Model risk in mean-variance portfolio selection: an analytic solution to the worst-case approach

Abstract

In this paper we consider the worst-case model risk approach described in Glasserman and Xu (2014). Portfolio selection with model risk can be a challenging operational research problem. In particular, it presents an additional optimisation compared to the classical one. We find the analytical solution for the optimal mean-variance portfolio selection in the worst-case scenario approach and for the special case with the additional constraint of a constant mean vector considered in Glasserman and Xu (2014).

Moreover, we prove in two relevant cases –the minimum-variance case and the symmetric case, i.e. when all assets have the same mean– that the analytical solutions in the alternative model and in the nominal one are equal; we show that this corresponds to the situation when model risk reduces to estimation risk.

| Politecnico di Milano, Department of Mathematics, 32 p.zza L. da Vinci, Milano |

Keywords: Model Risk, robust portfolio selection, mean-variance portfolio, Kullback-Leibler divergence.

JEL Classification: C51, D81, G11.

Address for correspondence:

Roberto Baviera

Department of Mathematics

Politecnico di Milano

32 p.zza Leonardo da Vinci

I-20133 Milano, Italy

Tel. +39-02-2399 4575

Fax. +39-02-2399 4621

roberto.baviera@polimi.it

1 Introduction

Markowitz (1952) was the first to introduce an optimal portfolio selection according to the mean and the variance. Since that seminal paper, this problem has been extensively studied (see e.g. Li and Ng 2000, and references therein). This criterion is at the base of modern portfolio theory and it is widely used in finance due to its simplicity given that it models asset returns as Gaussian random variables.

The accuracy of this portfolio selection crucially depends on the reliability of this model, which is named nominal model. Model risk is the risk arising from using an insufficiently accurate model. A quantitative approach to model risk is the worst-case approach, which was introduced in decision theory by Gilboa and Schmeidler (1989). According to this methodology, one considers a class of alternative models and minimises the loss encountered in the worst-case scenario.

The literature distinguishes between estimation and misspecification risk (see e.g. Kerkhof et al. 2010). In general, it is interesting to identify vulnerabilities to model error that result not only from parameter perturbations (estimation risk) but also from an error in the joint distribution of returns (misspecification risk). The deviation between statistical distributions can be measured by the Kullback and Leibler (1951) relative entropy, which is also known as KL divergence, as proposed by Hansen and Sargent (2008) in the context of model risk. The problem of determining an optimal robust portfolio under KL divergence has been studied by Calafiore (2007); he proposed two numerical schemes to find an optimal portfolio in the mean-variance and the mean-absolute deviation cases, considering a discrete setting. This approach has been studied by Glasserman and Xu (2014) in a continuous setting in a mean-variance case; the authors identified the worst-case alternative models to the nominal model and numerically found the optimal portfolio selection in these cases. More recently, Penev et al. (2019) have analyzed the mean-standard deviation case in detail showing that this case presents a semi-analytic solution.

Let us briefly summarise the portfolio selection problem in presence of model risk. Let denote the stochastic asset returns. The p.d.f. associated with , , corresponds to the nominal model, while the p.d.f. corresponds to the alternative model. The KL divergence between the two models is

| (1) |

where is the change of measure and denotes the expectation w.r.t. . In particular, we are interested in the alternative models within a ball of radius around the nominal model; i.e., characterised by a KL divergence lower or equal to .

Let denote a measure of risk associated with , that depends on the portfolio weights a ranging over a set ; the classical optimal portfolio selection problem is

| (2) |

while the worst-case portfolio selection corresponds to

| (3) |

It can be shown that it is equivalent to the dual problem (see, e.g. Boyd and Vandenberghe 2004)

| (4) |

where

is the Lagrangian function associated to the constrained maximisation problem in (3).

Thus, in the worst-case portfolio selection, one has to solve three nested optimisation problems where the inner problem is an infinite dimensional optimisation. While the inner optimisation problem is a standard one in functional analysis and a closed form solution can be found (see e.g. Lam 2016), the presence of the other two makes the optimal selection a challenging operational research problem. Glasserman and Xu (2014) propose a numerical approach to solve this problem. In this study, we provide an analytical solution and we show that the problem can be challenging from a numerical point of view.

This paper makes three main contributions. First, we analytically solve the model risk optimisation problem in the worst-case approach when asset returns are Gaussian. This result is achieved for a class of problems that are even wider than those solved numerically by Glasserman and Xu (2014). In particular, we consider

-

•

a generic mean-variance selection, and not just the case where we impose the additional constraint of the worst-case mean equal to the nominal one (cf. Glasserman and Xu 2014, p.36);

-

•

all possible values of , which allow a well-posed problem and we do not limit the analysis to “ sufficiently small” (cf. Glasserman and Xu 2014, p.31); i.e., we do not consider only small balls .

Second, we provide the solution also in the special case where we impose the additional constraint of constant mean in the alternative model: this is the optimization problem considered by Glasserman and Xu (2014, cf. Eq.(30), p.36).

Third, we prove that, in the minimum-variance case and in the symmetric case with equal mean values for all assets in the portfolio, the optimal worst-case portfolio is the same as the optimal nominal portfolio. Moreover, we prove that in these cases model risk and estimation risk coincide: we show that any alternative model within the ball can be obtained through a parameter change. This result is different from the numerical solution in Glasserman and Xu (2014, Figure 1, p.37).

