Introduction of the MapDE algorithm for determination of

mappings relating differential equations

Abstract

This paper is the first of a series in which we develop exact and approximate algorithms for mappings of systems of differential equations. Here we introduce the MapDE algorithm and its implementation in Maple, for mappings relating differential equations. We consider the problem of how to algorithmically characterize, and then to compute mappings of less tractable (Source) systems to more tractable (Target) systems by exploiting the Lie algebra of vector fields leaving invariant. Suppose that is a (Source) system of (partial or ordinary) differential equations with independent variables and dependent variables . Similarly suppose is a (Target) system in the variables . For systems of exact differential polynomials , our algorithm MapDE can decide, under certain assumptions, if there exists a local invertible mapping that maps the Source system to the Target . We use a result of Bluman and Kumei who have shown that the mapping satisfies infinitesimal (linearized) mapping equations that map the infinitesimals of the Lie invariance algebra for to those for .

MapDE involves applying the differential-elimination algorithm to the defining systems for infinitesimal symmetries of , , and also to the nonlinear mapping equations (including the Bluman-Kumei mapping subsystem); returning them in a form which includes its integrability conditions and for which an existence uniqueness theorem is available. Once existence is established, a second stage can determine features of the map, and some times by integration, explicit forms of the mapping. Examples are given to illustrate the algorithm.

Algorithm MapDE also allows users to enter broad target classes instead of a specific system . For example we give an algorithmic approach that avoids the integrations of the Bluman-Kumei approach where MapDE can determine if a linear differential equation can be mapped to a linear constant coefficient differential equation.

Keywords: Symmetry, Lie algebra, defining equations, structure constants, algorithm, differential algebra, differential elimination, involutivity, numerical

Categories and Subject Descriptors: I.1.2; I.1.4.

1 Introduction

This paper is the first of a series in which we explore algorithmic aspects of mappings of differential equation systems that transform differential equations (DEs) to DEs. Naturally this exploration includes symmetry transformations – transformations of a DE to itself, and also equivalence transformations where one member of a class of DEs is mapped to another member of the class. In this paper we introduce the algorithm MapDE for characterizing mappings between DEs. For algorithmic implementation we restrict our treatment to differential polynomial systems (DPS), systems which are polynomially nonlinear functions of their derivatives and dependent variables; with coefficients from some computable field (e.g. ).

In earlier work we developed approximate methods for determination of approximate Lie symmetry algebra of DEs [8, 17]. A key motivation for our current work, is how to practically use such approximate methods. We see determination of approximate mappings of DPS, to be explored later in this series, as a practical way in which to exploit such approximate symmetry information. Our interest in mappings was also motivated by recent work [19], which used Reid [26] on the algorithmic determination of structure of Lie algebras of symmetries of DE, to give an algorithm to determine the existence of mappings exactly linearizable ODE. We give an algorithmic implementation of the methods of Bluman and Kumei [7, 15] for exploiting the Lie symmetries of a system in the determination of mappings between DEs.

In particular in this paper we introduce an algorithm for such mappings in the presence of symmetry. The algorithm MapDE is implemented as part of Huang and Lisle’s LAVF object-oriented Maple package [16]. We give examples to illustrate the algorithm and compare it with the approach of Bluman and Kumei. We extend the algorithm, to determine the existence of a mapping from linear DE, to linear constant coefficient DE, avoiding the heuristic integrations of Bluman and Kumei’s approach.

We consider systems of (partial or ordinary) differential equations with independent variables and dependent variables. Suppose has independent variables and dependent variables and has independent variables and dependent variables . In particular we consider local analytic mappings : , so that is locally and invertibly mapped to :

| (1) |

where and . The mapping is locally invertible so the determinant of the Jacobian of the mapping is nonzero:

| (2) |

where is the usual Jacobian matrix of first order derivatives of the functions with respect to the variables . Note throughout this paper, we will call the Target system of the mapping, which will generally have some more desirable features than , which we call the Source system.

