An Accelerated Fitted Value Iteration Algorithm for MDPs with Finite and Vector-Valued Action Space

Abstract

This paper studies an accelerated fitted value iteration (FVI) algorithm to solve high-dimensional Markov decision processes (MDPs). FVI is an approximate dynamic programming algorithm that has desirable theoretical properties. However, it can be intractable when the action space is finite but vector-valued. To solve such MDPs via FVI, we first approximate the value functions by a two-layer neural network (NN) with rectified linear units (ReLU) being activation functions. We then verify that such approximators are strong enough for the MDP. To speed up the FVI, we recast the action selection problem as a two-stage stochastic programming problem, where the resulting recourse function comes from the two-layer NN. Then, the action selection problem is solved with a specialized multi-cut decomposition algorithm. More specifically, we design valid cuts by exploiting the structure of the approximated value functions to update the actions. We prove that the decomposition can find the global optimal solution in a finite number of iterations and the overall accelerated FVI is consistent. Finally, we verify the performance of the FVI algorithm via a multi-facility capacity investment problem (MCIP). A comprehensive numerical study is implemented, where the results show that the FVI is significantly accelerated without sacrificing too much in precision.

Key words: Markov decision process; finite and vector-valued action space; approximate dynamic programming; decomposition algorithm; multi-facility capacity investment problem

1 Introduction

Sequential decision problems under uncertainty are common in the community of production and operations management. In these problems, decision makers observe uncertain parameters and make decisions alternately and sequentially. Such problems can be found in inventory control (Feng et al. 2015), capacity investment (Zhao et al. 2018), patient scheduling (Yu et al. 2020), revenue management (Luo et al. 2016), to name a few.

Markov decision process (MDP) is one prevalent method to model sequential decision problems, and the MDP models, with either infinite or finite horizon, can be solved via value iteration (VI). VI is a dynamic programming (DP)-based algorithm which uses lookup table representations of the value functions and solve it in a recursive manner. However, VI becomes intractable when the state space of the MDP is multi-dimensional or continuous. To address this issue, one can use approximation.

Fitted value iteration (FVI), or approximate value iteration in some literature, is developed from the traditional VI. In FVI, the value functions are firstly approximated via some approximators, such as linear/piecewise linear functions, polynomial functions, or neural networks (NNs). The algorithm then proceeds via solving the Bellman equations recursively using the approximated value functions, instead of its exact representations. This type of algorithms is also known as approximate dynamic programming (ADP). Munos and Szepesvári (2008) has provided desirable theoretical supports for FVI by showing when this algorithm will yield good policy. More specifically, if the approximators are rich enough and the MDP models satisfy some mild conditions, we can achieve -optimal policy with high probability.

Though the FVI algorithm has desirable theoretical properties, it still has limitations in practice. That is, it assumes that the underlying MDP has a finite action space so that we can enumerate all possible actions. For a sample-based FVI, we need to solve the action selection problems for each state sample in each period once the value functions are approximated. This, however, can be extensively time-consuming when the action space is finite but vector-valued.

Our main contribution in this paper addresses the tension between the theory and solvability of FVI in the context of MDPs with finite and vector-valued action space by developing a novel acceleration scheme for the action selection procedure. Our acceleration algorithm for the action selection procedure requires that the transition function of the MDP model is linear with respect to the actions. This type of models are common in practice; inventory control problems, capacity expansion problems (Zhao et al. 2017), or dynamic assignment problems (Spivey and Powell 2004) all fall into this community.

We first propose a neural network-based FVI (abbreviated as NN-FVI) where the value functions are approximated via a two-layer NN with rectified linear units (ReLU) being activation functions. We verify that this choice of approximator is rich enough so that our FVI is consistent with some mild assumptions of the MDP. Then, we recast the action selection procedure of FVI as a two-stage stochastic programming model, where the recourse value function is returned from the NNs and so it may be non-concave. A two-stage stochastic programming with non-concave recourse function is notoriously difficult when we are maximizing the objective function. To address this, we further exploit the structure of the recourse function and propose a customized decomposition algorithm. In the algorithm, several types of valid inequalities are added to speed up the search of the optimal action. We prove that this acceleration scheme can converge to the optimal action with a finite number of iterations.

To verify the performance of the proposed method, we apply it to a multi-facility capacity investment problem (MCIP). In particular, the capacity of the facilities can either be expanded or contracted, which is different from the exiting models where the capacity investment is irreversible (Zhao et al. 2017, 2018). We model this problem as an MDP and then analyze the properties of its value functions. We solve the model via the proposed FVI method and implement a comprehensive numerical study, where the results show that the FVI is significantly accelerated without sacrificing too much in precision.

The remainder of the paper is organized as below. We review the related work in Section 2. In Section 3, we present some preliminaries about MDP and the main assumptions in our paper. The proposed NN-FVI, along with the analysis of its consistency, are presented in Section 4. Section 5 introduces the proposed multi-cut decomposition algorithm to solve the action selection procedure. An application about multi-facility capacity investment problems, along with the problem analysis and a comprehensive numerical studies, are presented in Section 6. In the last section, we conclude the major findings and arguments of this study. All of our proofs may be found in the Appendix.

2 Related Literature

Sequential decision problems with finite and vector-valued action spaces can be found in capacity expansion problems of engineering systems, where the capacity is usually quantified by the number of production lines, machines, and facilities, which is discrete (Huang and Ahmed 2009, Zhao et al. 2018, Sun and Schonfeld 2015). Similar applications can also be found in multi-item inventory control models (Vairaktarakis 2000, Topan et al. 2010).

Sequential decision problems can be modeled as MDP and solved via ADP if the model has high-dimensional state or action space. The basic idea of ADP is to approximate the value functions or functions via state aggregation (Bertsekas 2012), basic functions approximation (Munos and Szepesvári 2008, Antos et al. 2008, Powell 2011), or sample average approximation (Haskell et al. 2016). Many of the ADPs in the literature assumed that the action space of the MDP is finite, so that we can enumerate all possible actions in the action selection procedure. However, it can be extensively time-consuming to find the optimal action via enumeration when the action space is high-dimensional. Policy gradient algorithms have been proposed to find the optimal action for problems with continuous and high-dimensional action spaces (Lillicrap et al. 2015, Schulman et al. 2015), but this type of methods may not work for derivative-free problems such as MCIPs with discrete capacity. Other methods to handle with the derivative-free problems include direct policy search—the policy of the problem is approximated, for example, via NNs—and the optimization of such policy is done by a black-box optimization (Hu et al. 2017). Jain and Varaiya (2010) approximated the policies via sampling and proposed a simulation-based optimization framework for policy improvements. However, the required number of samples of this type of methods could be large.

We note that multi-stage stochastic programming is another method that can solve sequential decision problems with finite and vector-valued decisions. This method usually models the evolution of the uncertain parameters as a scenario tree, but this may have limitations as the size of the tree grows exponentially with the number of stages (Shapiro et al. 2009). To address this issue, stochastic dual dynamic integer programming is proposed, and it combines the sampling technique with a nested decomposition scheme to find the optimal policy (Zou et al. 2018). Another stream of methods is the decision rule-based methods, where the policy of the sequential decision problems are approximated via a specific class of functions, including linear (Kuhn et al. 2011), piecewise linear (Georghiou et al. 2015), binary functions (Bertsimas and Georghiou 2018), or nonparametric approach based on Gaussian processes (Defourny et al. 2013). However, these methods usually require the objective functions of the models being convex or linear. Zhao et al. (2018) proposed an if-then decision rule to solve a capacity expansion problem with a non-convex objective function and vector-valued decisions, but the optimality of the solution is not guaranteed.

3 Preliminaries

We consider discounted finite horizon Markov decision processes (MDP) with the following ingredients:

-

•

planning horizon with (with );

-

•

state space (possibly continuous);

-

•

action space (vector-valued and finite, but possibly very large);

-

•

exogenous uncertainty (possibly continuous);

-

•

state transition function ;

-

•

reward functions ;

-

•

discount factor .

