Dynamic Energy Management

Abstract

We present a unified method, based on convex optimization, for managing the power produced and consumed by a network of devices over time. We start with the simple setting of optimizing power flows in a static network, and then proceed to the case of optimizing dynamic power flows, i.e., power flows that change with time over a horizon. We leverage this to develop a real-time control strategy, model predictive control, which at each time step solves a dynamic power flow optimization problem, using forecasts of future quantities such as demands, capacities, or prices, to choose the current power flow values. Finally, we consider a useful extension of model predictive control that explicitly accounts for uncertainty in the forecasts. We mirror our framework with an object-oriented software implementation, an open-source Python library for planning and controlling power flows at any scale. We demonstrate our method with various examples. Appendices give more detail about the package, and describe some basic but very effective methods for constructing forecasts from historical data.

0.1 Introduction

We present a general method for planning power production, consumption, conversion, and transmission throughout a network of interconnected devices. Our method is based on convex optimization. It provides power flows that meet all the device constraints, as well as conservation of power between devices, and minimizes a total cost associated with the devices. As a by-product, the method determines the locational marginal price for power at each point on the network where power is exchanged.

In the simplest setting we ignore time and consider static networks. In the next simplest setting, we optimize power flows for multiple time periods, over a finite time horizon, which allows us to include ramp rate constraints, energy storage devices, and deferrable loads. We leverage this to develop a real-time control method, model predictive control, which uses forecasts of unknown quantities and optimization over a horizon to create a plan, the first step of which is used or executed in each time period. It is well known that, despite uncertainty in the forecasts, model predictive control often works reasonably well. Finally, we consider an extension of model predictive control that explicitly handles uncertainty in the forecasts by considering several possible scenarios, and creating a full contingency plan for each one, coupled by the requirement that the power flows in the first period of each contingency must be the same.

In addition to providing optimal power flows, our method computes the locational marginal price of power over the network. These prices can be used as the basis of a system of payments, in which each device is paid for the power it produces, or pays for the power it consumes, and each transmission line or conversion device is paid its service. We show that, under this payment scheme, the optimal power flows maximize each individual device’s profit, i.e., the income from payments to it minus the cost of operating the device. This means that the optimal power flows are not only socially optimal, but also provide an economic equilibrium, i.e., there is no incentive for any device to deviate from the optimal power flows (in the absence of price manipulation).

Our exposition is accompanied by cvxpower, a Python software implementation of our method, which is available at http://github.com/cvxgrp/cvxpower. cvxpower is an object-oriented package which provides a declarative language for describing and optimizing power networks. Object-oriented software design is well suited for building complex applications with many inter-operating components, whose users need not understand the internal details of these components. In this sense, we aim to abstract away the technical details of the individual devices in the network, as well as the underlying optimization problem, allowing users to focus on modeling. More advanced users can extend our software framework, for example, by defining and implementing a new device.

Most of the ideas, and much of the material in this paper has appeared in other works or is well known. Our contribution is to assemble it all into one coherent framework, with uniform notation and an organization of ideas that shows how a very basic method of optimizing static power flows generalizes naturally to far more complex settings. We also note that more sophisticated work has appeared on closely related topics, such as using convex optimization relaxations to solve (nonconvex) AC power flow optimization problems, or advanced forms of robust model predictive control. Some of this work is discussed in the section below on related work, as well as in the main body of this paper.

0.1.1 Related work

Mathematical optimization has been used to manage electric power grids for nearly a century. Modern overviews of the field are provided by wood2012power and taylor2015convex , and many examples by baldick2006applied . For an overview of economic and financial issues related to energy markets see harris2011electricity .

Optimal dispatch.

One of the earliest applications of optimization to power systems is the optimal dispatch problem, which considers the problem of planning the operation of multiple generators in order to meet power demand. This method dates back to 1922. (See davison1922dividing .) and a good classical treatment can be found in steinberg1943economy . This early work was based on the incremental rate method, which involves solving the optimality conditions of a convex optimization problem by hand, using graphical methods. (These conditions are (4) in our formulation, for a problem with a single net.) For a typical, modern formulation, see (wood2012power, , Ch. 3). Variations, including minimum generation constraints and the possibility of turning off generators, are typically called the unit commitment problem. (See, e.g., (wood2012power, , Ch. 4) or the survey padhy2004unit .) These additions to the problem formulation, which model the important limitations of many types of power generation, generally result in a nonconvex optimization problem.

Static optimal power flow.

The static optimal power flow problem extends the optimal dispatch problem by considering the spatial distribution of generators and loads in a network. In addition to planning operation of the generators, the system operator must also consider how power flows through this network to the loads. It was first formulated in carpentier1962 ; a modern treatment can be found in (wood2012power, , Ch. 8). Good historical treatments of the development of optimization for power systems can be found in happ1977optimal and cain2012history .

DC optimal power flow.

Most formulations of optimal power flow consider AC power, which typically results in a nonconvex problem. This substantially complicates the formulation, and we do not consider it in this paper. Our formulation is similar to the so-called DC optimal power flow, or the network optimal power flow problem described in taylor2015convex . This simplified problem does not consider the physical method by which power flows through the network, and has the benefit of retaining convexity, which we exploit in our exposition. We also note that convexity raises the possibility of a distributed solution method; this idea is explored in kraning2014dynamic . The possibility of using a blockchain to coordinate transactions in such a distributed method is considered in blockchain2017 , and a similar decentralized market structure is studied in liu2018novel .

AC optimal power flow.

We do note that although the AC optimal power flow problem is not convex, substantial progress has been made in the last 10 years toward approximating the AC problem using convex optimization. These involve relaxing the (nonconvex) quadratic equality constraints associated with AC power flow, and result in second-order cone programs or semidefinite programs; see lavaei2012zero and (taylor2015convex, , Ch. 3) for details.

Symbolic languages for optimization.

Object-oriented programming is ideal for software that encapsulates technical details and offers a simple interface to (even advanced) users. This has been used to develop languages for specifying optimization problems yalmip ; cvx ; cvxpy ; convexjl ; cvxr . On top of these, domain-specific languages have been developed, for example for portfolio management in finance BBDKKNS:17 .

0.1.2 Outline

We start with a simple network power flow model, and increase the complexity of the formulation in each subsequent section, adding additional levels of complexity. In §0.2, we begin with a basic network model, representing the distribution of devices across a network. This allows our formulation to capture spatial phenomena, and in particular, the fact that the price of power can vary at different locations on a network. (For example, power is typically cheaper close to cheap generators, and more expensive close to loads, especially if transmission is difficult or constrained.) In §0.3, we extend this model to account for phenomena occurring over time, such as time-varying loads and availability of renewable power generation, energy storage, generator ramp rate restrictions, and deferrable loads. Here we see that the price of power varies both across the network and in time. In §0.4, we use the dynamic formulation for model predictive control, a method that replaces uncertain future quantities with forecasts. As seen in many other applications of model predictive control, the feedback inherent in such a system gives good performance even when the forecasts are not particularly accurate. Finally, in §0.5, we add an explicit uncertainty model to account for our prediction or forecast errors, leading to an improved model predictive control formulation. We also present, in Appendix 0.6, a simple method for forecasting dynamic quantities, such as power availability of renewable generators.

0.2 Static optimal power flow

In this section we describe our basic abstractions, which we use throughout the paper (sometimes in more sophisticated forms). Our abstractions follow kraning2014dynamic .

In this section we work in a static setting, i.e., we consider power flows that are constant over time, or more realistically, constant over some given time interval such as one minute, 15 minutes, or one hour. Thus any power that we refer to in this section can be converted to energy by multiplying by the given time interval.

0.2.1 Network model

We work with three abstractions: devices, terminals, and nets. We first describe the setup in words, without equations; after that, we introduce our formal notation.

Devices and terminals

Devices produce, consume, and transfer power. Examples include generators, loads, transmission lines, and power converters. Each device has one or more terminals, across which power can flow (in either direction). We adopt the sign convention that positive terminal power means power flows into the device at that terminal; negative power corresponds to power flowing out of the device at that terminal. For example, we would expect a load (with a single terminal) to have positive power, whereas a generator would have negative power at its (single) terminal. As another example, a transmission line (or other energy transport or conversion device) has two terminals; we would typically expect one of its terminal powers to be positive (i.e., the terminal at which the power enters) and the other terminal power (at which the power leaves) to be negative. (The sum of these two terminal powers is the net power entering the device, which can be interpreted as the power lost or dissipated.)

