Optimal Mini-Batch and Step Sizes for SAGA

SUPPLEMENTARY MATERIAL

Optimal Mini-Batch and Step Sizes for SAGA

Abstract

Recently it has been shown that the step sizes of a family of variance reduced gradient methods called the JacSketch methods depend on the expected smoothness constant. In particular, if this expected smoothness constant could be calculated a priori, then one could safely set much larger step sizes which would result in a much faster convergence rate. We fill in this gap, and provide simple closed form expressions for the expected smoothness constant and careful numerical experiments verifying these bounds. Using these bounds, and since the SAGA algorithm is part of this JacSketch family, we suggest a new standard practice for setting the step and mini-batch sizes for SAGA that are competitive with a numerical grid search. Furthermore, we can now show that the total complexity of the SAGA algorithm decreases linearly in the mini-batch size up to a pre-defined value: the optimal mini-batch size. This is a rare result in the stochastic variance reduced literature, only previously shown for the Katyusha algorithm. Finally we conjecture that this is the case for many other stochastic variance reduced methods and that our bounds and analysis of the expected smoothness constant is key to extending these results.

1 Introduction

Consider the empirical risk minimization (ERM) problem:

| (1) |

where each is -smooth and is -strongly convex. Each represents a regularized loss over a sampled data point. Solving the ERM problem is often time consuming for large number of samples , so much so that algorithms scanning through all the data points at each iteration are not competitive. Gradient descent (GD) falls into this category, and in practice its stochastic version is preferred.

Stochastic gradient descent (SGD), on the other hand, allows to solve the ERM incrementally by computing at each iteration an unbiased estimate of the full gradient, for randomly sampled in (Robbins & Monro, 1951). On the downside, for SGD to converge one needs to tune a sequence of asymptotically vanishing step sizes, a cumbersome and time-consuming task for the user. Recent works have taken advantage of the sum structure in Eq. 1 to design stochastic variance reduced gradient algorithms (Johnson & Zhang, 2013; Shalev-Shwartz & Zhang, 2013; Defazio et al., 2014; Schmidt et al., 2017). In the strongly convex setting, these methods lead to fast linear convergence instead of the slow rate of SGD. Moreover, they only require a constant step size, informed by theory, instead of sequence of decreasing step sizes.

In practice, most variance reduced methods rely on a mini-batching strategy for better performance. Yet most convergence analysis (with the Katyusha algorithm of Allen-Zhu (2017) being an exception) indicates that a mini-batch size of gives the best overall complexity, disagreeing with practical findings, where larger mini-batch often gives better results. Here, we show both theoretically and numerically that is not the optimal mini-batch size for the SAGA algorithm (Defazio et al., 2014).

Our analysis leverages recent results in (Gower et al., 2018), where the authors prove that the iteration complexity and the step size of SAGA, and a larger family of methods called the JacSketch methods, depend on an expected smoothness constant. This constant governs the trade-off between the increased cost of an iteration as the mini-batch size is increased, and the decreased total complexity. Thus if this expected smoothness constant could be calculated a priori, then we could set the optimal mini-batch size and step size. We provide simple formulas for computing the expected smoothness constant when sampling mini-batches without replacement, and use them to calculate optimal mini-batches and significantly larger step sizes for SAGA.

