An Integrated Panel Data Approach

to Modelling Economic Growth

††∗Department of Economics, University of North Texas, Denton, TX 76201, USA. Email: Guohua.Feng@unt.edu♯Department of Econometrics and Business Statistics, Monash University, Caulfield East, Victoria 3145, Australia. Email: Jiti.Gao@monash.edu†Department of Economics, University of Bath, Bath BA2 7JP, UK. Email: B.Peng2@bath.ac.uk

Guohua Feng∗, Jiti Gao♯ and Bin Peng†

∗University of North Texas, ♯Monash University and †University of Bath

Empirical growth analysis has three major problems — variable selection, parameter heterogeneity and cross-sectional dependence — which are addressed independently from each other in most studies. The purpose of this study is to propose an integrated framework that extends the conventional linear growth regression model to allow for parameter heterogeneity and cross-sectional error dependence, while simultaneously performing variable selection. We also derive the asymptotic properties of the estimator under both low and high dimensions, and further investigate the finite sample performance of the estimator through Monte Carlo simulations. We apply the framework to a dataset of 89 countries over the period from 1960 to 2014. Our results reveal some cross-country patterns not found in previous studies (e.g., “middle income trap hypothesis”, “natural resources curse hypothesis”, “religion works via belief, not practice”, etc.).

Following the seminal works of Kormendi and Meguire (1985) and Barro (1991), a vast amount of studies in the empirical growth literature have attempted to identify salient determinants of economic growth. A main tool used by these studies is “cross-country growth regressions” — that is, to regress observed GDP growth on a plethora of possible explanatory variables that could possibly affect growth across countries. Excellent surveys of these studies and their role in the broader context of economic growth theory are provided in Durlauf and Quah (1999), Temple (1999) and Durlauf et al. (2005).

Despite the vast amount of research, the literature has identified a number of problems with conventional growth regressions, among which three deserve particular attention. The first problem is determining what variables to be included in growth regressions. This problem arises because of the nature of growth theories: although a plethora of growth theories have been proposed to identify factors that affect growth, these theories are open-ended in the sense that the validity of one causal theory of growth does not imply the falsity of another (Brock and Durlauf, 2001). In words of Durlauf et al. (2008), “a given body of candidate growth theories defines a space of possible models rather than a single specification”. From an empirical perspective, this problem stems from the fact that the number of potential explanatory variables is large (over 140 identified in Durlauf et al., 2005) relative to the number of countries with enough data availability, rendering the all-inclusive regression computationally infeasible (Sala-I-Martin et al., 2004; Durlauf et al., 2005). In dealing with this problem some studies have resorted to simply “trying” combinations of variables which could be potentially important determinants of growth and report the results of their preferred specification. However, as noted by Leamer (1983) and Sala-I-Martin et al. (2004) such “data-mining” could lead to spurious inference.

The second problem with conventional growth analysis is that most empirical growth studies assume that the parameters of growth regressions are identical across countries. This assumption complies with the classical Solow model (Mankiw et al., 1992), which assumes that all countries share an identical aggregate Cobb-Douglas production function. However, an increasing number of studies (e.g., Durlauf and Johnson, 1995; Durlauf et al., 2001; Salimans, 2012) have suggested that the parameters are heterogeneous across countries. These studies, though using different econometric methods, all suggest that the assumption of a single linear growth model that applies to all countries is inappropriate. For example, Durlauf and Johnson (1995) employ a regression tree analysis to show that a cross-sectional regression using the Summers and Heston (1991) data appears to provide support for several distinct regimes in which aggregate production functions vary among countries according to their level of development, while Durlauf et al. (2001), employing a varying coefficient growth model, also find strong evidence of parameter heterogeneity across countries.

The third problem is that few studies in the empirical growth literature allow for cross-sectional dependence of individual countries. Panel data econometrics has recently seen an increasing interest in models with unobserved time-varying heterogeneity caused by latent common shocks influencing all units, possibly to a different degree. This type of heterogeneity introduces cross-sectional dependence to individual countries, which, when neglected, can lead to biased estimates and spurious inference (Pesaran, 2006; Bai, 2009). In the context of cross-country growth analysis, the problem of cross-sectional dependence seems particularly salient due to the omnipresence of common global shocks (such as global financial crises and world oil price shocks) that affect all countries through trade and financial linkages (Chudik et al., 2017). Durlauf and Quah (1999) discuss the possibility of cross-sectional dependence in a Lucas (1993) growth model with human capital spillovers. They find that these spillovers markedly change the dynamics of convergence and the authors call for the modelling of cross-country interactions in empirical convergence analysis.

The three aforementioned problems have received more or less individual attention in the growth literature. For example, Durlauf et al. (2001) address the problem of parameter heterogeneity using a varying coefficient growth model, but do not deal with the problems of variable selection and cross-sectional dependence; both Sala-I-Martin et al. (2004) and Moral-Benito (2012) select growth determinants using Bayesian averaging, but do not account for parameter heterogeneity and cross-sectional dependence.

The main goal of this study is to propose an integrated framework that is capable of dealing with parameter heterogeneity and cross-sectional dependence, while simultaneously performing variable selection. Specifically, parameter heterogeneity is allowed for by permitting the coefficients to vary across countries according to a country’s initial conditions, while cross-sectional dependence is accounted for via a factor structure. We then propose a least absolute shrinkage and selection operator (LASSO) estimator to select growth determinants, establish the associated asymptotic results, and further verify our asymptotic results through extensive simulations, which constitutes another contribution of this paper. We apply this framework to a new dataset of 89 countries over the period 1960-2014. Our findings broadly support the more “optimistic” conclusion of Sala-I-Martin (1997), that is, some variables are important regressors for explaining cross-country growth patterns. Moreover, our empirical results also provide support to some important hypotheses in the growth literature, e.g., “middle income trap hypothesis”, “natural resources curse hypothesis”, “religion works via belief, not practice”, etc.

The rest of the paper is organized as follows. Section 2 explains how to extend the canonical cross-country growth regression to account for the aforementioned issues. Section 3 describes a procedure for estimating the extended growth regression model in Section 2, and presents the associated asymptotic properties. Section 4 describes the data. The empirical results are presented in Section 5. Section 6 concludes. Due to space limitations, preliminary lemmas, proofs of the main theorems and Monte Carlo simulations, together with auxiliary tables and figures, are presented in the supplementary Appendix A of this paper. The proofs of the preliminary lemmas are presented in the supplementary Appendix B of this paper, which can be found at the authors’ website (https://papers.ssrn.com/sol3/cf_dev/AbsByAuth.cfm?per_id=646779).

2 A Varying Coefficient Growth Regression Model with Factor Structure and Sparsity

A generic representation of the canonical cross-country growth regression is

(2.1)

where index countries; index time; is the rate of economic growth; represents a set of observable explanatory variables, including those originally suggested by Solow as well as other growth theories, and is an error term. Equation (2.1) represents the baseline for much of growth econometrics.

However, as discussed in the Introduction, (2.1) is based on two problematic assumptions. First, it assumes that the parameters (i.e., ) are homogeneous across all countries. Second, it assumes that there is no cross-sectional dependence across countries.

To relax the two assumptions, in what follows we extend the conventional cross-country growth regression in (2.1) in two ways. First, in Section 2.1 we allow for parameter heterogeneity by allowing to vary across countries according to a country’s initial conditions. Second, in Section 2.2 we introduce cross-sectional dependence into the model by means of a factor structure.

2.1 Parameter Heterogeneity

Following Durlauf et al. (2001), we allow for parameter heterogeneity by generalizing (2.1) into a varying coefficient model:

(2.2)

where can be interpreted as some measure of “development” (or initial condition) of a country, and is a vector of smooth functions that maps the scalar index variable into a set of country-specific parameters.

This generalization in (2.2) provides a framework within which one can bridge the gap between cross-country regression models and new growth theories. For instance, if one believes that initial GDP per capita causally affects a country’s production technology and growth as in Durlauf et al. (2001), then initial GDP per capita can be introduced as a

“development” index. As pointed out by Durlauf and Johnson (1995), (2.2) is compatible both with a model in which economies pass through distinct phases of development towards a unique steady state as well one in which multiple steady states exist.

2.2 Cross-Sectional Error Dependence

Having accounted for parameter heterogeneity, we next introduce the cross-sectional dependence of error terms into (2.2) using a factor structure:

(2.3)

where is an vector of unobservable common factors, is an vector of factor loadings that capture country-specific responses to the common shocks, and is the idiosyncratic error term. These common factors can be a combination of “strong” factors, such as world oil price shocks, global financial crises, and recessions in major advanced economies; and “weak” factors, such as local spillover effects along channels determined by shared culture heritage, geographic proximity, economic or social interaction (Chudik et al., 2011). Moreover, the components of the factor structure are allowed to drive both economic growth and explanatory variables, thus partially accounting for potential endogeneity of explanatory variables, which is neglected by the traditional approaches to causal interpretation of cross-country empirical analysis.

