Combinatorial Auctions with Interdependent Valuations:

SOS to the Rescue

††thanks: The work of A. Eden and M. Feldman was partially supported by the European Research Council under the

European Unions Seventh Framework Programme (FP7/2007-2013) / ERC grant agreement number 337122, by

the Israel Science Foundation (grant number 317/17), and by an Amazon research award. The work of A. Eden and A. Fiat was partially supported by ISF 1841/14. The work of A. Karlin and K. Goldner was supported by NSF grants CCF-1420381 and CCF-1813135. The work of K. Goldner was also supported by a Microsoft Research PhD Fellowship.

Abstract

We study combinatorial auctions with interdependent valuations. In such settings, each agent has a private signal that captures her private information, and the valuation function of every agent depends on the entire signal profile, . The literature in economics shows that the interdependent model gives rise to strong impossibility results, and identifies assumptions under which optimal solutions can be attained. The computer science literature provides approximation results for simple single-parameter settings (mostly single item auctions, or matroid feasibility constraints). Both bodies of literature focus largely on valuations satisfying a technical condition termed single crossing (or variants thereof).

We consider the class of submodular over signals (SOS) valuations (without imposing any single-crossing type assumption), and provide the first welfare approximation guarantees for multi-dimensional combinatorial auctions, achieved by universally ex-post IC-IR mechanisms. Our main results are: 4-approximation for any single-parameter downward-closed setting with single-dimensional signals and SOS valuations; 4-approximation for any combinatorial auction with multi-dimensional signals and separable-SOS valuations; and - and -approximation for any combinatorial auction with single-dimensional signals, with -sized signal space, for SOS and strong-SOS valuations, respectively. All of our results extend to a parameterized version of SOS, -SOS, while losing a factor that depends on .

1 Introduction

Maximizing social welfare with private valuations is a solved problem. The classical Vickrey-Clarke-Grove (VCG) family of mechanisms [Vickrey, 1961; Clarke, 1971; Groves, 1973], of which the Vickrey second-price auction is a special case, are dominant strategy incentive-compatible and guarantee optimal social welfare in general social choice settings.

In this paper, we consider combinatorial auctions, where each agent has a value for every subset of items, and the goal is to maximize the social welfare, namely the sum of agent valuations for their assigned bundles. As a special case of general social choice settings, the VCG mechanism solves this problem optimally, as long as the values are independent.

There are many settings, however, in which the independence of values is not realistic. If the item being sold has money-making potential or is likely to be resold, the values different agents have may be correlated, or perhaps even common. A classic example is an auction for the right to drill for oil in a certain location [Wilson, 1969]. Importantly, in such settings, agents may have different information about what that value actually is. For example, the value of an oil lease depends on how much oil there actually is, and the different agents may have access to different assessments about this. Consequently, an agent might change her own estimate of the value of the oil lease given access to the information another agent has. Similarly, if an agent had access to the results of a house inspection performed by a different agent, that might change her own estimate of the value of a house that is for sale.

The following model due to Milgrom and Weber [1982], described here for single-item auctions, has become standard for auction design in such settings. These are known as interdependent value settings (IDV) 111 See also [Krishna, 2009; Milgrom, 2004]. and are defined as follows:

-

•

Each agent has a real-valued, private signal . The set of signals may be drawn from a (possibly) correlated distribution.

The signals summarize the information available to the agents about the item. For example, when the item to be sold is a house, the signal could capture the results of an inspection and privately collected information about the school district. In the setting of oil drilling rights, the signals could be information that each companies’ engineers have about the site based on geologic surveys, etc.

-

•

The value of the item to agent is a function of the signals (or information) of all agents.

A typical example is when , for some . This type of valuation function captures settings where an agent’s value depends both on how much he likes the item () and on the resale value which is naturally estimated in terms of how much other agents like the item () [Myerson, 1981].

In the economics literature, interdependent settings have been studied for about 50 years (with far too many papers to list; for an overview, see [Krishna, 2009]). Within the theoretical computer science community, interdependent (and correlated) settings have received less attention (see Section 1.4 for further discussion and references).

1.1 Maximizing Social Welfare

Consider the goal of maximizing social welfare in interdependent settings. Here, a direct revelation mechanism consists of each agent reporting a bid for their private signal , and the auctioneer determining the allocation and payments. (It is assumed that the auctioneer knows the form of the valuation functions .)

In interdependent settings, it is not possible222 Except perhaps in degenerate situations. to design dominant-strategy incentive-compatible auctions, since an agent’s value depends on all of the signals, so if, say, agent misreports his signal, then agent might win at a price above her value if she reports truthfully. The next strongest equilibrium notion one could hope for is to maximize efficiency in ex-post equilibrium: bidding truthfully is an ex-post equilibrium if an agent does not regret having bid truthfully, given that other agents bid truthfully. In other words, bidding truthfully is a Nash equilibrium for every signal profile.333 Note that, of course, every ex-post equilibrium is a Bayes-Nash incentive compatible equilibrium, but not necessarily vice versa, and therefore ex-post equilibria are much more robust: they do not depend on knowledge of the priors and bidders need not think about how other bidders might be bidding. This increases our confidence that an ex-post equilibrium is likely to be reached. A strong impossibility result due to Jehiel and Moldovanu [2001] shows that with multi-dimensional signals, maximizing welfare is generically impossible even in Bayes-Nash equilibrium.444For more details on this and other related work, see Section 1.4.

For single-item auctions with single-dimensional signals, a characterization of ex-post incentive compatibility in the IDV setting is known, analogous to Myerson’s characterization for the independent private values model (e.g., Roughgarden and Talgam-Cohen [2016]). The characterization says that there are payments that yield an ex-post incentive-compatible mechanism if and only if the corresponding allocation rule is monotone in each agent’s signal, when all other signals are held fixed. Maximizing efficiency in ex-post equilibrium is also provably impossible unless the valuation functions satisfy a technical condition known as the single-crossing condition [Milgrom and Weber, 1982; d’Aspremont and Gérard-Varet, 1982; Maskin, 1992; Ausubel, 1999; Dasgupta and Maskin, 2000; Athey, 2001; Bergemann et al., 2009; Chawla et al., 2014; Che et al., 2015; Li, 2016; Roughgarden and Talgam-Cohen, 2016]. I.e., the influence of agent ’s signal on his own value is at least as high as its influence on other agents’ values, when all other signals are held fixed 555This implies that given signals , if agent has the highest value when , then agent continues to have the highest value for . This is precisely the monotonicity needed for ex-post incentive compatibility.. When the single-crossing condition holds, there is a generalization of VCG that maximizes efficiency in ex-post equilibrium. (See [Crémer and McLean, 1985, 1988; Krishna, 2009].)

Unfortunately, the single crossing condition does not generally suffice to obtain optimal social welfare in settings beyond that of a single item auction with single-dimensional signals. It is insufficient in fairly simple settings, such as two-item, two-bidder auctions with unit-demand valuations (see Section A), or single-parameter settings with downward-closed feasibility constraints (see Section B).

Moreover, there are many relevant single-item settings where the single-crossing condition does not hold. For example, suppose that the signals indicate demand for a product being auctioned, agents represent firms, and one firm has a stronger signal about demand, but is in a weaker position to take advantage of that demand. A setting like this could yield valuations that do not satisfy the single crossing condition. For a concrete example, consider the following scenario given by [Maskin, 1992] and [Dasgupta and Maskin, 2000].

Example 1.1.

Suppose that oil can be sold in the market at a price of 4 dollars per unit and two firms are competing for the right to drill for oil. Firm 1 has a fixed cost of 1 to produce oil and a marginal cost of 2 for each additional unit produced, whereas firm 2 has a fixed cost of 2 and a marginal cost of 1 for each additional unit produced. In addition, suppose that firm 1 does a private test and discovers that the expected size of the oil reserve is units. Then , whereas . These valuations don’t satisfy the single-crossing condition since firm 1 needs to win when is low and lose when is high.

1.2 Research Problems

This paper addresses the following two issues related to social welfare maximization in the interdependent values model:

-

1.

To what extent can the optimal social welfare be approximated in interdependent settings that do not satisfy the single-crossing condition?