We do not specify the physical transport mechanism by which power flows across terminals; it is simply a power, measured in Watts (or kW, MW, or GW). The physical transport could be a DC connection (at some specific voltage), or a single- or multi-phase AC connection (at some specific voltage). We do not model AC quantities like voltage magnitude, phase angle, or reactive power flow. In addition, power can have a different physical transport mechanism at its different terminals. For example, the two terminals (in our sense, not the electrical sense) of an AC transformer transfer power at different voltages; but we keep track only of the (real) power flow on the primary and secondary terminals.

Each device has a cost function, which associates a (scalar) cost with its terminal powers. This cost function can be used to model operating cost (say, of a generator), or amortized acquisition or maintenance cost. The cost can be infinite for some device terminal powers; we interpret this as indicating that the terminal powers violate a constraint or are impossible or infeasible for the device. The cost function is a quantity that we would like to be small. The negative of the cost function, called the utility function, is a quantity that we would like to be large.

Nets

Nets exchange power between terminals. A net consists of a set of two or more terminals (each of which is attached to a device). If a terminal is in a net, we say it is connected, attached, or adjacent to the net. At each net we have (perfect) power flow conservation; in other words, the sum of the attached terminal powers is zero. This means that the sum of total power flowing from the net to the device terminals exactly balances the total power flowing into the net from device terminals. A net imposes no constraints on the attached terminal powers other than conservation, i.e., they sum to zero. We can think of a net as an ideal bus with no power loss or limits imposed, and without electrical details such as voltage, current, or AC phase angle.

A one-terminal net is not very interesting, since power conservation requires that the single attached terminal power is zero. The smallest interesting net is a two-terminal net. The powers of the two connected terminals sum to zero; i.e., one is the negative of the other. We can think of a two-terminal net as an ideal lossless power transfer point between two terminals; the power flows from one terminal to the other.

Network

A network is formed from a collection of devices and nets by connecting each terminal of each device to one of the nets. The total cost associated with the network is the sum of the costs of its devices, which is a function of the device terminal powers. We say that the set of terminal powers in a network is feasible if the cost is finite, and if power conservation holds at each net. We say that the set of terminal powers in a network is optimal if it is feasible, and it minimizes the total cost among all feasible terminal power flows. This concept of optimal terminal powers is the central one in this paper.

Notation

We now describe our notation for the abstractions introduced above. We will use this notation (with some extensions described later) throughout this paper.

There are devices, indexed as . Device has terminals, and there are terminals in total (i.e., ). We index terminals using . We refer to this ordering of terminals as the global ordering. The set of all terminal powers is represented as a vector , with the power flow on terminal (in the global ordering). We refer to as the global power vector; it describes all the power flows in the network.

The terminal powers of a specific device are denoted . This involves a slight abuse of notation; we use to denote the (scalar) power flow on terminal (under the global ordering); we use to denote the vector of terminal powers for the terminals of device . We refer to the scalar as the power on terminal of device . We refer to the ordering of terminals on a multi-terminal device as the local ordering. For a single-terminal device, is a number (i.e., in R).

Each device power vector consists of a subvector or selection from the entries of the global power vector . We can express this as , where is the matrix that maps the global terminal ordering into the terminal ordering for device . These matrices have the simple form

We refer to as the global-local matrix, since it maps the global power vector into the local device terminal powers. For a single-terminal device, is a row vector, , where is the th standard unit vector, and is the global ordering index of the terminal. The cost function for device is given by . The cost for device is

The nets are labeled . Net contains terminals, and we denote by the vector of powers corresponding to the terminals in , ordered under the global ordering. (Because each terminal appears in exactly one net, we have .) Here too we abuse notation: is the number of terminals of device , whereas is the number of terminals in net . The symbol by itself always refers to the global power vector. It can have two meanings when subscripted: is the (scalar) power flow on (global) terminal ; is the vector of power flows for device . The power flow on (local) terminal on device is .

The terminals in each net can be described by an adjacency matrix , defined as

Each column of is a unit vector corresponding to a terminal; each row of corresponds to a net, and consists of a row vector with entries and indicating which nets are adjacent to it. We will assume that every net has at least one adjacent terminal, so every unit vector appears among the columns of , which implies it is full rank.

The number is the sum of the terminal powers over terminals in net , so the -vector gives the total or net power flow out of each net. Conservation of power at the nets can then be expressed as

| (1) |

which are equalities.

The total cost of the network, denoted , maps the power vector to the (scalar) cost. It is the sum of all device costs in the network:

| (2) |

A power flow vector is called feasible if and . It is called optimal if it is feasible, and has smallest cost among all feasible power flows.

Example

As an example of our framework, consider the three-bus network shown in figure 1. The two generators and two loads are each represented as single-terminal devices, while the three transmission lines, which connect the three buses, are each represented as two-terminal devices, so this network has devices and terminals. The three nets, which are the connection points of these seven devices, are represented in the figure as circles. The device terminals are represented as lines (i.e., edges) connecting a device and a net. Note that our framework puts transmission lines (and other power-transfer devices) on an equal footing with other devices such as generators and loads.

In the figure we have labeled the terminal powers with the global index. For the network, we have

The conservation of power condition can be written explicitly as

(for nets 1, 2, and 3, respectively). The third device is line 1, with global-local matrix

The generators typically produce power, not consume it, so we expect the generator powers and to be negative. Similarly, we expect the load powers and to be positive, since loads typically consume power. If line 3 is lossless, we have ; if power is lost or dissipated in line 3, (which is power lost or dissipated) is positive.

Generators, loads, and transmission lines

Our framework can model a very general network, with devices that have more than two terminals, and devices that can either generate or consume power. But here we describe a common situation, in which the devices fall into three general categories: Loads are single-terminal devices that consume power, i.e., have positive terminal power. Generators are single-terminal devices that generate power, i.e., have negative terminal power. And finally, transmission lines and power conversion devices are two-terminal devices that transport power, possibly with dissipation, i.e., the sum of their two terminal powers is nonnegative.

For such a network, power conservation allows us to make a statement about aggregate powers. Each net has total power zero, so summing over all nets we conclude that the sum of all terminal powers is zero. (This statement holds for any network.) Now we partition the terminals into those associated with generators, those associated with loads, and those associated with transmission lines. Summing the terminal powers over these three groups, we obtain the total generator power, the total load power, and the total power dissipated or lost in the transmission lines. These three powers add to zero. The total generator power is negative, the total load power is positive, and the total power dissipated in transmission lines is nonnegative. Thus we find that the total power generated (expressed as a positive number) exactly balances the total load, plus the total power loss in transmission lines.

0.2.2 Optimal power flow

The static optimal power flow problem consists of finding the terminal powers that minimize the total cost of the network over all feasible terminal powers:

| (3) |

The decision variable is , the vector of all terminal powers. The problem is specified by the cost functions of the devices, the adjacency matrix , and the global-local matrices , for . We refer to this problem as the static OPF problem. We will let denote an optimal power flow vector, and we refer to as the optimal cost for the power flow problem (3). The OPF problem is a convex optimization problem if all the device cost functions are convex cvxbook . Roughly speaking, this means that it can be solved exactly and efficiently, even for large networks.

Optimality conditions

If all the device cost functions are convex and differentiable, a terminal power vector is optimal for (3) if and only if there exists a Lagrange multiplier vector such that

| (4) |

where is the gradient of at bertsekas2016nonlinear . The second equation is the conservation of power constraint of the OPF problem (3). For a given optimal flow vector , there is a unique Lagrange multiplier vector satisfying (4). (This follows since the matrix has full rank.) The Lagrange multiplier vector will come up again in §0.2.3, where it will be interpreted as a vector of prices.

Some of the aforementioned assumptions (convexity and differentiability of the cost function) can be relaxed. If the cost function is convex but not differentiable, the optimality conditions (4) can be extended in a straightforward manner by replacing the gradient with a subgradient. (In this case, the Lagrange multiplier vector may not be unique.) For a detailed discussion, see (rockafellar1997convex, , §28). If the cost function is differentiable but not convex, the conditions (4) are necessary, but not sufficient, for optimality; see (bertsekas2016nonlinear, , Ch. 4). When the cost function is neither convex nor differentiable, optimality conditions similar to (4) can be formulated using generalized (Clarke) derivatives clarke1975generalized .

