Wiener-Hopf Factorization for the Normal Inverse Gaussian Process

Abstract

We derive the Lévy-Khintchine representation of the Wiener-Hopf factors for the Normal Inverse Gaussian (NIG) process as well as a representation which is similar to the moment generating function (MGF) of a generalized gamma convolution (GGC). We show, via this representation, that for some parameters the Wiener-Hopf factors are, in fact, the MGFs of GGCs. Further, we develop two seperate methods of approximating the Wiener-Hopf factors, both based on Padé approximations of their Taylor series expansions; we show how the latter may be calculated exactly to any order. The first approximation yields the MGF of a finite gamma convolution, the second that of a finite mixture of exponentials. Both provide excellent approximations as we demonstrate with numerical experiments and by considering applications to the ultimate ruin problem and to the pricing of perpetual options.

1 Introduction

In order to determine the Wiener-Hopf factorization for the Normal Inverse Gaussian (NIG) process we are required to solve the following problem:

For , , , , , factor the expression

| (1) |

into the product of two functions, and , such that: a) is the moment generating function (MGF) of an infinitely divisible (ID) probability distribution on without drift or Gaussian component; and b) , is the MGF of an ID probability distribution on also without drift or Gaussian component.

That such a factorization exists is a well established fact, see e.g. [9], Chapter VI.2. That is, we may replace in (1) by the Laplace exponent of any Lévy process and be certain not only that the factorization exists, but also that

where and are the running supremum and infimum process repectively, i.e.

and is an exponentially distributed random variable with mean , which is independent of . Consequently, the Wiener-Hopf factorization is arguably one of the most remarkable and well-known results in the theory of fluctuations of Lévy processes.

It is easy to see that the Wiener-Hopf factors, i.e. and , if known explicitly, are in some sense the “next best thing” to knowing the distributions of and . In fact, many practical problems involving the exit of a Lévy process (or some function thereof) from a region in the state space – examples include the calculation of ruin probabilities (see [2] and Section 7.2), whose study originates from the insurance industry, and the pricing of financial products such as barrier options (see, e.g. [18]) – can be solved via the Wiener-Hopf factors. The distributions of and also appear in the pricing of perpetual options (see [24] and Section 7.3) and more generally in optimal stopping problems, see e.g. [23], Chapter 11.

Unfortunately, explicit, tractable expressions for are not known for many processes (see Chapter 6.5 in [23] and the introduction of [22] for a good overview of known Wiener-Hopf factorizations). In particular, among those classes of processes with infinite activity jumps and infinite variation paths for which there is no restriction on either positive or negative jumps, only two have known, explicit factorizations. These are: a) the stable class of processes (see [20]); and b) the meromorphic class of processes (see [21]).

The methods of finding tractable expressions for the Wiener-Hopf factors and determining the distributions of and for processes with two-sided jumps fall into roughly three categories: a) by inspection; b) by solving the equivalent problem of factorizing (1) into the product of two functions analytic and zero-free on the left and right half-planes respectively (plus a growth condition) (see [19], Theorem 1. (f)); c) by evaluating a general integral representation (see [19], Theorem 1. (b)). Method a) is only applicable in the simplest cases, e.g. when is a Brownian Motion, and the integral representation of method c) is not generally tractable, although, with some rather inspired methods, it has been used in the stable case [20]. Method b) is primarily useful when is a meromorphic or rational function, as, in this case, it is possible to group poles and zeros to determine the Wiener-Hopf factors (see for example [25] and [21]). This approach is not applicable when has branching singularities, as is the case for the NIG process as well as many other processes popular in applications (e.g. CGMY or KoBoL processes and the Variance Gamma process).

Before describing the approach taken in this article, which differs from the above mentioned three, we take a moment to consider a special case of (1). Let and . In this case it is easy to derive the factorization

where and are just the positive and negative zeros of respectively. We conclude that and are gamma distributed random variables. Writing, for example,

we might conjecture that, in general, has the form

| (2) |

which, given the right restrictions on the measure , would imply that the distributions of and belong to the class of generalized gamma convolutions (GGCs) (see [11]).

It turns out that this conjecture is nearly correct. In particular, we show in Corollary 2 that has the form (2), but that is not necessarily a positive measure. Our approach in deriving this representation differs from the approaches discussed thus far. It is based on the idea that we can derive the Lévy measures of and by considering the inverse Laplace transform of the function . This allows us to derive the Lévy-Khintchine representation of in Theorem 4, which leads almost directly to the representation (2) and an explicit formula for the measure . This representation of the Wiener-Hopf factors is tractable in the sense that we are able to generate a full Taylor series expansion of by calculating the negative of moments of . This we are able to do exactly, i.e. without numerical integration, for all orders (see Section 6). An important consequence of this fact, is that we are able to calculate Padé Approximants (rational approximations) based on the Taylor series expansion, which yield, by virtue of an interesting connection to the theory of Stieltjes functions and an important theorem due to Rogers [26], convergent approximations of that are either: a) the MGFs of finite gamma convolutions (GCs) (when is positive); or b) the MGFs of finite exponential mixtures (MEs) (irrespective of whether is positive or not). The convergence of the approximations to is exponential in the degree of the rational approximation, and the approximating distributions match the first moments of the distributions of and .

This article is organized as follows: In Section 2 we present some basic facts about the NIG process and state a technical lemma about solutions of the equation , which will be important for the remainder of the paper. It is perhaps important to note here, although details and references will be given in Section 2, that the NIG process is, in fact, a process with two-sided jumps, infinite jump activity and infinite variation paths, which is widely used for modeling both physical processes as well as economic ones. In Section 3 we review some basic facts about GGCs, MEs and the connection between MEs and the class of Lévy processes whose Lévy measures have completely monotone densities. Section 4 reviews the connection between GGCs, MEs and Padé Approximants of Stieltjes functions. The main theoretical results are given in Section 5 in which we derive the Lévy-Khintchine representation of as well as the GGC-like representation (2). We show that the distributions of and belong to the class of GGCs when is a positive measure and that they do not belong to this class when is not positive. We also show that the representation (2) holds also for in the cases where this makes sense. In Section 6 we present an easy method for computing the negative moments of , which are the basis for the above mentioned Taylor series expansions and Padé Approximants. Finally, in Section 7 we conduct some numerical experiments with our theoretical results and demonstrate convenient applications to the ultimate ruin problem and the pricing of perpetual stock options.

