Stable-Predictive Optimistic Counterfactual

Regret Minimization

Abstract

The CFR framework has been a powerful tool for solving large-scale extensive-form games in practice. However, the theoretical rate at which past CFR-based algorithms converge to the Nash equilibrium is on the order of , where is the number of iterations. In contrast, first-order methods can be used to achieve a dependence on iterations, yet these methods have been less successful in practice. In this work we present the first CFR variant that breaks the square-root dependence on iterations. By combining and extending recent advances on predictive and stable regret minimizers for the matrix-game setting we show that it is possible to leverage “optimistic” regret minimizers to achieve a convergence rate within CFR. This is achieved by introducing a new notion of stable-predictivity, and by setting the stability of each counterfactual regret minimizer relative to its location in the decision tree. Experiments show that this method is faster than the original CFR algorithm, although not as fast as newer variants, in spite of their worst-case dependence on iterations.

1 Introduction

Counterfactual regret minimization (CFR) (Zinkevich et al., 2007) and later variants such as Monte-Carlo CFR (Lanctot et al., 2009), CFR+ (Tammelin et al., 2015), and Discounted CFR (Brown & Sandholm, 2019), have been the practical state-of-the-art in solving large-scale zero-sum extensive-form games (EFGs) for the last decade. These algorithms were used as an essential ingredient for all recent milestones in the benchmark domain of poker (Bowling et al., 2015; Moravčík et al., 2017; Brown & Sandholm, 2017b). Despite this practical success all known CFR variants have a significant theoretical drawback: their worst-case convergence rate is on the order of , where is the number of iterations. In contrast to this, there exist first-order methods that converge at a rate of (Hoda et al., 2010; Kroer et al., 2015; 2018b). However, these methods have been found to perform worse than newer CFR algorithms such as CFR+, in spite of their theoretical advantage (Kroer et al., 2018b; a).

In this paper we present the first CFR variant which breaks the square-root dependence on the number of iterations. By leveraging recent theoretical breakthroughs on “optimistic” regret minimizers for the matrix-game setting, we show how to set up optimistic counterfactual regret minimizers at each information set such that the overall algorithm retains the properties needed in order to accelerate convergence. In particular, this leads to a predictive and stable variant of CFR that converges at a rate of .

Typical analysis of regret-minimization leads to a convergence rate of for solving zero-sum matrix games. However, by leveraging the idea of optimistic learning (Chiang et al., 2012; Rakhlin & Sridharan, 2013a; b; Syrgkanis et al., 2015; Wang & Abernethy, 2018), Rakhlin and Sridharan show in a series of papers that it is possible to converge at a rate of when leveraging cancellations that occur due to the optimistic mirror descent (OMD) algorithm (Rakhlin & Sridharan, 2013a; b). Syrgkanis et al. (2015) build on this idea, and introduce the optimistic follow-the-regularized-leader (OFTRL) algorithm; they show that even when the players do not employ the same algorithm, a rate of can be achieved as long as each algorithm belongs to a class of algorithms that satisfy a stability criterion and leverage predictability of loss inputs. We build on this latter generalization. Because we can only perform the optimistic updates locally with respect to counterfactual regrets we cannot achieve the cancellations that leads to a rate of ; instead we show that by carefully instantiating each counterfactual regret minimizer it is possible to maintain predictability and stability with respect to the overall decision-tree structure, thus leading to a convergence rate of . In order to achieve these results we introduce a new variant of stable-predictivity, and show that each local counterfactual regret minimizer must have its stability set relative to its location in the overall strategy space, with regret minimizers deeper in the decision tree requiring more stability.

In addition to our theoretical results we investigate the practical performance of our algorithm on several poker subgames from the Libratus AI which beat top poker professionals (Brown & Sandholm, 2017b). We find that our CFR variant coupled with the OFTRL algorithm and the entropy regularizer leads to better convergence rate than the vanilla CFR algorithm with regret matching, while it does not outperform the newer state-of-the-art algorithm Discounted CFR (DCFR) (Brown & Sandholm, 2019). This latter fact is not too surprising, as it has repeatedly been observed that CFR+, and the newer and faster DCFR, converges at a rate better than for many practical games of interest, in spite of the worst-case rate of .

The reader may wonder why we care about breaking the square-root barrier within the CFR framework. It is well-known that a convergence rate of can be achieved outside the CFR framework. As mentioned previously, this can be done with first-order methods such as the excessive gap technique (Nesterov, 2005) or mirror prox (Nemirovski, 2004) combined with a dilated distance-generating function (Hoda et al., 2010; Kroer et al., 2015; 2018b). Despite this, there has been repeated interest in optimistic regret minimization within the CFR framework, due to the strong practical performance of CFR algorithms. Burch (2017) tries to implement CFR-like features in the context of FOMs and regret minimizers, while Brown & Sandholm (2019) experimentally tries optimistic variants of regret minimizers in CFR. We stress that these prior results are only experimental; our results are the first to rigorously incorporate optimistic regret minimization in CFR, and the first to achieve a theoretical speedup.

