

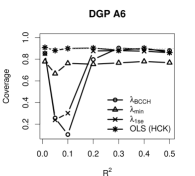

The OVBs have important consequences for making inferences based on post double Lasso. Figure 10 displays the coverage rates of 90% confidence intervals based on the DGPs in Section 5.1 and shows that the OVB of post double Lasso can cause substantial under-coverage even when and . The most important determinant of the under-coverage is the sparsity parameter . Our results show that the requirement on for guaranteeing a good finite sample coverage accuracy for all can be quite stringent. [FIGURE 10 HERE.]

These results prompt the question of how to make inference in a reliable manner when one is concerned about OVBs. In many economic applications, is comparable to but still smaller than . In such settings, OLS-based inference procedures provide a natural alternative to Lasso-based methods. Under classical conditions, OLS is the best linear unbiased estimator and admits exact finite sample inference as long as (recalling that the number of regression coefficients is in (1)). Unlike the Lasso-based inference methods, OLS does not rely on any sparsity assumptions. This is important because sparsity assumptions may not be satisfied in applications and, as we show in this paper, the OVBs of Lasso-based inference procedures can be substantial even when is small and is large and larger than . Indeed, OLS-based inference exhibits desirable optimality properties absent sparsity (or other restrictions) on .888 For one-sided testing problems, the one-sided -test based on OLS with all controls is the uniformly most powerful test; for two-sided problems, the two-sided -test is the uniformly most powerful unbiased test (van der Vaart, 1998). We refer to Section 4 in Armstrong and Kolesar (2016), Section 5.5 in Elliott et al. (2015), and Section 2.1 in Li and Müller (2021) for further discussions.

While OLS is unbiased, constructing standard errors is challenging when is large. For instance, Cattaneo et al. (2018) show that conventional Eicker-White robust standard errors are inconsistent under asymptotics where grows as fast as . This result motivates a recent literature to develop high-dimensional OLS-based inference procedures that are valid in settings with many controls (e.g., Cattaneo et al., 2018; Jochmans, 2020; Kline et al., 2020).

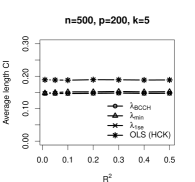

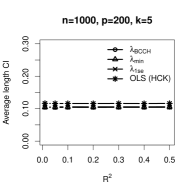

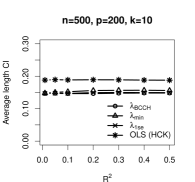

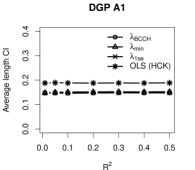

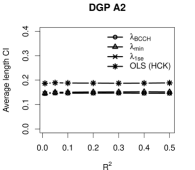

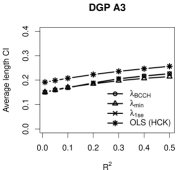

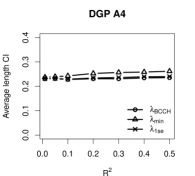

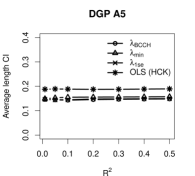

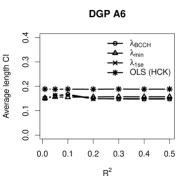

Figures 11(b) compares the finite sample performance of post double Lasso and OLS with the heteroscedasticity robust HCK standard errors proposed by Cattaneo et al. (2018). Panel (a) shows that OLS exhibits close-to-exact empirical coverage rates irrespective of the magnitude of the coefficients and the implied . The additional simulation evidence in Appendix C confirms the excellent performance of OLS with HCK standard errors. Panel (b) displays the average length of 90% confidence intervals and shows that OLS yields somewhat wider confidence intervals than post double Lasso. [FIGURE 11(b) HERE.]

In sum, our simulation results suggest that modern OLS-based inference methods that accommodate many controls may constitute a viable alternative to Lasso-based inference methods. These methods are unbiased and demonstrate an excellent size accuracy, irrespective of the magnitude of the coefficients corresponding to the relevant controls. However, there is a trade-off because OLS yields somewhat wider confidence intervals than post double Lasso.

Finally, it is worth noting that we consider settings where one can easily invert and the OLS and HCK variance estimators are numerically stable. In the case of singular or nearly singular , regularization is often unavoidable; see Section 7 for a discussion of alternatives to OLS and Lasso-based inference methods.