Throughout the paper we will write , , , and , where

with analogous definitions for and . When working with complex or imaginary numbers we will always write for the imaginary unit. As well as working with the Wiener-Hopf factors directly we will also work with the cumulant generating functions (CGFs) or Laplace exponents

2 The NIG process

The NIG probability distribution was first introduced by Barndorff-Nielsen in [7]. NIG distributions form an subclass of the set of normal variance-mean mixtures, the set of generalized hyperbolic (GH) distributions [6] and the set of ID distributions [8]. Within the class of GH distributions, the NIG distribution is the only distribution that is closed under convolutions; in general, it is a mathematically tractable version of a GH distribution that can be used to approximate the majority of GHs quite well [6]. In this context it has been used to model turbulence as well as financial data. When the NIG distribution is taken as the basis for a Lévy process, it has the advantage of an explicitly defined transition density (see e.g. Table 4.5 in [30]). Additionally, its statistical properties (e.g. semiheavy tails) and the fact that NIG processes have infinite jump activity are a desirable feature when modeling stock market returns [8, 1]. NIG processes belong to the popular class of processes, see Section 3, as well as to the class of regular Lévy processes of exponential type [12].

Like all Lévy processes, we can define a NIG process via its Laplace exponent , which we will do using the parameterization found in [13], pg. 128111In many sources, including [7, 8], the NIG process is defined via Laplace exponent , where , , and . In this case, the process can also be defined via subordination except that the subordinator is an inverse Gaussian process with parameters and and the Brownian motion has drift and diffusion coefficient equal to one. It is easy to find a bijection between the sets of parameters and and so the approaches are equivalent. The one caveat is that in the above mentioned sources the case is allowed, which would imply for the parameter set used in this article. This extreme case is not included here, as it does not fit into our approach. Other authors also exclude the case in their definifions of the NIG process, see in particular [30, 12]. Note that in this extreme case we leave the class of processes defined by subordinating Brownian motion with a tempered stable subordinator; in the extreme case the subordinator becomes a stable process., via the subordination of a Brownian motion with drift by an inverse Gaussian subordinator. Consider the subordinator with Lévy measure

and note that with this parameterization is in fact the variance of . The Laplace exponent of the process is then

| (3) |

Subordinating the Brownian motion with drift, , with Laplace exponent

by the process gives us the Laplace exponent of a NIG process without drift, i .e.

where

| (4) |

such that . Adding a drift to gives a general NIG process with parameters , which has Laplace exponent

| (5) |

where the funtion on the righthand side of (5) can be extended to an analytic function in the cut complex plane . If is an exponential random variable with mean , which is independent of , then we have

| (6) |

where the equalities hold on some non-empty, vertical strip in the complex plane containing zero. The righthand side of (6) is again a well-defined and analytic function of on except at those points where

| (7) |

It is easy to see that if solutions of (7) exist, they will have the form

In fact, and are just the solutions of the associated quadratic equation

| (8) |

where . The following technical proposition is important in helping us determine the number, mutiplicity, and location of solutions of (7) and will be referenced throughout the article. Its proof is straightforward and a little tedious, so we relegate it to Appendix A.

Proposition 1.

3 Generalized gamma convolutions, exponential mixtures, and the class of processes

In this brief section we review some facts about generalized gamma convolutions, exponential mixtures, and Lévy processes whose jumps are determined by Lévy measures with completely monotone densities. We denote this latter group of processes by . The content in this section is taken primarily from Bondesson [11] and Rogers [26]. Going forward we will write for the Gamma distribution with density

Definition 1.

A generalized gamma convolution is a probability distribution on with MGF

where and is a radon measure on satisfying

The measure is referred to as the Thorin measure and the name generalized gamma convolution is easy to justify given that a convolution of a finite number of independent gamma distributions is a special case of a GGC with a Thorin measure that has finite support. The inclusion of the constant in the definition owes to the fact that the distribution converges weakly to the degenerate distribution at the point as . For our purposes it is important to note that: a) an arbitrary GGC is the weak limit of a sequence of convolutions of finite numbers of independent gamma distributions (see Theorem 3.1.5 in [11]); and b) that GGCs are ID distributions such that the following relationship holds.

Theorem 1 (Theorem 3.1.1 in [11]).

A probability distribution on is a GGC iff it is an ID distribution whose Lévy measure has a density , such that is a completely monotone function. In this case, we have the following relationship between the Lévy density and the Thorin measure

We recall that a completely monotone function , defined for , is a smooth function that satisfies

and that by Bernstein’s theorem, every completely monotone function has a representation of the form for a measure on .

Definition 2.

A process Lévy process if its Lévy measure has the form

for measures and , which satisfy

That every NIG process belongs to is perhaps not obvious from the discussion thus far, however, it is clear from the Lévy-Khintchine representation of the Laplace exponent, which was first derived by Barndorff-Nielsen in [7] and then again more directly in [8].

Definition 3.

A probability distribution on is a mixture of exponentials if its MGF has the form

| (9) |

where is a probabilty distribution on . A finite mixture of exponentials results when has finite support.

Note that while all non-degenerate GGCs are absolutely continuous with respect to the Lebesgue measure, this is not the case for MEs, since the measures can have an atom at . In this case an ME will have an atom at zero and a density with respect to the Lebesgue measure on (see also discussion on pg. 25 and 30 in [11]).

What ties MEs and the class of processes together is the following important theorem due to Rogers [26].

Theorem 2 (Theorem 2 in [26]).

-

(i)

If , then the distributions of and are MEs for each .

-

(ii)

If the distributions of and are MEs for some , then .

4 Padé approximants of Stieltjes functions and the connection to GCCs and MEs

This section is the companion to Section 3 in the sense that we present a very natural and elegant way to approximate general GGCs and MEs by gamma convolutions and finite MEs respectively. The technique in both cases relies on Stieltjes functions and their Padé approximants.

Definition 4.

A Stieltes function is defined by the Stieltjes-integral representation,

where is a positive measure on with infinite support and finite moments

Formally, we may also express as a Stieltjes series, which may converge only at and has the following form:

| (10) |

It is easy to see that the above series converges for if and only if the support of lies in . In this case we will call a Stieltjes function (or a Stieltjes series) with the radius of convergence . For such functions, the domain of definition extends to all .

For the following, we assume is a function (not necessarily a Stieltjes function) with a power series representation at zero.

Definition 5.

If there exist polynomials and satisfying , , and

then we say that is the Padé approximant of the function (at zero).

The connection between Stieltjes functions and Padé approximants is nicely summarized in the following theorem due to Baker [5].

Theorem 3 (Corollary 5.1.1, and Theorems 5.2.1, 5.4.4 in [5]).

If is a Stieltjes function with radius of convergence , then exists provided and . The approximant has simple poles in , which have positive residues. Further, on any compact subset

where and are both greater than zero.

To make the connection with GGCs, let us assume is the MGF of a GGC with corresponding random variable and Thorin measure with infinite support. We further assume that , and therefore also , is analytic at zero such that has radius of convergence . For simplicity we assume the constant in Definition 1 is zero. Further, from here on, we will denote the pushforward measure of under the transformation by .

