Fair Estimation of Capital Risk Allocation

This Version: November 20, 2019 )

| Abstract: | In this paper we develop a novel methodology for estimation of risk capital allocation. The methodology is rooted in the theory of risk measures. We work within a general, but tractable class of law-invariant coherent risk measures, with a particular focus on expected shortfall. We introduce the concept of fair capital allocations and provide explicit formulae for fair capital allocations in case when the constituents of the risky portfolio are jointly normally distributed. The main focus of the paper is on the problem of approximating fair portfolio allocations in the case of not fully known law of the portfolio constituents. We define and study the concepts of fair allocation estimators and asymptotically fair allocation estimators. A substantial part of our study is devoted to the problem of estimating fair risk allocations for expected shortfall. We study this problem under normality as well as in a nonparametric setup. We derive several estimators, and prove their fairness and/or asymptotic fairness. Last, but not least, we propose two backtesting methodologies that are oriented at assessing the performance of the allocation estimation procedure. The paper closes with a substantial numerical study of the subject. |

|---|---|

| Keywords: | capital allocation, fair capital allocation, asymptotic fairness, expected shortfall, risk measures, Euler principle, value-at-risk, tail-value-at-risk, backtesting capital allocation. |

1 Introduction

The measurement and the management of risk is without doubt of highest importance in the financial and the insurance industries. Arguably, the theory and applications of risk measures are most useful for this purpose. For early applications in the insurance context see [Büh70, Ger74], and for a historical perspective in the financial context see [Gui16]. The seminal article [ADEH99] placed risk measurements on an axiomatic foundation paving the way to coherent risk measures which have been treated in numerous works since then. We refer to [Del00, FS11, MFE15] for an in-depth treatment of the topic.

The application of risk measures to portfolio management naturally leads to the problem of allocating portions of the risk capital to the constituents of the portfolio, i.e. to the risk allocation problem. There are a number of different approaches to risk capital allocation, depending on the one hand on the class of the used risk measures, and on the other hand on the used allocation principles. The Euler principle, often used in risk management practice, is one example, see e.g. [Tas04, Tas07]. For coherent risk measures, the Euler principle coincides with the axiomatic approach proposed in [Kal05]. For the more general case of convex risk measures we refer to [Tsa09, MFE15] and references therein.

Risk measures as we consider them here are mathematical tools which require as inputs probability distributions of the underlying risk factors. In practical applications one is typically confronted with the fact that these probability distributions are not fully specified. For example, let represent a P&L, which is a function of some underlying risk factors, and let be the risk measure used to measure the riskiness of , so that the desired quantity to compute is the risk . Since the probability laws of the risk factors are not fully specified, then one needs to approximate , perhaps by estimating this quantity exploiting historical data. As a consequence, the risk allocations, which are usually computed in terms of risk measures, need to be approximated, in particular by estimation.

The problem of estimation of risk has, to a great extent, been neglected in the literature. In the recent paper [PS18] a new statistical methodology for efficient estimation of risk capital was proposed. The methodology introduced in that paper is based on the key concept, which the authors call unbiased estimation of risk also introduced in [PS18], and is based on economic principle.111The concept of unbiased estimation of risk must not be confused with the classical concept of unbiased estimator. Inspired by the ideas from [PS18], in this paper we develop a novel methodology for estimation of capital risk allocation.222In this paper we will occasionally write capital allocation or risk allocation in place of capital risk allocation. We work within a general, but tractable class of coherent risk measures, the so-called weighted value-at-risk measures introduced in [Che06], with focus on the expected shortfall risk measure, which is broadly accepted in the risk management practice.

The underlying key concept introduced in this paper is the fair capital risk allocation, which builds upon the robust representation of coherent risk measures. Our concept of fairness aligns well with what has been done in some of the existing literature. In particular, it implies fairness in the sense of fuzzy games introduced in [Del00]. The fair capital risk allocation can be also viewed as version of the Euler principle of risk allocation. The fair allocation principle used here has been also applied in [BCF18] in the context of allocation of the total default fund among the clearing members of a CCP. For additional insight about fair risk allocation we refer to the recent work [CD19]. We provide explicit formulae for fair capital allocations in case when the constituents of the portfolio are jointly normally distributed.

The major focus of the paper is on the problem of approximating fair portfolio allocations when the law of the portfolio constituents is not fully known. Motivated by the concept of the fair capital allocation, we define and study the concepts of fair allocation estimators and asymptotically fair allocation estimators. A substantial portion of our study is devoted to the problem of estimating the risk allocation under expected shortfall and normality. In addition we consider a nonparametric approach to this problem. We derive several estimators, and prove their fairness and/or asymptotic fairness. Last, but not least, we propose two backtesting methodologies that are oriented at assessing the performance of the allocation estimation procedure. Finally, we perform relevant numerical studies. The results of the numerical studies that we have conducted so far are encouraging for practical use of the estimation and backtesting of the capital allocation.

This work is a first step towards developing formal methodologies for estimating and backtesting of fair capital allocation. As such, it has potential to open new theoretical and practical research avenues.

2 The fair allocation principle

Let be an atomless probability space, and let be the expectation under . In what follows, all needed integrability and regularity assumptions are taken for granted.

We consider a random vector whose components are interpreted as discounted future profits and losses (P&Ls). The marginal random variable (margin – for short) might correspond to the th clearing member of a central clearing counterparty (CCP), to the th position in the portfolio, to the th trader portfolio in a trading desk, or to the th desk in the financial institution portfolio. In the following, we will refer to as portfolio and to as the th portfolio margin or the th portfolio constituent.

Let and let be a normalized monetary risk measure. That is: is monotone, i.e. for all such that ; is cash-additive, i.e. for all and all ; is normalized, i.e. .

The riskiness of the portfolio is measured by applying the risk measure to the aggregated portfolio P&L denoted by

We call the quantity the aggregated risk, or total risk, of the portfolio .

Our objective is to study the issue of allocating the aggregated risk of the portfolio to the individual constituents of the portfolio. Specifically, we intend to find a vector , called a risk allocation, such that the following balance condition holds

| (2.1) |

The component is interpreted as the risk contribution of to the aggregated risk, and therefore is interpreted as the th secured margin of portfolio . Correspondingly, we call the secured portfolio, and the secured aggregated position.

Stated as such, the risk allocation problem is ill–posed. Indeed, any collection of numbers satisfying the balance condition (2.1) constitutes a risk allocation. In order to deal with a meaningful risk allocation problem we need to impose additional conditions, that reflect some additional and desired features of the portfolio allocation. With this in mind, we impose an additional condition on , which we will call the fairness condition.

Towards this end, we require more structure on the risk measure . We additionally assume that the monetary risk measure is finite, law-invariant, comonotonic and coherent; see [Kus01] for details. In view of [Sha13, Theorem 2(iii)] we conclude that is a weighted value-at-risk measure,333Following the traditional nomenclature, we use the name ‘weighted value-at-risk measure’, although a more appropriate name would be ‘weighted expected shortfall’. so that it admits representation (1.1) in [Che06] for a fixed probability measure on . Specifically, for a continuously distributed random variable ,

| (2.2) |

where is the Expected Shortfall444For a formal definition of expected shortfall in the context of this paper see (2.12). (ES) risk measure (sometimes also called tail value-at-risk or conditional value-at-risk) for reference level . Moreover, admits a robust-type representation of the form

| (2.3) |

where is a determining family of probability measures absolutely continuous with respect to . As shown in [Che06, Theorem 6.3], for any there exists a unique minimal extreme measure such that555Note that the set of extreme measures, i.e. the set of measures that satisfy (2.4), might contain more than one element. The term minimal corresponds to the minimal element with respect to the convex stochastic order; see [Che06] for details.

| (2.4) |

Sometimes, we refer to as the worst-case scenario measure (for position ). We denote by the associated Radon-Nikodym derivative . In particular, as shown in [Che06] (cf. formula (6.2) there), if has a continuous distribution then we have

| (2.5) |

for some Borel function . For example if is the expected shortfall at level , then we have

| (2.6) |

where is the –quantile of .

In what follows, for simplicity, we write instead of . The value represents the average performance of the secured margin under the extremal measure . The following fairness condition selects risk allocations which are comparable under the extremal measure of the aggregated portfolio P&L.

Definition 2.1.

The capital allocation is called fair, if

| (2.7) |

The economic intuition behind this definition is as follows: the worst-case-scenario is, in our setting, the determining scenario of the capital allocation for the portfolio through resulting from Equation (2.4). A fair capital allocation is meant to create secured positions , , so that the averages of all secured positions with respect to the worst-case-scenario are all equal.

Since is a monetary risk measure, the extremal measures for and , , coincide. Thus, for any fair capital allocation satisfying the balance condition in (2.1) we have

| (2.8) |

and consequently the risk allocations are given by

| (2.9) |

In view of (2.5), we also have that

| (2.10) |

First, we note that the fair risk allocation is unique, which is due to the existence and uniqueness of the extreme measure . Secondly, we also note that the concept of fairness introduced in Definition 2.1 is actually equivalent to the concept of Euler risk allocation. This observation is readily demonstrated by (2.9). However, it is the characterization of the fairness property of risk allocation as presented in (2.7) that underlies the notion of fair allocation estimator given in Definition 3.1, which is the key definition in this paper. That is why we defined fairness of risk allocation via (2.7) rather than via (2.9).

We also note that the above notion of fairness implies fairness in the sense of fuzzy games introduced in [Del00]. Indeed, this follows from Theorems 17 and 18 therein taking representation (2.3) into account. The fair allocation principle of Definition 2.1 has been applied in [BCF18] in the context of allocation of the total default fund among the clearing members of a CCP.

The following example illustrates the concept of fair allocation.

Example 2.2 (Mean risk allocation).

Consider expectation for measuring risk, i.e. , in which case . Then, clearly, for any , the capital allocation given as

is fair.

2.1 Risk allocation under normality

As an example where explicit formulae can be obtained, we study the case of normally distributed profits and losses. In this regard, let us assume that the vector is normally distributed under with mean and covariance matrix and fix . Then, is bivariate normal, and the conditional expectation takes the form

with , and . Since this conditional expectation is the orthogonal projection of on the linear space spanned by we obtain

where and are independent under , and . For any weighted value-at-risk measure , Equation (2.9) implies that a fair capital allocation is given by

| (2.11) |

where we have used (2.5) in the fourth equality, independence of and under in the fifth equality, and the fact that has zero mean under , in the last equality. As expected, the total allocated risk is divided among constituents using the regression slope allocations which is typically referred to as the covariance principle, see [MFE15, Section 8.5].

Expected shortfall. To be more specific, we consider as an important example the expected shortfall (ES). In this regard, let denote ES under for the level . Then, for a continuously distributed real valued random variable we have

| (2.12) |

where is an -quantile of . Thus, since is normally distributed, (2.12) yields

| (2.13) |

where and are the density and the cumulative distribution function of the standard normal distribution; see [MFE15, Example 2.14]. Putting together (2.1) and (2.13) we see that the capital allocation for ES is given as

| (2.14) |

3 Fair allocation estimators

In practice, the probability distribution under of , the portfolio’s P&L, is not fully specified. Since, in view of (2.5) and (2.10), we have

| (3.1) |

then, in almost all practically relevant applications, neither the aggregated risk nor the fair risk allocation are known, and thus need to be estimated. Hence, appropriate estimation procedures have to be developed, in particular estimation procedures based on the historical data about realizations of the portfolio. This will involve estimating, in some way, the probability distribution of under .

In the following, we set the relevant statistical framework and propose efficient procedures to deal with this estimation issue. We refer to as to the population. Historical information about is given in terms of a random sample of size drawn from , which we denote by , so that are independently drawn copies of the random variable . Our aim is to estimate the aggregated risk using the information contained in the sample. Towards this end we let

represent the random sample, and let us denote its realization by

| (3.2) |

where corresponds to the -th observed (realized) value of the portfolio’s th margin.

The formal statistical setup for this situation is as follows: consider a family of probability measures on , where denotes the parameter space. To avoid unnecessary technical difficulties, we assume that all measures in are equivalent. Furthermore, we assume that for any the random sample is i.i.d. under . Moreover, we assume that for some (unknown) parameter . We will denote by and, respectively , the risk measure , and respectively the expectation, under the probability measure . Similarly to the notation and , corresponding to the reference measure , we will use notation and with regard to the reference measure .

Given the random sample , the allocation is estimated using an allocation estimator defined as

| (3.3) |

for some measurable function .

Next, we define a property that should be satisfied by any reasonable allocation estimator.

Definition 3.1.

An allocation estimator is called fair if, for all ,

| (3.4) |

where .

We emphasize that is a random variable, and is the Radon-Nikodym derivative corresponding to .

We stress that the definition of the fair allocation estimator requires that property (3.4) is satisfied for all populations from the population space , that is for all .

Intuitively, the above definition means that an allocation estimator is fair if it mimics the balanced fairness condition (2.9) for all relevant scenarios (given by probability distributions ). In particular, the aggregated risk estimator obtained from a fair allocation estimator by summation turns out to be unbiased in the sense of [PS18, Definition 4.1], namely, for any we get

| (3.5) |

Equality (3.5) guarantees that the secured aggregated portfolio position is acceptable in the sense that it bears no risk, while Equality (3.4) ensures that the average performance of the secured marginal positions under the worst-case scenario measure for the secured portfolio are the same and that the joint position is secured. In particular, for , the definitions of fairness and unbiasedness coincide.

It should be noted that (3.5) means that a fair allocation estimator charges an adequate amount of capital to secure the portfolio. This is a consequence of (3.4), which means that a fair allocation estimator applies an adequate amount of capital charge to each position constituent.

We end this section with a simple example to illustrate the concept of fairness.

Example 3.2.

Consider the mean risk allocation given in Example 2.2. This leads to the family of risk measures , . Then, the risk allocation estimator

is a fair allocation estimator. Indeed, note that here, for each , the extremal measure coincides with the original probability measure , i.e. . Thus, for we obtain

3.1 Estimating capital allocation under expected shortfall and normality

Following Section 2.1, we study the case where the -dimensional random vector is normally distributed under every , and we assume that the risk is measured by the expected shortfall , at a fixed level . In what follows, for the random sample , we will use the notation , , and we set666To ease the notation, we will drop the superscript in the following. So, we will write rather than , etc.

to denote the sample mean of the th constituent, the sample mean of the portfolio, the sample variance of the portfolio, and the sample covariance of the th constituent and the portfolio, respectively.

Motivated by the Representation (2.1) we define the allocation estimator as

| (3.6) |

where and are the estimators of the slope and intercept regression coefficient from the orthogonal projection of the th margin of onto , and where is an unbiased risk estimator (in the sense of [PS18]) for the Expected Shortfall of the secured position . It has been shown in [PS18, Example 5.4] that under normality can be represented as

| (3.7) |

where is deterministic, and depends only on the sample size , and risk level . Consequently, the estimator becomes

Before we show that satisfies the fairness property, we show an important conditional unbiasedness property of the estimators and , in the usual statistical sense. Towards this end, for , we use

to denote the true regression coefficients of the –orthogonal projection of th margin of onto under , for ; see Section 2.1. Note that, in view of our assumption that for any the random sample is i.i.d. under , we get and , for .

Proposition 3.3.

For any it holds that

| (3.8) |

Proof.

Recall from Section 2.1 that under normality, for , , and , we have

| (3.9) |

where is a zero mean Gaussian random variable independent of . As a simple consequence of (3.9) we obtain that is independent of and under for all . Then, by definition,

| (3.10) | ||||

Inserting (3.9), and using that , we obtain

We use again (3.9) and obtain

| (3.11) |

with satisfying , so that

| (3.12) |

and hence yielding our first claim. With this result and using (3.11), we obtain

which concludes the proof of (3.8). ∎

Proposition 3.3 shows that we can estimate the portfolio risk expressed through and without impacting the statistical unbiasedness property of the regression coefficients; cf. Equation (3.7). Consequently, the risk allocation estimation procedure could be split into two independent steps. First, we estimate the aggregated portfolio risk, and then we estimate the proper allocation of the risk within portfolio constituents. Now, we use this property to show that the allocation estimator given in (3.6) satisfies the fairness property.

Theorem 3.4.

Proof.

In what follows we will simply write instead of . We note that for any the Radon-Nikodym density is -measurable; see [Che06, Proposition 6.2] and recall that . Moreover, since

we obtain that

Consequently, as expected,

| (3.13) |

and Equation (3.7) yields that is -measurable. With a view towards (3.4), we compute

by Proposition 3.3. Analogously,

and we obtain

| (3.14) |

Next, using (3.5) and (3.13) yields that

| (3.15) |

This result, together with representation (3.9) for , and letting , imply that

| (3.16) |

where we used the fact that is bivariate normal with uncorrelated margins, so that is independent of , and consequently from . This concludes the proof. ∎

4 Asymptotic fairness

We now introduce the definition of fairness for a sequence of estimators, , and we define the notion of asymptotic fairness.

Definition 4.1.

A sequence of allocation estimators will be called fair at , if is fair. If fairness holds for all , we call the sequence fair. The sequence is called asymptotically fair if

| (4.1) |

In view of Theorem 3.4 it is clear that the sequence of capital allocation estimators defined in (3.6), for varying , is a fair sequence.777Recall that the superscript is omitted in (3.6) for the ease of notation.

In the rest of the section we assume that the risk allocation is done using ES with reference level .

4.1 Asymptotic fairness of capital allocation estimators under normality

Using (2.14), we now define a sequence of “plug-in type” capital allocation estimators as

| (4.2) |

The sequence is not fair, in general, but it is asymptotically fair, as proven below.

Proposition 4.2.

