On the Statistical Consistency of Risk-Sensitive Bayesian Decision-Making

†{varao@purdue.edu} Department of Statistics, Purdue University.)

Abstract

We study data-driven decision-making problems in the Bayesian framework, where the expectation in the Bayes risk is replaced by a risk-sensitive entropic risk measure. We focus on problems where calculating the posterior distribution is intractable, a typical situation in modern applications with large datasets and complex data generating models. We leverage a dual representation of the entropic risk measure to introduce a novel risk-sensitive variational Bayesian (RSVB) framework for jointly computing a risk-sensitive posterior approximation and the corresponding decision rule. The proposed RSVB framework can be used to extract computational methods for doing risk-sensitive approximate Bayesian inference. We show that our general framework includes two well-known computational methods for doing approximate Bayesian inference viz. naive VB and loss-calibrated VB. We also study the impact of these computational approximations on the predictive performance of the inferred decision rules and values. We compute the convergence rates of the RSVB approximate posterior and also of the corresponding optimal value and decision rules. We illustrate our theoretical findings in both parametric and nonparametric settings with the help of three examples: the single and multi-product newsvendor model and Gaussian process classification.

1 Introduction

This paper focuses on risk-sensitive Bayesian decision-making, considering objective functions of the form

| (SO) |

Here is the decision/action space, is a random model parameter lying in an arbitrary measurable space , and is a problem-specific model risk function. The distribution is the Bayesian posterior distribution over the parameters given observations : , while the scalar is user-specified and characterizes the sensitivity of the decision-maker (DM) to the distribution . Recall that the posterior distribution is obtained by updating a prior probability distribution , capturing subjective beliefs of the decision maker over , according to the Bayes rule

| (1.1) |

where is the likelihood of observing .

The functional is also known as the entropic risk measure, and models a range of risk-averse or risk-seeking behavior in a succinct manner through the parameter . Consider only strictly positive , and observe that

that is, there is no sensitivity to potential risks due to large tail effects and the decision-maker is risk neutral. On the other hand,

the essential supremum of the model risk . In other words, a decision maker is completely risk averse and anticipates the worst possible realization (-almost surely). While similar conclusions can be drawn when , resulting in risk-seeking behavior, we restrict ourselves to in this paper. Observe that (SO) strictly generalizes the standard Bayesian decision-theoretic formulation of a decision-making problem, where the goal is to solve . Furthermore, it also coincides with other risk-based Bayesian methods, such as the penalized posterior variance method studied in [33] for solving the Markowitz portfolio optimization problem, under certain parameterizations. More precisely, for (for any loss function ) and small, but strictly positive , a Taylor expansion of straightforwardly shows that (SO) is equivalent to problem (3.1) in [33].

The risk-sensitive formulation (SO) is very general and can be used to model a wide variety of decision-making problems in operations research/management science [42, 16, 37], simulation optimization [15, 52], and finance [33, 5, 11]. Moreover, it presents a natural way to address epistemic model uncertainty by being Bayesian and risk sensitive. However, solving (SO) to compute an optimal decision over is challenging. The difficulty mainly stems from the fact that, with the exception of conjugate priors, the posterior distribution in (1.1) is an intractable quantity. The use of conjugate priors is restrictive and moreover, for many important likelihood models, they often do not exist. Canonically, posterior intractability is addressed using either a sampling- or optimization-based approach. Sampling-based approaches, such as Markov chain Monte Carlo (MCMC), offer a tractable way to compute the integrals and theoretical guarantees of exact inference in the large computational budget limit. However, these asymptotic guarantees are offset by issues like poor mixing, large variance and complex diagnostics in practical settings with finite computational budgets.

In response, optimization-based methods such as variational Bayes (VB) or variational inference (VI) have emerged as a popular alternative [10]. The VB approximation of the true posterior is a tractable distribution, chosen from a ‘simpler’ family of distributions known as variational family, by minimizing the discrepancy between the true posterior and members of that family. Kullback-Liebler (KL) divergence is the most often used measure of the approximation discrepancy, although other divergences (such as the -Rényi divergence [35, 47, 29]) have been used. The minimizing member, termed the VB approximate posterior, can be used as a proxy for the true posterior. Empirical studies have shown that VB methods are computationally faster and far more scalable to higher-dimensional problems and large datasets. Theoretical guarantees, such as large sample statistical inference, have been a topic of recent interest in theoretical statistics community, with asymptotic properties such as convergence rate and asymptotic normality of the VB approximate posterior recently established in [54, 38] and [50] respectively.

Our ultimate goal is not to merely approximate the posterior distribution, but to also make decisions when that posterior is intractable. A naive approach would be to plug in the VB approximation in place of the true posterior in (SO) and compute the optimal decision. However, it has been noted in [32] that such a naive loss-unaware approach can be suboptimal. In particular, [32] demonstrated, through an example, that a naive posterior approximation only captures the most dominant mode of the true posterior which may not be relevant from decision-making perspective. Consequently, they proposed a loss-calibrated variational Bayesian (LCVB) algorithm for solving Bayesian decision making problems where the underlying risk function is discrete. [31] extended their approach to continuous risk functions. Despite these algorithmic advances in developing decision-centric variational Bayesian methods, their statistical properties such as asymptotic consistency and convergence rates of the loss-aware posterior approximation and the associated decision rule are not well understood. In fact, it is not even clear that the convergence rates of VB approximate posterior established in [54, 38] can be used to establish statistical guarantees on the decision rules learnt using the näive approach. With an aim to address these gaps, we summarize our contribution in this paper below:

-

1.

We introduce a minimax optimization framework titled ‘risk sensitive variational Bayes’ (RSVB), extracted from the dual representation of (SO) using the so-called Donsker-Varadhan variational free-energy principle [21]. The decision-maker computes a risk-sensitive approximation to the true posterior (termed as RSVB posterior) and the decision rule simultaneously by solving a minimax optimization problem. Moreover, for and , we recover the naive and LCVB approaches as special cases of RSVB.

-

2.

We identify verifiable regularity conditions on the prior, likelihood model and the risk function under which the RSVB posterior enjoys the same rate of convergence as the true posterior to a Dirac delta distribution concentrated at the true model parameter , as the sample size increases. Using this result, we also prove the rate of convergence of the RSVB decision rule, when the decision space is compact. Moreover, our theoretical results directly imply the asymptotic properties of the LCVB posterior and the associated decision rule. It is also worth noting that our results are applicable to non-parametric problems such as Gaussian process classification, where the parameter space is infinite-dimensional, as well as non independent and identically distributed data generating processes. Moreover, our analysis also recovers consistency and rate of convergence of decision-rules under the ‘true’ posterior distribution as a special case.

-

3.

We demonstrate our theoretical results with help of three applications:

-

(a)

First, we consider the classic single-product newsvendor problem and verify all the regularity conditions required to establish the convergence rate of the RSVB posterior and the decision rule. We recover the frequentist rate of convergence upto logarithmic factor. Moreover, we present simulation results demonstrating the interplay between the risk-sensitive parameter and number of samples .

-

(b)

Second, we consider the multi-product newsvendor problem and establish the rate of convergence of the corresponding RSVB posterior and decision rule. Here also, we recover the frequentist rate of convergence upto logarithmic factor.

-

(c)

Finally, we consider a binary Gaussian process classification problem, where the model parameter lie in a set of continuous functions on a compact subset of . We construct a wavelet prior and prove all the regularity conditions and compute the rate of convergence of the RSVB posterior (on function space) and the decision rule. The rate of convergence of the RSVB posterior matches to that of the true posterior as established in [48, Theorem 4.5] for the same wavelet prior.

-

(a)

In our theoretical analysis, we mainly establish three important results. First, in Theorem 4.1, we compute a bound on the expected distance of a model from the true model, where expectation is taken with respect to the RSVB posterior. The bound depends on the risk sensitivity parameter and the number of samples , and is a sum of two terms: first one quantifies the rate of convergence of the true posterior and the second one is a consequence of the variational approximation. We further establish regularity conditions on the variational family to compute the rate of convergence of the second term in the bound. In the next two results, we use Theorem 4.1 to derive high probability bounds on the optimality gaps in values (Theorem 4.2) and decisions (Theorem 4.3) computed using the RSVB approach. We define optimality gap in decisions as the deviation of the true optimal decision (when true model is known) from the RSVB decision and define optimality gap in values as the absolute difference between oracle risk evaluated at true and RSVB decision rules. In our simulation results, we first demonstrate the consistency of the RSVB decision with respect to for various values of . We then demonstrate the effect of changing on the optimality gaps and the variance of the RSVB posterior for a given . In particular, we observe that for smaller , increasing (after a certain value) result into a significantly more risk-averse decision, however the effect of increasing on risk-averse decision-making reduces as increases.

