On Robustness of Principal Component Regression

Abstract

Principal component regression (PCR) is a simple, but powerful and ubiquitously utilized method. Its effectiveness is well established when the covariates exhibit low-rank structure. However, its ability to handle settings with noisy, missing, and mixed-valued, i.e., discrete and continuous, covariates is not understood and remains an important open challenge. As the main contribution of this work we establish the robustness of PCR, without any change, in this respect and provide meaningful finite-sample analysis.

To do so, we establish that PCR is equivalent to performing linear regression after pre-processing the covariate matrix via hard singular value thresholding (HSVT). As a result, in the context of counterfactual analysis using observational data, we show PCR is equivalent to the recently proposed robust variant of the synthetic control method, known as robust synthetic control (RSC). As an immediate consequence, we obtain finite-sample analysis of the RSC estimator that was previously absent. As an important contribution to the synthetic controls literature, we establish that an (approximate) linear synthetic control exists in the setting of a generalized factor model, or latent variable model; traditionally in the literature, the existence of a synthetic control needs to be assumed to exist as an axiom. We further discuss a surprising implication of the robustness property of PCR with respect to noise, i.e., PCR can learn a good predictive model even if the covariates are tactfully transformed to preserve differential privacy.

Finally, this work advances the state-of-the-art analysis for HSVT by establishing stronger guarantees with respect to the -norm rather than the frobenius norm as is commonly done in the matrix estimation literature, which may be of interest in its own right.

Keywords: principal component regression, synthetic controls, error-in-variables regression, hard singular value thresholding, matrix estimation

1 Introduction

A common thread of many modern datasets is that they are high-dimensional, and often noisy and partially observed. When such datasets are used for regression, this means that both the response variables (also known as the label of target) and the covariates (also known as features) are corrupted. This setting is known in the statistics literature as error-in-variables regression. Another common feature of most real-world datasets are that they are mixed valued, i.e., contain both discrete and continuous data, which further complicates the regression procedure. Within this context, we are interested in developing a better understanding of a popular prediction method known as principal component regression (PCR). Indeed, PCR’s ability to handle settings with noisy, missing, and mixed-valued covariates is not understood and remains an important open challenge [17].

A further motivation of this work is to connect the error-in-variables setting to the exciting and growing literature on synthetic controls (SC), a standard framework in econometrics (and beyond) to make counterfactual predictions utilizing only observational data ([2, 1, 24, 22, 49, 8, 7, 5, 30, 29, 25, 13, 6]). Broadly speaking, there is a notion of a “target” and “donor” units, for which we collect observations over time. While the donors units remain under control, the target undergoes an intervention at some time period. Here, the goal is to estimate what would have happened to the target unit had it also remained under control. Towards answering this question, standard SC methods build a synthetic model of the target unit using observations associated with the donor units. In the language of regression, the target unit observations represent the response variables and the donor unit observations represent the covariates. In the SC literature, the observations associated with both the target and donor units are assumed to be noisily observed due to the presence of idiosyncratic shocks at each time step. As a result, SC can be seen as an instance of error-in-variables regression; more generally, panel data settings, where one collects measurements over time, can also be viewed through this error-in-variables lens.

As the main contribution of this work, we establish the effectiveness of PCR, without any change, for error-in-variables regression and provide meaningful finite-sample analysis for both in- and out-of-sample prediction error. Given the connection between error-in-variables regression and SC, our analysis also implies that using PCR in this context leads to it implicitly de-noising the observations we have of the donor units, which are corrupted by idiosyncratic shocks. Thus, we advocate for PCR’s usage in panel data settings.

1.1 Problem Statement

In a typical prediction problem setup, we are given access to a labeled dataset over ; here, represents the response variable we wish to predict, and represents the associated covariate to be utilized in the prediction process. Let denote the total number of observations, where the number of predictors can possibly exceed . Let denote the matrix of true covariates.

Error-in-variables. Rather than perfectly observing the covariates , the error-in-variables setting only reveals a corrupted version denoted as . That is, the -th entry of , denoted as , is defined as with probability and with probability , for some ; here, denotes a missing value and denotes the noise in the -th entry. In other words, each entry is observed with probability , independently of other entries; however, even when observed, is still only a noisy instance of the true .

Approximate linear model. We assume the response variables are generated as follows: for , the random response is associated with the covariate via

| (1) |

where is the unknown latent model parameter, denotes zero mean response noise with variance bounded by , and is the linear model misspecification, or mismatch, error; for simplicity, we assume the mismatch error is deterministic. Additionally, the observed response variables are restricted to a subset of the observations. More formally, we denote , with , as the index set of observed responses, i.e., we observe for .

Goal. Given noisy observations of all covariates and a subset of response variables , our aim is to produce an estimate so that the prediction error is minimized. Specifically, we measure performance in terms of the training error

| (2) |

and testing error

| (3) |

We note that for the bound to be meaningful, (the size of the test set) should be of the same order as that of the the training set .

Transductive semi-supervised learning. It is worth remarking that in (3), the algorithm is given access to the observations associated with the covariates for both training and testing data during the training procedure. Of course, however, the algorithm does not access the test response variables. This is commonly referred to in the literature as transductive semi-supervised learning; here, we want to infer the response variables for the specific unlabeled data. Traditionally, it is assumed that a statistical estimator only has access to the training covariates and response variables during the model learning process. The reason we consider a transductive learning setting is a consequence of the nature of the algorithm of interest, PCR. Specifically, PCR pre-processes the covariates using PCA, which changes the training procedure if only a subset of the covariates are utilized. Therefore, to allow for a meaningful evaluation, it is natural to allow the algorithm to have access to all available covariate information. Indeed, as we will discuss in Section 4, as well as Appendices B and C, it is natural to have access to all covariates in many important real-world applications.

1.2 Contributions

PCR implicitly de-noises. As the main contribution of this work, we argue that PCR, without any change, is robust to noise and missing values in the observed covariates. In particular, despite only having access to , we show the training error of PCR scales (up to logarithmic factors) as , where denotes the fraction of observed (noisy) covariates and is the rank of (Corollary 3.1). That is, PCR implicitly de-noises by projecting it onto the subspace spanned by the top right singular vectors. We note that the prediction error rate of for the training data matches (up to log factors) the minimax rate achievable by ordinary least squares (OLS) if one had perfectly observed the true underlying covariate matrix (see [46] and references therein).

We extend our results to the case where is only approximately low-rank (Theorem 3.1 and Corollaries 3.2 and 3.3). To the best of our knowledge, under this setting, there do not exist prediction consistency results for OLS or regularized variants thereof such as Lasso and Ridge, without making additional assumptions on the sparsity of . This remains true even if is perfectly observed. Thus, the first step in PCR of finding a low-dimensional representation is likely crucial for this setting, and further motivated if the covariates are noisily observed. Given the ubiquity of approximately low-rank matrices in real-world datasets, it reinforces the utility and robustness of applying PCR in practice.

Moreover, we note that PCR does not require any knowledge about the underlying noise model that corrupts the covariates in order to to have vanishing train and test errors. Despite the exciting recent advancement in the high-dimensional error-in-variables literature, such as in [31, 20, 38], the current inventory of methods require knowledge of the underlying covariate noise model (in particular, exact knowledge of its second moment of matrix) and do not provide finite sample guarantees for train or test error. We do note, however, that the aim of these previous papers is to estimate the latent linear model parameter (assuming it is sparse), rather than to analyze prediction errors. For a detailed comparison, see Appendix A.

PCR implicitly regularizes. We define an appropriate notion of generalization error for the transductive learning setting we consider. We establish that the testing prediction error of PCR is bounded above by the training error plus a term that scales as , where is the number of retained principal components (Theorem 3.2). Our testing error result provides a systematic way to select the correct number of principal components in a data-driven manner, i.e., to choose the value of that minimizes the training error plus the generalization penalty term .

Our test error analysis utilizes the standard framework of Rademacher complexity (see [10] and references therein). However, there are two crucial differences that we need to overcome in order to obtain sharp, meaningful bounds. First, our notion of generalization is different from that of the traditional setup since the noisy test covariates (but not responses) are included in the training process, which requires careful analysis. Second, we argue that the Rademacher complexity under PCR scales with the dimensionality of the number of principle components utilized, denoted as , rather than the ambient covariate dimension . To do so, we identify the Rademacher complexity class of PCR with -sparse ’s.

PCR applications. We discuss the robustness of PCR to contaminated covariates by analyzing its ability to learn a predictive model when only differentially private covariates are available. In particular, we find that it is feasible for PCR to achieve good prediction accuracy and simultaneously maintain differential privacy of the covariates (Appendix B). We also describe how the robustness of PCR allows it to seamlessly utilize mixed valued covariates under a general probabilistic model (Appendix C).

SC literature. First, we note that regardless of method used to construct synthetic controls, the fundamental hypothesis that drives these prior works is the existence of a linear relationship between the target and donors; in fact, the original proposal of [2, 1] suggests restricting the linear model coefficients to be non-negative and sum to one, i.e., a convex combination. However, it is not clear when such a hypothesis holds. Second, meaningful finite-sample analysis of the mean-squared post-intervention error of SC has remained elusive. We tackle these two questions via our results on PCR. Towards the first question, we establish that (approximate) synthetic controls exist under a generalized factor model (also known as a latent variable model). Here, the measurement associated with a given unit and time is a sufficiently smooth function of the latent unit and time factors. Therefore in a general sense, a synthetic control almost always exists and need not be assumed as a hypothesis or axiom (see Proposition 4.1). Towards the second question, we show that PCR is identical to a recently proposed SC estimator known as robust synthetic control (RSC) [5]. Hence, we immediately establish meaningful training (pre-intervention) and testing (post-intervention) error guarantees for RSC (see Theorem 4.1).

1.3 Organization of Paper

In Section 2, we describe the PCR algorithm. Section 3 then details the various training and test prediction error bounds for PCR and the conditions under which they hold. In Section 4, we formally connect PCR to SC. In Appendix A, we do a detailed comparison with previous related works. In Appendices B and C, we discuss the application of PCR for differentially private regression and mixed valued covariates, respectively. The remaining appendices are to prove our theoretical results.

2 Principal Component Regression

We recall the description of PCR, as in [26]. We suggest a minor modification of PCR in the presence of missing data where we simply re-scale the observed covariates by the inverse of the fraction of observed data.

Algorithm. Let denote the fraction of observed entries in , i.e., . Let represent the rescaled version of , where every unobserved value is replaced by , i.e., if and otherwise.

The singular value decomposition (SVD) of is denoted as , where , , and . Without loss of generality, assume that the singular values ’s are arranged in decreasing order, i.e., . Note that and are orthogonal matrices, i.e., the ’s and ’s are orthonormal vectors.

For any , let , , and . Then, the -dimensional representation of , as per PCA, is given by . Let be the solution to the linear regression problem under , i.e., is the minimizer of

Then, the estimated -dimensional response vector .

Intuition. Using all the noisily observed observed covariates, PCR first finds a dimensional representation of the covariate matrix using the method of principal component analysis (PCA), where might be much smaller than . Specifically, PCA projects every covariate onto the subspace spanned by the top right singular vectors of the observed covariate matrix, . PCR then uses the -dimensional features to perform linear regression.

2.1 Connecting PCR to the Matrix Estimation Literature

To establish our results, we study PCR via its equivalence with performing linear regression after pre-processing covariates via hard singular value thresholding (HSVT), as described below.

Linear regression with covariate pre-processing via HSVT. Given any , we define the map , which simply shaves off the input matrix’s singular values that are below the threshold . Precisely, given a matrix , denote its SVD as , and let . For any , given as before, define . Let be a solution of linear regression under , i.e., is the minimizer of

| (4) |

Then, the estimated -dimensional response vector .

Equivalence with PCR. We now state a simple, yet key relation between PCR and the algorithm above. Precisely, the two algorithms produce identical estimated response vectors.

Proposition 2.1.

For any ,

By establishing the equivalence above, it allows us to analyze PCR through the growing matrix estimation/completion literature, of which HSVT is one of the most commonly analyzed methods. In fact, there is significant literature establishing that HSVT is a noise-model-agnostic method that recovers the ground-truth matrix given a sparse, noisy observation of it, e.g., see [18]

-norm error bound for HSVT. The limitation of the current results concerning HSVT is that they only establish its estimation accuracy in terms of the mean-squared error or expected squared Frobenius norm of the error matrix. To establish our above mentioned results on the prediction error of PCR, it seems necessary to bound the expected squared -norm of the error matrix (see Lemmas 3.1 and 3.2), which is a stronger guarantee than the Frobenius norm. To see this, let denote the error matrix; then,

Given the ubiquity of HSVT, the -norm result for HSVT may be of interest in its own right.

2.2 Connecting PCR to Synthetic Controls

We briefly describe the application of the analysis of PCR to SC, which has become a standard method in econometrics (and beyond) to make counterfactual predictions utilizing only observational data.

Robust synthetic control. In [5], the authors propose the robust synthetic control (RSC) method, which pre-processes observations using HSVT before performing linear regression to learn the model. They observed empirically that the resulting synthetic control had attractive robustness properties such as robustness to noisy and partially observed data, and thus suggested an alternative model to the convex weights originally proposed by [2, 1]; compare Figures 4(b) and 6(c) with Figures 2(b) and 6(b). Using Proposition 2.1, we establish PCR is identical to the RSC estimator. This provides empirical evidence of the importance of pre-processing the covariates (in the setting of SC, this is the donor pool data) by finding its low-dimensional representation. See Section 4 for details.

3 Main Results

Notations. For any matrix , let denote the Frobenius norm, operator norm, and max norm (i.e., largest absolute value among all entries) of a matrix , respectively; let denote the max column -norm of . For an index set , let denote the submatrix of formed by stacking the rows of according to , i.e., is the concatenation of . The superscript is sometimes omitted if the matrix representation is clear from context. Let and for any . Lastly, let denote the indicator function.

3.1 Key Modeling Assumptions

We recall the approximate linear model given by (1).