The rest of this paper is structured as follows. In Section 2, we recall the problem formulation. In Section 3, we present model risk analytical solution in the mean-variance framework. In Section 4, we study in detail the case of mean-variance with fixed mean considered by Glasserman and Xu (2014). In Section 5, we focus on the case where the optimal portfolio in the alternative model and the one in the nominal model coincide and provide numerical examples. Section 6 concludes this paper.

2 Problem formulation

In this section we recall the worst-case approach for model risk. Let denote the stochastic element of a model and a the parameters’ vector ranging over the set ; the nominal model corresponds to solve the optimisation problem (2) in the nominal measure, while the alternative model corresponds to the same problem with respect to an alternative measure, chosen within a KL-ball with ; i.e., within all models with a KL-divergence from the nominal model lower than a positive constant . In the best-case and in the worst-case approaches, the optimisation problem becomes

In portfolio selection, to have a robust measure, we are more interested in the worst-case approach, so hereafter we focus, unless stated differently, on this case that corresponds to the highest possible value of the measure of risk; mutatis mutandis similar results hold in the other case.

The rest of this section is organised as follows. First, to clarify the notation used in the case of interest, we summarise the classical mean-variance portfolio theory with its main results (Markowitz 1952, Merton 1972). Then, we sum up the main results for the worst-case model risk approach in a rather general setting, following Glasserman and Xu (2014) notation.

2.1 Classical portfolio theory

In this study, the nominal model is characterised by risky securities that are modeled as a vector of asset returns distributed as a multivariate normal , with a positive definite matrix with strictly positive diagonal elements. Let be the vector of portfolio weights, defined in the set , where 1 is the vector in of all s.

In the mean-variance framework, one considers a quadratic measure of risk; i.e., the difference between the variance (multiplied by , a positive risk aversion parameter) and the expected return of the portfolio

| (5) |

The value of the risk measure is

The problem consists in minimising the value of the risk measure on all portfolios a with weights summing to 1. Using a Lagrange multiplier, the mean-variance portfolio selection problem can be written as

| (6) |

where is the multiplier.

Following Merton (1972), we introduce the notation

| (7) |

it is straightforward to show that and (see, e.g. Merton 1972).

The optimal mean-variance portfolio (see, e.g. Merton 1972, equation (9), p.1854) is

| (8) |

Any optimal portfolio is the linear combination of two portfolios in the optimal frontier and , where the latter is the portfolio of minimum variance. This important result is also known as the two mutual fund theorem.

2.2 Worst case model risk

We briefly recall the model risk formulation for the construction of the alternative model. In particular, we focus on the worst-case portfolio selection (3); i.e., the one that considers the maximum value of the risk measure within the KL-ball . This worst-case problem is equivalent to the dual problem (4) with defined in (5); mutatis mutandis the same result holds in the best-case with .

Remark. Glasserman and Xu (2014) consider the special case with the additional constraint ; in their case, it is equivalent to consider, instead of (5), the measure of risk

| (9) |

In Section 4, we show that all results obtained in the mean-variance framework hold even in this special case.

Thus, we have to consider the three nested optimisation problems in (4). The inner optimisation problem is standard in functional analysis. For a given and for a given , the solution of the internal maximisation problem on the variable in (4) is

| (10) |

This result is known in the literature (see e.g. Glasserman and Xu 2014, Hansen and Sargent 2008). For a complete proof, the interested reader can refer to Lam (2016, proposition 3.1). Unfortunately, the other two optimisations are more challenging and closed form solutions cannot be found in the literature for the case of interest.

Before entering into the details of the two optimisations in a and , it is interesting to observe some properties for the entropy computed on the optimal solution of the internal maximisation problem

| (11) |

where is defined in (1). They are stated in the following lemma.

Lemma 1

For any s.t. in (10) is well-defined, is a monotone increasing function in for any portfolio a (and monotone decreasing for ).

Proof. See Appendix A

Let us underline that the previous lemma shows a general property that does not depend on the distribution of X and on the measure of risk . As already stated in the introduction, in this paper we consider X distributed as a multivariate normal and the general mean-variance framework (i.e. with the measure of risk defined as in (5)). We now deduce a necessary and sufficient condition for which the change of measure (10) is well-defined and we find the distribution of X in the alternative model for any portfolio .

Lemma 2

Let , the change of measure in (10) is well-defined if and only if where

| (12) |

Moreover, for any , in the alternative model corresponding to , X is distributed as a multivariate normal r.v., i.e. , where

| (13) |

Proof. First, we prove that in (10) is well defined. Let us observe that a necessary and sufficient condition to have a well-defined change of measure (10) is that is finite. We consider and as in (5), thus we get

where is a symmetric matrix.

The integral is finite if and only if the matrix is positive-definite. To prove this fact we proceed in two steps: first we compute the determinant of and we then state a property on the signs of its eigenvalues.

To compute the determinant, we use the Matrix Determinant Lemma (see e.g. Harville 1997, theorem 18.1.1, p. 416) that states

| (14) |

Thus, the determinant of is positive if and only if the condition (12) holds. If is positive, then is also invertible; we define as its inverse. We have verified that (12) is a necessary condition to get , thus , positive-definite.

