Penalized Interaction Estimation for Ultrahigh Dimensional Quadratic Regression

Abstract

Quadratic regression goes beyond the linear model by simultaneously including main effects and interactions between the covariates. The problem of interaction estimation in high dimensional quadratic regression has received extensive attention in the past decade. In this article we introduce a novel method which allows us to estimate the main effects and interactions separately. Unlike existing methods for ultrahigh dimensional quadratic regressions, our proposal does not require the widely used heredity assumption. In addition, our proposed estimates have explicit formulas and obey the invariance principle at the population level. We estimate the interactions of matrix form under penalized convex loss function. The resulting estimates are shown to be consistent even when the covariate dimension is an exponential order of the sample size. We develop an efficient ADMM algorithm to implement the penalized estimation. This ADMM algorithm fully explores the cheap computational cost of matrix multiplication and is much more efficient than existing penalized methods such as all pairs LASSO. We demonstrate the promising performance of our proposal through extensive numerical studies.

keywords:

[class=AMS] 62H20, 62H99, 62G99.keywords:

, and

1 INTRODUCTION

In many scientific discoveries, a fundamental problem is to understand how the features under investigation interact with each other. Interaction estimation has been shown to be very attractive in both parameter estimation and model prediction (Bien, Taylor and Tibshirani, 2013; Hao, Feng and Zhang, 2017), especially for data sets with complicated structures. Efron et al. (2004) pointed out that for Boston housing data, prediction accuracy can be significantly improved if interactions are included in addition to all main effects. In general, ignoring interactions by considering main effects alone may lead to an inaccurate or even a biased estimation, resulting in poor prediction of an outcome of interest, whereas considering interactions as well as main effects can improve model interpretability and prediction substantially, thus achieve a better understanding of how the outcome depends on the predictive features (Fan et al., 2015). While it is important to identify interactions which may reveal real relationship between the outcome and the predictive features, the number of parameters scales squarely with that of the predictive features, making parameter estimation and model prediction very challenging for problems with large or even moderate dimensionality.

1.1 Interaction Estimation, Feature Selection and Screening

Estimating interactions is a challenging problem because the number of pairwise interactions increases quadratically with the number of the covariates. In the past decade, there has been a surge of interest in interaction estimation in quadratic regression. Roughly speaking, existing procedures for interaction estimation can be classified into three categories. In the first category of low or moderate dimensional setting, standard techniques such as ordinary least squares can be readily used to estimate all the pairwise interactions as well as the main effects. This simple one-stage strategy, however, becomes impractical or even infeasible for moderate or high dimensional problems, owing to rapid increase in dimensionality incurred by interactions. In the second category of moderate or high dimensional setting where feature selection becomes imperative, several one-stage regularization methods are proposed and some require either the strong or the weak heredity assumption. See, for example, Yuan, Joseph and Zou (2009), Choi, Li and Zhu (2010), Bien, Taylor and Tibshirani (2013), Lim and Hastie (2015), and Haris, Witten and Simon (2016). These regularization methods are computationally feasible and the theoretical properties of the resulting estimates are well understood for moderate or high dimensional problems. However, in the third category of ultrahigh dimension problems, these regularization methods are no longer feasible because their implementation requires storing and manipulating large scale design matrix and solving complex constrained optimization problems. The memory and computational cost is usually extremely expensive and prohibitive. Very recently, several two-stage approaches are proposed for both ultrahigh dimensional regression and classification problems, including Hao and Zhang (2014), Fan et al. (2015), Hao, Feng and Zhang (2017) and Kong et al. (2017). Two-stage approaches estimate main effects and interactions at two separate stages, so their computational complexity is dramatically reduced. However, these two-stage approaches hinge heavily on either the strong or weak heredity assumption. These methods are computationally scalable but may completely break down when the heredity assumption is violated.

1.2 Heredity Assumption and Invariance Principle in Quadratic Regression

As an extra layer of flexibility to linear models, quadratic regressions include both main effects and pairwise interactions between the covariates. Denote the outcome variable and the covariate vector. For notational clarity, we define . In general, quadratic regression has the form of

| (1.1) |

where , and are all unknown parameters. To ensure model identifiability, we further assume that is symmetric, that is, , or equivalently, , . Our goal is to estimate and which characterize respectively main effects and interactions. We remark here that the intercept is also useful for prediction.

In the literature, heredity structures (Nelder, 1977; Hamada and Wu, 1992) have been widely imposed to avoid quadratic computational cost of searching over all pairs of interactions. The heredity structures assume that the support of could be inferred from the support of . The strong heredity assumption requires that an interaction between two covariates be included in the model only if both main effects are important, while the weak one relaxes such a constraint to the presence of at least one main effect being important. In symbols, the strong and weak heredity structures are defined, respectively, as follows:

| strong heredity: | ||||

| weak heredity: |

With the heredity assumptions, one can first seek a small number of important main effects and then only consider interactions involving these discovered main effects. It is however quite possible that main effects corresponding to important interactions are hard to detect. An example is , where and are drawn independently from and is standard normal. In this example, . The main effects and are thus unlikely detectable through a working linear model , indicating that the heredity assumptions do not facilitate to find interactions by searching for main effects first. From a practical perspective, Ritchie et al. (2001) provided a real data example to demonstrate the existence of pure interaction models in practice. Cordell (2009) also raised serious concerns that many existing methods that depend on the heredity assumption may miss pure interactions in the absence of main effects.

An ideal quantification of importance of the main effects and interactions should satisfy the invariance principle with respect to location-scale transformation of the covariates. It is natural and a common strategy to quantify the importance of main effects and interactions through the supports of and in model (1.1). In conventional linear model where only main effects are present and interactions are absent (i.e., in model (1.1)), the invariance principle is satisfied. In contrast, in quadratic regression (1.1) with a general the invariance principle is very likely violated. To demonstrate this issue, we can recast model (1.1) as

| (1.2) |

In this model, the importance of main effects and interactions is naturally characterized through the support of and , respectively, indicating that the interactions are invariant whereas the main effects are sensitive to location transformation. In ultrahigh dimensional quadratic regression, using one-stage approaches which simultaneously estimate main effects and interactions under the heredity assumption or using two-stage approaches which search for main effects prior to searching for interactions in model (1.1) and model (1.2) may lead to quite different conclusions. It is thus desirable to estimate interactions directly without knowing the main effects in advance. Direct interaction estimation without heredity constraints is, however, to the best of our knowledge, much more challenging and still unsolved in the literature.

1.3 Our Contributions

In this article we consider interaction estimation in ultrahigh dimensional quadratic regressions without heredity assumption. We make at least the following two important contributions to the literature.

-

1.

We motivate our proposal with the goal of obtaining a general and explicit expression for quadratic regression with as minimal assumptions as possible. Surprisingly, it turns out that such an explicit solution only relies on certain moment conditions on the ultrahigh dimensional covariates, which will be automatically satisfied by the widely used normality assumption. Explicit forms can be derived for both the main effects and the interactions, from which it can be seen that the quadratic regression could be implemented as two independent tasks relating to the main effects and interactions separately. Under weaker moment assumptions, our approach is still valid in detecting the direction of the true interactions. Our proposal is different from existing one-step or two-step procedures in that we do not require the heredity assumption and our proposal give explicit forms for both the main effects and the interactions. Estimating the main effects through a separate working linear model ensures that the resulting estimate satisfies the desirable invariance principle. What is more, we show that our approach for interaction detection is robust to the estimation of main effects in that even when the linear effect can not be well estimated, we can still successfully detect the interactions.

-

2.

We show that the interaction inference is equivalent to a particular matrix estimation at the population level. We estimate the interactions of matrix form under penalized convex loss function, which yields a sparse solution. We derive the theoretical consistence of our proposed estimation when the covariate dimension is an exponential order of the sample size. Compared with the conventional penalized least squares approach, the penalization of matrix form is appealing in both memory storage and computation cost. An efficient ADMM algorithm is developed to implement our procedure. This algorithm fully explores the cheap computational cost for matrix multiplication and is even much more efficient than existing penalized methods. We have also developed an R package “PIE” to implement our proposal.