Lemma 1.

The function is a Stieltjes function with radius of convergence , in particular has the following analytic continuation to the cut complex plane

Proof.

The assumptions that is analytic with radius of convergence implies has support in . Therefore, for

where we have made the change of variables in the last step. That the measure has moments of all orders is guaranteed by the conditions imposed on in Definition 1 and the fact that the support of lies in . ∎

Proposition 2.

For all the function

is the MGF of a convolution of independent gamma distrubtions. The corresponding random variable has the property

Proof.

According to Theorem 3 we have

where and for all . As a result

which demonstrates the first part of the claim. For the second part, we simply need to observe that by defintions of Padé approximations and Stieltjes functions we have

where for . From here, it is easy to see that the first cumulants of and , and therefore also the first moments, are identical. ∎

A connection between Stieltjes functions and Padé approximations and MEs is also easy to establish. In what follows suppose that is a random variable whose distribution is a ME with MGF such that the measure in Definition 3 has infinite support. Further assume that is analytic at zero such that its power series has radius of convergence .

Lemma 2.

The function is a Stieltjes function with radius of convergence .

Proof.

This leads us directly to the result which is the analogy for MEs to Proposition 2.

Proposition 3.

For , the function (resp. ) is a MGF of a finite mixtures of exponentials. The corresponding random variable (resp. ) has the property

Remark 1.

Recall that the MGF of an ME distributed random variable has the form

where is a probability distribution, which may have an atom with weight at . If this is the case, then the distribution of will have an atom with weight at zero. In choosing an approximation by a finite mixture of exponentials via the Padé approximation, it is clear from Proposition 3 that we can adjust the approximation to be either absolutely continuous (by choosing the approximation) or to have an atom at zero (by choosing the approximation). Further, according to Theorem 2, and the fact that NIG processes belong to , the distribution of will be an ME, and it is easy to show that , which holds essentially because the NIG process is an infinite variation process. Therefore, the distribution of will be absolutely continuous, and we will focus only on the approximation in this article. The same is true of , of course.

We end this section with a brief description of the computation of the coefficients of Padé approximants. For the interested reader, the book [5] by Baker is a good source for information on Padé approximants in general. Consider a function , whose Padé approximant is known to exist. First, we solve the system of linear equations

| (26) |

whose solutions , , give us the coefficients of the denominator . Then, the coefficients of the numerator can be calculated as follows:

| (27) | |||

In practice, when is even moderately large, the system in (26) will have a very large condition number, and solving the system of linear equations (26) will likely involve a loss of accuracy. This can be avoided by using higher precision arithmetic. For the computations in this article we use Mathematica, which supports arbitrary precision arithmetic, as well as the MPFUN90 arbitrary precision package for Fortran-90 [3].

5 The Wiener-Hopf factorization for the NIG process

Before we state the main results, we consider a general method for determining the Wiener-Hopf factors, which will be used in the proof of Theorem 4, but is theoretically valid for those Lévy processes whose Laplace exponents are analytic at zero. Let be a Lévy process and let (resp. ) be the running supremum (resp. infimum) process. The standard Wiener-Hopf theory for Lévy process (see for example Theorem 6.15 in [23]) then shows: a) and are positive, ID random variables without drift or Gaussian component; and b) . Therefore, we must have

for some Lévy measure on , which satisfies the condition

| (28) |

It follows that

| (29) |

where is the measure restricted to and is the measure restricted to . In what follows, the central idea is to determine by inversion of the Laplace transform, from which it is straightforward to identify and and therefore derive the explicit Lévy-Khintchine representation (29) of the Wiener-Hopf factors.

To this end we make some observations, which are either well-known facts, or have straightforward proofs:

-

(O1)

If is analytic at zero, then

(30) which is finite at least on some strip , .

-

(O2)

It follows from (28) and (O1) that the measure is a finite, signed measure.

-

(O3)

From (O2) it follows that the function is a right continuous function of bounded variation with the property (see [15], pg. 104, Theorem 3.29).

-

(O4)

From (O1) it follows that as for and as for , from which, together with (O3), it follows, via integration by parts, that

- (O5)

-

(O6)

From (O5) and (O3) it follows that if is continuous at , then is also continuous at and . I.e. the procedure in (O5) actually returns the original function values , or , wherever is continuous.

-

(O7)

If, in addition, we can determine almost everywhere (w.r.t. the Lebesgue measure), and , then .

We now use the above described approach for the NIG process. The reader should assume that the notation , , , and refers to a NIG process for the remainder of this section. We will see shortly that the form of the Lévy-Khintchine representation of the Wiener-Hopf factors of the NIG process depends on: a) whether or not and are solutions of (7), i.e. of ; and b) whether or not or (see Section 2 and Proposition 1 for definitions and properties of , , , and ) . Let us define the following cases for

Similarly, for we define

Next, let us define the (not necessarily positive) measures

| (33) | |||

where

| (34) |

Similarly, we define

| (35) | |||

| (36) |

where and are as in (34).

With these definitions we can give our first main result, the Lévy-Kintchine representation of the Wiener-Hopf factors of the NIG process.

Theorem 4.

For the NIG process, the measures and are absolutely continuous with respect to the Lebesgue measure with densities

where the forms of and are case dependent and are given in Table 1.

| I | II | III | |

|---|---|---|---|

| A | |||

| B | |||

| C |

Proof.

Our goal will be to determine the function from the preceding discussion and its derivative. To do this, we will derive an expression for the function via the Formulas 31 and 32. Specifically, we will derive an expression for using Formula 31 and an expression for using Formula 32 for the cases I-A, II-A, and III-A. The other cases can be treated in an analogous manner.

To begin, note that

| (37) |

which is a well defined function on except possibly at the points and , which may be simple poles. Let us now proceed on a case-by-case basis.

Case: I-A

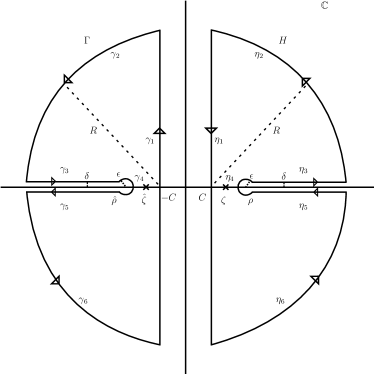

In this case, the function has no zeros. In particular, the singularities of in the open right half-plane are restricted to . To derive a general expression for we apply Formula 32 with some and consider the integral of along the line for fixed . To evaluate this, we consider instead the integral of our function along the contour of Figure 1, i.e.

| (38) |

where we have used Cauchy’s integral theorem in the last equality. In the limit the integrals along the contours and vanish. Then, letting we have

along the contour . Similarly along we have

Now, adding these integrands together and letting – note that the integral along vanishes with – we arrive at

| (39) |

Using , the contour from Figure 1, and the identical approach we can show that for

| (40) |

Note that since we have assumed that and , and since and by Proposition 1 (vi), the singularities in the integrals (39) and (40) at and remain integrable.

