Optimal cleaning for singular values of cross-covariance matrices

Abstract.

We give a new algorithm for the estimation of the cross-covariance matrix of two large dimensional signals , in the context where the number of observations of the pair is large but and are not supposed to be small. In the asymptotic regime where are large, with high probability, this algorithm is optimal for the Frobenius norm among rotationally invariant estimators, i.e. estimators derived from the empirical estimator by cleaning the singular values, while letting singular vectors unchanged.

Key words and phrases:

Random matrices; Cross-covariance matrices; Rotationally Invariant Estimator2010 Mathematics Subject Classification:

60B20;62G05;15B521. Introduction

1.1. Context

In high-dimensional statistics, it is well known that the classical empirical estimator (i.e. the one based on an average over the sample) has little efficiency when the sample size is not much larger than the dimension of the object we want to estimate. For example, the spectrum of the empirical covariance matrix of a sample of independent observations of an -dimensional Gaussian signal with covariance is not concentrated in the neighborhood of when has the same order as , but distributed according to the Marchenko-Pastur law with parameter . In the same way, for a sample of observations of a pair of random vectors, the singular values of the empirical estimator

| (1) |

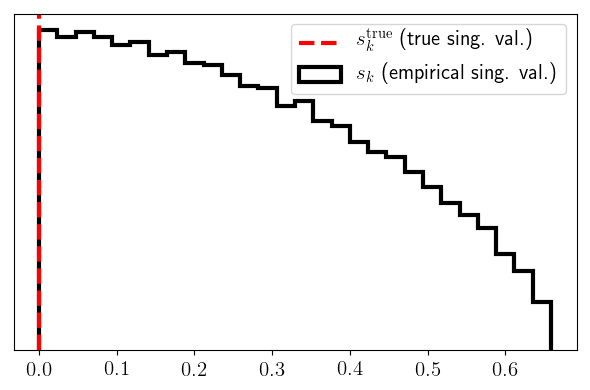

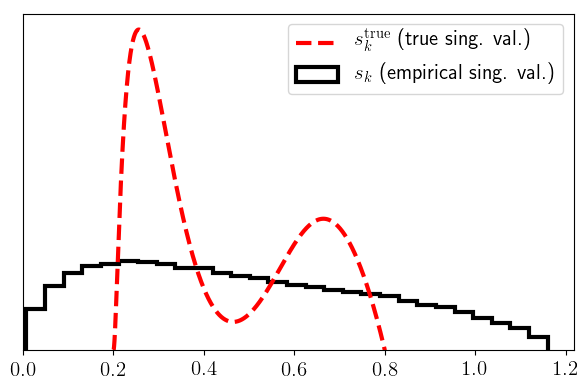

of the true cross-covariance matrix are not distributed as the singular values of the true cross-covariance matrix when is not large with respect to and (see Figure 1, where we plot both the true singular values density and the histogram of the empirical singular values).

In the case of covariance estimation, a problem of interest in finance [22, 24, 8, 9], several methods have been developed to circumvent these difficulties and improve the empirical estimator, based on regularization [13, 6, 15], shrinkage [23, 26, 25, 8, 9], specific sparsity or low-rank assumptions on the true covariance matrix [14, 19, 21, 20], robust statistics [11, 12] or fixed-point analysis [1].

However, the problem of the estimation of cross-covariance matrices has, to our knowledge, not been addressed so far, despite its numerous applications in various fields (see e.g. [7], where the null model is studied).

Of course, cross-covariance estimation can formally be considered as a sub-problem of covariance estimation, as any pair of random vectors can be concatenated in a vector whose covariance matrix has upper-right corner the cross-covariance of and . The problem with this idea is that the above covariance estimation methods rely on prior information on the structure of the covariance matrix: some of them are based on the hypothesis that the covariance matrix of is sparse or low-rank or essentially supported by a neighborhood of its diagonal and some others work in the Bayesian framework where the true covariance matrix of has been chosen at random with a prior distribution that is invariant under the action of the orthogonal group by conjugation (rotationally invariant estimators [26, 25]), which implies that the entries of can naturally be blended in linear combinations. This clearly does not make sense when and are of different nature, for example if contains commodity price returns and , say, weather data111The prices of lots of commodities (e.g. energy, agricultural products) indeed exhibit strong correlations with the weather.. However, an analogue notion exists for cross-covariance matrices, that we also call rotationally invariant estimators: estimators based on the empirical estimator from (1), modifying (we say cleaning) its singular values, but letting its singular vectors unchanged, i.e. estimators relevant to the Bayesian framework where the true cross-covariance matrix has been chosen at random, with a prior distribution that is invariant under the actions of the orthogonal groups by multiplication on the left and on the right.