-

2.

How far beyond the single item, single-dimensional setting can we go?

Given the impossibility result of Jehiel and Moldovanu [2001], we ask if it is possible to approximately maximize social welfare in combinatorial auctions with interdependent values?

The first question was recently considered by Eden et al. [2018] who gave two examples pointing out the difficulty of approximating social welfare without single crossing. Example 1.2 shows that even with two bidders and one signal, there are valuation functions for which no deterministic auction can achieve any bounded approximation ratio to optimal social welfare.

Example 1.2 (No bound for deterministic auctions Eden et al. [2018]).

A single item is for sale. There are two players, and , only has a signal . The valuations are

where is an arbitrary large number. If doesn’t win when , then the approximation ratio is infinite. On the other hand, if does win when , then by monotonicity, must also win at , yielding a fraction of the optimal social welfare.

The next example can be used to show that there are valuation functions for which no randomized auction performs better (in the worst case) than allocating to a random bidder (i.e., a factor approximation to social welfare), even if a prior over the signals is known.

Example 1.3 ( lower bound for randomized auctions Eden et al. [2018]).

There are bidders that compete over a single item. For every agent , , and

that is, agent ’s value is high if and only if all other agents’ signals are high simultaneously. When all signals are 1, then in any feasible allocation, there must be an agent which is allocated with probability of at most . By monotonicity, this means that the probability this agent is allocated when the signal profile is is at most as well. Therefore, the achieved welfare at signal profile is at most , while the optimal welfare is , giving a factor gap 666 Eden et al. [2018] show that there exists a prior for which the gap still holds, even if the mechanism knows the prior..

Therefore, some assumption is needed if we are to get good approximations to social welfare. The approach taken by Eden et al. [2018] was to define a relaxed notion of single-crossing that they called -single crossing and then provide mechanisms that approximately maximize social welfare, where the approximation ratio depends on and , the number of agents.

In this paper, we go in a different direction, starting with the observation that in Example 1.3, the valuations treat the signals as highly-complementary–one has a value bounded away from zero only if all other agent’s signals are high simultaneously. This suggests that the case where the valuations treat the signals more like “substitutes” might be easier to handle.

We capture this by focusing on submodular over signals (SOS) valuations. This means that for every and , when signals are lower, the sensitivity of the valuation to changes in is higher. Formally, we assume that for all , for any , , and for any and such that component-wise , it holds that

Many valuations considered in the literature on interdependent valuations are SOS (though this term is not used) Milgrom and Weber [1982]; Dasgupta and Maskin [2000]; Klemperer [1998]. The simplest (yet still rich) class of SOS valuations are fully separable valuation functions 777 This type of valuation function is ubiquitous in the economics literature on inderdependent settings; often with the function simply assumed to be a linear function of the signals (see, e.g., Jehiel and Moldovanu [2001]; Klemperer [1998])., where there are arbitrary (weakly increasing) functions for each pair of bidders and such that

A more general class of SOS valuation functions are functions of the form , where is a weakly increasing concave function.

We can now state the main question we study in this paper: to what extent can social welfare be approximated in interdependent settings with SOS valuations? Unfortunately, Example 1.2 itself describes SOS valuations, so no deterministic auction can achieve any bounded approximation ratio, even for this subclass of valuations. Thus, we must turn to randomized auctions.

1.3 Our Results and Techniques

All of our positive results concern the design of randomized, prior-free, universally ex-post incentive-compatible (IC), individually rational (IR) mechanisms. Prior-free means that the rules of the mechanism makes no use of the prior distribution over the signals, thus need not have any knowledge of the prior.

Our first result provides approximation guarantees for single-parameter downward-closed settings. An important special case of this result is single-item auctions, which was the focus of Eden et al. [2018].

Theorem 4.1 (See Section 4): For every single-parameter downward-closed setting, if the valuation functions are SOS, then the Random Sampling Vickrey auction is a universally ex-post IC-IR mechanism that gives a 4-approximation to the optimal social welfare.

Interestingly, no deterministic mechanism can give better than an -approximation for arbitrary downward-closed settings, even if the valuations are single crossing, and this is tight. Recall that for a single item auction, or even multiple identical items, with single crossing valuations, the deterministic generalized Vickrey auction obtains the optimal welfare Maskin [1992]; Ausubel [1999].

We then turn to multi-dimensional settings. In the most general combinatorial auction model that we consider, each agent has a signal for each subset of items, and a valuation function . For this setting, it is not at all clear under what conditions it might be possible to maximize social welfare in ex-post equilibrium.888 See the related work and also Lemmas A.2 and A.3, which show that under one natural generalization of single-crossing to the setting of two items and two agents that are unit demand, single crossing is not sufficient for full efficiency.

However, rather surprisingly (see the related work section below), for the case of separable SOS valuations999 A valuation is separable-SOS if the valuation for an agent can be split into two parts, an SOS function of all other signals and an arbitrary function of the agents’ own signal. Such valuations generalize the fully separable case discussed above. See definition 2.16, we are able to extend the 4-approximation guarantee to combinatorial auctions.

Theorem 5.1 (See Section 5): For every combinatorial auction, if the valuation functions are separable-SOS, then the Random Sampling VCG auction is a universally ex-post IC-IR mechanism that gives a 4-approximation to the optimal social welfare.

Finally, we consider combinatorial auctions where each agent has a single-dimensional signal , but where the valuation function for each subset of items is an arbitrary SOS valuation function . For this case, we show the following:

Theorems 6.1 and 6.5 (See Sections 6.1 and 6.2): Consider combinatorial auctions with single-dimensional signals, where each signal takes one of possible values. If the valuation functions are SOS, then there exists a universally ex-post IC-IR mechanism that gives a -approximation to the optimal social welfare. If the valuations are strong-SOS 101010See definition 2.14., the approximation ratio improves to .

All of the above results, as well as our lower bounds, are summarized in Table 1. In addition, all of the results in this paper generalize easily, with a corresponding degradation in the approximation ratio, to the weaker requirement of -SOS valuations 111111 A valuation function is -SOS if for all , for all , and for any and such that component-wise , it holds that .

1.3.1 Intuition for results

The fundamental tension in settings with interdependent valuations that is not present in the private values setting is the following. Consider, for example, a single item auction setting where agent 1’s truthful report of her signal increases agent 2’s value. Since, this increases the chance that agent 2 wins and may decrease agent 1’s chance of winning, it might motivate agent 1 to strategize and misreport.

Our approach is to simply prevent this interaction. Without looking at the signals, our mechanism randomly divides the agents into two sets121212 as in [Goldberg et al., 2001].: potential winners and certain losers. Losers never receive any allocation. When estimating the value of a potentially winning agent , we use only the signals of losers and ’s own signal(s). Thus, potential winners can not impact the estimated values and hence allocations of other potential winners. This resolves the truthfulness issue. The remaining question is: can we get sufficiently accurate estimates of the agents’ values when we ignore so many signals?

The key lemma (Lemma 3.1 Section 3) shows that we can do so, when the valuations are SOS. Specifically, for any agent , if all agents other than are split into two random sets (losers) and (potential winners), and the signals of agents in the random subset are “zeroed out”, then the expected value agent has for the item is at least half of her true valuation. That is,

Dealing with combinatorial settings is more involved as the truthfullness characterization is less obvious, but the key ideas of random partitioning and using the signals of certain losers remain at the core of our results.

1.3.2 Additional remarks

While this paper deals entirely with welfare maximization, our results have significance for the objective of maximizing the seller’s revenue. Eden et al. [2018] give a reduction from revenue maximization to welfare maximization in single-item auctions with SOS valuations. Thus, the constant factor approximation mechanism presented in this paper implies a constant factor approximation to the optimal revenue in single-item auctions with SOS valuations. We note that this is the first revenue approximation result that does not assume any single-crossing type assumption ([Chawla et al., 2014; Eden et al., 2018; Roughgarden and Talgam-Cohen, 2016; Li, 2016] require single crossing or approximate single crossing).

