A Concave Value Function Extension for the Dynamic Programming Approach to Revenue Management in Attended Home Delivery∗

Abstract

We study the approximate dynamic programming approach to revenue management in the context of attended home delivery. We draw on results from dynamic programming theory for Markov decision problems, convex optimisation and discrete convex analysis to show that the underlying dynamic programming operator has a unique fixed point. Moreover, we also show that – under certain assumptions – for all time steps in the dynamic program, the value function admits a continuous extension, which is a finite-valued, concave function of its state variables. This result opens the road for achieving scalable implementations of the proposed formulation, as it allows making informed choices of basis functions in an approximate dynamic programming context. We illustrate our findings using a simple numerical example and conclude with suggestions on how our results can be exploited in future work to obtain closer approximations of the value function.

1 Introduction

1.1 Revenue Management and Attended Home Delivery

The expenditure of US households on online grocery shopping could reach $100 billion in 2022 according to the Food Marketing Institute [1]. Although growth forecasts vary and more conservative estimates lie, for example, at $30 billion for the year 2021 [2], the overall trend is clear: The online grocery sector is likely to grow if some of its main challenges can be overcome.

One of these challenges is managing the logistics as one of the main cost-drivers. In particular, one can seek to exploit the flexibility of customers by offering delivery options at different prices to create delivery schedules that can be executed in a cost-efficient manner. There are a number of ways to achieve this. Recent proposals include, for example, giving customers the choice between narrow delivery time windows for high prices and vice versa [3] or charging customers different prices based on the area and their preferred delivery time [4, 5, 6].

In this paper, we focus on the latter. We refer to the problem of finding the profit-maximising delivery slot prices as the revenue management problem in attended home delivery, where “attended” refers to the requirement that customers need to be present upon delivery of the typically perishable goods, which is in contrast to, for example, standard mail delivery. Note that attended home delivery problems are more complex than standard delivery services, because goods need to be delivered in time windows that were pre-agreed with the customers.

We adopt a dynamic programming (DP) model of an expected profit-to-go function, the value function of the DP, given the current state of orders and time left for customers to book a delivery slot. This DP was initially devised in the fashion industry [7], but subsequently adopted and refined by the transportation sector and the attended home delivery industry [5].

To find the optimal delivery slot prices, we need to compute the value function (at least approximately) for all states and times. The main challenge with this is that the state space of the DP grows exponentially with the set of delivery time slots, i.e. it suffers from the “curse of dimensionality”. This means that for industry-sized problems, the value function cannot be computed exactly, even off-line, because there are too many states. Our ultimate objective is to compute improved value function approximations. Therefore, we study in this paper how the value function of the exact DP behaves mathematically in time and across state variables.

In this paper we show that – under certain assumptions – for all time steps in the dynamic program, the value function admits a continuous extension, which is a finite-valued, concave function of its state variables. This result opens the road for achieving scalable implementations of the proposed formulation, as it becomes possible to make informed choices of basis functions in an approximate dynamic programming context.

Improved value function approximations could finally be used for calculating optimal delivery slot prices. This has been shown by [8], where it is proven that a unique set of optimal delivery slot prices exists, which can be found using simple Newton root search algorithms if estimates of the value function are known for all states and times.

Our paper is structured as follows: In the remainder of Section 1, we introduce some notation. Then in Section 2, we define the revenue management problem in attended home delivery and formulate it as a DP. In Section 3, we state the definitions and assumptions that our analysis is based on and present our main result, Theorem 2, which says that there exists a continuous extension of the value function of the exact DP that is a finite-valued, concave function in its state variables. Section 4 contains reformulations of the DP into mathematically more convenient forms and develops a series of supporting results leading to the proof of Theorem 2. Section 5 presents a numerical illustration of the proposed scheme, while Section 6 concludes the paper and suggests directions for future research.

1.2 Notation

Let denote a column vector of ones. Given some , let be a column vector build by stacking the transposed rows of a unit matrix with at the th entry. Let be the non-negative real numbers and let dim denote the dimension of its argument. Let conv denote the convex hull of its argument.

2 Revenue Management Problem Formulation

In this section, we derive a discrete-state formulation of the revenue management problem in attended home delivery.