7 Recommendations for empirical practice

Here we summarize the practical implications of our results and provide guidance for empirical researchers.

First, the simulation evidence in Section 5 and Appendix C along with the theoretical results (see Section 4.3) suggest the following heuristic: if the estimates of are robust to increasing the theoretically recommended regularization parameters in the two Lasso steps, post double Lasso could be a reliable and efficient method. Therefore, we recommend to always check whether empirical results are robust to increasing the regularization parameters. Based on our simulations, a simple rule of thumb is to increase by the regularization parameters proposed in Belloni et al. (2014). Robustness checks are standard in other contexts (e.g., bandwidth choices in regression discontinuity designs), and our results highlight the importance of such checks in the context of Lasso-based inference methods.

Second, following Belloni et al. (2014), we recommend to always augment the union of selected controls with an “amelioration” set of controls motivated by economic theory and prior knowledge to mitigate the OVBs.

Third, our simulations show that in moderately high-dimensional settings where is comparable to but smaller than , recently developed OLS-based inference methods that are robust to the inclusion of many controls exhibit better size properties. These simulation results suggest that high-dimensional OLS-based procedures constitute a possible alternative to Lasso-based inference methods.

Forth, OLS-based methods are not applicable when , and the OLS and variance estimators can be numerically unstable under severe multi-collinearity even if . In such cases, regularization is often needed. Ridge regressions, which impose restrictions on the Euclidean norm of , avoid variable selection and may be a useful alternative to the Lasso; see also Armstrong et al. (2020) for related restrictions on .

Finally, in many economic applications, researchers start with a small number of raw controls and want to use a flexible non-parametric model to capture the dependence of outcomes on controls while maintaining a simple parametric form for modeling the variables of interest. Such a specification leads to the classical partially linear models. In fact, Belloni et al. (2014) motivate post double Lasso with these models. If one is concerned about OVBs, inference methods that do not rely on variable selection are natural alternatives to post double Lasso. Under suitable smoothness restrictions on the non-parametric component, inference on the parameter of interest in partially linear models is a well-studied problem (e.g., Robinson, 1988; Newey and McFadden, 1994). The frameworks proposed in these papers can be built upon procedures such as sieves (e.g., Chen, 2007), local non-parametric methods (e.g., Fan and Gijbels, 1996), and kernel ridge regressions (e.g., Schölkopf and Smola, 2002).

8 Conclusion

Given the rapidly increasing popularity of Lasso and Lasso-based inference methods in empirical economic research, it is crucial to better understand the merits and limitations of these new tools, and how they compare to other alternatives such as the high-dimensional OLS-based procedures.

This paper presents theoretical results as well as simulation and empirical evidence on the finite sample behavior of post double Lasso and the debiased Lasso (in the appendix). Specifically, we analyze the finite sample OVBs arising from the Lasso not selecting all the relevant control variables. Our results have important practical implications, and we provide guidance for empirical researchers.

We focus on the implications of under-selection for post double Lasso and the debiased Lasso in linear regression models. However, our results on the under-selection of the Lasso also have important implications for other inference methods that rely on Lasso as a first-step estimator. Towards this end, an interesting avenue for future research would be to investigate the impact of under-selection on the performance of the Lasso-based approaches proposed by Belloni et al. (2014), Farrell (2015), Belloni et al. (2017b), and Chernozhukov et al. (2018) for non-linear models. In moderately high-dimensional settings where is smaller than but comparable to , it would also be interesting to compare the treatment effects estimators in Belloni et al. (2014) to the robust finite sample methods proposed by Rothe (2017).

Finally, this paper motivates further examinations of the practical usefulness of Lasso-based inference procedures and other modern high-dimensional methods. For example, Angrist and Frandsen (2019) present interesting simulation evidence on the finite sample behavior of Lasso-based IV methods (e.g., Belloni et al., 2012). It would be interesting to explore the implications of our theoretical results on the under-selection of the Lasso in problems with weak instruments.

References

- Abadie (2003) Alberto Abadie. Semiparametric instrumental variable estimation of treatment response models. Journal of Econometrics, 113(2):231–263, 2003.

- Angrist and Frandsen (2019) Joshua D. Angrist and Brigham Frandsen. Machine labor. Working Paper, 2019.