Notation. Throughout the paper, we use the following notation when dealing with . We use to denote the dot product of two vectors and . We assume that a pair of dual norms has been chosen. These norms need not be induced by inner products. Common examples of such norm pairs are the norm which is self dual, and the norms, which are are dual to each other. We will make explicit use of the 2-norm: .

2 Sequential Decision Making and EFG Strategy Spaces

A sequential decision process can be thought of as a tree consisting of two types of nodes: decision nodes and observation nodes. The set of all decision nodes is denoted as , and the set of all observation nodes with . At each decision node , the agent chooses a strategy from the simplex of all probability distributions over the set of actions available at that decision node. An action is sampled according to the chosen distribution, and the agent then waits to play again. While waiting, the agent might receive a signal (observation) from the process; this possibility is represented with an observation node. At a generic observation point , the agent might receive signals; the set of signals that the agent can observe is denoted as . The observation node that is reached by the agent after picking action at decision point is denoted by . Likewise, the decision node reached by the agent after observing signal at observation point is denoted by . The set of all observation points reachable from is denoted as . Similarly, the set of all decision points reachable from is denoted as . To ease the notation, sometimes we will use the notation to mean . A concrete example of a decision process is given in the next subsection.

At each decision point in a sequential decision process, the decision of the agent incurs an (expected) linear loss . The expected loss throughout the whole process is therefore where is the probability of the agent reaching decision point , defined as the product of the probability with which the agent plays each action on the path from the root of the process to .

In extensive-form games where all players have perfect recall (that is, they never forget about their past moves or their observations), all players face a sequential decision process. The loss vectors are defined based on the strategies of the opponent(s) as well as the chance player. However, as already observed by Farina et al. (2019), sequential decision processes are more general and can model other settings as well, such as POMDPs and MDPs when the decision maker conditions on the entire history of observations and actions.

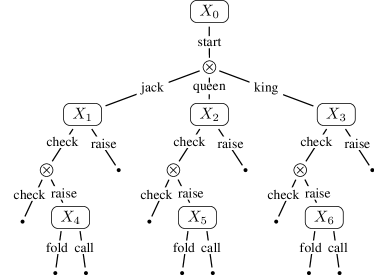

2.1 Example: Sequential Decision Process for the First Player in Kuhn Poker

As an illustration, consider the game of Kuhn poker (Kuhn, 1950). Kuhn poker consists of a three-card deck: king, queen, and jack. Each player first has to put a payment of 1 into the pot. Each player is then dealt one of the three cards, and the third is put aside unseen. A single round of betting then occurs:

-

•

Player can check or bet .

-

–

If Player checks Player can check or raise .

-

*

If Player checks a showdown occurs.

-

*

If Player raises Player can fold or call.

-

·

If Player folds Player takes the pot.

-

·

If Player calls a showdown occurs.

-

·

-

*

-

–

If Player raises Player can fold or call.

-

*

If Player folds Player takes the pot.

-

*

If Player calls a showdown occurs.

-

*

-

–

If no player has folded, a showdown occurs where the player with the higher card wins. The sequential decision process the Player 1 is shown in Figure 1, where denotes an observation point. In that example, we have: ; ; for all ; , , ; , , ; etc.

2.2 Sequence Form for Sequential Decision Processes

The expected loss for a given strategy, as defined in Section 2, is non-linear in the vector of decisions variables . This non-linearity is due to the product of probabilities of all actions on the path to from the root to . We now present a well-known alternative representation of this decision space which preserves linearity.

The alternative formulation is called the sequence form. In the sequence-form representation, the simplex strategy space at a generic decision point is scaled by the decision variable leading of the last action in the path from the root of the process to . In this formulation, the value of a particular action represents the probability of playing the whole sequence of actions from the root to that action. This allows each term in the expected loss to be weighted only by the sequence ending in the corresponding action. The sequence form has been used to instantiate linear programming (von Stengel, 1996) and first-order methods (Hoda et al., 2010; Kroer et al., 2015; 2018b) for computing Nash equilibria of zero-sum EFGs. There is a straightforward mapping between a vector of decisions , one for each decision point, and its corresponding sequence form: simply assign each sequence the product of probabilities in the sequence. We will let denote the sequence-form representation of a vector of decisions . Likewise, going from a sequence-form strategy to a corresponding vector of decisions can be done by dividing each entry (sequence) in by the value where is the entry in corresponding to the unique last action that the agent took before reaching .

Formally, the sequence-form representation of a sequential decision process can be obtained recursively, as follows:

-

•

At every observation point , we let

(1) where are the children decision points of .

-

•

At every decision point , we let

(2) where are the children observation points of .