Finally, one can easily verify that, based on Yao’s min-max theorem, the existence of a randomized prior-free mechanism that gives some approximation guarantee (in expectation over the coin flips of the mechanism) implies the existence of a deterministic prior-dependent mechanisms that gives the same approximation guarantee (in expectation over the signal profiles).

| Setting | Approximation Guarantees | |||||

|---|---|---|---|---|---|---|

|

|

|||||

|

|

|||||

|

|

|||||

|

|

1.4 More on Related Work

As discussed above, in single-parameter settings, there is an extensive literature on mechanism design with interdependent valuations that considers social welfare maximization, revenue maximization and other objectives. However, the vast majority of this literature assumes some kind of single-crossing condition and, in the context of social welfare, focuses on exact optimization.

There are two papers that we are aware of that study the question of how well optimal social welfare can be approximated in ex-post equilibrium without single-crossing. The first is the aforementioned paper [Eden et al., 2018] on single item auctions with interdependent valuations. They defined a parameterized version of single-crossing, termed -single crossing, where is a parameter that indicates how close is the valuation profile to satisfy single-crossing. For -single crossing valuations, they provide a number of results including a lower bound of on the approximation ratio achievable by any mechanism, a matching upper bound for binary signal spaces, and mechanisms that achieve approximation ratios of and (the first is deterministic and the second is randomized).

Ito and Parkes [2006] also consider approximating social welfare in the interdependent setting. Specifically, they propose a greedy contingent-bid auction (a la [Dasgupta and Maskin, 2000]) and show that it achieves a approximation to the optimal social welfare for goods, in the special case of combinatorial auctions with single-minded bidders.

For multidimensional signals and settings, the landscape is sparser (and bleaker) and, to our knowledge, focuses on exact social welfare maximization. Maskin [1992] has observed that, in general, no efficient incentive-compatible single item auction exists if a buyer’s valuation depends on a multi-dimensional signal.

Jehiel and Moldovanu [2001] consider a very general model in which there is a set of possible alternatives, and a multidimensional signal space, where each agent has a signal for each outcome and other agent . In their model the valuation function of an agent for outcome is linear in the signals, that is, . Thus, their valuation functions are, in one sense, a special case of our separable valuation functions. On the other hand, they are more general in that all quantities depend on the outcome . Thus, there are allocation externalities. Their main result is that, generically, there is no Bayes-Nash incentive compatible mechanism that maximizes social welfare in this setting. However, they do give an ex-post IC mechanism that maximizes social welfare with both information and allocation externalities if the signals are one-dimensional, the valuation functions are linear in the signals, and a single-crossing type condition holds.

Jehiel et al. [2006] go on to show that the only deterministic social choice functions that are ex-post implementable in generic mechanism design frameworks with multidimensional signals, interdependent valuations and transferable utilities, are constant functions.

Finally, Bikhchandani [2006] considers a single item setting with multidimensional signals but no allocation externalities and shows that there is a generalization of single-crossing that allows some social choice rules to be implemented ex-post.

For further analysis and discussion of implementation with interdependent valuations, see e.g., Bergemann and Morris [2005] and McLean and Postlewaite [2015].

For further literature in computer science on interdependent and correlated values, see [Ronen, 2001; Constantin et al., 2007; Constantin and Parkes, 2007; Klein et al., 2008; Papadimitriou and Pierrakos, 2011; Dobzinski et al., 2011; Babaioff et al., 2012; Abraham et al., 2011; Robu et al., 2013; Kempe et al., 2013; Che et al., 2015; Li, 2016; Chawla et al., 2014].

2 Model and Definitions

2.1 Single Parameter Settings

In Section 4, we will consider single-parameter settings with interdependent valuations and downward-closed feasibility constraints. In these settings, a mechanism decides which subset of agents are to receive “service” (e.g., an item). The feasibility constraint is defined by a collection of subsets of agents that may feasibly be served simultaneously. We restrict attention to downward-closed settings, which means that any subset of a feasible set is also feasible. A simple example is a -item auction, where is the collection of all subsets of agents of size at most .

For these settings, we use the interdependent value model of Milgrom and Weber [1982]:

Definition 2.1 (Single Dimensional Signals, Single Parameter Valuations).

Each agent has a private signal . The value agent gives to “receiving service” , is a function of all agents’ signals . The function is assumed to be weakly increasing in each coordinate and strictly increasing in .

2.1.1 Deterministic Mechanisms

Definition 2.2 (Deterministic Single Parameter Mechanisms).

A deterministic mechanism in the downward closed setting is a mapping from reported signals to allocations and payments , where indicates whether or not agent receives service and is the payment of agent . It is required that the set of agents that receive service is feasible, i.e., . (The mechanism designer knows the form of the valuation functions but learns the private signals only when they are reported.)

Definition 2.3 (Agent utility).

Given a deteministic mechanism , the utility of agent when her true signal is , she reports and the other agents report is

Agent will report so as to maximize . We use to denote the utility when she reports truthfully, i.e., .

Definition 2.4 (Deterministic ex-post incentive compatibility (IC)).

A deterministic mechanism in the interdependent setting is ex-post incentive compatible (IC) if, irrespective of the true signals, and given that all other agents report their true signals, there is no advantage to an agent to report any signal other than her true signal. In other words, assuming that are the true signals of other bidders, is maximized by reporting truthfully.

Definition 2.5 (Deterministic ex-post individual rationality (IR)).

A deterministic mechanism in the interdependent setting is ex-post individually rational (IR) if, irrespective of the true signals, and given that all other agents report their true signals, no agent gets negative utility by participating in the mechanism.

If a deterministic mechanism is both ex-post IR and ex-post IR we say that it is ex-post IC-IR.

Definition 2.6.

A deterministic allocation rule is monotone if for every agent , every signal profile of all other agents , and every , it holds that .

Proposition 2.1.

[Roughgarden and Talgam-Cohen, 2016] For every deterministic allocation rule for single parameter valuations, there exist payments such that the mechanism is ex-post IC-IR if and only if is monotone for every agent .

2.1.2 Randomized Mechanisms

Definition 2.7.

A randomized mechanism is a probability distribution over deterministic mechanisms.

Definition 2.8 (Universal ex-post IC-IR).

A randomized mechanism is said to be universally ex-post IC-IR if all deterministic mechanisms in the support are ex-post IC-IR.

2.2 Combinatorial Valuations with Interdependent Signals

Sections 5 and 6 focus on combinatorial auctions, where there are agents and items. In these settings, a mechanism is used to decide how the items are partitioned among the agents. We consider two models for the interdependent valuations: 131313 For other types of signals and interdependent valuation models, see, e.g., Jehiel and Moldovanu [2001].

Definition 2.9 (Single Dimensional Signals, Combinatorial Valuations).

Each agent has a signal . The value agent gives to subset of items , which we denote by , is a function of .

Definition 2.10 (Multidimensional Combinatorial Signals, Combinatorial Valuations).

Here, each agent has a signal for each subset of items; for any agent , we use to denote agent ’s signal for subset of items . The value agent gives to set is denoted by where . We use to denote the set of all signals .

In both cases, each is assumed to be a weakly increasing function of each signal and strictly increasing in (or respectively), and known to the mechanism designer.

We give subsequent definitions only for multidimensional combinatorial signals, as single dimensional signals can be viewed as a special case of multi-dimensional signals where for all .

2.2.1 Deterministic Mechanisms

Definition 2.11 (Deterministic mechanisms for combinatorial settings).

A deteministic mechanism is a mapping from reported signals to allocations (where each ) and payments for all and such that:

-

•

Agent is allocated the set iff ;

-

•

For each agent , there is at most one for which ;

-

•

The sets allocated to different agents do not intersect.

-

•

The payment for agent when her allocation is set is .

Definition 2.12 (Agent Utility).

The utility of agent when her signals are , she reports and the other agents report is

Given a mechanism , agent will report so as to maximize . We use to denote the utility when she reports truthfully, i.e., .

2.2.2 Randomized Mechanisms

As with single parameter mechanisms, a randomized mechanism for a combinatorial setting is a probability distribution over deterministic mechanisms for the combinatorial setting, and a randomized mechanism is said to be universally ex post IC-IR if all deterministic mechanisms in the support are themselves ex-post IC-IR.

