On a dividend problem with random funding

Kopernikusgasse 24/III, 8010 Graz, Austria

18th January 2019)

Abstract

We consider a modification of the dividend maximization problem from ruin theory. Based on a classical risk process we maximize the difference of expected cumulated discounted dividends and total expected discounted additional funding (subject to some proportional transaction costs). For modelling dividends we use the common approach whereas for the funding opportunity we use the jump times of another independent Poisson process at which we choose an appropriate funding height. In case of exponentially distributed claims we are able to determine an explicit solution to the problem and derive an optimal strategy whose nature heavily depends on the size of the transaction costs.

Keywords: Ruin Theory, Classical Risk Model, Dividends, Stochastic Control.

1 Introduction and some first considerations

1.1 Overview

In this article we deal with an extension of the classical dividend maximization problem for an underlying classical (compound Poisson) surplus process. Our proposed extension considers a random funding opportunity which is modelled by the following procedure. The insurer actively searches for investors who are willing to provide additional funding for the insurance portfolio under consideration. If the search is successful, the insurer can choose the height of the funding, increase the surplus and possibly pay out higher dividends in the future. We model the search procedure by means of an intensity , such that the insurer finds funding opportunities at the jump-times of an additional and independent Poisson process. Naturally, new funding is costly or investors want to participate in future dividends respectively. That is why we weight this additional capital with a factor which plays the role of a proportional transaction cost. The corresponding value function of our problem is the difference of expected cumulated discounted dividends and weighted expected cumulated discounted fundings, both up to the time of ruin.

For the case our approach just matches the classical dividend problem, i.e., no additional funding source can be found. Its treatment goes back to Gerber [5] and is analyzed in terms of optimal stochastic control by Azcue & Muler [2, 3] and Schmidli [9]. The opposite extremal case somehow resembles the situation of a possible capital injection at any point in time. This problem is by now well known under the keywords maximal dividends and capital injections and was firstly formulated and solved by Kulenko & Schmidli [7] with the subtle difference that the controlled surplus process is not allowed to get ruined and thus resulting in a different value function.

Certainly, the approach of interventions at the jump times of another process is related to the formulation of ruin theoretic problems under random observations. Such a model comprising dividends is introduced by Albrecher et al. [1] and gained some relevance in actuarial research over the last years. We need to emphasize that our present model is continuously monitored, i.e., dividend decisions can be made at any point in time and also the ruin event is immediately observed.

Another framework where dividend maximization problems for firm value determinations play a crucial role is finance. There the underlying process, typically given by a diffusion process, is interpreted as a cash reservoir of a company and the expected value of cumulated dividends reflects the value of this company. The present question is studied in a similar fashion in this financial diffusion framework by Hugonnier et al. [6] in combination with an optimal stopping problem. As mentioned, the problem studied there is based on a continuous sample paths process and also the transaction costs parameter equals one, which results in a common single barrier type optimal strategy, both for dividends and fundings.

Interestingly, the recent paper by Zhang et al. [11] study a compound Poisson risk model with a particular capital injection procedure, which is very similar to the optimal one derived in our contribution.

In contrast to our considerations, the focus is put on the determination of discounted penalty functions and dividend decisions are not part of the setup.

The paper is organized as follows. We start with the mathematical formulation of the model and associated stochastic optimization problem. In a next step we establish some basic properties of the value function and study parameter constellations which lead to degenerate optimal strategies. Having understood the crucial dependence on the magnitude of the transaction costs, we can subsequently determine the optimal strategy and corresponding value function. The key in this step is to prove the existence of a solution of a free-boundary value problem comprising two boundaries. We close the paper by some numerical illustrations which focus on the optimal strategy as a function of the transaction costs parameter .

1.2 Model setup

In the subsequent lines we introduce the model of interest and the underlying stochastic protagonists. First of all we set up the stochastic basis of our considered model. We suppose a given probability space which carries the following underlying stochastic processes.

Let be a Poisson process with intensity and let be a sequence of independent and identically distributed random variables with distribution function denoted by with , we set and assume to be independent of . Then we consider the following compound Poisson process ,

which describes, as common in the classical risk model, the sum of all claims up to time .

