The ineffectiveness of coherent risk measures

Abstract

We show that coherent risk measures are ineffective in curbing the behaviour of investors with limited liability or excessive tail-risk seeking behaviour if the market admits statistical arbitrage opportunities which we term -arbitrage for a risk measure . We show how to determine analytically whether such -arbitrage portfolios exist in complete markets and in the Markowitz model. We also consider realistic numerical examples of incomplete markets and determine whether expected shortfall constraints are ineffective in these markets. We find that the answer depends heavily upon the probability model selected by the risk manager but that it is certainly possible for expected shortfall constraints to be ineffective in realistic markets. Since value at risk constraints are weaker than expected shortfall constraints, our results can be applied to value at risk. By contrast, we show that reasonable expected utility constraints are effective in any arbitrage-free market.

Keywords: ineffective risk measures, -arbitrage, limited liability, tail-risk seeking behaviour, coherent risk measures, positive homogeneity, s-shaped utility, classic utility risk limit, Markowitz model, incomplete markets.

Introduction

In Armstrong and Brigo, (2019) it was shown that neither value-at-risk constraints nor expected-shortfall constraints are sufficient to curb the behaviour of a risk-seeking trader or risk-seeking institution in typical complete markets.

In that paper a risk-seeking trader was modelled as an investor who wishes to optimize an S-shaped utility curve. This is an increasing utility curve that is convex on the left and concave on the right. An investor with such a utility curve is conventionally risk-averse in profitable situations, but risk-seeking in loss-making situations. This idea is motivated by the theory of Kahneman and Tversky, (1979) who observed such behaviour empirically. It can also be justified theoretically by observing that traders have limited liability as they can lose no more than their job and their reputation. Similarly shareholders in banks have limited liability.

Armstrong and Brigo, (2019) shows that subject to mild technical assumptions, in complete markets, including the case of the Black-Scholes model, a trader with S-shaped utility operating under cost and expected shortfall constraints can achieve any desired expected utility, bounded only by the supremum of their utility function. Moreover it is shown that the trader will take a position with infinitely bad utility if that utility were to be measured with a conventional concave utility function. We will refer to such a utility function as the risk-manager’s utility function. This suggests that, in this context, expected conventional utility could be a more effective risk measure for the risk manager than expected shortfall and VaR.

The most significant assumption of Armstrong and Brigo, (2019) is that the market is complete. This paper seeks to ask how the results change if one studies incomplete markets or other coherent risk measures (as introduced by Artzner et al., (1999)).

We begin by identifying why expected shortfall is ineffective in Section 1. We give a formal definition of what we mean for a risk measure to be ineffective in terms of whether it successfully reduces the utility that can be achieved by the “worst-case” trader, namely a risk-neutral trader with limited liability. We show that coherent risk measures, , are ineffective if and only if the market contains a specific type of portfolio associated with which we call a -arbitrage portfolio. These are portfolios which give a potentially positive return for a non-positive price without incurring a positive risk as measured using . We will see that if the market admits a -arbitrage, then the risk constraint will be ineffective against traders with a broad range of S-shaped utility functions, not just the worst-case example. Our results in this section apply to rather general markets, our key assumption is that the market is positive-homogeneous, implying that unlimited quantities of assets can be purchased at a given price. Our analysis shows that the key fault of expected shortfall is that it is a coherent risk measure, in particular it is positive-homogeneous. We conclude that if one wants to use risk-measures that are effective one should consider convex measures, as introduced by Föllmer and Schied, (2002).

After Section 1 the paper focuses on expected shortfall. We will write for the expected shortfall at confidence level . Our theory tells us that to determine if is effective we must look for -arbitarge portfolios.

In Section 2 we show how this characterization of ineffectiveness allows us to compute analytically whether or not expected shortfall is effective at a given confidence level in certain simple markets. We first consider the case of a market in assets which follow a multi-variate normal distribution, as considered by Markowitz, (1952). We next consider the case of complete markets. Our results show that arbitrage is unlikely in the Markowitz model for low values of but inevitable for all in the Black–Scholes model.

