On the Importance of Asymmetry and Monotonicity Constraints in Maximal Correlation Analysis

Abstract

The maximal correlation coefficient is a well-established generalization of the Pearson correlation coefficient for measuring non-linear dependence between random variables. It is appealing from a theoretical standpoint, satisfying Rényi’s axioms for measures of dependence. It is also attractive from a computational point of view due to the celebrated alternating conditional expectation algorithm, allowing to compute its empirical version directly from observed data. Nevertheless, from the outset, it was recognized that the maximal correlation coefficient suffers from some fundamental deficiencies, limiting its usefulness as an indicator of estimation quality. Another well-known measure of dependence is the correlation ratio but it too suffers from some drawbacks. Specifically, the maximal correlation coefficient equals one too easily whereas the correlation ratio equals zero too easily. The present work recounts some attempts that have been made in the past to alter the definition of the maximal correlation coefficient in order to overcome its weaknesses and then proceeds to suggest a natural variant of the maximal correlation coefficient. The proposed dependence measure at the same time resolves the major weakness of the correlation ratio measure and may be viewed as a bridge between the two classical measures.

I Introduction

Pearson’s correlation coefficient is a measure indicating how well one can approximate (estimate in an average least squares sense) a (response) random variable as a linear (more precisely affine) function of a (predictor/observed) random variable , i.e., as .111We assume that the random variables and have finite variance. The coefficient is given by

| (1) |

The coefficient is symmetric in and so it just as well measures how well one can approximate as a linear function of .

The correlation ratio of on , also suggested by Pearson (see, e.g., [1]), similarly measures how well one can approximate as a general admissible function of , i.e., as .222We define a function to be admissible w.r.t. the random variable if it is a Borel-measurable real-valued functions such that and it has finite and positive variance. Specifically, the correlation ratio of on is given by

| (2) | ||||

The correlation ratio can also be expressed as

| (3) |

where the supremum is taken over all (admissible) functions (see, e.g., [2]). This measure is naturally nonsymmetric. A drawback of the correlation ratio is that it “equals zero too easily”. Specifically, it can vanish even where the variables are dependent.

We note that one may equivalently say that the correlation ratio measures how well one can approximate as for some admissible transformation of the random variable . While perhaps seeming superfluous at this point, this view will prove useful when considering different generalizations of the correlation ratio to the case where the observations are a random vector.

The Hirschfeld-Gebelein-Rényi maximal correlation coefficient [3, 4, 5] measures the maximal (Pearson) correlation that can be attained by transforming the pair into random variables and ; that is, how well holds in a mean squared error sense for some pair of functions and . More precisely, the maximum correlation coefficient is defined as the supremum over all (admissible) functions of the correlation between and :

| (4) |

This measure is again symmetric by definition. We use the superscript “**” to indicate that both functions (applied to the response and the predictor random variables) need not satisfy any restrictions beyond being admissible.

The maximal correlation coefficient has some very pleasing properties. In particular, in [5], Rényi put forth a set of seven axioms deemed natural to require of a measure of dependence between a pair of random variables and established that the maximal correlation coefficient satisfies the full set of axioms. In particular, unlike the correlation ratio, the maximal correlation coefficient “does not equal zero too easily”. Further, unlike the correlation ratio it is symmetric, which was set as one of the axioms. Nonetheless, these pleasing properties come at the price of introducing new problems as elaborated on below.

Another appealing trait of the maximal correlation coefficient, greatly contributing to its popularity, is its tight relation to a Euclidean geometric framework and to operator theory. In particular, it is readily computable numerically via the alternating conditional expectation (ACE) algorithm of Breiman and Friedman [6]. Moreover, and as recalled in the sequel, the ACE algorithm naturally extends to cover linear estimation of a (transformed) random variable from a component-wise transformed random vector.

Rényi’s seminal work inspired substantial subsequent work aiming to identify other measures of dependence satisfying the set of axioms. We refer the reader to [7] for a survey of some of these.

Despite its elegance and it being amenable to computation, the maximal correlation coefficient suffers from some significant deficiencies as was recognized since its inception. Specifically, it is well known that it “equals one too easily”; see, e.g. [8], [9], as well as Footnote 3 in [5]. In fact, it can equal one even for two random variables that are nearly independent (as also demonstrated below).

Disconcerted by this behavior of the maximal correlation coefficient, Kimeldorf and Sampson [9] proposed to alter its definition, introducing monotonicity constraints. They defined a monotone dependence measure as follows.

| (5) |

where and are not only admissible but also monotone. Nevertheless, as stated in [9], while the imposed constraints somewhat mitigate the “easiness of attaining the value of one”, the measure (5) still can equal one for a pair of random variables that are not completely dependent.