Next we consider a jump process with constant intensity , i.e. a Poisson process,

with which we are able to describe the occurrence times of new investors. In particular investors occur at the jump-times of .

Again, independence between is assumed.

Based on these ingredients we identify the filtration which models the available information at time .

Consequently, we have to set

where and are the filtrations generated by the respective processes and denotes the sets of measure zero.

Assuming that the insurance company has an initial surplus and receives premiums according to a rate , we define the uncontrolled surplus or cash reserve process , by

The control processes for the state process are on the one hand the dividend process , an adapted and cáglád process, hence it is previsible, which is increasing and fulfills . It represents the cumulated dividends up to time t. On the other hand we consider the control process , previsible as well, and - almost surely non-negative, i.e. . The control corresponds to the magnitude of the new funding at time in case jumps. According to that, the controlled cash reserve process reads as follows

In our setting it is not allowed that ruin is induced by dividend payments and therefore the relation

has to hold

Remark 1.

Due to the independence assumptions we have that the two Poisson processes and do not jump at the same time. Since the paths of the dividend process are left-continuous one needs to read .

1.3 Optimization problem and value function

The stated aim in our setting is to find the optimal combined dividend and funding strategy which maximizes the expected cumulated discounted future dividends deducting at least the received total additional funding. The deduction depends on a proportional funding cost parameter denoted by . Hence the value function is defined by

here denotes the first time when the controlled cash reserve process becomes negative, namely and is the set containing those admissible processes such that

If we assume that the controls are constant and the dividend control suffices for some , we face a Markov process whose infinitesimal generator is

Naturally, the function above has to be in the domain of the generator , which contains absolutely continuous functions satisfying an integrability condition , see Rolski et al. [8, Th. 11.2.2]. Using this expression we can state the Hamilton-Jacobi-Bellman equation of this problem

| (1) |

From the shape of the HJB-equation we can immediately derive some properties of its solutions.

Lemma 1.

Let be a continuously differentiable solution to the HJB-equation (1), then is strictly monotone increasing () and bounded from below by .

Proof.

From the equation we directly obtain that and if we consider the limit we get . Since is monotone increasing and continuous the assertion follows. ∎

Furthermore, we can bound the value function from below similarly as done by Azcue & Muller [2] or by Schmidli [9, p. 80 Lemma 2.37].

Lemma 2.

In the present model setup the value function fulfills

Proof.

For the special choice we face an admissible dividend strategy for the original dividend maximization problem. The bound follows from the above cited (by now classical) results. ∎

2 Solution of the optimization problem

In the following we assume that the claim size distribution coincides with an exponential distribution with parameter . We try to identify an optimal strategy and determine an explicit solution to the problem. In case of an arbitrary claim size distribution one can expect a strategy of band type to be optimal. One needs to mention that the presence of the financing control complicates the situation in comparison to other modifications of the dividend problem with exponentially distributed claims in the literature.

We start with identifying parameter sets which lead to somehow degenerate optimal strategies.

2.1 Optimality of keeping the reserve at zero

For a special parameter configuration we obtain that the optimal strategy is to payout the initial reserve immediately and keep on paying dividends such that the current reserve remains zero, which means that the dividend rate is and the first claim causes ruin. Compare to classical results as presented in [9, p. 93].

Lemma 3.

The optimal strategy is to payout immediately the initial reserve and then payout dividends at the premium rate if . Consequently, the value function has the following form

| (2) |

Proof.

Using the proof is analogous to the one given in [9, p. 93]. Just note that in the present problem with capital supply the additional part of the HJB-equation corresponding to is zero,

since . ∎

From the latter result we see that we need to focus on , which in turn implies that , since we assume that all parameters are positive.

2.2 An embedded problem

At the outset of tackling the problem we try as first conjectures some common types of controls such as barrier and simple band strategies.

It turned out that they can not be optimal in general. Therefore, in order to get an idea of the shape of the optimal strategy we exploit a numerical approach.

At first fix and allow for at most capital injections (at the jump times of ), the corresponding family of value functions is defined by

One may notice that is the value function of the classical dividend maximization problem and in the situation of exponentially distributed claims is explicitely known. However, the method below does not need to assume exponential claims but is focused on barrier type dividend strategies. Certainly, this can be generalized.

