MS-0001-1922.65

Meta Dynamic Pricing

Meta Dynamic Pricing: Transfer Learning Across Experiments

Hamsa Bastani \AFFOperations, Information and Decisions, Wharton School, \EMAILhamsab@wharton.upenn.edu \AUTHORDavid Simchi-Levi \AFFInstitute for Data, Systems, and Society, Massachusetts Institute of Technology, \EMAILdslevi@mit.edu \AUTHORRuihao Zhu \AFFInstitute for Data, Systems, and Society, Massachusetts Institute of Technology, \EMAILrzhu@mit.edu

We study the problem of learning shared structure across a sequence of dynamic pricing experiments for related products. We consider a practical formulation where the unknown demand parameters for each product come from an unknown distribution (prior) that is shared across products. We then propose a meta dynamic pricing algorithm that learns this prior online while solving a sequence of Thompson sampling pricing experiments (each with horizon ) for different products. Our algorithm addresses two challenges: (i) balancing the need to learn the prior (meta-exploration) with the need to leverage the estimated prior to achieve good performance (meta-exploitation), and (ii) accounting for uncertainty in the estimated prior by appropriately “widening” the estimated prior as a function of its estimation error. We introduce a novel prior alignment technique to analyze the regret of Thompson sampling with a mis-specified prior, which may be of independent interest. Unlike prior-independent approaches, our algorithm’s meta regret grows sublinearly in , demonstrating that the price of an unknown prior in Thompson sampling can be negligible in experiment-rich environments (large ). Numerical experiments on synthetic and real auto loan data demonstrate that our algorithm significantly speeds up learning compared to prior-independent algorithms.

Thompson sampling, mis-specified prior, transfer learning, meta learning, empirical bayes

1 Introduction

Experimentation is popular on online platforms to optimize a wide variety of elements such as search engine design, homepage promotions, and product pricing. This has led firms to perform an increasing number of experiments, and several platforms have emerged to provide the infrastructure for these firms to perform experiments at scale (see, e.g., Optimizely 2019). State-of-the-art techniques in these settings employ bandit algorithms (e.g., Thompson sampling), which seek to adaptively learn treatment effects while optimizing performance within each experiment (Thompson 1933, Scott 2015). However, the large number of related experiments begs the question: can we transfer knowledge across experiments?

We study this question for Thompson sampling algorithms in dynamic pricing applications that involve a large number of related products. Dynamic pricing algorithms enable retailers to optimize profits by sequentially experimenting with product prices, and learning the resulting customer demand (Kleinberg and Leighton 2003, Besbes and Zeevi 2009). Such algorithms have been shown to be especially useful for products that exhibit relatively short life cycles (Ferreira et al. 2015), stringent inventory constraints (Xu et al. 2019), strong competitive effects (Fisher et al. 2017), or the ability to offer personalized coupons/pricing (Zhang et al. 2017, Ban and Keskin 2017). In all these cases, the demand of a product is estimated as a function of the product’s price (chosen by the decision-maker) and a combination of exogenous features as well as product-specific and customer-specific features. Through carefully chosen price experimentation, the decision-maker can learn the price-dependent demand function for a given product, and choose an optimal price to maximize profits (Qiang and Bayati 2016, Cohen et al. 2016, Javanmard and Nazerzadeh 2019). Dynamic pricing algorithms based on Thompson sampling have been shown to be particularly successful in striking the right balance between exploring (learning the demand) and exploiting (offering the estimated optimal price), and are widely considered to be state-of-the-art (Thompson 1933, Agrawal and Goyal 2013, Russo and Van Roy 2014, Ferreira et al. 2018).

The decision-maker typically runs a separate pricing experiment (i.e., dynamic pricing algorithm) for each product (or for a set of simultaneously-offered products). However, this approach can waste valuable samples re-discovering information that could have been learned from previously-offered related products. For example, students may be more price-sensitive than general customers; as a result, many firms such as restaurants, retailers and movie theaters offer student discounts. This implies that the coefficient of student-specific price elasticity in the demand function is positive for many products (although the specific value of the coefficient likely varies across products). Similarly, winter clothing may have higher demand in the fall and lower demand at the end of winter. This implies that the demand functions of winter clothing may have similar coefficients for the features indicating time of year. In general, there may even be complex correlations between coefficients of the demand functions of products that are shared. For example, the price-elasticities of products are often negatively correlated with their demands, i.e., customers are willing to pay higher prices when the demand for a product is high. When offering multiple products simultaneously, one must additionally learn cross-product price elasticities in the demand function (to model substitution effects), which may also exhibit patterns that can be learned from substitution patterns of related products in historical data. For example, substitution effects may be stronger between more similar products, or among more price-sensitive customers like students.

Thus, one may expect that the demand functions for related products may share some (a priori unknown) common structure, which can be learned across products. Note that the demand functions are unlikely to be exactly the same, so a decision-maker would still need to conduct separate pricing experiments for each product. However, accounting for shared structure during these experiments may significantly speed up learning per product (or per set of products, if offering multiple products simultaneously), thereby improving profits.

In this paper, we propose an approach to learn shared structure across pricing experiments. We begin by noting that the key (and only) design decision in Thompson sampling methods is the Bayesian prior over the unknown parameters. This prior captures shared structure of the kind we described above — e.g., the mean of the prior on the student-specific price-elasticity coefficient may be positive with a small standard deviation. It is well known that choosing a good (bad) prior significantly improves (hurts) the empirical performance of the algorithm (Chapelle and Li 2011, Honda and Takemura 2014, Liu and Li 2015, Russo et al. 2018). However, the prior is typically unknown in practice, particularly when the decision-maker faces a cold start. While the decision-maker can use a prior-independent algorithm (Agrawal and Goyal 2013), such an approach achieves poor empirical performance due to over-exploration; we demonstrate a substantial gap between the prior-independent and prior-dependent approaches in our experiments on synthetic and real data. In particular, knowledge of the correct prior enables Thompson sampling to appropriately balance exploration and exploitation (Russo and Van Roy 2014). Thus, the decision-maker needs to learn the true prior (i.e., shared structure) across products to achieve good performance. We propose a meta dynamic pricing algorithm that efficiently achieves this goal.

We first formulate the problem of learning the true prior online while solving a sequence of pricing experiments for different products. Our meta dynamic pricing algorithm requires two key ingredients. First, for each product, we must balance the need to learn about the prior (“meta-exploration”) with the need to leverage the prior to achieve strong performance for the current product (“meta-exploitation”). In other words, our algorithm balances an additional exploration-exploitation tradeoff across price experiments. Second, a key technical challenge is that finite-sample estimation errors of the prior may significantly impact the performance of Thompson sampling for any given product. In particular, vanilla Thompson sampling may fail to converge with an incorrect prior; as a result, directly using the estimated prior across products can result in poor performance. To this end, we introduce a novel “prior alignment” technique to analyze the regret of Thompson sampling with a mis-specified prior, which may be of independent interest.

Using our alignment technique, we show surprisingly that despite prior mis-specification, greedy updating of the prior is sufficient to learn effectively across pricing experiments when the prior covariance is known. However, when the prior has an unknown covariance matrix, it is beneficial to widen the estimated prior covariance by a term that is a function of the prior’s estimated finite-sample error. Thus, we use a more conservative approach (a wide prior) for earlier products when the prior is uncertain; over time, we gain a better estimate of the prior, and can leverage this knowledge for better empirical performance. Our algorithm provides an exact prior correction path over time to achieve strong performance guarantees across all pricing problems. We prove that, when using our algorithm, the price of an unknown prior for Thompson sampling is negligible in experiment-rich environments (i.e., as the number of products grows large).

1.1 Related Literature

Experimentation is widely used to optimize decisions in a data-driven manner. This has led to a rich literature on bandits and A/B testing (Lai and Robbins 1985, Auer 2002, Dani et al. 2008, Rusmevichientong and Tsitsiklis 2010, Besbes et al. 2014, Johari et al. 2015, Bhat et al. 2019). This literature primarily proposes learning algorithms for a single experiment, while our focus is on meta-learning across experiments. Meta-learning can take the form of constructing an empirical Bayesian prior (Raina et al. 2006, Anderer et al. 2019), data pooling (Gupta and Kallus 2020), or leveraging low-dimensional structure between problems (Bastani 2020). We take an empirical Bayesian approach to sequential decision-making. While there has been some prior work on meta-learning in bandits (Hartland et al. 2006, Maes et al. 2012, Wang et al. 2018, Sharaf and Daumé III 2019) and more generally in reinforcement learning (Finn et al. 2017, 2018, Yoon et al. 2018), these papers only provide heuristics for learning exploration strategies given a fixed set of past problem instances. They do not prove any theoretical guarantees on the performance or regret of the meta-learning algorithm. To the best of our knowledge, our paper is the first to propose a meta-learning algorithm in a bandit setting with provable regret guarantees.

We study the specific case of dynamic pricing, which aims to learn an unknown demand curve in order to optimize profits. We focus on dynamic pricing because meta-learning is particularly important in this application, e.g., online retailers such as Rue La La may run numerous pricing experiments for related fashion products. We believe that a similar approach could be applied to multi-armed or contextual bandit problems, in order to inform the prior for Thompson sampling across a sequence of related bandit problems.

