Nonparametric smoothing for extremal quantile regression with heavy tailed distributions

Abstract

In several different fields, there is interest in analyzing the upper or lower tail quantile of the underlying distribution rather than mean or center quantile. However, the investigation of the tail quantile is difficult because of data sparsity. In this paper, we attempt to develop nonparametric quantile regression for the extremal quantile level. In extremal quantile regression, there are two types of technical conditions of the order of convergence of the quantile level: intermediate order or extreme order. For the intermediate order quantile, the ordinary nonparametric estimator is used. On the other hand, for the extreme order quantile, we provide a new estimator by extrapolating the intermediate order quantile estimator. The performance of the estimator is guaranteed by asymptotic theory and extreme value theory. As a result, we show the asymptotic normality and the rate of convergence of the nonparametric quantile regression estimator for both intermediate and extreme order quantiles. A simulation is presented to confirm the behavior of the proposed estimator. The data application is also assessed.

Keywords: Asymptotic normality; Extrapolation; Extremal quantile regression; Extreme value theory; Nonparametric estimator

MSC codes: 62G08, 62G20, 62G32

1 Introduction

In a wide variety of areas, such as in the study of heavy rainfall, low birth weight, and high-risk finance, the tail behavior of the distribution of the target variable is of interest rather than the average or median. In these cases, we often investigate the upper or lower quantile of the data. However, the estimation of the tail quantile is difficult because of data sparsity. Therefore, the development of the mathematical properties of the tail quantile would be welcome. The theoretical performance of the tail behavior of the distribution function is provided by extreme value theory (EVT). The fundamental properties of EVT were surveyed by Coles (2001), Beirlant et al. (2004a), and de Haan and Ferreira (2006). On the other hand, the performance of the estimator is often guaranteed by a large sample or asymptotic theory in statistics. Thus, the mathematical properties of the estimator of the tail quantile are analyzed using a hybrid of EVT and asymptotic theory. In many cases, it is important to research the target variable along with the information of other variable. Then we should analyze the data in the literature of regression. In this paper, we consider the estimation of the extremal conditional quantile of the response given .

Many researchers have developed the extremal conditional quantile estimation. Beirlant and Goegebeur (2004) developed a Pareto distribution approach. Gardes et al. (2010) and Gardes and Girard (2010) studied the nearest-neighbor estimation. Daouia et al. (2011, 2013), El Methni et al. (2014), and Girard and Louhichi (2015) investigated the extremal quantile of the nonparametric estimator of the conditional distribution function of given . The local-moment-type methods were studied by Goegebeur et al. (2017). Durrieu et al. (2015) have developed the weighted quasi-log-likelihood method. On the other hand, quantile regression, which was pioneered by Koenker and Bassett (1978), is a typical approach used to investigate the conditional quantile. For the center quantile, several authors have developed quantile regression methods. These fundamental developments have been summarized by Koenker (2005). However, much less work has been done on quantile regression for the extremal quantile. Chernozhukov (2005), Chernozhukov and Fernández-val (2011), Wang et al. (2012), and He et al. (2016) studied extremal quantile regression, but they focused only on linear models. For the tail quantile, the linear structure assumption is strong and its assumption is violated in several cases. Therefore, a nonparametric approach should be used in extremal quantile regression in such situations. Beirlant et al. (2004b) studied extremal nonparametric quantile regression, but the theoretical property was not investigated. In this paper, we develop nonparametric quantile regression for the extremal quantile and mathematical properties.

Before we describe our study, we review extremal quantile regression with linear models in more detail. For extremal quantile regression, the quantile level approaches 0 or 1 as the sample size increases. This paper treats only the upper quantile and, hence, as . Thus, there are two important types of the order of : the intermediate order quantile and the extreme order quantile. The former means that and as , whereas in the latter and as . If is fixed, it is the so-called center quantile. According to Chernozhukov (2005) and Chernozhukov and Fernández-val (2011), the quantile regression estimator with linear models has asymptotic normality for the intermediate order quantile but it converges to a non-degenerated distribution (not normal) for the extreme order quantile. Thus, the extreme order quantile is difficult to handle. Wang et al. (2012) provided a nice approach to obtain the extreme order quantile estimator by extrapolation from the intermediate order quantile estimator. As a result, this extrapolated estimator has asymptotic normality. It seems that above results should be extended to the nonparametric quantile regression for many applications.

In this paper, we first construct the ordinary nonparametric estimator for the intermediate order quantile. We then use the -spline method with penalty. This approach was originally considered by O’Sullivan (1986) and Eilers and Marx (1996) in mean regression. Pratesi et al. (2009), Reiss and Huang (2012), and Yoshida (2013) used the quantile regression for only the center quantile. We show the asymptotic bias and variance as well as the asymptotic normality of the penalized spline estimator. Next, the extrapolated estimator is obtained for the extreme order quantile. Similar to the approach of Wang et al. (2012), we use the Weissman-type extrapolation method (see Weissman 1978). The asymptotic normality and the optimal rate of convergence of the extreme order quantile estimator are shown. To the best of our knowledge, this is the first time that the rate of convergence of the nonparametric estimator is revealed in the extremal quantile regression.

This paper is organized as follows. In Section 2, we coordinate the conditions of the true conditional quantile by EVT in nonparametric extremal quantile regression. Section 3 presents the nonparametric estimator and its asymptotic property for both intermediate and extreme order quantiles. In Section 4 the Monte Carlo simulation is conducted to confirm the performance of the proposed estimator. Section 5 addresses the application to Beijing’s pollution data. The conclusions and future research are described in Section 6. In the Appendix, the computational aspects of the penalized spline estimator and the proofs of the mathematical results that appear in this paper are presented. Throughout the paper and without loss of generality, we focus on the conditional high quantile because a low quantile of the response can be viewed as a high quantile of the inverted sign of the response.

2 Conditional extremal quantiles

2.1 Extreme value theory

Let be the independent copies of a random pair . We assume that the support of is bounded on , where . The conditional distribution function of given is denoted by . Then the conditional quantile of given is

The main purpose of this study is to estimate for a high quantile level . The tail behavior of the distribution or quantile function can be characterized by EVT. To analyze the conditional high quantile of given , we introduce the EVT conditions of and . We first provide the error to incorporate the stochastic structure of given . Here, we assume that is independent to predictor . Define and as the marginal distribution function and quantile of . Throughout the paper, we assume that and belong to the maximum domain of attraction of an extreme value distribution , denoted by . The distribution function belongs to the maximum domain of attraction, which means that for the random sample from , there exists a constant and such that for ,

as . Here, is the extreme value index (EVI). The EVI is very important since this generally controls the tail behavior of the distribution function. For , if or , has a light tail or short tail. When , has a heavy tail. This paper only discusses the heavy-tail case and, hence, we assume that from now on. The maximum domain of attraction is a very weak condition. For example, uniform, beta, Gaussian, , Pareto, Cauchy, and many other distributions belong to the maximum domain of attraction with appropriately specified . The details of the maximum domain of attraction and EVI are given in fundamental books such as that by de Haan and Ferreira (2006).

