Achim Ahrens

The Economic and Social Research Institute

Dublin, Ireland

achim.ahrens@esri.ie

and Christian B. Hansen

University of Chicago

christian.hansen@chicagobooth.edu

and Mark E. Schaffer

Heriot-Watt University

Edinburgh, United Kingdom

m.e.schaffer@hw.ac.uk

lassopack: Model selection and prediction with regularized regression in Stata

Abstract

This article introduces lassopack, a suite of programs for regularized regression in Stata. lassopack implements lasso, square-root lasso, elastic net, ridge regression, adaptive lasso and post-estimation OLS. The methods are suitable for the high-dimensional setting where the number of predictors may be large and possibly greater than the number of observations, . We offer three different approaches for selecting the penalization (‘tuning’) parameters: information criteria (implemented in lasso2), -fold cross-validation and -step ahead rolling cross-validation for cross-section, panel and time-series data (cvlasso), and theory-driven (‘rigorous’) penalization for the lasso and square-root lasso for cross-section and panel data (rlasso). We discuss the theoretical framework and practical considerations for each approach. We also present Monte Carlo results to compare the performance of the penalization approaches.

keywords:

lasso2, cvlasso, rlasso, lasso, elastic net, square-root lasso, cross-validation1 Introduction

Machine learning is attracting increasing attention across a wide range of scientific disciplines. Recent surveys explore how machine learning methods can be utilized in economics and applied econometrics (Varian, 2014; Mullainathan and Spiess, 2017; Athey, 2017; Kleinberg et al., 2018). At the same time, Stata offers to date only a limited set of machine learning tools. lassopack is an attempt to fill this gap by providing easy-to-use and flexible methods for regularized regression in Stata.111This article refers to version 1.2 of lassopack released on the 15th of January, 2019. For additional information and data files, see https://statalasso.github.io/.

While regularized linear regression is only one of many methods in the toolbox of machine learning, it has some properties that make it attractive for empirical research. To begin with, it is a straightforward extension of linear regression. Just like ordinary least squares (OLS), regularized linear regression minimizes the sum of squared deviations between observed and model predicted values, but imposes a regularization penalty aimed at limiting model complexity. The most popular regularized regression method is the lasso—which this package is named after—introduced by Frank and Friedman (1993) and Tibshirani (1996), which penalizes the absolute size of coefficient estimates.

The primary purpose of regularized regression, like supervised machine learning methods more generally, is prediction. Regularized regression typically does not produce estimates that can be interpreted as causal and statistical inference on these coefficients is complicated.222This is an active area of research, see for example Buhlmann (2013); Meinshausen et al. (2009); Weilenmann et al. (2017); Wasserman and Roeder (2009); Lockhart et al. (2014). While regularized regression may select the true model as the sample size increases, this is generally only the case under strong assumptions. However, regularized regression can aid causal inference without relying on the strong assumptions required for perfect model selection. The post-double-selection methodology of Belloni et al. (2014a) and the post-regularization approach of Chernozhukov et al. (2015) can be used to select appropriate control variables from a large set of putative confounding factors and, thereby, improve robustness of estimation of the parameters of interest. Likewise, the first stage of two-step least-squares is a prediction problem and lasso or ridge can be applied to obtain optimal instruments (Belloni et al., 2012; Carrasco, 2012; Hansen and Kozbur, 2014). These methods are implemented in our sister package pdslasso (Ahrens et al., 2018), which builds on the algorithms developed in lassopack.

The strength of regularized regression as a prediction technique stems from the bias-variance trade-off. The prediction error can be decomposed into the unknown error variance reflecting the overall noise level (which is irreducible), the squared estimation bias and the variance of the predictor. The variance of the estimated predictor is increasing in the model complexity, whereas the bias tends to decrease with model complexity. By reducing model complexity and inducing a shrinkage bias, regularized regression methods tend to outperform OLS in terms of out-of-sample prediction performance. In doing so, regularized regression addresses the common problem of overfitting: high in-sample fit (high ), but poor prediction performance on unseen data.

Another advantage is that the regularization methods of lassopack—with the exception of ridge regression—are able to produce sparse solutions and, thus, can serve as model selection techniques. Especially when faced with a large number of putative predictors, model selection is challenging. Iterative testing procedures, such as the general-to-specific approach, typically induce pre-testing biases and hypothesis tests often lead to many false positives. At the same time, high-dimensional problems where the number of predictors is large relative to the sample size are a common phenomenon, especially when the true model is treated as unknown. Regularized regression is well-suited for high-dimensional data. The -penalization can set some coefficients to exactly zero, thereby excluding predictors from the model. The bet on sparsity principle allows for identification even when the number of predictors exceeds the sample size under the assumption that the true model is sparse or can be approximated by a sparse parameter vector.333Hastie et al. (2009, p. 611) summarize the bet on sparsity principle as follows: ‘Use a procedure that does well in sparse problems, since no procedure does well in dense problems.’

Regularized regression methods rely on tuning parameters that control the degree and type of penalization. lassopack offers three approaches to select these tuning parameters. The classical approach is to select tuning parameters using cross-validation in order to optimize out-of-sample prediction performance. Cross-validation methods are universally applicable and generally perform well for prediction tasks, but are computationally expensive. A second approach relies on information criteria such as the Akaike information criterion (Zou et al., 2007; Zhang et al., 2010). Information criteria are easy to calculate and have attractive theoretical properties, but are less robust to violations of the independence and homoskedasticity assumptions (Arlot and Celisse, 2010). Rigorous penalization for the lasso and square-root lasso provides a third option. The approach is valid in the presence of heteroskedastic, non-Gaussian and cluster-dependent errors (Belloni et al., 2012, 2014b, 2016). The rigorous approach places a high priority on controlling overfitting, thus often producing parsimonious models. This strong focus on containing overfitting is of practical and theoretical benefit for selecting control variables or instruments in a structural model, but also implies that the approach may be outperformed by cross-validation techniques for pure prediction tasks. Which approach is most appropriate depends on the type of data at hand and the purpose of the analysis. To provide guidance for applied reseachers, we discuss the theoretical foundation of all three approaches, and present Monte Carlo results that assess their relative performance.

The article proceeds as follows. In Section 2, we present the estimation methods implemented in lassopack. Section 3-5 discuss the aforementioned approaches for selecting the tuning parameters: information criteria in Section 3, cross-validation in Section 4 and rigorous penalization in Section 5. The three commands, which correspond to the three penalization approaches, are presented in Section 6, followed by demonstrations in Section 7. Section 8 presents Monte Carlo results. Further technical notes are in Section 9.

Notation.

We briefly clarify the notation used in this article. Suppose is a vector of dimension with typical element for . The -norm is defined as , and the -norm is . The ‘-norm’ of is denoted by and is equal to the number of non-zero elements in . denotes the indicator function. We use the notation to denote the maximum value of and , i.e., .

2 Regularized regression

This section introduces the regularized regression methods implemented in lassopack. We consider the high-dimensional linear model

where the number of predictors, , may be large and even exceed the sample size, . The regularization methods introduced in this section can accommodate large- models under the assumption of sparsity: out of the predictors only a subset of are included in the true model where is the sparsity index

We refer to this assumption as exact sparsity. It is more restrictive than required, but we use it here for illustrative purposes. We will later relax the assumption to allow for non-zero, but ‘small’, coefficients. We also define the active set , which is the set of non-zero coefficients. In general, , , and may depend on but we suppress the -subscript for notational convenience.

We adopt the following convention throughout the article: unless otherwise noted, all variables have been mean-centered such that and , and all variables are measured in their natural units, i.e., they have not been pre-standardized to have unit variance. By assuming the data have already been mean-centered we simplify the notation and exposition. Leaving the data in natural units, on the other hand, allows us to discuss standardization in the context of penalization.

Penalized regression methods rely on tuning parameters that control the degree and type of penalization. The estimation methods implemented in lassopack, which we will introduce in the following sub-section, use two tuning parameters: controls the general degree of penalization and determines the relative contribution of vs. penalization. The three approaches offered by lassopack for selecting and are introduced in 2.2.

2.1 The estimators

Lasso

The lasso takes a special position, as it provides the basis for the rigorous penalization approach (see Section 5) and has inspired other methods such as elastic net and square-root lasso, which are introduced later in this section. The lasso minimizes the mean squared error subject to a penalty on the absolute size of coefficient estimates:

| (1) |

The tuning parameter controls the overall penalty level and are predictor-specific penalty loadings.

Tibshirani (1996) motivates the lasso with two major advantages over OLS. First, due to the nature of the -penalty, the lasso sets some of the coefficient estimates exactly to zero and, in doing so, removes some predictors from the model. Thus, the lasso serves as a model selection technique and facilitates model interpretation. Secondly, lasso can outperform least squares in terms of prediction accuracy due to the bias-variance trade-off.

The lasso coefficient path, which constitutes the trajectory of coefficient estimates as a function of , is piecewise linear with changes in slope where variables enter or leave the active set. The change points are referred to as knots. yields the OLS solution and yields an empty model, where all coefficients are zero.

The lasso, unlike OLS, is not invariant to linear transformations, which is why scaling matters. If the predictors are not of equal variance, the most common approach is to pre-standardize the data such that and set for . Alternatively, we can set the penalty loadings to The two methods yield identical results in theory.