2.1 Problem Statement

We model an online business that delivers goods to locations of known customers. We adopt a local approximation of the revenue management problem by dividing the service area geographically into a set of non-overlapping rectangular sub-areas , where the customers in each area are served by one delivery vehicle. This model resembles the setting in [6].

We consider a finite booking horizon with possibly unequally-spaced time steps indexed by . We refer to [5, Section 4.3] for details on how to obtain a customer arrivals model using a Poisson process with time-invariant event rate for all from a Poisson process with homogeneous time steps, but time-varying event rate. The probability that a customer arrives from sub-area is given by with .

Customers can choose from a number of (typically 1-hour wide) delivery time windows, which we call slots , where . Let correspond to a customer not choosing any slot. Each sub-area/delivery slot pair is assigned a delivery charge , for some minimum allowable charge (which is typically, though not necessarily, positive) and some maximum allowable charge . The role of is a convention to indicate that slot is not offered in area . This will be explained in more detail when introducing the customer choice model below.

We define consisting of the set of delivery charges that the business decides to charge at any time step , where it is to be understood that is a stacked vector including the different values that can take as and vary. Let the set of allowed decision vectors be .

For each sub-area/delivery slot pair , we denote the number of placed orders by . We define , where is a scalar indicating the maximum number of deliveries that can be fulfilled in the sub-area/delivery slot pair . In general, we do not require the maximum number of deliveries to be the same for all areas and all slots, e.g. because this will depend on the size of the delivery area. Examples of computing this quantity can be found in [6, Section 4]. Let us also define . Let denote the expected net revenue of an order, i.e. expected revenue minus costs prior to delivery. This is assumed to be invariant across all orders. We define

| (1) |

where . The function approximates the delivery cost to fulfil the set of orders . The precise delivery cost cannot be computed, as it is the solution to a vehicle routing problem with time windows, which is intractable for industry-sized applications [9].

Let the probability that a customer chooses sub-area/delivery slot pair if offered prices be , such that for all . For all areas , note that , where denotes the probability of a customer from sub-area leaving the online ordering platform without choosing any delivery slot. A typical choice for is the multinomial logit model that was also used in [6]:

| (2) |

where denotes a constant offset, represents a measure of the popularity for all delivery slots and is a parameter for the price sensitivity. Note that the no-purchase utility is normalised to zero, i.e. for the no-purchase “slot” , we have and hence, the in the denominator of (2) arises from .

Note that our results on the fixed point computation do not depend on the particular form of the customer choice model. We only require that it is a probability distribution and in the limit as for all , we have that tends to zero with a higher than linear rate of convergence. This is important, because otherwise the expected profit-to-go will be unbounded.

For convenience, let the probability that a customer arrives from sub-area and chooses slot given prices be denoted by . We define and . Finally, it is to be understood that sums over and are always computed over their entire sets and , respectively. Similarly, decisions are made such that .

2.2 Dynamic Programming Formulation

We can express the problem described above as a DP. The expected profit-to-go, , closely resembles the DP formulation in [6] and we define it as

| (3) |

i.e. denotes the terminal condition. The difference represents the value foregone by accepting a additional (discrete spatial) order, which in economic terms is the opportunity cost of an order. Note that – similar to [6] – we ignore any vehicle load capacity constraints in the problem, as they are much less restricting than the time constraints on the delivery slots. Therefore, including the vehicle load capacity constraints would only increase computational costs, but would not substantially improve the decision policy.

For convenience in the sequel, let us define an abstract operator notation which expresses (2.2) in a more compact form:

| (4) |

3 Concave Continuous Extension Theorem

As the state space is discrete, it is not possible to establish convexity properties from standard, i.e. continuous, convexity theory. In this section, we therefore first provide some definitions from discrete convex analysis and the assumptions upon which our main results are based. We then state our main result, Theorem 2, and two intermediate results, Theorem 3 and Proposition 4.

3.1 Definitions

Definition 1.

We define the set of stochastic vectors in as

| (5) |

Definition 2.

Let and let be a finite set. Then is defined to be an enclosing set of if conv.

Definition 3.

We define as the set of all sets enclosing .

Definition 4 (cf. [10, (2.1)]).

Let and . Then the concave closure of a function is defined as

| (6) |

for all and for all .

Definition 5 (cf. [10, Lemma 2.3] and [11, Proposition 2.31]).