Here is a brief roadmap for the rest of the paper. In the next section we provide a literature survey of relevant results from machine learning, theoretical statistics and operations research, placing our results in appropriate context. In Section 3, we present the problem formulation and introduce RSVB framework with relevant notations, definitions and regularity conditions. We develop our theoretical results in Section 4. Thereafter, in Section 5, we discuss naive and loss-calibrated VB as special cases of RSVB. We then illustrate the bounds obtained in Section 4 by specializing the results to the single and multi-product newsvendor problem and Gaussian process classification problem in Section 6 and also present some numerical results. We end with concluding remarks in Section 6.

2 Existing literature and our work

Our paper fits in with a growing body of work in developing rigorous theoretical understanding of variational Bayesian methods in statistics and machine learning. Moreover, our proposed methodology also contributes to the work in machine learning and operations research that lies at the intersection of decision-making under uncertainty and statistical estimation.

The primary goal in data-driven decision-making is to learn empirical decision-rules (or predictive prescriptions as [6] term them) that prescribes a decision, given an observation of the covariates . Early work in this direction, including classic work by Herbert Scarf on Bayesian solutions to the newsvendor problem [43], focused on two-stage solutions - estimation followed by optimization. Our setting is most related to recent work on Bayesian risk optimization (BRO) in [52, 55]. In BRO, the authors consider optimal decision-making using various coherent risk measures computed under the posterior distribution. The authors establish several important results, including that the optimal values and decisions are asymptotically consistent as the sample size tends to infinity, and central limit theorems for these quantities. However, there are substantial differences with our paper. First, all of the analysis in [52] presumes that the posterior risk measures are actually computable. The authors do not address the critical computational questions surrounding Bayesian methods or the impact of (inevitable) computational approximations on BRO – indeed, this is not their focus. Second, extended coherent risk measures are not considered (in particular, the log-exponential risk measure used here), and it is unclear if the asymptotic results continue hold otherwise. Third, while we use a risk measure to derive the computational framework (RSVB), the focus in [52] is purely on the analytical properties of optimal decisions.

More recently, there has been significant interest in methods that use empirical risk minimization (ERM) or sample average approximation (SAA) for directly estimating decision-rules that optimize Monte Carlo or empirical approximations [6, 7, 2, 8, 17, 22, 51]. The survey by [27] consolidates recent results on Monte Carlo methods for stochastic optimization. It is important to note that this recent surge of work in data-driven decision-making has largely focused on explicit black-box models. On the other hand, there are many situations where optimal decisions must be made in the presence of a well-defined parametrized stochastic model. Bayesian methods are a natural means for estimating distributions over the parameters of a stochastic model; though, as noted before, the computational complexity of Bayesian algorithms can be high. The interplay between optimization and estimation, in the sense of discovering predictive prescriptions for Bayesian models has largely been ignored. Furthermore, as [36] show in the newsvendor context, SEO methods can be suboptimal in terms of expected regret and long-term average losses. [36] introduced operational statistics (OS) as an alternative to SEO (see [16, 37] as well), whereby the optimal empirical order quantity is determined as a function of an optimization parameter that can be determined for each sample size. OS has demonstrably better performance, especially on single parameter newsvendor problems (though there is much less known about its statistical properties).

In the machine learning literature, [32] observe that calibrating a Gaussian process classification algorithm to a fixed loss function can improve classification performance over a loss-insensitive algorithm – indeed, this is the first documented presentation of the LCVB algorithm. Similarly, surrogate loss functions [4, 46] that are regularized upper bounds that depend on the cost function, also implicitly loss-calibrate frequentist classification algorithms.

While standard VB methods for posterior estimation have been extensively used in machine learning [10], it is only recently that the theoretical questions surrounding VB have been addressed [50, 54, 38, 29, 53, 1, 30, 14, 3]. In particular, we note [50] who prove asymptotic consistency of VB in the large sample limit, [54] and [38] on the other hand establish bounds on the rate of convergence of the VB posterior to the ‘true’ posterior providing a more refined analysis, and [29] where asymptotic consistency of -Rényi VB was demonstrated. Our analysis in this paper, extends these results to establish convergence rates of the approximate posterior and learnt decision rules in risk-sensitive variational Bayesian decision-making framework. These bounds, in turn, are complementary to large sample analyses in [28].

3 Problem Setup

Let be a measure space with sigma-algebra generated by , where, in general, denote the -fold product of a set . Let represent a set of samples from the true model with parameter . Denoting the likelihood of observing as and the prior distribution , we define the posterior distribution as We also write as for brevity. Moreover, we denote the corresponding prior and posterior density (if they exist) as and .

As noted in the introduction, our objective is to optimize the posterior log-exponential or entropic risk measure of , that is

| (SO) |

In practical settings, the posterior typically cannot be easily computed, and decision makers are often led to restrictive modeling choices such as assuming the likelihood function has a conjugate prior. Nonetheless, incorporating non-conjugate priors and complicated hierarchical models is critical for realizing the full utility of decision-theoretic Bayesian methods - however this entails the use of computational approximations. Therefore, in the next paragraph we introduce a framework from which can be extracted computational methods for approximately computing and optimizing posterior decision risk.

3.1 Risk-Sensitive Variational Bayes

Our approach exploits the dual representation of the log-exponential risk measure in (SO), which is convex (or extended coherent) [41, 23]. From the Donsker-Varadhan variational free energy principle [20, 18, 19, 21] we observe that,

| (DV) |

where is the set of all distribution functions that are absolutely continuous with respect to the posterior distribution and ‘KL’ represents the Kullback-Leibler divergence. Formally, for any two distributions and defined on measurable space , the KL divergence is defined as

| (3.1) |

where denotes that measure is absolutely continuous with respect to . Notice that this dual formulation exposes the reason we choose to use the log-exponential risk – the right hand side provides a combined assessment of the risk associated with model estimation (computed by the KL divergence ) and the decision risk under the estimated posterior (computed by ).

In this paper, we restrict our analyses to the risk-averse case, that is . However, it can be extended easily to the case when to obtain similar theoretical insights.

As stated above, the reformulation presented in (DV) offers no computational gains. However, restricting ourselves to an appropriately chosen subset , that consists of distributions where the integral can be tractably computed, we immediately obtain a risk-sensitive variational Bayesian (RSVB) formulation of (DV):

| (RSVB) |

RSVB is our framework for data-driven risk-sensitive decision-making. The family of distributions is popularly known as the variational family. The choice of the family , disutility/ risk , and parameter encodes specific problem settings. Our analysis in subsequent Section 4.1 below reveals general guidelines on how to choose that ensures a small optimality gap (defined below) with high probability.

With an appropriate choice of , the optimization on the RHS can yield a good approximation to the log-exponential risk measurement on the left hand side (LHS). For brevity, for a given we define the RSVB approximation to the true posterior as

and the RSVB optimal decision as

Observe that and are random quantities, conditional on the data . Intuitively, it can be observed that the risk averseness of increases with increase in . To observe this consider the RSVB formulation and note that , therefore as increases there is more incentive to deviate from the true posterior and choose that maximizes expected risk for a given . Consequently as increases, the RSVB decision rule becomes more risk-averse.

Examples of include the family of Gaussian distributions, delta functions, or the family of factorized ‘mean-field’ distributions that discard correlations between components of . The choice of is decisive in determining the performance of the algorithm. In general, however the requirements on are minimal, and part of the analysis in this paper is to articulate sufficient conditions on that ensure small optimality gap (defined below) for the optimal decision, . This establishes the “statistical goodness” of the procedure as number of samples increase. In this paper, we analyze the efficacy of the decision rules obtained using the RSVB approximation, by providing high-probability bounds on the optimality gap. We define the optimality gap for any with value as,

Definition 3.1 (Optimality Gap).

Let be the optimal value and be the optimal decision for the true model parameter . Then, the optimality gap in the value is the difference and the optimality gap in decision variables is where is the appropriate norm on the decision sapce .