In Section 3 we show how our characterization of ineffectiveness can be used in practice for realistic markets. Using the techniques of Rockafellar et al., (2000), we are able to give a practical numerical method for determining if is effective. We demonstrate this technique in practice by considering the market of European options with a fixed maturity on the S&P 500. We find that the values for which is effective depend heavily upon the probability model chosen. We find that for some ostensibly reasonable fat-tailed probability models calibrated to market data, is ineffective for even very low values of . In particular we found this for a model calibrated to historic data and a mixture model calibrated to option prices. Thus the ineffectiveness of constraints found in Armstrong and Brigo, (2019) cannot be put down simply to the use of an idealised market model.

The paper ends with an appendix which collects together the proofs.

We finally note that we are not the only authors to have identified that positive-homogeneity as a problematic property for a risk-measure. Herdegen and Khan, (2020) have independently reached a similar conclusion by studying a concept which they term regulatory arbitrage, which is closely related to -arbitrage. They define regulatory arbitrage as occuring when the problem of maximising expected return subject to constraints becomes ill-posed. The possibility of such ill-posed problems was first noticed by Alexander and Baptista, (2002) in the case of VaR. See Herdegen and Khan, (2020) for a review of the subsequent literature. While the existing literature focuses on the problem of maximising an expected return, and hence on the behaviour of risk-neutral agents, we consider the further dangers posed by agents which are tail-risk-seeking. In addition we study the effectiveness of expected utility constraints against such agents, thereby demonstrating that the strategies taken by tail-risk-seekers under positively homogeneous constraints will yield arbitrarily low utilities for the risk-manager, who would find such trades unacceptable.

1 Ineffective constraints and -arbitrage

We will begin by giving general definitions of a financial market. We wish to give definitions that are broad enough to include incomplete markets where there may be a bid-ask spread or even an order book. Our treatment is based on that of Pennanen, (2011, 2012).

A market consists of a probability space and a function

Each random variable represents the payoff of an asset and computes the price of an asset. Assets with price cannot be purchased. Because we have included in the range of , we can safely assume that is defined on the whole of and not just some subset. (Mathematically one can extend the definition to allow markets where may take the value on liabilities so bad that the market is willing to pay arbitrarily large sums to anyone willing to take on this liability. However, in this paper we restrict our attention to markets without such liabilities.)

Definition 1.1.

A market is positive-homogeneous if for . A market is coherent if it is positive-homogeneous and

| (1) |

| (2) |

Note that by requiring only positive-homogeneity, one allows for a bid-ask spread. Assuming that a market is positive-homogeneous is an idealisation; for example it implies that there are no quantity constraints or price impact. However, once one has assumed positive-homogeneity, the assumption of sub-additivity (1) is rather innocuous as one should be able to replicate the payoff by purchasing the assets and separately once one assumes there are no quantity constraints. Assuming positive-homogeneity, equation (2) is the assumption that there is a risk-free asset.

We use the term coherent simply by analogy with so-called coherent risk-measures. We do not wish to imply that there is anything logically incoherent about markets which are not coherent, the word is merely intended to convey the uniformity arising from positive-homogeneity.

A trading constraint is a subset of the set of random variables representing the assets that a trader is allowed to purchase.

Let . This can be thought of as the utility function of an risk-neutral investor with limited liability.

Definition 1.2 (Ineffective Constraint).

A trading constraint is ineffective if for any cost

Note that we include negative costs in this definition. So under ineffective constraints even heavily indebted traders with utility would be able to achieve arbitrarily large utilities from their investments while at the same time clearing their debts.

Since any conventional utility function or any of the S-Shaped utility functions studied by Kahneman and Tversky can be bounded above by some affine transformation of , the utility function represents a worst-case scenario for the risk manager. Thus a trading-constraint is ineffective if it is possible for a trader’s expected utility to be unperturbed by the constraint in this worst case scenario, but the constraint may still have an effect on less aggressively risk-seeking traders.

Definition 1.3 (-arbitrage).

If is a function on the space of random variables, then a random variable is called a -arbitrage if , and has a positive probability of taking a positive value.

We will define a true arbitrage to be a random variable which has a positive probability of being positive, is almost surely non-negative and has a non-positive price. Although many authors prefer to insist that an arbitrage has a price of zero, allowing negative prices is more natural from the point of view of convex analysis. If assigns the value to any random variable which takes negative values with positive probability, then a true arbitrage is equivalent to a -arbitrage. This justifies the name -arbitrage (we remark that a variance-arbitrage or a standard-deviation-arbitrage will also be a true arbitrage).