A function is concave extensible if and only if any of the following equivalent conditions hold:

-

(a)

The evaluations of coincide with the evaluations of its concave closure , i.e. for all .

-

(b)

For all and for all , the evaluation of at does not lie below any possible linear interpolation of on the points , i.e. for all , for all and for all , such that , it holds that

(7)

3.2 Assumptions

We now state the assumptions that our main result builds on.

Assumption 1.

The negative cost function is concave extensible.

Assumption 2.

The marginal cost of an additional, feasible order is always smaller than the maximum marginal profit, i.e. , for all .

Let us define:111Section 4.2.1 details why we have dropped the argument in and and write simply and instead.

| (8) |

for all and .

Assumption 3.

For all , we assume that is concave extensible in , for any that is concave extensible in .

Assumption 1 is satisfied for the class of affine functions typically used in the literature [6]. Assumption 2 is not restrictive, as it offers the means to ensure that every additional order can generate profit. Otherwise, the delivery slot prices, which maximise (2.2), would always be for all , resulting in not offering any slots. Assumption 3 intuitively states that , a weighted perturbation of in , should be concave extensible. This assumption appears to be strong, but it can always be satisfied by choosing a small enough customer arrival probability . Hence, and can be made arbitrarily small and one of the following two cases occurs:

1) Consider that is strictly concave extensible, by which we mean that the condition for concave extensibility (7) is satisfied with strict inequality, i.e. . The inequality condition for concave extensibility (7) of then becomes

| (9) |

where . Let us define as well as , where the minimisation is taken with respect to and and the maximisation is taken with respect to , and . Then the inequality in (9) can be tightened to obtain

| (10) |

As and , there exists a that satisfies the above inequality for all . Therefore, implicitly depends on , but for simplicity, we will just write .

2) Consider that , i.e. the points lie on a hyperplane. Then for all and . Therefore, (9) holds with equality, independently of the particular choice of .

Remark 1.

There are a few more special cases, where Assumption 3 is trivially satisfied. For example, if is a degenerate interval, i.e. it only contains a single , then there is only a single , which also means that for all and (9) holds for all .

Similarly, in the case that there is only one delivery sub-area/slot pair , i.e. and are both singleton sets, the inequality condition (9) simplifies to

| (11) |

As in this scenario is a one-dimensional concave extensible function, we can express this inequality in terms of the concave closure of .

| (12) |

Noting that , (12) holds, since is concave (in the ordinary sense) by Definition 4.

3.3 Statement of Main Results

Based on the aforementioned definitions and assumptions, we formulate our main result:

The proof of Theorem 2 mainly depends on the following two results:

Proposition 4.

Consider Assumption 3 and fix any . If is concave extensible in , then is also concave extensible in .

4 Fixed Point Theorem and Concavity Preservation

4.1 Fixed Point Characterisation

To prove Theorem 3, we first establish a helpful, alternative formulation of (2.2). We then state some supporting lemmata and proceed with the proof. The proofs of all supporting lemmata can be found in the Appendix.

4.1.1 Stochastic Shortest Path Problem Reformulation

In this section, we reformulate (2.2) as an equivalent stochastic shortest path problem, a special version of an undiscounted, finite-state, discrete-time Markov decision problem. We can follow the arguments of [12, Chapter 3] to rewrite (2.2) as

| (14) |

where and are defined as follows: If , then and for all , if , then . In all other cases, . Note that the first case is associated with no transition, the second case is a valid, i.e. unit-sized, order and the third group covers all invalid cases.

In a similar way, for all , if , then and in all other cases, . For convenience, similarly to [12, Chapter 3], we define to simplify (14):

| (15) |

Let be the solution to a different, stationary DP with the same transition probabilities as in (15), but if and , otherwise.

| (16) |

Note that for all . Let us also define as

| (17) |

Since we have for all , we conclude that . Finally, let

| (18) |

be a weighted sup-norm of .

Lemma 5.

The mapping defined by the operator is contractive with modulus of contraction , i.e.

| (19) |

for all and .

4.1.2 Proof of Theorem 3

We start with the necessary and sufficient condition for to have a fixed point , which is . This translates into (2.2) as

| (20) |

Substituting (13) into (20) yields

| (21) |

The values of all are non-negative for all and for all . The value of is non-positive and only if for all . It follows that the maximum non-negatively weighted sum of the terms is , so (21) holds. As the value function is invariant at and at this point , is indeed a fixed point of for all . ∎

4.2 Preserving Concavity

The structure of this section is similar to the structure of Section 4: We first reformulate (2.2), then we state some supporting lemmata and finally, we prove Proposition 4.