II-A

For this case, the derivation of the function remains the same. The major difference is that since is a solution of (7), has a simple pole in the interval (see Proposition 1 (iii) and (iv)). The effect of this is that (39) becomes

III-A

In this case the key difference is that both and solve the associated quadratic equation (8). It is easy to see that if this is the case and , then also and therefore also (see Proposition (1) (vii)), which we explicitly assume is not the case here (we have chosen case A). Thus, we assume that , which together with our previous assumptions implies that . This has two consequences. The first is that (40) simplifies to

and the second is that the integral along the contour does not vanish as . Making the change of variables , taking the limit as , and applying the dominated convergence theorem shows that

Therefore we have

where the same simplification takes place in the integrand as for .

Now, independent of the case, we remark that and are not only continuous, but also differentiable functions on and respectively. By (O6), this implies that we have identified an explicit expression for at every point . However, since is by assumption right-continuous, and since , we can actually conclude that is continuous also at zero and define as either or equivalently as . If we define for and for , the above discussion shows that

Employing (O7) then gives the desired result. ∎

Going forward, for a measure , let denote the pushforward measure under the transformation .

Corollary 1.

If (resp. ) is a positive measure then (resp. ) has a distribution that is a GGC. The corresponding Thorin measure is given by (resp. ).

Remark 2.

From the definition of the measures and , it is clear they are not always positive (see Example 1 below). That is, we may not conlude, in general, that the distributions of and of are GGCs. Determining whether or not the measures are positive or signed is straightforward, we simply need to determine the slope and intercept of the line in (33) or the sign of in (35) and (36). In doing so, it is easy to see that in the signed case the measure always breaks down into the difference of two finite, positive measures with the following characteristics: The measure that contributes positive mass is supported either on an interval, at one point, or on the union of an interval and a disjoint point. The measure that contributes negative mass will always be supported on a non-empty interval. Each measure assigns no mass to a non-empty interval , where either or . This breakdown describes the Jordan decomposition of the measure , which we can always determine exactly in this manner. Further, the above statements are equally true for the measure , with or .

Example 1.

We consider an example to demostrate an instance of the previous remark. Let

In this case , the slope of the line , is positive, and the intercept with the horizontal axis, , occurs to the right of . Additionally, while solves (7) does not, i.e. we have described an instance of Case II-A. Thus we have

where and denote the positive and negative contributions of respectively.

For the following Corollary, we will require the ideas from the previous discussion as well as the Frullani identity, which states that for a continuously differentiable function we have

where we assume and that and are finite.

Corollary 2.

Proof.

If is a postive measure, then the result follows immediately from Corollary 1. Otherwise, let denote the Jordan decomposition of , which has the relatively simple form described in the discussion preceding the statement of the corollary, and assume first that . Then

since each of and is finite and assigns no mass to the interval . Applying Frullani’s identity with , , we get

with the identical result for . It follows that we may apply Fubini’s Theorem for each of and separately, which, after recombining, establishes the result for . For repeating the above excercise with , , shows that the result can be extend to . However, it is not difficult to see that

are analytic functions for . By analytic continuation, the functions must be equal on this half-plane. The proof for is identical. ∎

We can also use the given results to determine the distribution of the overall supremum and overall infimum , which exist as real valued random variables when and respectively. To do so, we need to consider the limits and .

In what follows, we allow and to extend to the case . It is easy to show that for this case we have , where the assignment of the zero root to either or depends on the value of . Likewise, the terms and from (34) and therefore also the measures , and from (33), (35), and (36) respectively are all well-defined also for .

Corollary 3.

If (resp. ) then the Laplace exponent of (resp. ) has the form

| (42) |

where (resp. ) and

The equality (42) holds for , where (resp. ) whenever (resp. ) satisfies and (resp. ) otherwise.

Proof.

We will work through the three possible cases for ; the derivation for is identical. First, let us make five observations – essentially extensions of Proposition 1 for the case plus two obvious facts – that are easy to verify: (a) and are real for small enough; (b) neither nor is possible; (c) is a solution of iff or and ; (d) the equation (resp. ) has at most two solutions; and (e) the assumption implies that and, in particular since , that .

Case 1

We assume first that does not solve such that . It is easy to see that the first part of our assumption, together with observations (a) and (c), implies that for small enough. Applying Proposition 1 (ii), we see that is not a solution of (7) when is small. Further, from observation (d) it is clear that we may also assume that neither nor and therefore that for small . Then, since: a) the function is bounded for for every fixed such that ; b) the measure

is finite; and c) the function

| (43) |

is bounded for for small enough (due to our assumption that , observations (a) and (b), and Proposition 1 (v) we know that and are both strictly less than ), we can apply the dominated convergence theorem in the integral in (41) to get the result. Note that observations (d) and (e) ensure that we do not have any cancellation in the numerator and denominator in (43) as , i.e. it is not possible that becomes in the limit.

Case 2

If we assume that solves and , then the approach is essentially the same, except that we must show that for small enough, i.e. that becomes a solution of (7) for small enough. Proposition 1 (ii) together with the fact that our assumptions imply that

| (44) |

shows that does solve (7) for small . To verify (44) we recall that observation (e) states that and consider cases for . If , then clearly (44) clearly holds. If instead and , then is not a solution of according to general observation (c), which contradicts our assumptions. Finally, if and , then solving for yields . Plugging this into the expression for yields , which again contradicts our assumptions.

Case 3

Assuming now that , we solve this equation for , which yields . Plugging this value of into the expression for , shows that from which it follows that . General observations (a) and (d) and Proposition 1 (v), show that for small enough. It follows that for small enough, which, according to Proposition 1 (ii), implies that solves (7) for small enough. Therefore, when is small.

To complete the proof for this case, we need to following facts, which have straightforward proofs that are therefore omitted (although (c) requires some rather tedious algebra): (a) for small enough; (b) such that for every we have

and (c) . We now aim to show that

| (45) |

as this, together with the already mentioned fact that the function is bounded for for every fixed such that , would allow us to use the generalized form of the dominated convergence theorem (see Theorem 19 pg. 89 in [27]) in the integral (41) and complete the proof for this case.