Functions on that are intended to measure risk have been studied extensively, notably by Artzner et al., (1999). They gave a set of axioms that must obey for it to be called a coherent risk-measure. We adapt their definition slightly to match our conventions for the domain and range of .

Definition 1.4.

A coherent risk measure with satisfies

-

(i)

Normalization:

-

(ii)

Montonicity: if almost surely.

-

(iii)

Sub-additivity: .

-

(iv)

Translation invariance: for .

-

(v)

Positive homogeneity: for .

We may now state our main theoretical results which connect the effectiveness of a risk-measure to the existence of -arbitrage. Note that the axiom of positive homogeneity plays a crucial role in their proofs, which can be found in Appendix A.

Theorem 1.5.

(Arbitrarily good trader utilities can be otbained if there is a -arbitrage). Let be a coherent risk-measure. If a coherent market contains a -arbitrage then for any random variable of finite expectation

| (3) | ||||

| (4) | ||||

| (5) |

If in addition , then for utility functions of the form

| (6) |

where , and we have

| (7) |

Theorem 1.6.

(Equivalence between existence of -arbitrage and ineffectiveness). In a market containing a -arbitrage, the constraint

is ineffective for all . Conversely if is ineffective then the market admits a -arbitrage.

The first result shows that a -arbitrage can be exploited by a trader to obtain arbitrarily good utilities . The second gives a characterisation of effectiveness in terms of -arbitrage. Our next result shows how the same portfolios perform when measured with typical conventional concave increasing utility functions , which might be thought of as the utility function of the risk-manager, the business overall or wider society.

Theorem 1.7.

(Arbitrarily good trader utilities are ruled out by a classic utility used as risk measure). Let be a coherent risk-measure. Let be any concave increasing utility function satisfying

| (8) |

If is a -arbitrage and not a true arbitrage, and if both and are finite for some then

| (9) |

Even very mildly risk-averse utility functions will satisfy (8) for example the function defined by

satisfies (8) for any . Thus for any such , -arbitrage opportunities give unbounded upward potential for the utility of a rogue investor and unbounded downward potential for the utility of a risk manager with utility .

In a similar vein, the next theorem shows that utility based risk constraints will typically be effective in finite-dimensional linear markets.

Definition 1.8.

A finite-dimensional linear market is a market where is a vector subspace of and where is a linear functional on .

Theorem 1.9.

(Classic utilities are ineffective as risk measures if and only if the market is arbitrageable in the classic sense). Let be a concave increasing utility function satisfying (8) and , then for a finite-dimensional linear market with , the set

is ineffective if and only if the market contains a true arbitrage.

Theorem 1.6 tells us that we can detect whether a given coherent risk measure leads to ineffective risk-constraints in a given coherent market by solving the convex optimization problem

Our assumptions on the coherence of the market and of ensure that constraints are indeed convex. The minimum achieved will be negative (indeed it will then equal ) if and only if is ineffective. Since this is a convex optimization problem it is relatively straightforward to solve in practice. We will use this method to find a number of markets which contain a -arbitrage in the later sections of this paper.

2 Analytic results

We will write for the coherent risk measure given by expected shortfall at confidence level (Acerbi and Tasche,, 2002). This is defined by

where value at risk at confidence level , , is defined in turn by

where is the cumulative distribution function of .

In this section we consider the question of when -arbitrage opportunities exist in some simple markets where we can find analytical results. We consider the contrasting cases of a highly incomplete and a complete market.

In section 2.1 we will consider the markets of normally distributed assets as considered by Markowitz, (1952), this is a highly incomplete market. In section 2.2 we will consider complete markets. We will find that in the highly incomplete market of normally distributed assets -arbitrage is unrealistic. Whereas in a typical complete market such as the Black-Scholes model -arbitrage should be expected for all .

2.1 Normally distributed assets

We suppose that we wish to invest in the market of the Markowitz model. We suppose there are assets , , …, whose payoffs follow a multivariate normal distribution with mean vector and covariance matrix . A portfolio represented by the vector consists of units of stock . The expected return of this portfolio is and the variance is . The cost of portfolio is assumed to be for some vector . So is given by:

We will suppose that, up to scale there is only one risk-free portfolio.