We assume the initial state is known. At time , the current state is , the current action is , and the reward is . Let denote the exogenous information that arrives at the end of period (which is independent of and ) and drives the next state transition to state .

We gather our main assumptions below for easy reference.

Assumption 1.

The state space and the support are closed and bounded. The action space satisfies . The reward functions satisfy for all and .

Our assumption that the actions are non-negative vectors is without loss of generality, since we can suitably translate any finite set of actions. We further assume that the reward function is Lipchitz in .

Assumption 2.

There exists such that for all , , and .

Next we assume that the state transition function is affine in , which is the case for many problems (e.g. inventory control, portfolio optimization, and capacity investment problems). This special structure plays a material role in our upcoming algorithm.

Assumption 3.

The state transition function is affine in , i.e., where and .

The following assumption is for simplicity; we can do without it at the expense of more complicated notation.

Assumption 4.

The exogenous information is i.i.d.

Under Assumption 4, there is a transition kernel defined by

for all measurable subsets (this transition kernel is stationary because are i.i.d.).

Assumption 5.

The transition kernel admits a uniformly bounded density, i.e., there exists such that for all and .

Let be the set of all deterministic Markov policies where for all . We seek a policy that maximizes the cumulative reward:

| (1) |

We denote an optimal policy as (it is not necessarily unique).

4 Neural Network-based Fitted Value Iteration Algorithm

When the state space is large or continuous, it is impossible to exactly solve Eq. (2) because of the curse of dimensionality (see Powell (2011)). To respond to this challenge, we will use FVI (see Munos and Szepesvári (2008)), which is a scheme for approximately solving Eq. (2) based on randomly sampling from the state space, estimating the value function at the sampled states, and then doing function fitting to generate an approximate value function on the entire state space.

FVI depends on two main ingredients: the value function approximation architecture and the state space sampling distribution. Let be a set of adjustable parameters which control the value function approximation. For each , let for all be parametrized approximate value functions on (e.g. linear basis functions, polynomial basis functions, radial basis functions, etc.). Next we introduce the state space sampling distribution , a probability distribution on the state space . In each iteration, we will randomly generate an i.i.d. sample of size indexed by .

Let us describe FVI starting with the terminal period . First, a sample is drawn from according to , and the values are computed exactly according to Eq. (2) for (they can only be computed exactly in the terminal period when there is no expected future value). Then, our data set consists of the sampled states and the Bellman estimates .

We want to find the best fit to the data within some tractable class of functions. In period , can be trained by solving the regression problem:

| (3) |

where is a regularization parameter. Regularizing the objective function can sometimes improve the generalization of the function fitting and avoid overfitting.

After solving Problem (3) for period , the algorithm proceeds inductively. In period , we generate samples of the state space from , denoted by . Then, we need to simulate state transitions for each of these states, for every possible action . For each state sample , we generate via Monte Carlo simulation, and then for any we get a sample of the next state visited. We let index these sampled state transitions such that . Then, we can calculate using the trained function , and compute by solving Problem (5). The details of the algorithm are summarized in Algorithm 1.

-

•

Step 0: Initialize , , initial state , and the MDP parameters. Set .

-

•

Step 1: Draw samples independently from the state space and generate samples to calculate future transitions for all .

-

•

Step 2: Compute for ,

(4) -

•

Step 3: Given samples , fit the approximate value functions

(5) -

•

Step 4: If , set and go to Step 1; otherwise, generate samples to calculate future transitions , return

and terminate the algorithm.

There are two questions that need to be answered about the above FVI algorithm. First, what approximation architecture should we use for the value functions? Second, the action selection problem in Eq. (4) optimizes over a multi-dimensional action space . It is difficult to solve this problem via direct enumeration, so how can we do this optimization? We will answer both questions. Next, in Subsection 4.1 we choose a value function approximation architecture based on NNs. Then, in Section 5 we introduce a decomposition algorithm to accelerate the action selection in Problem (4).

4.1 Two-layer Neural Network with ReLU

There is a well-known exploration vs. exploitation trade-off in general function approximation problems. One can use a rich functional family, such as deep NNs, to approximate the value functions in Eq. (2). However, the training and inference may then be time-consuming given that we need to solve the action selection problem times. In this paper, we propose an FVI, where the value functions are approximated via a two-layer NN with rectified linear units (ReLU). As we will see, this approximation is powerful enough to reach any desired accuracy in our problem, as long as sufficient neurons are provided. We will see also that this approximation leads to efficient optimization in the action selection problem.

A two-layer NN consists of inputs (the state ), one hidden layer for intermediate computations, and a single output (the approximate value of the value function). Let index the neurons in the hidden layer of our network, so the two-layer NN is

where and are the adjustable weights of the input layer and the hidden layer respectively, and is the activation function for neuron . We choose the activation functions to be ReLU, i.e.,

which are themselves piecewise linear. The architecture of the NN is shown in Figure 1.

The adjustable weights for the input of neuron in include and a vector of (the dimension of ) adjustable coefficients for all . Let denote the vector of all adjustable weights for the input layer and let denote the vector of the adjustable weights for the output of the hidden layer. We then let succinctly denote all parameters for the period value function approximation. The NN at time is then a function of the input and the adjustable weights :

| (6) |

We use the specific approximation in Eq. (6) in Step 3 of Algorithm 1. From now on, we refer to our algorithm as NN-based FVI (NN-FVI).

4.2 Consistency of the algorithm

In this subsection, we show that our customized NN is powerful enough to approximate the value funtions of our MDP. Specifically, we show that NN-FVI is consistent.

First, we show that the value functions are Lipschitz continuous under our assumptions.

Proposition 1.

We then define the class

of -Lipschitz functions. The approximation power of a function class on with respect to is measured by the inherent Bellman error (see Munos and Szepesvári (2008)):

for . Since , if is small then the function class contains a good approximation of . If a sequence satisfies , then it is universal (Antos et al. 2007). This condition implies that the inherent approximation error between the two function spaces converges to zero as becomes “richer”.

The richness of an NN is quantified by the number of layers and weights (Bartlett et al. 2019). The approximation power of our customized two-layer NN increases with the number of neurons, and we have the following result about its approximation quality.

Lemma 1.

The two-layer NN with ReLU activation functions is a universal approximator.

Given Assumptions 1 and 5, the consistency of NN-FVI follows from (Munos and Szepesvári 2008, Corollary 4). We state this result below and present its detailed proof in Appendix A.

Theorem 1.

Remark 1.

Theorem 1 confirms the consistency of NN-FVI. However, the NN training problem Eq. (5) in Algorithm 1 is non-convex. Fortunately, it has been demonstrated numerically that the chance of getting stuck at a poor local minimum decreases as the size of the NN increases. In addition, when the NN is large enough, finding the global minimum may also be unnecessary as it often leads to overfitting (Choromanska et al. 2014).

5 Accelerate the Action Selection Procedure in NN-FVI

In NN-FVI, once the approximate value function in time has been fitted, one needs to solve Problem (4) (the action selection problem). This problem can in principle be solved by enumerating all possible actions since is finite (just the brute-force method). However, we are concerned with the situation where the action space is very large so this method is not practical for our purposes. For example, consider a capacity expansion problem with five facilities, each of which can install units of capacity (e.g. production lines). The complexity of brute-force action selection is for each instance of the action selection problem, which makes the overall FVI algorithm time-consuming. To address this issue, we formulate the action selection problem as a two-stage stochastic programming problem. This transformation allows us to achieve a speed up with a specialized decomposition algorithm.

5.1 Formulation of the Action Selection Problem

For period , suppose we have already trained the NN in time and computed its adjustable weights in Step 3 of Algorithm 1. The upcoming procedure is the same for each sampled state in , so with some abuse of notation we suppress the dependence of the coefficients and parameters on the particular sampled state. Instead, we just let denote a specific state sample in , and we write for all to denote samples of future transitions that are generated via Monte Carlo simulation given a specific state-action pair .