Dynamic pricing has been found to be especially useful in settings with short life cycles or limited inventory (e.g., fast fashion or concert tickets, see Ferreira et al. 2015, Xu et al. 2019), among online retailers that constantly monitor competitor prices and adjust their own prices in response (Fisher et al. 2017), or when prices can be personalized based on customer-specific price elasticities (e.g., through personalized coupons, see Zhang et al. 2017). Several papers have designed near-optimal dynamic pricing algorithms for pricing a product by balancing the resulting exploration-exploitation tradeoff (Kleinberg and Leighton 2003, Besbes and Zeevi 2009, Araman and Caldentey 2009, Farias and Van Roy 2010, Harrison et al. 2012, Broder and Rusmevichientong 2012, den Boer and Zwart 2013, Keskin and Zeevi 2014). Recently, this literature has shifted focus to pricing policies that dynamically optimize the offered price with respect to exogenous features (Qiang and Bayati 2016, Cohen et al. 2016, Javanmard and Nazerzadeh 2019) as well as customer-specific features (Ban and Keskin 2017, Elmachtoub et al. 2020). We adopt the linear demand model proposed by Ban and Keskin (2017), which allows for feature-dependent heterogeneous price elasticities.

When sellers offer multiple products simultaneously, one may wish to perform price experiments jointly on a set of products to capture substitution effects or overlapping inventory constraints (Keskin and Zeevi 2014, Agrawal and Devanur 2014, Ferreira et al. 2018). However, in these papers, price experimentation is still performed independently on the current set of products, and any learned parameter knowledge is not shared across future sets of products to inform future demand learning. In contrast, we propose a meta dynamic pricing algorithm that learns the distribution of unknown parameters of the demand function across products. While we focus largely on the single-product setting for ease of exposition, we show how our algorithm and theoretical results carry over straightforwardly for multi-product settings with substitution effects; in fact, transfer learning from historical data may be even more valuable in these settings since the number of parameters (e.g., cross-product elasticities) to learn is much larger.

Our learning strategy is based on Thompson sampling, which is widely considered to be state-of-the-art for balancing the exploration-exploitation tradeoff (Thompson 1933). Several papers have studied the sensitivity of Thompson sampling to prior misspecification. For example, Honda and Takemura (2014) show that Thompson sampling still achieves the optimal theoretical guarantee with an incorrect but uninformative prior, but can fail to converge if the prior is not sufficiently conservative. Liu and Li (2015) provide further support for this finding by showing that the performance of Thompson sampling for any given problem instance depends on the probability mass (under the provided prior) placed on the underlying parameter; thus, one may expect that Thompson sampling with a more conservative prior (i.e., one that places nontrivial probability mass on a wider range of parameters) is more likely to converge when the true prior is unknown. It is worth noting that Agrawal and Goyal (2013) and Bubeck and Liu (2013) propose a prior-independent form of Thompson sampling, which is guaranteed to converge to the optimal policy even when the prior is unknown by conservatively increasing the variance of the posterior over time. However, the use of a more conservative prior creates a significant cost in empirical performance (Chapelle and Li 2011). For instance, Bastani et al. (2020) empirically find through simulations that the conservative prior-independent Thompson sampling is significantly outperformed by vanilla Thompson sampling even when the prior is misspecified.111We provide some theoretical support for this finding, since we show that limited prior mis-specification does not affect the rate of convergence (e.g., when the prior covariance is known but the mean is unknown). We empirically find, through experiments on synthetic and real datasets, that learning and leveraging the prior can yield much better performance compared to a prior-independent approach. As such, the choice of prior remains an important design choice in the implementation of Thompson sampling (Russo et al. 2018). We propose a meta-learning algorithm that learns the prior across pricing experiments on related products to attain better performance. We also empirically demonstrate that a naive approach of greedily using the updated prior performs poorly when the prior covariance is unknown, since it may cause Thompson sampling to fail to converge to the optimal policy for some products. Instead, our algorithm gracefully tunes the width of the estimated prior as a function of the uncertainty in the estimate over time.

1.2 Main Contributions

We highlight our main contributions below:

-

1.

Model: We formulate our problem as a sequence of different dynamic pricing problems, each with horizon . Importantly, the unknown parameters of the demand function for each product are drawn i.i.d. from a shared (unknown) multivariate Gaussian prior.

-

2.

Algorithm: We propose two meta-learning pricing policies, Meta-DP and Meta-DP++. The former learns only the mean of the prior, while the latter learns both the mean and the covariance of the prior across products. Both algorithms balance the need to learn the prior (meta-exploration) with the need to leverage the current estimate of the prior to achieve good performance (meta-exploitation). Meta-DP++ additionally accounts for uncertainty in the estimated prior by conservatively widening the prior as a function of its estimation error.

-

3.

Theory: Unlike standard approaches, our algorithm can leverage shared structure across products to achieve regret that scales sublinearly in the number of products . We prove upper bounds and on the meta regret of Meta-DP and Meta-DP++ respectively. In both cases, our meta-learning approach matches the performance of prior-independent algorithms for small , and outperforms them in experiment-rich experiments (i.e., when and respectively). A key ingredient of our analysis is a “prior alignment” proof technique that may be of general interest for analyzing the regret of mis-specified Thompson Sampling instances.

-

4.

Numerical Experiments: We demonstrate on both synthetic and real auto loan data that our approach significantly speeds up learning compared to ignoring shared structure (i.e., using prior-independent Thompson sampling).

2 Problem Formulation

For ease of exposition, we primarily focus on a seller offering a single product at a time. Our approach and results generalize straightforwardly when multiple products are offered simultaneously, where a seller must also learn cross-product elasticities to capture substitution effects (see extension in Appendix 12).

Notation:

Throughout the paper, all vectors are column vectors by default. We define to be the set for any positive integer We use to denote the norm of a vector but we often omit the subscript when we refer to the norm. For a matrix is the operator norm of For a positive definite matrix and vectors , let denote the matrix norm and denote the inner product . For two matrices and we use to denote their Kronecker product. We also denote and as the maximum and minimum between respectively. We use the standard notation and to characterize the asymptotic growth rate of a function (Cormen et al. 2009); when logarithmic factors are omitted, we use and . Finally, let and denote the minimum and maximum eigenvalues of a matrix respectively.

2.1 Model

We first describe the classical dynamic pricing formulation for a single product; we then formalize our meta-learning formulation over a sequence of products.

Classical Formulation:

Consider a seller who offers a single product over a selling horizon of periods. The seller can dynamically adjust the offered price in each period. At the beginning of each period , the seller observes a random feature vector (capturing exogenous and/or customer-specific features) that is independently and identically distributed from an unknown distribution. Upon observing the feature vector, the seller chooses a price for that period. The seller then observes the resulting demand, which is a noisy function of both the observed feature vector and the chosen price. The seller’s revenue in each period is given by the chosen price multiplied by the corresponding realized demand. The goal in this setting is to develop a policy that maximizes the seller’s cumulative revenue by balancing exploration (learning the demand function) with exploitation (offering the estimated revenue-maximizing price).

Meta-learning Formulation:

We consider a seller who sequentially offers related products, each with a selling horizon of periods. For simplicity, a new product is not introduced until the life cycle of the previous product ends.222We model epochs as fully sequential for simplicity; if epochs overlap, we would need to additionally model a customer arrival process for each epoch. Our algorithms straightforwardly generalize for overlapping epochs; see remark in §4.4. We call each product’s life cycle an epoch, i.e., there are epochs that last periods each. Each product (and corresponding epoch) is associated with a different (unknown) demand function, and constitutes a different instance of the classical dynamic pricing problem described above. We now formalize the problem.

In epoch at time , the seller observes a random feature vector , which is independently and identically distributed from a known distribution . She then chooses a price for that period. Based on practical constraints, we will assume that the allowable price range is bounded across periods and products, i.e., and . The seller then observes the resulting induced demand

where and are unknown fixed constants throughout epoch , and is i.i.d. Gaussian noise with variance This demand model was recently proposed by Ban and Keskin (2017), and captures several salient aspects. In particular, the observed feature vector in period determines both the baseline demand (through the parameter ) and the price-elasticity of the demand (through the parameter ) of product .

Example 2.1 (Rue La La)

Rue La La sells a limited set of new products in multi-day “events” (Ferreira et al. 2015). In this case, is the number of price changes during the event (events are typically 1-4 days, and prices are updated no more than a few times a day), is the number of events offered so far by the seller (note that ), and is the number of simultaneously-offered products in an event. For ease of exposition, we primarily consider , but Appendix 12 provides a straightforward extension to general values of , accounting for substitution effects.

Remark 2.2 (Alternative Demand Models)

Our demand model utilizes a continuous outcome variable, motivated by the setting where many customers simultaneously view the same product with the same price in a given time unit. One can alternatively modify the demand model to follow a generalized linear model (e.g., logistic) to consider a binary purchase outcome variable for each customer. Our proposed algorithms easily generalize by appropriately modifying our Bayesian posterior update rules; however, we restrict our regret analysis to the linear case since OLS Bayesian posterior updates have a closed form, yielding a tractable analysis.

Shared Structure:

For ease of notation, we denote ; following the classical formulation of dynamic pricing, is the unknown parameter vector that must be learned within a given epoch in order for the seller to maximize her revenues over periods. When there is no shared structure between the , our problem reduces to independent dynamic pricing problems.

However, we may expect that related products share a similar potential market, and thus may have some shared structure that can be learned from previously offered products. We model this relationship by positing that the product demand parameter vectors are independent and identically distributed draws from a common unknown distribution, i.e., for each .333Following the literature on Thompson sampling, we consider a multivariate Gaussian distribution since the posterior has a simple closed form, thereby admitting a tractable theoretical analysis. When implementing such an algorithm in practice, more complex distributions can be considered (e.g., see discussion in Russo et al. 2018). As discussed earlier, knowledge of the distribution over the unknown demand parameters can inform the prior for Thompson sampling, thereby avoiding the need to use a conservative prior that can result in poor empirical performance (Honda and Takemura 2014, Liu and Li 2015). The mean of the shared distribution is unknown; we will consider settings where the covariance of this distribution is known and unknown. We propose using meta-learning to learn this distribution from past epochs to inform and improve the current product’s pricing strategy.