The sequence form strategy space for the whole sequential decision process is then , where is the root of the process. Crucially, is a convex and compact set, and the expected loss of the process is a linear function over .

With the sequence-form representation the problem of computing a Nash equilibriun in an EFG can be formulated as a bilinear saddle-point problem (BSPP). A BSPP has the form

| (3) |

where and are convex and compact sets. In the case of extensive-form games, and are the sequence-form strategy spaces of the sequential decision processes faced by the two players, and is a sparse matrix encoding the leaf payoffs of the game.

2.3 Notation when dealing with the extensive form

In the rest of the paper, we will make heavy use of the sequence form and its inductive construction given in (12) and (13). We will consistently denote sequence-form strategies with a triangle superscript. As we have already observed, vectors that pertain to the sequence-form have one entry for each sequence of the decision process, that is one entry for pair where . Sometimes, we will need to slice a vector and isolate only those entries that refer to all decision points and actions that are at or below some ; we will denote such operation as . Similarly, we introduce the syntax to denote the subset of entries of that pertain to all actions at decision point .

3 Stable-Predictive Regret Minimizers

In this paper, we operate within the online learning framework called online convex optimization (Zinkevich, 2003). In particular, we restrict our attention to a modern subtopic: predictive (also often called optimistic) regret minimization (Chiang et al., 2012; Rakhlin & Sridharan, 2013a; b).

As usual in this setting, a decision maker repeatedly plays against an unknown environment by making a sequence of decisions , where the set of feasible decisions for the decision maker is convex and compact. The evaluation of the outcome of each decision is , where is a convex loss vector, unknown to the decision maker until after the decision is made. The peculiarity of predictive regret minimization is that we also assume that the decision maker has access to predictions of what the loss vectors will be. In summary, by predictive regret minimizer we mean a device that supports the following two operations:

-

•

it provides the next decision given a prediction of the next loss vector and

-

•

it receives/observes the convex loss vectors used to evaluate decision .

The learning is online in the sense that the decision maker’s (that is, device’s) next decision, , is based only on the previous decisions , observed loss vectors , and the prediction of the past loss vectors as well as the next one .

Just as in the case of a regular (that is, non-predictive) regret minimizer, the quality metric for the predictive regret minimizer is its cumulative regret, which is the difference between the loss cumulated by the sequence of decisions and the loss that would have been cumulated by playing the best-in-hindsight time-independent decision . Formally, the cumulative regret up to time is

| (4) |

We introduce a new class of predictive regret minimizers whose cumulative regret decomposes into a constant term plus a measure of the prediction quality, while maintaining stability in the sense that the iterates change slowly.

Definition 1 (Stable-predictive regret minimizer).

A predictive regret minimizer is -stable-predictive if the following two conditions are met:

-

•

Stability. The decisions produced change slowly:

(5) -

•

Prediction bound. For all , the cumulative regret up to time is bounded according to

(6) In other words, small prediction errors only minimally affect the regret accumulated by the device. If, in particular, the prediction matches the loss vector perfectly for all , the cumulative regret remains asymptotically constant.

Our notion of stable-predictivity is similar to the Regret bounded by Variation in Utilities (RVU) property given by Syrgkanis et al. (2015), which asserts that

| (RVU) |

However, there are several important differences:

-

•

Syrgkanis et al. (2015) assume that ; this explains the term in (RVU) instead of in (6). One of the reason why we do not make assumptions on is that, unlike in matrix games, we will need to use modified predictions for each local regret minimizer, since we need to predict the local counterfactual loss.

-

•

Our notion ignores the cancellation term ; instead, we require the stabilty property (5).

-

•

The coefficients in the regret bound (6) are forced to be inversely proportional, and tied to the choice of the stability parameter . Syrgkanis et al. (2015) show that same correlation holds for the optimistic follow-the-regularized leader, but they don’t require it in their definition of the RVU property.

Syrgkanis et al. (2015) show that their optimistic follow-the-regularized-leader (OFTRL) algorithm, as well as the variant of the mirror descent algorithm presented by Rakhlin & Sridharan (2013a), satisfy (RVU). In Section 3.2 we show that OFTRL also satisfies stable-predictivity.

3.1 Relationship with Bilinear Saddle-Point Problems

In this subsection we show how stable-predictive regret minimization can be used to solve a BSPP such as a Nash equilibrium problem in two-player zero-sum extensive-form games with perfect recall (Sections 2 and 2.2). The solutions of (3) are called saddle points. The saddle-point residual (or gap) of a point , defined as

measures how close is to being a saddle point (the lower the residual, the closer).

It is known that regular (non-predictive) regret minimization yields an anytime algorithm that produces a sequence of points whose residuals are . Syrgkanis et al. (2015) observe that in the context of matrix games (i.e., when and are simplexes), RVU minimizers that also satisfy the stability condition (5) can be used in place of regular regret minimizers to improve the convergence rate to . In what follows, we show how to extend the argument to stable-predictive regret minimizers and general bilinear saddle-point problems beyond Nash equilibria in two-player zero-sum matrix games.