We now state the conditions to connect the tail behavior of and . For this, we need an additional definition. Let be the set of regularly varying functions, where . When , is the so-called slowly varying function.

Conditions A

-

A1.

For the error , there exists such that the distribution function satisfies as .

-

A2.

We have regularly varying at 0 with index . That is, for ,

-

A3.

For and , there exists an auxiliary function such that has the distribution function satisfying, as ,

where is a positive, continuous, and bounded function on and has .

-

A4.

For , uniformly in as .

Conditions A may not hold if either or is not included in . In other words, if , Conditions A are natural. Condition A1 is the formal notation of a Pareto-type tail (see Chernozhukov and Fernández-val 2011). The equivalent to condition A1 is

| (1) |

with . Therefore, if the distribution is continuous and as , condition A2 holds from condition A1. Actually, as . Therefore, we have . Thus, condition A2 is weak. Condition A3 provides the extremely location-scale shifted model having the Pareto-type conditional quantile tail of given along with an auxiliary function . Actually, it it easy to show from A3 that as . Furthermore, since , we obtain . Consequently, we have

| (2) |

where . Chernozhukov (2005), Chernozhukov and Fernández-val (2011) and Wang et al. (2012) also provided this type of condition in multiple linear models. That is, they further assumed that and for , where and are unknown -dimensional parameter vectors. Thus, A3 is the nonparametric model version of the above previous studies. Condition A4 guarantees the existence of a conditional quantile density function (the derivative of the quantile function). Furthermore, the conditional quantile density function also behaves like a Pareto-type function by condition A4. Assumption A3 is strengthened by condition A4.

Remark 1. Let and let . In several articles (see, for example, de Haan and Ferreira 2006), the conditions of EVT are applied to and as . Since , the condition (1) is similar to with . Condition A4 can also be expressed as with . Thus, we can reconsider the EVT conditions for quantiles by using and . In particular, the use of is appropriate when using the second-order condition of EVT (see Section 3.2).

2.2 -spline model

The conditional quantile can be written as

| (3) |

where is Koenker’s check function (Koenker 2005) and is the indicator function. The estimator of is often obtained along with an empirical version of (3). To estimate , we use the -spline regression method as the nonparametric technique in this paper. Let be the th degree of the -spline basis with knots . In addition, other sets of knots are defined as and . We then define the -spline model as

where and is an unknown parameter vector. We now describe the relationship between the -spline model and EVT discussed in the previous section. Let be the th-order Sobolev space. From Barrow and Smith (1978), for any function , there exists such that as , where . For simplicity, we assume that , that is . Actually, is the standard condition of -spline smoothing.

For , let

and let . We then found that for . If , Conditions A and (2) yield that and, hence, as and , which indicates that the condition B4 below is required.

If and defined in (2) belong to , there exists such that and . We then obtain as and . Therefore, (1) and condition A4 indicate that is satisfied since and are not dependent on . Thus, the -spline model also holds (2) and condition A4 and, hence, the tail behavior of the -spline model can be studied by using Conditions A. The following conditions are the fundamental assumptions for -spline regression.

Conditions B

-

B1.

For some constant , .

-

B2.

The functions and in (2) are included in .

-

B3.

We have .

-

B4.

For some , the number of knots .

-

B5.

As and , .

Condition B1 is needed to that the estimator satisfies the Lyapunov condition of central limit theorem. When condition B2 holds, the -spline model can approximate to . Conditions B3 and B4 are standard conditions for -spline models. Together with condition B2, the -spline model and EVT are connected for high quantile level. Condition B5 guarantees that the model bias between the conditional quantile and -spline model converges to 0.

3 Penalized -spline estimator for extremal quantiles

In this section, we define the nonparametric -spline estimator and develop the asymptotic result. Then, we consider two scenario of extremal quantile rate: (i) intermediate order quantiles that and as and (ii) extreme order quantiles that and as . We denote the intermediate order quantile level by and the extreme order quantile level by , respectively. That is, as , , , , and .

3.1 Estimation of intermediate order quantiles

The ordinary -spline quantile estimator for is defined based on minimizing . However, it is known that the ordinary estimator tends to have a wiggly curve caused by data sparsity. To avoid this, we introduce the penalization method to control the behavior of the estimator. Although various types of penalties have been developed to prevent overfitting, we will use O’Sullivan’s (1986) penalty. For , the penalized spline estimator of vector is constructed by minimizing

| (4) |

where is the smoothing parameter. Using , for the intermediate order quantile level , we define

We study the asymptotic theory for the penalized spline estimator . Then, the conditions of the number of knots and the smoothing parameter included in are very important. The penalty can be written as , where the -matrix has elements and the matrix satisfies , where , and for

From now on, we use the symbols and . Let be the -matrix with elements and

Let be with . Define

which controls the asymptotic scenario branch discussed in Remark 1 below.

Conditions C

-

C1.

We have .

-

C2.

We have as .

-

C3.

We have as .

Condition C concerns with the asymptotic property of the penalized spline estimator. C1 is detailed in Remark 2. C2 allows us to use the large . If C3 fails, the asymptotic bias of the penalized spline estimator cannot be vanished. We now show the asymptotic distribution of . First, we derive the two types of bias, model bias and shrinkage bias. Roughly speaking, the model bias is the bias between the -spline model and the true function, and the shrinkage bias is the difference between the expectation of the penalized estimator and the unpenalized estimator. According to Section 2,2, the model bias is . This model bias becomes the negligible order from condition C2. That is, the bias is dominated by the shrinkage bias. Define

As a result, is the asymptotic shrinkage bias and is the asymptotic variance of . The following theorem shows the asymptotic order of the asymptotic bias and variance of the intermediate order quantile estimator.

Theorem 1.

Under Conditions A–C, as ,

From condition C3 and Theorem 1, we see that the shrinkage bias and variance converge to 0 as . Using the central limit theorem, Lyapunov’s condition, and a Cramér–Wold device, the asymptotic normality of the estimator can be shown.

Theorem 2.