Remark 2.3 (Product Features)

A complementary form of shared structure can be captured through product features. However, even after conditioning on observed product features, the demand functions for two products may behave very differently, e.g., two black dresses may cater to very different types of customers or have very different price elasticities due to attributes like fit or design that may be hard to capture as features. To capture product-specific (i.e., SKU-level) demand behaviors, we allow the coefficients of the demand function (e.g., price-elasticity) to differ.

2.2 Assumptions

We now describe some mild assumptions on the parameters of the problem for our regret analysis.

[Boundedness] The support of the features are bounded, i.e.,

Furthermore, there exists a positive constant such that Our first assumption is that the observed feature vectors as well as the mean of the product demand parameters are bounded. This is a standard assumption made in the bandit and dynamic pricing literature, ensuring that the expected regret at any time step is bounded. This is likely satisfied since features and outcomes are typically bounded in practice.

[Positive-Definite Feature Covariance] The minimum eigenvalue of the feature covariance matrix in every epoch is lower bounded by some positive constant , i.e.,

Our second assumption imposes that the covariance matrix of the observed feature vectors in every epoch is positive-definite. This is a standard assumption for the convergence of OLS estimators; in particular, our demand model is linear, and therefore requires that no features are perfectly collinear in order to identify each product’s true demand parameters.

[Positive-Definite Prior Covariance] The maximum and minimum eigenvalues of are upper and lower bounded by positive constants and respectively i.e.,

Our final assumption imposes that the covariance matrix of the random product demand parameter is also positive-definite and bounded. Again, this assumption ensures that each product’s true demand parameter is identifiable using standard OLS estimators.

2.3 Background on Thompson Sampling with Known Prior

In this subsection, we consider the setting where the true prior over the unknown product demand parameters is known. This setting will inform our definition of the meta oracle and meta regret in the next subsection. When the prior is known, a natural candidate policy for minimizing Bayes regret is the Thompson sampling algorithm (Thompson 1933). The Thompson sampling algorithm adapted to our dynamic pricing setting for a single epoch is formally given in Algorithm 1 below. Since the prior is known, there is no additional shared structure to exploit across products, so we can treat each epoch independently.

We denote TS as the Thompson sampling algorithm with prior and a positive input parameter for initialization. In line with pricing algorithms in the literature (see, e.g., Keskin and Zeevi 2014, Ban and Keskin 2017), to ensure that we can obtain a well-defined OLS estimate of the underlying parameter at the end of an epoch, our algorithm initially performs random price exploration (alternating between and ) until the Fisher information matrix has minimum eigenvalue of at least . Let be the (random) length of this initialization period in epoch

| (1) |

We show that with high probability (see Lemma 7.1 in Appendix 7), and therefore this initialization period forms a negligible portion of the epoch.

For each time step after initialization, , the algorithm (1) samples the unknown product demand parameters from the posterior , and (2) solves and offers the resulting optimal price based on the demand function given by the sampled parameters

| (2) |

Upon observing the actual realized demand , the algorithm computes the posterior for round . Specifically, using the update rule for Bayesian linear regression (Bishop 2006) and letting , the posterior at time is

The same algorithm is applied independently to each epoch .

As evidenced by the large literature on the practical success of Thompson sampling (Chapelle and Li 2011, Russo and Van Roy 2014, Ferreira et al. 2018), Algorithm 1 is a very attractive choice for implementation in practice.

Algorithm 1 attains a strong performance guarantee under the classical formulation compared to an oracle that knows all product demand parameters in advance. In particular, the oracle would offer the expected optimal price in each period in epoch , i.e.,

| (3) |

The resulting Bayes regret (Russo and Van Roy 2014) of a policy relative to the oracle is:

| (4) |

where the expectation is taken with respect to the unknown product demand parameters, the observed random feature vectors, and the noise in the realized demand. The following theorem bounds the Bayes regret of the Thompson sampling dynamic pricing algorithm:

Theorem 2.4

When the prior over the demand parameters is known, Algorithm 1 satisfies

Theorem 2.4 follows from a similar argument used for the linear bandit setting presented in Russo and Van Roy (2014), coupled with standard concentration bounds for multivariate normal distributions. The proof is given in Appendix 7 for completeness. Note that the regret scales linearly in , since each epoch is an independent learning problem.

2.4 Meta Oracle and Meta Regret

We cannot directly implement Algorithm 1 in our setting, since the prior over the product demand parameters is unknown. In this paper, we seek to learn the prior (shared structure) across products in order to leverage the superior performance of Thompson sampling with a known prior. Thus, a natural question to ask is:

What is the price of not knowing the prior in advance?

To answer this question, we first define our performance metric. Since our goal is to converge to the policy given in Algorithm 1 (which knows the true prior), we define this policy as our meta oracle.444We use the term meta oracle to distinguish from the oracle in the classical formulation. Comparing the revenue of our policy relative to the meta oracle leads naturally to the definition of meta regret for a policy , i.e.,

where the expectation is taken with respect to the unknown product demand parameters, the observed random feature vectors, and the noise in the realized demand.

Note that prior-independent Thompson sampling and UCB treat each epoch independently, and would thus achieve meta regret that grows linearly in . Our goal is to design a policy with meta regret that grows sublinearly in . Recall that Theorem 2.4 bounds the Bayes regret of Thompson sampling with a known prior as . Thus, if our meta regret (i.e., the performance of our meta-learning policy relative to Algorithm 1) grows sublinearly in , then the price of not knowing the prior in advance is negligible in experiment-rich environments (large ) compared to the cost of learning the demand parameter for each product (the Bayes regret of Algorithm 1).

The values of the prior mean as well as the actual product demand parameter vectors are unknown; we consider two settings — known and unknown (covariance of the prior).

Remark 2.6 (Choice of meta oracle)

To the best of our knowledge, the optimal prior to use for Thompson sampling remains a difficult, open problem. Existing theory shows (in limited settings) that priors that fail to place sufficient mass on the true parameter fare poorly: the closest setting to ours is the linear bandit construction in Proposition 3.1 of Hamidi and Bayati (2020), which shows that prior-dependent Thompson sampling with a mis-specified prior can achieve regret that scales exponentially in ; Theorem 1 of Liu and Li (2015) and Theorem 2 of Honda and Takemura (2014) also provide illustrative constructions with the same insight. In the other extreme, many empirical evaluations suggest that overly conservative priors (such as prior-independent approaches) also fare poorly relative to using the true prior (see, e.g., Section 6 of Bastani et al. (2020), the discussions in Chapelle and Li (2011), or our numerical results in Section 5). As a result, we choose Thompson Sampling with the true prior as our meta oracle. However, one can choose alternative meta oracles — e.g., one that “widens” the true prior to place more weight on parameters that may induce higher regret — implementing such a meta oracle would still likely require learning the true prior, which is our primary contribution.

Non-anticipating Policies:

We restrict ourselves to the family of non-anticipating policies = that form a sequence of random functions that depend only on price and demand observations collected until time in epoch (including all times from prior epochs), and feature vector observations up to time in epoch . In particular, let , and denote the history of prices and corresponding demand realizations from prior epochs and time periods, as well as the observed feature vectors up to the next time period; let denote the -field generated by . Then, we impose that is measurable.

3 Meta-DP Algorithm

We begin with the case where the prior’s covariance matrix is known, and describe the Meta Dynamic Pricing (Meta-DP) algorithm for this setting. We will consider the case of unknown in the next section.

3.1 Overview

The Meta-DP algorithm begins by using initial product epochs as an exploration phase to initialize our estimate of the prior mean . These exploration epochs use the prior-independent Thompson sampling algorithm to ensure no more than meta regret for each epoch. After this initial exploration period, our algorithm sequentially updates the estimated prior and leverages this estimate in each subsequent epoch. The key technical challenge is that the estimated prior has finite-sample estimation error, resulting in a Thompson sampling instance with a mis-specified prior. We introduce a prior alignment proof technique to show that, despite prior mis-specification, our Meta-DP algorithm still achieves meta regret that grows sublinearly in .

3.2 Algorithm

The Meta-DP algorithm is presented in Algorithm 2. We first define some additional notation, and then describe the algorithm in detail.

Additional Notation:

Throughout the rest of the paper, we use to denote the price and feature information and to denote the Fisher information matrix of round in epoch for all and

Algorithm Description:

The first epochs are treated as exploration epochs, where we define

| (5) |

where ( is a high probability upper bound on all ’s, see Lemma 7.1 in Appendix 7), and the constant is given by

As described in the overview, the Meta-DP algorithm proceeds in two phases. In particular, we distinguish the following two cases for each epoch :

- 1.

-

2.

Epoch the Meta-DP algorithm first computes the OLS estimate of the true parameter for each previous epoch . It then average these parameter estimates to form an estimator of the prior mean i.e.,

(6) Then, the Meta-DP algorithm runs Thompson Sampling (Algorithm 1) with the estimated prior , i.e., TS. Specifically, after some random initialization steps (these steps are identical to our meta oracle), our Meta-DP algorithm (1) samples the unknown product demand parameters from its posterior , and (2) solves and offers the resulting optimal price based on the demand function given by the sampled parameters

(7) Upon observing the actual realized demand , the algorithm computes the posterior for round .

We now state our main result upper bounding the meta regret of our Meta-DP algorithm (Algorithm 2). The proof is provided in Section 3.3 and Appendix 9.