1.2. Contents of the paper

1.2.1. Purpose

The purpose of this text is precisely to compute the optimal rotationally invariant estimator for the true cross-covariance in the regime where we have at disposal a large number of observations of the pair , but where and are not supposed to be small. It is optimal in the sense that for Gaussian data, for

the true cross-covariance of and , it is the solution of

| (2) |

among the estimators whose singular vectors are those of the empirical estimator given at (1) above. Here, denotes the Frobenius norm , i.e. the standard Euclidean norm on matrices:

| (3) |

Let us introduce the SVD of the empirical estimator from (1):

with the singular values and (resp. ) the left (resp. right) singular vectors. One easily gets (see (13) below) that optimality rewrites

| (4) |

The numbers

called oracle estimates, are of course unknown, and the main problem is to estimate them. Rather than computing them directly, we shall introduce, at (11), a function (), which allows to estimate them (at least their weighted averages, which is enough for our purpose). The function is called the oracle function for a reason explained below (see Proposition 2.1 and right above it) and is estimated in terms of observable variables (Theorems 2.3 and 2.5).

Note that the optimality of the matrix estimator does not imply that as the dimensions tend to infinity, the numbers tend to zero (see (24) and Proposition 2.9). The reason is that the optimal matrix estimator keeping empirical singular vectors unchanged takes into account the fact that these vectors are noisy versions of the true ones, hence reduces their weights by shrinking the singular values.

1.2.2. Main contributions

The main contributions of the paper are the following ones:

-

•

In Proposition 2.1, we express our oracle estimates in terms of the observable function and of the unobservable function (called oracle function ) .

-

•

The main achievement of the paper is then to provide an approximation of our oracle function defined at (11) in terms of observable variables (Theorems 2.3 and 2.5). The proofs, given in Section 4, are based on classical concentration results (Proposition 5.3) and on long computations starting from the Stein formula for Gaussian random vectors (Proposition 5.1). This approach is completely different from the one of the proofs of the Ledoit-Péché paper [26] (where an analogue estimator for covariance matrices was proposed) and, incidentally, allows to recover the main formula of [26] very directly (see [3]).

Remark 1.1.

One of the advantages of the proofs of Ledoit-Péché’s paper is that they do not rely on any Gaussian hypothesis. One can then wonder whether the method of the present paper (and its main results) could be extended beyond the Gaussian framework. It happens that the Stein formula can be generalized, with an error term, beyond Gaussian variables (see e.g. [5, Lem. 1.13.9]) and that even though we did not include it here for brevity, we checked that the main lines of the proof still work under much more general assumptions (including of course the fact that is centered, has covariance and moments up to a reasonable order).

-

•

We provide precise, presumably close to sharp, error terms for the approximation of the oracle function, which, contrarily to [26], do not rely on convergence hypotheses for empirical spectral distributions and are controlled by very few quantities.

-

•

In Section 3, devoted to numerical simulations, we assess and illustrate algorithm accuracy by comparing it with the empirical estimator and the upper-right corner of Ledoit-Péché’s estimator for a quite diversified set of models, which is not at all restricted to the invariance class this estimator was thought for (i.e. the one described (36)). For all the models we simulate, our algorithm outperforms (most times by far) both other algorithms in the sense that its output is closer to the true cross-covariance matrix, for the Frobenius norm as well as for the operator norm (see Tables 1 and 2). The python code for the numerical simulations of this paper is available at https://github.com/CFMTech/Optimal_cleaning_for_singular_values_of_cross-covariance_matrices

-

•

In Section 2.5, we provide an interpretation of the bias in the optimal cleaning procedure (i.e. of the lack of convergence of as estimator of ) in terms of the overfitting factor of the estimator, out of , of a certain projection of .

1.3. Notations

Throughout this text, for a matrix, denotes the transpose of . For a random variable, denotes the expectation of .

Here, error terms in approximations depend on the parameters , , and of the problem, on the complex number and on the randomness. We will suppose that , , the operator norm of and are bounded by a constant and use the notation

for error terms with the following definition: for a complex random variable depending on , we write if there exists depending only on such that , i.e. if is Sub-Gaussian222Definition and basic properties of Sub-Gaussian variables can be found in [27, Sec. 2.5]. with Sub-Gaussian norm controlled by .

2. Main results and Algorithms

2.1. Model

Let and let be a pair of (column) random vectors333We suppose that to avoid spurious null eigenvalues for the matrix . such that

for a given symmetric and non negative definite.

We are interested in the estimation of the true cross-covariance matrix

out of its empirical version

| (5) |

where

| (6) |

are defined thanks to a sequence

| (7) |

of independent copies of .

More precisely, we are looking for a Rotationally Invariant Estimator of , i.e. an estimator deduced from the estimator from (5) by changing (following other papers on close questions, we say cleaning) its singular values but not changing its singular vectors, so that for any orthogonal matrices, if and are respectively changed into and , then is changed into .

Let us introduce the SVD of . We set

| (8) |

for some and two orthonormal column vectors systems , and .

Thus our estimator will have the form

and the cleaned singular values

| (9) |

will be considered optimal when solving the optimization problem

| (10) |

where the Frobenius norm has been defined at (3). Let us introduce the (implicitly depending on ) random variables

| (11) |

for (resp. , that we shall also use below) the resolvent, estimated at , of (resp. of ) defined through

| (12) |

Note that can be computed with the observed data, so that by (14) bellow, the function is all one needs to compute the cleaned singular values . For this reason, it is called the oracle function.