The definition of the monotone dependence measure (5) is unsatisfactory in two respects. The first is that is imposes symmetric constraints on the two transformations. As the process of estimation/prediction (and more generally inference) is directional, if the goal of the dependence measure is to characterize how well one can achieve the latter tasks, there is no apparent reason to impose any restriction on the transformation applied to the observed data. In this respect, it is worth quoting the incisive comments (in reference to [10]) of Hastie and Tibshirani [11]:

“…a monotone restriction makes sense for a response transformation because it is necessary to allow predictions of the response from the estimated model. … On the other hand, why restrict predictor transformations (such as for displacement and weight in the city gas consumption problem) to be monotone? Instead, why not leave them unrestricted and let the data suggest the shape of the relevant transformation?”

The second and more subtle deficiency of the monotone dependence measure of Kimeldorf and Sampson (as well as the semi-monotone variant suggested by Hastie and Tibshirani) is that when it comes to the response variable, the requirement that the transformation be monotone is not strong enough.

The goal of the present work is first to reiterate some of the known drawbacks of both the correlation ratio and of the maximal correlation coefficient, and then to suggest a possible resolution. In particular, we demonstrate that while allowing a transformation to be applied to the response variable is important, it is not sufficient to require that it be monotonic. Rather, one must strengthen the required “degree” of monotonicity.

Specifically, we introduce the notion of -monotonicity and argue in favor of constraining (only) the transformation applied to the response random variable to be -monotonic, leading to a proposed semi--monotone maximal correlation measure. The parameter dictates a minimal and maximal slope that the function applied to the response variable must maintain.

We show that requiring that yields a measure that does not suffer from the drawbacks of neither the maximal correlation coefficient nor from those of the correlation ratio. The proposed measure satisfies a set of modified Rényi axioms that does not sacrifice the natural requirements of capturing both independence and complete dependence.

It is important to note that setting amounts to requiring merely monotonicity, as already suggested in [11], without imposing a minimal (or maximal) positive slope. Setting , on the other hand, the semi--monotone maximal correlation measure reduces to the correlation ratio. This implies that while both of these choices are not sufficient to satisfy the proposed set of modified Rényi axioms, they lie right on the boundary of the set of values that do. Thus, in a sense, these choices may be considered satisfactory if we rule out “pathological” examples. The same cannot be said of the maximal correlation coefficient. These points are illustrated in Section V.

Finally, as the usefulness of the maximal correlation coefficient is due in part to it being readily computable, we suggest modifications to the ACE algorithm and exemplify the resulting performance via several examples.

The rest of the paper is organized as follows. Section II describes the shortcomings of the correlation ratio and maximal correlation coefficient as well as presents the proposed dependence measure. Section III puts forth a set of modified Rényi axioms, outlining the main steps involved in proving that the proposed measure satisfies the latter. Section IV provides some modifications to the ACE algorithm, enforcing monotonicity constraints. Finally, several numerical examples illustaring the main ideas are given in Section V.

II Shortcomings of the Correlation Ratio and Maximal Correlation Coefficient and a Proposed Resolution

As a simple example, consider two (sequences of) random variables that share only the least significant bit:

| (6) |

where are mutually independent random variables, all taking the values or with equal probability. Clearly, applying modulo to both variables yields a correlation of one. This seems quite unsatisfactory if our goal is estimation subject to any reasonable distortion metric as the two random variables become virtually independent as grows. Specifically, the pair converges in distribution to a uniform distribution over the unit square.

Remark 1.

It should be noted in this respect that the maximal correlation coefficient is a good measure for a different goal. It quantifies to what extent two random variables share any common “features”.

Remark 2 (Discrete random variables).

While the emphasis in this paper is on continuous random variables, symmetric measures are also generally not appropriate for measuring the dependence between discrete random variables. For instance, a natural measure in this case is the minimal possible probability of error when predicting one from the other. Clearly, this measure is also not symmetric. While minimum error probability is related via universal lower and upper bounds to the conditional entropy and mutual information (the latter being a symmetric measure), as shown in [12] (Equations 5 and 6), the gap between the lower and upper bounds (keeping the probability of error fixed) grows unbounded with the cardinality of the random variables. This is yet another indication that symmetric measures are ill-suited for estimation/prediction purposes.

A natural and quite satisfying measure of directional dependence between random variables, that takes the value of one only when the response variable is a function of the predictor variable, is the correlation ratio defined in (2). While Rényi objected to the correlation ratio due to its asymmetric nature, as was noted in [8], when our goal is asymmetric (i.e., estimating from ), there is no reason for requiring that the measure be symmetric.

Nonetheless, in some cases one does not have strong grounds to assume a particular “parameterization” of the desired (response) random variable. Thus, not allowing to apply any transformation to the response variable, as is the case of the correlation ratio, may be too restrictive. In other words, in the absence of a preferred “natural” parameterization of the response variable, one may consider choosing a strictly monotone transformation (change of variables) so as to make it easier to estimate. A more severe drawback of the correlation ratio is that it vanishes too easily, i.e., it can be zero for two dependent random variables.

