On confidence intervals centered on bootstrap smoothed estimators

Paul Kabaila∗ and Christeen Wijethunga

Department of Mathematics and Statistics, La Trobe University, Australia

ABSTRACT

Bootstrap smoothed (bagged) estimators have been proposed as an improvement on estimators found after preliminary data-based model selection.

Efron, 2014, derived a widely applicable formula for a delta method approximation to the standard deviation of the bootstrap smoothed estimator. He also considered a confidence interval centered on the bootstrap smoothed estimator, with width proportional to the estimate of this standard deviation.

Kabaila and Wijethunga, 2019, assessed the performance of this confidence interval in the scenario of two nested linear regression models, the full model and a simpler model, for the case of known error variance and preliminary model selection using a hypothesis test. They found that the performance of this confidence interval was not substantially better than the usual confidence interval based on the full model, with the same minimum coverage.

We extend this assessment to the case of unknown error variance

by deriving a computationally convenient exact formula for the ideal (i.e. in the limit as the number of bootstrap replications diverges to infinity) delta method approximation to the standard deviation of the bootstrap smoothed estimator.

Our results show that, unlike the known error variance case, there are circumstances in which this confidence interval has attractive properties.

In applied statistics there is usually some uncertainty as to which explanatory

variables should be included in the model. The first attempt to deal with this

‘model uncertainty’ was to use preliminary data-based model selection employing

either hypothesis tests or minimizing a criterion such as the Akaike Information Criterion

(Akaike, 1974).

This model selection was followed by the statistical inference of interest, based on the assumption that the selected model had been given to us a priori,

as the true model. This assumption is false and typically leads to incorrect and misleading inference (see e.g. Kabaila,

2009 and Leeb and Pötscher, 2005).

Bootstrap smoothed (or bagged; Breiman,

1996) estimators have been proposed as an

improvement on estimators found after preliminary data-based model selection (post-model-selection estimators). Bootstrap smoothed estimators are

smoothed versions of the post-model-selection estimator.

The key result of Efron (2014) is a formula for a delta method approximation,

, to the standard deviation of the bootstrap smoothed estimator.

This formula is valid for any exponential family of models and has the attractive feature that it simply re-uses

the parametric bootstrap replications that were employed to find this estimator.

It also has the attractive feature that it is applicable in the context of complicated data-based model selection.

Kabaila and Wijethunga (2019) consider a confidence interval (CI) centered on the bootstrap

smoothed estimator, with nominal coverage , and half-width equal to the quantile of the standard normal distribution multiplied by the estimate of .

We call this interval the .

This CI has similarities with the frequentist model averaged CIs proposed

by Buckland et al. (1997), Fletcher and Turek (2011) and Turek and Fletcher (2012).

All of these CIs need to have their performances, in terms of coverage probability and expected length, carefully assessed before they can be recommended for general use by applied statisticians. We believe that such assessments are best carried out

through a sequence of increasingly complicated ‘test scenarios’.

The simplest test scenario consists of

two nested linear regression models, where the simpler model is given by a specified linear combination of the regression parameters being set to zero. In this test scenario, the scalar parameter of interest is a distinct linear combination of the regression parameters and we assume independent and identically distributed normal errors, with error variance assumed known.

Kabaila and Wijethunga (2019) provide a detailed assessment of the performance of the in this test scenario if the

simpler model is selected when a preliminary hypothesis test accepts the null hypothesis that this simpler model is correct.

They found that, while this CI performed much better than the post-model-selection confidence interval in terms of minimum coverage

probability, its performance in terms of expected length was not substantially better than the usual CI based on the full model, with the same minimum coverage.

The next simplest test scenario is the same, but with

unknown error variance. Kabaila et al. (2016) and Kabaila et al. (2017) used this test scenario to provide a detailed assessment of the performance of the CIs proposed by Fletcher and Turek (2011) and Turek and Fletcher (2012).

Our aim is to extend the assessment

made by Kabaila and Wijethunga (2019) of the performance of the

to this test scenario.

We apply Theorem 2 of Efron (2014)

to derive a computationally convenient exact formula for the ideal (i.e. in the limit as the number of bootstrap replications diverges to infinity) delta method approximation to the standard deviation of the bootstrap smoothed estimator.

An outline of this derivation, which is quite complicated, is provided in Appendix A.1.

Our computed results show that, unlike the case that the error variance is assumed known, there are circumstances

in which the expected length properties of the

are quite attractive.

2. The two nested regression models and the post-model-selection estimator

We consider two nested linear regression models: the full model

and the simpler model .

Suppose that the full model is given by

where is a random -vector of responses, is a known matrix with linearly independent columns

(), is an unknown -vector of parameters and , with an unknown positive parameter.