Proposition 2.1.

Remark 2.2 (Impact of a error on ).

Equation (14) provides us with an exact formula for , that, once an explicit approximation for the function obtained, we shall convert into an approximate formula for in (20). One can wonder what the effect of this approximation is on the optimality (in Frobenius norm, with asymptotic probability tending to one) of estimator . We are thus interested in the matrix error term

The question is: How small must the errors be for the matrix error term above to be negligible with respect to the true cross-covariance matrix for the Frobenius norm? Given and are orthogonal matrices, the Frobenius norm of the matrix error term is

Under the sole hypothesis that the operator norm of is bounded by the constant , the Frobenius norm of has order a priori so that the error on is negligible as soon as

Regimes where the actual Frobenius norm of has lower order (e.g. when is simply null) have to be the object of specific studies.

2.2. Estimations of the oracle function

The problem with Formula (13) is that while the function is explicit from the data , the definition of the function involves the unknown true cross-covariance matrix . In Theorems 2.3 and 2.5, we give asymptotic approximations of that can be estimated from the data alone, as is the case of the Ledoit-Péché estimator for covariance matrices [26].

Let us introduce the random variables

| (15) |

for , as in (12) and the empirical covariance matrices of and defined by

| (16) |

The following result makes the function of (11) explicit from the data alone, allowing a practical implementation of Formula (13) for the RIE.

Theorem 2.3 (Oracle function estimation I).

The function of (11) satisfies

| (17) |

Remark 2.4 (Case where ).

In the case where, as tends to infinity, and stay bounded, it can easily be seen that , so that

Indeed, the estimate follows for example from the formulas (true for large ):

and from standard complex analysis.

In the particular case where the covariance matrices of and are both identity matrices, is in fact an estimator of the cross-correlation matrix of and , and (13) can be simplified into (19), a formula leading to an algorithm with lower computational complexity (see Remark 2.8). For , let

| (18) |

Theorem 2.5 (Oracle function estimation II).

Suppose that the true covariance matrices of and are respectively and . Then, the function of (11) satisfies

| (19) |

for the analytic version of the square root on with value at .

2.3. Algorithmic consequences

Formula (13) gives an expression for the cleaned singular values of the cross-covariance matrix, i.e. for the RIE of this matrix. The function is explicit from the data , as well as the approximation of given by formulas (17) and (19) above. Choosing for the ”small ” (and using the formula , for as in (15)) leads to the explicit implementation formula

| (20) |

Remark 2.6.

As explained in Remark 2.2, we need the error (squared, and averaged over ) to be , so that with the error terms of (17) and (19), we should have slightly increased the imaginary part of in (20), to have large. It happens that in practice, the algorithms below work well with as imaginary part of . In fact, we believe that, following the method developed by Erdős, Yau and co-authors (see e.g. [16, 17, 5]), our local laws in Theorems 2.3 and 2.5 can be improved roughly up to the scale , i.e. that the error terms, in (17) and (19), are in fact controlled essentially by . This conjecture has been tested in Section 3.1 (see the caption of Figure 4).

Using the approximation of given by formula (17), we get the first algorithm below, whose complexity is kept reasonable thanks to the following. With

| (21) |

the SVD of , where the orthonormal system of is completed to an orthonormal basis , we have

| (22) |

for

| (23) |

so that the functions , , and from (15) can be computed without any matrix inversion (nor any matrix product) once the SVD of has been computed, which has only to be done once in the algorithm.

Algorithm 1: Optimal cleaning for cross-covariance matrices

Input: , with .

Output: cleaned singular values .

-

(1)

Compute , ,

-

(2)

Compute the SVD of

-

(3)

Compute the vectors and and the number using (23)

-

(4)

For each ,

-

•

set for the -th singular value of

-

•

compute , , using (22)

-

•

compute and

-

•

compute

-

•

-

(5)

possibly: apply the isotonic regression algorithm to the

One can also write an algorithm based on (19) instead of (17), with slightly lower computational complexity, but only works when the true covariance matrices of and are both identities (which can be the case in practice, when the associated data has been made standard in a preprocessing):

Algorithm 2: Optimal cleaning for cross-correlation of signals with identity covariance matrix

Input: singular values of for , .

Output: cleaned singular values .

For each ,

-

(1)

set

-

(2)

compute

and

-

(3)

compute

-

(4)

possibly: apply the isotonic regression algorithm to the

Remark 2.7.

Ledoit-Péché’s RIE is not working when the ratio of the signal size by the sample size is too close to 1 because its formula involves a division by . No such singularity appears here.

Remark 2.8 (Compared computational complexities of Algorithms 1 and 2).

