Distributionally Robust Inference for Extreme Value-at-Risk††thanks: SS and DC were partially funded by the NSF grants DMS-1830293 and DMS-1243102, respectively.

Abstract

Under general multivariate regular variation conditions, the extreme Value-at-Risk of a portfolio can be expressed as an integral of a known kernel with respect to a generally

unknown spectral measure supported on the unit simplex. The estimation of the spectral measure is challenging in practice and virtually impossible in high dimensions.

This motivates the problem studied in this work, which is to find universal lower and upper bounds of the extreme Value-at-Risk under practically estimable constraints. That

is, we study the infimum and supremum of the extreme Value-at-Risk functional, over the infinite dimensional space of all possible spectral measures that meet a finite set of

constraints. We focus on extremal coefficient constraints, which are popular and easy to interpret in practice. Our contributions are twofold. First, we show that

optimization problems over an infinite dimensional space of spectral measures are in fact dual problems to linear semi-infinite programs (LSIPs)

– linear optimization problems in Euclidean space with an uncountable set of linear constraints.

This allows us to prove that the optimal solutions are in fact attained by discrete spectral measures supported on finitely many atoms. Second, in the case of balanced

portfolia, we establish further structural results for the lower bounds as well as closed form solutions for both the lower- and upper-bounds of extreme Value-at-Risk in the

special case of a single extremal coefficient constraint. The solutions unveil important connections to the Tawn-Molchanov max-stable models. The results are illustrated

with two applications: a real data example and closed-form formulae in a market plus sectors framework.

Keywords: value-at-risk, extreme value-at-risk, distributionally robust, regular variation, Tawn-Molchanov, linear semi-infinite programming, extremal coefficients.

1 Introduction

Value-at-Risk (VaR) is one of the predominant risk measures used in determining minimum capital requirements placed upon financial institutions in order to cover potential losses in the market. In essence, VaR is the largest loss having a ‘reasonable chance’ of occurring through the placement of a risky bet. Formally, if a random variable represents a loss (negative return) on an asset after a fixed holding period, and is a probability representing ‘reasonable chance’, we have the following definition

Definition 1.1.

The Value-at-Risk of a random variable at the level denoted is defined as

That is, is the (generalized) -th percentile of the loss distribution.

In practice, financial institutions deal with a multi-dimensional portfolio of statistically dependent losses . In this case capital requirements should be determined by the value-at-risk for the sum of losses , where . In these scenarios it is essential to account for tail dependence in the components of , see e.g., Embrechts et al [12]. Furthermore, regulatory guidelines such as Basel III [2] typically prescribe . Hence, the scenario of extreme losses where is close to the value is of great interest. Specifically, one is interested in extreme VaR. Namely, fix a reference asset . Mild multivariate regular variation conditions on the distribution of , imply the existence of the limit:

| (1.1) |

Following the seminal works of [3] and [12], we shall refer to the limit ratio as to extreme VaR. It is desirable to be able to bound the extreme VaR coefficient since it provides the first order approximation of value-at-risk:

The general goal of this paper is to determine lower- and upper-bounds for extreme VaR under natural constraints on the portfolio. This should be contrasted with the statistical problems of estimation of VaR or extreme VaR. Here, we would like to understand and characterize the best- and worst-case scenaria for extreme VaR among all possible models for the joint (asymptotic) dependence of the losses subject to certain classes of constraints. In this sense, the type of problem we study is a constrained and extremal version of the so-called Fréchet optimization problems investigated in [28] and recently in [25, 29].

Our motivation stems from potential insolvency in insurance and financial sectors due to catastrophic loss. In this setting, data on extreme portfolia losses are scarce or non-existent. Thus, conventional statistical estimation methods are either difficult to justify or in fact inappropriate for the estimation of extreme VaR. At the same time, adopting a specific parsimonious model amounts to imposing (explicitly or implicitly) constraints on the asymptotic dependence of the assets. This can lead to significantly under- or over-estimating the portfolio risk. Such types of challenges motivate us to adopt an alternative perspective of distributionally robust inference. That is, we provide upper- and lower-bounds valid under all possible extremal dependence scenarios. Our framework allows the practitioners to incorporate either quantitative constraints on easy-to-estimate extremal dependence coefficients or qualitative/structural information such as (partial) extremal independence of the portfolio.

Value-at-Risk has been studied extensively in the literature. Important theoretical aspects such as the in-coherence of VaR [1] and its elicitability [35], for example, are well-understood. At the same time, advanced statistical methodology for the estimation of VaR has been developed accounting for both complex temporal dependence and heavy-tailed marginal distribution of the losses (see e.g., the monograph [22]). Advanced methods for the statistically robust estimation of VaR [10] exist. The notion of robust statistical inference should be distinguished from our use of the term distributionally robust inference. In the former, robustness refers to resilience to outliers in the data within a specified model, in the latter, distributionally robust context, the goal is to guard against mis-specifications of the model. While this perspective has been very popular and actively studied in the optimization community (see e.g., [4] and the references therein), only a handful of studies adopt this philosophy in the context of risk measures (see e.g. [20, 13, 5, 8]). To the best of our knowledge, our work is the first to address the general context of extreme VaR for a multi-dimensional portfolio under extremal coefficient constraints. To be able to describe our contribution, in the following Section 1.1, we review some important concepts and notation. A summary of our results is given in Section 1.2.

1.1 Notation and preliminaries

Regular variation. Recall that a random vector is said to be multivariate regularly varying (RV), if there exists a non-zero Borel measure on and a sequence , such that

| (1.2) |

for all -continuity sets bounded away from the origin.

The measure in (1.2) necessarily satisfies the scaling property:

| (1.3) |

for some fixed positive constant . We shall write and refer to as the index of regular variation of the portfolio . It also follows that the normalization sequence is regularly varying with index , i.e., for all , we have . The index does not depend on the choice of the normalization sequence , and the measure is also essentially unique up to a positive multiplicative constant. For more details, see the Appendix A below and the monograph [27].

The scaling relation (1.3) entails that can be conveniently factorized in polar coordinates:

where and are the radial and angular components of , relative to any (fixed) norm in . Here, is a finite positive measure on the unit sphere , referred to as a spectral measure of the vector . It is unique up to rescaling by a positive multiplicative factor.

For simplicity, we shall focus here on the case of non-negative losses, i.e., when takes values in the orthant , use the -norm

and adopt the following.

Assumption 1.2.

Suppose that , where the measure is not entirely supported on the hyper-planes .

This assumption implies that each of the components is heavy-tailed with the same tail index . Indeed, by choosing , in (1.2), and using the scaling property (1.3), we obtain that for all ,

| (1.4) |

where is the asymptotic scale coefficient of . Relation (1.4) implies in particular that the moment is infinite if and finite if . The finite-mean case where is of primary interest in practice. Therefore, we shall assume throughout that

In the infinite-mean case an intriguing anti-diversification phenomenon arises (cf Appendix A.4 below.)

Remark 1.3.

Assumption 1.2 is not very restrictive. Indeed, it implies that all assets have asymptotically equivalent tails. Had this not been the case, only the assets with the heaviest tails would dominate and determine the asymptotic tail behavior of the cumulative loss . Thus, when studying extreme VaR, without loss of generality one can focus on the sub-set of losses with heaviest tails.

We also standardize the assets to have equal, unit scales such that (1.4) holds with

| (1.5) |

This standardization does not restrict generality since one can consider the weighted portfolio

with suitable positive weight vector .

Finally, to separate the roles of the tail behavior and asymptotic dependence, it is convenient to consider the vector

| (1.6) |

It can be readily shown that , where and .

Extreme VaR formula. Now, under the established notation and conditions, Relation (A.10) and Proposition A.6 below imply that (1.1) holds. That is, extreme VaR is well-defined, and it has, moreover, the following closed-form expression:

| (1.7) |

where is the unit simplex in .

Here is the (unique) spectral measure of the vector satisfying the marginal moment constraints

| (1.8) |

Note that since we have

Well-known Hoeffding-Fréchet type universal bounds on the value of are given by

| (1.9) |

(see e.g. Corollary 4.2 in Embrechts et al [12]). These inequalities follow readily from (1.7).

The lower bound in (1.9) corresponds to (asymptotic) independence and the upper bound to complete tail dependence, where all components of the vector are asymptotically identical. This agrees with our intuition about diversification, where holding independent assets leads to the lowest value of extreme VaR, while complete dependence corresponds to the worst case of risk. Surprisingly, this intuition is reversed in the infinite-mean regime (see Appendix A.4 below.)