Theorem 3.1

The meta regret of the proposed Meta-DP algorithm satisfies

It is worthwhile to compare the bound in Theorem 3.1 to the meta regret bound for prior-independent Thompson Sampling (Lemma 9.2 in Appendix 9). When , our bound matches that of prior-independent Thompson Sampling, since we simply treat all our epochs as exploration epochs. In the large regime, our meta regret scales as . Thus, our approach of learning the prior is particularly valuable in experiment-rich settings (). Combining the two regimes yields a bound that is sublinear in both and .

Theorem 3.1 is somewhat surprising in the context of a growing theoretical literature that suggests that a mis-specified prior can result in very poor regret for prior-dependent Thompson Sampling (see, e.g., Honda and Takemura 2014, Liu and Li 2015, Hamidi and Bayati 2020). Indeed, one may expect that the mis-specification induced by using the prior instead of can be substantial, since the ratio between these two probability density functions is unbounded when . Yet, using our prior alignment proof strategy (described in the next subsection), we establish that Thompson Sampling is remarkably robust to mis-specification of the prior mean, lending theoretical support to previous empirical observations (Bastani et al. 2020).

3.3 “Prior Alignment” Proof Strategy

Since we only have a logarithmic number (in and ) of exploration epochs, the meta regret accrued from these epochs is (see Lemma 9.2 in Appendix 9).

In each non-exploration epoch , the meta oracle starts with the true prior while our algorithm Meta-DP starts with the estimated prior . The following lemma (whose proof is in Appendix 8) bounds the error of the estimated prior mean with high probability:

Lemma 3.2

For any fixed and with probability at least ,

Thus, the key challenge in proving Theorem 3.1 is bounding the difference in regret incurred by using a Thompson Sampling algorithm with a boundedly mis-specified prior. We introduce a new “prior alignment” proof technique to address this challenge. At a high level, we show that after the exploration time steps, the distributions of the meta oracle’s (random) posterior estimate and Meta-DP’s (random) posterior estimate are close. More specifically, there is a continuum of realizations of the stochastic noise (in the observed demands) such that Meta-DP achieves the same posterior estimate despite starting with a different prior; when such a match occurs, the expected regret moving forward from time is the same for both policies. Using this approach, the regret of our Meta-DP algorithm can be expressed as a weighted distribution of the regret of the meta oracle (which we bounded in Theorem 2.4).

More specifically, the following lemma (whose proof is in Appendix 9) establishes the difference in Bayesian posteriors between the meta oracle and our Meta-DP algorithm. Note that only the means of the posterior differ but the variance is the same.

Lemma 3.3

Conditioned on and the posteriors of the meta oracle and our algorithm Meta-DP algorithm satisfy

Now, consider any non-exploration epoch . If upon completion of all exploration steps at time , we have that the posteriors of the meta oracle and our Meta-DP algorithm coincide — i.e., — then both policies would achieve the same expected revenue over the time periods . By Lemma 3.3, we know that always, so all that remains is establishing when .

Since the two algorithms begin with different priors but encounter the same covariates and take the same decisions in , their posteriors can only align at time due to the stochasticity in the observations . For convenience, denote the noise terms from of the meta oracle and the Meta-DP algorithm respectively as

| (8) | ||||

| (9) |

Furthermore, let . Lemma 3.3 indicates that if

| (10) |

then the posteriors of both algorithms align with . Thus for every realization of the meta oracle’s noise terms and the prior mean estimation error , there exists a well-defined and feasible choice of Meta-DP algorithm’s error that allows the two posteriors to coincide. Furthermore, by Lemma 3.2, is bounded as a function of with high probability, ensuring that the difference in noise terms needed to achieve alignment is small for later epochs (as grows large). With this observation, we can perform a change of measure over our noise terms and integrate over the resulting distributions, yielding the desired bound on the meta regret. The proof is provided in Appendix 9.

Remark 3.4

Our prior alignment approach may be of general interest for analyzing the regret of mis-specified Thompson Sampling instances. Russo and Van Roy (2014) propose a related but different approach in Section 3.1 of their paper. Specifically, they relate the regret of implementing in an environment with true prior to the regret of in an environment with a different true prior . In contrast, we wish to compare the regret of implementing (Meta-DP, Algorithm 2) and (meta oracle, Algorithm 1) in the same environment with true prior . We cannot adopt their approach since one must additionally quantify the difference in regret between TS algorithms learning in environments with different true priors; while this regret difference clearly scales sublinearly in , we require a bound that limits to as the difference in priors (as ). This requirement is because even a constant nonzero difference in regret between the meta oracle and our Meta-DP algorithm would result in meta regret over epochs. To our knowledge, it is an open problem to derive such a bound. Our “prior alignment” sidesteps this issue by directly relating and in an environment with true prior .

4 Meta-DP++ Algorithm

In this section, we consider the setting where the prior covariance matrix is also unknown. We propose the Meta-DP++ algorithm, which builds on top of the Meta-DP algorithm and additionally estimates the unknown prior covariance

4.1 Overview

The Meta-DP++ algorithm also begins by using initial product epochs as an exploration phase to initialize our estimate of the prior mean and covariance . After this initial exploration period, our algorithm sequentially updates the estimated prior and leverages this estimate in each subsequent epoch. Once again, the estimated prior has finite-sample estimation error, resulting in a Thompson sampling instance with a mis-specified prior. The key challenge compared to the previous section is that we can no longer exactly “align” our algorithm’s posterior with that of the meta oracle when is also estimated. We leverage importance sampling arguments from off-policy evaluation to bound the additional meta regret accrued due to this mismatch. Importantly, to ensure that our importance weights remain well-behaved, we widen the estimated covariance via a correction term that scales as the finite-sample estimation error of estimating .

4.2 Algorithm

The Meta-DP++ algorithm is presented in Algorithm 3. We first define some additional notation, and then describe the algorithm in detail.

Additional Notation:

As with the Meta-DP algorithm, at the beginning of each epoch , we update our estimate of the prior mean according to Eq. (6). To estimate , we need unbiased and independent estimates for the unknown true demand parameter realizations across epochs.555When estimating the prior covariance, we cannot use an estimator of that uses all observations from epoch (as we do when estimating the prior mean). This is because the use of the learned prior from past epochs renders observations from later epochs non-independent. We avoid this issue by restricting our estimator of to observations from the initialization periods in each epoch, . We use the initialization steps to produce an estimate for i.e.,

Algorithm Description:

The first epochs are treated as exploration epochs, where we employ the prior-independent Thompson Sampling algorithm. We define

| (11) |

and the constants are given by

Note that we now require exploration epochs, whereas we only required exploration epochs for the Meta-DP algorithm.

As described in the overview, the Meta-DP++ algorithm proceeds in two phases:

- 1.

-

2.

Epoch : the Meta-DP++ algorithm computes an estimator of the prior mean using Eq. (6) (same as Meta-DP algorithm), and an estimator of the prior covariance as

(12) The second term accounts for the estimation error in .

As noted earlier, we then widen our estimator to account for finite-sample estimation error:

(13) where is the -dimensional identity matrix.

Then, the Meta-DP++ algorithm runs Thompson Sampling (Algorithm 1) with the estimated prior , i.e., TS. Specifically, after some random initialization steps (these steps are identical to our meta oracle), our Meta-DP++ algorithm (1) samples the unknown product demand parameters from the posterior , and (2) solves and offers the resulting optimal price based on the demand function given by the sampled parameters

(14) Upon observing the actual realized demand , the algorithm computes the posterior for round .

We now state our main result upper bounding the meta regret of our Meta-DP++ algorithm (Algorithm 3). The proof is provided in Section 4.3 and Appendix 11.

Theorem 4.1

The meta regret of the proposed Meta-DP++ algorithm satisfies

It is worthwhile to compare the bound in Theorem 4.1 to the meta regret bound for prior-independent Thompson Sampling (Lemma 9.2 in Appendix 9). When , our bound matches that of prior-independent Thompson Sampling, since we simply treat all our epochs as exploration epochs. In the large regime, our meta regret scales as . Thus, our approach of learning the prior is particularly valuable in settings with many short-horizon experiments (). For instance, as discussed in Example 2.1, sellers like Rue La La host many events, offering new items with short selling seasons. Combining the two regimes yields a bound that is sublinear in both and .

4.3 Proof Strategy

The number of exploration epochs is logarithmic number in but quadratic in . This motivates the analysis of two cases: (i) when the number of epochs , the meta regret guarantees given by existing prior-independent approaches is already good; (ii) when we transition to an experiment rich environment with , the meta regret accrued from these epochs is small since their cardinality scales logarithmically in (see argument in Appendix 11). We now focus on the latter case where is large.

Once again, following the proof strategy employed for Meta-DP algorithm, we employ “prior alignment” to match the means of the meta oracle’s (random) posterior estimate and Meta-DP++’s (random) posterior estimates. However, since was known in the previous section, matching the posterior means implied equality of the entire distribution of the posterior (see Lemma 3.3). This equivalence allowed us to exactly equate the expected regret (after alignment) for the meta oracle and our Meta-DP algorithm.

However, when is unknown, matching the posterior means no longer implies that the posterior distributions are equal. Furthermore, since the Bayesian update for the covariance matrix does not depend on the noise terms (it depends only on the observed covariates and chosen prices), we cannot use any alignment strategy based on and to get exact equivalence of the posterior distributions. Thus, the key added challenge in proving Theorem 4.1 is bounding the difference in regret between our Meta-DP++ algorithm and the meta oracle after alignment of the means of their posteriors at time .