Suppose that Conditions A–C hold. As , and are the asymptotic bias and variance of and

Furthermore, under , the optimal rate of convergence of the mean integrated squared error (MISE) of is

Theorems 1 and 2 yield that the trade-off between bias and variance is controlled by . Thus, this indicates that the careful choice of is not important in the penalized spline methods. According to Yoshida (2013), for the center quantile level , the MISE of the penalized spline quantile estimator has the order . Thus, the rate of convergence of the MISE of the penalized spline estimator for the intermediate quantile level is slower than that for the center quantile level. This result is not surprising in the context of the difficulties of the estimation for the tail quantile.

When and , the estimator is reduced to the ordinary quantile regression with the linear model. In the linear regression, the model bias is 0 and, hence, the bias term vanishes. On the other hand, since and , the asymptotic variance becomes

which is similar in form to the asymptotic variance of the linear estimator of Lemma 3 of Wang et al. (2012). Then, the rate of convergence of the MISE of the linear estimator is . Thus, it can be considered that Theorem 2 is the generalization of the asymptotic result of the linear-type parametric estimator.

Remark 2. Claeskens et al. (2009) have studied the asymptotic properties of the penalized spline mean estimator in two scenarios: roughly speaking, case (a) small scenario and case (b) large scenario. In case (a), the asymptotic behavior of penalized splines is similar to that of regression splines, which have the unpenalized estimator (). Case (b) results in the penalized splines nearing the smoothing splines. We briefly describe the asymptotic scenario branch along with the result of Claeskens et al. (2009). The penalized spline mean estimator is obtained as , where is the design matrix and . Then, the two asymptotic scenarios are divided by the asymptotic order of the maximum eigenvalue of , which is obtained as

If for a sufficiently large , , and , we achieve case (a). When for a sufficiently large , , and , we achieve case (b). Although Claeskens et al. (2009) focused only on mean regression, these two scenarios can also be discussed with respect to quantile regression. The asymptotic scenario branch discussed in this section is dependent on the asymptotic order of . Similar to Claeskens et al. (2009), the order of the maximum eigenvalue of can be obtained as , which corresponds to in mean regression. Consequently, condition C1 indicates that the large scenario should be studied. We finally note why we focus on the large scenario. Ruppert (2002) recommended that one should first set the knots with a large to obtain the overfitted estimator and control to achieve smoothness and fitness. Therefore, the large scenario matches the concept of Ruppert (2002) and this motivates us to consider the large scenario.

3.2 Estimation of extreme order quantiles

For the extreme order quantile, the estimator discussed in the previous section would not have asymptotic normality (Chernozhukov 2011). In this paper, we try to approximate the extreme conditional quantile from intermediate quantile. According to Weissman (1978), the following holds:

From this, using the estimator of the intermediate order quantile , we define the extrapolated estimator of the extreme order quantile. To achieve this, we need to estimate the EVI .

Let be the sequence of quantile levels, where , and is the integer part of . Then, since as , all are intermediate order quantiles. Using this sequence, we define the Hill-types estimator of as

In this paper, we assume that the tail behavior of and are equivalent (see, Condition A1). Therefore, it is somewhat unnatural that the estimator of varies with . Nevertheless, we define the extrapolated estimator with and investigate the mathematical property. For , using , we define the estimator of the extreme order quantile as

We next consider the EVI estimator along with condition A1. Define the common index (pooled) estimator

and the extrapolated estimator with common index estimator as

To investigate the asymptotic distribution of and , we impose the second-order condition in Conditions A.

-

A5

The function satisfies the second-order condition with . That is, there exist and such that as ,

Furthermore, with .

-

There exist and positive, continuous and bounded function such that as ,

Condition A5 is the standard second-order condition of EVT and is detailed in de Haan and Ferreira (2006). Condition provides the second order of tail behavior of . From conditions A5 and , we see that also satisfy the second-order condition with and with , which were proven in Lemma 2 of Wang et al. (2012). Using this, we show the asymptotic property of the Hill-type estimator of the EVI in the following.

Theorem 3.

Suppose that the smoothing parameter included in satisfies . Furthermore, suppose that , and as . Under Conditions A–C, as ,

and

where and are defined in (11) of Appendix and have an asymptotic order . Furthermore,

and

Using Theorem 3, we obtain the asymptotic normality of the ratio of and .

Theorem 4.

For the asymptotic order in Theorem 4, the term is derived from and the another term is derived from . If we use or , we have since . That is, the asymptotic inference of is dominated by that of and hence, the rate of convergence of the estimator is

One may have sense of discomfort with this result since the extreme order quantile estimator and the intermediate order quantile estimator has same rate of convergence. Indeed, the leading terms of and are similar. However, the convergence speed of the subsequent term of is obviously slower than that of because of the influence of . Therefore, for the application with a finite sample, the behavior of would be more stable than . On the other hand, when or , which leads to , is adopted, is heavily affected by but not by . Actually, since and , we have

For the common index quantile estimator with , the asymptotic order of are dominated by the term of , and this do not vary with . This result is quite unnatural in the quantile regression although , which is the difference between the asymptotic inference of and , is quite small. Therefore, if the common index quantile estimator is mainly used, we may have to choose the baseline quantile so that . Thus, the balance of and controls the asymptotic behavior of . The same is true of .

Wang et al. (2012) obtained the extrapolated estimator in the linear model with . From their result, the rate of convergence of the MISE of the linear estimator is . That is, the difference in the rate of convergence between the parametric estimator and the nonparametric estimator is and , which could be intuitively derived from the classical works on parametric and nonparametric regression.

Remark 3

The intermediate order quantile and the extreme order quantile are separated mathematically by the rate of the quantile level. However, in data analysis, the distinction between these two rates should be drawn for fixed . Define . Using , Chernozhukov and Fernández-val (2011) suggested the following rule of thumb. For the quantile level , if , it is the extreme order inference, that is, and we should use . When , it is sufficient to use the intermediate order quantile estimator . If the predictor is the continuous, this threshold is –20. However, they noted that the above rule is conservative. In this paper, we treat as the intermediate order quantile. For example, when , leads to . Then, we have . For , and correspond to . On the other hand, Wang et al. (2012) suggested to use . In their rule, we have for . Thus, it seems that the rule of Chernozhukov and Fernández-val (2011) is more conservative rather than that of Wang et al. (2012). In our experience, the rule of Wang et al. (2012) worked well for . Therefore, in the simulation study of the next section, we also use . However, the determination of the split of the intermediate order and the extreme order is still a difficult problem and further study would be welcomed.