Suppose that

, where is the scalar parameter of interest,

is a scalar parameter used in specifying the model and is a ()-dimensional parameter vector. The model is with . As shown in Appendix A of Kabaila and Wijethunga (2019), this scenario can be obtained by a change of parametrization from a more

general scenario. Let .

Let denote the least squares estimator of , so that

,

and .

Also let and denote the first and second components of

, respectively.

Now

let , and

, where .

Note that , , and are known.

Let , which is an unknown parameter, and

.

Suppose that we carry out a preliminary test of the null hypothesis against the alternative hypothesis

and that we choose the model if this null hypothesis is accepted;

otherwise we choose the model .

Let be defined by for .

Suppose that we accept the null hypothesis when

; otherwise we reject the null hypothesis. The size of this

preliminary test is .

Therefore the post-model-selection estimator of is equal to

Henceforth, suppose that

and are given.

3. Computationally convenient exact formulas for the ideal bootstrap smoothed estimate and the delta method approximation to its standard deviation

The parametric bootstrap smoothed estimate of is obtained as follows.

Note that

and, independently, (if then is said to have a distribution).

To make the dependence of on

explicit, write

.

For the estimate treated as the true parameter value, suppose that

and, independently, .

A parametric bootstrap sample of size consists of independent observations

of the random vector

.

The parametric smoothed estimate of is defined to be

The limit as the number

of boostrap replications

of this quantity is called by Efron (2014) the ideal bootstrap smoothed estimate of . We denote this ideal boostrap smoothed estimate by and observe that it may be obtained as follows.

Let denote the expected value of ,

for true parameter value .

The ideal bootstrap smoothed estimate

is obtained by first evaluating

and then replacing

by .

Let and define to be

(1)

where and denote the pdf and cdf, respectively, and denotes the probability density function of . As proved in Appendix B of Kabaila and Wijethunga (2019),

. Therefore

An outline of the proof of the following new theorem is given in Appendix A.1.

Theorem 1.

An application of Theorem 2 of Efron (2014) leads to the ideal

(i.e. in the limit as the number

of boostrap replications ) delta method approximation

to the standard deviation of , denoted by

, which is

, where

(2)

Here is defined to be

(3)

and

(4)

where, as before, .

We expect, intuitively, that the results obtained for the case that is

unknown (so that it must be estimated from the data) and should be the same as for the case that is known.

Suppose that is fixed and , so that also diverges to . As expected, the ideal delta method approximation to the standard deviation of given by Theorem 1 converges to the

corresponding quantity

given by Theorem 2 of Kabaila and Wijethunga (2019), which deals with the case that

is known.

4. Computationally convenient exact formula for the coverage probability of the confidence interval centered on the bootstrap smoothed estimator

Consider the CI for centered on the bootstrap smoothed estimator , with nominal coverage ,

which we call the interval.

Note that when , this CI is identical to the usual CI, with actual coverage , based on the full model .

It may be shown that the coverage probability

is a function of . We therefore denote this coverage probability by

. The following theorem is proved in Appendix A.2.

Theorem 2.

Let

(5)

(6)

Then is given by

where for .

The expression (2) suggests that, for all sufficiently large ,

is determined by , for any given .

Computational results for

(described later in this section) and (not described either here or in the Supporting Material) suggest that, for all ,

is, for practical purposes, determined by , for any given .

It may be shown that is (a) an even function of for each and (b) an even function of for each .

It follows that,

for given and ,

we are able to encapsulate the coverage probability of

the

, for all possible choices of design matrix, parameter of interest and parameter that specifies the simpler model, using only the parameters and .

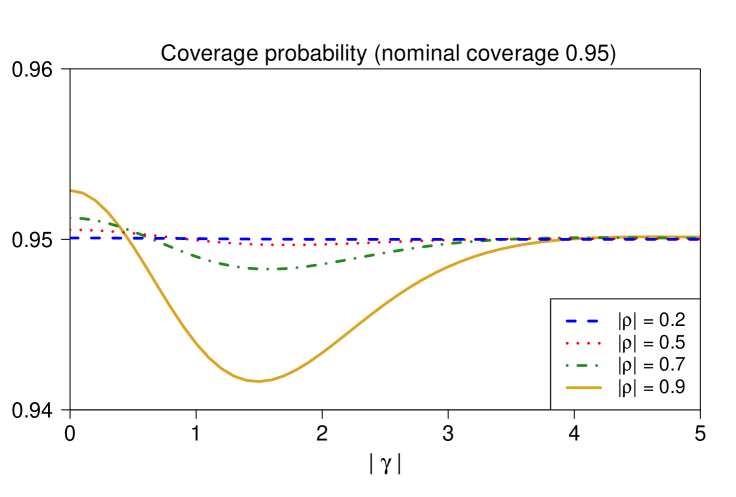

Figure 1 is the graph of coverage probability of the confidence interval centered on the bootstrap smoothed estimator, which is based on the post-model-selection estimator obtained after a preliminary hypothesis test, with size , of the null hypothesis that the simpler model is correct. We consider the case

that the nominal coverage is 0.95,

, and and 0.9.