We now prove that the condition is also sufficient to have the matrix positive-definite. Let be the eigenvalues of . The eigenvalues of the inverse matrix are the reciprocals . Let us define the eigenvalues of . The following inequalities hold (see e.g. Gantmacher and Kreĭn 1960, theorem 17, pp. 64-66)

Because the matrix is positive-definite, are all positive, thus has positive eigenvalues. Also having a positive determinant (cf. equation (14)), we conclude that it is positive-definite and condition (12) is necessary and sufficient to have the whole problem well defined. In this case, after a completion of the square, we get

Second, we consider , the density of X in the alternative model. For any , it is

which is well-defined if and only if is well defined. In this case, is a Gaussian density with mean and variance (13)

We notice that in the best-case approach, with , it is not necessary to impose any additional condition for ; i.e., the alternative measure is well defined : this is the only difference that should be considered when dealing with the best-case approach.

Condition (12) determines the domain with all possible values of that allow a well-posed problem, not limited to only small values of and to asymptotic results, as in Glasserman and Xu (2014, p.31). In the rest of this paper, we consider and a in the domain defined as

| (15) |

We now consider the two external optimisation problems in (4). First, let us define the Lagrangian function computed in the optimal change of measure

| (16) |

obtained substituting the optimal change of measure (10) in (4), with defined in (5). Thus, the optimisation problem to be solved becomes

| (17) |

The standard technique to solve this problem is to exchange the order of the other two minimisation problems in (17). Before entering into details, we state some properties for the Lagrangian function in the following lemma.

Lemma 3

Proof. First, we prove that the Lagrangian function in the alternative worst-case approach (i.e. with ) is convex in a, s.t. . We can apply Sherman and Morrison (1950) formula to get

| (21) |

then, we obtain

| (22) |

The Lagrangian function in (16) becomes

| (23) |

Recalling that the sum of convex functions is itself a convex function (see e.g. Boyd and Vandenberghe 2004, Section 3.2.1, p.79), we focus on the non-linear terms in a in (23). We define

where is defined in (19).

It is easy to show that is convex and increasing in and that is convex in a for . Thus, using the composition rule for convexity (see e.g. Boyd and Vandenberghe 2004, Section 3.2.4, p.84), we can conclude that is convex in a and then the Lagrangian function (23) is convex in a.

Second, we prove the expression (18) for . From (11), we have

| (24) |

After some simplifications, we get

where is a Gaussian r.v. with mean and variance (13). Finally, using equation (21) and substituting (19) and (20), the relative entropy (18) follows.

Finally, we prove that the Lagrangian function for any given a has a unique minimum in , called , and, in particular, that it is a monotone decreasing function in and a monotone increasing function in .

Because is optimal for the Lagrangian function in (4) and the alternative model is a sufficiently regular function (a multinomial Gaussian p.d.f.), we can exchange the derivative with the expected value (cf. e.g., Protter and Morrey 2012, Th.4, p.429) and we get

Observing that the relative entropy is null in , it is monotone increasing for (cf. Lemma 1) and it tends to infinity if (straightforward using (18) and (20)), the thesis follows

Glasserman and Xu (2014) prove that, under certain conditions, it is possible to exchange the two infima in (17) and subsequently they solve the optimisation problem in the variables a and numerically. We use the same inversion as Glasserman and Xu (2014), but we solve analytically the problem: as already stated in the introduction, this is our main theoretical contribution.

To find the optimal portfolio in the alternative measure and the corresponding optimal change of measure, we recall Proposition 2.1 of Glasserman and Xu (2014) for the portfolio selection.

Lemma 4

Proof. See Proposition 2.1 in Glasserman and Xu (2014), applied to the mean-variance case

This lemma is an important result known from literature about the worst-case model risk. As in Glasserman and Xu (2014), we follow the same approach in this paper. We first find the optimal worst-case portfolio given and then select the optimal value of within the KL-ball . It is straightforward to prove that in the best-case approach the same equations of Lemma 4 hold with .

3 Analytical solution for the worst-case portfolio selection

In this section, we solve analytically the optimisation problem (26) and find the optimal portfolio in the alternative model for a given value of ; i.e., the robust portfolio in the mean-variance framework. Then, we prove that the optimum in (25) stays on the surface of the ball .

Theorem 5

Proof. In the alternative worst-case approach, it is possible to find the optimal portfolio solving (26). Using (22) and introducing a Lagrange multiplier for the constraint (i.e. ), (26) is equivalent to

Following the same method as in the nominal model, we get the equation (28) for a, where is defined in (19). By substituting (28) in (19), we get the equation (29) for the optimal .

Let us study the solutions of equation (29) given in (20). The domain of is s.t. must be included in the interval

| (30) |

because i) corresponds to the minimum-variance case even in the alternative model and ii) , i.e. .