Extremal coefficients. The Hoeffding–Fréchet type bounds in (1.9) are rather wide. In practice, however, the range of possible values can be significantly reduced under suitable constraints on the extremal dependence of the portfolio. In this work, we focus on so-called extremal coefficient constraints, which capture (in a rough sense) the strength of tail dependence amongst a given subset of assets in the portfolio .

Specifically, for any non-empty set of assets by taking , in Relation (1.2), we obtain

where is now the asymptotic scale coefficient of the maximum loss over . The coefficients will be referred to as extremal coefficients of the portfolio . By Lemma A.7 below

| (1.10) |

where is the same spectral measure appearing in (1.7). This, in view of (1.8), readily implies

| (1.11) |

where is the size of the set . The upper bound is attained when the ’s are asymptotically independent, while the lower bound corresponds to the case of perfect asymptotic dependence, e.g., , for .

The extremal coefficients naturally encode a great variety (although not all) extremal dependence relationships among the assets. For example, the classic upper tail dependence coefficient is expressed as follows

for all , where denotes the cumulative distribution function of a random variable . In this case, the bounds (1.11) amount to , where corresponds to asymptotic independence and to perfect asymptotic dependence.

As another example, the -variate extremal coefficient

| (1.12) |

takes values in the range . It quantifies the degree to which all assets in the portfolio experience an extreme loss simultaneously. For example, equals under perfect asymptotic dependence (e.g., ) and it equals if the assets are asymptotically independent with equal scales.

1.2 Summary of our contributions

In view of (1.7) determining the best- and worst-case extreme VaR scenaria amounts to solving a pair of infinite-dimensional optimization problems over a space of admissible spectral measures . Namely, we consider a large family of spectral measures and posit the optimization problems

| (1.13) |

where

Then, in view of (1.7), we obtain the following universal lower and upper bounds for extreme VaR:

| (1.14) |

If the class includes all admissible (normalized) spectral measures, these bounds can be rather wide (see Relation 1.9), which may limit their practical value in establishing capital requirements. As indicated, we consider classes of all possible spectral measures that satisfy extremal coefficient constraints such that

for a given family of non-empty subset of assets . The standardization (1.5) corresponds to the singleton sets and , which for our applications, will be always included as constraints.

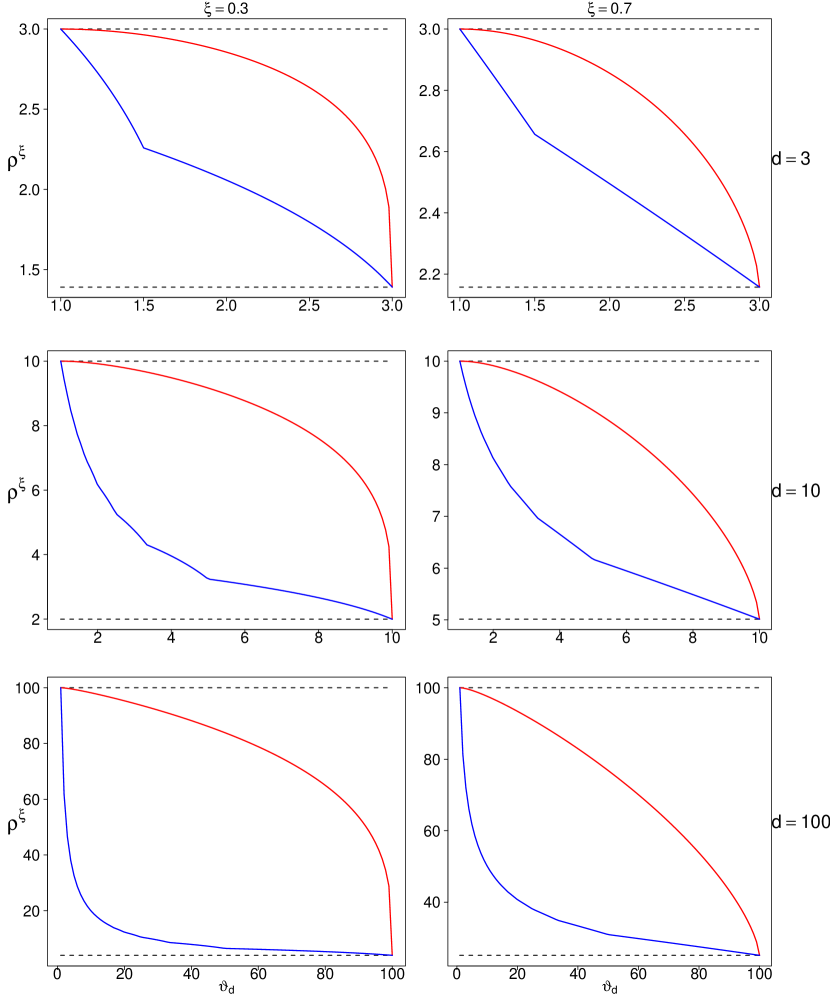

The constants can be either estimated or assigned by a domain expert. They can be used to encode structural information such as asymptotic independence (cf Section 4.2, below). Figure 1 illustrates that the knowledge of the single -variate extremal coefficient constraint in (1.12) can dramatically reduce the range of all possible extreme VaR , even in dimensions as high as .

Contributions. Observe that both the objective function in (1.7) and the constraints in (1.10) are linear in the parameter . The challenge is, however, that takes values in an infinite-dimensional space of measures. Our findings can be summarized by three main themes:

Optimal measures have finite support. We establish structural results showing that the infimum and supremum of are attained by discrete measures that are supported on a finite set of atoms. In each case, the number of atoms is not more than the number of constraints (Theorem 3.2). Thus, in principle, the linear infinite-dimensional problems reduce to non-linear finite-dimensional optimization problems. These results stem from a fundamental connection with the theory of linear semi-infinite optimization outlined in Section 2.2 below.

A Tawn-Molchanov minimizer and a convex maximizer. Surprisingly, the infimum of and in turn the lower bound on is attained by measures with the same support as the celebrated Tawn-Molchanov models in Strokorb and Schlather [34]. This allows us to further reduce the optimization to a linear program, which can be solved exactly using conventional linear solvers in moderate dimension. We also establish that the maximization problem reduces to an ordinary convex optimization problem which can be solved in polynomial time within arbitrary precision. Efficient solvers for these optimization problems have yet to be implemented, nevertheless our theoretical results suggest that they can be efficiently solved.

Closed form solutions. Finally, in the case of a single -variate constraint, we establish closed form expressions for both the lower- and upper-bounds, which are valid in arbitrary dimensions. These formulae were used in Figure 1 and further leveraged in Section 4.2 to illustrate how conditional independence can lead to very substantial reduction of the range of extreme VaR.

The rest of the paper is structured as follows. Section 2 reviews key results from the theory of linear semi-infinite programming (LSIP) and demonstrates that our optimization problem can be viewed as a dual of a LSIP. This connection is further explored in Section 3, where the main results on the general characterization of the spectral measures attaining the minimum and maximum extreme VaR are presented. Section 3.2 proceeds with more detailed results on in the cases of the Tawn-Molchanov minimizer and our closed form solutions. Section 4 briefly illustrates the established theory. In Section 4.1, using a data set of industry portfolia, we show how utilizing all bi-variate extremal coefficient constraints can lead to tight bounds on extreme VaR, which are in close agreement with semi-parametric estimates obtained using Extreme Value Theory. In Section 4.2, we provide a practical application of the closed-form formulae for the bounds on extreme VaR in a context of a market and sectors model. This demonstrates, how expert knowledge on the structure of the market can be encoded via extremal coefficient constraints in cases where data may be scarce. The proofs and auxiliary facts from optimization are collected in the Appendix.

2 A Connection to Linear Semi-Infinite Programming

In this section, we will show that our optimization problems are in fact duals to linear semi-infinite programming (LSIP) problems. This will lead to profound structural results and certain closed-form solutions for upper and lower bounds on extreme VaR.

2.1 Problem formulation

Recall that we want to solve the pair of optimization problems:

| (2.1) | |||||

| (2.2) | |||||

| subject to: | (2.3) |

where , is a collection of non-empty subsets of indices ; the functional is in (1.7); and the supremum and infimum are taken over all finite measures on that satisfy the extremal coefficient constraints in (2.3).