Ridge regression

Ridge regression (Tikhonov, 1963; Hoerl and Kennard, 1970) replaces the -penalty of the lasso with a -penalty, thus minimizing

| (2) |

The interpretation and choice of the penalty loadings is the same as above. As in the case of the lasso, we need to account for uneven variance, either through pre-estimation standardization or by appropriately choosing the penalty loadings .

In contrast to estimators relying on -penalization, the ridge does not perform variable selection. At the same time, it also does not rely on the assumption of sparsity. This makes the ridge attractive in the presence of dense signals, i.e., when the assumption of sparsity does not seem plausible. Dense high-dimensional problems are more challenging than sparse problems: for example, Dicker (2016) shows that, if , it is not possible to outperform a trivial estimator that only includes the constant. If jointly, but converges to a finite constant, the ridge has desirable properties in dense models and tends to perform better than sparsity-based methods (Hsu et al., 2014; Dicker, 2016; Dobriban and Wager, 2018).

Ridge regression is closely linked to principal component regression. Both methods are popular in the context of multicollinearity due to their low variance relative to OLS. Principal components regression applies OLS to a subset of components derived from principal component analysis; thereby discarding a specified number of components with low variance. The rationale for removing low-variance components is that the predictive power of each component tends to increase with the variance. The ridge can be interpreted as projecting the response against principal components while imposing a higher penalty on components exhibiting low variance. Hence, the ridge follows a similar principle; but, rather than discarding low-variance components, it applies a more severe shrinkage (Hastie et al., 2009).

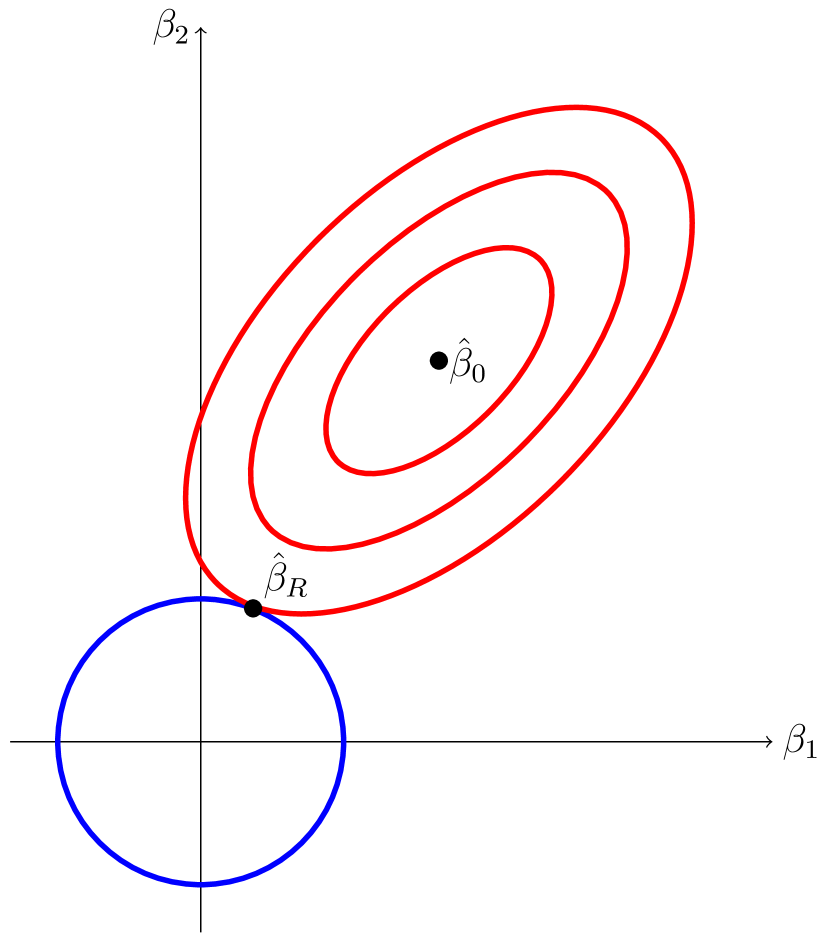

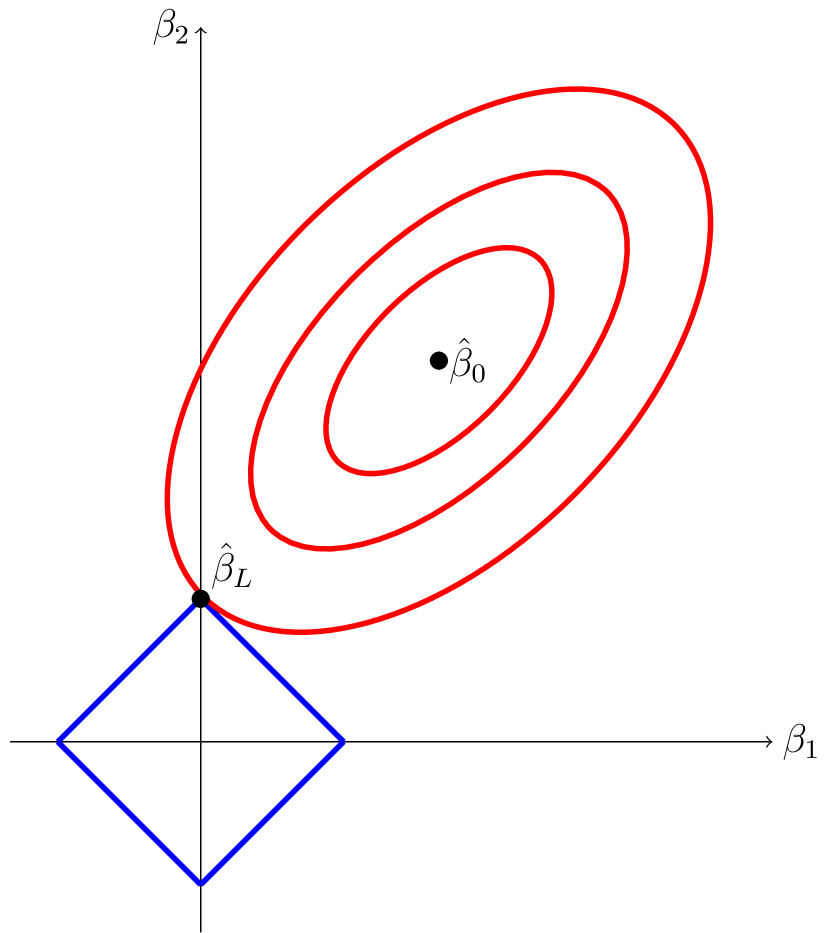

A comparison of lasso and ridge regression provides further insights into the nature of and penalization. For this purpose, it is helpful to write lasso and ridge in constrained form as

and to examine the shapes of the constraint sets. The above optimization problems use the tuning parameter instead of . Note that there exists a data-dependent relationship between and .

Figure 1 illustrates the geometry underpinning lasso and ridge regression for the case of and (i.e., unity penalty loadings). The red elliptical lines represent residual sum of squares contours and the blue lines indicate the lasso and ridge constraints. The lasso constraint set, given by , is diamond-shaped with vertices along the axes from which it immediately follows that the lasso solution may set coefficients exactly to 0. In contrast, the ridge constraint set, , is circular and will thus (effectively) never produce a solution with any coefficient set to 0. Finally, in the figure denotes the solution without penalization, which corresponds to OLS. The lasso solution at the corner of the diamond implies that, in this example, one of the coefficients is set to zero, whereas ridge and OLS produce non-zero estimates for both coefficients.

While there exists no closed form solution for the lasso, the ridge solution can be expressed as

Here is the matrix of predictors with typical element , is the response vector and is the diagonal matrix of penalty loadings. The ridge regularizes the regressor matrix by adding positive constants to the diagonal of . The ridge solution is thus well-defined generally as long as all the and are sufficiently large even if is rank-deficient.

Elastic net

The elastic net of Zou and Hastie (2005) combines some of the strengths of lasso and ridge regression. It applies a mix of (lasso-type) and (ridge-type) penalization:

| (3) |

The additional parameter determines the relative to contribution of vs. penalization. In the presence of groups of correlated regressors, the lasso typically selects only one variable from each group, whereas the ridge tends to produce similar coefficient estimates for groups of correlated variables. On the other hand, the ridge does not yield sparse solutions impeding model interpretation. The elastic net is able to produce sparse solutions for some greater than zero, and retains or drops correlated variables jointly.

Adaptive lasso

The irrepresentable condition (IRC) is shown to be sufficient and (almost) necessary for the lasso to be model selection consistent (Zhao and Yu, 2006; Meinshausen and Bühlmann, 2006). However, the IRC imposes strict constraints on the degree of correlation between predictors in the true model and predictors outside of the model. Motivated by this non-trivial condition for the lasso to be variable selection consistent, Zou (2006) proposed the adaptive lasso. The adaptive lasso uses penalty loadings of where is an initial estimator. The adaptive lasso is variable-selection consistent for fixed under weaker assumptions than the standard lasso. If , OLS can be used as the initial estimator. Huang et al. (2008) prove variable selection consistency for large and suggest using univariate OLS if . The idea of adaptive penalty loadings can also be applied to elastic net and ridge regression (Zou and Zhang, 2009).