A folk theorem explains the tight connections between low regret and low residual (Cesa-Bianchi & Lugosi, 2006). Specifically, by setting up two regret minimizers (one for and one for ) that observe loss vectors given by the profile of average decisions

| (7) |

has residual bounded from above according to

Hence, by letting the predictions be defined as and assuming that the predictive regret minimizers are -stable-predictive, we obtain that the residual of the average decisions (7) satisfies

where the first inequality holds by (6), the second by noting that the operator norm of a linear function is equal to the operator norm of its transpose, and the third inequality by the stability condition (5). This shows that if the stability parameter of the two stable-predictive regret minimizers is , then the saddle point residual is , an improvement over the bound obtained with regular (that is, non-predictive) regret minimizers.

3.2 Optimistic Follow the Regularized Leader

Optimistic follow-the-regularized-leader (OFTRL) is a regret minimizer introduced by Syrgkanis et al. (2015). At each time , OFTRL outputs the decision

| (8) |

where is a free constant and is a 1-strongly convex regularizer with respect to the norm . Furthermore, let denote the diameter of the range of , and let be the maximum (dual) norm of any loss vector or prediction thereof.

A theorem similar to that of Syrgkanis et al. (2015, Proposition 7), which was obtained in the context of the RVU property, can be shown for the stable-predictive framework:

Theorem 1.

OFTRL is a -stable-predictive regret minimizer.

4 CFR as Regret Decomposition

In this section we offer some insights into CFR, and discuss what changes need to be made in order to leverage the power of predictive regret minimization. CFR is a framework for constructing a (non-predictive) regret minimizer that operates over the sequence-form strategy space of a sequential decision process. In accordance with Section 2.3, we denote the decision produced by at time as ; the corresponding loss functions is denoted as .

One central idea in CFR is to define a localized notion of loss: for all , CFR constructs the following linear counterfactual loss function . Intuitively, the counterfactual loss of a local strategy measures the loss that the agent would face were the agent allowed to change the strategy at decision point only. In particular, is the loss of an agent that follows the strategy instead of at decision point , but otherwise follows the strategy everywhere else. Formally,

| (9) |

Since is a linear function, it has a unique representation as a counterfactual loss vector , defined as

| (10) |

With this local notion of loss function, a corresponding local notion of regret for a sequence of decisions , called the counterfactual regret, is defined for each decision point :

Intuitively, represents the difference between the loss that was suffered for picking and the minimum loss that could be secured by choosing a different strategy at decision point only. This is conceptually different from the definition of regret of , which instead measures the difference between the loss suffered and the best loss that could have been obtained, in hindsight, by picking any strategy from the whole strategy space, with no extra constraints.

With this notion of regret, CFR instantiates one (non-stable-predictive) regret minimizer for each decision point . Each local regret minimizer operates on the domain , that is, the space of strategies at decision point only. At each time , prescribes the strategy that, at each information set , behaves according to the decision of . Similarly, any loss vector input to is processed as follows: (i) first, the counterfactual loss vectors , one for each decision point , are computed; (ii) then, each observes its corresponding counterfactual loss vector .

Another way to look at CFR and counterfactual losses is as an inductive construction over subtrees. When a loss function relative to the whole sequential decision process is received by the root node, inductively each node of the sequential decision process does the following:

-

•

If the node receiving the loss vector is an observation node, the incoming loss vector is partitioned and forwarded to each child decision node. The partition of the loss vector is done so as to ensure that only entries relevant to each subtree are received down the tree.

-

•

If the node receiving the loss vector is a decision node, the incoming loss vector is first forwarded as-is to each of the child observation points, and then it is used to construct the counterfactual loss vector which is input into .

This alternative point of view differs from the original one, but has been recently used by Farina et al. (2018; 2019) to simplify the analysis of the algorithm. When viewed from the above point of view, CFR is recursively building—in a bottom-up fashion—regret minimizers for each subtree starting from child subtrees.

In accordance with our convention (Section 2.3), we denote , for , the regret minimizer that operates on obtained by only considering the local regret minimizers in the subtree rooted at vertex of the sequential decision process. Analogously, we will denote with the regret of up to time , and with the loss function entering at time . In accordance with the above construction, we have that

| (11) |

Finally, we denote the decisions produced by at time as . As per our discussion above, the decisions produced by are tied together inductively according to

| (12) |

and

| (13) |

The following two lemmas can be easily extracted from Farina et al. (2018):

Lemma 1.

Let be an observation node. Then,

Proof.

Lemma 2.

Let be a decision point. Then,

Proof.