Remark 2.1.

Extremal coefficients are only summary, moment-type functionals, and they alone do not fully characterize the spectral measure , except in special cases [34]. In general, however, it is not known to what extent the full or partial knowledge of the extremal coefficients confine the set of possible values of and hence extreme VaR. This is one of the motivations for our work.

Assumption 2.2.

We assume that the marginal constraints (1.8) are always included in (2.3) by requiring that the singletons belong to and for To avoid further situations that result in trivial optimization problems, we also assume is sufficiently rich such that

In particular, this holds if includes all pairs or the set .

2.2 Linear semi-infinite programming

The purpose of this section is to review definitions and notations from the field of linear semi-infinite programming (LSIP) that we will use throughout this paper (see also Appendix B.1). Our main contributions in the following Section 3 such as the existence of solutions to and with finite support (reducibility) and and exact formulae for the optimum will leverage powerful results from this established theory. Those interested in a more comprehensive treatment is referred to the monograph of Goberna and Lopez [16] as well as the review by Shapiro [33]. See also [15] for a survey of recent advancements in LSIP.

Formulation. Linear semi-infinite programs are formulated as follows:

| subject to: |

where is a (possibly infinite) index set. For a given mathematical program, say , we use the notation to denote its optimal value while denotes the solution set, i.e. the set of feasible points that yield optimal values. Generally, may be infinite and my be empty. If , then by convention and we say is unsolvable.

The following assumption establishing the continuity of (in the language of LSIPs) has far reaching consequences in terms of the structure of solutions to .

Assumption 2.3.

In , we suppose is a compact subset of and , are continuous and hence bounded on .

Thus, we define the Lagrangian of problem as the function

| (2.4) |

where is the space of finite (non-negative) Borel measures on .

Remark 2.4.

Remark 2.5.

Duality. We define the dual function as

The dual function yields a lower bound on the optimal value of . Indeed, by , for any feasible , it follows that

which implies

| (2.5) |

The fact that the feasible was arbitrary implies This inequality is trivial unless . Indeed, otherwise if , then for some we have , and hence by Assumption 2.3, it follows that .

Therefore, only measures for which holds are of interest and they are referred to as dual feasible. Thus we arrive at the following dual problem:

| subject to: |

In view of (2.5), we have that

| (2.6) |

A common task with many optimization problems is to determine the existence (or non-existence) of a duality gap, . If , then it suffices to solve either or to obtain the optimal value, so long as both problems are solvable. The condition with is known as strong duality. If is solvable, i.e. , then under assumption 2.3, a sufficient condition for strong duality of is Slater’s Condition, i.e. there exists such that

| (2.7) |

See Theorem 2.3 in [33] for further details on Slater’s condition and strong duality for LSIPs.

The above discussion reveals a fundamental connection between the two optimization problems in (2.1) and (2.2) and the theory of LSIP.

Corollary 2.6.

The problem of finding the upper bound in (2.2) under extremal coefficient constraints (2.3) is the dual to an LSIP problem , where

Similarly, the problem of finding the lower bound in (2.1) is the dual of an LSIP involving maximization, where formally ‘’ is reduced to ‘’ by changing the sign of the objective function.

This connection allows us to employ powerful results from the LSIP theory discussed next.

Reducibility. The following discussion lays the groundwork for establishing the finite support of optimal solutions to and . Consider a finite index set with Solving problem when the constraints are restricted to the finite set reduces to a standard linear program

| subject to: |

which yields the corresponding dual

| subject to: |

Problem is called a discretization of . The feasible set for is contained in the feasible set for . Hence, If for every , there exists such that than we say is discretizable. Whereas, if there exists such that then is said to be reducible. In this case, on the language of measures, the optimum is attained by a discrete measure with a finite support .

Remark 2.7.

Even if an LSIP is theoretically reducible, it may be challenging to find the actual support set of an . This is because finding the support amounts to solving a non-linear optimization problem.

The following proposition establishes conditions for the reducibility of the LSIP .

Proposition 2.8 (Theorem 3.2 in [33]).

Suppose that for problem , Assumption 2.3 holds and . If for any , there exists such that

| (2.8) |

Then there exists with such that for corresponding discretizations and

Note that if Slater’s condition holds for , then (2.8) is satisfied. Which yields the following corollary

Corollary 2.9.

If Assumption 2.3 holds for , and Slater’s condition holds, then there exists a (strong) dual pair and such that is finitely supported on at most atoms .

3 Main results

3.1 Optimal measures with finite support

In this section, we establish general structural results for problems and by exploiting their duality to linear semi-infinite programs (LSIPs) discussed above. We show that the optimum are attained by measures with finite support and we prove that is equivalent to a finite dimensional convex optimization problem, which can be solved in polynomial time.

Theorem 3.1.

If Assumption 2.2 holds, then there exist (primal) linear semi-infinite programs and , whose dual problems are and , respectively. Furthermore, for and , we have:

(i) Assumption 2.3 is satisfied.

(ii) The Slater condition holds.

(iii) The optimal values are finite.

(iv) Strong duality holds for the pairs and .

(v) The problems are reducible.

(vi) There exists solutions to and that are supported on at most atoms.

Proof.

We consider only problems and . The arguments for and are similar.

Let and Define the continuous functions ,

Consider the linear semi-infinite program

| (3.1) | |||||

| subject to: |

Letting denote the space of finite Borel measures on , by the Lagrangian duality theory discussed in Section 2.2, it follows that the dual of is

| subject to: |

which is in fact problem in (2.2). This establishes the desired duality of to the above LSIP .

Now, observe that satisfies Assumption 2.3, since is compact and the functions and are continuous on . This proves (i).

The fact that Theorem 3.1(vi) implies that the optimal values of and can be achieved by measures concentrated on at most atoms leads to the following characterization of and .

Theorem 3.2.

Recall the extremal coefficient constraints in (2.3) for problems and . Define the set of non-negative matrices

| (3.3) |

Then, by letting , we have

Proof.

Theorem 3.1(vi) implies that there exists a discretization with such that The last statement means that there exist such that

| (3.4) | |||||

making the change of variables gives

Thus we have proved the result for The proof for follows by replacing with . ∎

The consequence of Theorem 3.2 is that the linear semi-infinite optimization problems and may be reduced to finite yet non-linear optimization problems. Fundamentally, there is tradeoff between linearity in the semi-infinite case, versus non-linearity in the finite case, amounting to having to search for the finite support of the optimal measures in and . This is because both the objective function and the constraints now depend on the unknown set of support points , in Relation (3.4) in a non-linear fashion. Note however that the size of the unknown support is no greater than the number of constraints, which is one of the appealing consequences of Theorem 3.1 (vi).

In the case of , implies that is a convex function. This, together with the fact that is a convex set means that is a convex optimization problem. Hence can be solved to within arbitrary precision in polynomial time[6]. In-practice, an exact and efficient solver for still needs to be developed and is outside the scope of this work.

In the case of , implies is non-convex and generally more challenging. However, if one makes a further assumption of balanced portfolio, i.e. the weights in are equal , then further solutions are readily available as discussed in the following section.

3.2 Solutions for balanced portfolia

In this section, we provide further structural results and closed form solutions in the important special case of balanced portfolia, where :

| (3.5) |

Remark 3.3.

We show first that the minimization problem reduces to a standard linear program. Interestingly, is attained by spectral measures corresponding to the celebrated Tawn-Molchanov max-stable models [34]. This leads to efficient and exact solutions in practice for moderate number of constraints and dimensions.

The second contribution are exact formulae for both the lower and upper bounds on in the case when we impose only one constraint on the -variate extremal coefficient

in addition to the standard marginal extremal coefficient constraints. These results are possible thanks to the symmetry in the objective function when all portfolio weights are equal. Their proofs are given in Appendix B.

Theorem 3.4 (Tawn-Molchanov Minimizer).

Under assumption (3.5), we have

This result shows that obtaining the lower bound for extreme VaR in the case of a balanced portfolio amounts to solving a high-dimensional but standard linear program.

Remark 3.5.