In light of these considerations, we propose the following modification to the definition of the maximal correlation coefficient.

Definition 1.

For , a function is said to be -increasing, if for all :

Definition 2.

For a given , the semi--monotone maximal correlation measure is defined as

where and the supremum is taken over all admissible functions , and over -increasing admissible functions .

Remark 3.

Limiting to be -increasing implies that, in particular, it is invertible, which is a natural requirement. Moreover, the set of -increasing admissible functions is closed. We further note that the value of controls how far the measure can deviate from the correlation ratio.

II-A The vector observation case

Let be a vector of predictor variables. The maximal correlation coefficient becomes

| (7) |

where the supremum is over all admissible functions.

Following Breiman and Friedman [6], we may also consider a simplified (quasi-additive) relationship between and where we seek an optimal linear regression between a transformation of and a component-wise non-linear transformation of the predictor random vector . Denote the fraction of the variance not explained by a regression of on as

| (8) |

where zero-mean functions are assumed. In [6], conditions for the existence of optimal transformations such that the supremum is attained are given, and it is shown that under these conditions the ACE algorithm converges to the optimal transformations.

Going back to the rationale for requiring -monotonicity, one may object to the example (6) as being artificial and argue that the maximum correlation coefficient merely captures whatever dependence there is between the random variables. In this respect, it is worthwhile quoting Breiman [13] (commenting on [10]):

“I only know of infrequent cases in which I would insist on monotone transformations. Finding non-monotonicity can lead to interesting scientific discoveries. If the appropriate transformation is monotone, then the fitted spline functions (or ACE transformations) will produce close to a monotonic transformation. So it is hard to see what there is to gain in the imposition of monotonicity.”

We now demonstrate that the problematic nature of the maximal correlation coefficient becomes more pronounced when considering the multi-variate case and so does the necessity of restricting the transformation of the response variable (only) to be monotone.

Specifically, let us consider again the example of (6). Suppose that and are as defined but that in addition to , there is another slightly noisy observation of , say where the variance of is small with respect to that of . Clearly, the maximal correlation coefficient will still equal , and the observation will be discarded even though it could have allowed to estimate with small distortion. Thus, in this example, the maximal correlation coefficient is maximized by perfectly estimating the least significant bit while doing away with the more significant bits even though nearly distortionless reconstruction is possible. See also Section V below for a numerical example.

III modified Rényi axioms

We follow the approach of Hall [8] in defining an asymmetric variant of the Rényi axioms; more precisely, we adopt a slight variation on the somewhat stronger version formulated by Li [14]. However, unlike both of these works, when it comes to putting forward a candidate dependence measure satisfying the modified axioms, we adhere to a mean square error methodology.

Assume is to measure the degree of dependence of on . Then we require that it satisfy the following:

-

(a)

is defined for all non-constant random variables having finite variance.333In [14], the first axiom only requires that be defined for continuous random variables .

-

(b)

may not be equal to .

-

(c)

.

-

(d)

if and only if are independent.

-

(e)

if and only if almost surely for some admissible function .

-

(f)

If is an admissible bijection on , then

-

(g)

If are jointly normal with correlation coefficient , then .444In [14], the last axiom only requires that if are jointly normal with correlation coefficient , is a strictly increasing function of .

Remark 4.

We note that the correlation ratio, defined in (3), satisfies all of the modified axioms except for the “only if” part of axiom (d).

We next observe that for absolutely continuous (or discrete) distributions, the semi--monotone maximal correlation measure of Definition 2 satisfies the proposed axioms.

It is readily verified that axioms (a), (b) and (c) hold. To show that axiom (d) holds, we note that if are independent, then obviously , as so is even . As for the other direction, we first note that it suffices to consider the case where the correlation ratio equals and are dependent. Since the correlation ratio is , it follows from (2) that (in the mean square sense), i.e.,

| (9) |

We may break the symmetry of by defining, e.g.,

| (10) |

Consider two values of and for which the functions are not identical (as functions of ), as must exist by the assumption of dependence. Let be a value such that

| (11) |

Without loss of generality, we may assume that the left hand side is smaller than the right hand side (we may rename and ). Recalling that , it follows that

| (12) |

Thus,

and hence the correlation ratio of on is non-zero, giving a lower bound to the semi--monotone maximal correlation measure between and . Note that (10) imposes only a lower bound on the slope of the function applied to the response variable.

To show that axiom (e) holds, we note that by definition, if (almost surely), then . To show that the opposite direction holds, we first note that it can be shown that the supremum in (2) is attained. Recalling that if , then by the properties of Pearson’s correlation coefficient, there is a perfect linear regression between and ( being maximizing functions of the measure). Now, it can be shown that the supremum Hence, we have where is an increasing function with slope greater than . Since is strictly positive, it follows that not only is invertible, but also has finite variance (since the slope of is at most and has finite variance). Therefore we have . Denoting , we note that if is admissible, then so is .