Algorithms for existence of such mappings, and methods for their explicit construction, is the topic of this paper. A very general approach to such problems, Cartan’s famous Method of Equivalence [25], finds invariants, that label the classes of systems, equivalent under the pseudogroup of such mappings. The fundamental importance of such equivalence questions, and the associated demanding computations has attracted attention from symbolic computation researchers. For example, Neut, Petitot and Dridi [23], implemented Cartan’s method for ODE and certain classes of PDE of finite type (i.e. with finite dimensional solution space). Olver and collaborators developed a new version of Cartan’s moving frames [11]. Valiquette [31] applied this method to equivalence problems and further results are given by Arnaldson [3]. Also see [2] which introduces the DifferentialGeometry package, available in Maple and has been applied to equivalence problems. Also see [13, 20] for approaches to the non-commutative calculus that results in calculations. Underlying these calculations, is that overdetermined PDE systems, with some non-linearity, are required to be reduced to forms that enable the statement of a local existence and uniqueness theorem (such include passive and involutive forms). See [12] for estimates of complexity of such methods, which indicate their difficulty.

Our initial approach, is fairly direct, and exploits the linearity of the Bluman-Kumei mapping equations. It also is motivated by in the longer term, we wish to include invariant differential operators and using the newly developed methods of Numerical Jet Geometry, to investigate approximate equivalence.

In contrast, Bluman and Kumei [15] consider a narrower class of mapping problems, which is focused on the case where the Target system, is uniquely characterized in terms of its Lie symmetry invariance algebra (See [7, 15]). In this article we will implement an algorithm based on the Bluman and Kumei approach.

Suppose that a Source system, has an associated Lie symmetry algebra, together with its defining system. Such infinitesimal Lie point symmetries for are found by seeking vector fields

| (3) |

whose associated one-parameter group of transformations

| (4) |

which away from exceptional points preserves the jet locus of such systems - mapping solutions to solutions. See [5, 6] for applications. The infinitesimals of a symmetry vector field (3) for a system of DEs are found by solving an associated system of linear homogeneous defining equations (or determining equations) for the infinitesimals. The defining system is derived by an explicit algorithm, for which numerous computer implementations are available [9, 10, 27]. Similarly we suppose that the Target admits symmetry vector fields

| (5) |

in the Target infinitesimals . Computations with defining systems of both systems will be essential in our approach. We have implemented our algorithms in Huang and Lisle’s powerful object oriented LAVF, Maple package [16].

In §2 we give preliminaries and the Bluman-Kumei Mapping equations, together with a simple illustrative example. In §3 we describe our core algorithm MapDE, which takes and as input, and returns the reduced involutive form rif-form for , establishing existence, non-existence of the mapping. Once existence of the mapping is established, a further phase, is to try to obtain an explicit form for the mapping by integrating the mapping equations. We treat two cases: one in which and are specified and another where TargetClass = ConstantCoeffDE. In §4 we give examples of application MapDE and conclude with a discussion in §5.

2 Preliminaries & Mapping Equations

For an algorithmic treatment, we limit the systems considered to being differential polynomials, with coefficients from computable subfield of (e.g. ). Some non-polynomial systems can be converted to differential polynomial form by the use of the Maple command, dpolyform.

In the geometric approach to DEs centers around the jet locus, where the derivatives are regarded as formal variables and a map to polynomials, in our case, where the tools of algebraic geometry can be used. In general systems of polynomial equations and inequations must be considered (differences of varieties). The union of prolonged graphs of local solutions is a subset of the jet locus in , the jet space of order . For details concerning the Jet geometry of DEs see [24, 30].

example 2.1.

Consider the famous Black Schole’s equation which is fundamental in financial applications [21], we will use as an introductory simple example:

| (6) |

By inspection this equation has the obvious symmetry of translation in and scaling in . Moreover the infinitesimal form of these symmetries (1) is generated by the operators (3) given by and . Since these vector fields obviously commute, it is natural to map to new coordinates in which:

| (7) |

So by trivial integration the transformation , should map the Black Schole’s Equation into an equation invariant under two commuting translations, i.e. to a constant coefficient equation. Indeed by inspection we find:

| (8) |

which is the famous Black-Schole’s transformation of (6) to the backwards heat equation. This example simply illustrates that there can be a strong connection between symmetries admitted by an equation and mappings of the equation to convenient forms.