From the proof of Theorem 3.4, it follows that the lower bounds for extreme VaR in balanced portfolia are attained by spectral measures supported on the set of vectors

Such types of spectral measures correspond to the Tawn-Molchanov max-stable model [34]. This is an interesting finding since, as shown in the last reference, the Tawn-Molchanov max-stable models are maximal elements with respect to the lower orthant stochastic order, for the set of all max-stable distributions sharing a fixed set of extremal coefficients. Theorem 3.4, however, is not a consequence of the lower orthant order dominance and its proof is based on optimization results.

Remark 3.6 (terminology).

According to a personal communication with Dr. Kirstin Strokorb, the Tawn-Molchanov or more completely Schlather-Tawn-Molchanov max-stable model originates in the works of [32] and [23]. In the work [24] it is shown to arise from a Choquet integral and is therefore more descriptively referred to as a Choquet max-stable model.

Closed form solutions. Next, we focus on the case of a single constraint, involving the extremal coefficient associated with the entire set That is, the extremal coefficient constraints (2.3) in and are given by

| (3.7) |

where . The following results show that in this special case, exploiting the symmetry in the constraints yields closed form solutions for both and .

Theorem 3.7 (lower bounds).

Let , Under assumption (3.7), for all , we have that is given by the piecewise linear function:

| (3.8) |

Theorem 3.8 (upper bounds).

Under assumption (3.7), for all , we have

| (3.9) |

The bounds in (3.8) and (3.9) can be computed for arbitrary dimension and all tail index values . The results shown in Figure 1 show that the information about extreme VaR provided by a single d-variate extremal coefficient increases with the tail index and decreases with dimension . More concretely, computing the maximum width of the bounds using the closed form solutions and comparing to the width of the universal dependance bounds allow us to show that even in the high-dimensional setting of , with realistic tail exponent , the knowledge of a single -variate extremal coefficient always reduces the range of uncertainty of extreme VaR by at least . This is a remarkable fact given that no other assumptions on the asymptotic dependence are imposed.

4 Applications

The goal of this section is to briefly illustrate the theoretical structural results as well as closed-form formulae established above. We start with a quantitative example of a -dimensional industry portfolio, where the bi-variate constraints are estimated from data. Then, in Section 4.2, we demonstrate how extremal coefficient constraints can be used to encode qualitative structural information and arrive at practical closed-form formulae.

4.1 An illustration: Scale-balanced industry portfolia

In this section, we briefly sketch an application of the above general results using a -dimensional portfolio of daily returns for industries available in [14]. The portfolio is obtained by assigning each of the stocks in NYSE, AMEX, and NASDAQ to one of the ten industries and then their average is computed. Then, a vector time-series of daily returns in percent are computed. We shall focus on the vector time-series of losses (negative returns) and study their extreme value-at-risk. We first argue that it is reasonable to model the (multivariate) marginal distribution as regularly varying. To this end, we briefly recall the standard peaks-over-threshold methodology used to estimate the tail index and scale of the losses.

Let the random variable represent the loss of an asset. The Pickands-Balkema-de Haan Theorem (see e.g. Theorem 3.4.13 and page 166 in [11]) implies that under general conditions, there exist normalizing constants , such that

as , where is the upper end-point of the distribution of . Here is a shape parameter referred to as the tail index and . This result suggests that the conditional distribution of the distribution of the excess over a large threshold can be approximated with the so-called Generalized Pareto (GP) distribution, i.e.,

The case corresponds to heavy, power-law tails; (interpreted by continuity) is the Exponential distribution and is a distribution with bounded right tail. In practice, one picks a large threshold , focuses on the part of the sample exceeding , and estimates the tail index and scale parameter via maximum likelihood applied to the excesses. (In the presence of significant temporal dependence, extremes tend to cluster, i.e., losses occur in batches. In this case, an important methodological step is to de-cluster the exceedances, i.e., to pick one observation from each cluster or otherwise reduce the dependence (see, e.g., [7]). In our case, declustering had virtually no effect on the estimates.

Table 1 shows the tail index and scale estimates along with their standard errors for each of the industries. They were obtained by fitting a GP model via the method of maximum likelihood to the excesses over the th empirical quantile, for each of the daily loss time series. The first important observation is that all losses are heavy tailed, where the tail index estimates are not significantly different. Indeed, the p-value of a chi-square test for equality of means applied to the tail index estimates (assuming normal approximation) is . On the other hand, the scales are significantly different with p-value . While these marginal estimators are dependent and the chi-square test is likely to be conservative. Therefore, with some confidence we can assume that the daily losses have a common tail index and are multivariate regularly varying. Furthermore, the GP tail asymptotics entail

| (4.1) |

where .

| NoDur | 0.21 | 0.06 | 0.77 | 0.05 |

| Durbl | 0.18 | 0.06 | 1.32 | 0.10 |

| Manuf | 0.22 | 0.06 | 1.06 | 0.08 |

| Enrgy | 0.19 | 0.05 | 1.05 | 0.07 |

| HiTec | 0.13 | 0.05 | 1.29 | 0.09 |

| Telcm | 0.22 | 0.05 | 0.84 | 0.06 |

| Shops | 0.20 | 0.06 | 0.92 | 0.07 |

| Hlth | 0.25 | 0.06 | 0.92 | 0.07 |

| Utils | 0.14 | 0.05 | 1.21 | 0.08 |

| Other | 0.14 | 0.06 | 1.25 | 0.09 |

In order to apply our closed-form solutions from Section 3.2, we consider the balanced portfolio

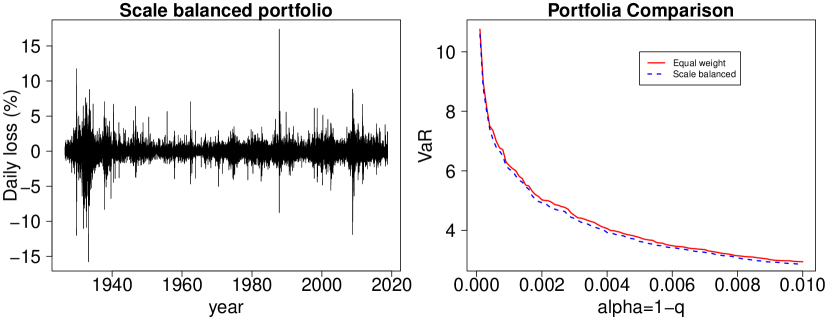

where . Thus, the scales of all assets are balanced so that as . Figure 2 (left) shows the time series of daily losses for the scale-balanced portfolio. The right panel therein shows the empirical value-at-risk as a function of for the balanced as well as for the equally weighted portfolio .

Observe that the VaR of the balanced portfolio is always lower (by about 1% to 4.5%) for a wide range of risk levels . This difference is significant and indicates that the balanced portfolio is preferable in practice. The reduction of risk may be explained by the fact that the extremal dependence in the assets is relatively balanced. Had there been a group of industries which were significantly more dependent than the rest, the scale-balanced portfolio might not have outperformed the equally weighted one. In such a case, one should balance the marginal risk (through the scales) as well as consider diversification due to extremal dependence. Such portfolio optimization problems can be considered with the same tools that we employed here but they go beyond the scope of the present study.

Now, for the scale-balanced portfolio, the marginal constraints are met and one has

| (4.2) |

where with as in (1.7). Theorems 3.7 and 3.8 yield closed-form expressions for the upper and lower bounds on as a function of the single -variate extremal index . On the other hand, Theorem 3.4 shows that the lower bound on can be obtained by solving a linear program. We used empirical estimates of the -variate and all bi-variate extremal coefficients of the scale-balanced portfolio based on the th empirical quantiles (see Table 4 below and Section A.2 for more details). These estimates are in fact valid extremal coefficients in the sense of Remark 2.1 (see Remark A.3, below). The resulting bounds are given in Table 2. Observe that the additional information in the bi-variate extremal coefficients substantially narrows the gap between the bounds based on a single constraint. At the same time, relative to the wide Fréchet bounds, the improvement in the bounds due to single d-variate extremal coefficient is remarkable.

| Constraints | Lower bound | Upper bound |

|---|---|---|

| Single d-variate | 4.1219 | 9.7818 |

| All bi-variate | 6.6852 | – |

| Fréchet bounds (no constraints) | 1.5782 | 10 |

Finally, to obtain the estimate of in (4.2), one needs to calculate the baseline . We did so using empirical quantiles and also from the Generalized Pareto tail approximation in (4.1), which entails

where and is obtained through ML by assuming that the excess losses of all time series have a common tail index but different scales.