This defines a coherent market which we will call a Markowitz market with risk free asset.

Theorem 2.1.

Suppose . Let denote the expected shortfall of a standard normal random variable at confidence level . Then a Markowitz market with risk free asset admits a -arbitrage if and only either

or

where is the gradient of the capital allocation line and is the risk free return.

Proof.

A normally distributed asset with mean and standard deviation satisfies

So represents a -arbitrage portfolio if and only if

| (10) |

and

| (11) |

By the classification of Markowitz markets in Armstrong, (2018) we may assume without loss of generality that

where is the identity matrix of size and . So equations (11) and (10) become

| (12) |

and

respectively. If we can always solve (12) simply by choosing a sufficiently small value for . If then any solution to (12) must satisfy

and hence

The result now follows. ∎

So for an -arbitrage to exist in a Markowitz market with positive interest rates, one would require . This is an unrealistically steep capital allocation line for investments over a time period of a year or less.

2.2 -arbitrage portfolios in complete markets

We now consider the case of complete markets.

Theorem 2.2.

Let be a complete market given by an atomless probability space equipped with a measure equivalent to . We suppose that any can be purchased at the price

where is the time horizon of the investment and is the risk-free rate. This market admits an -arbitrage if and only if

Remark 2.3.

It already follows from the results of Armstrong and Brigo, (2019) that expected shortfall is ineffective for any confidence level in complete markets where the Radon-Nikodym derivative

is essentially unbounded. Thus the new result in Theorem 2.2 is the proof of the converse. As was shown in Armstrong and Brigo, (2019, 2018), in complete markets such as the Black–Scholes model with non-zero market price of risk, one should expect to be essentially unbounded and hence for expected shortfall to be ineffective at all confidence levels.

3 Numerical results

In this section we will see how one can detect whether exists in a realistic market numerically. In Section 3.1 we will outline a general approach to detecting arbitrage. In Section 3.2 we will apply this to the specific case of options on the S&P 500.

3.1 Detecting arbitrage numerically

Let us begin by introducing some notation. We will assume that there are available instruments that one can invest in at time . The price of instrument is and the payoff at time is the random variable . We write for the vector of the prices of each instrument, and for the random vector containing all the payoffs. The investor chooses a portfolio containing units of instrument . We write for the vector with components . To model a bid ask spread, we require that each and model shorting a security as purchasing positive quantities of an asset with a negative price.

To find -arbitrage portfolios, we seek portfolios of negative cost and negative expected shortfall. Thus we will consider the convex optimization problem:

| (13) | |||||||

| subject to | |||||||

| cost constraint | |||||||

| quantity constraints | |||||||

If the minimizing portfolio has strictly negative expected shortfall then it must be a -arbitrage portfolio. Note that we impose an upper bound constraint on each in order to ensure that the optimization problem always has a finite solution. Since one can always rescale an -arbitrage portfolio, this additional upper bound constraint is harmless.

To solve this convex optimization problem in practice, we may use the techniques of Rockafellar et al., (2000). Theorem 1 of that paper proves that

where we define

We next choose a quadrature rule for expectations with evaluation points and weights so that we can make the approximation

| (14) |

for suitably well-behaved random variables . We may then approximate the expected shortfall as

where

Following Rockafellar et al., (2000), if we introduce auxiliary variables to replace the terms we may approximate (13) with the linear programming problem:

| (15) | |||||||

| subject to | |||||||

| cost constraint | |||||||

| quantity constraints | |||||||

| auxiliary constraints | |||||||

The simplest choice of quadrature rule is Monte Carlo. We simply simulate sample points and give each sample point equal weight.

However, in the one dimensional case where the underlying is a single stock price , if we know how to compute the integrals

| (16) |

analytically, a better choice of quadrature rule can be obtained by first choosing integration points and then selecting the weights such that the quadrature rule is exact for payoff functions which are continuous and linear except at the points . If the points include all the strike prices of European puts and calls available in the market, then all possible portfolio payoffs for European option portfolios will be of this form.

As we have seen, once we have chosen our quadrature rule we can find out if a -arbitrage portfolio exists by solving the optimization problem (15). We can then use the method of bisection to find the lowest for which arbitrage portfolios exist.