Solving the optimal power flow problem

When all the device cost functions are convex, the objective function is convex, and the OPF problem is a convex optimization problem. It can be solved exactly (and efficiently) using standard algorithms; see cvxbook ; all such methods also compute the Lagrange multiplier as well as an optimal power flow .

If any of the device cost functions is not convex, the OPF problem is a nonconvex optimization problem. In practical terms, this means that finding (and certifying) a global solution to (3) is difficult in general. Local optimization methods, however, can efficiently find power flows and a Lagrange multiplier vector that satisfy the optimality conditions (4).

0.2.3 Prices and payments

In this section we describe a fundamental concept in power flow optimization, locational marginal prices. These prices lead to a natural scheme for payments among the devices.

Perturbed problem

Suppose a network has optimal power flow , and we imagine extracting additional power from each net. We denote this perturbation by a vector . When , we extract additional power from net ; means we inject additional power into net . Taking these additional power flows into account, the power conservation constraint becomes . The perturbed optimal power flow problem is then

Note that when , this reduces to the optimal power flow problem.

We define , the perturbed optimal cost function, as the optimal cost of the perturbed optimal power flow problem, which is a function of . Roughly speaking, is the minimum total network cost, obtained by optimizing over all network power flows, taking into account the net power perturbation . We can have , which means that with the perturbed power injections and extractions, there is no feasible power flow for the network. The optimal cost of the unperturbed network is .

Prices

The change in the optimal cost from the unperturbed network is . Now suppose that is differentiable at (which it need not be; we discuss this below). We can approximate the cost change, for small perturbations, as

This shows that the approximate change in optimal cost is a sum of terms, each associated with one net and proportional to the perturbation power . We define the locational marginal price (or just price) at net to be

The locational marginal price at net has a simple interpretation. We imagine a network operating at an optimal power vector . Then we imagine that a small amount of additional power is extracted from net . We now re-optimize all the power flows, taking into account this additional power perturbation. The new optimal cost will (typically) rise a bit from the unperturbed value, by an amount very close to the size of our perturbation times the locational marginal price at net .

It is a basic (and easily shown) result in optimization that, when is convex and differentiable, and is differentiable, we have schweppe1988spot ; papavasiliou2017analysis

| (5) |

In other words, the Lagrange multiplier in the OPF optimality condition (4) is precisely the vector of locational marginal prices.

Under usual circumstances, the prices are positive, which means that when we extract additional power from a net, the optimal system cost increases; for example, at least one generator or other power provider must increase its power output to supply the additional power extracted, so its cost (typically) increases. In some pathological situations, locational marginal prices can be negative. This means that by extracting power from the net, we can decrease the total system cost. While this can happen in practice, we consider it to be a sign of poor network design or operation.

If is not differentiable at , it is still possible to define the prices, but the treatment becomes complicated and mathematically intricate, so we do not include it here. When the OPF problem is convex, the system cost function is convex, and the prices would be given by a subgradient of at ; see (rockafellar1997convex, , §28). In this case, the prices need not be unique. When the OPF problem is differentiable but not convex, the vector in the (local) optimality condition (4) can be interpreted as predicting the change in local optimal cost with net perturbations.

Payments

The locational marginal prices provide the basis for a natural payment scheme among the devices. With each terminal (in the global ordering) we associate a payment (by its associated device) equal to its power times the associated net price. We sum these payments over the terminals in each device to obtain the payment that is to be made by device . Define as the vector of prices at the nets containing the terminals of device , i.e.,

(These prices are given in the local terminal ordering for device .) The payment from device is the power flow at its terminals multiplied by the corresponding locational marginal prices, i.e.,

For a single-terminal device, this reduces to paying for the power consumed (i.e., ) at a rate given by the locational marginal price (i.e., ). A generator would typically have , and as mentioned above, we typically have , so the payment is negative, i.e., it is income to the generator.

For a two-terminal device, the payment is the sum of the two payments associated with each of the two terminals. For a transmission line or other power transport or conversion device, we typically have one terminal power positive (where power enters the device) and one terminal power negative (where power is delivered). When the adjacent prices are positive, such a device receives payment for power delivered, and pays for the power where it enters. The payment by the device is typically smaller than the payment to the device, so it typically derives an income, which can be considered its compensation for transporting the power.

The total of all payments at net is times the sum of the powers at the net. But the latter is zero, by power conservation, so the total of all payments by devices connected to a net is zero. Thus the device payments can be thought of as an exchange of money taking place at the nets; just as power is preserved at nets, so are the payments. We can think of nets as handling the transfer of power among devices, as well as the transfer of money (i.e., payments), at the rate given by its locational marginal price. This idea is illustrated in figure 2, where the dark lines show power flow, and the dashed lines show payments, i.e., money flow. Both are conserved at a net. In this example, device 1 is a generator supplying power to devices 2 and 3, which are loads. Each of the loads pays for their power at the locational marginal price; the sum of the two payments is income to the generator.

Since the sum of all payments at each net is zero, it follows that the sum of all payments by all devices in the network is zero. (This is also seen directly: the sum of all device payments is , and we have .) This means that the payment scheme is an exchange of money among the devices, at the nets.

Profit maximization

According to the payment scheme described above, device pays for power at its terminals at rates given by the device price vector . If we interpret the device cost function as a cost (in the same units as the terminal payments), the device’s net revenue or profit is

We can think of the first term as the revenue associated with the power produced or consumed at its terminals; the second term is the cost of operating the device.

When is differentiable, this profit is maximized when

| (6) |

This is the first equation of (4) (when evaluated at ). We conclude that, given the locational marginal prices , the optimal power vector maximizes each device’s individual profit. (This assumes that device acts as a price taker, i.e., it maximizes its profit while disregarding the indirect impact of its terminal power flows on the marginal prices of power at neighboring nets. Violations of this assumption can result in deviations from optimality; see (luenberger1995microeconomic, , Ch. 8) and (taylor2015convex, , §6.3).) The same profit maximization principle can be established when is convex but not differentiable. In this case any optimal device power maximizes the profit . (But in this case, this does not determine the device optimal power uniquely.)

Note that (6) relates the price of power at adjacent nets to the (optimal) power consumed by the device. For a single-terminal device with differentiable and optimal power , we see that the adjacent net price must be . This is the demand function for the device. When is invertible, we obtain

| (7) |

which can be interpreted as a prescription for how much power to consume or produce as a function of the adjacent price.

For a multi-terminal device with differentiable , and optimal power , the vector of prices at the adjacent nets is , which is the (multi-terminal) demand function for the device. When the device gradient function is invertible, its inverse maps the (negative) adjacent net prices into the power generated or supplied by the device.

| (8) |

(In the case of nondifferentiable, convex cost functions, the subgradient mapping is used here, and the demand function is set valued.)

The demand functions or their inverses (7) and (8) can be used to derive a suitable cost function for a device. For example if a single-terminal device connected to net uses (decreasing, invertible) demand function , we have , and we can take as cost function

which is convex.

The discussion above for single-terminal devices uses the language appropriate when the device represents a load, i.e., has positive terminal power, and is typically decreasing. While the equations still hold, the language would change when the device represents a generator, i.e., has negative terminal power and is typically decreasing.

0.2.4 Device examples

Here we list several practical device examples. All cost functions discussed here are convex, unless otherwise noted. We also discuss device constraints; the meaning is that power flows that do not satisfy the device constraints result in infinite cost for that device.

Generators

A generator is a single-terminal device that produces power, i.e., its terminal power satisfies . We interpret as the (nonnegative) power generated. The device cost is the cost of generating power , and is the marginal cost of power when operating at power .

A generic generator cost function has the form

| (9) |

where and are the minimum and maximum possible values of generator power, and is the cost of generating power , which is convex and typically increasing. Convexity means that the marginal cost of generating power is nondecreasing as the power generated increases. When the generation cost is increasing, it means that the generator ‘prefers’ to generate less power.

The profit maximization principle connects the net price to the generator power . When lies between and , we have

i.e., the net price is the (nonnegative) marginal cost for the generator. When , we must have . When , we must have . Since is convex, is nondecreasing, so and are the minimum and maximum marginal costs for the generator, respectively. Roughly speaking, the generator operates at its minimum power when the price is below the minimum marginal cost, and it operates at its maximum power when the price is above its maximum marginal cost; when the price is in between, the generator operates at a point where its marginal cost matches the net price.

Conventional quadratic generator.

A simple model of generator uses the generation cost function

| (10) |

where , , and are parameters. For convexity, we require . (We also typically have .) The value of the constant cost term has no effect on the optimal power of the generator.