2.3 Submodularity over signals (SOS)

As discussed in the introduction, our results will rely on an assumption about the valuation functions that we call submodularity over signals or SOS. The SOS (resp. strong-SOS) notion we use is the same as the weak diminishing returns (resp. strong diminishing returns) submodularity notion in [Bian et al., 2017; Niazadeh et al., 2018]141414 Weak diminishing returns submodularity was introduced in [Soma and Yoshida, 2015], where it’s termed “diminishing returns submodularity”. . SOS was also used in [Eden et al., 2018], generalizing a similar notion in [Chawla et al., 2014].

Definition 2.13 (-approximate submodular-over-signals valuations (-SOS valuations)).

A valuation function is a -SOS valuation if for all , , ,

such that is smaller than or equal to coordinate-wise, it holds that

| (1) |

If satisfies this condition with , we say that is an SOS valuation function.

Definition 2.14 (-approximate strong submodular-over-signals valuations (-strong-SOS valuations)).

The valuation function is a strong-SOS valuation if for any , ,

such that is smaller than or equal to coordinate-wise, it holds that

| (2) |

If satisfies this condition with , we say that ’s valuation functions are “strong-SOS”.

Definition 2.15 (SOS-valuations settings).

We say that a mechanism design setting with interdependent valuations is an SOS-valuations setting or, equivalently, that the agents have SOS-valuations, in each of the following cases:

-

•

Single parameter valuations (as in definition 2.1): for every , the valuation function is SOS.

-

•

Combinatorial valuations with single-parameter signals (as in definition 2.9): for every and , the valuation function is SOS;

-

•

Combinatorial valuations with multi-parameter signals (as in definition 2.10): for every and , is SOS, where .

Similar definitions can be given for -SOS valuation settings and -strong-SOS valuation settings.

Finally, in section 5, we will specialize to the case of separable SOS valuations.

Definition 2.16 (Separable SOS valuations).

We say that a set of valuations as in Definition 2.10 are separable SOS valuations if for every agent and subset of items, can be written as

where and are both weakly increasing and is itself an SOS valuation function.

Observation 2.2.

A separable SOS valuation function is itself an SOS valuation function.

We can similarly define separable -SOS valuations.

2.4 A useful fact about SOS valuations

Lemma 2.3.

Let be a -SOS function. Let and . For any , and such that is smaller than coordinate wise,

Proof.

Let be the elements of . For , let and denote the vectors

Note that , and .

It follows from the -SOS definition that for every ,

| (3) |

where and .

Summing Equation (3) for proves the claim. ∎

3 The Key Lemma

The following is a key lemma which is used for both single parameter and combinatorial settings.

Lemma 3.1.

Let be a -SOS function. Let be a uniformly random subset of , and let . It now holds that

where the expectation is over the random choice of .

Proof.

We consider two equiprobable events,

-

•

is chosen as the random subset.

-

•

is chosen as the random subset.

Normalize the valuations so that and define such that

It follows that

where the first inequality follows from non-negativity of , and the second inequality follows from being -SOS and Lemma 2.3.

Similarly, we have that

It follows that

Solving for equality of the two terms, we get that which implies that

Partition the event space into pairs that partition . For every such pair, it follows that .

We conclude with the following, where the third line follows from the fact that there are such pairs that partition :

as desired. ∎

4 Single-Parameter Valuations

In this section we describe the Random Sampling Vickrey (RS-V) mechanism that achieves a 4-approximation for single-parameter downward-closed environments with SOS valuations and a -approximation for -SOS valuations. We then give a lower bound of 2 and for SOS and -SOS valuations respectively, even in the case of selling a single item.

Let be a downward-closed set system. We present a mechanism that serves only sets in and gets a -approximation to the optimal welfare.

Random Sampling Vickrey (RS-V):

-

•

Elicit bids from the agents.

-

•

Partition the agents into two sets, and , uniformly at random.

-

•

For , let .

-

•

Allocate to a set of bidders in

Theorem 4.1.

For agents with SOS valuations, and for every downward-closed feasibility constraint , RS-V is an ex-post IC-IR mechanism that gives -approximation to the optimal welfare. For -SOS valuations, the mechanism gives a -approximation to the optimal welfare.

Proof.

We first show the allocation is monotone in one’s signal, and hence, by Proposition 2.1, the mechanism is ex-post IC-IR. Fix a random partition .

-

•

Agents in are never allocated anything and thus their allocation is weakly monotone in their signal.

-

•

For an agent , increasing can only increase , whereas it leaves unchanged for all . Thus, this only increases the weight of feasible sets (subsets of in ) that belongs to. Therefore, increasing can only cause to go from being unallocated to being allocated.

For approximation, consider a set that maximizes social welfare. For every , from the Key Lemma 3.1, we have that

| (4) |

For every set , the fact that is downward-closed implies that . Therefore, is eligible to be selected by RS-V as the allocated set of bidders. We have that the values of the bidders we allocate to are at least

as desired. Since the allocated bidders’ true values at are only higher than the proxy values , this continues to hold.

∎

We note that for the case of downward-closed feasibility constraints, even if the valuations satisfy single-crossing, there can be an gap between the optimal welfare and the welfare that the best deterministic mechanism can get. This is stated in Theorem B.1 in Section B.

The following lower bounds, Theorem 4.2 show that even for a single item setting, one cannot hope to get a better approximation than and for SOS and -SOS valuations respectively.The lower bounds apply to arbitrary randomized mechanisms151515 A randomized mechanism takes as input the set of signals and produces as output and for each agent , where is the probability that agent wins and is agent ’s expected payment. Such a mechanism is ex-post IC (but not necessarily universally so) if and only if is monotonically increasing in ..

Theorem 4.2.

No ex-post IC-IR mechanism (not necessarily universal) for selling a single item can get a better approximation than

-

(a)

a factor of 2 for SOS valuations.

-

(b)

a factor of for -SOS valuations.

Proof.

Let be the probability agent is allocated at signal profile . Notice that for every , , otherwise the allocation rule is not feasible.

-

(a)

Consider the case where there are two agents, 1 and 2, and agent 2 has no signal. The valuations are , , and for . It is easy to see the valuations are SOS.

In order to get better than a 2-approximation at , we must have . By monotonicity, this forces as well, and hence by feasibility. This implies that the expected welfare when is , while the optimal welfare when is . For a large , this approaches a 2-approximation. Note that this lower bound applies even given a known prior distribution on the signals in the event that we have a prior on the signals that satisfies: .

-

(b)

Consider the case where there are agents and for every agent . The valuation of agent is

where .

To see that the valuations are -SOS, notice that whenever a signal changes from 0 to 1, the valuation of agent increases by 1 unless all other signals beside ’s are already set to , in which case the valuation increases by . Consider valuation profiles . Note that by monotonicity, for every truthful mechanism, it must be the case that . Since any feasible allocation rule must satisfy , then it must be the case there exists some agent such that , which by monotonicity implies that . However, at profile , while for all , so we get that the expected welfare of the mechanism at is at most while the optimal welfare is . Again, the lower bound also applies to the setting with known priors on the signals using a prior that satisfies: for all and .

∎

5 Combinatorial Auctions with Separable Valuations

In this section we present an ex-post IC-IR mechanism that gives of the optimal social welfare in any combinatorial auction setting with separable SOS valuations (as in Definition 2.16). The mechanism, that we call the Random-sampling VCG auction is a natural extension of the Random-Sampling Vickrey (RS-V) auction presented in Section 4. Note that unlike RS-V, here we need to explicitly define payments so that the obtained mechanism is ex-post IC-IR. We derive VCG-inspired payments which align the objective of the mechanism with that of the agents. Separability is used here, as without it, the payment term would have been affected by the agent’s report (while with separability, only the allocation is affected by it).

Random-Sampling VCG (RS-VCG):

-

•

Agents report their signals .

-

•

Partition the agents into two sets and uniformly at random.

-

•

For each agent and bundle , let

-

•

Let the allocation be

i.e., is the allocation that maximizes the “welfare” using ’s.

-

•

Set the payment for a winning agent receiving set of goods to be:

where

that is, is the weight of the best allocation without agent .