All of the computations reported in this paper were carried out using programs written in

R.

The minimum coverage probability of this CI is a continuous decreasing function of

which equals the nominal coverage

when . Graphs of the coverage probability of

for the same values of nominal coverage, size of the preliminary hypothesis test, and are

provided

in the Supporting Material for and 10.

Further extensive numerical investigations, not reported either here

or in the Supporting Material, show that the

outperforms the post-model-selection CI, with the same nominal coverage and based on the same preliminary test, in terms of coverage probability.

Figure 1: The coverage probability of the interval,

which is based on the post-model-selection estimator obtained after a preliminary hypothesis test, with size , of the null hypothesis that the simpler model is correct. The nominal coverage is 0.95,

, and and 0.9.

5. Computationally convenient exact formula for the scaled expected length of the confidence interval centered on the bootstrap smoothed estimator

We define the scaled expected length of , with nominal coverage ,

to be the expected length of divided by the expected length of the usual CI, based on the full model, with the same coverage

as the minimum coverage probability of . Let denote this minimum coverage probability. Now let denote the usual CI for , with coverage probability , based on the full model. In other words,

.

It may be shown that the scaled expected length of

is a function of . We therefore denote this scaled expected length by .

The following theorem is proved in Appendix A.3.

Theorem 3.

Let denote the minimum coverage probability of the confidence interval , with nominal coverage . Then is given by

The expression (2) suggests that, for all sufficiently large ,

is determined by , for any given .

Computational results for

(described later in this section) and (not described either here or in the Supporting Material) suggest that, for all ,

is, for practical purposes,

determined by , for any given .

It may be shown that is (a) an even function of for each and (b) an even function of for each .

It follows that,

for given and , we are able to encapsulate the scaled expected length of

the

, for all possible choices of design matrix, parameter of interest and parameter that specifies the simpler model,

using only the

parameters

and .

The bootstrap smoothed estimator is obtained by smoothing the post-model-selection estimator that results from a preliminary test of the null hypothesis that the simpler model is correct i.e. that .

This post-model-selection estimator is usually motivated by a desire for

good performance when the simpler model is correct. Therefore, ideally, the

should have a scaled expected length that is substantially less than 1 when . In addition, ideally, this confidence interval should have a scaled expected length that (a) has maximum value that is not too much larger than 1 and (b) approaches 1 as approaches infinity.

Figure 2 is the graph of scaled expected length of the confidence interval centered on the bootstrap smoothed estimator, which is based on the post-model-selection estimator obtained after a preliminary hypothesis test, with size , of the null hypothesis that the simpler model is correct. We consider the case

that the nominal coverage is 0.95,

, and and 0.9.

For and 0.9, the scaled expected length is substantially less than 1 when . In addition, the scaled expected length (a) has maximum value that is not too much larger than 1 and (b) approaches 1 as approaches infinity. This shows that for and

the scaled expected length of interval has the desired properties. This finding is similar to that reported in Kabaila and Giri (2013)

concerning the performance of the CIs constructed by

Kabaila and Giri (2009) to have the desired coverage probability and these desired scaled expected length properties. Namely, the performance of this CI improves as increases and decreases.

By contrast, for the case that is assumed known, examined by Kabaila and Wijethunga (2019),

the

scaled expected length of the CI centered on the bootstrap smoothed estimator (a)

is either greater than 1 or only

slightly less than 1 at and (b) has maximum value that is an increasing function of that can be much larger than 1 for large .

As noted earlier, we expect that as increases (which implies that also increases), the results obtained in the present paper will approach the corresponding results obtained by Kabaila and Wijethunga (2019). Therefore we expect that as increases the interval will get further and further away from possessing the desired scaled expected length properties.

This is confirmed by the graphs of the scaled expected length of

for nominal coverage 0.95, size of the preliminary hypothesis test, and that are

provided

in the Supporting Material for and 10.

Figure 2: The scaled expected length of the interval,

which is based on the post-model-selection estimator obtained after a preliminary hypothesis test, with size , of the null hypothesis that the simpler model is correct. The nominal coverage is 0.95,

, and and 0.9.