Specifically, in each non-exploration epoch , the meta oracle starts with the true prior while our algorithm Meta-DP++ starts with the (widened) estimated prior . Lemma 3.2 from the previous section already provides a bound on , and the following lemma (whose proof is in Appendix 10) bounds the error of the estimated covariance (and thus the error of our widened covariance ) with high probability:

Lemma 4.2

For any fixed and , with probability at least ,

At time , we use a change of measure to “align” our Meta-DP++ algorithm’s prior to . Combining Lemma 4.2 and the fact that both policies offer the same prices in the random exploration periods, we know that and are close with high probability for later epochs. However, it remains to bound the regret difference between the meta oracle’s policy, which employs the prior , and our Meta-DP++ algorithm, which employs the prior . We leverage importance sampling arguments from off-policy evaluation (Precup et al. 2000, Murphy et al. 2001) to bound this remaining term. Prior widening is instrumental in this last step, ensuring that our importance weights do not diverge.

Remark 4.3

While our Meta-DP algorithm does not require prior widening, we widen our prior for our Meta-DP++ algorithm as described above. This allows us to shave off some extra factors of the dimension in our analysis, by ensuring that the importance weights are well-behaved post-alignment. This is consistent with recent work by Hamidi and Bayati (2020), who show that Thompson sampling can in general incur a worst-case regret that scales exponentially in , unless it uses a widened posterior variance at each step. Furthermore, we observe (often significantly) improved empirical performance on both synthetic and real datasets by employing our Meta-DP++ algorithm compared to its non-widened analog (see Section 5).

4.4 Additional Remarks

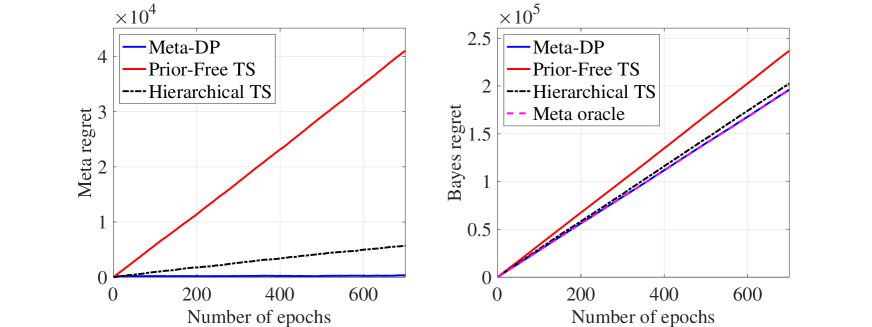

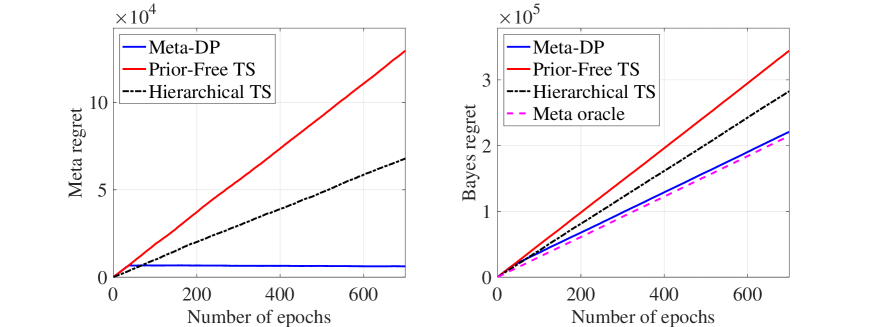

Hierarchical Model:

An alternative heuristic to leverage shared structure is to use hierarchical Thompson Sampling, maintaining a posterior on the shared prior and updating it after each epoch. In Appendix 13.1, we compare the Meta-DP algorithm to a hierarchical approach; while the hierarchical algorithm outperforms prior-independent Thompson Sampling by leveraging shared structure, we find that it still significantly underperforms compared to the Meta-DP algorithm for moderate to large values of due to excessive exploration.

Knowledge of :

Our formulation assumes knowledge of and . However, this assumption can easily be removed using the well-known “doubling trick”. In particular, we can initially fix any values and , and iteratively double the length of the respective horizons; we refer the interested reader to Cesa-Bianchi and Lugosi (2006) for details. For the Meta-DP algorithm, we would simply continue to update the estimated prior mean; for the Meta-DP++ algorithm, we would need to also follow the prior widening schedule. It is easy to see that our regret bounds are preserved up to logarithmic terms under such an approach.

Overlapping Epochs:

We model epochs as fully sequential for simplicity; if epochs overlap, we would need to additionally model a customer arrival process for each epoch. Our algorithms straightforwardly generalize to a setting where arrivals are randomly distributed across overlapping epochs. In particular, both the Meta-DP algorithm and the Meta-DP++ algorithm can be modified to only use samples from the initialization period in each epoch for estimating the prior mean (note that our estimation of the prior covariance already only uses samples from initialization periods) without affecting the meta regret bounds and analysis. Therefore, when epochs overlap, we will update our estimate of the prior as soon as we see customer responses for any product.

5 Numerical Experiments

We now validate our theoretical results by empirically comparing the performance of our proposed algorithms against prior-independent Thompson Sampling (Agrawal and Goyal 2013). As discussed earlier, this approach ignores learning shared structure (the prior) across products, and achieves meta regret (see Lemma 9.2 in Appendix 9). When the prior covariance is unknown, we illustrate the benefits of prior widening by additionally comparing against a version of the Meta-DP++ algorithm that greedily uses the estimated covariance matrix (i.e., ).

In addition to meta regret, we present results on Bayes regret (relative to the classical oracle) to illustrate that our transfer learning approach significantly increases performance under the standard metric. We perform numerical experiments on both synthetic data as well as a real dataset on auto loans provided by the Columbia University Center for Pricing and Revenue Management.

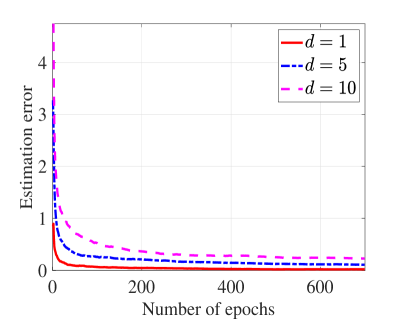

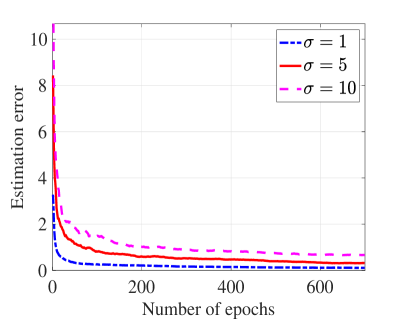

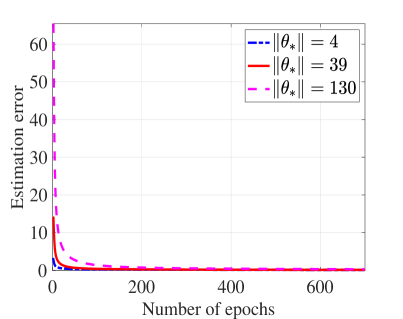

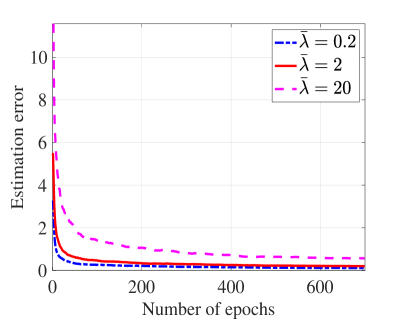

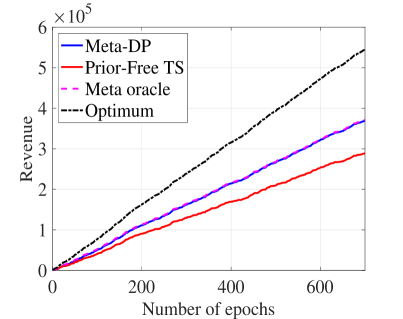

A number of additional numerical results are presented in Appendix 13, including comparison to a hierarchical Thompson Sampling heuristic (13.1), examining the estimation error of the prior as a function of (13.2), as well as results under a revenue metric (13.3).

5.1 Synthetic Data

We begin with the case where the prior covariance is known.

Parameters:

We consider products, each with a selling horizon of periods. We set the feature dimension the prior mean and the prior covariance In each epoch and each round , each entry of the observed feature vector is drawn i.i.d. from the uniform distribution over ; note that this ensures the norm of each feature vector is upper bounded by For each product , we randomly draw a demand parameter i.i.d. from the true prior The allowable prices lie in . Finally, the noise distribution is the standard normal distribution, i.e.,

Results:

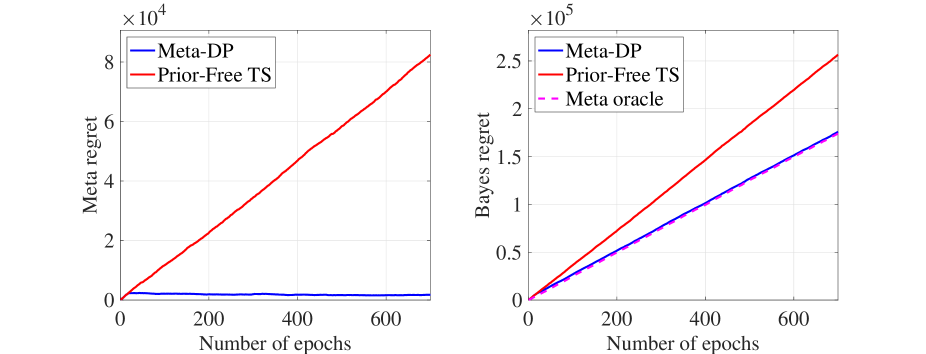

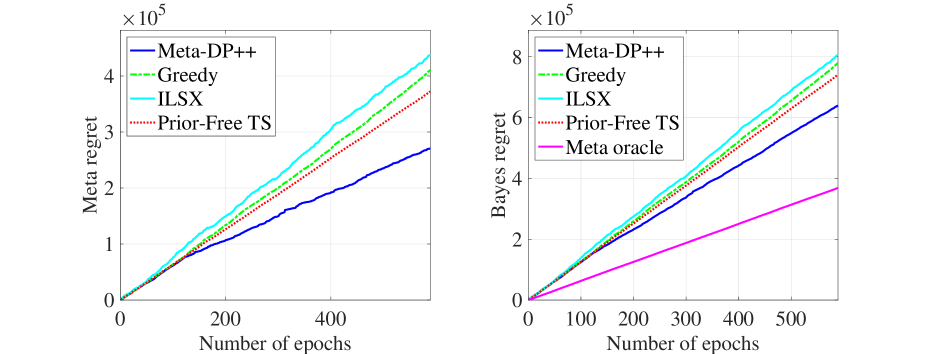

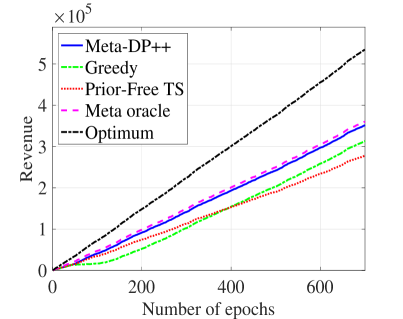

We plot the cumulative meta regret and Bayes regret of each algorithm, averaged over 20 random trials, as a function of the number of epochs (recall that each epoch lasts for periods). The results are shown in Figure 1. Both algorithms are identical during the initial exploration epochs.

As expected, the prior-independent approach achieves meta regret that scales linearly in , since each epoch is treated independently. In contrast, the left panel of Figure 1 shows that Meta-DP achieves nearly zero meta regret after the exploration epochs as it has learned the prior.

The right panel of Figure 1 examines Bayes regret; note that even the meta-oracle achieves Bayes regret (Theorem 2.4). However, the slope of Meta-DP closely matches that of the meta-oracle after the initial exploration epochs, i.e., we do not accrue additional regret (relative to the meta oracle) as grows large. In contrast, the slope of prior-independent Thompson Sampling is significantly larger, resulting in additional regret continually accruing as grows large. In particular, when the Bayes regret of prior independent Thompson Sampling is 39% larger than that of Meta-DP and 48% larger than that of the meta oracle. Thus, our approach of learning shared structure is particularly valuable in experiment-rich environments.

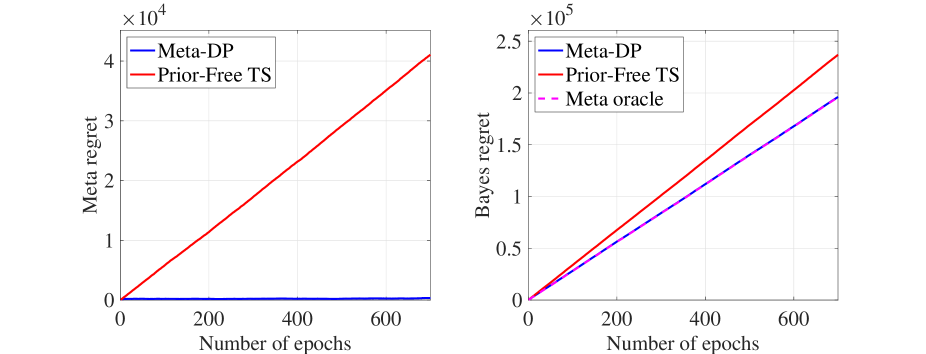

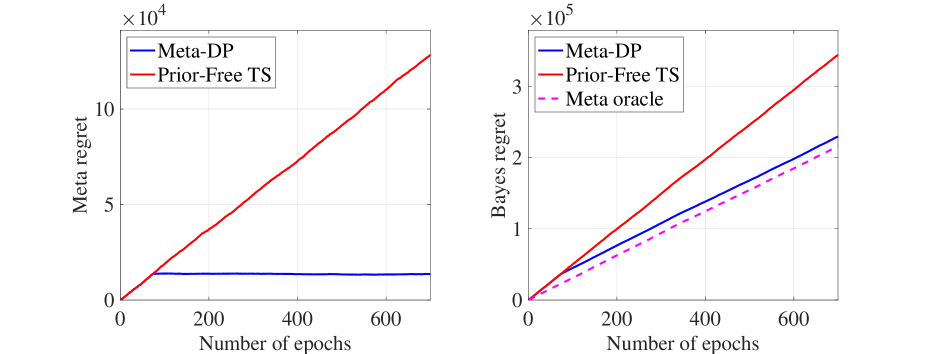

Varying the feature dimension :

We now explore how our results vary as we change the dimension of the observed features. Our previous results considered . We now additionally consider:

-

1.

No features, : We set for all and

-

2.

Many features, : Each entry of the observed feature vector is again drawn i.i.d. from the uniform distribution over for all and

The results for both cases, averaged over 20 random trials, are shown in Figures 5(a) and 5(b) respectively. Again, we see that Meta-DP substantially outperforms prior-independent Thompson sampling algorithm in both meta regret and Bayes regret, regardless of the choice of feature dimension . Note that we require more exploration epochs when is larger (recall that scales as ).

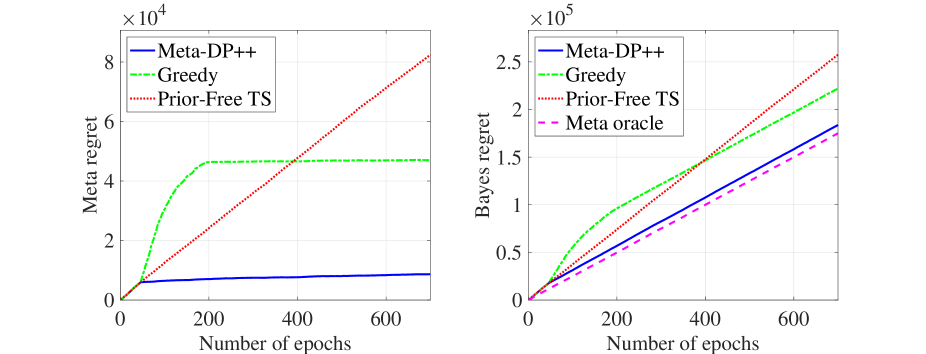

Unknown prior covariance :

We now shift our attention to the Meta-DP++ algorithm, and follow the same setup described earlier. To quantify the benefit of prior widening, we additionally consider a version of the Meta-DP++ algorithm that greedily uses the estimated covariance matrix, i.e., The results, averaged over 20 random trials, are shown in Figure 3. We see that the Meta-DP++ algorithm significantly outperforms both the prior-independent Thompson sampling algorithm as well as the non-widened greedy benchmark in meta regret (left panel) and Bayes regret (right panel). Interestingly, the greedy approach performs significantly worse in earlier epochs after the initial exploration epochs (when it relies on a prior that is likely to be significantly mis-specified); in later epochs, the greedy approach’s slope begins to match that of Meta-DP++ as it starts learning the true prior. Thus, prior widening appears critical to ensure good performance on each pricing problem — particularly earlier ones, where we should be careful not to over-rely on a prior is likely to be significantly mis-specified. The overall success of Meta-DP++ suggests that the price of not knowing the prior in advance is negligible in experiment-rich environments (large ).

5.2 Real Data on Online Auto-Lending

We now turn to the on-line auto lending dataset. This dataset was first studied by Phillips et al. (2015), and subsequently used to evaluate dynamic pricing algorithms by Ban and Keskin (2017). We will follow a similar set of modeling assumptions.

The dataset records all auto loan applications received by a major online lender in the United States from July 2002 through November 2004. It contains loan applications. For each application, we observe some loan-specific features (e.g., date of application, the term and amount of loan requested, and the borrower’s personal information), the lender’s pricing decision (i.e., the monthly payment required of the borrower), and the resulting demand (i.e., whether or not this offer was accepted by the borrower). We refer the interested reader to Columbia University Center for Pricing and Revenue Management (Columbia 2015) for a detailed description of the dataset.

Algorithms:

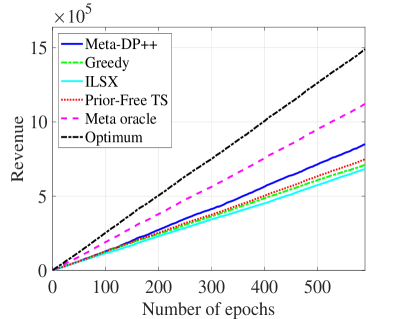

We consider the setting where both the prior mean and prior covariance are unknown. Thus, we compare the performance of Meta-DP++ algorithm against that of prior-independent Thompson Sampling, the ILSX algorithm proposed in Ban and Keskin (2017), and the greedy version of Meta-DP++ that does not employ prior widening.

Products:

We first define a set of related products. We segment loans by the borrower’s state (there are 50 states), the term class of the loan (0-36, 37-48, 49-60, or over 60 months), and the car type (new, used, or refinanced). The expected demand and loan decisions offered for each type of loan is likely different based on these attributes. We consider loans that share all three attributes as a single “product” offered by the online lender. We thus obtain a total of unique products. The number of applicants in the data for each loan type determines for each product; importantly, note that is not identical across products.

Remark 5.1

We use three categorical features (state, term of loan, and car type) to define products. In contrast, the ILSX algorithm (Ban and Keskin 2017) sets and encodes this information as product features; this results in a feature vector of dimension , since each possible value of the categorical feature will be represented as 1-hot encoding. The resulting meta regret of ILSX will therefore still grow superlinearly in (unlike our proposed algorithms). Moreover, their demand model is less expressive compared to ours since it does not allow for different price elasticities by state/term/car type (see our earlier Remark 2.3 for discussion).