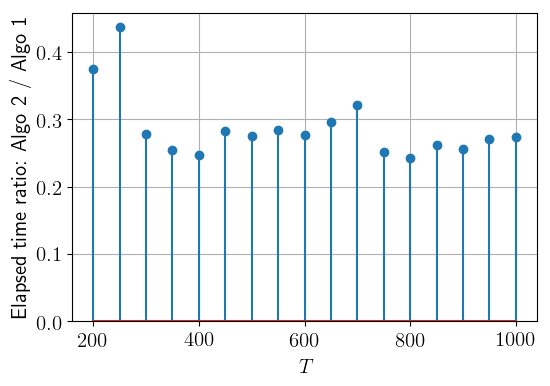

Using the classical linear algebra operations computational complexity estimates (multiplication, inversion and singular value decomposition of matrices have complexity), we see that both algorithms have complexities . That being said, Algorithm 2 involves less matrix multiplications than Algorithm 1, given it does not use the numbers defined at (23). It follows that when both algorithms apply, Algorithm 2 needs less computation time, as Figure 2 illustrates.

2.4. Cleaned vs empirical vs true singular values: some exact formulas

As explained above in Section 1.2, due to the unavoidable error in the singular vectors, the fact that our estimator realizes the optimal of (2) does not imply that the cleaned singular values should be close to the true ones. Precisely, we show in Proposition 2.9 that on average,

| (24) |

for the true singular values (the left inequality being conditional to ).

An analogous phenomenon for rotationally invariant estimators of covariance matrices is explained in [9, Section 6.3].

Proposition 2.9.

Let (resp. ) denote the eigenvalues of the true covariance matrix of (resp. ) and let , denote the empirical covariance matrices of and from (16). Then the following equations hold:

| (25) |

| (26) |

and

| (27) |

2.5. Interpretation of the cleaning in terms of overfitting

Overfitting is a very common issue in machine learning. It refers to the problem that any model is fitted, in sample, on noisy data, which can degrade its out of sample performance if the fit has been significantly impacted by the random specificity of the noise. In this section, we relate the cleaning procedure to this problem, proving that in some contexts,

Suppose to be given a sample

of observations of a pair of vectors, where is a collection of factors thanks to which we want to explain .

Given this set of observations, if we observe an “out-of-sample” (oos) realization of the factors, a natural predictor444This predictor, a matched-filter, corresponds to the normalized Ridge predictor with large (namely the large limit of [18, Eq. (3.47)] times ). We could also consider the OLS predictor, but notations are lighter this way. of the corresponding is given by

where is the SVD of the in-sample cross-covariance matrix

Each term of the previous sum defines a partial predictor555Note that we do not name this an estimator but a predictor: the purpose of is not to approximate the better but to exhibit a positive alignment with . This kind of object is widely used in finance (see Remark 2.11), where for various reasons (risk aversion, volatility, liquidity, crowding, better predictability), an investor mights want to focus on some specific directions in the market.

Let us now focus on the overlap of these predictors with the true values of .

Out of sample overlap: it is given by

Over the out-of-sample time series

it averages out to the mean out of sample overlap given by

for

By (4) and the concentration of measure Lemma 4.7, we get

| (28) |

In sample overlap: it is given, at each date of the sample, by

which, by (4), averages out, in sample, to the mean in sample overlap given by

| (29) |

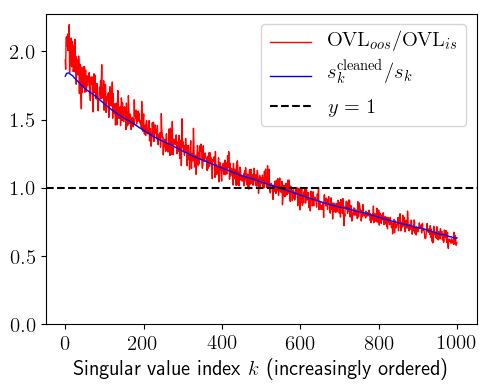

Out of sample / in sample: From (28) and (29), we deduce the following nice relation between the overfitting and the cleaning, illustrated at Figure 3:

| (30) |

Remark 2.10.

If, instead of considering the partial predictor , we consider sums, over , of such predictors, then the previous ratio can still be expressed thanks to the numbers and .

Remark 2.11 (Investment strategies interpretation).

In the case where is the vector of returns of a collection of financial assets and a collection of factors we want to build an investment strategy on, the vectors

(as well as linear combinations of such vectors) correspond to portfolios constructed thanks to the factors : each component of is the (positive or negative) amount of money invested in the corresponding asset. In this context, the out-of-sample overlaps

are simply be the realized gains of these strategies, whereas the mean in-sample overlaps are the predicted gains of these strategies.