Square-root lasso

The square-root lasso,

| (4) |

is a modification of the lasso that minimizes the root mean squared error, while also imposing an -penalty. The main advantage of the square-root lasso over the standard lasso becomes apparent if theoretically grounded, data-driven penalization is used. Specifically, the score vector, and thus the optimal penalty level, is independent of the unknown error variance under homoskedasticity as shown by Belloni et al. (2011), resulting in a simpler procedure for choosing (see Section 5).

Post-estimation OLS

Penalized regression methods induce an attenuation bias that can be alleviated by post-estimation OLS, which applies OLS to the variables selected by the first-stage variable selection method, i.e.,

| (5) |

where is a sparse first-step estimator such as the lasso. Thus, post-estimation OLS treats the first-step estimator as a genuine model selection technique. For the case of the lasso, Belloni and Chernozhukov (2013) have shown that the post-estimation OLS, also referred to as post-lasso, performs at least as well as the lasso under mild additional assumptions if theory-driven penalization is employed. Similar results hold for the square-root lasso (Belloni et al., 2011, 2014b).

2.2 Choice of the tuning parameters

Since coefficient estimates and the set of selected variables depend on and , a central question is how to choose these tuning parameters. Which method is most appropriate depends on the objectives and setting: in particular, the aim of the analysis (prediction or model identification), computational constraints, and if and how the i.i.d. assumption is violated. lassopack offers three approaches for selecting the penalty level of and :

-

1.

Information criteria: The value of can be selected using information criteria. lasso2 implements model selection using four information criteria. We discuss this approach in Section 3.

-

2.

Cross-validation: The aim of cross-validation is to optimize the out-of-sample prediction performance. Cross-validation is implemented in cvlasso, which allows for cross-validation across both and the elastic net parameter . See Section 4.

-

3.

Theory-driven (‘rigorous’): Theoretically justified and feasible penalty levels and loadings are available for the lasso and square-root lasso via rlasso. The penalization is chosen to dominate the noise of the data-generating process (represented by the score vector), which allows derivation of theoretical results with regard to consistent prediction and parameter estimation. See Section 5.

3 Tuning parameter selection using information criteria

Information criteria are closely related to regularization methods. The classical Akaike’s information criterion (Akaike, 1974, AIC) is defined as . Thus, the AIC can be interpreted as penalized likelihood which imposes a penalty on the number of predictors included in the model. This form of penalization, referred to as -penalty, has, however, an important practical disadvantage. In order to find the model with the lowest AIC, we need to estimate all different model specifications. In practice, it is often not feasible to consider the full model space. For example, with only 20 predictors, there are more than 1 million different models.

The advantage of regularized regression is that it provides a data-driven method for reducing model selection to a one-dimensional problem (or two-dimensional problem in the case of the elastic net) where we need to select (and . Theoretical properties of information criteria are well-understood and they are easy to compute once coefficient estimates are obtained. Thus, it seems natural to utilize the strengths of information criteria as model selection procedures to select the penalization level.

Information criteria can be categorized based on two central properties: loss efficiency and model selection consistency. A model selection procedure is referred to as loss efficient if it yields the smallest averaged squared error attainable by all candidate models. Model selection consistency requires that the true model is selected with probability approaching 1 as . Accordingly, which information information criteria is appropriate in a given setting also depends on whether the aim of analysis is prediction or identification of the true model.

We first consider the most popular information criteria, AIC and Bayesian information criterion (Schwarz, 1978, BIC):

where and are the residuals. is the effective degrees of freedom, which is a measure of model complexity. In the linear regression model, the degrees of freedom is simply the number of regressors. Zou et al. (2007) show that the number of coefficients estimated to be non-zero, , is an unbiased and consistent estimate of for the lasso (). More generally, the degrees of freedom of the elastic net can be calculated as the trace of the projection matrix, i.e.,

where is the matrix of selected regressors. The unbiased estimator of the degrees of freedom provides a justification for using the classical AIC and BIC to select tuning parameters (Zou et al., 2007).

The BIC is known to be model selection consistent if the true model is among the candidate models, whereas AIC is inconsistent. Clearly, the assumption that the true model is among the candidates is strong; even the existence of the ‘true model’ may be problematic, so that loss efficiency may become a desirable second-best. The AIC is, in contrast to BIC, loss efficient. Yang (2005) shows that the differences between AIC-type information criteria and BIC are fundamental; a consistent model selection method, such as the BIC, cannot be loss efficient, and vice versa. Zhang et al. (2010) confirm this relation in the context of penalized regression.

Both AIC and BIC are not suitable in the large--small- context where they tend to select too many variables (see Monte Carlo simulations in Section 8). It is well known that the AIC is biased in small samples, which motivated the bias-corrected AIC (Sugiura, 1978; Hurvich and Tsai, 1989),

The bias can be severe if is large relative to , and thus the AICc should be favoured when is small or with high-dimensional data.

The BIC relies on the assumption that each model has the same prior probability. This assumptions seems reasonable when the researcher has no prior knowledge; yet, it contradicts the principle of parsimony and becomes problematic if is large. To see why, consider the case where (following Chen and Chen, 2008): There are models for which one parameter is non-zero (), while there are models for which . Thus, the prior probability of is larger than the prior probability of by a factor of . More generally, since the prior probability that is larger than the probability that (up to the point where ), the BIC is likely to over-select variables. To address this shortcoming, Chen and Chen (2008) introduce the Extended BIC, defined as

which imposes an additional penalty on the size of the model. The prior distribution is chosen such that the probability of a model with dimension is inversely proportional to the total number of models for which . The additional parameter, , controls the size of the additional penalty.444We follow Chen and Chen (2008, p. 768) and use as the default choice. An upper and lower threshold is applied to ensure that lies in the [0,1] interval. Chen and Chen (2008) show in simulation studies that the EBICξ outperforms the traditional BIC, which exhibits a higher false discovery rate when is large relative to .

4 Tuning parameter selection using cross-validation

The aim of cross-validation is to directly assess the performance of a model on unseen data. To this end, the data is repeatedly divided into a training and a validation data set. The models are fit to the training data and the validation data is used to assess the predictive performance. In the context of regularized regression, cross-validation can be used to select the tuning parameters that yield the best performance, e.g., the best out-of-sample mean squared prediction error. A wide range of methods for cross-validation are available. For an extensive review, we recommend Arlot and Celisse (2010). The most popular method is -fold cross-validation, which we introduce in Section 4.1. In Section 4.2, we discuss methods for cross-validation in the time-series setting.

4.1 K-fold cross-validation

For -fold cross-validation, proposed by Geisser (1975), the data is split into groups, referred to as folds, of approximately equal size. Let denote the set of observations in the th fold, and let be the size of data partition for . In the th step, the th fold is treated as the validation data set and the remaining folds constitute the training data set. The model is fit to the training data for a given value of and . The resulting estimate, which is based on all the data except the observations in fold , is . The procedure is repeated for each fold, as illustrated in Figure 2, so that every data point is used for validation once. The mean squared prediction error for each fold is computed as

The -fold cross-validation estimate of the MSPE, which serves as a measure of prediction performance, is

This suggests selecting and as the values that minimize . An alternative common rule is to use the largest value of that is within one standard deviation of the minimum, which leads to a more parsimonious model.

Cross-validation can be computationally expensive. It is necessary to compute for each value of on a grid if is fixed (e.g. when using the lasso) or, in the case of the elastic net, for each combination of values of and on a two-dimensional grid. In addition, the model must be estimated times at each grid point, such that the computational cost is approximately proportional to .555An exception is the special case of leave-one-out cross-validation, where . The advantage of LOO cross-validation for linear models is that there is a closed-form expression for the MSPE, meaning that the model needs to be estimated only once instead of times.

Standardization adds another layer of computational cost to -fold cross validation. An important principle in cross-validation is that the training data set should not contain information from the validation dataset. This mimics the real-world situation where out-of-sample predictions are made not knowing what the true response is. The principle applies not only to individual observations, but also to data transformations such as mean-centering and standardization. Specifically, data transformations applied to the training data should not use information from the validation data or full dataset. Mean-centering and standardization using sample means and sample standard deviations for the full sample would violate this principle. Instead, when in each step the model is fit to the training data for a given and , the training dataset must be re-centered and re-standardized, or, if standardization is built into the penalty loadings, the must be recalculated based on the training dataset.

The choice of is not only a practical problem; it also has theoretical implications. The variance of decreases with , and is minimal (for linear regression) if , which is referred to as leave-one-out or LOO CV. Similarly, the bias decreases with the size of the training data set. Given computational contraints, between 5 and 10 are often recommended, arguing that the performance of CV rarely improves for larger than 10 (Hastie et al., 2009; Arlot and Celisse, 2010).

If the aim of the researcher’s analysis is model identification rather than prediction, the theory requires training data to be ‘small’ and the evaluation sample to be close to (Shao, 1993, 1997). The reason is that more data is required to evaluate which model is the ‘correct’ one rather than to decrease bias and variance. This is referred to as cross-validation paradox (Yang, 2006). However, since -fold cross-validation sets the size of the training sample to approximately , -fold CV is necessarily ill-suited for selecting the true model.