3.2 -arbitrage opportunities on the S&P 500

We apply the theory of Section 3.1 to the market of European options on the S&P 500. We consider buy and hold strategies in exchange traded European options on this index. We only consider portfolios where all the options expire on the same maturity date and use this maturity date as the time horizon in our computation of expected shortfall.

For every day in the week commencing 10 Feb 2014, we obtained bid and ask prices for all the exchange traded options on the S&P 500 with maturity 22nd March 2014 (Bloomberg L.P.,, 2018). This data determines our pricing function for a portfolio of options.

We must then choose a probability model for the S&P 500 Index value on the maturity date. We may then view the option payoffs as random variables in this probability model, and this will describe the market in full. The idea of studying this market is taken from Armstrong et al., (2017).

The choice of probability model for the index value is subjective. We considered the following possibilities:

-

(i)

A model for the log returns, calibrated to the same historic return data. This was estimated using the MATLAB functions

garchandestimate. We then simulated returns to obtain a Monte Carlo quadrature rule for this model. -

(ii)

We calibrated a -measure probability model given by a mixture of two normal to fit the market volatility smile for the options and assumed this was also the -measure model. Mixture dynamical models have been used under the pricing measure for smile modelling, see for example Brigo and Mercurio, (2002); Alexander, (2004).

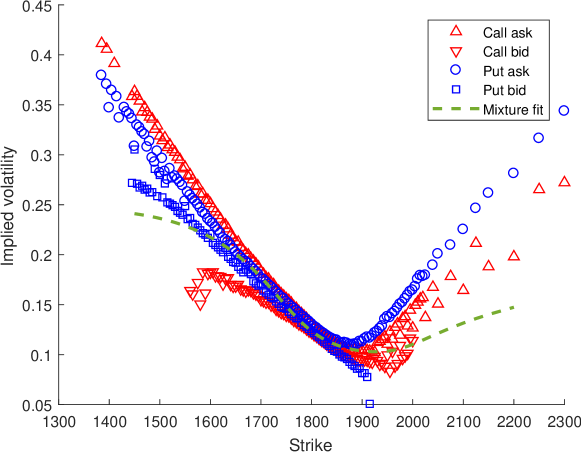

Mixture models have also been used under the measure P for portfolio allocation, see for example the work by Roncalli and co-authors Bruder et al., (2016); Lezmi et al., (2018), or for inclusion of liquidity risk in risk measures via random holding period, see Brigo and Nordio, (2015). Our choice of a mixture model as both and measure is not intended to be a realistic approach to choosing a -measure model, simply an attempt to find a statistical model that is close to market prices to discover whether -arbitrage persists even when the and measures are very close. The fit of the calibrated model to the market volatility smile is shown in figure 1. Because the integrals (16) can be computed analytically for this model we were able to test whether arbitrage exists without using Monte Carlo quadrature.

The results are shown in Table 1.

| Date | run 1 | run 2 | Mixture |

|---|---|---|---|

| 10 Feb | |||

| 11 Feb | |||

| 12 Feb | |||

| 13 Feb | |||

| 14 Feb |

Our results show that -arbitrage opportunities can exist in real markets for low values of and with reasonable choices of -measure model.

4 Conclusions

We have shown that the ineffectiveness of expected shortfall as a means of controlling the behaviour of tail-risk-seeking investors stems from its positive-homogeneity. Whether a positive-homogeneous risk constraint is effective or not depends upon whether or not the market contains a -arbitrage. This is undesirable as risk constraints are typically set without reference to market conditions.

In the idealisation of the Black-Scholes model, expected-shortfall arbitrage opportunities exist for any confidence level . We have shown how one can determine efficiently whether such an arbitrage exists and have used this to show that expected-shortfall arbitrage for small values of may exist in more realistic market models, including incomplete markets featuring transaction costs.

Positively-homogeneous risk measures have a natural attraction in that a regulator can use them to impose risk constraints that are proportionate to the size of investments and so, superficially, appear to treat large and small institutions “fairly”. For example, in Artzner et al., (1999), the axiom of sub-additivity (which follows from convexity and positive homogeneity) is justified in part by the observation: “If a firm were forced to meet a requirement of extra capital which did not satisfy this property [sub-additivity], the firm might be motivated to break up into two separately incorporated affiliates, a matter of concern for the regulator.” From a post-crisis perspective, this argument seems to have lost some of its persuasive force.