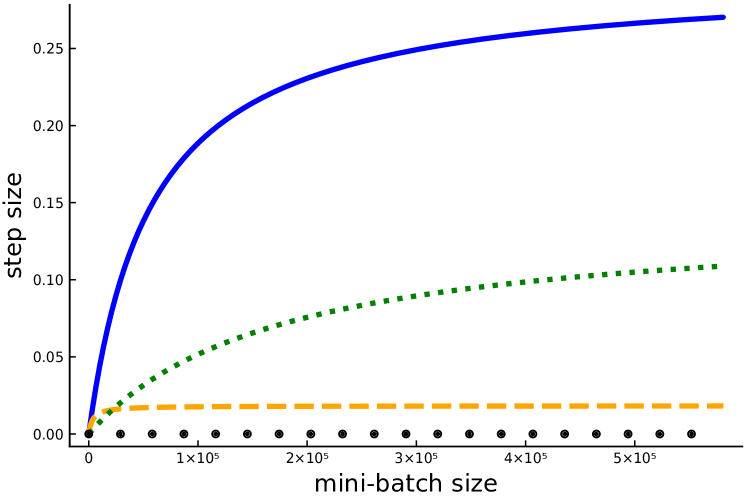

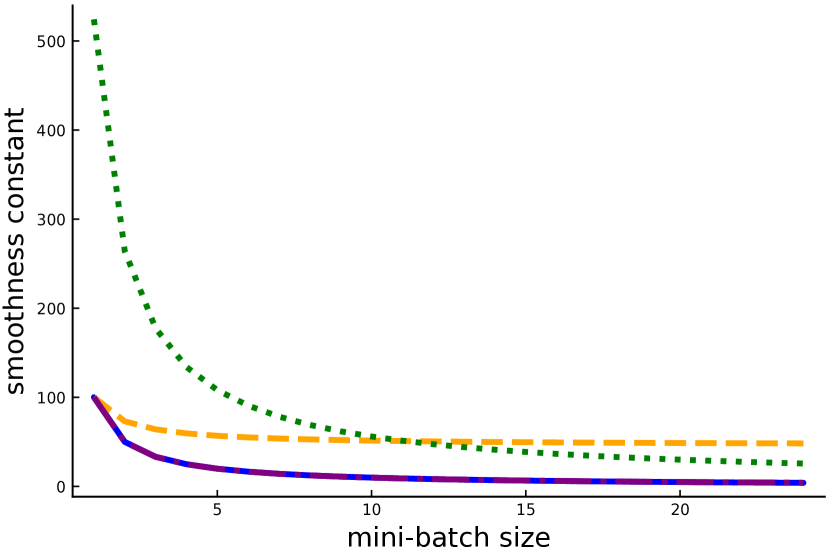

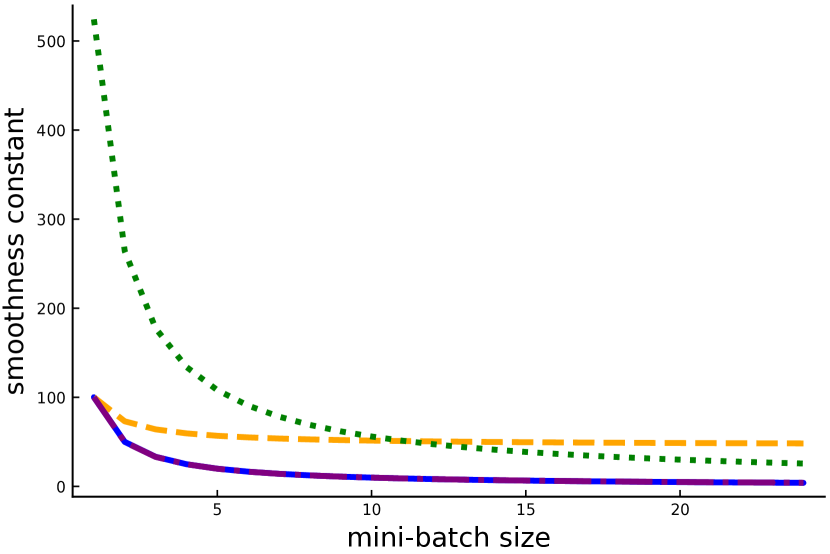

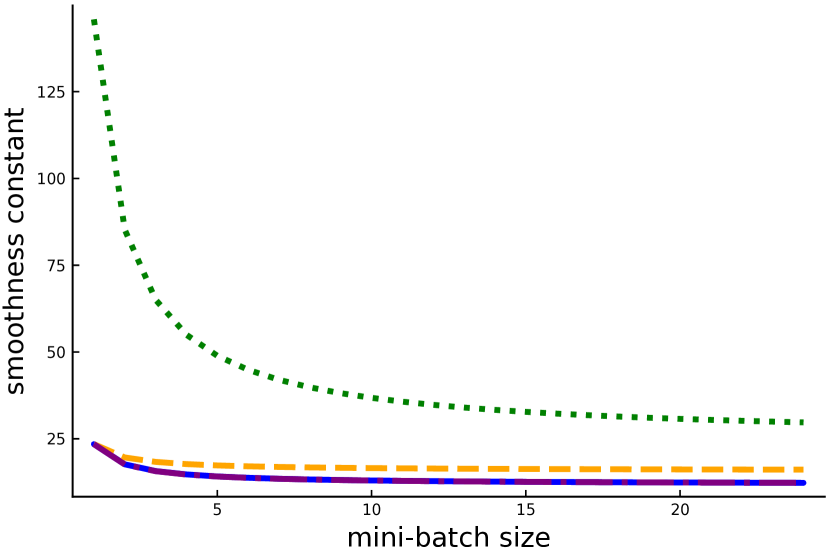

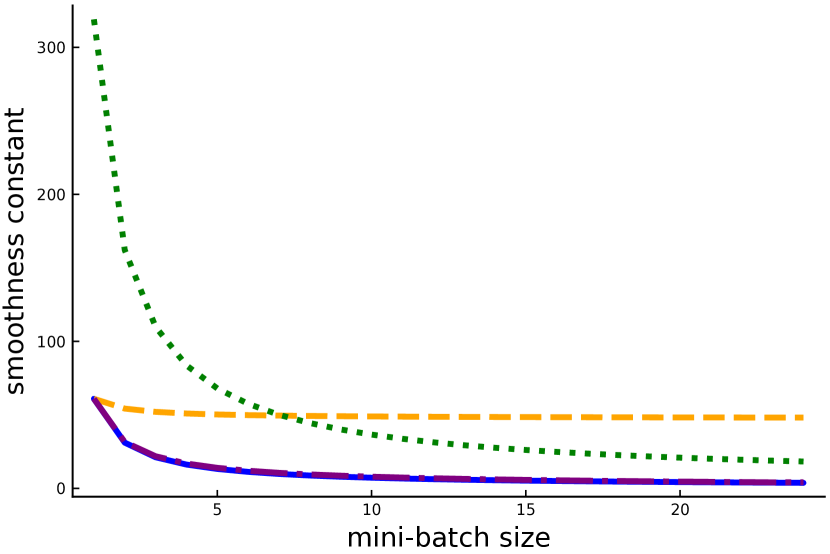

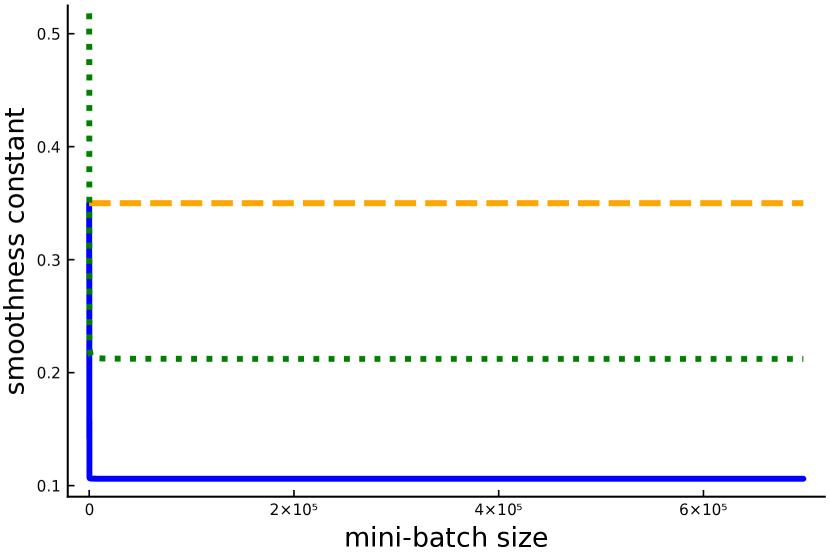

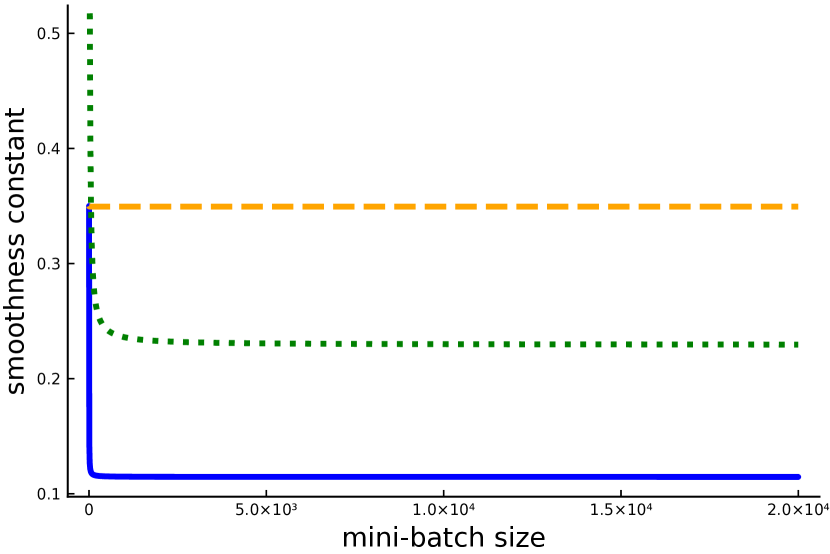

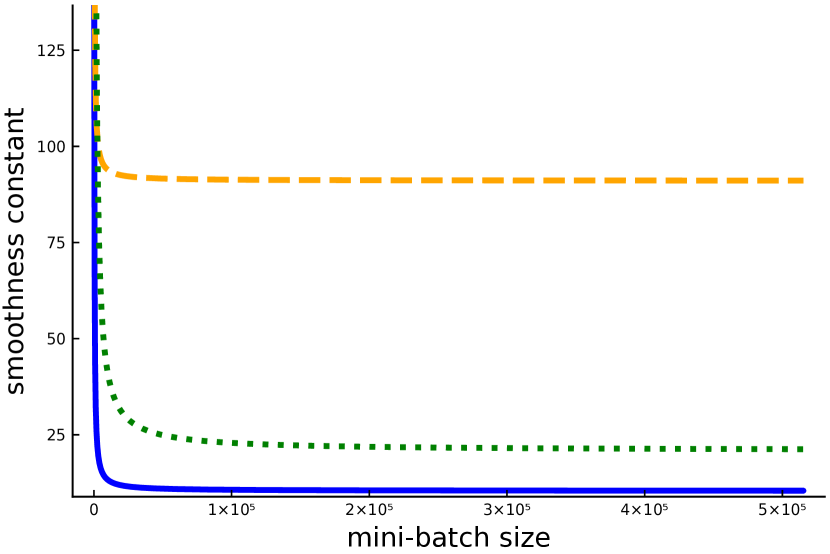

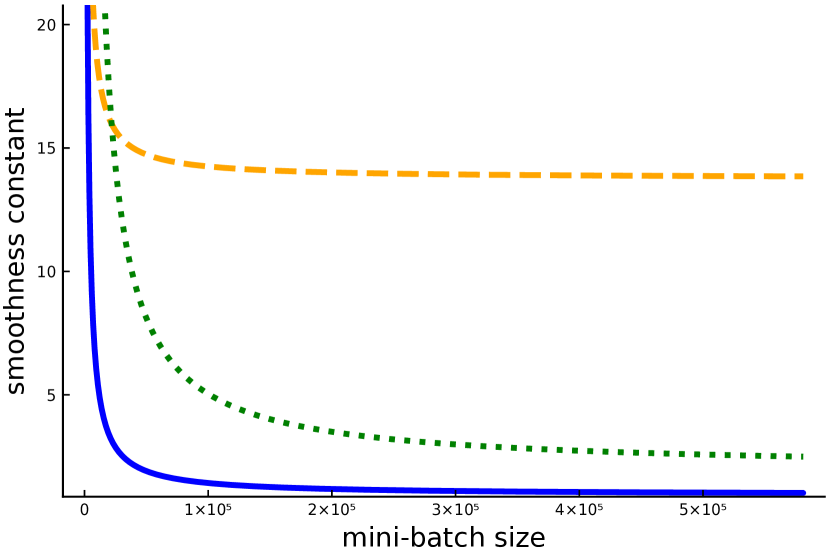

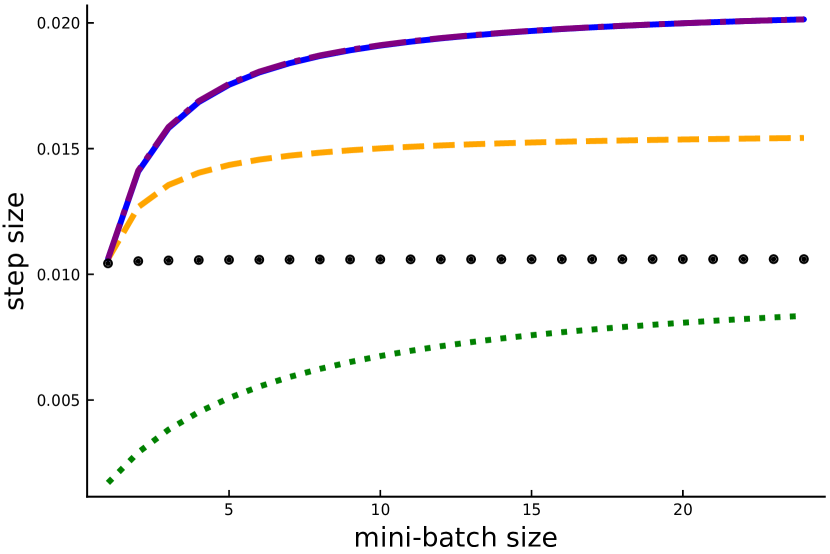

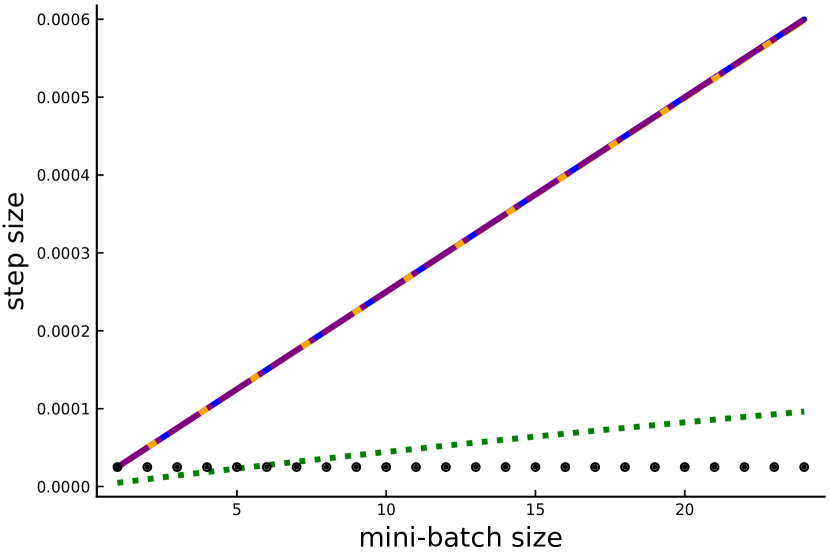

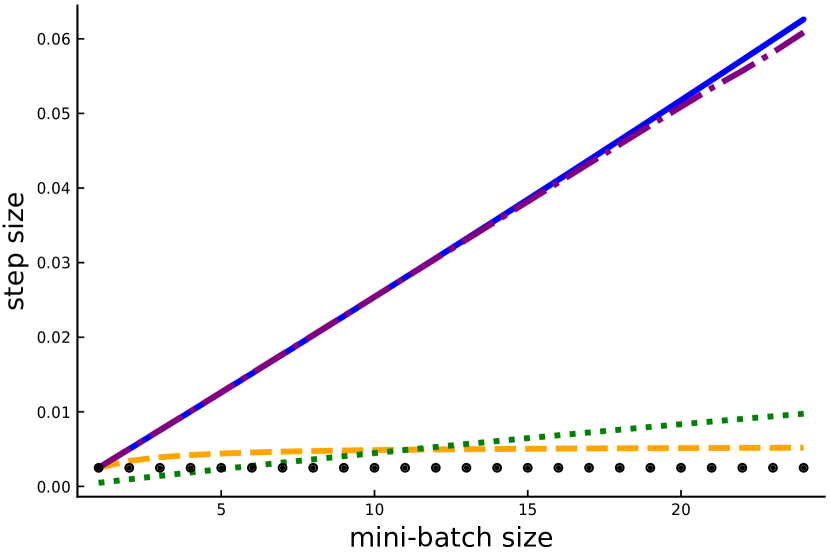

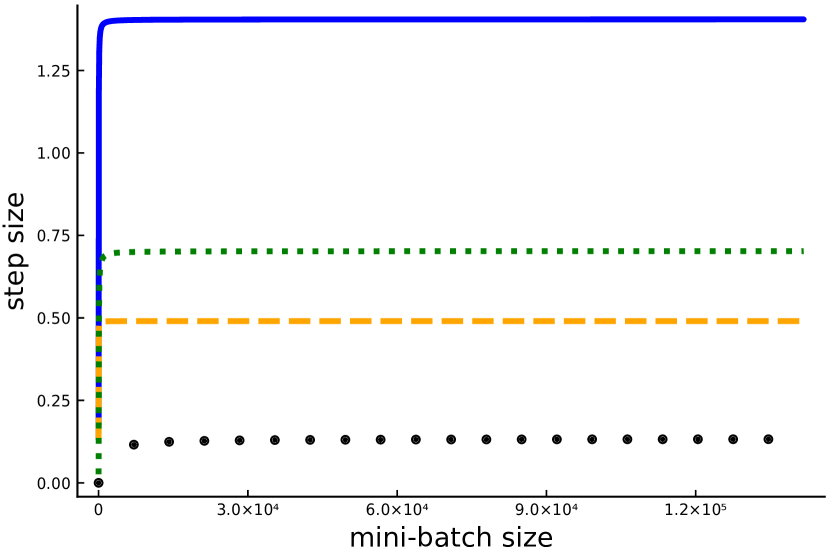

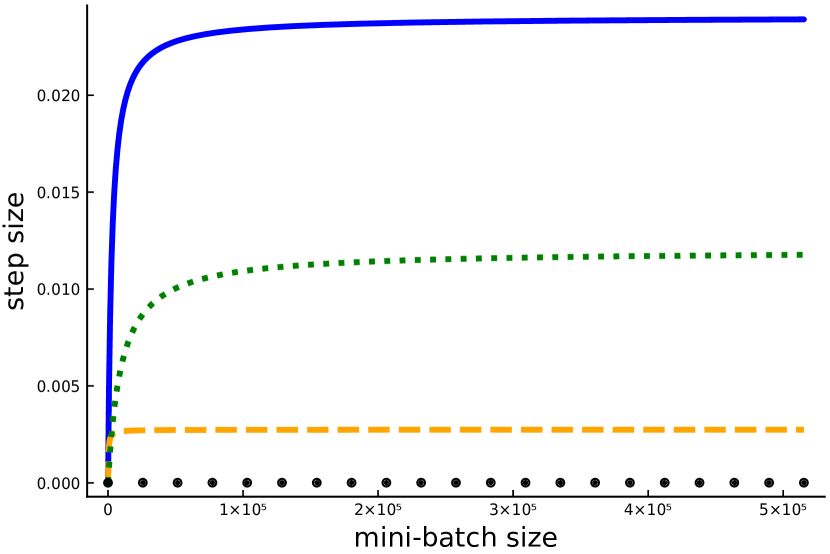

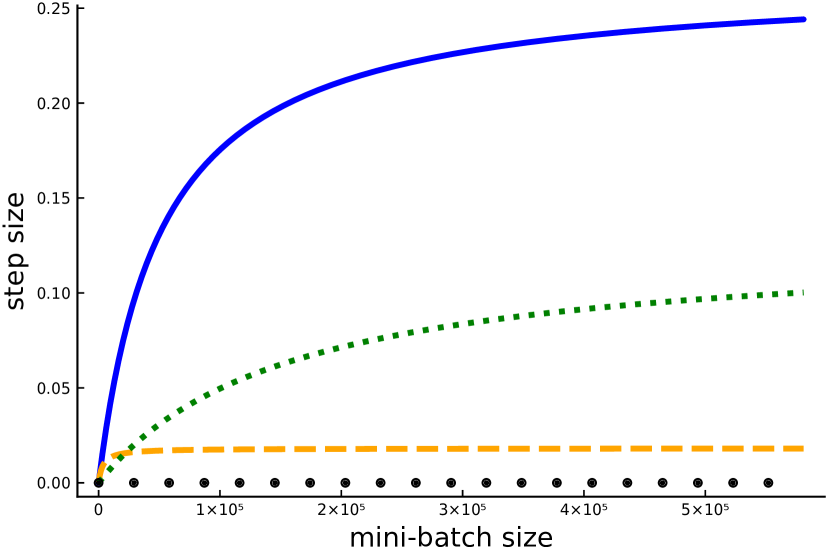

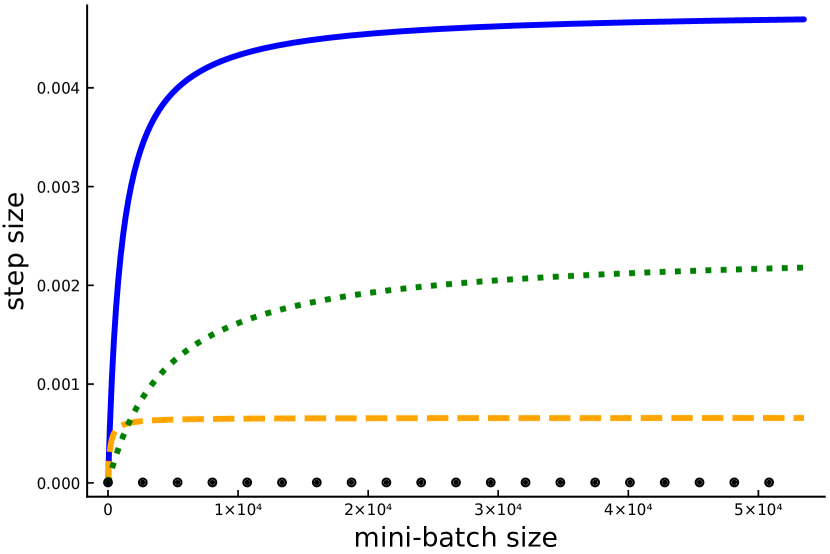

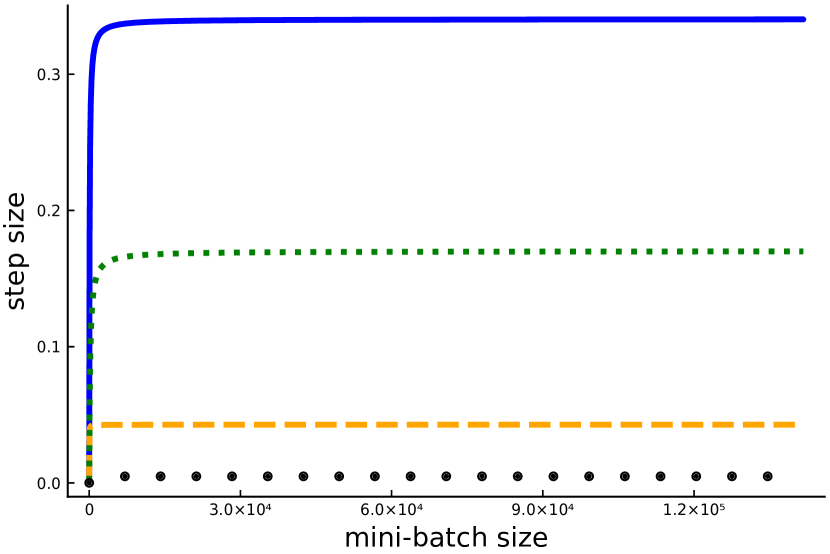

In particular, we provide two bounds on the expected smoothness constant, each resulting in a particular step size formula. We first derive the simple bound and then develop a matrix concentration inquality to obtain the refined Bernstein bound. We also provide substantial theoretical motivation and numerical evidence for practical estimate of the expected smoothness constant. For illustration, we plot in Figure 1 the evolution of each resulting step size as the mini-batch size grows on a classification problem (Section 5 has more details on our experimental settings).

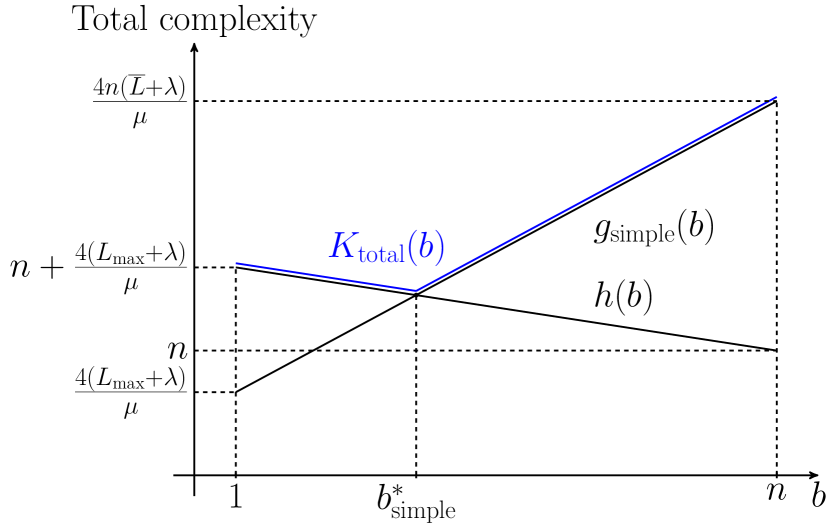

Furthermore, our bounds provide new insight into the total complexity, denoted hereafter, of SAGA. For example, when using our simple bound we show for regularized generalized linear models (GLM), with as in Eq. 10, that is piecewise linear in the mini-batch size :

with , and is the desired precision.