2.3 The Varying Coefficient Growth Regression Model with Factor Structure and Sparsity

Substituting (2.3) into (2.2) yields the following growth regression model that allows for parameter heterogeneity and cross-sectional dependence

(2.4)

The model in (2.4) extends the local Solow growth model investigated in Durlauf et al. (2001) into a panel data context with interactive fixed effects (or factor structure). From an econometric perspective, (2.4) extends the panel data model with interactive fixed effects in Bai (2009) into a varying coefficient context. Some closely related studies include, but are not limited to, Dong et al. (2018) on (2.4) with partially observed factor structure, Feng et al. (2017) on a special case of (2.4) with discrete and being reduced to fixed-effects , Liu et al. (2018) on a time-varying heterogeneous model with , and Malikov et al. (2016) on a binary varying-coefficient panel data setting with endogenous selection and fixed-effects. There are some key differences between this paper and the relevant literature. First, it is worth pointing out that these previous studies introduce parameter heterogeneity and cross-sectional dependence in different manners. Second, none of them consider performing variable selection on their varying coefficient models as we will show below particularly in the high-dimensional setting. Finally and most importantly, both model (2.4) and its asymptotic theory in Section 3 below are naturally motivated by the relevant empirical literature in economic growth.

In addition to parameter heterogeneity and cross-sectional dependence, we are also interested in another issue that is prominent in the empirical growth literature — variable selection. This issue is important because (1) the dimension of can be very large; and (2) not all elements of drive economic growth. In other words, for those factors not driving economic growth, it is reasonable to assume that their associated coefficients are zero, which is called “sparsity” in the literature of high dimensional econometrics.

In order to formally introduce the sparsity to the model (2.4), we assume that there exists an unknown set satisfying that if and only if . For notational simplicity, we assume for an unknown integer satisfying . Further, let , , and . Throughout this study, we always define the variables or functions corresponding to the sets and with super-indices ∗ and † respectively. Thus, identifying growth determinants is equivalent to distinguishing and , which will be achieved by a LASSO estimator presented in the following section. Finally, regarding the dimension of regressors, we consider two cases where (1) is fixed, and (2) diverges as the sample size increases. We refer to them as the low dimensional (LD) case and the high dimensional (HD) case, respectively. In terms of econometric methodology, both cases with the sparsity setting have not been studied in the literature to the best of our knowledge.

As discussed in the Introduction, failure to perform variable selection may result in spurious inference, failure to allow parameters to differ across countries is inconsistent with the increasing body of research that find cross-country parameter heterogeneity, and failure to account for cross-sectional dependence can lead to biased estimates and spurious inference. These possible consequences thus necessitate an integrated approach to simultaneously addressing the three issues.

In the following section, we introduce a LASSO estimator that is designed specifically for performing variable selection on the extended growth regression model in (2.4). The combination of varying coefficients, factor structure, and the LASSO

estimator provides us an integrated framework that is capable of simultaneously addressing the three problems mentioned in Section 1 — variable selection, parameter heterogeneity, and cross-sectional dependence.

3 Estimation

In this section, we describe a procedure for estimating the model in (2.4) and derive the associated asymptotic properties. Specifically, we propose a LASSO estimator to select the appropriate variables, adopt a sieve method to recover the functional components, and employ the principle component analysis (PCA) technique to estimate the unobservable factor structure.

Before proceeding further, it is convenient to introduce some notations. We let , , , , , and . denotes the Euclidean norm of a vector or the Frobenius norm of a matrix; for a square matrix , let and stand for the minimum and maximum eigenvalues of respectively; denotes the orthogonal projection matrix generated by matrix , where , and is a matrix with full column rank.

We adopt the sieve method (e.g., Dong and Linton, 2018) to estimate the functional component of (2.4). Specifically, assume that for , where is a Hilbert space. Suppose that there exists an orthonormal function sequence in such that . Then, for , we have an orthogonal series expansion , where , , , and is the so-called truncation parameter. By the Parseval equality, the norm can be expressed as . For a vector of functions , its norm is defined by .

Without loss of generality, truncating the expansions of all the elements of by the same gives

(3.1)

where , , , and . Thus, the first elements of can be expressed by , where .

by projecting out the factor structure, where for any vector of functions . The objective function is then defined by

(3.2)

where , stands for the row of , and are the regularizers of the coefficient functions and are to be determined by data. The estimators of and for both LD and HD cases are always obtained by

(3.3)

where . In what follows, we always partition , according to the partition and , as wherever necessary.

At this point it is convenient to state some fundamental assumptions that are needed for the derivation of the asymptotic results for both LD and HD cases.

Assumption 1.

1.

Let and denote the -algebras generated by and respectively, where , , . Let be the mixing coefficient.

(a)

is identically distributed over . is strictly stationary and -mixing such that for some , , and the mixing coefficient satisfies .

(b)

, , and is independent of the other variables. Let for , , and .

2.

Let and , where and are deterministic and positive definite. Moreover, and .

Assumption 2.

1.

Suppose that , and with probability approaching one, where and .

2.

Let , and . Suppose , where .

Assumption 1 is standard in the literature. The mixing conditions are similar to Assumption C of Bai (2009) and Assumption 3.4 of Fan et al. (2016). In Assumption 2.1, the condition is the same as Assumption 3 of Newey (1997), and essentially requires certain smoothness of the elements of . The condition of Assumption 2.1 is similar to Assumption 3.1 of Fan et al. (2016). Now, consider a special case where , and are mutually independent, and . Under this setting, it is easy to see that holds true for both of the LD and HD cases by some standard analyses. Assumption 2.2 ensures that the estimators given in (3.3) are well defined, and is equivalent to Assumption A of Bai (2009).

Based on the above setting, we move on to investigate the asymptotic results associated with (3.3) under the LD setting.

3.1 Low Dimensional Case

In order to identify and and establish the asymptotic distribution, we further make the following assumptions.

Assumption 3.

1.

and , where .

2.

and , where , , and .

Assumption 4.

1.

Suppose that for , , and , where . Moreover, , , and .

2.

Let and for , where

Suppose that for , as , .

The conditions of Assumption 3, though seemingly complicated, can be easily satisfied. For example, let , , , and , where means the largest integer part of a real number . Then Assumption 3 essentially requires that , , and .

The current requirements of Assumption 4.1 are in the same spirit as Connor et al. (2012, Eq. 3 and Eq. 20) and Jiang et al. (2017, pp. 21-22). Without this assumption, some other types of conditions would be needed to achieve asymptotic normality. For example, one can require with and establish the normality with biases as in Theorem 3 of Bai (2009). Assumption 4.2 is equivalent to Assumption E of Bai (2009). It is worth mentioning that deriving the rates of convergence in Lemma A.3 and Lemma A.5 of the supplementary Appendix A does not require Assumption 4 at all. For better presentation and in order not to deviate from our main goal, we present these lemmas in the supplementary Appendix A instead of the main text.

Suppose Assumption 4 also holds. Then for , as , where .

The first result of Theorem 3.1 indicates that we are able to distinguish and ; while the second result of Theorem 3.1 establishes the asymptotic distribution of the coefficient functions associated with the variables which truly drive economic growth.

To complete our discussion on the LD case, we propose the following BIC type criteria in order to select practically.

(3.4)

where , , are obtained by implementing (3.3) using as the weight vector, and is the number of nonzero coefficient functions identified by . The penalty term of (3.4) is constructed in view of the slow rate documented in Lemma A.2 of the supplementary Appendix A. We select by

(3.5)

Further let indicate the set of relevant variables identified by . Then the next result follows.

Again, Assumption 4 is unnecessary for establishing Theorem 3.2.

3.2 High Dimensional Case

In this subsection, we allow the dimension of to diverge as the sample size increases. The following assumptions are crucial for deriving the asymptotic results for the HD case.

Assumption 5.

1.

, where denotes the spectral norm of a matrix and ;

2.

, , , where , and .

Assumption 5.1 is identical to Assumption iii of Li et al. (2016) and Assumption A.1.v of Lu and Su (2016). Assumption 5.2 further imposes bounds on some parameters, and can be verified in exactly the same way as shown under Assumption 3.

With regard to the selection of , we still use the BIC criterion with a minor modification:

(3.6)

where is a penalty term satisfying as ; and all other notations are defined in exactly the same way as in the LD case. Select by .

Once the zero coefficient functions are identified, the rest of the analysis (such as the investigation of the rate of convergence) will be similar to that done in Section 3.1 except that one needs to account for the divergence of both and . To avoid repetition, we will not present the analysis here again.

In summary, in either of the two cases (LD and HD), when , all zero coefficient functions can be identified. In the growth regression context, this is equivalent to saying that when , all variables not driving economic growth can be identified and thus removed from the growth regression. In the meantime, the varying coefficients can be recovered using the sieve method, while the factor structure can be estimated by the PCA technique. Thus, all the three aforementioned issues that are prominent in the empirical growth literature (i.e., variable selection, parameter heterogeneity, and cross-sectional dependence) can be addressed simultaneously within a single, integrated framework. Before moving on to the empirical analysis, we next describe the data employed in this study.

4 Data

Of the many variables that have been found to be significantly correlated with growth in the literature, we choose a total of 60 (including the dependent variable, the growth rate of per capita GDP). The choice of these variables is based on previous studies (e.g., Sala-I-Martin et al., 2004; Moral-Benito, 2012) and data availability. Our final dataset covers 89 countries over the period 1960 - 2014. It contains countries in different stages of development and with a wide geographic dispersion. The explanatory variables cover a wide range of factors, including stage of development, social issues, health, geography, politics, education and more. The variable names, their means, and standard deviations are presented in Table Table LABEL:Table_Var. Table LABEL:Tabel_Country provides a list of the included countries.