The sequence is asymptotically fair.

Proof.

Set and note that

Proceeding analogously to the proof of Theorem 3.4, with replaced by and with replaced by , we see that in order to prove proposition it is enough to show that for any we have

| (4.3) |

Now, note that

and, in the terminology of [PS18], is the standard Gaussian expected shortfall plug-in estimator for . Consequently, noting that for the definition of asymptotic fairness coincides with the definition of asymptotic unbiasedness given in [PS18, Definition 6.1], and using [PS18, Proposition 6.4] we conclude the proof. ∎

4.2 Asymptotic fairness of non-parametric capital allocation estimators

We assume throughout this section that the population , and hence the aggregated portfolio , are continuous random variables under any . Given that the ES is used to determine the risk allocation, and taking (2.6) and (2.9) into account, we consider two natural non-parametric expected shortfall capital allocation estimators

| (4.4) | ||||

| (4.5) |

where , with denoting the th order statistics, and denoting the largest integer less or equal than .

Proposition 4.3.

The sequences and are asymptotically fair.

We will show only that is asymptotically fair. The proof for follows by similar arguments. Before we prove Proposition 4.3, let us introduce supplementary notation and a lemma that will be useful for the proof. For any we use to denote the true expected shortfall allocation for under and so we have (cf. (2.6))

where denotes the true -quantile of under . Similarly, we have

Lemma 4.4.

For any we get , as .

Proof.

Let us fix . For brevity we will use the notation and . First, using classical trimmed-mean convergence arguments (see e.g. [Sti97]) we will show that

| (4.6) |

Let and , . Since , we get

where . Next, we will show that . Due to the consistency of the empirical quantiles, we have that and , as . Hence, noting that

it is sufficient to prove that . For this, we observe that

Since , , and, by the Law of Large Numbers, , we have that . Also, by the Law of Large Numbers we get at once that

which concludes the proof of (4.6).

Next, for a fixed , we get

| (4.7) | ||||

| (4.8) |

We want to show that (4.7) and (4.8) go to zero as . For brevity, we show the proof only for (4.7); the proof for (4.8) is analogous. For any we get

| (4.9) |

Using (4.6), and recalling that convergence in probability implies convergence in distribution which in turn implies convergence of quantiles (at continuity points) for we get

| (4.10) |

Combining (4.9) with (4.10), noting that the choice of was arbitrary, and that is continuous, we conclude the proof. ∎

Now, we are ready to prove Proposition 4.3.

Proof of Proposition 4.3.

Let us fix and . We want to show that

Noting that

where , we need to prove that

| (4.11) |

and

| (4.12) |

We start with the proof of (4.11). Noting that for any we have and

we get

| (4.13) |

Now, noting that and using Lemma 4.4 we get

Combining this with (4.13), noting that and are integrable, and as , we conclude the proof of (4.11).

Next, we prove (4.12). Recalling that is a true allocation for under we get

Consequently, noting that and are independent under we get

| (4.14) |

where , and where in the last equality we used the property . By similar reasoning as in (4.9), we get

for any . Since is a consistent estimator of , we conclude that , as . Consequently, as the choice of was arbitrary and is continuous, we obtain that , as . Combining this with (4.14), and since is integrable, and as , the proof of (4.12) is complete.

∎

5 Backtesting and numerical examples

In this section we analyze the proposed fair capital allocation methodology via examples using simulated data and real market data. It goes without saying that any quantitative methodology used for measuring and allocating risk relies on an adopted formal model. It also goes without saying that actual results of risk measurement and/or risk allocation need to be tested for their adequacy. Often, testing adequacy of the results of risk measurement is done in practice using backtesting, and we will use this approach in testing the estimation procedures of fair capital allocation introduced in the previous sections.

Backtesting, applied for risk measurement in the financial context, can be summarized as follows: given a time series of capital forecasts, one compares these forecasts with the realized losses; the accumulated performance is the key ingredient of the backtesting. Backtesting might be also treated as a specific case of assessment of quality of a point forecast, which aims at assessing whether the forecasted capital is sufficient; see [Zie16, SKG15, NZ17]. In particular, backtesting value-at-risk goes back to [Kup95] and recently has gained a lot of practical and theoretical interest; see [AS14, PS18] for further details on this topic and the related literature. Undoubtedly, similar backtesting procedure should be developed for testing the adequacy of risk capital allocation methodologies.

We focus our attention on assessing the performance of a statistical capital allocation methodology when the underlying reference risk measure is expected shortfall at the fixed level , used in computing of the values of our estimators. For this purpose we propose two backtesting frameworks:

-

•

absolute deviation from fairness backtesting;

-

•

risk level shifts adjustments backtesting.

The backtesting framework adopted for assessment of adequacy of estimators of capital allocations, say , that were created using some capital allocation methodology,888We refer to such methodology as to an Internal Capital Allocation Model (ICAM). uses as its input the observations of past P&Ls. The key ingredient to both backtesting methods is the estimation of

| (5.1) |

and the estimation of

| (5.2) |

We assume that the length of the backtesting window is days. With each day we associate the P&Ls and allocation estimators , The estimators can be obtained in various ways. One way is to proceed in accordance to what was proposed previously in this paper. Specifically, to produce allocation estimators on day one uses market observations from the previous days. We denote these observations as . Based on these observations, and following (3.3), we compute the estimators of the allocations as .

The realizations of and are denoted as and , respectively. We set , where , , and . We also let , to denote the realized aggregated secured position on day , and we set .

In order to proceed we introduce the following functions of ,

| (5.3) |

and

| (5.4) |

with being the empirical value-at-risk at level . Note that s are computed using as the reference risk measure ES at the fixed risk level . If no confusions arise, we will write , respectively , instead of , respectively .

Now, similarly to the derivation of , we estimate the expectation in (5.1) as , and we estimate (5.2) as .

Deviation from fairness backtesting. If the capital allocation methodology is fair, then the obtained empirical values , should be close to zero, for the fixed reference level ; the bigger the obtained estimate, the bigger the potential (true) deviation from fairness for the th margin. The deviation from fairness backtest assesses proximity to zero of . A comprehensive study of properties of s, such as ‘how far from zero is an acceptable value’ is beyond the scope of this manuscript. Nevertheless, the following backtesting methodology is one way to address this question.

Risk level shift backtesting. Instead of measuring the deviation from fairness directly, it is natural to find the reference risk level that makes closest to zero; equivalently, we want to answer the question by how much one needs to shift the reference risk level to make the position acceptable. This approach hinges on duality-based performance measurement introduced in [PM18]. It should be noted that this approach is different from the elicitability-based backtests as it focuses on capital conservativeness assessment rather than the general forecast fit; cf. [NZ17]. Formally, for the estimators of capital allocation , we define

| (5.5) | ||||

| (5.6) | ||||

| (5.7) |

where in (5.6) we use the convention , and correspondingly, in (5.7) we put . Similar to , we may simple write , and . Note that is a monotone decreasing function in , while generally speaking is not monotone. Hence, the quantities are defined as the smallest shift in the reference risk level from , to the right or to the left, that makes the th secured position acceptable. Thus, the closer is to the initial reference risk level the better is the total risk estimation procedure. Similarly, the closer are to zero, the better is the risk allocation procedure. One can look at as the performance index that is dual to the ES family; see [PM18, Proposition 4.3] for more details.

Finally, by combining the left and right minimal shifts, we define the the minimal shift estimator as

| (5.8) |

Before moving to numerical examples, several comments on backtesting procedure are in order.

-

(a)

It goes without saying that the results produced by the deviation from fairness and the risk level shift approaches should be compared with each other for consistency and reality check.

-

(b)

It is worth mentioning that the two proposed backtesting methodologies can be applied to any ICAM, not necessarily those discussed in this paper.

-

(c)

Our study of the backtesting procedure of the estimation of the risk capital allocation is preliminary. A thorough investigation of the statistical properties of and is deferred to future studies.

Next we will illustrate the performance of the capital allocation estimators , , and on simulated data by applying the two backtesting procedures described above. For brevity and to ease the notation, we will write , , and as , , and , respectively.

For simulations, we consider two cases of probability distributions of the P&Ls vector - the Gaussian distribution and the Student’s -distribution. We also fix the reference level . All numerical evaluations are performed using R statistical software; the source codes are available from the authors upon request.

Example 5.1 (Gaussian P&Ls).

We assume that the portfolio of eight (discounted) P&Ls follows an eight dimensional Gaussian distribution , with the (true) mean

and the (true) variance-covariance matrix

For the purpose of obtaining the above mean vector and the variance-covariance matrix we used values of daily returns of eight stocks from S&P 500 index, namely: AAPL, AMZN, BA, DIS, HD, KO, JPM, and MSFT; these data were taken for the period from January 2015 till December 2018. We will use this sample again in Example 5.4. The first six stocks represent long positions in our portfolio and the last two represent short positions; this gives the negative entries in and . The positions in each stock are equally weighted with nominal (absolute) value $1.

We took the learning period of days, and the backtesting period of days. Below, we present the results for the Gaussian plug-in estimator and the non-parametric estimator ; we omit results for estimators and , since, due to large size of the learning period, the results are almost identical to and , respectively. Additionally, for comparison, we present results for the true allocations ; these allocations were obtained by plugging-in true mean and covariance matrix into (2.14).