A similar performance measure was used in [31], to measure the effectiveness of loss-calibrated VB (LCVB) approach, which can be obtained by setting , as a special case of our RSVB formulation. Nonetheless, in Section 5, we discuss two well-known variational Bayesian algorithms (one of them is LCVB) for decision making, which are special cases of RSVB. Moreover, we establish bounds on their respective optimality gaps as a corollary to the bounds derived for RSVB.

Note that the RSVB algorithm described above is idealized – clearly the objective cannot be computed since it requires the calculation of the posterior distribution – the very object we are approximating! Note, however that optimizing is equivalent to optimizing , where is known, and for which the optimizers are the same. Since our focus is on bounding the optimality gap, in the remainder of the paper any reference to the RSVB algorithm is an allusion to the idealized objective .

In the following section, we lay down important assumptions and definitions used throughout the paper to establish our theoretical results.

3.2 Notations and Definitions

We provide the definitions of important terms used throughout the paper. First, recall the definition of covering numbers:

Definition 3.2 (Covering numbers).

Let be a parametric family of distributions and be a metric. An cover of a subset of the parametric family of distributions is a set such that, for each there exists a that satisfies . The covering number of is where represents the cardinality of the set.

Next, recall the definition of a test function [44]:

Definition 3.3 (Test function).

Let be a sequence of random variables on measurable space . Then any -measurable sequence of functions , is a test of a hypothesis that a probability measure on belongs to a given set against the hypothesis that it belongs to an alternative set. The test is consistent for hypothesis against the alternative if as , where is an indicator function.

A classic example of a test function is that is constructed using the Kolmogorov-Smirnov statistic , where and are the empirical and true distribution respectively, and is the confidence level. If the null hypothesis is true, the Glivenko-Cantelli theorem [49, Theorem 19.1] shows that the KS statistic converges to zero as the number of samples increases to infinity.

Furthermore, we define the Hellinger distance between the two probability distributions and is defined as We define the one-sided Hausdorff distance between sets and in a metric space with distance function is defined as:

Next, we define an arbitrary loss function that measures the distance between models . At the outset, we assume that is always positive. We define as a sequence such that as and .

We also define

Definition 3.4 (convergence).

A sequence of functions , for each , converges to , if

-

•

for every and every such that ,

-

•

for every , there exists some such that ,

In addition, we define

Definition 3.5 (Primal feasibility).

For any two functions and , a point is primal feasible to the following constraint optimization problem

if , for a given .

3.3 Assumptions

In order to bound the optimality gap, we require some control over how quickly the posterior distribution concentrates at the true parameter . Our next assumption in terms of a verifiable test condition on the model (sub-)space is one of the conditions required to quantify this rate.

Assumption 3.1 (Model indentifiability).

Fix . Then, for any such that as and , there exists a measurable sequence of test functions and sieve set such that (i) (ii) .

Observe that Assumption 3.1 quantifies the rate at which a type 1 error diminishes with the sample size, while the condition in Assumption 3.1 quantifies that of a type 2 error. Notice that both of these are stated through test functions; indeed, what is required are consistent test functions. Opportunely, [24, Theorem 7.1] (stated in Appendix as Lemma A.7 for completeness) roughly implies that an appropriately bounded model subspace (the size of which is measured using covering numbers) guarantees the existence of consistent test functions, to test the null hypothesis that the true parameter is against an alternate hypothesis – the alternate being defined using the ‘distance function’ . Subsequently, we will use a specific distance function to obtain finite sample bounds for the optimality gap in decisions and values. In some problem instances, it is also possible to construct consistent test functions directly without recourse to Lemma A.7. We demonstrate this in Section 6.1 below.

Next, we assume a condition on the prior distribution that ensures that it provides sufficient mass to the set , as defined above in Assumption 3.1.

Assumption 3.2.

Fix . Then, for any such that as and , the prior distribution satisfies

Notice that Assumption 3.2 is trivially satisfied if . The next assumption ensures that the prior distribution places sufficient mass around a neighborhood – defined using Rényi divergence – of the true parameter .

Assumption 3.3 (Prior thickness).

Fix and a constant . Let where is the Rényi divergence between and , assuming is absolutely continuous with respect to . The prior distribution satisfies

Notice that the set defines a neighborhood of the distribution corresponding to in the model subspace . The assumption guarantees that the prior distribution covers this neighborhood with positive mass. This is a standard assumption and if it is violated then the posterior too will place no mass in this neighborhood ensuring asymptotic inconsistency. The above three assumptions are adopted from [24] and has also been used in [54] to prove convergence rates of variational posteriors. Interested readers may refer to [24] and [54] to read more about the above assumptions.

It is apparent by the first term in (RSVB) that in addition to Assumption 3.1, 3.2, and 3.3, we also require regularity conditions on the risk function . Thus, the next assumption restricts the prior distribution with respect to .

Assumption 3.4.

Fix and . For any , ,

where and are scalar positive functions of .

Note that the set represents the subset of the model space where the risk (for a fixed decision ) is large, and the prior is assumed to place sufficiently small mass over such sets. Moreover, using Cauchy-Schwarz inequality observe that

which implies that if the risk function is bounded in , then above condition can be trivially satisfied. Finally, we also require the following condition lower bounding the risk function .

Assumption 3.5.

is assumed to satisfy

Note that any risk function which is bounded from below in both the arguments satisfies this condition. Furthermore, following [39] we define a growth condition on the ‘true’ risk function .

Assumption 3.6 (Growth condition).

Let be a growth function if it is strictly increasing as and . Then for any , satisfies a growth condition with respect to , if

| (3.2) |

The growth condition above is a generalization of strong-convexity. Indeed, if the true risk is strongly convex, then this condition is automatically satisfied.

In the next, section we derive high-probability bounds on the optimality gap in values and decisions, by proving a series of results.

4 Asymptotic Analysis of the Optimality Gaps

In this section, we establish high-probability bounds on the optimality gap in values and decision rules computed using RSVB approach for sufficiently large . Our results in here identify the regularity conditions on the data generating model , the prior distribution , the variational family , the risk function to compute the bounds.

We can now state our first result, establishing an upper bound on the expected deviation from the true model , measured using distance function , under the RSVB approximate posterior. We also note that the following result generalizes Theorem 2.1 of [54], which is exclusively for the case when . However, the proof techniques are motivated from the proof of Theorem 2.1 in [54].

Theorem 4.1.

First recall that is the convergence rate of the true posterior [24, Theorem 7.3]. Notice that the additional term emerges from the posterior approximation and depends on the choice of the variational family , risk function , and the parameter . The appearance of this term in the bound also signifies that, to minimize expected gap between true model and any other model, defined using , under the RSVB posterior, the average (with respect to ) RSVB objective has to be maximized. Later in this section, we specify the conditions on the family of distributions , the prior and the variational family that ensure as . Moreover, we also identify mild regularity conditions on to show that is . Furthermore, we show that as increases decreases. We discuss this result and the bound therein later in the next subsection. Before that, we establish our main result (the bounds on the optimality gap) using the theorem above.

Since the result in Theorem 4.1 holds for any positive distance function, we now fix

| (4.2) |

Notice that for a given , is the uniform distance between the and . Intuitively, Theorem 4.1 implies that the expected uniform difference with respect to the RSVB approximate posterior is , and if as then it converges to zero at that rate.

Also, note that in order to use (4.2) we must demonstrate that it satisfies Assumption 3.1. This can be achieved by constructing bespoke test functions for a given . We demonstrate this approach by an example in Section 6.2. Nonetheless, we also provide sufficient conditions for the existence of the test functions in the appendix. These conditions are typically easy to verify when the loss function are bounded, for instance.

Now, we first bound the optimality gap between and .

Theorem 4.2.

Next, we bound the optimality gap between the approximate optimal decision rule and the true optimal decision. The bound, in particular, depends on the curvature of around the true optimal decision, defined using the growth condition in Assumption 3.6.

Theorem 4.3.

To fix the intuition, suppose and , then represents the Hessian of the true risk, , near its optimizer. It is easy to see from the above result the rate of convergence of is scaled by a factor . That is, higher the curvature near the optimizer, the faster converges.

Evidently, the bounds obtained in all three results that we have proved so far depends on . Consequently, in the next section, with an aim to understand the properties of the bounds in Theorem 4.1, 4.2, and 4.3, we prove some of the important properties of with respect to and under some additional regularity conditions.