- Armstrong and Kolesar (2016) Timothy Armstrong and Michal Kolesar. Optimal inference in a class of regression models. arXiv 1511.06028v2, 2016.

- Armstrong et al. (2020) Timothy B. Armstrong, Michal Kolesár, and Soonwoo Kwon. Bias-aware inference in regularized regression models. arXiv:2012.14823, 2020.

- Belloni and Chernozhukov (2013) Alexandre Belloni and Victor Chernozhukov. Least squares after model selection in high-dimensional sparse models. Bernoulli, 19(2):521–547, 05 2013.

- Belloni et al. (2012) Alexandre Belloni, Daniel Chen, Victor Chernozhukov, and Christian Hansen. Sparse models and methods for optimal instruments with an application to eminent domain. Econometrica, 80(6):2369–2429, 2012.

- Belloni et al. (2014) Alexandre Belloni, Victor Chernozhukov, and Christian Hansen. Inference on treatment effects after selection among high-dimensional controls. The Review of Economic Studies, 81(2):608–650, 2014.

- Belloni et al. (2016) Alexandre Belloni, Victor Chernozhukov, Christian Hansen, and Damian Kozbur. Inference in high-dimensional panel models with an application to gun control. Journal of Business & Economic Statistics, 34(4):590–605, 2016.

- Belloni et al. (2017a) Alexandre Belloni, Victor Chernozhukov, Iván Fernández-Val, and Christian Hansen. Supplement to “Program evaluation and causal inference with high-dimensional data”. Econometrica Supplemental Materials, 2017a.

- Belloni et al. (2017b) Alexandre Belloni, Victor Chernozhukov, Iván Fernández-Val, and Christian Hansen. Program evaluation and causal inference with high-dimensional data. Econometrica, 85(1):233–298, 2017b.

- Benjamin (2003) Daniel J. Benjamin. Does 401(k) eligibility increase saving?: Evidence from propensity score subclassification. Journal of Public Economics, 87(5):1259–1290, 2003.

- Bickel et al. (2009) Peter J. Bickel, Ya’acov Ritov, and Alexandre B. Tsybakov. Simultaneous analysis of lasso and dantzig selector. Ann. Statist., 37(4):1705–1732, 08 2009.

- Breza and Chandrasekhar (2019) Emily Breza and Arun G. Chandrasekhar. Social networks, reputation, and commitment: Evidence from a savings monitors experiment. Econometrica, 87(1):175–216, 2019.

- Caner and Kock (2018) Mehmet Caner and Anders Bredahl Kock. Asymptotically honest confidence regions for high dimensional parameters by the desparsified conservative lasso. Journal of Econometrics, 203(1):143–168, 2018.

- Cattaneo et al. (2018) Matias D. Cattaneo, Michael Jansson, and Whitney K. Newey. Inference in linear regression models with many covariates and heteroscedasticity. Journal of the American Statistical Association, 113(523):1350–1361, 2018.

- Chen (2015) Daniel L. Chen. Can markets stimulate rights? On the alienability of legal claims. The RAND Journal of Economics, 46(1):23–65, 2015.

- Chen (2007) Xiaohong Chen. Chapter 76 large sample sieve estimation of semi-nonparametric models. volume 6 of Handbook of Econometrics, pages 5549–5632. Elsevier, Amsterdam, 2007.

- Chernozhukov and Hansen (2004) Victor Chernozhukov and Christian Hansen. The effects of 401(k) participation on the wealth distribution: An instrumental quantile regression analysis. The Review of Economics and Statistics, 86(3):735–751, 2004.

- Chernozhukov et al. (2016) Victor Chernozhukov, Christian Hansen, and Martin Spindler. hdm: High-dimensional metrics. R Journal, 8(2):185–199, 2016.

- Chernozhukov et al. (2018) Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):1–68, 2018.

- Chernozhukov et al. (2020) Victor Chernozhukov, Ivan Fernandez-Val, Blaise Melly, and Kaspar Wüthrich. Generic inference on quantile and quantile effect functions for discrete outcomes. Journal of the American Statistical Association, 115(529):123–137, 2020.

- Chetverikov et al. (2020) Denis Chetverikov, Zhipeng Liao, and Victor Chernozhukov. On cross-validated lasso in high dimensions. Annal. Stat.(Forthcoming), 40, 2020.