4.2 Cross-validation with time-series data

Serially dependent data violate the principle that training and validation data are independent. That said, standard -fold cross-validation may still be appropriate in certain circumstances. Bergmeir et al. (2018) show that -fold cross-validation remains valid in the pure auto-regressive model if one is willing to assume that the errors are uncorrelated. A useful implication is that -fold cross-validation can be used on overfit auto-regressive models that are not otherwise badly misspecified, since such models have uncorrelated errors.

Rolling -step ahead CV is an intuitively appealing approach that directly incorporates the ordered nature of time series-data (Hyndman, Rob and Athanasopoulos, 2018).666Another approach is a variation of LOO cross-validation known as -block cross-validation (Burman et al., 1994), which omits observations between training and validation data. The procedure builds on repeated -step ahead forecasts. The procedure is implemented in lassopack and illustrated in Figure 3-4.

| Step | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | ||

| 1 | \bigstrut[t] | |||||

| 2 | ||||||

| 3 | ||||||

| 4 | ||||||

| 5 | ||||||

| 6 | ||||||

| 7 | ||||||

| 8 | ||||||

| Step | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | ||

| 1 | \bigstrut[t] | |||||

| 2 | ||||||

| 3 | ||||||

| 4 | ||||||

| 5 | ||||||

| 6 | ||||||

| 7 | ||||||

| 8 | ||||||

| 9 | ||||||

| Step | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | ||

| 1 | \bigstrut[t] | |||||

| 2 | ||||||

| 3 | ||||||

| 4 | ||||||

| 5 | ||||||

| 6 | ||||||

| 7 | ||||||

| 8 | ||||||

| Step | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | ||

| 1 | \bigstrut[t] | |||||

| 2 | ||||||

| 3 | ||||||

| 4 | ||||||

| 5 | ||||||

| 6 | ||||||

| 7 | ||||||

| 8 | ||||||

| 9 | ||||||

Figure 3(a) corresponds to the default case of 1-step ahead cross-validation. ‘’ denotes the observation included in the training sample and ‘’ refers to the validation sample. In the first step, observations 1 to 3 constitute the training data set and observation 4 is the validation point, whereas the remaining observations are unused as indicated by a dot (‘.’). Figure 3(b) illustrates the case of 2-step ahead cross-validation. In both cases, the training window expands incrementally, whereas Table 4 displays rolling CV with a fixed estimation window.

4.3 Comparison with information criteria

Since information-based approaches and cross-validation share the aim of model selection, one might expect that the two methods share some theoretical properties. Indeed, AIC and LOO-CV are asymptotically equivalent, as shown by Stone (1977) for fixed . Since information criteria only require the model to be estimated once, they are computationally much more attractive, which might suggest that information criteria are superior in practice. However, an advantage of CV is its flexibility and that it adapts better to situations where the assumptions underlying information criteria, e.g. homoskedasticity, are not satisfied (Arlot and Celisse, 2010). If the aim of the analysis is identifying the true model, BIC and EBIC provide a better choice than -fold cross-validation, as there are strong but well-understood conditions under which BIC and EBIC are model selection consistent.

5 Rigorous penalization

This section introduces the ‘rigorous’ approach to penalization. Following Chernozhukov et al. (2016), we use the term ‘rigorous’ to emphasize that the framework is grounded in theory. In particular, the penalization parameters are chosen to guarantee consistent prediction and parameter estimation. Rigorous penalization is of special interest, as it provides the basis for methods to facilitate causal inference in the presence of many instruments and/or many control variables; these methods are the IV-Lasso (Belloni et al., 2012), the post-double-selection (PDS) estimator (Belloni et al., 2014a) and the post-regularization estimator (CHS) (Chernozhukov et al., 2015); all of which are implemented in our sister package pdslasso (Ahrens et al., 2018).

We discuss the conditions required to derive theoretical results for the lasso in Section 5.1. Sections 5.2-5.5 present feasible algorithms for optimal penalization choices for the lasso and square-root lasso under i.i.d., heteroskedastic and cluster-dependent errors. Section 5.6 presents a related test for joint significance testing.

5.1 Theory of the lasso

There are three main conditions required to guarantee that the lasso is consistent in terms of prediction and parameter estimation.777For a more detailed treatment, we recommend Hastie et al. (2015, Ch. 11) and Bühlmann and Van de Geer (2011). The first condition relates to sparsity. Sparsity is an attractive assumption in settings where we have a large set of potentially relevant regressors, or consider various different model specifications, but assume that only one true model exists which includes a small number of regressors. We have introduced exact sparsity in Section 2, but the assumption is stronger than needed. For example, some true coefficients may be non-zero, but small in absolute size, in which case it might be preferable to omit them. For this reason, we use a weaker assumption:

Approximate sparsity.

Belloni et al. (2012) consider the approximate sparse model (ASM),

| (6) |

The elementary regressors are linked to the dependent variable through the unknown and possibly non-linear function . The aim of the lasso (and square-root lasso) estimation is to approximate using the target parameter vector and the transformations , where denotes a dictionary of transformations. The vector may be large relative to the sample size, either because itself is high-dimensional and , or because a large number of transformations such as dummies, polynomials, interactions are considered to approximate .

The assumption of approximate sparsity requires the existence of a target vector which ensures that can be approximated sufficiently well, while using only a small number of non-zero coefficients. Specifically, the target vector and the sparsity index are assumed to meet the condition

and the resulting approximation error is bounded such that

| (7) |

where is a positive constant. To emphasize the distinction between approximate and exact sparsity, consider the special case where is linear with , but where the true parameter vector violates exact sparsity so that . If has many elements that are negligible in absolute size, we might still be able to approximate using the sparse target vector as long as is sufficiently small as specified in (7).

Restricted sparse eigenvalue condition.

The second condition relates to the Gram matrix, . In the high-dimensional setting where is larger than , the Gram matrix is necessarily rank-deficient and the minimum (unrestricted) eigenvalue is zero, i.e.,

Thus, to accommodate large , the full rank condition of OLS needs to be replaced by a weaker condition. While the full rank condition cannot hold for the full Gram matrix if , we can plausibly assume that sub-matrices of size are well-behaved. This is in fact the restricted sparse eigenvalue (RSEC) condition of Belloni et al. (2012). The RSEC formally states that the minimum sparse eigenvalues

are bounded away from zero and from above. The requirement implies that all sub-matrices of size have to be positive definite.888The RSEC is stronger than required for the lasso. For example, Bickel et al. (2009) introduce the restricted eigenvalue condition (REC). However, here we only present the RSEC which implies the REC and is sufficient for both lasso and post-lasso. Different variants of the REC and RSEC have been proposed in the literature; for an overview see Bühlmann and Van de Geer (2011).

Regularization event.

The third central condition concerns the choice of the penalty level and the predictor-specific penalty loadings . The idea is to select the penalty parameters to control the random part of the problem in the sense that

| (8) |

with high probability. Here, is a constant slack parameter and is the th element of the score vector , the gradient of at the true value . The score vector summarizes the noise associated with the estimation problem.

Denote by the maximal element of the score vector scaled by and , and denote by the quantile function for .999That is, the probability that is at most is . In the rigorous lasso, we choose the penalty parameters and and confidence level so that

| (9) |

A simple example illustrates the intuition behind this approach. Consider the case where the true model has for , i.e., none of the regressors appear in the true model. It can be shown that for the lasso to select no variables, the penalty parameters and need to satisfy .101010See, for example, Hastie et al. (2015, Ch. 2). Because none of the regressors appear in the true model, . We can therefore rewrite the requirement for the lasso to correctly identify the model without regressors as , which is the regularization event in (8). We want this regularization event to occur with high probability of at least . If we choose values for and such that , then by the definition of a quantile function we will choose the correct model—no regressors—with probability of at least . This is simply the rule in (9).

The chief practical problem in using the rigorous lasso is that the quantile function is unknown. There are two approaches to addressing this problem proposed in the literature, both of which are implemented in rlasso. The rlasso default is the ‘asymptotic’ or X-independent approach: theoretically grounded and feasible penalty level and loadings are used that guarantee that (8) holds asymptotically, as and . The X-independent penalty level choice can be interpreted as an asymptotic upper bound on the quantile function . In the ‘exact’ or X-dependent approach, the quantile function is directly estimated by simulating the distribution of , the -quantile of conditional on the observed regressors . We first focus on the X-independent approach, and introduce the X-dependent approach in Section 5.5.

5.2 Rigorous lasso

Belloni et al. (2012) show—using moderate deviation theory of self-normalized sums from Jing et al. (2003)—that the regularization event in (8) holds asymptotically, i.e.,

| (10) |

if the penalty levels and loadings are set to

| (11) |

under homoskedasticity and heteroskedasticity, respectively. is the slack parameter from above and the significance level is required to converge towards 0. rlasso uses and as defaults.111111The parameters and can be controlled using the options c(real) and gamma(real). Note that we need to choose greater than 1 for the regularization event to hold asymptotically, but not too high as the shrinkage bias is increasing in .,121212 An alternative X-independent choice is to set . Since , this will lead to a more parsimonious model, but also to a larger bias. To use the alternative X-independent, specify the lalt option.

Homoskedasticity.