Indeed this illustrates the key idea of Bluman-Kumei’s method for determining when a linear differential equation (DE) in independent variables can be mapped to a (Target) linear constant coefficient DE: that the Target admits commuting translations. Geometrically the Source must correspondingly admit a subalgebra of its Lie symmetry algebra consisting of commuting symmetries (that act transitively on the space of its independent variables).

One can try to devise an algorithm for determining such symmetries explicitly. In general this involves integrating systems of overdetermined PDE, and, though advantageous in many applications, no general algorithm is known for this task. In our paper we describe algorithms using a finite number of differentiations and eliminations, and no integrations, that guarantees the algorithmic determination of the existence of such transformations. The computer algebra system Maple has several excellent such differential elimination algorithms, and also excellent algorithms for generating the linearized equations for symmetries.

example 2.2.

For the Black-Schole’s Equation (6), the defining system for the infinitesimal symmetry operator has form . Here comparing with (5) yields and . The automatically generated unsimplified system of defining equations for infinitesimal symmetries is:

| (9) | |||

Application of a differential-elimination algorithm to this system augmented with yields:

| (10) |

Application of rif’s initial data algorithm yields:

| (11) |

The key aspect relevant for our paper is that (2.2) and (2.2) are obtained with algorithmic operations and in particular without integration. In addition further algorithms from the LAVF package can determine the structure of its Lie Algebra. Indeed we find a two dimensional abelian subalgebra from that output, a necessary condition for the existence of a map of the Black-Schole’s equation to a constant coefficient equation.

2.1 Mapping Equations

Assuming existence of a local analytic invertible map between the Source system and the Target system and applying it to the infinitesimals yields what we will call the Bluman-Kumei (BK) mapping equations:

| (12) |

where and . See Bluman and Kumei [4, 7] for details and generalizations (e.g. to contact transformations). Note that all quantities on the LHS of the BK mapping equations (2.1) are functions of including and .

example 2.3.

We informally illustrate the BK mapping equations on Example 2.1. Here we follow an approach based on heuristic integration of the symmetry defining system. Indeed the defining system is easily integrated to find the full dimensional Lie symmetry algebra. And among the basis of symmetries the reader can easily find the two operators previously by inspection:

| (13) |

which implies that mapping has form: , , . When the corresponding coefficients of (13) are substituted into the BK system (2.1) we get:

| (14) |

which yields by simple integration the same result as before for the mapping of the Black-Schole’s to constant coefficient:

| (15) |

Indeed this integrating and breaking down into a basis, is the method used by Bluman and Kumei. However it does not yield an algorithm, since it depends on heuristic integration.

Finally we mention, that we are not opposed to integration, and in fact, a combination of integration and the algorithmic methods of this article, are probably a preferable way to proceed in practice.

Let , denote the symmetry defining systems for the Source system and the Target system respectively, with corresponding Lie symmetry algebras and . If an invertible map exists mapping to then it most generally depends on parameters. But we only need one such . So reducing the number of such parameters, e.g. by restricting to a Lie subalgebra of with corresponding Lie subalgebra of that still enables the existence of such , is important in reducing the computational difficulty of such methods. We will use the notation denote the symmetry defining systems of Lie sub-algebras , respectively. See [7, 25] discussion on this matter.

example 2.4.

The mapping of the linear Black-Schole’s equation (6) to a constant coefficient linear equation; we exploited the existence of a two dimensional abelian subalgebra. Indeed if we are lucky enough to identify this subalgebra immediately, then it gives very simple mapping equations with only two parameters. In the general algorithm for mapping linear equations to constant coefficient equations we described later, we can first bring such equations to homogeneous form. Restricting to symmetries, and mappings that retain the homogeneous form, can be imposed by restricting to symmetries with , which has a finite parameter Lie group of symmetries. Thus we rejection the unhelpful infinite super-position subgroup as we did in the Black-Schole’s example earlier. For more details see Bluman et al. [7].

2.2 Algorithms EquivDetSys and DimEquivTest

With the Source system , the Target system and the mapping , the algorithm is to return the full non-nonlinear defining equations for mappings from to which are invertible (i.e. ). As preparation for the description of this algorithm we introduce the following algorithm.