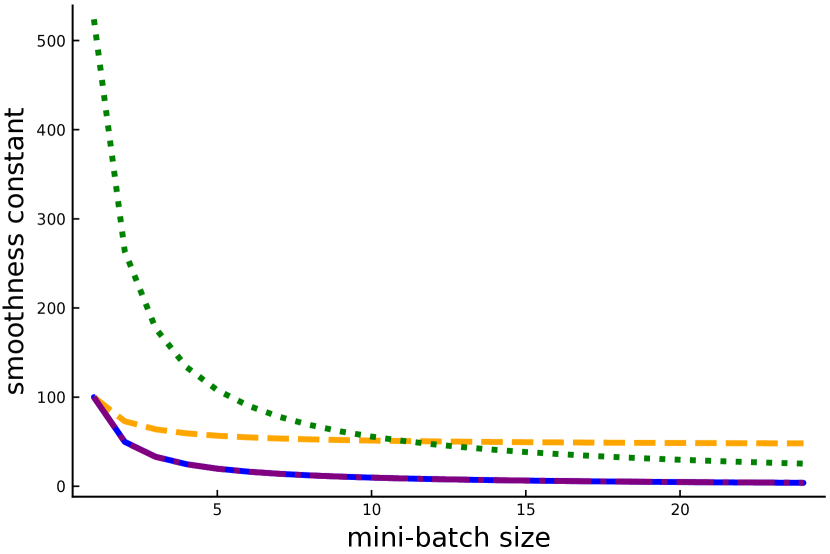

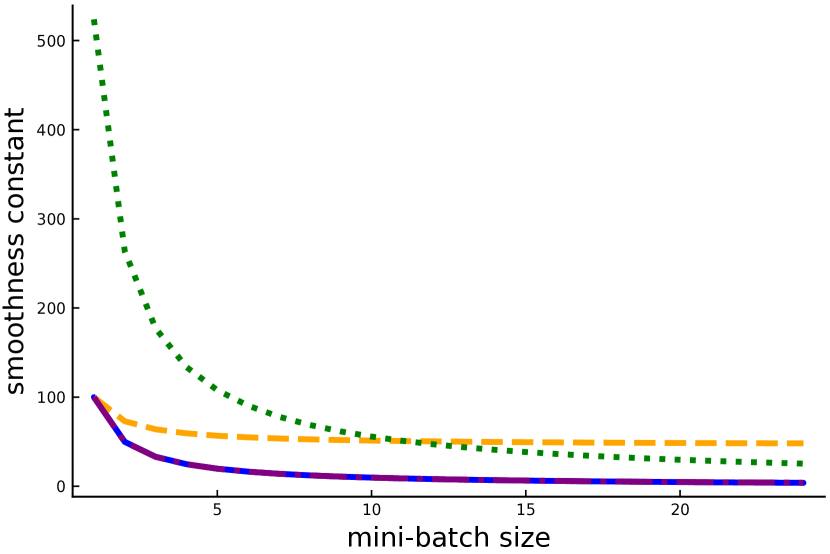

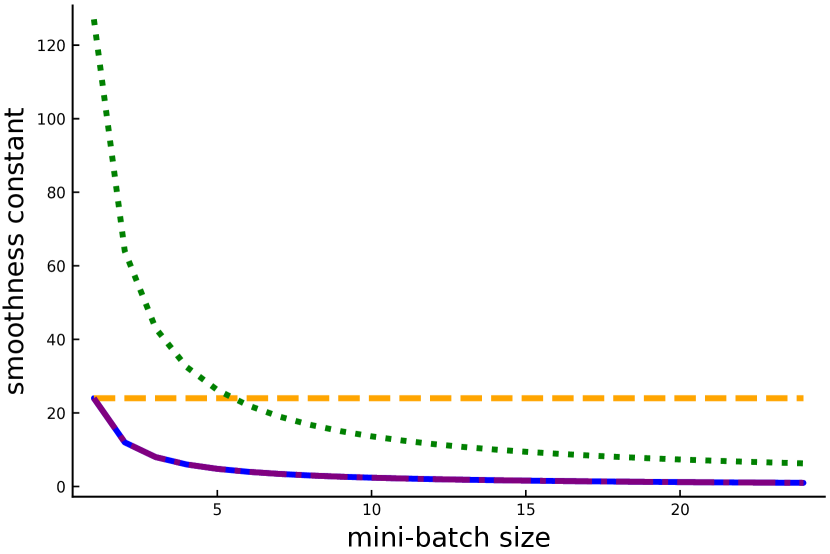

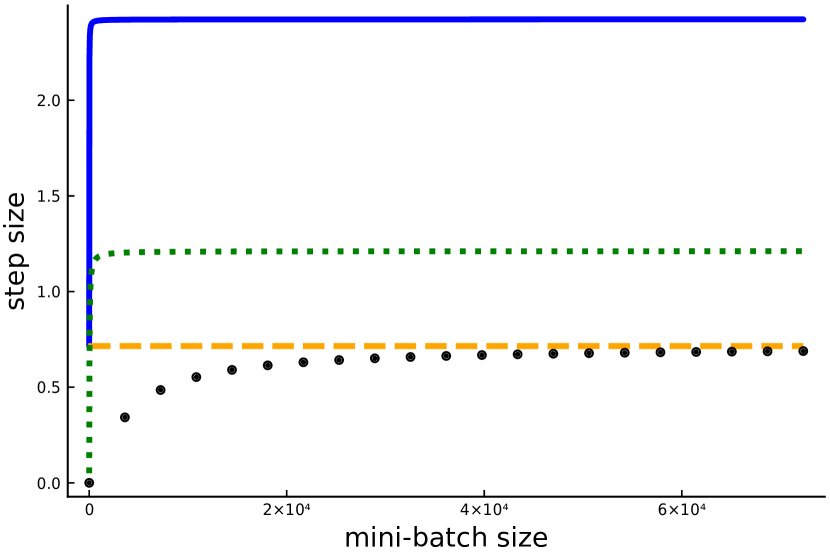

This complexity bound, and others presented in Section 3.3 show that SAGA enjoys a linear speedup as we increase the mini-batch size until an optimal one (as illustrated in Figure 2). After this point, the total complexity increases. We use this observation to develop optimal and practical mini-batch sizes and step sizes.

The rest of the paper is structured as follows. In Section 2 we first introduce variance reduction techniques after presenting our main assumption, the expected smoothnes assumption. We highlight how this assumption is necessary to capture the improvement in iteration complexity, and conclude the section by showing that to calculate the expected smoothness constant we need evaluate an intractable expectation. Which brings us to Section 3 where we directly address this issue and provide several tractable upper-bounds of the expected smoothness constant. We then calculate optimal mini-batch sizes and step sizes by using our new bounds. Finally, we give numerical experiments in Section 5 that verify our theory on artificial and real datasets. We also show how these new settings for the mini-batch size and step size lead to practical performance gains.

2 Background

2.1 Controlled stochastic reformulation and JacSketch

We can introduce variance reduced versions of SGD in a principled manner by using a sampling vector.

Definition 1.

We say that a random vector with distribution is a sampling vector if

With a sampling vector we can re-write (1) through the following stochastic reformulation

| (2) |

where is called a subsampled function. The stochastic Problem (2) and our original Problem (1) are equivalent :

Consequently the gradient is an unbiased estimate of and we could use the SGD method to solve (2). To tackle the variance of these stochastic gradients we can further modify (2) by introducing control variates which leads to the following controlled stochastic reformulation:

| (3) |

where are the control variates. Clearly (3) is also equivalent to (1) since has zero expectation. Thus, we can solve (3) using an SGD algorithm where the stochastic gradients are given by

| (4) |

That is, starting from a vector , given a positive step size , we can iterate the steps

| (5) |

where are i.i.d. samples at each iteration.

The JacSketch algorithm introduced by Gower et al. (2018) fits this format (5) and uses a linear control , where is a matrix of parameters. This matrix is updated at each iteration so as to decrease the variance of the resulting stochastic gradients. Carefully updating the covariates through results in a method that has stochastic gradients with decreasing variance, i.e., , which is why JacSketch is a stochastic variance reduced algorithm. This is also why the user can set a single constant step size a priori instead of tuning a sequence of decreasing ones. The SAGA algorithm, and all of its mini-batching variants, are instances of the JacSketch method.

2.2 The expected smoothness constant

In order to analyze stochastic variance reduced methods, some form of smoothness assumption needs to be made. The most common assumption is

| (6) |

for each . That is each is uniformly smooth with smoothness constant , as is assumed in (Defazio et al., 2014; Hofmann et al., 2015; Raj & Stich, 2018) for variants of SAGA111The same assumption is made in proofs of SVRG (Johnson & Zhang, 2013), S2GD (Konečný & Richtárik, 2017) and the SARAH algorithm (Nguyen et al., 2017).. In the analyses of these papers it was shown that the iteration complexity of SAGA is proportional to and the step size is inversely proportional to

But as was shown in (Gower et al., 2018), we can set a much larger step size by making use of the smoothness of the subsampled functions For this Gower et al. (2018) introduced the notion of expected smoothness, which we extend here to all sampling vectors and control variates.

Definition 2 (Expected smoothness constant).

Consider a sampling vector with distribution We say that the expected smoothness assumption holds with constant if for every we have that

| (7) |

Remark 1.

Note that we refer to any positive constant that satisfies (7) as an expected smoothness constant. Indeed is a valid constant in the extended reals, but as we will see, the smaller , the better for our complexity results.

Gower et al. (2018) show that the expected smoothness constant plays the same role that does in the previously existing analysis of SAGA, namely that the step size is inversely proportional to and the iteration complexity is proportional to (see details in Theorem 1). Furthermore, by assuming that is –smooth, the expected smoothness constant is bounded

| (8) |

as was proven in Theorem 4.17 in (Gower et al., 2018). Also, the bounds and are attained when using a uniform single element sampling and a full batch, respectively. And as we will show, the constants and can be orders of magnitude apart on large dimensional problems. Thus we could set much larger step sizes for larger mini-batch sizes if we could calculate . Though calculating is not easy, as we see in the next lemma.

Lemma 1.

Let be an unbiased sampling vector. Suppose that is -smooth and each is convex for . It follows that the expected smoothness constant holds with .

Proof.

The proof is given in Section A.1. ∎

If the sampling has a very large combinatorial number of possible realizations — for instance sampling mini-batches without replacement — then this expectation becomes intractable to calculate. This observation motivates the development of functional upper-bounds of the expected smoothness constant that can be efficiently evaluated.

2.3 Mini-batch without replacement: –nice sampling

Now we will choose a distribution of the sampling vector based on a mini-batch sampling without replacement. We denote a mini-batch as and its size as .

Definition 3 (-nice sampling).

is a -nice sampling if is a set valued map with a probability distribution given by

We can construct a sampling vector based on a -nice sampling by setting , where is the canonical basis of . Indeed, is a sampling vector according to Definition 1 since for every we have

| (9) |

where denotes the indicator function of the random set . Now taking expectation in (9) gives

using .

Here we are interested in the mini-batch SAGA algorithm with -nice sampling, which we refer to as the -nice SAGA. In particular, -nice SAGA is the result of using -nice sampling, together with a linear model for the control variate . Different choices of the control variate also recover popular algorithms such as gradient descent, SGD or the standard SAGA method (see Table 1 for some examples).

A naive implementation of -nice SAGA based on the JacSketch algorithm is given in Algorithm 1222We also provide a more efficient implementation that we used for our experiments in the appendix in Algorithm 2..

3 Upper Bounds on the Expected Smoothness

To determine an optimal mini-batch size for -nice SAGA, we first state our assumptions and provide bounds of the smoothness of the subsampled function. We then define as the mini-batch size that minimizes the total complexity of the considered algorithm, i.e., the total number of stochastic gradients computed. Finally we provide upper-bounds on the expected smoothness constant , through which we can deduce optimal mini-batch sizes. Many proofs are deferred to the supplementary material.

| Parameters | ||

|---|---|---|

| GD | ||

| SGD | 0 | |

| SAGA | ||

| -nice SAGA |

3.1 Assumptions and notation

We consider that the objective function is a GLM with quadratic regularization controlled by a parameter :

| (10) |

with is the Euclidean norm, are convex functions and a sequence of observations in . This framework covers regularized logistic regression by setting for some binary labels in , ridge regression if for real observations , and conditional random fields for when the ’s are structured outputs.

We assume that the second derivative of each is uniformly bounded, which holds for our aforementioned examples.

Assumption 1 (Bounded second derivatives).

There exists such that .

For a batch , we rewrite the subsampled function as

and its second derivative is thus given by

| (11) |

where denotes the identity matrix of size .

For a symmetric matrix , we write (resp. ) for its largest (resp. smallest) eigenvalue. Assumption 1 directly implies the following.

Lemma 2 (Subsample smoothness constant).

Let , and let denote the column concatenation of the vectors with The smoothness constant of the subsampled loss function is given by

| (12) |

Another key quantity in our analysis is the strong convexity parameter.

Definition 4.

The strong convexity parameter is given by

Since we have an explicit regularization term with , is strongly convex and

We additionally define , resp. , as the smoothness constant of the individual function , resp. the whole function . We also recall the definitions of the maximum of the individual smoothness constants by and their average by . The three constants satisfies

| (13) |

3.2 Path to the optimal mini-batch size

Our starting point is the following theorem taken from combining Theorem 3.6 and Eq. (103) in (Gower et al., 2018)333Note that has been added to every smoothness constant since the analysis in Gower et al. (2018) depends on the -smoothness of and the -smoothness of the subsampled functions ..

Theorem 1.

Through Theorem 1 we can now explicitly see how the expected smoothness constant controls both the step size and the resulting iteration complexity. This is why we need bounds on so that we can set the step size. In particular, we will show that the expected smoothness constant is a function of the mini-batch size . Consequently so is the step size, the iteration complexity and the total complexity. We denote the total complexity defined as the number of stochastic gradients computed, hence with (15),

| (16) | ||||

Once we have determined as a function of , we will calculate the mini-batch size that optimizes the total complexity .