We have that after using one intervention restarts with , which can be used when maximizing with respect to . The deduced numerical procedure is as follows:

-

1.

Compute without additional capital (), by solving

for and for . If the optimal is not known one can do this for different values of . Choosing the maximizing , we obtain an approximation to with optimal barrier, say . Then we can compute the optimal state dependent by setting

-

2.

Compute , where we allow for one financial injection, exactly , and solve for different values of

for and for . The usage of the maximizing results in an approximation of . As next step replace by in the first step and go on.

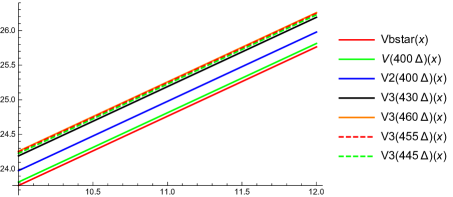

Of course we have to choose in every step the best value for the threshold , which is illustrated in Figure 1. There Vbstar denotes the numerical solution of the usual dividend problem, further denotes the solution of the iteration, when funding opportunities are allowed. The value inside the brackets correspond to the values of the barrier , where .

This approach reveals a new type of possibly optimal strategy to us, which turns out to be the right conjecture.

2.3 Resulting new strategy

Using the results from the numerical approach, we are able to construct a new strategy for our problem. The new strategy is of band type and specified by two parameters such that

-

•

the dividend strategy is of barrier type at level ,

-

•

the financing strategy only applies at reserve levels . It is given by , with the feature that only below level we search for a funding source. If one appears, we choose the funding height to such an extent that the surplus jumps up to and in general not to the barrier level .

For initial surplus we denote the value, i.e., performance function, according to such a strategy by . By construction it makes sense to write this function in the following form:

| (3) |

Whereby, using Dynkin-formula type arguments or classical arguments based on conditioning on the first claim occurence, the functions and have to fulfill the equations

| (4) |

| (5) |

| (6) |

We get immediately, using the above equations, that is continuously differentiable in .

Furthermore, we obtain that continuity implies differentiability, i.e. if and only if .

This means that the condition in (6) is equivalent to the condition .

We use the method of equating coefficients in order to solve the above equations (4), (5) and (6) explicitely.

This yields functions

| (7) | ||||

| (8) |

where are solutions to .

The exponents solve

Note that under our assumptions we have that . The coefficients are obtained by a system of five linear equations and do heavily depend on the parameters .

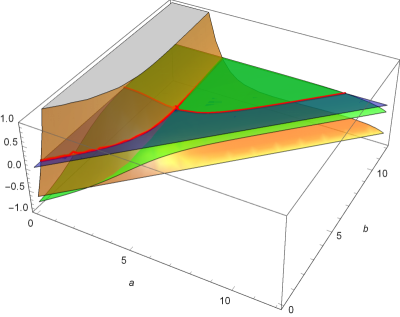

We observe that numerical maximization of the function in and for fixed results in levels and which are independent of . These particular levels also coincide with the solutions of second order smooth fit conditions in and . Additionally, we need to fulfill these second order smooth fit conditions in order to get a function which is twice continuously differentiable. This seems to be superfluous, since the domain of the generator only asks for absolut continuity, but in combination with concavity it serves as a basis for a direct proof of the associated verification theorem. The conditions read as follows:

| (9) |

In Figure 2 the green surface corresponds to , the orange surface corresponds to and the blue plane highlights the zero level. The red curves mark the intersection of the two surfaces with the zero level.

Finally, we have to prove the existence of thresholds and such that the smooth fit conditions are fulfilled. In our treatment we are able to derive an interesting condition, which turns out to be equivalent to one of the conditions above.

If we differentiate the two integro-differential equations (for and ), which characterize and , we obtain

and

If we now set and calculate the difference of those two equations, we get using and that

Hence we have that if and only if .

Remark 2.

If we consider the following part of the HJB-equation:

we obtain for the function , if it is concave, that the term inside the supremum is maximal if . This means that using an such that , yields that the corresponding term () in the equation above is zero.