A common practice in the literature is to take a five-year simple moving average of both dependent and independent variables111Another popular method of looking at annual data in empirical growth literature is to use averaged five-year period data. But, as is stressed by Soto (2003) and Attanasio et al. (2000), the use of n-year averages is not suitable because of the lost of information that it implies, and attempting to use data on averaged five-year periods severely limited the number of observations to draw from in the data.. This technique has the advantages of reducing the potential effects of short-term fluctuations and maintaining a high number of time series observations. Despite these advantages, this technique may still suffer from reverse causality or simultaneity, because causality between regressors and growth could go the other way as well or some regressors and growth may be simultaneously determined (e.g., Bils and Klenow, 2000). To mitigate this problem, we deviate from the common practice by measuring dependent and independent variables differently. Specifically, while the dependent variable is measured as a five-year moving average of economic growth, all explanatory variables are measured at the beginning of each five-year period, with the exception of the variables related to war, geography, and terms of trade222Specifically, these variables include: fraction spent in war (each five-year period); number of war participation (each five-year period); number of revolutions (each five-year period); coups d’etat and coup attempts within (each five-year period); time of independence; East Asian dummy; African dummy; European dummy; Latin American dummy; British colony dummy; Spanish colony dummy; landlocked country dummy; percentage of land area in Koeppen-Geiger tropics; percentage of land area within 100 km of ice-free coast; terms of trade; and terms of trade growth. (Salimans, 2012). These latter explanatory variables are expected to be truly independent of contemporaneous economic growth, and thus also are measured as five-year moving averages (as with the dependent variable). This treatment further alleviates endogeneity, which is already mitigated by the use of multi-factor error structure as discussed in Section 2.

5 Empirical Results

5.1 Choices of the Number of Factors and the Development Index

In Section 3, we assume that the number of factors is known. In practice, is unknown and has to be estimated. The main tool for estimating the number of factors of large dimensional datasets is the use of information criteria. In view of the fact that there are 59 observable explanatory variables in our case, we follow Ando and Bai (2017) to choose the number of the factors by minimizing the next criteria function:

(5.1)

where , and for , , and are the corresponding estimates using the approach of Section 2.

We now turn to the choice of the development index, . In Section 2 we have specified a varying coefficient growth regression model capable of capturing parameter heterogeneity by means of a development index. Of the possible development indexes, output and human capital are believed to be the most important ones in previous studies (e.g., Durlauf and Johnson, 1995; Liu and Stengos, 1999; Minier, 2007; Salimans, 2012). Following those studies, we consider four alternative development indexes in log form: (1) initial GDP per capita, (2) initial primary schooling enrolment rate, (3) initial secondary schooling enrolment, and (4) initial higher education enrolment rate.

When choosing among the four alternative development indices, we use the in-sample root mean squared error (RMSE) which is consistent with the criterion function used in estimation. Specifically, for each development index, we first choose the number of factors and select the regressors. Then we run post selection regression as documented in Section A.1 of the supplementary Appendix A without including the weight parameters to calculate the corresponding RMSE. Table 4 presents the chosen number of factors and in-sample RMSE for each of the four development indices. In addition, we also consider the homogeneous parameter growth regression model where (i.e., the coefficients of growth determinants) is homogeneous across countries, and the results are reported in the first column of Table 4. This table shows that the model with initial GDP per capita as the development index has the lowest in-sample RMSE and thus fits the data best.

In summary, the model with six factors and initial GDP per capita as the development index (i.e., and ) receives the most support from the data. Hence, in what follows we concentrate on the results obtained from this model.

5.2 Estimates of the Common Factors and Their Associated Loadings

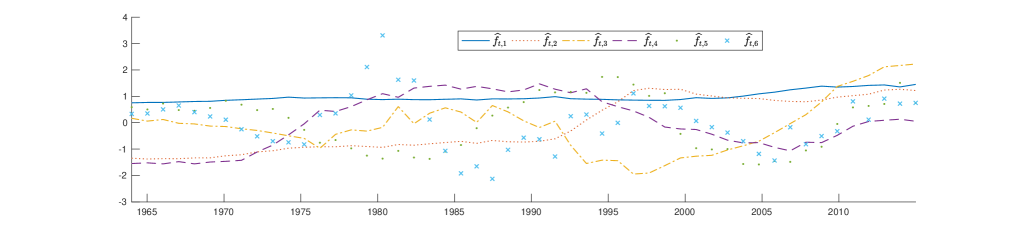

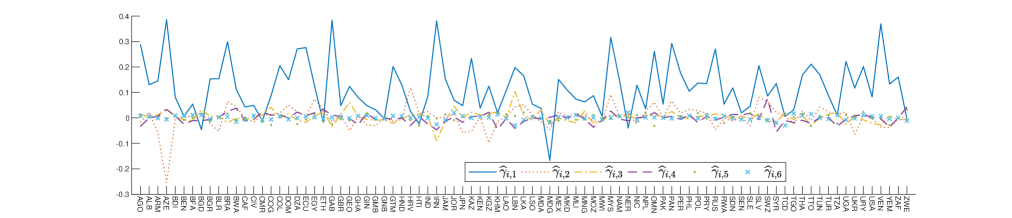

Figure 1 and Figure 2 plot the estimates of the factors identified above and their corresponding loadings respectively. The former shows that all the common factors varies considerably over time with the exception of the first factor which exhibits a relatively small amount of variation during the sample period, while the latter shows that all the factor loadings vary substantially across countries.

We are also interested in the importance of each common factor in explaining the total variance of the error terms ’s of (2.3). Table 4 shows the proportion of the total variance attributed to each common factor. As the table shows, the first common factor accounts for 87.86% percent of the total variance, and the other five factors account for 7.01%, 1.78%, 1.45%, 0.61%, 0.30% respectively. Overall these six common factors account for 99.01% of the total variance, indicating a fairly parsimonious description of the data.

5.3 Estimates of the Coefficient Functions of Selected Variables

5.3.1 General Findings

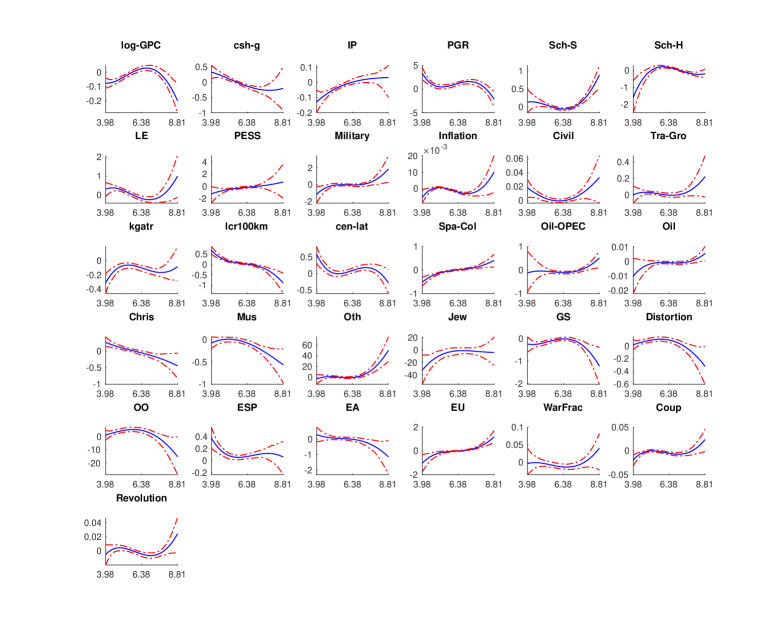

Our results are broadly consistent with those of Fernández et al. (2001) and Sala-I-Martin et al. (2004) in that we have identified a number of robust growth determinants (variables) that are also found to be significant in the previous studies. In this sense, our results broadly support the more “optimistic” conclusion of Sala-I-Martin (1997), that is, some variables are important regressors for explaining cross-country growth patterns. Specifically, we have identified 31 robust growth determinants, providing evidentiary support for the canonical neoclassical growth variables; i.e., initial income, investment, and population growth, as well as macroeconomic policies, geography, institutions, religion and ethnic fractionalization. Table LABEL:Tabel_Est reports the estimates of the coefficients of each of the 31 robust growth determinants for initial GDP per capita (minimum), , , , , and (maximum), together with their associated 95% bootstrapped confidence intervals (CI)333Note that these confidence intervals need to be interpreted carefully. As well understood, one cannot establish the confidence intervals for the estimates under HD case unless certain transformation is further employed (e.g., Huang et al., 2008; Dong et al., 2017). However, if one regards 31 (the number of selected variables) as a relatively small number, then one can treat our regression as a LD case and employ the same bootstrap procedure as in Su et al. (2015). In order to ensure the validity of the bootstrap procedure, stronger assumptions on the error terms are needed. For example, one can employ the martingale difference type of assumptions (see Assumption A.4 of Su et al., 2015), or simply assume that the error terms are i.i.d. over both and . Generally speaking, when the error term exhibits both cross-sectional and serial correlation, the bootstrap results are not reliable or incorrect.. To see these coefficients more clearly, we also plot them against initial GDP per capita in Figure A.5 of the supplementary file.

Despite the similarity, there are at least three differences between the results of this study and those of the previous studies. First, our set of robust growth determinants differs from those identified in the previous studies, in spite of many overlaps between them. Specifically, some variables appear to be robust in our study but not in the previous (such as secondary school enrolment rate and terms of trade growth) or vice versa (such as primary school enrolment rate and fraction GDP of mining). There are at least three possible reasons for this difference: (1) we use a different model specification that allows for both parameter heterogeneity and cross-sectional dependence; (2) we use a different variable selection procedure (i.e., a LASSO estimator); and (3) we use a different dataset that spans a longer time period and covers a slightly different set of countries.