Axiom (f) trivially holds. To show that axiom (g) holds, we recall that it is well known that when are jointly normal with correlation coefficient , then (see, e.g., [15] and [16]). Since this implies that the maximal correlation is achieved taking (i.e., a monotone function) and or , it follows that

| (13) |

We note that the restriction is necessary. Specifically, for , axiom (d) is not satisfied whereas for , axiom (e) is not satisfied.

Finally, we note that one may define other dependence measures satisfying modified Rényi axioms, most notably via the theory of copulas (which is inherently related to monotone constraints); e.g., a symmetric measure is given in [17] and a directional one is given in [14]. Nonetheless, we believe that the proposed measure has the advantage of being closely tied to linear regression methods and geometric considerations.

IV Modified ACE Algorithm

We begin by presenting a modification of the ACE algorithm with the goal of computing the semi--monotone maximal correlation measure , restricting the function applied to the response variable only to be weakly monotone.

As we do not know of a simple means to enforce the slope constraints, we do not have an algorithm for computing the semi--monotone maximal correlation measure. Instead, we have employed a regularized version of the original ACE algorithm as described in Section IV-B.

IV-A Evaluating the semi--monotone maximal correlation measure

We now present a modification of the ACE algorithm to compute the semi--monotone maximal correlation measure for the case of single predictor variable. It is readily seen that the correlation increases in each iteration of the algorithm and thus converges but we do not pursue proving optimality. We then generalize the algorithm to the quasi-additive multi-variate scenario.

Following in the footsteps of [6], recall that the space of all random variables with finite variance is a Hilbert space, which we denote by , with the usual definition of the inner product , for . We may further define the subspace as the set of all random variables that correspond to an admissible function of . We similarly define the subspace . Now, if we further limit the functions applied to to be non-decreasing, we obtain a closed and convex subset of the Hilbert space . We denote this set by .

Denoting by the orthogonal projection of onto the closed convex set ,555Note that . the modified ACE algorithm is described in Algorithm 1 for the case of single predictor variable.

In the case of a multi-variate predictor, the original ACE algorithm seeks an optimal linear regression between a transformation of and a component-wise non-linear transformation of the predictor random vector . The latter transformations are defined by a set of admissible functions , each function operating on the corresponding random variable, yielding an estimator of the form .

Therefore Algorithm 1 becomes

IV-B Regularized ACE algorithm

We may enforce that the transformation be -monotone by applying the following regularization. Given a monotone transformation (e.g., the outcome of Algorithm 1), do:666Note that this method of regularization actually forces the slope to be between and .

A similar regularization can be applied to Algorithm 2.

V Numerical examples

As we do not know of an efficient means to evaluate the semi--monotone maximal correlation measure for , we for the most part demonstrate the advantage of the semi--monotone maximal correlation measure over the standard maximal correlation measure, in the context of estimation of a random variable from a random vector . We further demonstrate its potential for improvement over the correlation ratio. To that end, we compute the semi--monotone maximal correlation measure using Algorithm 1 presented in Section IV.

We begin with a multi-variate example where one of the two observed random variables “masks” the other while the latter is more significant for estimation purposes. We then demonstrate why taking is inadequate and hence the semi--monotone maximal correlation measure may be advantageous with respect to the correlation ratio. The third example illustrates why taking is not sufficient in general, and heuristically demonstrates that Algorithm 3 yields more satisfying results.

For simulating ACE, we used the ACE Matlab code provided by the authors of [18]. To limit to be a monotonic function, we used isotonic regression.

V-A Example 1 - Multi-variate predictor

Assume that the response variable is distributed uniformly over the interval and that we have two predictor variables

| (14) |

where are independent zero-mean Gaussian variables with and .

