Multivariate risk measures in the non-convex setting

Abstract

The family of admissible positions in a transaction costs model is a random closed set, which is convex in case of proportional transaction costs. However, the convexity fails, e.g. in case of fixed transaction costs or when only a finite number of transfers are possible. The paper presents an approach to measure risks of such positions based on the idea of considering all selections of the portfolio and checking if one of them is acceptable. Properties and basic examples of risk measures of non-convex portfolios are presented.

1 Introduction

Multivariate financial positions (portfolios) are usually described by vectors in Euclidean space. However, if one aims to take into account possible exchanges between the components of the portfolio, it is necessary to consider the whole set of points in space that may be attained from the original position by allowed exchanges. In other words, considering a multiasset portfolio is indispensable from specifying which transactions may be applied to its components. For instance, if all components of the portfolio represent cash amounts in the same currency and transfers between the components are unrestricted with short-selling permitted, then the attainable positions are all random vectors such that the sum of their components equals the sum of components of . By allowing disposal of assets (e.g., in the form of consumption), we arrive at the half-space

In this case and also in the presence of transaction costs not influenced by , the attainable positions are points from , where is the set of portfolios available at price zero, see [7]. In other situations, possible attainable positions may depend on in a non-linear way, for instance, when components represent capitals of members of a group and admissible transfers satisfy further restrictions, e.g., requiring that they do not cause insolvency of an otherwise solvent agent, see [3].

In view of the above reasons, it is natural to represent multiasset portfolios as random closed sets. Recall that a random closed set is a measurable map from a probability space to the space of closed sets in equipped with the -algebra generated by the Fell topology. In other words, the measurability of means that for all compact sets in , see [11, Sec. 1.1.1].

A random closed set is said to be lower if almost all its realisations are lower sets, that is, for almost all , and coordinatewisely imply that . A random closed set is said to be convex if almost all its realisations are convex. If is a random closed set, then its closed convex hull is also a random closed set, see [11, Th. 1.3.25].

For , denote by the family of -integrable (essentially bounded if ) random vectors such that a.s.; such random vectors are called -integrable selections of . Furthermore, is the family of all selections of ; this family is not empty if is a.s. non-empty, see [11, Th. 1.4.1]. A random closed set is called -integrable if it admits at least one -integrable selection; it is called -integrably bounded if

is a -integrable random variable for . The random closed set is said to be essentially bounded if is a.s. bounded by a constant.

If is integrable (that is, -integrable), its selection expectation is defined by

| (1) |

where denotes the topological closure in . The closed Minkowski sum

of two random closed sets and is also a random closed set. Note that

denotes the reflection of with respect to the origin; this is not the inverse operation to the addition. We refer to [11] for further material concerning random closed sets.

The paper is organised as follows. In Section 2 we introduce the selection risk measure of possibly non-convex random lower closed sets, thereby generalising the setting of [3] and [12]. Due to the non-convexity, it is not possible to assess the risk by working with half-spaces containing the portfolio, as it is the case in [4, 5]. In Section 3 we discuss two basic set-valued risk measures, one based on considering the fixed points of set-valued portfolio, the other is given by the selection expectation of . These two cases correspond to taking the negative essential infimum and the negative expectation as the underlying numerical risk measures. Section 4 explores the cases when the selection risk measure takes convex values and is law invariant. The important case of fixed transaction costs is considered in Section 5. Finally, Section 6 deals with the case of only a finite set of admissible transactions.

2 Selection risk measure of non-convex portfolios

2.1 Definition

Fix and a vector of monetary -risk measures applied to components of a -integrable random vector . We refer to [1] and [2] for the facts concerning risk measures for random variables. Assume that and that all components of are finite on -integrable random variables. When saying that is coherent or convex, we mean that all its components are coherent or convex. The convexity or coherency properties will be imposed only when necessary and will be explicitly mentioned.

In many cases below, we consider the following basic numerical risk measures.

-

1.

The negative essential infimum , which is an -risk measure.

-

2.

The negative expectation , an -risk measure.

-

3.

The Average Value-at-Risk (or Expected Shortfall in the non-atomic case)

at level for , where is the cumulative distribution function of and is the quantile function.