4 Simulation

The practical performance of the proposed estimator is confirmed by Monte Carlo simulation. Define the true regression model as

| (5) |

where

and . The predictor is independently generated from the standard uniform distribution. This setting was introduced by Daouia et al. (2013). We consider two types of error distribution: (a) and (b) , where

The error type (b) is also used by Daouia et al. (2013). For the distribution, the EVI is and hence, and for (a) and (b), respectively For both cases, the EVI is larger than 0, which indicates that the distribution of has a heavy tail. In (5), the conditional th quantile of given is , where is the th quantile of . For the case (a), is the th quantile of and is not dependent on . Thus, the model (5) with (a) is the location-scale shifted model and is of the form of (2). In the case of (b), for and otherwise. That is, the model (5) with (b) has high EVI at the center and low (but larger than 0) EVI at the boundary. The conditional quantile with (b) fail due to Conditions A. However, it is important to confirm the performance of the estimator under (b).

We construct the intermediate order quantile estimator , the Hill-type estimator , and the extreme order quantile estimator and . For the intermediate order quantile estimator, we use the number of knots and the smoothing parameter selected via generalized approximated cross-validation (Yuan 2006). To obtain , , and , we need to determine (). In this simulation, is chosen so that and . Such and are selected from a pilot study. Wang et al. (2012) used and in the linear regression. Thus, our is somewhat larger than that of Wang et al. (2012).

For the estimator of the true function , the Mean Integrated Squared Error (MISE):

is used as the accuracy measure of the estimator. We calculate the estimated MISE of , and over 400 replications. The estimators , and are denoted by PSE-I, PSE-E and PSE-Ep. As the competitors, we consider the functional nonparametric estimator (Gardes et al. 2010) and the kernel smoothing estimator (Daouia et al. 2013). The estimators and defined in Gardes et al. (2010) are denoted by FNS-I and FNS-E, respectively. Furthermore, the estimators and defined by Daouia et al. (2013) are labeled by KSE-I and KSE-E in this section. Thus, FNS-I, FNS-E, KSE-I and KSE-E are also demonstrated in simulation.

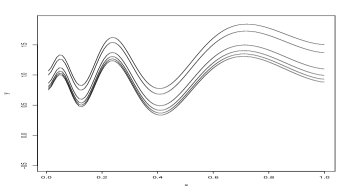

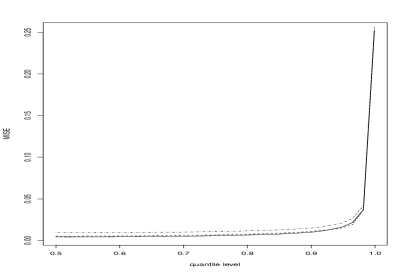

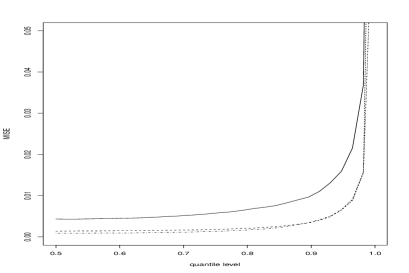

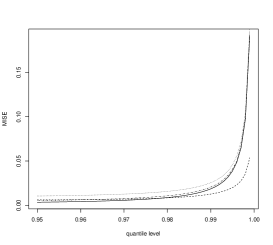

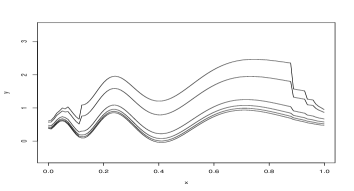

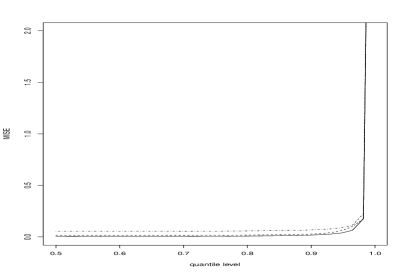

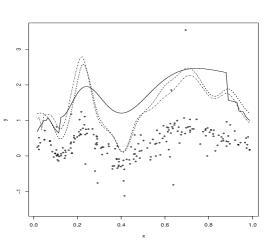

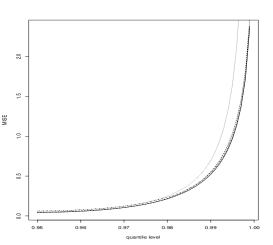

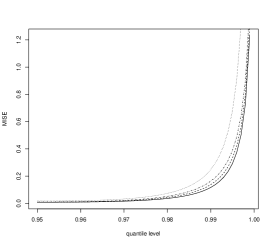

We report the simulation results for the case (a). Figure 1 shows the true conditional quantiles and the intermediate order quantile estimators for one dataset with and 1000. For and 0.9, the estimator behaved well, but for , there was a significant difference between the true function and the intermediate order quantile estimator. In Figure 2, the MISEs of the estimators for are illustrated. We can observe that the proposed estimator behaves better than the competitors. From Figure 2 (d), we can find that the estimator behaves well as increases. This indicates that the estimator has a consistency property. However, as increases, the performance of the estimator becomes drastically decreases. Therefore, for , it is difficult to predict the conditional quantile using the intermediate order quantile estimator.

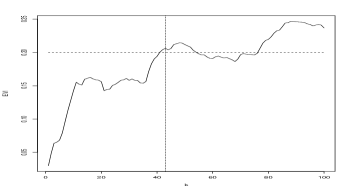

We next show the performance of the EVI estimator. Figure 3 shows the behavior of over for one dataset and the distribution of using by Monte Carlo simulation. From the results, we see that the suggested is good choice. When , the behavior of is stable from (c) and (d).