4.1 Properties of

In order to characterize , we specify conditions on variational family such that , for some and . We impose following condition on the variational family that lets us obtain a bound on in terms of and .

Assumption 4.1.

There exists a sequence of distribution in the variational family such that for a positive constant ,

| (4.4) |

If the observations in are i.i.d, then observe that

Intuitively, this assumption implies that the variational family must contain a sequence of distributions that converges weakly to a Dirac delta distribution concentrated at the true parameter otherwise the second term in the LHS of (4.4) will be non-zero. Also note that the above assumption does not imply that the minimizing sequence (automatically) converges weakly to a dirac-delta distribution at the true parameter . Furthermore, unlike Theorem 2.3 of [54], our condition on in Assumption 4.1, to obtain a bound on , does not require the support of the distributions in to shrink to the true parameter at some appropriate rate, as the numbers of samples increases.

Proposition 4.1.

Under Assumption 4.1 and for a constant and ,

In Section 6, we present an example where the likelihood is exponentially distributed, the prior is inverse-gamma (non-conjugate), and the variational family is the class of gamma distributions, where we construct a sequence of distributions in the variational family that satisfies Assumption 4.1. We also provide another example where the likelihood is multivariate Gaussian with unknown mean and variational family is uncorrelated Gaussian restricted to compact subset of with an uniform prior on the same compact set satisfy Assumption 4.1.

By definition and as , and therefore it follows from Proposition 4.1 that . However, the bound obtained in the last proposition might be loose with respect to , when . To see this, we prove the following result.

Proposition 4.2.

If the solution to the optimization problem in is primal feasible then decreases as increases.

5 Special Cases of RSVB

Recall from the RSVB formulation that encodes the risk sensitivity of the decision maker. In this section, we show that RSVB generalizes two well-known variational Bayesian approaches for decision making, ‘naive’ VB (NVB) and loss-calibrated VB(LCVB). In particular, the RSVB method is equivalent to NVB when and LCVB for . In what follows, we discuss NVB and LCVB briefly and demonstrate our theoretical results to these settings.

5.1 Naive VB

The naive VB (NVB) method, summarized below in Algorithm 1, is a “separated estimation and optimization” method wherein we use the VB approximation to the posterior distribution as a plug-in estimator for computing the posterior predictive loss, and then optimize the resulting approximate posterior predictive loss.

The NVB method completely isolates the statistical estimation problem from the decision-making problem. Observe that as , and converges to and respectively; that is

To see this, recall the RSVB formulation and multiply by on either side to obtain:

| (5.1) | ||||

Note that, since converges uniformly in to as , therefore former converges to the latter and hence their respective minimizers and minimum values [13]. In particular, to prove the uniform convergence, let be a sequence of rational numbers on , such that is dense in and as . Now observe that for every and given and , there exists a , such that for all and , , hence uniform convergence follows.

Now taking limit , the equation (5.1) reduces to the well known evidence lower bound [10] , that is

where is the prior density. Therefore, it follows that for any

Since , we do not require Assumption 3.4 and 3.5 to obtain an analogous result to Theorem A.1 for NVB method. Therefore, the condition on the constants in Theorem A.1 ( ) is simplified to by choosing as a small and as a large number.

Theorem 5.1.

The next result establishes a bound on the optimality gap of the naive VB estimated optimal value from the true optimal value .

Theorem 5.2.

Next, we bound the optimality gap between the approximate optimal decision rule and the true optimal decision. The bound, in particular, depends on the curvature of around the true optimal decision. The growth function is denoted as . The following theorem is a special case of the general result for in Theorem 4.3.

Theorem 5.3.

5.2 Loss Calibrated VB

Algorithm 2 summarizes the Loss-calibrated VB (LCVB) method [32].

Observe that this method combines the posterior approximation and decision-making problems into one minimax optimization problem. The objective here can be directly contrasted with that in Algorithm 1. Note that the inner maximization will result in an approximate (loss calibrated) posterior distribution at each decision point . Moreover, also note that LCVB is same as RSVB for .

In this section, we compute a bound on the optimality gaps loss-calibrated optimal decision and optimal value.

Theorem 5.4.

Note that, the second term (inside the expectation) in the definition of could result in either or vice versa and therefore could play an important role in comparing the LCVB and naive VB approximations to the true optimal decision.

The next result establishes a bound on the optimality gap of the LCVB estimated optimal value from the true optimal value .

Theorem 5.5.

Next, we bound the optimality gap between the approximate LC optimal decision rule and the true optimal decision.

6 Applications

We illustrate our theoretical findings with the help of three examples: the single and multi-product newsvendor model and Gaussian process classification. In the examples, we study the interplay between sample size and the risk parameter , and their effect on the optimality gap in decisions and values.

6.1 Single-product Newsvendor Model

In this section, we study a canonical data-driven decision-making problem with a ‘well-behaved’ risk function , the data-driven newsvendor model. This problem has received extensive study in the literature, and remains a cornerstone of inventory management [43, 9, 34]. Recall that the newsvendor loss function is defined as

where (underage cost) and (overage cost) are given positive constants, the random demand, and the inventory or decision variable, typically assumed to take values in a compact decision space with and , and . The distribution over the random demand, is assumed to be exponential with unknown rate parameter . The model risk can easily be derived as

| (6.1) |

which is convex in . We assume that be observations of the random demand, assumed to be i.i.d random samples drawn from .

We fix the model space for some and assume that lies in the interior of . We now assume a non-conjugate truncated inverse-gamma () prior distribution restricted to , with shape and rate parameter and respectively, that is for a set , we define . We now verify Assumptions 3.2, 3.1, 3.3, 3.5 and 3.4 (in that order) in this newsvendor setting. The proofs of the lemmas are delayed to the electronic companion for readability.

First, we fix the sieve set , which clearly implies that the restricted inverse-gamma prior , places no mass on the complement of this set and therefore satisfies Assumption 3.2.

Second, under the condition that the true demand distribution is exponential with parameter (and ), we demonstrate the existence of test functions satisfying Assumption 3.1.

Lemma 6.1.

Fix . Then, for any with , and , there exists a test function (depending on ) such that satisfies

| (6.2) | ||||

| (6.3) |

where and for a constant and .

The proof of the above result follows by showing that can be bounded above by the Hellinger distance between two exponential distributions on (under which a test function exists) in Lemma A.11 in the appendix.

Third, we show that there exist appropriate constants such that the inverse-gamma prior satisfies Assumption 3.3 when the demand distribution is exponential.

Lemma 6.2.

Fix and any . Let , where is the Rényi divergence between and . Then for and any such , the truncated inverse-gamma prior satisfies

Fourth, it is straightforward to see that the newsvendor model risk is bounded below for a given .

Lemma 6.3.

For any and positive constants and , the newsvendor model risk

where and satisfies .

This implies that satisfies Assumption 3.5. Finally, we also show that the newsvendor model risk satisfies Assumption 3.4.

Lemma 6.4.

Fix and . For any and any , satisfies

for any and , where .

Note that Lemma 6.1 implies that for any constant . Fixing and using Lemma 6.2 we can choose . Now, can be chosen large enough such that for a given risk sensitivity . Therefore, the condition on constants in Theorem 4.1 reduces to , and it can be satisfied easily by fixing (say).

These lemmas show that when the demand distribution is exponential and with a non-conjugate truncated inverse-gamma prior, our results in Theorem 4.2 and 4.3 can be used for RSVB method to bound the optimality gap in decisions and values for various values of the risk-sensitivity parameter . Recall that the bound obtained in Theorem 4.3 depends on and .

Lemma 6.2 implies that , but in order to get the complete bound we further need to characterize . Recall that, as a consequence of Assumption 4.1 in Proposition 4.1, for a given that and

Therefore, in our next result, we show that in the newsvendor setting, we can construct a sequence that satisfies Assumption 4.1, and thus identify and the constant . We fix to be the family of shifted gamma distributions with support .

Lemma 6.5.

Let be a sequence of shifted gamma distributions with shape parameter and rate parameter , then for truncated inverse gamma prior and exponentially distributed likelihood model

where and and prior parameters are chosen such that .

As a specific instance, consider the naive VB case. Since , the term in Theorem 5.3 is bounded above by , where and are derived in the result above. For the LCVB case, observe that Lemma 6.3 implies that is bounded below and therefore , where are given to the modeler or are easily computable. Now since , it is straight forward to observe that term in Theorem 5.6 is bounded above by .

