Robust Asset Allocation for Robo-Advisors111The authors are very grateful to Silvia Bocchiotti, Arnaud Gamain, Patrick Herfroy, Matthieu Keip, Didier Maillard, Hassan Malongo, Binh Phung-Que, Christophe Romero and Takaya Sekine for their helpful comments.

Abstract

In the last few years, the financial advisory industry has been impacted by the emergence of digitalization and robo-advisors. This phenomenon affects major financial services, including wealth management, employee savings plans, asset managers, private banks, pension funds, banking services, etc. Since the robo-advisory model is in its early stages, we estimate that robo-advisors will help to manage around $1 trillion of assets in 2020 (OECD, 2017). And this trend is not going to stop with future generations, who will live in a technology-driven and social media-based world.

In the investment industry, robo-advisors face different challenges: client profiling, customization, asset pooling, liability constraints, etc. In its primary sense, robo-advisory is a term for defining automated portfolio management. This includes automated trading and rebalancing, but also automated portfolio allocation. And this last issue is certainly the most important challenge for robo-advisory over the next five years. Today, in many robo-advisors, asset allocation is rather human-based and very far from being computer-based. The reason is that portfolio optimization is a very difficult task, and can lead to optimized mathematical solutions that are not optimal from a financial point of view (Michaud, 1989). The big challenge for robo-advisors is therefore to be able to optimize and rebalance hundreds of optimal portfolios without human intervention.

In this paper, we show that the mean-variance optimization approach is mainly driven by arbitrage factors that are related to the concept of hedging portfolios. This is why regularization and sparsity are necessary to define robust asset allocation. However, this mathematical framework is more complex and requires understanding how norm penalties impacts portfolio optimization. From a numerical point of view, it also requires the implementation of non-traditional algorithms based on ADMM methods and proximal operators.

Keywords: Robo-advisor, asset allocation, active management, portfolio optimization, Black-Litterman model, spectral filtering, machine learning, Tikhonov regularization, mixed penalty, ridge regression, lasso method, sparsity, ADMM algorithm, proximal operator.

JEL classification: C61, C63, G11.

1 Introduction

The concept of portfolio optimization has a long history and dates back to the seminal work of Markowitz (1952). In this paper, Markowitz defined precisely what portfolio selection means: “the investor does (or should) consider expected return a desirable thing and variance of return an undesirable thing”. This was the starting point of mean-variance optimization and portfolio allocation based on quantitative models. In particular, the Markowitz approach became the standard model for strategic asset allocation until the end of the 2000s.

Since the financial crisis of 2008, another model has emerged and is now a very serious contender for asset allocation (Roncalli, 2013). The risk budgeting approach is successfully used for managing multi-asset portfolios, equity risk factors or alternative risk premia. The main difference with mean-variance optimization is the objective function. The Markowitz approach mainly focuses on expected returns and exploits the trade-off between performance and volatility. The risk budgeting approach is based on the risk allocation of the portfolio, and does not take into account expected returns of assets.

The advantage of the risk budgeting approach is that it produces stable and robust portfolios. On the contrary, mean-variance optimization is very sensitive to input parameters. These stability issues make the practice of portfolio optimization less attractive than the theory (Michaud, 1989). Even for strategic asset allocation, many weight constraints need to be introduced in order to regularize the mathematical solution and obtain an acceptable financial solution. In the case of tactical asset allocation, professionals generally prefer to implement the model of Black and Litterman (1991, 1992), because the optimized portfolio depends on the current allocation. Therefore, the Black-Litterman model appears to be slightly more robust than the Markowitz model because having a benchmark or introducing a tracking error constraint is already a form of portfolio regularization. However, since the Black-Litterman model is a slight modification of the Markowitz model, it suffers from the same drawbacks.

Since the 1990s, academics have explored how to robustify portfolio optimization in two different directions. The first one deals with the estimation of the input parameters. For instance, we can use de-noising methods (Laloux et al., 1999) or shrinkage approaches (Ledoit and Wolf, 2004) to reduce estimation errors of the covariance matrix. The second one deals with the objective function. As explained by Roncalli (2013), the Markowitz model is an aggressive model of active management due to the mean-variance objective function. Academics have suggested regularizing the optimization problem by adding penalization functions. For instance, it is common to include a or norm loss function. The advantage of this is to obtain a “sparser” or “smoother” solution.

The success of risk parity, equal risk contribution (ERC) and risk budgeting portfolios has put these new developments in second place. However, the rise of robo-advisors is changing the current trend and highlights the need for active allocation models that are focused on expected returns. Indeed, the challenge of robo-advice concerns tactical asset allocation and not the portfolio construction of strategic asset allocation. Building a defensive, balance or dynamic portfolio profile is not an issue, because they are defined from an ex-ante point of view. Quantitative models can be used to define this step, but they are not necessarily required. For example, this step can also be done using a discretionary approach, since portfolio profiles are revised once and for all. The difficulty lies with the life of the invested portfolio and the dynamic allocation. A robo-advisor that would consist in rebalancing a constant-mix allocation is not a true robo-advisor, since it is reduced to the profiling of clients. The main advantage of robo-advisors is to perform dynamic allocation by including investment views, side assets or the client’s dynamic constraints, or some alpha engines provided by the robo-advisor’s manager or distributor.

The challenge for a robo-advisor is therefore to perform dynamic allocation or tactical asset allocation in a systematic way without human interventions. In this case, expected returns or trading signals must be taken into account. One idea is to consider an extension of the ERC portfolio by using a risk measure that depends on expected returns (Roncalli, 2015). However, this approach is not always suitable when we target a high tracking error. Otherwise, it makes a lot of sense for the mean-variance optimization to be the allocation engine of robo-advisors. As said previously, the challenge is to develop a robust asset allocation model. The purpose of this research is to provide a practical solution that does not require human interventions.

This paper is organized as follows. Section Two illustrates the practice of mean-variance optimization and highlights the limits of such models. In Section Three, we apply the theory of regularization to asset allocation. In particular, we point out the calibration procedure of the Lagrange coefficients of norm functions. In Section Four, we consider application to robo-advisory. Finally, Section Five offers some concluding remarks.

2 Practice and limits of mean-variance optimization

2.1 The mean-variance optimization framework

We follow the presentation of Roncalli (2013). We consider a universe of assets. Let be the vector of weights in the portfolio. We denote by and the vector of expected returns and the covariance matrix of asset returns. It follows that the expected return and the volatility of the portfolio are equal to and . The Markowitz approach consists in maximizing the expected return of the portfolio under a volatility constraint (-problem):

| (1) |

or minimizing the volatility of the portfolio under a return constraint (-problem):

| (2) |

Replacing the volatility by the variance scaled with the factor does not change the solution. Therefore, we deduce that the Lagrange functions associated with Problems (1) and (2) are:

and:

They satisfy where is the risk aversion of the quadratic utility function. As strong duality holds, these two problems are equivalent. Moreover, we can show that they can be written as a standard quadratic programming problem (Markowitz, 1956):

| (3) |

where is the risk/return trade-off parameter. Since the problem is strongly convex and the solution is , we deduce that the solution of the -problem is given by:

whereas the solution of the -problem is obtained for the following value of :

The previous framework can be extended by considering a risk-free asset and portfolio constraints:

| s.t. |

where is the risk-free rate and is the set of restrictions. Let and be the bounds of the expected return and the volatility such that . It follows that there is a solution to the -problem and the -problem if and .

Remark 1

The Sharpe ratio is the standard risk/return measure used in finance, and corresponds to the zero-homogeneous quantity:

The capital asset pricing model (CAPM) defines the tangency portfolio as the optimized portfolio that has the maximum Sharpe ratio. When the capital budget is reached (meaning that ), the solution of Problem (2.1) is equal to where . Since the matrix has a unique symmetric positive definite square root denoted by , the Cauchy-Schwarz inequality yields:

The equality holds if and only if there exists a scalar such that . It follows that:

| (5) |

We deduce that the set of portfolios maximizing the Sharpe ratio is the one-dimensional vector space defined by . This means that unconstrained and constrained portfolio optimizations are related when we impose only one simple constraint like the capital budget restriction. In more complex cases, the constrained solution is not necessarily related to the unconstrained solution. However, the bound remains valid, because it only depends on the Cauchy-Schwarz inequality.

The previous result highlights the importance of constraints in portfolio optimization. A portfolio is long-only if whereas it is long-short if such that and . For long-only portfolios, a capital budget is usually assumed, meaning that the portfolio is fully invested (). For long-short portfolios, professionals sometimes impose a neutral or zero-capital budget, implying that the long exposure is financed by the short exposure (). They can also impose leverage constraints (), while risk-budgeting portfolios require adding a logarithmic barrier constraint ().

In practice, the quantities and are unknown and must be specified. We can assume that they are estimated using an historical sample where is the vector of asset returns at time . Let and be the corresponding estimators. We have:

and:

where is the weighting scheme such that . In Appendix A.2 on page A.2, we show that Problem (2.1) can be written as follows222The norm is equal to . All the notations are defined in Appendix A.1 on page A.1.:

| s.t. |

where , and . In this case, the Markowitz solution is the portfolio that maximizes the backtest for a given volatility. When , we conclude that Problem (2.1) is a trend-following optimization program, whose moving average is defined by the weighting scheme . In order not to be trend-following, we have to use a vector of expected returns that does not satisfy or that does not depend on the sample of asset returns.

2.2 Stability issues

According to Hadamard (1902), a well-posed problem must satisfy three properties:

-

1.

a solution exists;

-

2.

the solution is unique;

-

3.

the solution’s behavior changes continuously with the initial conditions.

We recall that the solution to Problem (3) is . If has no zero eigenvalues, it follows that the existence and uniqueness is ensured, but not necessarily the stability. Indeed, this third property implies that has no “small” eigenvalues. This problem is extensively illustrated by Bruder et al. (2013) and Roncalli (2013). If we consider the eigendecomposition , we have and . It follows that or:

| (7) |

where and . By applying the change of basis , we notice that the Markowitz solution is proportional to the vector of return and inversely proportional to the eigenvectors. We conclude that the mean-variance optimization problem mainly focuses on the small eigenvalues. This is why the stability property is lacking in the original portfolio optimization problem.