Bounded covariates. We assume the entries of are bounded. Without loss of generality, we assume the entries are bounded by .

Property 3.1.

The entries of are bounded by one in absolute value, i.e., .

Noise on response variables. We make the standard assumption that the noise on the response variable, denoted by , is mean zero and has bounded variance.

Property 3.2.

The response noise is a random vector with independent, mean zero entries such that each of its components has variance bounded above by .

Noise on covariates. Recall that rather than observing , we are given access to its partially observed and noisy version . Let denote the covariate noise matrix. We define as the noisy perturbation of the covariate matrix, without missing values. We assume the following property about the noise matrix (see Definition E.1 for the definition of -random variables/vectors).

Property 3.3.

Let be a matrix of independent, mean zero -rows for some , i.e., there exists an and such that for all . Further, assume there exists a such that for all . Lastly, for all , assume variance of is bounded above .

Remark 3.1.

One can verify that if the entries of are independent, then (e.g., for independent standard normal random variables, ). In general, will scale linearly with the number of correlated entries in ; similarly, scales with the square root of the correlated entries.

Remark 3.2.

We assume that the response noise and covariate noise are independent of each other. Further, if we denote as the random variable indicating whether is missing or not, we assume is independent of and . Relaxing these assumptions and allowing for dependencies between these three sources of noise remains interesting future work.

3.2 Training Prediction Error

In this section, we present bounds on the training error under different settings.

3.2.1 General Results

We first state Theorem 3.1 (proof in Appendix G), which bounds the training error of PCR in terms of three natural quantities, as described below.

Theorem 3.1 (Training Error of PCR: Generic Result).

Interpretation. The bound in (5) has three terms on the right hand side: (a) represents the standard “regression” prediction error, which scales with the model complexity and inversely with number of samples ; (b) , which is a consequence of the corruption of (if was fully observed and rank , then this error term would vanish); (c) represents the (inevitable) impact of the model mismatch.

Quantification. To quantify (5), we need to evaluate , where is the estimate of produced from the sparse, noisy observation of it, . Our interest is in evaluating the estimation error with respect to the -error. As stated earlier, the estimation error for HSVT is typically evaluated with respect to the Frobenius norm and this quantity is well understood, e.g., see [18]. On the other hand, the error bound with respect to -norm is unknown. To that end, we provide a novel characterization of this error in Lemma 3.1 below (proof in Appendix I).

Let with its singular values arranged in descending order. Let denote the truncation of obtained by retaining the top components.

3.2.2 Low-Rank Covariates, Well-Balanced Spectra

We state the following result for PCR when the covariate matrix is low-rank, i.e., admits a low-dimensional representation, and PCR chooses the correct number of principal components.

Property 3.4.

Let denote the rank of . The -th largest singular value (i.e., the smallest nonzero singular value) of satisfies .

Property 3.4 combined with Property 3.1 imply the singular spectrum of is “well-balanced” in the sense that . Below, we describe another natural setting under which Property 3.4 holds.

Remark 3.3.

Corollary 3.1.

Interpretation. The statement of Corollary 3.1 requires that the correct number of principal components are chosen in PCR. In settings where all singular values of are roughly equal (Property 3.4), the training prediction decays (up to logarithmic factors) as . We note that for this exact low-rank setting, analyzing the case where (e.g., as done in [33]) is interesting future work.

Example: embedded Gaussian features. We present a classical data generating process under which PCR (and PCA) is justified. Consider the setting where is generated by sampling its rows from a distribution on , which in turn, is an embedding of some underlying latent distribution on ; this is similar in spirit to the probabilistic model for PCA, cf. [14, 40].

Proposition 3.1.

Let , where the entries of are independent standard normal random variables, i.e., and is another random matrix with independent entries drawn uniformly at random from . Suppose, and Then and Property 3.4 holds with probability at least for some constant .

In a strict sense, in Proposition 3.1 does not satisfy Property 3.1 because of the extra factor. Taking a closer look at the proof of Lemma 3.1, we can see that this slack only makes the exponent of the log slightly larger () in Lemma 3.1 and Corollary 3.1. Proof of Proposition 3.1 can be found in Appendix N.1.

3.2.3 Beyond Low-Rank Covariates—Low-Rank Approximation in -norm

In Corollary 3.2, we generalize the result of Corollary 3.1 to the setting where the low-rank model is misspecified, i.e., does not equal .

Corollary 3.2.

Interpretation. Corollary 3.2 implies the training prediction error, not including the linear model mismatch , decays to zero if: (i) the gap between the -th and -st singular values of grows faster than (ignoring log factors); (ii) ; (iii) . Below, we show that if the spectrum of is geometrically decaying, then there exists a range of such that Properties 3.1, 3.2, and 3.3 are satisfied.