The integral on the right of (45) is easily evaluated (see (6.1)):

| (46) |

If we ignore the absolute value in the integral on the left of (45) for the moment, and treat it as an indefinite integral, we can evaluate the resulting integral exactly – after a partial fraction decomposition and the substitutions and – by using the same techniques as for the integral on the right (constant of integration omitted):

| (47) | ||||

In order to evaluate the integral on the left-hand side of (45) we need to evalaute over the interval where the integrand is negative and then over the interval where the integrand is positive. We see, however, that irrespective of the limits of integration for , the contribution from this term will vanish as since the arctangent function is bounded and since goes to zero with (fact (c) from above). Thus, we need only consider the integral over these intervals. It is easy to see that evaluated over (i.e. expressed using transformed variable ) will vanish with , since since as . Using this fact again, and also the fact that as , the value of over the interval converges to (46) as goes to 0, and so we have proven (45). ∎

Remark 3.

Note that since both the class of GGCs and the class of MEs are closed with respect to weak convergence (see Proposition 9.10 and Corollary 9.6 together with Thereom A.4 in [29]), the distributions of both and will be MEs, and they will also be GGCs if the measures and are positive for small enough. This means that in the remainder of this paper, we can treat the case in exactly the same way that we would treat the case . Thus, unless otherwise stated, the reader may assume that the notation and includes the case , i.e. and .

We have shown that and always have a Laplace exponent of the

| (48) |

where is the signed measure from Corollaries 1, 2, and 3 , which is derived from some linear combination of the measures (33), (35), and (36), and the Dirac delta measure. At this point we have strong evidence that the distributions of and are not GGCs whenever is not a positive measure. The following final corollary for this section confirms this assumption.

Corollary 4.

Let denote either or with Laplace exponent and associated measure as described in (48). If is not a positive measure, then the distribution of is not a GGC.

Proof.

We assume that the distribution of is a GGC and that is not a positive measure. Therefore, must be a finite, signed measure such that there exist for which and . Now we apply Lemma 1, which guarantees that has an analytic continuation of the form

for some positive measure . The measure is uniquely determined by the function (by virtue of the fact that is a Pick function; see discussion top of pg. 30 and Theorem 2.4.1 in [11]). In particular,

| (49) |

Expanding the left-hand side of (49) we get

| (50) | ||||

| (51) |

where the interchange in the order of integration in the second equality in (50) is justified by the fact that is a bounded, positive function for each and an argument identical to the one used in the proof of Corollary 2. Now, the integrand on the right-hand side of (50) is bounded by one, and, in fact, converges to one as approaches zero for . For the integrand converges to zero. Applying the Dominated Convergence Theorem then shows that

which is a contradiction, since is a positive measure. ∎

Remark 4.

Since (and also ) the result of Corollary 4 is not really surprising. However, the results of this section raise a potentially interesting avenue of further research, namely to attempt to define the class of probability distributions whose CGF has the form (48). The potentially difficult part of this exercise, is to settle on the proper definition of the “Thorin” measure for this class, as it is easy to leave the realm of viable CGFs by a poor choice of signed measure. Additionally, while the literature on finite signed or complex measures is well developed, the literature on measures with infinite total variation is somewhat more limited, indicating the fact that working with such measures is more difficult. Ideally, we would like our class of distributions to include the class of GGCs, which would require at least some of the measures to have infinite total mass. The result of Corollary 4 is also interesting in the sense that although the NIG distribution is an extended generalized gamma convolution (EGGC), essentially a GGC extended to the real line (see Chapter 7 in [11]), the Wiener-Hopf factors of the NIG process are not generally MGFs of GGCs.

6 Technical Details of the Approximation Algorithm

In what follows, let denote an NIG process and denote either or . Further let and . We have seen (Corollaries 2 and 3) that has the form

| (52) |

where is a finite, possibly signed measure on , which assigns no mass to a non-empty interval . From Proposition 2 and Corollary 1 we know that if is a positive measure, then the Padé approximant of can be used to construct a function, which is the MGF of an -fold convolution of gamma distributions and matches the first moments of the distribution of . Further we know from Theorem 2, Proposition 3, and the fact that that regardless of whether or not is positive, the Padé approximant of is the MGF of a finite mixture of exponentials, which also matches the first moments of the distribution of . Thus we have potentially two approaches for approximation, which depend on the Taylor series expansion of either or of .

Regardless of whether or not is positive, we may readily show that is analytic near zero and that we may repeatedly differentiate under the integral sign, such that

for near zero. Thus, has the following Taylor series expansion at zero

We see that are simply the negative moments of the measure and that these are related to the cumulants of the distribution of by the relation . If are the moments of the distribution of , then we also have

for , which follows from the well known relationship between moments and cumulants. We see that our approximation depends only on our ability to compute the negative moments of .

6.1 Computing the negative moments of

Conveniently, we can compute the negative moments of exactly, i.e. without resorting to numerical integration. Recalling that is a stand-in for the measures , and and consulting Table 1 along with Formulas 33 through 36, we observe that the challenging part of computing the negative moments of is computing an integral whose general form is

where , , such that: , , and whenever and are both real. In particular, for we have , and . Further, and are either both real or both have nonzero imaginary part; in the latter case we have .

The approach to computing is simply to recognize that

where is a rational function and . It is always possible to reduce this rational function via partial fraction decomposition into a sum of integrals of the form

| (53) |

for constants and . If is real, then the integrals (53) can be computed exactly via the following identities (see Formulas 2.266, 2.268, 2.269.1-2 in [17]), where , , and the integrals are intended in the indefinite sense; the constant of integration is omitted:

| (54) | ||||

where

If is not real, then we require a different approach, which we demostrate in the following example, in which we show how to compute the most challenging version of .

Example 2.

Let

and expand the rational portion of the integrand as a partial fraction, such that

| (55) |

where

Note that the above recursion can also be solved explicitly, but for computational purposes the recursion will be faster. With this decomposition, we recognize that the integrals in the first term on the right-hand side of (55) can be calculated using (6.1) directly. The method of computing the second integral on the right-hand side of (55) depends on the values of and . If and are real and , then we must do one more partial fraction expansion in the integral on the right in (55). The substitutions and in the resulting integrals, combined with the fact that and and (6.1) allow for exact evaluation of . Note that if , then we can omit the partial fraction decomposition and use (6.1) directly.

If and are complex we proceed analogously with one further partial fraction expansion plus one additional step, namely the Euler substitution . This transforms the second integral in (55) into two integrals with rational integrands, in particular

| (56) |

where

By expressing and in terms of and we can show that the interval is never empty, and from our assumptions that , we can show that the function has no roots in . Therefore the integral on the right of (56) is easily evaluated exactly as

Of course, the same approach works also for .

7 Examples and Applications

In this section refers to a NIG process as do the random variables , and .

We will denote the random variable whose distribution approximates the distribution of (resp. ) with an -fold convolution of gamma distributions by (resp. ). The notation and is used for the MGF and CGF of respectively, which, we recall, can both be derived via the Padé Approximant of using the result of Proposition 2. These will have the form

for positive constants and , which are easily extracted from the Padé Approximant of by a partial fraction decomposition. The cumulative distribution function (CDF) of is denoted . We adopt the analogous notation for the MGF, CGF and CDF of .