Let us consider an example to illustrate this problem. The investment universe is composed of 4 assets. The expected returns are equal to , , and whereas the volatilities are equal to , , and . The correlation matrix is the following:

The portfolio manager’s objective is to maximize the expected return for a volatility target and a full investment333We only impose that the sum of the weights is equal to .. The optimal portfolio is . In Table 1, we indicate how this solution differs when we slightly change the value of input parameters. For example, if the volatility of the third asset is equal to , the weight of the third asset becomes instead of . In real life, we know exactly the true parameters. For instance, there is a low probability that the realized correlation matrix is exactly the one specified above. If we consider a uniform correlation matrix of , we observe significant differences in terms of allocation.

We have seen that the lack of stability is due to the small eigenvalues of the covariance matrix. More specifically, we notice that the important quantity in mean-variance optimization is not the covariance matrix itself, but the precision matrix, which is the inverse of the covariance matrix. In Tables 2 and 3, we have reported the eigendecomposition of and . We verify that the eigenvectors of the precision matrix are the same as those of the covariance matrix, but the eigenvalues of the precision matrix are the inverse of the eigenvalues of the covariance matrix.

| Factor | 1 | 2 | 3 | 4 | |

|---|---|---|---|---|---|

| Asset | |||||

| Eigenvalue | |||||

| cumulated | |||||

| Factor | 1 | 2 | 3 | 4 | |

|---|---|---|---|---|---|

| Asset | |||||

| Eigenvalue | |||||

| cumulated | |||||

This means that the risk factors are the same, but they are in reverse order. We see that the most important risk factor for portfolio optimization is a long/short portfolio, which is short on the first asset and long on the other assets. The second most important risk factor is another long/short portfolio, which is short on the second asset and long on the third asset444On Page 23, we have reported the representation quality and the contribution of each variable for the PCA factors of . Since the second risk factor of is the third risk factor of , we deduce that the first and fourth assets have a very small contribution (respectively and ).. Any changes in the covariance matrix then impacts the largest eigenvalues of and the long/short risk factors.

2.3 Which risk factors are important?

The previous eigendecomposition analysis is the traditional way to illustrate the stability issue (Roncalli, 2017). However, the corresponding arbitrage factors are difficult to interpret and, moreover, they do not fully help understand the Markowitz machinery, in particular how mean-variance portfolios are built. In this section, we use the method developed by Stevens (1998) in order to better characterize the underlying mechanism.

We have seen that the solution is . If we assume that asset returns are independent – , we obtain the famous result:

The optimal weights are proportional to expected returns and inversely proportional to variances of asset returns. In the general case – , Stevens (1998) shows that the optimal portfolio is connected to the linear regression555This means that: :

| (8) |

where denotes the vector of asset returns excluding the asset. By noting the coefficient of determination and the variance of , we have:

and:

We deduce that:

where is the vector of expected returns excluding the asset. Since we have666See Appendix A.3 on page A.3. and , we obtain:

In the general case, the optimal weights are proportional to idiosyncratic returns and inversely proportional to idiosyncratic variances .

We notice that represents the best portfolio for replicating the returns of Asset . This is why it is called the hedging (or tracking) portfolio of Asset . The idiosyncratic return is the difference between the expected return of Asset and the expected return of its hedging portfolio. The idiosyncratic volatility is the standard deviation of residuals . It is also equal to the volatility of the tracking errors where is the return of the hedging portfolio. The hedging portfolio concept is at the core of the Markowitz optimization. Indeed, the Markowitz framework consists in estimating the hedging strategy for each asset, and in forming two portfolios:

-

1.

the first portfolio is the optimal portfolio of assets assuming that assets are not correlated:

-

2.

the second portfolio is the optimal portfolio of the hedging strategies:777Because the hedging strategies are independent and we have .:

We deduce that:

where:

To take into account the correlation diversification, the optimal portfolio adds to the portfolio a long/short exposure between and with a leverage that depends on the quality of the hedge.

Let us consider the previous example. In Table 6, we have reported the linear regressions between the four assets, which are the hedging portfolios of each asset. We observe that the coefficient of determination lies between and . is the highest for the first asset, because it exhibits the largest cross-correlations. Therefore, it is the lowest contributor to the diversification whereas the third asset is the highest contributor to the diversification.

| Asset | ||||||

|---|---|---|---|---|---|---|

| 1 | ||||||

| 2 | ||||||

| 3 | ||||||

| 4 | ||||||

| Asset | |||||||

|---|---|---|---|---|---|---|---|

| 1 | |||||||

| 2 | |||||||

| 3 | |||||||

| 4 |

| Asset | ||||

|---|---|---|---|---|

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 |

We then calculate the risk/return statistics of hedging portfolios in Table 6. We verify that the following equalities hold888We have: and: : and . Finally, we obtain the optimal portfolio given in Table 6. is set to in order to obtain a exposure. In this example, the optimal portfolio is: , , and . There is no short position, because the alpha is positive for all the assets, meaning that hedging portfolios are not able to produce a better expected return than the corresponding assets.

We now modify the correlation between the third and fourth assets, and set . This high correlation changes the results of the linear regression (see Tables 9 and 9). Indeed, the coefficient of determination for Assets and is larger than , and the fourth hedging portfolio has an expected return that is higher than that of the fourth asset. Since is the only negative alpha, the optimal portfolio is short on the fourth asset and long on the other assets (see Table 9). Another important factor is the impact of on the weights . Thus, and are larger than whereas and are smaller than . Even if the difference between and is the smallest for Assets 3 and 4, the leverage effect largely compensates the long/short effect, and explains why the optimal portfolio has a large exposure on Assets 3 and 4.

| Asset | ||||||

|---|---|---|---|---|---|---|

| 1 | ||||||

| 2 | ||||||

| 3 | ||||||

| 4 | ||||||

| Asset | |||||||

|---|---|---|---|---|---|---|---|

| 1 | |||||||

| 2 | |||||||

| 3 | |||||||

| 4 |

| Asset | ||||

|---|---|---|---|---|

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 |

The theoretical analysis presented in this paragraph also highlights the importance of the expected returns. Indeed, even if they do not change the composition and the risk analysis of hedging portfolios, they impact the return analysis. An example is provided in Appendix C.1 on page 23. We change the expected return of the first asset and set . In this case, the expected return of the first asset is largely smaller than the expected return of the corresponding hedging portfolio. At the same time, the alpha of the other three assets increases sharply. This is why Markowitz optimization increases the allocation in the third asset and takes a short position on the first asset.

Let us write Equation (8) as follows:

where the coefficients only depend on the correlation matrix . We have the following correspondence:

and:

Moreover, we notice that:

and:

where is the correlation matrix excluding the asset. We obtain the following effects:

-

•

A change in the expected return impacts the alpha of the hedging portfolios. It does not change the composition of hedging portfolios or the weights ;

-

•

A change in the volatility impacts the exposures of the hedging portfolios. It does not change the weights , but modifies the value of alphas. As such, the composition of the portfolio changes;

-

•

A change in the correlation impacts all the parameters (, and ).

We also notice that the correlations are the only parameters that are used for calculating the coefficient of determination . Therefore, correlations are the key parameters for understanding the leverage effects in the Markowitz model. Indeed, they impact both the tracking error volatilities and the weights . The main effect of the volatility concerns the tracking error, because is an increasing function of . A high volatility therefore negatively impacts the allocation and .

3 Theory of regularization

The stability issue has been considered by Michaud (1989) in a very famous publication “The Makowitz Optimization Enigma: Is Optimized Optimal?”. In his works, Michaud clearly makes the distinction between mathematical optimization and financial optimality. For instance, if we consider two assets that are highly similar in terms of risk and return, a fund manager will most likely spread a long exposure into these two assets, whereas Markowitz will play an arbitrage between them. Academics have proposed several approaches to make Markowitz’s solutions more robust. Two main directions have been explored. The first one concerns the regularization of the covariance matrix. As seen in Equation (7), the problem is ill-conditioned because of the magnitude of eigenvectors. One solution is therefore to change the eigenvalues of . For instance, the direct approach consists in deleting the lowest eigenvalues (Laloux et al., 1999). The indirect approach mixes different covariance matrices in order to obtain a more robust estimator, and is called the shrinkage method (Ledoit and Wolf, 2003). The second direction concerns the regularization of the optimization problem (e.g. adding penalty) or the sparsity of the solution (e.g. adding penalty). The simplest way is to add some weight constraints. For instance, we can impose that the sum of weights is equal to one, the weights are positive, etc. Another approach consists in modifying the objective function by adding some penalties, such as ridge or lasso norms.

3.1 Adding constraints

Let us specify the Markowitz problem in the following way:

| s.t. |

where is the set of weight constraints. This is a variant of the -problem (2) described on page 2. We consider two optimized portfolios:

-

•

The first one is the unconstrained portfolio with .

-

•

The second one is the constrained portfolio with some constraints added.

Jagannathan and Ma (2003) assume that the weight of asset is between a lower bound and an upper bound :

They show that the constrained optimal portfolio is the solution of the unconstrained problem:

with:

where and are the Lagrange coefficients vectors associated with the lower and upper bounds. Introducing weight constraints is then equivalent to using another covariance matrix , or shrinking the covariance matrix. More generally, if we introduce linear inequality constraints:

we obtain a similar result. The covariance matrix is shrunk as follows999The shrinkage covariance matrix is not necessarily positive definite (Roncalli, 2013).:

where is the vector of Lagrange coefficients associated with the constraints .