By definition of ,

By combining (13) and (11), we can break the dot products and the minimization problem into independent parts, one for each , as well as a part that depends solely on :

where the equality follows by the definition of , and the inequality follows from breaking the minimization of a sum into a sum of minimization problems. By identifying the difference between the first two terms as the counterfactual regret (that is, the regret of up to time ), we obtain

as we wanted to show. ∎

The two lemmas above do not make any assumption about the nature of the (localized) regret minimizers , and therefore they are applicable even when the are predictive or, specifically, stable-predictive.

5 Stable-Predictive Counterfactual Regret Minimization

Our proposed algorithm behaves exactly like CFR, with the notable difference that our local regret minimizers are stable-predictive and chosen to have specific stability parameters. Furthermore, the predictions for each local regret minimizer are chosen so as to leverage the predictivity property of the regret minimizers. Given a desired value of , by choosing the stability parameters and predictions as we will detail later, we can guarantee that is a -stable-predictive regret minimizer.111Throughout the paper, our asymptotic notation is always with respect to the number of iterations .

5.1 Choice of Stability Parameters

We use the following scheme to pick the stability parameter of . First, we associate a scalar to each node of the sequential decision process. The value of the root decision node is set to , and the value for each other node is set relative to the value of their parent

| (14) |

The stability parameter of each decision point is chosen according to

| (15) |

where is an upper bound on the 2-norm of any vector in . A suitable value of can be found by recursively using the following rules:

| (16) |

At each decision point , any stable-predictive regret minimizer that is able to guarantee the above stability parameter can be used. For example, one can use OFTRL where the stepsize is chosen appropriately. For example, assuming without loss of generality that all loss vectors involved have (dual) norm bounded by , we can simply set the stepsize of the local OFTRL regret minimizer at decision point to be .

5.2 Prediction of Counterfactual Loss Vectors

Let be the prediction received by , concerning the future loss vector . We will show how to process the prediction and produce counterfactual prediction vectors (one for each decision point ) for each local stable-predictive regret minimizer .

Following the construction of the counterfactual loss functions defined in (9), for each decision point we define the counterfactual prediction function as

Observation. It important to observe that the counterfactual prediction function depends on the decisions produced at time in the subtree rooted at . In other words, in order to construct the prediction for what loss will observe after producing the decision , we use the “future” decisions from the subtrees below .

Similarly to what is done for the counterfactual loss function, we define the counterfactual loss prediction vector , as the (unique) vector in such that

| (17) |

5.3 Proof of Correctness

We will prove that our choice of stability parameters (14) and (localized) counterfactual loss predictions (17) guarantee that is a -stable-predictive regret minimizer. Our proof is by induction on the sequential decision process structure: we prove that our choices yield a -stable-predictive regret minimizer in the sub-sequential decision process rooted at each possible node . For observation nodes the inductive step is performed via Lemma 3, while for decision nodes the inductive step is performed via Lemma 4.

We will prove both Lemma 3 and Lemma 4 with respect to the 2-norm. This does not come at the cost of generality, since all norms are equivalent on finite-dimensional vector spaces, that is, for every choice of norm , there exist constants such that for all , .

Lemma 3.

Let be an observation node, and assume that is a -stable-predictive regret minimizer over the sequence-form strategy space for each . Then, is a -stable-predictive regret minimizer over the sequence-form strategy space .

Proof.

By hypothesis, for all we have

| (18) |

and

| (19) |

where is the decision output by at time .

Lemma 4.

Let be a decision node, and assume that is a -stable-predictive regret minimizer over the sequence-form strategy space for each . Suppose further that is a -stable-predictive regret minimizer over the simplex . Then, is a -stable-predictive regret minimizer over the sequence-form strategy space .

Proof.

By hypothesis, for all we have

| (21) |

and

| (22) |

We substitute (21) into the regret bound of Lemma 2. The key observation is that the loss vector—and their predictions—entering the subtree rooted at () are simply forwarded from ; with this, we obtain:

| (23) |

On the other hand, by hypothesis is a -stable-predictive regret minimizer. Hence,

| (24) |

where the equality comes from the definition of (Equation (15)) and the fact that

By substituting (24) into (23) and noting that , we obtain

which establishes the predictivity of .

To conclude the proof, we show that has stability parameter . To this end, note that by (2)

where we have used the Cauchy-Schwarz inequality and the definition of (Equation 16). By using the stability of , that is , as well as the hypothesis (22) and (14):

Hence, has stability parameter as we wanted to show. ∎

Putting together Lemma 3 and Lemma 4, and using induction on the sequential decision process structure, we obtain the following formal statement.

Corollary 1.

Let . If:

-

1.

Each localized regret minimizer is -stable-predictive and produces decisions over the local (simplex) action space , where is as in (15); and

-

2.

observes the counterfactual loss prediction as defined in (17); and

-

3.

observes the counterfactual loss vectors as defined in (10),

then is a -stable-predictive regret minimizer that operates over the sequence-form strategy space .