Fixed-power generator.

A fixed-power generator produces units of power; this is an instance of the generic generator with . (The function is only defined for , and its value has no effect on the optimal power, so we can take it to be zero.) A fixed-power generator places no constraint on the adjacent net price.

Renewable generator.

A renewable generator can provide any amount of power between and , and does so at no cost, where is the power available for generation. It too is an instance of the generic generator, with , , and .

The profit maximization principle tells us that if the adjacent net price is positive, we have ; if the adjacent net price is negative, we have . In other words, a renewable generator operates (under optimality) at its full available power if the net price is positive, and shuts down if it is negative. If the generator operates at a power in between and , the adjacent price is zero.

Loads

A load is a single-terminal device that consumes power, i.e., . We interpret as the operating cost for consuming power . We can interpret as the utility to the load of consuming power . This cost is typically decreasing, i.e., loads ‘prefer’ to consume more power. The marginal utility is . Convexity of , which is the same as concavity of the utility, means that the marginal utility of a load is nonincreasing with increasing power consumed.

A generic load cost function has the form

| (11) |

where and are the minimum and maximum possible values of load power, and is the cost of consuming power , which is convex and typically decreasing.

The profit maximization principle connects the net price to the load power . When lies between and , we have

i.e., the net price is the (typically nonnegative) marginal utility for the load. When , we must have . When , we must have . Since is convex, is nondecreasing, so and are the minimum and maximum marginal utilities for the load, respectively. Roughly speaking, the load operates at its minimum power when the price is above the maximum marginal utility, and it operates at its maximum power when the price is below its minimum marginal cost.

Fixed load.

A fixed load consumes a fixed amount of power; i.e., the device power flow satisfies . It is an instance of the generic load with . The value of does not affect the power, so we can take it to be zero.

Power dissipation device.

A power dissipation device has no operating cost, and can consume (dissipate) any nonnegative power. This is an instance of our generic load, with , , and for , .

Curtailable load.

A curtailable load has a desired or target power consumption level , and a minimum allowable power consumption . If it consumes less power than its desired value, a penalty is incurred on the shortfall, with a price . The cost is

A curtailable load is also an instance of our generic load.

If the adjacent net price is less than , we have , i.e., there is no shortfall. If the adjacent net price it is greater than , the load consumes its minimum possible power . If the adjacent net price is , the curtailable device can consume any power between and .

Grid ties

A grid tie is a single-terminal device representing a connection to an external power grid. When , we interpret it as power being injected into the grid. When , we interpret as the power extracted from the grid.

It is possible to buy power from the grid at price , and sell power to the grid at price . We assume arbitrage-free nonnegative prices, i.e., . From the point of view of our system optimizer, the cost of the grid tie is the cost of power bought from (or sold to) the grid, i.e.,

(Recall that is power that we take from the grid connection, so we are buying power when , and selling power when , i.e., .)

Any net adjacent to a grid tie with (i.e., power flows from the grid) has price ; when (i.e., power flows into the grid) it has price . When , the adjacent net price is not determined, but must be between the buy and sell prices.

As a variation on the basic grid tie device, we can add lower and upper limits on , representing the maximum possible power we can sell or buy,

where and are the maximum power we can sell and buy, respectively.

Transmission lines and converters

Here we consider transmission lines, power converters, transformers, and other two-terminal devices that transfer power between their terminals, As usual, constraints on the power flows are encoded into the cost function. We denote the power flow on distinct terminals of a device with numbered subscripts, for example as and . (That is, the subscripts 1 and 2 are in the local device terminal ordering.) We interpret as the net power consumed or dissipated by the device, which is typically nonnegative. If and is negative, then power enters the device at terminal 1 and exits the device at terminal 2, and vice versa when and .

Transmission lines.

An ideal, lossless transmission line (or power converter) has a cost of zero, provided that the power conservation constraint

is satisfied, where and are the power flows into the two terminals of the device. (Note that such an ideal power converter is the same as a two-terminal net.)

Additionally, we can enforce power limits

(This is the same as requiring .) The resulting cost function (with or without power limits) is convex. When , the transmission line or converter is symmetric, i.e., its cost function is the same if we swap and . When this is not the case, the device is directional or oriented; roughly speaking, its terminals cannot be swapped.

For a lossless transmission line for which the limits are not active, i.e., , the prices at the two adjacent nets must be the same. When the prices at the two adjacent nets are not the same, the transmission line operates at its limit, with power flowing into the device at the lower priced net, and flowing out to the higher priced net. In this case the device is paid for transporting power. For example with , we have and , and the device earns revenue .

Lossless transmission line with quadratic cost.

We can add a cost to a lossless transmission line, , with . This (convex) cost discourages large power flows across the device, when the optimal power flow problem is solved. This objective term alone does not model quadratic losses in the transmission line, which would result in ; while it discourages power flow in the transmission line, it does not take into account the power lost in transmission. For such a transmission line, the profit maximization principle implies that power flows from the terminal with higher price to the terminal of lower price, with a flow proportional to the difference in price between the two terminals.

Transmission line with quadratic loss.

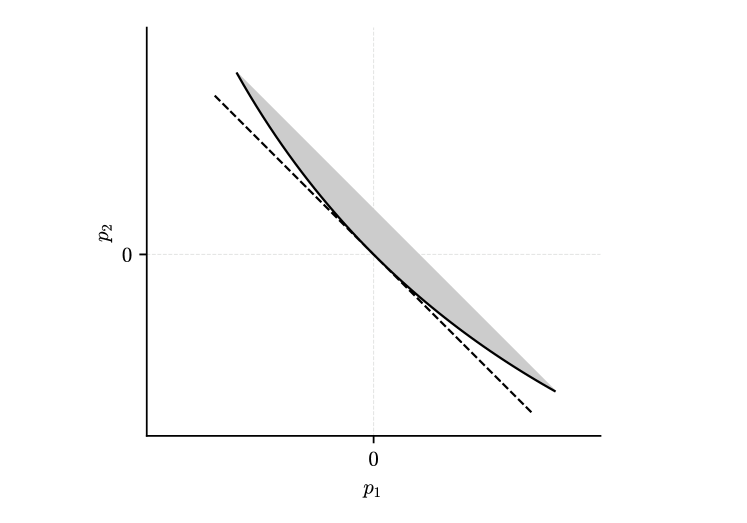

We consider a bi-directional transmission line with power loss with parameter , and limit . (This loss model can be interpreted as an approximation for resistive loss.) This model has constraints

| (12) |

The set of powers and that satisfy the above conditions is the dark line shown in figure 3. Note that this set (and thus the device cost function) is not convex. The ends of the curve are at the points

and

One way to retain convexity is to approximate this set with its convex hull, described by the constraints

With this approximation, the set of feasible powers is the shaded region in figure 3. Power flows that are in this region, but not on the dark line, correspond to artificially wasting power. This approximation is provably exact (i.e., the power flows lie on the dark line) if the optimal price at a neighboring net is positive. In practice, we expect this condition to hold in most cases.

Constant-efficiency converter.

We consider terminal 1 as the input and terminal 2 as the output of a converter (in forward mode). The forward conversion efficiency is given by , and the reverse conversion efficiency is given by . The device is characterized by

Here is the maximum input power to the converter; is the maximum power that can be extracted from the converter. For (forward conversion mode), the conversion loss is , justifying the interpretation of as the forward efficiency. For (reverse conversion mode, which implies ), the loss is .

This set of constraints (and therefore the cost function) is not convex, but we can form a convex relaxation (similar to the case of a lossy transmission line) which in this case is described by a triangular region. The approximation is exact if prices are positive at an adjacent net.

Composite devices

The interconnection of several devices at a single net can itself be modeled as a single composite device. We illustrate this with a composite device consisting of two single-terminal devices connected to a net with three terminals, one of which is external and forms the single terminal of the composite device. (See figure 4.) For this example we have composite device cost function

| (13) |

(The function is the infimal convolution of the functions and ; see (rockafellar1997convex, , §5).) This composite device can be connected to any network, and the optimal power flows will match the optimal power flows when the device is replaced by the subnetwork consisting of the two devices and extra net. The composite cost function (13) is easily interpreted: Given an external power flow into the composite device, it splits into the powers and (as the net requires) in such a way as to minimize the sum of the costs of the two internal devices. The composite device cost function (13) is convex if the two component device cost functions are convex.