We define to be the empirical recourse function given action and and the next state samples in , defined by:

| (7) |

Then, Problem (4) which computes is equivalent to:

| (8) |

Note that is a known state sample and is a constant, so is the only decision variable in Problem (8). This problem can be viewed as a two-stage stochastic programming problem with a simple recourse function: the first-stage is to determine the action , and then the recourse function returns the expectation of the future reward based on the NN trained in time .

Problem (8) has two notable properties:

-

Property 1. The recourse function is complete; that is, given any , the recourse is not empty.

-

Property 2. The recourse function can be decomposed into a sum indexed by , given any .

Given these properties, one may prefer to decompose Problem (8) and then update the decisions by a cut generation method (e.g. Benders decomposition), especially when is large. This type of algorithm is based on constructing some valid inequalities for the feasible region of Problem (8). We recall the hypograph of the recourse function is:

Our procedure is based on constructing valid inequalities for the hypograph of the recourse function.

Definition 1.

An inequality is valid for the set if

A cut generation algorithm approximates the hypograph of Problem (8) via some valid cuts iteratively. Let index the iterations of the algorithm, and let denote the optimal solution of the first-stage problem in the th iteration. The approximate first-stage problem in the th iteration is of the general form:

| (9a) | |||||

| s.t. | (9b) | ||||

where the inequality constraints are the cuts constructed so far. The decomposition procedure is as follows:

-

1.

First, we solve the first-stage problem and compute in the th iteration.

-

2.

Then, we construct a valid inequality given , add it into the first-stage problem, and update the first-stage decision in the th iteration.

-

3.

The algorithm is run iteratively and the approximation of the recourse function is improved via valid inequalities from above.

If the recourse function is concave in , then we can compute a supporting hyperplane of the hypograph of the recourse function at any and this hyperplane would be a valid inequality. In this situation, the cut generation algorithm behaves exactly like Benders decomposition.

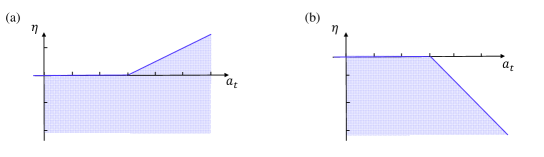

However, since the activation function of our NN is ReLU, the recourse function may not be concave in . As can be seen in Fig. 2, the hypograph of neuron is a convex set if . On the other hand, if , then the hypograph is not convex in which case the objective of Problem (8) may fail to be concave with respect to . The sign of does not effect convexity of the hypograph. We have the following property.

-

Property 3. The recourse function in Eq. (7) is not necessarily concave in if there exists any neuron such that .

Based on these observations, we separate the neurons with positive and non-positive weights into different sets:

Then, we may define the hypographs

corresponding to the output of the neurons with positive/non-positive weights, respectively.

In the following subsections, we design valid cuts for and separately, and find the optimal action via a decomposition algorithm.

5.2 Valid Cuts for the Action Selection Problem

5.2.1 Valid cuts for

In this subsection, we construct valid cuts for neurons with negative weights (i.e., for ) by using gradient information. Suppose we have solved the first-stage problem in the th iteration and computed the first-stage decision . In Problem (8), the gradient of the output of neuron at point can be computed directly, and the corresponding supporting hyperplane is a valid cut for since it is convex.

Let be the indicator function for the positive reals where if and otherwise. We propose the following cuts for neurons with negative weights:

| (10) |

where:

Note that and depend on the index .

Proposition 2.

Cut (10) is a valid inequality for .

5.2.2 Valid cuts for

To derive a valid cut for neurons , we need to find a supporting hyperplane for , which is a non-convex set. We propose the following inequality

| (11) |

which is constructed in the following way. First, we write

where and , and we define sets

Because the function is linear in , its minimum/maximum values can be computed explicitly and are and , respectively. We denote

We then define for all the constants

and

to complete the construction of Cut (11). This cut can be computed easily because of its linear structure. In addition, Cut (11) is independent of the current and so we only need to compute it once for a specific state sample in .

Proposition 3.

Cut (11) is a valid inequality for .

Remark 2.

When training an NN, one may prefer to use leaky ReLU, instead of ReLU, as activation functions to avoid the vanishing gradient issue (or the so-called “dying ReLU” problem). Our valid cuts are also applicable to NNs with leaky ReLU after some minor modification.

We sum up Cuts (10) (for negative neurons) and (11) (for positive neurons) to immediately get the following result.

Corollary 1.

The following cut is a valid inequality for :

| (12) |

5.2.3 Integer Optimality Cuts

In each iteration of the decomposition algorithm, we add Cuts (12) to the first-stage problem. These cuts are valid, but may not be tight. To ensure global optimality, we also introduce the integer optimality cuts from (Laporte and Louveaux 1993) into our algorithm. When the first-stage decision is solved in the th iteration, an integer optimality cut is constructed and added to the first-stage problem. This cut exactly recovers the recourse function value corresponding to if the first-stage decision is equal to , and it recovers an upper bound otherwise.

To formulate integer optimality cuts, let be an upper bound on the value of the recourse function. Also define the function where if and otherwise (we may need to transform the general integer variables into binary variables to properly formulate , the details are in the Appendix). From (Laporte and Louveaux 1993), we then obtain the following integer optimality cuts:

where is given by Eq. (7). This cut recovers if , i.e., ; otherwise, it recovers an upper bound.

5.3 A Multi-Cuts Decomposition Algorithm

We now present our complete multi-cuts decomposition (MCD) algorithm for solving Problem (8). In our algorithm, Cuts (10) and (11) exploit the structure of the recourse function, and the integer optimality cuts ensure global convergence. We continue to let index the iterations of our decomposition algorithm and denote the optimal solution of the first-stage problem in the th iteration. The first-stage problem in the th iteration of the MCD algorithm is

| () | |||||

| s.t. | (13) | ||||

| (14) | |||||

There are two types of cuts in the above formulation. Cuts (13) are the integer optimality cuts generated up to iteration , and Cuts (14) follow directly from Cuts (12).

Our algorithm proceeds by adding Cuts (13)–(14) to Problem () simultaneously to update the first-stage decision. An upper bound can be obtained by solving Problem () in the th iteration, and a lower bound can be obtained from the objective value of the best-found decision up to iteration . One can therefore terminate the algorithm when the difference between the upper and lower bounds falls below a preset tolerance. The finite convergence of the MCD algorithm can be established as follows.

Theorem 2.

The MCD algorithm yields a globally optimal solution in a finite number of iterations.

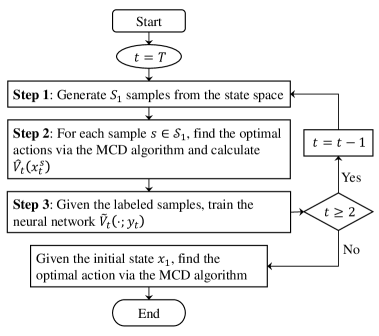

Cuts (13) are the mechanism which ensures convergence to a global optimum. However, they can theoretically cause slow convergence when the problem size is large. Yet, as we will see in our numerical study, the MCD algorithm usually finds a high-performance solution (or even the optimal solution) in a relatively small number of iterations well before the gap between the lower/upper bound reaches the preset tolerance. Therefore, one can choose a suitable maximum number of iterations to trade off between performance and computational budget. The flow of NN-FVI combined with MCD is summarized in Figure 3, and the detailed procedure of MCD is presented in Algorithm 2.