2.3.1 Extremal behaviour of optimal strategy

First of all we want to know, whether the optimal strategy uses the additional funding or not, which means that we have to determine the reasons for the choice . For that purpose we consider the solution of the usual dividend problem, which is well-known in the literature, see [9],

Here

where and are the same exponents as before and the optimal barrier ensuring twice continuous differentiability of the value function has the following form

In this case we have to assume that

in order to make sure that holds. This yields that in the usual dividend problem is the value function. We have that .

Remark 3.

At first one notices that

A second thought concerns the behaviour of an possibly optimal level with respect to the parameter . The following is more a heuristic intuition than a rigorous treatment. But if we consider , where is the maximizing argument of the supremum part of the HJB-equation

as mentioned in the previous remark, we get (considering as a function of , i.e. ) that

if we assume that is concave, which will be true if is the value function. This means that the lower threshold is decreasing in .

Proposition 1.

Let the optimal barrier in the classical dividend problem be positive. For the optimal levels in the dividend problem with random funding we obtain that and if and only if .

This means that the simple barrier strategy is optimal and the solution of the classical dividend problem coincides with the solution of the extended problem.

Proof.

We assume that and have to show that and are the optimal thresholds so that solves the HJB-equation, is concave and - the ingredients we later need in the verification theorem.

We know that this candidate function is concave, and solves the HJB-equation of the classical dividend problem with . Using this, we obtain for that

For the first part of the HJB-equation it remains to show that

If we choose the term inside the supremum is zero. Otherwise, if we obtain that

This holds true because if we use we get

and from , the above inequality follows.

For the values we know that , and that the first part of the HJB-equation (which coincides with the first part of the classical HJB-equation) is negative. So it remains to check whether

holds. But this is true since if we plug in the linear function for we get that , since . The special case is analogue to the situation .

For the other direction, if and are optimal, we have to show . For that purpose we assume the opposite, namely that .

But in this case we can exploit the fact that and , in addition to the above assumption . Putting this together yields by the intermediate value theorem that . We want to show that

Differentiating the inner term and setting it equal to zero yields that

so we obtain that which is positive, if . Applying Taylor’s formula gives for some the following

Finally we obtain that this function does not solve the HJB-equation and being optimal cannot work out, which is a contradiction. ∎

The above proposition gives us the optimal strategy in the case . Furthermore, only in that case the usual dividend barrier strategy is optimal. In the next step we consider the lowest bound for the parameter where a non-trivial strategy appears namely .

Lemma 4.

Let be positive. For the optimal levels for the dividend problem with random funding we obtain that if .

In this case we are in the following situation, if an investor occurs we generate external funding to such an extent that we arrive with the surplus process at the dividend barrier, which triggers dividend payments. Hence, there is no gap between the dividend barrier and the funding level.

Proof.

Solving the above equations for , we get the function .

It remains to prove the existence of , resulting in , such that the assumptions of the verification theorem are fulfilled.

At this point we know that and we have to find such that the smooth fit condition is fulfilled:

.

Evaluating this function at yields

which is negative according to our assumptions. Otherwise, we would have a value function of the form

as treated in the corresponding lemma above.

Furthermore, if we obtain that . This is also in line with the just mentioned case of a linear value function.

On the other hand we know that

is continuous and is strictly positive. This yields that there exists an such that . If there would be more than one point, such that the smooth fit conditions are fulfilled, we decide to choose the smallest one. At this we are able to exploit the equations and to get that and . This yields that for all , moreover together with we obtain that for . Which in turn implies that for . So the obtained function

| (10) |

is twice continuously differentiable and concave, in addition to that it fulfills the HJB-equation with . Altogether, this enables us to apply the verification theorem. ∎

2.3.2 The case of moderate

Up to now we have investigated the following cases and obtained in each case the optimal combined strategy:

-

•

and ,

-

•

.

In this section we fill the missing gaps in order to have an optimal solution for every admissible value of .

Theorem 1.

Proof.