Since the ’s do not depend on agent ’s report (since is in ), doesn’t depend on agent ’s report. Therefore, we can (and will) ignore this term when considering incentive compatibility below.

Note also that since the maximal partition guarantees that , and monotonicity of valuations in signals guarantees that . Therefore, the payments are always nonnegative.

Theorem 5.1.

Random-Sampling VCG is an ex-post IC-IR mechanism that gives a 4-approximation to the optimal social welfare for any combinatorial auction setting with separable SOS valuations.

Proof.

First we show that if the agents bid truthfully, then the mechanism gives a 4-approximation to social welfare. For every agent and bundle ,

| (5) |

where the inequality follows by applying Lemma 3.1 with .

Let be the true welfare maximizing allocation. Then,

where the last inequality follows by substituting in in Equation (5) for every . Since is always at least , this proves the approximation ratio.

Next, we show that RS-VCG is universally ex-post IC. Fix a random partition . Suppose that when all agents bid truthfully

Suppose that all agents but bid truthfully and bids instead of his true signal vector . Let be the resulting allocation. Therefore, agent ’s utility when reporting (after disregarding the term as mentioned above) is:

where is ’s utility for bidding truthfully.

Finally, we show that the mechanism is ex-post IR. Indeed, from above, agent ’s utility when reporting truthfully (and without disregarding the term) is

∎

In the case of separable -SOS valuations, the Random-Sampling VCG is an ex-post IC-IR mechanism that gives -approximation to the social welfare. The proof is identical to Theorem 5.1, except that Equation (5) is changed to

since we apply Lemma 3.1 with an arbitrary .

Remark 5.2.

Theorem 5.1 is clearly analogous to the VCG mechanism for combinatorial auctions with private values. As with VCG for private values, in many cases, there is unlikely to be a polynomial time algorithm to compute allocations and payments. Exceptions include settings we know and love such as unit-demand auctions, additive valuations, etc.

6 Combinatorial Auctions with Single-Dimensional Signals

In this section we consider combinatorial valuations (general combinatorial auctions) with single-dimensional signals (as given by Definition 2.9).

When the signal space of each agent is of size at most , we present a mechanism that gets -approximation for SOS valuations (see Section 6.1), and a mechanism that gets -approximation for strong-SOS valuations (Definition 2.14, see Section 6.2 for details regarding the mechanism). For -SOS and -strong-SOS valuations, the mechanism generalizes to give - and -approximations respectively, as shown in Section C.

We first decompose the optimal welfare into two parts, and . Each part will be covered by a corresponding mechanism. Let be a welfare-maximizing allocation at signal profile , and let be the social welfare of at . Consider the following decomposition:

| (6) | |||||

| (7) |

where Equation (6) follows from the definition of submodularity (and therefore, also follows the definition of strong-submodularity). The last inequality follows from the non-negativity of . The first term in the decomposition represents the contribution of others’ signals to one’s value from his allocated bundle, while the second term represents one’s contribution to his own value. Each of these terms will be targeted using a different mechanism. Whereas the term will be targeted using the same mechanism in both the SOS and strong-SOS cases, the term will be treated differently.

6.1 -approximation for SOS valuations

Suppose for all . The mechanism is as follows:

Mechanism signals High-Low (-HL):

With probability , run Random Threshold; otherwise, run Random Sampling, as described below:

Mechanism Random Threshold

-

•

Choose a random threshold uniformly in .

-

•

Let be the “high” agents; i.e., agents with signal at least , and let be the “low” agents.

-

•

For every high agent and bundle , let

-

•

For every low agent and bundle , let .

-

•

Let the allocation be

(i.e., the allocation that maximizes the “welfare” of high agents using values .)

-

•

Agent that receives bundle pays .

Mechanism Random Sampling

-

•

Split the agents into sets and uniformly at random.

-

•

For each and bundle , let .

-

•

For each and bundle , let .

-

•

Let the allocation be

(i.e., the allocation that maximizes the “welfare” of agents in using values .)

-

•

Charge no payments.

The k-HL mechanism is a random combination of two mechanisms: Random Threshold approximates the welfare contribution of the bidders’ signals to their own value (the SELF term); Random Sampling approximates the welfare contributions of the bidders’ signals to other bidders’ values (the OTHER term). We wish to prove the following theorem.

Theorem 6.1.

For every combinatorial auction setting with SOS valuations, single-dimensional signals, and signal space of size , i.e. , mechanism -HL is an ex-post IC-IR mechanism that gives -approximation to the optimal social welfare.

We first argue that the mechanism is ex-post IC-IR.

Proof of ex-post IC-IR.

Random Sampling is ex-post IC-IR since the agents that might receive items (agents in ) cannot change the allocation since their signals are ignored (and they pay nothing).

As for Random Threshold, consider a threshold chosen by the mechanism. If the agent’s signal is below and the agent reports or above, then his payment, if allocated bundle is ; i.e., the agent’s utility is non-positive. Bidding a different value below will grant the agent no items. If his value is or above, then bidding a different signal above will result in the same outcome, since the sets and remain the same. If he bids a signal below , then he won’t receive any item, and his utility will be 0, while bidding his true signal will result in non-negative utility. ∎

In Lemma 6.3, we prove that Random Sampling covers the component of the social welfare, and in Lemma 6.2, we show that Random Threshold covers the component.

Lemma 6.2.

For SOS valuations, the Random Threshold mechanism gives a -approximation to the SELF component of the optimal social welfare.

Proof.

Consider a threshold chosen in Random Threshold. Whenever is chosen, we have that

Since Random Threshold chooses an allocation that maximizes the welfare under ’s, the value of the allocation is only larger than the left expression above. Because , we get that if was chosen, which happens with probability , the welfare achieved is at least Therefore, the welfare from running Random Threshold is at least

∎

Lemma 6.3.

For SOS valuations, the Random Sampling mechanism gives a -approximation to the OTHER component of the optimal social welfare.

Proof.

Consider a set . Using an application of the Key Lemma 3.1 with respect to , we see that

| (8) |

Therefore, the expected weight of the allocation using weights ’s is

Since the mechanism chooses the optimal allocation according to the ’s, its weight can only be larger. Moreover, since , the welfare achieved by the mechanism is at least , as desired. ∎

We conclude by proving the claimed approximation ratio.

Proof of approximation.

6.2 -Approximation with Strong-SOS Valuations

Strong-SOS valuations means the effect on the valuation is concave in one’s own signal. This allows us to use a bucketing technique in order to give an -approximation to the SELF component in the decomposition depicted by Equation (7).

Consider the SELF term in Equation (7). We can bound this term as follows:

| (9) | |||||

where the inequality follows the definition of strong-SOS valuations.

We introduce mechanism Random Bucket to give an -approximation to the upper bound in Equation (9).

Mechanism Random Bucket:

-

•

choose uniformly in .

-

•

Let be the agents with signal at least and .

-

•

For and bundle , let (and for ).

-

•

Let the allocation be

(i.e., the allocation that maximizes the “welfare” of high agents using values .)

-

•

Agent that receives bundle pays .

We show the following approximation guarantee regarding Random Bucket.

Lemma 6.4.

For strong-SOS valuations, the Random Bucket mechanism is ex-post IC-IR and gives a approximation to the SELF component of the optimal social welfare.

Proof.

The proof of ex-post IC-IR is identical to that of mechanism Random Threshold, as both are threshold-based mechanisms. The proof of the approximation guarantee is also very similar to that of Random Threshold.

Consider a threshold for chosen in Random Bucket. Whenever is chosen, we have that

Since Random Bucket chooses an allocation that maximizes the ’s, the value of the allocation is only larger. Because , we get that if was chosen, which happens with probability , the welfare achieved is at least Therefore, the welfare from running Random Bucket is at least

∎

Mechanism -signals Strong-SOS (-SS) runs Random Bucket with probability and mechanism Random Sampling with probability .

Theorem 6.5.

For every combinatorial auction with single-dimensional signals with strong-SOS valuations and signal space of size , i.e. , mechanism -SS is ex-post IC-IR, and gives -approximation to the optimal social welfare.