-

4.

The distortion risk measure

(2) for , where is a (concave) distortion function, is the dual distortion function, and is chosen to ensure that the integral is finite.

The selection risk measure of a -integrable lower random closed set is defined as

| (3) |

where the union is taken over all -integrable selections of . Thus, if and only if for , . The inequalities between vectors are always coordinatewise and the lower limit is also taken coordinatewisely. The selection risk measure takes values being upper sets, and (3) can be seen as the primal representation of . A dual representation is not feasible without imposing convexity on .

A random set is said to be acceptable if . In other words, is acceptable if contains a sequence of selections whose risk converges to zero. The monetary property of yields that is the set of all such that is acceptable, that is,

2.2 Properties of the selection risk measure

The selection risk measure was introduced in [12] for convex and coherent . Some of its properties for non-convex and general monetary are easy-to-show replica of those known in the convex coherent setting adopted in [12].

Theorem 2.1.

The selection risk measure satisfies the following properties for -integrable random lower closed sets and .

-

i)

Monotonicity, that is, if a.s.

-

ii)

Cash-invariance, that is, for all deterministic .

-

iii)

If is homogeneous, then is homogeneous, that is, for all deterministic .

-

iv)

If is convex, then is convex, that is,

(4) for all deterministic .

Proof.

We prove only the convexity, the rest is straightforward. All elements of the set on the right-hand side of (4) are coordinatewisely larger than or equal to

for and , . Then it suffices to note that this convex combination of risks of and dominates , which is an element of the left-hand side of (4). ∎

The monotonicity property of yields that for . The selection risk measure is said to be coherent if it is homogeneous and convex; this is the case if has all coherent components. If is coherent, is a -integrable random vector, and is a -integrable random lower closed set, then

| (5) |

This is easily seen from (4) choosing , , and using the homogeneity of . Note that the equality in (5) is not guaranteed even if is a deterministic set. Still, in this case, it provides a useful acceptability condition: is acceptable if .

A general set-valued function (not necessarily constructed using selections) defined for -integrable random sets is said to be monotonic, cash invariant, homogeneous or convex if it satisfies the corresponding properties from Theorem 2.1. The set-valued (selection) risk measure is called law invariant if its values on identically distributed random sets coincide.

2.3 Choice of selections

The definition of the selection risk measure involves taking union over all -integrable selections of . This family may be very rich even for simple random closed sets. In the following, we discuss general approaches suitable to reduce the family of selections needed to determine the selection risk measure.

With a lower closed set we associate the set of its Pareto optimal points, that is, the set of points such that for is only possible if . If is a random lower closed convex set, then the set of Pareto optimal points of is a random closed set, see [3, Lemma 3.1]. In the non-convex case, the cited result establishes that is graph measurable, so that its closure is a random closed set, see [10, Prop. 2.6]. If is closed and -integrable, then it is possible to reduce the union in (3) to selections of .

A lower random closed set is said to be quasi-bounded if is essentially bounded; is -integrably quasi-bounded if is -integrable.

Consider

| (6) |

where are deterministic lower convex closed cones. For the following result, assume that is convex law invariant, and the probability space is non-atomic. In this case, satisfies the dilatation monotonicity property, that is, dominates coordinatewisely the risk of a conditional expectation of , see [2, Cor. 4.59] and [9].

Proposition 2.2.

Proof.

Consider for , . By the dilatation monotonicity, dominates the risk of the conditional expectation of given . Thus, it is possible to replace by its conditional expectation, which is also a point in . ∎

In the convex setting, if is the sum of and a convex closed set , then the union in (3) can be reduced to the selections that are measurable with respect to the -algebra generated by .

3 Fixed points and the expectation

For a random closed set ,

denotes the set of its fixed points. The set is a lower closed set if is a lower closed set, it is convex if is convex.

Proposition 3.1.

Let be a -integrable random lower closed set. For the selection risk measure generated by any monetary risk measure , we have

| (7) |

If all components of are the negative of the essential infimum, then equals the set of fixed points of .

Proof.