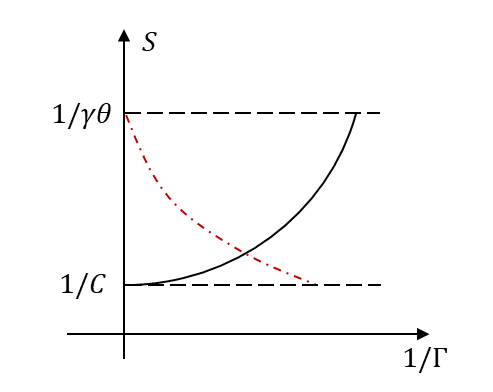

First, let us consider as a function of in equation (29) in the domain (30), which is one branch of a parabola (and then monotone increasing) with a minimum in . Then, consider as a function of in equation (20) in the same domain for , which is equal to a positive value in and it is derivable in the domain of with a derivative always strictly negative and it tend to zero in the limit . Hence, Equation (29) has a unique solution, as shown in Figure 1

Depending on , the worst-case mean-variance optimal portfolio is the (unique) analytical solution in equation (29). Let us observe that, in the mean-variance framework, the optimal worst-case portfolio is similar to the optimal nominal one (8). Also in the worst-case approach a two mutual fund theorem holds: the optimal portfolio is the linear combination –with a different weight– of the same two portfolios and of the nominal problem. The solution in the alternative model has exactly the same form of the nominal one with an increased risk aversion “parameter” in the worst-case approach ( for . It can be shown that a similar solution holds also in the best-case approach with a decreased risk aversion ( for ).

Let us notice that, given the optimal portfolio , we are now able to find the corresponding relative entropy, i.e. the KL-divergence between the nominal and the alternative model, depending only on parameter . Substituting the unique solution of (29) in (18), we get

| (31) |

We conclude this section proving that the optimal parameter in the optimisation problem (25) stays on the surface of the ball . This result is crucial because solves completely (25), i.e. the mean-variance portfolio selection in the worst-case approach.

Proposition 6

Proof. We first show that the optimum that solves the original optimisation problem (4) is on the surface of the ball for any given portfolio a; then, we consider problem (25) obtained inverting the two infima.

First, we consider the internal maximisation problem in (3) for a given a, that is the primal problem. Following the notation in Boyd and Vandenberghe (2004, pp.216-225) we call the primal problem , we indicate with the corresponding Lagrangian dual problem in (4), while and denote the optimal values respectively of the primal problem and of the dual one.

Because the objective function is convex in and the set is non-empty, Slater’s theorem ensures that strong duality holds, i.e. (see, e.g. Boyd and Vandenberghe 2004, Section 5.2.3, p.226). In other words, for a given a, given a primal optimum and a dual optimum where is a function of a, we have

The second line comes from Boyd and Vandenberghe (2004, eq.(5.45), p.238). The third line considers the optimum of the dual problem. The fourth line follows because the supremum of the Lagrangian over is greater or equal to its value at any other and then also choosing . The last inequality is due to the fact that the second term in fourth line is non-negative.

Thus, since all inequalities hold with equality, we can draw two conclusions. First, maximises the Lagrangian. This result, added to the concavity of the Lagrangian in , implies that .

Second, the following equality holds

| (32) |

Because must remain finite, due to condition (12), we get that the expectation in (32) must be null; i.e., stays on the surface of the ball , or equivalently s.t. .

Because i) the relative entropy is a monotone increasing function in (cf. Lemma 1), ii) it is null when and iii) it tends to infinity in the limit (cf. also the end in the proof of Lemma 3), then there exists a unique solution of (32) for and then also a unique solution for the dual optimum .

In Lemma 4 we have proven that it is possible to change the order of the two infima in (4), obtaining the same solution. This is the inverted dual problem (25). Thus, the optimum value of the inverted dual problem is as well on the surface of the ball, that ends the proof

4 Mean-variance with constant mean

In this section we analyse in detail the mean-variance case considered by Glasserman and Xu (2014), in which they consider a special case with a constraint on the mean vector that must be equal to the nominal mean even in the alternative model. The problem in this case becomes

as in Glasserman and Xu (2014, p.36), that is equivalent to

with the measure of risk defined in (9).

In the remaining part of this section, we show that all results proved in previous sections can be replicated in this special case.

First, let us show that the basic properties of Lemmas 2, 3 and 4 can be adapted to this special case, considering the measure of risk (9). This is proven in the next Lemmas 7 and 35.

Lemma 7

Proof. See proof of Lemma 2, noting that attains the same value as in mean-variance framework with a linear constant term in the exponential instead of the linear stochastic term . Thus, the first part of the proof holds and it is straightforward to show that is the density of a Gaussian r.v. with mean (the new constraint that we are imposing) and variance

Defining as in (16), using instead of , we can show that results similar to Lemma 3 and Lemma 4 hold as well.

Lemma 8

Let . is convex in a and it has a unique minimum in , interior point of the set (12). In the alternative worst-case approach, the relative entropy is

| (33) |

where

| (34) |

Moreover, it is possible to exchange the order of the two inferior in the optimisation problem (4), that becomes equivalent to

the optimal portfolio in the alternative measure is found solving

| (35) |

Proof. See proof of Lemma 3 and Lemma 4, noting that

and for the relative entropy that

Following similar computations as in mean-variance case, all previous results hold

Then, similarly to Theorem 5 we can find the closed form solution of problem (35) for a given positive and prove that the optimum stays on the surface of the ball also in this special case.

Theorem 9

Let . In the alternative worst-case approach, the optimal portfolio is

| (36) |

where

| (37) |

with

Proof. As in the mean-variance case, it is possible to find the optimal portfolio in the alternative measure solving (35), that becomes

that, introducing a Lagrange multiplier for the constraint , is equivalent to

Following the same method as in the nominal model, we get equation (29) with defined in (34) instead of defined in (20).

As in the mean-variance case, the domain for is (30). Moreover, in this special case, equation (29) and (34) represent a second order degree system, that can be solved in closed form.