The remainder of this paper is organized as follows. We begin in Section 2 with the quadratic regression model and derive closed forms for both the main effects and the interactions. We propose a direct penalized estimation for high dimensional sparse quadratic model. To implement our proposal an efficient ADMM algorithm is provided. We also study the theoretical properties of our proposed estimates. We illustrate the performance of our proposal through simulations in Section 3 and an application to a real world problem in Section 4. We give some brief comments in Section 5. All technical details are relegated to Appendix.

2 THE ESTIMATION PROCEDURE

2.1 The Rationale

In this section we discuss how to estimate and , which characterize the main effects and interactions in model (1.1), respectively. Note that and Therefore, estimating and amounts to estimating and , respectively, which is however not straightforward, especially when is ultrahigh dimensional. To illustrate the rationale of our proposal, we assume for now that follows . It follows immediately from Stein’s Lemma (Stein, 1981; Li, 1992) that

where . Define , which is the residual obtained by regressing on linearly. The Hessians of and are equal. Accordingly, we have

By Stein’s Lemma, we can obtain that

where . This indicates that, if is normal, we have explicit forms for and . Specifically,

We remark here that the normality assumption is widely used in the literature of interaction estimation. See, for example, Hao and Zhang (2014), Simon and Tibshirani (2015), Bien, Simon and Tibshirani (2015) and Hao, Feng and Zhang (2017). In the present context we show that the normality assumption can be relaxed. Let be the trace operator of matrix . In particular, .

Proposition 1.

Suppose that is drawn from the factor model , where satisfies and where are independent and identically distributed (i.i.d.) with , , , . We further assume either (C1): or (C2): . Then the parameters , and in model (1.1) have the following explicit forms:

| (2.1) | |||

The factor model was widely assumed in random matrix theory (Bai and Saranadasa, 1996) and high dimensional inference (Chen, Zhang and Zhong, 2010) where higher order moment assumptions of are quite often required. The moment conditions on play an important role to derive an explicit form for . Condition (C1) is satisfied if is normal. When , condition (C2) implicitly requires the absence of quadratic terms of the form in model (1.1), i.e.,

where are i.i.d covariates.

We provide two explicit forms for estimating , one is based on the response and the other is based on the residual . The difference between and is that we remove the main effects in , or equivalently, the linear trend in model (1.1), before we estimate the interactions . It is thus natural to expect that the residual-based is superior to the response-based in that the sample estimate of has smaller variabilities than that of (Cheng and Zhu, 2017). In effect, we can replace with an arbitrary , which yields that . Similarly, we can define . Under the normality assumption, is symmetric about and hence . This ensures that, to estimate accurately, our proposal does not hinge on the sparsity of main effects because we do not require to be estimated consistently. Even if the main effects are not sufficiently sparse or are not estimated very accurately, we can either directly use the response-based method , or the lousy residual-based method which utilizes a lousy residual and can be a lousy estimate of . In effect equals by setting in . This makes our proposal quite different from existing procedures which assume the heredity conditions and hence require to estimate the main effects accurately in order to recover the interactions. By contrast, our proposal does not require to estimate the main effects precisely. We will illustrate this phenomenon through simulation studies in Section 3.

2.2 Interaction Estimation

We show that both and have explicit forms under moment conditions in Section 2.1. In particular, and for being or . In this subsection, we discuss how to estimate and at the sample level. Estimating is indeed straightforward by noting that it is a solution to the minimization problem

Therefore, we can simply estimate with the penalized least squares by regressing on the ultrahigh dimensional covariates linearly. We do not give many details about how to estimate because the penalized least squares estimation has already been well documented (Tibshirani, 1996; Fan and Li, 2001). Throughout our numerical studies we use the LASSO (Tibshirani, 1996) to estimate . The resulting solution is denoted by .

In what follows we concentrate on how to estimate , where can be or . For an arbitrary matrix , we have

and

Ignoring the constant, the term quantifies the distance between and . Therefore, to seek a matrix which can approximate very well, it suffices to consider the following minimization problem

as long as we have faithful estimates of and . The above loss function of matrix form is convex which guarantees that local minimum must be a global minimum.

To construct faithful estimates for and , suppose is a random sample of . Denote

where . We propose the following penalized interaction estimation (PIE) to estimate , for being or :

| (2.2) |

where is a tuning parameter and . To ease subsequent illustration, we further define the following two notations:

| (2.3) | |||||

| (2.4) |

2.3 Implementation

In this section we discuss how to solve (2.2) which includes (2.3) and (2.4) as special cases. Making use of the matrix structure of (2.2), we next develop an efficient algorithm using the Alternating Direction Method of Multipliers (Boyd et al., 2011, ADMM). We rewrite the optimization problem in (2.2) as

| (2.5) |

which motivates us to form the augmented Lagrangian as

where is a step size parameter in the ADMM algorithm, and stands for the Frobenius norm of . Given the current estimate , the augmented Lagrangian (2.3) can be solved by successively updating by:

| (2.7) | |||||

| (2.8) | |||||

| (2.9) |

Define the elementwise soft thresholding operator . For the step, given , , and , the solution is then given by

The step amounts to solving the equation

| (2.10) |

where . We make the singular value decomposition to obtain , where , and is a diagonal matrix. Define , where . Given , and , the solution to (2.10) is given by

where denotes the Hadamard product.

Details of the algorithm is summarized in Algorithm 1. This algorithm yields a symmetric estimate of , which is denoted by . The computational complexity of each iteration is no more than O and the memory requirement is no more than O since we only need to store a few or matrices in computer memory. The algorithm explores the advantages of matrix multiplications and is efficient in memory storage and computation cost and hence is appealing for high dimensional quadratic regression.

Furthermore, as a first-order method for convex problems, convergence analysis of the ADMM algorithm under various conditions has been well documented in the recent optimization literature. See, for example, Nishihara et al. (2015), Hong and Luo (2017) and Chen, Sun and Toh (2017). The following lemma states that our proposed ADMM algorithm converges linearly to zero.

Lemma 1.

It remains to choose an appropriate tuning parameter for PIEy or PIEr. Motivated by LARS–OLS hybrid (Efron et al., 2004), we use PIE to find the model but not to estimate the coefficients. For a given , we fit a least squares model on the support of estimated by PIEy or PIEr and get the residual sum of squares. We then choose by the Bayesian information criterion (BIC). Our limited experience indicates that this procedure is very fast and effective.

2.4 Asymptotic Properties

Suppose is a sparse matrix. For notational clarity, we denote the support of by , the complement of by , and the cardinality of by . Similarly, we denote by and the respective support of and , and and the respective complement of and . We define , , and , for . We further define , and . Denote a sequence of generic constants which may take different values at various places. We assume the following regularity conditions to study the asymptotic properties of and .

-

(A1):

Assume , where and are the respective smallest and largest eigenvalues of .

-

(A2):

Assume s are sub-Gaussian, i.e., for any unit-length vector .

-

(A3)

Assume for some .

-

(A4)

Assume the irrepresentability condition holds, i.e., .

-

(A5)

Assume is symmetric about .

Conditions (A1) and (A2) are widely assumed in high dimensional data analysis. Condition (A3) is assumed to control the tail behavior of through concentration inequalities. The irrepresentability condition (A4) is nearly necessary for the consistence of -penalization (Zhao and Yu, 2006; Zou, 2006). This condition was first used by Ravikumar et al. (2011). See also Zhang and Zou (2014) and Liu and Luo (2015). We assume condition (A5) to ensure the consistency of residual-based approaches.

Theorem 1.

Let for sufficiently large and assume that . Under the conditions (A1)-(A4), we have

-

(i)

.

-

(ii)

If we further assume for sufficiently large , then .

-

(iii)

, for sufficiently large .

-

(iv)

, for sufficiently large .