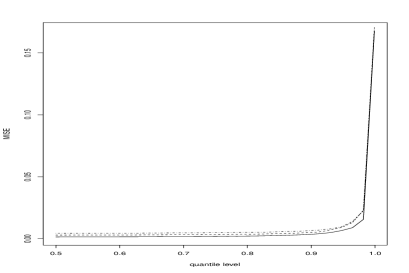

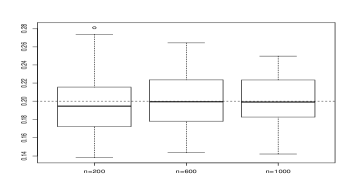

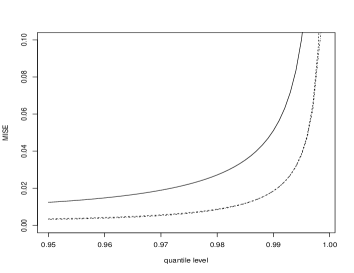

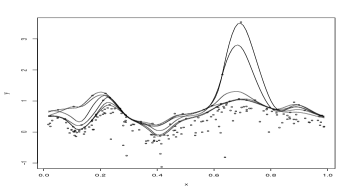

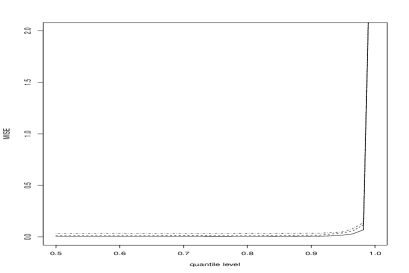

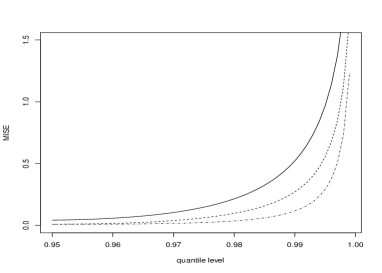

Figure 4 shows the extreme order quantile estimators PSE-E and PSE-Ep for one dataset and the MISE of the extreme order quantile estimators for . From (a–c), we can observe that the estimator behaves well. We can see that the behavior of the PSE-Ep is stable than the PSE-E. This is not a surprising result since the estimator of EVI included in PSE-Ep is not dependent on unlike PSE-E. It can be recognized from Figure 4 (d–f) that the proposed estimator has better behavior than the competitors although the differences are not large. Furthermore, the performance of the PSE-Ep was superior to that of PSE-E. We think that this is a result of the stability of . It can be recognized from Figure 5 that the extrapolated estimator has consistency.

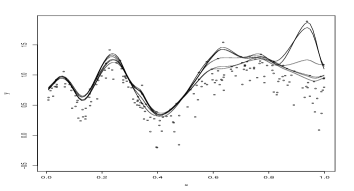

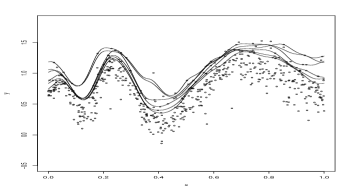

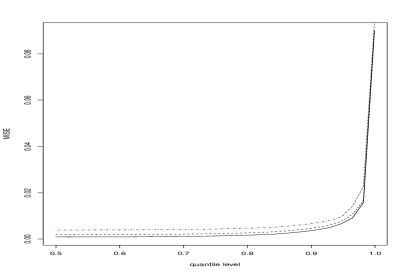

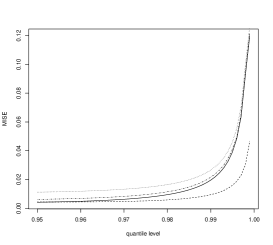

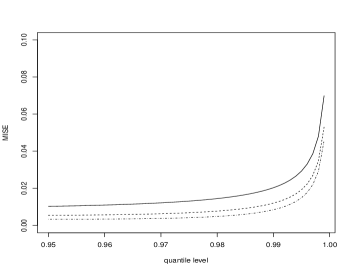

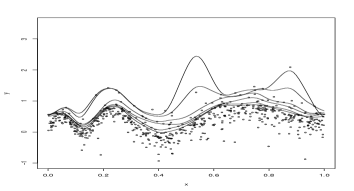

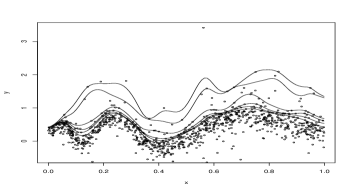

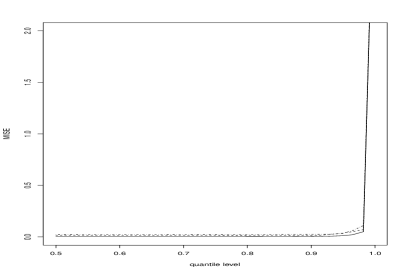

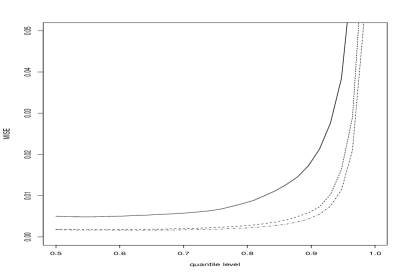

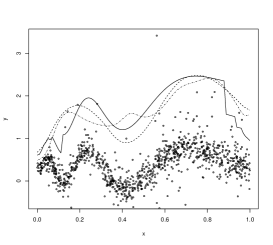

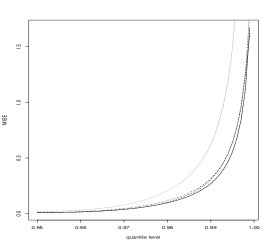

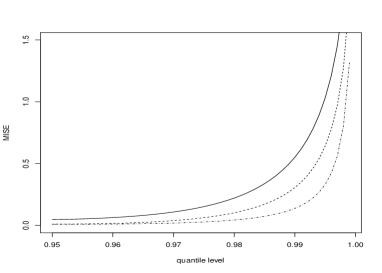

From now on, we describe the simulation results for the model (b). Figure 6 shows the true conditional quantiles and the intermediate order quantile estimators for for one dataset. It appears that for , the estimator can capture the true conditional quantile even for . However, for , the estimator has a wiggly curve. In Figure 7, the results of MISE of the intermediate order quantile estimators for each are illustrated. We found that the proposed estimator performs well for . However, the MISE drastically grows as increases. The behaviors of PSE-E and PSE-Ep for one dataset are described in Figure 8 (a–c). It can be seen from Figures 6 and 8 (a–c) that the PSE-E and PSE-Ep performed better than PSE-I. Figure 8 (d)–(f) shows the MISE of the extreme order quantile estimators. It can be confirmed that the performance of PSE-E is slightly better than that of PSE-Ep. We see that the proposed estimators have better behavior than the competitors. Figure 9, the consistency of the PSE-E and the PSE-Ep can be observed in numerically. Although the performance of the proposed estimator is drastically superior to that of Daouia et al. (2013), this simulation result indicates that our method is one of useful tools to the problem of extremal quantile regression.