The random variable corresponding to the approximation based on a mixture of exponential distributions will be denoted (resp. ). The notation and will be used for the MGF and CGF of , which are derived via the Padé Approximant of using the result of Proposition 3. These will have the form

where and are again positive constants obtained from the partial fraction decomposition of the Padé Approximant of . The CDF of will be denoted ; analogous notation will be used for the MGF, CGF, and CDF of .

7.1 Approximation of the CDF Two Ways

7.1.1 Cumulant Check

As an initial test of the results of Section 5 we consider the cumulants of , which we can calculate exactly via the CGF whenever . Via the CGFs and , derived in Corollaries 1 and 2, and the methods of Section 6 we can also calculate the cumulants of and exactly. If the results are correct, then the following relationship must hold for all :

| (57) |

Additionally, by construction, the relationship must also hold up to for the approximations based on the Padé Approximant, i.e. we must also have

| (58) |

whenever approximation by a gamma convolution is applicable. Additionally,

| (59) |

must always hold for the ME approximation. Note that while the identities (57), (58), and (59) are theoretically exact the degree of precision to which (58), and (59) hold when actually computed may depend on the level of precision we use in deriving the Padé Approximants (see discussion at the end of Section 4).

For this example, we consider the parameter set

since, in this case, both the approximation by gamma convolution and by finite exponential mixture is applicable. In Table 2 we compute identities (57) - (59) using this parameter set. The left-hand side of (57) - (59) up to is displayed in the column labeled . In column Exact, we compute the right-hand side of (57). As expected, the values match those in column exactly. In column G 500 , we compute the right-hand side of (58) for the random variables and using 500 digit precision to calculate the Padé Approximant. We do the same for the right-hand side of (59) using the random variables and in column E 500. Note, we only use higher precision arithmetic to compute the Padé Approximants, all other values are computed using 17 digits of precision. We see that at this level of precision, the approximations also satisfy the identities exactly. On a laptop with 4GB of memory and an Intel i5 CPU @ 2.27 GHz the entire computation to derive the parameters that define the distribution of – i.e. calculating the Taylor Series expansion of , deriving the Padé Approximation from this series, completing a partial fraction decomposition of the resulting function to isolate the parameters of the -fold gamma convolution – takes approximately 0.3 seconds. The same is true also for , and . The code for this example is written using Mathematica.

| Exact | G 500 | E 500 | ||

|---|---|---|---|---|

| 1 | -5.0000000000000000 | -5.0000000000000000 | -5.000000000000000 | -5.000000000000000 |

| 2 | 28.921875000000000 | 28.921875000000000 | 28.92187500000000 | 28.92187500000000 |

| 3 | -343.20581054687500 | -343.20581054687500 | -343.20581054687500 | -343.20581054687500 |

| 4 | 6196.8737068176270 | 6196.8737068176270 | 6196.8737068176270 | 6196.8737068176270 |

| 5 | -150452.69069820643 | -150452.69069820643 | -150452.69069820643 | -150452.69069820643 |

| 6 | 4.5921017309017433E6 | 4.5921017309017433E6 | 4.5921017309017433E6 | 4.5921017309017433E6 |

| 7 | -1.6888501187015734E8 | -1.6888501187015734E8 | -1.6888501187015734E8 | -1.6888501187015734E8 |

| 8 | 7.2689737036613218E9 | 7.2689737036613218E9 | 7.2689737036613218E9 | 7.2689737036613218E9 |

| 9 | -3.5843731491371288E11 | -3.5843731491371288E11 | -3.5843731491371288E11 | -3.5843731491371288E11 |

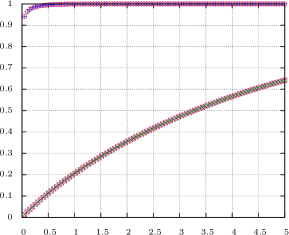

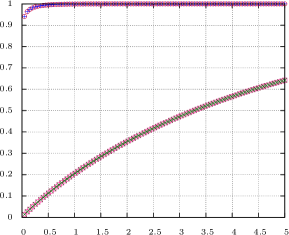

7.1.2 The CDF

Continuing with the example in Section 7.1.1 we now consider the CDFs of and ( and respectively) and the associated approximations. In Figure 2a we plot the (blue ) and (green ) as generated by a Monte Carlo simulation. That is, we simulate the exponential random variable and the discretize the interval using step sizes of . The random variables are simulated using the technique described in [28] and summed to generate a path; the maximum (resp. minimum) along this path is taken as an approximation of a realization of (resp. ). The process is repeated times to generate an empirical CDF.

Additionally plotted in Figure 2a are (red ) and (fuchsia ) as derived by numerical inversion of the Laplace Transforms . The general technique we use for numerical inversion is described in Appendix A of [16]. Note, that for numerical inversion we are required to evaluate along a line in the complex plane, which means that we need to evaluate integrals of the form

| (60) |

numerically for on this line. This, however, does not pose a serious challenge: we make a change of variables , such that the interval of integration becomes and then use the Tanh-Sinh Quadrature as described in [4] (precision and step size in the notation of [4]).

In Figure 2b along with (red ) and (fuchsia ) as computed by numerical inversion of the Laplace transform, we also plot (blue ) and (green ). In Figure 2c we make the same comparison using (blue ) and (green ). Note that in the latter case, we also generate the CDF via numerical inversion of the Laplace transform – this is much easier than computing and , however, since we do not have to calculate the integral (60) at every step of the algorithm – while in the former case we have explicit expressions for and , e.g.

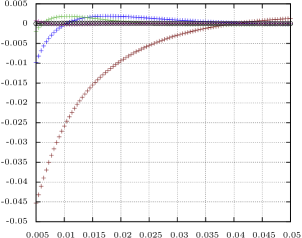

Thus from Figure 2a we get a numerical validation of our theoretical results and from Figures 2b and 2c we get a sense that both of our approximations work well, even when we employ a relative low degree Padé approximant. To get a better sense of the quality of the approximation along the steep part of the CDF of near 0, which is not captured in Figures 2a - 2c, we also plot the errors between as computed by numerical Laplace inversion and (maroon ), (blue ), (green ), (purple ) and (black ) over the interval in Figure 2d. We see that the lower degree ME approximations do not perform as well here and, depending on our desired level of accuracy, we may wish to choose a higher degree approximation (although already yields errors smaller than 0.005). By contrast, the fifth degree GGC approximation continues to perform well, which may justify the additional numerical effort required to compute the CDF in this case.