Obviously, we have to solve the equations related to our band strategy for . This leads to a solution heavily depending on as in the previous case and it remains to choose the values and such that the equivalent smooth fit conditions are fulfilled, which are restated here

| (11) | |||

| (12) |

Anyway, the coefficients and are fixed such that

| (13) |

holds true. Transforming this equation twice, leads to

Now we insert this expression into the equations (11) and (12) and obtain

Note that according to our assumptions we have . Combining those equations and rearranging terms results in

| (14) |

For define , then we have that , since , and for , which means that there exists a unique such that the equation is fulfilled.

Further it holds that if then . Namely if there would exist an such that then we would have

since the term on the left hand side of the inequality is strictly monotonically increasing in for all . But this is a contradiction to the assumption for . On top of this note that if or then we obtain that or respectively, which is in line with the former investigations.

Finally, it remains to prove that for this given there exists an such that

For this purpose we plug into this equation in order to work with the correct value for . We obtain that

since . On the other hand, if we let tend to infinity we get that

This holds true since

where

If we interpret as a function in and evaluate it in zero, we see that .

Using this and the continuity of we obtain that such that .

On top of this it even holds that , which implies that for all . Note that the denominator of is strictly positive.

Finally, since the limit is positive, there exists an such that , moreover note that since , if then . If there exists more than one such that this identity holds we decide to choose the smallest one, due to the shape of the function . At this point, for , we know there exists and such that the second order smooth fit conditions are fulfilled. Hence, the function

| (15) |

is twice continuously differentiable.

As a next step we have to make sure that indeed our constructed function solves the HJB-equation and is concave.

First of all we obtain that for the coefficients of it holds that and . This is valid, since if we plug the equation

into the equation and rearrange some terms, we obtain that , follows analogously. This directly implies that for all , together with we get that for all , and this together with yields that for all .

Furthermore, the first coefficient of satisfies that , since we can use the identity

in order to derive from the inequality that . Knowing that ,

we distinguish between the following cases, namely if then for all and this property together with yields that for all .

If , then for all , which implies that for all , since .

Now the concavity together with yields that for all .

Additionally, we can deduce that .

This can be shown as already done in Lemma 1, just by using the equation for in and exploiting that

, due to concavity and .

In the end, if we insert the function into the HJB-equation we obtain that for the first part of the HJB-equation is zero and the second part is less than zero. For the same holds true, since the supremum term in the first part is zero, because

holds true, for a , provided that , otherwise if the supremum part is also zero.

For we have to show that the second part of the HJB-equation is zero and the first part is less than zero.

For that reason we consider the function

We have to show that for all . We already know that and that the supremum part in is zero, since is linear for and . Furthermore, we use the properties of the coefficients of and . Together with the smooth fit conditions (11) and (12) we get, surprisingly nice,

In addition to that, we use the identity for given in (14) to obtain

| (16) |

Finally, this yields that for , which verifies that satisfies the first part of the HJB-equation for . Obviously, the function satisfies for and this shows that solves the second part of the HJB-equation. Overall, this means that the function specified in (15) solves the HJB-equation (1). ∎

3 Verification Theorem

Here we state a verification theorem which fits to our constructed function in (15).

Theorem 2.

Let be a positive solution to the HJB-equation

We set , if . Further let be concave, then

where

and .

Proof.

Let and be an admissible control strategy. In the following we will denote the state process depending on with and with for the sake of clarity. Because we want to make use of important theorems from stochastic calculus we have to switch to the right-continuous process, see also Shreve et al. [10, p. 60-62]. We consider the process

| (17) |

where . First of all we apply the integration by parts formula to the first part of and It’s formula for . We get

Moreover, we can split up the above sum of the discontinuous parts such that we obtain

As in [4, p. 19 - 20] with , we obtain for the sum belonging to the jumps of the dividend process the estimate

For the sums with comprising the other jumps we take expectations and use the compensation formula to get

and

Now, we exploit the results from above to obtain

Next we use that solves the HJB-equation

Adding on both sides and using the concavity of yields that

The last inequality yields that the process is a supermartingale. Now we use this property to obtain

where we exploited that . Considering the limit and using monotone convergence yields that

taking the supremum over all admissible strategies gives the desired result:

∎

Since for all parameter constellations our constructed functions are linked to an admissible strategy, are twice differentiable and concave, we have that they dominate the value function. Furthermore, using the band type strategy specified by we have that the corresponding from (17) is a martingale. Instead of using dominated convergence in the limitation procedure, one can even use bounded convergence, since and observe that .