If , then , since is a lower set. Choosing with all components being negative of the essential infima, it is easily seen that is acceptable if it has a selection with all a.s. non-negative components. In this case, a.s., whence . Note also that . ∎

The set of fixed points is a coherent selection risk measure, which is law invariant and not necessarily convex-valued.

Example 3.2.

The convex hull of is a (possibly, strict) subset of the set of fixed points of . Let be a random set in which equally likely take values and for . Then , while the set of fixed points of is the sum of the segment with end-points and .

Example 3.3.

The set of fixed points appears also in the following context. Let be a finite probability space, and let all components of be the Average Value-at-Risk at level , . Then

Indeed, since for all , we have for any . Because each is a lower set, we have for all . To show the reverse inclusion, assume that . Then is a deterministic selection of , whence .

If and is the negative expectation of , then becomes the selection expectation of . Note that is a coherent selection risk measure, which is law invariant on convex random sets, but may be not law invariant on non-convex ones. Indeed, if the non-convex deterministic set is considered a random closed set defined on the trivial probability space, then , while if the underlying probability space is non-atomic, see [11, Th. 2.1.26].

It might be tempting to define a set-valued risk measure by taking intersection of expected random sets with respect to varying probability measures. This would correspond to the construction of a convex function by taking the supremum of linear ones. However, taking expectation results in convex values for the risk measure if the probability space is non-atomic; otherwise, it depends on the atomic structure of the space. Furthermore, even in the convex setting, such a construction might not correspond to the existence of an acceptable selection from , as the following remark shows.

Remark 3.4.

For any family such that for all , define

| (8) |

where . Note that we use vector notation, e.g., means that all components of have mean , and

is the coordinatewise product of and . The so defined satisfies all properties from Theorem 2.1. However, in general is not a selection risk measure. Indeed, by letting , we see that the corresponding coherent vector-valued risk measure is given by

Assume that is -integrably bounded, so that is closed for all . Then if and only if for all , equivalently, for each there is such that . Since these selections may be different for different , we cannot infer that is acceptable with respect to a selection risk measure. Indeed, the acceptability of requires the existence of a single selection such that for all . Thus, is an example of a coherent set-valued risk measure, which, however, is not necessarily a selection one. The acceptability of under does not guarantee the existence of an acceptable selection of . Furthermore, this risk measure does not distinguish between and its convex hull.

4 Convexity and law invariance

The monotonicity property yields that is a subset of . It is well known that the selection expectation of an integrable random closed set is convex if the underlying probability space is non-atomic, see [11, Th. 2.1.26]. This result follows from Lyapunov’s theorem on ranges of vector-valued measures. The same holds for selection risk measures of convex random sets, if the underlying risk measure is convex, see [12, Th. 3.4]. This is however not the case for non-convex arguments, see Example 3.2 and Section 5.2.

Still, in some cases is convex even for non-convex . Assume that , and the components of are -lower semicontinuous convex risk measures, so that

| (9) |

where , , are the penalty functions corresponding to the components of . The following result generalises Lyapunov’s theorem in the sublinear setting, see also [13].

Theorem 4.1.

Let be a non-atomic probability space, and let the components of admit representation (9) with being all infinite unless belongs to a finite family from . Then is convex.

Proof.

We need to show that for two selections and , there is such that . In view of the convexity of , it suffices to ensure that

Assume that all components of are infinite for outside a finite set . Consider the mapping which assigns to each measurable subset the vector

It is easily verified that this map is a vector-valued measure. By Lyapunov’s theorem, its image is closed convex, hence there is a measurable subset such that

Then and for all . Hence,

where is a selection of . Therefore,

for all , so is indeed the required selection. ∎

Remark 4.2.

For a deterministic lower closed set , the selection risk measure is not always equal to . For instance, this is not the case in the framework of Theorem 4.1, or in the context of fixed transaction costs in Section 5.2. The set is said to be -convex (or risk-convex for ), if with any and any we also have . Then is -convex if and only if . It is easy to see that the intersection of risk convex sets is also risk convex. If is the negative expectation and the probability space is non-atomic, the risk convexity corresponds to the usual notion of convexity. If is the negative essential infimum, each lower set is risk convex.

Remark 4.3.