EquivDetSys: This is Maple implementation of returning the nonlinear DPS for invertible mappings from to . Our implementation currently requires that , are in solved form for their leading derivatives with respect to a ranking graded by total differential order; though this could be weakened in the future. Then Maple’s general purpose routine for changing variables is applied, yielding expressions in the parametric derivatives of . Setting coefficients of independent powers of the parametric derivatives to zero, together with simplified with respect to yields the nonlinear determining system for . This construction is well-known (indeed it is used in [19] in the special case of mappings linearizing ODE). However the nonlinear overdetermined systems are challenging to compute due to the expansion of determinants as the number of variables and differential order of increase.

Our approach in this paper, is to take advantage of such linearized infinitesimal information, available from Lie symmetries and in particular via the BK equations, which are linear in the mapping variables. Then if necessary, at the end of MapDE apply EquivDetSys, which can be much simplified by the earlier computed conditions in .

Also we employ a number of efficient preliminary tests that can some times quickly determine if and are not equivalent via .

DimEquivTest: Differential-elimination algorithms such as those in the packages

, DifferentialAlgebra and

DifferentialThomas

allow a determination of a coordinate dependent description of initial data, and using that the determination of the

coordinate independent quantities , . Thus a quick first test applied

by DimEquivTest is .

If the input ranking is graded first by total derivative order, then further dimension invariants can be derived from that initial data: which are the number of parametric derivatives at each derivative order (determining the Differential Hilbert Series). DimEquivTest tests the equality of these invariants up to the maximum involutivity order for . One further invariant is the number of arbitrary functions of the maximum number of independent variables appearing in the initial data. For background information see [30].

3 MapDE Algorithm

In this section we describe algorithms for mapping a system to .

In §3.1 we describe MapDE for a specific Source system and specific Target system . In §3.2 we give a description of MapDE for a linear input equation and a class of Target systems (where the Target is constant coefficient linear equation).

3.1 The MapDE Agorithm for specific and

First we describe MapDE which is really a general class of methods for mapping systems to (i.e. TargetClass). The algorithm returns the system of mapping equations in rif-form, and, if their integration is successful, an explicit form of the transformations to map the system to the TargetClass. It is described in the MapDE Algorithm 1 provided next. In that algorithm we suppose that are respectively the Lie algebras of symmetries of , , with defining systems , .

For mathematical properties of the algorithms, including finiteness, see the following references. For LAVF see [16], for rif’s existence and uniqueness theory see [29], for the classification of differential rankings see [28]. For the algorithmic determination of structure of transitive Lie pseudogroups see Lisle and Reid [18].

Notes for the MapDE Algorithm

-

Input:

The input Source consists differential polynomial system (DPS) of differential polynomials with coefficients in some computable field (e.g. ); Opts are additional Options such as input rankings if not default.

-

Output:

pdsolve is Maple general purpose exact PDE solver: the application of Maple’s pdsolve which can not guarantee successful integration of DE.

-

Step 1:

Here and throughout rif and ID refer to Maple’s DEtools package commands rifsimp and initialdata commands. Alternatively one could use other Maple packages such as diffalg or DifferentialThomas.

-

Step 2:

As introduced in §2.2, is a simple algorithm for checking some necessary conditions for the existence of a mapping: the simplest being , and include others corresponding to coefficients of the Differential Hilbert Series for and .

-

Steps 3, 4:

Restriction to a subalgebra is also possible and can improve efficiency. Similarly to Step 2, invariant dimension information can lead to early rejection of existence of a mapping: the first being that .

-

Steps 5, 6:

LAVF command StructureCoefficients algorithmically determines the structure constants of the algebras for . Maple’s LieAlgebras and DifferentialGeometry packages, are then used to generate the polynomial system for in a change of basis matrix which is then analyzed by the solver Triangularize.

- Step 7:

-

Step 8:

Differential elimination with casesplitting is applied and useless computations on branches with ID mindim wrt avoided. The ranking ranks the map variables less than any derivative of the infinitesimals yielding an uncoupled system in whose ID is then examined and cases with less than dimensional data rejected. This ranking means that the linearity in is maintained in computations.

-

Step 11:

See §2.2.

-

Step 12:

SelSys selects a consistent system from the output of rif

3.2 MapDE for mapping Linear Homogeneous DE to Constant Coefficient Linear DE

Here we consider how to map a linear homogeneous source DE to a constant coefficient linear homogeneous DE, with an algorithm which results from straightforward changes to Algorithm 1.