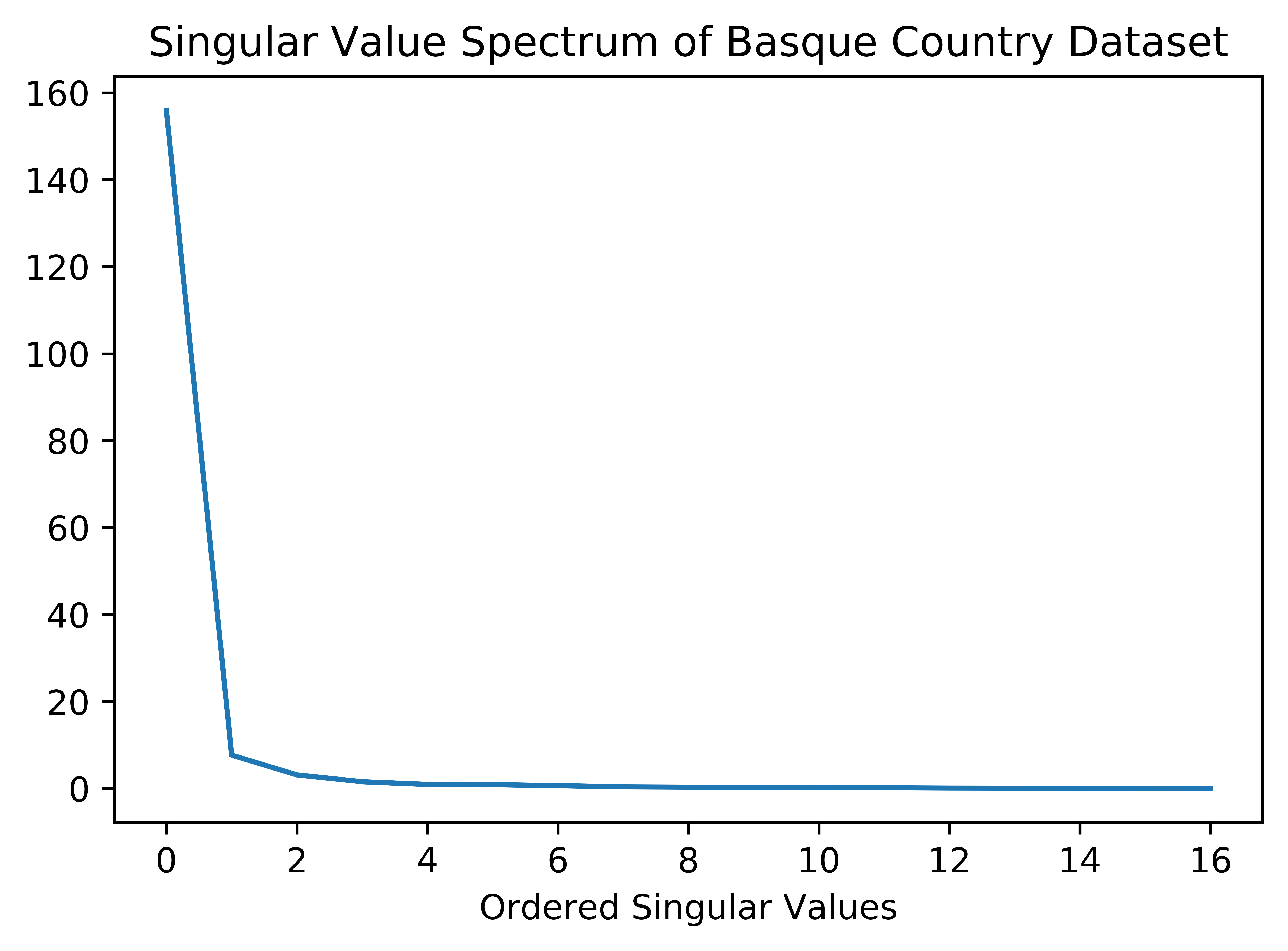

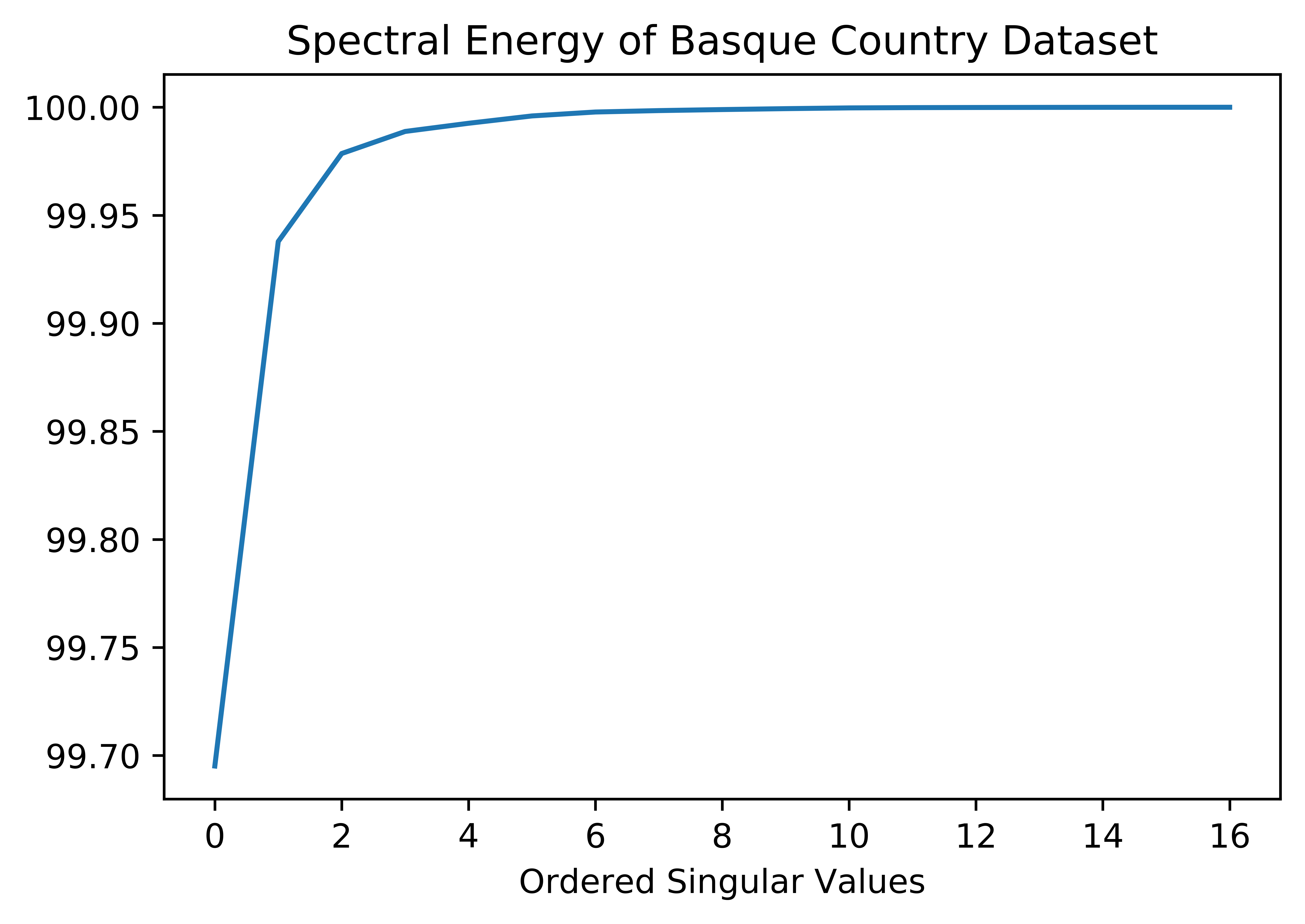

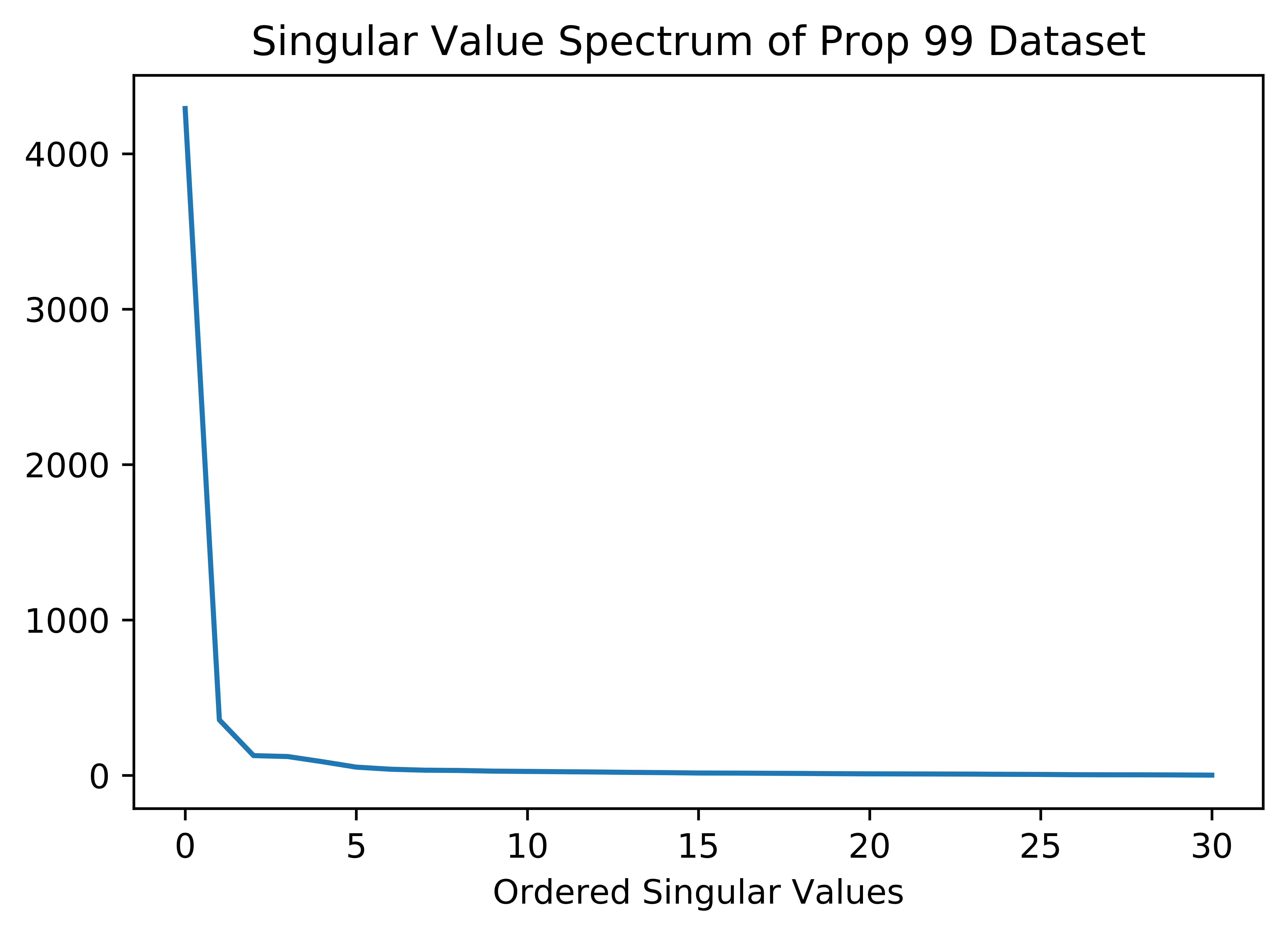

Example: geometrically decaying singular values. To explain the utility of Corollary 3.2, we consider a setting where has geometrically decaying singular values, and is thus approximately low-rank. We note that such a setting is representative of many real-world datasets; as an example, see Figures 3(a) and 5(a). Further, matrices with geometrically decaying singular values are also ubiquitous models in the study of a variety of domains including graphon estimation and signal processing.

Let denote the -th canonical basis vector. Recall that , and denote the left singular vectors, right singular vectors, and singular values of , respectively.

Proposition 3.2.

Interpretation. The conditions on the spectrum of in Proposition 3.2 are self-explanatory with potentially one exception, . In effect, this assumption states that the right singular vectors of satisfy an “incoherence” condition, cf. [15], with the canonical basis of ; or, equivalently, all entries of the right singular vectors are roughly of the same magnitude, . See Appendix N.3 for an explicit construction of such a matrix from signal processing. The bound in Proposition 3.2 implies that if the number of principal components is chosen as and , then the training prediction error is dominated by . This is precisely the unavoidable linear model mismatch error.

3.2.4 Beyond Low-Rank Covariates—Low-Rank Approximation in -norm

Thus far, in Sections 3.2.2 and 3.2.3, has been assumed to be well-approximated by a specific low-rank matrix that is induced by retaining the top singular values of . Such an approximation is optimal with respect to Frobenius and spectral norm. However, for approximating with respect to other norms, e.g., or , exciting progress has been made to obtain different styles of low-rank approximations (see for example [43, 48] and references therein). Indeed, such low-rank approximations of may not correspond to . For that reason, we provide an analogous result to Lemma 3.1 and Corollary 3.2 for the setting when is well-approximated by some arbritrary low-rank matrix.

Specifically, let . In words, denotes a low-rank matrix and denotes the approximation error between and . Let and let the SVD of (again, with the singular values arranged in descending order).

Lemma 3.2.

Interpretation. Lemma 3.2 is similar to the result of Lemma 3.1; however, because we now only assume that is well-approximated by an arbitrary low-rank matrix rather than as done in Section 3.2.3, this introduces an additional term compared to the bound in Lemma 3.1.

Corollary 3.3.

Interpretation. If satisfies Property 3.4, i.e., the well-balanced spectra condition, then one can verify (again, ignoring log factors) the prediction error scales as . This is identical to the bound in Corollary 3.1 with an additional term, which arises since is not assumed to be low-rank but rather is well-approximated by an arbitrary low-rank matrix . Below, we show that under a generalized factor model, vanishes to zero as grows.

Example: generalized factor model. We say the is generated as per a generalized factor model or latent variable model (LVM) if

| (12) |

where and are latent features that capture measurement and feature specific information, respectively, for some ; and the latent function captures the model relationship. If is “well-behaved”, e.g., Hölder continuous, and the latent spaces are compact, then Proposition 3.3 shows is well approximated by a low-rank matrix with respect to the -norm, where the approximation error vanishes as more data is collected.

Hölder continuous functions. We now define the Hölder class of functions, which is widely adopted in the non-parametric regression literature (see [48, 41]). Given a function , and a multi-index , let the partial derivate of at (if it exists) be denoted as

| (13) |

Definition 3.1 (-Hölder Class).

Let be two positive numbers. The Hölder class on is defined as the set of functions whose partial derivatives satisfy

| (14) |

Here, denotes the largest integer strictly smaller than . We note that the domain is easily extended to any compact subset of .

Remark 3.4.

Note if , then (14) is equivalent to the -Lipschitz condition, i.e.,

However, for , -Hölder smoothness no longer implies -Lipschitz smoothness.

Proposition 3.3.

Remark 3.5.

We remark on the Hölder continuity of a typical linear factor model, i.e., for some latent vectors . It is easily seen that such a model satisfies Definition 3.1 for all , and , for some absolute positive constant, . Thus, one can think of Hölder continuous functions as generalizations of typical linear factor models to sufficiently smooth non-linear functions.

Corollary 3.4.

3.3 Test Prediction Error

We now evaluate the generalization performance of PCR. As previously mentioned, the emphasis of this work is to provide a rigorous analysis on the prediction properties of the PCR algorithm through the lens of HSVT. Recall from Proposition 2.1, PCR with parameter is equivalent to linear regression with pre-processing of the noisy covariates using HSVT where the top singular values are retained. To that end, we study candidate vectors . In light of this observation, we establish the following simple but useful result that suggests restricting our model class to sparse linear models only (the proof of which can be found in Appendix L).

Proposition 3.4.

Let and . Without loss of generality, let form a collection of linearly independent vectors, i.e., for any , there exists some such that . Assume the following condition on holds:

| (16) |

Then if, for some , there exists such that , , and .

Interpretation. By Proposition 3.4, for any and , there exists a such that where and . Thus, for the purposes of bounding the test error of PCR with parameter via the toolkit of Rademacher complexity, it suffices to restrict our hypothesis class to linear predictors with sparsity . Condition (i) in Proposition 3.4 is a mild assumption circumventing the pathological case that the linear coefficients used to represent columns for in terms of are unbounded.

Theorem 3.2 (Test Error of PCR).

Interpretation. We note all our training error bounds do not depend on ; see (5), (24), (8), (9), (11), (15). Hence, the bound on also does not depend on for these settings. Note the test error decays at a rate , in comparison with for the training error. This “slow rate” of for test error is indeed the best achievable using the standard Rademacher complexity analysis (see Chapter 4 of [46]). An important open problem is to achieve the fast rate of for the test error in the error-in-variables setting; we remark that a related work [4] takes key steps towards solving this.

Choosing . We describe how the test prediction error can help in choosing the parameter for PCR (model complexity) in a data-driven manner. Specifically, Theorem 3.2 suggests that the overall error is at most the training error plus a term that scales as . Therefore, one should choose the that minimizes this bound. Naturally, as increases, the training error is likely to decrease, but the additional term will increase; an optimal can thus be found in a data-driven manner.

3.4 Discussion

Comparison with ordinary least squares (OLS). It is known that OLS implicitly performs regularization if the covariates are exactly low-rank, noiseless, and fully observed (see Lemma 3.1 of [36]). In most real-world settings, however, data is never precisely low-rank, but is rather approximately low-rank, such as in the examples detailed in Sections 3.2.3 and 3.2.4 (see [42] and references therein for further theoretical justification for approximately low-rank covariate matrices). In such a setting, it is not established, nor is it likely, that OLS has the same implicit regularization effect as before. Indeed, in the example shown in Figure 2(c), OLS has very poor empirical generalization performance even though over of the spectral energy is captured in the top singular value, i.e., the covariate matrix is very-well approximated by a rank-one matrix. In contrast, if the principal components are chosen correctly, then PCR continues to have the desired regularization property, even in the approximate low-rank case. The contrast can be seen in Figure 4(a). Additionally, we provide the explicit tradeoff between training and testing error based on the number of selected principal components .

“Information” spread across covariates is necessary. Within the high-dimensional (error-in-variables) regression literature, there are several different structural assumptions required of the covariate matrix to achieve vanishing prediction or parameter estimation error (see [34] and references therein for some detailed examples). Intuitively, these assumptions state that the signal is “well-spread” across the various columns of the covariate matrix. Below, we consider a simple yet illustrative example for which both PCR and traditional methods from the literature do not seem to provide meaningful answers.

Example. Suppose and , where are the canonical basis vectors in , and . Then, it is clear that .

What happens to PCR. To estimate , even with the additional (oracle) knowledge of the positions of and , one can verify the optimal estimators for and are and , respectively. This results in the following lower bound on the recovery error

yielding

which does not lead to prediction consistency. In fact, the second term, , is exactly what arises if the bias is not corrected in the error-in-variables regression setting of [31, 37, 11, 12].

What happens to traditional error-in-variables regression estimators. Now, consider the same setup as above but let be fully observed, i.e., . In such settings where is uncontaminated, it is known that the restricted eigenvalue (RE) condition (see Definition E.2 of Appendix E), which is the de-facto assumption in the literature, guarantees -recovery of the underlying via the Lasso method. However, this particular breaks the RE condition and thus cannot be accurately estimated. To see this, let in Definition E.2. Then, , hence violating the RE condition needed for all the existing analyses of methods for the error-in-variables regression setting.

In summary. From this simple example, we observe that a lack of information spread across the columns of seem to yield poor prediction and parameter estimation errors. However, it has been well established that a large ensemble of covariate matrices satisfy the RE condition; specifically, when the entries (or rows) of are sampled independently from a sub-gaussian distribution. Analogously, we show that two canonical generating processes for the covariate matrix, namely embedded Gaussian features and geometrically decaying singular values, satisfy the desired properties needed to achieve vanishing prediction error. That is, the singular value gap is sufficiently large under such generating processes for appropriate , where is the number of chosen principal components.

4 PCR and Synthetic Controls

4.1 Synthetic Controls Setup

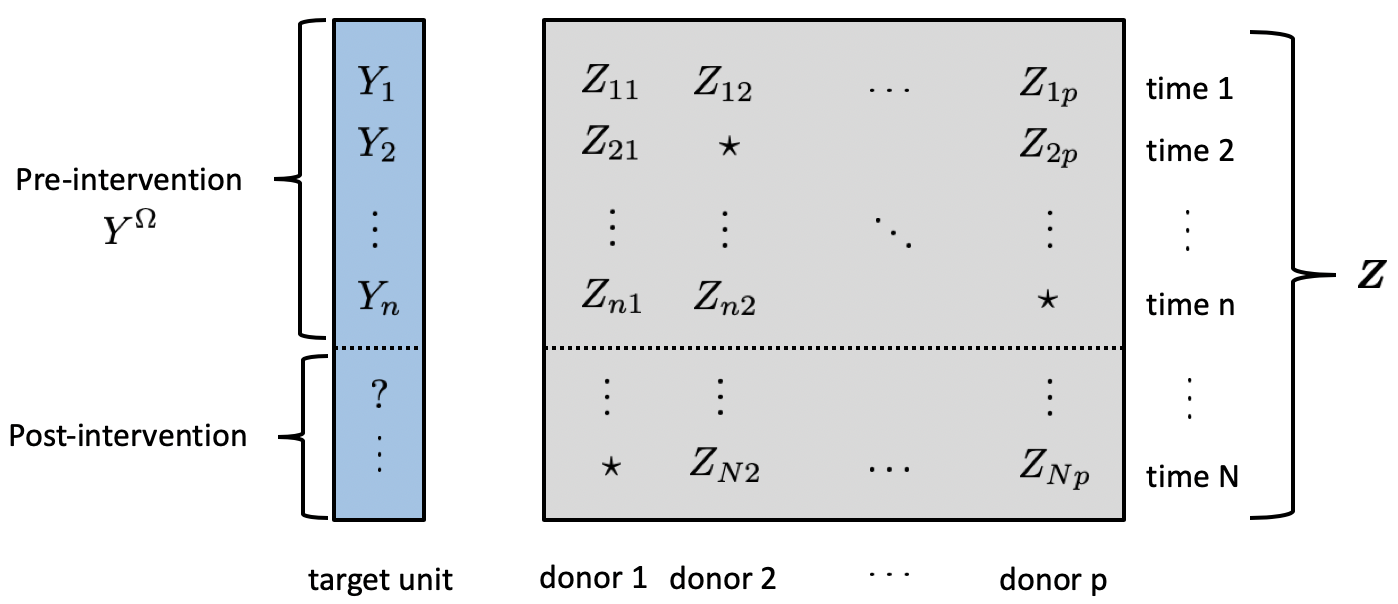

Pre- & post-intervention periods. As is standard in the SC literature, let there be different time series over periods associated with a target unit and donor units. Suppose the target unit receives the intervention at time period , where . We will refer to the pre- and post- intervention periods as the time periods prior to and after the intervention point.