We first focus on the case of homoskedasticity. In the rigorous lasso approach, we standardize the score. But since under homoskedasticity, we can separate the problem into two parts: the regressor-specific penalty loadings standardize the regressors, and moves into the overall penalty level. In the special case where the regressors have already been standardized such that , the penalty loadings are . Hence, the purpose of the regressor-specific penalty loadings in the case of homoskedasticity is to accommodate regressors with unequal variance.

The only unobserved term is , which appears in the optimal penalty level . To estimate , we can use some initial set of residuals and calculate the initial estimate as . A possible choice for the initial residuals is as in Belloni et al. (2012) and Belloni et al. (2014a). rlasso uses the OLS residuals where is the set of 5 regressors exhibiting the highest absolute correlation with .131313This is also the default setting in Chernozhukov et al. (2016). The number of regressors used for calculating the initial residuals can be controlled using the corrnumber(integer) option, where 5 is the default and 0 corresponds to . The procedure is summarized in Algorithm A:

\sboxsep= 2pt \sdim= 1pt \sboxrule= .2pt \shabox Algorithm A: Estimation of penalty level under homoskedasticity.

-

1.

Set , and define the maximum number of iterations, . Regress against the subset of predictors exhibiting the highest correlation coefficient with and compute the initial residuals as . Calculate the homoskedastic penalty loadings in (11).

-

2.

If , compute the homoskedastic penalty level in (11) by replacing with and obtain the rigorous lasso or post-lasso estimator . Update the residuals . Set .

-

3.

Repeat step 2 until or until convergence by updating the penalty level.

\sboxsep= 2pt \sdim= 1pt \sboxrule= .2pt \shabox

The rlasso default is to perform one further iteration after the initial estimate (i.e., ), which in our experience provides good performance. Both lasso and post-lasso can be used to update the residuals. rlasso uses post-lasso to update the residuals.141414The lassopsi option can be specified, if rigorous lasso residuals are preferred.

Heteroskedasticity.

The X-independent choice for the overall penalty level under heteroskedasticity is . The only difference with the homoskedastic case is the absence of . The variance of is now captured via the penalty loadings, which are set to . Hence, the penalty loadings here serve two purposes: accommodating both heteroskedasticity and regressors with uneven variance.

To help with the intuition, we consider the case where the predictors are already standardized. It is easy to see that, if the errors are homoskedastic with , the penalty loadings are (asymptotically) just . If the data are heteroskedastic, however, the standardized penalty loading will not be . In most practical settings, the usual pattern will be that for some . Intuitively, heteroskedasticity typically increases the likelihood that the term takes on extreme values, thus requiring a higher degree of penalization through the penalty loadings.151515To get insights into the nature of heteroskedasticity, rlasso also calculates and returns the standardized penalty loadings which are stored in e(sPsi).

The disturbances are unobserved, so we obtain an initial set of penalty loadings from an initial set of residuals similar to the i.i.d. case above. We summarize the algorithm for estimating the penalty level and loadings as follows:

\sboxsep= 2pt \sdim= 1pt \sboxrule= .2pt \shabox Algorithm B: Estimation of penalty loadings under heteroskedasticity.

-

1.

Set , and define the maximum number of iterations, . Regress against the subset of predictors exhibiting the highest correlation coefficient with and compute the initial residuals as . Calculate the heteroskedastic penalty level in (11).

-

2.

If , compute the heterokedastic penalty loadings using the formula given in in (11) by replacing with , obtain the rigorous lasso or post-lasso estimator . Update the residuals . Set .

-

3.

Repeat step 2 until or until convergence by updating the penalty loadings.

\sboxsep= 2pt \sdim= 1pt \sboxrule= .2pt \shabox

Theoretical property.

Under the assumptions SEC, ASM and if penalty level and the penalty loadings are estimated by Algorithm A or B, the lasso and post-lasso obey:161616For the sake of brevity, we omit additional technical conditions relating to the moments of the error and the predictors. These conditions are required to make use of the moderate deviation theory of self-normalized sums (Jing et al., 2003), which is employed to relax the assumption of Gaussian errors. See condition RF in Belloni et al. (2012) and condition SM in Belloni et al. (2014a).

| (12) | ||||

| (13) |

The first relation in (12) provides an asymptotic bound for the prediction error, and the second relation in (13) bounds the bias in estimating the target parameter . Belloni et al. (2012) refer to the above convergence rates as near-oracle rates. If the identity of the variables in the model were known, the prediction error would converge at the oracle rate . Thus, the logarithmic term can be interpreted as the cost of not knowing the true model.

5.3 Rigorous square-root lasso

The theory of the square-root lasso is similar to the theory of the lasso (Belloni et al., 2011, 2014b). The th element of the score vector is now defined as

| (14) |

To see why the square-root lasso is of special interest, we define the standardized errors as . The th element of the score vector becomes

| (15) |

and is thus independent of . For the same reason, the optimal penalty level for the square-root lasso in the i.i.d. case,

| (16) |

is independent of the noise level .

Homoskedasticity.

The ideal penalty loadings under homoskedasticity for the square-root lasso are given by formula (iv) in Table 1, which provides an overview of penalty loading choices. The ideal penalty parameters are independent of the unobserved error, which is an appealing theoretical property and implies a practical advantage. Since both and can be calculated from the data, the rigorous square-root lasso is a one-step estimator under homoskedasticity. Belloni et al. (2011) show that the square-root lasso performs similarly to the lasso with infeasible ideal penalty loadings.

Heteroskedasticity.

In the case of heteroskedasticity, the optimal square-root lasso penalty level remains (16), but the penalty loadings, given by formula (v) in Table 1, depend on the unobserved error and need to be estimated. Note that the updated penalty loadings using the residuals employ thresholding: the penalty loadings are enforced to be greater than or equal to the loadings in the homoskedastic case. The rlasso default algorithm used to obtain the penalty loadings in the heteroskedastic case is analogous to Algorithm B.171717The rlasso default for the square-root lasso uses a first-step set of initial residuals. The suggestion of Belloni et al. (2014b) to use initial penalty loadings for regressor of is available using the maxabsx option. While the ideal penalty loadings are not independent of the error term if the errors are heteroskedastic, the square-root lasso may still have an advantage over the lasso, since the ideal penalty loadings are pivotal with respect to the error term up to scale, as pointed out above.

5.4 Rigorous penalization with panel data

Belloni et al. (2016) extend the rigorous framework to the case of clustered data, where a limited form of dependence—within-group correlation—as well as heteroskedasticity are accommodated. They prove consistency of the rigorous lasso using this approach in the large , fixed and large , large settings. The authors present the approach in the context of a fixed-effects panel data model, , and apply the rigorous lasso after the within transformation to remove the fixed effects . The approach extends to any clustered-type setting and to balanced and unbalanced panels. For convenience we ignore the fixed effects and write the model as a balanced panel:

| (17) |

The intuition behind the Belloni et al. (2016) approach is similar to that behind the clustered standard errors reported by various Stata estimation commands: observations within clusters are aggregated to create ‘super-observations’ which are assumed independent, and these super-observations are treated similarly to cross-sectional observations in the non-clustered case. Specifically, define for the th cluster and th regressor the super-observation . Then the penalty loadings for the clustered case are

which resembles the heteroskedastic case. The rlasso default for the overall penalty level is the same as in the heteroskedastic case, , except that the default value for is , i.e., we use the number of clusters rather than the number of observations . lassopack also implements the rigorous square-root lasso for panel data, which uses the overall penalty in (16) and the penalty loadings in formula (vi), Table 1.

| lasso | square-root lasso | |||

| homoskedasticity | (i) | (iv) | ||

| heteroskedasticity | (ii) | (v) | ||

| cluster-dependence | (iii) | (vi) | ||

| Note: Formulas (iii) and (vi) use the notation . | ||||

5.5 X-dependent lambda

There is an alternative, sharper choice for the overall penalty level, referred to as the X-dependent penalty. Recall that the asymptotic, X-independent choice in (11) can be interpreted as an asymptotic upper bound on the quantile function of , which is the scaled maximum value of the score vector. Instead of using the asymptotic choice, we can estimate by simulation the distribution of conditional on the observed , and use this simulated distribution to obtain the quantile .

| lasso | square-root lasso | |||

| homoskedasticity | (i) | (iv) | ||

| heteroskedasticity | (ii) | (v) | ||

| cluster-dependence | (iii) | (vi) | ||

| Note: is an i.i.d. standard normal variate drawn independently of the data; . Formulas (iii) and (vi) use the notation . | ||||

In the case of estimation by the lasso under homoskedasticity, we simulate the distribution of using the statistic , defined as

where is the penalty loading for the homoskedastic case, is an estimate of the error variance using some previously-obtained residuals, and is an i.i.d. standard normal variate drawn independently of the data. The X-dependent penalty choice is sharper and adapts to correlation in the regressor matrix (Belloni and Chernozhukov, 2011).

Under heteroskedasticity, the lasso X-dependent penalty is obtained by a multiplier bootstrap procedure. In this case the simulated statistic is defined as in formula (ii) in Table 2. The cluster-robust X-dependent penalty is again obtained analogously to the heteroskedastic case by defining super-observations, and the statistic is defined as in formula (iii) in Table 2. Note that the standard normal variate varies across but not within clusters.