Corollary 1.

If and , the function is the value function and the corresponding band type strategy is optimal.

4 Numerical illustration

In this concluding section we present a numerical example which nicely illustrates the dependence of the optimal strategy on the parameter .

For this purpose we have chosen the parameters as follows. Concerning the reserve process we take for the premium rate, for the intensity of the Poisson process corresponding to the claims, for the parameter of the exponential distribution of the claim size.

Furthermore, for the jump process we take , which corresponds to the expected arrivals of investors per time unit.

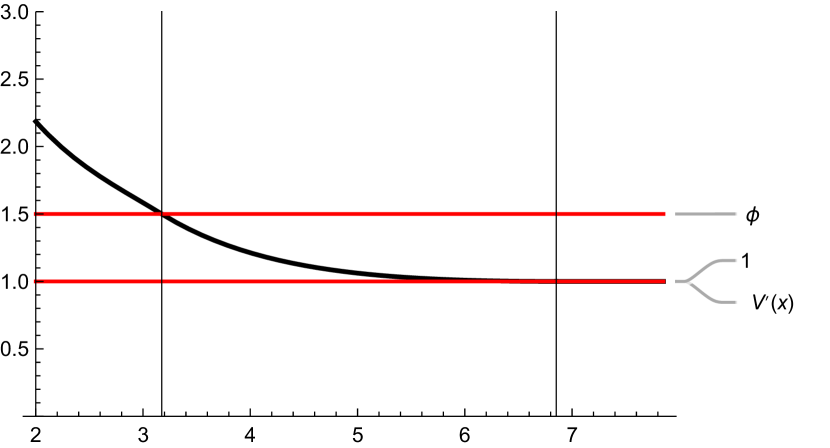

In terms of the interest rate we choose and in order to illustrate the value function and the smooth fit conditions we fix temporarily.

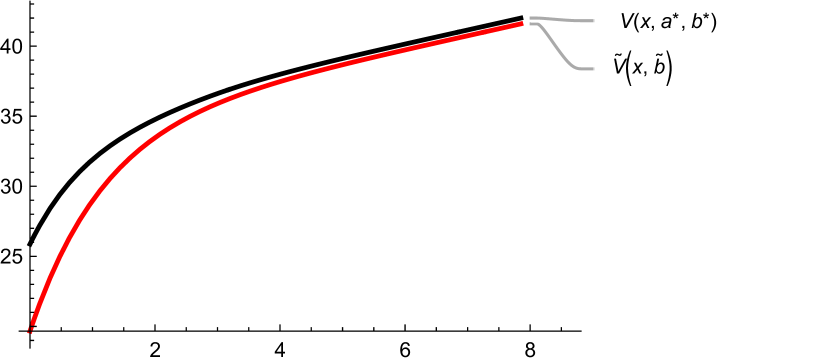

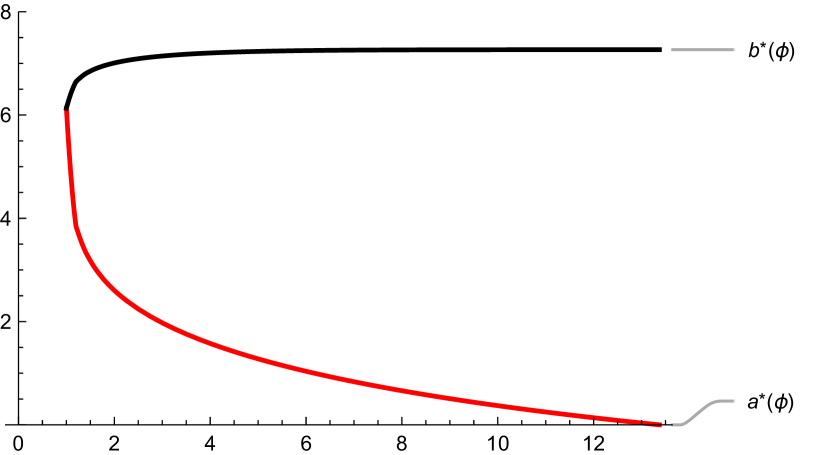

In Figure 4 we depict the difference between the value function of the usual dividend problem and the value function of the model with random capital supply with . Figure 4 illustrates how the transaction cost parameter affects the nature of the optimal strategy in terms of . As proved above, we observe that for the case the two thresholds and coincide. Further, if increases, the area where we search for additional funding shrinks exactly up to the certain point where it disappears.