Theorem 1 shows that, as long as the signal strength of the interactions is not too small, our proposal can identify the support correctly with a very high probability. In other words, is asymptotically selection consistent. Theorem 1 also shows that is a consistent estimate of under both the infinity norm and the Frobenius norm.

Theorem 2.

Let for sufficiently large and assume that . Under the conditions (A1)-(A5), we have

-

(i)

.

-

(ii)

If we further assume for sufficiently large , then .

-

(iii)

, for sufficiently large .

-

(iv)

, for sufficiently large .

Theorem 2 shows that , as well as , possesses both the selection and estimation consistency asymptotically. Moreover, the convergence rate of depends on . If , the convergence rate term involving will be absorbed in the first term of Theorem 2. In other words, unless the estimation error of diverges faster than , and would share the same convergence rate.

2.5 Connections to All-Pairs-LASSO

For quadratic regression, a nature way is to fit LASSO model on all pairs of interactions,

Following Bien, Taylor and Tibshirani (2013), we refer to this approach as the all-pairs-LASSO. For brevity, we assume and ignore the main effects. Write and . The all-pairs-LASSO is equivalent to

| (2.11) | |||||

where denotes the Kronecker product and stands for the vectorization of a matrix. Recall that our proposed method can be re-expressed as

It is straightforward to show that . Plug this into (2.11) and compare with (2.5). We can see that the only difference between all-pairs-LASSO and our proposed PIEy is the first term. The all-pairs-LASSO directly uses the sample version to mimic the covariance structure while our method propose to use since we have under the moment condition of Proposition 1.

Using gives at least two advantages. The first is the computational efficiency. The complexity of our proposed method is . When is larger than , the computation complexity is linear in both and the number of parameters which is of order . Comparing with all-pairs-LASSO, the memory our proposed method required is much less. In all-pairs-LASSO, we need to store design matrix where our methods only depends on several matrices. The second advantage is on the theoretical properties. Under mild conditions, we can show that

By Lemma 2 in Appendix,

It can be seen that using gives a better convergence rate. We will demonstrate these issues through simulations in the next section.

3 SIMULATIONS

In this section we conduct simulations to evaluate the performance of our proposal and to compare it with the RAMP method (Hao, Feng and Zhang, 2017) and the all-pairs-LASSO which fits a LASSO model on all main effects and interactions. By Hao, Feng and Zhang (2017), RAMP will outperforms other methods such as iFOR(Hao and Zhang, 2014) and hierNet (Bien, Taylor and Tibshirani, 2013) under heredity assumptions and hence in our simulations we only include RAMP as a representative. In what follows, we refer to the RAMP method under the strong heredity condition as “RAMPs” and the RAMP method under the weak heredity condition as “RAMPw”. We also include the oracle estimate as a benchmark which assumes the main effects and the support of interactions are known in advance. The oracle estimate simply fits the least squares estimation on the support of interactions using the truly important main effects and we denote it as “Oracle”. The RAMP method and all-pairs-LASSO are implemented by the R packages “RAMP” and “glmnet” (Friedman, Hastie and Tibshirani, 2010). The developed R package “PIE” which implements our proposal is available online.

To ease illustration, we denote the estimate of by obtained with different approaches. We evaluate the accuracy of the estimation through three criteria: the support recovery rate, denoted by “rate”, the Frobenius loss, denoted by “loss” and the number of interactions that are estimated as nonzero, denoted by “size”. To be specific, the criteria are defined as follows,

| rate | ||||

| loss |

Here is an indicator function which equals 1 if the random event is true and 0 otherwise. The closer the “rate” is to one, the “loss” is to zero and the “size” is to the number of truly important interactions, the better performance a proposal has.

We consider the following four models.

| (3.1) | |||||

| (3.2) | |||||

| (3.3) | |||||

| (3.4) |

The strong heredity condition holds in model (3.1) and the weak heredity condition holds in model (3.2), respectively. Neither the strong nor the weak heredity condition holds in model (3.3) or (3.4). In particular, model (3.4) is a pure interaction model. We replicate each scenario 100 times to evaluate the performance of different proposals.

3.1 Estimation Accuracy

We draw independently from where is the power decay covariance matrix and generate an independent error from . We set the sample size and the dimension or .

The simulation results are charted in Tables 1. We can observe that our proposal has a stable performance across almost all scenarios. It is not very surprising to see that, the RAMP method with strong heredity condition, denoted RAMPs, completely fails in models (3.2)-(3.4) where the strong heredity condition is violated; in addition, the RAMP method with weak heredity condition, denoted RAMPw, fails in models (3.3)-(3.4) where the weak heredity condition is also violated. The RAMP method has a satisfactory performance when the required heredity condition is satisfied. In particular, the RAMPs performs quite well in model (3.1). For models (3.2)-(3.4), the oracle estimate has the smallest Frobenius loss, followed by our proposals. Comparing with the all-pairs-LASSO, under all the settings, our proposal has a better performance in terms of Frobenious loss and model size. For the pure interaction model (3.4) where no main effects are present, fitting linear regression to obtain residuals very likely introduces some redundant bias. It is thus not surprising to see that our proposed response-based procedure (PIEy) slightly outperforms our residual-based procedure (PIEr).

| PIEy | PIEr | RAMPs | RAMPw | all-pairs-LASSO | Oracle | ||

| model (3.1) where the strong heredity condition is satisfied | |||||||

| 100 | rate | 99.33(4.69) | 99.67(3.33) | 85.00(35.89) | 97.33(12.25) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.33(0.21) | 0.22(0.14) | 0.42(0.81) | 0.17(0.34) | 0.37(0.08) | 0.09(0.04) | |

| size | 4.31(2.21) | 3.55(0.87) | 3.03(1.67) | 3.38(1.56) | 9.36(5.50) | 3.00(0.00) | |

| 200 | rate | 98.33(7.30) | 99.33(4.69) | 88.00(31.61) | 99.00(7.42) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.43(0.30) | 0.29(0.22) | 0.37(0.72) | 0.13(0.24) | 0.43(0.10) | 0.09(0.04) | |

| size | 5.57(3.66) | 4.79(4.34) | 2.83(1.15) | 3.62(2.70) | 10.21(7.72) | 3.00(0.00) | |

| model (3.2) where the weak heredity condition is satisfied | |||||||

| 100 | rate | 100.00(0.00) | 100.00(0.00) | 35.33(24.07) | 86.33(34.20) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.18(0.08) | 0.17(0.09) | 1.93(0.43) | 0.41(0.81) | 0.40(0.10) | 0.08(0.04) | |

| size | 3.64(1.37) | 3.54(1.27) | 1.85(2.43) | 3.91(3.96) | 5.31(2.55) | 3.00(0.00) | |

| 200 | rate | 98.33(7.30) | 99.00(5.71) | 35.00(20.85) | 86.00(34.87) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.24(0.24) | 0.22(0.19) | 1.95(0.41) | 0.42(0.82) | 0.43(0.11) | 0.09(0.04) | |

| size | 4.17(3.18) | 4.45(4.44) | 1.48(1.49) | 3.68(3.05) | 5.93(2.98) | 3.00(0.00) | |

| model (3.3) where the heredity conditions is violated | |||||||

| 100 | rate | 99.00(5.71) | 100.00(0.00) | 21.33(34.98) | 46.00(26.29) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.30(0.23) | 0.17(0.10) | 1.93(0.62) | 1.51(0.69) | 0.39(0.10) | 0.09(0.04) | |

| size | 4.65(3.31) | 3.64(1.55) | 1.12(1.85) | 3.83(4.48) | 7.17(5.40) | 3.00(0.00) | |

| 200 | rate | 98.67(6.56) | 99.33(4.69) | 16.00(29.01) | 41.33(23.27) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.36(0.24) | 0.21(0.17) | 2.06(0.39) | 1.60(0.58) | 0.42(0.09) | 0.09(0.04) | |

| size | 4.97(2.63) | 3.88(2.05) | 0.88(1.47) | 2.84(3.68) | 7.62(5.68) | 3.00(0.00) | |

| model (3.4) is a pure interaction model where the heredity conditions are violated | |||||||

| 100 | rate | 100.00(0.00) | 100.00(0.00) | 13.33(24.16) | 28.00(42.30) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.11(0.05) | 0.14(0.08) | 2.13(0.36) | 1.73(0.94) | 0.41(0.10) | 0.10(0.04) | |

| size | 3.48(1.03) | 3.54(1.10) | 1.06(2.06) | 3.49(5.27) | 5.05(3.85) | 3.00(0.00) | |

| 200 | rate | 99.33(4.69) | 99.33(4.69) | 6.67(18.35) | 15.67(34.96) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.12(0.14) | 0.14(0.15) | 2.17(0.27) | 1.97(0.78) | 0.45(0.09) | 0.09(0.04) | |

| size | 3.68(2.97) | 3.68(2.88) | 0.29(0.81) | 2.72(5.14) | 4.61(2.55) | 3.00(0.00) | |