Composite devices can be also formed from other, more complicated networks of devices, and can expose multiple external terminals. The composite device cost function in such cases is a simple generalization of the infimal convolution (13) for the simple case of two internal devices and one external terminal. Such composite devices preserve convexity: Any composite device formed from devices with convex cost functions also has a convex cost function.

Composite devices can simplify modeling. For example, a wind farm, solar array, local storage, and a transmission line that connects them to a larger grid can be modeled as one device. We also note that there is no need to analytically compute the composite device function for use in a modeling system. Instead we simply introduce the sum of the internal cost functions, along with additional variables representing the internal power flows, and the constraints associated with internal nets. (This is the same technique used in the convex optimization modeling systems CVX gb08 ; cvx and CVXPY cvxpy to represent compositions of convex functions.)

0.2.5 Network examples

Two-device example

We consider the case of a generator and a load connected to a single net, as shown in figure 5.

For this network topology, the static OPF problem (3) is

| (14) |

Assuming the cost function is differentiable at , the optimality condition is

We interpret as the price, and and as the marginal costs of the generator and load, respectively.

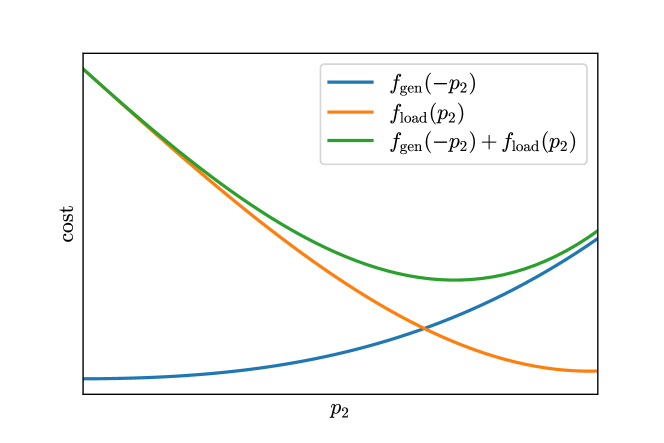

We can express this problem in a more natural form by eliminating using . The power would typically be positive, and corresponds to the power consumed by the load, which is the same as the power produced by the generator, . The OPF problem is then to choose to minimize . This is illustrated in figure 6, which shows these two functions and their sum.

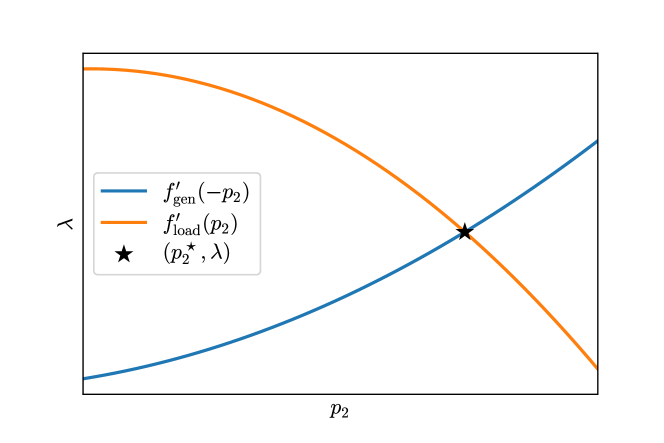

The optimality condition is . We can interpret this as the crossing of the generator supply curve and the load demand curves. This is shown graphically in figure 7, with the optimal point given by the intersection of the supply and demand functions at the point .

Three-bus example

We return to the three-bus example shown in figure 1. The units of power are MW, with an implicit time period of one hour, and the units of payment are US dollars.

The two generators have quadratic cost functions. The first has parameters , , , and MW. The second has parameters , , , and . Both of the loads are fixed loads; the first consumes , and the second . The three transmission lines are lossless, and have transmission limits , , and , respectively.

Results.

The solution of the OPF problem is shown in figure 8, and the payments to each device are given in table 1. The yellow numbers, displayed next to the terminals, show the optimal power flows . The green numbers, next to the nets, show the optimal prices . First note that the power flows into each net sum to zero, indicating that this power flow satisfies the conservation of power, i.e., condition (1). Furthermore, all device constraints are satisfied: the transmission lines transmit power according to their capacities, each load receives its desired power, and the generators supply positive power.

We see that power is cheapest near the second generator, which is not near any load, and expensive near the second load, which is not near any generator. Also note that although generator 2 produces power more cheaply than generator 1, the capacity limits of the transmission lines limit production. This has the effect that this generator is not paid much. (See table 1.) Generator 1, on the other hand, is paid much more, which is justified by its advantageous proximity to load 1. In addition to the generators, the transmission lines earn payments by transporting power. For example, the third transmission line is paid a substantial amount for transporting power from net 3, where power is generated cheaply, to net 2, where there is a load, but no generation. (The payment can be calculated as the difference in price across its adjacent nets multiplied by the power flow across it.) So, we see that the two generators are paid for producing power, the two loads pay for the power they consume, and the three transmission lines are paid for transporting power. The payments balance out; they sum to zero. The cvxpower code for this example is given in appendix 0.7.

| Device | Payment ($) |

|---|---|

| generator 1 | |

| generator 2 | |

| load 1 | |

| load 2 | |

| line 1 | |

| line 2 | |

| line 3 |

0.3 Dynamic optimal power flow

0.3.1 Dynamic network model

In this section we generalize the static power flow model of §0.2 to dynamic optimization over time periods. Each terminal has not just one power flow (as in the static case), but instead a power schedule, which is a collection of power flows, each corresponding to one of the time periods. Each device has a single cost function, which associates a scalar cost with the power schedules of its terminals.

The nets losslessly exchange power at each time period. Power conservation holds if the powers flowing into the net from the terminal devices sum to zero for each of the time periods. If this condition holds, and if the cost associated with the terminal powers is finite, then we say the powers are feasible.

Notation

Much of the notation from the static case is retained. However, in the dynamic case, the power flows are now described by a matrix . The th row of this matrix describes the power schedule of terminal . The th column describes the powers of all terminals corresponding to time period , i.e., it is a snapshot of the power flow of the system at time period . The matrix contains the power schedules of device ’s terminals. The cost function of device is . The system cost is again the sum of the device costs, i.e., . Conservation of power is written as the matrix equation (i.e., scalar equations). Note that in the case of a single time period () the dynamic case (and all associated notation) reduces to the static case.

0.3.2 Optimal power flow

The dynamic optimal power flow problem is

| (15) |

with decision variable , which is the vector of power flows across all terminals at all time periods. The problem is specified by the cost functions of the devices, the adjacency matrix , and the global-local matrices , for . Note that if , (15) reduces to the static OPF problem (3).

Optimality conditions

If the cost function is convex and differentiable, the prices are again the Lagrange multipliers of the conservation of power constraint. That is, the power flow matrix and the price matrix are optimal for (15) if and only if they satisfy

Note that is a matrix of partial derivatives of with respect to the elements of , which means that the first equation consists of scalar equations. As in §0.2.2, these optimality conditions can be modified to handle the case of a convex, nondifferentiable cost function (via subdifferentials), or a nonconvex, differentiable cost function (in which case they are necessary conditions for local optimality).

Solving the dynamic optimal power flow problem

If all the device cost functions are convex, then (15) is a convex optimization problem, and can be solved exactly using standard algorithms, even for large networks over many time periods (cvxbook, , §1.3). Without convexity of the device cost functions, finding (and certifying) a global solution to the problem is computationally intractable in general. However, even in this case, effective heuristics (based on methods for convex optimization) can often obtain practically useful (if suboptimal) power flows, even for large problem instances.

0.3.3 Prices and payments

Here we explore the concept of dynamic locational marginal prices.

Perturbed problem.

As in §0.2.3, here we consider the perturbed system obtained by extracting a (small) additional amount of power into each net. Now, however, the perturbation is a matrix , i.e., the perturbation varies over the terminals and time periods. The perturbed dynamic power flow problem is

The optimal value of this problem, as a function of , is denoted .

Prices.

Assuming the function is differentiable at the point , the price matrix is defined as

This means that if a single unit of power is extracted into net at a time period , then the optimal value of problem (15) is expected to increase by approximately . Any element of is, then, the marginal cost of power at a given network location over a given time period. The th row of this matrix is a vector of length , describing a price schedule at that net, over the time periods. The th column of this matrix is a vector of length , describing the prices in the system at all nets at time period . The price matrix is also a Lagrange multiplier matrix: together with the optimal power matrix , it satisfies the optimality conditions (0.3.2).