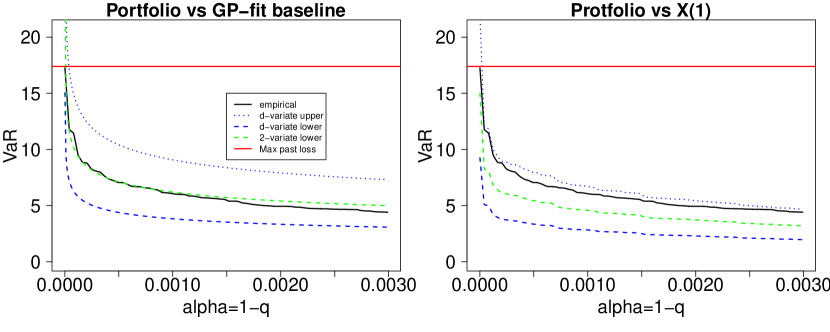

Figure 3 shows the upper and two types of lower bounds on as a function of . The empirical portfolio VaR is also given (solid line). The bounds in the left panel are relative to the baseline value-at-risk computed from the Generalized Pareto model approximation, while in the right panel is replaced by the corresponding empirical quantile. Relative to the GP-fit baseline, the empirical portfolio VaR is within the upper and the larger lower bound (green dashed line) for extreme loss levels . It falls slightly below the lower bound based on bi-variate extremal coefficient constraints for less-extreme loss levels, which can be attributed to both variability in the constraints estimates and uncertainty in the GP model. Nevertheless, the agreement is remarkable, especially for extreme loss levels where the asymptotic approximation kicks-in. In the right panel the bounds are relative to the empirical value-at-risk baseline. In this case, the portfolio VaR is always enclosed between the bi-variate lower bound and the d-variate upper bound and in fact the gap between them is more narrow relative to that in the left panel. This illustrates that the asymptotic approximation is quite accurate for a wide range of extreme quantiles and that the extremal coefficient constraints capture well the extremal dependence between the assets in the portfolio. One advantage of the GP-fit baseline however is that one can extrapolate the bounds on the portfolio VaR beyond the historically available quantile levels.

| Return levels (years) | 10 | 100 | 1000 |

|---|---|---|---|

| d-variate upper | 10.90 | 17.20 | 27.14 |

| d-variate lower | 4.59 | 7.25 | 11.44 |

| bi-variate lower | 7.45 | 11.75 | 18.55 |

Indeed, Table 3 provides bounds on the , and -year return levels, where a year is assumed to have trading days. These results indicate for example that one should expect to encounter daily losses exceeding once in years on the average, even for the relatively diversified scale-balanced portfolio, but daily losses of or more are unusual 1-in-a-100 year type events. Even though these results hinge on the assumption of stationarity in the extremal dependence structure, they provide novel distributionally robust bounds of extreme portfolio or insurance risk and can be used to validate most if not all other model-based estimators of extreme value-at-risk.

| NoDur | Durbl | Manuf | Enrgy | HiTec | Telcm | Shops | Hlth | Utils | Other | |

|---|---|---|---|---|---|---|---|---|---|---|

| NoDur | 1.00 | 1.46 | 1.37 | 1.50 | 1.48 | 1.54 | 1.38 | 1.44 | 1.48 | 1.40 |

| Durbl | 1.46 | 1.00 | 1.30 | 1.50 | 1.46 | 1.58 | 1.44 | 1.57 | 1.46 | 1.35 |

| Manuf | 1.36 | 1.29 | 1.00 | 1.43 | 1.40 | 1.53 | 1.36 | 1.49 | 1.40 | 1.26 |

| Enrgy | 1.49 | 1.50 | 1.43 | 1.00 | 1.60 | 1.61 | 1.52 | 1.60 | 1.54 | 1.47 |

| HiTec | 1.48 | 1.45 | 1.40 | 1.60 | 1.00 | 1.55 | 1.43 | 1.55 | 1.47 | 1.45 |

| Telcm | 1.53 | 1.58 | 1.54 | 1.61 | 1.55 | 1.00 | 1.55 | 1.60 | 1.61 | 1.52 |

| Shops | 1.37 | 1.44 | 1.36 | 1.52 | 1.43 | 1.55 | 1.00 | 1.48 | 1.47 | 1.38 |

| Hlth | 1.43 | 1.56 | 1.49 | 1.60 | 1.55 | 1.60 | 1.48 | 1.00 | 1.60 | 1.54 |

| Utils | 1.47 | 1.46 | 1.40 | 1.55 | 1.47 | 1.61 | 1.47 | 1.60 | 1.00 | 1.44 |

| Other | 1.39 | 1.35 | 1.26 | 1.47 | 1.45 | 1.52 | 1.38 | 1.54 | 1.44 | 1.00 |

4.2 Market and sectors framework

While the quantitative methods in previous section based on the knowledge of all bi-variate constraints yield tight bounds, their use in practice is limited to small and moderate dimensions due to practical challenges in solving the optimization problems. In this section, our goals is two-fold. First, we illustrate how one may encode structural/expert knowledge through extremal coefficient constraints. Secondly, we show that the closed-form expressions in Theorems 3.7 and 3.8 can lead to practical and tight bounds on extreme VaR in high-dimensions, where numerical optimization is either challenging or impossible.

We do so over a simple but instructive ‘market plus sectors’ framework. Namely, suppose that the vector of portfolio losses is regularly varying with index and standardized marginal scales in the sense of (1.5).

Let , and suppose that

| (4.3) |

where and are independent and also regularly varying with index and asymptotically standardized margins (as in (1.5)). The components and represent the overall market and individual sector-specific risks, respectively.

We shall assume that the market risk affects all stocks and therefore model it as asymptotically completely dependent, i.e.,

We shall also assume that is partitioned into independent sub-vectors , each corresponding to a sector. That is, and

where are pairwise disjoint sets of indices.

Relation (4.3) leads to a simple but natural 2-tier asymptotic dependence structure. The parameter controls the proportion of risk due to overall market-wide events, while the individual sectors may experience independent, and largely arbitrary internal risk exposures accounted for by the sector-specific component. We demonstrate next how the closed form formulae in Theorems 3.7 and 3.8 lead to tight lower- and upper-bounds on extreme VaR for the portfolio .

Using the independence of the market and the sectors, it can be shown that:

| (4.4) |

where with the corresponding sub-script is the properly normalized spectral measure of the corresponding vector , where we naturally embed into the higher-dimensional space .

In view of (1.7), Relation (4.4) entails

where , , and are the corresponding -functionals of the overall portfolio, its market, and sector components, respectively.

Notice that , for all non-empty sets , since the market factor is completely dependent.

These decomposition results allow us to obtain closed-form lower- and upper-bounds on in terms of and . Indeed, we have:

| (4.6) |

Now, using the closed-form expressions for for each of the sectors based on the single -variate constraint , for , we obtain

| (4.7) |

where and denotes either the lower- or upper-bound formulae from (3.8) or (3.9).

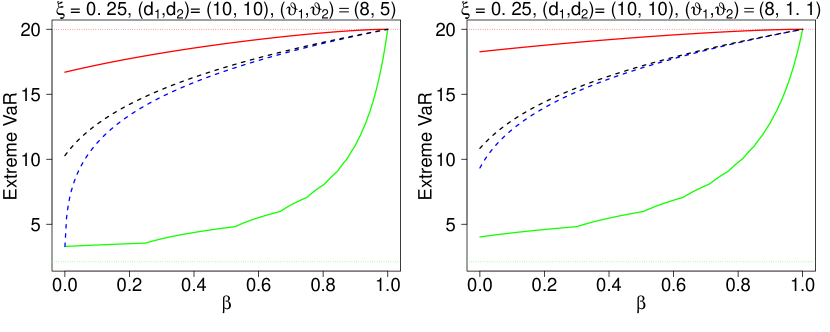

Figure 4 illustrates the significant reduction in the range of possible extreme VaR values based on the above setup for a range of -values. We have the simple partition into sectors and . Considered are two cases where the within-sector -variate extremal coefficients in (4.6) are (left panel) and (right panel). In both cases . The dotted horizontal lines indicate the Hoeffding-Fréchet bounds on extreme VaR. The solid green and red lines correspond to the exact lower/upper bounds obtained by imposing a single -variate constraint with

Finally, the dashed blue/black lines correspond to the lower/upper bounds for obtained by using the decomposition into a single market factor effect plus independent sector-specific risks. Observe the significant reduction in the range of possible values for extreme VaR. This is naturally attributed to the assumption of independence among the sectors. The presence of a single asymptotically completely dependent market factor, however, can make this range approach the ultimate upper bound for . Alternatively, if the proportion of the market risk is low (), the lower bound approaches the ultimate single d-variate constraint lower bound (solid green curve) in the left panel. In the right panel, however, one observes a non-trivial gap between the two lower bounds at . This can be attributed to the fact that the constraint is rather close to complete dependence for the second sector, while the overall portfolio constraint on is far from complete dependence. Thus, the additional sector-specific information leads to far less optimistic lower bound on extreme VaR than in the market-structure-agnostic case.