Of course, realized gains are usually different, even on average, from predicted gains. This phenomenon can be seen as a consequence of overfitting (or in-sample bias). For the simple model presented in this section, (30) relates their ratio to the singular values cleaning procedure via the formula:

3. Numerical simulations

3.1. Oracle estimation

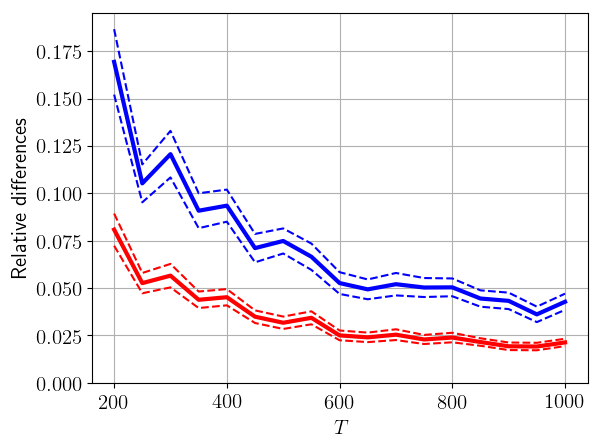

The cornerstones of this work are (17) and (19) from Theorems 2.3 and 2.5: these formulas allow us to approximate the (unknown) oracle function by some functions that are explicit from the data. We conducted numerical simulations to verify these formulas for various models (i.e. various choices of ), all confirming their accuracy. In Figure 4, we present the relative differences

| (31) |

and

| (32) |

for

| (33) |

with a matrix with singular values distributed according to the bi-modal density from the right graph in Figure 1 and independent, Haar-distributed, left and right singular vectors, independent from the singular values. We see that both approximations of are very efficient and that the approximation of given at (17) is slightly better, which is confirmed by other simulations.

3.2. Effect of cleaning

In Figure 5 and Figure 6, we show the effect of cleaning in the simulations from Figure 1. In the two graphs of Figure 6, we observe that for most values of (all but the smallest ones), we have , as stated informally in (24). The histograms of the right graph of Figure 5 show the same, with less precision for the set of ’s for which this is true.

3.3. Compared performance with empirical and Ledoit-Péché’s estimators

3.3.1. Numerical simulations

We have implemented Algorithms 1 and 2 from the present paper666Both give approximately the same result when and have identity covariance matrices, so we shall focus on Algorithm 1 in this section. for various models, i.e. various choices of the true total covariance matrix such that

We then compared their performance to that of the empirical estimator , thanks to the relative distances

| (34) |

where denotes the estimator of obtained with Algorithm 1 and where denotes the operator norm777Our algorithm is optimal, in the sense given in this paper, for the Frobenius norm, but the operator norm of the error is of course also interesting.. We also compared with the upper-right corner of Ledoit-Péché’s estimator of the total covariance matrix (the estimator from [26], which assumes -invariance), thanks to the relative distances

| (35) |

The values of the quotients from (34) and (35) are reported in Table 1 and 2 (and discussed in Section 3.3.2 below) for the following models, all with for , and :

-

•

Models (1) to (5):

where and has:

-

–

independent Haar-distributed left and right singular vectors,

-

–

0%, 10%, 20%, 30% or 40% (for respectively Model (1)888Model (1) corresponds in fact the null case from Figures 1 and 5 even if , given it can easily be seen that if or is multiplied by a positive constant, then the outputs from our algorithms are also multiplied by this constant.,…, Model (5)) of non zero singular values, distributed uniformly in (and independent of the singular vectors),

so that .

-

–

-

•

Models (6) to (10): for an matrix with i.i.d. entries with common law , which is either the standard Gaussian law (Model (6)) or a symmetric heavy-tailed distribution with exponent (specifically the symmetric law such that for any ), with , , , for Models (7), (8), (9), (10) respectively.

-

•

For Models (11), , (15), use the block decomposition

of the matrix of respectively Model (6), , (10) and replace the covariance matrices and of and by respectively and , where denotes the largest singular value of .

| Model | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Algo/Empirical | 0.01 0.00004 | 0.19 0.00001 | 0.26 0.00001 | 0.31 0.00001 | 0.35 0.00001 |

| Algo/Ledoit-Péché | 0.02 0.00013 | 0.53 0.00003 | 0.67 0.00003 | 0.75 0.00003 | 0.80 0.00002 |

| Model | (6) | (7) | (8) | (9) | (10) |

|---|---|---|---|---|---|

| Algo/Empirical | 0.56 0.00003 | 0.56 0.00003 | 0.57 0.00031 | 0.47 0.00682 | 0.01 0.00152 |

| Algo/Ledoit-Péché | 0.95 0.00002 | 0.94 0.00004 | 0.85 0.00058 | 0.35 0.00533 | 0.01 0.00152 |

| Model | (11) | (12) | (13) | (14) | (15) |

|---|---|---|---|---|---|

| Algo/Empirical | 0.53 0.00006 | 0.53 0.00006 | 0.32 0.00180 | 0.10 0.00062 | 0.07 0.00018 |

| Algo/Ledoit-Péché | 0.97 0.00008 | 0.96 0.00009 | 0.54 0.00392 | 0.01 0.00017 | 0.00 0.00003 |

| Model | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Algo/Empirical | 0.01 0.00009 | 0.39 0.00009 | 0.38 0.00009 | 0.37 0.00008 | 0.36 0.00009 |