The idea introduced in Bluman et al. [7, §2.5] for this problem is to introduce a chain of Lie subalgebras whose purpose is to focus on the Target: and via also a chain .

Now where is the set of derivatives of of order differential order of . The unspecified constants are the coefficients of the target. It is natural to restrict to transformations that preserve the linearity an homogeneity of the input DE and result from eliminating the superposition symmetry: and where (see Bluman et al. [7]). Correspondingly its natural to consider a subalgebra that results by appending the equations and to to form :

| (16) |

and similarly for . To avoid the early calculations that involve , we focus like Bluman et al, on accessible infinitesimal information encoded in a Lie algebra . In this case corresponds to commuting translations in the independent variables , i.e. translations with generators . The corresponding differential system for and is

| (17) |

4 Examples

In this section we apply our algorithm to examples.

4.1 Equivalence

example 4.1.

Bluman et al. [7, §2.3.2, pg 133-137] apply their mapping method based on explicit integrations to determine an invertible mapping by a point transformation of the cylindrical KdV equation to the KdV equation that first appeared in the work of Korobeinikov [14]:

| (18) | ||||

| (19) |

They give details of their calculations and for illustration we apply the MapDE algorithm 1 to the same example. Here we seek transformations .

-

Steps 1, 2:

Both and are already in rif-form with respect to any orderly ranking. The initial data for the and are

Here there are arbitrary functions in the initial data,

so . Their Hilbert Series obviously are equal, and up to the order of involutivity: where the coefficient of is the number of parametric derivatives of order . So in Step 2. -

Step 3, 4:

The rif-form systems are

(20) (21) and yield ID giving . Also DimEquivTest true in Step 4.

-

Step 5:

Here MapDE uses the LAVF command StructureConstants to compute the structure of the dimensional Lie algebras for and obtaining:

(22) (23) -

Steps 5, 6:

We obtain and the explicit isomorphism:

(24) Bluman et al. [7, Eqs (2.39), (2.40), pg 134]obtain the structure and an isomorphism by explicitly integrating the defining systems, whereas we avoid this. This isomorphism is a necessary but not sufficient condition for the existence of a local analytic invertible map to .

-

Steps 7, 8:

The rif-form of the mapping system results in one consistent case with -dim ID in the infinitesimals for . The rif-form of the system is:

(25) -

Steps 9, 10:

Step 9 does not apply. The above rif-form for the system has ID for :

Geometrically, since the ID has dimension , there is class of systems with the same dimensional invariance group, that possibly includes the Target system. So Step 10 does not apply. Thus we have to apply to find missing condition(s). After explicit integration Bluman et al also find that they don’t uniquely specify the target, and essentially they substitute the transformations to obtain the parameter values to specify the target.

-

Steps 11, 12:

Applying rif to the combined system yields a single case:

where the constraint is , and the inequation . The ID shows we now have parameters, confirming the existence of the transformations, without integration.

-

Step 13

Applying pdsolve yields the solution for the transformation below:

where

subject to the determinental condition. The last condition implies . Specializing the values of the give the transformations obtained also in Bluman et al.

4.2 Mapping to constant coefficient DE

example 4.2.

The harmonic-oscillator Schrödinger Equation which in normalized rif-form is:

| (26) |

Applying the algorithm using the option Target = ConstantCoeffDE shows that (26) maps to a constant coefficient linear DE:

| (27) |

Existence of such a mapping is given algorithmically and the output includes the system for with :

Integrating the system and specializing the constants gives:

where is .

When the mapping system is reduced to rif-form as in Step 4, of Algorithm 2 it yields a consistent system for with arbitrary constants in its initial data, hence establishing existence of a mapping to a constant coefficient DE. Since this means that there is a dimensional target class of constant coefficient linear DE. Indeed there are two options here, one would be attempt to (heuristically) integrate this system. We did try this, and succeeded to find the solutions with 10 parameters. Instead in the spirit of our approach in this paper, to reduce as much as possible to algorithmic differential elimination, we also experimented with inserting a step in the algorithm, that executes a general change of coordinates from the TargetDE which has arbitrary constants, ranking those constants highest in the ordering and obtained as a subsystem:

The transforming system is updated by adding these equations. So the constants amount to integrations, and can be used to reduce the dimension of the system for by specializing their values. This yielded the final dimensional system. Note that it was reduced by dimensions (after elimination the relation ).

example 4.3.