4.2.1 Change of Decision Variables

We start the derivation of Proposition 4 by reformulating (2.2) as a maximisation over instead of . As shown by [8], this is possible, because the following unique mapping between and exists:

| (22) |

where by solving with respect to we obtain

| (23) |

Hence, we can rewrite (2.2) and break it down into two parts:

| (24) |

where we have defined

| (25) |

and is from (8). This allows us to make the next statement:

Lemma 6.

The function is concave extensible in .

We are finally ready to prove Proposition 4 showing that preserves concave extensibility of in .

4.2.2 Proof of Proposition 4 and Theorem 2

By Lemmata 6 and Assumption 3, and have continuous extensions and , which are both jointly concave in . Therefore, is also jointly concave in . We define . This allows us to exploit a standard convex optimisation result (see [11, Proposition 2.22] or [13, Section 3.2.5]), according to which the maximisation with respect to some variables of a continuous multivariate function that is jointly concave in all its variables, yields a concave function. Therefore is a concave function of .

Repeating the same calculation, now with the discrete in place of , i.e. , note that for all grid points . Therefore, for all grid points . This shows that is a continuous extension of , which is concave in . Hence, is concave extensible in . ∎

Having proved Theorem 3 and Proposition 4 in the previous sections, the stage is set for the proof of Theorem 2.

By the definition of , is finite-valued and by Theorem 3, is also finite-valued. Hence for all , the difference is finite-valued. Let us use Lemma 5, according to which for all and :

| (26) |

Let , where the limit uniquely exists and is well-defined, let and apply times:

| (27) |

As , the pointwise difference in between and is finite for all , which implies that is finite for all .

By Assumption 1, for all is concave extensible. Hence, due to Proposition 4, which is effectively an inductive step, we can conclude that for all , is finite-valued, concave extensible in .∎

Due to this result and based on [12, Chapter 3], we can also show that the fixed point (13) is unique. Assume by contradiction that there are two fixed points of (4), and . Substituting and for and in (19), respectively we obtain

| (28) |

Applying times and taking the limit as , yields

| (29) |

By reversing the roles of and , we can conclude that and therefore, there can be at most one fixed point.

5 Illustrative Example

We illustrate our findings using a simple numerical example of a 1-area, 2-slot problem. The parameters are listed in Table 1 below.

| 1 | |

These parameters yield the terminal condition

| (30) |

and the fixed point

| (31) |

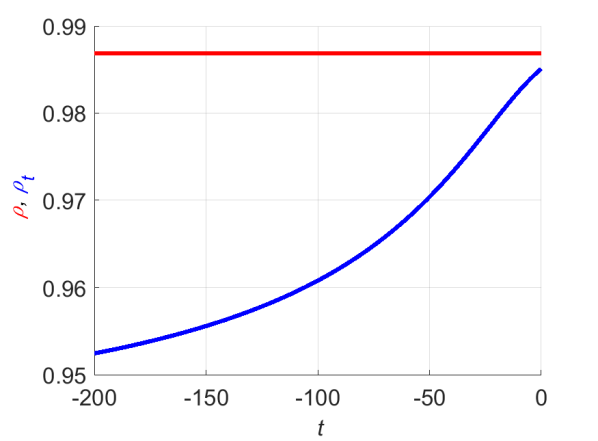

for all . To illustrate the contractive mapping property described by (19), we compute numerically by solving the auxiliary DP in (16) and compare it with the running contractive ratio with respect to the fixed point :

| (32) |

By choosing to be the reference point, we also show that the DP converges to the fixed point as defined in (13). Fig. 1 below illustrates this by showing that is an upper bound for for all .