| Algo/Ledoit-Péché | 0.04 0.00028 | 0.96 0.00022 | 0.92 0.00017 | 0.88 0.00017 | 0.86 0.00014 |

| Model | (6) | (7) | (8) | (9) | (10) |

|---|---|---|---|---|---|

| Algo/Empirical | 0.46 0.00014 | 0.46 0.00014 | 0.58 0.00217 | 0.50 0.01145 | 0.02 0.00185 |

| Algo/Ledoit-Péché | 0.97 0.00012 | 0.95 0.00035 | 0.75 0.00247 | 0.43 0.01058 | 0.02 0.00188 |

| Model | (11) | (12) | (13) | (14) | (15) |

|---|---|---|---|---|---|

| Algo/Empirical | 0.45 0.00011 | 0.45 0.00011 | 0.52 0.00050 | 0.58 0.00010 | 0.58 0.00010 |

| Algo/Ledoit-Péché | 0.97 0.00017 | 0.97 0.00017 | 0.53 0.00355 | 0.01 0.00013 | 0.00 0.00005 |

3.3.2. Comments

On the examples from Tables 1 and 2, our estimator always outperforms the empirical estimator by far, for the Frobenius norm as well as the operator norm.

For most of these examples, our estimator also outperforms significantly the upper-right corner of Ledoit-Péché’s estimator for both norms.

Two factors seem to increase the advantage of our estimator over the two other ones considered here:

-

•

Bayesian models with prior distributions of the true total covariance matrix invariant under the action of defined by

(36) (i.e. Models (1) to (5)) are better fitted for our estimator than others, even the -invariant Bayesian models (case of Model (6)).

-

•

The sparser the true cross-covariance of a model, the higher our advantage over the two other algorithms: Models (7), (8), (9), (10) (or (12), (13), (14), (15)) are increasingly sparse (in the sense that a small part of the entries of contains most of its total mass). Also, the set of singular values of for Models (1) to (5) are decreasingly sparse.

Remark 3.2.

The -invariance from (36) implies that the singular vectors of are Haar-distributed, but does not imply that the singular vectors of are independent from the other observables (e.g. the eigenvectors of and ), hence does not define Bayesian models where the right way to estimate is necessarily rotationally invariant999Bayesian models where the right way to estimate is necessarily rotationally invariant are those with prior distribution on invariant under the action of defined by .. This means that for Models (1) to (5), our estimator could be sub-optimal, and a cleaning of the singular vectors, based e.g. on the observation of the eigenvectors of and , should possibly also be performed.

4. Proofs

4.1. Proof of Proposition 2.1

Proposition 2.1 follows directly from both following claims.

Claim 1. The solution of the optimization problem (10) is given by

| (37) |

Claim 2. For any ,

Proof of Claim 1. Let be a orthogonal matrix with the same first columns as the matrix with orthogonal columns . Then

and, given the Frobenius norm is invariant by left and right multiplication by orthogonal matrices, the optimization problem (10) rewrites

i.e.

| (38) |

As the squared Frobenius norm of a matrix is simply the sum its squared entries, the solution of (38) is given by the diagonal entries of , i.e. by (37) .

Remark 4.1.

The two keys to prove Claim 1, first the invariance of the Frobenius norm under the left and right actions of the orthogonal group and second the fact that for any matrix , the diagonal matrix the closest to for the Frobenius norm is the diagonal matrix with the same diagonal entries as , are, together, specific to the Frobenius norm (at least among classical matrix norms). This is the reason why extending our results to other classical norms, such as the operator norm, has so far remained out of reach. That being said, simulations (see Table 2) show that though possibly not optimal for the operator norm, using our estimator also makes sense (at least when compared to the empirical estimator) when the error is measured with this norm.

Proof of Claim 2. The of (37) can be expressed as the Radon-Nikodym derivative

| (39) |

for the null mass signed measure

| (40) |

and the symetrized empirical singular values distribution of , defined by

| (41) |

4.2. Proof of Theorem 2.3

Let us introduce the implicitly depending on random variables

| (45) |

Set

The following concentration of measure lemma can be proved using the Log-Sobolev inequality satisfied by the standard Gaussian law (a detailed proof is given in Section 4.6.1).

Lemma 4.2.

There is a constant , depending only on the bound of the hypothesis, such that for any , we have, for any ,

In other words, is a Sub-Gaussian random variable, with Sub-Gaussian norm

Besides, the same is true for any of the random variables , , , , , .

By this lemma, using the decomposition

it suffices to prove that

| (46) |

Then, the key of the proof is the following proposition, whose proof, based on the multidimensional Stein formula for Gaussian vectors, is postponed to Section 4.4.

Proposition 4.3.

We have

| (47) | ||||

| (48) | ||||

| (49) |

4.3. Proof of Theorem 2.5

In the case where and , the random variables and from (45) are respectively equal to and , and rather than using (50) to estimate , we shall solve (47) without using and . Using (48) and (49), after multiplication by , (47) rewrites

for . For , we get

| (51) |

where we have used the fact, following from lemma 4.2, Cauchy-Schwarz inequality and first part of Proposition 5.3, that

Second order polynomial equation (51) solves as

Considering the case where and are small (where we should have , as explained in Remark 2.4) and using analytic continuation, we have

| (52) |

for the analytic version of the square root on with value at . Then, again, conclude using Lemma 4.2.