3.2 Ultrahigh Dimensional Covariates

Our algorithm is very efficient with cheap computation complexity and computer memory. In this part, we demonstrate the performance of our proposal under ultrahigh dimension settings. Apart from the three criteria considered in the previous subsection, we also compare the computation time among all the methods to illustrate the computation efficiency of our method. The parameter settings are the same as those in Subsection 3.1 except that the data dimension is now set to be 500, 1000 or 2000, and the sample size is set to be 400 or 800. To save space, we only report the results for model (3.2) where the weak heredity condition holds.

Table 2 summaries the simulations results including the “rate”, “loss”, “size” and the computation time in seconds (denoted as “time”). All methods are implemented with a PC with a 3.3 GHz Intel Core i7 CPU and 16GB memory. Overall, the patterns of the estimation accuracy are similar to those in Table 1. For the computation time, it can be seen that our methods are very effective comparing with other methods. In addition, we can observed that the computation time of our methods increase linearly in and , which is consistent with the computation complexity we claimed in the last section. The computation time of RAMP is not so sensitive to the sample size or data dimension since it used the structure information of heredity conditions. For the all-pairs-LASSO, we test the computation time using LARS (Efron et al., 2004) and it turns out to be very slow. We instead implemented the all-pairs-LASSO using “glmnet” (Friedman, Hastie and Tibshirani, 2010). We remark that “glmnet” (Friedman, Hastie and Tibshirani, 2010) is the state of art algorithm for LASSO problems and the package was further accelerated by strong rules (Tibshirani et al., 2012). From Table 2 we can see that the computation time also seems to be increasing linearly in and quadratically in . However, the all-pairs-LASSO uses more computer memory since the number of covariates is of order and will break down when due to out of memory in R. In summary, our proposal are more efficient than the all-pairs-LASSO in both computation complexity and computation memory.

| PIEy | PIEr | RAMPs | RAMPw | all-pairs-LASSO | Oracle | ||

| 500 | rate | 100.00(0.00) | 100.00(0.00) | 38.00(13.42) | 99.00(10.00) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.14(0.08) | 0.11(0.07) | 1.94(0.27) | 0.09(0.24) | 0.31(0.06) | 0.06(0.02) | |

| size | 3.56(1.29) | 3.15(0.58) | 1.27(0.74) | 3.24(1.91) | 5.11(4.17) | 3.00(0.00) | |

| time | 3.90(0.41) | 3.75(0.33) | 28.71(8.54) | 26.37(5.39) | 32.90(3.43) | 0.02(0.00) | |

| 1000 | rate | 100.00(0.00) | 100.00(0.00) | 37.00(15.64) | 95.33(20.66) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.13(0.08) | 0.09(0.05) | 1.93(0.33) | 0.17(0.52) | 0.34(0.06) | 0.06(0.03) | |

| size | 3.60(1.62) | 3.20(0.95) | 1.38(1.20) | 3.76(3.85) | 4.02(2.09) | 3.00(0.00) | |

| time | 12.70(0.49) | 12.56(0.55) | 48.26(8.88) | 50.84(10.54) | 126.66(0.55) | 0.04(0.01) | |

| 2000 | rate | 100.00(0.00) | 100.00(0.00) | 31.67(11.96) | 88.00(32.66) | - | 100.00(0.00) |

| loss | 0.15(0.10) | 0.13(0.09) | 2.02(0.14) | 0.34(0.78) | - | 0.06(0.02) | |

| size | 3.83(2.00) | 3.29(0.82) | 1.19(0.92) | 4.67(6.38) | - | 3.00(0.00) | |

| time | 58.46(6.15) | 59.33(6.21) | 34.61(4.62) | 92.41(21.77) | - | 0.19(0.03) | |

| 500 | rate | 100.00(0.00) | 100.00(0.00) | 38.67(13.99) | 100.00(0.00) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.09(0.04) | 0.06(0.04) | 1.92(0.33) | 0.04(0.02) | 0.22(0.04) | 0.04(0.02) | |

| size | 3.20(0.64) | 3.05(0.26) | 1.98(3.08) | 3.04(0.20) | 3.50(1.45) | 3.00(0.00) | |

| time | 4.24(0.55) | 4.13(0.58) | 102.20(15.51) | 132.41(15.95) | 62.85(0.72) | 0.02(0.00) | |

| 1000 | rate | 100.00(0.00) | 100.00(0.00) | 38.33(11.96) | 100.00(0.00) | 100.00(0.00) | 100.00(0.00) |

| loss | 0.09(0.05) | 0.06(0.03) | 1.94(0.21) | 0.04(0.02) | 0.23(0.03) | 0.04(0.01) | |

| size | 3.28(0.98) | 3.06(0.37) | 1.77(2.24) | 3.01(0.10) | 3.41(0.78) | 3.00(0.00) | |

| time | 25.95(2.65) | 25.64(2.42) | 116.46(23.30) | 131.51(25.39) | 261.54(9.76) | 0.06(0.01) | |

| 2000 | rate | 100.00(0.00) | 100.00(0.00) | 37.00(12.44) | 100.00(0.00) | - | 100.00(0.00) |

| loss | 0.09(0.06) | 0.06(0.04) | 1.94(0.31) | 0.04(0.02) | - | 0.04(0.02) | |

| size | 3.52(1.73) | 3.08(0.37) | 1.37(1.32) | 3.01(0.10) | - | 3.00(0.00) | |

| time | 90.72(6.72) | 96.52(7.18) | 243.33(72.01) | 249.13(46.48) | - | 0.24(0.02) | |

| out of memory in R | |||||||

3.3 Estimation of Main Effects

In this section we evaluate how estimation of main effects affects the estimation of interactions. Both our proposed residual-based penalized interaction estimation and the RAMP method involve estimating the main effects. To fixed the signal-to-noise ratio for all the settings, we simply draw the covariates from and consider the following quadratic model

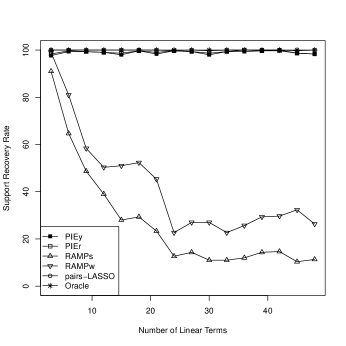

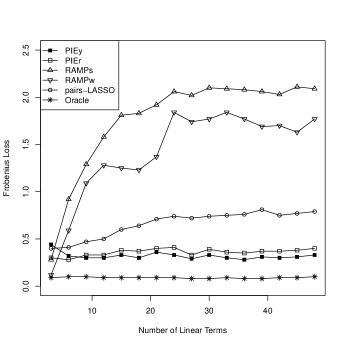

The number of main effects is increased from to . We always include , and to ensure that the strong heredity condition holds true. We also randomly choose from . Figure 1 reports the support recovery rate of and the Frobenius loss of .