6. Discussion

For the test scenario of two nested linear regression models and error variance assumed known, Kabaila and Wijethunga (2019) found that the interval does not perform any better in terms of expected length than the usual confidence interval, with the same minimum coverage probability and based on the full model. Intuitively, the case that the error variance is assumed to be known corresponds to the case that the error variance is unknown (so that it must be estimated) and the number of degrees of freedom for the estimation of the error variance is large.

In the present paper, we deal with the case

that the error variance is unknown. We find that, for small and large magnitude of correlation between the least squares estimators of the parameter of interest and the parameter that is set to zero to specify the simpler model, the expected length of the interval possesses some attractive features.

Acknowledgement

This work was supported by an Australian Government Research Training Program Scholarship.

References

Akaike (1974)

Akaike, H., 1974.

A new look at statistical model identification.

IEEE Transactions on Automatic Control

19, 716–723.

Barndorff-Nielsen and Cox (1989)

Barndorff-Nielsen, O.E., Cox, D.R.,

1989.

Asymptotic Techniques for Use in Statistics.

Chapman & Hall, London.

Barndorff-Nielsen and Cox (1994)

Barndorff-Nielsen, O.E., Cox, D.R.,

1994.

Inference and Asymptotics.

Chapman & Hall, London.

Buckland et al. (1997)

Buckland, S.T., Burnham, K.P.,

Augustin, N.H., 1997.

Model selection: an integral part of inference.

Biometrics 53,

603–618.

Efron (2014)

Efron, B., 2014.

Estimation and accuracy after model selection.

Journal of the American Statistical Association

109, 991–1007.

Fletcher and Turek (2011)

Fletcher, D., Turek, D.,

2011.

Model-averaged profile likelihood intervals.

Journal of Agricultural, Biological, and

Environmental Statistics 17, 38–51.

Kabaila (2009)

Kabaila, P., 2009.

The coverage properties of confidence regions after

model selection.

International Statistical Review

77, 405–414.

Kabaila and Giri (2009)

Kabaila, P., Giri, K.,

2009.

Confidence intervals in regression utilizing prior

information.

Journal of Statistical Planning and Inference

139, 3419–3429.

Kabaila and Giri (2013)

Kabaila, P., Giri, K.,

2013.

Further properties of frequentist confidence

intervals in regression that utilize uncertain prior information.

Australian & New Zealand Journal of Statistics

55, 259–270.

Kabaila et al. (2016)

Kabaila, P., Welsh, A.H.,

Abeysekera, W., 2016.

Model-averaged confidence intervals.

Scandinavian Journal of Statistics

43, 35–48.

Kabaila et al. (2017)

Kabaila, P., Welsh, A.H.,

Mainzer, R., 2017.

The performance of model averaged tail area

confidence intervals.

Communications in Statistics - Theory and Methods

46, 10718–10732.

Kabaila and Wijethunga (2019)

Kabaila, P., Wijethunga, C.,

2019.

Confidence intervals centred on bootstrap smoothed

estimators.

Australian & New Zealand Journal of Statistics

doi:10.1111/anzs.12252.

Leeb and Pötscher (2005)

Leeb, H., Pötscher, B.M.,

2005.

Model selection and inference: facts and fiction.

Econometric Theory 21,

21–59.

Turek and Fletcher (2012)

Turek, D., Fletcher, D.,

2012.

Model-averaged wald confidence intervals.

Computational Statistics & Data Analysis

56, 2809–2815.

Appendix

Let , so that

, where

. Note that and are independent and has the same distribution as where .

To find convenient formulas for expectations and probabilities of interest, we will express all

quantities of interest in terms of and the random vector

, which has

a bivariate normal distribution with mean and known covariance matrix with diagonal elements 1 and off-diagonal elements .

For the sake of brevity, we present only an outline of the proof of Theorem 1.

By (1.6) of Barndorff-Nielsen and Cox (1994), the pdf

of can be expressed in the exponential family form

, where is a sufficient statistic and is the unknown parameter vector, with

For any two random vectors and , define

.

By Theorem 2 of Efron (2014), the ideal delta method approximation

to the standard deviation of , which we denote by

, is given by

(7)

where

and

Now . Thus

Also, . Thus

Hence

(11)

Let and observe that

is equal to

where . It may be shown that

and

It may also be shown, using the definitions of the Hermite polynomials of degrees 1, 2 and 3 (given e.g. by Barndorff-Nielsen and Cox, 1989), that

where the functions , and are defined by (1), (3) and (4), respectively.

Thus

By the substitution theorem for conditional expectations and

since and are independent random variables, this is equal to

Obviously

where the functions and are defined by (5) and (6), respectively.

The distribution of , conditional on , is . Thus

,

where .

Therefore the coverage probability is equal to

The result follows by changing the variable of integration

of the inner integral to .