6 Application: Multi-facility Capacity Investment Problem

We apply NN-FVI with MCD to solve a generic multi-facility capacity investment problem (MCIP) with discrete capacity decisions. Strategic capacity decisions are important to production firms because of the high expenditures entailed and the uncertainty about the future business environment (e.g. customer demand). To deal with uncertainty, it is wiser to adjust the capacity periodically as new information about the uncertainty is revealed, instead of establishing facilities with large capacities at the very beginning of the planning horizon. Real options analysis gives a framework to evaluate the value of a system with dynamically adjusted capacity. Namely, in each period, decision makers have the right (but not the obligation) to invest or salvage the capacity once new demand information is revealed (Dixit and Pindyck 1994, Huang and Ahmed 2009, Cardin et al. 2017b, Taghavi and Huang 2018).

To solve this problem, Cardin et al. (2017a) and Zhao et al. (2018) have earlier proposed a decision rule-based multi-stage stochastic programming method, where the policy space of the problem is approximated by a family of if-then functions. The performance of the decision rule-based method is promising, but it only allows for capacity expansion decisions. We go in a different direction here and consider an MCIP where the capacity can be both expanded and contracted. We formulate the MCIP as a finite horizon MDP, and analyze the properties of its value functions. Then, we solve the problem via NN-FVI with MCD. Our comprehensive numerical experiments help to verify the performance of our algorithm.

6.1 Problem Description

We consider a multi-stage capacity investment problem with customers and facilities . In each period, customer demand is observed and then assigned to the various facilities to be satisfied. The objective is to maximize the net present value (NPV) by determining the optimal capacity investment plan and demand allocation plan over the planning horizon . Let denote the random demand from customer in period , and let denote the vector of customer demands in period . Let denote a realization of , and the corresponding vector of realizations is . Define to be the support of the customer demand.

Let be the initial capacity vector, and let be the installed capacity vector at the end of period . Define to be a vector of capacity limits, so that the domain of the capacity is

We summarize the notation for our model in Table 1.

Our main assumptions on the MCIP are listed below.

Assumption 6.

The demand process is Markov. Without loss of generality, is independent of the capacity decisions for all , and is known.

Under Assumption 6, we may let denote the conditional probability distribution for demand so that for all and . If demand is continuous, we assume that has a conditional probability density.

Assumption 7.

The demand is non-negative and bounded (i.e., there exists such that for all ). If the demand is continuous, the conditional probability densities exist and are Lipschitz continuous for all . Specifically, there exists such that

Assumption 7 is standard since real-world demand is always finite and their variation from one period to the next does not surge to infinity.

Assumption 8.

The decision maker has the option to expand/contract the installed capacity from to at the end of each period , and capacity adjustments are instantaneous.

We assume that the lead time for capacity adjustment (compared to the length of each period) is negligible.

Assumption 9.

The expansion cost and salvage value are linear with respect to the capacity, and the per unit expansion cost is not smaller than the per unit salvage value.

Though we consider an MCIP with linear expansion cost and salvage value, our proposed method can be extended to more general cases whose expansion cost/salvage value are nonlinear. In addition, the resale value of an asset is usually smaller than its purchase price, so the second statement of Assumption 9 is realistic.

| Indices and sets | |

|---|---|

| Index for customers | |

| Index for facility | |

| Index for period | |

| Set of customers, , and | |

| Set of facilities, , and | |

| Set of periods, , and | |

| Parameters | |

| Demand generated from customer in time ; the vector form is | |

| Initial capacity of facility ; the vector form is | |

| Discount factor of time value of money, | |

| Unit revenue from satisfying customer with facility in time | |

| Unit penalty cost for unsatisfied customer in time | |

| Coefficient parameters of per unit expansion cost of facility in time | |

| Coefficient parameters of per unit salvage value of facility in time | |

| Variables | |

| Capacity of facility in time ; the vector form is | |

| Amount of demand allocated from customer to facility in time | |

In each period, we allocate realized demand to the facilities, given the limits of the currently installed capacity . A unit penalty cost is incurred for all unsatisfied demand from customer . Let denote the amount of demand from customer allocated to facility in period , and let be the corresponding revenue. The operating profit in period is given by the following linear program (LP):

| (15a) | |||||

| s.t. | (15b) | ||||

| (15c) | |||||

| (15d) | |||||

The objective in (15a) is to maximize the current rewards, which consist of the revenue minus the penalty for unsatisfied demand. Constraints (15b) and (15c) are the capacity and demand constraints, respectively. Note that the allocation decisions depend on the current state only.

Let and denote the unit expansion cost and unit salvage value for facility respectively. The reward is then

| (16) |

According to Assumption 9, we have for all and .

This MCIP can be modeled as an MDP where the state in period is (i.e., the installed capacity in time and the realized demands) and the action is the adjusted capacity . The state space of our problem is therefore and the action space is for all . Without loss of generality, we assume the initial state for the MCIP is known, and the system salvages all installed capacity at the end of period so . The DP equations for MCIP are then:

| (17a) | ||||

| (17b) | ||||

If the demand has finite support, then complexity of VI for Eq. (17) is , where has dimension and has dimension . For example, consider a system with four customers, three facilities, and planning horizon . If , and customer demand is integer-valued ranging from to , then the complexity of VI is . This observation suggests that VI is intractable even for a medium size MCIP problem. If demand is continuous, then the state space is infinite and VI cannot even be done exactly.

6.2 Problem Analysis

In this subsection, we analyze the value functions of the MCIP corresponding to the DP Eq. (17). Then, we check if NN-FVI can solve the problem properly. We first show that the assumptions in Section 3 are satisfied.

We observe that the value functions for all provided by Eq. (17) are defined over . However, is not a connected set since is finite. In addition, if the demand is discrete, then this aspect of the state space is finite and discrete as well. We wish to extend to its smallest connected superset on which we will construct a set of extended value functions which are easier to analyze.

We first define

It is automatic that . Note that can be either continuous or discrete in the above display. Now, we define extended value functions for all . If can recover the exact values of on , then we can analyze to learn about . The analysis of is easier because is a connected set.

The DP equations for the extended value functions at are:

| (18a) | ||||

| (18b) | ||||

Note that the values of are well-defined for all .

Next we show that the value functions can be recovered from the extended functions on .

Proposition 5.

for all and .

We analyze the structure of the extended value functions by backward induction.

Proposition 6.

Let be the extended value functions defined in Eq. (18).

-

(i)

is piecewise linear.

-

(ii)

Suppose is finite, then is piecewise linear for all .

Remark 3.

Note that for all is not necessarily concave in given . As is concave in given , is concave in given (see the proof in Proposition 6). Yet, may fail to be concave as it is a finite maximum of concave functions.

According to Proposition 6(i), the extended value function is piecewise linear if the capacity is defined over a connected space . However, for , Proposition 6(ii) the value functions are only piecewise linear when the demand is discrete. Fortunately, if the demand is continuous, we can use Monte-Carlo simulation to generate finitely many state transitions to approximate the expectation in Eq. (17). In this setting, the approximate extended value functions will be piecewise linear. However, as observed in Remark 3, we may need to solve a non-convex optimization problem for each .

6.3 Numerical Studies

We now test the numerical performance of NN-FVI in solving MCIP in three parts. First, we compare the performance of the ReLU-based NN-FVI to NNs with other activation functions. This part is intended to verify that the value functions of MCIP have some piecewise linear structure, so that ReLU outperforms other activation functions. Second, we compare the performance of the proposed MCD algorithm with exhaustive enumeration (i.e., the brute-force method) and the integer L-shaped algorithm in the action selection problem in NN-FVI. Third, we combine NN-FVI with MCD and test its performance in a case study where we analyze its economic performance over an inflexible counterpart. The inflexible counterpart does not have the option to change the capacity dynamically. Instead, it is modeled as a two-stage capacity investment problem and it is solved with Benders decomposition (see Zhao et al. (2018) for implementation details). These numerical studies are performed on a workstation with an Intel Xeon 5218 processor and 32 GB RAM in the Matlab R2018a environment. The NNs are trained by the Levenberg–Marquardt algorithm via the NN toolbox of Matlab (Beale et al. 2018).