Proof.

We already established that both Random Bucket and Random Sampling are ex-post IC-IR, hence -SS is ex-post IC-IR as well. As for the approximation, according to Lemma 6.4, with probability we get -approximation to SELF, and according to Lemma 6.3, with probability we get a -approximation to OTHER. Overall, the expected welfare is at least

as desired.

∎

7 Open Problems

Our analysis and results suggest many open problems:

-

•

For combinatorial auctions with multi-dimensional signals: is separability a necessary condition for achieving constant approximation to welfare? This problem is open even for single-dimensional signals, and even for “simple” combinatorial valuations, such as unit-demand.

-

•

For single-parameter SOS valuations, downward closed feasibility, and single-dimensional signals, closing the gap between and is open.

-

•

The exact same gap applies for combinatorial, separable-SOS valuations with multi-dimensional signals.

-

•

How does the distinction between SOS and strong-SOS affect the problems above, if at all?

-

•

When considering the relaxation of SOS valuations to -SOS valuations, there is a gap between the positive and negative results with respect to the dependence on .

More generally, what other classes of valuations give rise to approximately efficient mechanisms in settings with interdependent valuations?

Acknowledgements We gratefully thank an anonymous referee who pointed out that many of the proofs in this paper, hold, with minor adjustments, for subadditive over signals valuations. Surprisingly, submodular over signals valuations are not a special case of subadditive over signals valuations. However, strong submodular over signals valuations are so. The actual situation is rather subtle and we will address this issue in a subsequent version of this paper.

References

- Abraham et al. [2011] Ittai Abraham, Susan Athey, Moshe Babaioff, and M Grubb. Peaches. Lemons, and Cookies: Designing Auction Markets with Dispersed Information, 2011.

- Athey [2001] Susan Athey. Single crossing properties and the existence of pure strategy equilibria in games of incomplete information. Econometrica, 69(4):861–889, 2001. ISSN 00129682, 14680262.

- Ausubel [1999] Lawrence M Ausubel. A generalized vickrey auction. Econometrica, 1999.

- Babaioff et al. [2012] Moshe Babaioff, Robert Kleinberg, and Renato Paes Leme. Optimal mechanisms for selling information. In Proceedings of the 13th ACM Conference on Electronic Commerce, EC ’12, pages 92–109, New York, NY, USA, 2012. ACM. ISBN 978-1-4503-1415-2.

- Bergemann and Morris [2005] Dirk Bergemann and Stephen Morris. Robust mechanism design. Econometrica, 73(6):1771–1813, 2005.

- Bergemann et al. [2009] Dirk Bergemann, Xianwen Shi, and Juuso Välimäki. Information acquisition in interdependent value auctions. Journal of the European Economic Association, 7(1):61–89, 2009.

- Bian et al. [2017] Andrew An Bian, Kfir Yehuda Levy, Andreas Krause, and Joachim M. Buhmann. Non-monotone continuous dr-submodular maximization: Structure and algorithms. In Advances in Neural Information Processing Systems 30: Annual Conference on Neural Information Processing Systems 2017, 4-9 December 2017, Long Beach, CA, USA, pages 486–496, 2017.

- Bikhchandani [2006] Sushil Bikhchandani. Ex post implementation in environments with private goods. 2006.

- Chawla et al. [2014] Shuchi Chawla, Hu Fu, and Anna Karlin. Approximate revenue maximization in interdependent value settings. In Proceedings of the Fifteenth ACM Conference on Economics and Computation, pages 277–294, New York, NY, USA, 2014. ACM. ISBN 978-1-4503-2565-3.

- Che et al. [2015] Yeon-Koo Che, Jinwoo Kim, and Fuhito Kojima. Efficient assignment with interdependent values. Journal of Economic Theory, 158:54–86, 2015.

- Clarke [1971] Edward H Clarke. Multipart pricing of public goods. Public choice, 11(1):17–33, 1971.

- Constantin and Parkes [2007] Florin Constantin and David C. Parkes. On revenue-optimal dynamic auctions for bidders with interdependent values. In AMEC/TADA, volume 13 of Lecture Notes in Business Information Processing, pages 1–15. Springer, 2007.

- Constantin et al. [2007] Florin Constantin, Takayuki Ito, and David C. Parkes. Online auctions for bidders with interdependent values. In AAMAS, page 110. IFAAMAS, 2007.

- Crémer and McLean [1985] Jacques Crémer and Richard P. McLean. Optimal selling strategies under uncertainty for a discriminating monopolist when demands are interdependent. Econometrica, 53(2):345–361, 1985. ISSN 00129682, 14680262.

- Crémer and McLean [1988] Jacques Crémer and Richard P. McLean. Full extraction of the surplus in bayesian and dominant strategy auctions. Econometrica, 56(6):1247–1257, 1988. ISSN 00129682, 14680262.

- Dasgupta and Maskin [2000] Partha Dasgupta and Eric Maskin. Efficient auctions. The Quarterly Journal of Economics, 115(2):341–388, 2000.

- d’Aspremont and Gérard-Varet [1982] C d’Aspremont and L.-A Gérard-Varet. Bayesian incentive compatible beliefs. Journal of Mathematical Economics, 10(1):83 – 103, 1982. ISSN 0304-4068.

- Dobzinski et al. [2011] Shahar Dobzinski, Hu Fu, and Robert D. Kleinberg. Optimal auctions with correlated bidders are easy. In Proceedings of the Forty-third Annual ACM Symposium on Theory of Computing, pages 129–138, New York, NY, USA, 2011. ACM. ISBN 978-1-4503-0691-1.

- Eden et al. [2018] Alon Eden, Michal Feldman, Amos Fiat, and Kira Goldner. Interdependent values without single-crossing. In Proceedings of the 2018 ACM Conference on Economics and Computation, EC ’18, pages 369–369, New York, NY, USA, 2018. ACM. ISBN 978-1-4503-5829-3.

- Goldberg et al. [2001] Andrew V. Goldberg, Jason D. Hartline, and Andrew Wright. Competitive auctions and digital goods. In Proceedings of the 12th Annual ACM-SIAM Symposium on Discrete Algorithms, pages 735–744, Philadelphia, PA, USA, 2001. ISBN 0-89871-490-7.

- Groves [1973] Theodore Groves. Incentives in teams. Econometrica: Journal of the Econometric Society, pages 617–631, 1973.

- Ito and Parkes [2006] Takayuki Ito and David C. Parkes. Instantiating the contingent bids model of truthful interdependent value auctions. In AAMAS, pages 1151–1158. ACM, 2006.

- Jehiel and Moldovanu [2001] Philippe Jehiel and Benny Moldovanu. Efficient design with interdependent valuations. Econometrica, 69(5):1237–1259, 2001.

- Jehiel et al. [2006] Philippe Jehiel, Moritz Meyer-ter Vehn, Benny Moldovanu, and William R Zame. The limits of ex post implementation. Econometrica, 74(3):585–610, 2006.

- Kempe et al. [2013] David Kempe, Vasilis Syrgkanis, and Eva Tardos. Information asymmetries in common-value auctions with discrete signals. SSRN eLibrary, 2013.

- Klein et al. [2008] Mark Klein, Gabriel A. Moreno, David C. Parkes, Daniel Plakosh, Sven Seuken, and Kurt C. Wallnau. Handling interdependent values in an auction mechanism for bandwidth allocation in tactical data networks. In NetEcon, pages 73–78. ACM, 2008.

- Klemperer [1998] Paul Klemperer. Auctions with almost common values: The wallet game’and its applications. European Economic Review, 42(3):757–769, 1998.

- Krishna [2009] Vijay Krishna. Auction theory. Academic press, 2009.

- Li [2016] Yunan Li. Approximation in mechanism design with interdependent values. Games and Economic Behavior, 2016.

- Maskin [1992] Eric Maskin. Auctions and privatization. Privatization, H. Siebert, ed. (Institut fur Weltwirtschaften der Universita¨t Kiel: 1992), pages 115––136, 1992.

- McLean and Postlewaite [2015] Richard McLean and Andrew Postlewaite. Implementation with interdependent valuations. Theoretical Economics, 10(3), 2015.