Second, our estimates of the coefficients of the robust growth determinants vary considerably across countries according to their level of development, while those in most previous studies are identical across countries. Specifically, we find that some coefficients have the same sign but different values across different levels of initial GDP per capita (such as civil liberty, terms of trade growth, and percentage of land area in tropics), while other coefficients not only have different signs but also different magnitudes across different levels of initial GDP per capita (such as consumption share of government, life expectancy, military expenditure, and OPEC dummy). These findings suggest that it is inappropriate to apply a growth regression with homogeneous parameters to all countries.

Third, our estimates of the coefficients of the robust growth determinants reveal some cross-country patterns not found in previous studies. Taking the coefficient of initial GDP per capita for example, we find that its estimate is positive for countries with GDP per capita between $1,780 and $2,117 in 1960 U.S. dollars (between $13,166 and $15,665 in 2014 U.S. dollars) while being negative for all other countries. This finding is in accordance with the “middle income trap hypothesis”, which refers to countries that have experienced rapid growth and thus quickly reached middle-income status but then failed to overcome that income range to further catch up to the developed countries (Gill and Kharas, 2007). To give another example, our estimate of the oil reserve coefficient increases monotonically with GDP per capita and eventually becomes positive for economies with initial GDP per capital above $2,175 in 1960 U.S. dollars ($16,094 in 2014 U.S. dollars). This latter finding is consistent with recent studies (e.g., Leite and Weidmann, 1999) which suggest that in developed economies where economic institutions are generally well-developed, natural resources tend to promote economic growth; whereas in developing economies where economic institutions are generally weak, natural resources tend to hamper economic growth. We will discuss these two examples in more details below where it is appropriate.

5.3.2 Specific Findings

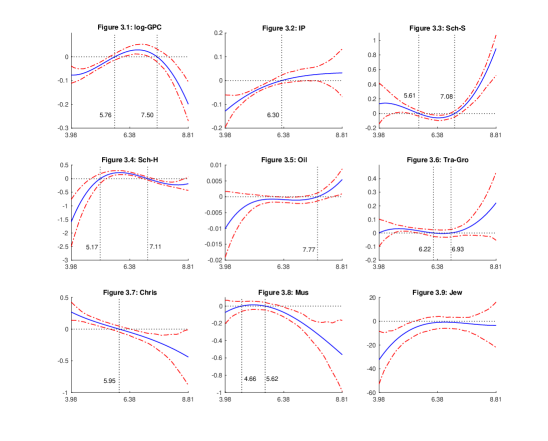

We now analyse some of the variables that are “significantly” related to growth in more details. Figure 3.1 presents our estimate of the coefficient of initial GDP per capita. This figure reveals three findings. First, this estimate is negative for most GDP per capita levels, thus being largely consistent with findings in the existing conditional convergence literature as well as previous studies that have employed model averaging methods to growth. Second, the coefficient has an inverse U-shaped relationship with initial GDP per capita. This finding is consistent with those reported by previous studies. For example, Durlauf et al. (2001) find that the coefficient of initial GDP per capita does not exhibit any sort of monotonicity with respect to level of development; Salimans (2012) finds that the coefficient of initial GDP per capita first increases with level of development up to a point and then declines afterwards; and Durlauf and Johnson (1995) find that the coefficient of initial GDP per capita is not monotonic with respect either GDP per capita or literacy rate. Third, the coefficient is positive for countries with GDP per capita between $319 and $1,812 in 1960 U.S. dollars (or between $2,554 and $14,510 in 2014 U.S. dollars), suggesting that some of these countries have been unable to catch up with more developed countries. This finding is in line with the “middle-income trap” hypothesis, which refers to the phenomenon of hitherto rapidly growing economies stagnating at middle-income levels and failing to graduate into the ranks of high-income countries (e.g., Eichengreen et al., 2014). In our sample South Africa and Columbia are two example countries that have never been able leave the “middle-income range” over the entire sample period since their GDP per capita fell into this range at the beginning of the sample period (i.e., 1960).

Figure 3.2 shows our estimate of the coefficient of price for investment goods. Three findings emerge from this figure. First, this estimate is negative for countries with initial GDP per capita up to $543 in 1960 U.S. dollars (or $4,348 in 2014 U.S. dollars), suggesting that for these countries a relative low price of investment goods in the first year of each five-year period is strongly and positively related to subsequent income growth. This finding is not surprising because a low investment price stimulates investment (including investment in machinery and equipment), which further spurs economic growth (De Long and Summers, 1991, 1992). Second, the estimated coefficient falls in absolute value as initial GDP per capita increases, meaning that the marginal effect of investment price on growth is stronger for poor countries than for rich countries. This latter finding is consistent with Temple (1999) who find that the growth-spurring effects of investment is greater for developing countries, because total investment includes machinery embodying well-established technologies and developing countries may be able to take advantage of new and old equipment because they have little of any technology. Third, for countries with initial GDP per capita above $543 in 1960 U.S. dollars (or $4,348 in 2014 U.S. dollars) the estimated coefficient of investment goods price is positive but insignificant, because the associated confidence intervals contain zero. This suggests that investment goods price has no growth effects for these countries. A possible reason for this latter finding is that the data from the Penn World Table is not disaggregated enough to distinguish price of equipment investment, which has strong growth effects, and price of other forms of investment, which have little growth effects (De Long and Summers, 1991).

Figure 3.3 shows our estimate of the coefficient of secondary schooling enrolment. As this figure shows, this estimate is positive for most levels of initial GDP per capita. This is not surprising because secondary education is a vital part of a virtuous circle of economic growth within the context of a globalized knowledge economy. Many studies have documented that a large pool of workers with secondary education is indispensable for knowledge spillover to take place and for attracting imports of technologically advanced goods and foreign direct investment (Borensztein et al., 1998; Caselli and Coleman II, 2001). That said, we also note that the estimated coefficient for secondary schooling is negative for middle income countries with initial GDP per capita between $272 and $1,192 in 1960 U.S. dollars (or between $2178 and $9,545 in 2014 U.S. dollars). This result suggests that a possible reason for the “middle income trap” discussed above is that these middle income countries, unlike other countries, fail to take advantage of the benefits brought by secondary schooling.

We also note from Figure 3.4 that the estimate of the coefficient of higher education is negative for almost all countries with the exception of middle income countries. This finding is consistent with Sala-I-Martin et al. (2004) and Salimans (2012), both of which find that the higher schooling coefficient is negative for most of their sample countries but positive for the rest. It also parallels the concavity argument that the earnings function is concave in education, meaning that returns are higher for lower levels of education (Psacharopoulos, 1994; Psacharopoulos and Patrinos, 2004).

Figure 3.5 shows our estimate of the coefficient of oil reserve. Two findings stand out from this figure. First, this estimate is negative for countries with initial GDP per capita below $2,373 in 1960 U.S. dollars (or $19,002 in 2014 U.S. dollars). This finding is consistent with the “natural resources curse hypothesis” (e.g., Sachs and Warner, 2001) and can be explained by the rent-seeking behaviour of countries with large endowments of natural resources. Second, the oil reserve coefficient increases monotonically with GDP per capita and eventually becomes positive for economies with initial GDP per capita above $2,373 in 1960 U.S. dollars (or $19,002 in 2014 U.S. dollars). This latter finding accords with recent studies (e.g., Leite and Weidmann, 1999) on the nexus between natural resources and economic growth. Specifically, these studies suggest that the contribution of natural resources to a country’s economy does not take place in isolation, but rather in the overall context of the country’s economic management and institutions. It is thus the quality and competency of these policies and institutions that will determine whether natural resources can promote economic growth, or whether revenues generated by the sector might impede development. Therefore, in developed economies where economic institutions are generally well-developed, natural resources tend to promote economic growth; whereas in developing economies where economic institutions are generally weak, natural resources tend to hamper economic growth.

Figure 3.6 presents the estimate of the coefficient of terms of trade growth. As this figure shows, our estimate of the terms of trade growth coefficient is positive for all countries, suggesting that growth tends to be faster in countries where the rate of change of terms of trade is higher. This finding is consistent with previous studies (Mendoza, 1995, 1997; Kose and Riezman, 2001; Bleaney and Greenaway, 2001) that find that an improvement in the terms of trade leads to higher levels of investment, and hence long-run economic growth. In addition, this figure shows that the terms of trade growth coefficient increases with GDP per capita, indicating that the marginal effect of terms of trade growth is larger in richer countries than in poorer ones. This latter finding is also consistent with previous studies (e.g., Blattman et al., 2007). Specifically, those studies argue that higher volatility in the terms of trade reduces investment and hence growth because of aversion to risk, and that rich countries with more sophisticated institutions and markets are likely to have cheaper ways to insure against price volatility than poor countries, so terms of trade instability is likely to have a smaller negative impact on rich countries.

Here we note that as in Sala-I-Martin et al. (2004), trade openness (defined as exports plus imports as a share of GDP) is insignificant, presumably reflecting the crudity of this measure, and perhaps the distinction between opening to international trade generating a one-time step increase in income as factors are reallocated according to comparative advantage versus an ongoing growth impact associated with greater openness.