Consider . Then is convex if and only if, for each , there exists such that

The families of selections of random sets are not necessarily law invariant, i.e. they can differ for two random sets having the same distribution, see [11, Sec. 1.4.1]. This could result in the selection risk measure not being law invariant. Still, the law invariance of yields the law invariance of the selection risk measure for convex , see [12]. Below we consider the case of a possibly non-convex .

The risk measure is said to be Lebesgue continuous if it is continuous on a.s. convergent uniformly -integrably bounded sequences of random vectors.

Theorem 4.4.

Assume that the probability space is non-atomic and that is a Lebesgue continuous risk measure. Then the selection risk measure is law invariant on -integrably quasi-bounded portfolios.

Proof.

Let and share the same distribution, so that the corresponding closures and of their Pareto optimal points are -integrably bounded and share the same distribution. By the Lebesgue property and the -integrable boundedness of and , it is possible to take the union in (3) over -integrable selections of and respectively.

Let for . Since the weak closures of and coincide (see [11, Th. 1.4.3]), there is a sequence converging weakly to . Then , and the latter random variable is integrable. Thus, is relatively compact in . By passing to a subsequence, it is possible to assume that almost surely.

The Lebesgue continuity property yields that . Thus, , since the latter set is closed. Finally, , since the latter set is upper. ∎

It is known that each -risk measure with finite values and is Lebesgue continuous, see [8]. For , [6, Thms. 2.4, 5.2] provide equivalent formulations of the Lebesgue continuity property for convex risk measures. We give below another criterion.

Proposition 4.5.

Assume that is a coherent -risk measure such that

where is a uniformly integrable subset of . Then is Lebesgue continuous.

Proof.

Assume that a.s. and a.s. for all and . By Egorov’s theorem, for each , there is an event of probability at most such that uniformly on the complement of .

Using the fact that the absolute value of the difference of two suprema is bounded by the suprema of the absolute values of the differences, we have

The first term on the right-hand side converges to zero by the uniform convergence on , while the second converges to zero by the uniform integrability of . ∎

5 Fixed transaction costs

5.1 Bounds on the selection risk measure

Assume that the components of represent the same currency and transfers are not restricted, but whenever a transfer is made, a fixed cost is incurred. If is the capital position, then the corresponding set of attainable positions is given by with non-convex set

of portfolios available at price zero, where

The following bounds for the selection risk measure of are straightforward.

Proposition 5.1.

We have

| (10) |

Proof.

The first inclusion follows from the fact that is a selection of for all deterministic and that . The second inclusion holds, since . ∎

Example 5.2.

The inclusion on the left-hand side of (10) can be strict. Let , and let be with probability and otherwise. For any , we can define a selection such that equals with probability , with probability , and with probability . Taking the risk measure of such selections shows that contains all points on the segments with end-points and .

The following result provides rather simple bounds on the selection risk measure in case of fixed transaction costs.

Proposition 5.3.

-

i)

If and componentwisely, then

-

ii)

If is subadditive, then

whenever .

Proof.

i) Note that for , and

ii) follows from and the monotonicity of the selection risk measure. ∎

The following result identifies the selection risk measure of in some cases in terms of the risk of the total payoff

If is coherent with all identical components, it is easy to see that is acceptable if and only if is acceptable. The following result concerns the case, when all but one components of are identical.

Proposition 5.4.

-

i)

If all the components of are identical convex risk measures , then

-

ii)

If one of the components of is the negative essential infimum and all others are identical convex risk measures , then

-

iii)

If one of components of is the negative expectation and all others are identical convex risk measures such that for all , then

Proof.

By cash-invariance, it is possible to asssume that . The statement i) is shown in [3, Th. 5.1].

ii) Assume that the first component of is the negative essential infimum. Note that if and only if there is a selection such that , a.s. and for . By convexity and monotonicity of ,

Hence, if for all , then . On the other hand, if , then letting and , , yields a selection of such that .

iii) If , then there is such that and , . Denote . Since , we have

Thus,

| (11) |

Note that is equivalent to . Inequality (11) yields that . Therefore, as desired.