We again consider the previous example given on page 2.2. If we compute the global minimum variable, the solution is equal to , , and . Let us suppose that the portfolio manager is not satisfied with this optimized portfolio and decides to impose some constraints. For instance, he could decide that the portfolio must contain at least of all assets. In order to achieve a certain degree of diversification, he could also decide to impose an upper bound of . With these constraints and , the solution becomes , , and . Thanks to the Jagannathan-Ma framework, we can compute the shrinkage covariance matrix101010We have bps and bps. The other Lagrange coefficients are equal to zero., and deduce the shrinkage volatilities and correlation matrix , which are reported in Table 10. To obtain this new solution, one must increase (implicitly) the volatility of the first asset, and decrease (implicitly) the volatility of the fourth asset. Concerning the correlations, we also notice that they have changed. In Table 11, we report the results when the objective function is to target an expected return of . In this case, we notice that introducing constraints is equivalent to introducing some views on the first asset. Indeed, this allows us to impose a better Sharpe ratio and a lower correlation with the second asset.

| Asset | |||||||

|---|---|---|---|---|---|---|---|

| 1 | |||||||

| 2 | |||||||

| 3 | |||||||

| 4 | |||||||

| Asset | |||||||

|---|---|---|---|---|---|---|---|

| 1 | |||||||

| 2 | |||||||

| 3 | |||||||

| 4 | |||||||

Remark 2

Constraints are inherent to Markowitz optimization. Indeed, the raw solution given by the mean-variance optimization is generally not satisfied. This is why Quants spend a lot of time adding and testing constraints. This is particular true for strategic asset allocation, for which the annual exercises are very time-consuming. However, adding constraints introduces the personal views of the Quant in charge of the optimization. Moreover, this process of trial and error must be repeated each time the allocation problem changes. Therefore, Markowitz optimization is more a handmade solution, and not an industrial solution. This is why it cannot be used “as is” by robo-advisors, whose mass production/customization approach is incompatible with human intervention.

3.2 Adding a benchmark

Let us now consider a benchmark which is represented by a portfolio . The tracking error between the portfolio and its benchmark is the difference between the return of the portfolio and the return of the benchmark:

where is the vector of asset returns. The expected excess return is:

whereas the volatility of the tracking error is:

The investor’s objective is to maximize the expected tracking error with a constraint on the tracking error volatility. Like the Markowitz problem, we transform this -problem into a -problem:

| s.t. |

The objective function is then:

We deduce that:

| s.t. |

where . Let be the vector of implied expected returns such that the benchmark is the optimal portfolio. Since we have , the optimization problem becomes:

| s.t. |

where . Introducing a benchmark constraint is then equivalent to regularizing the expected returns.

3.3 Tikhonov and ridge regularization

Previously, we have seen a method that regularizes the covariance matrix and an approach that regularizes the vector of expected returns. We now turn to a framework that regularizes the two input parameters of Markowitz optimization problems, and not only the covariance matrix or the vector of expected returns. While the two previous approaches are more specific to financial optimization, the following methods have been developed in PDEs and later in statistics. This is why we consider the following general optimization problem:

| (10) | |||||

| s.t. | (13) |

We recognize a standard quadratic programming problem. Problems (1) – (2.1) can easily be written as Problem (10). For instance, the -problem (3) is obtained with and , while we have , and for the -problem. If we prefer to use the empirical model (2.1), we specify and . We notice that the norm is natural because of the specification of .

3.3.1 Formulation of the Tikhonov problem

In order to regularize the Markowitz optimization problem, we can add a penalty term. For instance, the most famous approach is the Tikhonov regularization. The general problem can be written as follows:

| s.t. |

where is a positive number, , and . The vector is an initial solution. The Tikhonov regularization matrix forces the solution to be close to with respect to the semi-norm whereas the Tikhonov regularization parameter indicates the strength of the regularization.

Remark 3

In portfolio optimization, can be seen as a reference portfolio. For instance, it can be a benchmark, an heuristic portfolio111111For instance, it can be the equally-weighted (EW) portfolio or the equal risk contribution (ERC) portfolio (Roncalli, 2013). or the investment portfolio of the previous period. The penalty term may then be used to control the deviation between the new portfolio and the reference portfolio, the tracking error or the portfolio turnover.

Remark 4

The previous approach was introduced in asset management by Jorion (1988, 1992), who considered the Bayes-Stein estimator based on the one-factor model developed by Sharpe (1963). With the notations above, we have the following correspondence: and .

In Appendix A.4 on page A.4, we show that the optimal solution is the -coordinate of the linear system solution121212We obtain a linear system of the form where is a symmetric block matrix. The (1,1) block depends on the matrix while the (2,1) block depends on the matrix .:

| (15) |

where is the vector of Lagrange coefficients associated with the constraint . The OLS regression corresponds to whereas the ridge regression is obtained with . For and , the OLS solution is simply where is the Moore-Penrose pseudo-inverse matrix of . For and , the regularized solution becomes where may be interpreted as the Tikhonov regularization of :

We also notice that is invertible if the matrix is invertible. Indeed, if , we have:

This ensures the property that the matrix is positive definite. This idea can be extended using spectral decomposition of , which naturally leads to defining the regularization of the matrix through spectral filters.

3.3.2 Relationship with covariance shrinkage methods

Let us consider the regularized Markowitz problem:

where is the regularization function. If we consider the Tikhonov formulation (3.3.1), we have the following correspondence: and . We deduce that the regularization on the matrix can be written as a regularization on the covariance matrix when there is no target portfolio ():

Therefore, there is a strong relationship between regularization and shrinkage. Indeed, the empirical covariance matrix is an unbiased estimator of , but its convergence is very slow in particular when is large. We know also that the estimator based on factor models converges more quickly, but it is biased. Ledoit and Wolf (2003) propose combining the two estimators and in order to obtain a more efficient estimator. Let be this new estimator. Ledoit and Wolf estimate the optimal value of by minimizing the expected value of the quadratic loss:

where the loss function is equal to:

We have, up to a scaling factor131313This is not an issue since is not a fixed parameter, but is calibrated to solve a -problem or a -problem., the following correspondence:

where is the upper Cholesky factor of the matrix . Therefore, the Ledoit-Wolf shrinkage technique is a special case of Tikhonov regularization. In a similar way, the double shrinkage method proposed by Candelon et al. (2012) is obtained by setting and .

3.3.3 Ridge regularization

The ridge regularization is defined by . We deduce that the mean-variance objective function becomes:

where and . Let be the unconstrained solution of the ridge optimization problem:

We have:

where is the Markowitz solution. We deduce that the regularized solution is the average of two portfolios: the Markowitz portfolio and the optimal portfolio when the vector of expected returns is equal to and the risk/return trade-off parameter is . Bruder et al. (2013) also show that:

where the matrix of weights is equal to . We verify that:

Without any constraints, the ridge regularization reduces the leverage of Markowitz portfolio when there is no target portfolio. When we impose that the portfolio is fully invested (), this is equivalent imposing that the target portfolio is the equally-weighted portfolio.

We consider an example where the investment universe is composed of 4 assets. The expected returns are equal to , , and whereas the volatilities are equal to , , and . The correlation matrix is the following:

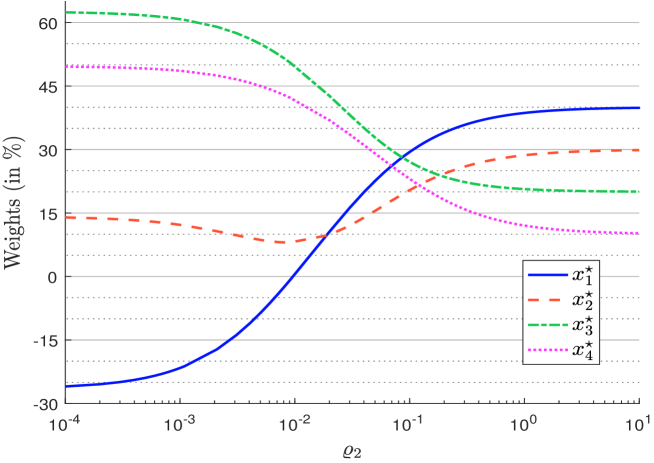

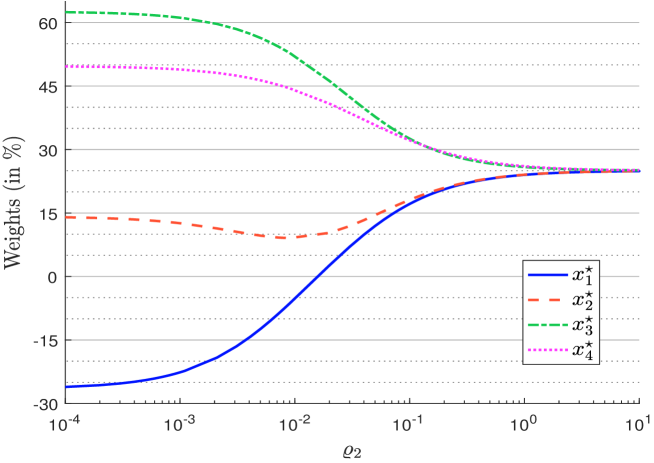

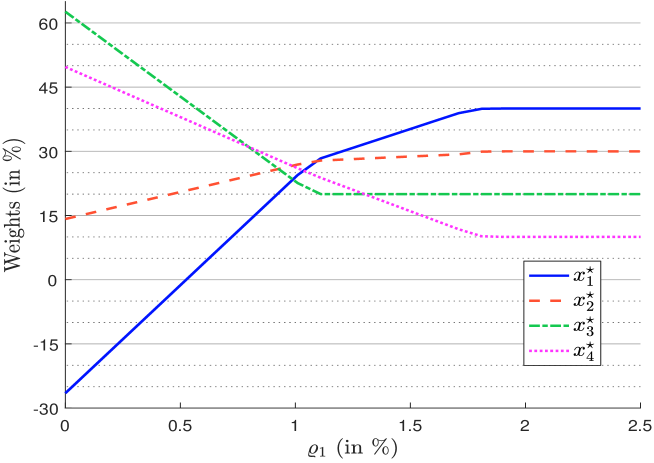

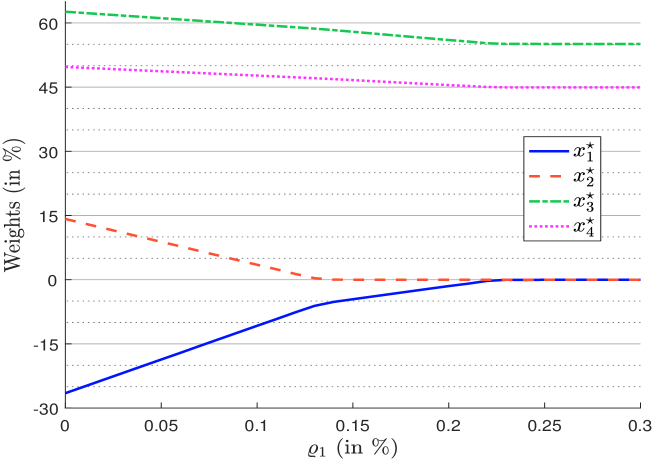

We assume that and the portfolio is fully invested. We impose that the target portfolio is equal to . Figure 1 show the optimal weights with respect to the penalization factor . We verify that the optimized portfolio converges to the target portfolio when increases. When there is no target portfolio, it converges to the equally-weighted portfolio (see Figure 2). This result is due to the capital budget constraint. Indeed, if we do not impose the constraint , the ridge portfolio converges to the zero solution . We also notice that the paths of weights are not necessarily monotonous (increasing or decreasing). For instance, the weight of the second asset decreases when is small and increases when is large.