Figures 3.7-3.9 show the estimates of the coefficients of fraction of Christian, Muslim, and Jewish respectively. These coefficients are negative at all levels of development or nearly all levels of development. This finding is consistent with that of Barro and McCleary (2005) who find that religion works via belief, not practice. They argue that higher church attendance uses up time and resources and eventually runs into diminishing returns. The “religion sector”, as they call it, can consume more than it yields.

6 Conclusion

A rigorous cross-country growth regression analysis should simultaneously account for three major problems identified in the literature — variable selection, parameter heterogeneity, and cross-sectional dependence. Though these three problems have received individual attention, little or no research has sought to integrate them into a single, comprehensive framework. The purpose of this study is to fill this void by proposing a new, integrated framework that is capable of dealing with parameter heterogeneity and cross-sectional dependence, while simultaneously performing variable selection. Specifically, parameter heterogeneity is allowed for by means of a varying coefficient growth regression model, while cross-sectional dependence is introduced into the model via a multi-factor structure. For simplicity, we refer to the resulting growth regression model as the “varying coefficient growth regression model with factor structure and sparsity”. We then propose a LASSO estimator that is capable of performing variable selection on this model. In addition, we have established the associated asymptotic results for this estimator and further investigate the performance of the estimator by conducting extensive simulations.

We apply the above framework to a new dataset that covers 89 countries over the period from 1960 to 2014. We have identified 31 robust growth determinants, providing evidentiary support for the canonical neoclassical growth variables; i.e., initial income, investment, and population growth, as well as macroeconomic policies, geography, institutions, religion and ethnic fractionalization. Moreover, we find that all the coefficients of the robust growth determinants vary considerably across countries according to their level of development, which reveals some interesting cross-country patterns not found in previous studies. For example, we find that the coefficient of the initial GDP per capita is positive for countries with GDP per capita between $319 and $1,812 in 1960 U.S. dollars (or between $2,554 and $14,510 in 2014 U.S. dollars), suggesting that some of these countries have fallen into the so-called “middle income trap”. As another example, we find that the oil reserve coefficient increases monotonically with GDP per capita and eventually becomes positive for economies with initial GDP per capita above $2,373 in 1960 U.S. dollars (or $19,002 in 2014 U.S. dollars), thus being consistent with recent studies that stress the role of institutions in determining how natural resources affect economic growth.

References

(1)

Ando and Bai (2017)

Ando, T. and Bai, J. (2017),

‘Clustering huge number of financial time series: A panel data approach with

high-dimensional predictors and factor structures’, Journal of the

American Statistical Association112(519), 1182–1198.

Attanasio et al. (2000)

Attanasio, O. P., Picci, L. and Scorcu, A. E. (2000), ‘Saving, growth, and investment: A macroeconomic

analysis using a panel of countries’, Review of Economics and

Statistics82(2), 182–211.

Bai (2009)

Bai, J. (2009), ‘Panel data models with

interactive fixed effects’, Econometrica77(4), 1229–1279.

Barro (1991)

Barro, R. J. (1991), ‘Economic growth in a

cross section of countries’, Quarterly Journal of Economics106(2), 407–443.

Barro and McCleary (2005)

Barro, R. J. and McCleary, R. M. (2005), ‘Which countries have state religions?’, Quarterly Journal of Economics120(4), 1331–1370.

Bernstein (2005)

Bernstein, D. S. (2005), Matrix

Mathematics: Theory, Facts, and Formulas, Princeton University Press.

Bils and Klenow (2000)

Bils, M. and Klenow, P. J. (2000),

‘Does schooling cause growth?’, American Economic Review90(5), 1160–1183.

Blattman et al. (2007)

Blattman, C., Hwang, J. and Williamson, J. G. (2007), ‘The impact of the terms of trade on economic

development in the periphery, 1870-1939: Volatility and secular change’, Journal of Development Economics82(1), 156–179.

Bleaney and Greenaway (2001)

Bleaney, M. and Greenaway, S. D. (2001), ‘The impact of terms of trade and real exchange rate

volatility on investment and growth in sub-saharan africa’, Journal of

Development Economics65(2), 491–500.

Borensztein et al. (1998)

Borensztein, E., De Gregorioand, J. and Lee, J. (1998), ‘How does foreign direct investment affect economic

growth?’, Journal of International Economics45(1), 115–135.

Brock and Durlauf (2001)

Brock, W. A. and Durlauf, S. N. (2001), ‘Discrete choice with social interactions’, Review of Economic Studies68(2), 235–260.

Caselli and Coleman II (2001)

Caselli, F. and Coleman II, W. J. (2001), ‘The U.S. structural transformation and regional

convergence: A reinterpretation’, Journal of Political Economy109(3), 584–616.

Chen et al. (2012)

Chen, J., Gao, J. and Li, D. (2012),

‘Semiparametric trending panel data models with cross–sectional dependence’,

Journal of Econometrics171(1), 71–85.

Chudik et al. (2017)

Chudik, A., Mohaddes, K., Pesaran, M. H. and Raissi, M.

(2017), ‘Is there a debt-threshold effect on

output growth?’, Review of Economics and Statistics99(1), 135–150.

Chudik et al. (2011)

Chudik, A., Pesaran, M. H. and Tosetti, E. (2011), ‘Weak and strong cross-section dependence and

estimation of large panels’, Econometrics Journal14(1), C45–C90.

Connor et al. (2012)

Connor, G., Hagmann, M. and Linton, O. (2012), ‘Efficient semiparametric estimation of the

fama-french model and extensions’, Econometrica80(2), 713–754.

De Long and Summers (1991)

De Long, J. B. and Summers, L. (1991), ‘Equipment investment and economic growth’, The

Quarterly Journal of Economics106(2), 445–502.

De Long and Summers (1992)

De Long, J. B. and Summers, L. (1992), ‘Equipment investment and economic growth: How strong

is the nexus?’, Brookings Papers on Economic Activity2, 157–199.

Dong et al. (2017)

Dong, C., Gao, J. and Linton, O. (2017), High dimensional semiparametric moment restriction

models.

https://ssrn.com/abstract=3045063.

Dong et al. (2018)

Dong, C., Gao, J. and Peng, B. (2018), Varying-coefficient panel data models with partially observed factor

structure.

https://ssrn.com/abstract=3102631.

Dong and Linton (2018)

Dong, C. and Linton, O. (2018),

‘Additive nonparametric models with time variable and both stationary and

nonstationary regressors’, Journal of Econometrics207(1), 212–236.

Durlauf and Johnson (1995)

Durlauf, S. N. and Johnson, P. A. (1995), ‘Multiple regimes and cross‐country growth

behaviour’, Journal of Applied Econometrics10(4), 365–384.

Durlauf et al. (2005)

Durlauf, S. N., Johnson, P. A. and Temple, J. R. (2005), ‘Growth econometrics’, Handbook of

Macroeconomics1, Part A, 555–677.

Durlauf et al. (2001)

Durlauf, S. N., Kourtellos, A. and Minkin, A. (2001), ‘The local solow growth model’, European

Economic Review45(4-6), 928–940.

Durlauf et al. (2008)

Durlauf, S. N., Kourtellos, A. and Tan, C. M. (2008), ‘Are any growth theories robust’, Economic

Journal118(527), 329–346.

Durlauf and Quah (1999)

Durlauf, S. N. and Quah, D. T. (1999), ‘The new empirics of economic growth’, Handbook of Macroeconomics1, Part A, 235–308.

Eberhardt and Teal (2011)

Eberhardt, M. and Teal, F. (2011),

‘Econometrics for grumblers: A new look at the literature on cross-country

growth empirics’, Journal of Economic Surveys25(1), 109–155.

Eichengreen et al. (2014)

Eichengreen, B., Park, D. and Shin, K. (2014), ‘Growth slowdowns redux: New evidence on the

middle-income trap’, Japan and the World Economy32, 65–84.

Fan et al. (2016)

Fan, J., Liao, Y. and Wang, W. (2016), ‘Projected Principal Component Analysis in Factor Models’, Annals of

Statistics44(1), 219–254.

Feng et al. (2017)

Feng, G., Gao, J., Peng, B. and Zhang, X. (2017), ‘A varying-coefficient panel data model with fixed

effects: theory and an application to the US commercial banks’, Journal of Econometrics196(1), 68–82.

Fernández et al. (2001)

Fernández, C., Ley, E. and Steel, M. F. J. (2001), ‘Model uncertainty in cross‐country growth

regressions’, Journal of Applied Econometrics16(5), 563–576.

Gao (2007)

Gao, J. (2007), Nonlinear Time Series:

Sem– and Non–Parametric Methods, Chapman & Hall/CRC.

Gao et al. (2018)

Gao, J., Xia, K. and Zhu, H. (2018),

‘Heterogeneous panel data models with cross-sectional dependence’, Journal of Econometrics p. forthcoming.

Gill and Kharas (2007)

Gill, I. and Kharas, H. (2007), An East Asian Renaissance : Ideas for Economic Growth, Washington, DC: World

Bank.

Hall et al. (2007)

Hall, P., Li, Q. and Racine, J. S. (2007), ‘Nonparametric estimation of regression functions in

the presence of irrelevant regressors’, Review of Economics and

Statistics89(4), 784–789.

Huang et al. (2008)

Huang, J., Horowitz, J. L. and Ma, S. (2008), ‘Asymptotic properties of bridge estimators in sparse

high-dimensional regression models’, Annals of Statistics36(2), 587–613.