Donor observations under control. Let represent the true utilities of the donor units across the entire time horizon in the absence of intervention; i.e., represents the time series over periods for donor . Rather than observing , we assume we are only given access to , a sparse, noisy instantiation of . In words, denotes the corrupted donor pool observations; as made precise later in the section, we assume follows the distributional characteristics described in Section 3.1.

Target unit observations under control. For every , let denote the noisy utility associated with the target unit in the absence of intervention (control). However, since the target unit experiences an intervention for all time instances , we only have access to a noisy version of the target unit’s utility for the pre-intervention period, i.e., we only observe for . Analogously, we denote for as the target’s (noisy) utility in the post-intervention period. We will denote as the true, latent utility at time for the target unit, if the intervention never occurred. In summary, given data , the aim is to recover , the counterfactual trajectory of the target unit under control in the post-intervention period. For a pictorial view of the setup of the problem, please refer to Figure 1.

4.2 (Approximate) Linear Synthetic Controls Exist

Existence of linear synthetic controls. In the SC literature, two standard assumptions are made: first, there exists a linear relationship between the target and donor units—in [1, 2], a more restrictive assumption is made that a convex relationship between the target and units exists; second, the underlying utilities follow a low-rank factor model.

Below, we show that if the underlying utilities of the target and donor units follow a generalized factor model or latent variable model (LVM) as in (12), then an (approximate) linear relationship between the target and donor units is actually implied by such a model. That is, the existence of an (approximate) linear synthetic control does not need to be additionally assumed. Further, we establish that the linear approximation error goes to zero the more data that is collected. As stated in Section 3.2.4, LVMs are a natural nonlinear generalization of the typical factor model ubiquitous in studying panel data in econometrics.

To that end, let denote the concatenation of , the latent donor pool utilities, with , the vector of underlying utilities for the target unit in the absence of an intervention. We denote as the latent true utility vector for the target unit, and for all as the latent true utilities for the donor pool. We assume follows a LVM as detailed below:

Property 4.1.

Interpretation. If satisfies a LVM as defined in (12), then the existence of as in Property 4.1 is simply a restatement of Proposition 3.3. To analyze SC, we make the additional mild assumption in Property 4.1 that lies within . This assumption helps avoid the “pathological” case where the right singular vector associated with the target unit, , does not lie within the span of the right singular vectors associated with the donor units, . Even in the worst case, by the definition of a rank of a matrix, there can only exist out of the right singular vectors that do not lie within the span of the remaining singular vectors. Indeed, we can pick as defined in Property 4.1, such that , rendering this pathological case overwhelmingly unlikely to hold. Lastly, we note this assumption that lies within is implicitly always made in the SC literature.

Proposition 4.1.

Interpretation. Proposition 4.1 shows that if follows a LVM as in (12), then a (approximate) linear synthetic control exists, where the linear misspecification error decays to zero for appropriate choice of in (18). Moreover, empirically a LVM is well-motivated – across many real-world datasets, including the canonical SC case studies of California Proposition 99 and terrorism in Basque Country of [1, 2], we see they exhibit an approximate (very) low-rank structure (see Figures 3(a), 3(b), 5(a), and 5(b)).

4.3 Synthetic Controls and Error-in-variables Regression

SC framework fits error-in-variables regression with model mismatch. If satisfies Property 4.1, Proposition 4.1 establishes that we can express the underlying utility of the target unit under no intervention for all as

| (19) |

Here is defined as in Proposition 4.1, and is the model mismatch bounded by . That is, in the SC framework, (1) holds under Property 4.1. In summary Proposition 4.1 reduces the question of interest in SC of estimating – the counterfactual trajectory of the target unit under no intervention in the post-intervention period – to that of linear regression with model mismatch. We note that we are in the error-in-variable setting as instead of observing , we only get to observe .

Restating objective in SC framework. Given (19), we can write the pre-intervention error as

| (20) |

and the post-intervention error as

| (21) |

(20) is precisely the training error defined in (2) and (21) is a slightly modified form of (3) since the objective now is to accurately estimate the counterfactual in the absence of any intervention only during the post-intervention stage. Observe that the objective in SC exactly fits the setting of transductive semi-supervised learning as described in Section 1.1.

4.4 Finite-sample Analysis of RSC via PCR

RSC is equivalent to PCR. The RSC method proposed by [5] has exhibited empirical success in duplicating the celebrated results of [1, 2] for the California Proposition 99 and terrorism in Basque Country case studies, respectively, using: (i) only the outcome data, i.e., without any usage of auxiliary covariates (ii) in the presence of noisy data. Under these two conditions, the classical SC algorithm of [1, 2] provides poor post-intervention predictions (see Figures 2(b) and 6(b)).

The RSC method is a three step procedure: (i) perform HSVT on the donor matrix (include both pre- and post-intervention data); (ii) linearly regress thresholded donor matrix with pre-intervention data of the target unit to learn linear weights for each of the donors; (iii) apply these linear weights on the post-intervention donor data to estimate the counterfactual trajectory for the target unit.

Observe that the RSC method is precisely the algorithm detailed in Section 2.1, of doing HSVT followed by OLS. Empirically, [5] demonstrated that the RSC method’s first step of pre-processing via HSVT effectively de-noises and imputes missing values in the donor observations, which is crucial in building a robust linear synthetic control that has good post-intervention performance. Pleasingly, by Proposition 2.1, we can equivalently interpret the RSC method as simply PCR.

It is worth noting that one of the primary motivations for utilizing convex regression (as proposed in [1, 2]) was to impose sparsity in the number of donors chosen, i.e., enforcing most of the coefficients of the synthetic control to be zero. Rather than introducing sparsity in the original donor space, PCR can be interpreted as introducing sparsity in the subspace induced by the right singular vectors corresponding to the donors since only the top few right singular components are retained. Indeed, as made precise by Proposition 3.4, PCR performs implicit -regularization on the learnt linear model.

Theoretical results. By viewing RSC via the lens of PCR, it allows us to bound the post-intervention prediction error for the target unit. We recall some necessary notation. Recall the definition of and from Section 4.1; the definition of from Section 4.2; and denote and as the de-noised donor matrix and the fitted linear model outputted from RSC, respectively.

Theorem 4.1.

Let satisfy Properties 3.1, 3.2, 3.3. Let satisfy: (i) (12) and further assume for , the latent parameters associated with time, are sampled i.i.d from some latent distribution ; (ii) Property 4.1 and further assume , the restriction of to the donor units, satisfies Property 3.4. Let satisfies (16) in Proposition 3.4. Let . Then,

| (22) |

where: ; and are defined as in Property 4.1; , with defined as in Proposition 3.4; is an absolute constant.

Interpretation. We highlight that Theorem 3.2 bounds , while Theorem 4.1 bounds . That is, Theorem 4.1 differs from Theorem 3.2 in that the set of observations for which we see labels (i.e., observations of the target in the pre-intervention period) is not assumed to be drawn uniformly at random. Such an assumption obviously cannot hold in the setting of SC as the pre-intervention period chronologically occurs before the post-intervention period. Instead, we make a more standard assumption that the latent features , which correspond to different time periods, are sampled i.i.d. from some unknown distribution, . Lastly, we leave it as open problem of how to achieve confidence intervals for the post-intervention error for RSC; one could possibly do so by extending our results to hold in high-probability rather than in expectation.

Comparison with related works in SC. The most relevant results to compare against are Corollary 4.1 (pre-intervention prediction error) and Theorem 4.6 (post-intervention prediction error) in [5]. To begin with, as in standard in the SC literature, [5] does not establish the existence of a synthetic control, rather it simply assumes one exists. Corollary 4.1 in [5] does not show consistency of the RSC method with respect to pre-intervention error as there is an irreducible term, , the measurement noise in the donor pool, that does not vanish. Further, with respect to post-intervention error, Theorem 4.6 of [5] suffers from the same irreducible term. In addition, the authors do not show that the second term of their bound decays to zero as more data is collected. As importantly, in both bounds, it is assumed that the RSC method picks the correct number of singular components, i.e., the rank of the underlying matrix of donor utilities is correctly chosen and is of a lower order compared to the ambient dimensions. In contrast, in our setting, we allow the low-rank condition of the underlying donor matrix to be misspecified, i.e., follows a generalization factor model. Finally, their result does not provide guidance for picking the right parameter for rank (or in PCR) as done by our result through the generalization or post-intervention error analysis.

Additionally, [6] considers a similar setting where the observed covariates are a corrupted version (additive noise model) of the true, underlying covariates , which follow an approximately low-rank factor model, i.e., cannot have too many large singular values (specifically, refer to Assumption 3 of [6]). However, they do not allow for missing data within . Here, the authors perform convex regression (with -norm constraints) along both the unit and time axes (unlike standard SC methods, such as RSC, which only consider regression along the unit axis) to estimate the causal average treatment effect. As is classically done in the SC literature, the authors of [6] assume that convex weights exist amongst the rows of ; in contrast, we show that (approximate) linear weights are directly implied by a (approximate) low-rank factor model. For this setting, they establish a rigorous asymptotic normality result for their causal estimand of interest, which is the average treatment effect of all treated units over the entire post-intervention period; in contrast, our target causal estimand is the entire post-intervention vector for each treated unit, for which we show mean squared error consistency at rate . The work of [6] complements our own in terms of clarifying the tradeoff between the assumptions made on (i.e., the low-rank approximation error), the constraints on the synthetic control weights (linear vs. convex), and the target causal estimand. Building on these works to explicitly define the tradeoff between what can be assumed on the spectra of , the synthetic control weights, and the subsequent results one can get for various target causal estimand is an interesting future research direction.

Another work that is less related, but is worth commenting on, as it also heavily relies on matrix estimation techniques for SC, is [7]. Here, the authors consider an underlying low-rank matrix of units and measurements per unit, and the entries of the observed matrix are considered “missing” once that unit has been exposed to a treatment. To estimate the counterfactuals, [7] applies a nuclear norm regularized matrix estimation procedure. Some key points of difference are that their performance bounds are with respect to the Frobenius norm over all entries (i.e., units and measurements) in the matrix; meanwhile, we provide a stronger bound that is specific to the single treated unit and only during the post-intervention period. Additionally, the bound of [7] depends on a parameter, which they denote as , that represents the minimum probability of observe all measurements associated with a given unit. The authors establish consistency of their estimator provided that . When data is randomly missing, even if the probability of observing each entry is for any , then ; thus, this result is not applicable for our setting.

4.5 Empirical Results

We present empirical results using the RSC method on several well-known datasets in the literature to highlight its robustness properties in comparison with the traditional SC estimator and OLS.