We notice that the ridge regularization impacts entirely the covariance matrix. Indeed, the shrinkage volatilities are equal to whereas the shrinkage correlation matrix is defined by:

It follows that . Since the volatilities tend to , the ridge regularization can be viewed as a shrinkage covariance method between the input covariance matrix and the identity matrix:

Remark 5

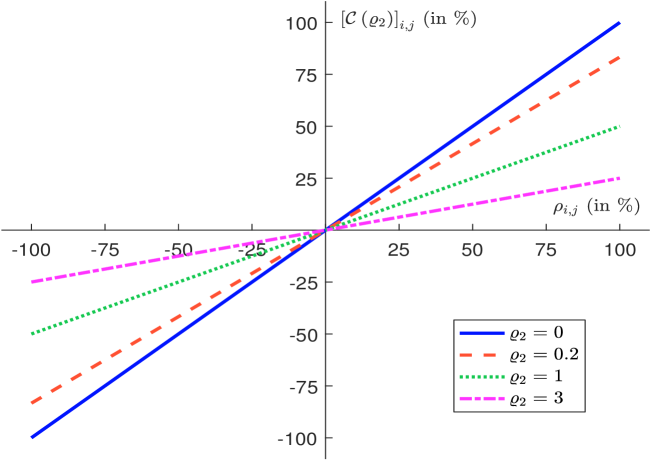

A variant of the ridge regularization is to define as a diagonal matrix. For instance, if , the regularized correlation matrix satisfies:

In Figure 3, we have reported the impact of the parameter on the correlation values.

3.4 Spectral filtering

Spectral filtering is a general approach based on the singular value decomposition (SVD) of the matrix . Ridge regularization and denoising techniques can be seen as special cases of the SVD method.

3.4.1 General filters

We consider the SVD decomposition of the matrix by assuming that :

where the matrices141414In the case of the empirical model, we have . , , and satisfy and . The Moore-Penrose pseudo-inverse of can be defined as:

where . Let us denote the largest singular value of .

As instability is raised by small eigenvalues, filtering can be applied to keep eigenvalues away from . A filter is a vector-valued function, where the entry satisfies:

for all and . The parameter controls the magnitude of the regularization of :

As a consequence, we verify the property of convergence:

This method can be extended to regularize the matrix . On one hand, if has full rank, we can approximate by . On the other hand, a direct computation leads to . Therefore, we can regularize by:

where is a vector that may be equal to , or or . Once again, we have the convergence property:

If we consider the problem:

| s.t. |

the normal equations are:

| (16) |

Spectral filtering is then equivalent to replacing the linear system (16) by the following set of normal equations:

| (17) |

3.4.2 Application to Tikhonov regularization

To define the spectral regularization of the Tikhonov problem, the matrices and have to be able to be factored in a coherent way:

and:

Direct computations gives:

We deduce that the entry of the spectral filter is defined by:

Using the previous notations, we have:

where . In this case, the optimal portfolio is the -coordinate of the solution to the linear system:

| (18) |

We notice that only the right singular vectors appear in Equation (18). Ridge regularization can be viewed as particular filters151515For , we have . For (ridge regularization), the entry of the spectral filter is defined by: . More generally, when and have the same right singular vectors, Tikhonov regularization can be stated in terms of a filter.

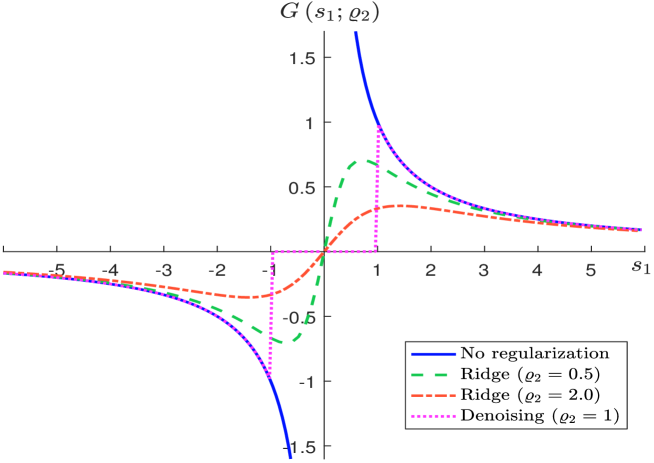

In Figure 4, we report the spectral filter of the ridge regularization. The spectral filtering approach includes another popular method, which is the denoising method (Laloux et al., 1999):

We notice that deleting singular values is equivalent to applying a hard thresholding method while ridge regularization is a smoothing approach.

3.4.3 Improvement of the stability condition

The condition number of the matrix summarizes the level of difficulty when performing the optimization in a stable way. More specifically, it measures how much an error on the vector changes the solution of the linear equation . We have:

It follows that , and we have the property . When is low, the problem is numerically stable and easy to solve. The closer to one, the better the stability.

With the norm, we obtain:

| (19) |

where the ’s are the singular values of . Using the filter , we obtain:

| (20) |

For a fixed value of , all previous filters satisfy the two following properties:

-

1.

for ;

-

2.

is bounded from above on .

As a consequence, if we compare Equations (19) and (20), the denominator is essentially unchanged while the numerator is decreased161616From an unbounded function to a bounded function.. Therefore, spectral filtering decreases the condition number of , because these techniques reduce the dispersion of singular values.

3.5 Mixed penalties

The Euclidian regularization is natural because the norm appears in Problem (3). Explicit formulas are obtained, and can be implemented at once. Other regularization techniques have been introduced to impose other constraints on the optimal solution . As the unit ball for the norm is not uniformly convex, sparse solutions may be obtained by penalizing with instead of .

3.5.1 regularization

Instead of Tikhonov regularization, one may consider the regularization:

| s.t. |

where is a targeted portfolio and .

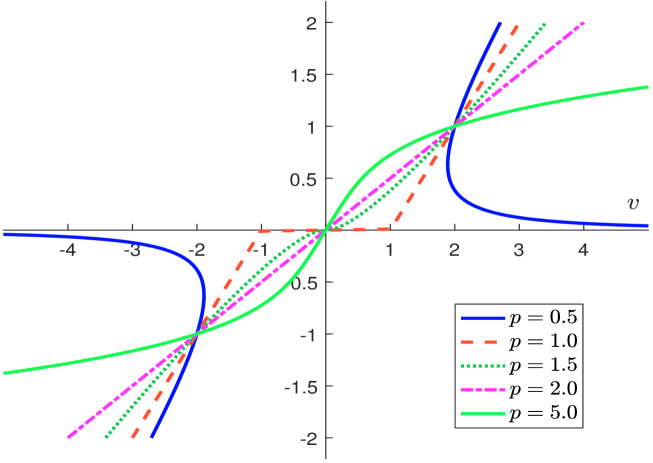

For , the function is strictly convex and its gradient is Lipschitz continuous. Indeed, the gradient is equal , where the functions and are taken component wise. For , the function is convex, lower semi-continuous but may not be differentiable at . An explicit expression for its subgradient can be formulated in terms of proximal operators. For , the function is not convex, and Problem (3.5.1) is not convex.

The penalties for are used for regularization, while the penalties for are used for sparsity. The case is the most interesting since it corresponds to the lasso regression (Tibshirani, 1996). In this case, a large value of associated with the constraint forces the optimal portfolio to have long-only positions (Brodie et al., 2009).

We consider the example given on page 3.3.3. We use a (or lasso) penalty with . Figure 5 show the optimal weights with respect to the penalization factor . Like in the ridge approach, the optimized portfolio converges to the optimal portfolio when the parameter increases. When there is no target portfolio, we observe a divergence of the limit portfolio between ridge and lasso approaches. While the ridge portfolio converges to the equally-weighted portfolio, the lasso portfolio converges to the long-only mean-variance optimized portfolio (Figure 6). If we compare Figures 1 and 5, we notice that the magnitude of the regularization factor is not the same. We also observe that the paths are different. The path is smoothed and continuous for the ridge approach, while it is more a piecewise linear function for the lasso approach. We verify that the penalty produces a sparse optimized portfolio. This is obvious for the case where there is no target portfolio since weights may be equal to zero. When there is a target portfolio, the sparsity concerns the bets between the optimized portfolio and the target portfolio . In this case, relative (and not absolute) weights are equal to zero. Another difference between the two approaches is that the lasso method produces a monotonic path (decreasing or increasing) contrary to the ridge method.

3.5.2 regularization

We can also consider a mixed penalty:

| s.t. |

where . In the case , we obtain:

| s.t. |

This regularization is called elastic net (Hastie et al., 2009). This is the most common mixed penalty used in portfolio optimization (Roncalli, 2013).

We consider again the example given on page 3.3.3. We use a lasso-ridge penalty with . Results are reported in Figures 7 and 8. We notice a large difference concerning the convergence. Indeed, we recall that the lasso and ridge approaches converge to the same portfolio when we impose a target portfolio, but to two different portfolios when there is no target portfolio. When mixing the two norms, the limit portfolio is generally the ridge portfolio, because of the magnitude of and in portfolio management (see Appendix A.5 on page A.5). This result is true because we have imposed .

3.5.3 Solving the mixed penalty problem

Problems (3.5.2) and (3.5.2) are more complex to solve than a traditional quadratic programming problem. In the case of the regularization problem and if we assume that is a matrix with non-negative entries171717Which is generally the case (Bruder et al., 2013; Roncalli, 2013)., we can use a modified QP solver. The underlying idea is to write in the following way:

where and . Therefore we obtain a standard QP problem by augmenting the vector of unknown variables181818See Appendix A.6 on page A.6 for a comprehensive presentation.. Thus, the optimization is performed with respect to and no longer with respect to . In the other cases, when we consider an penalty with or when is a matrix with some negative entries, the general approach is to use the ADMM algorithm, which is described in Appendix A.7 on page A.7. For instance, Problem (3.5.2) can be written as:

| s.t. |

where:

and:

where . The interest of this choice is that the -step includes the constraint and can be explicitly computed191919We have , while the -step requires to compute the proximal operator of the function :

The update of the scaled dual variable is:

The previous results can be extended when and is a set of more complex constraints.