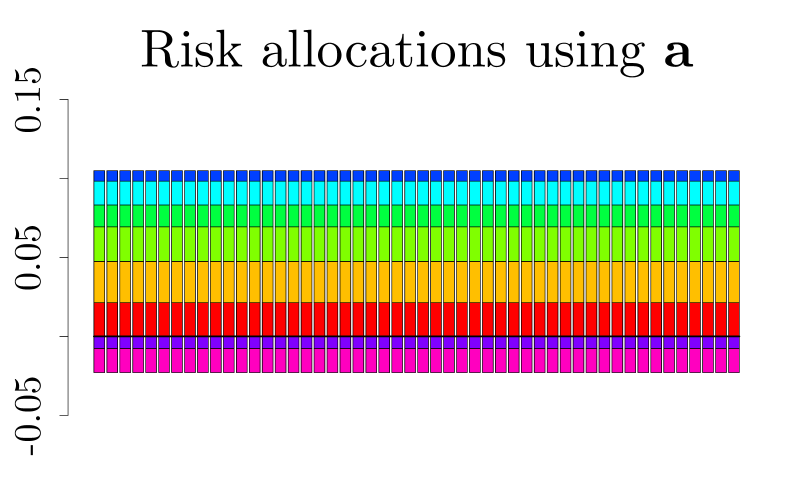

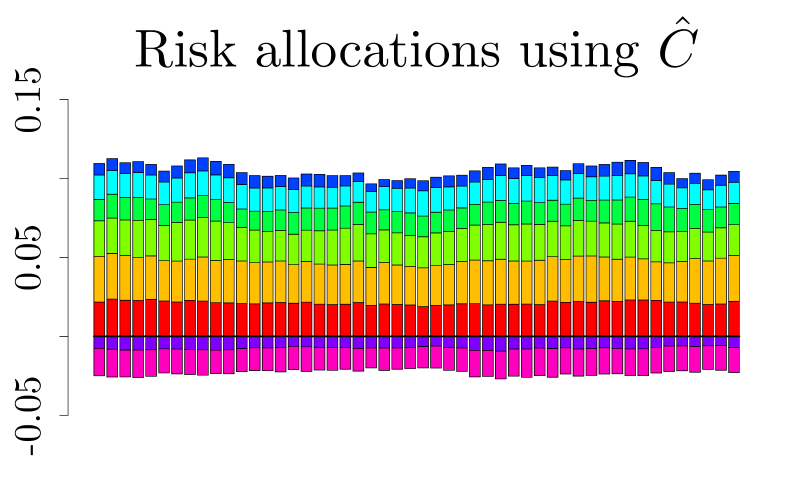

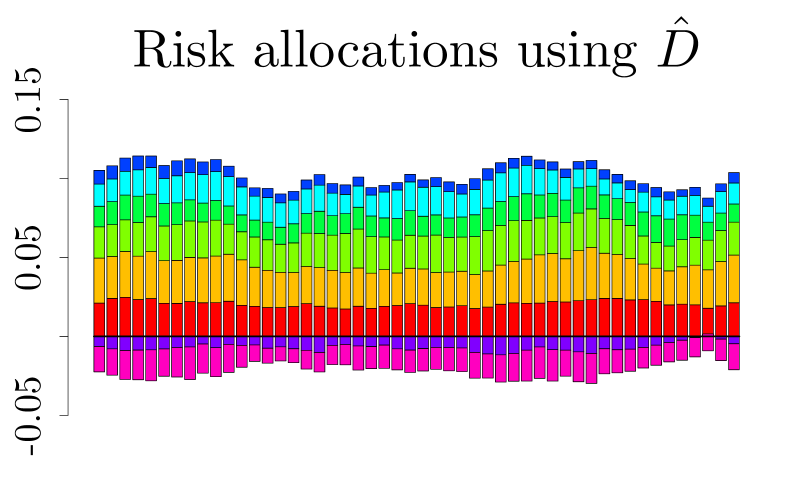

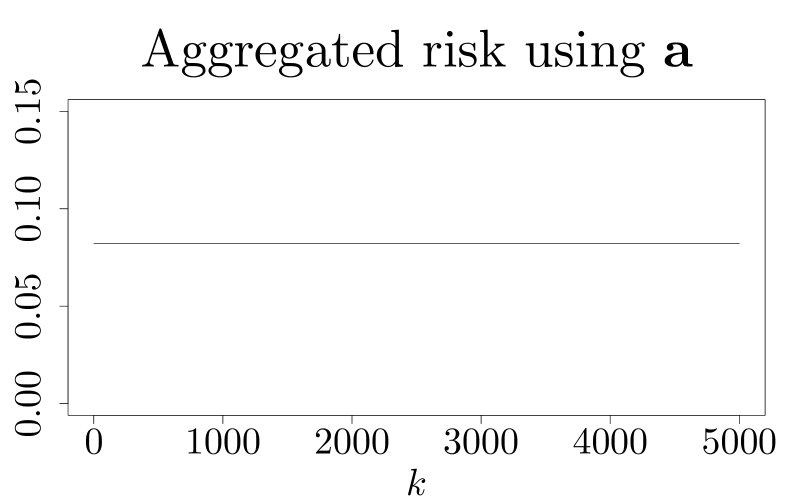

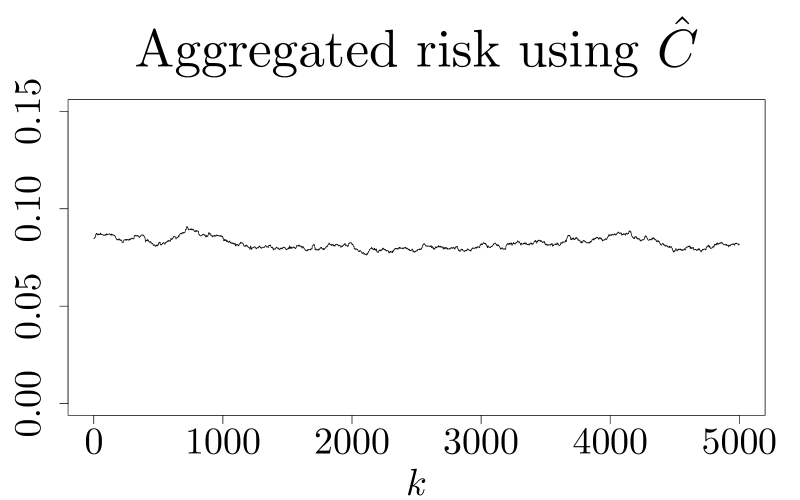

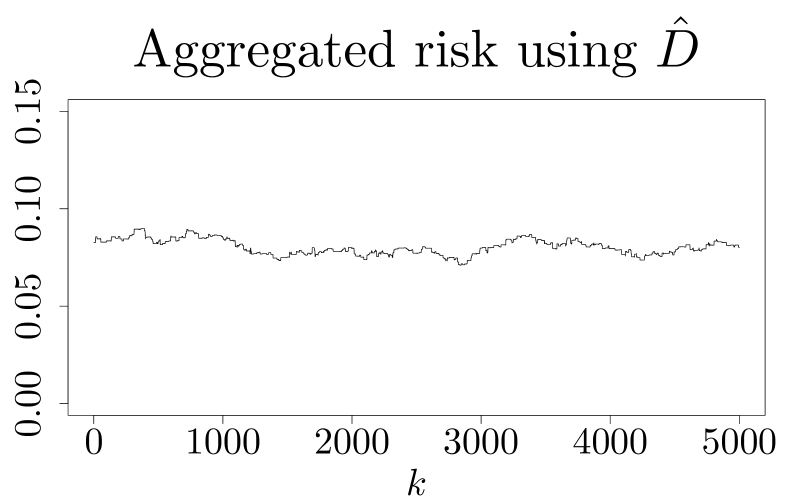

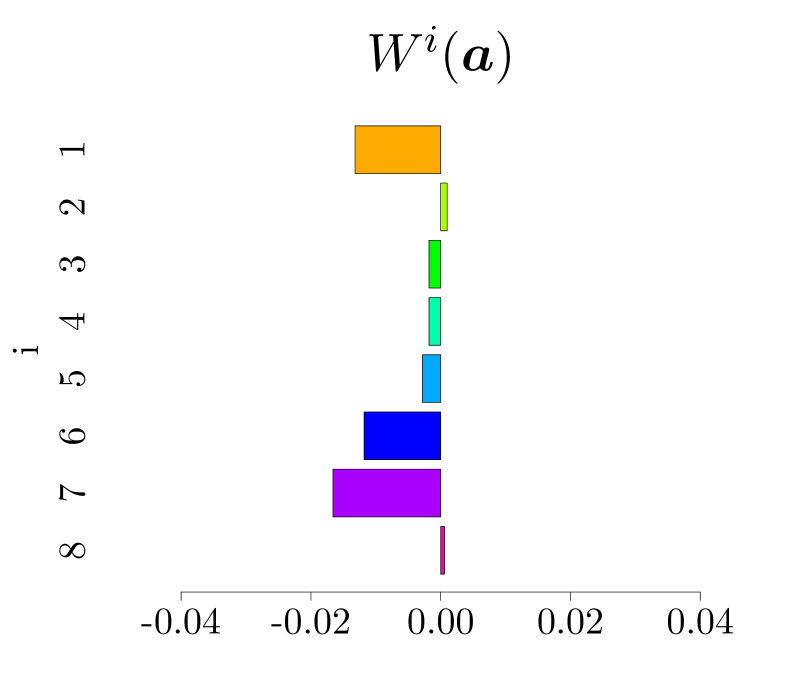

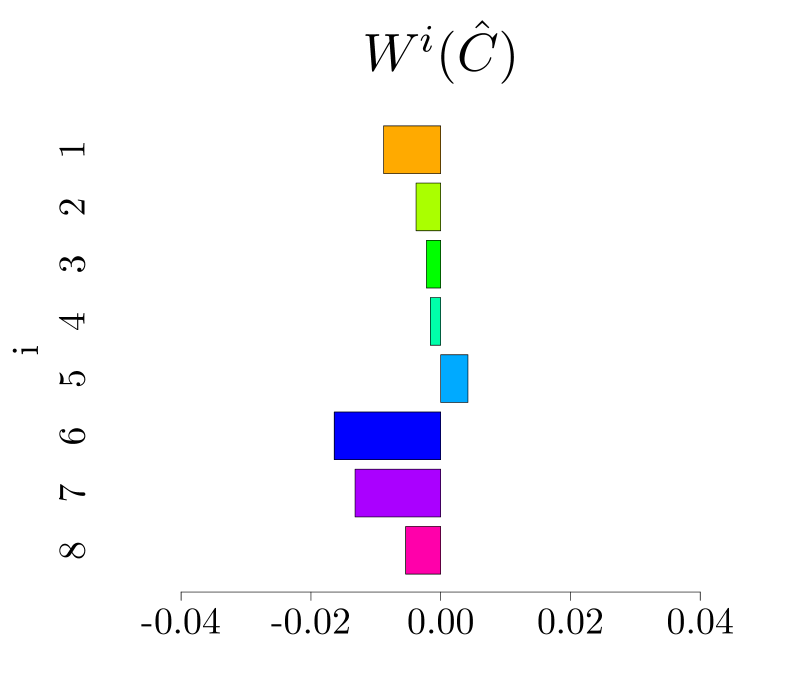

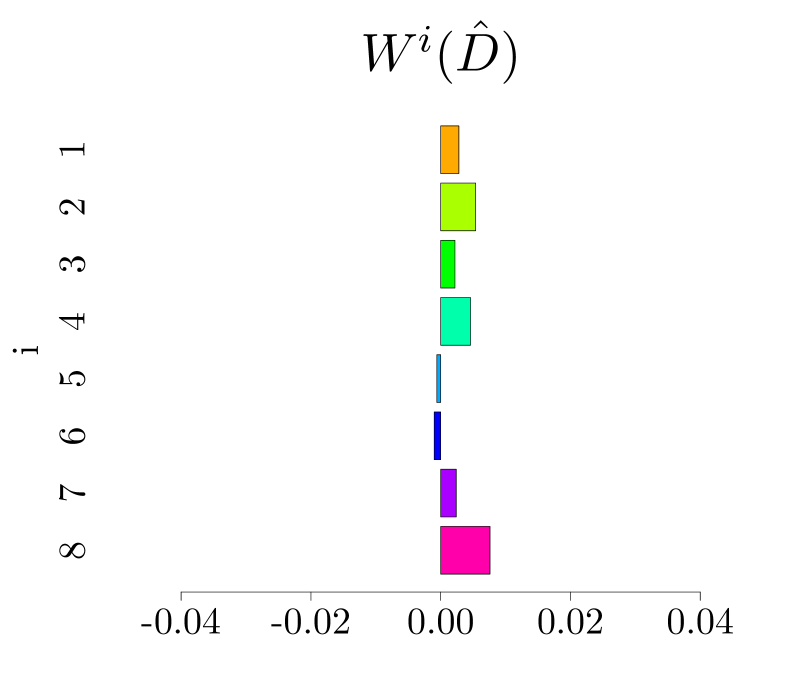

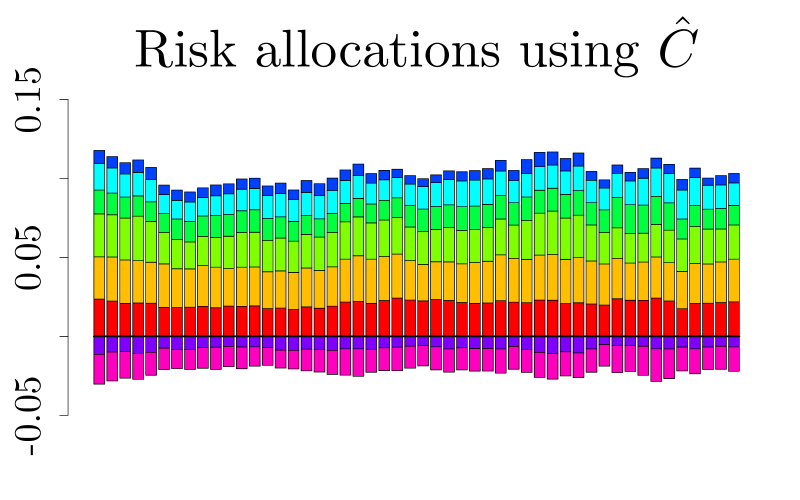

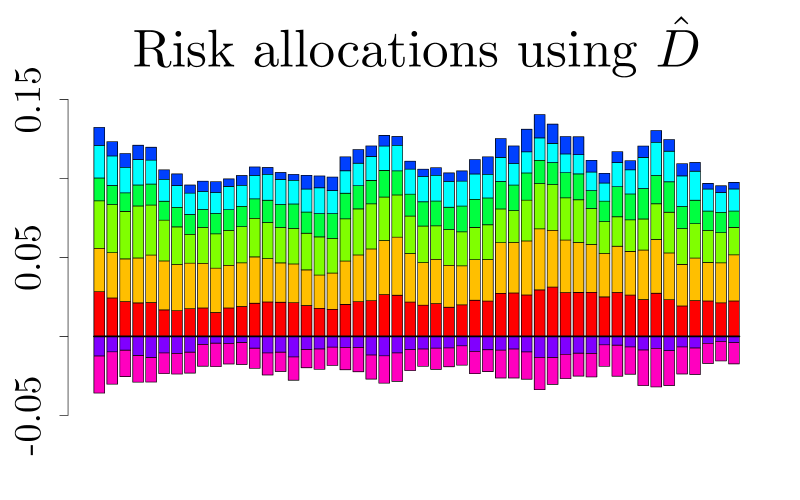

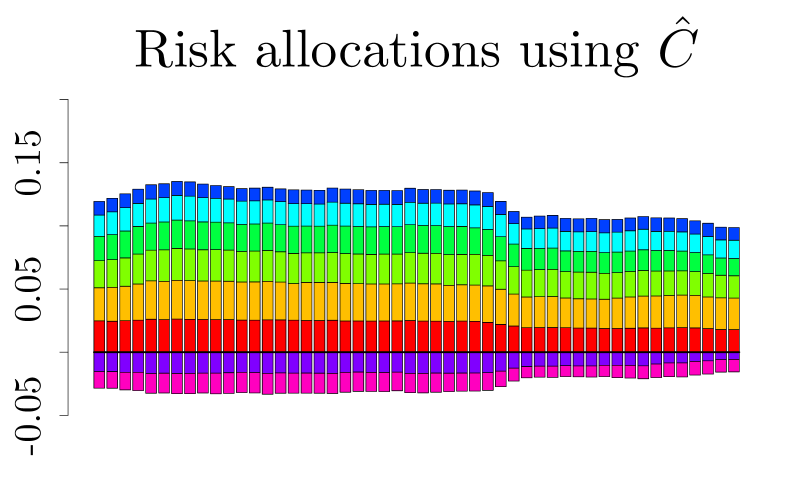

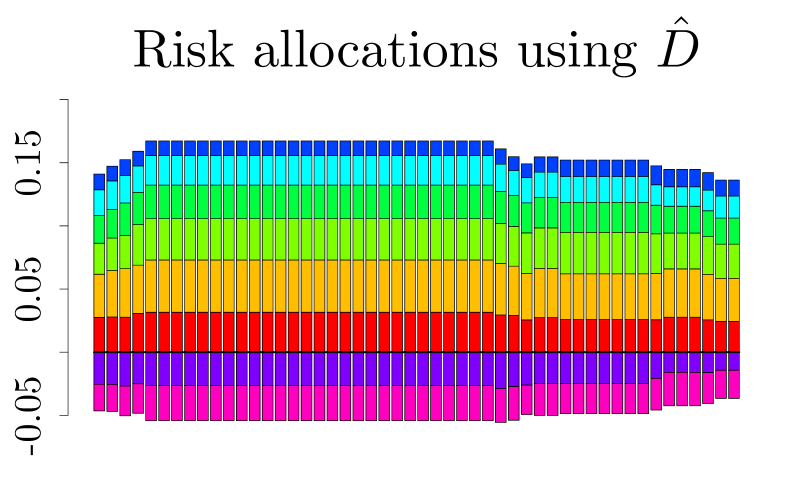

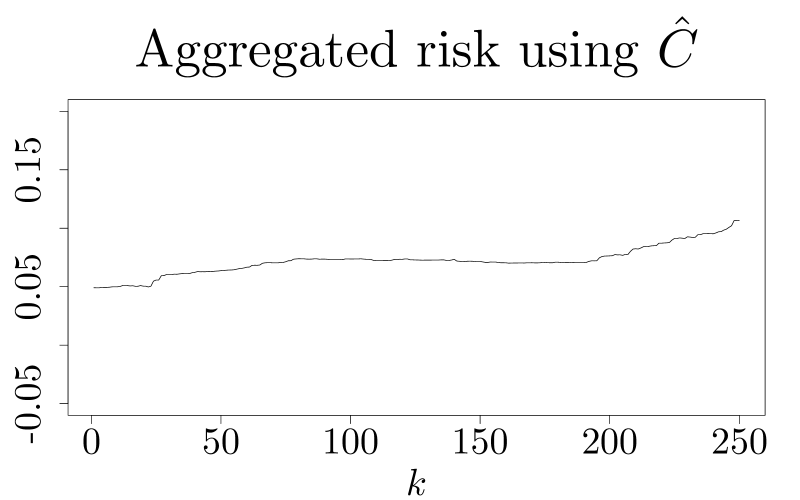

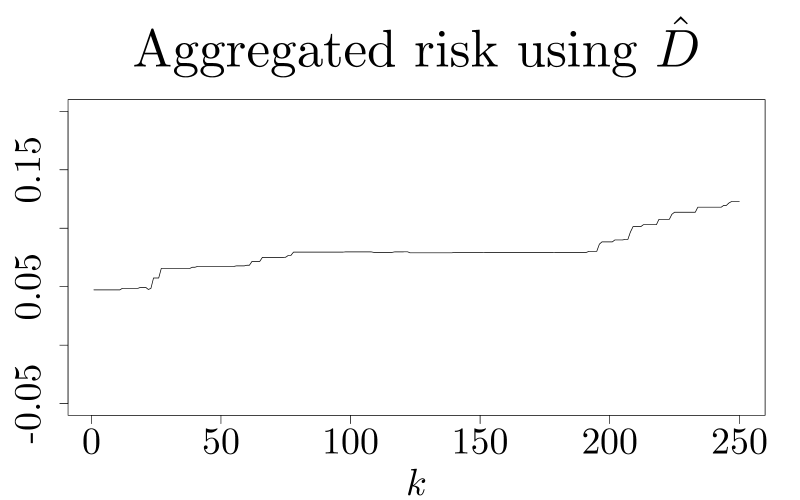

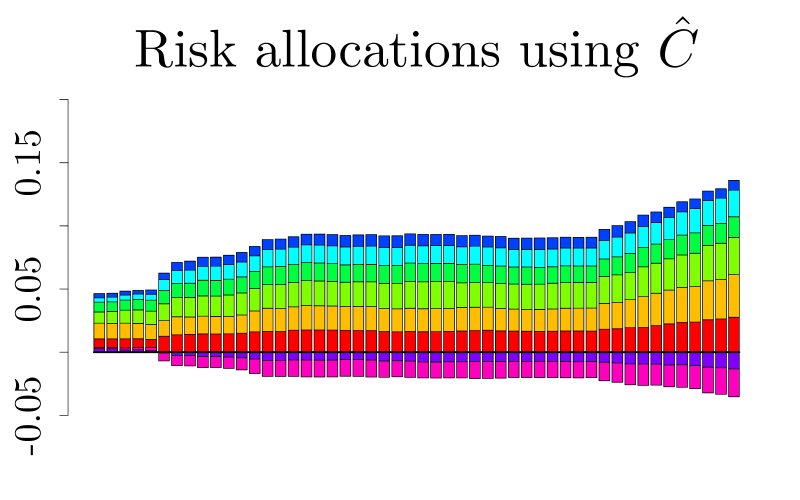

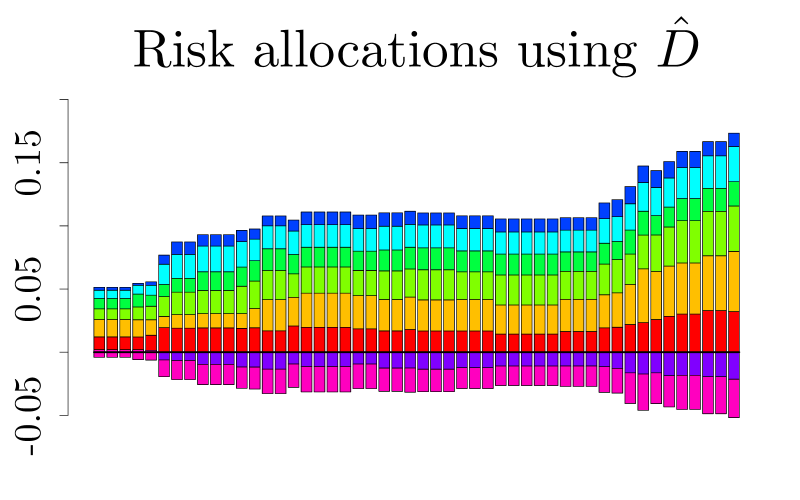

The obtained results validate, as expected, the proposed methods. In Figure 1 we present the values of the risk allocation to each constituent (top row), and the aggregated risk (bottom row). In this example, the fair risk allocation computed with the true underlying distribution can be considered as reference for the backtesting results. The estimated risk allocations using and are close to the reference allocations, and as expected, the results computed using the non-parametric method are not as close to the reference results as those obtained using that explicitly exploits the Gaussian distribution structure of the data.