- Cole and Fernando (2020) Shawn A. Cole and Nilesh A. Fernando. ‘Mobile’izing Agricultural Advice Technology Adoption Diffusion and Sustainability. The Economic Journal, 131(633):192–219, 07 2020.

- D’Adamo (2018) Riccardo D’Adamo. Cluster-robust standard errors for linear regression models with many controls. arXiv:1806.07314, 2018.

- Decker and Schmitz (2016) Simon Decker and Hendrik Schmitz. Health shocks and risk aversion. Journal of Health Economics, 50:156 – 170, 2016.

- Elliott et al. (2015) Graham Elliott, Ulrich K. Müller, and Mark W. Watson. Nearly optimal tests when a nuisance parameter is present under the null hypothesis. Econometrica, 83(2):771–11, 2015.

- Enke (2020) Benjamin Enke. Moral values and voting. Journal of Political Economy, 128(10):3679–3729, 2020.

- Fan and Gijbels (1996) Jianqing Fan and Irene Gijbels. Local Polynomial Modelling and Its Applications: Monographs on Statistics and Applied Probability 66 (1st ed.). Routledge, Boca Raton, 1996.

- Farrell (2015) Max H. Farrell. Robust inference on average treatment effects with possibly more covariates than observations. Journal of Econometrics, 189(1):1 – 23, 2015.

- Friedman et al. (2010) Jerome Friedman, Trevor Hastie, and Robert Tibshirani. Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software, 33(1):1–22, 2010.

- Fryer and Levitt (2013a) Roland G. Fryer and Steven D. Levitt. Replication data for: Testing for racial differences in the mental ability of young children. Nashville, TN: American Economic Association [publisher], 2013. Ann Arbor, MI: Inter-university Consortium for Political and Social Research [distributor], 2019-10-11. https://doi.org/10.3886/E112609V1, 2013a.

- Fryer and Levitt (2013b) Roland G. Fryer and Steven D. Levitt. Testing for racial differences in the mental ability of young children. American Economic Review, 103(2):981–1005, April 2013b.

- Homrighausen and McDonald (2013) Darren Homrighausen and Daniel J. McDonald. The Lasso, persistence, and cross-validation. Proceedings of the 30th International Conference on Machine Learning, 28, 2013.

- Homrighausen and McDonald (2014) Darren Homrighausen and Daniel J. McDonald. Leave-one-out cross-validation is risk consistent for Lasso. Machine Learning, 97(1):65–78, Oct 2014.

- Javanmard and Montanari (2014) Adel Javanmard and Andrea Montanari. Confidence intervals and hypothesis testing for high-dimensional regression. Journal of Machine Learning Research, 15(1):2869–2909, 2014.

- Jochmans (2020) Koen Jochmans. Heteroscedasticity-robust inference in linear regression models with many covariates. Journal of the American Statistical Association, 0(0):1–10, 2020.

- Jones et al. (2019) Damon Jones, David Molitor, and Julian Reif. What do Workplace Wellness Programs do? Evidence from the Illinois Workplace Wellness Study*. The Quarterly Journal of Economics, 134(4):1747–1791, 08 2019.

- Kline et al. (2020) Patrick Kline, Raffaele Saggio, and Mikkel Sølvsten. Leave-out estimation of variance components. Econometrica, 88(5):1859–1898, 2020.

- Kolesár and Rothe (2018) Michal Kolesár and Christoph Rothe. Inference in regression discontinuity designs with a discrete running variable. American Economic Review, 108(8):2277–2304, 2018.

- Lahiri (2021) Soumendra N. Lahiri. Necessary and sufficient conditions for variable selection consistency of the lasso in high dimensions. The Annals of Statistics, 49(2):820–844, 2021.

- Leeb and Pötscher (2005) Hannes Leeb and Benedikt M. Pötscher. Model selection and inference: Facts and fiction. Econometric Theory, 21(1):21–59, 2005.

- Leeb and Pötscher (2008) Hannes Leeb and Benedikt M. Pötscher. Can one estimate the unconditional distribution of post-model-selection estimators? Econometric Theory, 24(2):338–376, 2008.

- Leeb and Pötscher (2017) Hannes Leeb and Benedikt M. Pötscher. Testing in the Presence of Nuisance Parameters: Some Comments on Tests Post-Model-Selection and Random Critical Values, pages 69–82. Springer International Publishing, Cham, 2017.