5 Data example

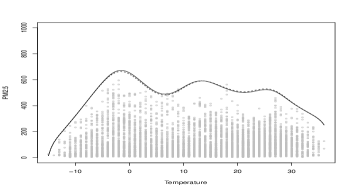

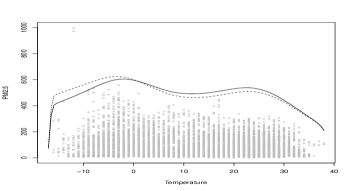

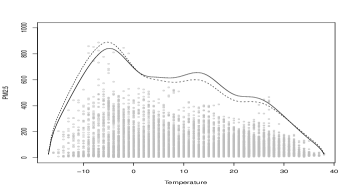

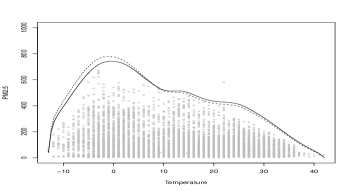

In this section, we apply the proposed methods to Beijing’s Pollution data. The data is available from the website of the UCI Machine Learning Repository and Liang et al. (2016) provided several analyses for this data. One of fundamental purposes of this data is to analyze the relationship between concentration and other meteorological variables. Our particular interest here is the prediction of high conditional quantiles of , concentration (), with the predictor , temperature (degrees Celsius). We can observe from the scatter plot of and (see Figure 10) that this relationship is not linear for the upper quantile. Therefore, the nonparametric approach is suitable for this data. We demonstrate the analysis for each year from 2011 to 2014. We then omit the missing data and hence the sample size is , 8295, , and 8661 in 2011, 2012, 2013, and 2014. We construct the extreme order quantile estimator for . The quantile level indicates that about only eight events occur each year.

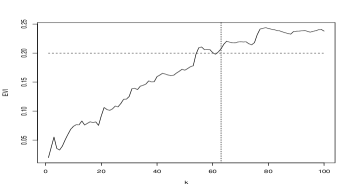

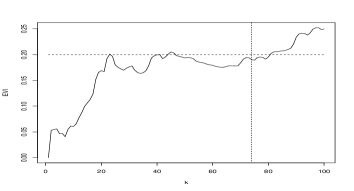

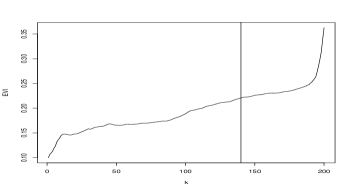

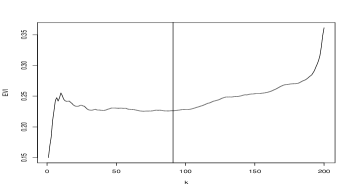

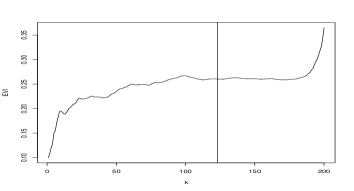

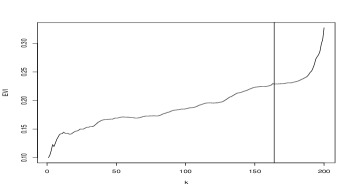

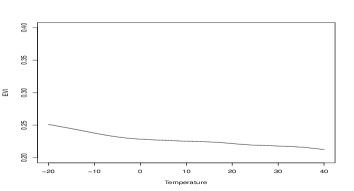

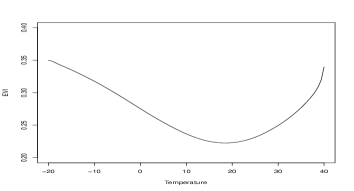

Figure 10 shows the extreme order quantile estimators for . It seems that the tail behavior is stable in 2011 and 2012. In 2013 and 2014, the estimator of the conditional quantile at has a large value compared with those in 2011 and 2012. Thus, in the cold season of 2013 and 2014, the risk of of pollution was increased. We can observe that and are quite similar. This indicates that the estimator of EVI hardly changes with . We report the EVI estimator used for constructing the extrapolated estimator and . To obtain the estimator of EVI, we utilized as so that about . Then, EVI is estimated by using the intermediate order quantiles estimators for . This choice leads to and, hence, this is a very conservative situation in the study of Chernozhukov and Fernández-val (2011). Furthermore, we then adopted to use so that the sample path of the pooled EVI estimator is stable in each year. Figure 11 shows the sample path of and selected . As a result, , 0.226, , and 0.231 in 2011, 2012, 2013, and 2014. Thus, the pooled EVI estimators are the same in 2011, 2012, and 2014, and it is only slightly larger in 2013.

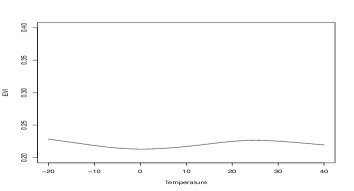

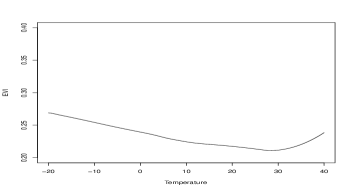

Figure 12 illustrates with selected for each year. We can observe that has a narrow curve with in 2011, 2012, and 2014. On the other hand, in 2013, at the boundary is rather larger than at the center. Indeed, it can be seen from Figure 10 that the extreme point can be observed at in 2013.

6 Conclusion

We have developed the nonparametric extremal quantile regression methods for heavy-tailed data. To show the mathematical property of the proposed estimator, we have used the hybrid techniques of asymptotic theory for the nonparametric regression and EVT for the tail behavior of the conditional distribution. We then considered two quantile rates: (i) the intermediate order quantile that as ; and (ii) the extreme order quantile that . For the intermediate order quantile, the penalized spline estimator and its asymptotic normality have been developed. On the other hand, for the extremal order quantile, we have studied the Weissman-type extrapolated estimator using the intermediate order quantile estimator and its asymptotic normality. For the both intermediate and extreme order quantile, we show the asymptotic normality and the optimal rate of convergence of the proposed estimator. In particular, we found that the convergence speed of the estimator for extremal quantile is slower than that for center quantile. This result would be intuitively correct.

We now discuss some future directions of study. First, for technical reasons, we assumed that the tail behavior of the conditional distribution of given is equivalent across the predictor (see Conditions A1). Since the estimation of the tail behavior is difficult due to data sparsity, this assumption is helpful in data analysis. However, if this assumption is violated, additional research is needed to explicate the performance of the estimator.

Second, in this paper, we focused on the spline smoothing with penalty. On the other hand, Koenker et al. (1994) and Koenker (2011) studied the smoothing spline with the -type penalty. That is, the penalty is defined as instead of . It is known that the estimator with penalty has local adaptiveness. Therefore, for some cases, the performance of the estimator with penalty would be better than that with penalty. Recently, the -type penalty has been rapidly developed in mean regression (Kim et al. 2009; Tibshirani 2014; Sadhanala and Tibshirani 2017). Although it is difficult to show the asymptotic distribution of an penalized estimator, the developments of the penalized smoothing to the extremal quantile regression is an interesting problem.