6.3.1 ReLU Outperforms Other Activation Functions in Solving MCIP

In this subsection, we test the performance of NN-FVI with different types of activation functions, including ReLU, tanH (hyperbolic function), and sigmoid. Here, the action selection problem is solved by the brute-force method as MCD is not applicable for NNs using tanH and sigmoid functions.

In Table 2, we test a small-scale case (Case 1.1) with discrete demands that it is solvable by DP, and compare the approximate objective values obtained from NN-FVI to the exact objective values obtained by DP. As can be seen, the exact ENPV computed by DP is 357.9, and the approximate objective computed by NN-FVI with ReLU is 357.7. However, the approximate ENPVs computed by NN-FVI with tanH and sigmoid activation functions are 441.3 and 628.9 respectively, both of which are far from the exact value.

| Algorithms | Activation fun. | CPU time | Obj. values* | Relative gaps | |

|---|---|---|---|---|---|

| DP | - | 160 s | 357.9 | - | |

| NN-FVI | ReLU | 6 s | 357.7 | <0.1% | |

| NN-FVI | tanH | 10 s | 441.3 | 23.3% | |

| NN-FVI | Sigmoid | 10 s | 628.9 | 75.7% |

*The ENPVs are computed from the approximated objective values directly.

For a larger scale case, DP is not applicable due to the curse of dimensionality. Instead, we benchmark using an inflexible two-stage stochastic capacity investment model. We perform out-of-sample tests on the optimal policies computed by both the inflexible method and NN-FVI, on an identical sample set with 10,000 sample paths; in this case, a better policy should lead to a higher ENPV in the out-of-sample tests. In Table 3, simulation results for a medium-scale case with indicate that the optimal policy computed by NN-FVI with ReLU outperforms the policies computed by NNs with tanH and sigmoid activation functions. Also, the CPU time for NN-FVI with ReLU is much less than NN-FVI with tanH and sigmoid. We suspect this is because the piecewise linear activation functions are easier to use in computation compared to the nonlinear ones. We can conclude that ReLU leads to more accurate NNs compared to tanH and sigmoid.

| Algorithms | Activation fun. | CPU time | ENPV | VoF | |

|---|---|---|---|---|---|

| Inflexible design | - | 306 s | 1530.9 | - | |

| NN-FVI | ReLU | 21 040 s | 1634.9 | 104.0 | |

| NN-FVI | tanH | 25 624 s | 1625.4 | 94.5 | |

| NN-FVI | Sigmoid | 27 452 s | 1518.2 |

6.3.2 The Action Selection Procedure Can be Solved in Reasonable Time

In this subsection, we compare the performance of our MCD algorithm with two alternatives—(1) the brute-force algorithm and (2) the integer L-shaped algorithm. In the integer L-shaped algorithm, only Cuts (13) (integer optimality cuts) are added in each iteration and our valid cuts are not included.

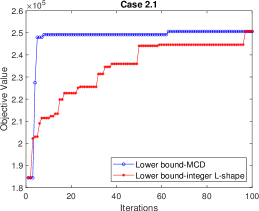

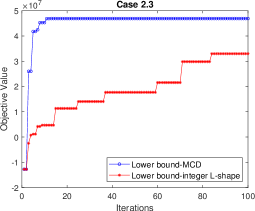

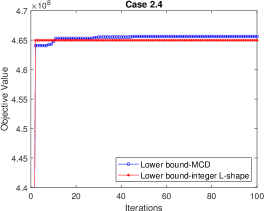

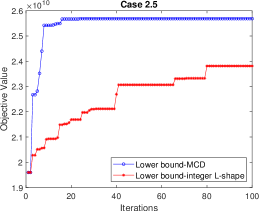

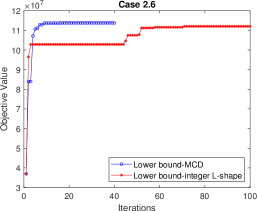

Seven NNs with different sizes are randomly generated to create Cases 2.1–2.7, each is formulated as Problem (8), and then solved by the aforementioned methods. The performance of the algorithms is measured in terms of the CPU time and their best-found objective value achieved before the algorithm is terminated. As can be seen, in Cases 2.1 and 2.2, the CPU time of the brute-force method is around 11 seconds. Both the integer L-shaped algorithm and MCD converge to the optimal solution in around 6-7 seconds, which is slightly faster than the brute-force method. This is not surprising since the brute-force method is plausible when the problem size is small. By increasing the number of facilities from three to five, we can see from Table 4 that the CPU time of the brute-force method increases significantly. On the contrary, MCD achieves the global optimal/near-optimal solutions within 10 seconds. Based on this evidence, we speculate that the CPU time of the MCD algorithm might be much less than the brute-force method in even larger scale cases.

| Algorithms | Stop criterion* | Iterations | CPU time | Exp. profits | Relative gaps | |

| Case 2.1 | Brute-force | - | - | 11.3 s | 2506.0 | - |

| () | Integer L-shaped | 0.35%/100 steps | 100 | 6.7 s | 2506.0 | 0% |

| MCD | 0.35%/100 steps | 100 | 7.8 s | 2506.0 | 0% | |

| Case 2.2 | Brute-force | - | - | 11.2 s | 6731.9 | - |

| () | Integer L-shaped | 0.35%/100 steps | 100 | 6.5 s | 6721.6 | 0.15% |

| MCD | 0.35%/100 steps | 100 | 7.6 s | 6731.9 | 0% | |

| Case 2.3 | Brute-force | - | - | 47.9 s | - | |

| () | Integer L-shaped | 0.35%/200 steps | 200 | 18.7 s | 33.11% | |

| MCD | 0.35%/100 steps | 100 | 8.5 s | <0.1% | ||

| Case 2.4 | Brute-force | - | - | 48.6 s | - | |

| () | Integer L-shaped | 0.35%/100 steps | 100 | 14.7 s | 0.26% | |

| MCD | 0.35%/100 steps | 100 | 8.3 s | 0.13% | ||

| Case 2.5 | Brute-force | - | - | 643.4 s | - | |

| () | Integer L-shaped | 0.35%/100 steps | 100 | 14.3 s | 7.30% | |

| MCD | 0.35%/100 steps | 100 | 11.0 s | 0% | ||

| MCD | 0.35%/50 steps | 50 | 4.3 s | 0% | ||

| Case 2.6 | Brute-force | - | - | 764.7 s | - | |

| () | Integer L-shaped | 0.35%/100 steps | 100 | 55.2 s | 1.54% | |

| MCD | 0.35%/100 steps | 40 | 4.4 s | 0% | ||

| Case 2.7 | Brute-force | - | - | 815.5 s | - | |

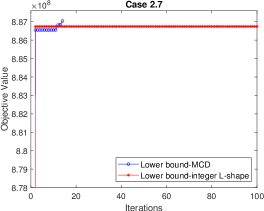

| () | Integer L-shaped | 0.35%/100 steps | 100 | 66.2 s | <0.1% | |

| MCD | 0.35%/100 steps | 14 | 1.6 s | <0.1% |

*The algorithm is stopped if the relative gap between the lower bound and the upper bound is smaller than 0.35% or the total number of iteration reaches 100.

We now compare the convergence of MCD and the integer L-shaped algorithm. As can be seen, MCD converges to the global optimum in fewer iterations than the integer L-shaped algorithm. In Case 2.1, where the number of facilities is , the integer L-shaped method can converge to the global optimum within 100 iterations. However, when the number of facilities increases, the best-found solutions by the integer L-shaped method within 100 iterations are sub-optimal. In particular, the relative gaps of the best-found objective values and the global optima for Case 2.3 (), Case 2.5 (), and Case 2.6 () are , , and respectively. In contrast, MCD can find the global optimum (or a near-optimal solution) within 100 steps. These numerical results verify that MCD ensures faster convergence by using the valid cuts with gradient information (i.e., Cuts (14)).