Remark 5.2

Following our model, we simulate each epoch sequentially. In reality, customers will likely arrive randomly for each loan type at different points of time. We note that the Meta-DP algorithm only uses the initial sample from each epoch for estimating the prior mean, and thus, in principle, it can be adapted to a setting where arrivals are randomly distributed across overlapping epochs as well (see discussion in §4.4).

Features:

We use the feature selection results from Ban and Keskin (2017), which yields the following features: FICO score, the loan amount approved, prime rate, and the competitor’s rate.

Setup:

Following the approach of Phillips et al. (2015) and Ban and Keskin (2017), we impute the price of a loan as the net present value of future payments (a function of the monthly payment, customer rate, and term approved; we refer the reader to the cited references for details). The allowable price range in our experiment is .

We note that, although we use a linear demand model, our responses are binary (i.e., whether a customer accepts the loan). This approach is common in the literature (see, e.g., Li et al. 2010). Besbes and Zeevi (2015) provide theoretical justification for this approach by showing that we may still converge to the optimal price despite the demand model being misspecified.

Finally, unlike our model and analysis, the true distribution over loan demand parameters across products may not be a multivariate Gaussian. We use the entire dataset to estimate each product’s demand parameter, and then fit a multivariate Gaussian prior over the empirical distribution of product demand parameters — our meta oracle uses this prior. However, our regret is evaluated with respect to the true data (i.e., our meta oracle may perform poorly in Bayes regret if the prior is far from a multivariate Gaussian). Thus, this experiment can provide a check on whether our algorithms (which seek to mimic the meta oracle) are robust to model misspecification of the prior.

Results:

We average our results over 100 random permutations of the data. The results are shown in Figure 4. We first note that, despite potential misspecification of the prior’s model class, the meta oracle (prior-dependent Thompson Sampling) achieves much better Bayes regret (right panel) than all algorithms. This implies that the (potentially mis-specified) shared prior across products is informative, and thus leveraging shared structure may be valuable. Then, by design, our Meta-DP++ algorithm learns this shared structure, incurring meta regret that grows sublinearly in (left panel). Consistent with our results on synthetic data, we see that the Meta-DP++ algorithm significantly outperforms the benchmark algorithms; this is true even though the multivariate Gaussian prior that we estimate may not be the true prior. This result suggests that our proposed algorithms may be robust to model misspecification of the prior.

6 Discussion & Conclusions

Firms are increasingly performing experimentation. This provides an opportunity for decision-makers to learn not just within experiments, but also across experiments. In this paper, we consider the multi-product dynamic pricing setting where a decision-maker must learn a sequence of related unknown parameters through experimentation; we capture the relationship across these unknown parameters by imposing that they arise from a shared distribution (the prior). We propose meta-learning policies that efficiently learn both the shared distribution across experiments and the individual unknown parameters within experiments.

Our meta-learning approach can easily be adapted beyond dynamic pricing applications to classical multi-armed and contextual bandit problems as well. For instance, consider clinical trials, which were the original motivation for bandit problems (Thompson 1933, Lai and Robbins 1985). Many have argued the benefits of Bayesian clinical trials, which allow for the use of historical information and for synthesizing results of past relevant trials, e.g., past clinical trials on the same disease may indicate that patients with certain biomarkers or concomitant medications are less likely to benefit from standard therapy. Such information can be encoded in a Bayesian prior to potentially allow for more informative clinical trials and improved treatment allocations to patients within the trial (see, e.g., Berry 2006, Anderer et al. 2019). Our meta-learning approach can inform how such priors are constructed. Importantly, prior widening gracefully transitions from an uninformative to an informative prior as we accrue data from more related clinical trials.

Our prior widening technique is inspired by the emerging literature studying prior misspecification in Thompson sampling. In general, adopting a more conservative prior allows Thompson sampling to still achieve the optimal theoretical guarantee, while a less conservative prior may cause failure to converge (Honda and Takemura 2014, Liu and Li 2015). However, the use of a conservative prior often results in poor empirical performance, and can erode the benefit of using Thompson sampling over UCB and other prior-free approaches (see, e.g., Russo and Van Roy 2014, Bastani et al. 2020). We take the view that a successful implementation of Thompson sampling requires learning an appropriate prior, and propose meta-learning policies to achieve this goal across a sequence of learning problems.

The authors gratefully acknowledge Columbia University Center for Pricing and Revenue Management for providing us the dataset on auto loans. We are also grateful to Amit Peleg, Jackie Baek, Omar Besbes, Dan Russo, various seminar participants and an anonymous review team for valuable feedback on earlier drafts.

References

- Abbasi-Yadkori et al. (2011) Abbasi-Yadkori, Yasin, David Pál, Csaba. Szepesvári. 2011. Improved algorithms for linear stochastic bandits. NIPS.

- Abeille and Lazaric (2017) Abeille, Marc, Alessandro Lazaric. 2017. Linear thompson sampling revisited. Proceedings of the 20th International Conference on Artificial Intelligence and Statistics.

- Agrawal and Devanur (2014) Agrawal, Shipra, Nikhil R Devanur. 2014. Bandits with concave rewards and convex knapsacks. EC. ACM, 989–1006.

- Agrawal and Goyal (2013) Agrawal, Shipra, Navin Goyal. 2013. Thompson sampling for contextual bandits with linear payoffs. International Conference on Machine Learning. 127–135.

- Anderer et al. (2019) Anderer, Arielle, Hamsa Bastani, John Silberholz. 2019. Adaptive clinical trial designs with surrogates: When should we bother? Available at SSRN 3397464 .

- Araman and Caldentey (2009) Araman, Victor F, René Caldentey. 2009. Dynamic pricing for nonperishable products with demand learning. Operations research 57(5) 1169–1188.

- Auer (2002) Auer, Peter. 2002. Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research 3(Nov) 397–422.

- Ban and Keskin (2017) Ban, Gah-Yi, N Bora Keskin. 2017. Personalized dynamic pricing with machine learning .

- Bastani (2020) Bastani, Hamsa. 2020. Predicting with proxies: Transfer learning in high dimension. Management Science .

- Bastani et al. (2020) Bastani, Hamsa, Mohsen Bayati, Khashayar Khosravi. 2020. Mostly exploration-free algorithms for contextual bandits. Management Science .

- Berry (2006) Berry, Donald A. 2006. Bayesian clinical trials. Nature reviews Drug discovery 5(1) 27.

- Besbes et al. (2014) Besbes, Omar, Yonatan Gur, Assaf Zeevi. 2014. Stochastic multi-armed-bandit problem with non-stationary rewards. NIPS. 199–207.

- Besbes and Zeevi (2009) Besbes, Omar, Assaf Zeevi. 2009. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research 57(6) 1407–1420.

- Besbes and Zeevi (2015) Besbes, Omar, Assaf Zeevi. 2015. On the (surprising) sufficiency of linear models for dynamic pricing with demand learning. Management Science 61(4):723–739.

- Bhat et al. (2019) Bhat, Nikhil, Vivek F Farias, Ciamac C Moallemi, Deeksha Sinha. 2019. Near optimal ab testing. Management Science .

- Bishop (2006) Bishop, Christopher M. 2006. Pattern Recognition and Machine Learning. Springer.

- Bolstad and Curran (2016) Bolstad, William M., James M. Curran. 2016. Introduction to Bayesian Statistics. John Wiley & Sons, Inc.

- Broder and Rusmevichientong (2012) Broder, Josef, Paat Rusmevichientong. 2012. Dynamic pricing under a general parametric choice model. Operations Research 60(4) 965–980.

- Bubeck and Liu (2013) Bubeck, Sébastien, Che-Yu Liu. 2013. Prior-free and prior-dependent regret bounds for thompson sampling. NIPS. 638–646.

- Cesa-Bianchi and Lugosi (2006) Cesa-Bianchi, Nicolò, Gábor Lugosi. 2006. Prediction, Learning, and Games. Cambridge University Press.

- Chapelle and Li (2011) Chapelle, Olivier, Lihong Li. 2011. An empirical evaluation of thompson sampling. NIPS. 2249–2257.

- Cohen et al. (2016) Cohen, Maxime, Ilan Lobel, Renato Paes Leme. 2016. Feature-based dynamic pricing .

- Columbia (2015) Columbia. 2015. Center for pricing and revenue management datasets. URL https://www8.gsb.columbia.edu/cprm/sites/cprm/files/files/CPRM_AutoLoan_Data%20dictionary%283%29.pdf.

- Cormen et al. (2009) Cormen, Thomas H., Charles E. Leiserson, Ronald L. Rivest, Clifford Stein. 2009. Introduction to Algorithms. MIT Press.

- Dani et al. (2008) Dani, Varsha, Thomas Hayes, Sham Kakade. 2008. Stochastic linear optimization under bandit feedback. COLT .

- den Boer and Zwart (2013) den Boer, Arnoud V, Bert Zwart. 2013. Simultaneously learning and optimizing using controlled variance pricing. Management science 60(3) 770–783.

- Elmachtoub et al. (2020) Elmachtoub, Adam N., Vishal Gupta, Michael Hamilton. 2020. The value of personalized pricing. Forthcoming at Management Science .

- Farias and Van Roy (2010) Farias, Vivek F, Benjamin Van Roy. 2010. Dynamic pricing with a prior on market response. Operations Research 58(1) 16–29.

- Ferreira et al. (2018) Ferreira, Kris, David Simchi-Levi, He Wang. 2018. Online network revenue management using thompson sampling. Operations Research.