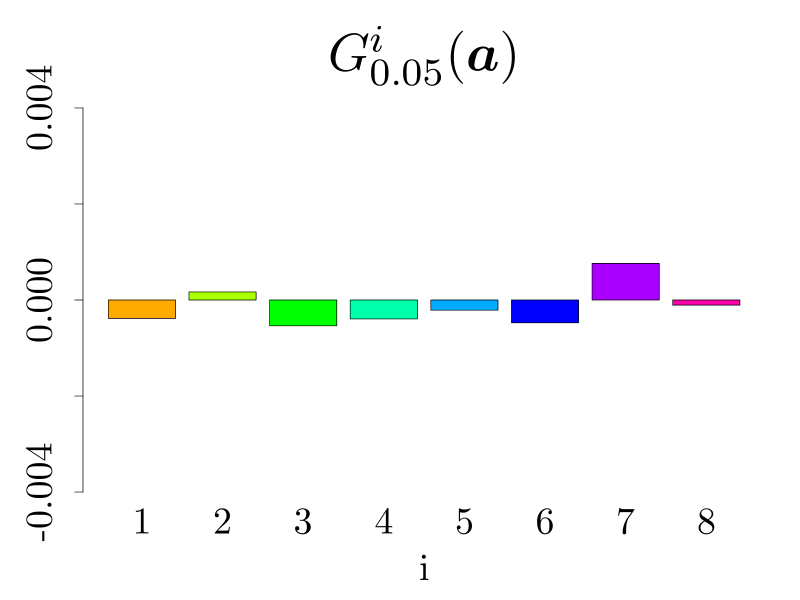

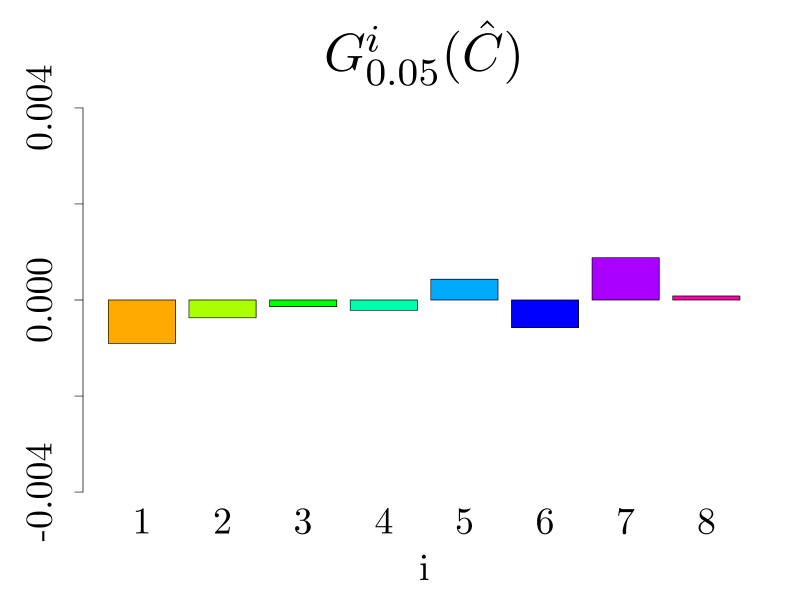

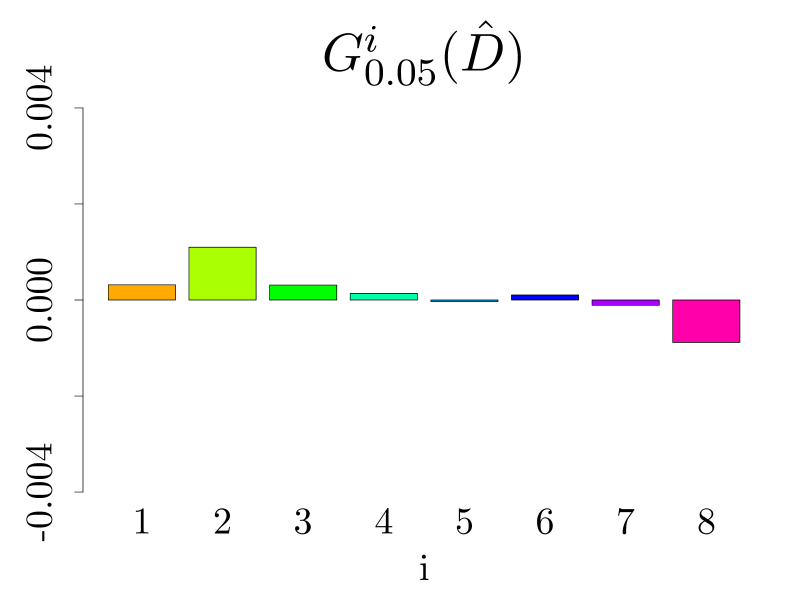

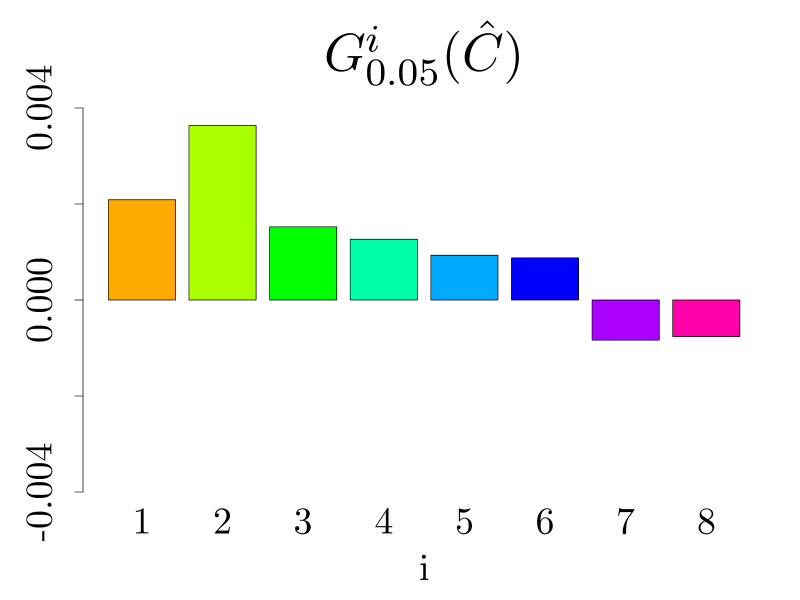

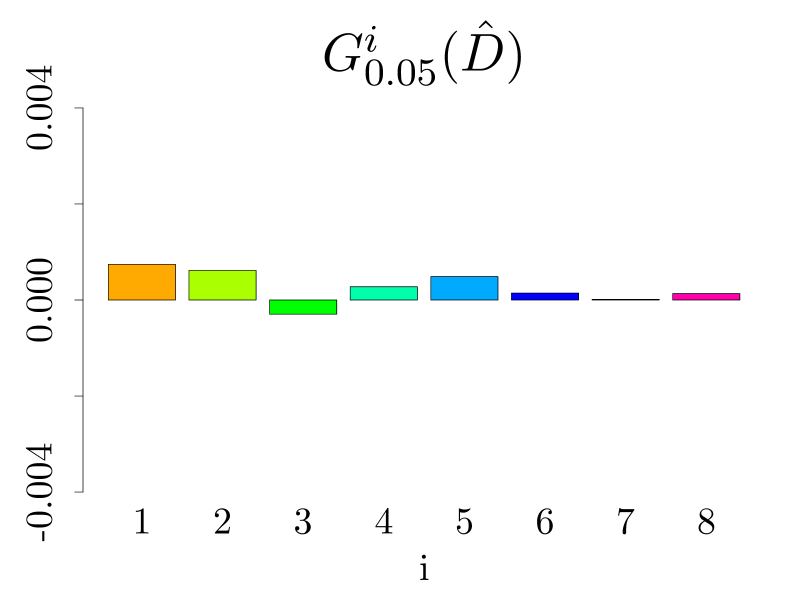

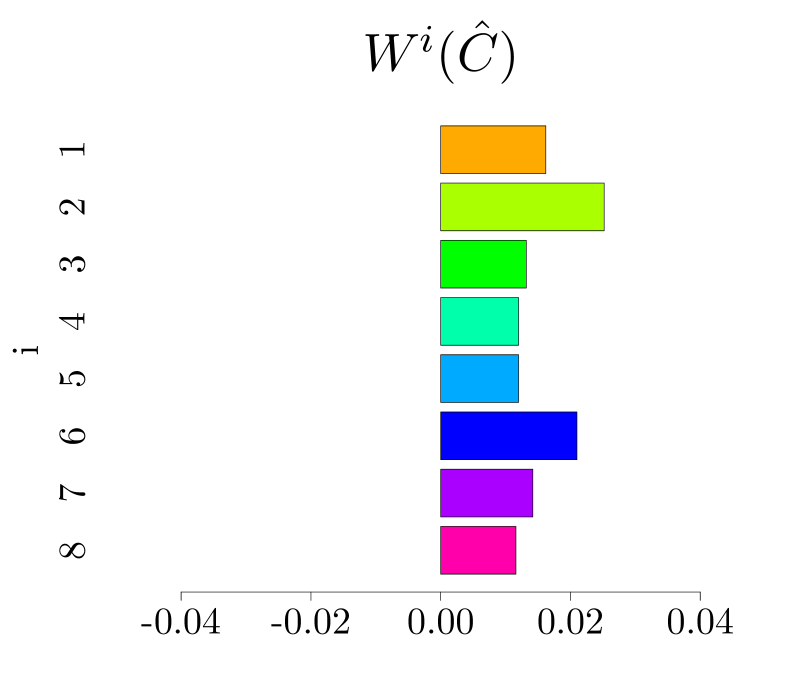

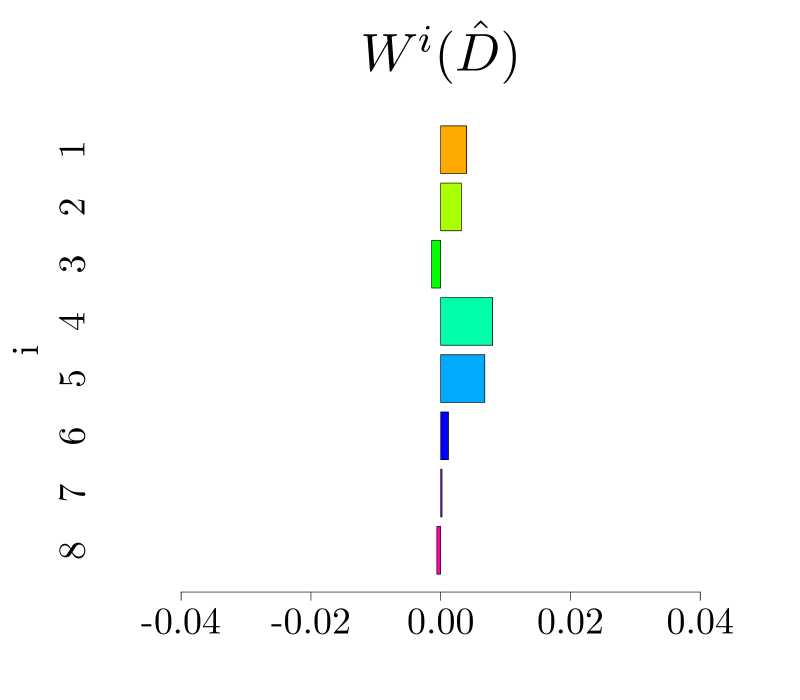

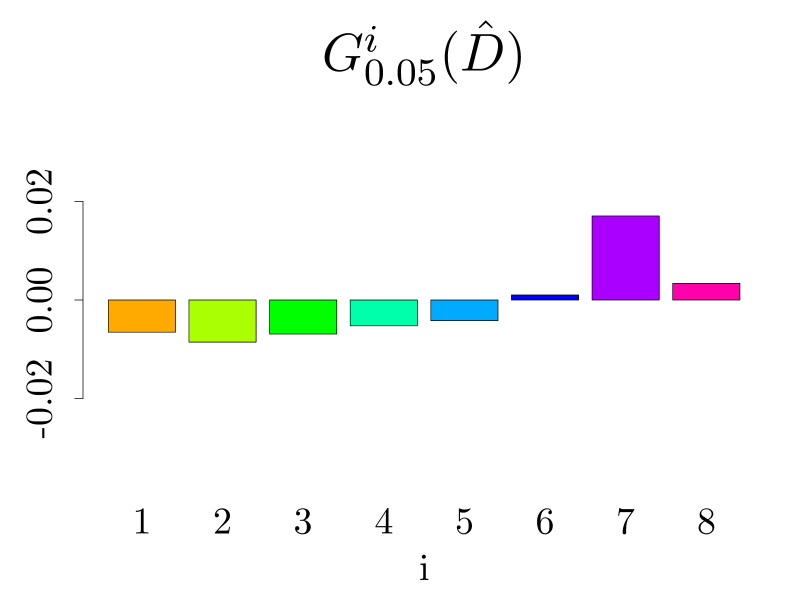

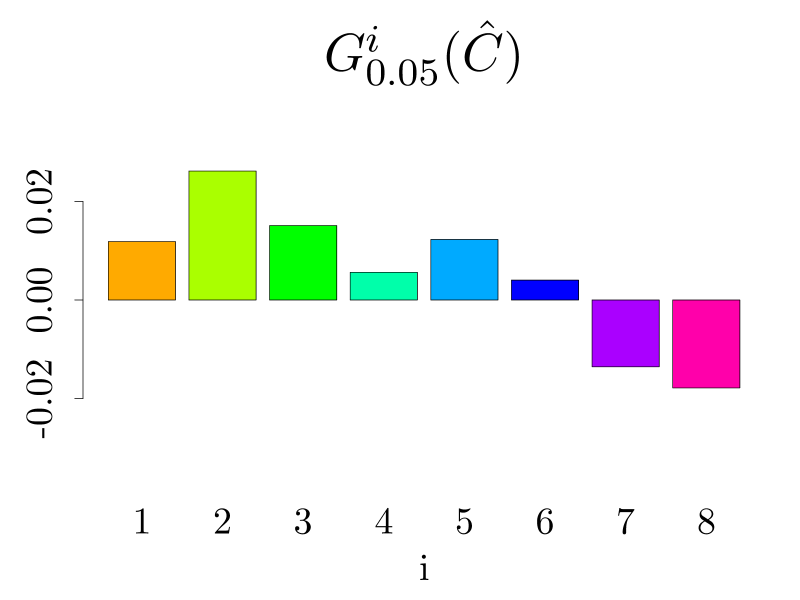

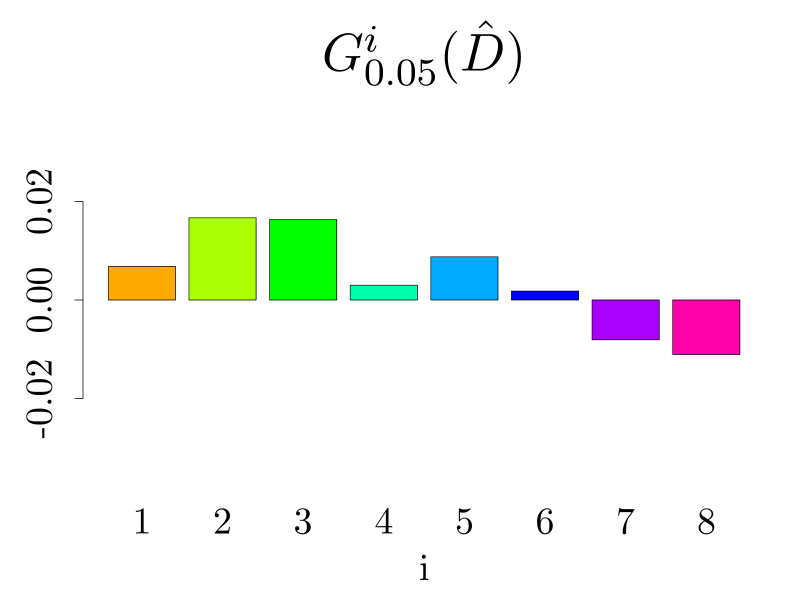

Table 1 contains the summary of the estimated backtesting measures and . First, we note that the values of and corresponding to backtesting the fair allocation are, as expected, close to zero. In addition, is close to . This indicates that the proposed backtesting methodologies are adequate. The obtained values give the benchmark for the following results produced by using and . We note that indeed, the values of and corresponding to and are in the same ballpark as for , indicating that and are suitable risk allocation methodologies. We also provide a graphical representation of in Figure 2 (top row), and in Figure 2 (bottom row) we as function of .

| -0.00038 | 0.00017 | -0.00054 | -0.00039 | -0.00021 | -0.00048 | 0.00076 | -0.00011 | -0.00118 | ||

| -0.013 | 0.001 | -0.002 | -0.002 | -0.003 | -0.012 | -0.017 | 0.001 | 0.047 | ||

| -0.00090 | -0.00037 | -0.00014 | -0.00022 | 0.00043 | -0.00058 | 0.00088 | 0.00008 | -0.00081 | ||

| -0.009 | -0.004 | -0.002 | -0.002 | 0.004 | -0.016 | -0.013 | -0.005 | 0.048 | ||

| 0.00032 | 0.00110 | 0.00031 | 0.00014 | -0.00003 | 0.00010 | -0.00011 | -0.00088 | 0.00094 | ||