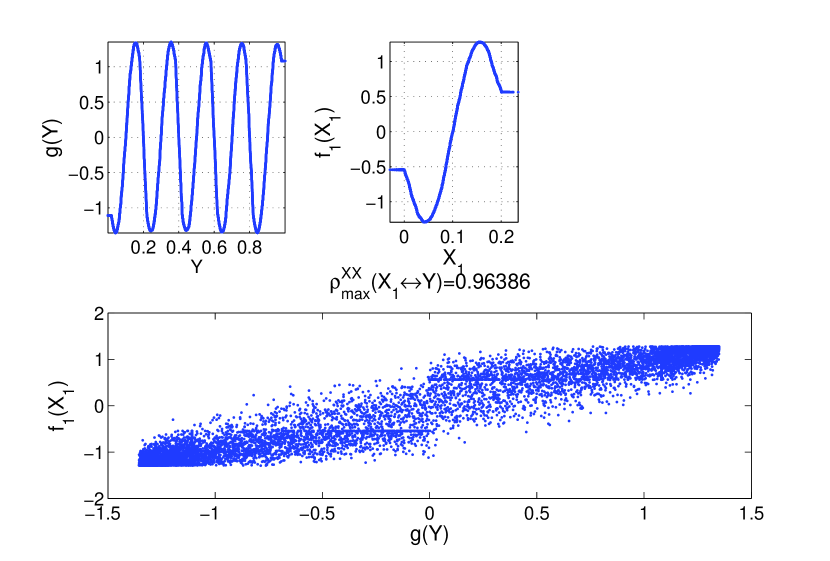

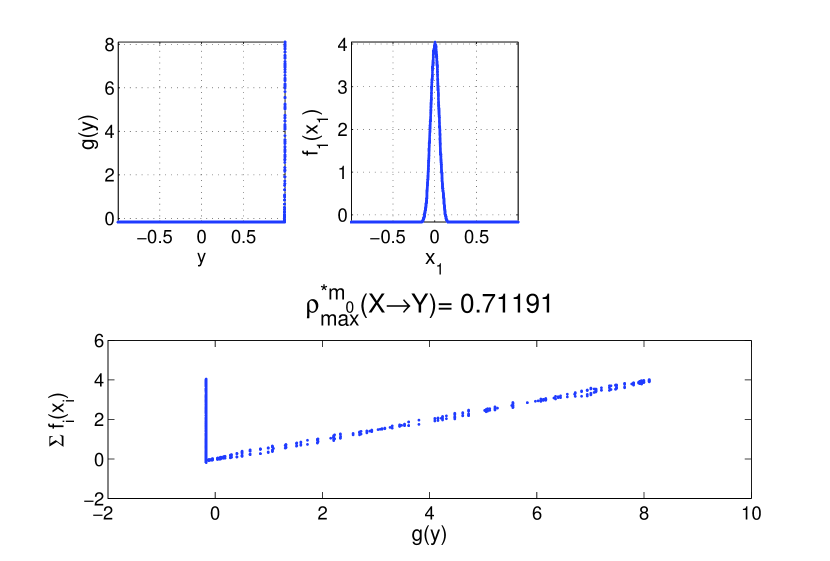

The optimization invloved in the maximal correlation coefficient results in “shadowing” the more significant variable, , for estimation purposes of the response . To see this, we start by running the ACE algorithm to evaluate the maximal correlation coefficient between and . As can be seen from Figure 1, this results in a very high value. Inspecting the transformations yielding this result, we observe that is not monotonic and hence we cannot recover from .