- Li and Müller (2021) Chenchuan Li and Ulrich K. Müller. Linear regression with many controls of limited explanatory power. Quantitative Economics, 12(2):405–442, 2021.

- MATLAB (2020) MATLAB. R2020a. The MathWorks, Inc., 2020.

- Newey and McFadden (1994) Whitney K. Newey and Daniel McFadden. Chapter 36 large sample estimation and hypothesis testing. volume 4 of Handbook of Econometrics, pages 2111–2245. Elsevier, Amsterdam, 1994.

- Poterba et al. (1994) James M. Poterba, Steven F. Venti, and David A. Wise. 401(k) plans and tax-deferred saving. In David A. Wise, editor, Studies in the Economics of Aging. University of Chicago Press, Chicago, 1994.

- Poterba et al. (1995) James M. Poterba, Steven F. Venti, and David A. Wise. Do 401(k) contributions crowd out other personal saving? Journal of Public Economics, 58(1):1–32, 1995.

- Poterba et al. (1998) James M. Poterba, Steven F. Venti, and David A. Wise. Personal retirement saving programs and asset accumulation: Reconciling the evidence. In David A. Wise, editor, Frontiers in the Economics of Aging. University of Chicago Press, Chicago, 1998.

- R Core Team (2021) R Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, 2021.

- Ravikumar et al. (2010) Pradeep Ravikumar, Martin J. Wainwright, and John D. Lafferty. High dimensional ising model selection using -regularized logistic regression. The Annals of Statistics, 38(3):1287–1319, 06 2010.

- Robinson (1988) Peter M. Robinson. Root-n-consistent semiparametric regression. Econometrica, 56(4):931–954, 1988.

- Rothe (2017) Christoph Rothe. Robust confidence intervals for average treatment effects under limited overlap. Econometrica, 85(2):645–660, 2017.

- Schmitz and Westphal (2017) Hendrik Schmitz and Matthias Westphal. Informal care and long-term labor market outcomes. Journal of Health Economics, 56:1 – 18, 2017.

- Schölkopf and Smola (2002) Bernhard Schölkopf and Alexander J. Smola. Learning with kernels: support vector machines, regularization, optimization, and beyond. The MIT Press, Cambridge MA, 2002.

- StataCorp. (2021) StataCorp. Stata Statistical Software: Release 17. College Station, TX, 2021.

- Tibshirani (1996) Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), 58(1):267–288, 1996.

- van de Geer et al. (2014) Sara van de Geer, Peter Bühlmann, Ya’acov Ritov, and Ruben Dezeure. On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42(3):1166–1202, 2014.

- van der Vaart (1998) Adrianus W. van der Vaart. Asymptotic Statistics. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, New York, 1998.

- Vershynin (2012) Roman Vershynin. Introduction to the non-asymptotic analysis of random matrices. In Yonina C. Eldar and GittaEditors Kutyniok, editors, Compressed Sensing: Theory and Applications, pages 210–268. Cambridge University Press, 2012.

- Wainwright (2009) Martin J. Wainwright. Sharp thresholds for high-dimensional and noisy sparsity recovery using -constrained quadratic programming (lasso). IEEE Transactions on Information Theory, 55(5):2183–2202, May 2009.

- Wainwright (2019) Martin J. Wainwright. High-Dimensional Statistics: A Non-Asymptotic Viewpoint. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 2019.

- Wüthrich (2019) Kaspar Wüthrich. A closed-form estimator for quantile treatment effects with endogeneity. Journal of Econometrics, 210(2):219–235, 2019.

- Zhang and Zhang (2014) Cun-Hui Zhang and Stephanie S. Zhang. Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):217–242, 2014.

- Zhang and Cheng (2017) Xianyang Zhang and Guang Cheng. Simultaneous inference for high-dimensional linear models. Journal of the American Statistical Association, 112(518):757–768, 2017.

Figures and tables

Notes: The figure shows the bias (solid line) of the post double Lasso estimator and the average number of selected controls (dotted line) as a function of the magnitude of the coefficients associated with the relevant controls. We generate the data based on (1)–(2), where , , and are independent of each other. We set , , and . We vary the magnitude of and for , where , and set for . We use the Lasso regularization choice by Bickel et al. (2009).