We obtain the following solution for a second order degree equation in the variable

Observing from (30) that and from (34) that , we can deduce that the solution for with the negative sign is non-acceptable in the worst-case approach, thus (37) is the unique solution for , that concludes the proof

As in the mean-variance case, let us notice that, given the optimal portfolio (36), we are able to obtain from (33) the corresponding relative entropy that depends only on parameter ; i.e.,

| (38) |

Also Proposition 6 can be replicated in this special case.

Proposition 10

Let . The optimal value for in the worst-case portfolio selection is on the ball, i.e. , with in (38).

Proof. The proof follows the same steps of Proposition 6 with the Lagrangian and entropy of this special case

We conclude the section noting that the value of the risk measure in this framework simply becomes

| (39) |

where in the second equality we have used (21) and the optimal portfolio in (36).

In practice, an efficient way to obtain a graphical representation of the result is first to identify the alternative model through the parameter , (e.g. in a range ), and then to get the relative entropy (38) for that value of . The numerical examples in next section are carried out in this way, obtaining at the same time the relative entropy (38) and the associated value of the risk measure (39).

5 Equality of optimal portfolio in alternative and nominal models and numerical examples

In this section, we analyse the cases where the optimal portfolio in the nominal model and in the alternative one are equal. We prove that this equality holds only in two relevant cases: the minimum-variance problem in which the uncertainty is limited only to the covariance matrix and a symmetric case where all assets have the same mean, i.e. .

The minimum-variance case is an interesting subcase of the mean-variance portfolio selection –as of the mean-variance with fixed mean portfolio selection considered in Glasserman and Xu (2014)– and it is a purely risk-based approach to portfolio construction. This corresponds to selecting a very large risk adversion parameter in (5) or equivalently in (9). In this case, the measure of risk is

In the minimum-variance case, we can prove the interesting analytical result that the optimal portfolio in the worst-case approach is exactly the same as the optimal portfolio in the nominal model. Moreover, we can adapt all results obtained in previous Sections to this case.

First, we can adapt Lemma 7 and Proposition 10 to the minimum-variance case, obtaining that: i) in the alternative model, X is distributed as a multivariate normal r.v. with the same mean as the nominal model and variance as in (13), if and only if the same condition (12), with , holds; ii) the relative entropy associated to the optimal worst-case and nominal portfolio has the same expression (38) as in previous section, with , and the optimal is on the surface of the ball .

Then, we can prove that the optimal portfolio in the alternative model (i.e. the robust portfolio) is the same of the optimal one in the nominal model, as shown in the next proposition.

Proposition 11

Let . In the minimum-variance case, the optimisation problem (26) is equivalent to

| (40) |

thus, the optimal portfolio in the alternative model is the same as the one of the nominal model , i.e. .

Proof. The optimal portfolio is found solving optimisation problem (26). After some computations and using (14), we get

Hence, the worst-case problem (26) is equivalent to the classical problem. Then, the solution is the same of the nominal model and it is unique

Let us stress that two main properties hold in the minimum-variance framework: not only the exponential change of measure stays in the family of multivariate normal distributions, but also the robust portfolio is equal to the optimal one in the nominal model. These two properties lead to the consequence that in the minimal-variance framework the worst-case approach corresponds to a change in the parameters of the Gaussian distribution: in this situation model risk can be explained simply as an estimation risk.

In the remaining part of this section, we get back to the mean-variance framework and we focus our attention on a symmetric case

We first prove a general result of a necessary and sufficient condition for the equality of the optimal portfolio in the nominal and in the alternative model: in this case model risk is equivalent to an estimation risk. Then, we show some numerical examples.

In the general mean-variance framework (and also in the special case), it is possible to prove the following proposition, that guarantees the equality of the optimal portfolios in the nominal and in the alternative model.

Proposition 12

Let and a finite risk aversion. The optimal mean-variance portfolio in the nominal and alternative models are equal if and only if with .

Proof. From equations (8) and (28), we have

where and have been defined in (7) and 0 is the null vector in . The equation has a solution only if either . While, for finite , the condition ii) cannot be fulfilled in the alternative model, condition i) proves the proposition: it corresponds to have in the same direction of 1 with

It can be interesting to underline that Proposition 12 holds even in the mean-variance case with a constraint on the mean vector considered by Glasserman and Xu (2014).

In order to show some numerical examples, let us consider, as in Glasserman and Xu (2014), the case of mean-variance with fixed mean and a fully symmetric variance, i.e.

with . This case presents the advantage of a complete detailed analytical solution for a generic and it allows to understand in an interesting example what can happen in the numerical determination of the optimal solution in the alternative model. The eigenvalues of the variance-covariance matrix are (see, e.g. Lemma 13 in Appendix A):

| (41) |

Similarly, also the inverse matrix , can be computed .