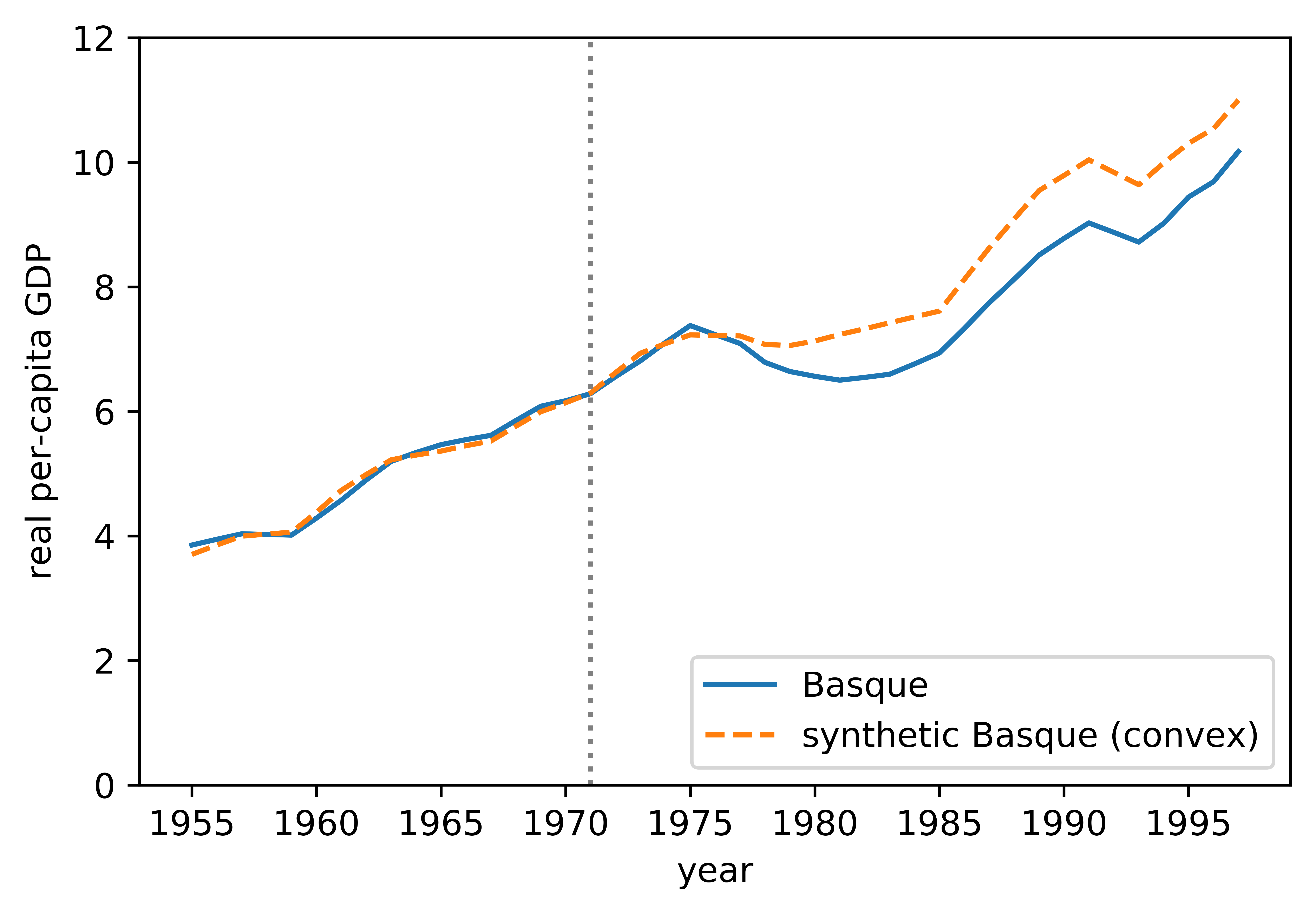

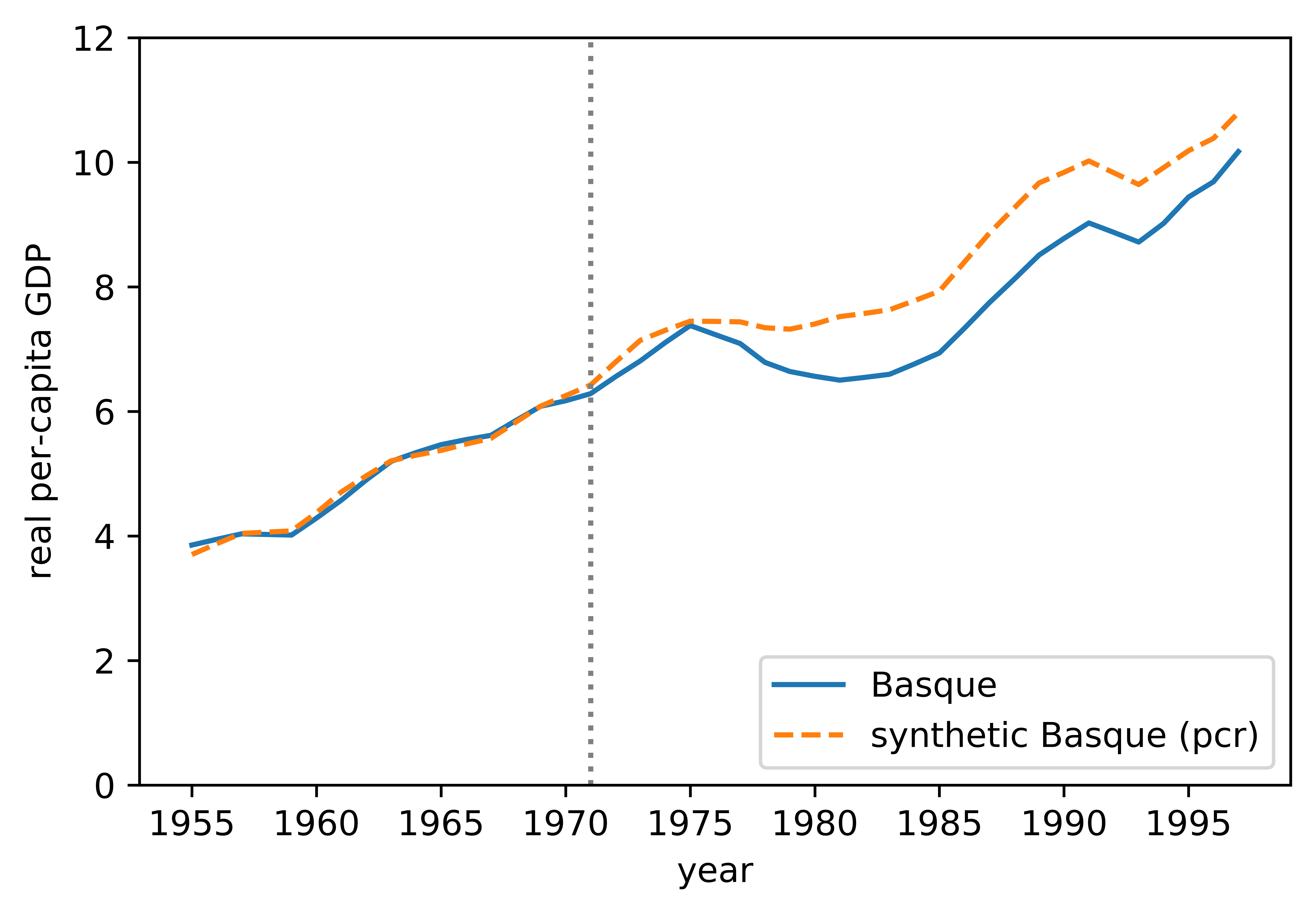

Terrorism in Basque Country. A canonical case study within the SC literature investigates the impact of terrorism on the economy in Basque Country (see [2]). Here, the target unit of interest is Basque Country, the donor pool consists of neighboring Spanish regions, and the intervention is represented by the first wave of terrorist activity in 1970. The aim in this study is to isolate the effect of terrorism on the GDP of Basque Country. In other words, to evaluate the effect of terrorism, SC-like methods aim to estimate the unobservable counterfactual GDP growth in the absence of terrorism for Basque Country using observations from various other Spanish regions, which are assumed to be unaffected by the terrorist activity.

Since we do not have access to the counterfactual realities of the Basque Country GDP post 1970 in the absence of terrorism, we will use the celebrated estimates of [2] as our baseline; this is our chosen “ground-truth” because these counterfactual trajectories of Basque’s GDP in the absence of terrorism have been widely accepted in the econometrics community. The resulting synthetic Basque is displayed in Figure 2(a).

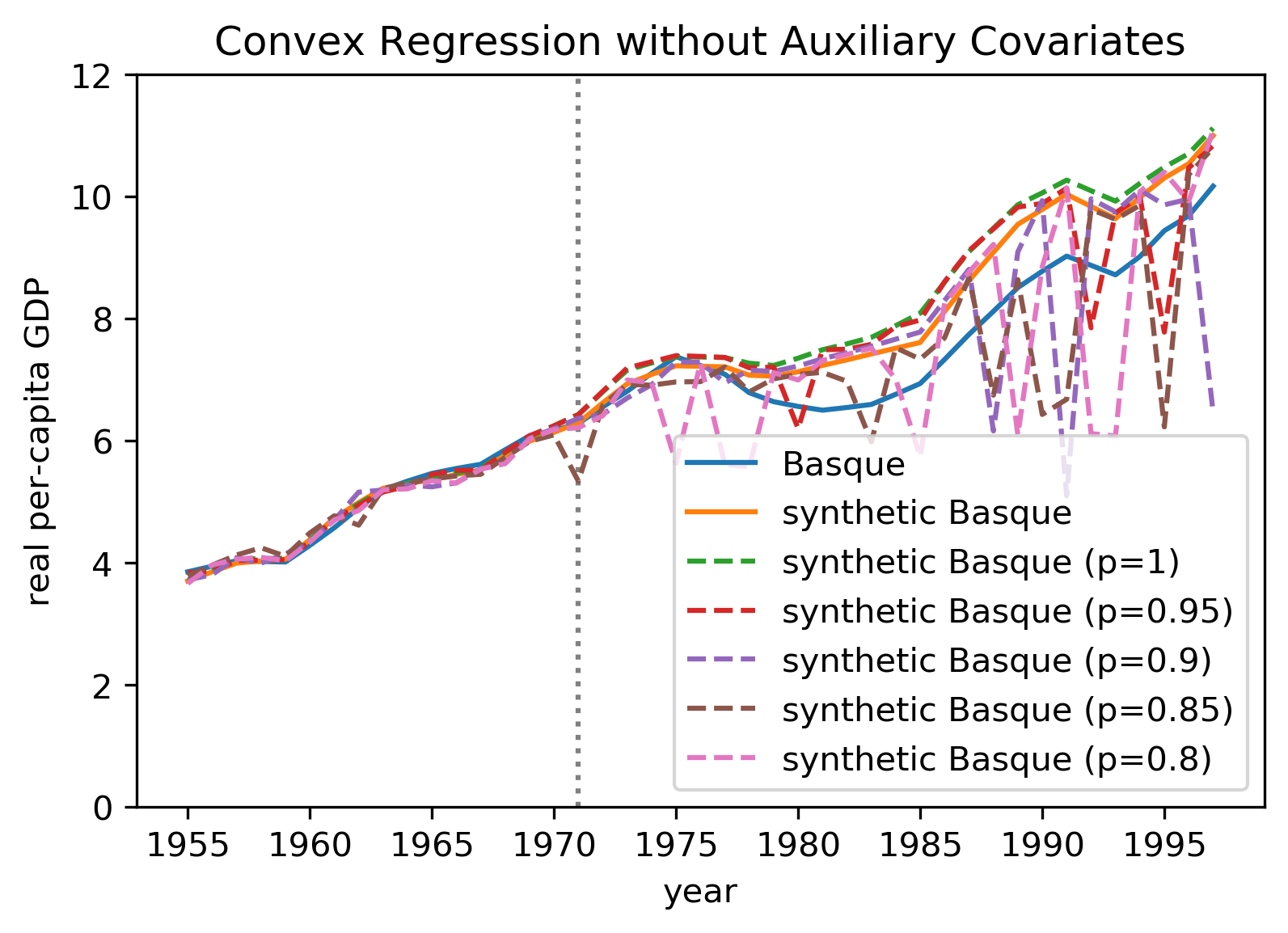

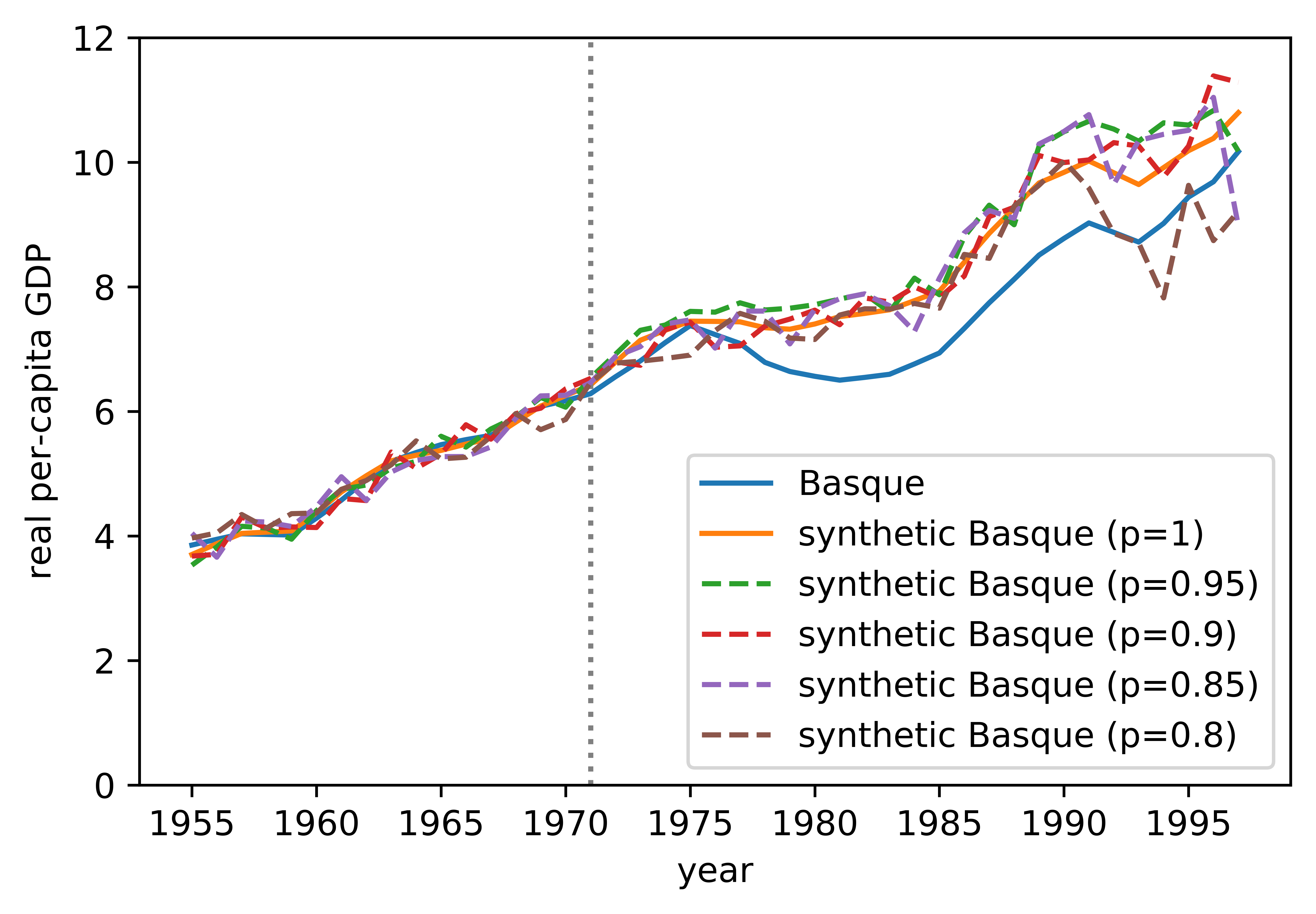

Classical SC and OLS under missing data. We randomly obfuscate data, ranging from 5-20%, and in Figure 2(b) we plot the resulting synthetic Basque GDPs predicted via convex regression on the outcome GDP data, i.e., the original SC method without auxiliary covariates – the solid blue and orange lines represent the observed and synthetic Basque (predicted by [2]), respectively, while the dashed lines represent the synthetic Basques under varying levels of missing data. As clearly seen from the figure, the original SC method is not robust to sparse observations, which may explain its dependency on auxiliary covariates to learn its model.