It can be clearly seen that, as the number of main effects increases from to , both versions of the RAMP method, RAMPs and RAMPw, deteriorate gradually in terms of both criteria, indicating that the RAMP method heavily relies on estimating the main effects accurately. For all-pairs-LASSO, the support recovery rate is good while the Frobenius loss becomes worse when increases. By contrast, our proposal is very robust to the number of main effects under both criteria. Moreover, when the number of main effects increases, PIEy will be slightly better than PIEr in terms of Frobenius loss. Theses findings confirm our theoretical results in Theorem 2 since the estimation will become worse when increases.

3.4 Non-Normal Covariates

In this part, we investigate the performance of our proposal when the covariates are non-normal, and the factor model assumptions are violated. Let and . We draw s independently from (i) uniform distribution on the interval where , (ii) Student’s t-distribution where and (iii) Laplace distribution where . In all scenarios, the ’s are symmetric and have unit variance.

Table 3 reports the support recovery rate (“rate”) and the number of interactions that are estimated as nonzero (“size”) and the Frobenius loss (“loss”) of . From Table 3 we can see that PIEy and PIEr are still very effective when the covariates are non-normal, and the performance comparing with other methods are similar to those we have observed under normal assumptions, indicating that our proposal is practically robust to the violation of the theoretical assumptions.

| PIEy | PIEr | RAMPs | RAMPw | all-pairs-LASSO | Oracle | ||

|---|---|---|---|---|---|---|---|

| model (3.1) where the strong heredity condition is satisfied | |||||||

| Unif | rate | 99.33(4.69) | 99.67(3.33) | 100.00(0.00) | 100.00(0.00) | 100.00(0.00) | 100.00(0.00) |

| size | 3.86(1.73) | 3.19(0.72) | 3.00(0.00) | 3.03(0.17) | 5.96(3.94) | 3.00(0.00) | |

| loss | 0.22(0.18) | 0.13(0.12) | 0.06(0.02) | 0.06(0.03) | 0.26(0.05) | 0.06(0.02) | |

| t(5) | rate | 93.33(17.08) | 95.33(14.23) | 93.00(25.64) | 99.00(5.71) | 100.00(0.00) | 100.00(0.00) |

| size | 6.12(3.35) | 5.99(5.80) | 3.40(2.27) | 3.59(1.93) | 7.61(4.96) | 3.00(0.00) | |

| loss | 0.47(0.55) | 0.33(0.50) | 0.22(0.62) | 0.11(0.27) | 0.25(0.06) | 0.06(0.03) | |

| Lap | rate | 100.00(0.00) | 100.00(0.00) | 90.67(28.85) | 98.67(6.56) | 100.00(0.00) | 100.00(0.00) |

| size | 5.87(4.12) | 4.90(3.61) | 2.93(1.27) | 3.75(3.15) | 7.10(5.27) | 3.00(0.00) | |

| loss | 0.25(0.12) | 0.15(0.06) | 0.27(0.66) | 0.11(0.24) | 0.23(0.06) | 0.06(0.03) | |

| model (3.2) where the weak heredity condition is satisfied | |||||||

| Unif | rate | 99.67(3.33) | 99.67(3.33) | 46.67(20.65) | 100.00(0.00) | 100.00(0.00) | 100.00(0.00) |

| size | 3.19(0.61) | 3.14(0.62) | 2.17(2.28) | 3.01(0.10) | 4.30(2.53) | 3.00(0.00) | |

| loss | 0.13(0.11) | 0.11(0.11) | 1.75(0.53) | 0.07(0.04) | 0.28(0.06) | 0.07(0.03) | |

| t(5) | rate | 94.33(15.75) | 95.00(14.51) | 51.33(27.80) | 98.00(14.07) | 100.00(0.00) | 100.00(0.00) |

| size | 6.17(4.74) | 6.14(6.50) | 2.99(2.85) | 3.39(1.98) | 5.20(3.39) | 3.00(0.00) | |

| loss | 0.36(0.55) | 0.31(0.53) | 1.61(0.69) | 0.11(0.36) | 0.25(0.05) | 0.06(0.03) | |

| Lap | rate | 100.00(0.00) | 100.00(0.00) | 48.67(28.59) | 94.00(23.87) | 100.00(0.00) | 100.00(0.00) |

| size | 5.37(3.72) | 5.21(4.17) | 2.54(2.72) | 3.56(3.07) | 4.87(2.41) | 3.00(0.00) | |

| loss | 0.17(0.08) | 0.13(0.08) | 1.63(0.69) | 0.20(0.57) | 0.25(0.06) | 0.05(0.02) | |

| model (3.3) where the heredity conditions is violated | |||||||

| Unif | rate | 99.67(3.33) | 99.67(3.33) | 14.00(29.66) | 46.33(25.47) | 100.00(0.00) | 100.00(0.00) |

| size | 3.95(1.83) | 3.13(0.44) | 1.19(2.91) | 4.27(5.99) | 5.26(3.89) | 3.00(0.00) | |

| loss | 0.22(0.16) | 0.12(0.12) | 2.05(0.50) | 1.46(0.66) | 0.28(0.06) | 0.06(0.02) | |

| t(5) | rate | 94.00(15.98) | 94.33(15.02) | 37.00(41.81) | 68.33(30.84) | 100.00(0.00) | 100.00(0.00) |

| size | 5.93(3.25) | 5.24(3.01) | 2.99(4.30) | 5.07(5.39) | 6.26(4.24) | 3.00(0.00) | |

| loss | 0.40(0.54) | 0.33(0.55) | 1.65(0.85) | 0.98(0.87) | 0.25(0.07) | 0.06(0.03) | |

| Lap | rate | 99.67(3.33) | 100.00(0.00) | 42.00(41.47) | 62.00(31.79) | 100.00(0.00) | 100.00(0.00) |

| size | 5.80(4.08) | 5.08(4.07) | 2.76(3.16) | 6.02(6.95) | 5.86(3.35) | 3.00(0.00) | |

| loss | 0.21(0.17) | 0.11(0.06) | 1.59(0.85) | 1.12(0.87) | 0.24(0.06) | 0.06(0.03) | |

| model (3.4) is a pure interaction model where the heredity conditions are violated | |||||||

| Unif | rate | 99.67(3.33) | 99.67(3.33) | 6.67(17.08) | 15.67(32.29) | 100.00(0.00) | 100.00(0.00) |

| size | 3.08(0.53) | 3.06(0.34) | 0.48(1.42) | 3.28(6.52) | 3.82(1.50) | 3.00(0.00) | |

| loss | 0.08(0.11) | 0.09(0.11) | 2.18(0.17) | 1.98(0.71) | 0.31(0.06) | 0.06(0.03) | |

| t(5) | rate | 94.33(15.75) | 94.67(14.77) | 26.00(33.02) | 49.67(46.30) | 100.00(0.00) | 100.00(0.00) |

| size | 6.00(6.19) | 5.97(6.15) | 1.81(2.92) | 5.66(7.17) | 5.10(4.03) | 3.00(0.00) | |

| loss | 0.29(0.57) | 0.29(0.55) | 1.92(0.61) | 1.28(1.09) | 0.27(0.07) | 0.06(0.03) | |

| Lap | rate | 100.00(0.00) | 100.00(0.00) | 27.67(30.72) | 52.00(45.52) | 100.00(0.00) | 100.00(0.00) |

| size | 5.11(4.34) | 5.07(4.43) | 2.78(4.39) | 5.55(6.93) | 4.41(2.79) | 3.00(0.00) | |

| loss | 0.07(0.04) | 0.08(0.05) | 1.95(0.50) | 1.25(1.09) | 0.26(0.06) | 0.06(0.02) | |