3.6 Optimal choice of the regularization factor

To choose the optimal regularization parameter, we first have to define an optimization criterion. For instance, the optimal value of or is generally obtained by cross-validation techniques. Exhaustive methods such as leave--out cross-validation (LpOCV) or leave-one-out cross-validation (LOOCV) are computationally intensive. This is why it may be better to use non-exhaustive methods such as -fold cross-validation or out-of-sample testing. However, in the case of the Tikhonov regularization, an explicit formula is known. Indeed, the generalized cross-validation procedure for choosing does not depend on the dual variable or the constraints. In the case of the penalty, no explicit formula is known and the brute force algorithm must be used for finding the optimal value of .

3.6.1 Cross-validation and the PRESS statistic

Let us consider the data matrix where , and a response vector where . Since the Tikhonov regularization problem is defined as follows:

we have:

where:

It follows that is a function of . Therefore, the underlying idea is to find the optimal value .

In order to accurately estimate the hyperparameters of the model and to avoid overfitting problems, the cross-validation (CV) method comprises several steps:

-

1.

the sample of data is partitioned into two sets, the training set and the test (or validation) set;

-

2.

the model is fitted on the training set;

-

3.

the model is tested on the validation set.

In order to reduce variability, steps 2 and 3 are performed using different partitions of the data sample (step 1). The validation results are combined, according to a measure of fit, to give an estimate of the model predictive performance. The hyperparameters are then chosen in order to maximize this goodness-of-fit measure. Two types of CV may be performed: exhaustive and non-exhaustive cross-validation. For the first type, the model is estimated and tested on all possible ways to divide the original sample into training/test sets. This type of CV consists of the leave--out cross validation (LpOCV). In this approach, observations are used in the test set and the remaining observations are used in the training set202020The leave-one-out cross validation (LOOCV) procedure corresponds to the special case .. This requires training and validating the model times, which can be extremely expensive if is large, even for . Nevertheless, an explicit expression for the sum of squares of the errors is known in the case of Tikhonov regression. This formula may lead to operations. For this reason, non-exhaustive cross-validation may be preferred in practice, such as -fold CV, holdout method, repeated random sub-sampling, jackknife, etc. Performing -fold CV is the most popular tool for model selection (Stone, 1974; Wahba, 1977; Stone, 1978).

In -fold CV, the sample of data is randomly shuffled and split into (almost) equally sized groups, the model is fitted using all but the group of data, and the group of data is used for the test set. We repeat the procedure times, in such a way that each group is tested exactly once. The -fold cross validated error is generally computed as:

where denotes the observations of the group and the estimation of obtained by leaving out the group. Even in simple cases, it cannot be guaranteed that the function has a unique minimum. The simple grid search approach is probably the best approach. The exhaustive Leave-one-out cross validation (LOOCV) is a particular case when is equal to the size of the dataset. The LOOCV is asymptotically equivalent to Akaike Information Criterion (AIC), which is commonly used in statistics (Stone, 1977). Interestingly, For Tikhonov regression, the cross validated error has an explicit expression known as the Predicted Sum of Squares (or PRESS) statistic (Allen, 1971 & 1974).

We note and the vector and matrix by leaving out the observation to the vector and the matrix . We have:

The explicit expression for the LOOCV procedure is212121Proof is given in Appendix A.9 on page A.9.:

where is the projection matrix defined as:

If is a band matrix, which is the case for spline models, the coefficients and can be computed in operations thanks to the Hutchinson-De Hoog algorithm (Hutchinson and De Hoog, 1985).

3.6.2 GCV for centered data as the selection criterion

The generalized cross-validation (GCV) method is a rotation-invariant version of LOOCV (Craven and Wahba, 1978). Even if it is not its main purpose, this approach replaces the factor by the average value :

| (24) |

We deduce that the GCV criterion depends on and the residual sum of squares . We recall that is the hat matrix. The value is called the leverage value (Craven and Wahba, 1978) and determines the amount by which the predicted value is influenced by . We also know that . From the Woodbury formula, we have222222The Woodbury matrix identity is: :

Let be the eigenvalues232323Computing the eigenvalues of can be done in operations. of the symmetric real matrix . We have:

This formula allows the value of to be computed for every value of . Like the PRESS statistic, the optimal value of is obtained by minimizing the GCV function given by Equation (24).

4 Application to robo-advisory

The previous techniques are of particular interest for portfolio optimization when building a strategic asset allocation (SAA), a trend-following strategy or more generally a mean-variance diversified portfolio. Depending on the approach, they can diversify or concentrate the portfolio. By mixing the different approaches, we can also obtain a diversified allocation on some selected stocks. In this case, portfolio regularization and portfolio sparsity are combined. The previous techniques can also be used when implementing tactical asset allocation (TAA). In this case, regularization and sparsity are imposed in a relative way with respect to a benchmark or a current investment portfolio. In this section, we show why these techniques are necessary when building a robo-advisor based on an automated allocation engine.

4.1 Robo-advisory and the secret sauce of portfolio optimization

The idea that portfolio optimization is a simple mathematical problem is mistaken. It is a process that requires manual interventions and may take considerable time before a solution is found. And this human intervention has little in common with numerical algorithms. Indeed, Quants know that the secret sauce of portfolio optimization lies in the alchemy of defining the right constraints in order to obtain an acceptable solution that makes sense. Let us consider the traditional strategic asset allocation exercise that is performed by institutional investors almost every year. We assume that the SAA team has already produced the two inputs: the vector of expected returns and the covariance of asset returns. We could think that the hard work has therefore been done, and that computing the SAA portfolio will take a matter of seconds since we just have to run a Markowitz optimization. In reality, solving one Markowitz optimization generally produces a bad solution and is not sufficient. This is why Quants will use an iterative process based on this optimization program:

| (25) | |||||

| s.t. | (29) |

where and is the step. They will begin by solving the traditional Markowitz problem with long-only constraints and will find an initial solution . Then, they will analyze this solution and define a new set of constraints that might produce a more acceptable solution. The concept of “acceptable solution” remains unclear, but it means one that can be accepted by the chief investment officer. Once is defined, Quants will run the optimization problem (25) and obtain a new solution . Next, they will analyze this new solution and define a new set of constraints that might produce an even more acceptable solution. They will iterate this process a number of times. Therefore, this iterative process can be represented by the sequence defined as follows:

Using this tool, we can evaluate Quants and draw some conclusions:

-

•

A good Quant is a person that is able to “close” this sequence in a limited number of steps.

-

•

A bad Quant is a person that produces an infinite sequence and is not able to end the process.

-

•

Quant is more efficient than Quant if:

Let us illustrate the previous process with an example242424This example is taken from Roncalli (2013) on page 287.. We consider a universe of nine asset classes: (1) US 10Y Bonds, (2) Euro 10Y Bonds, (3) Investment Grade Bonds, (4) High Yield Bonds, (5) US Equities, (6) Euro Equities, (7) Japan Equities, (8) EM Equities and (9) Commodities. In Tables 12 and 13, we indicate the statistics used to compute the optimal allocation. The objective is to find the optimal allocation for an ex-ante volatility of around .

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

|---|---|---|---|---|---|---|---|---|---|

| (1) | |||||||||

| (2) | |||||||||

| (3) | |||||||||

| (4) | |||||||||

| \hdashline(5) | |||||||||

| (6) | |||||||||

| (7) | |||||||||

| (8) | |||||||||

| \hdashline(9) |

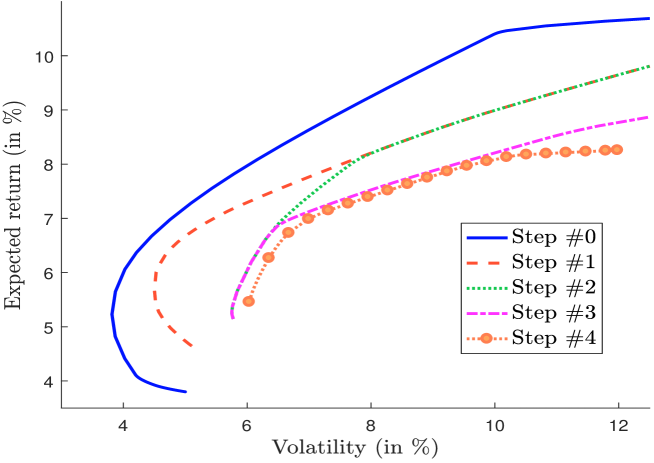

Using these figures, we obtain an initial allocation that is reported in Table252525The weights and the risk/return statistics are given in . 14. The optimal portfolio is invested in only four asset classes. The allocation in US 10Y Bonds is , while the allocation in High Yield Bonds is . It is obvious that this portfolio cannot be a SAA policy. This is why the Quant will add some constraints in order to obtain a better solution. We can impose that the weight of one asset class cannot exceed . Using this new set of constraints , we obtain Portfolio that is less concentrated than Portfolio . The allocation in US 10Y Bonds and High Yield Bonds reaches the cap of . The portfolio is now invested in Euro 10Y Bonds (), US Equities () and EM Equities (). The drawback of this solution could be the allocation in equities, which is too small. This is why the Quant will add another constraint in order to obtain an equity allocation that is larger than . At the third iteration, we then obtain Portfolio . If we assume that the SAA exercise is complete for a European institutional investor, this solution is not acceptable because it contains many US assets and too few European assets. This is why the Quant will add two new constraints. He can require that the allocation in Euro 10Y Bonds is larger than the allocation in US 10Y Bonds, and that the allocation in Euro Equities is larger than the allocation in US Equities. By using this new set of constraints , we obtain the following solution: the weight of US 10Y Bonds is , the weight of Euro 10Y Bonds is , the weight of IG Bonds is , etc. Again, this solution may not be acceptable, because there is no allocation in Japanese equities. Therefore, the Quant may impose that there is at least invested in this asset class. After few additional iterations, the solution is given by the last column in Table 14.

| Step | #0 | #1 | #2 | #3 | #4 | #K | ||

|---|---|---|---|---|---|---|---|---|

| US 10Y Bonds | (1) | |||||||

| Euro 10Y Bonds | (2) | |||||||

| IG Bonds | (3) | |||||||

| HY Bonds | (4) | |||||||

| \hdashlineUS Equities | (5) | |||||||

| Euro Equities | (6) | |||||||

| Japan Equities | (7) | |||||||

| EM Equities | (8) | |||||||

| \hdashlineCommodities | (9) | |||||||

We notice that the previous iterative process satisfies:

The underlying idea is to define an increasingly constrained investment universe. For instance, we verify that the efficient frontiers are ordered and that they are more and more constrained (see Figure 9).