Consider the DE arises in financial models known as Black Schole’s[21] as the Source system ,

Using our algorithm with TargetClass = ConstantCoeffDE, automatically yields the mapping :

and the Target system is .

5 Discussion

Mappings of mathematical models are a fundamental tool of mathematics and its applications. This fact and the notorious difficulty of their computation motivates us to explore the approach we presented in this article. This resulted in our algorithm, MapDE, which is given algorithmic realization for two cases. The first is where the input systems and are specified as polynomially nonlinear DEs and MapDE returns a reduced involutive rif-form for the mapping equations. The second is where is a linear homogeneous DE and the TargetClass is a constant coefficient linear homogeneous DE (Target = ConstantCoeffDE). A key aspect of our approach is to exploit the linearity of the Bluman-Kumei mapping equations that arise in the presence of symmetry, and postpone, simplify and even avoid direct computations with the full nonlinear determining equations for the mappings. We also implement some fast preliminary tests for equivalence under mappings.

The closest approach to the our work, are the works of Bluman and collaborators and in particular the work by Anco, Bluman and Wolf [1] and also Wolf [32], which considered a computer program for computing linearization mappings. It exploits Wolf’s program ConLaw’s strong facilities for integrating systems of PDE exactly in addition to the BK mapping equations, as well as an embedding technique involving multipliers and conservation laws. They also mention that the problem of full algorithmization using differential algebra as an important open problem.

In another paper [22], we give various extensions MapDE. One of these involves extending it to determining existence of exact linearization mappings of DE. In so doing we provide algorithm and combining aspects of the approach of Bluman, Anco and Wolf [1, 32] and also of Gerdt et al [19].

Building in invariant properties into the completion process is also a possibility; borrowing aspects of the more geometrical approaches.