We would argue that a larger institution should be able to manage risk more effectively, making it reasonable for a regulator to insist that as institutions scale they should abide by increasingly stringent risk constraints. We believe our results show that not only is it reasonable for a regulator to insist upon this, but it is essential if the regulator’s constraints are intended to be effective irrespective of market conditions.

References

- Acerbi and Tasche, (2002) Acerbi, C. and Tasche, D. (2002). On the coherence of expected shortfall. Journal of Banking and Finance, (26):1487–1503.

- Alexander, (2004) Alexander, C. (2004). Normal mixture diffusion with uncertain volatility: Modelling short-and long-term smile effects. Journal of Banking & Finance, 28(12):2957–2980.

- Alexander and Baptista, (2002) Alexander, G. J. and Baptista, A. M. (2002). Economic implications of using a mean-var model for portfolio selection: A comparison with mean-variance analysis. Journal of Economic Dynamics and Control, 26(7-8):1159–1193.

- Armstrong, (2018) Armstrong, J. (2018). The Markowitz category. SIAM Journal on Financial Mathematics, 9(3):994–1016.

- Armstrong and Brigo, (2018) Armstrong, J. and Brigo, D. (2018). Rogue traders versus value-at-risk and expected shortfall. Risk Magazine.

- Armstrong and Brigo, (2019) Armstrong, J. and Brigo, D. (2019). Risk managing tail-risk seekers: VaR and expected shortfall vs S-shaped utility. Journal of Banking and Finance.

- Armstrong et al., (2017) Armstrong, J., Pennanen, T., and Rakwongwan, U. (2017). Pricing index options by static hedging under finite liquidity. Available at arXiv.org.

- Artzner et al., (1999) Artzner, P., Delbaen, F., Eber, J.-M., and Heath, D. (1999). Coherent measures of risk. Mathematical finance, 9(3):203–228.

- Bloomberg L.P., (2018) Bloomberg L.P. (2018). Retrieved from Bloomberg database.

- Brigo and Mercurio, (2002) Brigo, D. and Mercurio, F. (2002). Displaced and mixture diffusions for analytically-tractable smile models. In Geman, H., Madan, D., Pliska, S. R., and Vorst, T., editors, Mathematical Finance — Bachelier Congress 2000: Selected Papers from the First World Congress of the Bachelier Finance Society, Paris, June 29–July 1, 2000, pages 151–174, Berlin, Heidelberg. Springer Berlin Heidelberg.

- Brigo and Nordio, (2015) Brigo, D. and Nordio, C. (2015). A random holding period approach for liquidity-inclusive risk management. In Glau, K., Scherer, M., and Zagst, R., editors, Innovations in Quantitative Risk Management, pages 3–18, Cham. Springer International Publishing.

- Bruder et al., (2016) Bruder, B., Kostyuchyk, N., and Roncalli, T. (2016). Risk parity portfolios with skewness risk: An application to factor investing and alternative risk premia. Lyxor Asset Management technical report.

- Föllmer and Schied, (2002) Föllmer, H. and Schied, A. (2002). Convex measures of risk and trading constraints. Finance and stochastics, 6(4):429–447.

- Herdegen and Khan, (2020) Herdegen, M. and Khan, N. (2020). A dual characterisation of regulatory arbitrage for coherent risk measures. Available at arXiv.org.

- Kahneman and Tversky, (1979) Kahneman, D. and Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica: Journal of the econometric society, pages 263–291.

- Lezmi et al., (2018) Lezmi, E., Malongo, H., Roncalli, T., and Sobotka, R. (2018). Portfolio allocation with skewness risk: A practical guide. Amundi Asset Management technical report.

- Markowitz, (1952) Markowitz, H. (1952). Portfolio selection. The journal of finance, 7(1):77–91.

- Pennanen, (2011) Pennanen, T. (2011). Convex duality in stochastic optimization and mathematical finance. Mathematics of Operations Research, 36(2):340–362.

- Pennanen, (2012) Pennanen, T. (2012). Introduction to convex optimization in financial markets. Mathematical programming, 134(1):157–186.