Finally, we can consider extending the proposed method to the multidimensional case. In particular, it is important to use the additive models (Hastie and Tibshirani 1990) that for , the true function is can be decomposed as

where each is the univariate function. The additive model is known to enables us to avoid the problem of dimensionality. The nonparametric additive quantile regression (for center quantile) was studied by Lu and Yu (2004), Horowitz and Lee (2005), Cheng et al. (2011), Koenker (2011), Lee et al. (2012) and references therein. However, the extremal inference of the additive quantile regression has not yet been studied until now. It seems that the developments of the extremal quantile regression with the additive model is an important issue.

Appendix

Appendix A: Computation of the intermediate order quantile estimator

We describe here the approximation algorithm to solve (4). Nychka et al. (1995) and Reiss and Huang (2012) proposed the penalized iteratively reweighted least squares algorithm. We use here the modified version of Nychka et al. (1995). Nychka et al. (1995) proposed the following optimization:

| (6) |

where

Obviously, the loss function tends to as . However, for the tail quantile (), the above algorithm will not converge in our implementation. Therefore, we suggest using the slightly modified version of (6). The idea is similar to the proximal gradient method and it is very simple. The modified algorithm is defined as given the th iteration estimate ,

| (7) |

where and are the step sizes. For , it is sufficient to use some sequence satisfying as . On the other hand, the choice of is more important than . If is large, and hence the speed of convergence is very fast. When is small, on the other hand, there is almost no difference between (7) and (6), that is, the algorithm does not converge in many cases. In Sections 4 and 5, we used and .

Appendix B: Proof of theorems

Let be the design matrix having elements , and let . For any matrix , we denote . We first state the technical lemmas to prove theorems in this paper.

Lemma 1.

Suppose that . Under Conditions A–C, the following statements holds: , , , , and .

Lemma 2.

Suppose that . Under Assumptions 2–3, for any square matrix satisfying for , and .

Lemma 1 is proved by Lemma 6.3 and 6.4 of Zhou et al. (1998) and Lemma A1 and A2 of Claeskens et al. (2009). Lemma 2 says that the order of product of matrices is dependent only on the order of element of these matrices although the each element of and is infinite sum as . The proof of Lemma 2 can also be shown by Lemma A1 of Claeskens et al. (2009). Therefore, we only describe the outline here.

Proof of Lemma 2.

For any continuous and bounded function , the matrix is the band matrix from property of -splines and hence is obvious. Next, is the inverse of the band matrix. From Demko (1977), there exists and such that . Thus, straightforward calculation yields that the infinite sum of each element of is bounded by order of and the absolute of the maximum of element of .

∎

Proof of Theorem 1.

Define . We write and hence and as . By the fundamental property of -spline basis, can be written as , where is the vector having element and ’s are th degree -spline bases. Therefore, the shrinkage bias can be expressed as

From Conditions A–B, we have and as . Since is bounded function, we get . From the property of -spline basis, we also obtain . Thus, each element of has the order Furthermore, the result of Cardot (2000) provides . Therefore, Lemmas 1, 2 and the fact that yield that

Next, we show the asymptotic order of . Since , from Lemmas 1–2, we have

which completes the proof. ∎

Proof of Theorem 2.

We write and hence and as . Let , and

Then the minimizer of is obtained as

Using Knight’s identity (Knight, 1998), we have

and writing

where

Since and , we obtain . The variance of can be evaluated as

as and . Lyapnov’s condition for the central limit theorem and Cramr-Wold device yield that is asymptotically distributed as , which is the normal with mean and variance .

Next, we show that as and ,

| (8) |

Before that, we provide some differential results. Let and be the marginal density of and conditional density of given , respectively. From A3, as . In addition, since , we have . Meanwhile, A4 and yield that . Consequently, as ,

Furthermore, by ,

We return to show (8). Since

we obtain

From the simple but tedious calculation, can be evaluated. These results yield that

Thus, is asymptotically equivalent to

By the convexity lemma (see, Pollard, 1991 and Knight, 1998), the minimizer of and are asymptotically equivalent and hence we have

Since , we obtain from that

| (9) |

The second term of right hand side of (9) is the shrinkage bias. Consequently, as ,

Finally, we obtain

| (10) | |||||

We now derive the optimal rate of convergence of MISE of . For the constant , the solution of

is for . By applying this in (10), we obtain

which completes the proof. ∎

To improve the outlook, we now describe about the asymptotic bias and variance of before prove Theorem 3. Define

| (11) |

where

As the result, and are the asymptotic bias and standard deviation of . We here get the asymptotic order of and from easy calculation.

Since and each element of has , we have

and

We then have from that

and

This indicates that and .

Proof of Theorem 3.

Theorem 1 indicates that as . Therefore, the proposed estimator can be calculated as for ,

We then note that is not random variable. Similar to the proof of Theorem 2.3 of Wang et al. (2012), we have as ,

for . Next, we consider . Under the conditions for Theorem 3, using the result of Theorems 1–2 and the property of -spline basis, we have

where . Therefore, can be evaluated as

That is,

where and . Consequently, we get

and . For the common index version , similar to above, the straightforward calculation yields that

This completes the proof. ∎

Proof of Theorem 4.

First, the second order condition for yields that

Furthermore, the result of Theorem 3 indicates that

Meanwhile, we obtain

where is that given in the proof of Theorem 3. Using above, we have

Consequently, we obtain

where

| (12) |

and

| (13) |

Here, for a vector , means the -norm of . Furthermore, we get

Similarly, for the common index estimator , we have

Accordingly,

where

| (14) |

and

| (15) |

Finally, we obtain the optimal rate of convergence of MISE of the common index estimator as

∎

Acknowledgements

The authors are grateful to Associate Editor and anonymous referees for their valuable comments and suggestions, which led to improvements of the paper. The research of the author was partially supported by KAKENHI 18K18011.

References

- [1] Barrow,D.L. and Smith,P.W. (1978). Asymptotic properties of best approximation by spline with variable knots. Quart. Appl. Math. 36 293–304.

- [2] Beirlant,J., Goegebeur,Y., Segers,J. and Teugels,J. (2004a). Statistics of extremes: theory and applications. John Wiley & Sons.

- [3] Beirlant,J., de Wet,T. and Goegebeur,Y. (2004b). Nonparametric estimation of extreme conditional quantiles. J. Statist. Comput. Simul. 74 567–580.

- [4] Beirlant,J. and Goegebeur,Y.(2004). Local polynomial maximum likelihood estimation for Pareto-type distributions. J. Multivar. Anal. 89 97–118.

- [5] Coles,S. (2001). An Introduction to Statistical Modeling of Extreme Values. Springer-Verlag.

- [6] Cardot,H. (2000). Nonparametric estimation of smoothed principal components analysis of sampled noisy functions. J. Nonparam. Statist. 12 503–538.