Remark 6

Quants may use variants of Problem (25). When they are also in charge of producing and , they may also consider the iterative process with the following optimization problem:

In this case, the sequence is defined as follows:

It is obvious that the iterative process for defining the optimal portfolio conflicts with an automated and algorithm-driven robo-advisor. First, this is not the intent of a robo-advisor, unless we reduce the concept of robo-advisory to a digital application or a data-visualization tool, meaning that allocation decisions are made outside the robo-advisor. Second, a robo-advisor should be able to manage many portfolios on an industrial scale. If we consider the traditional lifestyle approach based on three portfolios (defensive, balanced and dynamic), which are rebalanced at the end of each month, it is obvious that the robo-advisor can be manually loaded every month. Again, this approach does not correspond to the robo-advisory concept. Indeed, robo-advisors claim that they better meet the expectations of investors by taking into account their constraints and by being more granular. This is particularly true with the emergence of goal-based investing in wealth management:

“While mass production has happened a long time ago in investment management through the introduction of mutual funds and more recently exchange traded funds, a new industrial revolution is currently under way, which involves mass customization, a production and distribution technique that will allow individual investors to gain access to scalable and cost-efficient forms of goal-based investing solutions” (Martellini, 2016, page 5).

Lastly, the iterative process does not help improve the portfolio management in a scientific manner. Indeed, it is a blind-eye approach, because it is difficult to explain the performance of the portfolio. We don’t know if it comes from the expected returns step (or the active bets) or the portfolio optimization step. In robo-advisory, these two steps must be easily identified and distinguished. Indeed, the portfolio optimization engine is part of the robo-advisor while expected returns may be designed outside the robo-advisor. This is generally the case because they can be imposed by the final investor himself, they can change from one third-party distributor to another, some investors will want to introduce trend-following patterns, etc. Contrary to the optimization method, the engine of expected returns is therefore not necessarily decided by the fintech that produces the robo-advisor. This is why the two steps must be perfectly differentiated.

4.2 Formulation of the optimization problem

We note the reference portfolio262626which is also called the strategic or the benchmark portfolio. and the current portfolio. The optimized portfolio for the next period is the solution of this comprehensive optimization program:

| s.t. | (34) |

where is a set of predetermined constraints. This problem considers both and penalty functions with respect to the reference portfolio and the current portfolio. Concerning , we can use the Markowitz function:

However, it is certainly better to consider the tracking-error function with respect to the reference portfolio:

where is a constant that does not depend on the variable .

The aims of Problem (4.2) are multiple:

-

1.

The first objective is naturally to optimize the traditional risk/return trade-off.

-

2.

The second objective is to control the active bets between the reference portfolio and the new optimized portfolio at various levels:

-

(a)

The first layer is to target a tracking error by using the TE objective function in place of the MVO objective function;

-

(b)

The second layer is the penalty that helps to smooth the tactical allocation with respect to the strategic allocation. This layer implies shrinking the covariance matrix ;

-

(c)

The third layer is the penalty that helps to sparsify the relative bets with respect to Portfolio ;

-

(a)

-

3.

The third objective is to control the turnover ( penalty) and the quadratic costs ( penalty) with respect to the current portfolio .

With all these safeguards, we are equipped to perform stable and robust dynamic allocation for robo-advisors. However, three issues remain unsolved: the specification of expected returns, the choice of the tracking error level and the calibration of the regularization parameters. The idea of the next section is not to give a solution or to publish our know-how on these topics (Malongo et al., 2016). However, we will indicate the shortcomings to be avoided.

4.3 Practical considerations

4.3.1 Incorporating active management views

In some cases, robo-advisors are closed systems, but most of the time, they are open systems. Often, the fintech that developed the robo-advisor technology enters into bilateral agreements with third-party distributors (asset managers, private banks, wealth managers, insurance companies, retail distributors, etc.). In this case, the robo-advisor platform is adapted to take into account the distributor’s specific requirements, constraints and objectives. For instance, the robo-advisor platform may be plugged with the distributor’s risk/return profiling system. The number of funds and the investment universe changes from one distributor to another one. One of the big specific features is the engine that produces expected returns. It is rare that the distributor uses the default engine provided by the fintech. For instance, some investors will want to incorporate momentum patterns, others prefer to use expected returns produced by their economic experts, etc.

In practice, it is extremely difficult to express bets in terms of absolute returns. Portfolio managers prefer to use a rating scale with different grades. The typical rating scale contains grades:

|

The challenge is then to transform these grades into expected returns. The most frequent empirical approach is based on the Black-Litterman model, which is described in Appendix B on page B.

Given a strategic portfolio , we compute the implied expected returns of Asset thanks to the CAPM equation:

| (35) |

We assume that the signal on Asset is homogeneous to a Sharpe ratio. In particular, we have:

where is the range index of the rating scale272727It is equal to: and is a scalar that indicates the flexibility of active tactical management282828Typically, is set to one.. Then, we deduce that the expected return of the portfolio manager is equal to:

where is the implied Sharpe ratio of Asset relative to the strategic portfolio and is the estimated volatility of Asset . The final step is to combine and using the Black-Litterman framework:

where is a parameter that measures the confidence into active bets. For instance, when , the manager’s views are not taken into account, while the conditional expected returns tends to manager’s views when .

| Volatility (in %) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | |

| 9.2 | 7.0 | 9.4 | 7.6 | 10.1 | 7.6 | 16.1 | 20.5 | 24.3 | 17.8 | |

| Correlation matrix (in %) | ||||||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | |

| \hdashline(1) | 100.0 | |||||||||

| (2) | 17.7 | 100.0 | ||||||||

| (3) | 98.1 | 19.4 | 100.0 | |||||||

| (4) | 16.5 | 99.5 | 18.1 | 100.0 | ||||||

| (5) | 71.1 | 2.4 | 76.3 | 2.1 | 100.0 | |||||

| (6) | 85.9 | 12.7 | 87.6 | 11.8 | 89.1 | 100.0 | ||||

| \hdashline(7) | 34.5 | 0.7 | 38.1 | 1.3 | 68.8 | 57.8 | 100.0 | |||

| (8) | -13.2 | 2.8 | -4.0 | 3.6 | 41.0 | 18.2 | 59.5 | 100.0 | ||

| (9) | 20.3 | 2.0 | 27.6 | 0.8 | 21.6 | 25.3 | 8.0 | 15.6 | 100.0 | |

| (10) | 16.6 | 10.2 | 26.0 | 10.5 | 57.2 | 44.6 | 54.3 | 67.7 | 42.9 | 100.0 |

We consider an example with 10 asset classes: (1) US Sovereign Bonds, (2) Euro Sovereign Bonds, (3) US Investment Grade Bonds, (4) EMU Investment Grade Bonds, (5) US High Yield Bonds, (6) EM Bonds, (7) US Equities, (8) Europe Equities, (9) Japan Equities and (10) EM Equities. In Table 15, we report the estimated covariance matrix for the period January 2016 – December 2016. We consider an equally-weighted portfolio , which corresponds to a 40/60 strategic allocation. By assuming that and , we calculate the vector of implied expected returns using Equation (35). The results are given in the second column in Table 16. For instance, the implied expected return of US Sovereign bonds is equal to . We now consider a set of manager’s views. The first scenario #1 corresponds to a weak bearish scenario on equity markets. Therefore, the grades are set to for the four equity asset classes and for the two sovereign bond asset classes. In Table 16, we calculate292929We assume that and . the expected returns implied by these views, and the final expected returns . For instance, and are equal to and for US Sovereign bonds. We verify that expected returns are increased for sovereign bonds, decreased for equities and neutral for the other asset classes.

| Asset class | ||||

|---|---|---|---|---|

| US Sov. Bonds | ||||

| Euro Sov. Bonds | ||||

| US IG Bonds | ||||

| EMU IG Bonds | ||||

| US HY Bonds | ||||

| EM Bonds | ||||

| \hdashlineUS Equities | ||||

| Europe Equities | ||||

| Japan Equities | ||||

| EM Equities |

| Asset class | ||||

|---|---|---|---|---|

| US Sov. Bonds | ||||

| Euro Sov. Bonds | ||||

| US IG Bonds | ||||

| EMU IG Bonds | ||||

| US HY Bonds | ||||

| EM Bonds | ||||

| \hdashlineUS Equities | ||||

| Europe Equities | ||||

| Japan Equities | ||||

| EM Equities |

| Asset class | ||||

|---|---|---|---|---|

| US Sov. Bonds | ||||

| Euro Sov. Bonds | ||||

| US IG Bonds | ||||

| EMU IG Bonds | ||||

| US HY Bonds | ||||

| EM Bonds | ||||

| \hdashlineUS Equities | ||||

| Europe Equities | ||||

| Japan Equities | ||||

| EM Equities |

We consider a second scenario that is more favorable to stock markets, in particular European stocks (see Table 17). By construction, the implied expected returns do not change because we consider the same strategic allocation. However, the expected returns and are different because we have changed the scenario. Finally, we consider a third scenario in Table 18, which is an adverse scenario on emerging markets303030 is set to in order to reflect stronger confidence in this scenario..

4.3.2 Choosing the right tracking error level

Volatility target strategies are very popular among Quants (Hallerbach, 2012; Hocquard et al., 2013). This explains why many robo-advisors are based on volatility or tracking error targeting. As said previously, we prefer TE objective function to MVO objective function. In this case, there is no constraint on the portfolio volatility, which is related to the volatility of the reference portfolio. However, the question of the TE level remains open. We provide some methods to set the right level of tracking error.