As we have shown in Lemma 1, computing a precise bound on can be computationally intractable. This is why we focus on finding upper bounds on that can be computed, but also tight enough to be useful. To verify that our bounds are sufficiently tight, we will always have in mind the bounds given in (8). In particular, after expressing our bounds of as a function of ,we would like the bounds (8) to be attained for and

3.3 Expected smoothness

All bounds we develop on are based on the following lemma, which is a specialization of (1) for -nice sampling.

Proposition 1 (Expected smoothness constant).

For the -nice sampling, with , the expected smoothness constant is given by

| (17) |

Proof.

Let the -nice sampling as defined in Definition 3 and let be its corresponding sampling vector. Note that

Finally from Lemma 1, we have that:

Taking the maximum over all gives the result. ∎

The first bound we present is technically the simplest to derive, which is why we refer to it as the simple bound.

Theorem 2 (Simple bound).

For a -nice sampling , for , we have that

| (18) |

Proof.

The proof, given in Section A.2, starts by using the that for all subsets , which follows from repeatedly applying Lemma 8 in the appendix. The remainder of the proof follows by straightforward counting arguments. ∎

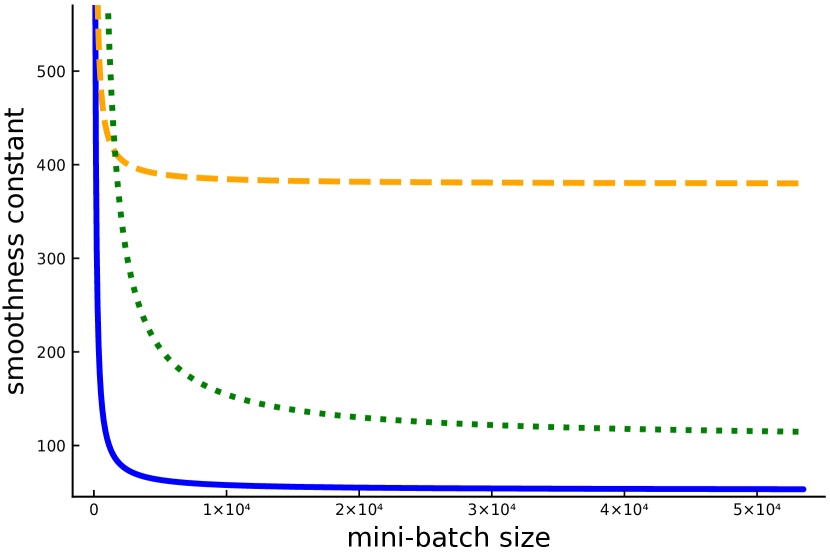

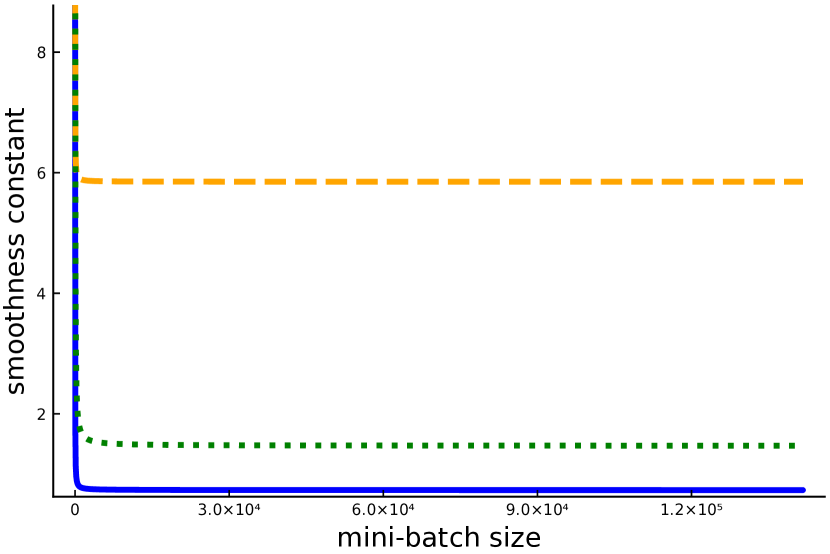

The previous bound interpolates, respectively for and , between and On the one hand, we have that is a good bound for when is small, since . Though may not be a good bound for large , since , thanks to (13). Thus does not achieve the left-hand side of (8). Indeed can be far from . For instance555We numerically explore such extreme settings in Section 5., if is a quadratic function, then we have that and . Thus if the eigenvalues of are all equal then . Alternatively, if one eigenvalue is significantly larger than the rest then .

Due to this shortcoming of we now derive the Bernstein bound. This bound explicitly depends on instead of , and is developed through a specialized variant of a matrix Bernstein inequality (Tropp, 2012, 2015) for sampling without replacement in Appendix C.

Theorem 3 (Bernstein bound).

The expected smoothness constant is upper bounded by

| (19) |

Checking again the bounds of , we have on the one hand that thus there is a little bit of slack for small. On the other hand, using (see Lemma 10 in appendix), we have that

which depends only logarithmically on . Thus we expect the Bernstein bound to be more useful in the large domains, as compared to the simple bound. We confirm this numerically in Section 5.1.

Remark 2.

The simple bound is relatively tight for small, while the Bernstein bound is better for large and large . Fortunately, we can obtain a more refined bound by taking the minimum of the simple and the Bernstein bounds. This is highlighted numerically in Section 5.

Next we propose a practical estimate of that is tight for both small and large mini-batch sizes.

Definition 5 (Practical estimate).

| (20) |

Indeed and achieving both limits of (8). The downside to is that it is not an upper bound of . Rather, we are able to show that is very close to a valid smoothness constant, but it can be slightly smaller. Our theoretical justification for using comes from a mid step in the proof of the Bernstein bound which is captured in the next lemma.

Lemma 3.

Let for and let be a -nice sampling over for every . It follows that

| (21) |

with .

Proof.

The proof is given in Section A.3. ∎

Lemma 3 shows that the expected smoothness constant is upper-bounded by and an additional term. In this additional term we have the largest eigenvalue of a random matrix. This matrix is zero in expectation, and we also find that its eigenvalues oscillate around zero. Indeed, we provide extensive experiments in Section 5 confirming that is very close to given in (17).

4 Optimal Mini-Batch Sizes

Now that we have established the simple and the Bernstein bounds, we can minimize the total complexity (16) in the mini-batch size.

Remark 3.

The right-hand side term is common to all our bounds since it does not depend on . It linearly decreases from to .

We note that is a linearly increasing function of , because (as proven in Lemma 10). One can easily verify that and cross, as presented in Figure 2, by looking at initial and final values:

-

•

At , . So, .

-

•

At , . Since , we get .

Consequently, solving in gives the optimal mini-batch size

| (22) |

For the Bernstein bound, plugging (19) into (16) leads to

| (23) |

where

The function is also linearly increasing in and its initial and final values are

-

•

At ,

-

•

At , . Since , we get .

Yet, it is unclear whether is dominated by . This is why we need to distinguish two cases to minimize the total complexity, which leads to the following solution

In the first case, the problem is well-conditioned and and do cross at a mini-batch size between and . In the second case, the total complexity is governed by because for all , and the resulting optimal mini-batch size is .

5 Numerical Study

All the experiments were run in Julia and the code is freely available on https://github.com/gowerrobert/StochOpt.jl.

5.1 Upper-bounds of the expected smoothness constant

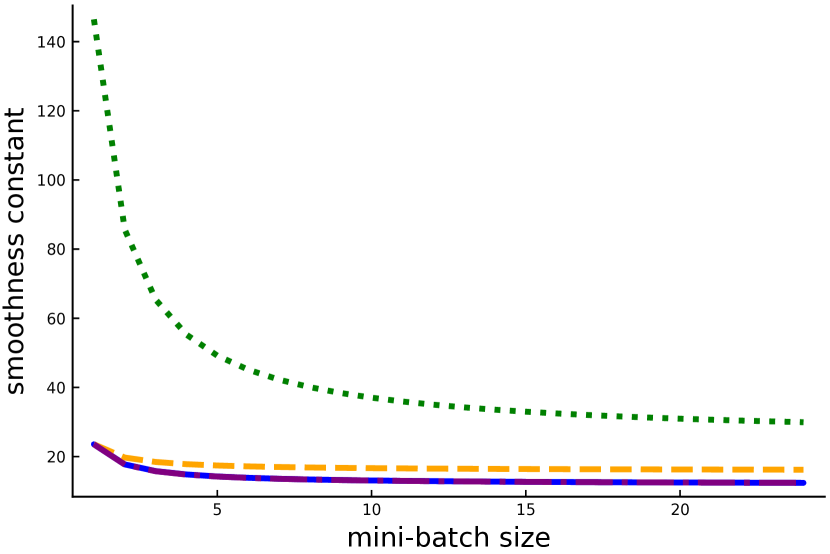

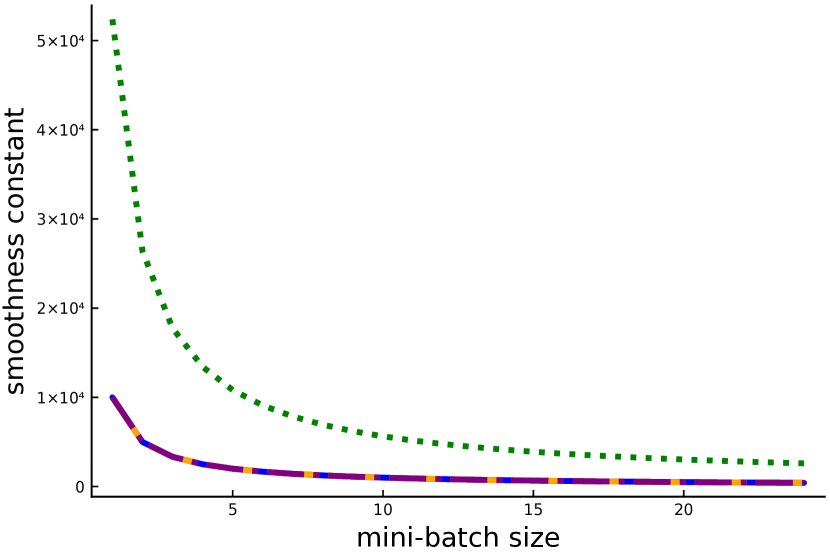

First we experimentally verify that our upper-bounds hold and how much slack there is between them and given in Equation 17. For ridge regression applied to artificially generated small datasets, we compute Equation 17 and compare it to our simple and Bernstein bounds, and our practical estimate. Our data are matrices defined as follows

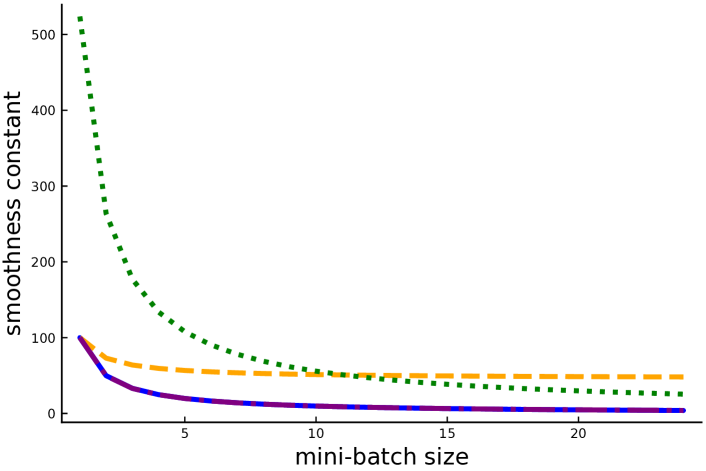

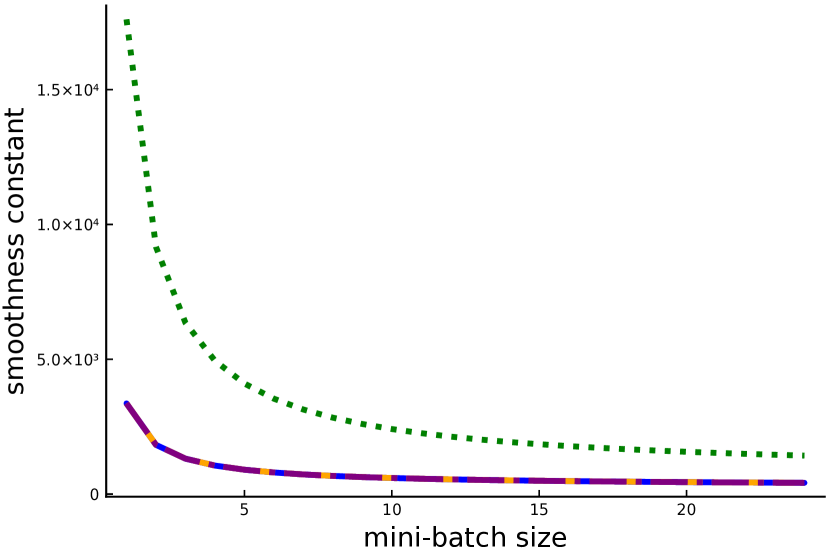

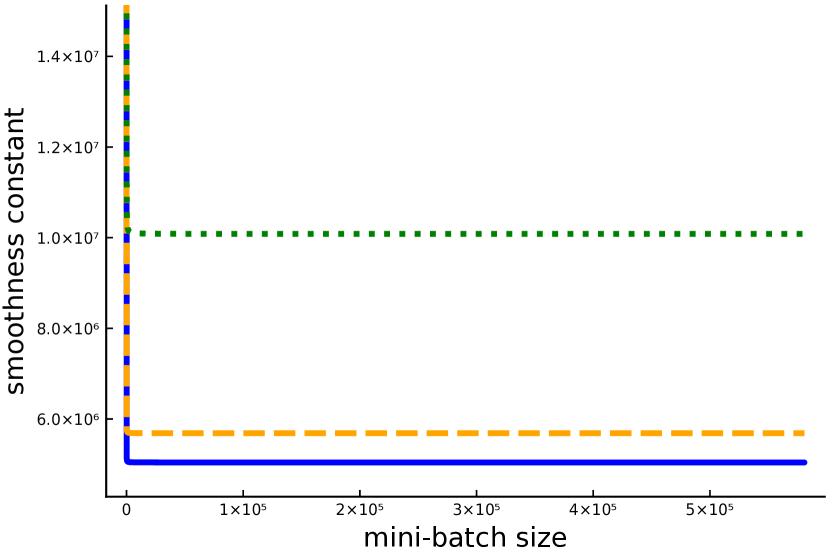

In Figure 4 we see that is arbitrarily close to , making it hard to distinguish the two line plots. This was the case in many other experiments, which we defer to Section E.1. For this reason, we use in our experiments with the SAGA method.