The proportion of market-wide risk here was assumed to be known, for illustration purposes. Using (4.5), however, can be readily estimated in practice from an extremal coefficient involving a set of two or more sectors. For example, given and , we obtain

By elimination, these linear equations yield

5 Summary and discussion

Under the general assumption of multivariate regular variation, the extreme Value-at-Risk of a -dimensional portfolio, relative to a baseline asset, can be expressed as an integral functional with respect to a finite measure on the unit simplex. This, unknown (spectral) measure, is an infinite-dimensional parameter that encodes the complete extremal (joint) dependence structure of the assets in the portfolio. In practice, the conventional estimation of the spectral measure is challenging or impossible. This motivated us to adopt distributionally robust perspective. Namely, study the optimization problems of finding the infimum and supremum of the extreme VaR functional over large classes of possible spectral measures. Using popular and interpretable extremal coefficient constraints, we expressed the above optimization problems as duals to linear semi-infinite programs, which in turn were shown to have no duality gap. Thus, a number of results on the structure of spectral measures corresponding to the best- and worst-case extreme VaR were obtained. In the special case of scale balanced portfolia, we have also shown that the lower bound on extreme VaR corresponds to a spectral measure of the so-called Tawn-Molchanov multivariate max-stable model, which can be solved with conventional linear programs. We have also established surprising closed-form expressions for the lower- and upper-bound on extreme VaR under single -variate extremal coefficient constraints, valid in all dimensions . These results were further illustrated and extended in the case of the market-and-sectors framework. The theoretical results were shown to provide practical bounds in a limited real data example, and compared with conventional extreme value theory method.

Our contributions are mostly theoretical. However, the established results, formulae and methods are motivated by important challenges in quantifying model uncertainty when studying the risk of extremes in high-dimensional portfolia. To provide a complete practical methodology for risk assessment a number of implortant problems remain to be addressed. Namely,

-

•

Develop practical or approximate solvers for the optimization problems in dimensions .

-

•

Study the optimal set of constraints in terms of greatest reduction of the range of possible extreme VaR.

-

•

Quantify the uncertainty in the resulting lower- and upper-bounds on extreme VaR stemming from the statistical error in the estimation of the tail index and extremal coefficient constraints.

Finally, one very important open problem that stands out in our opinion is to establish closed form formulae in the case of single -variate constraints (as in Theorems 3.7 and 3.8) for a general un-balanced portfolio. Such formulae, by the method of partitioning, can lead to significant improvements on the range of extreme VaR similar to the ones obtained in Section 4.2.

Acknowledgements

We thank two anonymous referees and an Associate Editor for their constructive criticism, which helped us significantly improve the presentation. Section 4.2 was motivated by a question raised by a referee. We also thank Dr. Kirstin Strokorb for mathematical insights on Tawn-Molchanov max-stable models and for inspiring discussions.

Appendix A Multivariate regular variation and extremes

For convenience of the reader, here we review some facts and technical results on multivariate regular variation and extremes. For more details, see the comprehensive monographs [26, 9, 27] and the recent general approach to regular variation in metric spaces [19]. Some applications and extensions can be found in [21] and [31].

Definition A.1.

A random vector in is said to be multivariate regularly varying (MRV), if there exist a sequence and a Borel measure on , such that:

(i) , for all Borel sets , bounded away from the origin, i.e., such that for some , where denotes a ball centered at with radius .

(ii) For all Borel sets , bounded away from and such that , we have

| (A.1) |

In this case, we write .

It can be shown that if , the sequence is necessarily regularly varying, i.e. there exist a positive constant , such that as , for all . Furthermore, the limit measure has the scaling property , for all . Different choices for the normalization sequence are possible, however, the exponent is uniquely defined, given a random vector . To indicate that, we sometimes write .

An alternative, equivalent approach to multivariate regular variation is through polar coordinates. Namely, let be an arbitrary norm in (In fact, one can consider any positive and -homogeneous continuous function on as the radial component see, e.g., [31].) Then, , if and only if, for any (all) ,

| (A.2) |

for some probability measure defined on the unit sphere . It can be easily seen from (A.1) and (A.2), by setting , that

for a Borel set Relation (A.2) can be interpreted in terms of polar coordinates as follows. Letting with and , we have that

as . This means, that the vector is MRV if and only if its radial component is regularly varying and the conditional distribution of its angular component, given that the radius is extreme, converges weakly to the probability measure (see, e.g., [19] and Prop 3.9 in [31]). The probability measure is referred to as the spectral measure of . Observe that, depending on the choice of the normalizing sequence , the measure in (A.1) and correspondingly, the constant in (A.2), may change. The spectral measure and the exponent , however, are uniquely defined, given a RV vector .

The measure has the polar coordinate representation , where is is a measure on , such that . More precisely, we have the disintegration formula:

| (A.3) |

A.1 Multivariate extremes

In the context of extreme value theory, the spectral measure can be used to express the cumulative distribution function of the asymptotic distribution of independent component-wise maxima. Specifically, let be iid RV. For simplicity, assume that the ’s are non-negative. Then, the measure concentrates on . Consider the component-wise maxima . Then, it can be shown that for all ,

| (A.4) |

That is, converges in distribution to a vector with the cumulative distribution function given above. Indeed, by the independence of the ’s, we have

| (A.5) |

where , and the above inequalities are considered component-wise. By using the scaling property of , it can be shown that is a continuity set, and hence (A.1) implies that , as . Hence, the right-hand side of (A.5) converges to , which is in fact the right-hand side of (A.4).

A.2 Extremal coefficients

Let be a non-empty subset of coordinates of the random vector in (A.6). Recall that the extremal coefficient is defined as follows

In view of (A.6), we have

| (A.7) |

Moreover, by (A.4) one can show that

Therefore, modulo a common scaling factor, all these extremal coefficients can be readily estimated via the asymptotic scale coefficients of the heavy-tailed distributions . Specifically, we have

By suitable rescaling of the reference asset (or equivalently, the normalization sequence ), without loss of generality, we may assume that Given independent copies of , define the self-normalized estimators

| (A.8) |

Remark A.2.

It can be shown that the estimators in (A.8) are weakly consistent for any choice of a regularly varying sequence such that , as , i.e., we have in probability. This is true for example for the sequence for any . The consistency of follows by applying Theorem 5.3.(ii) in [27] to both the numerator and denominator in (A.8), viewed as empirical measures of the type , where stands for either or . The sequence herein is chosen such that as , for all . The fact that such a sequence can be found follows from the regular variation property of and the distribution of .

Remark A.3.

Recall Remark 2.1. The empirically estimated extremal coefficients in (A.8) do satisfy the consistency relationships of a set of valid extremal coefficients. Indeed, it follows from Lemma A.5 (below), with that

for all . Thus, the desired consistency relationships in Remark 2.1, follow by summing over since the denominator in (A.8) is common and positive.

Remark A.4.

In practice, however, when the extremal coefficients are either imposed or estimated in some other way, different from (A.8), one needs to ensure they provide consistent constraints. This can be done by “projecting” them onto the convex set of valid vectors of extremal coefficients . Specifically, by Möbius inversion, we know that , where and a certain design matrix of dimension . In practice, if the vector of estimated coefficients is , we solve the quadratic optimization program

subject to , for some small regularization parameter . We take the solution as the constraints in our extreme VaR optimization algorithms. In our experience, the so-calibrated extremal coefficient constraints are quite close to the ones estimated in practice. This calibration and other important statistical issues merit further independent investigation.

The following elementary lemma follows by induction, although it may be possible to obtain with general Möbius inversion techniques. This result is used to show that the empirical extremal coefficients in (A.8) satisfy the consistency relationships of a valid set of extremal coefficients (cf Remark 2.1).