Now, using the result established in Lemmas above, we bound the optimality gap in values for the single product newsvendor model risk.

Theorem 6.1.

Fix . Suppose that the set is compact. Then, for the newsvendor model with exponentially distributed demand with rate , prior distribution , and the variational family fixed to shifted (by ) gamma distributions, and for any , the probability of the following event

| (6.4) |

is at least for sufficiently large and for some mapping , where is the newsvendor model risk.

Proof.

Next, we bound the optimality gap between the approximate optimal decision rule and the true optimal decision. The bound, in particular, depends on the curvature of around the true optimal decision, defined using the growth condition in Assumption 3.6.

Theorem 6.2.

Fix . Suppose that the set is compact and satisfies the growth condition in Assumption 3.6, with such that , for any . Then, for the newsvendor model with exponentially distributed demand with rate , prior distribution , and the variational family fixed to shifted (by ) gamma distributions, and for any , the probability of the following event

is at least for sufficiently large and for some mapping , where is the newsvendor model risk.

Proof.

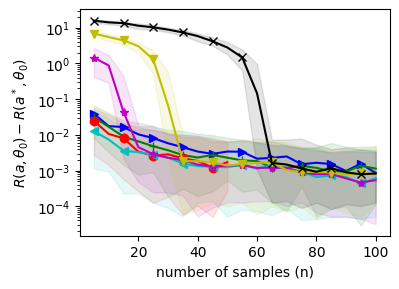

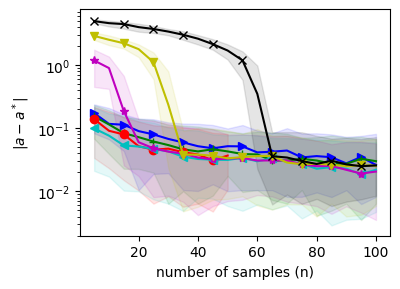

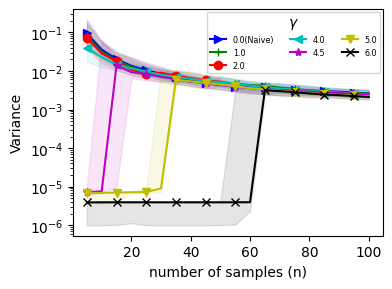

Next, we demonstrate the effect of varying the risk-sensitivity parameter . We fix , , , . We run RSVB algorithm with and repeat the experiment over 100 sample paths. We plot the results in Figure 1. In Figure 1(a) and (b), we plot the optimality gap in values and decisions, that is and respectively, for various values of . We observe that the gap decreases when increases. This observation supports our results in Propositions 4.1 and 4.2 that establishes the properties of as increases. Lastly, in Figure 1(c), we plot the variance of the RSVB posterior as increases for various values of ; as anticipated the variance reduces as increases. To observe the effect of , first recall that as increases the decision maker become more risk averse and so is our algorithmic framework RSVB. Indeed, from the rightmost variance plot in Figure 1 it is evident that for larger value of () the RSVB posterior is more concentrated on the subset of , where risk is more and consequently we observe large optimality gaps in values and decision (see first two plots in Figure 1 ). Moreover, as increase the effect of larger reduces, since as increases the incentive to deviate from the posterior reduces (due to increased KL divergence dominance for larger in RSVB).

6.2 Multi-product newsvendor problem

Analogous to the one-dimensional newsvendor loss function, the loss function in its multi-product version is defined as

where and are given vectors of underage and overage costs respectively for each product and mapping is defined component-wise. We assume that there are items or products and denotes the random vector of demands. Let be the inventory or decision variable, typically assumed to take values in a compact decision space with and , and , where is the marginal set of component of . The random demand is assumed to be multivariate Gaussian, with unknown mean parameter but with known covariance matrix . We also assume that is a symmetric positive definite matrix and can be decomposed as , where is an orthogonal matrix and is a diagonal matrix consisting of respective eigenvalues of . We also define and . The model risk

which is convex in . Here is the marginal distribution of for product, and are probability and cumulative distribution function of the standard Normal distribution. We also assume that the true mean parameter lies in a compact subspace . We fix the prior to be uniformly distributed on with no correlation across its components, that is , where is the Lebesgue measure (or volume) of As in the previous example, we fix the sieve set , which clearly implies that places no mass on the complement of this set and therefore satisfies Assumption 3.2.

Then under the condition that the true demand distribution has a multivariate Gaussian distribution (with known ) and mean (), we demonstrate the existence of test functions satisfying Assumption 3.1 by constructing a test function unlike the single-product newsvendor problem with exponential demand.

Lemma 6.6.

Fix . Then, for any with , and and test function , satisfies

| (6.5) | ||||

| (6.6) |

with , and for sufficiently large such that and , where .

In the following result, we show that there exist appropriate constants such that prior distribution satisfies Assumption 3.3 when the demand distribution is a multivariate Gaussian with unknown mean.

Lemma 6.7.

Fix and any . Let , where is the Rényi Divergence between and . Then for and any such that and for large enough , the uncorrelated uniform prior restricted to satisfies

Next, it is straightforward to see that the multi-product newsvendor model risk is bounded below for a given on a compact set and thus it satisfies Assumption 3.5. Finally, we also show that the newsvendor model risk satisfies Assumption 3.4.

Lemma 6.8.

Fix and . For any and , satisfies

for any and .

Similar to single product example, in our next result, we show that in the multi-product newsvendor setting, we can construct a sequence that satisfies Assumption 4.1, and thus identify and constant . We fix to be the family of uncorrelated Gaussian distributions restricted to .

Lemma 6.9.

Let be a sequence of product of univariate Gaussian distribution defined as and fix and for all . Then for uncorrelated uniform distribution restricted to and multivariate normal likelihood model

where and .

Now, using the result established in lemmas above, we bound the optimality gap in values for the multi-product newsvendor model risk.

Theorem 6.3.

Fix . Suppose that the set is compact. Then, for the multi-product newsvendor model with multivariate Gaussian distributed demand with known covariance matrix and unknown mean vector lying in a compact subset , prior , and the variational family fixed to uncorrelated Gaussian distribution restricted to , and for any , the probability of the following event

| (6.7) |

is at least for sufficiently large and for some mapping , where is the multi-product newsvendor model risk.

Proof.

Next, we bound the optimality gap between the approximate optimal decision rule and the true optimal decision.

Theorem 6.4.

Fix . Suppose that the set is compact and satisfies the growth condition in Assumption 3.6, with such that , for any . Then, for the multi-product newsvendor model with multivariate Gaussian distributed demand with known covariance matrix and unknown mean vector lying in a compact subset , prior , and the variational family fixed to uncorrelated Gaussian distribution restricted to , and for any , the probability of the following event

is at least for sufficiently large and for a known function , where is the multi-product newsvendor model risk.

6.3 Gaussian process classification

Consider a problem of classifying an input pattern or features lying in measure space into one of two classes , where denote the class of . For a given , we model the classifier using a Bernoulli distribution , where is a non-parametric model parameter in a separable Banach space and measurable functions and . Note that is a logistic function. We denote as the derivative of . We assume that is independent of . Thus the sequence of independent observations are assumed to be generated from model

In the above binary classification problem, the objective is to estimate using the observation vector . We posit a Gaussian process (GP) prior on (to be defined later). We also assume that is known and we do not place any prior on it. Consequently, the posterior distribution over given observations can be defined as

Consider the loss function defined as

| (6.8) |

where and are known positive constants. The model risk is given by

| (6.9) |

We define the distance function as . In anticipation of demonstrating that the binary classification model with GP prior and distance function satisfy the desired set of assumptions, we recall the following result, from [48], which will be central in establishing Assumptions 3.1, 3.2, and 3.3.

Lemma 6.10.

[Theorem 2.1 [48]] Let be a Borel measurable, zero-mean Gaussian random element in a separable Banach space with reproducing kernel Hilbert space (RKHS) and let be contained in the closure of in . For any satisfying , where

| (6.10) |

and any with , there exists a measurable set such that

| (6.11) | ||||

| (6.12) | ||||

| (6.13) |

The proof of the lemma above can be easily adapted from the proof of [48, Theorem 2.1], which is specifically for . Notice that the result above is true for any norm on the Banach space if that satisfies . Moreover, if is true, then it also holds for any , since by definition is a decreasing function of .