By combining the above result with the arguments of Section 3.1, we conclude that by constructing two -stable-predictive regret minimizers, one per player, using the construction above, we obtain an algorithm that can approximate a Nash equilibrium and at time the average strategy produces an -Nash equilibrium in a two-player zero-sum game.

6 Experiments

Our techniques are evaluated in the benchmark domain of heads-up no-limit Texas hold’em poker (HUNL) subgames. In HUNL, there are two players and that each start the game with $20,000. The position of the players switches after each hand. The players alternate taking turns and may choose to either fold, call, or raise on their turn. Folding results in the player losing and the money in the pot being awarded to the other player. Calling means the player places a number of chips in the pot equal to the opponent’s share. Raising means the player adds more chips to the pot than the opponent’s share. There are four betting rounds in the game. A round ends when both players have acted at least once and the most recent player has called. Players cannot raise beyond the $20,000 they start with. All raises must be at least $100 and at least as larger as any previous raise in that round.

At the start of the game must place $100 in the pot and must place $50 in the pot. Both players are then dealt two cards that only they observe from a 52-card deck. A round of betting then occurs starting with . will be the first to act in all subsequent betting rounds. Upon completion of the first betting round, three community cards are dealt face up. After the second betting round is over, another community card is dealt face up. Finally, after that betting round one more community card is revealed and a final betting round occurs. If no player has folded then the player with the best five-card poker hand, out of their two private cards and the five community cards wins the pot. The pot is split evenly if there is a tie.

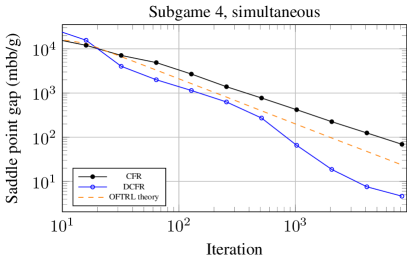

The most competitive agents for HUNL solve portions of the game (referred to as subgames) in real time during play (Brown & Sandholm, 2017a; Moravčík et al., 2017; Brown & Sandholm, 2017b; Brown et al., 2018). For example, Libratus solved in real time the remainder of HUNL starting on the third betting round. We conduct our experiments on four open-source subgames solved by Libratus in real time during its competition against top humans in HUNL.222https://github.com/CMU-EM/LibratusEndgames Following prior convention, we use the bet sizes of 0.5 the size of the pot, 1 the size of the pot, and the all-in bet for the first bet of each round. For subsequent bets in a round, we consider 1 the pot and the all-in bet.

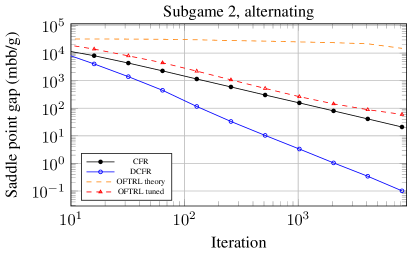

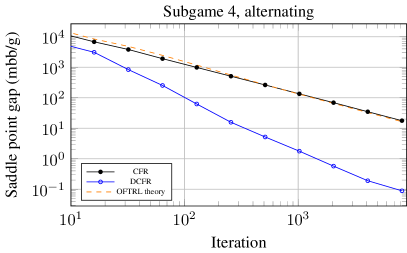

Subgames 1 and 2 occur over the third and fourth betting round. Subgame 1 has $500 in the pot at the start of the game while Subgame 2 has $4,780. Subgames 3 and 4 occur over only the fourth betting round. Subgame 1 has $500 in the pot at the start of the game while Subgame 4 has $3,750. We measure exploitability in terms of the standard metric: milli big blinds per game (mbb/g), which is the number of big blinds (’s original contribution to the pot) lost per hand of poker multiplied by 1,000 and is the standard measurement of win rate in the related literature.

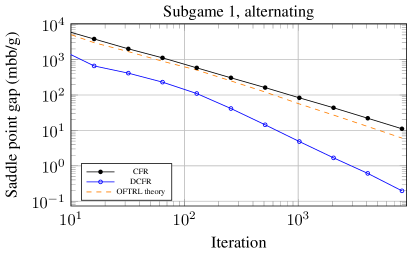

We compare the performance of three algorithms: vanilla CFR (i.e. CFR with regret matching; labeled CFR in plots), the current state-of-the-art algorithm in practice, Discounted CFR (Brown & Sandholm, 2019) (labeled DCFR in plots), and our stable-predictive variant of CFR with OFTRL at each decision point (labeled OFTRL in plots). For OFTRL we use the stepsize that the theory suggests in our experiments on subgames 3 and 4 (labeled OFTRL theory). For subgames 1 and 2 we found that the theoretically-correct stepsize is much too conservative, so we also show results with a less-conservative parameter found through dividing the stepsize by 10, 100, and 1000, and picking the best among those (labeled OFTRL tuned). For all games we show two plots: one where all algorithms use simultaneous updates, as CFR traditionally uses, and one where all algorithms use alternating updates, a practical change that usually leads to better performance.