Lemma A.5.

Let be an integer. For all , and , we have

where by convention .

Proof.

We establish the claim by induction. If , then trivially , if and , otherwise. This proves that , for all such that .

Suppose, now that and , for all . Let and observe that

The latter however is non-negative. Indeed, by the induction assumption, we have , while , for each , which since the ’s are non-negative implies that . Appealing to the induction principle, we conclude the proof. ∎

A.3 On Extreme VaR for homogeneous risk functionals

Let be a vector of losses. It is convenient to write , where , with and .

Consider a set of positive portfolio weights for the assets. Then, the cumulative portfolio loss can be expressed as

is a positive, -homogeneous function of .

The asymptotic scale of the loss relative to a reference asset is the key ingredient in computing extreme Value-at-Risk. Indeed, if

| (A.9) |

then by Lemma 2.3 in [12], we have that

| (A.10) |

The following result is extends the formulae in [3] (see also Theorem 4.1 of [12]), which address only the case of equal portfolio weights and tail-equivalent losses.

Proposition A.6.

Let be a non-negative regularly varying random vector with exponent equal to . Fix a norm in and let be the spectral measure of induced on the positive unit sphere . That is,

| (A.11) |

where and are the polar coordinates in .

The proof is a direct consequence of the next lemma, which establishes the asymptotic scale of for a general -homogeneous risk functional .

Lemma A.7.

Let be as in Proposition A.6 and be an arbitrary non-negative homogeneous function, i.e. . Then, for all , we have

where

| (A.13) |

This result shows that is regularly varying (provided ) and in fact it identifies its asymptotic scale coefficient in terms of the spectral measure .

Proof of Lemma A.7.

By Theorem 6 and Remark 7 of [18], we have that

| (A.14) |

Note that the above convergence is valid for all since the by the scaling property of and the homogeneity of , all sets are in fact continuity sets of . It remains to express the right-hand side of (A.14) in terms of the spectral measure . In view of (A.11) and by using the -homogeneity of , we obtain

The last expression equals , where is given in (A.13). ∎

Remark A.8.

By using Lemma 2.3 of [12] and our Lemma A.7, one can establish the asymptotic value-at-risk for more complicated instruments, which are non-linear homogeneous functions of the underlying assets. For example, one can consider . Thus, represents the minimum loss of a portfolio and bounds on its extreme VaR may be of interest. Note that in this case

does not depend on .

A.4 On the role of the tail index in risk diversification

Here, we briefly comment on an intriguing phase transition in the Fréchet-type bounds for the coefficient in (1.9) occurring in the case when . Recall that extreme VaR equals , where is the tail exponent of the portfolio .

The case corresponds to a finite-mean model for the losses. In the case , we have an infinite mean model, which may be viewed as ‘catastrophic’ since one has to have infinite capital in order to guard against such losses in the long-run. The bounds on can be interpreted as follows:

-

•

In the light-tailed case the means of the losses are finite and then the lower bound is achieved by the asymptotically independent portfolio. This agrees with the general intuition that accumulating independent assets leads to diversification and lower risk. On the other hand, the worst case scenario, naturally, corresponds to perfect (asymptotic) dependence where all assets are asymptotically identical or no diversification at all.

-

•

In the boundary case , the two bounds coincide, regardless of the asymptotic portfolio dependence.

-

•

In the extreme heavy-tailed setting the means of the losses are infinite and it turns out that the bounds in (1.9) are reversed. Indeed, by the triangle inequality, for the norm, we obtain:

where in the last relation we used the moment constraints in (1.8). Thus, the expression for the lower bound in the case in (1.9) now, in the case , becomes the upper bound.

On the other hand, by the Jensen’s inequality, for the concave function , we have

where , so that . By integrating the last bound with respect to , and using the moment constraints (1.8), we obtain

This shows that the expression for the upper bound in (1.9) (for the case ) now (in the case ) yields the lower bound.

In summary, for the case , we obtain the following universal bounds on (see also (1.9))

The bounds are sharp. The upper bound corresponds to asymptotic independence, and the lower to complete (asymptotic) dependence. This contradicts with our intuition about diversification. It shows that in the infinite-mean scenario, of potentially catastrophic losses, it is best to just hold a single asset rather than to ‘diversify’ among independent ones. The following argument provides some explanation of this counter-intuitive phenomenon.

Let be non-negative independent and identically distributed random variables modeling losses. Suppose that , with so that we are in the extreme heavy tailed regime of infinite expected loss . Suppose that unit investment is distributed evenly among such potentially catastrophic assets resulting in a portfolio loss

Then, by the heavy-tailed version of the central limit theorem, we have

where is a non-trivial totally skewed, -stable random variable [30]. In this case, since , the total loss stochastically grows to infinity as the number of independent assets in the portfolio increases. This counter-intuitive phenomenon where distributing an investment among multiple independent assets is in fact detrimental is due the extreme heavy-tailed nature of the model. Although such catastrophic models may not be practically relevant, the above argument shows that during regimes of very extreme losses our intuition about diversification may fail.

Appendix B Proofs

B.1 Karush–Kuhn–Tucker Conditions

The following proposition establishes sufficient conditions for optimal solutions to an LSIP . This version of the classic Karush–Kuhn–Tucker (KKT) optimality conditions for the case of LSIPs will be used in the proofs for Theorems 3.4, 3.7 and 3.8.

Proposition B.1 (KKT conditions).

Suppose Assumption 2.3 is satisfied and . Fix . If there exists dual variables and such that

| (B.1) |

| (B.2) |

and

| (B.3) |

Then .

Proof.

For every , define the set of active indices By Theorem 7.1.(ii) of [16] (see also Section 11.2 therein), a primal feasible vector is optimal for whenever

| (B.4) |

where denotes the smallest convex cone containing . This is true in our setting. Indeed, Relation (B.2) implies that , which in view of (B.1) entails (B.4). ∎

B.2 Proof for the Tawn-Molchanov minimizer

In this section, let . Denote as the power set of and We shall need two auxiliary lemmas.

Lemma B.2.

Let be the order statistics for arbitrary Fix and define . The following equality holds

| (B.5) |

Proof.

We will prove (B.5) under the assumption that there are no ties, i.e., . Since both the left- and right-hand sides of (B.5) are continuous functions of the ’s, the general result will follow by continuity for all .

We have

| (B.6) |

The second relation above follows from the fact that due to lack of ties, only sets containing at most indices will contribute to the inner sum therein. The last relation follows by a simple counting argument since is the number of sets with , for which Indeed, due to lack of ties, the latter equality holds only if the set contains the (unique!) index of and other indices among those of .

Now fix and consider

| (B.7) |

By using the fact that , where by convention if , we obtain

Now, by using the Newton’s binomial expansion of and , for the inner sum in the right-hand side of (B.7), we obtain that

By substituting in (B.7), we finally obtain

| (B.8) | |||||

Substituting (B.8) into (B.6) gives (B.5), which completes the proof. ∎

The next lemma establishes analytical solutions to the dual of problem () in (3.4) in the case where the set of constraints includes the entire set of extremal coefficients :

| subject to: |

Observe that the dual to the minimization problem () is a maximization problem. For convenience, we encode it equivalently as a minimization of the negative objective.

Lemma B.3.

The vector with elements

| (B.9) |

is optimal for Problem with

where is the unique solution to

| (B.10) |

Proof.

Fix We prove by verifying the KKT optimality conditions of Proposition B.1. That is, we need to show there exists and such that the following conditions hold:

-

Dual feasibility:

(B.11) -

Complementary slackness:

(B.12) -

Primal feasibility:

(B.13)

Theorem 4 of [32] asserts that for a consistent set of extremal coefficients Relation (B.10) holds for some non-negative . Define and We will show that the KKT conditions (B.11)-(B.13) hold. This will complete the proof.

Proof of Theorem 3.4.

Let denote the space of finite Borel measures on satisfying

Likewise, denote as the space of finite Borel measures on satisfying

Hence, we may write Problem as

| (B.15) |

where (Recall is the space of consistent extremal coefficients). Now Lemma B.3 together with strong duality for imply

| (B.16) |

where , with , is the unique solution to

(Uniqueness follows by Möbius inversion, see e.g. Theorem 4 of [32].) Substituting (B.16) into (B.15) gives

which completes the proof of Theorem 3.4. ∎

B.3 Proofs for the closed form solutions in Section 3.2

Proof of Theorem 3.7.