All the results in the previous lemma depend on being less than . In particular, observe that the second term in the definition of depends on the prior distribution on . Therefore, [48, Theorem 4.5] show that ( with as supremum norm and for as defined later in (6.17) ) is satisfied by the Gaussian prior of type

| (6.14) |

where is a sequence that decreases with , are i.i.d. standard Gaussian random variables and form a double-indexed orthonormal basis (with respect to measure ), that is ). is the smallest integer satisfying for a given . In particular, the GP above is constructed using the function class that is supported on and has a wavelet expansion,

The wavelet function space is equipped with the norm: ; the supremum norm: ; and the Besov norm: . Note that induces a measure over the RKHS , defined as a collection of truncated wavelet functions

with norm induced by the inner-product on as The RKHS kernel can be easily derived as

Indeed, by the definition of this kernel and inner product, observe that

Moreover, It is clear from its definition that is a centered Gaussian random field on the RKHS.

Next, using the definition of the kernel, we derive the covariance operator of the Gaussian random field . Recall that , which enables us to define the covariance operator , following [45, (6.19)] as

Also, observe that is the eigenvalue and eigen function pair of the covariance operator . Consequently, using Karhunen Loéve expansion [45, Theorem 6.19] the prior induced by on is a Gaussian distribution denoted as . We also recall the Cameron-Martin space denoted as associated with a Gaussian measure on to be the intersection of all linear spaces of full measure under [45, (page 530)]. In particular, is the Hilbert space with inner product .

Next, we show the existence of test functions in the following result.

Lemma 6.11.

For any with , , and , there exists a test function (depending on ) such that satisfies

| (6.15) | ||||

| (6.16) |

where , and .

Assumption 3.2 is a direct consequence of (6.12) in Lemma 6.10. Next, we prove that prior distribution and the likelihood model satisfy Assumption 3.3 using (6.13) of Lemma 6.10.

Lemma 6.12.

For any , let , where is the Rényi Divergence between and . Then for any satisfying and and , the GP prior satisfies

Assumption 3.4 and 3.5 are straightforward to satisfy since the model risk function is bounded from above and below.

Now, suppose the variational family is a class of Gaussian distributions on , defined as , belongs to and is the covariance operator defined as , for any which is a symmetric and Hilbert-Schmidt (HS) operator on (eigenvalues of HS operator are square summable). Note that and span the distributions in .

The following lemma verifies Assumption 4.1, for a specific sequence of distributions in .

Lemma 6.13.

For a given , let be a sequence variational distribution such that is the measure induced by a GP, , where and . Then for GP prior induced by and for some , , and lie in the Cameron-Martin space , we have

where

| (6.17) |

and , where is a positive constant satisfying .

Using the result above together with Proposition 4.2 implies that the RSVB posterior converges at the same rate as the true posterior, where the convergence rate of the true posterior is derived in [48, Theorem 4.5] for the binary GP classification problem with truncated wavelet GP prior.

Finally, we use the results above to obtain bound on the optimality gap in values of the binary GP classification problem.

Theorem 6.5.

Fix and for a given . For the binary GP classification problem with GP prior induced by and for some , , and lie in the Cameron-Martin space , the variational family , and for any , the probability of the following event

| (6.18) |

is at least for sufficiently large and for some mapping , where is defined in (6.9) and as derived in (6.17).

7 Conclusion

In this paper, we introduced a novel framework risk-sensitive variational Bayes (RSVB), which can be used to extract computational methods for risk-sensitive approximate Bayesian inference. There are number of future directions that we are currently working on. Recall from the simulation result presented in Section 6.1, that the performance of the RSVB framework is affected by the choice of the risk-sensitivity parameter . However, the high-probability (large-sample) bound derived in Section 4 does not reflect this dependence explicitly. Consequently, digging out this dependence of the RSVB predictive performance on is one of the future directions that we are currently working on. Although we briefly discuss in the introduction that the Bayesian Markowitz problem [33] is a special case of our RSVB framework, we do not discuss this as part of our examples. The main challenge in studying the Bayesian Markowitz problem under the RSVB framework is constructing a test function (Assumption 3.1) with exponentially bounded errors for all (as required to establish convergence rates of the variational posteriors in Theorem 4.1 and also in [54, Theorem 2.1] and in [53, Theorem 3.5]). We are currently studying the Bayesian Markowitz problem for portfolio selection under the RSVB framework, as this is one of the important problems where the RSVB framework could be relevant. Moreover, as part of future work, we also aim to extend this work to incorporate models with local latent variables such as mixture models, where VB methods have been empirically demonstrated to outperform sampling-based posterior approximation methods. Additionally, we are also investigating risk-sensitive frameworks comprising other types of divergence measures.

References

- [1] Pierre Alquier and James Ridgway. Concentration of tempered posteriors and of their variational approximations. Ann. Stat., 48(3), Jun 2020.

- [2] Gah-Yi Ban and Cynthia Rudin. The big data newsvendor: Practical insights from machine learning. Oper. Res., 67(1):90–108, 2018.

- [3] Imon Banerjee, Vinayak A Rao, and Harsha Honnappa. Pac-bayes bounds on variational tempered posteriors for markov models. Entropy, 23(3):313, 2021.

- [4] Peter L Bartlett, Michael I Jordan, and Jon D McAuliffe. Convexity, classification, and risk bounds. J. Am. Stat. Assoc., 101(473):138–156, 2006.

- [5] David Bauder, Taras Bodnar, Nestor Parolya, and Wolfgang Schmid. Bayesian mean–variance analysis: optimal portfolio selection under parameter uncertainty. Quant. Financ., 21(2):221–242, May 2020.

- [6] Dimitris Bertsimas and Nathan Kallus. From predictive to prescriptive analytics. arXiv preprint arXiv:1402.5481, 2014.

- [7] Dimitris Bertsimas, Nathan Kallus, and Amjad Hussain. Inventory management in the era of big data. Prod. Oper. Manage., 25(12):2006–2009, 2016.

- [8] Dimitris Bertsimas and Christopher McCord. Optimization over continuous and multi-dimensional decisions with observational data. In Adv. Neural Inf. Process. Syst., pages 2966–2974, 2018.

- [9] Dimitris Bertsimas and Aurélie Thiele. A data-driven approach to newsvendor problems. Working Paper, Massachusetts Institute of Technology, 2005.

- [10] David M. Blei, Alp Kucukelbir, and Jon D. McAuliffe. Variational inference: A review for statisticians. J. Am. Stat. Assoc., 112(518):859–877, Feb 2017.

- [11] Taras Bodnar, Stepan Mazur, and Yarema Okhrin. Bayesian estimation of the global minimum variance portfolio. Eur. J. Oper. Res., 256(1):292–307, Jan 2017.

- [12] Stéphane Boucheron, Gábor Lugosi, and Pascal Massart. Concentration inequalities: A nonasymptotic theory of independence. Oxford university press, 2013.

- [13] Andrea Braides. Gamma-Convergence for Beginners. Oxford University Press, Jul 2002.

- [14] Badr-Eddine Chérief-Abdellatif and Pierre Alquier. Consistency of variational bayes inference for estimation and model selection in mixtures. Electron. J. Stat., 12(2), Jan 2018.

- [15] Stephen E. Chick. Chapter 9 subjective probability and bayesian methodology. In Simulation, pages 225–257. Elsevier, 2006.

- [16] Leon Yang Chu, J.George Shanthikumar, and Zuo-Jun Max Shen. Solving operational statistics via a bayesian analysis. Oper. Res. Lett., 36(1):110–116, Jan 2008.

- [17] Yunxiao Deng, Junyi Liu, and Suvrajeet Sen. Coalescing data and decision sciences for analytics. In Recent Advances in Optimization and Modeling of Contemporary Problems, pages 20–49. INFORMS, 2018.

- [18] MD Donsker and SRS Varadhan. Asymptotic evaluation of certain markov process expectations for large time, ii. Commun. Pur. Appl. Math., 28(2):279–301, 1975.

- [19] MD Donsker and SRS Varadhan. Asymptotic evaluation of certain markov process expectations for large time—iii. Commun. Pur. Appl. Math., 29(4):389–461, 1976.

- [20] Monroe D Donsker and SR Srinivasa Varadhan. Asymptotic evaluation of certain markov process expectations for large time, i. Commun. Pur. Appl. Math., 28(1):1–47, 1975.