The X-dependent penalties for the square-root lasso are similarly obtained from quantiles of the simulated distribution of the square-root lasso , and are given by formulas (iv), (v) and (vi) in Table 2 for the homoskedastic, heteroskedastic and clustered cases, respectively.181818Note that since is standard normal, in practice the term that appears in the expressions for the square-root lasso will be approximately .

5.6 Significance testing with the rigorous lasso

Inference using the lasso, especially in the high-dimensional setting, is a challenging and ongoing research area of research (see Footnote 2). A test that has been developed and is available in rlasso corresponds to the test for joint significance of regressors using or tests that is common in regression analysis. Specifically, Belloni et al. (2012) suggest using the Chernozhukov et al. (2013, Appendix M) sup-score test to test for the joint significance of the regressors, i.e.,

As in the preceding sections, regressors are assumed to be mean-centered and in their original units.

If the null hypothesis is correct and the rest of the model is well-specified, including the assumption that the regressors are orthogonal to the disturbance , then and hence . The sup-score statistic is

| (18) |

where . Intuitively, the in (18) plays the same role as the penalty loadings do in rigorous lasso estimation.

The -value for the sup-score test is obtained by a multiplier bootstrap procedure simulating the distribution of by the statistic , defined as

where is an i.i.d. standard normal variate drawn independently of the data and is defined as in (18).

The procedure above is valid under both homoskedasticity and heteroskedasticity, but requires independence. A cluster-robust version of the sup-score test that accommodates within-group dependence is

| (19) |

where and .

The -value for the cluster version of comes from simulating

where again is an i.i.d. standard normal variate drawn independently of the data. Note again that is invariant within clusters.

rlasso also reports conservative critical values for using an asymptotically-justified upper bound: . The default value of the slack parameter is and the default test level is . These parameters can be varied using the c(real) and ssgamma(real) options, respectively. The simulation procedure to obtain -values using the simulated statistic can be computationally intensive, so users can request reporting of only the computationally inexpensive conservative critical values by setting the number of simulated values to zero with the ssnumsim(int) option.

6 The commands

The package lassopack consists of three commands: lasso2, cvlasso and rlasso. Each command offers an alternative method for selecting the tuning parameters and . We discuss each command in turn and present its syntax. We focus on the main syntax and the most important options. Some technical options are omitted for the sake of brevity. For a full description of syntax and options, we refer to the help files.

6.1 lasso2: Base command and information criteria

The primary purpose of lasso2 is to obtain the solution of (adaptive) lasso, elastic net and square-root lasso for a single value of or a list of penalty levels, i.e., for , where is the number of penalty levels. The basic syntax of lasso2 is as follows:

lasso2 depvar indepvars if in , alpha() sqrt adaptive adaloadings(numlist) adatheta(real) ols lambda(numlist) lcount(integer) lminratio() lmax() notpen(varlist) partial(varlist) ploadings(string) unitloadings prestd stdcoef fe noconstant tolopt() tolzero() maxiter(integer) plotpath(method) plotvar(varlist) plotopt(string) plotlabel lic(string) ic(string) ebicxi() postresults

The options alpha(real), sqrt, adaptive and ols can be used to select elastic net, square-root lasso, adaptive lasso and post-estimation OLS, respectively. The default estimator of lasso2 is the lasso, which corresponds to alpha(1). The special case of alpha(0) yields ridge regression.

The behaviour of lasso2 depends on whether the numlist in lambda(numlist) is of length greater than one or not. If numlist is a list of more than one value, the solution consists of a matrix of coefficient estimates which are stored in e(betas). Each row in e(betas) corresponds to a distinct value of and each column to one of the predictors in indepvars. The ‘path’ of coefficient estimates over can be plotted using plotpath(method), where method controls whether the coefficient estimates are plotted against lambda (‘lambda’), the natural logarithm of lambda (‘lnlambda’) or the -norm (‘norm’). If the numlist in lambda(numlist) is a scalar value, the solution is a vector of coefficient estimates which is stored in e(b). The default behaviour of lasso2 is to use a list of 100 values.

In addition to obtaining the coefficient path, lasso2 calculates four information criteria (AIC, AICc, BIC and EBIC). These information criteria can be used for model selection by choosing the value of that yields the lowest value for one of the four information criteria. The ic(string) option controls which information criterion is shown in the output, where string can be replaced with ‘aic’, ‘aicc’, ‘bic or ‘ebic’. lic(string) displays the estimation results corresponding to the model selected by an information criterion. It is important to note that lic(string) will not store the results of the estimation. This has the advantage that the user can compare the results for different information criteria without the need to re-estimate the full model. To save the estimation results, the postresults option should be specified in combination with lic(string).

Estimation methods

alpha(real) controls the elastic net parameter, , which controls the degree of -norm (lasso-type) to -norm (ridge-type) penalization. alpha(1) corresponds to the lasso (the default estimator), and alpha(0) to ridge regression. The real value must be in the interval [0,1].

sqrt specifies the square-root lasso estimator. Since the square-root lasso does not employ any form of -penalization, the option is incompatible with alpha(real).

adaptive specifies the adaptive lasso estimator. The penalty loading for predictor is set to where is the OLS estimator or univariate OLS estimator if . is the adaptive exponent, and can be controlled using the adatheta(real) option.

adaloadings(matrix) is a matrix of alternative initial estimates, , used for calculating adaptive loadings. For example, this could be the vector e(b) from an initial lasso2 estimation. The absolute value of is raised to the power (note the minus).

adatheta(real) is the exponent for calculating adaptive penalty loadings. The default is adatheta(1)

ols specifies that post-estimation OLS estimates are displayed and returned in e(betas) or e(b).

Options relating to lambda

lambda(numlist) controls the penalty level(s), , used for estimation. numlist is a scalar value or list of values in descending order.

Each must be greater than zero. If not specified, the default list is used which, using Mata syntax, is defined by

exp(rangen(log(lmax),log(lminratio*lmax),lcount)),

where lcount, lminratio and lmax are defined below, exp() is the exponential function, log() is the natural logarithm, and rangen(a,b,n) creates a column vector going from a to b in n-1 steps (see the mf_range help file). Thus, the default list ranges from lmax to lminratio*lmax and lcount is the number of values. The distance between each in the sequence is the same on the logarithmic scale.

lcount(integer) is the number of penalty values, , for which the solution is obtained. The default is lcount(100).

lmax() is the maximum value penalty level, . By default, is chosen as the smallest penalty level for which the model is empty. Suppose the regressors are mean-centered and standardized, then is defined as for the elastic net and for the square-root lasso (see Friedman et al., 2010, Section 2.5).

lminratio() is the ratio of the minimum penalty level, , to maximum penalty level, . must be between 0 and 1. Default is lminratio(0.001).

Information criteria

lic(string) specifies that, after the first lasso2 estimation using a list of penalty levels, the model that corresponds to the minimum information criterion will be estimated and displayer. ‘aic’, ‘bic’, ‘aicc’, and ‘ebic’ (the default) are allowed. However, the results are not stored in e().

postresults is used in combination with lic(string). postresults stores estimation results of the model selected by information criterion in e().191919This option was called postest in earlier versions of lassopack.

ic(string) controls which information criterion is shown in the output of lasso2 when lambda() is a list. ’aic’, ’bic’, ’aicc’, and ’ebic’ (the default are allowed).

ebicxi() controls the parameter of the EBIC. needs to lie in the [0,1] interval. is equivalent to the BIC. The default choice is .

Penalty loadings and standardisation

notpen(varlist) sets penalty loadings to zero for predictors in varlist. Unpenalized predictors are always included in the model.

partial(varlist) specified that variables in varlist are partialled out prior to estimation.

ploadings(matrix) is a row-vector of penalty loadings, and overrides the default standardization loadings. The size of the vector should equal the number of predictors (excluding partialled-out variables and excluding the constant).

unitloadings specifies that penalty loadings be set to a vector of ones; overrides the default standardization loadings.

prestd specifies that dependent variable and predictors are standardized prior to estimation rather than standardized “on the fly” using penalty loadings. See Section 9.2 for more details. By default the coefficient estimates are un-standardized (i.e., returned in original units).

stdcoef returns coefficients in standard deviation units, i.e., do not un-standardize. Only supported with prestd option.

Penalty loadings and standardisation

fe within-transformation is applied prior to estimation. The option requires the data in memory to be xtset.

noconstant suppress constant from estimation. Default behaviour is to partial the constant out (i.e., to center the regressors).

Replay syntax

The replay syntax of lasso2 allows for plotting and changing display options, without the need to re-run the full model. It can also be used to estimate the model using the value of selected by an information criterion. The syntax is given by:

lasso2 , plotpath(string) plotvar(varlist) plotopt(string) plotlabel postresults lic(method) ic(method)

Prediction syntax

predict type newvar if in , xb residuals ols lambda() lid(integer) approx noisily postresults

xb computes predicted values (the default).

residuals computes residuals.

ols specifies that post-estimation OLS will be used for prediction.

If the previous lasso2 estimation uses more than one penalty level (i.e. ), the following options are applicable:

lambda() specifies that lambda value used for prediction.

lid(integer) specifies the index of the lambda value used for prediction.

approx specifies that linear approximation is used instead of re-estimation. Faster, but only exact if coefficient path is piece-wise linear.

noisily prompts display of estimation output if re-estimation required.

postresults stores estimation results in e() if re-estimation is used.