Let be such that

| (B.17) |

That is, is the (unique) set in (3.8), such that . One can then write

| (B.18) |

In view of Theorem 3.4, the lower bound is the value of a standard linear program (3.4). This linear program is the dual to the following primal linear program:

where ,

We will exhibit a primal feasible vector and a dual feasible vector , for which

with as in in (3.8). This, will complete the proof by the strong duality between the standard linear programs.

Dual feasibility. We will first verify that is dual feasible. We need to verify, that for all ,

| (B.20) |

Indeed, when (i.e., ) we have

in view of (B.18). Let now that is, , for some arbitrary fixed . Then,

This completes the proof of (B.20), i.e., the dual feasibility of .

Primal feasibility. For all , we need to show

Since , the function is convex on and hence for any and such that it follows that

We shall apply this inequality with and . (Note that is an integer, and hence we always have .) We have:

where the last equality follows from (B.19), since there are precisely singleton sets with . This establishes the primal feasibility of .

Optimality. Finally, we will verify that the objective functions of the primal and dual linear programs coincide. In view of (B.18), with straightforward manipulations, we obtain

| (B.21) |

Proof of Theorem 3.8.

We need the following elementary result.

Lemma B.4.

Let , and . Then, for all , we have:

(i)

(ii)

(iii) For all , we have

Proof.

Parts (i) and (ii) can be verified with straightforward differentiation. Part (ii) implies that the function is concave, which entails part (iii). ∎

Recall the primal-dual correspondence established in Theorem 3.1 between the problems and . That is, problem is the dual of the LSIP problem in (3.1).

We call problem ‘primal’ and ‘dual’. We will construct a primal feasible vector and a dual feasible measure , such that

| (B.23) |

then will be the (common) optimal value of the two problems.

Let and and define the measure , where are such that

Notice that and also the measure is dual feasible. Indeed,

which shows that the marginal extremal index constraints are met. On the other hand, since

for each , we have . This implies that

and hence the -variate extremal index constraint is satisfied. We have thus shown that the measure is dual feasible, i.e., meets the constraints of .

Let now and consider the function

A straightforward calculation using Lagrange multipliers yields that

Observe that for all in the support of , we have

Therefore, the value of the dual problem at is:

| (B.24) |

Let us now deal with the primal problem. Consider the vector , where

We will show that is primal feasible. That is, with and , we have

Observe that by the definition of the function , we have

| (B.25) |

Now, by applying Lemma B.4.(iii), to with , and , we obtain that

| (B.26) |

Since the last inequality is true for all , Relations (B.25) and (B.3), imply the primal feasibility of the point .

References

- [1] Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent measures of risk. Math. Finance, 9(3):203–228, 1999.

- [2] Bank for International Settlements. Basel III: A global regulatory framework for more resilient banks and banking systems, 2011. http://www.bis.org/publ/bcbs189.pdf.

- [3] P. Barbe, A. Fougeres, and C. Genest. On the tail behavior of sums of dependent risks. Astin Bull, 36:361–373, 2006.

- [4] Dimitris Bertsimas, David B. Brown, and Constantine Caramanis. Theory and applications of robust optimization. SIAM Rev., 53(3):464–501, 2011.

- [5] Jose Blanchet, Lin Chen, and Xun Yu Zhou. Distributionally robust mean-variance portfolio selection with Wasserstein distances, 2018. https://arxiv.org/abs/1802.04885.

- [6] S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, 2004.

- [7] V. Chavez-Demoulin and A. C. Davison. Modelling time series extremes. REVSTAT, 10(1):109–133, 2012.

- [8] Bikramjit Das, Anulekha Dhara, and Karthik Natarjan. On the heavy-tail behavior of the distributionally robust newsvendor, 2018. https://arxiv.org/abs/1806.05379.

- [9] Laurens de Haan and Ana Ferreira. Extreme value theory. Springer Series in Operations Research and Financial Engineering. Springer, New York, 2006. An introduction.

- [10] Debbie J. Dupuis, Nicolas Papageorgiou, and Bruno Rémillard. Robust Conditional Variance and Value-at-Risk Estimation. Journal of Financial Econometrics, 13(4):896–921, 08 2014.

- [11] P. Embrechts, C. Klüppelberg, and T. Mikosch. Modelling Extreme Events. Springer-Verlag, New York, 1997.

- [12] P. Embrechts, D. D. Lambrigger, and M. V. Wuthrich. Multivariate extremes and the aggregation of dependent risks: examples and counter-examples. Extremes, 12:107–127, 2009.

- [13] Sebastian Engelke and Jevgenijs Ivanovs. Robust bounds in multivariate extremes. Ann. Appl. Probab., 27(6):3706–3734, 2017.

- [14] K. French. Data library of standardized industry portfolios. Available online, 2018.

- [15] M. A. Goberna and M. A. López. Recent contributions to linear semi-infinite optimization: an update. Ann. Oper. Res., 271(1):237–278, 2018.

- [16] M.A. Goberna and M.A. Lopez. Linear Semi-infinite Optimization. Wiley series in mathematical methods in practice. Wiley, 1998.

- [17] G.H. Hardy, J.E. Littlewood, and G. Pólya. Inequalities. Cambridge University Press, 1934.

- [18] H. Hult and F. Lindskog. Extremal behavior of regularly varying stochastic processes. Stochastic Processes and their Applications, 115(2):249–274, 2005.

- [19] Henrik Hult and Filip Lindskog. Regular variation for measures on metric spaces. Publ. Inst. Math. (Beograd) (N.S.), 80(94):121–140, 2006.

- [20] Henry Lam and Clementine Mottet. Tail analysis without parametric models: a worst-case perspective. Oper. Res., 65(6):1696–1711, 2017.

- [21] Filip Lindskog, Sidney I. Resnick, and Joyjit Roy. Regularly varying measures on metric spaces: hidden regular variation and hidden jumps. Probab. Surv., 11:270–314, 2014.

- [22] A.J. McNeil, R. Frey, and P. Embrechts. Quantitative Risk Management: Concepts, Techniques, and Tools. Princeton University Press, 2005.

- [23] I. Molchanov. Convex geometry of max-stable distributions. Extremes, 11:235–259, 2008.

- [24] Ilya Molchanov and Kirstin Strokorb. Max-stable random sup-measures with comonotonic tail dependence. Stochastic Process. Appl., 126(9):2835–2859, 2016.

- [25] Giovanni Puccetti, Ludger Rüschendorf, and Dennis Manko. VaR bounds for joint portfolios with dependence constraints. Depend. Model., 4(1):368–381, 2016.

- [26] S. I. Resnick. Extreme Values, Regular Variation and Point Processes. Springer-Verlag, New York, 1987.

- [27] Sidney I. Resnick. Heavy-tail phenomena. Springer Series in Operations Research and Financial Engineering. Springer, New York, 2007. Probabilistic and statistical modeling.

- [28] Ludger Rüschendorf. Developments on Fréchet-bounds. In Distributions with fixed marginals and related topics (Seattle, WA, 1993), volume 28 of IMS Lecture Notes Monogr. Ser., pages 273–296. Inst. Math. Statist., Hayward, CA, 1996.

- [29] Ludger Rüschendorf. Improved Hoeffding-Fréchet bounds and applications to VaR estimates. In Copulas and dependence models with applications, pages 181–202. Springer, Cham, 2017.

- [30] G. Samorodnitsky and M. S. Taqqu. Stable Non-Gaussian Processes: Stochastic Models with Infinite Variance. Chapman and Hall, New York, London, 1994.

- [31] H.-P. Scheffler and S. Stoev. Implicit Extremes and Implicit Max-Stable Laws. ArXiv e-prints, November 2014. http://arxiv.org/abs/1411.4688.

- [32] M. Schlather and J. A. Tawn. Inequalities for the extremal coefficients of multivariate extreme value distributions. Extremes, 5(1):87–102, 2002.

- [33] A. Shapiro. Semi-infinite programming, duality, discretization and optimality conditions. Optimization, 58(2):133–161, 2009.

- [34] Kirstin Strokorb and Martin Schlather. An exceptional max-stable process fully parameterized by its extremal coefficients. Bernoulli, 21(1):276–302, 02 2015.

- [35] Johanna F. Ziegel. Coherence and elicitability. Math. Finance, 26(4):901–918, 2016.