- [21] Monroe D Donsker and SR Srinivasa Varadhan. Asymptotic evaluation of certain markov process expectations for large time. iv. Commun. Pur. Appl. Math., 36(2):183–212, 1983.

- [22] Adam N Elmachtoub and Paul Grigas. Smart” predict, then optimize”. arXiv preprint arXiv:1710.08005, 2017.

- [23] Hans Föllmer and Thomas Knispel. Entropic risk measures: Coherence vs. convexity, model ambiguity and robust large deviations. Stoch. Dynam., 11(02n03):333–351, 2011.

- [24] Subhashis Ghosal, Jayanta K. Ghosh, and Aad W. van der Vaart. Convergence rates of posterior distributions. Ann. Stat., 28(2):500–531, 2000.

- [25] Alison L Gibbs and Francis Edward Su. On choosing and bounding probability metrics. Int. Stat. Rev., 70(3):419–435, 2002.

- [26] Manuel Gil, Fady Alajaji, and Tamas Linder. Rényi divergence measures for commonly used univariate continuous distributions. Inform. Sciences, 249:124–131, 2013.

- [27] Tito Homem-de Mello and Güzin Bayraksan. Monte carlo sampling-based methods for stochastic optimization. Surv. Oper. Res. Manage. Sci., 19(1):56–85, 2014.

- [28] Prateek Jaiswal, Harsha Honnappa, and Vinayak A. Rao. Asymptotic consistency of loss-calibrated variational bayes. Stat, 9(1), Jan 2020.

- [29] Prateek Jaiswal, Vinayak Rao, and Harsha Honnappa. Asymptotic consistency of -rényi-approximate posteriors. J Mach. Learn. Res., 21(156):1–42, 2020.

- [30] Jeremias Knoblauch. Frequentist consistency of generalized variational inference. arXiv preprint arXiv:1912.04946, 2019.

- [31] Tomasz Kuśmierczyk, Joseph Sakaya, and Arto Klami. Variational bayesian decision-making for continuous utilities. In Adv. Neur. In., pages 6395–6405, 2019.

- [32] Simon Lacoste-Julien, Ferenc Huszár, and Zoubin Ghahramani. Approximate inference for the loss-calibrated bayesian. In Int. Conf. Artif. Intell. Stat., pages 416–424, 2011.

- [33] Tze Leung Lai, Haipeng Xing, and Zehao Chen. Mean–variance portfolio optimization when means and covariances are unknown. Ann. Appl. Stat., 5(2A), Jun 2011.

- [34] Retsef Levi, Georgia Perakis, and Joline Uichanco. The data-driven newsvendor problem: new bounds and insights. Oper. Res., 63(6):1294–1306, 2015.

- [35] Yingzhen Li and Richard E Turner. Rényi divergence variational inference. In Adv. Neur. In., pages 1073–1081, 2016.

- [36] Liwan H Liyanage and J George Shanthikumar. A practical inventory control policy using operational statistics. Oper. Res. Lett., 33(4):341–348, 2005.

- [37] Mengshi Lu, J George Shanthikumar, and Zuo-Jun Max Shen. Technical note–operational statistics: Properties and the risk-averse case. Nav. Res. Log., 62(3):206–214, 2015.

- [38] Debdeep Pati, Anirban Bhattacharya, and Yun Yang. On statistical optimality of variational bayes. In Amos Storkey and Fernando Perez-Cruz, editors, Proceedings of the Twenty-First International Conference on Artificial Intelligence and Statistics, volume 84 of Proc. of Mach. Learn. Res., pages 1579–1588. PMLR, 09–11 Apr 2018.

- [39] G.Ch. Pflug. Stochastic optimization and statistical inference. In Stochastic Programming, volume 10 of Handbooks in Operations Research and Management Science, pages 427 – 482. Elsevier, 2003.

- [40] Minh Ha Quang. Regularized divergences between covariance operators and gaussian measures on hilbert spaces, 2019.

- [41] R Tyrrell Rockafellar. Coherent approaches to risk in optimization under uncertainty. In OR Tools and Applications: Glimpses of Future Technologies, pages 38–61. Informs, 2007.

- [42] Herbert Scarf. Bayes solutions of the statistical inventory problem. Ann. Math. Stat., 30(2):490–508, 1959.

- [43] Herbert E Scarf. Some remarks on bayes solutions to the inventory problem. Nav. Res. Log., 7(4):591–596, 1960.

- [44] Lorraine Schwartz. On bayes procedures. Z. Wahrscheinlichkeit., 4(1):10–26, Mar 1965.

- [45] A. M. Stuart. Inverse problems: A bayesian perspective. Acta Numer., 19:451–559, May 2010.

- [46] Ben Taskar, Vassil Chatalbashev, Daphne Koller, and Carlos Guestrin. Learning structured prediction models: A large margin approach. In Proceedings of the 22nd international conference on Machine learning, pages 896–903. ACM, 2005.

- [47] R. E. Turner and M. Sahani. Two problems with variational expectation maximisation for time-series models. Cambridge University Press, 2011.

- [48] A. W. van der Vaart and J. H. van Zanten. Rates of contraction of posterior distributions based on Gaussian process priors. Ann. Stat., 36(3):1435 – 1463, 2008.

- [49] Aad W Van der Vaart. Asymptotic statistics, volume 3. Cambridge university press, 2000.

- [50] Yixin Wang and David M. Blei. Frequentist consistency of variational bayes. J. Am. Stat. Assoc., pages 1–15, Jun 2018.

- [51] Bryan Wilder, Bistra Dilkina, and Milind Tambe. Melding the data-decisions pipeline: Decision-focused learning for combinatorial optimization. arXiv preprint arXiv:1809.05504, 2018.

- [52] Di Wu, Helin Zhu, and Enlu Zhou. A bayesian risk approach to data-driven stochastic optimization: Formulations and asymptotics. SIAM J. Optimiz., 28(2):1588–1612, 2018.

- [53] Yun Yang, Debdeep Pati, and Anirban Bhattacharya. -variational inference with statistical guarantees. Ann. Stat., 48(2):886 – 905, 2020.

- [54] Fengshuo Zhang and Chao Gao. Convergence rates of variational posterior distributions. Ann. Stat., 48(4), Aug 2020.

- [55] Enlu Zhou and Di Wu. Simulation optimization under input model uncertainty. In Advances in Modeling and Simulation, pages 219–247. Springer, 2017.

Appendix A Proofs

A.1 Alternative derivation of LCVB

We present the alternative derivation of LCVB. Consider the logarithm of the Bayes posterior risk,

| (A.1) |

where the inequality follows from an application of Jensen’s inequality (since, without loss of generality, for all and ), and . Then, it follows that

| (A.2) |

A.2 Proof of Theorem 4.1:

We prove our main result after series of important lemmas. For brevity we denote .

Lemma A.1.

For any , , and ,

| (A.3) |

Proof.

For any fixed , and , and using the fact that KL is non-negative, observe that the integral in the LHS of equation (A.3) satisfies,

Next, using the definition of in the second term of last equality, for any other

Finally, it follows from the definition of the posterior distribution that

| (A.4) |

where the last equality follows from adding and subtracting . Now taking expectation on either side of equation (A.4) and using Jensen’s inequality on the first and the last term in the RHS yields

| (A.5) |

where in the second term in RHS of (A.4), we first take infimum over all which upper bounds the second term in (A.4) and then take infimum over all , since the LHS does not depend on . ∎

Next, we state a technical result that is important in proving our next lemma.

Lemma A.2 (Lemma 6.4 of [54]).

Suppose random variable X satisfies

for all . Then for any ,

In the following result, we bound the first term on the RHS of equation (A.3). The arguments in the proof are essentially similar to Lemma 6.3 in [54]

Lemma A.3.

Proof.

First define the set

| (A.7) |

where set is defined in Assumption 3.3. We demonstrate that, under Assumption 3.3, is bounded above by an exponentially decreasing(in ) term. Note that for as defined in Assumption 3.3:

| (A.8) |

Let and use this in (A.8) for any to obtain,

Then, using the Chernoff’s inequality in the last equality above, we have

| (A.9) |

where the second inequality follows from first applying Jensen’s inequality (on the term inside ) and then using Fubini’s theorem, and the penultimate inequality follows from Assumption 3.3 and the definition of .