6.3.3 Verify the Performance of NN-FVI with MCD in a Real Case

This case study on a multi-facility waste-to-energy (WTE) system is adapted from (Zhao et al. 2018). In (Zhao et al. 2018), the system can only expand capacity, while in this paper we also allow capacity to contract. In addition, we adjust the original case into a smaller one where we can perform practical sensitivity analysis. The WTE system has four candidate sites located in different sectors. The facilities at each site are able to dispose of food waste collected from each sector by using an anaerobic digestion technique, which transforms the food waste into electricity. Undisposed waste will be subjected to further treatment via landfill, incurring greater disposal costs and penalties. The revenue comes from selling the electricity and the salvage value of the contracted capacity. The costs consist of the disposal, penalty, and transportation costs, as well as capacity expansion costs and land rental fees (incurred once the capacity is non-zero). The data and parameters of the case study are found in (Zhao et al. 2018).

Sensitivity analysis is implemented on the ratio of the per unit salvage value with the per unit expansion cost (S/E ratio) . If the S/E ratio is one, it means that the salvage value for per unit capacity is equivalent to the per unit expansion cost. As can be seen in Table 5, the flexible design outperforms the inflexible one under most parameter settings. When and the S/E ratio is 0, the expected net present value (ENPV) of the inflexible design is 23.9 million, while the ENPV of the flexible design is 35.5 million. In this case, flexibility improves the system performance by 48.5%. However, the percentage improvement of the system with a flexible design over an inflexible design decreases as the S/E ratio increases. The improvement decreases to 20.3% when the S/E ratio increases to 0.99. On the other hand, we see that if the discount factor and the S/E ratio are both close to one, then the improvement is only . This is reasonable since in this case the decision maker can establish facilities with large capacity in the beginning and then salvage all of them in the last period, without suffering a significant loss. In other words, the inflexible model may yield a high-performance solution for the problem when both and the S/E ratio are close to one.

| ENPV | |||||

|---|---|---|---|---|---|

| Inflexible design | NN-FVI | ||||

| 0.862 | 0 | 23.9 | 35.5 | 11.6 | 48.5 |

| 0.25 | 33.7 | 45.7 | 12.0 | 35.6 | |

| 0.50 | 43.8 | 58.0 | 14.2 | 32.4 | |

| 0.75 | 54.3 | 66.9 | 12.6 | 23.2 | |

| 0.99 | 64.9 | 78.1 | 13.2 | 20.3 | |

| 0.923 | 0 | 93.8 | 110.0 | 16.2 | 17.3 |

| 0.25 | 115.1 | 131.1 | 16.0 | 13.9 | |

| 0.50 | 137.2 | 156.8 | 19.6 | 14.3 | |

| 0.75 | 160.4 | 176.0 | 15.6 | 9.7 | |

| 0.99 | 184.0 | 194.8 | 10.8 | 5.9 | |

| 0.99 | 0 | 204.3 | 224.4 | 20.1 | 9.8 |

| 0.25 | 248.9 | 268.0 | 19.1 | 7.7 | |

| 0.50 | 295.2 | 312.3 | 17.1 | 5.8 | |

| 0.75 | 345.9 | 361.1 | 15.2 | 4.4 | |

| 0.99 | 398.4 | 402.4 | 4.0 | 1.0 | |

6.4 Extensions of NN-FVI with MCD

We focus on solving MCIP in this paper, but our method is applicable to many other problems where the action space is finite and high-dimensional. We mention some variations where our method can still be used.

-

1.

Lead time. In MCIPs where the capacity adjustment has nonzero lead time, we can express capacity under construction as part of the state variables. In this case, we may need additional inputs for our two-layer NN, but the action selection problem is unaffected.

-

2.

Uncertain rewards/costs. The proposed method can also solve MCIPs with uncertain parameters. For example, if the rewards are uncertain, then we can model them as state variables.

-

3.

Different types of capacity adjustment costs. If the capacity adjustment costs contain fixed costs or are non-convex, the proposed MCD algorithm can still solve the action selection problem. However, if the costs are non-convex in the capacity decisions then we may need to solve a mixed-integer nonlinear programming problem to update the first-stage decision in each iteration.

Earlier in this paper, we compared the economic performance of NN-FVI to an inflexible two-stage MCIP model via out-of-sample tests. However, as indicated by Zhao et al. (2018), the complexity of the out-of-sample tests for ADP can be even greater than solving the original problem. One possible way to simplify the out-of-sample tests is to approximate the policy of the NN-FVI offline. For example, after solving the action selection problem for each state sample, we can do function fitting on these samples and then approximate the policy. When the policy is approximated offline, it does not add to the cost of the original NN-FVI algorithm. Then, we can use this approximate policy in the out-of-sample tests. In this case, the out-of-sample tests are more tractable and it is easier to implement the resulting policy in practice. Future work can consider how to approximate the policy to achieve high precision in out-of-sample tests.

7 Conclusion

In this paper, we solve a class of MDPs with a continuous state space and a large but finite and high-dimensional action space. An NN-FVI algorithm is proposed, where the value functions are approximated with a two-layer NN with ReLU activation functions. The consistency of NN-FVI is also formally proved. Since the action selection procedure of NN-FVI is time-consuming, we formulate it as a two-stage stochastic programming problem with a non-concave recourse function, and we design an MCD algorithm to solve it. We verify that the MCD algorithm converges to the global optimum in a finite number of iterations. We test our new algorithms on a capacity investment problem. Our numerical studies show that the proposed acceleration method significantly speeds up the action selection problem when compared with the brute-force method and the integer L-shape algorithm.

We solve discounted finite horizon MDPs in this paper, but our results on NN-FVI with MCD also extend to infinite horizon MDPs with minor modification. In addition, acceleration techniques that work for Benders decomposition may also be included to speed up our MCD algorithm. Some other possible future research directions include using NNs with different activation functions or multi-layer NNs along with new valid cuts. We may also extend our method to solve other problems, e.g. MCIP with non-convex capacity expansion costs.

8 Acknowledgment

This research is supported by the National Natural Science Foundation of China (No. 72001141), and by the National Research Foundation, Prime Minister’s Office, Singapore under its Campus for Research Excellence and Technological Enterprise (CREATE) programme.

Appendix A Proofs of Main Mathematical Results

Proof of Proposition 1

We first show that there exists such that for all and . According to Assumption 1, there exists such that for all , , and . For , we have for all . For , we may take so that

Now we check Lipschitz continuity of . For , we have

In general, for , we have

using the fact that for are bounded according to Assumption 7. Thus, there exists such that are Lipschitz functions. ∎

Proof of Lemma 1

We only provide a sketch of proof here, and refer the interested readers to (Hornik et al. 1989) or (Sonoda and Murata 2015) for the details. According to (Hornik et al. 1989, Corollary 2.2), a two-layer NN is universal if the activation function of the network (denoted as ) is a squashing function. A squashing function satisfies the following properties according to (Hornik et al. 1989, Definition 2.3): is non-decreasing, , and .

ReLU does not satisfy the second property of a squashing function, but we can construct an equivalent network with a squashing activation function by taking a linear combination of two ReLUs. Suppose we have an ReLU network with sufficient neurons. We may assume the number of neurons is even without loss of generality. For neuron , we pick and specify its adjustable weights so that , , and . Then, we can construct an activation function by taking a linear combination of two neurons:

Given , a new network with neurons is thus constructed. It follows that is universal since are squashing functions: is non-decreasing, , and . Since the solutions of the weights of are a subset of those of , there always exists a network that is equivalent to . Thus, the two-layer network with ReLU is universal. ∎

Proof of Theorem 1

This result is derived from (Munos and Szepesvári 2008, Corollary, 4). Since we have shown that the two-layer NN is a universal approximator in Lemma 1, the only thing we need to prove now is that the MDP presented in this paper satisfies the assumptions of MDP regularity and uniformly stochastic transitions from (Munos and Szepesvári 2008, Corollary, 4). Let be the probability distribution of reward given state and action in time . The assumptions stated in (Munos and Szepesvári 2008) are presented below.