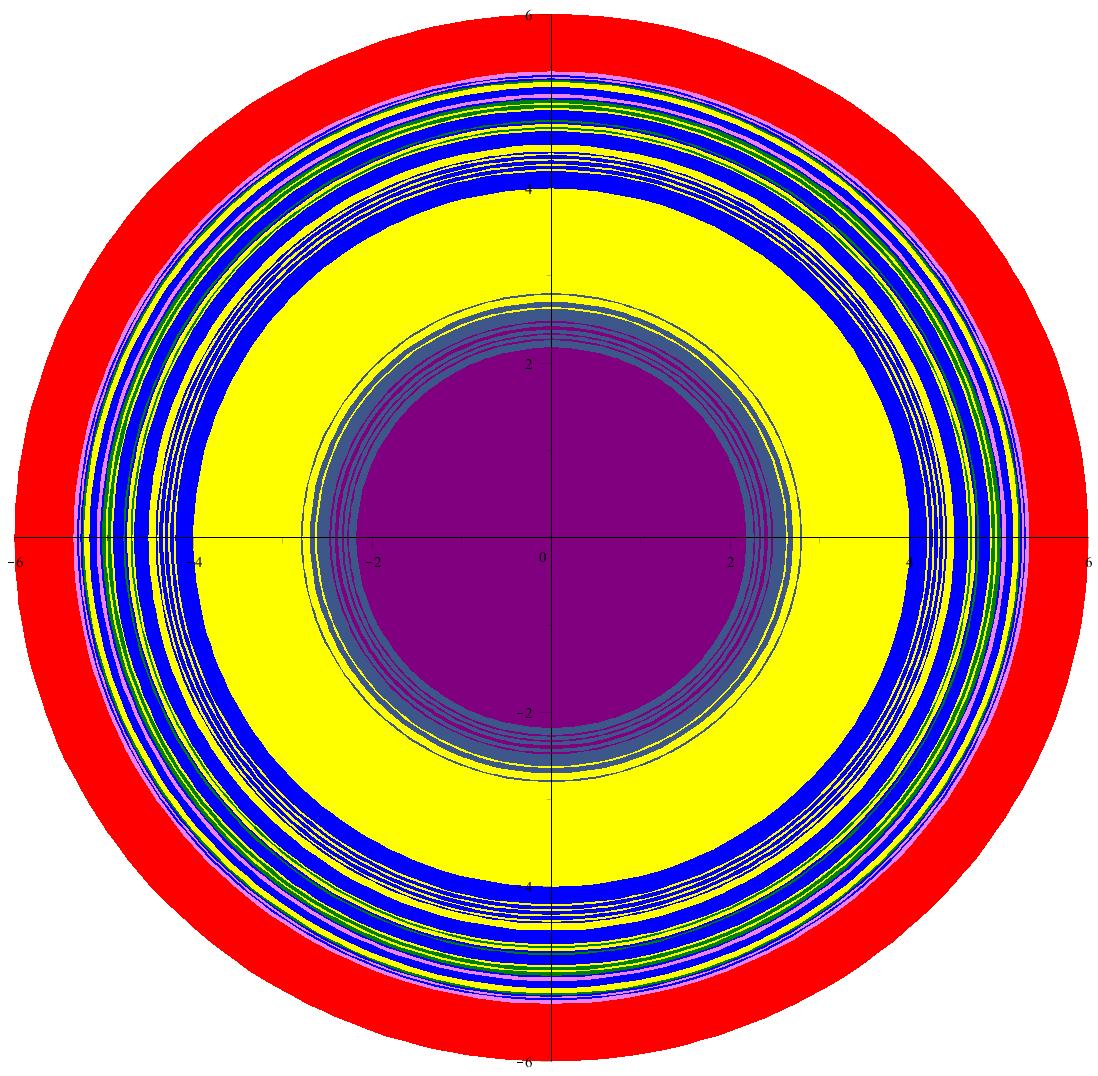

Longer term we are particularly interested in exploring approximate mappings and approximate equivalence. Indeed LAVF already has the first available algorithm for determining the structure of approximate symmetry of DE theoretically first described in Lisle, Huang and Reid [17]. Indeed consider Poisson’s equation for a gravitational potential : and an interstellar gas with density proportional to where and :

Applying Lie’s standard method where

Discarding the superposition via and performing an exact symmetry analysis yields only a dimensional rotation group about the axis; throughout all space no matter how small is.

We now apply our method to find approximate Lie algebra of symmetries of Poisson’s Equation at the point and . Recall we only found a dimensional Lie symmetry group of rotations in the plane about the axis. We find:

which we can recognize as

or after the basis change is :

Remarkably we get different regions with different approximate groups, plus transition bands. Potentially and intuitively the model can be mapped to various forms depending on the region, which is a longer term topic, for our research.

Acknowledgments

GJR acknowledges the support of an NSERC Discovery Grant from the government of Canada. GJR acknowledge the contribution of his colleague and departed friend Ian Lisle, whose inspiration lies behind this work in its spirit and many details.

References

- [1] S. Anco, G. Bluman, and T. Wolf. Invertible mappings of nonlinear pdes to linear pdes through admitted conservation laws. Acta Applicandae Mathematicae, 101:21–38, 2008.

- [2] Anderson, I. M. and Torre, C. G. New symbolic tools for differential geometry, gravitation, and field theory . Journal of Mathematical Physics, 53, 2012.

- [3] Arnaldsson, O. Involutive Moving Frames. Department of Mathematics, University of Minnesota, 2017.

- [4] G. Bluman and S. Kumei. Symmetries and Differential Equations. Springer, 1989.

- [5] G. Bluman and S. Kumei. Symmetry based algorithms to relate partial differential equations: I. Local symmetries. Eur. J. Appl. Math., 1:189–216, 1990.

- [6] G. Bluman and S. Kumei. Symmetry based algorithms to relate partial differential equations: II. Linearization by nonlocal symmetries. Eur. J. Appl. Math., 1:217–223, 1990.

- [7] G. W. Bluman, A. F. Cheviakov, and S. C. Anco. Applications of Symmetry Methods to Partial Differential Equations. Springer, 2010.

- [8] J. Bonasia, F. Lemaire, G. Reid, R. Scott, and L. Zhi. Determination of approximate symmetries of differential equations. In P. Winternitz et al., editors, Group Theory and Numerical Analysis, CRM Proceedings and Lecture Notes,(39): 233–249. AMS/CRM, 2005.