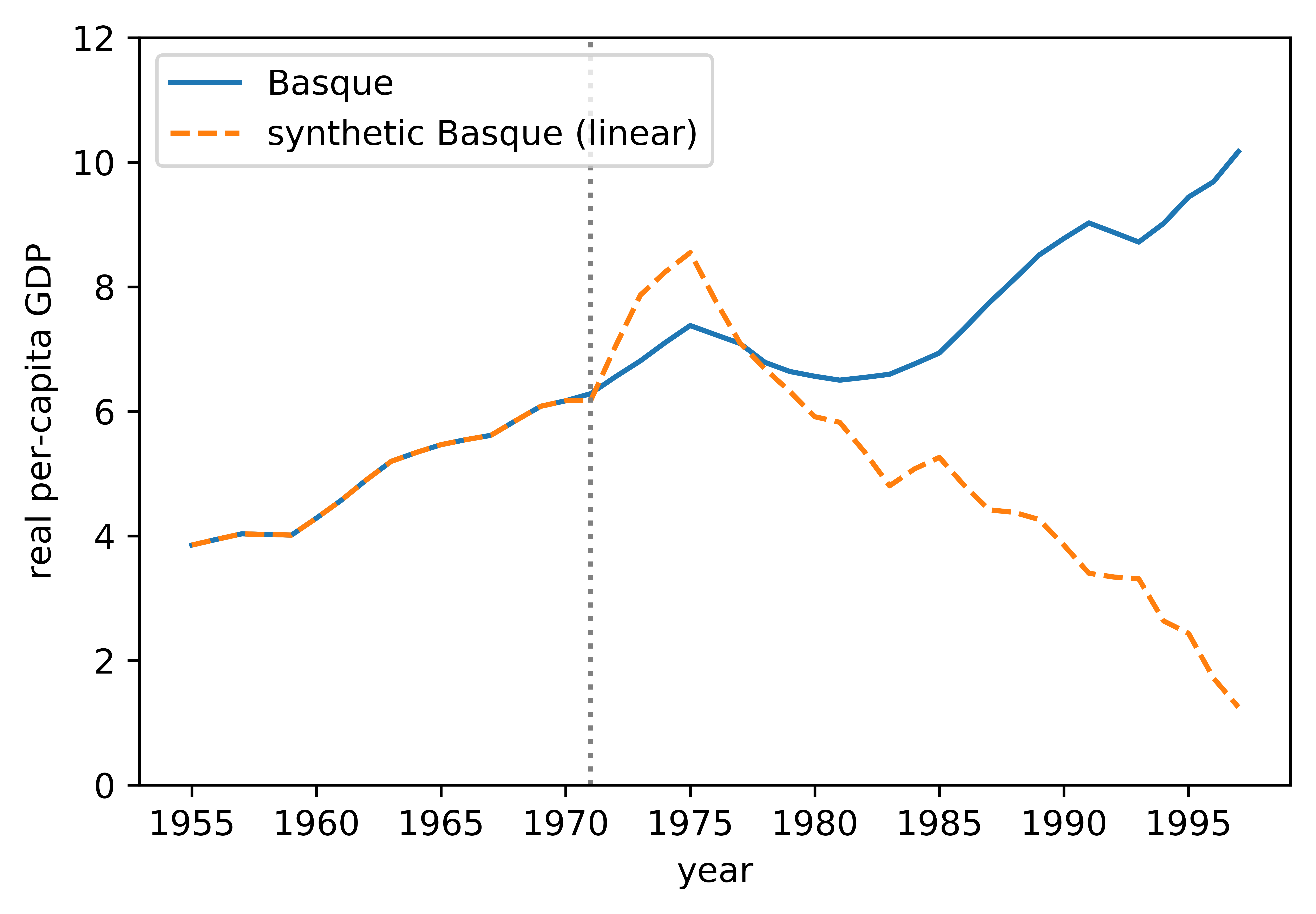

Additionally, we construct a synthetic Basque using OLS, i.e., running linear regression without any pre-processing of the donor observations (on only the outcome GDPs). As seen in Figure 2(c), OLS clearly overfits to the idiosyncratic noise of the pre-intervention data and fails to produce sensible post-intervention estimates. In fact, the synthetic Basque GDP as predicted by OLS suggests terrorism actually had a long-term benefit for the Basque economy! This example motivates the importance of appropriately regularizing and de-noising the donor data, as PCR does, prior to learning a synthetic control.

Importance of covariate pre-processing via PCA. The first step of PCR (i.e., PCA) is even more starkly empirically motivated by inspecting the singular value spectrum and cumulative energy of the Basque dataset, which are shown in Figures 3(a) and 3(b), respectively. The data exhibits low-dimensional structure with over 99% of the spectral energy captured in just the top singular value, which fits the setting under which our theoretical results imply low pre- and post-intervention prediction errors. The resulting synthetic Basque as per PCR (or, equivalently, the RSC method) is shown in Figure 4(a), which pleasingly closely matches that of [2]. Similarly, in Figure 4(b), we display various synthetic Basque GDPs after randomly obfuscating the donor observations. Across the varying levels of missing data from 5-20%, the synthetic Basque GDPs continue to resemble the baseline estimates of [2] such that the same conclusion on the negative economic effects of terrorism can be drawn.

Importantly, we underscore that all of the results computed via the PCR method shown in Figures 4(a) and 4(b) only use the outcome data (only the per-capita GDP values), i.e., the PCR estimator does not utilize the auxiliary covariate information that was required to achieve the results in [2]. Hence, PCR exhibits desirable robustness properties with respect to missing and noisy data, and with less stringent data requirements to achieve similar counterfactual estimates.

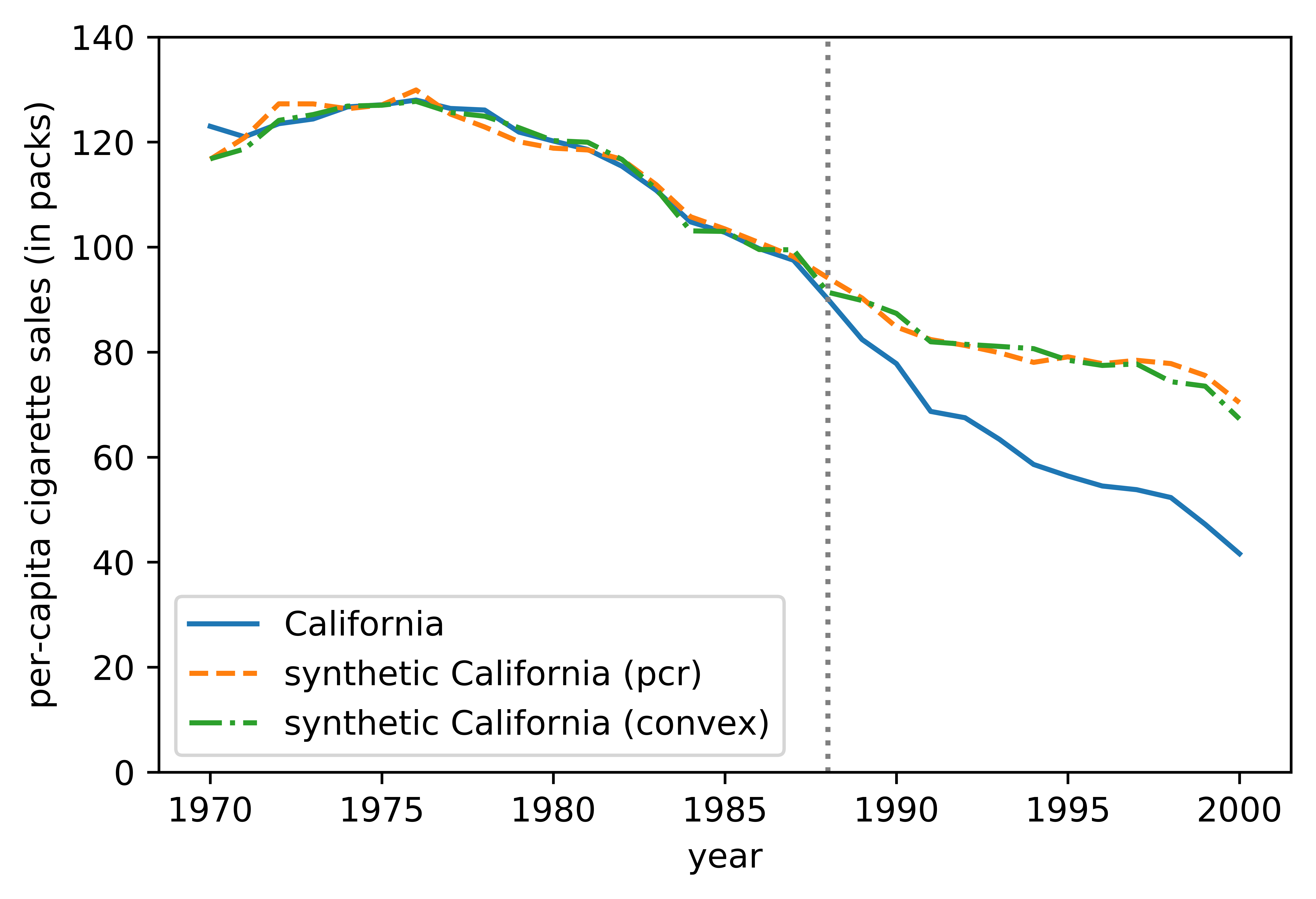

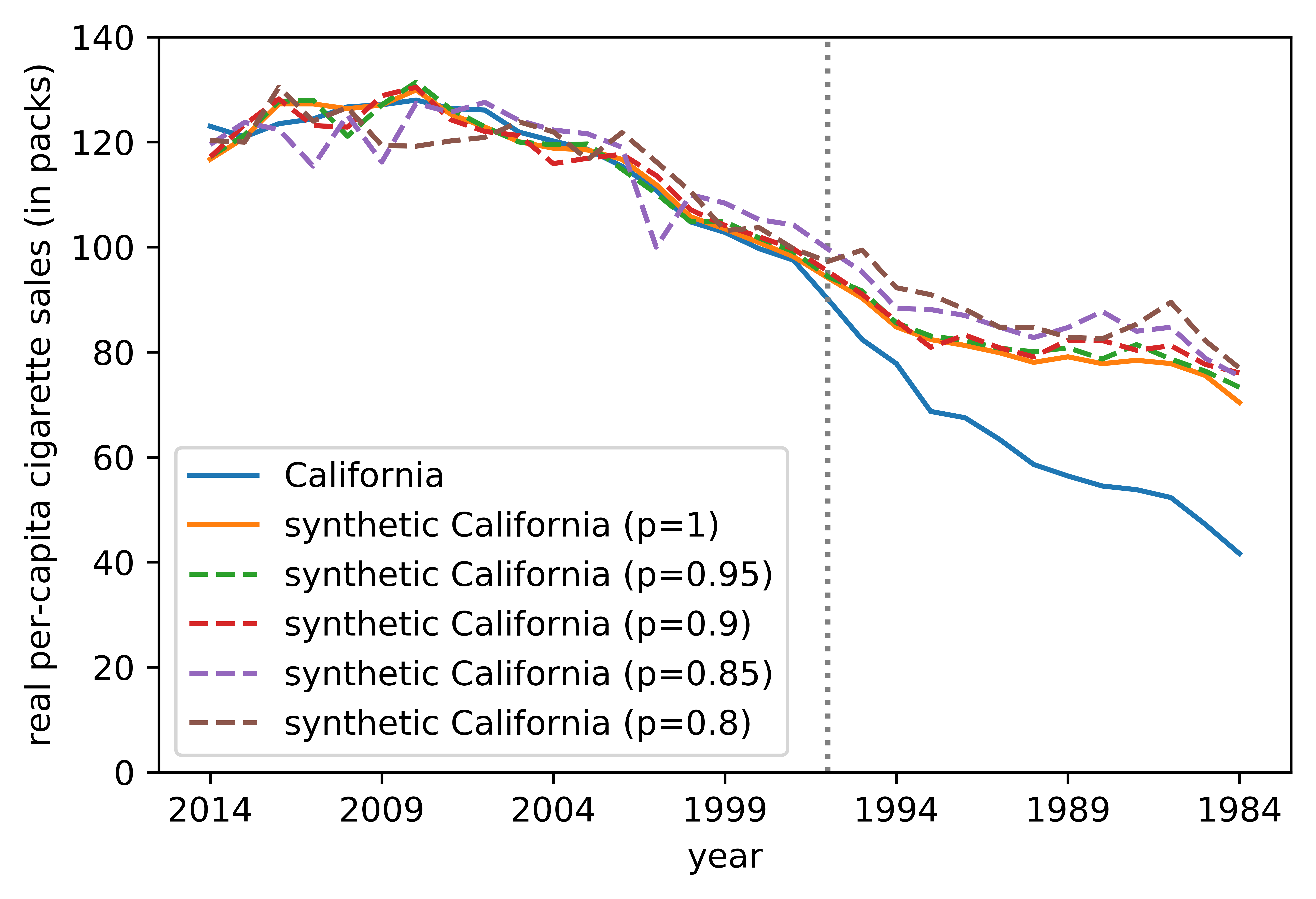

California Proposition 99. Another popular case study in the SC literature investigates the impact of California’s Proposition 99, an anti-tobacco legislation, on the per-capita cigarette consumption in the state (see [1]). Similar to the Basque example, we will use the widely accepted counterfactual estimate of [1] as our baseline, which is shown in Figure 6(a). Here, the authors of [1] considered California as the target state, the collection of states in the U.S. that did not adopt some variant of a tobacco control program as the donor pool, and Proposition 99 (enacted in 1988) as the intervention.