4.4. Proof of Proposition 4.3

4.4.1. Proof of (47): expansion of

Using , we have

| (53) | |||||

for

| (54) |

By (76) from Corollary 5.2, it follows that

| (55) | |||

To distinguish between the components of (the first ones) and the components (the last ones), we shall now rewrite the above sum as follows: for any ,

where the ’s denote the (column) vectors of the canonical basis of .

Let us now introduce the matrix

| (57) |

Note that for any integer, for we have

so that for large enough,

| (58) | |||||

which is true for all , by analytic continuation.

Lemma 4.4.

For any , we have, for ,

for the -th (column) vector of the canonical basis in and we have, for ,

for the -th (column) vector of the canonical basis in

Proof.

We want to compute the derivatives, at fixed, of the function

The differential of the function at the matrix is the operator

the differential of the function at the matrix is the operator

hence the differential of the function at the matrix is the operator

Besides, at fixed, the differential of the function at is the operator

so that the differential of the function at is the operator

It follows that at fixed, the differential of the function at is the operator

The conclusion follows. ∎

We deduce that

By (58),

Thus

Then, it is easy to see, by (58), that computing

amounts to take the same formula and change into . After, adding both and dividing by amounts to keep only, in the previous formula, the terms which are even in (and divide by ). We get

| (59) |

In the same way,

| (60) |

Let us write

4.4.2. Proof of (48): expansion of

4.4.3. Proof of (49): expansion of

4.5. Proof of Proposition 2.9

4.5.1. Proof of (25)

A simple application of equality from (13) gives:

4.5.2. Proof of (26) and (27)

We start with the following Gaussian integrals:

Lemma 4.5.

Let , and let be a matrix whose entries are independent standard Gaussian variables. Then we have

| (66) |

and

| (67) |

Proof.

We have

Using then the fact that the entries of are even and independent, we get

In the same way,

and using again the fact that the entries of are even and independent, we get

∎

Lemma 4.6.

We have

and

4.6. Proof of concentration results

4.6.1. Proof of Lemma 4.2

With the notation of the proof of Lemma 4.6, by the second part of Proposition 5.3, what we have to prove is that the functions mapping to the variables are all Lipschitz for the Frobenius norm from (3) on , with Lipschitz constant

As this argument is quite standard (close to e.g. [2, Sec. 2.3.1] or [10, Lem. 7.1] with [4, Lem. B.2] instead of [10, Lem. A.2]), we only give the main lines. Consider a variation of , and then:

-

(1)

Use (68).

-

(2)

Use the resolvant formula: for all square matrices ,

to expand the variations of the matrices and at first order in .

-

(3)

By non-commutative Hölder inequalities (see e.g. [2, Appendix A.3]), for any product of matrices with any size and any ,

where denotes the operator norm. This has to be used with the fact that and have operator norms .

-

(4)

On any square matrices space endowed with the Frobenius norm, the trace is the scalar product with the identity matrix, hence is Lipschitz with Lipschitz constant the Frobenius norm of the identity matrix (which depends on the dimension).

4.6.2. Concentration lemma for Section 2.5

Lemma 4.7.

With the notation from Section 2.1, for any deterministic vectors , , the random variable is centered with -norm .

Remark 4.8.

Using Hanson-Wright inequality [27], one could improve the variance control up to an exponential control on the tail.

5. Appendix

5.1. Stieltjes transform inversion

Any signed measure on can be recovered out of its Stieltjes transform

| (70) |

by the formula

| (71) |

where the limit holds in the weak topology (see e.g. [2, Th. 2.4.3] and use the decomposition of any signed measure as a difference of finite positive measures).

Note that for any and any , we have

so that for and , the Stieltjes transforms of the measures and rewrite

| (72) |

and

| (73) |

5.2. Linear algebra

We notify some formulas frequently used (and referred to) here: for a collection of column vectors defining an orthonormal basis, for any matrices ,

| (74) |

and for any column vectors ,

| (75) |

5.3. Stein formula for Gaussian random vectors

Proposition 5.1.

Let be a centered Gaussian vector with covariance and be a function with derivatives having at most polynomial growth. Then for all ,

(see e.g. [4, Lem. A.1])

Corollary 5.2.

With the same notation, considering as a column vector, for a matrix-valued function, we have

| (76) |

Proof.

5.4. Concentration of measure for Gaussian vectors

Proposition 5.3.

Let be a standard real Gaussian vector and be a function with gradient . Then we have

| (77) |

where denotes the standard Euclidean norm.

Besides, if is -Lipschitz, then for any , we have

| (78) |

i.e. is Sub-Gaussian with Sub-Gaussian norm , up to a universal constant factor.