Furthermore, in accordance with our discussion in Section 3.3, we have that and are close to when is small and large, respectively. In Section E.2 we show, by applying ridge and regularized logistic regression to publicly available datasets from LIBSVM666https://www.csie.ntu.edu.tw/~cjlin/libsvmtools/datasets/ and the UCI repository777https://archive.ics.uci.edu/ml/datasets/, that the simple bound performs better than the Bernstein bound when , and conversely for slightly smaller than , larger than or when scaling the data.

5.2 Related step size estimation

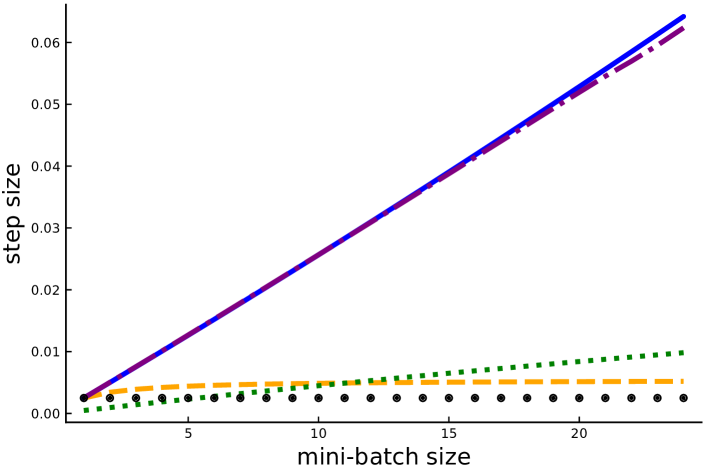

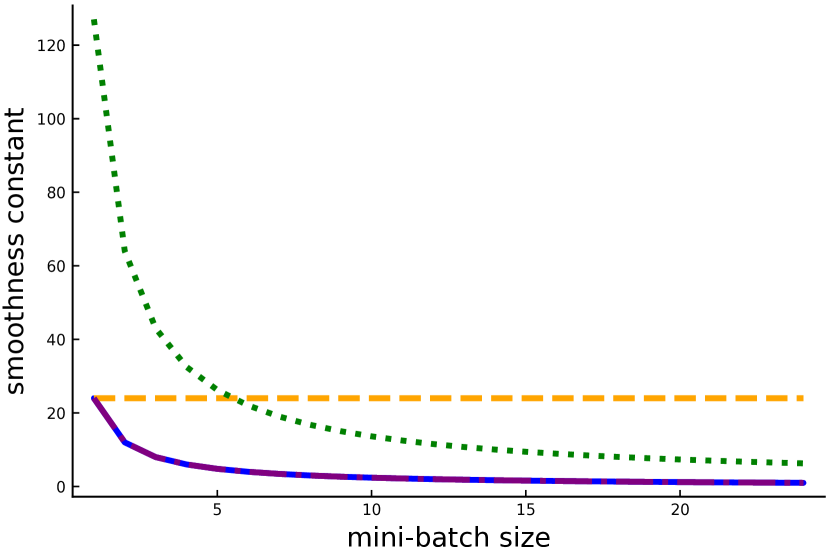

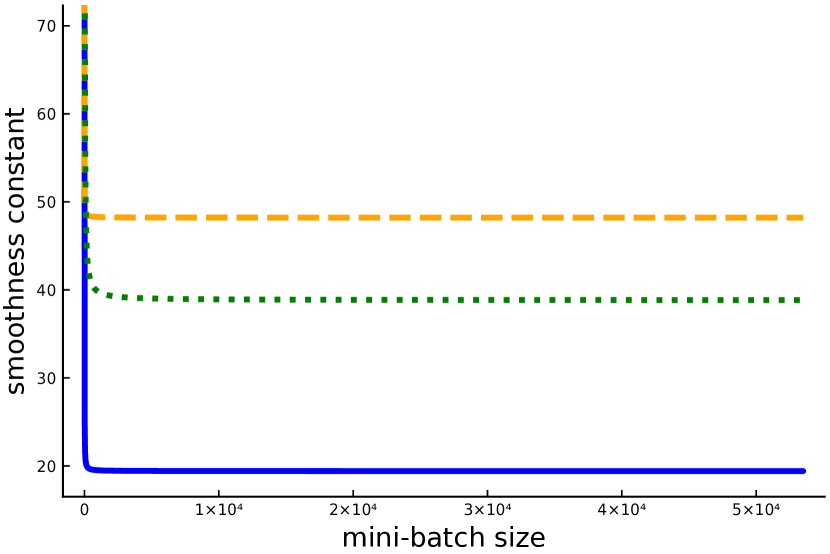

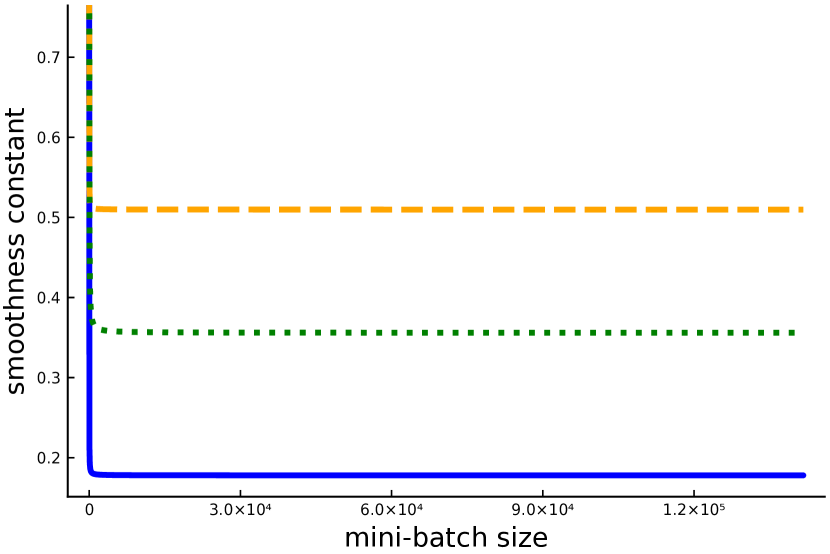

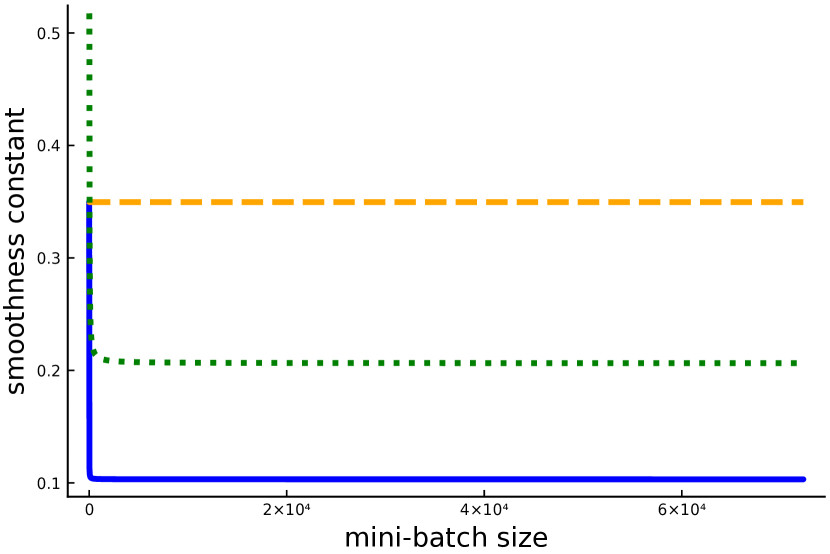

Different bounds on also give different step sizes (14). Plugging in our estimates , and into (14) gives the step sizes , and , respectively. We compare our resulting step sizes to where is given by Eq. 17 and to the step size given by Hofmann et al. (2015), which is , where We can see in Figure 4, that for , all the step sizes are approximately the same, with the exceptions of the Bernstein step size. For , all of our step sizes are larger than , in particular is significantly larger. These observations are verified in other artificial and real data examples in Sections E.3 and E.4.

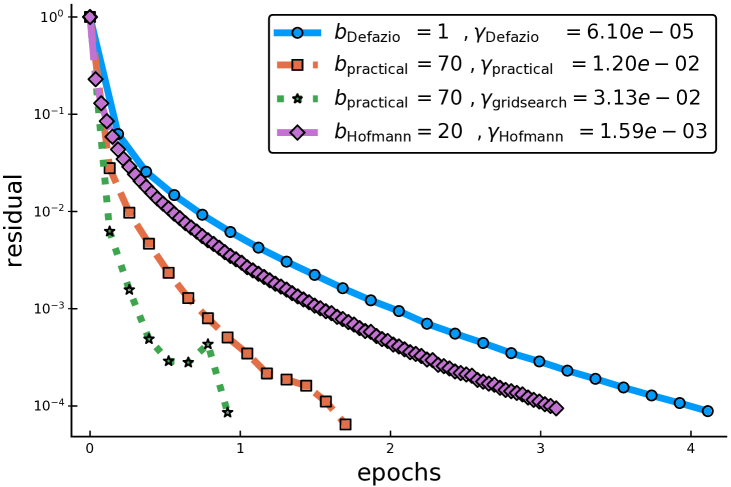

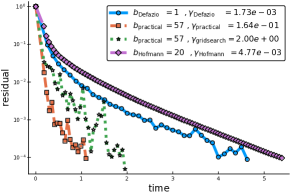

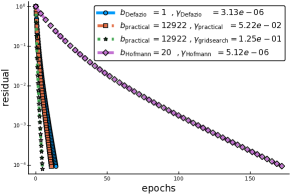

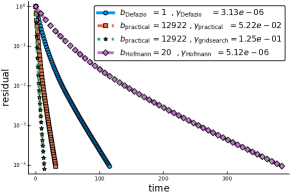

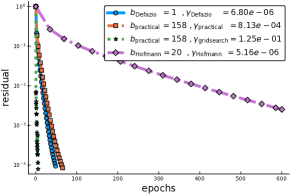

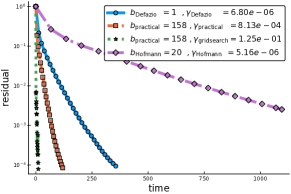

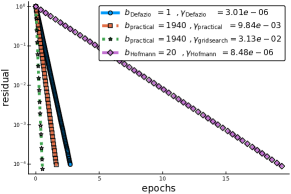

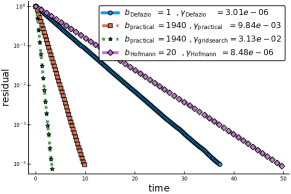

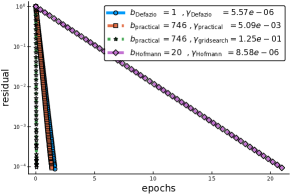

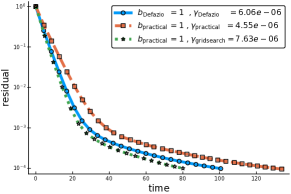

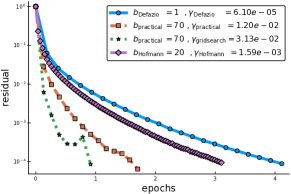

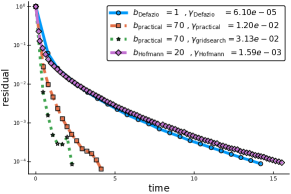

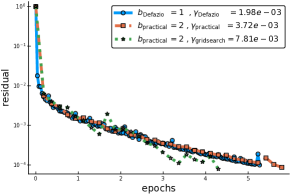

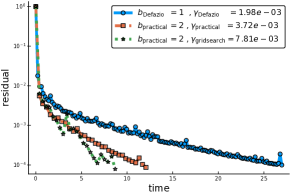

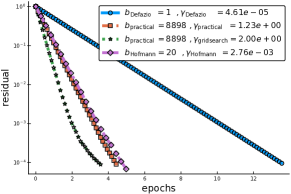

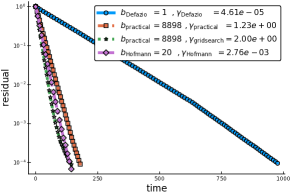

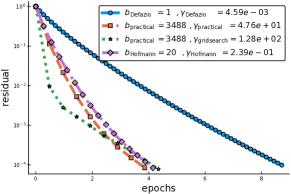

5.3 Comparison with previous SAGA settings

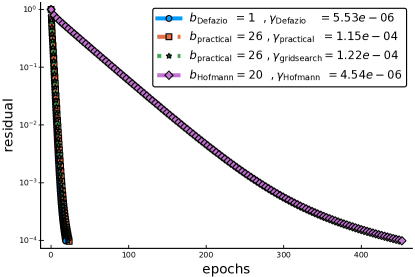

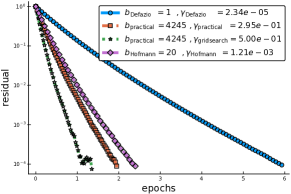

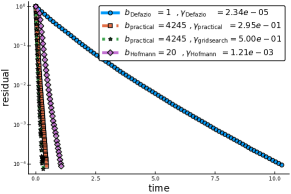

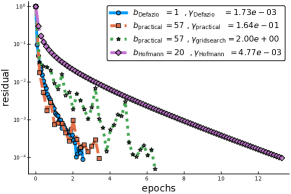

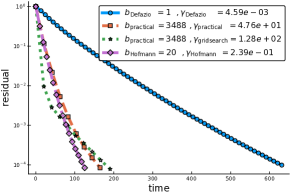

Here we compare the performance of SAGA when using the mini-batch size and step size given in (Defazio et al., 2014), and given in Hofmann et al. (2015), to our new practical mini-batch size and step size . Our goal is to verify how much our parameter setting can improve practical performance. We also compare with a step size obtained by grid search over odd powers of . These methods are run until they reach a relative error of .

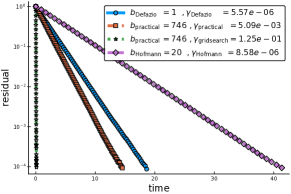

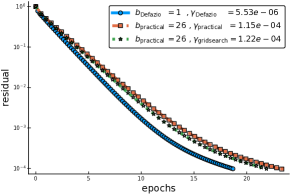

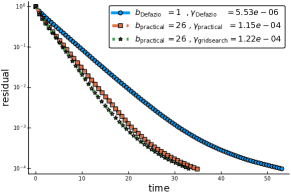

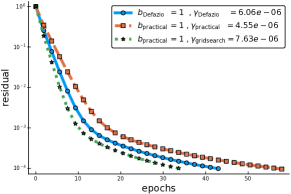

We find in Figure 5 that our parameter settings significantly outperforms the previously suggested parameters, and is even comparable to grid search. Finally, In we show in Section E.5 that the settings can lead to very poor performance compared to our settings.