Notes: The grey histograms show the finite sample distributions and the black curves show the densities of the oracle estimators.

| TWI specification () | ||

|---|---|---|

| Method | Point estimate | Robust std. error |

| Post double Lasso () | 6624.47 | 2069.62 |

| Post double Lasso () | 6432.36 | 2073.25 |

| Post double Lasso (1.5) | 7474.51 | 2052.89 |

| OLS with all controls | 6751.91 | 2067.86 |

| OLS without controls | 35669.52 | 2412.02 |

| QSI specification () | ||

| Method | Point estimate | Robust std. error |

| Post double Lasso () | 4558.97 | 2015.90 |

| Post double Lasso () | 5638.04 | 1992.68 |

| Post double Lasso (1.5) | 4406.55 | 2028.20 |

| OLS with all controls | 5988.41 | 2033.02 |

| OLS without controls | 35669.52 | 2412.02 |

| Method | Point estimate | Robust std. error |

|---|---|---|

| Post double Lasso () | -0.6770 | 0.0114 |

| Post double Lasso () | -0.6762 | 0.0114 |

| Post double Lasso (1.5) | -0.6778 | 0.0114 |

| OLS with all controls | -0.6694 | 0.0115 |

| OLS without controls | -0.8538 | 0.0105 |

Online Appendix to “Omitted variable bias of Lasso-based inference methods: A finite sample analysis”

[sections] \printcontents[sections]l1

Notation

Here we collect additional notation that is not provided in the main text. The norm of a vector is denoted by , , where . For a vector , denotes the dimensional vector . For a matrix , the operator norm of is defined as , where . For a square matrix , let and denote its minimum eigenvalue and maximum eigenvalue, respectively.

Appendix A Proofs for the main results

A.1 Lemma 1

Preliminary

We will exploit the following Gaussian tail bound:

for all , where . Note that the constant “” cannot be improved uniformly.

Given where and the tail bound

for , we have

| (21) |

with probability at least . Let the event

| (22) |

Note that .

Lemma 1 relies on the following intermediate results.

(i) On the event , (4) has a unique optimal solution such that for .

(ii) If , conditioning on , we must have

| (23) |

Claim (i) above follows from the argument in Wainwright (2019). To show claim (ii), we develop our own proof.

The proof for claim (i) above is based on a construction called Primal-Dual Witness (PDW) method developed by Wainwright (2009). The procedure is described as follows.

-

1.

Set .

-

2.

Obtain by solving

(24) and choosing such that .999For a convex function , is a subgradient at , namely , if for all .

-

3.

Obtain by solving

(25) and check whether or not (the strict dual feasibility condition) holds.

Lemma 7.23 from Chapter 7 of Wainwright (2019) shows that, if the PDW construction succeeds, then is the unique optimal solution of program (4). To show that the PDW construction succeeds on the event , it suffices to show that . The details can be found in Chapter 7.5 of Wainwright (2019). In particular, under the choice of stated in Lemma 1, we obtain that and hence the PDW construction succeeds conditioning on where .

In summary, conditioning on , under the choice of stated in Lemma 1, program (4) has a unique optimal solution such that for .

Main proof

In what follows, we let

To show (13) in (iv), recall we have established that conditioning on , (4) has a unique optimal solution such that for . Therefore, conditioning on , the KKT condition for (4) implies

| (30) |

for such that .

We first show that . Suppose . We may then condition on the event . Case (i): and . Then, the LHS of (30), ; consequently, the RHS, . However, given the choice of , conditioning on , and consequently, . This leads to a contradiction. Case (ii): and . Then, the LHS of (30), ; consequently, the RHS, . However, given the choice of , conditioning on , and consequently, . This leads to a contradiction.

It remains to show that . We first establish a useful fact under the assumption that . Let us condition on the event . If , we have (i.e., ); similarly, if , then we have (i.e., ). Putting the pieces together implies that, for such that ,

| (31) |

We now show that . Suppose . We may then condition on the event that . Because of (11) and (31), we have . On the other hand, (23) implies that . We have arrived at a contradiction. Consequently, we must have .