Figure 2 shows the results for simultaneous updates on subgames 2 and 4, while Figure 3 for games 1 and 3. In the smaller subgames 3 and 4 we find that OFTRL with the stepsize set according to our theory outperforms CFR: in subgame 4 almost immediately and significantly, in subgame 3 only after roughly 800 iterations. In contrast to this we find that in the larger subgames 1 and 2 the OFTRL stepsize is much too conversative, and the algorithm barely starts to make progress within the number of iterations that we run. With a moderately-hand-tuned stepsize OFTRL beats CFR somewhat significantly. In all games DCFR performs better than OFTRL, and also significantly better than its theory predicts. This is not too surprising, as both CFR+ and the improved DCFR are known to significantly outperform their theoretical convergence rate in practice.

Figure 4 shows the results for alternating updates on subgames 2 and 4, while games 1 and 3 are given in Figure 5. In the alternating-updates setting OFTRL performs worse relative to CFR and DCFR. In subgame 1 OFTRL with stepsizes set according to the theory slightly outperforms CFR, but in subgame 2 they have near-identical performance. In subgames 3 and 4 even the manually-tuned variant performs worse than CFR, although we suspect that it is possible to improve on this with a better choice of stepsize parameter. In the alternating setting DCFR performs significantly better than all other algorithms.

7 Conclusions

We developed the first variant of CFR that converges at a rate better than . In particular we extend the ideas of predictability and stability for optimistic regret minimization on matrix games to the setting of EFGs. In doing so we showed that stable-predictive simplex regret minimizers can be aggregated to form a stable-predictive variant of CFR for sequential decision making, and we showed that this leads to a convergence rate of for solving two-player zero-sum EFGs. Our result makes the first step towards reconciling the gap between the theoretical rate at which CFR converges, and the rate at which first-order methods converge.

Experimentally we showed that our CFR variant can outperform CFR on some games, but that the choice of stepsize is important, while we find that DCFR is faster in practice. An important direction for future work is to find variants of our algorithm that still satisfy the theoretical guarantee and perform even better in practice.

References

- Bowling et al. (2015) Bowling, M., Burch, N., Johanson, M., and Tammelin, O. Heads-up limit hold’em poker is solved. Science, 347(6218), January 2015.

- Brown & Sandholm (2017a) Brown, N. and Sandholm, T. Safe and nested subgame solving for imperfect-information games. In Proceedings of the Annual Conference on Neural Information Processing Systems (NIPS), pp. 689–699, 2017a.

- Brown & Sandholm (2017b) Brown, N. and Sandholm, T. Superhuman AI for heads-up no-limit poker: Libratus beats top professionals. Science, pp. eaao1733, Dec. 2017b.

- Brown & Sandholm (2019) Brown, N. and Sandholm, T. Solving imperfect-information games via discounted regret minimization. In AAAI Conference on Artificial Intelligence (AAAI), 2019.

- Brown et al. (2018) Brown, N., Sandholm, T., and Amos, B. Depth-limited solving for imperfect-information games. In Neural Information Processing Systems, NeurIPS 2018, 2018.

- Burch (2017) Burch, N. Time and Space: Why Imperfect Information Games are Hard. PhD thesis, University of Alberta, 2017.

- Cesa-Bianchi & Lugosi (2006) Cesa-Bianchi, N. and Lugosi, G. Prediction, learning, and games. Cambridge university press, 2006.

- Chiang et al. (2012) Chiang, C.-K., Yang, T., Lee, C.-J., Mahdavi, M., Lu, C.-J., Jin, R., and Zhu, S. Online optimization with gradual variations. In Conference on Learning Theory, pp. 6–1, 2012.

- Farina et al. (2018) Farina, G., Kroer, C., and Sandholm, T. Composability of Regret Minimizers. arXiv e-prints, art. arXiv:1811.02540, November 2018.

- Farina et al. (2019) Farina, G., Kroer, C., and Sandholm, T. Online convex optimization for sequential decision processes and extensive-form games. In AAAI Conference on Artificial Intelligence (AAAI), 2019.

- Hoda et al. (2010) Hoda, S., Gilpin, A., Peña, J., and Sandholm, T. Smoothing techniques for computing Nash equilibria of sequential games. Mathematics of Operations Research, 35(2), 2010.

- Kroer et al. (2015) Kroer, C., Waugh, K., Kılınç-Karzan, F., and Sandholm, T. Faster first-order methods for extensive-form game solving. In Proceedings of the ACM Conference on Economics and Computation (EC), 2015.