References

- [1] Amsalu, S., Duan, J., Matzinger, H., Popescu, I. Recovery of spectrum from estimated covariance matrices and statistical kernels for machine learning and big data, arXiv.

- [2] Anderson, G., Guionnet, A., Zeitouni, O. An Introduction to Random Matrices. Cambridge Studies in Advanced Mathematics, 118 (2009).

- [3] Benaych-Georges, F. A very short proof of Ledoit-Péché’s RIE formula for covariance matrices. Unpublished note available at http://www.cmapx.polytechnique.fr/~benaych/Short_proof_of_Ledoit_Peche.pdf

- [4] Benaych-Georges, F., Couillet, R. Spectral analysis of the Gram matrix of mixture models, ESAIM Probab. Statist., Vol. 20 (2016), 217–237.

- [5] Benaych-Georges, F., Knowles, A. Local semicircle law for Wigner matrices. Advanced topics in random matrices, 1–90, Panor. Synthèses, 53, Soc. Math. France, Paris, 2017.

- [6] Bose, A., Bhattacharjee, M. Large Covariance and Autocovariance Matrices, 2018, Chapman and Hall/CRC.

- [7] Bouchaud, J.-P., Laloux, L., Miceli, M.A., Potters M. Large dimension forecasting models and random singular value spectra, Eur. Phys. J. B (2007) 55: 201.

- [8] Bun, J., Bouchaud, J.-P., Potters, M. Cleaning correlation matrices, Risk magazine, 2016.

- [9] Bun, J., Bouchaud, J.-P., Potters, M. Cleaning large correlation matrices: Tools from Random Matrix Theory, Physics Reports Volume 666, Review article, 1–109, 2017.

- [10] Capitaine, M. Additive/multiplicative free subordination property and limiting eigenvectors of spiked additive deformations of Wigner matrices and spiked sample covariance matrices. J. Theoret. Probab. 26 (2013), no. 3, 595–648.

- [11] Couillet, R., Pascal, F., Silverstein, J., Robust estimates of covariance matrices in the large dimensional regime. IEEE Trans. Inform. Theory 60 (2014), no. 11, 7269–7278.

- [12] Couillet, R., Pascal, F., Silverstein, J., The random matrix regime of Maronna’s M-estimator with elliptically distributed samples. J. Multivariate Anal. 139 (2015), 56–78.

- [13] El Karoui, N. Spectrum estimation for large dimensional covariance matrices using random matrix theory. Annals of Statistics, 2008, 36(6):2757–2790.

- [14] El Karoui, N. Operator norm consistent estimation of large dimensional sparse covariance matrices, Annals of Statistics, 2008, 36(6): 2717–2756

- [15] El Karoui, N. Random matrices and high-dimensional statistics: beyond covariance matrices. Proceedings of the International Congress of Mathematicians, 2018.

- [16] Erdős, L., Schlein, B., Yau, H.-T. Semicircle law on short scales and delocalization of eigenvectors for Wigner random matrices. Ann. Probab. 37 (2009), no. 3, 815–852.

- [17] Erdős, L., Yau, H.-T. A dynamical approach to random matrix theory. Courant Lecture Notes in Mathematics, 28, New York; American Mathematical Society, Providence, RI, 2017.

- [18] Tibshirani, R., Hastie, T. Friedman, J. Elements of Statistical Learning Second Edition, Print 10. Springer Series in Statistics, 2008.

- [19] Klopp, O., Lounici, K., Tsybakov, A. B. Robust matrix completion. Probab. Theory Related Fields 169 (2017), no. 1–2, 523–564.

- [20] Klopp, O., Y. Lu, A. Tsybakov, A. B., Zhou, H. Structured Matrix Estimation and Completion, Bernoulli 25 (4B), 2019, 3883–3911 (2019).

- [21] Koltchinskii, V., Lounici, K., Tsybakov, A. B. Estimation of low-rank covariance function, Stochastic Process. Appl. 126 (2016), no. 12, 3952–3967.

- [22] Laloux, L., Cizeau, P., Bouchaud, J.-P., Potters, M. Noise Dressing of Financial Correlation Matrices, Phys. Rev. Lett. 83, 1467, 1999.

- [23] Ledoit, O., Wolf, M. A well-conditioned estimator for large-dimensional covariance matrices, Journal of Multivariate Analysis 88, 2004, 365–411.

- [24] Ledoit, O., Wolf, M. Honey, I shrunk the sample covariance matrix. Journal of Portfolio Management, 30, Volume 4, 2004, 110–119.

- [25] Ledoit, O., Wolf, M. Nonlinear shrinkage estimation of large-dimensional covariance matrices. Annals of Statistics 40, 2012, 1024–1060.

- [26] Ledoit, O., Péché, S. Eigenvectors of some large sample covariance matrix ensembles Probability Theory and Related Fields, 2011, 151.1, 233–264

- [27] Vershynin, R. High-Dimensional Probability: An Introduction with Applications in Data Science, Cambridge Series in Statistical and Probabilistic Mathematics, 2018.