Jiang et al. (2017)

Jiang, B., Yang, Y., Gao, J. and Hsiao, C. (2017), Recursive estimation in large panel data models:

Theory and practice.

Working paper available at https://ssrn.com/abstract=2915749.

Kapetanios et al. (2011)

Kapetanios, G., Pesaran, M. H. and Yamagata, T. (2011), ‘Panels with non-stationary multifactor error

structures’, Journal of Econometrics160(2), 326–348.

Kormendi and Meguire (1985)

Kormendi, R. C. and Meguire, P. G. (1985), ‘Macroeconomic determinants of growth:

Cross-country evidence’, Journal of Monetary Economics16(2), 141–163.

Kose and Riezman (2001)

Kose, A. and Riezman, R. (2001),

‘Trade shocks and macroeconomic fluctuations in africa’, Journal of

Development Economics65(1), 55–80.

Leamer (1983)

Leamer, E. (1983), ‘Let’s take the con out of

econometrics’, American Economic Review73(1), 31–43.

Leite and Weidmann (1999)

Leite, C. and Weidmann, J. (1999),

Does mother nature corrupt? natural resources, corruption, and economic

growth.

IMF Working paper 99/85.

Li et al. (2016)

Li, D., Qian, J. and Su, L. (2016),

‘Panel data models with interactive fixed effects and multiple structural

breaks’, Journal of the American Statistical Association111(516), 1804–1819.

Liu et al. (2018)

Liu, F., Gao, J. and Yang, Y. (2018), Nonparametric time-varying panel data models with heterogeneity.

https://ssrn.com/abstract=3214046.

Liu and Stengos (1999)

Liu, Z. and Stengos, T. (1999),

‘Non-linearities in cross-country growth regressions: A semiparametric

approach’, Journal of Applied Econometrics14(5), 527–538.

Lu and Su (2016)

Lu, X. and Su, L. (2016), ‘Shrinkage

estimation of dynamic panel data models with interactive fixed effects’, Journal of Econometrics190(1), 148–175.

Lucas (1993)

Lucas, R. (1993), ‘Making a miracle’, Econometrica61(2), 251–72.

Malikov et al. (2016)

Malikov, E., Kumbhakar, S. C. and Sun, Y. (2016), ‘Varying coefficient panel data model in the presence

of endogenous selectivity and fixed effects’, Journal of Econometrics190(2), 233–251.

Mankiw et al. (1992)

Mankiw, N. G., Romer, D. and Weil, D. N. (1992), ‘A contribution to the empirics of economic growth’,

Quarterly Journal of Economics107(2), 407–437.

Mendoza (1995)

Mendoza, E. G. (1995), ‘The terms of trade,

the real exchange rate, and economic fluctuations’, International

Economic Review36(1), 101–137.

Mendoza (1997)

Mendoza, E. G. (1997), ‘Terms-of-trade

uncertainty and economic growth’, Journal of Development Economics54(2), 323–356.

Minier (2007)

Minier, J. (2007), ‘Nonlinearities and

robustness in growth regressions’, American Economic Review97(2), 388–392.

Moral-Benito (2012)

Moral-Benito, E. (2012), ‘Determinants of

economic growth: A bayesian panel data approach’, Review of Economics

and Statistics94(2), 566–579.

Newey (1997)

Newey, W. K. (1997), ‘Convergence rates and

asymptotic normality for series estimators’, Journal of Econometrics79(1), 147–168.

Pedroni (2007)

Pedroni, P. (2007), ‘Social capital, barriers

to production and capital shares: implications for the importance of

parameter heterogeneity from a nonstationary panel approach’, Journal of

Applied Econometrics22(2), 326–348.

Pesaran (2006)

Pesaran, M. H. (2006), ‘Estimation and

inference in large heterogeneous panels with a multifactor error structure’,

Econometrica74(4), 967–1012.

Psacharopoulos (1994)

Psacharopoulos, G. . (1994), ‘Returns to

investment in education: A global update’, World Development22(9), 1325–1343.

Psacharopoulos and Patrinos (2004)

Psacharopoulos, G. and Patrinos, H. A. (2004), ‘Returns to investment in education: a further

update’, Education Economics12(2), 111–134.

Sachs and Warner (2001)

Sachs, J. D. and Warner, A. (2001),

‘The curse of natural resources’, European Economic Review45(4-6), 827–838.

Sala-I-Martin (1997)

Sala-I-Martin, X. (1997), ‘I just ran two

million regressions’, American Economic Review87(2), 178–183.

Sala-I-Martin et al. (2004)

Sala-I-Martin, X., Doppelhofer, G. and Miller, R. I. (2004), ‘Determinants of long-term growth: A bayesian

averaging of classical estimates (bace) approach’, American Economic

Review94(4), 813–835.

Salimans (2012)

Salimans, T. (2012), ‘Variable selection and

functional form uncertainty in cross-country growth regressions’, Journal of Econometrics171(2), 267–280.

Soto (2003)

Soto, M. (2003), ‘Taxing capital flows: an

empirical comparative analysis’, Journal of Development Economics72(1), 203–221.

Su and Jin (2012)

Su, L. and Jin, S. (2012), ‘Sieve

estimation of panel data models with cross section dependence’, Journal

of Econometrics169(1), 34–47.

Su et al. (2015)

Su, L., Jin, S. and Zhang, Y. (2015), ‘Specification test for panel data models with interactive fixed effects’,

Journal of Econometrics186(1), 222–244.

Summers and Heston (1991)

Summers, R. and Heston, A. (1991),

‘The Penn World Table (Mark 5): an expanded set of international

comparisons, 1950-1988’, Quarterly Journal of Economics106(2), 327–368.

Temple (1999)

Temple, J. (1999), ‘The new growth evidence’,

Journal of Economic Literature37(1), 112–156.

Wang and Xia (2009)

Wang, H. and Xia, Y. (2009),

‘Shrinkage estimation of the varying coefficient’, Journal of the

American Statistical Association104(486), 747–757.

Table 1: Definitions of All Variables in the Regression

Variables

Description

Formula

Mean

Std

EG

Economic growth rate

ln(rgdpot/rgdpot-1)

0.0363

0.0649

log(GPC)

log GDP per capita

6.0642

0.9861

csh_g

Government consumption share

0.2074

0.1163

Openness

Openness measure

csh_x + csh_m

-0.0322

0.1274

IP

Investment price, i.e., price level of capital formation

Percentage of population in Koeppen-Geiger tropics

0.3915

0.4217

lcr100km

Percentage of Land area within 100 km of ice-free coast

0.3788

0.3640

pop100cr

Ratio of population within 100 km of ice-free

0.4520

0.3728

coast/navigable river to total population

cen_lat

latitude of country centroid

0.1522

0.2197

Bri_Col

British colony dummy (1, yes; 0, no)

0.2584

0.4378

Spa_Col

Spanish colony dummy (1, yes; 0, no)

0.1910

0.3931

Oil_OPEC

Oil-producing country dummy (1, yes; 0, no)

0.0674

0.2508

Gas

proved reserves (cubic meters / 10^12)

1.3789

6.1997

Oil

proved reserves (bbl / 10^9)

4.5521

19.1378

Chris

Percentage of Christian

0.5369

0.3807

Mus

Percentage of Muslim

0.3046

0.3825

Hin

Percentage of Hindu

0.0263

0.1211

Bud

Percentage of Buddhist

0.0410

0.1541

Fol

Percentage of Folk religion

0.0284

0.0628

Oth

Percentage of other religion

0.0037

0.0064

Jew

Percentage of Jewish

0.0019

0.0027

GS

Government spending share of GDP

0.1501

0.0686

Distortion

Real exchange rate distortions

129.6824

35.8479

OO

Outward orientation

-2.7398

0.7542

SIL

Ethnolinguistic fractionalization

0.4886

0.3127

ESP

English-speaking population in percentage

0.1762

0.2692

EA

East Asian dummy

0.0225

0.1482

AF

African dummy

0.4270

0.4947

EU

European dummy

0.1124

0.3158

LA

Latin American dummy

0.1573

0.3641

WarFrac

Fraction spent in war (1960-2014)

0.3265

0.4343

NoWars

No. of war participation (1960-2014)

0.8028

1.2609

Coup

coups d’etat and coup attempts within (1960-2014)

0.1870

0.4964

Revolution

Number of revolutions (1960-2014)

0.1941

0.5038

Pop_Dens

Population Density/1000

0.0812

0.1135

WorkIR

Growth rate of work force

ln(WPt/WPt-1)

0.0210

0.0132

rgdpo — Size of economy (GDP in million)

pop — Population (in million)

csh_x — Share of merchandise exports

csh_m — Share of merchandise imports

WP — Fraction population of work force (1-A65-U15)