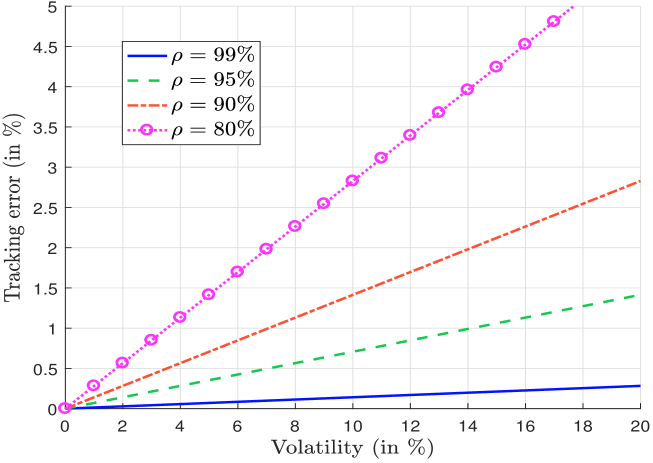

Let and be the tactical and strategic portfolios. We have:

where is the correlation between the portfolio and the benchmark . Generally, we have , implying that:

| (36) |

In Figure 10, we have reported the relationship between the volatility of the strategic portfolio and the tracking error of the portfolio. We notice that it depends on the correlation level. It follows that if the strategic portfolio’s volatility is low (less than ), we cannot target a high level of tracking error volatility. A level of is certainly the maximum. When the volatility is moderate between and , we can target a value between and . We can achieve a higher tracking error only if the portfolio’s volatility is high.

The previous result is of major importance, because it states that the tracking error level of the tactical portfolio must be related to the volatility of the strategic portfolio. In practice, the volatility is time-varying, implying that using a constant tracking error strategy is not optimal.

There is a second reason to consider a time-varying tracking error level, because another issue concerns the relationship between the tracking error and the active bets. We can show that (Grinold, 1994):

where is the transfer coefficient, is the information coefficient and is the number of assets. This relationship is known as “the fundamental law of active management”. If we assume that and are constant for a given active manager and a given portfolio, it follows that the excess return is proportional to the tracking error volatility:

However, alpha generation is also linked to the number and strength of active bets:

We deduce that the tracking error must be a function of the scores :

| (37) |

This relationship is essential when considering tactical allocation. Indeed, if all the scores are equal to zero, there is no active bet, implying that we must target a zero tracking error level. If all the scores are equal, we are in the same situation. Indeed, since we are bullish in all the asset classes, there is no reason to deviate from the strategic portfolio. In order to take a high tracking error risk, we need the bets to present a high dispersion:

|

Since the function is unknown and difficult to estimate, the function is also unknown. However, we may use the following rule of thumb:

| (38) |

where is the standard deviation of scores, is the mean absolute difference of scores, and is the maximum tracking error. The value of may be deduced from the relationship (36). By construction, we have:

and:

where is the number of assets. It follows that the scaling factor is approximatively equal to .