In summary, we have shown that and . Claim (i) in “Preliminary” implies that where denotes the event that for some . Therefore, on , none of the events , and can happen. This fact implies that, if (11) is satisfied for all , we must have

A.2 Proposition 1

We first show the case where . Let the events

| (32) | |||||

By tail bounds for Gaussian and Chi-Square variables, we have

| (33) | |||||

In the following proof, we exploit the bound

| (34) | |||||

where the third inequality follows from Lemma 1, which implies with probability at least . Note that , which is a “high probability” guarantee for sufficiently large and . Thus, working with is sensible under an appropriate choice of (as we will see below).

| (35) | |||||

as well as

| (36) | |||||

with probability at least

Conditioning on with , putting the pieces together yields

| (37) |

with probability at least . That is,

When in (15), the reduced form coefficients in (17) coincide with and coincides with . Given the conditions on , , and , we can then apply (13) in Lemma 1 and the fact to show that occurs with probability at least . Note that with the choice , , which is a “high probability” guarantee given sufficiently large .101010Because and are independent of each other, the bound can be further sharpened to . Therefore, it is sensible to work with where

| (38) |

Given , (9) becomes

| (39) |

As a result, we obtain and

| (40) | |||||

where (recall is a fixed design); the last line follows from , the distributional identicalness of and that is a constant over s.

It remains to bound . Note that conditioning on , is positive by (35). Applying a Markov inequality yields

Combining the result above with (40) and maximizing over gives the claim.

We now show the case where . The argument is almost similar. In particular, we use

and replace (35) with

Note that

So the rest of the proof follows from the argument for the case where .

A.3 Lower bounds on the OVBs of post double Lasso when

For functions and , we write to mean that for a universal constant and similarly, to mean that for a universal constant ; when and hold simultaneously. As a general rule, constants denote positive universal constants that are independent of , , , , , and may change from place to place.

Proposition 2 (Scaling of OVB lower bound, Case I).

Let Assumption 1(ii)-(iii) and Assumption 2 hold. Suppose ; the regularization parameters in (7) and (8) are chosen in a similar fashion as in Lemma 1 such that 111111In general, and the iterative algorithm for choosing in Belloni et al. (2014) achieves this scaling. Under the conditions on in Proposition 2, this scaling is equivalent to . and ; for all , and , but and . Let us consider obtained from (9). If , for (or, , for ), then for some positive universal constants ,

| (41) |

where is an event with .

Proposition 3 (Scaling of OVB lower bound, Case II).

Let Assumption 1(ii)-(iii) and Assumption 2 hold. Suppose ; the regularization parameters in (7) and (8) are chosen in a similar fashion as in Lemma 1 such that and ; for all , but . Let us consider obtained from (9).

(i) If for all , then there exist positive universal constants such that

| (42) |

where .

(ii) For all , suppose , and we have either (1) , , , , or (2) , , , . Then there exist positive universal constants such that (42) holds with .

Remark 3.

As the error in the reduced form equation (17) involves , the choice of in (7) depends on the unknown . Therefore, the scaling of the OVB lower bound can involve when the relevant controls are not selected, as suggested by Proposition (3). The dependence on in Proposition (2) has been suppressed because .

A.4 Proof for Proposition 2

Part (i) of Proposition 2 follows immediately from the proof for Proposition 1. It remains to establish part (ii) where , , for all (or, , for all ). Because of these conditions, we have

Note that and

with probability at least . The fact above justifies the choice of stated in 2. We can then apply (13) in Lemma 1 to show that with probability at least . Furthermore, under the conditions on and , (13) in Lemma 1 implies that with probability at least . Therefore, we have

Given , when , the event is not independent of , so (recalling ). Instead of (34), we apply

The rest of the proof follows from the argument for Proposition 1 and the bounds above.

A.5 Proof for Proposition 3

A.6 Upper bounds on the OVBs of post double Lasso

Proposition 4 (Scaling of OVB upper bound, Case I).

Let Assumption 1(ii)-(iii) and Assumption 2 hold. Suppose ; the regularization parameters in (7) and (8) are chosen in a similar fashion as in Proposition 2 such that and ; for all , , and , but and . Let us consider obtained from (9). Then for either , or subject to the conditions in part (ii) of Proposition 2, there exist positive universal constants such that

where and

for any .

Proposition 5 (Scaling of OVB upper bound, Case II).

Let Assumption 1(ii)-(iii) and Assumption 2 hold. Suppose ; the regularization parameters in (7) and (8) are chosen in a similar fashion as in Proposition 3 such that and ; for all , , , but . Let us consider obtained from (9).

(i) If for all , then there exist positive universal constants such that

| (43) |

where and

for any .