This exactly happens at . Simultaneously, the dividend threshold is increasing in and reaches its maximum level at the point where becomes zero, namely, again if . We observe that the maximum level for is the dividend barrier level of the usual dividend problem.

On top of this we even see (and indeed proved) that for values of larger than the optimal strategy does not change anymore.

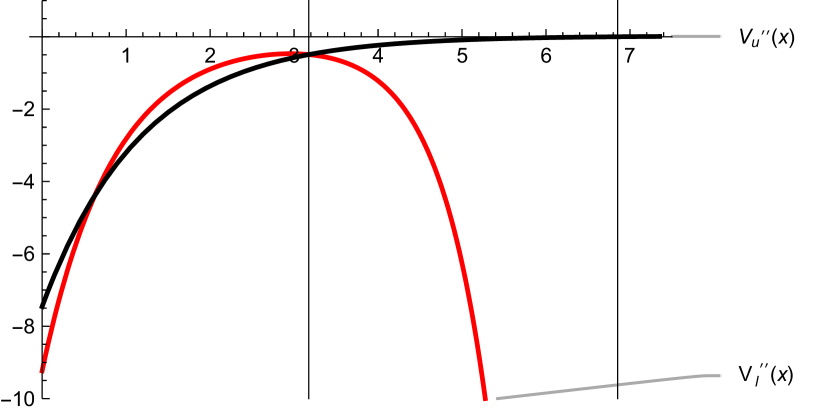

In the Figures 6 and 6 we illustrate the first and second order smooth fit property. In Figure 6 we plotted the first derivative of the value function to point out that at the lower optimal threshold we have , which is, according to our theoretical treatment, equivalent to the second order smooth fit condition. Further, at the upper optimal threshold we have that . Finally, Figure 6 shows the second derivative of the functions and and illustrates their behaviour in the respective domain of interest.

References

- [1] Albrecher, H., Cheung, E.C., Thonhauser, S.: Randomized observation periods for the compound poisson risk model: Dividends. ASTIN Bulletin 41(2), 645–672 (2011).

- [2] Azcue, P., Muler, N.: Optimal reinsurance and dividend distribution policies in the Cramér-Lundberg model. Math. Finance 15(2), 261–308 (2005).

- [3] Azcue, P., Muler, N.: Stochastic optimization in insurance. Springer Briefs in Quantitative Finance. Springer, New York (2014).

- [4] Azcue, P., Muller, N.: Optimal investment policy and dividend payment strategy in an insurance company. The Annals of Applied Probability 20(4), 1253 – 1302 (2010).

- [5] Gerber, H.U.: Entscheidungskriterien für den zusammengesetzten Poisson-Prozess. Schweiz. Aktuarver. Mitt. 69(2), 186–226 (1969).

- [6] Hugonnier, J., Malamud, S., Morellec, E.: Capital supply uncertainty, cash holdings, and, investment. The Review of Financial Studies 28(2), 391–445 (2015).

- [7] Kulenko, N., Hanspeter, S.: Optimal dividend strategies in a Cramér-Lundberg model with capital injections. Insurance Math. Econom. 43(2), 270–278 (2008).

- [8] Rolski, T., Schmidli, H., Schmidt, V., Teugels, J.L.: Stochastic Processes for Insurance and Finance. John Wiley & Sons, New York (1999).

- [9] Schmidli, H.: Stochastic control in insurance. Probability and its applications. Springer (2008).

- [10] Shreve, S.E., Lehoczky, J.P., Gaver, D.P.: Optimal consumption for general diffusions with absorbing and reflecting barriers. SIAM J. Control Optim. 22(1), 55–75 (1984).

- [11] Zhang, Z., Cheung, E.C., Yang, H.: On the compound Poisson risk model with periodic capital injections. ASTIN Bulletin 48(1), 435–477 (2018).