5.4 Optimality of our mini-batch size

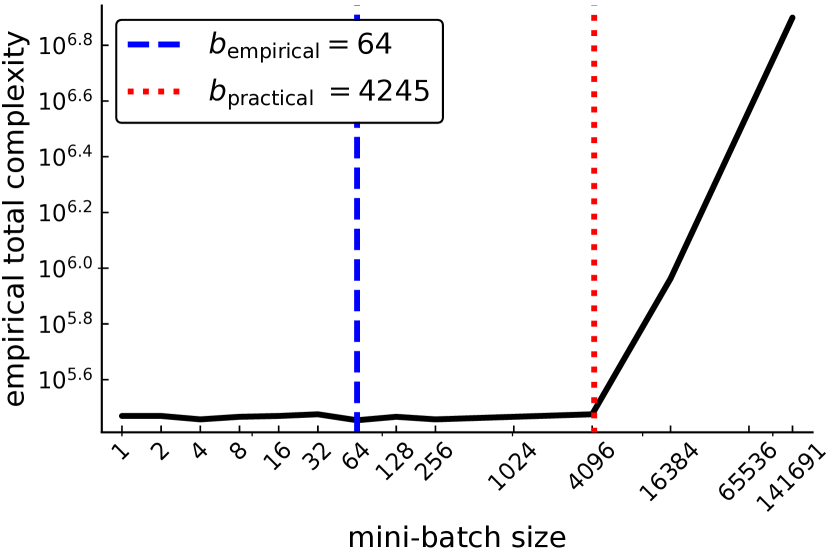

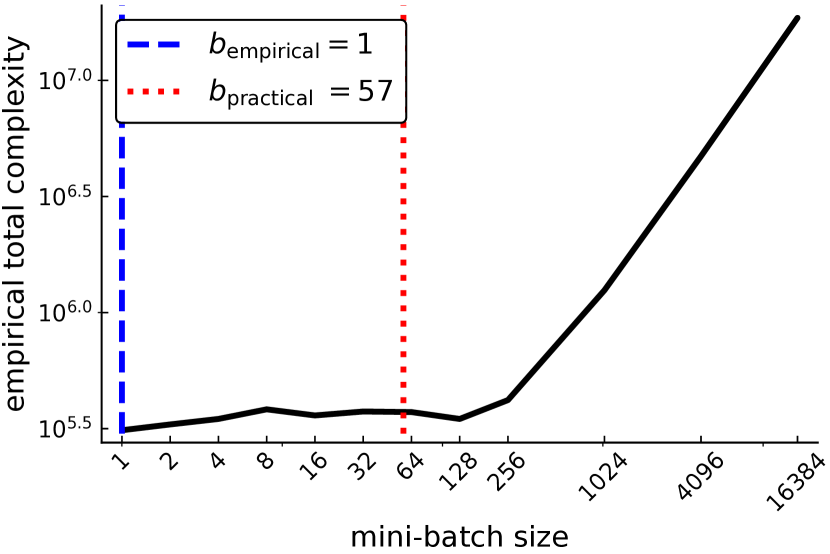

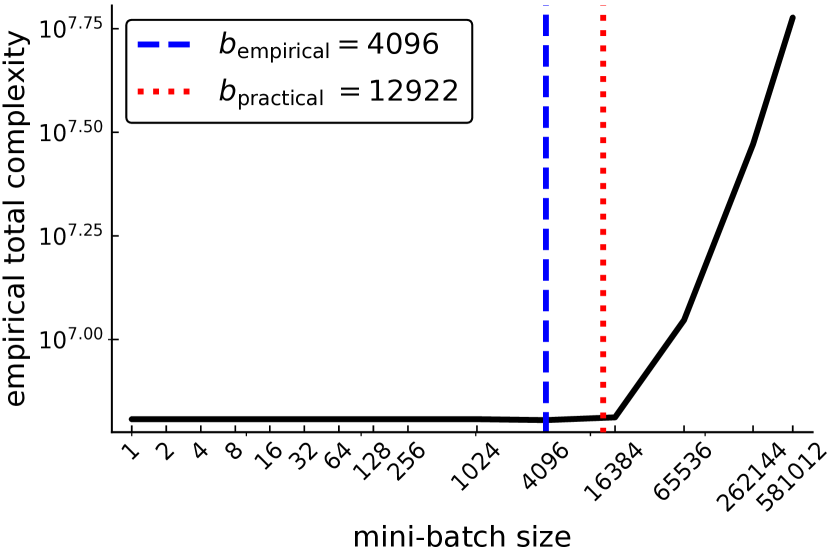

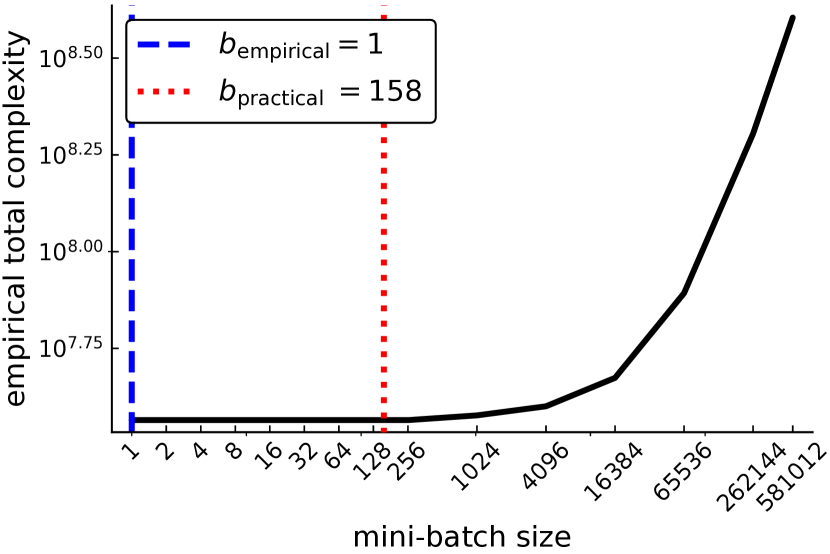

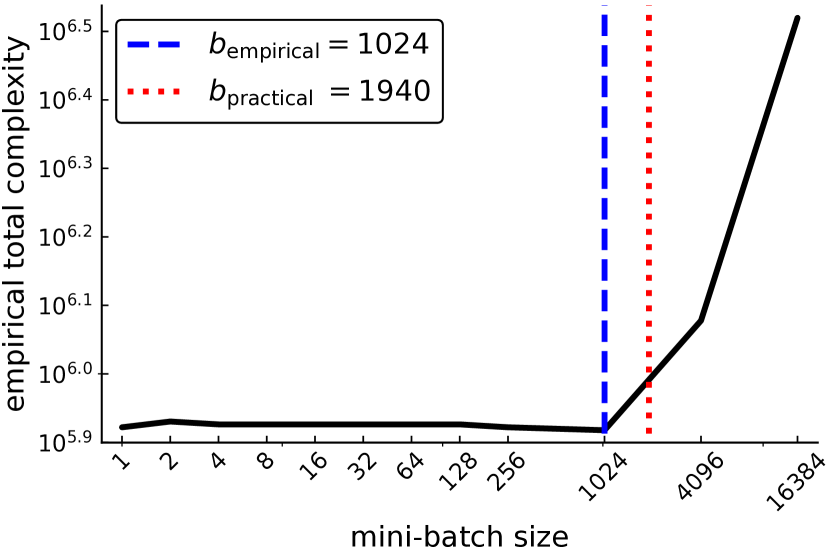

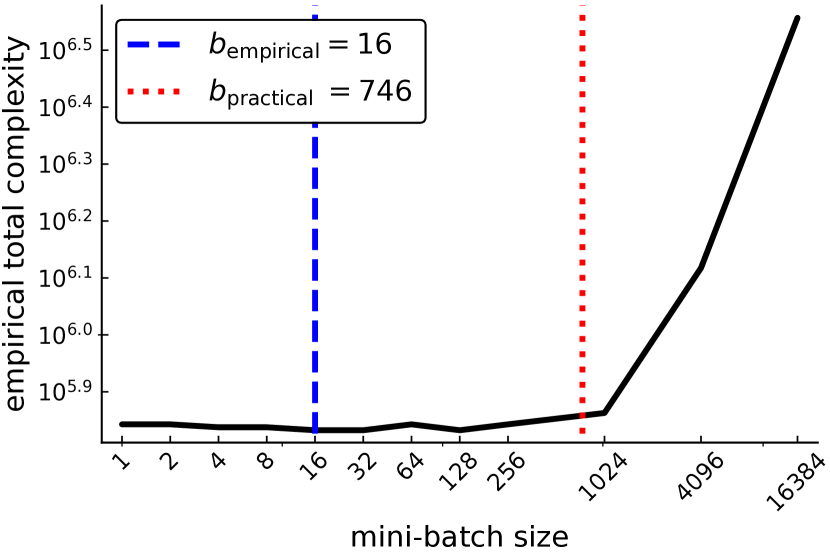

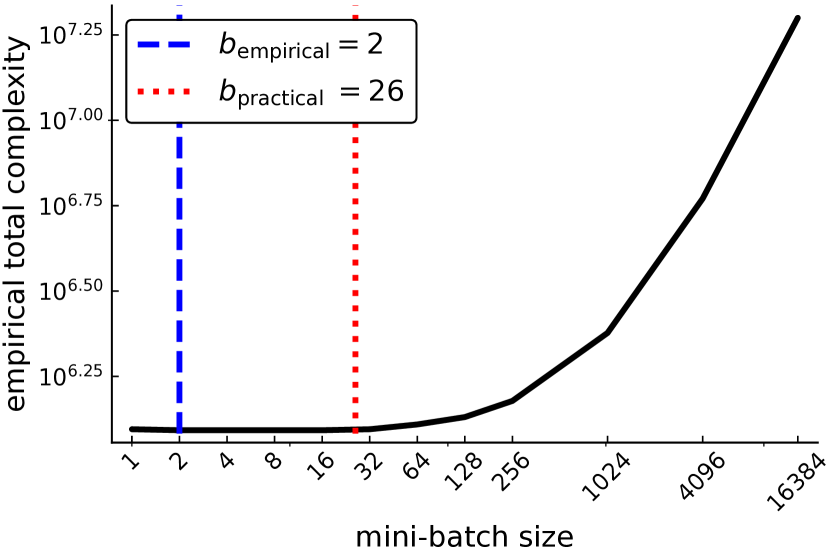

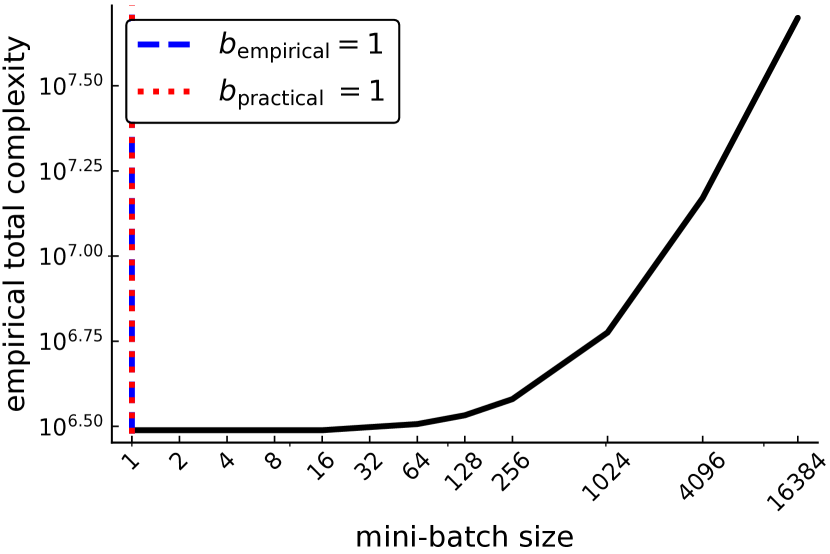

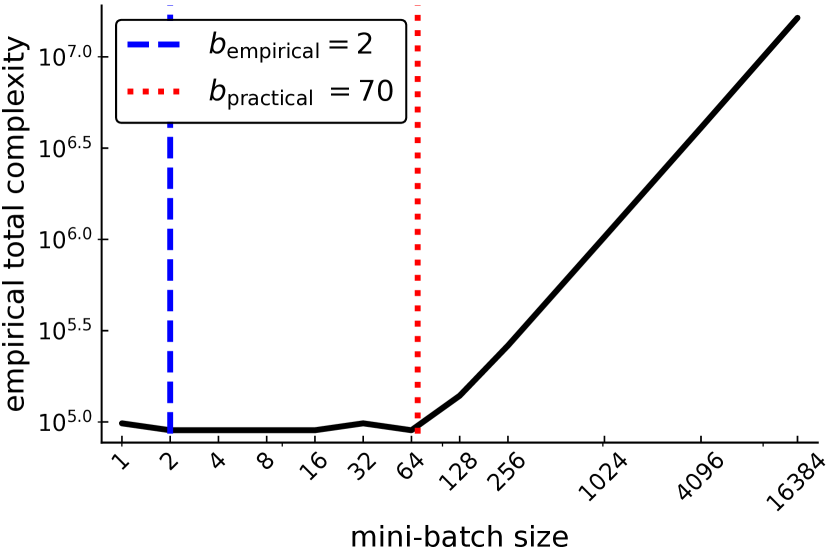

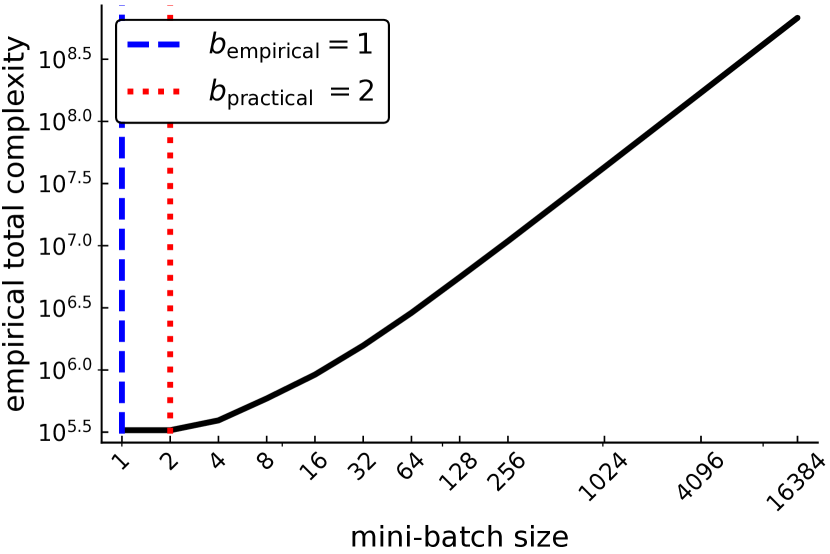

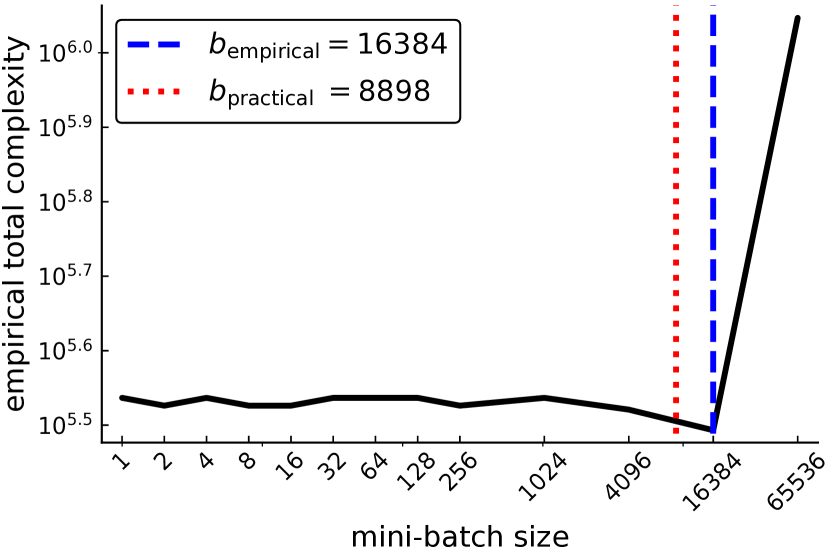

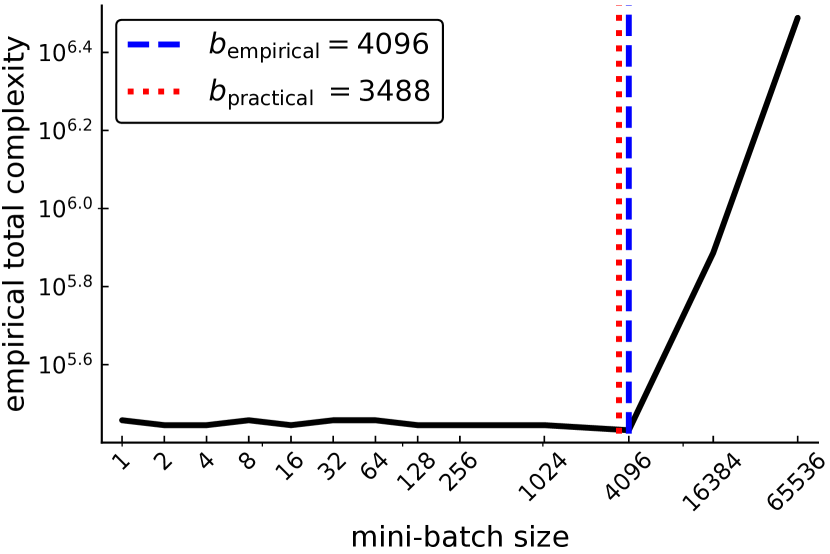

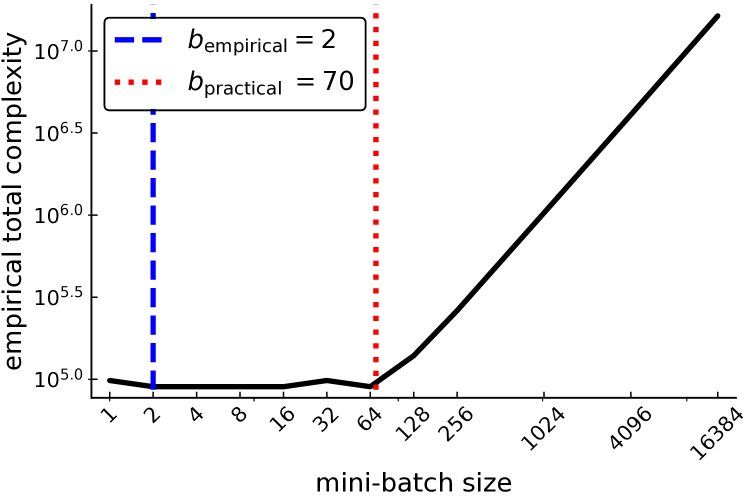

In the last experiment, detailed in Section E.6, we show that our estimation of the optimal mini-batch size leads to a faster implementation of SAGA. We build a grid of mini-batch sizes888Our grid is , with and being added when needed. and compute the empirical total complexity required to achieve a relative error of , as in Section 5.3.

In Figure 6 we can see that the empirical complexity when using is almost the same as one for the optimal mini-batch size calculated through grid search. Yet, our being always larger than the mini-batch obtained by grid search, it leads to a faster algorithm for two reasons. Firstly, the corresponding step size is larger and secondly, and secondly, computing the stochastic gradients in parallel improves the running time. What is even more interesting, is that always predicts a regime change, where using a larger mini-batch size results in a much larger empirical complexity.

6 Conclusions

We have explained the crucial role of the expected smoothness constant in the convergence of a family of stochastic variance-reduced descent algorithms. We have developed functional upper-bounds of this constant to build larger step sizes and closed-form optimal mini-batch values for the -nice SAGA algorithm. Our experiments on artificial and real datasets showed the validity of our upper-bounds and the improvement in the total complexity using our step and optimal mini-batch sizes. Our results suggest a new parameter setting for mini-batch SAGA, that significantly outperforms previous suggested ones, and is even comparable with a grid search approach, without the computational burden of the later.

Acknowledgements

This work was supported by grants from DIM Math Innov Région Ile-de-France (ED574 - FMJH) and by a public grant as part of the Investissement d’avenir project, reference ANR-11-LABX-0056-LMH, LabEx LMH, in a joint call with Gaspard Monge Program for optimization, operations research and their interactions with data sciences.

References

- Allen-Zhu (2017) Allen-Zhu, Z. Katyusha: The First Direct Acceleration of Stochastic Gradient Methods. In STOC, 2017.

- Bach (2013) Bach, F. Sharp analysis of low-rank kernel matrix approximations. In COLT 2013 - The 26th Annual Conference on Learning Theory, pp. 185–209, 2013.

- Chang & Lin (2011) Chang, C.-C. and Lin, C.-J. Libsvm: a library for support vector machines. ACM transactions on intelligent systems and technology (TIST), 2(3):27, 2011.

- Defazio et al. (2014) Defazio, A., Bach, F., and Lacoste-Julien, S. Saga: A fast incremental gradient method with support for non-strongly convex composite objectives. In Advances in Neural Information Processing Systems 27, pp. 1646–1654. 2014.

- Dheeru & Karra Taniskidou (2017) Dheeru, D. and Karra Taniskidou, E. UCI machine learning repository, 2017.

- Gower et al. (2018) Gower, R. M., Richtárik, P., and Bach, F. Stochastic quasi-gradient methods: Variance reduction via Jacobian sketching. arXiv preprint arXiv:1805.02632, 2018.

- Gross & Nesme (2010) Gross, D. and Nesme, V. Note on sampling without replacing from a finite collection of matrices. arXiv preprint arXiv:1001.2738, 2010.

- Hoeffding (1963) Hoeffding, W. Probability inequalities for sums of bounded random variables. Journal of the American statistical association, 58(301):13–30, 1963.

- Hofmann et al. (2015) Hofmann, T., Lucchi, A., Lacoste-Julien, S., and McWilliams, B. Variance reduced stochastic gradient descent with neighbors. In Advances in Neural Information Processing Systems, pp. 2305–2313, 2015.

- Johnson & Zhang (2013) Johnson, R. and Zhang, T. Accelerating stochastic gradient descent using predictive variance reduction. In Advances in Neural Information Processing Systems 26, pp. 315–323. Curran Associates, Inc., 2013.

- Konečný & Richtárik (2017) Konečný, J. and Richtárik, P. Semi-stochastic gradient descent methods. Frontiers in Applied Mathematics and Statistics, 3:9, 2017.

- Nesterov (2014) Nesterov, Y. Introductory Lectures on Convex Optimization: A Basic Course. Springer Publishing Company, Incorporated, 1 edition, 2014.

- Nguyen et al. (2017) Nguyen, L. M., Liu, J., Scheinberg, K., and Takáč, M. SARAH: A novel method for machine learning problems using stochastic recursive gradient. In Precup, D. and Teh, Y. W. (eds.), Proceedings of the 34th International Conference on Machine Learning, volume 70 of Proceedings of Machine Learning Research, pp. 2613–2621. PMLR, Aug 2017.

- Raj & Stich (2018) Raj, A. and Stich, S. U. SVRG meets SAGA: k-SVRG — a tale of limited memory. arXiv:1805.00982, 2018.

- Robbins & Monro (1951) Robbins, H. and Monro, S. A stochastic approximation method. Annals of Mathematical Statistics, 22:400–407, 1951.

- Schmidt et al. (2017) Schmidt, M., Le Roux, N., and Bach, F. Minimizing finite sums with the stochastic average gradient. Mathematical Programming, 162(1):83–112, Mar 2017.