(ii) If but for all , then there exist positive universal constants such that (43) holds with and

for any .

A.7 Proof for Proposition 4

Given , note that . We make use of the following bound on Chi-Square variables:

| (44) |

for all . On the event , choosing in (32) and in (44) yields

with probability at least .

We can also show that

Note that where

The inequalities above yield

We have already shown that, conditioning on , with probability at least . As a consequence,

Putting the pieces above together yields

where .

A.8 Proof for Proposition 5

Appendix B Debiased Lasso

In this section, we present theoretical and simulation results on the OVB of the debiased Lasso proposed by van de Geer et al. (2014).

B.1 Theoretical results

The idea of debiased Lasso is to start with an initial Lasso estimate of in equation (1), where

| (45) |

Given the initial Lasso estimator , the debiased Lasso adds a correction term to to reduce the bias introduced by regularization. In particular, the debiased Lasso takes the form

| (46) |

where and is the first row of , which is an approximate inverse of , . Several different strategies have been proposed for constructing the approximate inverse ; see, for example, Javanmard and Montanari (2014), van de Geer et al. (2014), and Zhang and Zhang (2014). We will focus on the widely used method proposed by van de Geer et al. (2014), which sets

where is defined in (8).

Proposition 6 (Scaling of OVB lower bound for debiased Lasso).

Let Assumption 1(ii) and Assumption 2 hold. Suppose: with probability at least , for some such that , where denotes the columns in excluding ; the regularization parameters in (8) and (45) are chosen in a similar fashion as in Lemma 1 such that and ; for all , and , but and . Let us consider obtained from (46). If , then there exist positive universal constants such that

where is an event with .

Proposition 7 (Scaling of OVB upper bound for debiased Lasso).

Let Assumption 1(ii) and Assumption 2 hold. Suppose: with probability at least , for some such that , where denotes the columns in excluding ; the regularization parameters in (8) and (45) are chosen in a similar fashion as in Proposition 6 such that and ; for all , , and , but and . Let us consider obtained from (46). If , then there exist positive universal constants such that

where and

for any .

Remark 5.

B.2 Proof for Propositions 6 and 7

Under the conditions in Proposition 6, (13) in Lemma 1 implies that with probability at least . Conditioning on this event, where . If , under the conditions in Proposition 6, we show that with probability at least . To achieve this goal, we slightly modify the argument for (13) in Lemma 1 by replacing (22) with , where

and denotes the columns in excluding . Note that by (66), and therefore, . We then follow the argument used in the proof for Lemma 1 to show and , where

Moreover, conditioning on , and . Putting these facts together yield the claim that with probability at least .

Letting with and recalling the event in the proof for Proposition 1, we can then show

where such that and the last line follows from the argument used to show (40).

B.3 Simulation evidence

Here we evaluate the performance of the debiased Lasso proposed by van de Geer et al. (2014) based on the simulation setting of the main text. We use cross-validation to choose the regularization parameters as this is the most commonly-used method in this literature. Figure 12(b) presents the results. Debiased Lasso exhibits substantial biases (relative to the standard deviation) and under-coverage for all except very small values of , and its performance is very sensitive to the regularization choice. A comparison to the results in the main text shows that post double Lasso performs better than debiased Lasso.121212We found that one of the reasons for the relatively poor performance of debiased Lasso is that is highly correlated with the relevant controls. Debiased Lasso exhibits a better performance when exhibit a Toeplitz dependence structure as in the simulations reported by van de Geer et al. (2014).

Appendix C Additional simulations for post double Lasso

C.1 Large sample simulations based on the numerical example

The issue documented in the numerical example is not a small-sample phenomenon. Figure 13(b) shows that, even when as in Angrist and Frandsen (2019) and , the finite sample distribution of post double Lasso may not be centered at the true value, and the bias can be large relative to the standard deviation. Compared to the results for , under-selection and large biases occur at lower values of , and all the relevant controls get selected when .

Notes: The grey histograms in Panel (a) show the finite sample distributions and the black curves show the densities of the oracle estimators.

C.2 Additional simulations

In the main text, we consider a setting with normally distributed control variables, normally distributed homoscedastic errors terms, and . Here we provide additional simulation evidence based on a more general model used in the simulations of Belloni et al. (2014):

| (48) | |||||

| (49) |