As a first numerical example, let us consider a symmetric case as considered by Glasserman and Xu (2014) in their numerical example. In this case, the optimal portfolio in the nominal model and in the alternative model is the equally weighted one . We also have an explicit expression for condition (12) for the optimal portfolio in the alternative model . Using (41), it becomes

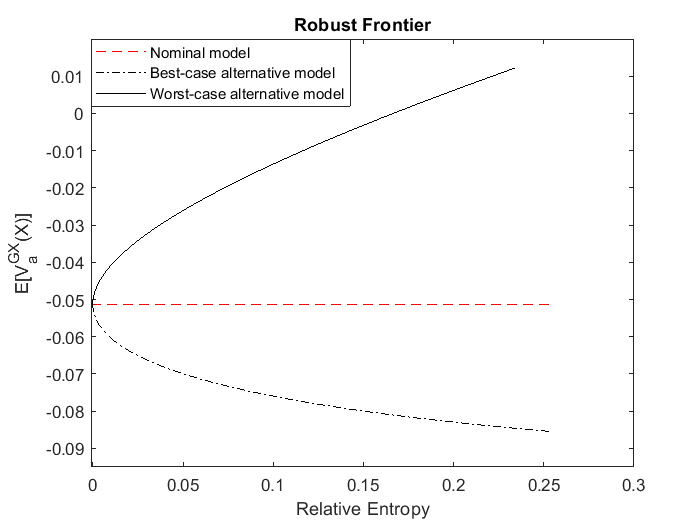

We consider exactly the same numerical example as that in Glasserman and Xu (2014, pp.36-37) with , assets, , and and we recall that they consider the special case with a mean-variance with fixed mean. We plot the value of the risk measure for the optimal portfolio as a function of the maximum allowed relative entropy (cf. Figure 1 in Glasserman and Xu 2014, p.37). The left-hand plot in Figure 2 shows, for a set of maximum relative entropy values , the value of the risk measure in the alternative model in the worst-case approach (continuous black line) and in the best-case approach (dot-dashed black line).

As already stated, in this case, due to Proposition 12, the optimal portfolios in the nominal and in the alternative model coincide. This is different from the result shown in Glasserman and Xu (2014, Figure 1, p.37) in which these two optimal portfolios do not coincide. This incoherence might be due to a slow convergence of the numerical algorithm. We return to this point in the following.

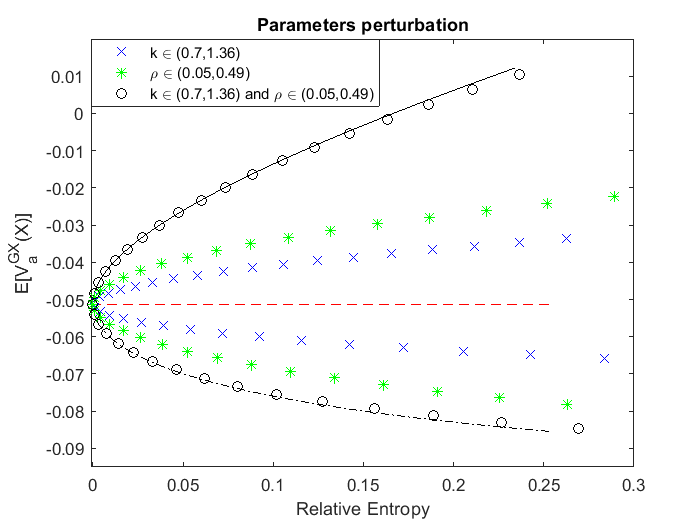

Moreover, Glasserman and Xu (2014) claim that “model error does not correspond to a straightforward error in parameters” (cf. p.37). To illustrate this idea –because in the mean-variance with fixed mean framework the alternative model differs from the nominal model just for the variance matrix– these authors studied the value of the risk measure obtained by varying just two parameters: the common correlation parameter and a parameter that multiplies the variance parameter in the the variance matrix . In particular, they let the correlation parameter vary between and , and the parameter vary between and .

The result obtained by varying and separately is shown in Glasserman and Xu (2014, Figure 1, p.37) and it is in agreement with blue crosses and green stars in the right-hand panel of Figure 2. The new result is that the perturbation of both parameters and , in the same range as before, modifies the value of the risk measure that reaches the value obtained in the alternative measure (see black circles in Figure 2); i.e., in this framework model error can be completely explained as estimation error.

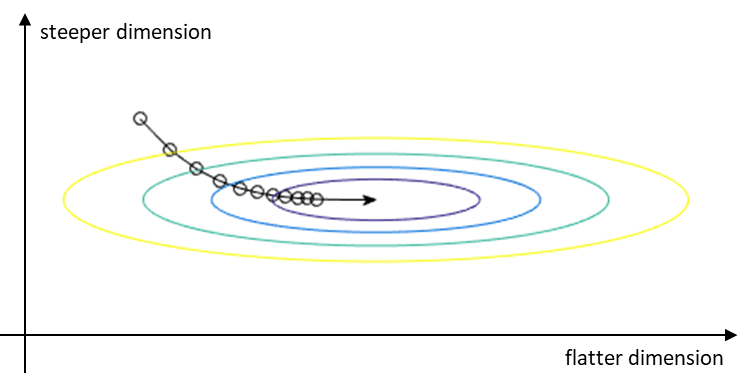

Furthermore, because we have in this case a complete analytical solution, we can understand the reason why a numerical approach can be slow. Solving the optimisation problem (40) is equivalent to selecting the minimum of a paraboloid. A first order algorithm decreases faster in the direction of higher eigenvalues and more slowly when eigenvalues are lower. For example, Figure 3 shows the evolution of the gradient descent numerical algorithm used in the minimisation of a quadratic function in two dimensions: the algorithm is fast in the direction with maximum variability but varies slowly in the direction of minimum variability; i.e., in the direction of the eigenvector of the matrix corresponding to the minimum eigenvalue.