7.2 Ruin Probabilities

A simple application of the results to a financial problem, is to consider ruin probabilities. That is, we suppose that the capital of a company at time is modeled by , where is the initial capital and is a NIG process. The probability of ruin is then given by

Of course, this problem only makes sense when is a.s. finite, i.e. when , a condition we assume from now on. The asymptotics of the ruin probability have been studied extensively in the context of insurance companies where was initially modeled as a compound Poisson process with only negative, exponentially distributed jumps. In this setting it was found that if Cramér’s condition is satisfied, i.e. if has a negative, real root , then , where is an explicitly defined constant. Doney and Bertoin [10] generalized this result, i.e. they showed the same asymptotics also apply when is a Lévy process satisfying Cramér’s condition plus an additional technical condition – specifically that 0 is regular for – which is satisfied by all NIG processes. A limiting formula for in this general setting was derived by Mordecki [25], who showed that

| (61) |

For the NIG process, with and the results of Corollary 3, we may then use (61) to get an explicit representation of the asymptotics of , i.e. when is a NIG process satisfying and Cramér’s condition we have

| (62) |

and is the appropriate measure from Corollary 3. The integral in (62) is easily evaluated numerically, for example via the Tanh-Sinh Quadrature (see (60) and the discussion thereafter).

Of course, we can also approximate by deriving (or when appropriate, although in this case the ME representation seems more convenient). In particular,

If we order and such that then we would expect that and and that this approximation gets better with increasing .

Consider the parameter sets

and note that for PS 1 we have , whereas for for PS 2. In Table 3 we compute and for and . As a comparison we give the values of and , where the latter has been computed numerically with the Tanh-Sinh quadrature, in the row Exact. We see that indeed and converge numerically to and respectively. The convergence is slower for PS 2; this seems to reflect the fact that the condition is somewhat extreme.

| PS 1 | PS 2 | |||

| 5 | 0.16000002709200613 | 0.73382866742186084 | 0.50109487544933153 | 0.66572495797628802 |

| 10 | 0.16000000000000098 | 0.73382714607681802 | 0.50014426312102660 | 0.62302276617409411 |

| 15 | 0.16000000000000000 | 0.73382714607669872 | 0.50004356706493831 | 0.60879935656462980 |

| 25 | 0.16000000000000000 | 0.73382714607669872 | 0.50000956018928113 | 0.59742364461027517 |

| 50 | 0.16000000000000000 | 0.73382714607669872 | 0.50000120963128605 | 0.58889316511778638 |

| 75 | 0.16000000000000000 | 0.73382714607669872 | 0.50000035988511168 | 0.58604984904352214 |

| Exact | 0.16 | 0.73382714607669872 | 0.5 | 0.58036339013109773 |

7.3 Perpetual Options

As a more complex application in finance, let us consider the problem of pricing perpetual stock options under the assumption that the stock price at time has the form , where is the price at time and is Lévy process. In [24], Theorem 2, it is shown that the value of a perpetual put option under such a model is given by

| (63) |

where is the interest rate, is the strike price, and . Further, the option is optimally exercised at time

Similar formulas are given for call options and the case where .

If is taken to be a NIG process, then can be computed directly using the the results from this paper (see in particular Corollary 2 as well as (60) and the discussion thereafter). That is, we can calculate the optimal exercise boundary exactly, and the value function can be approximated by

| (64) |

where we have used the fact that has a density of the form .

Consider the parameter set

and observe that the parameters have been chosen such that , or equivalently that is a martingale, i.e. that we are working with a risk neutral martingale measure. Using this parameter set, we calculate for various strikes and values of ; the results are summarized in Table 4. We see that the price converges numerically very rapidly and, in fact, is likely already good enough with .

| 5 | 50 | 100 | 150 | 195 | |

|---|---|---|---|---|---|

| 3 | 95.010756 | 87.212858 | 85.163045 | 83.990865 | 83.242228 |

| 5 | 95.000051 | 87.205429 | 85.158933 | 83.988238 | 83.240350 |

| 7 | 95.000000 | 87.205790 | 85.158900 | 83.988135 | 83.240238 |

| 9 | 95.000000 | 87.205757 | 85.158913 | 83.988149 | 83.240249 |

| 11 | 95.000000 | 87.205763 | 85.158911 | 83.988147 | 83.240248 |

| 75 | 95.000000 | 87.205762 | 85.158911 | 83.988147 | 83.240248 |

Appendix A Solutions of

Recall that the Laplace exponent of an NIG process has the form

| (65) |

where and . In this appendix we prove some basic facts about the solutions of the equation

| (66) |

which together prove the statements of Proposition 1. First, we recall the definitions

such that .

Lemma 3.

Proof.

Rewriting (66) as

| (68) |

where shows that if , then cannot be a solution of (66), since the positive square root function maps to the right half of the complex plane. If, however, does solve (66), then it also solves the associated quadratic equation, which we get by squaring both sides of (68). The solutions of the quadratic equation have the form (67). ∎

Together the requirement that or and will be referred to as Condition A from here on.

Lemma 4.

If satisfies (66), then and .

Proof.

Note that since and we cannot have . For the proof that is real with , we reduce the problem by considering cases for the variables and .

Condition A reduces to equal to one of

| (69) |

and , i.e. the result is immediate.

In this case the formulas for and reduce to

If we assume that , then also . However, under this assumption, the second part of Condition A reduces to

| (70) |

so that we arrive at a contradiction.

and

If we assume that , then from Condition A we must have

| (71) |

From this it follows that we must have . However, rewriting the inequality for as

implies that , which is a contradiction.

and

Proof identical to the case and .

and

We assume again for contradiction that . It is clear that if , then we must also have , otherwise will certainly be greater than zero and the contradiction is immediate. However, if , then

it follows that must be greater than 2. Under this assumption, we rearrange the inequality and the inequality (71) to get

Rewriting the right hand side of the first inequality as

shows that we have once again arrived at a contradiction.

and

Proof identical to the case and .

Finally, to show that we rewrite the equation as

| (72) |

We see that if we had or , then the left hand side of (72) would be a real number, whereas the right hand side of (72) would be purely imaginary number, i.e. the equality would not hold so that could not be a solution of (66). ∎

Lemma 5.

A number satisfies (66) iff , or , and .

Proof.

Lemma 6.

If (resp. ) satisfies (66), then (resp. ).

Proof.

Note that implies that and that

where the latter statement is equivalent to the requirement that . Recall also that if satisfies (66) we must have from Condition A that

| (74) |

Using these statements we consider various cases for and show that the assumption satisfies (66) and leads to a contradiction in each case.

Under the assumptions (74) results in the inequality , which is a contradiction since we have shown that .

and

Similar to the case , we will have strictly positive quantity on the left-hand side of the inequality (74) whereas the right-hand side is at most zero.

and

Since we must have

in order for (74) to hold. However squaring both sides of (74) and solving for yields, after some algebra,

| (75) |

so that we arrive once more at a contraction.

and

We have

| (76) |

which is a contradiction because the left-hand side of the above inequality is a strictly positive number and the right-hand side is at most zero.

and

From (76) we have

but squaring both sides of (74) and solving for yields,

| (77) |

which is a contradiction. Note: To reconcile the formulas in (75) and (77) simply add an subtract on the right-hand side of the first inequality in (75).