If , define a selection of by letting and , . Then and for , whence . ∎

5.2 Fixed transaction costs in case

If , then the portfolio is deterministic. However, in the non-convex case, may be a strict superset of . For instance, this happens in the context of Theorem 4.1 when .

In the following assume that is a coherent risk measure and . By Proposition 2.2, it suffices to consider selections satisfying with . If and so , then

If , then

Thus, the risk of is determined by the set

where varies between and . Then

| (12) |

Example 5.5.

Let , and let the both components of be the Average Value-at-Risk at level . If , then

Thus, if , then is the union of two segments and and it does not depend on . In this case, (12) yields that .

Assume now that . Then is the line that joins the points , , and . Only the middle segment differs from the case . If , then the points

constitute the segment with the end-points and . A calculation of the lower envelope of these segments yields that

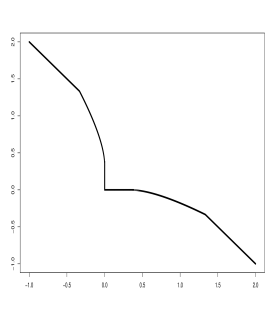

Figure 1 shows the risk of for . This set increases as grows and becomes if .

6 Finite sets of admissible transactions

We consider another special case when the selection risk measure of a non-convex set can be calculated explicitly. Assume that possible transactions are restricted to belong to a finite deterministic set in , that is,

Let have all components being the distortion risk measure (2) with distortion function . Since the analytical calculation of is not feasible, it is possible to use (5) to arrive at the bound

In the following we determine the last term on the right-hand side in dimension .

Example 6.1.

Consider the case of a two-point set . By translating, it is always possible to assume that . If consists of two points and with , then is determined by the set of values for all . Without loss of generality assume that and . Since and if , we have

Example 6.2.

Let consist of three points, and assume that and . In this case, possible selections can be either two-points-selections of two of these three points (in this case the risk is calculated as in Example 6.1), and three point selection attaining all three points with positive probabilities such that . The risk of the three-point selection can be directly calculated, so that

References

- [1] F. Delbaen. Monetary Utility Functions. Osaka University Press, Osaka, 2012.

- [2] H. Föllmer and A. Schied. Stochastic Finance. An Introduction in Discrete Time. De Gruyter, Berlin, 2 edition, 2004.

- [3] A. Haier, I. Molchanov, and M. Schmutz. Intragroup transfers, intragroup diversification and their risk assessment. Ann. Finance, 12:363–392, 2016.

- [4] A. H. Hamel and F. Heyde. Duality for set-valued measures of risk. SIAM J. Financial Math., 1:66–95, 2010.

- [5] A. H. Hamel, F. Heyde, and B. Rudloff. Set-valued risk measures for conical market models. Math. Finan. Economics, 5:1–28, 2011.

- [6] E. Jouini, W. Schachermayer, and N. Touzi. Law invariant risk measures have the Fatou property. Adv. Math. Econ., 9:49–71, 2006.

- [7] Yu. M. Kabanov and M. Safarian. Markets with Transaction Costs. Mathematical Theory. Springer, Berlin, 2009.

- [8] M. Kaina and L. Rüschendorf. On convex risk measures on -spaces. Math. Meth. Oper. Res., 69:475–495, 2009.

- [9] J. Leitner. Balayage monotonous risk measures. Int. J. Theor. Appl. Finance, 7:887–900, 2004.

- [10] E. Lépinette and I. Molchanov. Conditional cores and conditional convex hulls of random sets. Technical report, arXiv math: 1711.10303, 2017.

- [11] I. Molchanov. Theory of Random Sets. Springer, London, 2 edition, 2017.

- [12] I. Molchanov and I. Cascos. Multivariate risk measures: a constructive approach based on selections. Math. Finance, 26:867––900, 2016.

- [13] N. Sagara. A Lyapunov-type theorem for nonadditive vector measures. In Vicenç Torra, Yasuo Narukawa, and Masahiro Inuiguchi, editors, Modeling Decisions for Artificial Intelligence: 6th International Conference, MDAI 2009, Awaji Island, Japan, November 30–December 2, 2009. Proceedings, pages 72–80, Berlin, Heidelberg, 2009. Springer Berlin Heidelberg.