| 0.003 | 0.005 | 0.002 | 0.005 | -0.001 | -0.001 | 0.002 | 0.008 | 0.053 |

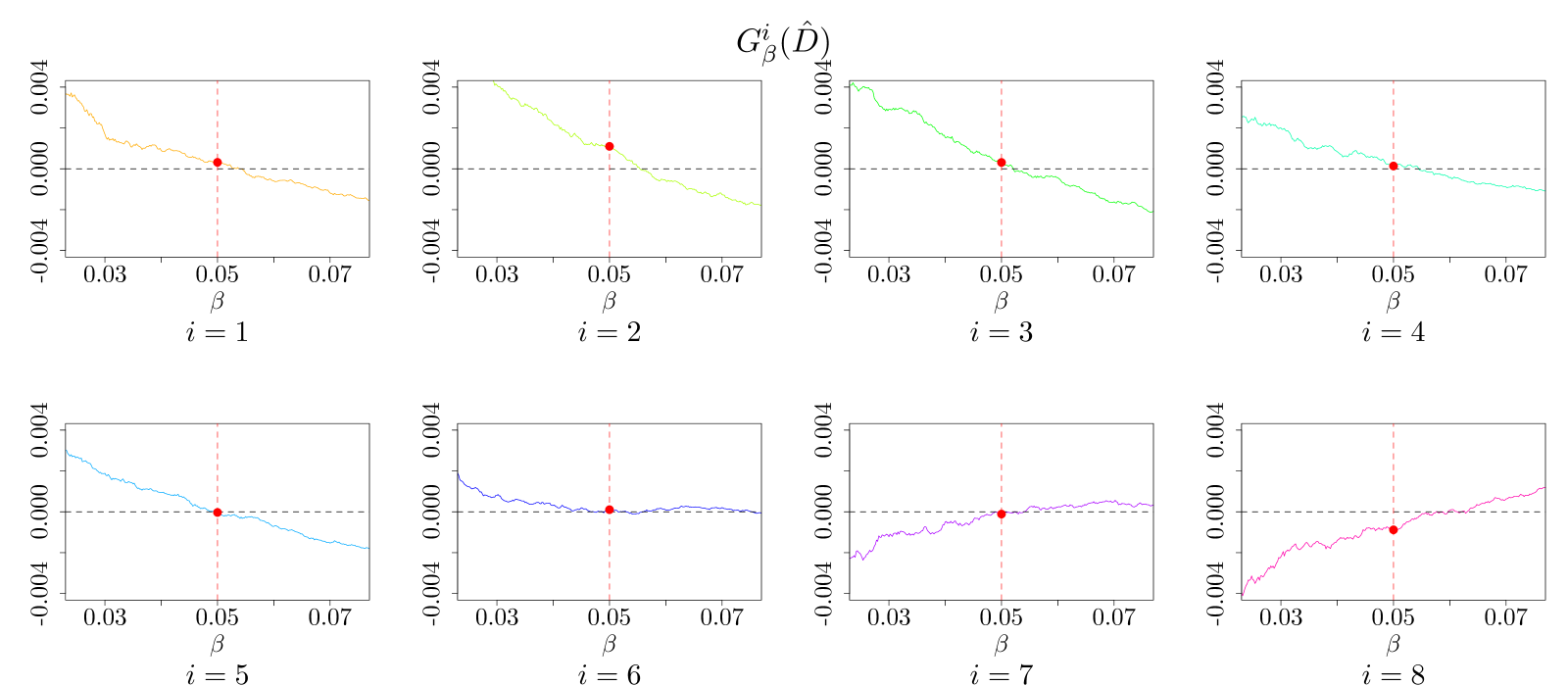

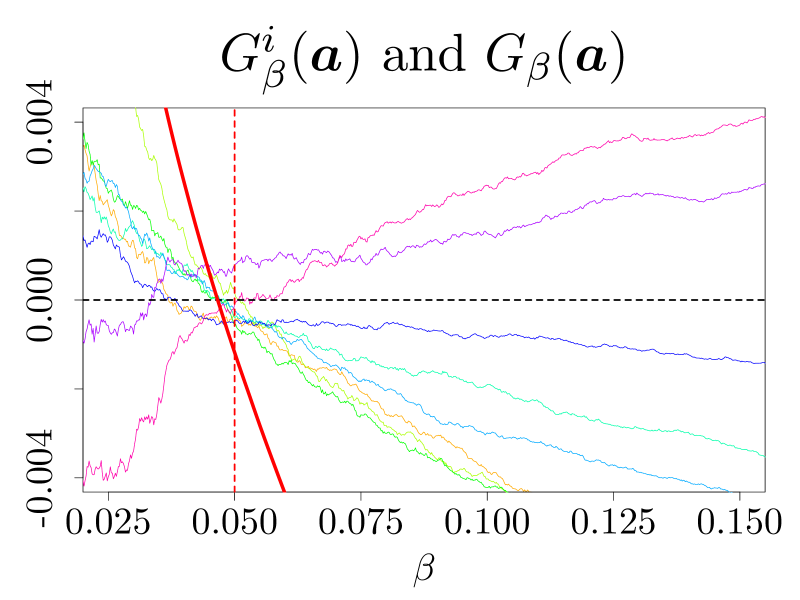

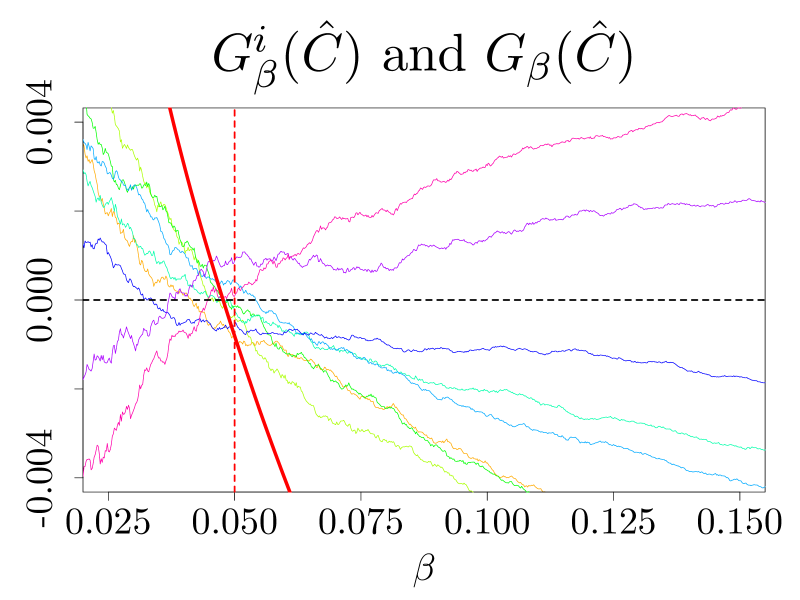

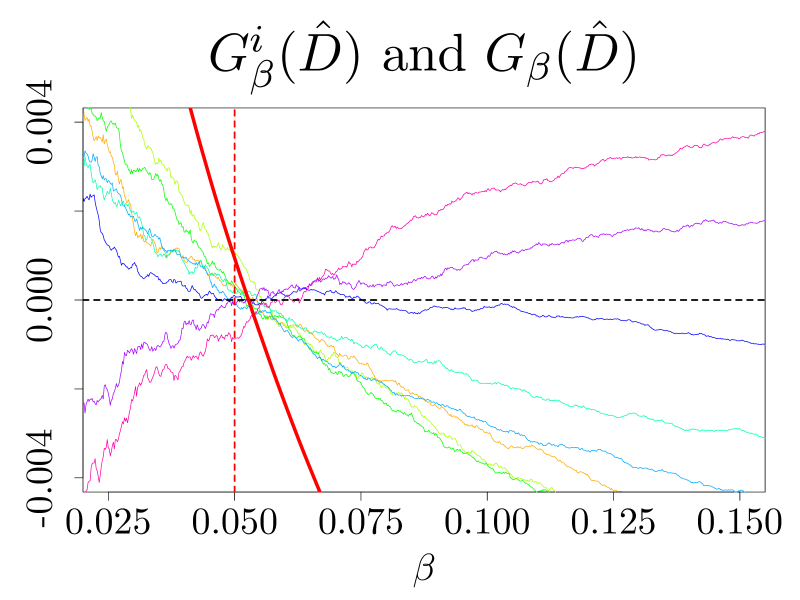

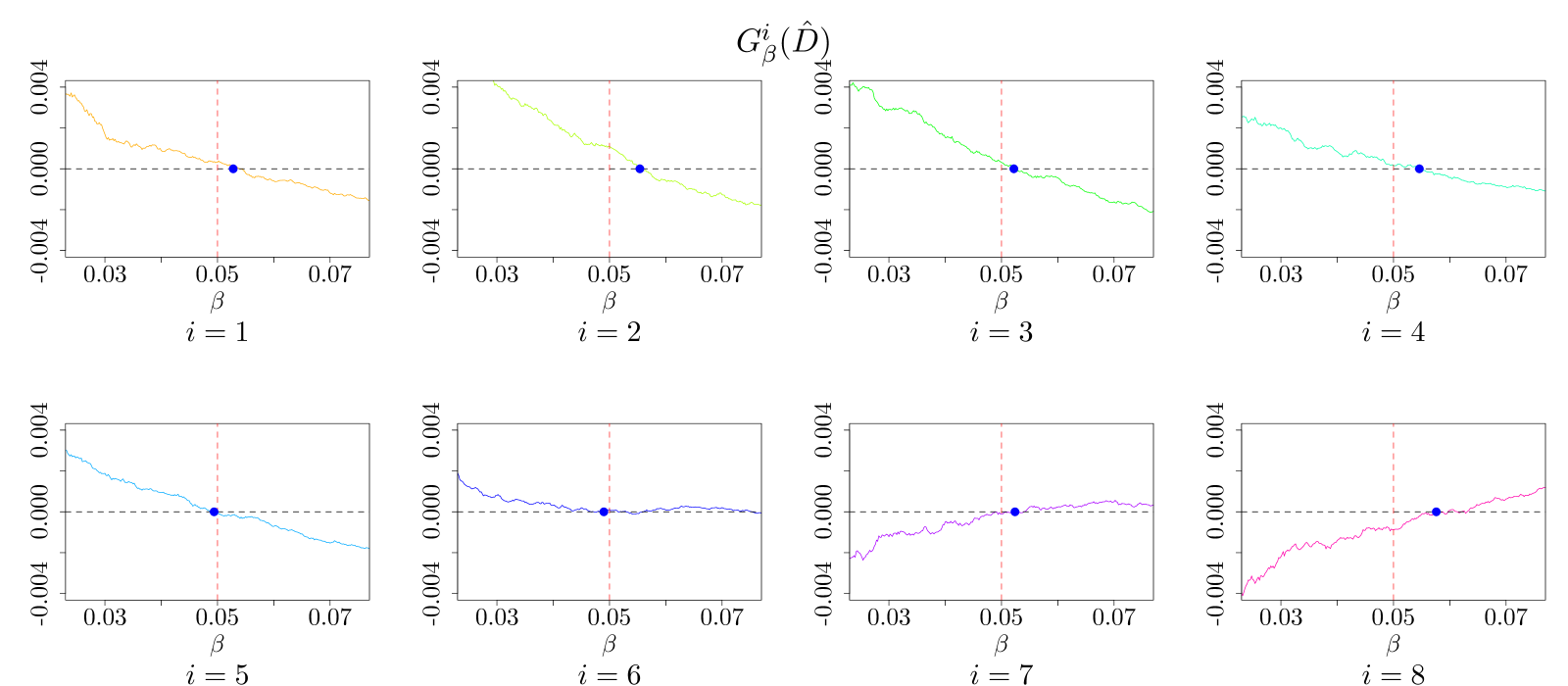

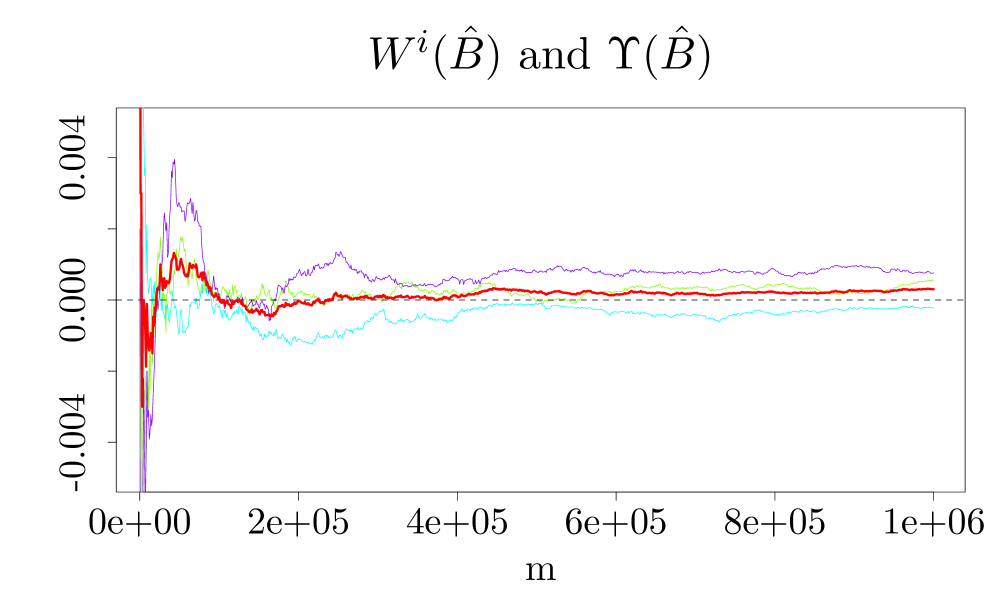

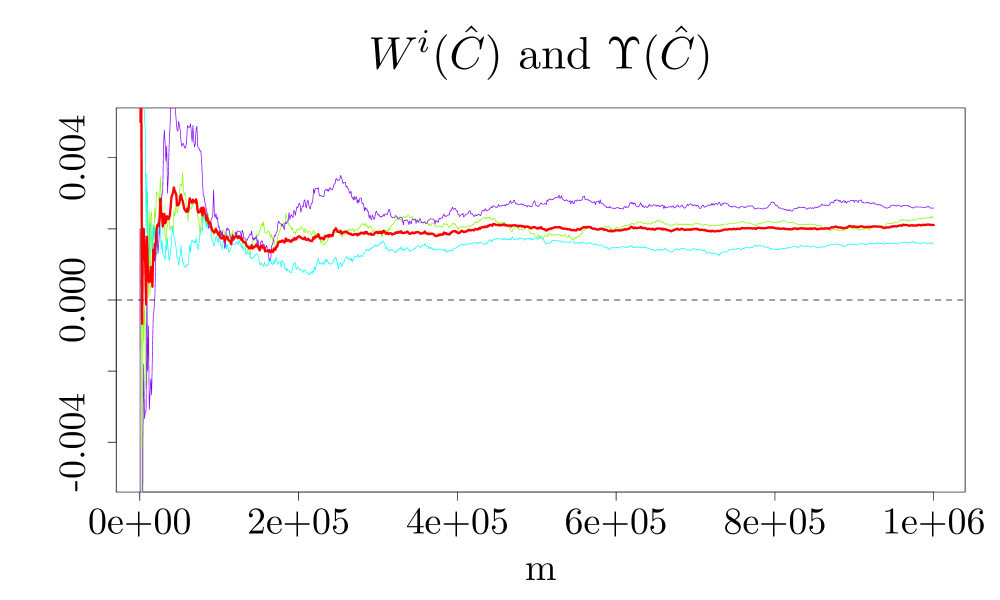

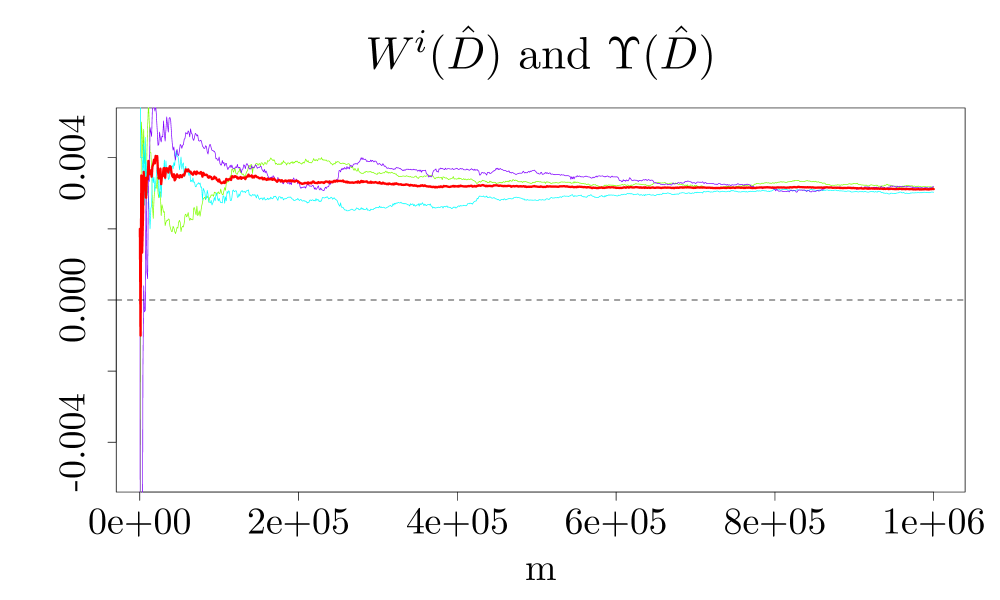

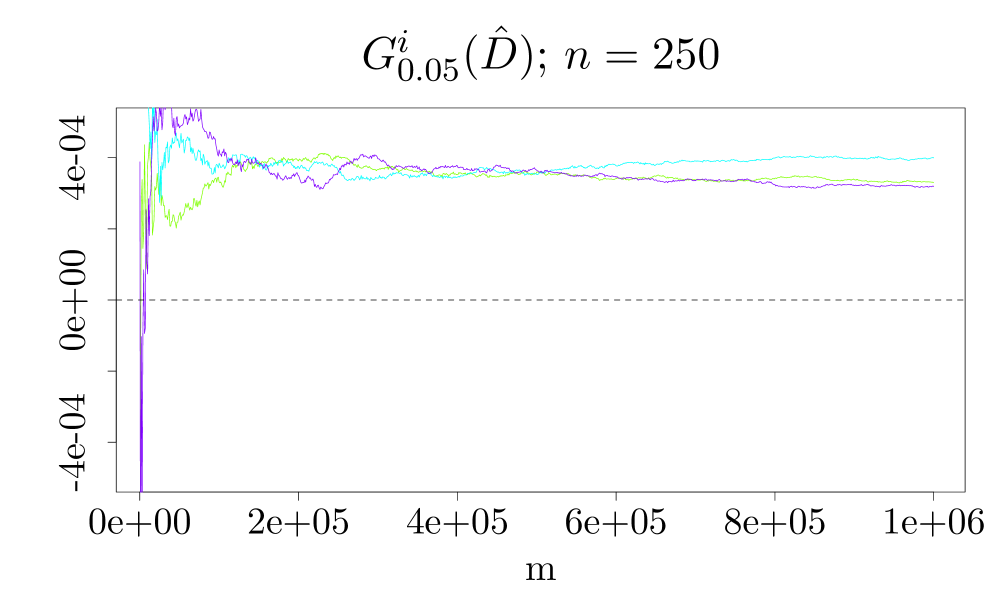

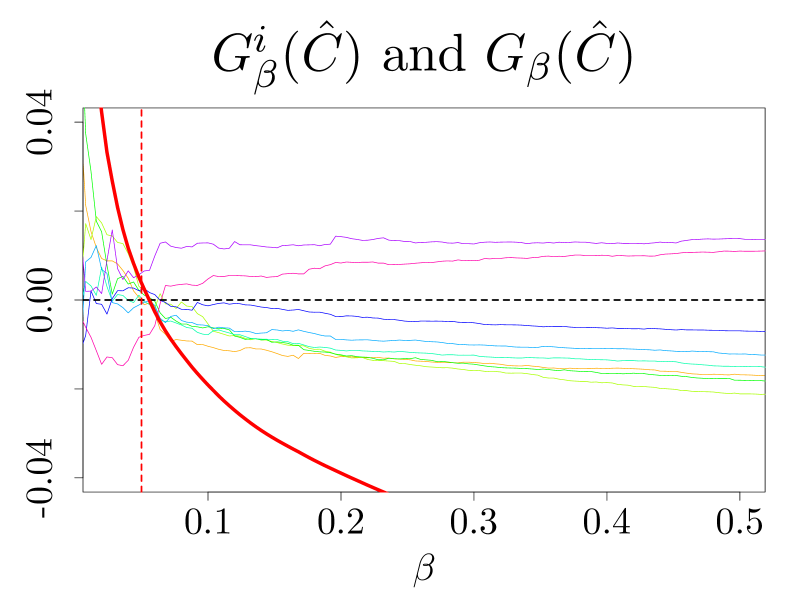

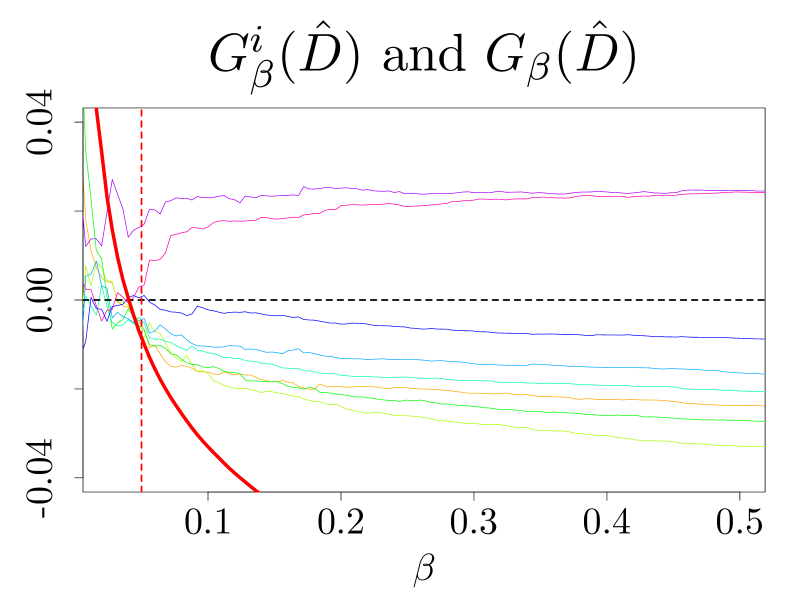

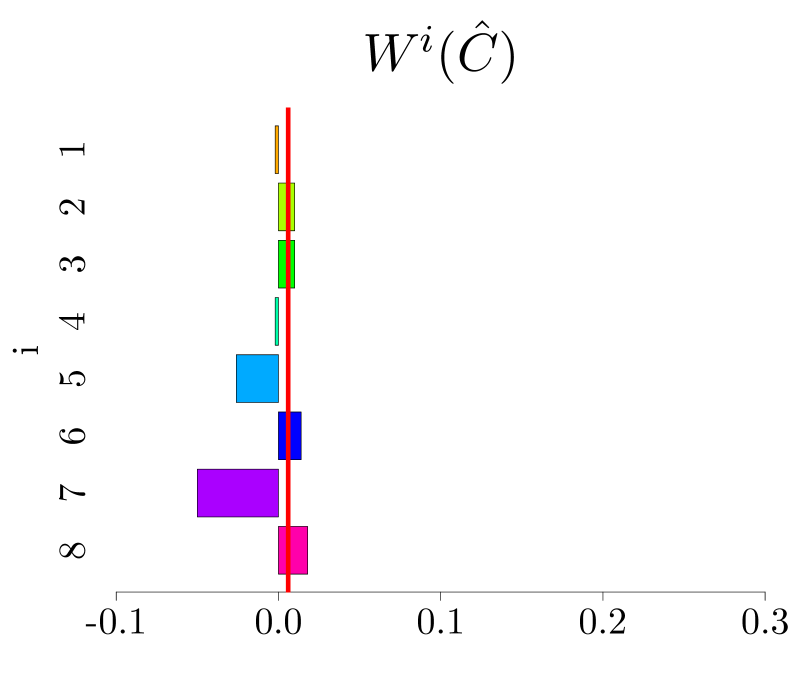

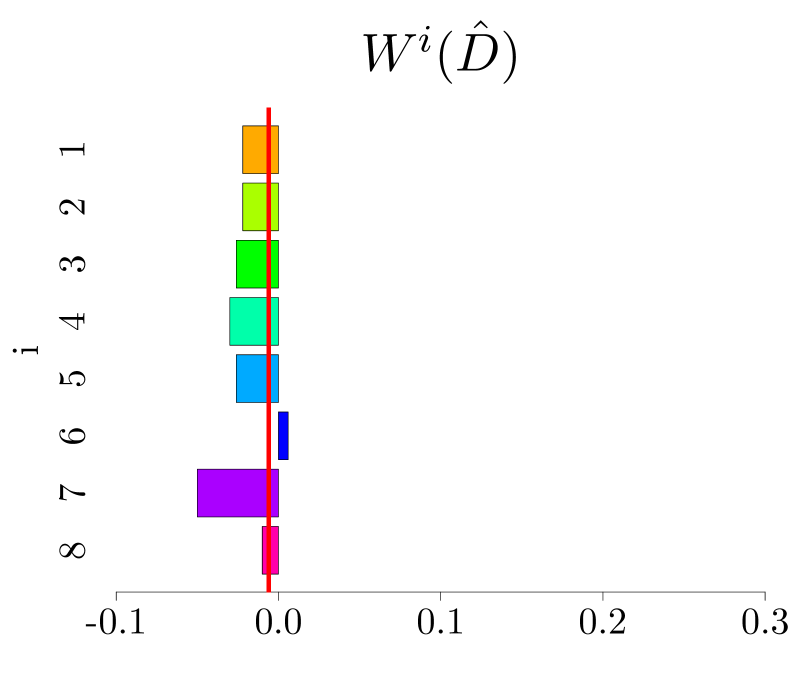

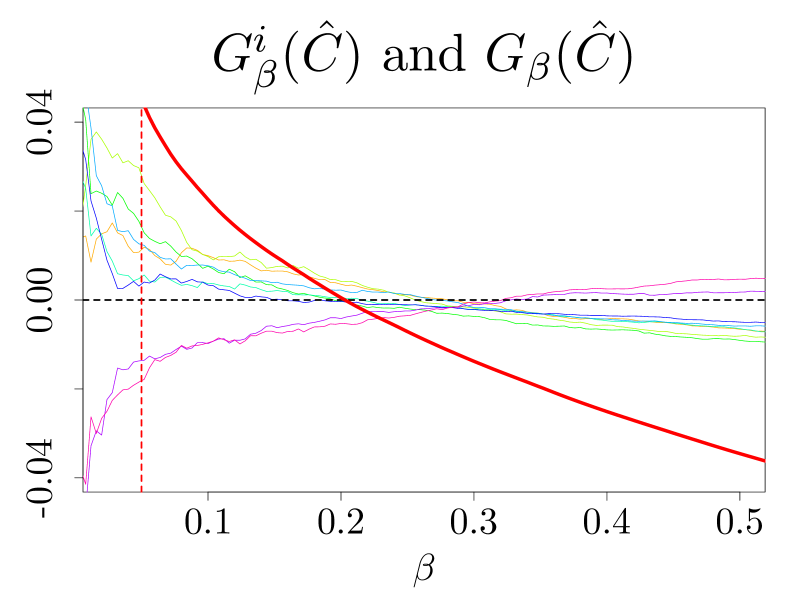

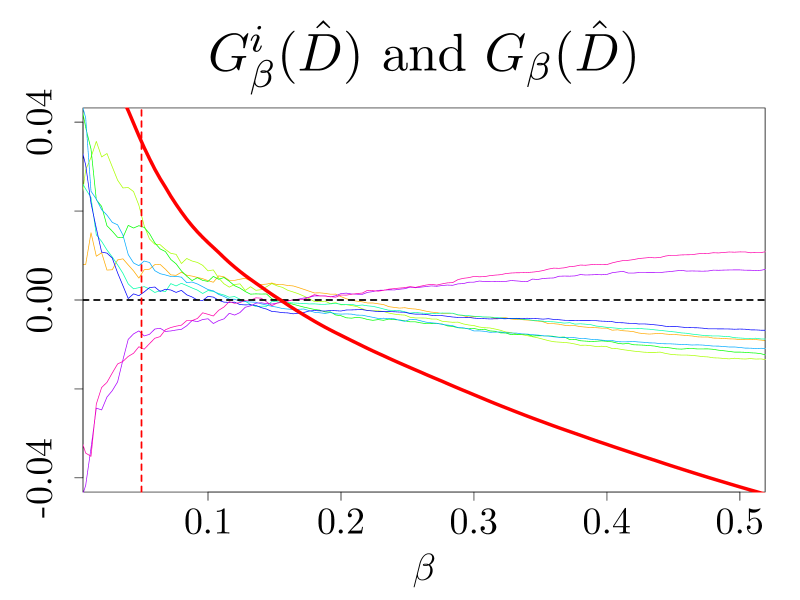

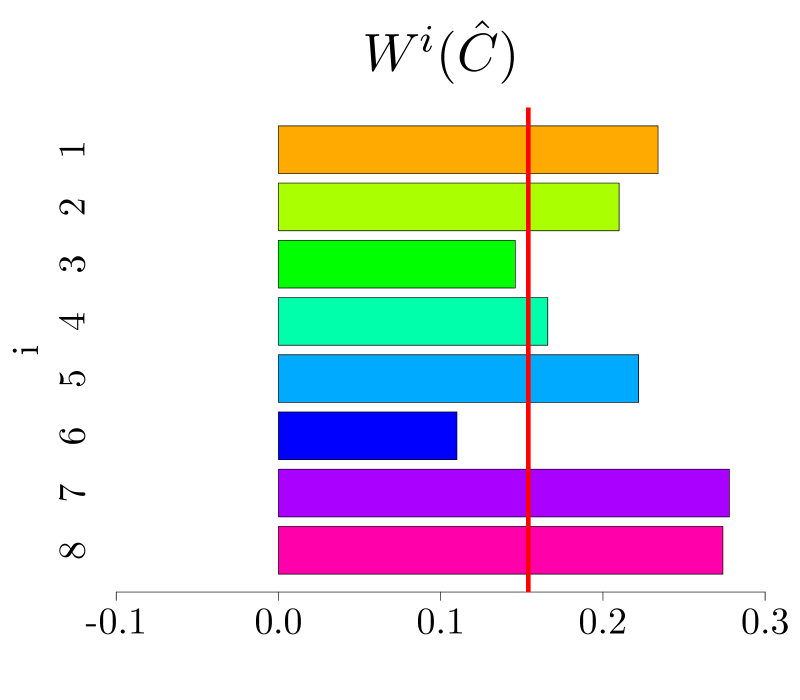

For convenience, we additionally present several graphical representations of the backtesting metrics. In Figure 3 we plot and as functions of , for the three risk allocation methods . All these functions should take zero value around , which is clearly the case. Finally, Figure 4 is dedicated to risk level shift backtesting. The top row shows the values of for risk allocations estimated using , and . The blue dots in the bottom graphs in Figure 4 depict the values of , all of them being close to the reference risk value , which again indicates adequacy of risk allocation estimation procedure .

| 0.00209 | 0.00363 | 0.00152 | 0.00127 | 0.00093 | 0.00088 | -0.00084 | -0.00076 | 0.00872 | ||