The price is the price of power at net in time period . If time period lasts for units of time, then is the price of energy during that time period.

Payments.

Here we extend the static payment scheme of §0.2.3. Device receives a total payment of

over the time periods, where is the matrix of price schedules at nets adjacent to device , i.e., . Note that we sum over the payments for each time period. The sequence for , is a payment schedule or cash flow. In the dynamic case, the payments clear at each time period and at each net, i.e., all payments made at a single net sum to zero in each time period. (This is a consequence of the fact that power is conserved at each time period, at each net.)

0.3.4 Profit maximization

Under the payment scheme discussed above, the profit of device is

If is differentiable, this is maximized over if

Over all devices, this is precisely the first optimality condition of (0.3.2). In other words, the optimal power flow vector also maximizes the individual device profits over the terminal power schedules of that device, provided the adjacent net prices are fixed. So, one can achieve network optimality by maximizing the profit of each device, with some caveats. (See, e.g., the recent work ma2018real .)

0.3.5 Dynamic device examples

Here we list several examples of dynamic devices and their cost functions. Whenever we list device constraints in the device definition, we mean that the cost function is infinite if the constraints are violated. (If we describe a device with only constraints, we mean that its cost is zero if the constraints are satisfied, and infinity otherwise.)

Static devices

All static devices, such as the examples from §0.2.4, can be generalized to dynamic devices. Let be the (static) cost of the device at time . Its dynamic cost is then the sum of all single-period costs

In this case, we say that the device cost is separable across time. If all device costs have this property, the dynamic OPF problem itself separates into static OPF problems; there are no constraints or objective terms that couple the power flows in different time periods. Static but time-varying devices can be used to model, for example, time-varying availability of renewable power sources, or time-varying fixed loads.

Smoothing.

Perhaps the simplest generic example of a dynamic device objective that is not separable involves a cost term or constraint on the change in a power flow from one time period to the next. We refer to these generically as smoothness penalties, which are typically added to other, separable, device cost functions. A smoothness penalty has the form

where is a convex function. (The initial value is a specified constant.) Possible choices for are quadratic (), absolute value or (), or an interval constraint function,

which enforces a maximum change in terminal power from one period to the next. (These are called ramp rate limits for a generator.) For more details on smoothing, see (cvxbook, , §6.3.2).

Dynamic generators

Conventional generator.

An example of extending a static model to a dynamic model is a conventional generator. (See §0.2.4.) The cost function is extended to

| (16) |

where the scalar parameters , , , and are the same as in §0.2.4. (These model parameters could also vary over the time periods.) We can also add a smoothing penalty or ramp rate limits, as discussed above.

Fixed generator.

Some generators cannot be controlled, i.e., they produce a fixed power schedule . The device constraint is , .

Renewable generator.

Renewable generators can be controlled, with their maximum power output depending on the availability of sun, wind, or other power source. That is, at each time period , a renewable generator can produce up to units of power. The device constraint is that .

Dynamic loads

Fixed load.

A traditional load that consumes a fixed power in each period can be described by the simple constraints

where is a fixed power schedule of length .

Deferrable load.

A deferrable load requires a certain amount of energy over a given time window, but is flexible about when that energy is delivered. As an example, an electric vehicle must be charged before the next scheduled use of the vehicle, but the charging schedule is flexible. If the required energy over the time interval is , then the deferrable load satisfies

where time periods and delimit the start and end periods of the time window in which the device can use power, and is the time elapsed between time periods. We also require

for time periods , where is the maximum power the device can accept. In addition, we have for time periods and .

Thermal load.

Here we model a temperature control system, such as the HVAC (heating, ventilation, and air conditioning) system of a building, the cooling system of a server farm, or an industrial refrigerator. The system has temperature at time period , and heat capacity . The system exchanges heat with its environment, which has constant temperature , and infinite heat capacity. The thermal conductivity between the system and the environment is .

We first consider the case of a cooling system, such as a refrigerator or air conditioner, with (cooling) coefficient of performance . The power used by the system at time is . The temperature changes with time according to

The second term is the heat flow to or from the environment, and the third term is heat flow from our cooling unit.

The temperature must be kept in some fixed range

The power consumption must satisfy the limits

The above model can be used to describe a heating system when . In particular, for an electric heater, is the efficiency, and is between and . For a heat pump, is the (heating) coefficient of performance, and typically exceeds . Other possible extensions include time-varying ambient temperature, and higher-order models of the thermal dynamics.

Storage devices

We consider single-terminal storage devices, including batteries, supercapacitors, flywheels, pneumatic storage, or pumped hydroelectric storage. We do not consider the specific details of these technologies, but instead develop a simple model that approximates their main features.

Ideal energy storage device.

We first model an ideal energy storage device, and then specialize to more complicated models. Let be the internal energy of the device at the end of time period . (This is an internal device variable, whose value is fully specified by the power schedule ). The internal energy satisfies

where is the (per-period) leakage rate, with , and is elapsed time between time periods. The energy at the beginning of the first time period is , where is given. We have minimum and maximum energy constraints

where and are the minimum and maximum energy limits. In addition, we have limits on the charge and discharge rate:

We can impose constraints on the energy in a storage device, for example, , i.e., that it be full at the last period.

The profit maximization principle allows us to relate prices in different time periods for an ideal lossless storage device (i.e., with ) that does not hit its upper or lower energy limit. The prices in different periods at the adjacent net must be the same. (If not, the storage device could increase its profit by charging a bit in a period when the price is low, and discharging the same energy when the price is high. This is analogous to a lossless transmission line that is not operating at its limits, which enforces equal prices at its two nets. The transmission line levels prices at two nets; the storage device levels the prices in two time periods.

Charge/discharge cost.

Many storage devices, such as batteries, degrade with use. A charge/discharge usage penalty can be added to avoid overusing the device (or to model amortization, or maintenance, cost). We propose, in addition to the constraints above, the cost

| (17) |

where is a positive constant, and we are implicitly treating the vector as a function of the vector . For a battery whose capital cost is , and with an estimated lifetime of (charge and discharge) cycles, a reasonable choice for is

Conversion losses.

In many cases, energy is lost when charging or discharging. This can be modeled by adding a lossy transmission line. (See §0.2.4.) between the ideal storage device and its net, as shown in figure 9.

0.3.6 Home energy example

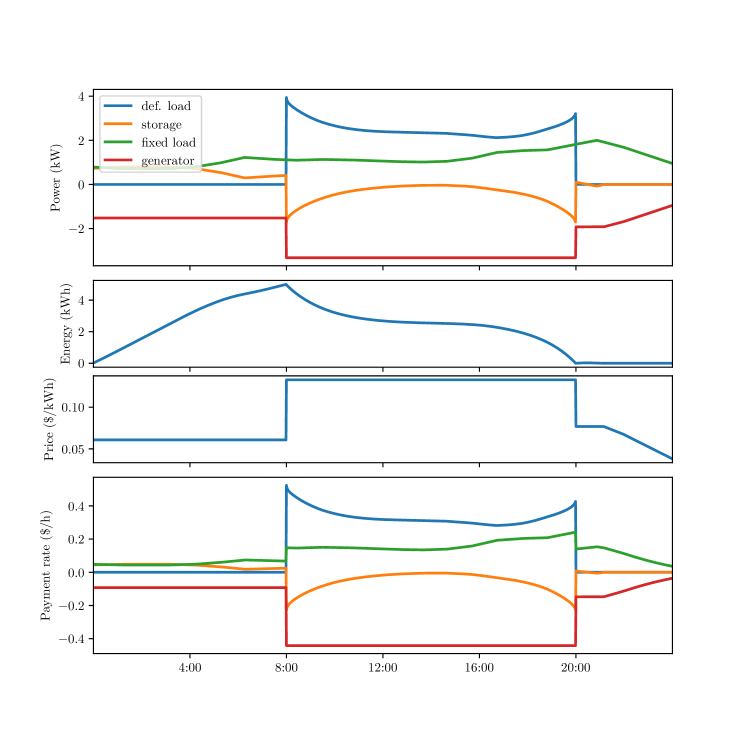

We consider a home network with four devices: a conventional generator, a fixed load, a deferrable load, and an energy storage device. They are all connected to a single net, as shown in figure 10. We operate them over a whole day, split into time periods of 1 minute each.