6.2 Cross-validation with cvlasso

cvlasso implements -fold and -step ahead rolling cross-validation. The syntax of cvlasso is:

cvlasso depvar indepvars if in , alpha(numlist) alphacount(integer) sqrt adaptive adaloadings(string) adatheta() ols lambda(numlist) lcount(stinteger) lminratio() lmax() lopt lse notpen(varlist) partial(varlist) ploadings(string) unitloadings prestd fe noconstant tolopt() tolzero() maxiter(integer) nfolds(integer) foldvar(varname) savefoldvar(varname) rolling h(integer) origin(integer) fixedwindow seed(integer) plotcv plotopt(string) saveest(string)

The alpha() option of cvlasso option accepts a numlist, while lasso2 only accepts a scalar. If the numlist is a list longer than one, cvlasso cross-validates over with and with .

plotcv creates a plot of the estimated mean-squared prediction error as a function of , and plotopt(string) can be used to pass plotting options to Stata’s line command.

Internally, cvlasso calls lasso2 repeatedly. Intermediate lasso2 results can be stored using saveest(string).

Options for K-fold cross-validation

nfolds(integer) is the number of folds used for -fold cross-validation. The default is nfolds(10), or .

foldvar(varname) can be used to specify what fold (data partition) each observation lies in. varname is an integer variable with values ranging from 1 to . If not specified, the fold variable is randomly generated such that each fold is of approximately equal size.

savefoldvar(varname) saves the fold variable variable in varname.

seed(integer) sets the seed for the generation of a random fold variable.

Options for h-step ahead rolling cross-validation

rolling uses rolling -step ahead cross-validation. The option requires the data to be tsset or xtset.

h(integer) changes the forecasting horizon. The default is h(1).

origin(integer) controls the number of observations in the first training dataset.

fixedwindow ensures that the size of the training data set is constant.

Options for selection of lambda

lopt specifies that, after cross-validation, lasso2 estimates the model with the value of that minimizes the mean-squared prediction error. That is, the model is estimated with .

lse specifies that, after cross-validation, lasso2 estimates model with largest that is within one standard deviation from . That is, the model is estimated with .

postresults stores the lasso2 estimation results in e() (to be used in combination with lse or lopt).

Replay syntax

Similar to lasso2, cvlasso also provides a replay syntax, which helps to avoid time-consuming re-estimations. The replay syntax of cvlasso can be used for plotting and to estimate the model corresponding to or . The replay syntax of cvlasso is given by:

cvlasso , lopt lse plotcv(method) plotopt(string) postresults

Predict syntax

predict type newvar if in , xb residuals lopt lse noisily

6.3 rlasso: Rigorous penalization

rlasso implements theory-driven penalization for lasso and square-root lasso. It allows for heteroskedastic, cluster-dependent and non-Gaussian errors. Unlike lasso2 and cvlasso, rlasso estimates the penalty level using iterative algorithms. The syntax of rlasso is given by:

rlasso depvar indepvars if in weight , sqrt partial(varlist) pnotpen(varlist) noconstant fe robust cluster(variable) center xdependent numsim(integer) prestd tolopt() tolups() tolzero() maxiter(integer) maxpsiiter(integer) lassopsi corrnumber(integer) maxabsx lalternative gamma() c() supscore ssnumsim(integer) ssgamma() testonly seed(integer) ols

pnotpen(varlist) specifies that variables in varlist are not penalized.202020This option differs from that of notpen(varlist) as used with cvlasso and lasso2; see the discussion in Section 9.

robust specifies that the penalty loadings account for heteroskedasticity.

cluster(varname) specifies that the penalty loadings account for clustering on variable varname.

center center moments in heteroskedastic and cluster-robust loadings.212121For example, the uncentered heteroskedastic loading for regressor is . In theory, should be mean-zero. The centered penalty loading is where .

lassopsi use lasso or square-root lasso residuals to obtain penalty loadings. The default is post-estimation OLS.222222The option was called lassoups in earlier versions.

corrnumber(integer) number of high-correlation regressors used to obtain initial residuals. The default is corrnumber(5), and corrnumber(0) implies that depvar is used in place of residuals.

prestd standardize data prior to estimation. The default is standardization during estimation via penalty loadings.

Options relating to lambda

xdependent specifies that the X-dependent penalty level is used; see Section 5.5.

numsim(integer) is the number of simulations used for the X-dependent case. The default is 5,000.

lalternative specifies the alternative, less sharp penalty level, which is defined as (for the square-root lasso, is replaced with ). See Footnote 12.

gamma() is the ‘’ in the rigorous penalty level (default ; cluster-lasso default ). See Equation (11).

c() is the ‘’ in the rigorous penalty level. The default is c(1.1). See Equation (11).

Sup-score test

supscore reports the sup-score test of statistical significance.

testonly reports only the sup-score test without lasso estimation.

ssgamma() is the test level for the conservative critical value for the sup-score test (default = 0.05, i.e., 5% significance level).

ssnumsim(integer) controls the number of simulations for sup-score test multiplier bootstrap. The default is 500, while 0 implies no simulation.

Predict syntax

predict type newvar if in , xb residuals lasso ols

xb generate fitted values (default).

residuals generate residuals.

lasso use lasso coefficients for prediction (default is to use estimates posted in e(b) matrix).

ols use OLS coefficients based on lasso-selected variables for prediction (default is to use estimates posted in e(b) matrix).

7 Demonstrations

In this section, we demonstrate the use of lasso2, cvlasso and rlasso using one cross-section example (in Section 7.1) and one time-series example (in Section 7.2).

7.1 Cross-section

For demonstration purposes, we consider the Boston Housing Dataset available on the UCI Machine Learning Repository.232323The dataset is available at https://archive.ics.uci.edu/ml/machine-learning-databases/housing/ housing.data, or in CSV format via our website at http://statalasso.github.io/dta/housing.csv. The data set includes 506 observations and 14 predictors.242424The following predictors are included: per capita crime rate (crim), proportion of residential land zoned for lots over 25,000 sq.ft. (zn), proportion of non-retail business acres per town (indus), Charles River dummy variable (chas), nitric oxides concentration (parts per 10 million) (nox), average number of rooms per dwelling (rm), proportion of owner-occupied units built prior to 1940 (age), weighted distances to five Boston employment centres (dis), index of accessibility to radial highways (rad), full-value property-tax rate per $10,000 (tax), pupil-teacher ratio by town (pratio), where Bk is the proportion of blacks by town (b), % lower status of the population (lstat), median value (medv). The purpose of the analysis is to predict house prices using a set of census-level characteristics.

Estimation with lasso2

We first employ the lasso estimator:

-

. lasso2 medv crim-lstat Knot ID Lambda s L1-Norm EBIC R-sq Entered/removed 1 1 6858.98553 1 0.00000 2250.74087 0.0000 Added _cons. 2 2 6249.65216 2 0.08440 2207.91748 0.0924 Added lstat. 3 3 5694.45029 3 0.28098 2166.62026 0.1737 Added rm. 4 10 2969.09110 4 2.90443 1902.66627 0.5156 Added ptratio. 5 20 1171.07071 5 4.79923 1738.09475 0.6544 Added b. 6 22 972.24348 6 5.15524 1727.95402 0.6654 Added chas. 7 26 670.12972 7 6.46233 1709.14648 0.6815 Added crim. 8 28 556.35346 8 6.94988 1705.73465 0.6875 Added dis. 9 30 461.89442 9 8.10548 1698.65787 0.6956 Added nox. 10 34 318.36591 10 13.72934 1679.28783 0.7106 Added zn. 11 39 199.94307 12 18.33494 1671.61672 0.7219 Added indus rad. 12 41 165.99625 13 20.10743 1669.76857 0.7263 Added tax. 13 47 94.98916 12 23.30144 1645.44345 0.7359 Removed indus. 14 67 14.77724 13 26.71618 1642.91756 0.7405 Added indus. 15 82 3.66043 14 27.44510 1648.83626 0.7406 Added age. Use ´long´ option for full output. Type e.g. ´lasso2, lic(ebic)´ to run the model selected by EBIC.

The above lasso2 output shows the following columns:

-

•

Knot is the knot index. Knots are points at which predictors enter or leave the model. The default output shows one line per knot. If the long option is specified, one row per value is shown.

-

•

ID shows the index, i.e., . By default, lasso2 uses a descending sequence of 100 penalty levels.

-

•

s is the number of predictors in the model.

-

•

L1-Norm shows the -norm of coefficient estimates.

-

•

The sixth column (here labelled EBIC) shows one out of four information criteria. The ic(string) option controls which information criterion is displayed, where string can be replaced with ‘aic’, ‘aicc’, ‘bic’, and ‘ebic’ (the default).

-

•

R-sq shows the value.

-

•

The final column shows which predictors are entered or removed from the model at each knot. The order in which predictors are entered into the model can be interpreted as an indication of the relative predictive power of each predictor.