- Shalev-Shwartz & Zhang (2013) Shalev-Shwartz, S. and Zhang, T. Stochastic dual coordinate ascent methods for regularized loss. Journal of Machine Learning Research, 14(1):567–599, February 2013.

- Tropp (2011) Tropp, J. A. Improved analysis of the subsampled randomized Hadamard transform. Advances in Adaptive Data Analysis, 3(01n02):115–126, 2011.

- Tropp (2012) Tropp, J. A. User-friendly tail bounds for sums of random matrices. Foundations of Computational Mathematics, 12(4):389–434, 2012.

- Tropp (2015) Tropp, J. A. An introduction to matrix concentration inequalities. Foundations and Trends in Machine Learning, 8(1-2):1–230, 2015.

Appendix A Proofs of the Upper Bounds of

A.1 Master lemma

Proof of Lemma 1.

Since the ’s are convex, each realization of is convex, and it follows from equation 2.1.7 in (Nesterov, 2014) that

| (24) |

Taking expectation over the sampling gives

where in the last equality the full gradient vanishes because it is computed at optimality. The result now follows by comparing the above with the definition of expected smoothness in (7). ∎

A.2 Proof of the simple bound

Proof of Theorem 2.

To derive this bound on we use that

| (25) |

which follows from repeatedly applying Lemma 8. For , it follows from Equation 17 and Equation 25 that

| (26) |

Using a double counting argument we can show that

| (27) |

Inserting this into Equation 26 gives

| (28) |

We also verify that this bound is valid for -nice sampling. Indeed, we already have that in this case . ∎

A.3 Proof of the Bernstein bound

To start the proof of Theorem 3, we re-write the expected smoothness constant as the maximum over an expectation. Let be a -nice sampling over We can write

| (29) | |||||

One can come back to the definition of the subsample smoothness constant Equation 12 and interpret previous expression as an expectation of the largest eigenvalue of a sum of matrices. This insight allows us to apply a matrix Bernstein inequality, see Theorem 7, to bound .

For the proof of Theorem 3, we first need the two following results.

Lemma 4.

Let , and let be a -nice sampling over the set . It follows that

| (30) |

Proof of Lemma 4.

This results follows using a double-counting argument at the fourth line of the computation.

∎

We then introduce another two lemmas which give a first intermediate bound.

Lemma 5.

Let for , let and let be a -nice sampling over We have

| (31) |

Proof of Lemma 5.

Expanding the expectation we have

where in the first inequality we add and remove the mean and then apply Lemma 8. In the second equality we explicit the mean with Lemma 4 and in the last inequality we use again Lemma 8 for the left-hand side term. Finally, we multiply by on both sides of the inequality. ∎

Proof of Lemma 3.

The result comes from applying re-writing as an expectation of the largest eigenvalue of a sum of matrices. Then we apply Lemma 5 and then taking the maximum over all . Thus, we have

∎

Proof of Theorem 3.

Applying the previous lemma we get

| (32) |

with .

To further our argument, we will encode different samplings using unit coordinate vectors. Let be the unit coordinate vectors. Let denote an arbitrary but fixed ordering of the elements of . With this we can encode the sampling without replacement as

| (33) |

Using this notation, the matrix which can be further decomposed as

where we have encoded the sampling using unit coordinate vectors. The matrices are sampled without replacement from the set

| (34) |

Now let be matrices sampled with replacement from (34) and let and thus the vectors are sampled with replacement from Consequently

We are now in a position to apply the Bernstein matrix inequality. To this end we have

-

•

A sum of centered random matrices: .

-

•

Let be the unique index such that We have a uniform bound of the largest eigenvalue of our

(35) where we applied the Lemma 9 in the first inequality.

- •

Considering Equations 35 and 37 and applying the matrix Bernstein concentration inequality in Theorem 7 we get

Taking the maximum over and using we have that

Combining the above result with (32) leads us to

where in the second inequality we used the inequality . ∎

Appendix B Linear Algebra Tools

This appendix is dedicated to the presentation of useful results to manipulate more easily the smoothness constants.

B.1 Spectral Lemmas

Let us recall some useful spectral results on Hermitian and positive semi-definite matrices.

Lemma 6.

(Weyl’s inequality) Let symmetric matrices. Assume that the eigenvalues of (resp. ) are sorted i.e., (resp. ). Then, we have

| (38) |

whenever and

Moreover, as a direct consequence of the variational characterization of eigenvalues, namely

| (39) |

we have an inequality between the maximum diagonal term of a positive semi-definite matrices and its maximum eigenvalue.

Lemma 7.

Let positive semi-definite matrix and the vector containing its diagonal . Then, we have

| (40) |

The following lemma is a direct consequence of Weyl’s inequality for

Lemma 8.

Let symmetric matrices. Then, we have

| (41) |

Lastly, we present a result arising from previous lemma.

Lemma 9.

Let symmetric matrices such that is positive semi-definite. Then, we have

| (42) |

Proof.

Let symmetric matrices such that is positive semi-definite. We get directly

where the first inequality stems from Lemma 8 and the second from ∎

B.2 Basic properties of the smoothness constants

The complexity results of Gower et al. (2018) depends on smoothness constants defined in Section 3.1. Here are some inequalities giving an idea of the order of those constants.