The generator cost function is given by (10), with , , , and . The (ideal) energy storage device has discharge and charge rates of , , and minimum and maximum capacities and , and is initially uncharged. The deferrable load has a maximum power , and must receive of energy between 8:00 and 20:00. The uncontrollable load has a time-varying power demand profile, which is shown, along with the problem solution, in figure 11.

Results.

The optimal power and price schedules are shown in figure 11, along with the internal energy of the storage device. We see that the storage device and the deferrable load smooth out the power demand over the time horizon, and thus the total generation cost is reduced (compared with the same system without a storage device, or with another fixed load instead of the deferrable one). The storage device charges (i.e., takes in energy) during the initial time periods, when power is cheap (because there is less demand), and discharges (i.e., returns the energy) later, when it is more expensive.

When the deferrable load becomes active in time period 450 (i.e., 8:00), there is even more flexibility in scheduling power, and the price stays constant. This is to be expected; due to the quadratic cost of the generator, the most efficient generation occurs when the generator power schedule is constant, and this can only happen if the price is constant.

The four payments by the devices are shown in table 2. We see that the generator is paid for producing power, the fixed load pays for the power it consumes, as does the deferrable load (which pays less than if it were a fixed load). The storage device is paid for its service, which is to transport power across time from one period to another (just as a transmission line transports power in one time period from one net to another).

| Device | Payment ($) |

|---|---|

| generator | |

| deferable load | |

| fixed load | |

| storage |

0.4 Model predictive control

The dynamic optimal power flow problem is useful for planning a schedule of power flows when all relevant quantities are known in advance, or can be predicted with high accuracy. In many practical cases this assumption does not hold. For example, while we can predict or forecast future loads, the forecasts will not be perfect. Renewable power availability is even harder to forecast.

0.4.1 Model predictive control

In this section we describe a standard method, model predictive control (MPC), also known as receding horizon control (RHC), that can be used to develop a real-time strategy or policy that chooses a good power flow in each time period, and tolerates forecast errors. MPC leverages our ability to solve a dynamic power flow problem over a horizon. MPC has been used successfully in a very wide range of applications, including for the management of energy devices long2019generalised .

MPC is a feedback control technique that naturally incorporates optimization (bemporad2006model ; mattingley2011receding ). The simplest version is certainty-equivalent MPC with finite horizon length , which is described below. In each time period , we consider a horizon that extends some fixed number of periods into the future, . The number is referred to as the horizon or planning horizon of the MPC policy. The device cost functions depend on various future quantities; while we know these quantities in the current period , we do not know them for future periods . We replace these unknown quantities with predictions or forecasts, and solve the associated dynamic power flow problem to produce a (tentative) power flow plan, that extends from the current time period to the end of our horizon, . In certainty-equivalent MPC, the power flow plan is based on the forecasts of future quantities. We then execute the first power flow in the plan, i.e., the power flows corresponding to time period in our plan. At the next time step, we repeat this process, incorporating any new information into our forecasts.

To use MPC, we repeat the following three steps at each time step :

-

1.

Forecast. Make forecasts of unknown quantities to form an estimate of the device cost functions for time periods , , …, .

-

2.

Optimize. Solve the dynamic optimal power flow problem (15) to obtain a power flow plan for time periods .

-

3.

Execute. Implement the first power flow in this plan, corresponding to time period .

We then repeat this procedure, incorporating new information, at time . Note that these steps can be followed indefinitely; the MPC method is always looking ahead, or planning, over a horizon that extends steps into the future. This allows MPC to be used to control power networks that run continuously. We now describe these three steps in more detail.

Forecast.

At time period , we predict any unknown quantities relevant to system operation, such as uncertain demand or the availability of renewable generators, allowing us to form an approximate model of the system over the next time periods. These predictions can be crude, for example as simple as a constant value such as the historical mean or median value of the quantity. The forecasts can also be sophisticated predictions based on previous values, historical data, and even other, related quantities such as weather, economic predictions, or futures prices (which are themselves market-based forecasts). Appendix §0.6 describes a method for creating basic forecasts, that are often adequate for MPC for dynamic energy management.

From predictions of these unknown quantities, predictions of the device cost functions are formed for time periods . At time , we denote the predicted cost function for device as . The cost function for the entire system is the sum of these cost functions, which we denote . (The hat above is a traditonal marker, signifying that the quantity is an estimate.)

Optimize.

We would like to plan out the power flows for the system for time periods to . We denote by the matrix of power flows for all of the devices, and for all of the time periods, from to . We denote by the planned power flows for time period .

To determine the planned power flows , we solve the dynamic optimal power flow problem (15). Using the notation of this section, this problem is

| (18) |

The variable is the planned power flow matrix . The first column contains the power flows for the current period; the second through last columns contain the planned power flows, based on information available at period .

The optimization problem (18) is sometimes augmented with terminal constraints or terminal costs, especially for storage devices. A terminal constraint for a storage device specifies its energy level at the end of the horizon; typical constraints are that it should be half full, or equal to the current value. (The latter constraint means that over the horizon, the net total power of the storage device is zero.) Without a terminal constraint, the solution of (18) will have zero energy stored at the end of the horizon (except in pathological cases), since any stored energy could have been used to reduce some generator power, and thereby reduce the cost. A terminal cost is similar to a terminal constraint, except that it assesses a charge based on the terminal energy value.

Execute.

Here, the first step of the planned power flow schedule is executed, i.e., we implement . (This could be as part of a larger simulation, or this could be directly on the physical system.) Note that the planned power flows are not directly implemented. They are included for planning purposes only; their purpose is only to improve the choice of power flows in the first step.

0.4.2 Prices and payments

Because the dynamic OPF problem (15) is the same as problem (18), the optimality conditions of §0.3.2 and the perturbation analysis of §0.3.3 also apply to (18), which allows us to extend the concept of prices to MPC. In particular, we denote the prices corresponding to a solution of (18) as . This matrix can be interpreted as the predicted prices for time periods , with the prediction made at time . (The first column contains the true prices at time .)

Payments.

We can extend the payment scheme developed in §0.3.3 to MPC. To do this, note that the payment scheme in §0.3.3 involves each device making a sequence of payments over the time periods. In the case of MPC, only the first payment in this payment schedule should be carried out; the others are interpreted as planned payments. Just as the planned power flows for are never implemented, but instead provide a prediction of future power flows, the planned payments are never made, but only provide a prediction of future payments.

Profit maximization.

In §0.3.4, we saw that given the predicted cost functions and prices, the optimal power flows maximize the profits of each device independently. (We recall that we obtain the prediction of prices over the planning horizon as part of the solution of the OPF problem.) Because the dynamic OPF problem is solved in each step of MPC, this interpretation extends to our case. More specifically, given all information available at time , and a prediction of the prices , the planned power flows maximize the profits of each device independently. In other words, if the managers (or owners) of each device agree on the predictions, they should also agree that the planned power flows are fair.

We can take this interpretation a step further. Suppose that at time , device predicts its own cost function as , and thus predicts the future prices to be (via the solution of the global OPF problem). If the MPC of §0.4.1 is carried out, each device can be interpreted as carrying out MPC to plan out its own terminal power flows to maximize its profit, using the predicted prices during time period .

0.4.3 Wind farm example

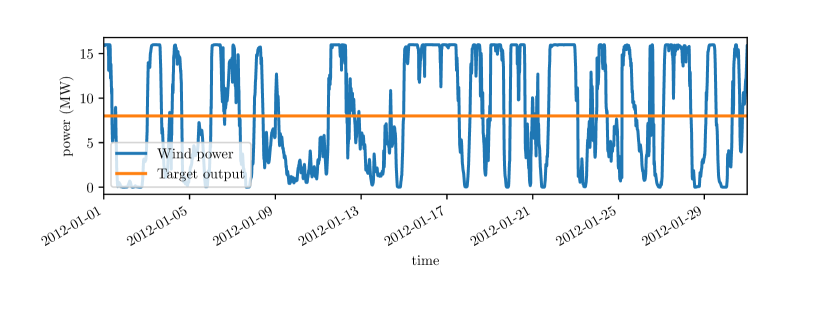

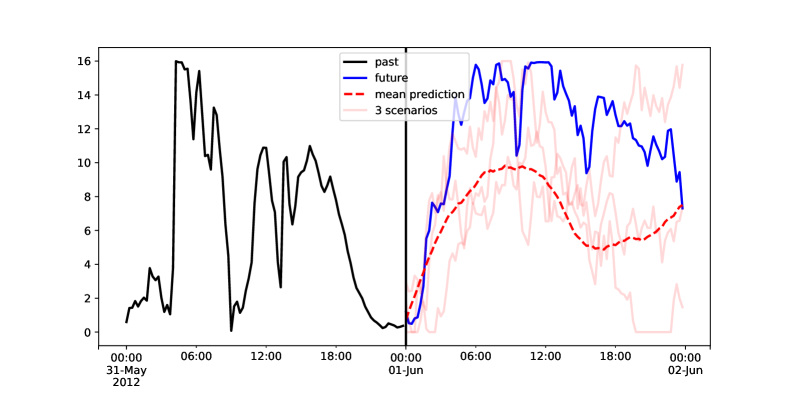

We consider a network consisting of a wind generator, a gas generator, and a storage device, and a fixed load, all connected to one net. The goal is to deliver a steady output of around to the fixed load, which is the average of the available wind power over the month. We consider the operation of this system for one month, with each time period representing minutes.