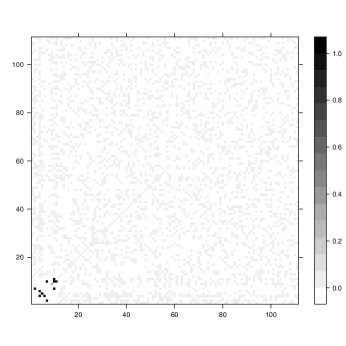

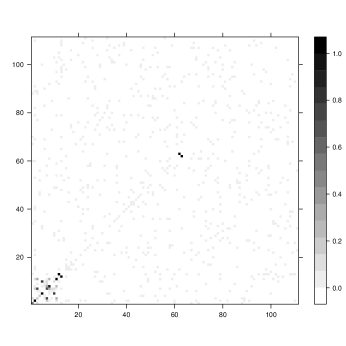

4 AN APPLICATION

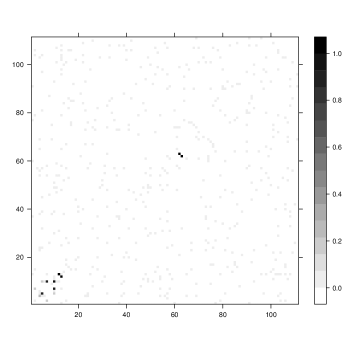

In this section, we apply our proposal to the red wine dataset which is publicly available at https://archive.ics.uci.edu/ml/datasets/Wine+Quality. The data consist of 11 measurements of several chemical constituents, including determination of density, alcohol or pH values for 1599 red wine samples from the northwest region of Portugal. The response variable is the median of the scores evaluated by human experts and each score ranges from 0 (very bad) to 10 (very excellent). The same dataset was once analyzed by Cortez et al. (2009). In their analysis, interactions are found to be very helpful for prediction. The original data are 1599 observations on 11 covariates. To accommodate high dimensional setting, we follow Radchenko and James (2010) and standardize all the variables and conduct the following two experiments:

-

•

Experiment 1. Denote the original 11 covariates as . We add 100 noise variables to the data, where are generated from the standard normal distribution and the remainders are generated by the uniform distribution on the interval .

-

•

Experiment 2. We generate the covariates in the same way as in Experiment 1. In addition, we modify the response variable by adding two more interactions: . In this experiment, both the strong and the weak heredity conditions are violated.

In both experiments the covariate dimension , leading to possible interactions. We randomly select 400 observations as the sample and the procedure is repeated 100 times. The heat map of the frequencies of the identified interactions are summarized in Figure 2. It can be clearly seen that, in Experiment 1, the detected interactions mainly occur among the first 11 covariates collected in the original dataset while the interactions related to the remaining 100 noisy covariates are rarely detected. This indicates that both PIEy and PIEr are able to exclude irrelevant interactions. In Experiment 2, both methods are able to exclude irrelevant interactions with high probability. In addition, the interactions and are successfully detected throughout.

(a) PIEy

(b) PIEr

(a) PIEy

(b) PIEr

(c) PIEy

(d) PIEr

(c) PIEy

(d) PIEr

5 DISCUSSION

In this paper we propose a penalized estimation to detect interactions without requiring heredity conditions. We develop an efficient ADMM algorithm to implement our estimation. We demonstrate the effectiveness of our proposal through extensive numerical studies. We remark here that, if the strong or the weak condition is satisfied, some existing methods, such as the RAMP method, work pretty well. However, when we have little prior information about whether the heredity condition holds true or not in an application, we advocate using our proposal in that it does not require this assumption. In effect, if the heredity condition is known to be satisfied, we can also incorporate it into our proposal through a two-stage procedure. In the first stage, we use the penalized least squares to identify the main effects; and in the second stage, we implement our procedure using only the main effects that are selected in the first stage. This allows us to handle ultrahigh dimensional problems efficiently. Another way to enhance the power of our proposal is to incorporate some screening procedures into our problems. We also remark here that, in the present context we focus on quadratic regression which contains pairwise interactions of the form . We remark here that our idea can be generalized naturally to higher-order interactions models of the form . However, estimating high-order interactions is generally much more challenging because there are possible interactions of order in total. The central task is possibly to develop efficient algorithms with minimal computational complexity. Researches along these lines are warranted.

Appendix

5.1 Appendix A: Some Useful Lemmas

We first show that the ADMM algorithm to minimize (2.5) converges linearly.

Lemma 2.

Proof.

The objective function in the minimization problem (2.5) can be decomposed into two components: , where and . Rewrite . Denote and . Let be a function defined on , and , be two functions defined on . Then and . Given , and , the gradient of is uniformly Lipschitz continuous and and are polyhedral. Lemma 2 thus follows immediately from Theorem 3.1 of Hong and Luo (2017). ∎

Next we present some useful lemmas for the proofs of the main theorems. Without loss of generality, in what follows we assume that and .

Lemma 3.

Let be independent variables and for some . Then for , there exist constants such that

Proof of Lemma 3: For , see Lemma B.4 of Hao and Zhang (2014). Here, we only need to show for some . By the integral identity of the expectation, we have

Consequently, The proof is completed.

Lemma 4.

Let and be two variables such that and , where . We have

Lemma 5.

Under condition (A2), we have there exists a constant ,

| (5.1) | |||||

| (5.2) |

Proof of Lemma 5: Writing as the unit-length -vector with its -th entry being one, we have Note that are independent centered sub-Gaussian variables. By Hoeffding’s inequality (Vershynin, 2017, Theorem 2.6.3), and then Therefore,

Set for large enough , which yields the conclusion (5.1).

Similarly, are independent centered sub-exponential variables. By Bernstein’s inequality (Vershynin, 2017, Theorem 2.8.2), we get

Choose with a sufficiently large to complete proof of (5.2).

Lemma 6.

Under conditions (A2) and (A3), there exists a constant such that,

| (5.3) | |||

| (5.4) | |||

Proof of Lemma 6: We prove (6) only in what follows and (6) can be proved using similar arguments. For ,

By condition (A2), there exist constants and such that

By condition (A3) and Lemma 4, we have there exist constants such that By Lemma 3, we have

Using the similar arguments as in the proofs of Lemma 5, we can show

The proof is completed.

5.2 Appendix B: The -Penalized Estimation

Let be unknown parameters and is a positive definite symmetric matrix. To estimate , we consider the -penalized approach:

| (5.5) |

where is the tuning parameter and and are the empirical estimators of and , respectively. In the sequel, we establish theoretical results for solving (5.5). These general results will then be used to prove the main theorems in our paper.

Lemma 7.

Denote and let be the support of . Assume that and we have

-

(i)

;

-

(ii)

Proof of Lemma 7: Given the true support , we consider the estimation

By the Karush-Kuhn-Tucker (KKT) condition, we have

| (5.6) |

where is the sub-gradient of . By the definition of , we have

and hence we have Consequently, we obtain,

| (5.7) |

Using the triangle inequality, we can show that,

which implies that

Next, we show that is exactly the minimizer to By the KKT condition, it is sufficient to prove

| (5.9) | |||

| (5.10) |

Since , (5.9) is true by (5.6). For (5.10), we have

Thus, it follows from (5.7) and (5.2) that is less than or equal to

When we have Consequently, and (5.10) is an immediate result of (5.2) by noting . The proof is completed.

5.3 Appendix C: Proof of Proposition 1

Recall that . Direct calculations show

The proof of the first part is completed. Next we prove the second part.

Thus, when or . The proof is completed.

5.4 Appendix D: Proof of Theorem 1

We provide proofs for (i) and (iii) in what follows because (ii) is an immediate result of (i) and (iii) and (iv) can be obtained analog to (iii). For the target parameter matrix , we consider its vectorization

| (5.11) |

where is a positive and symmetric matrix. For the estimation,

Equivalently, we have

where . Therefore, we can use Lemma 7 to derive the theoretical properties by letting

Recall the definition of and .

Lemmas 5 and 6 ensure that there exists a constant such that with probability greater than , and Note that with probability greater than , we have, for some constant and Next, we consider Note that

Under the conditions of the Proposition 1,

| (5.12) |

We thus conclude and . Then, and by invoking Lemma 5 and the fact Consequently, there exist a constant such that with probability larger than . Set and by Lemma 7. We can conclude that with probability larger than , , and The proof is now completed.