Next, define the set . Notice that set is the set of alternate hypothesis as defined in Assumption 3.1. We bound the calibrated posterior probability of this set to get a bound on the first term in the RHS of equation (A.3). Recall the sequence of test function from Assumption 3.1. Observe that

| (A.10) |

where in the second inequality, we first divide the second term over set and its complement, and then use the fact that . The third inequality is due the fact that . Next, using Assumption 3.3 and 3.5 observe that on set

Substituting the equation above in the third term of equation (A.10), we obtain

| () |

Now using Fubini’s theorem observe that,

where in the last inequality, we first divide the integral over set and its complement and then use the upper bound on in the first integral. Now, it follows that

where the second equality is obtained by dividing the first integral on set and its complement, and the second inequality is due the fact that . Now, using the equation above and Assumption 3.1, 3.2, and 3.4 observe that

Hence, choosing and such that implies

| (A.11) |

By Assumption 3.1, we have

| (A.12) |

Therefore, substituting equation (A.9), equation (A.11), and (A.12) into (A.10), we obtain

| (A.13) |

where . Using Fubini’s theorem, observe that the LHS in the equation (A.13) can be expressed as , where

Next, recall that the set . Applying Lemma A.2 above with , , , , and for , we obtain

| (A.14) |

∎

Further, we have another technical lemma, that will be crucial in proving the subsequent lemma that upper bounds the last term in the equation (A.3).

Lemma A.4.

Suppose a positive random variable X satisfies

for all , , and . Then,

Proof.

For any ,

Therefore, choosing ,

∎

Next, we establish the following bound on the last term in equation (A.3).

Proof.

Define the set

| (A.16) |

Using the set in equation (A.7), observe that the measure of the set , under the posterior distribution satisfies,

| (A.17) |

Now, the second term of equation (A.17) can be bounded as follows: recall Assumption 3.3 and the definition of set , both together imply that,

| () |

Then, using Fubini’s Theorem . Next, using the definition of set and then Assumption 3.4, we obtain

Hence, choosing the constants and such that implies

| (A.18) |

Therefore, substituting (A.9) and (A.18) into (A.17)

| (A.19) |

where . Using Fubini’s theorem, observe that the RHS in (A.19) can be expressed as , where the measure

Applying Lemma A.4 for , , , and , we obtain

| (A.20) |

∎

Proof.

Proof of Theorem 4.1: Finally, recall (A.3),

| (A.21) |

Substituting (A.15) and (A.6) into the equation above and then using the definition of , we get

where the last inequality uses the fact that . Choosing ,

| (A.22) |

where and depend on . Since the last two terms in (A.22) decrease and the first term increases as increases, we can choose large enough, such that for all

and therefore for ,

| (A.23) |

Also, observe that the LHS in the above equation is always positive, therefore and .

∎

A.3 Proof of Theorem 4.2 and 4.3

Lemma A.6.

Given and for a constant M, as defined in Theorem 4.1

| (A.24) |

Proof.

First, observe that

where the last inequality follows from Jensen’s inequality. Now, using the Jensen’s inequality again

Now, using Theorem 4.1 the result follows immediately.

∎

Proof of Theorem 4.2.

Observe that

| (A.25) |

It follows from above that the probability of the following event is at least :

| (A.27) |

∎

Proof of Theorem 4.3:.

Since, the result in Lemma A.6 holds for any , we fix . Now observe that for any and , the result in Lemma A.6 implies that the probability of

| (A.28) |

is at most . For , it follows from the definition of that

| (A.29) |

It follows from the inequality above that

| (A.30) |

Therefore, using the condition on the growth function in the statement of the theorem that, the probability of the following event is at least :

| (A.31) |

This concludes the proof.

∎

A.4 Proofs in Section 4.1

Proof of Proposition 4.1.

Using the definition of and the posterior distribution , observe that

Now, using Fubini’s in the last term of the equation above, we obtain

| (A.32) |

Observe that, . Since, KL is always non-negative, it follows from the equation above that

| (A.33) |

where the last inequality follows from the following fact, for any functions and ,

Recall . Now, using Assumption 4.1, it is straightforward to observe that the first term in (A.33),

| (A.34) |

Now consider the last term in (A.33). Notice that the coefficient of is independent of and is bounded from below. Therefore, there exist a constant , such that with equation (A.34) it follows that and the result follows.

∎

A.5 Sufficient conditions on for existence of tests

To show the existence of test functions, as required in Assumption 3.1, we will use the following result from [24, Theorem 7.1], that is applicable only to distance measures that are bounded above by the Hellinger distance.

Lemma A.7 (Theorem 7.1 of [24]).

Suppose that for some non-increasing function , some and for every ,

where is any distance measure bounded above by Hellinger distance. Then for every , there exists a test (depending on ) such that, for every ,

For the remaining part of this subsection we assume that . In the subsequent paragraph, we state further assumptions on the risk function to show as defined in (4.2) satisfies Assumption 3.1. For brevity we denote by , that is

| (A.37) |

and the covering number of the set as , where is the radius of each ball in the cover. We assume that the risk function satisfies the following bound.

Assumption A.1.

The model risk satisfies

where is the Hellinger distance between two models and .

For instance, suppose the definition of model risk is , where is an underlying loss function. Then, observe that Assumption A.1 is trivially satisfied if is bounded in for a given and is compact, since can be bounded by the total variation distance and total variation distance is bounded above by the Hellinger distance [25]. Under the assumption above it also follows that we can apply Lemma A.7 to the metric defined in (A.37). Now, we will also assume an additional regularity condition on the risk function.

Assumption A.2.

For every , there exists a constant such that

We can now show that the covering number of the set satisfies

Lemma A.8.

Given , and under Assumption A.2,

| (A.38) |

Proof of Lemma A.8:.

For any positive and , let . Now consider a set and with , where for and . Observe that for any , there exists a such that . Hence, union of the balls for each element in set covers , therefore .

Now, due to Assumption A.2, for any

For brevity, we denote by , that is

| (A.39) |

and the covering number of the set as , where is the radius of each ball in the cover.

Hence, -cover of set is cover of set with . Finally,

which implies for ,

∎

Observe that the RHS in (A.38) is a decreasing function of , infact for , it is a constant in . Therefore, using Lemmas A.7 and A.8, we show in the following result that in (4.2) satisfies Assumption 3.1.

Lemma A.9.

Proof of Lemma A.9:.

Recall and . Using Lemma A.8, observe that for every ,

Next, using Assumption A.1 we have

It follows from the above two observations and Lemma 2 that, for every , there exist tests such that

| (A.42) | ||||

| (A.43) |

where . Since the above two conditions hold for every , we can choose a constant such that for every

| (A.44) | ||||

| (A.45) |

where the second inequality in (A.44) holds , where Hence, the result follows for and . ∎

Corollary A.1.

A.6 Proof of Theorem 5.1, 5.2, and 5.3

Proof of Theorem 5.1:.

The proof follows immediately from Theorem 4.1 by taking limit on either side of its main result, that is

| (A.47) |

Fix . Now first consider the LHS, use the fact that for any , (5.1), the integrand is also non-negative , and due to Proposition 4.2 (since a decreasing sequence is bounded given ), therefore, using Fatou’s Lemma we have

| (A.48) |

On the other hand, using similar argument as used in (5.1) to show that as , it follows that

Thus the result follows.

∎

Next, we obtain a high-probability bound on the regret, defined as the uniform difference between the Naive VB approximate posterior risk and the expected loss under the true data generating measure .

Lemma A.10.

For a constant M as defined in Theorem 5.1

| (A.49) |

Proof.

The result follows immediately from the following inequalities

where the last inequality is a consequence of Jensens’ inequality. Now, using Jensen’s inequality again

Now the result follows immediately using Theorem 5.1. ∎

A.7 Proof of Theorem 5.4, 5.5 and 5.6

A.8 Newsvendor Problem

We fix . Next, we aim to show that the exponentially distributed model satisfies Assumption 3.1, for distance function . To show this, in the next result we first prove that satisfy Assumption A.1. Also, recall that the square of Hellinger distance between two exponential distributions with rate parameter and is

Lemma A.11.

For any , and ,

where and and lies in the interior of .

Proof.

Observe that for any ,

| (A.50) |

where the last inequality follows since for , and and vice versa if that together makes the last term in the penultimate equality negative for all . Moreover, the first derivative of the upperbound with respect to is

and it is negative when and positive when for all and . Therefore, the upperbound in (A.50) above is decreasing function of for all and increasing function of for all . The upperbound is tight at .