Lemma 10.

Let a batch set drawn randomly without replacement. The following inequalities hold

-

(i)

(43) -

(ii)

(44) -

(iii)

(45)

Proof.

-

(i)

One directly gets that .

-

(ii)

This inequality states that the smoothness constant of the averaged function is upper bounded by the average of the corresponding smoothness constants , over the batch . The proof consists in repetitive calls of Lemma 8.

-

(iii)

Direct implication of (ii) for .

Direct calculation

Let us first recall the matrix formulation of our smoothness constants:

and

Using the min-max theorem, we have that

Dividing the above by on both sides gives

Direct consequence of .

∎

Appendix C Matrix Bernstein Inequality: Sampling Without Replacement

In this appendix, we present the matrix Bernstein inequality for independent Hermitian matrices from Tropp (2015). We also provide another version of this theorem for matrices sampled without replacement and prove it as explicitly as possible, taking our inspiration from Tropp (2011). The proof is based the possibility of transferring the results from sampling with to without through the inequality (50) due to Gross & Nesme (2010). The exact same work can be done for the tail bound, which is for instance used in Bach (2013).

C.1 Original Bernstein inequality for independent matrices

We first present Theorem 4 which gives a Bernstein inequality for a sum of random and independent Hermitian matrices whose eigenvalues are upper bounded. If the matrices are sampled from a finite set , one can interpret this random sampling of independent matrices as a random sampling with replacement.

Theorem 4 (Tropp (2015), Theorem 6.6.1: Matrix Bernstein Inequality).

Consider a finite sequence of independent, random, Hermitian matrices with dimension . Assume that

Introduce the random matrix

Let be the matrix variance statistic of the sum:

| (46) |

Then

| (47) |

This theorem is the one we extend in Theorem 7 to the case when the random matrices are sampled without replacement from a finite set . We drew our inspiration from the proof of the matrix Chernoff inequality in Tropp (2011) and the one of the matrix Bernstein tail bound in Bach (2013), both in the case of sampling without replacement.

C.2 Technical random matrices prerequisites

Before proving Theorem 7, which extends the matrix Bernstein inequality to sampling without replacement, we need to introduce the key tools of the matrix Laplace transform technique. This technique is precious to prove tail bounds for sums of random matrices such as Chernoff, Hoeffding or Bernstein bounds, as presented in (Tropp, 2012).

Here, denotes the spectral norm, which is defined for any Hermitian matrix by

| (48) |

We also introduce the moment generating function (mgf) and the cumulant generating function (cgf) of a random matrix, which are essential in the Laplace transform method approach.

Definition 6 (Matrix Mgf and Cgf).

Let be a random Hermitian matrix. For all , the matrix generating function and the matrix cumulant generating function are given by

and

Remark 4.

These expectations may not exist for all values of .

Proposition 2 (Tropp (2015), Proposition 3.2.2: Expectation Bound of the Maximum Eigenvalue).

Let be a random Hermitian matrix. Then

| (49) |

Remark 5.

This proposition is an adaptation of the Laplace transform method to obtain a bound of the expectation of the maximum eigenvalue of a random Hermitian matrix. Contrary to the tail bounds, there is no exact analog of the expectation bounds in the scalar setting.

Proof of Proposition 2.

Fix a positive number . Because is a positive-homogeneous map, we have

where in the third line we used the Jensen’s inequality, in the fourth one the spectral mapping theorem and in the last line the domination by the trace of a positive-definite matrix. ∎

Theorem 5 (Tropp (2015), Theorem 8.1.1: Lieb).

Let be a fixed Hermitian matrix with dimension . The function

is a concave map on the the convex cone of positive-definite matrices.

Corollary 1.

Let be a fixed Hermitian matrix with dimension . Let be a random Hermitian matrix of same dimension. The following inequality holds

is a concave map on the the convex cone of positive-definite matrices.

Proof of Corollary 1.

Introducing , we have directly

where the inequality comes from the application of Theorem 5 and Jensen’s inequality. ∎

Lemma 11 (Tropp (2015), Lemma 3.5.1 or Tropp (2012), Lemma 3.4: Subadditivity of Matrix Cgfs).

Consider a finite sequence of independent, random, Hermitian matrices of the same dimension. Let , then

Proof of Lemma 11.

Let us assume, without loss of generality, that . Let a finite sequence of independent, random, Hermitian matrices of the same dimension. We write down the expectation with respect only to the -th random matrix .

where first and second inequalities result from Corollary 1, the last one comes the fact that and the final equality directly comes from an indentification of Definition 6. ∎

Lemma 12 (Tropp (2015), Lemma 6.6.2: Matrix Bernstein Mgf and Cgf Bounds).

Let a random Hermitian matrix such that

Then, for ,

and

C.3 Extended results for sampling without replacement

This section is dedicated to the main result, Lemma 13, needed for transferring results from sampling with to without replacement. This lemma is actually the matrix version of a classical result from Hoeffding (1963). We then combine it with previous results of Section C.2 to produce a new master bound in Theorem 6, which is the key inequality of the proof of Theorem 7.

Lemma 13 (Gross & Nesme (2010), Domination of the Trace of the Mgf of a Sample Without Replacement).

Consider two finite sequences, of same length , and of Hermitian random matrices sampled respectively with and without replacement from a finite set . Let , and , then

| (50) |

Proof of Lemma 13.

The left-hand side equality directly arises from Definition 6 and the fact that the trace commutes with the expectation because it is a linear operator. For the right-hand side inequality, see the proof in Gross & Nesme (2010). ∎

Theorem 6 (Master Bound for a Sum of Random Matrices Sampled Without Replacement).

Consider two finite sequences, of same length , and of Hermitian random matrices of same size sampled respectively with and without replacement from a finite set . Then

| (51) |

Remark 6.

This theorem is a modified version of Theorem 3.6.1 in Tropp (2015) for a sum of matrices sampled without replacement.

Proof of Theorem 6.

Consider two finite sequences, of same length, and of Hermitian random matrices of same size sampled respectively with and without replacement from a finite set . Let a positive number.

where we used successively Proposition 2, Lemma 13 and Lemma 11. First, we use the expectation bound for the maximum eigenvalue. We then use the main result of Gross & Nesme (2010) and invoked in Tropp (2011) to extend the matrix Chernoff bound for matrices sampled without replacement. This lemma allows us to transfer our results to sampling with replacement. And finally, we then apply the subadditivity of matrix cgfs to get the desired result. ∎

C.4 Bernstein inequality for sampling without replacement

The following theorem is almost the same than Theorem 4, but in the case of matrices sampled without replacement from a finite set. The proof stems from results established in previous Sections C.3 and C.2.

Theorem 7 (Matrix Bernstein Inequality Without Replacement).

Let be a finite set of Hermitian matrices with dimension such that

Sample two finite sequences, of same length , and uniformly at random from respectively with and without replacement such that

Introduce the random matrices

Let be the matrix variance statistic of the second sum

| (52) |

Then

| (53) |

Proof of Theorem 7.

Consider a finite set of Hermitian matrices of dimension such that

Sample two finite sequences, of same length, and uniformly at random from respectively with and without replacement such that

The matrices are thus independent. Introduce the sums and . Let us bound the expectation of the largest eigenvalue of the latter

where the inequalities sucessively derive from Theorem 6, Lemma 12 combined with the monotony of , the fact that , the spectral mapping theorem and lastly (48) with . Finally, one can complete the infimum, for instance using a computer algebra system, to finish the proof as it was stated in the original proof by Tropp (2015) 999For instance : Minimize[(log(d)/x) + ((x/2)/(1-(L/3)*x))*v, x >0, x < (3/L), x] in Wolfram Alpha.. In conclusion,

∎

Appendix D Miscellaneous

Lemma 14 (Double counting).

Let for and , where is a collection of subsets of . Then

| (54) |

Appendix E Additional Experiments

E.1 Experiment 1: estimates of the expected smoothness constant for artificial datasets

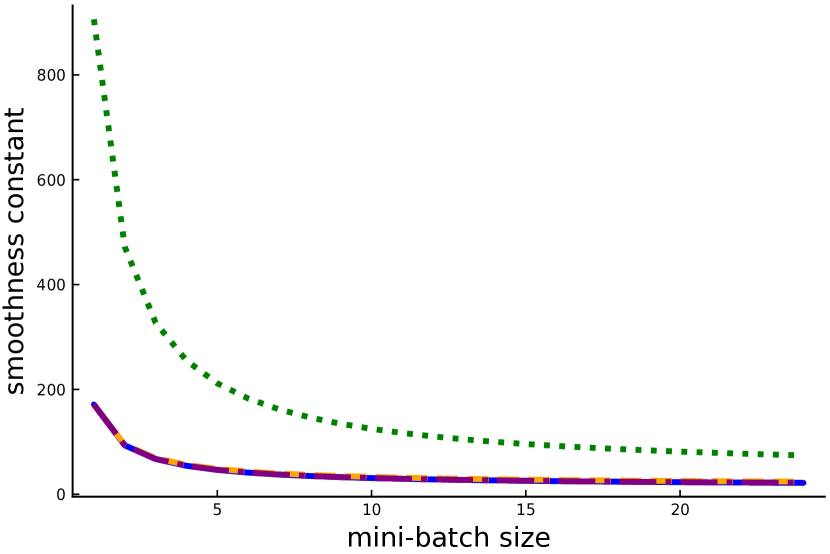

As described in Section 5, we compute our the simple and Bernstein bounds, our practical estimate and the true for ridge regression applied to small artificial datasets: uniform , staircase eigval and alone eigval . Figure 7 shows first that the practical estimate is a very close approximation of . On the one hand, we observe in Figure 7(a) that the Bernstein bound performs poorly since the feature dimension is very small . On the other hand, Figure 7(c) shows a regime change for , which highlight the usefulness of combining our bounds to approximate the expected smoothness constant. Finally, we observe that for the alone eigval dataset Figure 7(b), which has one very large eigenvalue far from the rest of the spectrum, the simple bound matches because the gap between and shrinks. Indeed, in this configuration . When the spectrum is more concentrated, like for staircase eigval, we get a significant gap between and as shown in Figure 7(c), where the simple bound is far from when .

We also report the influence of changing the value of the regularization parameter . Figure 8 shows that this parameter has little impact on the general shape of the bounds and of .

Finally, we study the impact of scaling or standardizing (i.e., removing the mean and dividing by the standard deviation for each feature) our artificial datasets. In order not to benefit from the diagonal shape of the alone eigval and staircase eigval datasets we also give examples of the bounds of after a rotation of the data. The rotation aims at preserving the spectrum while erasing the diagonal structure of the covariance matrix . This rotation procedure consists in transforming into , where is the orthogonal matrix given by the QR decomposition of a random squared matrix (with dimension the same as the one of ) with uniformly random coefficients , such that .

We observe in Figure 9 that rotations do not affect our estimates of , because they preserve the spectrum. Scaling non-diagonal datasets does not change the general shape neither. As predicted, scaling diagonal matrices leads to a particular case where the spectrum of the covariance matrix is flattened and for all , . This is why we get a flat simple bound in Figures 9(c) and 9(g). Even after those different types of preprocessing (rotation and scaling) and with different values of , we end up with the same strong observation that the practical estimate is a very sharp approximation of the expected smoothness constant.

E.2 Experiment 1: estimates of the expected smoothness constant for real datasets

In what folows, we also used publicly available datasets from LIBSVM101010https://www.csie.ntu.edu.tw/~cjlin/libsvmtools/datasets/ provided by Chang & Lin (2011) and from the UCI repository111111https://archive.ics.uci.edu/ml/datasets/ provided by Dheeru & Karra Taniskidou (2017). We applied ridge regression to the following datasets: YearPredictionMSD from LIBSVM and slice from UCI. We also applied regularized logistic regression for binary classification on ijcnn1 , covtype.binary , real-sim , rcv1.binary and news20.binary () from LIBSVM. When a test set was available, we concatenated it with the train set to have more samples.

One can observe in Figure 10, that for unscaled datasets the Bernstein bound performs better than the simple bound, except for YearPredictionMSD and covtype.binary . From Figure 11, we observe that after feature-scaling, the Bernstein bound is always a tighter upper bound of than the simple bound.

E.3 Experiment 2: step size estimates for artificial datasets

In this section we give the step sizes estimate corresponding to the expected smoothness constant, the simple and Bernstein upper-bounds and the practical estimate for our small artificial datasets. In Figure 12, we show that the practical step size estimate is larger than all others. Moreover, for except for small value sof , our or estimates are in most cases larger than the one proposed in (Hofmann et al., 2015).

E.4 Experiment 2: step size estimates for real datasets

Here we show the step sizes estimate corresponding to the simple and Bernstein upper-bounds and the practical estimate for real datasets detailed in Section E.2. On these real data, unscaled in Figure 13 and scaled in Figure 14, we see that the gap between our step size estimates and is even larger. We observe in Figure 13, accordlingly to previous remarks in Section E.2, that Bernstein bound leads to larger step sizes than the simple one, except for the unscaled YearPredictionMSD and covtype.binary datasets. Yet, as noticed before, Figure 14 seems to show that scaling the data leads to larger than .

E.5 Experiment 3: comparison with previous SAGA settings

In this section we provide more example of the performance of our practical settings compared to previously known SAGA settings. In Figures 16, 17, 18, 19, 20 and 21 we run our experiments on real datasets introduced in detail in Section E.1. SAGA implementations are run until the suboptimality reaches a relative error of , except in some cases where the Hofmann’s runs exceeded our maximal number of epochs like in Figure 17. In Figure 19, the curves corresponding to Hofmann’s settings are not displayed because they achieve a total complexity which is too large. Figure 15 shows an example of such a configuration.

These experiments show that our settings () most of the time outperforms whether the classical () or the () settings both in terms of epochs and running time.

E.6 Experiment 4: optimality of the mini-batch size

This experiment aims to estimate how close is our practical estimate to the empirical best mini-batch size one could get running a grid search. We recall that we use the following grid for the mini-batch sizes: , with and added in some cases. We show in the log-scaled Figures 22, 23, 24, 25, 26 and 27 the empirical total complexity , e.g., the number of computed stochastic gradients to reach a relative error of , as a function of the mini-batch . For each mini-batch of the grid , the step size used is the one corresponding to the practical estimate, i.e., when replacing by in Equation 14.

We always observe a change of regime in the empirical complexity. For small values of , the complexity is of the same order of magnitude, then, for values greater than the empirical optimal mini-batch size, the complexity explodes. This experiment shows that our optimal mini-batch size correctly designates the largest mini-batch achieving the best complexity as large as possible, without reaching the regime where the total complexity explodes.