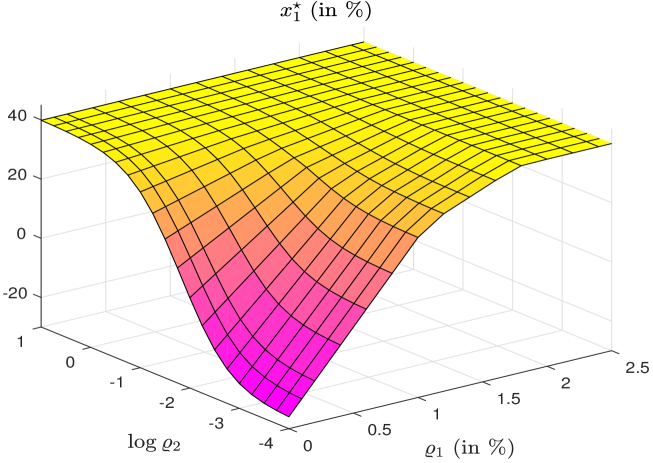

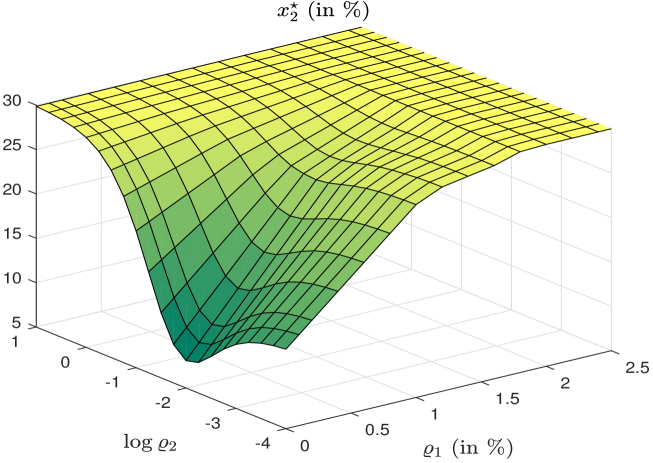

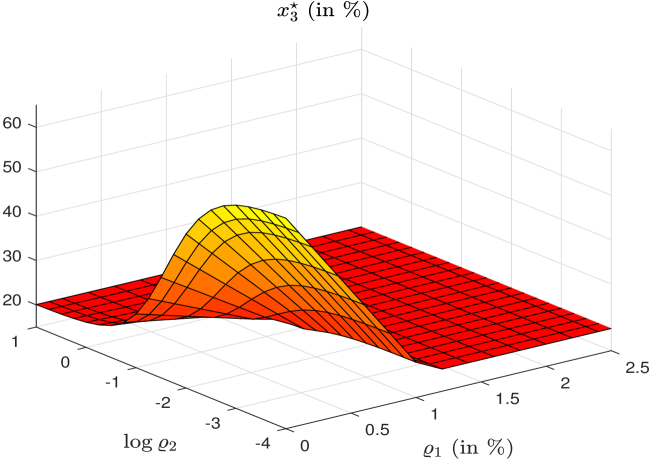

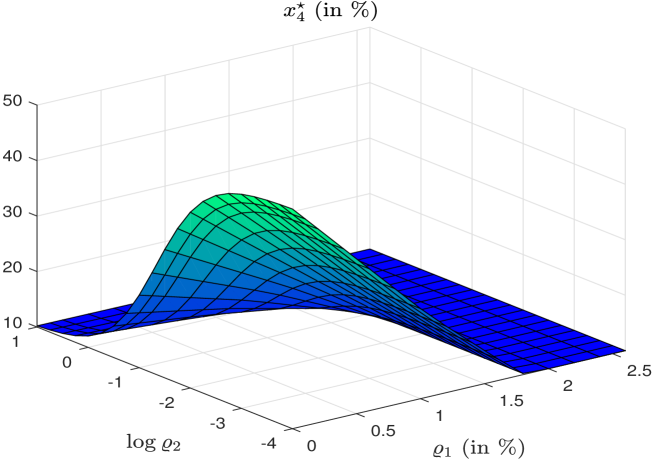

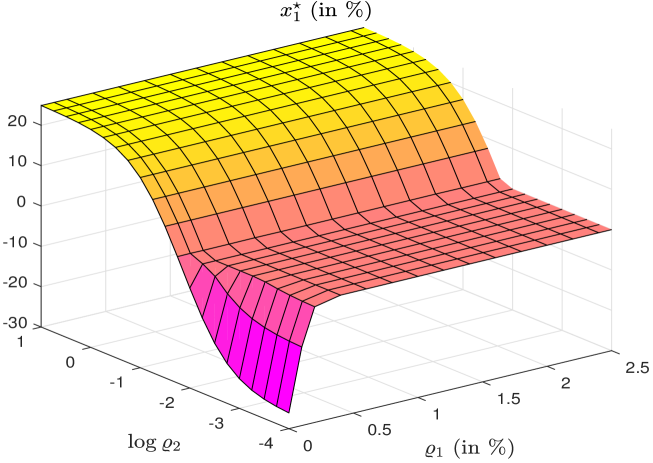

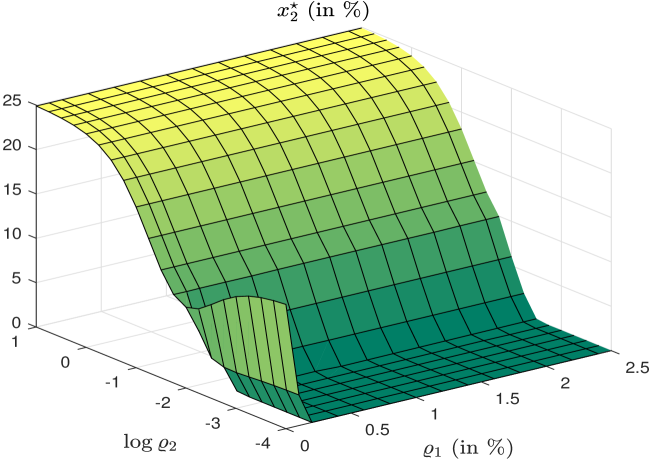

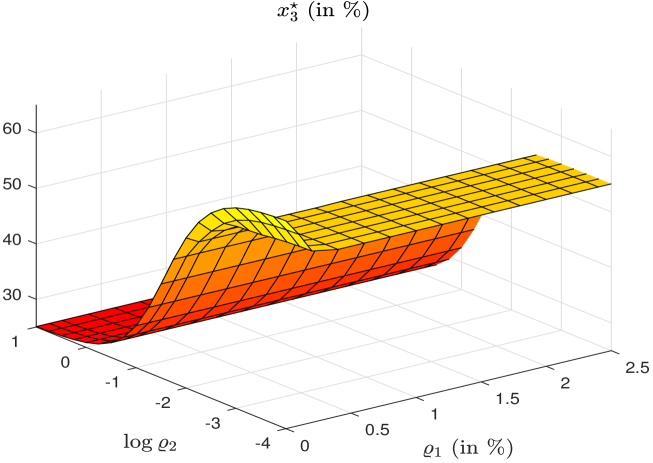

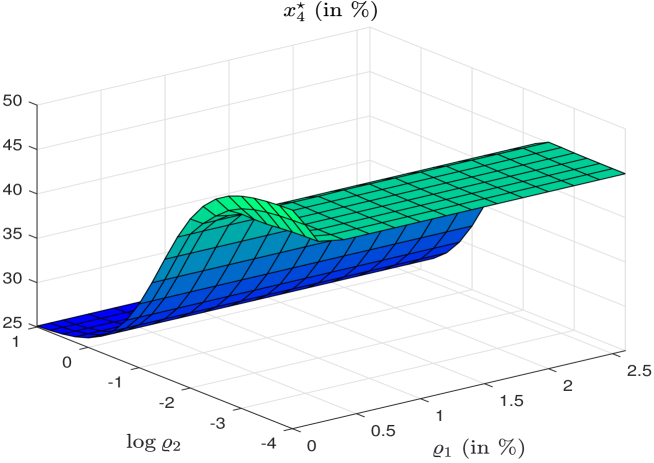

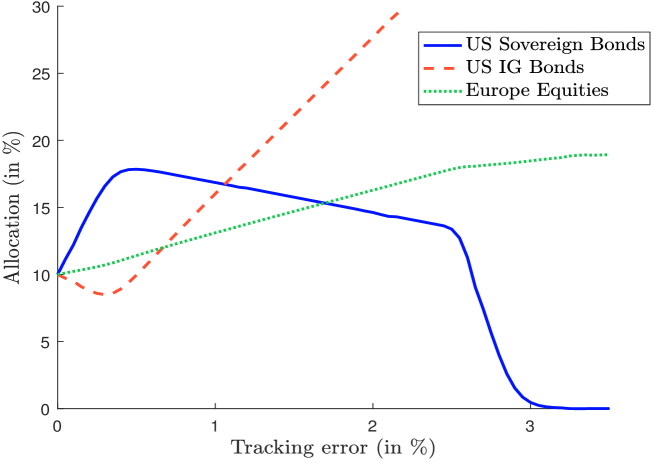

Equation (38) is a preliminary approach to set the level of tracking error. Nevertheless, this rule of thumb has a major drawback. It does not depend on the asset classes and their scores. Let us consider the previous example described on page 15. We assume that the signals are respectively , , , , , , , , and . In Figure 11, we report the tactical allocation when we target a tracking error level. For Europe Equities, we have a signal equal to , and we verify that the allocation is increasing with respect to the tracking error. For US Sovereign and IG Bonds, we also have a signal equal to , but the relationship between the allocation and the tracking error is not monotonically increasing. The case of US IG Bonds will be easily solved once we consider Problem (4.2) instead of a simple tracking error optimization. The case of US Sovereign Bonds is more problematic. Indeed, in an initial period when the tracking error is low, the relationship is increasing. However, when the tracking error increases too much, we obtain the opposite result. The reason is that the volatility of US Sovereign Bonds is low compared to the other asset classes (equities, investment grade and high yield). If we increase the tracking error, there is a threshold beyond which it is better to play only active bets on the most risky assets. Indeed, playing active bets on low risk assets does not give rise to a high tracking error budget. This is why the optimizer switches from low-risk assets to high-risk assets. This means that the choice of a tracking error level depends on the set of parameters: the maximum tracking error that depends on the strategic portfolio, the scores or active bets and the volatility of the assets that compose the tactical portfolio.

4.3.3 Calibrating the regularization parameters

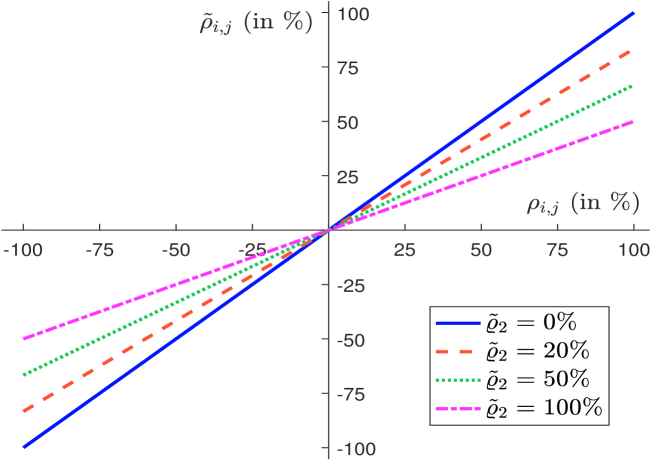

As said previously, the choice of the regularization parameters is not straightforward and requires a solid expertise and experience. However, we will provide some tips that can help to calibrate the model313131We can also implement cross-validation methods presented in Section 3.6 on page 3.6. The first thing to notice concerns the magnitude of and . On page 5, we have seen that if , the regularized correlations are:

In Figure 12, we have reported the relationship between the initial correlation and the shrinkage correlation . When is equal to zero, . When , the shrinkage correlation tends to zero. We then obtain a diagonal matrix with equal volatilities. Therefore, there is a trade-off between considering the initial covariance matrix and ignoring the dependence between assets. A good way to choose is to reduce the impact of arbitrage factors while keeping the significance of common risk factors. If we now consider the penalty and if we set , the norm measures the portfolio’s two-way turnover:

The parameter may then be used to control the turnover. If is a matrix with non-negative entries that contains the unit transaction costs, the norm measures the portfolio’s transaction cost (Scherer, 2007). This means that is the average transaction cost if is the identity matrix. It follows that the order of magnitude of is not comparable to the order of magnitude of . In the first case, it is expressed as a percentage (for instance, ) whereas in the lasso problem it is expressed in basis points (for instance, bps). This is in line with the practice that shows that optimal values of regularization are higher than those of regularization. The second thing to notice concerns the specification of regularization matrices , , and . Most of the time, they correspond to diagonal matrices, because it is not easy to consider the cross effects of regularization. The simplest way is to consider identity matrices, meaning that the regularization patterns reduce to ridge and lasso approaches. If we use the same parameters and , it is equivalent to considering that the two portfolios plays a symmetric role. However, this is not the case. Portfolio is used in order to limit the turnover and to smooth the dynamic allocation. Portfolio is used in order to control the relative active bets. This is why is more important than for implementing the active management. Last but not least, the calibration of the parameters highly depends on the investment profile. If the fund is composed of equities, we need to use more aggressive parameters in order to be more active than with a multi-asset fund. This means that there is no magic formula, and the calibration stage requires much empirical research and many tests in order to understand the interconnectedness between the different terms of the portfolio optimization problem.

5 Conclusion

According to Fisch et al. (2017), robo-advisors are “computer algorithms that provide advice on investment portfolios and then manage those portfolios”. Since they are digital-based tools that are generally implemented as web online services, fintechs compete in order to offer better customization, data visualization, analytics, process automation, etc. And the concepts of artificial intelligence, big data and machine learning are never far away when we see the presentation of a robo-advisor. Most of the time, fintechs prefer to insist on the application’s ergonomics and functionalities, and give little insight into the robo-advisor’s raison d’être: an automated portfolio allocation engine.

One of the reasons may be that portfolio allocation is more human-based than computer-based. It is true that automation in portfolio optimization is a big issue. Indeed, portfolio optimization is a hard task and does not always produce the desired results. This is because the mathematical problem is not necessarily well defined when we would like to obtain a smooth, sparse, active and dynamic allocation.

In this article, we come back to the traditional mean-variance optimization, and identify the reason for the issues. We have shown that it primarily corresponds to an alpha optimizer, and not to a beta optimizer. Then we have presented the theory of regularization and sparsity, and have demonstrated how it improves portfolio optimization. Finally, this approach is applied for building automated robo-advisory.

References

- [1] Allen, D.M. (1971), Mean Square Error of Prediction as a Criterion for Selecting Variables, Technometrics, 13(3), pp. 469-475.

- [2] Allen, D.M. (1974), The Relationship Between Variable Selection and Data Augmentation and a Method For Prediction, Technometrics, 16(1), pp. 125-127.

- [3] Beck, A. (2017), First-Order Methods in Optimization, MOS-SIAM Series on Optimization, 25, SIAM.

- [4] Black, F. and Litterman, R.B. (1991), Asset Allocation: Combining Investor Views with Market Equilibrium, Journal of Fixed Income, 1(2), pp. 7-18.

- [5] Black, F. and Litterman, R.B. (1992), Global Portfolio Optimization, Financial Analysts Journal, 48(5), pp. 28-43.

- [6] Boyd, S., Parikh, N., Chu, E., Peleato, B., and Eckstein, J. (2010), Distributed Optimization and Statistical Learning via the Alternating Direction Method of Multipliers, Foundations and Trends® in Machine learning, 3(1), pp. 1-122.

- [7] Broadie, M. (1993), Computing Efficient Frontiers using Estimated Parameters, Annals of Operations Research, 45(1), pp. 21-58.

- [8] Brodie, J., Daubechies, I., De Mol, C., Giannone, D., and Loris, I. (2009), Sparse and Stable Markowitz Portfolios, Proceedings of the National Academy of Sciences, 106(30), pp. 12267-12272.

- [9] Bruder, B., Gaussel, N., Richard, J-C., and Roncalli, T. (2013), Regularization of Portfolio Allocation, SSRN, www.ssrn.com/abstract=2767358.

- [10] Candelon, B., Hurlin, C., and Tokpavi, S. (2012), Sampling Error and Double Shrinkage Estimation of Minimum Variance Portfolios, Journal of Empirical Finance, 19(4), pp. 511-527.

- [11] Combettes, P.L., and Müller, C.L. (2018), Perspective Functions: Proximal Calculus and Applications in High-dimensional Statistics, Journal of Mathematical Analysis and Applications, 457(2), pp. 1283-1306.

- [12] Craven, P., and Wahba, G. (1978), Smoothing Noisy Data with Spline Functions, Numerische Mathematik, 31(4), pp. 377-403.

- [13] Diamond, S., Takapoui, R., and Boyd, S. (2018), A General System for Heuristic Solution of Convex Problems over Nonconvex Sets, Optimization Methods and Software, 33(1), pp. 165-193.

- [14] DeMiguel, V., Garlappi, L., Nogales, F.J., and Uppal, R. (2009), A Generalized Approach to Portfolio Optimization: Improving Performance by Constraining Portfolio Norms, Management Science, 55(5), pp. 798-812.

- [15] DeMiguel, V., Garlappi, L., and Uppal, R. (2009), Optimal Versus Naive Diversification: How Inefficient is the 1/N Portfolio Strategy?, Review of Financial Studies, 22(5), pp. 1915-1953.

- [16] DeMiguel, V., Martin-Utrera, A., and Nogales, F.J. (2013), Size Matters: Optimal Calibration of Shrinkage Estimators for Portfolio Selection, Journal of Banking & Finance, 37(8), pp. 3018-3034.