- Rockafellar et al., (2000) Rockafellar, R. T., Uryasev, S., et al. (2000). Optimization of conditional value-at-risk. Journal of risk, 2:21–42.

Appendix A Proofs

Proof of Theorem 1.5.

Let and be as in the statement of the theorem.

Using the subadditivity of , followed by its positive homogeneity, followed by the definition of -arbitrage we find:

For we have

| (17) |

The last bound arises by differentiating at and using the concavity of on the left.

Define

so that is continuous and increasing and satisfies the inequalities

| (18) |

The function is differentiable except at and . At points where the derivative exists

Hence for all

We deduce from (18) that for all

Hence

by (17).

There is a positive probability that , so . Hence if either or we find

∎

Proof of Theorem 1.6.

Using the notation of the previous proof, to see that the constraint is ineffective, simply take . Then by (3), will give a solution of arbitrarily high utility which lies in by (5) and which has a cost of less than by (4).

Let us assume that is ineffective. This implies that for all we can find with and . We see that and . If we take then so is greater than or equal to with positive probability, and hence so is . Therefore is greater than with positive probability. We conclude that is a -arbitrage. ∎

Proof of Theorem 1.7.

Let , so that . Since is concave

Rearranging we find

So, by our assumption that is finite, it suffices to prove that

| (19) |

Proof of Theorem 1.9.

By making an affine transformation of if necessary, we may assume for all and for all .

Suppose that is ineffective. Let be a basis for . Write . Define the set

The bound

shows that since is ineffective, will be unbounded. Since is also convex and contains the origin, it must contain some ray starting at the origin.

Hence we may find with for all .

Since

we have that .

Suppose for a contradiction that there is a positive probability that is negative. Then we may find such that . Hence using our bound for all and for all we have that for all

Using (8) and the fact that is concave and increasing, we find that the right hand side tends to as , yielding the desired contradiction.

Therefore is almost surely non-negative. Since and the are assumed to be linearly independent, we deduce that there is a positive probability that is positive. Hence is a true arbitrage. ∎

Proof Theorem 2.2.

As described in Armstrong and Brigo, (2019), since the market is atomless we can find a uniformly distributed random variable such that the Radon-Nikodym derivative

for some positive decreasing function of integral over . (In the event that has a continuous distribution we may simply take to the the image of under its own cumulative distribution function, the atomless assumption allows us to find in the general case).

It follows from the theory of rearrangements described in Armstrong and Brigo, (2019) that if an -arbitrage exists, then there exists an arbitrage of the form for some increasing function .

If is an arbitrage then so is . To see this, first note that and so

Second we have by the axioms of a coherent risk measure that

Next note that which shows that a non-positive random variable can only have an expected shortfall of zero if it is constant and equal to zero. It follows that is either constant or has a positive probability of being positive. But is constant if and only if is constant, and cannot be constant since it is an arbitrage. Therefore has a positive probability of being positive. We have now shown that is an -arbitrage as claimed.

It follows that we may restrict attention to looking for arbitrage of the form with increasing and .

Given and , let be the set of increasing functions which satisfy , and which have . We will say that is a -arbitrage if is a -arbitrage. We have shown above that the market contains an -arbitrage if and only if some contains an -arbitrage.

Define an increasing function by

where is chosen to ensure that . This requires

and hence

| (20) |

Since for we compute that for

| (21) |

We may rewrite the first term on the right hand side as follows

But on , on . Moreover is also a decreasing function. We deduce that

Using this we may obtain from equation (21) that

Hence by definition of , we have shown that for

| (22) |

We deduce that if contains any -arbitrage then must be an -arbitrage. This will be the case so long as and .

Let us now make the dependence of on , and explicit and write

We have

| (23) |

where is given in (20). We note that

So we may rewrite (23) as

| (24) |

Viewed as a function of , must be decreasing by (22). We also note that

| (25) |

where we have used (24), the fact is decreasing and the fundamental theorem of calculus. We deduce that if

then will be an arbitrage for sufficiently small . Suppose we have

then will not be an arbitrage for any value of . If we have equality

then the limit in (25) will be achieved for finite if and only if attains its supremum on . Hence will be a -arbitrage for sufficiently small if and only if this supremum is attained. The result follows. ∎