- Milgrom and Weber [1982] Paul R Milgrom and Robert J Weber. A theory of auctions and competitive bidding. Econometrica: Journal of the Econometric Society, pages 1089–1122, 1982.

- Milgrom [2004] Paul Robert Milgrom. Putting auction theory to work. Cambridge University Press, 2004.

- Myerson [1981] Roger B Myerson. Optimal auction design. Mathematics of operations research, 6(1):58–73, 1981.

- Niazadeh et al. [2018] Rad Niazadeh, Tim Roughgarden, and Joshua R. Wang. Optimal algorithms for continuous non-monotone submodular and dr-submodular maximization. In Annual Conference on Neural Information Processing Systems 2018, 3-8 December 2018, Montréal, Canada., pages 9617–9627, 2018.

- Papadimitriou and Pierrakos [2011] Christos H. Papadimitriou and George Pierrakos. On optimal single-item auctions. In Proceedings of the 43rd ACM Symposium on Theory of Computing, STOC 2011, San Jose, CA, USA, 6-8 June 2011, pages 119–128, 2011.

- Robu et al. [2013] Valentin Robu, David C. Parkes, Takayuki Ito, and Nicholas R. Jennings. Efficient interdependent value combinatorial auctions with single minded bidders. In IJCAI, pages 339–345. IJCAI/AAAI, 2013.

- Rochet [1987] Jean-Charles Rochet. A necessary and sufficient condition for rationalizability in a quasi-linear context. Journal of mathematical Economics, 16(2):191–200, 1987.

- Ronen [2001] Amir Ronen. On approximating optimal auctions. In Proceedings of the 3rd ACM conference on Electronic Commerce, pages 11–17. ACM, 2001.

- Roughgarden and Talgam-Cohen [2016] Tim Roughgarden and Inbal Talgam-Cohen. Optimal and robust mechanism design with interdependent values. ACM Trans. Econ. Comput., 4(3):18:1–18:34, June 2016. ISSN 2167-8375.

- Soma and Yoshida [2015] Tasuku Soma and Yuichi Yoshida. A generalization of submodular cover via the diminishing return property on the integer lattice. In Advances in Neural Information Processing Systems 28, pages 847–855. Curran Associates, Inc., 2015.

- Vickrey [1961] William Vickrey. Counterspeculation, auctions, and competitive sealed tenders. The Journal of finance, 16(1):8–37, 1961.

- Vohra [2007] Rakesh Vohra. Paths, cycles and mechanism design. Preprint, 2007.

- Wilson [1969] Robert B Wilson. Competitive Bidding with Disparate Information. Management Science, 15(7):446–452, 1969.

Appendix A Unit-Demand Valuations with Single-Crossing

Whereas single-crossing is a strong enough condition to implement the fully efficient mechanism in a variety of single-parameter environments, generalizations of this condition fail even in the simplest multi-parameter environments. We consider the case where bidders are unit demand and each bidder has a scalar as a signal. We define single-crossing for this setting as follows.

Definition A.1 (Single-crossing for unit-demand valuations).

A valuation profile is said to be single crossing if for every agent , signals , item and agent ,

| (10) |

In this section, we show that in the case two non-identical items are for sale, and the valuations are unit demand and satisfy single-crossing as defined in Equation (10), any truthful mechanism is bounded away from achieving full efficiency.

In order to give the lower bound, we first give a characterization of ex-post IC and IR mechanisms in multi-dimensional environments in interdependent values settings (Section A.1). We then turn to prove the lower bound (Section A.2).

A.1 Cycle Monotonicity

In the IPV model, Rochet [1987] introduced cycle monotonicity as a necessary and sufficient condition on the allocation to be implementable in dominant strategies (DSIC) for multidimensional environments. It was noticed that a straightforward analogue holds for the IDV value model, for ex-post implementability (EPIC) (in Vohra [2007], this fact is stated without a proof).

Fix a feasible allocation rule , where is the probability agent receives a bundle under bid profile . For each agent , consider the graph where there is a vertex for each signal profile , and there is a directed edge from to if . The weight of edge is

The following theorem states that a necessary and sufficient condition for ex-post implementability of is that for every agent , every directed cycle in is non-negative. The proof is a straightforward adjustment of the original proof in Rochet [1987], and is given below for completeness.

Theorem A.1.

The allocation rule is implementable by an ex-post IC mechanism if and only if for every agent , all directed cycles in have non-negative weight.

Proof.

We first show that if the allocation rule is implementable, then there are no negative cycles. Fix some payment rule , where is the payment of agent under bid profile . Let be the real signals of all bidders except , and consider a cycle in , where for . Since is an ex-post IC mechanism, for every true signal , agent is at least as well off bidding than any other bid . We get that

Summing over the above inequalities and using the convention that , we get that

where the LHS of the last inequality is exactly the weight of the cycle.

We now show how to compute payments that implement a given allocation rule that induces no negative cycles for any and . Given , one can compute payments as follows.

-

•

Add a dummy node with edges of weight 0 to all nodes in .

-

•

For every node of , let be the distance of the shortest path from to .

-

•

Set .

Fix signals of the other players . Let be player ’s true signal and be some other possible signal for . Denote and . Consider the nodes and in . Since is the length of the shortest path from , it must be that

where is the weight of the edge from to . Substituting , , and , we get

as desired. ∎

A.2 Lower Bounds for Deterministic and Randomized Mechanisms

Lemma A.2.

There exists a setting with two items and two agents with unit-demand and single crossing valuations, such that no deterministic truthful mechanism achieves more than of the optimal welfare.

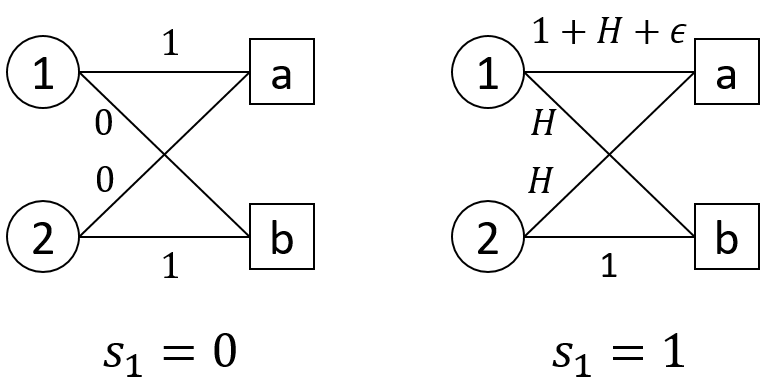

Proof.

Consider the setting depicted in Figure 1, with two agents, 1 and 2, and two items, and . and is fixed. The values at are

and at are

for some arbitrarily large and a sufficiently small . One can easily verify that the valuations satisfy Equation (10), and hence single crossing; indeed, when agent 1’s signal increases, the valuation of agent 1 for each one of the item increases by more than the change in agent 2’s valuation.

We show that no deterministic truthful mechanism can get better than 2-approximation. In order to get better than 2-approximation, the mechanism must allocate item to agent 1 and item to bidder 2 at signal . At , allocating item to agent 1 and item to agent 2 obtains a welfare of , while any other allocation obtains at most a welfare of . Since can be arbitrarily large, one must allocate item to agent 1 and item to agent 2 at signal in order to get an approximation ratio better than 2. Consider such an allocation rule , and the graph . This graph has one cycle, with one edge from to and one edge from to . The weight of this cycle is

Based on Theorem A.1, this implies that this allocation rule is not implementable ∎

Lemma A.3.

There exists a setting with two items and two agents with unit-demand and single crossing valuations, such that no randomized truthful mechanism achieves more than of the optimal welfare.