- [7] Chernozhukov,V. (2005). Extremal quantile regression. Ann. Statist. 33 806–839.

- [8] Chernozhukov,V. and Fernndez-val. (2011). Inference for extremal conditional quantile models, with an application to market and birthweight risks. The Review of Economic Studies. 78 559–589.

- [9] Cheng,Y., de Gooijer,J.G. and Zerom,D. (2011). Efficient estimation of an additive quantile regression model. Scandinavian Journal of Statistics. 38 46–62.

- [10] Claeskens,G., Krivobokova,T. and Opsomer,J.D. (2009). Asymptotic properties of penalized spline estimators. Biometrika. 96 529–544.

- [11] Daouia.A., Gardes.L, Girard,S and Lekina,A. (2011). Kernel estimators of extreme level curves. Test, 20 311–333.

- [12] Daouia,A., Gardes,L. and Girard,S. (2013). On kernel smoothing for extremal quantile regression. Bernoulli. 19 2557–2589.

- [13] de Haan,L. and Ferreira,A. (2006). Extreme value theory: an Introduction. New York: Springer-Verlag.

- [14] Demko,S. (1977). Inverses of band matrices and local convergence of spline projections. SIAM. J. Numer. Anal. 14 616–619.

- [15] Durrieu,G., Grama,I., Pham,Q.K. and Tricot,J.M. (2015). Nonparametric adaptive estimation of conditional probabilities of rare events and extreme quantiles. Extremes. 18 437–478.

- [16] Eilers,P.H.C. and Marx,B.D. (1996). Flexible smoothing with -splines and penalties. Statist.Sci. 11 89–121.

- [17] El Methni,J., Gardes,L. and Girard,S. (2014). Non-parametric estimation of extreme risk measures from conditional heavy-tailed distributions. Scand. J. Statist. 41 988–1012.

- [18] Gardes,L. and Girard,S. (2010). Conditional extremes from heavy-tailed distributions: An application to the estimation of extreme rainfall return levels. Extremes. 13 177–204.

- [19] Gardes,L., Girard,S. and Lekina,A. (2010). Functional nonparametric estimation of conditional extreme quantiles. Journal of Multivariate Analysis. 101 419–433.

- [20] Girard,S. and Louhichi,S. (2015). On the strong consistency of the kernel estimator of extreme conditional quantiles. Functional Statistics and Applications. 59–77.

- [21] Goegebeur,Y., Guillou,A. and Osmann,M. (2017). A local moment type estimator for an extreme quantile in regression with random covariates. Communications in Statistics-Theory and Methods. 46 319–343.

- [22] Hastie, T. and Tibshirani, R. (1990). Generalized additive models. Chapman and Hall.

- [23] He,F., Cheng,Y. and Tong,T. (2016). Estimation of extreme conditional quantiles through an extrapolation of intermediate regression quantiles. Statistics and Probability Letters. 113 30–37.

- [24] Hill,B.M. (1975). A simple general approach to inference about the tail of a distribution. Ann. Statist. 13 331–341.

- [25] Horowitz,J. and Lee,S. (2005). Nonparametric estimation of an additive quantile regression model. J. Amer. Statist. Assoc. 100 1238–1249.

- [26] Kim,S.J., Koh,K., Boyd,S. and Gorinevsky,D. (2009). trend filtering. SIAM Review. 51 339–360.

- [27] Knight.K. (1998). Limiting distributions for regression estimators under general conditions. Ann. Statist. 26 755–770.

- [28] Koenker,R. (2005). Quantile regression. Cambridge University Press, Cambridge.

- [29] Koenker,R. (2011). Additive models for quantile regression: Model selection and confidence bandaids. Brazilian Journal of Probability and Statistics. 25 239–262.

- [30] Koenker,R. and Bassett,G. (1978). Regression quantiles. Econometrica. 46 33–50.

- [31] Koenker,R., Ng,P. and Portnoy,S. (1994). Quantile smoothing splines. Biometrika. 81 673–680.

- [32] Lee,Y.K., Mammen,E. and Park,B.U. (2010). Backfitting and smooth backfitting for additive quantile models. Ann. Statist. 38 2857–2883

- [33] Liang,X., Zou,T., Guo,B., Li,S., Zhang,H., Zhang,S., Huang,H. and Chen,S.X. (2015). Assessing Beijing’s PM2.5 pollution: severity, weather impact, APEC and winter heating. Proceedings of the Royal Society A. 471.

- [34] Lu,Z. and Yu,K. (2004). Local linear additive quantile regression. Scand. J. Statist. 31 333–346.

- [35] Nychka,D., Gray,G., Haaland,P., Martin,D. and O’Connell,M. (1995). A nonparametric regression approach to syringe grading for quality improvement. J. Amer. Statist. Assoc. 90 1171–1178.

- [36] O’Sullivan,F. (1986). A statistical perspective on ill-posed inverse problems (with discussion). Statist. Sci. 1 505–27.

- [37] Pollard,D. (1991). Asymptotics for least absolute deviation regression estimators. Econometric Theory. 7 186–199.

- [38] Pratesi,M., Ranalli.M.G. and Salvati,N.(2009). Nonparametric M-quantile regression using penalised splines. J. Nonparam. Statist. 21, 287–304.

- [39] Reiss,P.T. and Huang,L. (2012). Smoothness selection for penalized quantile regression splines. The International Journal of Biostatistics. 8.1.

- [40] Ruppert,D. (2002). Selecting the number of knots for penalized splines. J. Comp. Graph. Statist. 11 735–757.

- [41] Sadhanala,V. and Tibshirani,R.J. (2017). Additive models with trend filtering. arXiv:1702.05037v2.

- [42] Tibshirani,R.J. (2014). Adaptive piecewise polynomial estimation via trend filtering. Ann. Statist. 42 285–323.

- [43] Wang,H.J., Li,D. and He,X. (2012). Estimation of high dimensional conditional quantiles for heavy-tailed distributions. J. Amer. Statist. Assoc. 107 1453–1464.

- [44] Weissman,I. (1978). Estimation of parameters and large quantiles based on the largest observations, J. Amer. Statist. Assoc. 73 812–815.

- [45] Yoshida,T. (2013). Asymptotics for penalized spline estimators in quantile regression. Communications in Statistics-Theory and Methods, DOI:10.1080/03610926.2013.765477.

- [46] Yuan,M. (2006). GACV for quantile smoothing splines. Computational Statistics Data Analysis. 50,813–829.

- [47] Zhou,S., Shen,X. and Wolfe,D.A. (1998). Local asymptotics for regression splines and confidence regions. Ann. Statist. 26 1760–1782.