- Kroer et al. (2018a) Kroer, C., Farina, G., and Sandholm, T. Solving large sequential games with the excessive gap technique. In Proceedings of the Annual Conference on Neural Information Processing Systems (NIPS), 2018a.

- Kroer et al. (2018b) Kroer, C., Waugh, K., Kılınç-Karzan, F., and Sandholm, T. Faster algorithms for extensive-form game solving via improved smoothing functions. Mathematical Programming, pp. 1–33, 2018b.

- Kuhn (1950) Kuhn, H. W. A simplified two-person poker. In Kuhn, H. W. and Tucker, A. W. (eds.), Contributions to the Theory of Games, volume 1 of Annals of Mathematics Studies, 24, pp. 97–103. Princeton University Press, Princeton, New Jersey, 1950.

- Lanctot et al. (2009) Lanctot, M., Waugh, K., Zinkevich, M., and Bowling, M. Monte Carlo sampling for regret minimization in extensive games. In COLT (Conference on Learning Theory) workshop on Online Learning with Limited Feedback, 2009.

- Moravčík et al. (2017) Moravčík, M., Schmid, M., Burch, N., Lisý, V., Morrill, D., Bard, N., Davis, T., Waugh, K., Johanson, M., and Bowling, M. Deepstack: Expert-level artificial intelligence in heads-up no-limit poker. Science, 356(6337), May 2017.

- Nemirovski (2004) Nemirovski, A. Prox-method with rate of convergence O(1/t) for variational inequalities with Lipschitz continuous monotone operators and smooth convex-concave saddle point problems. SIAM Journal on Optimization, 15(1), 2004.

- Nesterov (2005) Nesterov, Y. Excessive gap technique in nonsmooth convex minimization. SIAM Journal of Optimization, 16(1), 2005.

- Rakhlin & Sridharan (2013a) Rakhlin, A. and Sridharan, K. Online learning with predictable sequences. In Conference on Learning Theory, pp. 993–1019, 2013a.

- Rakhlin & Sridharan (2013b) Rakhlin, S. and Sridharan, K. Optimization, learning, and games with predictable sequences. In Advances in Neural Information Processing Systems, pp. 3066–3074, 2013b.

- Syrgkanis et al. (2015) Syrgkanis, V., Agarwal, A., Luo, H., and Schapire, R. E. Fast convergence of regularized learning in games. In Advances in Neural Information Processing Systems, pp. 2989–2997, 2015.

- Tammelin et al. (2015) Tammelin, O., Burch, N., Johanson, M., and Bowling, M. Solving heads-up limit Texas hold’em. In Proceedings of the 24th International Joint Conference on Artificial Intelligence (IJCAI), 2015.

- von Stengel (1996) von Stengel, B. Efficient computation of behavior strategies. Games and Economic Behavior, 14(2):220–246, 1996.

- Wang & Abernethy (2018) Wang, J.-K. and Abernethy, J. D. Acceleration through optimistic no-regret dynamics. In Advances in Neural Information Processing Systems, pp. 3828–3838, 2018.

- Zinkevich (2003) Zinkevich, M. Online convex programming and generalized infinitesimal gradient ascent. In International Conference on Machine Learning (ICML), pp. 928–936, Washington, DC, USA, 2003.

- Zinkevich et al. (2007) Zinkevich, M., Bowling, M., Johanson, M., and Piccione, C. Regret minimization in games with incomplete information. In Proceedings of the Annual Conference on Neural Information Processing Systems (NIPS), 2007.

Appendix A Stable-predictivity of OFTRL

We offer a proof of Theorem 8.

First, we introduce the following argmin-function:

| (25) |

Furthermore, let . With this notation, the decisions produced by OFTRL, as defined in (8), can be expressed as .

Continuity of the argmin-function. The first step in the proof is to study the continuity of the argmin-function . Intuitively, the role of the regularizer is to smooth out the linear objective function . So, it seems only reasonable to expect that, the higher the constant that multiplies , the less the argmin is affected by small changes of . In fact, the following holds:

Lemma 5.

The argmin-function is -Lipschitz continuous with respect to the dual norm, that is

Proof.

The variational inequality for the optimality of implies

| (26) |

Symmetrically for , we find that

| (27) |

Summing inequalities 26 and 27, we obtain

Using strong convexity of on the left-hand side and the generalized Cauchy-Schwarz inequality on the right-hand side, we obtain

and dividing by we obtain the Lipschitz continuity of the argmin-function . ∎

A direct consequence of Lemma 5 is the following corollary, which measures the stability (small step size) of the decisions output by OFTRL:

Corollary 2.

At each time , the iterates produced by OFTRL satisfy

Proof.

where the first inequality holds by Lemma 5 and the second one by definition of and the triangle inequality. ∎

The rest of the proof, specifically the predictivity parameters and of OFTRL follow directly from the proof of Theorem 19 in the appendix of Syrgkanis et al. (2015).