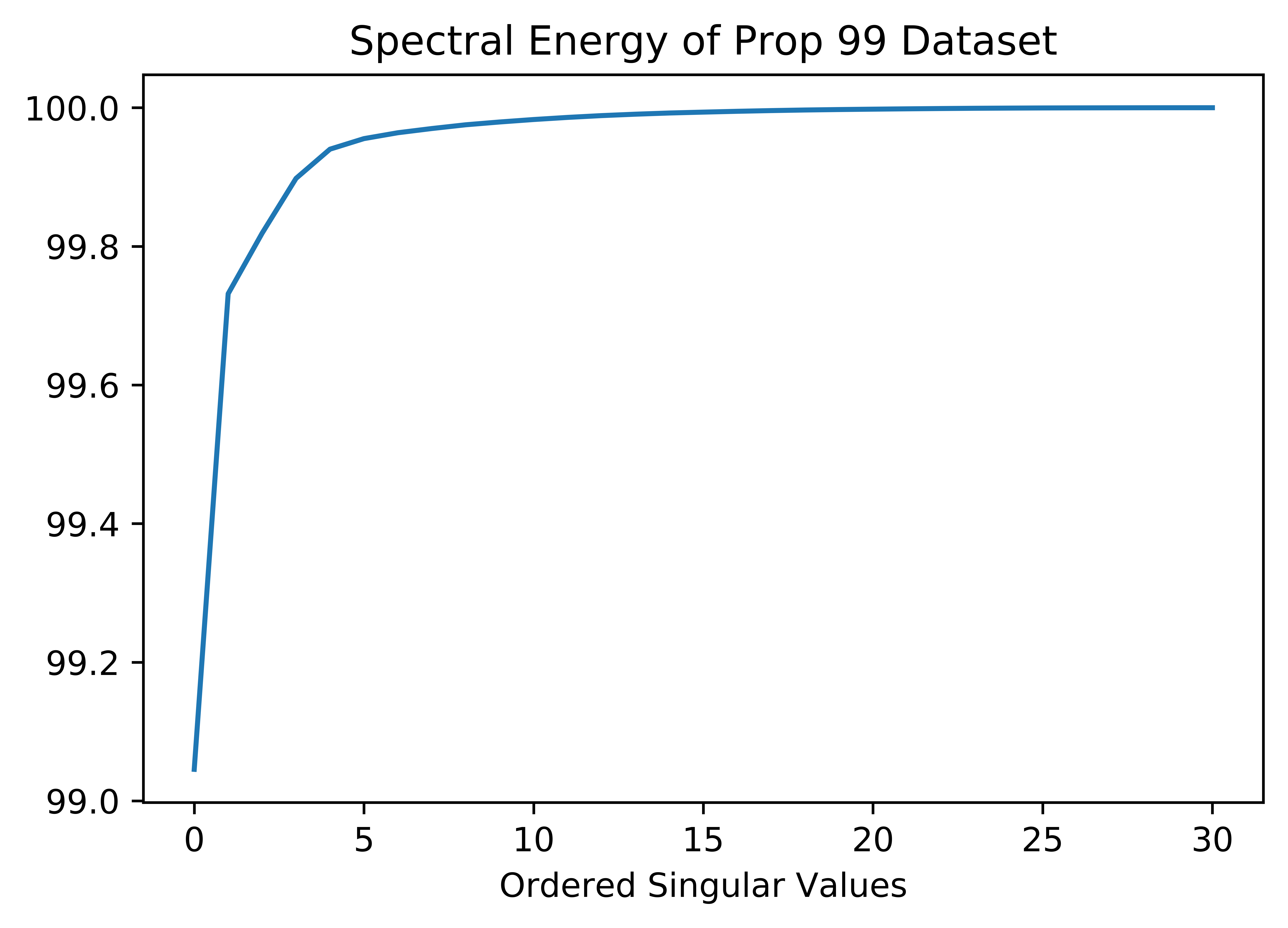

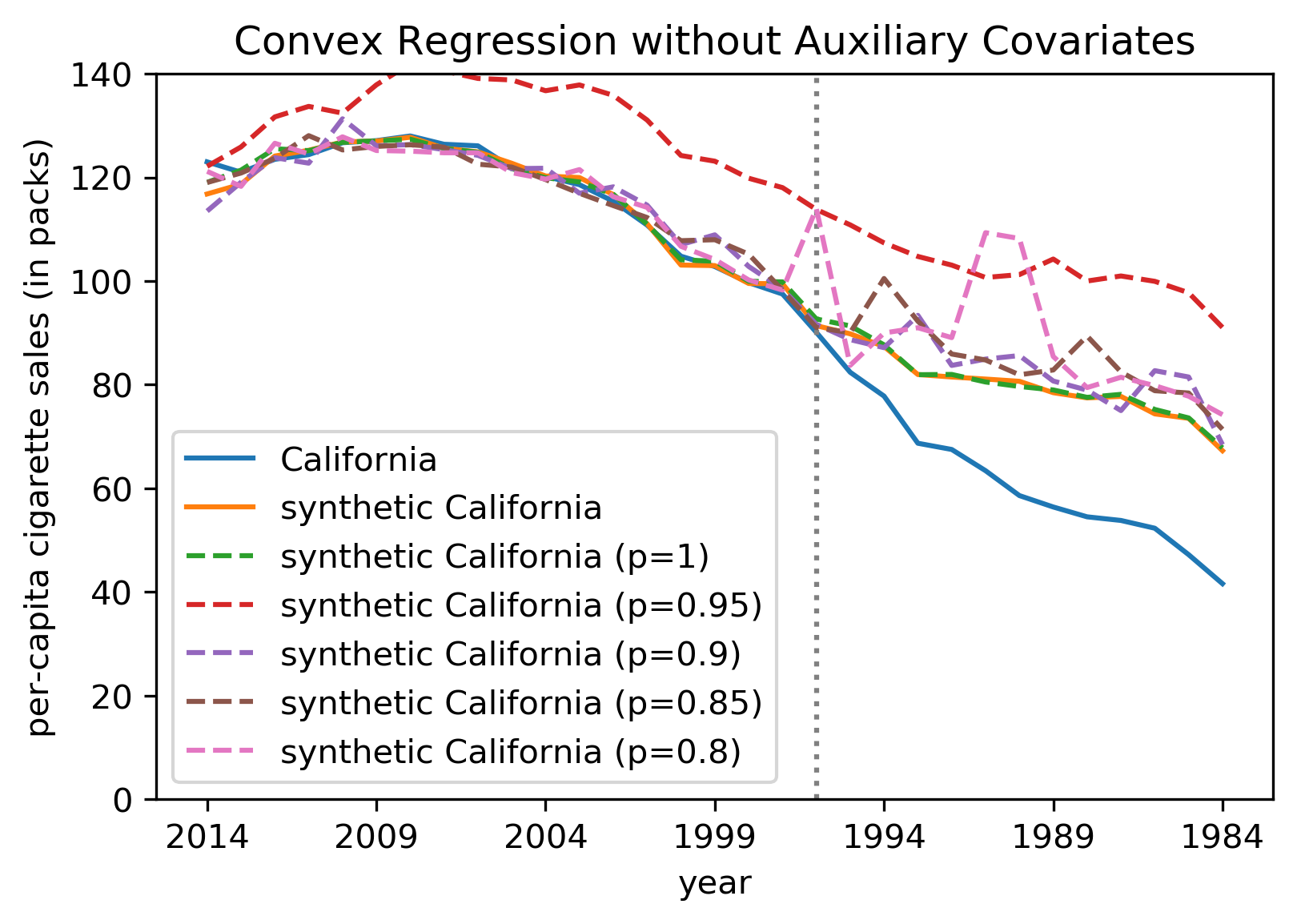

We again plot the resulting Californias learned via convex regression without auxiliary covariates and under varying levels of missing data (5-20%) in Figure 6(b); similar to the Basque case study, this highlights the poor performance of the original SC method in the presence of missing data. Further, we plot the singular value spectrum and energy of the California Proposition 99 dataset, seen in Figures 5(a) and 5(b), and observe that over 99% of the cumulative spectral energy is again captured by the top singular value, which fits the setting under which our theoretical results apply and motivates the application of PCR.

Empirically, we observe that the resulting synthetic California predicted via PCR, also displayed in Figure 6(a), closely matches the baseline, again without using any of the auxiliary covariates considered in the work of [1]. This is indeed expected from the theoretical analysis given the extremely low-dimensional structure of the data. Much like the previous Basque example, across the varying levels of missing data from 5-20%, the synthetic California per-capita cigarette consumption trajectories continue to mirror the baseline estimates of [1]—even in the presence of missing data, the counterfactual estimates produced by PCR suggest that Proposition 99 successfully cut smoking in California.

5 Conclusion

Summary of contributions. As the main contribution of this work, we address a long-standing problem of showing PCR (as is) is surprisingly robust to a wide array of problems that plague large-scale modern datasets, including high-dimensional and noisy, sparse, and mixed valued covariates. We provide meaningful non-asymptotic bounds for both the training and testing (transductive semi-supervised setting) errors for these settings, even when the covariate matrix is only approximately low-rank and the linear model is misspecified. From a practical standpoint, our testing error bound further provides guidance as to how to choose the PCR hyper-parameter in a data-driven manner. To achieving our formal results, we establish a simple, but powerful equivalence between PCR and linear regression with covariate pre-processing via HSVT; in the process, we provide a novel error analysis of HSVT with respect to the -norm. We then formally connect our theoretical results with three important applications to highlight the broad meaning of “noisy” covariates; namely, SC (measurement noise), differentially private regression (noise added by design), and mixed covariate regression (“structural” noise). Of particular note, given the equivalence between PCR and the RSC estimator, it immediately leads to a finite-sample bound for the post-intervention error of RSC under a generalized factor model, which is currently absent from the literature. We note that finite-sample analyses are absent for most SC estimators.

How to “robustify” an estimator. In essence, this work shows that the PCA component of PCR is an effective pre-processing tool in finding a linear low-dimensional embedding of the covariates, which carries the added benefits of implicit de-noising and -regularization. We postulate that when the covariate data is “unstructured” (e.g., speech or video), finding meaningful nonlinear low-dimensional embeddings of the data can also achieve similar implicit benefits, e.g., via a variational auto-encoder or a general adversarial network. We hope this work motivates a general statistical principle that to “robustify” a statistical estimator—first find a low-dimensional embedding of the data before fitting a prediction model.

References

- [1] A. Abadie, A. Diamond, and J. Hainmueller. Synthetic control methods for comparative case studies: Estimating the effect of californiaâs tobacco control program. Journal of the American Statistical Association, 2010.

- [2] A. Abadie and J. Gardeazabal. The economic costs of conflict: A case study of the basque country. American Economic Review, 2003.

- [3] R. Adamczak, A. E. Litvak, A. Pajor, and N. Tomczak-Jaegermann. Sharp bounds on the rate of convergence of the empirical covariance matrix. Comptes Rendus Mathematique, 349(3-4):195–200, 2011.

- [4] A. Agarwal, D. Shah, and D. Shen. On principal component regression in a high-dimensional error-in-variables setting, 2020.

- [5] M. J. Amjad, D. Shah, and D. Shen. Robust synthetic control. Journal of Machine Learning Research, 19:1–51, 2018.

- [6] D. Arkhangelsky, S. Athey, D. A. Hirshberg, G. W. Imbens, and S. Wager. Synthetic difference in differences. arXiv e-prints arXiv:1812.09970., 2018.

- [7] S. Athey, M. Bayati, N. Doudchenko, and G. Imbens. Matrix completion methods for causal panel data models. 2017.

- [8] S. Athey and G. Imbens. The state of applied econometrics - causality and policy evaluation. The Journal of Economic Perspectives, 31(2):3–32, 2016.

- [9] E. Bair, T. Hastie, D. Paul, and R. Tibshirani. Prediction by supervised principal components. Journal of the American Statistical Association, 101(473):119–137, 2006.

- [10] P. L. Bartlett and S. Mendelson. Rademacher and gaussian complexities: Risk bounds and structural results. J. Mach. Learn. Res., 3:463–482, Mar. 2003.

- [11] A. Belloni, V. Chernozhukov, A. Kaul, M. Rosenbaum, and A. B. Tsybakov. Pivotal estimation via self-normalization for high-dimensional linear models with errors in variables. arXiv:1708.08353, 2017.

- [12] A. Belloni, M. Rosenbaum, and A. B. Tsybakov. Linear and conic programming approaches to high-dimensional errors-in-variables models. Journal of the Royal Statistical Society, 79:939–956, 2017.

- [13] E. Ben-Michael, A. Feller, and J. Rothstein. The augmented synthetic control method, 2018.

- [14] C. M. Bishop. Bayesian pca. In Advances in neural information processing systems, pages 382–388, 1999.

- [15] E. Candes and J. Romberg. Sparsity and incoherence in compressive sampling. Inverse problems, 23(3):969, 2007.

- [16] E. J. Candès and T. Tao. The power of convex relaxation: Near-optimal matrix completion. IEEE Transactions on Information Theory, 56(5):2053–2080, 2010.

- [17] G. Chao, Y. Luo, and W. Ding. Recent advances in supervised dimension reduction: A survey. Machine Learning and Knowledge Extraction, 1(1):341–358, 2019.

- [18] S. Chatterjee. Matrix estimation by universal singular value thresholding. The Annals of Statistics, 43(1):177–214, 2015.

- [19] Y. Chen and C. Caramanis. Orthogonal matching pursuit with noisy and missing data: Low and high dimensional results. arXiv preprint arXiv:1206.0823, 2012.

- [20] A. Datta and H. Zou. Cocolasso for high-dimensional error-in-variables regression. The Annals of Statistics, 45(6):2400–2426, 2017.

- [21] C. Davis and W. M. Kahan. The rotation of eigenvectors by a perturbation. iii. SIAM Journal on Numerical Analysis, 7(1):1–46, 1970.

- [22] N. Doudchenko and G. Imbens. Balancing, regression, difference-in-differences and synthetic control methods: A synthesis. NBER Working Paper No. 22791, 2016.

- [23] C. Dwork and A. Roth. The algorithmic foundations of differential privacy. Foundations and Trends in Theoretical Computer Science, 9(3-4):211–407, 2014.

- [24] C. Hsiao, H. Steve Ching, and S. Ki Wan. A panel data approach for program evaluation: Measuring the benefits of political and economic integration of hong kong with mainland china. Journal of Applied Econometrics, 27(5):705–740, 2012.

- [25] C. Hsiao, S.-K. Wan, and Y. Xie. Panel data approach vs synthetic control method. Economics Letters, 164:121–123, 2018.

- [26] I. T. Jolliffe. A note on the use of principal components in regression. Journal of the Royal Statistical Society, 31(3):300–303, 1982.

- [27] A. Kaul and H. L. Koul. Weighted -penalized corrected quantile regression for high dimensional measurement error models. Journal of Multivariate Analysis, 140:72–91, 2015.