In our case, for every in the interval of interest, we have to solve an optimisation problem. Each optimisation has two main features, as shown in (41): i) the largest eigenvalue is almost times larger than the other ones and ii) there are minimum eigenvalues. Thus, the numerical algorithm becomes slow in the direction of minimum variability and it could stop before it reaches the correct optimum, in particular if is very large. This can be one reason why an analytical solution can be useful.

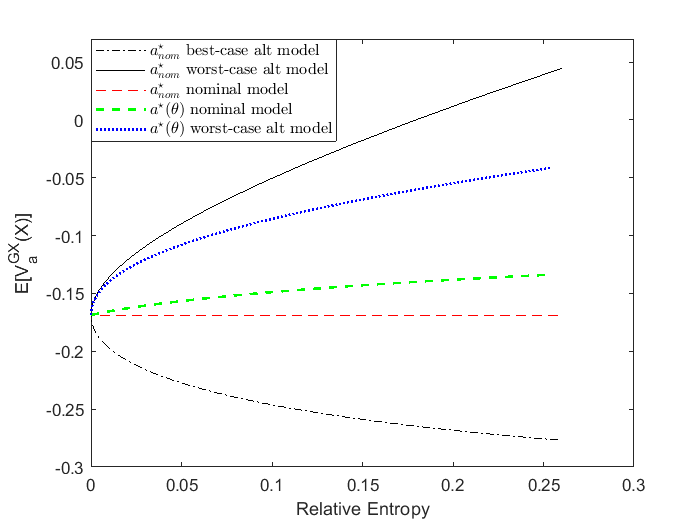

Finally, as a second numerical example we consider a non-symmetric case. The parameters are the same ones of previous numerical example, but with mean , , with drawn from a standard normal random distribution. The frontier obtained is shown in Figure 4. In this case the robust portfolio, i.e. the optimal portfolio in the worst-case alternative model (36) where is obtained via Proposition 10, is different from the optimal portfolio in the nominal model , as we have proven in Proposition 12. The result obtained in Figure 4 looks similar to the one in Glasserman and Xu (2014, Figure 1, p.37) and the two plots differ just for the values of the risk measure on the vertical axis, that depend on the chosen values for .

In Figure 4 we can observe the consequences of selecting the robust portfolio. On the one hand, the value of the risk measure in the nominal model is larger for the robust portfolio (dashed green line) w.r.t. the one for the optimal nominal portfolio (dashed red line), where the latter clearly does not depend on the relative entropy; on the other hand, the value of the risk measure in the alternative worst-case model (with variane in (13)) is significantly lower for the robust portfolio (dotted blue line) w.r.t. the one valued for the optimal nominal portfolio (continuous black line).

6 Conclusions

We have studied the effect of model risk on the optimal portfolio in the mean-variance selection problem. Model risk is measured via the worst-case approach, taking the relative entropy as measure of the divergence between the nominal and the alternative model; in particular, we have considered all alternative models within a KL-ball of radius . When asset returns are modeled with a multivariate normal, this problem has been numerically solved for small by Glasserman and Xu (2014) in the mean-variance case with an additional constraint on the mean, chosen equal to the one in the nominal model.

In this paper, we have analytically solved the optimal portfolio selection problem in the alternative model in a generic mean-variance framework for a generic KL-ball . We have proven that the optimal portfolio in the worst-case approach is unique and given by equation (28), where the optimal is the unique positive solution of the equation with given in (31).

We have also solved the special case considered in Glasserman and Xu (2014), in which they impose the alternative mean constrained (cf. solution (36) with entropy (38)).

Finally, we have analyzed in detail the situations when model risk and estimation risk coincide and we have shown two numerical examples. In particular, one of these examples considers exactly the same illustrative example of Glasserman and Xu (2014, Figure 1, p.37), without been able to reproduce their numerical solutions. This fact shows the relevance of the provided analytical solution in the worst-case approach for model risk because in some cases solving the nested optimizations (cf. problem (4)) can be a challenging operational research problem from a numerical point of view.

Acknowledgments

The authors thank all participants to the seminar at the European Investment Bank (EIB) and conference participants to the Quantitative Finance Workshop at ETH Zurich and to the SIAM Conference on Financial Mathematics & Engineering at University of Toronto. We are grateful in particular to Michele Azzone, Giuseppe Bonavolontá, Mohamed Boukerroui, Szabolcs Gaal, Juraj Hlinicky, Aykut Ozsoy, Oleg Reichmann, Sergio Scandizzo, Claudio Tebaldi, Pierre Tychon for useful comments.

The authors acknowledge EIB financial support under the EIB Institute Knowledge Programme. The findings, interpretations and conclusions presented in this document are entirely those of the authors and should not be attributed in any manner to the EIB. Any errors remain those of the authors.

References

- Boyd and Vandenberghe (2004) Boyd, S. and Vandenberghe, L., 2004. Convex optimization, Cambridge university press.

- Calafiore (2007) Calafiore, G.C., 2007. Ambiguous risk measures and optimal robust portfolios, SIAM Journal on Optimization, 18 (3), 853–877.

- Gantmacher and Kreĭn (1960) Gantmacher, F.R. and Kreĭn, M.G., 1960. Oszillationsmatrizen, oszillationskerne und kleine schwingungen mechanischer systeme, vol. 5, Akademie-Verlag.

- Gilboa and Schmeidler (1989) Gilboa, I. and Schmeidler, D., 1989. Maxmin expected utility with non-unique prior, Journal of Mathematical Economics, 18 (2), 141–153.