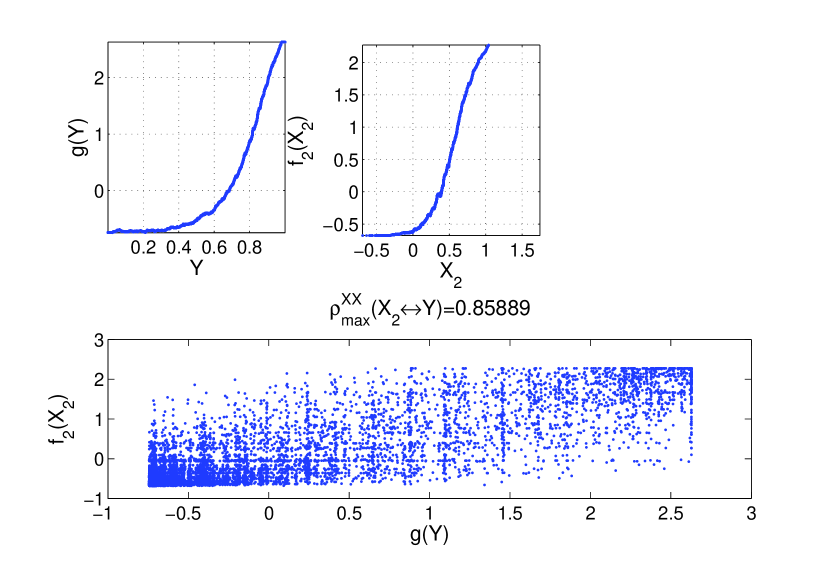

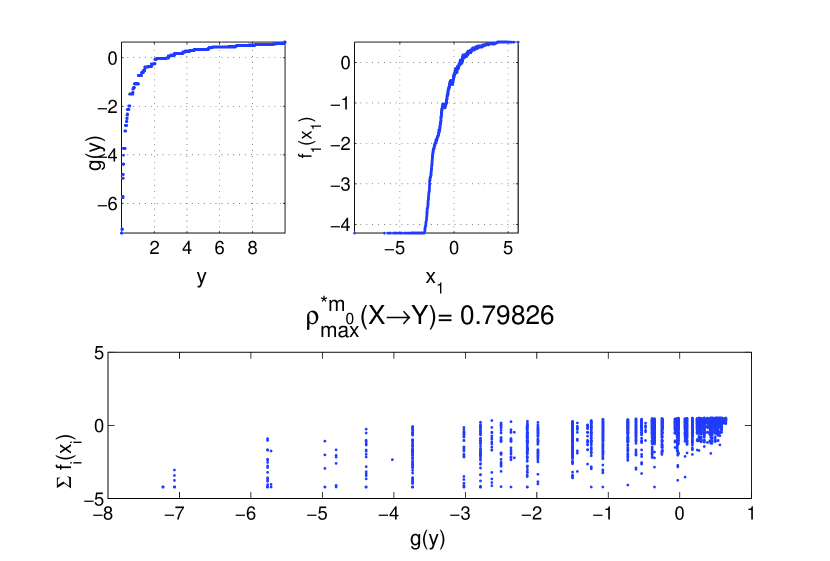

Next, we apply the ACE algorithm to calculate the maximal correlation coefficient between and . As can be seen from Figure 2, this value is much smaller (than that between and ) since in this case we have stronger additive noise. Nevertheless, the transformation applied to is now monotonic. Therefore, even though the maximal correlation coefficient is smaller, the observation can better serve the purpose of estimation of .

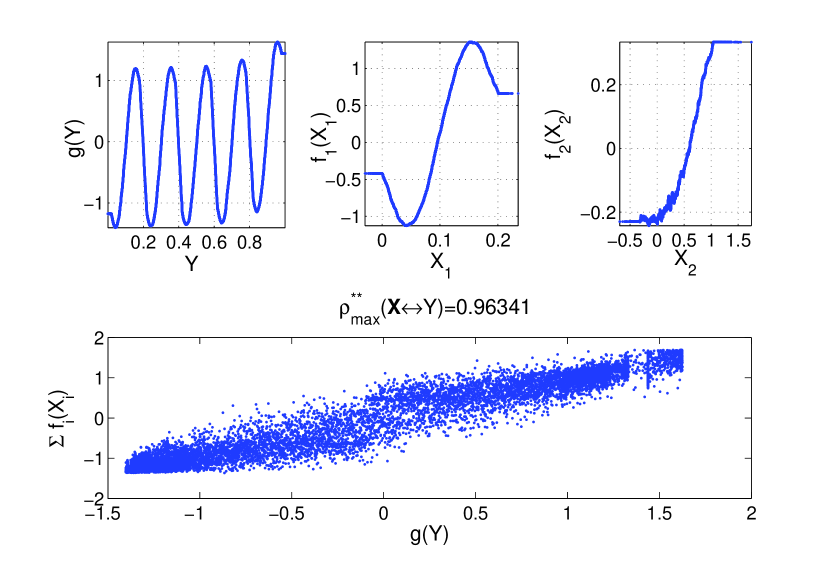

Next we apply the ACE algorithm to and the vector . As can be seen from Figure 3, the ACE algorithm, in order to maximize the correlation, chooses similar functions as in case of running only on and , practically choosing to ignore . While, indeed, this maximizes the correlation coefficient, it is far from satisfying from an estimation viewpoint.

As can be seen from Figure 4, the resulting value of the semi--monotone maximal correlation measure is very close to the maximal correlation value between and . Thus, the algorithm “chooses to ignore” (even though it suffers from a lower noise level) and bases the estimation on .

V-B Comparisons with the correlation ratio

V-B1 Example 2a

The proposed dependence measure can be viewed as a generalization of the correlation ratio (the correlation ratio amounts to setting to have a constant slope of ).