- [28] R. H. Keshavan, A. Montanari, and S. Oh. Matrix completion from a few entries. IEEE Transactions on Information Theory, 56(6):2980–2998, 2010.

- [29] K. T. Li. Inference for factor model based average treatment effects. Available at SSRN 3112775, 2018.

- [30] K. T. Li and D. R. Bell. Estimation of average treatment effects with panel data: Asymptotic theory and implementation. Journal of Econometrics, 197(1):65 – 75, 2017.

- [31] P.-l. Loh and M. J. Wainwright. High-dimensional regression with noisy and missing data: Provable guarantees with nonconvexity. The Annals of Statistics, 40(3):1637–1664, 2012.

- [32] R. Meir and T. Zhang. Generalization error bounds for bayesian mixture algorithms. Journal of Machine Learning Research, 4:839–860, 2003.

- [33] H. R. Moon and M. Weidner. Linear regression for panel with unknown number of factors as interactive fixed effects. Econometrica, 83(4):1543–1579, 2015.

- [34] G. Raskutti, M. J. Wainwright, and B. Yu. Restricted eigenvalue properties for correlated gaussian designs. J. Mach. Learn. Res., 11:2241–2259, Aug. 2010.

- [35] B. Recht. A simpler approach to matrix completion. Journal of Machine Learning Research, 12(Dec):3413–3430, 2011.

- [36] P. Rigollet and A. Tsybakov. Exponential screening and optimal rates of sparse estimation. Ann. Statist., 39(2):731–771, 04 2011.

- [37] M. Rosenbaum and A. B. Tsybakov. Sparse recovery under matrix estimation. The Annals of Statistics, 38(5):2620–2651, 2010.

- [38] M. Rosenbaum and A. B. Tsybakov. Improved matrix uncertainty selector. From Probability to Statistics and Back: High-Dimensional Models and Processes, 9:276–290, 2013.

- [39] D. Shah and D. Song. Learning mixture model with missing values and its application to rankings. arXiv preprint arXiv:1812.11917, 2018.

- [40] M. E. Tipping and C. M. Bishop. Probabilistic principal component analysis. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 61(3):611–622, 1999.

- [41] A. B. Tsybakov. Introduction to Nonparametric Estimation. Springer Publishing Company, Incorporated, 2008.

- [42] M. Udell and A. Townsend. Nice latent variable models have log-rank. CoRR, abs/1705.07474, 2017.

- [43] M. Udell and A. Townsend. Why are big data matrices approximately low rank? SIAM Journal on Mathematics of Data Science, 1(1):144–160, 2019.

- [44] R. Vershynin. Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027, 2010.

- [45] R. Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge University Press, 2018.

- [46] M. J. Wainwright. High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge University Press, 2019.

- [47] P.-Å. Wedin. Perturbation bounds in connection with singular value decomposition. BIT Numerical Mathematics, 12(1):99–111, 1972.

- [48] J. Xu. Rates of convergence of spectral methods for graphon estimation. arXiv preprint arXiv:1709.03183, 2017.

- [49] Y. Xu. Generalized synthetic control method: Causal inference with interactive fixed effects models. Econometrics: Multiple Equation Models eJournal, 2016.

6 Figures

Online Supplement:

On Robustness of Principal Component Regression

Anish Agarwal, Devavrat Shah, Dennis Shen, Dogyoon Song

MIT

Appendix A Related Works

We focus on the related literature pertaining to error-in-variable regression and PCR, but also include a brief discussion on the literature for matrix estimation/completion.

Error-in-variables regression. There exists a rich body of work regarding high-dimensional error-in-variable regression (see [31], [20], [37], [19], [27]). Three common threads of these works include: (1) making a sparsity assumption on ; (2) establishing error bounds with convergence rates for estimating under different norms, i.e., where denotes the -norm; (3) assuming the covariate matrix satisfying “incoherence”-like condition such as the Restricted Eigenvalue Condition, cf. [31]. In all of these works, the goal is to recover the underlying model, . In contrast, as discussed, the goal of PCR is to primarily provide good prediction. Some notable works closest to our setup include [31], [20], [38], which are described in some detail next.

In [31], a non-convex -penalization algorithm is proposed based on the plug-in principle to handle covariate measurement errors. This approach requires explicit knowledge of the unobserved noise covariance matrix and the estimator designed changes based on their assumption of . They also require explicit knowledge of a bound on the -norm of , the object they aim to estimate. In contrast, PCR does not require any such knowledge about the distribution of the noise matrix (i.e., the algorithm does not explicitly use this information to make predictions).

The work of [20] builds upon [31] by proposing a convex formulation of Lasso. Although the algorithm introduced does not require knowledge of , similar assumptions on and (e.g., sub-gaussianity and access to ) are made. This renders their algorithm to not be noise-model agnostic. In fact, many works (e.g., [37], [38], [11]) require either to be known or the structure of is such that it admits a data-driven estimator for its covariance matrix. This is so because these algorithms rely on correcting the bias for the matrix , which PCR does not need to compute.

It is worth noting that all these works in error-in-variables regression focus only on parameter estimation (i.e., learning ) and not explicitly de-noising the noisy covariates. Thus, even with the knowledge of , it is not clear how these methods can be used to produce predictions of the response variables associated with unseen, noisy covariates.

Principal Component Regression. A notable work is that of [9], which suggests a variation of PCR to infer the direction of the principal components. However, it stops short of providing meaningful finite sample analysis beyond what is naturally implied by that of standard Linear Regression. The regularization property of PCR is also well known, at least empirically, due to its ability to reduce the variance. As a contribution, we provide rigorous finite sample guarantees of PCR: (i) under noisy, missing covariates; (ii) when the linear model is misspecified; (iii) when the low-rank model for covariate matrix is misspecified.

As a further contribution, we argue that PCR’s regression model has sparse support (established using the equivalence between PCR and Linear Regression with covariate pre-processing via HSVT); this sparsity allows for improved generalization as the Rademacher complexity of the resulting model class scales with the sparsity parameter (i.e., the rank of the covariate matrix pre-processed with HSVT). Hence, PCR not only addresses the challenge of noisy, missing covariates, but also, in effect, performs implicit regularization.

Matrix estimation. Matrix estimation has spurred tremendous theoretical and empirical research across numerous fields (see [16, 28, 35, 18]), Traditionally, the end goal is to recover the underlying mean matrix from an incomplete, noisy sampling of its entries; the quality of the estimate is often measured through the Frobenius norm. Further, entry-wise independence and sub-gaussian noise is typically assumed. A key property of many matrix estimation methods is they are noise-model agnostic (i.e., the de-noising procedure does not change with the noise assumptions). We advance state-of-art for HSVT, arguably the most ubiquitous matrix estimation method, by (i) analyzing its error with respect to the -norm and (ii) allowing for a broader class of noise distributions (e.g., sub-exponential). Such generalizations are necessary to enable the various applications detailed in Section 4 and Appendices B and C.

Appendix B Differentially Private Regression

Setup and Question. With the increasing use of machine learning for critical operations, analysts must maximize the accuracy of their predictions and simultaneously protect sensitive information (i.e., covariates). An important notion of privacy is that of differential privacy; this requires that the outcome of a database query cannot greatly change due to the presence or absence of any individual data record (see [23] and references therein). More specifically, let be a positive real number, be a collection of datasets, and be a randomized algorithm that takes a dataset as input. The algorithm is said to provide -differential privacy if, for all datasets and in that differ on a single element, and all subsets , the following holds:

| (23) |

where the randomness lies in the algorithm. Thus, (23) guarantees that little can be learned about any particular record within the database.

The canonical mechanism to guarantee differential privacy is known as the Laplacian mechanism. In this setting, noise is drawn from a Laplacian distribution and added to query responses. In particular, introducing additive noise to any database query guarantees -privacy (see [23] and references therein); here, , where the maximum is taken over all pairs of datasets and in differing in at most one element, and is a vector-valued function denoting the true, latent query response. We now describe how PCR can be applied in the context of a differentially private framework.

How it fits our framework. Let denote the true, fixed database of sensitive individual records and covariates. We consider the setting where an analyst is allowed to ask two types of queries of the data: (1) - querying for individual data records, i.e., for ; (2) - querying for a linear combination of an individual’s covariates, i.e. . A typical example would be where is the genomic information for patient and denotes patient ’s outcome for a clinical study.

In order to provide -differential privacy, the Laplacian mechanism will return query responses with additive Laplacian noise. For query type (1), let for be the returned response; here, with probability and with probability , where for is independent Laplacian noise with the variance parameter proportional to ; we note that an auxiliary benefit of our setup is that it allows for a significant fraction of the query response to be masked, in addition to to the Laplacian noise corruption. For query type (2), when an analyst queries for the response variable , she observes , where is again independent Laplacian noise with variance parameter proportional to . We note that the above setup naturally fits our framework since the Laplacian distribution belongs to the family of sub-exponential distributions, i.e., satisfying Property 3.3 with .

Finally, let denote the noisy observed responses (e.g., corresponding to the outcomes of patient clinical trials), and let denote the noisy observed covariates (e.g., the collection of genomic information of all patients). Ultimately, the goal in such a setup is to accurately learn in- and out-of-sample global statistics (e.g., having low and , respectively) about the data, while preserving the individual privacy of the users.

Is privacy preserved? Lemma 3.1 demonstrates that the estimated covariate matrix via HSVT achieves small average -norm error (column-squared error); hence, for instance, HSVT can accurately learn the average age of all patients. However, this does not translate to accurately estimating the age of any particular patient – this would correspond to a small -norm error. Similarly, Corollary B.1 (stated below), establishes that PCR can estimate the vector well on average, but not any particular element of this vector. We leave it as an open question as to whether or not de-noising the covariate matrix through HSVT can give a -norm bound.

Results. We now state the following corollary, an instantiation of Corollary 3.1, which demonstrates the efficacy of PCR (with respect to prediction) in the context of differential privacy. We note a similar bound could easily be produced for any of the results in Section 3 – see (5), (24), (8), (9), (11), (15), (17) – by appropriately substituting with and with .

Corollary B.1.

Let the conditions of Corollary 3.1. Let be sampled independently from for . Let be sampled independently from . Let . Then, PCR preserves -differential privacy of and with

| (24) |

where and is an absolute constant.

Proof.

Proof is immediate from Corollary 3.1 by substituting with and with . ∎

Interpretation. From Corollary B.1, we observe that PCR learns a predictive linear model in a differentially private framework, where the covariates are purposefully contaminated with Laplacian noise to maintain -differential privacy.

Appendix C Regression with Mixed Valued Covariates

Setup and Question. Regression models with mixed discrete and continuous covariates are ubiquitous in practice. With respect to discrete covariates, a standard generative model assumes the covariates are generated from a categorical distribution (i.e., a multinomial distribution). Formally, a categorical distribution for a random variable is such that has support in and the probability mass function (pmf) is given by for with .

For simplicity, we focus on the case where the regression is being done with a collection of Bernoulli random variables (i.e., each has support in ). The extension to general categorical random variables is straightforward and discussed below.

A standard model in regression with Bernoulli random variables assumes that the response variable is a linear function of the latent parameters of the observed discrete outcomes. Formally, , where for is the latent Bernoulli parameter for the -th feature and -th measurement. Further, the mean of the response variable satisfies . However, for each feature, we only get binary observations, i.e., .

As an example, consider to be the expected health outcome of patient . Let there be a total of possible observable binary symptoms (e.g., cold, fever, headache, etc.). Then denotes the vector of (unobserved) probabilities that patient has some collection of symptoms (e.g., ). However, for each patient, we only observe the “noisy” binary outcome of these symptoms (i.e., ). Ideally, we get to observe the underlying probabilities of the symptoms as that is what we assume the response is linearly related to. The objective in such a setting is to accurately recover given and .

Current practice for mixed valued features. A common practice for regression with categorical variables is to build a separate regression model for every possible combination of the categorical outcomes (i.e., to build a separate regression model conditioned on each outcome). In the healthcare example above, this would amount to building separate regression models corresponding to each combination of the observed binary symptoms. This is clearly not ideal for the following two major reasons: (i) the sample complexity is exponential in ; (ii) we do not have access to the underlying probabilities (recall ), which is what we actually want to regress against.

How it fits our framework. Recall from Property 3.3 that the key structure we require of the covariate noise is that . Now even though , it still holds that , which immediately implies . Further, is sub-Gaussian () since . Thus, the key conditions on the noise are satisfied for PCR to effectively (in the -norm) de-noise to recover the underlying probability matrix ; this, in turn, allows PCR to produce accurate estimates through regression, as seen by Theorem 3.2.

Pleasingly, the required sample complexity grows with the rank of (the inherent model complexity of the underlying probabilities), rather than exponentially in . Further, the de-noising step allows us to regress against the estimated latent probabilities rather than their “noisy”, binary outcomes.

Extension from Bernoulli to general categorical random variables. Recall from above that a categorical random variable has support in for . In this case, one can translate a categorical random variable to a a collection of binary random variables using the standard one-hot encoding method. It is worth highlighting that by using one-hot encoding, clearly will not be independent of for any pair, which encodes the same categorical variable. However, from Property 3.3, we only require independence of the noise across rows, not within them. Thus this lack of independence is not an issue. Further, the generalization to multiple categorical variables, in addition to continuous covariates, is achieved by simply appending these features to each row and collectively de-noising the entire matrix before the regression step.

Appendix D Useful Theorems Known from Literature

D.1 Bounding -norm

Lemma D.1.

Sum of independent sub-gaussians random variables.

Let be independent, mean zero, sub-gaussian random variables. Then is also a sub-gaussian random variable, and

| (25) |

where is an absolute constant.

Lemma D.2.

Product of sub-gaussians is sub-exponential.

Let and be sub-gaussian random variables. Then is sub-exponential. Moreover,

| (26) |

D.2 Concentration Inequalities for Random Variables

Lemma D.3.

Bernstein’s inequality.