The proof for follows from identical arguments.

∎

Lemma 7.

If satisfies (66) and , then is a simple zero of .

Proof.

From their definition (67) and Lemma 4 it is clear that if at least one of or is a solution of (66), then , i.e. has no zeros of multiplicity two when at least one of its zeros is a solution of . Suppose is a zero of multiplicity two of . Then by definition, there is an open ball around and a function analytic on such that and

| (78) |

However, multiplying both sides of (78) by the analytic (on ) function yields

| (79) |

Since is a zero of both and only if or , the preceding shows that can be factored into the product of and the function , which is analytic on and non-zero at . That is, must also be a zero of multiplicity two for , which is a contradiction. ∎

Lemma 8.

If (resp. ) then (resp. ).

Proof.

By definition is a solution of

| (80) |

If and or , then the left-hand side of the above equation, when evaluated at , yields a strictly negative number, and the right-hand evaluated at yields a number that is greater than or equal to zero. That is, does not satisfy (80), i.e. we have arrived at a contradiction. The same exercise can be repeated with and yields the same conclusion. ∎

Lemma 9.

Neither nor is possible.

Proof.

By definition, and are either both real or both have nonzero imaginary part. In the latter case, the result follows immediately. If they are real, it is clear that . Therefore, the assumption that either or contradicts the result of Lemma 8, which stipulates that both and lie in the interval . ∎

Lemma 10.

Both and iff and .

Proof.

() Since both and satifsy the associated quadratic equation , we may plug these values in to get the following system of equations

from which it follows that .

() If then the associated quadratic equation reduces to

from which it is clear that and . ∎

References

- [1] Y. AÏt-Sahalia and J. Jacod. Testing whether jumps have finite or infinite activity. The Annals of Statistics, 39(3):1689–1719, 2011.

- [2] S. Asmussen. Ruin probabilities. World Scientific Publishing Co. Pte. Ltd., Singapore, 2000.

- [3] D.H. Bailey. A fortran-90 based multiprecision system. ACM Transactions on Mathematical Software, 21:379–387, 1995.

- [4] D.H. Bailey. Tanh-sinh high-precision quadrature. \urlhttps://www.davidhbailey.com/dhbpapers/dhb-tanh-sinh.pdf, 2006. Lecture Notes.

- [5] S. G. Baker and P. Graves-Morris. Padé Approximants, volume 1. Cambridge University Press, Cambridge–New York, 2 edition, 1996.

- [6] O.E. Barndorff-Nielsen. Exponentially decreasing distributions for the logarithm of particle size. Proc. Roy. Soc. London A, 353:401–419, 1977.

- [7] O.E. Barndorff-Nielsen. Normal inverse Gaussian distributions and stochastic volatility modelling. Scand. J. Stat., 24:1–13, 1997.

- [8] O.E. Barndorff-Nielsen. Processes of normal inverse Gaussian type. Finance Stochast., 2:41–68, 1998.

- [9] J Bertoin. Lévy Processes. Cambridge University Press, 1996.

- [10] J. Bertoin and R.A. Doney. Cramér’s estimate for lévy processes. Statistics & Probability Letters, 21:363–365, 1994.

- [11] L Bondesson. Generalized gamma convolutions and related classes of distributions and densities. Springer-Verlag, New York, 1992.

- [12] S. Boyarchenko and S.Z. Levendorskiĭ. Non-Gaussian Merton-Black-Scholes Theory. World Scientific Publishing Co. Pte. Ltd., Singapore–River Edge–London, 2002.

- [13] R. Cont and P. Tankov. Financial modeling with jump processes. Chapman & Hall, 2004.

- [14] G. Doetsch. Einführung in Theorie und Anwendung der Laplace-Transformen. Birkhäuser Verlag, Basel, 1970.

- [15] G.B. Folland. Real Analysis: Modern Techniques and Their Applications. John Wiley & Sons, New York, 2 edition, 1999.

- [16] E. Furman, D. Hackmann, and Kuznetsov A. On log-normal convolutions: An analytical-numerical method with applications to economic capital determination. \urlhttp://dx.doi.org/10.2139/ssrn.3034540, 2017. Preprint.

- [17] I. S. Gradshteyn and I. M. Ryzhik. Table of integrals, series, and products. Elsevier/Academic Press, Amsterdam, seventh edition, 2007.

- [18] O. Kudryavtsev and S. Levendorskiĭ. Fast and accurate pricing of barrier options under Lévy processes. Finance Stoch., 13:531–562, 2009.

- [19] A. Kuznetsov. Analytic proof of Pecherskii-Rogozin identity and Wiener-Hopf factorization. Theoty Probab. Appl., 55(3):432–443, 2011.

- [20] A. Kuznetsov. On extrema of stable processes. The Annals of Probability, 39(3):1027–1060, 2011.

- [21] A. Kuznetsov, A.E Kyprianou, and J.C Pardo. Meromorphic Lévy processes and their fluctuation identities. Ann. Appl. Probab., 22(3):1101–1135, 2012.

- [22] A. Kuznetsov and X. Peng. On the wiener-hopf factorization for levy processes with bounded positive jumps. Stochastic Processes and their Applications, 122(7):2610–2638, 2012.

- [23] A.E Kyprianou. Fluctuations of Lévy processes with applications. Springer, second edition, 2014.

- [24] E. Mordecki. Optimal stopping and perpetual options for Lévy processes. Finance and Stochastics, VI(4):473–493, 2002.

- [25] E. Mordecki. Wiener-Hopf factorization for Lévy processes having negative jumps with rational transforms. Journal of Applied Probability, 45(1):118–134, 2008.

- [26] L. C. G. Rogers. Wiener-Hopf factorization of diffusions and Lévy processes. Proceedings of the London Mathematical Society, s3-47(1):177–191, 1983.

- [27] H.L. Royden and P.M. Fitzpatrick. Real Analysis. Prentice Hall, Boston, 4 edition, 2010.

- [28] T.H. Ryberg. The normal inverse Gaussian Lévy process: simulation and approximation. Communications in Statistics. Stochastic Models, 13(4):887–910, 1997.

- [29] R.L. Schilling, R. Song, and Z. Vondracek. Bernstein Functions: Theory and Applications. De Gruyter Studies in Mathematics. De Gruyter, 2012.

- [30] P. Tankov and R. Cont. Financial Modelling with Jump Processes. Chapman and Hall/CRC, Boca Raton–London–New York–Washington,D.C., 2004.