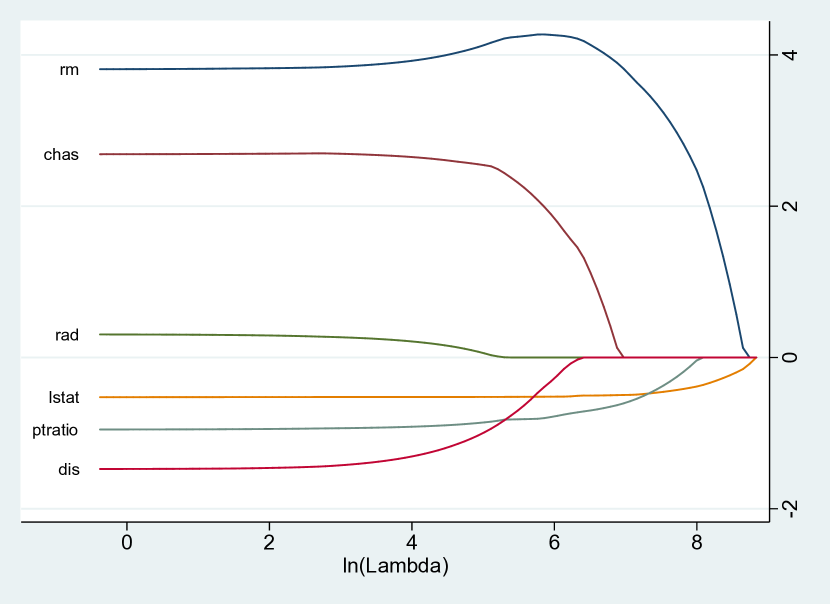

Since lambda() is not specified, lasso2 obtains the coefficient path for a default list of values. The largest penalty level is 6858.99, in which case the model does only include the constant. Figure 5 shows the coefficient path of the lasso for selected variables as a function of .252525Figure 5 was created using the following command:

. lasso2 medv crim-lstat, plotpath(lnlambda) plotopt(legend(off)) plotlabel plotvar(rm chas rad lstat ptratio dis)

lasso2 supports model selection using information criteria. To this end, we use the replay syntax in combination with the lic() option, which avoids that the full model needs to be estimated again. The lic() option can also be specified in the first lasso2 call. In the following example, the replay syntax works similar to a post-estimation command.

-

. lasso2, lic(ebic) Use lambda=16.21799867742649 (selected by EBIC). Selected Lasso Post-est OLS crim -0.1028391 -0.1084133 zn 0.0433716 0.0458449 chas 2.6983218 2.7187164 nox -16.7712529 -17.3760262 rm 3.8375779 3.8015786 dis -1.4380341 -1.4927114 rad 0.2736598 0.2996085 tax -0.0106973 -0.0117780 ptratio -0.9373015 -0.9465246 b 0.0091412 0.0092908 lstat -0.5225124 -0.5225535 Partialled-out* _cons 35.2705812 36.3411478

Two columns are shown in the output; one for the lasso estimator and one for post-estimation OLS, which applies OLS to the model selected by the lasso.

K-fold cross-validation with cvlasso

Next, we consider -fold cross-validation.

-

. set seed 123 . cvlasso medv crim-lstat K-fold cross-validation with 10 folds. Elastic net with alpha=1. Fold 1 2 3 4 5 6 7 8 9 10 Lambda MSPE st. dev. 1 6858.9855 84.302552 5.7124688 2 6249.6522 77.022038 5.5626292 3 5694.4503 70.352232 5.3037622 (Output omitted.) 30 461.89442 27.034557 3.5821586 31 420.86099 26.695961 3.5812873 32 383.47286 26.365176 3.5552884 ^ 33 349.40619 26.095202 3.5350981 34 318.36591 25.857426 3.51782 (Output omitted.) 62 23.529539 23.421433 3.1339813 63 21.43924 23.419627 3.131822 64 19.534637 23.418936 3.1298343 * 65 17.799234 23.419177 3.1280902 66 16.217999 23.419668 3.1266572 (Output omitted.) 98 .82616724 23.441147 3.1134727 99 .75277282 23.441321 3.1134124 100 .68589855 23.441481 3.1133575 * lopt = the lambda that minimizes MSPE. Run model: cvlasso, lopt ^ lse = largest lambda for which MSPE is within one standard error of the minimal MSPE. Run model: cvlasso, lse

The cvlasso output displays four columns:

the index of (i.e., ),

the value of ,

the estimated mean squared prediction error,

and the standard deviation of the mean squared prediction error.

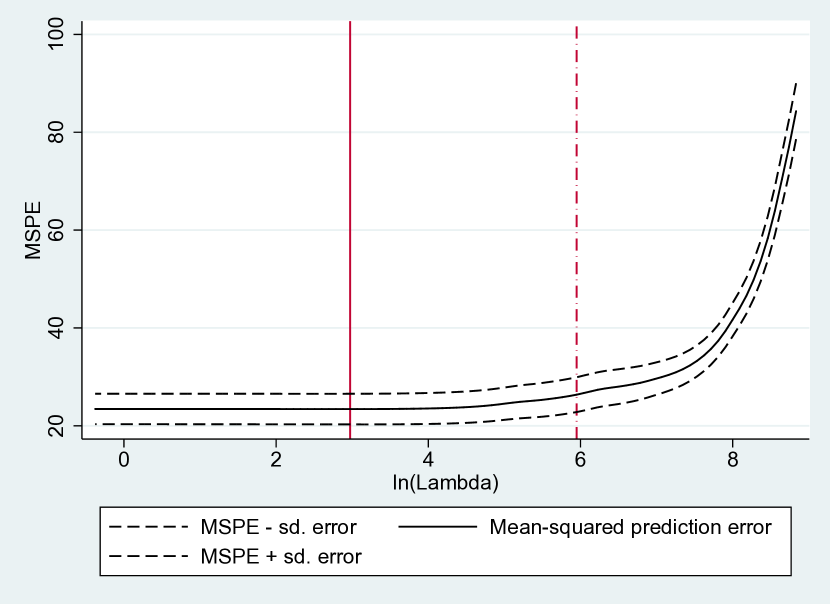

The output indicates the value of that corresponds to the lowest MSPE with an asterisk (*). We refer to this value as . In addition, the symbol ^ marks the largest value of that is within one standard error of , which we denote as .

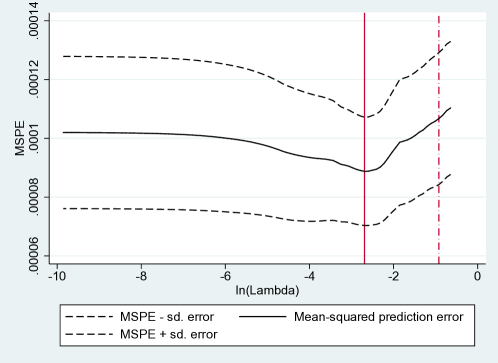

The mean squared prediction is shown in Figure 5, which was created using the plotcv option. The graph shows the mean squared prediction error estimated by cross-validation along with one standard error. The continuous and dashed vertical lines correspond to and , respectively.

To estimate the model corresponding to either or , we use the lopt or lse option, respectively. Similar to the lic() option of lasso2, lopt and lse can either specified in the first cvlasso call or after estimation using the replay syntax as in this example:

-

. cvlasso, lopt Estimate lasso with lambda=19.535 (lopt). Selected Lasso Post-est OLS crim -0.1016991 -0.1084133 zn 0.0428658 0.0458449 chas 2.6941511 2.7187164 nox -16.6475746 -17.3760262 rm 3.8449399 3.8015786 dis -1.4268524 -1.4927114 rad 0.2683532 0.2996085 tax -0.0104763 -0.0117780 ptratio -0.9354154 -0.9465246 b 0.0091106 0.0092908 lstat -0.5225040 -0.5225535 Partialled-out* _cons 35.0516465 36.3411478

Rigorous penalization with rlasso

Lastly, we consider rlasso. The program rlasso runs an iterative algorithm to estimate the penalty level and loadings. In contrast to lasso2 and cvlasso, it reports the selected model directly.

-

. rlasso medv crim-lstat, supscore Selected Lasso Post-est OLS chas 0.6614716 3.3200252 rm 4.0224498 4.6522735 ptratio -0.6685443 -0.8582707 b 0.0036058 0.0101119 lstat -0.5009804 -0.5180622 _cons * 14.5986089 11.8535884 *Not penalized Sup-score test H0: beta=0 CCK sup-score statistic 16.59 p-value= 0.000 CCK 5% critical value 3.18 (asympt bound)

The supscore option prompts the sup-score test of joint significance. The -value is obtained through multiplier bootstrap. The test statistic of 16.59 can also be compared to the asymptotic 5% critical value (here 3.18).

7.2 Time-series data

A standard problem in time-series econometrics is to select an appropriate lag length. In this sub-section, we show how lassopack can be employed for this purpose. We consider Stata’s built-in data set lutkepohl2.dta, which includes quarterly (log-differenced) consumption (dln_consump), investment (dln_inv) and income (dln_inc) series for West Germany over the period 1960, Quarter 1 to 1982, Quarter 4. We demonstrate both lag selection via information criteria and by -step ahead rolling cross-validation. We do not consider the rigorous penalization approach of rlasso due to the assumption of independence, which seems too restrictive in the time-series context.

Information criteria

After importing the data, we run the most general model with up to 12 lags of dln_consump, dln_inv and dln_inc using lasso2 with lic(aicc) option.

-