| 0.016 | 0.025 | 0.013 | 0.012 | 0.012 | 0.021 | 0.014 | 0.012 | 0.069 | ||

| 0.00074 | 0.00062 | -0.00030 | 0.00028 | 0.00049 | 0.00014 | 0.00001 | 0.00013 | 0.00212 | ||

| 0.004 | 0.003 | -0.001 | 0.008 | 0.007 | 0.001 | 0.000 | -0.001 | 0.054 |

Example 5.2 (Student -distributed P&Ls).

Similar to the previous example we consider a portfolio of eight constituents and with discounted P&L following a -distribution with five degrees of freedom. For comparison reasons, the distribution of is modified so that it has the same mean and variance covariance structure as in Example 5.1.

First, note that there is no available counterpart of for this setup. Second, as we will show below, since does not follow a Gaussian distribution, one should not use to estimate the risk allocation, and only is an appropriate methodology in estimating risk allocation. In Figure 5, we present the estimated risk allocations computed using and , over the entire backtesting period . It is apparent that the estimated risk allocation by these two methods are quite different. Table 2 contains the values of the estimated backtesting metrics, and for the reader’s convenience and are represented graphically in Figure 6. The values of are of one order of magnitude further away from zero than , indicating that indeed risk allocation methodology is more adequate for this experiment. We also note that magnitude of in this example aligns with the benchmark values from Example 5.1. Similar arguments hold true for and .