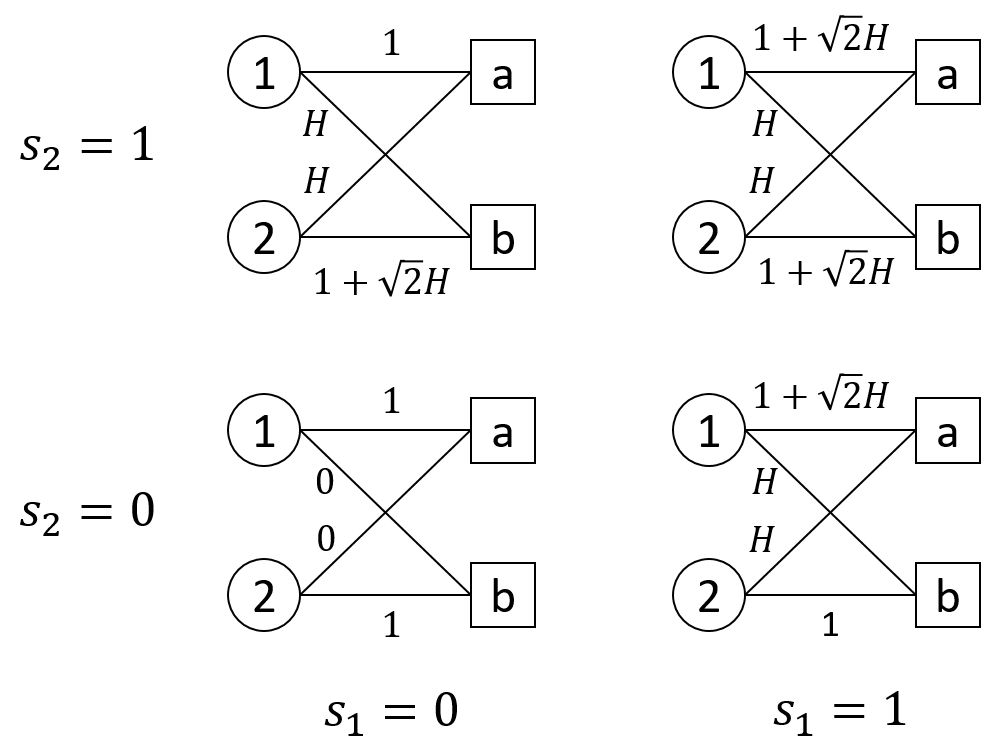

Proof.

Consider the setting depicted in Figure 2, with two agents, 1 and 2, and two items, and . and . The values are

for an arbitrarily large . One can easily verify that the valuations are single crossing. We claim that the following equalities hold with respect to the allocation rule of the optimal randomized mechanism:

-

(a)

For every , and .

-

(b)

For some , and .

-

(c)

For some , and .

We next prove the above equalities.

-

(a)

Consider some implementable allocation rule , and consider the allocation rule where and for every . Note that the valuations are symmetric; i.e., the role of item (resp. ) for agent 1 is the same as the role of items (resp. ) for agent 2. By symmetry, is implementable if and only if is implementable, and both allocation rules have the same approximation guarantee. Clearly, an allocation rule that applies allocation rules and , with probability each, maintains the same approximation guarantee. Moreover, this allocation rule satisfies the desired property.

-

(b)

The optimal mechanism gains nothing from assigning any positive probability for allocating item to agent 1 under signal profile . This is because item grants no value to agent 1, and in terms of incentives, it can only incentivize agent 1 to misreport his signal at signal profile . Analogously, the optimal mechanism gains nothing from assigning any positive probability for allocating item to agent 2 under signal profile . By (a), for some . To conclude the proof of (b), note that the only other feasible set for the agents is the empty set (otherwise, agent 1 has some probability to get item and agent 2 has some probability to get item ).

-

(c)

Consider and the cycle in . This is the only cycle that contains the node in . Assume . Transferring probability from to decreases the weight of the edge by , and increases the weight of the edge by . Therefore, its net effect on the weight of is positive. Transferring probability from to does not affect the weight of the edge , and increases the weight of the edge by . Therefore, its net effect on the weight of is positive. Since transferring to and increases welfare and does not violate cycle monotonicity, the optimal mechanism clearly assigns no probability to .

Now assume . By Moving this probability to , we get the same expected welfare at , and the weight of the edges in does not change. Therefore, we may also assume the mechanism does not assign positive utility to .

According to Theorem A.1, in any truthful mechanism, the weight of the cycle must be non-negative . This translates to the following condition.

In the optimal mechanism, will be as large as possible in order to maximize the expected welfare at signal profile . Hence, we can assume . Therefore, the approximation ratio at profile is at most . At profile , if item is allocated to agent 1 (which happens with probability ), the welfare of the mechanism is at most , while the welfare of the optimal allocation is . As can be arbitrarily large, this approximation ratio tends to . Therefore, the approximation ratio at profile is at most . The optimal mechanism would balance between the approximation ratio at and at , therefore uses that solves

Solving for , we get . This leads to an approximation ratio of at most , as promised. ∎

Appendix B Lower Bound for Deterministic Mechanisms with Single-Crossing SOS Valuations.

We show that for downward-closed environments, even if valuations satisfy a single-crossing condition and are SOS, any deterministic mechanism cannot obtain a better approximation to the optimal welfare than .

Theorem B.1.

There exists a downward-closed environment with valuations that satisfy single-crossing for which no deterministic mechanism more than a fraction of the optimal welfare.

Proof.

Consider a set of bidders, where , where is the power set of the set . Only agent 1 has a signal , and other players do not have signals. The valuations are:

for an arbitrary large value . Once can easily verify these valuations satisfy single-crossing and SOS.

Any deterministic mechanism that wants to get any approximation to the social welfare must allocate to agent 1 when . In addition, if a deterministic mechanism wants to get a better approximation than to the optimal social welfare, agent 1 cannot be allocated when . Otherwise, none of the bidders in can get allocated because the only set in that contains agent 1 is the singleton set. Therefore, if agent 1 is allocated at , the achieved welfare is , whereas the optimal welfare is (when serving all agents in ). For an arbitrary large This ratio approaches .

The proof follows since serving agent 1 at and not serving agent 1 at is violates monotonicity. ∎

Remark B.2.

The factor is tight for single-crossing valuations. If , then the mechanism can always allocate all agents. Otherwise, one can always allocate only to the highest valued agent, which is monotone because of single crossing. Since the largest feasible set is of size at most in this case, allocating to the highest valued agent yields an approximation ratio of .

Appendix C Results for -SOS

We now extend the results in Section 6 to the case of combinatorial -SOS and combinatorial -strong-SOS valuations with single-dimensional signals. We first note that if we consider -SOS valuations, then Equation (6) in the decomposition becomes

| (11) | |||||

We now show the extension of Theorem 6.1 to -SOS valuations.

Theorem C.1.

For every combinatorial auction with -SOS valuations over single-dimensional signals, and signal space of size , i.e., , there exists a truthful mechanism that gives -approximation to the optimal social welfare.

Proof.

The mechanism is identical to -HL, but runs (Random Threshold) with probability and (Random Sampling) With probability . The mechanism was already proved to be truthful in Section 6.1.

Random Threshold now gives a -approximation to the new SELF term. The proof is the same as of Lemma 6.2, but the extra factor of comes from the fact the the new SELF term is times larger.

Random Sampling gives a -approximation to the OTHER term. While this term is the same for -SOS, the new factor is due to the fact that when applying Lemma 3.1 in the proof of Lemma 6.3, we get that instead of the bound we get in Equation (8).

The new approximation guarantee follows from the new decomposition, the new approximation guarantees the various mechanisms get for the terms of the decomposition, and the updated probability . ∎

We next extend Theorem 6.5.

Theorem C.2.

For every combinatorial auction with -strong-SOS valuations over single-dimensional signals, and signal space of size , i.e., , there exists a truthful mechanism that gives -approximation to the optimal social welfare.

Proof.

The mechanism is identical to mechanism -SS from Section 6.2, but runs Random Bucket with probability and (Random Sampling) With probability .

The SELF term from Equation (9) is now bounded via the following:

| (12) | |||||

where the inequality follows the definition of -strong-SOS valuations.

The new bound changes the guarantee of Random Bucket to get a -approximation to the SELF term, where the proof is identical to that of Lemma 6.4.

As stated in Theorem C.1, Random Sampling approximates the OTHER term to a factor . The proof of the new bound follows the new decomposition, the updated probabilities and the new approximation guarantees of the mechanisms being run. ∎