Assumption 10.

[MDP regularity] The MDP satisfies the following conditions: is a bounded, closed subset of some Euclidean space, is finite and the discount factor satisfies . The reward kernel is such that the immediate reward function is a bounded measurable function with bound . Further, the support of is included in independently of .

Assumption 11.

[Uniformly stochastic transitions] For all and , is absolutely continuous w.r.t. . Also, the Radon-Nikodym derivative of w.r.t. is bounded uniformly with bound

We first show that the MDP presented in Section 3 satisfies Assumption 10 According to Assumption 1, there exists such that . As is deterministic and bounded, the support of is included in the bounded set which is independent of .

Now we show that Assumption 11 is satisfied. First, according to (Munos and Szepesvári 2008), Assumption 11 is equivalent to assuming that the transition kernel admits a uniformly bounded density when is the Lebesgue measure over , which is essentially Assumption 5. Therefore, all of the required conditions are satisfied. ∎

Proof of Proposition 2

For all , we have . For all , denote

Then, we have

The first equality holds because . The second line follows from the definitions of and given a specific : if , the inequality holds trivially; if , then and are all zero and so the inequality holds because the first line is always non-positive. Summing up over all neurons and then taking expectations on both sides of the inequality, we have

Thus, according to the definition of the hypograph, we have

and so Eq. (10) is a valid inequality. ∎

Proof of Proposition 3

To prove that Eq. (11) is a valid inequality for , we need to prove

(i) If , then we have

The first equality is derived from the definitions of and . The second equality holds because for all .

(ii) If , the result holds trivially because is the maximum value of , such that .

(iii) We prove that the inequality is valid when and . First, since for all , we have

according to the definitions of and . Then, we have

where the inequality holds because . Note that for all by definition. Therefore, for any we have

The inequality holds because we have and when for all .

The last step is to show that for all :

The inequality holds because when , for all , and for all . ∎

Proof of Theorem 2

According to (Laporte and Louveaux 1993, Proposition 2) and Corollary 1, Cuts (13) and (14) are all valid. Since the action space is finite, Problem () has finitely many feasible solutions. As a result, there are only finitely many cuts that can be added to Problem (). Thus, the algorithm will converge to the global optimal solution in a finite number of iterations. ∎

Proof of Proposition 4

We need to check Assumptions 1 and 3. Assumption 2 holds trivially as the unit revenue and unit penalty cost in Eq. (15a) are finite. Assumption 4 holds according to (Kallenberg 2002, Proposition 8.6). Assumption 5 holds trivially if Assumption 3 is satisfied.

To verify Assumption 1, we need to confirm that the reward function given by Eq. (16) is bounded. As and for all , an upper and lower bound on follows if we have unlimited or no capacity:

Therefore,

Similarly, upper bounds on the capacity adjustment cost follow by assuming that the capacity is changed from zero to or the reverse:

Since we have assumed , it follows that

Then, for all and , we have

For Assumption 3, we let be the -dimensional matrix of zeros and be the -dimensional identity matrix. According to (Kallenberg 2002, Proposition 8.6), since is Markov there exist measurable functions and i.i.d. random variable such that . If we let be the state variable, then the transition function follows by

which is a linear function with respect to . ∎

Proof of Proposition 5

Proof of Proposition 6

First, we know that the property of piecewise linearity is preserved under finite summation and the max/min of a finite collection. Now, observe that is a piecewise linear function when defined over . This observation follows by transforming into its dual problem. Since is a linear programming problem and the optimal value is finite and attained for all , strong duality holds (see e.g. (Bertsimas and Tsitsiklis 1997, Chapter 4)) and we have:

| s. t. |

Let denote the feasible set of for the above problem, where and . Also let be the set of extreme points of . Since the dual problem is an LP, there is an optimal solution among (Bertsimas and Tsitsiklis 1997, Chapter 3), and so the above problem is equivalent to

It follows that is piecewise linear and concave in since it is the min of a finite collection of linear functions. Since and is concave in , is piecewise linear for all and concave in .

To prove (ii), for the induction step suppose that is piecewise linear. We have

Since is finite, is piecewise linear as it is a finite sum of piecewise linear functions. Therefore, is piecewise linear as the max of a finite set of piecewise linear functions, and the desired result follows. ∎

Appendix B Formulation of Integer Optimality Cuts

To formulate the integer optimality cuts, we first define a set of indices for all , such that for all . Then, we define binary variables for all such that . We let denote the binary variables corresponding to the optimal action in the th iteration of MCD. We also let

and

be the index sets for the binary variables that are equal to one and zero, respectively. Then, can be expressed as:

where is the cardinality of the set . If , then ; otherwise . Other possible formulations for can also be found in (Laporte and Louveaux 1993).

References

- Antos et al. (2007) Antos A, Szepesvari C, Munos R (2007) Value-Iteration Based Fitted Policy Iteration: Learning with a Single Trajectory. 2007 IEEE International Symposium on Approximate Dynamic Programming and Reinforcement Learning, 330–337, URL http://dx.doi.org/10.1109/ADPRL.2007.368207, iSSN: 2325-1867.

- Antos et al. (2008) Antos A, Szepesvári C, Munos R (2008) Fitted Q-iteration in continuous action-space MDPs. Advances in neural information processing systems, 9–16, URL http://papers.nips.cc/paper/3233-fitted-q-iteration-in-continuous-action-space-mdps.

- Bartlett et al. (2019) Bartlett PL, Harvey N, Liaw C, Mehrabian A (2019) Nearly-tight VC-dimension and Pseudodimension Bounds for Piecewise Linear Neural Networks. Journal of Machine Learning Research 20(63):1–17, ISSN 1533-7928, URL http://jmlr.org/papers/v20/17-612.html.

- Beale et al. (2018) Beale M, Hagan M, Howard D (2018) Neural network toolbox™ (The MathWorks, Inc.), URL https://www.mathworks.com/help/pdf_doc/nnet/nnet_ug.pdf.

- Bertsekas (2012) Bertsekas DP (2012) Dynamic Programming and Optimal Control, volume II (Athena Scientific), 4th edition edition.

- Bertsimas and Georghiou (2018) Bertsimas D, Georghiou A (2018) Binary decision rules for multistage adaptive mixed-integer optimization. Mathematical Programming 167(2):395–433, ISSN 0025-5610, 1436-4646, URL http://dx.doi.org/10.1007/s10107-017-1135-6.

- Bertsimas and Tsitsiklis (1997) Bertsimas D, Tsitsiklis JN (1997) Introduction to linear optimization, volume 6 (Athena Scientific Belmont, MA).

- Cardin et al. (2017a) Cardin MA, Xie Q, Ng TS, Wang S, Hu J (2017a) An approach for analyzing and managing flexibility in engineering systems design based on decision rules and multistage stochastic programming. IISE Transactions 49(1):1–12, ISSN 2472-5854, 2472-5862, URL http://dx.doi.org/10.1080/0740817X.2016.1189627.

- Cardin et al. (2017b) Cardin MA, Zhang S, Nuttall WJ (2017b) Strategic real option and flexibility analysis for nuclear power plants considering uncertainty in electricity demand and public acceptance. Energy Economics 64:226–237, ISSN 01409883, URL http://dx.doi.org/10.1016/j.eneco.2017.03.023.

- Choromanska et al. (2014) Choromanska A, Henaff M, Mathieu M, Arous GB, LeCun Y (2014) The Loss Surfaces of Multilayer Networks. arXiv:1412.0233 [cs] URL http://arxiv.org/abs/1412.0233, arXiv: 1412.0233.

- Defourny et al. (2013) Defourny B, Ernst D, Wehenkel L (2013) Scenario Trees and Policy Selection for Multistage Stochastic Programming Using Machine Learning. INFORMS Journal on Computing 25(3):488–501, ISSN 1091-9856, 1526-5528, URL http://dx.doi.org/10.1287/ijoc.1120.0516.