A65 — Fraction population over 65 years old

U15 — Fraction population under 15 years old

GFCF — Gross fixed capital formation

GFCF_PS — Gross fixed capital formation, private sector

Exports_OM — Percentage of Ores and metals exports

Exports_ARM — Percentage of Agricultural raw materials exports

GGFCE — General government final consumption expenditure share in GDP

Table 2: Sample Countries and Their Associated ISO 3166-1 alpha-3 Codes

AGO

Angola

HND

Honduras

PAK

Pakistan

ALB

Albania

HRV

Croatia

PAN

Panama

ARM

Armenia

HTI

Haiti

PER

Peru

AZE

Azerbaijan

IND

India

PHL

Philippines

BDI

Burundi

IRN

Iran, Islamic Republic of

POL

Poland

BEN

Benin

JAM

Jamaica

PRY

Paraguay

BFA

Burkina Faso

JOR

Jordan

RUS

Russian Federation

BGD

Bangladesh

JPN

Japan

RWA

Rwanda

BGR

Bulgaria

KAZ

Kazakhstan

SDN

Sudan

BLR

Belarus

KEN

Kenya

SEN

Senegal

BRA

Brazil

KGZ

Kyrgyzstan

SLE

Sierra Leone

BWA

Botswana

KHM

Cambodia

SLV

El Salvador

CAF

Central African Republic

LAO

Lao People’s Democratic Republic

SWZ

Swaziland

CIV

Côte d’Ivoire

LBN

Lebanon

SYR

Syrian Arab Republic

CMR

Cameroon

LKA

Sri Lanka

TCD

Chad

COG

Congo

LSO

Lesotho

TGO

Togo

COL

Colombia

MDA

Moldova, Republic of

THA

Thailand

DOM

Dominican Republic

MDG

Madagascar

TTO

Trinidad and Tobago

DZA

Algeria

MEX

Mexico

TUN

Tunisia

ECU

Ecuador

MKD

Macedonia

TUR

Turkey

EGY

Egypt

MLI

Mali

TZA

Tanzania, United Republic of

ETH

Ethiopia

MNG

Mongolia

UGA

Uganda

GAB

Gabon

MOZ

Mozambique

UKR

Ukraine

GBR

United Kingdom

MWI

Malawi

URY

Uruguay

GEO

Georgia

MYS

Malaysia

USA

United States

GHA

Ghana

NAM

Namibia

VEN

Venezuela, Bolivarian Republic of

GIN

Guinea

NER

Niger

YEM

Yemen

GMB

Gambia

NIC

Nicaragua

ZAF

South Africa

GNB

Guinea-Bissau

NPL

Nepal

ZWE

Zimbabwe

GTM

Guatemala

OMN

Oman

Table 3: Comparison among Alternative Development Indexes ()

Parametric

of Varying Coefficient

(GPC)

School_P

School_S

School_H

RMSE

0.022

0.017

0.019

0.027

0.020

No. of factors

6

6

6

3

5

Table 4: Cumulative Variation of the Residuals Explained by the Factors

No. Factors

1

2

3

4

5

6

Cumulative Variation

87.86%

94.87%

96.65%

98.10%

98.71%

99.01%

Table 5: Estimates of Coefficients at log(GPC)=3.98, 5, 6, 7, 8 and 8.81

log(GPC)=3.98

log(GPC)=5

log(GPC)=6

log(GPC)=7

log(GPC)=8

log(GPC)=8.81

log(GPC)

-0.0766

-0.0447

0.0117

0.0255

-0.0531

-0.2055

(-0.1145, -0.0429)

(-0.0618, -0.0305)

(-0.0038, 0.0249)

(0.0080, 0.0469)

(-0.0886, -0.0034)

(-0.2883, -0.0898)

csh_g

0.3341

0.1483

-0.0587

-0.2143

-0.2619

-0.1964

(0.1077, 0.5534)

(0.0706, 0.2248)

(-0.1110, -0.0107)

(-0.3141, -0.1454)

(-0.5782, 0.0082)

(-0.9416, 0.4733)

IP

-0.1284

-0.0545

-0.0093

0.0160

0.0282

0.0325

(-0.1971, -0.0621)

(-0.0686, -0.0422)

(-0.0191, 0.0059)

(-0.0046, 0.0406)

(-0.0146, 0.0638)

(-0.0895, 0.1209)

PGR

3.2821

0.5353

0.8485

1.5689

0.6502

-2.2853

(1.7325, 4.7072)

(0.0426, 0.9486)

(0.4054, 1.2542)

(1.1371, 1.9781)

(-0.1228, 1.3620)

(-3.5441, -0.7206)

School_S

0.1322

0.0823

-0.0420

-0.0147

0.3303

0.9119

(-0.1505, 0.4845)

(0.0108, 0.1495)

(-0.0780, -0.0081)

(-0.0548, 0.0177)

(0.1989, 0.4201)

(0.5495, 1.1719)

School_H

-1.5869

-0.1175

0.2220

0.0326

-0.2066

-0.1808

(-2.4454, -0.7631)

(-0.3214, 0.1119)

(0.1562, 0.3020)

(-0.0157, 0.0921)

(-0.2810, -0.1039)

(-0.3986, 0.1401)

LE

0.3148

0.2935

-0.0597

-0.2370

0.1455

1.0373

(-0.0171, 0.6403)

(0.1811, 0.3938)

(-0.1739, 0.0389)

(-0.3918, -0.0990)

(-0.2875, 0.5411)

(0.0000, 1.9922)

PESS

-1.2399

-0.5737

-0.2476

-0.0158

0.3070

0.7260

(-2.4950, 0.0107)

(-0.7969, -0.3513)

(-0.4210, -0.0944)

(-0.2163, 0.1716)

(-0.6249, 1.3302)

(-1.5776, 3.4530)

Military

-1.1748

-0.1436

-0.0428

-0.0020

0.6417

1.9197

(-2.4253, -0.0639)

(-0.3588, 0.1047)

(-0.1667, 0.0719)

(-0.2609, 0.1609)

(0.0134, 1.1085)

(0.1982, 3.4369)

Inflation

-0.0055

0.0006

-0.0011

-0.0031

0.0007

0.0107

(-0.0094, -0.0012)

(0.0000, 0.0012)

(-0.0016, -0.0005)

(-0.0039, -0.0023)

(-0.0043, 0.0048)

(-0.0020, 0.0209)

Civil

0.0183

0.0050

-0.0004

0.0033

0.0166

0.0340

(0.0048, 0.0308)

(0.0011, 0.0085)

(-0.0027, 0.0024)

(0.0000, 0.0064)

(0.0027, 0.0282)

(-0.0036, 0.0661)

Tra_Gro

0.0009

0.0304

0.0048

0.0018

0.0796

0.2279

(-0.1138, 0.1100)

(0.0117, 0.0458)

(-0.0162, 0.0252)

(-0.0248, 0.0351)

(-0.0062, 0.1727)

(-0.0124, 0.4799)

kgatr

-0.3099

-0.0815

-0.0763

-0.1422

-0.1597

-0.0776

(-0.4367, -0.1693)

(-0.1281, -0.0391)

(-0.1161, -0.0447)

(-0.1887, -0.0969)

(-0.2602, -0.0333)

(-0.3270, 0.2396)

lcr100km

0.6793

0.1930

0.0511

-0.0621

-0.3850

-0.9133

(0.5005, 0.8498)

(0.1396, 0.2461)

(0.0127, 0.0940)

(-0.1305, -0.0005)

(-0.5977, -0.2168)

(-1.4617, -0.5189)

cen_lat

0.5894

0.0293

0.0360

0.1693

0.0873

-0.3058

(0.3011, 0.8198)

(-0.0723, 0.1294)

(-0.0315, 0.1114)

(0.0985, 0.2655)

(-0.0526, 0.2459)

(-0.6344, 0.0789)

Spa_Col

-0.5174

-0.1564

-0.0204

0.0548

0.1945

0.4167

(-0.6748, -0.3222)

(-0.2111, -0.1080)

(-0.0503, 0.0091)

(0.0171, 0.0950)

(0.1040, 0.3131)

(0.1867, 0.6800)

Oil_OPEC

-0.1254

-0.0460

-0.0947

-0.0815

0.1358

0.5247

(-1.0835, 0.6246)

(-0.2325, 0.1181)

(-0.1496, -0.0423)

(-0.1383, -0.0344)

(-0.0124, 0.2413)

(0.1090, 0.8785)

Oil

-0.0100

-0.0021

-0.0008

-0.0011

0.0008

0.0057

(-0.0217, 0.0018)

(-0.0051, 0.0009)

(-0.0017, 0.0000)

(-0.0022, -0.0001)

(-0.0010, 0.0023)

(0.0004, 0.0099)

Chris

0.2689

0.1112

-0.0056

-0.1262

-0.2818

-0.4469

(0.1164, 0.4267)

(0.0650, 0.1711)

(-0.0535, 0.0461)

(-0.2001, -0.0629)

(-0.4824, -0.1333)

(-0.8908, -0.0694)

Mus

-0.0736

0.0130

-0.0292

-0.1685

-0.3744

-0.5692

(-0.1864, 0.0735)

(-0.0383, 0.0599)

(-0.0774, 0.0195)

(-0.2344, -0.1004)

(-0.5710, -0.2335)

(-1.0085, -0.2474)

Oth

-3.7386

0.6890

-1.1133

2.9016

21.6126

51.3537

(-13.0771, 4.1928)

(-1.3860, 2.4081)

(-3.0584, 0.7782)

(0.2919, 6.3889)

(11.6269, 32.3911)

(27.3474, 75.2005)

Jew

-32.4452

-10.5477

-2.0163

-0.9826

-2.7502

-3.6114

(-55.7335, -10.0679)

(-18.6022, -3.8609)

(-7.6269, 3.6243)

(-6.9105, 4.0461)

(-12.1471, 5.8912)

(-27.3730, 18.2231)

GS

-0.2516

-0.2079

-0.0476

-0.0738

-0.5101

-1.2583

(-0.5709, 0.0529)