- Glasserman and Xu (2014) Glasserman, P. and Xu, X., 2014. Robust risk measurement and model risk, Quantitative Finance, 14 (1), 29–58.

- Hansen and Sargent (2008) Hansen, L.P. and Sargent, T.J., 2008. Robustness, Princeton university press.

- Harville (1997) Harville, D.A., 1997. Matrix algebra from a statistician’s perspective, vol. 1, Springer.

- Kerkhof et al. (2010) Kerkhof, J., Melenberg, B., and Schumacher, H., 2010. Model risk and capital reserves, Journal of Banking & Finance, 34 (1), 267–279.

- Kullback and Leibler (1951) Kullback, S. and Leibler, R.A., 1951. On information and sufficiency, The annals of mathematical statistics, 22 (1), 79–86.

- Lam (2016) Lam, H., 2016. Robust sensitivity analysis for stochastic systems, Mathematics of Operations Research, 41 (4), 1248–1275.

- Li and Ng (2000) Li, D. and Ng, W.L., 2000. Optimal dynamic portfolio selection: Multiperiod mean-variance formulation, Mathematical Finance, 10 (3), 387–406.

- Markowitz (1952) Markowitz, H., 1952. Portfolio selection, The Journal of Finance, 7 (1), 77–91.

- Merton (1972) Merton, R.C., 1972. An analytic derivation of the efficient portfolio frontier, Journal of Financial and Quantitative Analysis, 7 (4), 1851–1872.

- Penev et al. (2019) Penev, S., Shevchenko, P.V., and Wu, W., 2019. The impact of model risk on dynamic portfolio selection under multi-period mean-standard-deviation criterion, European Journal of Operational Research, 273, 772–784.

- Protter and Morrey (2012) Protter, M.H. and Morrey, C.B.J., 2012. Intermediate calculus, Springer Science.

- Sherman and Morrison (1950) Sherman, J. and Morrison, W.J., 1950. Adjustment of an inverse matrix corresponding to a change in one element of a given matrix, The Annals of Mathematical Statistics, 21 (1), 124–127.

Shorthands and notation

Shorthands

Notation

| Symbol | Description |

|---|---|

| 1 | Vector of all s in |

| Lagrange multiplier | |

| a | Portfolio’s weights vector, named portfolio |

| , | Optimal portfolio in the nominal measure and in the alternative measure |

| Domain for the portfolio a, satisfying the constraint | |

| Risk aversion parameter | |

| Defined in (20) | |

| Defined in (34) | |

| , | Dual Lagrangian problem corresponding to and related optimal value |

| Domain for defined in (15) | |

| Probability densities in nominal and alternative model | |

| Maximum KL-divergence between the alternative and the nominal one | |

| , | Optimisation parameter and corresponding optimum |

| Upper bound for defined in (12) | |

| Argmin in of for a given portfolio a | |

| Identity matrix | |

| Multiplicative parameter of the variance parameter | |

| , | Eigenvalues of the variance matrices and |

| Lagrangian function associated to constrained maximisation problem (3) | |

| Lagrangian function computed in the optimal change of measure (10) | |

| Change of measure, defined as | |

| Worst-case change of measure depending on parameter a | |

| Worst-case change of measure corresponding to the optimal portfolio | |

| , | Optimal change of measures for the primal and dual problem and |

| , | Mean vector in the nominal and in the alternative model |

| Number of assets considered | |

| , | Primal problem optimisation in (3) and related optimal value |

| KL-ball with radius | |

| Correlation parameter | |

| Relative entropy function between nominal and alternative models | |

| Relative entropy corresponding to the optimal change of measure (10) | |

| Relative entropy corresponding to the optimal portfolio | |

| , | Defined as for a portfolio a and for the optimal one |

| , | Variance matrix in the nominal and in the alternative model |

| Variance parameter | |

| Measure of risk associated with and with parameter a | |

| Measure of risk in the special case with constant mean | |

| Stochastic asset returns |

Appendix A

In this appendix we prove Lemma 1 on the monotonicity of the relative entropy function. We also state and prove a technical Lemma, which is useful to compute the eigenvalues of the nominal variance-covariance matrix in the fully symmetric case.

Proof of Lemma 1. For any value of a and s.t. a solution (10), we get

We now study the behaviour of this function. First, we notice that the function is continuous s.t. is well-defined. Then, to evaluate the slope of the relative entropy, we compute the first derivative. Supposing to choose within a class of sufficiently regular functions, we can exchange the derivative with the expected value (cf. e.g., Protter and Morrey 2012, Th.4, p.429). We get

| (42) |

where is the variance of in the alternative measure.

Being the variance non-negative, the sign of the derivative, i.e. the slope of the relative entropy function, depends only on the sign of and the relative entropy is a monotone increasing function for positive values of , and a monotone decreasing function for negative

Lemma 13

Given a matrix with two values, on the diagonal and extra-diagonal, i.e. of the form

has an eigenvalue with eigenvector with constant weights and the remaining eigenvalues .

Proof. We write as

We simply have to find eigenvalues of because the eigenvalues of are the sum of eigenvalues of and . The matrix has one eigenvalue equal to corresponding to the eigenvector . The remaining eigenvalues are all with eigenvectors equal to any basis of the kernel (due to the rank-nullity theorem). We then get the eigenvalues and the eigenvectors of