- Dixit and Pindyck (1994) Dixit AK, Pindyck RS (1994) Investment Under Uncertainty (Princeton University Press), ISBN 978-0-691-03410-2, google-Books-ID: VahsELa_qC8C.

- Feng et al. (2015) Feng H, Wu Q, Muthuraman K, Deshpande V (2015) Replenishment Policies for Multi-Product Stochastic Inventory Systems with Correlated Demand and Joint-Replenishment Costs. Production and Operations Management 24(4):647–664, ISSN 10591478, URL http://dx.doi.org/10.1111/poms.12290.

- Georghiou et al. (2015) Georghiou A, Wiesemann W, Kuhn D (2015) Generalized decision rule approximations for stochastic programming via liftings. Mathematical Programming 152(1-2):301–338, ISSN 0025-5610, 1436-4646, URL http://dx.doi.org/10.1007/s10107-014-0789-6.

- Haskell et al. (2016) Haskell WB, Jain R, Kalathil D (2016) Empirical Dynamic Programming. Mathematics of Operations Research 41(2):402–429, ISSN 0364-765X, URL http://dx.doi.org/10.1287/moor.2015.0733.

- Haussler (1995) Haussler D (1995) Sphere packing numbers for subsets of the boolean n-cube with bounded vapnik-chervonenkis dimension. J. Comb. Theory, Ser. A 69(2):217–232.

- Hornik et al. (1989) Hornik K, Stinchcombe M, White H (1989) Multilayer feedforward networks are universal approximators. Neural Networks 2(5):359–366, ISSN 0893-6080, URL http://dx.doi.org/10.1016/0893-6080(89)90020-8.

- Hu et al. (2017) Hu YQ, Qian H, Yu Y (2017) Sequential Classification-Based Optimization for Direct Policy Search. Proceedings of the Thirty-First AAAI Conference on Artificial Intelligence, 2029 (San Francisco, California USA: AAAI Press).

- Huang and Ahmed (2009) Huang K, Ahmed S (2009) The Value of Multistage Stochastic Programming in Capacity Planning Under Uncertainty. Operations Research 57(4):893–904, ISSN 0030-364X, URL http://dx.doi.org/10.1287/opre.1080.0623.

- Jain and Varaiya (2010) Jain R, Varaiya P (2010) Simulation-based optimization of Markov decision processes: An empirical process theory approach. Automatica 46(8):1297–1304, ISSN 00051098, URL http://dx.doi.org/10.1016/j.automatica.2010.05.021.

- Kallenberg (2002) Kallenberg O (2002) Foundations of Modern Probability (New York: Springer), 2nd edition edition, ISBN 978-0-387-95313-7.

- Kuhn et al. (2011) Kuhn D, Wiesemann W, Georghiou A (2011) Primal and dual linear decision rules in stochastic and robust optimization. Mathematical Programming 130(1):177–209, ISSN 0025-5610, 1436-4646, URL http://dx.doi.org/10.1007/s10107-009-0331-4.

- Laporte and Louveaux (1993) Laporte G, Louveaux FV (1993) The integer L-shaped method for stochastic integer programs with complete recourse. Operations Research Letters 13(3):133–142, ISSN 0167-6377, URL http://dx.doi.org/10.1016/0167-6377(93)90002-X.

- Lillicrap et al. (2015) Lillicrap TP, Hunt JJ, Pritzel A, Heess N, Erez T, Tassa Y, Silver D, Wierstra D (2015) Continuous control with deep reinforcement learning. arXiv:1509.02971 [cs, stat] URL http://arxiv.org/abs/1509.02971, arXiv: 1509.02971.

- Luo et al. (2016) Luo T, Gao L, Akçay Y (2016) Revenue Management for Intermodal Transportation: The Role of Dynamic Forecasting. Production and Operations Management 25(10):1658–1672, ISSN 1937-5956, URL http://dx.doi.org/10.1111/poms.12553.

- Munos and Szepesvári (2008) Munos R, Szepesvári C (2008) Finite-time bounds for fitted value iteration. Journal of Machine Learning Research 9(May):815–857, URL http://www.jmlr.org/papers/v9/munos08a.html.

- Powell (2011) Powell WB (2011) Approximate Dynamic Programming: Solving the Curses of Dimensionality (Hoboken, N.J: Wiley), 2nd edition edition, ISBN 978-0-470-60445-8.

- Schulman et al. (2015) Schulman J, Moritz P, Levine S, Jordan M, Abbeel P (2015) High-Dimensional Continuous Control Using Generalized Advantage Estimation. arXiv:1506.02438 [cs] URL http://arxiv.org/abs/1506.02438, arXiv: 1506.02438.

- Shapiro et al. (2009) Shapiro A, Dentcheva D, Ruszczyński AP (2009) Lectures on stochastic programming: modeling and theory. Number 9 in MPS-SIAM series on optimization (Philadelphia: Society for Industrial and Applied Mathematics : Mathematical Programming Society), ISBN 978-0-89871-687-0, oCLC: ocn402540716.

- Sonoda and Murata (2015) Sonoda S, Murata N (2015) Neural Network with Unbounded Activation Functions is Universal Approximator. arXiv:1505.03654 [cs, math] URL http://arxiv.org/abs/1505.03654, arXiv: 1505.03654.

- Spivey and Powell (2004) Spivey MZ, Powell WB (2004) The Dynamic Assignment Problem. Transportation Science 38(4):399–419, ISSN 0041-1655, URL http://dx.doi.org/10.1287/trsc.1030.0073, publisher: INFORMS.

- Sun and Schonfeld (2015) Sun Y, Schonfeld P (2015) Stochastic capacity expansion models for airport facilities. Transportation Research Part B: Methodological 80:1–18, ISSN 01912615, URL http://dx.doi.org/10.1016/j.trb.2015.06.009.

- Taghavi and Huang (2018) Taghavi M, Huang K (2018) A Lagrangian relaxation approach for stochastic network capacity expansion with budget constraints. Annals of Operations Research ISSN 0254-5330, 1572-9338, URL http://dx.doi.org/10.1007/s10479-018-2862-7.

- Topan et al. (2010) Topan E, Pelin Bayındır Z, Tan T (2010) An exact solution procedure for multi-item two-echelon spare parts inventory control problem with batch ordering in the central warehouse. Operations Research Letters 38(5):454–461, ISSN 01676377, URL http://dx.doi.org/10.1016/j.orl.2010.05.006.

- Vairaktarakis (2000) Vairaktarakis GL (2000) Robust multi-item newsboy models with a budget constraint. International Journal of Production Economics 66(3):213–226, ISSN 09255273, URL http://dx.doi.org/10.1016/S0925-5273(99)00129-2.

- Yu et al. (2020) Yu S, Kulkarni VG, Deshpande V (2020) Appointment Scheduling for a Health Care Facility with Series Patients. Production and Operations Management 29(2):388–409, ISSN 1937-5956, URL http://dx.doi.org/10.1111/poms.13117.

- Zhao et al. (2017) Zhao S, Haskell WB, Cardin MA (2017) An Approximate Dynamic Programming Approach for Multi-Facility Capacity Expansion Problem with Flexibility Design. IIE Annual Conference Proceedings, 440–445, URL http://search.proquest.com/docview/1951122270/abstract/11A7A0DCA754DD7PQ/1.

- Zhao et al. (2018) Zhao S, Haskell WB, Cardin MA (2018) Decision rule-based method for flexible multi-facility capacity expansion problem. IISE Transactions 50(7):553–569, ISSN 2472-5854, URL http://dx.doi.org/10.1080/24725854.2018.1426135.

- Zou et al. (2018) Zou J, Ahmed S, Sun XA (2018) Stochastic dual dynamic integer programming. Mathematical Programming ISSN 0025-5610, 1436-4646, URL http://dx.doi.org/10.1007/s10107-018-1249-5.