- Ferreira et al. (2015) Ferreira, Kris Johnson, Bin Hong Alex Lee, David Simchi-Levi. 2015. Analytics for an online retailer: Demand forecasting and price optimization. Manufacturing & Service Operations Management 18(1) 69–88.

- Finn et al. (2017) Finn, Chelsea, Pieter Abbeel, Sergey Levine. 2017. Model-agnostic meta-learning for fast adaptation of deep networks. ICML. 1126–1135.

- Finn et al. (2018) Finn, Chelsea, Kelvin Xu, Sergey Levine. 2018. Probabilistic model-agnostic meta-learning. NIPS.

- Fisher et al. (2017) Fisher, Marshall, Santiago Gallino, Jun Li. 2017. Competition-based dynamic pricing in online retailing: A methodology validated with field experiments. Management Science 64(6) 2496–2514.

- Gupta and Nagar (1999) Gupta, A. K., D. K. Nagar. 1999. Matrix Variate Distributions. CRC Press.

- Gupta and Kallus (2020) Gupta, Vishal, Nathan Kallus. 2020. Data-pooling in stochastic optimization. arXiv preprint arXiv:1906.00255 [math.OC] .

- Hamidi and Bayati (2020) Hamidi, Nima, Mohsen Bayati. 2020. On worst-case regret of linear thompson sampling. arXiv preprint arXiv:2006.06790 .

- Harrison et al. (2012) Harrison, J Michael, N Bora Keskin, Assaf Zeevi. 2012. Bayesian dynamic pricing policies: Learning and earning under a binary prior distribution. Management Science 58(3) 570–586.

- Hartland et al. (2006) Hartland, Cédric, Sylvain Gelly, Nicolas Baskiotis, Olivier Teytaud, Michéle Sebag. 2006. Multi-armed bandit, dynamic environments and meta-bandits .

- Honda and Takemura (2014) Honda, Junya, Akimichi Takemura. 2014. Optimality of thompson sampling for gaussian bandits depends on priors. AISTATS. 375–383.

- Javanmard and Nazerzadeh (2019) Javanmard, Adel, Hamid Nazerzadeh. 2019. Dynamic pricing in high-dimensions. JMLR .

- Jin et al. (2019) Jin, Chi, Praneeth Netrapalli, Michael I. Jordan. 2019. A short note on concentration inequalities for random vectors with subgaussian norm. arXiv:1902.03736 .

- Johari et al. (2015) Johari, Ramesh, Leo Pekelis, David J Walsh. 2015. Always valid inference: Bringing sequential analysis to a/b testing. arXiv preprint arXiv:1512.04922 .

- Keskin and Zeevi (2014) Keskin, N Bora, Assaf Zeevi. 2014. Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies. Operations Research 62(5) 1142–1167.

- Kleinberg and Leighton (2003) Kleinberg, Robert, Tom Leighton. 2003. The value of knowing a demand curve: Bounds on regret for online posted-price auctions. FOCS. IEEE, 594.

- Lai and Robbins (1985) Lai, Tze Leung, Herbert Robbins. 1985. Asymptotically efficient adaptive allocation rules. Advances in applied mathematics 6(1) 4–22.

- Laub (2004) Laub, Alan. 2004. Matrix Analysis for Scientists and Engineers. Society of Industrial and Applied Mathematics.

- Li et al. (2010) Li, Lihong, Wei Chu, John Langford, Robert Schapire. 2010. A contextual-bandit approach to personalized news article recommendation. Proceedings of the 19th international conference on World wide web (WWW).

- Liu and Li (2015) Liu, Che-Yu, Lihong Li. 2015. On the prior sensitivity of thompson sampling. arXiv preprint arXiv:1506.03378 .

- Maes et al. (2012) Maes, Francis, Louis Wehenkel, Damien Ernst. 2012. Meta-learning of exploration/exploitation strategies: The multi-armed bandit case. International Conference on Agents and Artificial Intelligence. Springer, 100–115.

- Murphy et al. (2001) Murphy, Susan, Mark van der Laan, James Robins, CPPRG. 2001. Marginal mean models for dynamic regimes. Journal of the American Statistical Association (JASA) .

- Optimizely (2019) Optimizely. 2019. Online. URL https://www.optimizely.com/optimization-glossary/ab-testing/. [Last accessed January 21, 2019].

- Phillips et al. (2015) Phillips, Robert, A. Serdar Simsek, Garrett van Ryzin. 2015. The effectiveness of field price discretion: Empirical evidence from auto lending. Management Science 61(8):1741–1759.

- Precup et al. (2000) Precup, Doina, Richard Sutton, Satinder Singh. 2000. Eligibility traces for off-policy policy evaluation. International Conference on Machine Learning (ICML) .

- Qiang and Bayati (2016) Qiang, Sheng, Mohsen Bayati. 2016. Dynamic pricing with demand covariates .

- Raina et al. (2006) Raina, Rajat, Andrew Y Ng, Daphne Koller. 2006. Constructing informative priors using transfer learning. ICML. ACM, 713–720.

- Rigollet and Hütter (2018) Rigollet, R., J. Hütter. 2018. High Dimensional Statistics. Lecture Notes.

- Rinaldo (2017) Rinaldo, Alessandro. 2017. Lecture notes on advanced statistical theory. Available at: http://www.stat.cmu.edu/ arinaldo/Teaching/36755/F17/.

- Rossi et al. (2005) Rossi, Peter E., Greg M. Allenby, Robert McCulloch. 2005. Bayesian Statistics and Marketing. John Wiley & Sons, Ltd.

- Rusmevichientong and Tsitsiklis (2010) Rusmevichientong, Paat, John N Tsitsiklis. 2010. Linearly parameterized bandits. Mathematics of Operations Research 35(2) 395–411.

- Russo and Van Roy (2014) Russo, Daniel, Benjamin Van Roy. 2014. Learning to optimize via posterior sampling. Mathematics of Operations Research 39(4):1221–1243. https://doi.org/10.1287/moor.2014.0650.

- Russo et al. (2018) Russo, Daniel J, Benjamin Van Roy, Abbas Kazerouni, Ian Osband, Zheng Wen, et al. 2018. A tutorial on thompson sampling. Foundations and Trends® in Machine Learning 11(1) 1–96.

- Scott (2015) Scott, Steven L. 2015. Multi-armed bandit experiments in the online service economy. Applied Stochastic Models in Business and Industry 31(1) 37–45.

- Sharaf and Daumé III (2019) Sharaf, Amr, Hal Daumé III. 2019. Meta-learning for contextual bandit exploration. arXiv preprint arXiv:1901.08159 .

- Thompson (1933) Thompson, William R. 1933. On the likelihood that one unknown probability exceeds another in view of the evidence of two samples. Biometrika 25(3/4) 285–294.

- Tropp (2011) Tropp, Joel. 2011. User-friendly tail bounds for matrix martingales. Available at: http://www.dtic.mil/dtic/tr/fulltext/u2/a555817.pdf.

- Wainwright (2019) Wainwright, Martin. 2019. High-Dimensional Statistics: A Non-Asymptotic Viewpoint. Cambridge University Press.

- Wang et al. (2018) Wang, Zi, Beomjoon Kim, Leslie Pack Kaelbling. 2018. Regret bounds for meta bayesian optimization with an unknown gaussian process prior. NIPS. 10498–10509.

- Xu et al. (2019) Xu, Joseph, Peter Fader, Senthil K Veeraraghavan. 2019. Designing and evaluating dynamic pricing policies for major league baseball tickets. MSOM .

- Yoon et al. (2018) Yoon, Jaesik, Taesup Kim, Ousmane Dia, Sungwoong Kim, Yoshua Bengio, Sungjin Ahn. 2018. Bayesian model-agnostic meta-learning. NIPS. 7343–7353.

- Zhang et al. (2017) Zhang, Dennis J, Hengchen Dai, Lingxiu Dong, Fangfang Qi, Nannan Zhang, Xiaofei Liu, Zhongyi Liu. 2017. How does dynamic pricing affect customer behavior on retailing platforms? evidence from a large randomized experiment on alibaba .

- Zhu and Modiano (2018) Zhu, Ruihao, Eytan Modiano. 2018. Learning to route efficiently with end-to-end feedback: The value of networked structure. Available at: https://arxiv.org/abs/1810.10637.

We begin by defining some helpful notation. First, let

be the expected total revenue over time steps obtained by running TS — the Thompson sampling algorithm in Algorithm 1 with the (possibly incorrect) prior and exploration parameter — in an epoch with true parameter . Second, let

be the expected total revenue over time steps obtained by the oracle — recall is the oracle price defined in Eq. (2.3) — in an epoch with true parameter

All norms refer to the norm unless stated otherwise.

7 Meta oracle Regret Analysis

We first state the following lemma, whose proof is provided in Section 7.1.

Lemma 7.1

For any epoch the length of the random exploration periods is upper bounded by

| (15) |

with probability at least . The constants are given by

In other words, we incur at most logarithmic regret due to the initial random exploration in Algorithm 1.

Proof 7.2

Proof of Theorem 2.4 The proof proceeds in three steps. We first show that the regret incurred in the initial random exploration steps is negligible. We then map the remaining regret to a linear bandit formulation, and bound the resulting terms.

First, define the event

| (16) |

By Lemma 7.1, . We can decompose the regret from Algorithm 1 into exploration and non-exploration periods, conditioned on whether or not holds:

| (17) |

where we have used the facts that , the worst-case regret achievable in a single time period is , and on the event .

The first two terms in Eq. (17) are . To analyze the third term in Eq. (17), we construct a mapping between the dynamic pricing and linear bandit problems, in order to leverage existing results on TS and UCB for linear bandits (Russo and Van Roy 2014, Abbasi-Yadkori et al. 2011). In particular, we can map the Bayes regret of an epoch