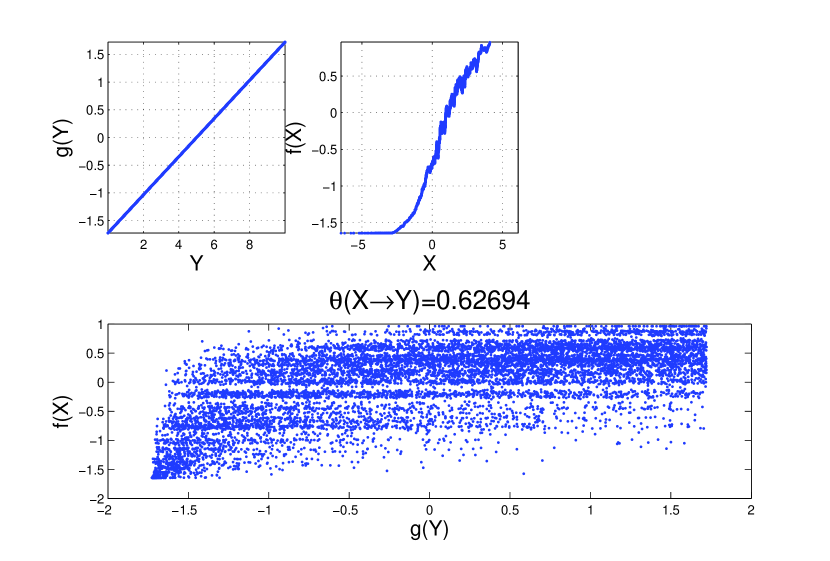

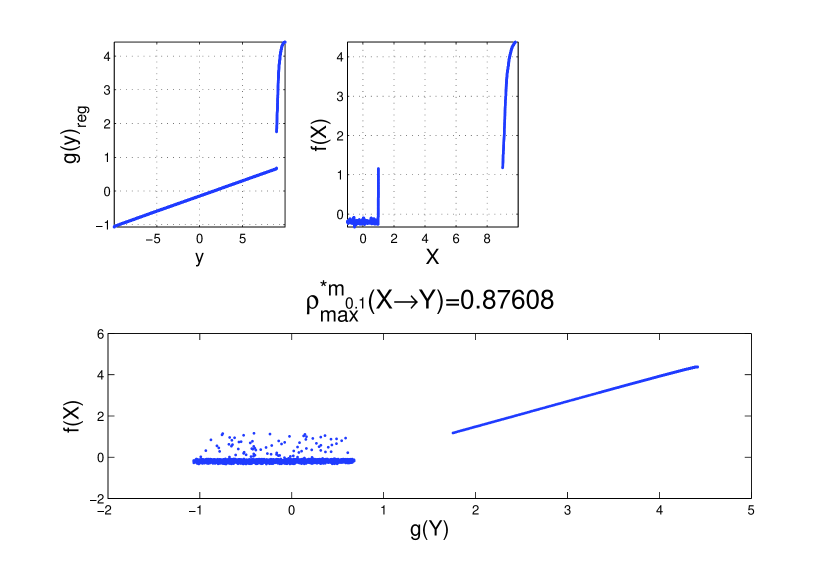

We first demonstrate how the semi--monotone maximal correlation measure deals with a well-known example where the correlation ratio equals for a pair of dependent random variables. Specifically, we consider a vector that is uniformly distributed over a circle with radius . The correlation ratio is as depicted in Figure 5 where we ran ACE enforcing .

.

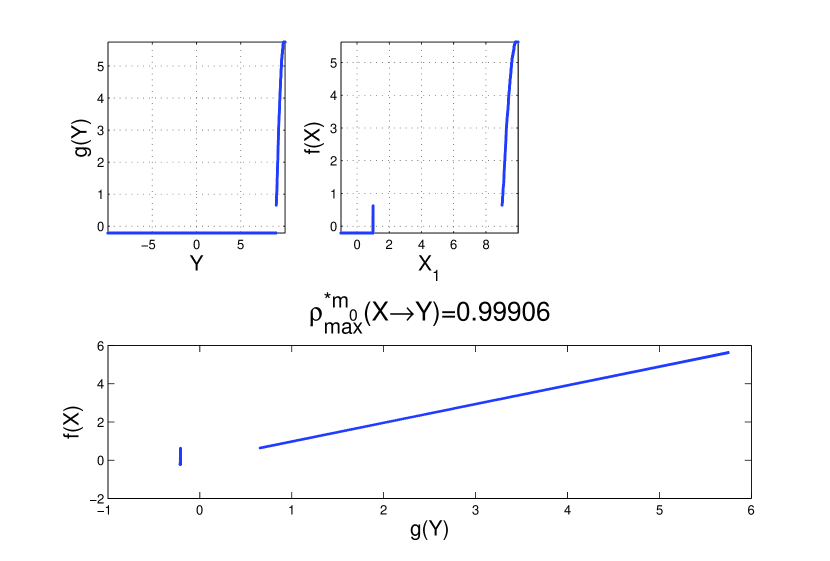

Applying Algorithm 1 with yields a much larger correlation. Thus, it manages to capture the dependence between and . This is depicted in Figure 6.

.

V-B2 Example 2b

The next example demonstrates another potential advantage over the correlation ratio. As was already noted, there are cases where there is no a priori preferred (natural) parameterization for the response variable and thus choosing one that maximizes the correlation may be a reasonable approach as we now demonstrate.

Assume that the response variable is distributed uniformly over the interval and that the predictor variable is

| (15) |

where is a zero-mean Gaussian (and independent of ) with unit variance. Comparing the correlation ratio (Figure 7) and the results of Algorithm 1 with (Figure 8), reveals that the correlation of the latter is significantly higher.

.

V-C Example 3 - Semi--monotonicity is insufficient

To illustrate why it does not suffice to limit to be merely monotone, consider the following example. Assume that the response is distributed uniformly over the interval and that

| (16) |

where and is independent of .