The gas generator has the cost function given in §0.3.5, with parameters and . The storage device has maximum charge and discharge rate of , and a maximum capacity of . The wind generator is modeled as a renewable device, as defined in §0.3.5, i.e., in each time period, the power generated can be any nonnegative amount up to the available wind power . We show as a function of the time period in figure 12, along with the desired output power. The wind power availability data is provided by NREL (National Renewable Energy Laboratory), for a site in West Texas. We solve the problem with two different methods, detailed below, and compare the results. (Later, in §0.5.6, we will introduce a third method.)

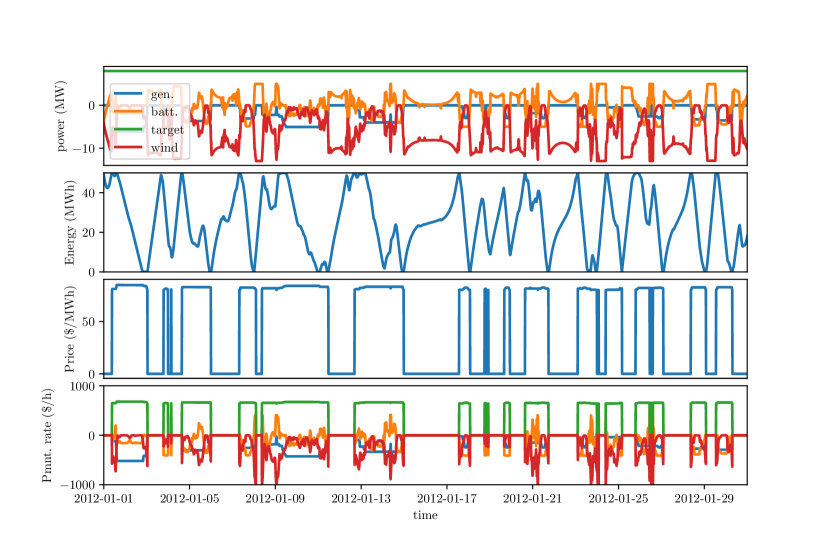

Whole-month dynamic OPF solution.

We first solve the problem as a dynamic OPF problem. This requires solving a single problem that takes into account the entire month, and also requires full knowledge of the available wind power. This means our optimization scheme is prescient, i.e., knows the future. In practice this is not possible, but the performance in this prescient case is a good benchmark to compare against, since no control scheme could ever attain a lower cost.

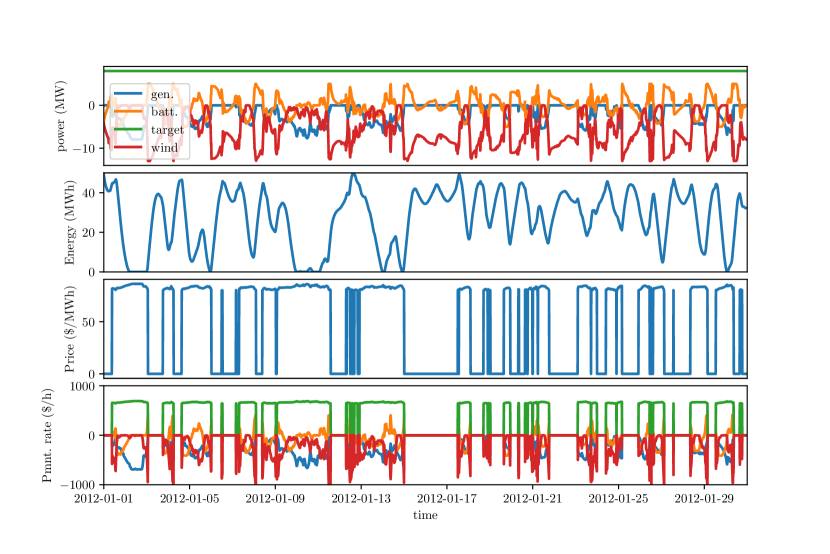

MPC.

We then consider the practical case in which the system planner does not know the available wind power in advance. To forecast the available wind power, we use the auto-regressive model developed in §0.6.6, trained on data from the preceding year. By comparing the performance of MPC with the dynamic OPF simulation given above, we get an idea of the value of (perfect) information, which corresponds to the amount of additional cost incurred due to our imperfect prediction of available wind power.

Results.

The power flows obtained by solving the problem using dynamic OPF and MPC are shown in figure 13. The values of the cost function obtained using dynamic OPF and MPC were and , respectively. This difference reflects the cost of uncertainty, i.e., the difference gives us an idea of the value of having perfect predictions. In this example the difference is not negligible, and suggests that investing in better wind power forecasting could yield greater efficiency.

In figure 13, we also show the prices (in time), as well as the payments made by each device. Note that the price is “set” by the power production of the gas generator. (This is because the price is given be the derivative of the cost functions of adjacent devices.) This means that when the gas generator produces power, the price is positive; otherwise, it is zero. Also note that when the price is zero, no payments are made.

In table 3, we show the total payment of each device, using dynamic OPF and MPC. We see that under the dynamic OPF method, the storage device is paid more than under MPC. This is because storage is more useful precisely when forecasting is accurate. (For example, with no knowledge of future wind power availability, the storage device would not be useful.) Similarly, the gas generator is paid more under MPC. This makes sense; a dispatchable generator is more valuable if there is more uncertainty about future renewable power availability.

| Device | Dynamic OPF | MPC |

|---|---|---|

| wind generator | ||

| storage | ||

| load | ||

| gas generator |

0.5 Optimal power flow under uncertainty

In this section, we first extend the dynamic model of §0.3 to handle uncertainty. We do this by considering multiple plausible predictions of uncertain values, and extending our optimization problem to handle multiple predictions or forecasts. We will see that prices extend naturally to the uncertain case. We then discuss how to use the uncertain optimal power flow problem in the model predictive control framework of §0.4.

0.5.1 Uncertainty model

Scenarios.

Our uncertainty model considers discrete scenarios. Each scenario models a distinct contingency, i.e., a different possible outcome for the uncertain parameters in the network over the time periods. The different scenarios can differ in the values at different time periods of fixed loads, availability of renewable generators, and even the capacities of transmission lines or storage devices. (For example, a failed transmission line has zero power flow.)

Scenario probabilities.

We assign a probability of realization to each scenario, for . For example, we might model a nominal scenario with high probability, and a variety of fault scenarios, in which critical components break down, each with low probability. The numbers form a probability distribution over the scenarios, i.e., and .

Scenario power flows.

We model a different network power flow for each scenario. The power flows for all terminals, time periods, and scenarios form a (three-dimensional) array . For each scenario there is a power flow matrix , which specifies the power flows on each of the terminals at each of the time periods, under scenario . From the point of view of the system planner, these constitute a power flow policy, i.e., a complete contingency plan consisting of a power schedule for each terminal, under every possible scenario.

We refer to the vector of powers for a device as , where is the number of terminals for device . This array can be viewed as a power flow policy specific to device . We denote by the submatrix of terminal power flows incident on device under scenario .

As before, for each time period, and under each scenario, the power flows incident on each net sum to zero:

In the case of a single scenario () is a matrix, which corresponds to the power flow matrix of §0.3.

Scenario device cost functions.

The device cost functions may be different under each scenario. More specifically, under scenario , device has cost , such that . Note that the network topology, including the number of terminals for each device, does not depend on the scenario. We define the cost function of device as its expected cost over all scenarios

In the case of a single scenario, this definition of device cost coincides with the definition given in §0.3. The expected total system cost is the sum of the expected device costs

0.5.2 Dynamic optimal power flow under uncertainty