- [9] J. Carminati and K. Vu. Symbolic computation and differential equations: Lie symmetries. Journal of Symbolic Computation, 29:95–116, 2000.

- [10] A. F. Cheviakov. GeM software package for computation of symmetries and conservation laws of differential equations. Computer Physics Communications, 176(1):48–61, 2007.

- [11] Fels, M. and Olver, P. Moving Coframes II. Regularization and theoretical foundations. Acta Applicandae Mathematicae, 55: 127–208, 1999.

- [12] O. Golubitsky, M. Kondratieva, A. Ovchinnikov, and A. Szanto. A bound for orders in differential Nullstellensatz. Journal of Algebra, 322: 3852 - 3877 (11), 2009.

- [13] E. Hubert. Differential invariants of a Lie group action: Syzygies on a generating set. Journal of Symbolic Computation, 44(4):382–416, 2009.

- [14] Korobeinikov, V.P. Certain types of solutions of Korteweg–de VriesBurgers’ equations for plane, cylindrical, and spherical waves. Proceedings IUTAM Symposium on Nonlinear Wave Deformations,Tallinn , 1982, in Russian.

- [15] S. Kumei and G. Bluman. When nonlinear differential equations are equivalent to linear differential equations. SIAM Journal of Applied Mathematics, 42:1157–1173, 1982.

- [16] I. Lisle and S.-L. Huang. Algorithms calculus for Lie determining systems. Journal of Symbolic Computation, 482–498, 2017.

- [17] I. Lisle, S.-L. Huang, and G. Reid. Structure of symmetry of pde: Exploiting partially integrated systems. Proceedings of the 2014 Symposium on Symbolic-Numeric Computation, 61–69, 2014.

- [18] Lisle, Ian G. and Reid, Gregory J. Geometry and Structure of Lie Pseudogroups from Infinitesimal Defining Systems. J. Symb. Comput., 26: 355–379, (3), 1998.

- [19] D. Lyakhov, V. Gerdt, and D. Michels. Algorithmic verification of linearizability for ordinary differential equations. In Proc. ISSAC ’17, ACM,285–292, 2017.

- [20] E. Mansfield. A Practical Guide to the Invariant Calculus. Cambridge Univ. Press, 2010.

- [21] T. Masebe and J. Manale. New symmetries of Black-Scholes equation. In Proc. AMCM ’13: 221–231, 2013.

- [22] Mohammadi, Z. and Reid, G. and Huang, S.-L.T. Extensions of the MapDE algorithm for mappings relating differential equations. To be submitted to arXiv, 2019.

- [23] S. Neut, M. Petitot, and R. Dridi. Élie Cartan’s geometrical vision or how to avoid expression swell. Journal of Symbolic Computation, 44(3):261 – 270, 2009. Polynomial System Solving in honor of Daniel Lazard.

- [24] P. Olver. Application of Lie groups to differential equations. Springer-Verlag, 2nd edition, 1993.

- [25] P. Olver. Equivalence, invariance, and symmetry. Cambridge University Press, 1995.

- [26] Reid, G.J. Finding abstract Lie symmetry algebras of differential equations without integrating determining equations. European Journal of Applied Mathematics, 2:319–340, 1991.

- [27] T. Rocha Filho and A. Figueiredo. SADE: A Maple package for the symmetry analysis of differential equations. Computer Physics Communications, 182(2):467–476, 2011.

- [28] Rust, C.J. and Reid, G.J. Rankings of partial derivatives. Proc. ISSAC ’97, 9–16, 1997.

- [29] Rust, C.J. and Reid, G.J. and Wittkopf, A.D. Existence and uniqueness theorems for formal power series solutions of analytic differential systems. Proc. ISSAC ’99, 105–112, 1999.

- [30] W. Seiler. Involution: The formal theory of differential equations and its applications in computer algebra, Algorithms and Computation in Mathematics. (24) Springer, 2010.

- [31] Valiquette, F. Solving local equivalence problems with the equivariant moving frame method. SIGMA: Symmetry Integrability Geom. Methods Appl., 9, 2013.

- [32] T. Wolf. Investigating differential equations with crack, liepde, applsymm and conlaw. Handbook of Computer Algebra, Foundations, Applications, Systems,, 37:465–468, 2002.