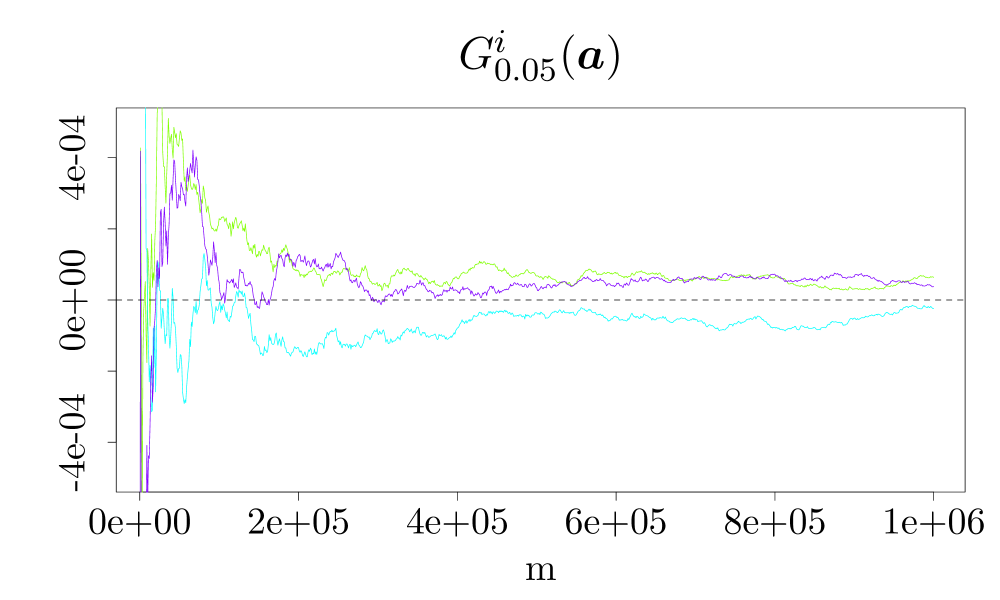

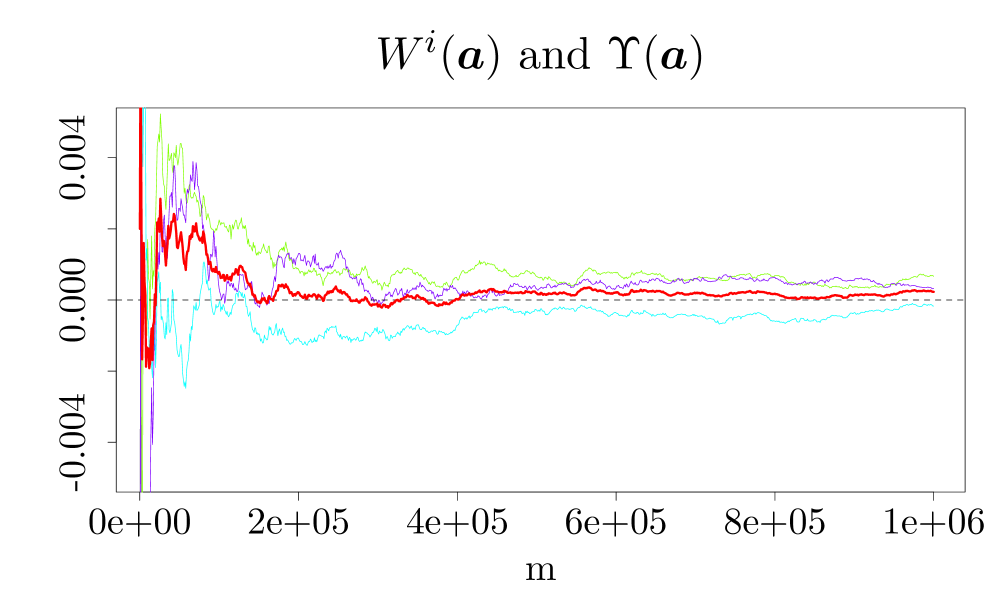

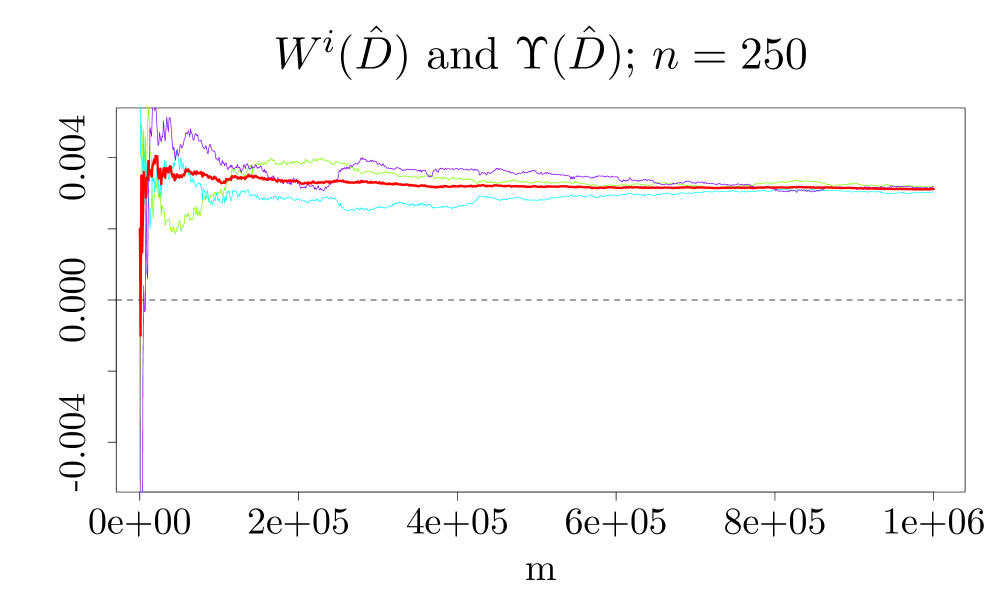

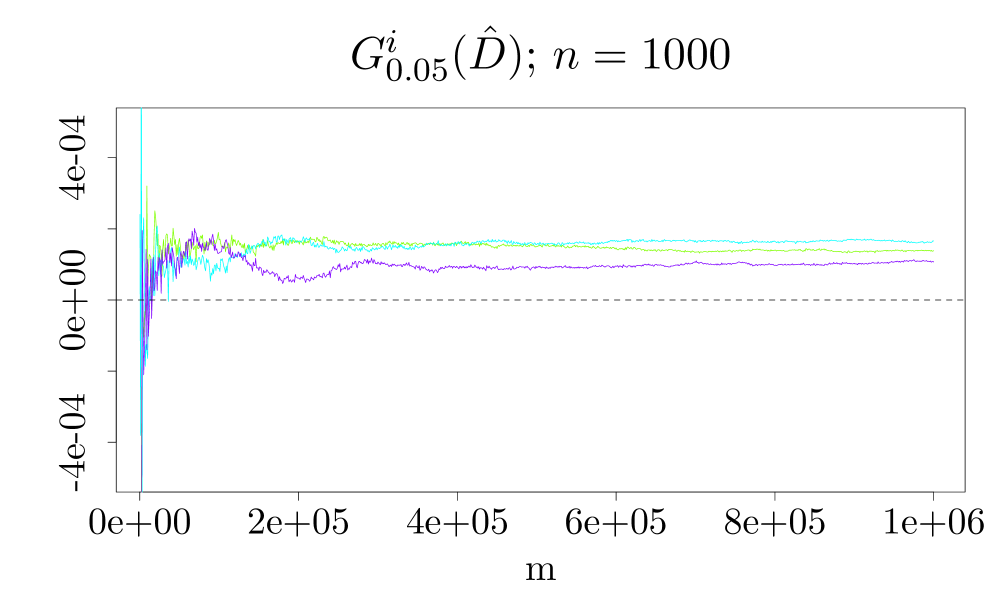

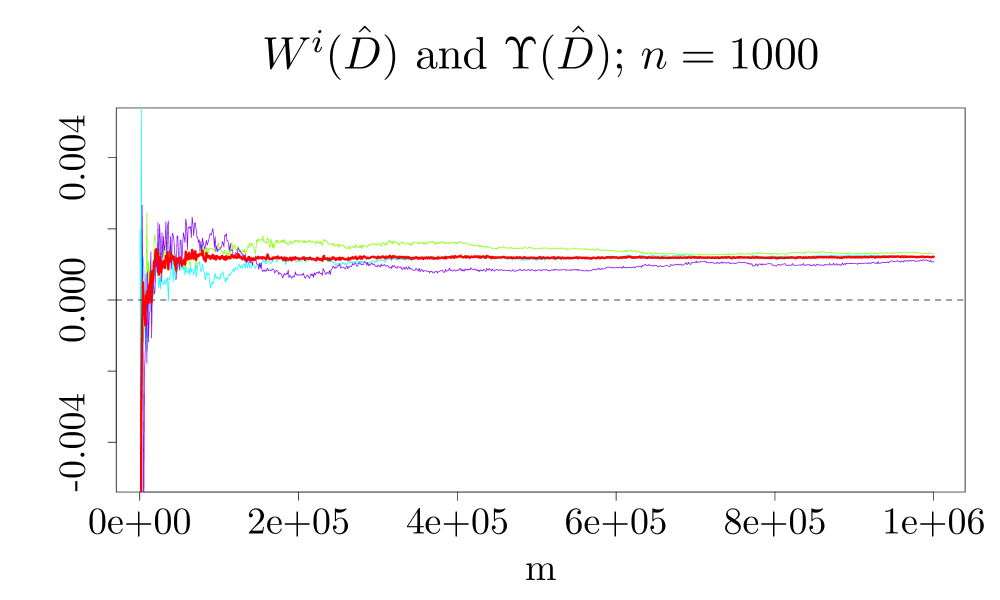

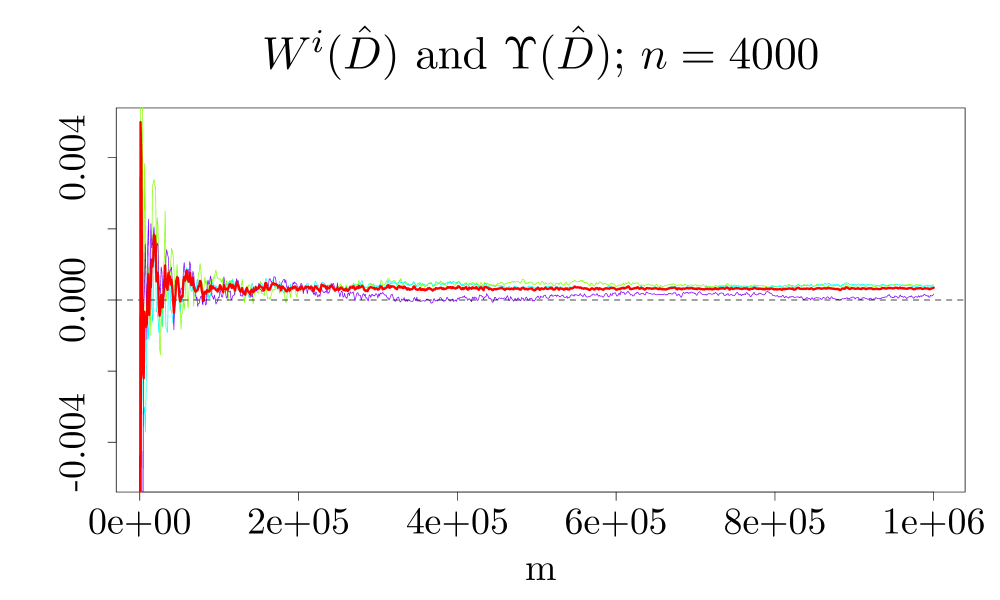

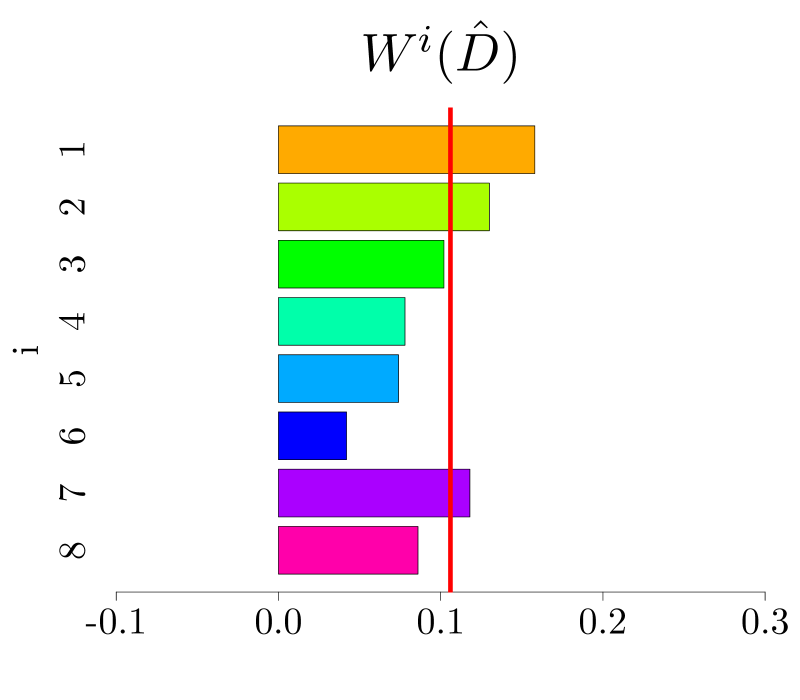

Example 5.3 (Fairness and asymptotic fairness).

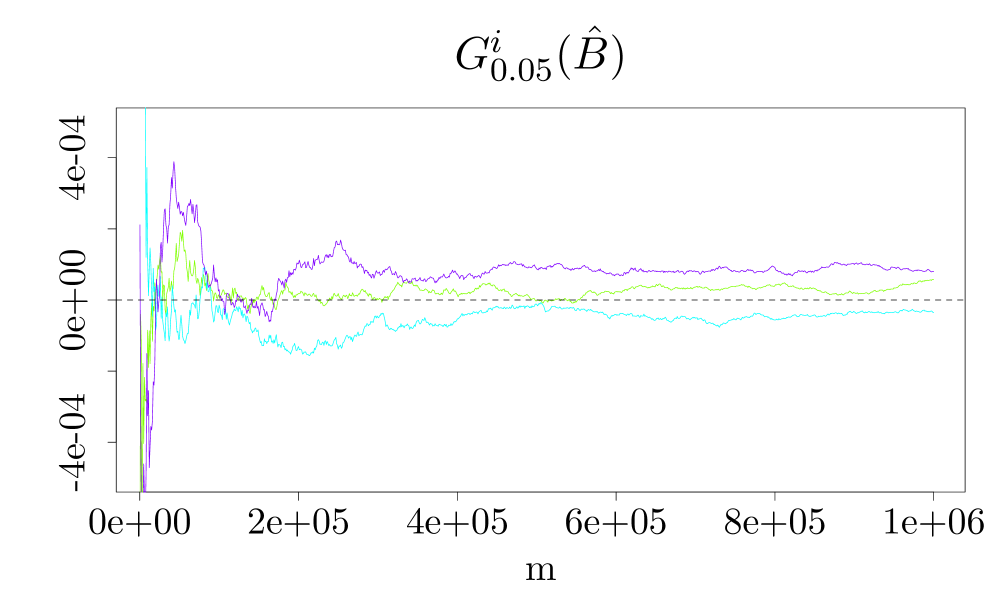

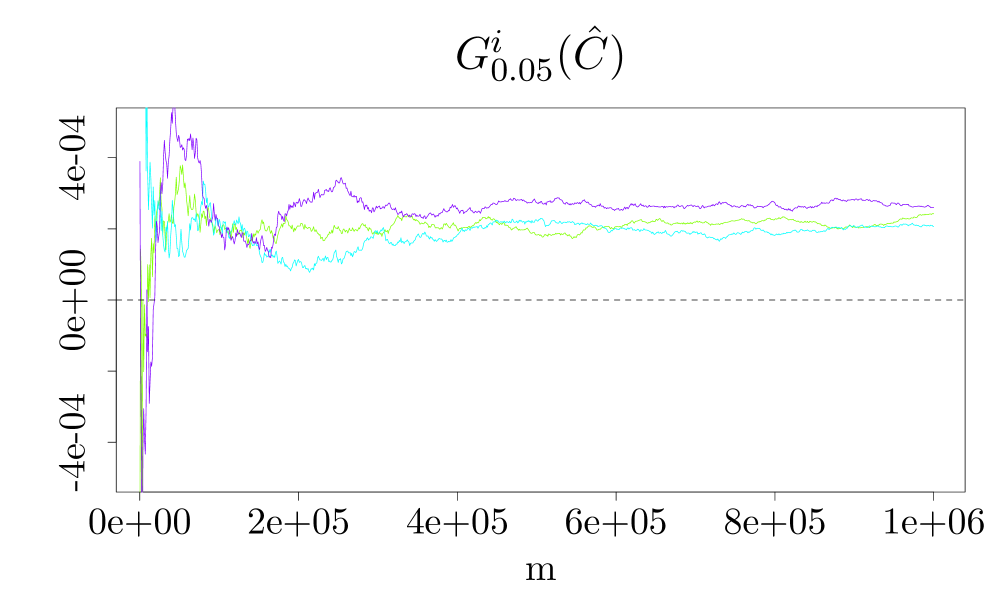

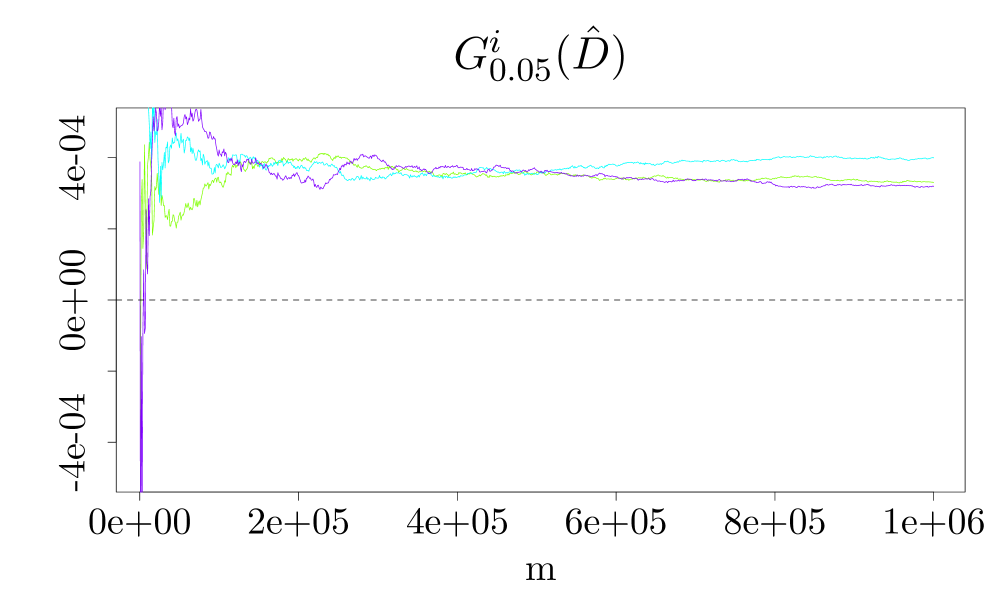

In this example we illustrate the fairness and the asymptotic fairness properties. Again, for the sake of a reference statistic which eases the presentation, we work under the normality assumption. Moreover, we consider only the first three constituents from Example 5.1, that is , because the other constituents show similar behavior. The numerical results presented below confirm that allocations and are fair. In addition, these results confirm that the allocations and are asymptotically fair even though they are not fair in this example.

Figure 7 deals with the issue of a short learning period, that is a small sample size, of . We see that for allocations and the ’s and ’s are getting close to zero with increasing , and that gets close to with increasing , confirming that these are fair allocations. We also see that ’s and ’s stay away from zero, and stays away from with increasing for allocations and , indicating that these are not fair allocations.

Figure 8 illustrates the asymptotic fairness of with . The left panel shows that get closer to zero for large with increasing . Similarly for the right panel, with regard to and .

Example 5.4 (Market data example).