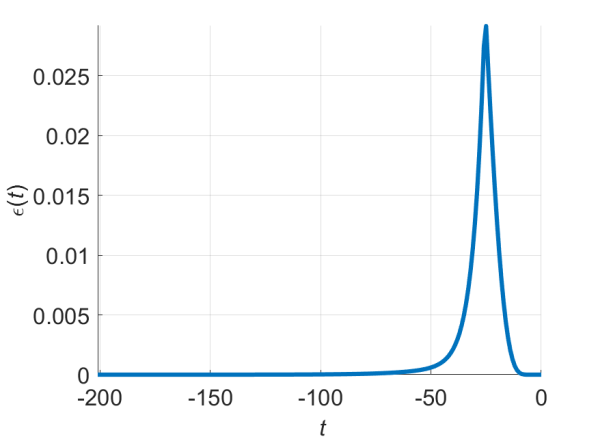

We define a measure of discrete concavity

| (33) |

such that for all . Note that implies that is concave extensible. We compute this quantity by enumeration of all possible enclosing sets and plot the result in Fig. 2, from which it can easily be seen that for all .

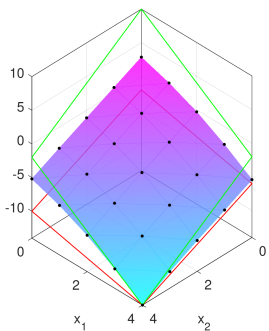

Finally, we plot the value function for in Fig. 3 below. Note that the value function lies between the terminal condition and the fixed point. When it comes to approximating , this information can be used to limit the range of basis function parameters, such that the approximated version of always lies between the terminal condition and the fixed point.

6 Conclusions and Future Work

We have studied the mathematical properties of the value function of a dynamic program modelling the revenue management problem in attended home delivery exactly. We have shown that the recursive dynamic programming mapping has a unique, finite-valued fixed point and concavity-preserving properties. Hence, we have derived our main result stating that – under certain assumptions – for all time steps in the dynamic program, the value function admits a continuous extension, which is a finite-valued, concave function of its state variables. We have illustrated our findings using a simple numerical example and now conclude with suggestions on how our results can be exploited in the future to obtain closer approximations of the value function.

Recent approaches have estimated as an affine function of for each [6]. Based on our result, we believe that closer approximations can be found by pursuing different approximation strategies.

One possible direction of future research involves investigating the use of parametric models comprising concave basis functions. This idea can be exploited directly by using the given DP formulation – as suggested in [14, Section 8.2] – or by reformulating the problem as a linear program – as shown by [15]. Note that a priori knowledge of concave extensibility of for all creates some intuitive regularity. Therefore, it can be expected to get good approximations of from a relatively small sample size even with simple models.

Another possible direction would be to adapt techniques that fit convex functions (or equivalently concave functions for our purposes) to multidimensional data. For example, [16] and [17] show how data can be fitted by a function defined as the maximum of a finite number of affine functions. More sophisticated examples of convex (concave) function fitting techniques include adaptive partitioning [18] and Bayesian non-parametric regression [19].

Future work will show which strategy will find the best compromise between accuracy of the approximation and computational cost.

Appendix

Proof of Lemma 5.

Proof of Lemma 6.

By inspection, is only a function of the continuously-valued variable , so it will be concave extensible in if it is concave in (in the ordinary, continuous sense of concavity). First, note that the function is separable, i.e.

| (40) |

where we have defined

| (41) |

Previously, [8] have shown that a structurally similar function is concave in its variables. We adopt their approach – computing the Hessian and showing that it is negative definite – to verify that is jointly concave in for all . We first compute the first-order partial derivatives of :

| (42) |

The second-order partial derivatives are:

| (43) |

Note that the partial derivatives show that is independent of all , for which . The resulting Hessian of with its second partial derivatives with respect to for all is:

| (44) |

where we have defined block sub-matrices and such that is a scalar corresponding to the last entry of . Note that is negative definite, because for all and . We compute the Schur complement of in :

| (45) |

As is negative definite and as is non-positive, is negative semi-definite. This implies that for all , is concave in . As taking the sum of concave functions preserves concavity (see [13, Section 3.2.1]), is also concave in . Hence, is concave extensible in . ∎

References

- [1] “Food marketing institute,” https://www.fmi.org/digital-shopper/, 2018, accessed: 2018-05-16.

- [2] “Are meal-kit delivery companies a threat or an opportunity?” https://pitchbook.com/news/articles/are-meal-kit-delivery-companies-a-threat-or-an-opportunity, 2017, accessed: 2018-05-16.