(-0.3047, -0.1254)

(-0.1142, 0.0215)

(-0.1676, 0.0172)

(-0.8230, -0.1881)

(-2.1023, -0.4396)

Distortion

0.0231

0.0884

0.1085

0.0482

-0.1148

-0.3280

(-0.0449, 0.1048)

(0.0580, 0.1187)

(0.0701, 0.1435)

(-0.0064, 0.1025)

(-0.2793, 0.0061)

(-0.6718, -0.0148)

OO

1.0569

4.1811

5.1496

2.3016

-5.4384

-15.5641

(-2.1588, 4.9579)

(2.7557, 5.6164)

(3.3263, 6.8047)

(-0.2707, 4.8851)

(-13.1848, 0.3040)

(-31.9253, -0.7429)

ESP

0.3819

0.1039

0.0581

0.1010

0.1193

0.0577

(0.2151, 0.5483)

(0.0575, 0.1465)

(0.0214, 0.0975)

(0.0494, 0.1631)

(-0.0059, 0.2319)

(-0.2260, 0.2967)

EA

0.2924

0.0841

0.0263

-0.1256

-0.5515

-1.1753

(-0.1574, 0.7975)

(-0.0589, 0.2081)

(-0.0668, 0.1185)

(-0.2975, 0.0293)

(-1.0307, -0.1357)

(-2.2484, -0.2191)

EU

-1.0237

-0.2206

-0.0275

0.0738

0.4780

1.2174

(-1.7313, -0.3070)

(-0.3896, -0.0438)

(-0.0797, 0.0197)

(0.0169, 0.1225)

(0.3182, 0.6845)

(0.7527, 1.7964)

WarFrac

-0.0044

-0.0035

-0.0120

-0.0130

0.0058

0.0411

(-0.0372, 0.0351)

(-0.0121, 0.0072)

(-0.0179, -0.0040)

(-0.0208, -0.0036)

(-0.0157, 0.0235)

(-0.0227, 0.0882)

Coup

-0.0190

-0.0004

-0.0028

-0.0070

0.0016

0.0251

(-0.0287, -0.0089)

(-0.0031, 0.0020)

(-0.0051, -0.0005)

(-0.0102, -0.0038)

(-0.0086, 0.0113)

(-0.0005, 0.0502)

Revolution

-0.0052

0.0044

-0.0016

-0.0066

0.0021

0.0252

(-0.0198, 0.0090)

(0.0007, 0.0075)

(-0.0042, 0.0011)

(-0.0106, -0.0020)

(-0.0054, 0.0084)

(-0.0034, 0.0464)

Figure 1: Estimates of Common Factors

stands for the estimate of the factor, where .

Figure 2: Estimates of Factor Loadings

stands for the estimate of the factor loading, where .

Figure 3: Estimates of Selected Coefficient Functions

Supplementary Appendix A to

“An Integrated Panel Data Approach to

Modelling Economic Growth”

Guohua Feng∗, Jiti Gao♯ and Bin Peng†

∗University of North Texas, ♯Monash University and †University of Bath

Appendix A is divided into five sections. Section A.1 provides the numerical algorithm. Section A.2 examines the asymptotic results of Section 3 through several simulations. Section A.3 presents the preliminary lemmas and the proofs of the main theorems. Section A.4 explains why our method can partially solve the issue of time trend that has found limited attention in the empirical growth literature. In Section A.5, we provide auxiliary tables and figures of the empirical study.

Recall that in the main text, we have let , be the spectral norm of a matrix, and stand for the largest integer part of a real number . Here we further define some notations, which will be used throughout this file. Let , and , where and are and respectively. Moreover, means constructing block diagonal matrix from matrices (or scalars) .

A.1 Numerical Implementation

The following procedure essentially combines two algorithms discussed in Bai(2009) and Wang and Xia(2009) together. For each given , the estimates can be obtained using the following iteration procedure. Let and be the estimates obtained from the iteration. Then, for the iteration, the estimates are obtained as

where ; and is a diagonal matrix with the diagonal being the largest eigenvalues of

arranged in descending order. We stop the iteration when the estimates reach certain criteria, say . To start the above iteration, we randomly generate , where each element of follows from .

To choose the optimal , we follow Wang and Xia(2009) to simplify it as follows:

(A.1.1)

where is a scalar, and stands for the row of the unregularized estimator (i.e., implementing (3.3) of the main text with ). With the specification of (A.1.1), the idea for choosing lambda becomes straightforward. The unregularized estimator is a consistent estimator. It provides information on how likely each row of is a zero row. In other words, smaller implies that the row of is more likely to be zero and hence suggests a larger regularizer on . Given (A.1.1), the selection on the vector reduces to the selection on the scalar .

Finally, we consider the possible value of over a sufficiently large interval of the real line. The optimal is chosen by minimizing the BIC type criteria proposed in the main text. For the HD case, is chosen as in view of the development of Lemma A.7 and Theorem 3.3.

A.2 A Numerical Study

In this section, we examine the performance of the methodology of Section 3 through several simulations. Consider the model (2.4) of the main text. For the factor structure, let and . In order to generate the regressors and univariate index variable, we firstly generate , where . Then let , and , where stands for the first element of . By doing so, we generate certain correlation between the regressors and the factor structure, and also introduce some correlation between and . The error terms are generated as in which and , so that the weak cross-sectional dependence among individuals, and serial correlation over time dimension are generated. For both LD and HD cases, the rest settings are as follows:

•

LD Case:, , , and let and ;

•

HD Case:, , . For , when is odd, and when is even.

For each dataset generated, we implement the procedure of Section 3 to perform variable selection first. After identifying and , we implement post-selection estimation (i.e., remove the irrelevant regressors and then implement (3.3) of the main text with ) for the coefficient functions. We adopt the Hermite functions of Dong and Linton(2018) as the basis functions, repeat the above procedure 1000 times, and let444Note that the optimal choice of may not be the optimal one, but it satisfies all the requirements of our assumptions. Although the optimal choice of truncation parameter and the optimal bandwidth selection have been solved for some cross-sectional models and time series models (e.g., Gao, 2007; Hall et al., 2007) under the low dimensional cases, it is well understood that the question is still open even for the nonparametric panel data model with fixed effects (cf., Chen et al., 2012; Su and Jin, 2012). The question is even more daunting when the factor structure and variable selection procedure get involved., , and .

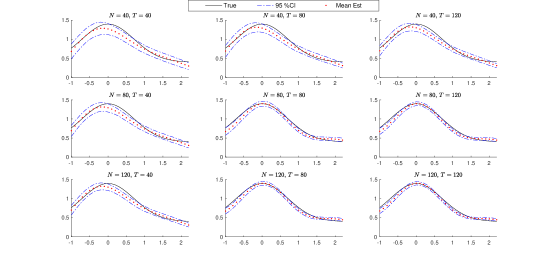

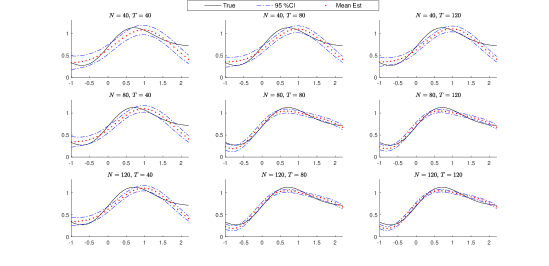

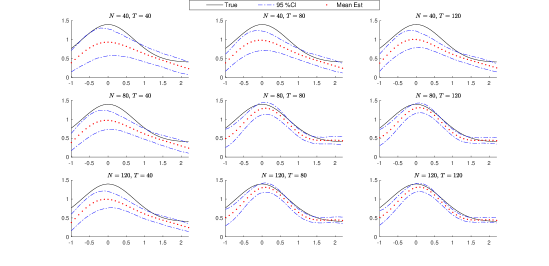

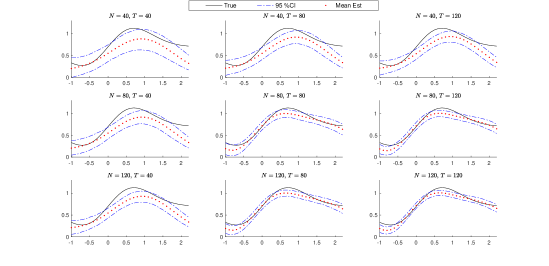

To evaluate our simulation results, we firstly report two percentages: (1) the percentage of missed true regressors (i.e., false negative rate, FNR); and (2) the percentage of falsely selected noise regressors (i.e., false positive rate, FPR). Secondly, we evaluate the estimates on the components of . Take as an example. For the replication, we obtain for (given it is not identified as 0; otherwise, we record 0 as the estimate). For , we calculate , and also record the 95% confidence bands based on . We plot these values over a certain range of . The values of are plotted in solid black line, and the values of are plotted in red dotted line, and the associated 95% confidence bands are plotted in blue dashed curves.

Table A.1 summarizes the FNR and FPR for the LD and HD cases respectively. It is clear that our method proposed in Section 3 works well, as both FNR and FPR are either 0 or very close to 0. It is worth mentioning that although FPR is slightly higher than zero for the HD case, over selecting the regressors will still yield consistent estimation.

Table A.1: FNR & FPR

FNR

FPR

40

80

120

40

80

120

LD

40

0.00%

0.00%

0.00%

0.00%

0.00%

0.00%

40