5.5 Appendix E: Proof of Theorem 2

Given ,

Given true , (5.12) ensures that , indicating that for some constant . Thus, and with probability greater than ,

| (5.13) |

Writing we have,

For , . By Lemma 6, there exists a large constant such that,

which implies

Note that . With probability greater than ,

which together with Lemma 5 yields

| (5.14) |

Combing (5.13) and (5.14), with probability greater than ,

Similarly to the proof of the Theorem 1, we can set

and conclude that with probability lager than , and for some constant .

References

- Bai and Saranadasa (1996) {barticle}[author] \bauthor\bsnmBai, \bfnmZhidong\binitsZ. and \bauthor\bsnmSaranadasa, \bfnmHewa\binitsH. (\byear1996). \btitleEffect of high dimension: by an example of a two sample problem. \bjournalStatistica Sinica \bvolume6 \bpages311–329. \endbibitem

- Bien, Simon and Tibshirani (2015) {barticle}[author] \bauthor\bsnmBien, \bfnmJacob\binitsJ., \bauthor\bsnmSimon, \bfnmNoah\binitsN. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear2015). \btitleConvex hierarchical testing of interactions. \bjournalThe Annals of Applied Statistics \bvolume9 \bpages27–42. \endbibitem

- Bien, Taylor and Tibshirani (2013) {barticle}[author] \bauthor\bsnmBien, \bfnmJacob\binitsJ., \bauthor\bsnmTaylor, \bfnmJonathan\binitsJ. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear2013). \btitleA lasso for hierarchical interactions. \bjournalThe Annals of Statistics \bvolume41 \bpages1111. \endbibitem

- Boyd et al. (2011) {barticle}[author] \bauthor\bsnmBoyd, \bfnmStephen\binitsS., \bauthor\bsnmParikh, \bfnmNeal\binitsN., \bauthor\bsnmChu, \bfnmEric\binitsE., \bauthor\bsnmPeleato, \bfnmBorja\binitsB. and \bauthor\bsnmEckstein, \bfnmJonathan\binitsJ. (\byear2011). \btitleDistributed optimization and statistical learning via the alternating direction method of multipliers. \bjournalFoundations and Trends in Machine Learning \bvolume3 \bpages1–122. \endbibitem

- Chen, Sun and Toh (2017) {barticle}[author] \bauthor\bsnmChen, \bfnmLiang\binitsL., \bauthor\bsnmSun, \bfnmDefeng\binitsD. and \bauthor\bsnmToh, \bfnmKim-Chuan\binitsK.-C. (\byear2017). \btitleA note on the convergence of ADMM for linearly constrained convex optimization problems. \bjournalComputational Optimization and Applications \bvolume66 \bpages327–343. \endbibitem

- Chen, Zhang and Zhong (2010) {barticle}[author] \bauthor\bsnmChen, \bfnmSongxi\binitsS., \bauthor\bsnmZhang, \bfnmLixin\binitsL. and \bauthor\bsnmZhong, \bfnmPingshou\binitsP. (\byear2010). \btitleTests for high-dimensional covariance matrices. \bjournalJournal of the American Statistical Association \bvolume105 \bpages810–819. \endbibitem

- Cheng and Zhu (2017) {barticle}[author] \bauthor\bsnmCheng, \bfnmQing\binitsQ. and \bauthor\bsnmZhu, \bfnmLiping\binitsL. (\byear2017). \btitleOn relative efficiency of principal Hessian directions. \bjournalStatistics & Probability Letters \bvolume126 \bpages108–113. \endbibitem

- Choi, Li and Zhu (2010) {barticle}[author] \bauthor\bsnmChoi, \bfnmNam Hee\binitsN. H., \bauthor\bsnmLi, \bfnmWilliam\binitsW. and \bauthor\bsnmZhu, \bfnmJi\binitsJ. (\byear2010). \btitleVariable selection with the strong heredity constraint and its oracle property. \bjournalJournal of the American Statistical Association \bvolume105 \bpages354–364. \endbibitem

- Cordell (2009) {barticle}[author] \bauthor\bsnmCordell, \bfnmHeather J\binitsH. J. (\byear2009). \btitleDetecting gene-gene interactions that underlie human diseases. \bjournalNature reviews. Genetics \bvolume10 \bpages392. \endbibitem

- Cortez et al. (2009) {barticle}[author] \bauthor\bsnmCortez, \bfnmPaulo\binitsP., \bauthor\bsnmCerdeira, \bfnmAntónio\binitsA., \bauthor\bsnmAlmeida, \bfnmFernando\binitsF., \bauthor\bsnmMatos, \bfnmTelmo\binitsT. and \bauthor\bsnmReis, \bfnmJosé\binitsJ. (\byear2009). \btitleModeling wine preferences by data mining from physicochemical properties. \bjournalDecision Support Systems \bvolume47 \bpages547 - 553. \endbibitem

- Efron et al. (2004) {barticle}[author] \bauthor\bsnmEfron, \bfnmBradley\binitsB., \bauthor\bsnmHastie, \bfnmTrevor\binitsT., \bauthor\bsnmJohnstone, \bfnmIain\binitsI. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear2004). \btitleLeast angle regression. \bjournalThe Annals of Statistics \bvolume32 \bpages407–499. \endbibitem

- Fan and Li (2001) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmLi, \bfnmRunze\binitsR. (\byear2001). \btitleVariable selection via nonconcave penalized likelihood and its oracle properties. \bjournalJournal of the American Statistical Association \bvolume96 \bpages1348–1360. \endbibitem

- Fan et al. (2015) {barticle}[author] \bauthor\bsnmFan, \bfnmYingying\binitsY., \bauthor\bsnmKong, \bfnmYinfei\binitsY., \bauthor\bsnmLi, \bfnmDaoji\binitsD. and \bauthor\bsnmZheng, \bfnmZemin\binitsZ. (\byear2015). \btitleInnovated interaction screening for high-dimensional nonlinear classification. \bjournalThe Annals of Statistics \bvolume43 \bpages1243–1272. \endbibitem

- Friedman, Hastie and Tibshirani (2010) {barticle}[author] \bauthor\bsnmFriedman, \bfnmJerome\binitsJ., \bauthor\bsnmHastie, \bfnmTrevor\binitsT. and \bauthor\bsnmTibshirani, \bfnmRob\binitsR. (\byear2010). \btitleRegularization paths for generalized linear models via coordinate descent. \bjournalJournal of statistical software \bvolume33 \bpages1. \endbibitem

- Hamada and Wu (1992) {barticle}[author] \bauthor\bsnmHamada, \bfnmMichael\binitsM. and \bauthor\bsnmWu, \bfnmCF Jeff\binitsC. J. (\byear1992). \btitleAnalysis of designed experiments with complex aliasing. \bjournalJournal of Quality Technology \bvolume24 \bpages130–137. \endbibitem

- Hao, Feng and Zhang (2017) {barticle}[author] \bauthor\bsnmHao, \bfnmNing\binitsN., \bauthor\bsnmFeng, \bfnmYang\binitsY. and \bauthor\bsnmZhang, \bfnmHao Helen\binitsH. H. (\byear2017). \btitleModel selection for high dimensional quadratic regression via regularization. \bjournalJournal of the American Statistical Association, in press. \endbibitem

- Hao and Zhang (2014) {barticle}[author] \bauthor\bsnmHao, \bfnmNing\binitsN. and \bauthor\bsnmZhang, \bfnmHao Helen\binitsH. H. (\byear2014). \btitleInteraction screening for ultrahigh-dimensional data. \bjournalJournal of the American Statistical Association \bvolume109 \bpages1285–1301. \endbibitem

- Haris, Witten and Simon (2016) {barticle}[author] \bauthor\bsnmHaris, \bfnmAsad\binitsA., \bauthor\bsnmWitten, \bfnmDaniela\binitsD. and \bauthor\bsnmSimon, \bfnmNoah\binitsN. (\byear2016). \btitleConvex modeling of interactions with strong heredity. \bjournalJournal of Computational and Graphical Statistics \bvolume25 \bpages981–1004. \endbibitem