- [3] A. M. Campbell and M. Savelsbergh, “Incentive schemes for attended home delivery services,” Transportation Science, vol. 40, no. 3, pp. 327–341, 2006. [Online]. Available: https://pubsonline.informs.org/doi/abs/10.1287/trsc.1050.0136

- [4] K. Asdemir, V. S. Jacob, and R. Krishnan, “Dynamic pricing of multiple home delivery options,” European Journal of Operational Research, vol. 196, no. 1, pp. 246–257, 2009. [Online]. Available: http://www.sciencedirect.com/science/article/pii/S0377221708002634

- [5] X. Yang, A. K. Strauss, C. S. M. Currie, and R. Eglese, “Choice-based demand management and vehicle routing in e-fulfillment,” Transportation Science, vol. 50, no. 2, pp. 473–488, 2016. [Online]. Available: https://doi.org/10.1287/trsc.2014.0549

- [6] X. Yang and A. K. Strauss, “An approximate dynamic programming approach to attended home delivery management,” European Journal of Operational Research, vol. 263, no. 3, pp. 935–945, 2017. [Online]. Available: http://www.sciencedirect.com/science/article/pii/S0377221717305738

- [7] G. Gallego and G. van Ryzin, “Optimal dynamic pricing of inventories with stochastic demand over finite horizons,” Management Science, vol. 40, no. 8, pp. 999–1020, 1994. [Online]. Available: https://doi.org/10.1287/mnsc.40.8.999

- [8] L. Dong, P. Kouvelis, and Z. Tian, “Dynamic pricing and inventory control of substitute products,” Manufacturing & Service Operations Management, vol. 11, no. 2, pp. 317–339, 2009. [Online]. Available: https://pubsonline.informs.org/doi/abs/10.1287/msom.1080.0221

- [9] P. Toth and D. Vigo, Vehicle Routing, D. Vigo and P. Toth, Eds. Philadelphia, PA: Society for Industrial and Applied Mathematics, 2014. [Online]. Available: https://epubs.siam.org/doi/abs/10.1137/1.9781611973594

- [10] K. Murota and A. Shioura, “Relationship of m-/l-convex functions with discrete convex functions by miller and favati–tardella,” Discrete Applied Mathematics, vol. 115, no. 1, pp. 151–176, 2001, first Japanese-Hungarian Symposium for Discrete Mathematics and its Applications. [Online]. Available: http://www.sciencedirect.com/science/article/pii/S0166218X01002220

- [11] R. Rockafellar and R. J.-B. Wets, Variational Analysis. Heidelberg, Berlin, New York: Springer Verlag, 1998.

- [12] D. P. Bertsekas, Dynamic Programming and Optimal Control, Vol. II, 4th ed. Athena Scientific, 2012.

- [13] S. Boyd and L. Vandenberghe, Convex Optimization. New York, NY, USA: Cambridge University Press, 2004.

- [14] W. B. Powell, Approximate Dynamic Programming: Solving the Curses of Dimensionality (Wiley Series in Probability and Statistics). New York, NY, USA: Wiley-Interscience, 2007.

- [15] D. P. de Farias and B. V. Roy, “The linear programming approach to approximate dynamic programming,” Operations Research, vol. 51, no. 6, pp. 850–865, 2003. [Online]. Available: https://doi.org/10.1287/opre.51.6.850.24925

- [16] J. Kim, J. Lee, L. Vandenberghe, and C.-K. K. Yang, “Techniques for improving the accuracy of geometric-programming based analog circuit design optimization,” in IEEE/ACM International Conference on Computer Aided Design, 2004. ICCAD-2004., 2004, pp. 863–870. [Online]. Available: https://ieeexplore.ieee.org/document/1382695/

- [17] A. Magnani and S. P. Boyd, “Convex piecewise-linear fitting,” Optimization and Engineering, vol. 10, no. 1, pp. 1–17, 2009. [Online]. Available: https://doi.org/10.1007/s11081-008-9045-3

- [18] L. A. Hannah and D. B. Dunson, “Multivariate convex regression with adaptive partitioning,” J. Mach. Learn. Res., vol. 14, no. 1, pp. 3261–3294, 2013. [Online]. Available: http://www.jmlr.org/papers/v14/hannah13a.html

- [19] L. A. Hannah and D. B. Dunson, “Bayesian nonparametric multivariate convex regression,” ArXiv e-prints, 2011. [Online]. Available: https://arxiv.org/abs/1109.0322