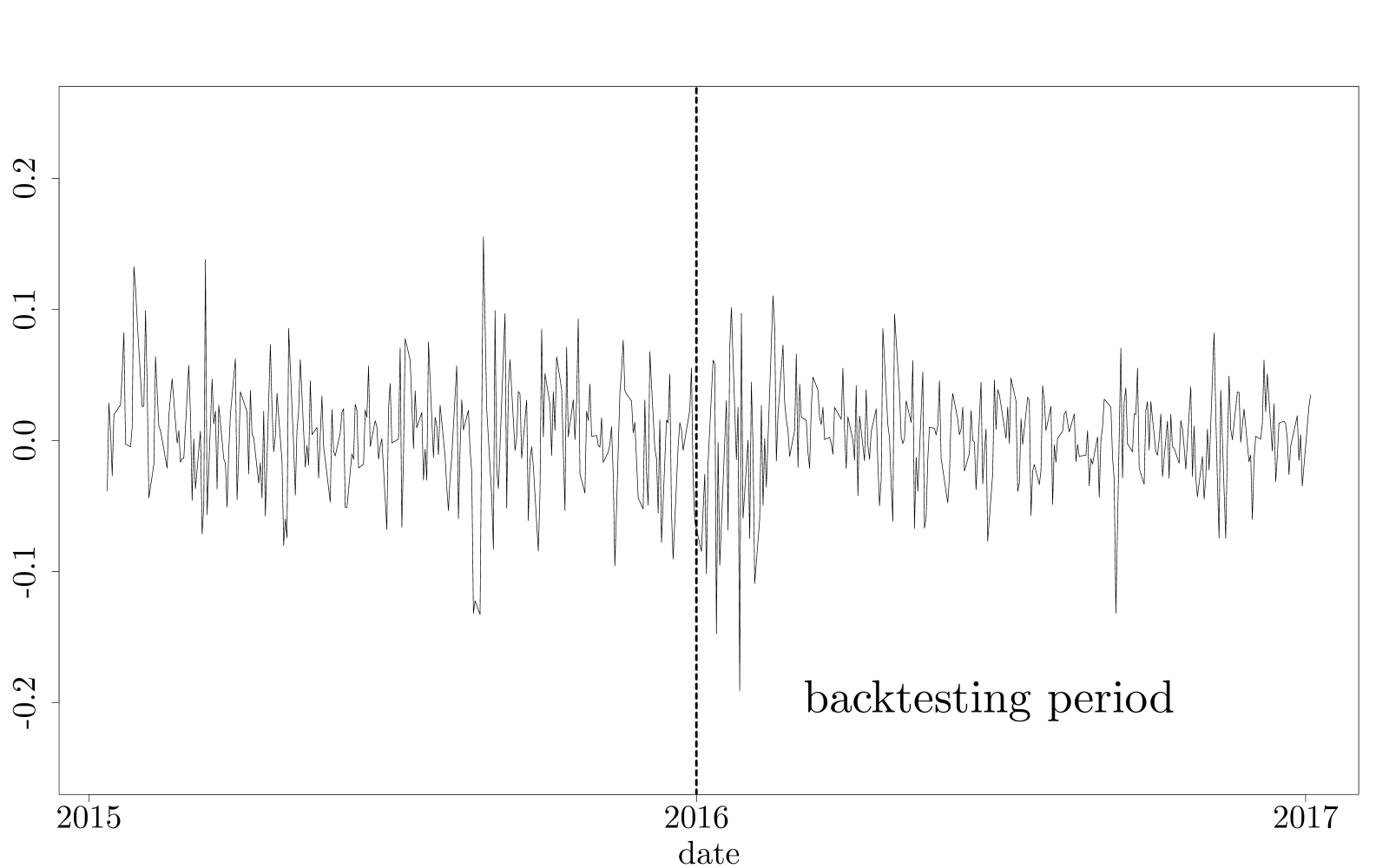

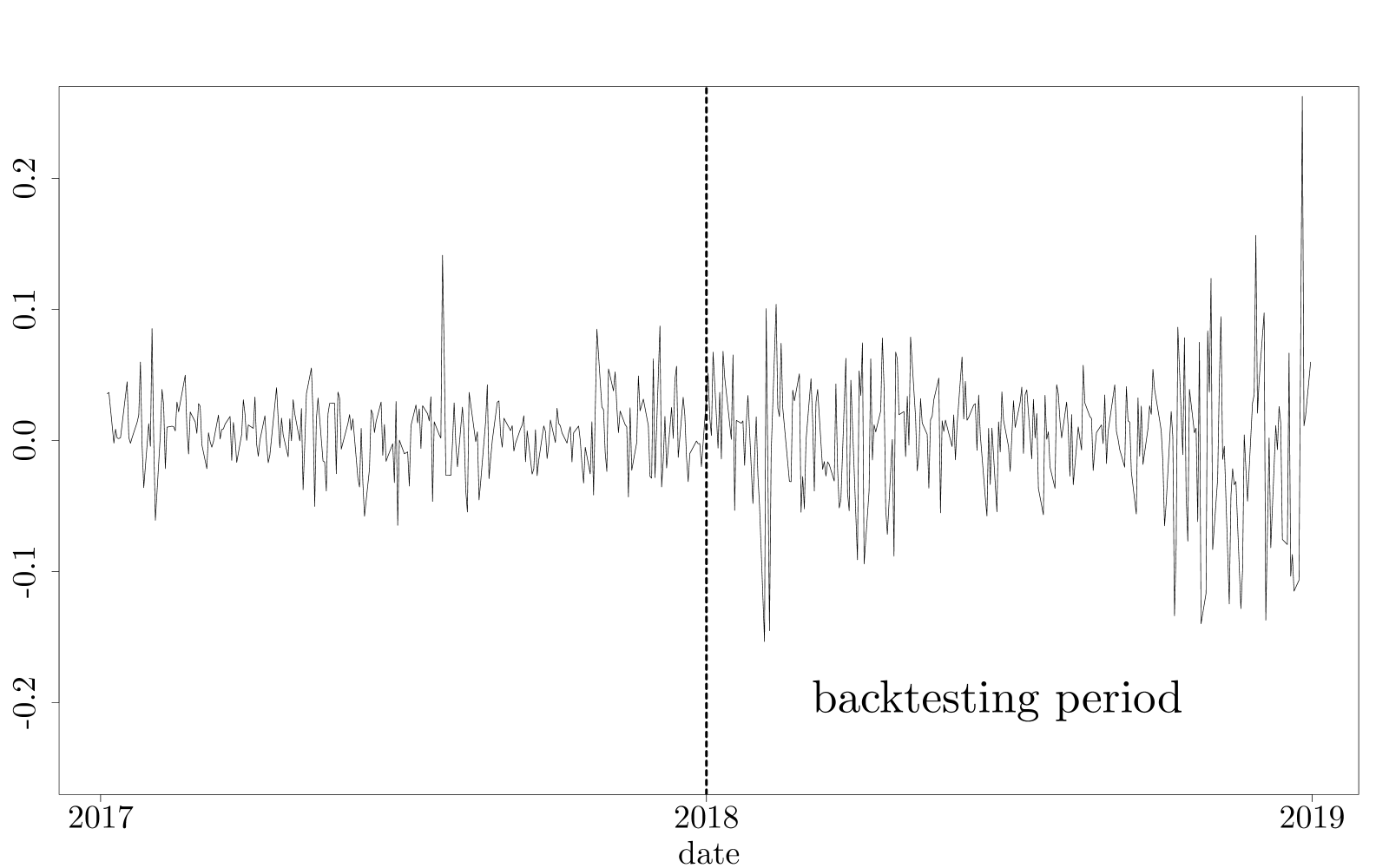

In this example we analyze the performance of the backtesting methodologies on market data. We consider the same portfolio formation as in Example 5.1, by taking eight stocks (AAPL, AMZN, BA, DIS, HD, KO, JPM, and MSFT) from the S&P 500 index, and form an equally weighted long-short portfolio. Namely, we hold a long position in the first six stocks, and a short position in the last two stocks, with nominal (absolute) value $1 in each stock. For this study, we use the daily stock returns, for the period January 2015 - December 2018. Throughout we set both, learning period () and backtesting period (), equal to 250 days. We split the dataset into two subsets: January 2015 - December 2016 (Dataset 1), and January 2017 - December 2018 (Dataset 2). As before, for each dataset, we use the standard 1-day rolling window and compare forecasted capital allocations with realized portfolio values.

One reason to split the data into these two time frames stems from the distinctively different patterns of the the aggregated P&L of the portfolio; see Figure 9. Dataset 1 is more homogeneous, with slightly larger volatility in the first half. Specifically, the sample standard deviation of the aggregated P&L portfolio for Dataset 1 is equal to 0.0425; the sample standard deviation for the first half is 0.0456, and for the second half is 0.0392. Dataset 2 exhibits a higher volatility in the second half compared to its first half and compared to Dataset 1; the standard deviation for the first half is 0.0267, and for the second half is 0.0522. As we will show later, these differences will propagate into the capital risk allocation and they will be picked up by the backtesting procedure. Similar to the previous examples, for both datasets we will use the risk allocation estimators and , and we will use both backtesting procedures proposed in Section 5. We also performed the Jarque-Bera normality test for the aggregated portfolio P&Ls for both datasets, which was rejected at significance level 0.01.

In the following, we will analyze each dataset separately. A first overview is presented in Figure 10, where the first two columns (left panel) correspond to Dataset 1, and the rightmost two columns (right panel) to Dataset 2.

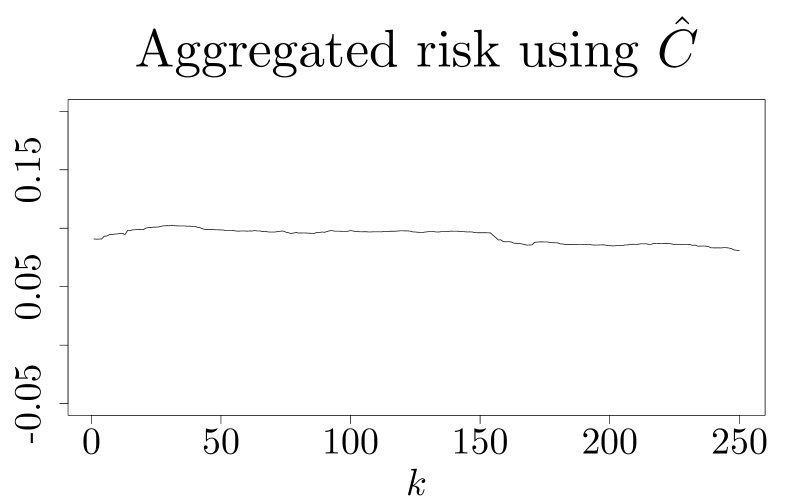

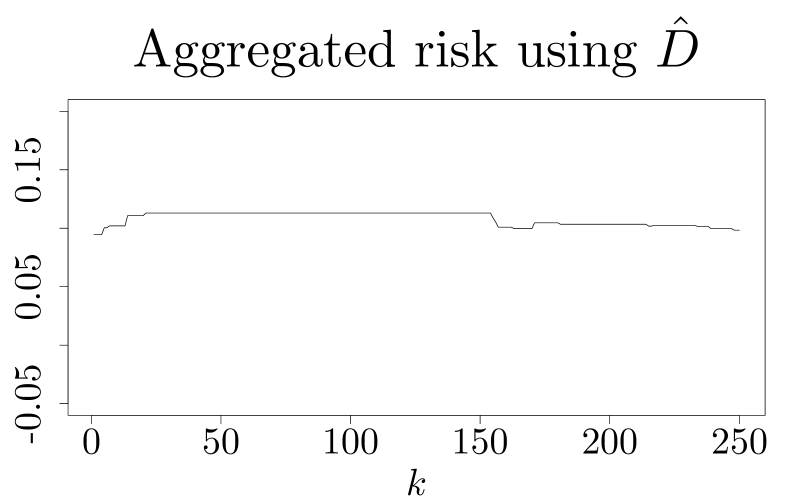

Dataset 1, January 2015 - December 2016, Figure 10, left panel, and Table 3. The aggregated (total) risk of the portfolio is displayed in the first row of Figure 10, which was computed by using estimators and . The aggregated portfolio risk seems to be well estimated by both and . The noticeable slight decrease in time of the aggregated risk is partially due to the lower volatility of the returns in the second part of the Dataset 1. The estimated risk capital allocations are presented in the second row, and the backtesting statistics , and are graphically displayed in rows 3-5 of Figure 10 and the numerical values are presented in Table 3.

| Dataset 1 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| -0.00107 | 0.00221 | 0.00110 | -0.00036 | -0.00052 | 0.00255 | 0.00653 | -0.00797 | 0.00247 | ||

| -0.002 | 0.010 | 0.010 | -0.002 | -0.026 | 0.014 | -0.050 | 0.018 | 0.056 | ||

| -0.00653 | -0.00855 | -0.00692 | -0.00525 | -0.00419 | 0.00102 | 0.01707 | 0.00339 | -0.00996 | ||

| -0.022 | -0.022 | -0.026 | -0.030 | -0.026 | 0.006 | -0.050 | -0.010 | 0.044 |

Overall, the capital allocations are well estimated by both999We note that while data is not normally distributed, the estimator performed similarly well as the nonparametric estimator . and , with exception of the seventh constituent, for which and . To see whether this is a problem with the estimator or a result of time-correlation structure change we checked the sample correlations between each constituent and the portfolio for two disjoint subsets. The results are presented in Table 4. One could see that for the correlation difference is noticeably higher than for the rest which might be a result of a structural change. Consequently, we believe that the proposed backtesting procedures correctly identified a wrong allocation in this particular case.

| 01/2015 – 12/2015 | 0.70 | 0.66 | 0.75 | 0.66 | 0.68 | 0.58 | -0.54 | -0.38 |

| 01/2016 – 12/2016 | 0.59 | 0.65 | 0.56 | 0.6 | 0.59 | 0.52 | -0.18 | -0.33 |

| Difference | 0.11 | 0.01 | 0.18 | 0.06 | 0.09 | 0.06 | -0.36 | -0.04 |

Dataset 2, January 2017 - December 2018, Figure 10, right panel, and Table 5. Due to the increase of the volatility in the second half of the Dataset 2, the aggregated portfolio risk increases throughout the backtesting period; see Figure 10, first row. In the second row of the same figure we present the nominal value of the allocated risk among constituents computed by using risk allocation estimators and . In contrast to Dataset 1, the backtesting results for Dataset 2 reveal a significant underestimation of the aggregated risk. This can be seen by noticing that the values of and , for both and , are far from zero; see last column in Table 5, or the third and fourth rows of Figure 10, right panel. The graph of function is plotted in the third row of Figure 10, solid red line, and the value of corresponds to the red vertical line in the last row. Comparing these plots with the corresponding plots from previous examples and datasets, we also conclude that the aggregated risk is significantly underestimated. Inevitably, this error propagates to the risk allocation estimation, as shown in the plots from rows 3-5. Clearly, the values of and are significantly different from zero (see also Table 5), in comparison to those from Dataset 1 and the previous examples. On the other hand, arguably, the risk allocation using the nonparametric estimators performs better than that one using ; see for instance the values of and versus and . Finally, we note that, for the estimator , the zeros of functions are essentially the same as the zero of the function , indicating that the risk allocation itself (as proportion of the total risk) is done properly, and failure of the backtesting procedure is due to underestimation of the total risk.

| Dataset 2 | ||||||||||

| 0.01187 | 0.02618 | 0.01512 | 0.00562 | 0.01229 | 0.00404 | -0.01356 | -0.01785 | 0.0437 | ||

| 0.234 | 0.210 | 0.146 | 0.166 | 0.222 | 0.110 | 0.278 | 0.274 | 0.204 | ||

| 0.00680 | 0.01669 | 0.01633 | 0.00301 | 0.00876 | 0.00181 | -0.00809 | -0.01106 | 0.03425 | ||

| 0.158 | 0.130 | 0.102 | 0.078 | 0.074 | 0.042 | 0.118 | 0.086 | 0.156 |

Dataset 1

Dataset 2

Acknowledgments

Tomasz R. Bielecki and Igor Cialenco acknowledge support from the National Science Foundation grant DMS-1907568. Marcin Pitera acknowledges support from the National Science Centre, Poland, via project 2016/23/B/ST1/00479. The authors would also like to thank the anonymous referees, the associate editor and the editor for their helpful comments and suggestions which improved greatly the final manuscript.

References

- [ADEH99] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath. Coherent measures of risk. Math. Finance, 9(3):203–228, 1999.

- [AS14] C. Acerbi and B. Székely. Back-testing expected shortfall. Risk magazine, (November), 2014.

- [BCF18] T. R Bielecki, I. Cialenco, and S. Feng. A dynamic model of Central Counterparty Risk. International Journal of Theoretical and Applied Finance, 21(8):1850050, 2018.

- [Büh70] H. Bühlmann. Mathematical methods in risk theory. Springer, Berlin, 1970.

- [Che06] A. Cherny. Weighted VaR and its properties. Finance Stoch., 10(3):367–393, 2006.

- [CD19] D. Coculescu and F. Delbaen, Surplus Sharing with Coherent Utility Functions. Risks, 7, 7, 2019.

- [Del00] F. Delbaen. Coherent risk measures. Scuola Normale Superiore, 2000.

- [FS11] H. Föllmer and A. Schied. Stochastic finance: an introduction in discrete time. Walter de Gruyter, 3rd edition, 2011.

- [Ger74] H. U. Gerber. On additive premium calculation principles. ASTIN Bulletin: The Journal of the IAA, 7(3):215–222, 1974.

- [Gui16] Gene D Guill. Bankers trust and the birth of modern risk management. Journal of applied corporate finance, 28(1):19–29, 2016.

- [Kal05] M. Kalkbrener. An axiomatic approach to capital allocation. Mathematical Finance, 15(3):425–437, 2005.

- [Kup95] P. H. Kupiec. Techniques for verifying the accuracy of risk measurement models. The Journal of Derivatives, 3(2):73–84, 1995.

- [Kus01] S. Kusuoka. On law invariant coherent risk measures. In Advances in mathematical economics, Vol. 3, volume 3 of Adv. Math. Econ., pages 83–95. Springer, 2001.

- [MFE15] A.J. McNeil, R. Frey, and P. Embrechts. Quantitative risk management: concepts, techniques, and tools. Princeton university press, first revised edition, 2015.

- [NZ17] N. Nolde and J. F. Ziegel. Elicitability and backtesting: Perspectives for banking regulation. The Annals of Applied Statistics, 11(4):1833–1874, 2017.

- [PM18] M. Pitera and F. Moldenhauer. Backtesting Expected Shortfall: a simple recipe? Journal of Risk, 22(1):17–42, 2019.

- [PS18] M. Pitera and T. Schmidt. Unbiased estimation of risk. Journal of Banking & Finance, 91:133–145, 2018.

- [Sha13] A. Shapiro. On Kusuoka representation of law invariant risk measures. Mathematics of Operations Research, 38(1):142–152, 2013.

- [SKG15] P. Schmidt, M. Katzfuss, and T. Gneiting. Interpretation of point forecasts with unkown directive Preprint, 2015.

- [Sti97] S. M. Stigler. The Asymptotic Distribution of the Trimmed Mean The Annals of Statistics, 1(3):472–477, 1973.

- [Tas04] D. Tasche. Allocating portfolio economic capital to sub-portfolios. Economic capital: a practitioner guide, pages 275–302, 2004.

- [Tas07] D. Tasche. Euler allocation: Theory and practice. Preprint, 2007.

- [Tsa09] A. Tsanakas. To split or not to split: Capital allocation with convex risk measures. Insurance: Mathematics and Economics, 44(2):268–277, 2009.

- [Zie16] J. F. Ziegel. Coherence and elicitability. Mathematical Finance, 26:901 – 918, 2016.