- Hong and Luo (2017) {barticle}[author] \bauthor\bsnmHong, \bfnmMingyi\binitsM. and \bauthor\bsnmLuo, \bfnmZhi-Quan\binitsZ.-Q. (\byear2017). \btitleOn the linear convergence of the alternating direction method of multipliers. \bjournalMathematical Programming \bvolume162 \bpages165–199. \endbibitem

- Kong et al. (2017) {barticle}[author] \bauthor\bsnmKong, \bfnmYinfei\binitsY., \bauthor\bsnmLi, \bfnmDaoji\binitsD., \bauthor\bsnmFan, \bfnmYingying\binitsY. and \bauthor\bsnmLv, \bfnmJinchi\binitsJ. (\byear2017). \btitleInteraction pursuit in high-dimensional multi-response regression via distance correlation. \bjournalThe Annals of Statistics \bvolume45 \bpages897–922. \endbibitem

- Li (1992) {barticle}[author] \bauthor\bsnmLi, \bfnmKer-Chau\binitsK.-C. (\byear1992). \btitleOn principal Hessian directions for data visualization and dimension reduction: Another application of Stein’s lemma. \bjournalJournal of the American Statistical Association \bvolume87 \bpages1025–1039. \endbibitem

- Lim and Hastie (2015) {barticle}[author] \bauthor\bsnmLim, \bfnmMichael\binitsM. and \bauthor\bsnmHastie, \bfnmTrevor\binitsT. (\byear2015). \btitleLearning interactions via hierarchical group-lasso regularization. \bjournalJournal of Computational and Graphical Statistics \bvolume24 \bpages627–654. \endbibitem

- Liu and Luo (2015) {barticle}[author] \bauthor\bsnmLiu, \bfnmWeidong\binitsW. and \bauthor\bsnmLuo, \bfnmXi\binitsX. (\byear2015). \btitleFast and adaptive sparse precision matrix estimation in high dimensions. \bjournalJournal of Multivariate Analysis \bvolume135 \bpages153–162. \endbibitem

- Nelder (1977) {barticle}[author] \bauthor\bsnmNelder, \bfnmJ. A.\binitsJ. A. (\byear1977). \btitleA Reformulation of Linear Models. \bjournalJournal of the Royal Statistical Society, Series A \bvolume140 \bpages48-77. \endbibitem

- Nishihara et al. (2015) {barticle}[author] \bauthor\bsnmNishihara, \bfnmRobert\binitsR., \bauthor\bsnmLessard, \bfnmLaurent\binitsL., \bauthor\bsnmRecht, \bfnmBenjamin\binitsB., \bauthor\bsnmPackard, \bfnmAndrew\binitsA. and \bauthor\bsnmJordan, \bfnmMichael I\binitsM. I. (\byear2015). \btitleA general analysis of the convergence of ADMM. \bjournalarXiv preprint arXiv:1502.02009. \endbibitem

- Radchenko and James (2010) {barticle}[author] \bauthor\bsnmRadchenko, \bfnmPeter\binitsP. and \bauthor\bsnmJames, \bfnmGareth\binitsG. (\byear2010). \btitleVariable selection using adaptive nonlinear interaction structures in high dimensions. \bjournalJournal of the American Statistical Association \bvolume105 \bpages1541–1553. \endbibitem

- Ravikumar et al. (2011) {barticle}[author] \bauthor\bsnmRavikumar, \bfnmPradeep\binitsP., \bauthor\bsnmWainwright, \bfnmMartin\binitsM., \bauthor\bsnmRaskutti, \bfnmGarvesh\binitsG. and \bauthor\bsnmYu, \bfnmBin\binitsB. (\byear2011). \btitleHigh-dimensional covariance estimation by minimizing -penalized log-determinant divergence. \bjournalElectronic Journal of Statistics \bvolume5 \bpages935–980. \endbibitem

- Ritchie et al. (2001) {barticle}[author] \bauthor\bsnmRitchie, \bfnmMarylyn D\binitsM. D., \bauthor\bsnmHahn, \bfnmLance W\binitsL. W., \bauthor\bsnmRoodi, \bfnmNady\binitsN., \bauthor\bsnmBailey, \bfnmL Renee\binitsL. R., \bauthor\bsnmDupont, \bfnmWilliam D\binitsW. D., \bauthor\bsnmParl, \bfnmFritz F\binitsF. F. and \bauthor\bsnmMoore, \bfnmJason H\binitsJ. H. (\byear2001). \btitleMultifactor-dimensionality reduction reveals high-order interactions among estrogen-metabolism genes in sporadic breast cancer. \bjournalThe American Journal of Human Genetics \bvolume69 \bpages138–147. \endbibitem

- Simon and Tibshirani (2015) {barticle}[author] \bauthor\bsnmSimon, \bfnmNoah\binitsN. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear2015). \btitleA Permutation Approach to Testing Interactions for Binary Response by Comparing Correlations Between Classes. \bjournalJournal of the American Statistical Association \bvolume110 \bpages1707–1716. \endbibitem

- Stein (1981) {barticle}[author] \bauthor\bsnmStein, \bfnmCharles M\binitsC. M. (\byear1981). \btitleEstimation of the mean of a multivariate normal distribution. \bjournalThe Annals of Statistics \bvolume9 \bpages1135-1151. \endbibitem

- Tibshirani (1996) {barticle}[author] \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear1996). \btitleRegression Shrinkage and Selection via the Lasso. \bjournalJournal of the Royal Statistical Society, Series B \bvolume58 \bpages267–288. \endbibitem

- Tibshirani et al. (2012) {barticle}[author] \bauthor\bsnmTibshirani, \bfnmRobert\binitsR., \bauthor\bsnmBien, \bfnmJacob\binitsJ., \bauthor\bsnmFriedman, \bfnmJerome\binitsJ., \bauthor\bsnmHastie, \bfnmTrevor\binitsT., \bauthor\bsnmSimon, \bfnmNoah\binitsN., \bauthor\bsnmTaylor, \bfnmJonathan\binitsJ. and \bauthor\bsnmTibshirani, \bfnmRyan J\binitsR. J. (\byear2012). \btitleStrong rules for discarding predictors in lasso-type problems. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume74 \bpages245–266. \endbibitem

- Vershynin (2017) {bbook}[author] \bauthor\bsnmVershynin, \bfnmRoman\binitsR. (\byear2017). \btitleHigh Dimensional Probability. \bpublisherIn press. \endbibitem

- Yuan, Joseph and Zou (2009) {barticle}[author] \bauthor\bsnmYuan, \bfnmMing\binitsM., \bauthor\bsnmJoseph, \bfnmRoshan\binitsR. and \bauthor\bsnmZou, \bfnmHui\binitsH. (\byear2009). \btitleStructured variable selection and estimation. \bjournalThe Annals of Applied Statistics \bvolume3 \bpages1738–1757. \endbibitem

- Zhang and Zou (2014) {barticle}[author] \bauthor\bsnmZhang, \bfnmTeng\binitsT. and \bauthor\bsnmZou, \bfnmHui\binitsH. (\byear2014). \btitleSparse precision matrix estimation via lasso penalized D-trace loss. \bjournalBiometrika \bvolume101 \bpages103–120. \endbibitem

- Zhao and Yu (2006) {barticle}[author] \bauthor\bsnmZhao, \bfnmPeng\binitsP. and \bauthor\bsnmYu, \bfnmBin\binitsB. (\byear2006). \btitleOn model selection consistency of Lasso. \bjournalJournal of Machine Learning Research \bvolume7 \bpages2541–2563. \endbibitem

- Zou (2006) {barticle}[author] \bauthor\bsnmZou, \bfnmHui\binitsH. (\byear2006). \btitleThe adaptive lasso and its oracle properties. \bjournalJournal of the American Statistical Association \bvolume101 \bpages1418–1429. \endbibitem