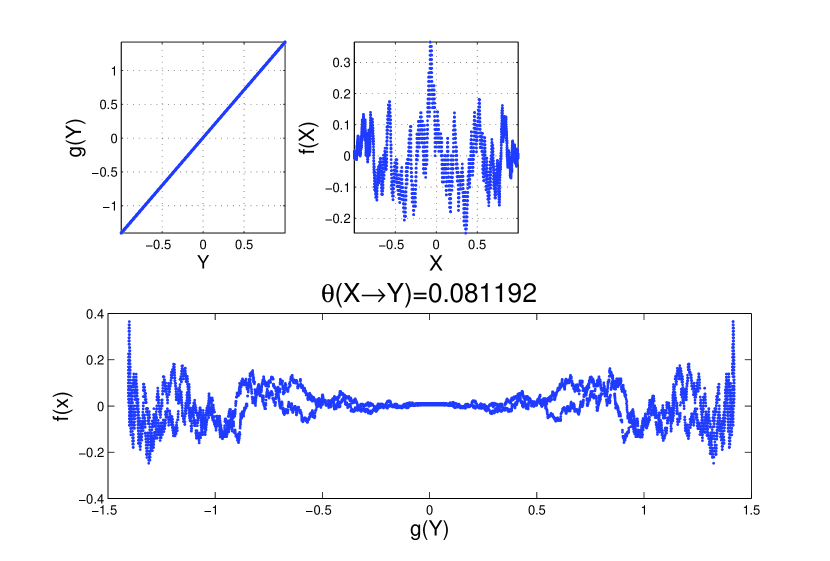

Limiting only to be monotone (with no slope limitations) results in a correlation value of since the optimal solution is to set in the region it cannot be estimated and otherwise (and then apply normalization). Clearly, the function is non-invertible as is depicted in Figure 9.

Next, we ran Algorithm 3 - the regularized ACE algorithm, enforcing a minimal slope of . The results are depicted in Figure 10.

.

This example sheds light on the trade-off that exists when setting the value of . Setting to be large limits the possible gain over the correlation ratio whereas setting it too low risks overemphasizing regions where the noise is weaker.

References

- [1] H. Cramér, Mathematical methods of statistics (PMS-9). Princeton University Press, 2016, vol. 9.

- [2] A. Rényi, “New version of the probabilistic generalization of the large sieve,” Acta Mathematica Hungarica, vol. 10, no. 1-2, pp. 217–226, 1959.

- [3] H. O. Hirschfeld, “A connection between correlation and contingency,” in Mathematical Proceedings of the Cambridge Philosophical Society, vol. 31, no. 4. Cambridge University Press, 1935, pp. 520–524.

- [4] H. Gebelein, “Das statistische Problem der Korrelation als Variations-und Eigenwertproblem und sein Zusammenhang mit der Ausgleichsrechnung,” ZAMM-Journal of Applied Mathematics and Mechanics/Zeitschrift für Angewandte Mathematik und Mechanik, vol. 21, no. 6, pp. 364–379, 1941.

- [5] A. Rényi, “On measures of dependence,” Acta Mathematica Hungarica, vol. 10, no. 3-4, pp. 441–451, 1959.

- [6] L. Breiman and J. H. Friedman, “Estimating optimal transformations for multiple regression and correlation,” Journal of the American Statistical Association, vol. 80, no. 391, pp. 580–598, 1985.

- [7] D. Drouet-Mari and S. Kotz, Correlation and dependence. World Scientific, 2001.

- [8] W. Hall, On characterizing dependence in joint distributions. University of North Carolina, Department of Statistics, 1967.

- [9] G. Kimeldorf and A. R. Sampson, “Monotone dependence,” The Annals of Statistics, pp. 895–903, 1978.

- [10] J. O. Ramsay, “Monotone regression splines in action,” Statistical Science, vol. 3, no. 4, pp. 425–441, 1988.

- [11] T. Hastie and R. Tibshirani, “[monotone regression splines in action]: Comment,” Statistical Science, vol. 3, no. 4, pp. 450–456, 1988.

- [12] D. Tebbe and S. Dwyer, “Uncertainty and the probability of error (corresp.),” IEEE Transactions on Information Theory, vol. 14, no. 3, pp. 516–518, 1968.

- [13] L. Breiman, “[monotone regression splines in action]: Comment,” Statistical Science, vol. 3, no. 4, pp. 442–445, 1988.

- [14] H. Li, “A true measure of dependence,” University Library of Munich, Germany, Tech. Rep., 2016.

- [15] H. O. Lancaster, “Some properties of the bivariate normal distribution considered in the form of a contingency table,” Biometrika, vol. 44, no. 1/2, pp. 289–292, 1957.

- [16] Y. Yu, “On the maximal correlation coefficient,” Statistics & Probability Letters, vol. 78, no. 9, pp. 1072–1075, 2008.

- [17] B. Schweizer, E. F. Wolff et al., “On nonparametric measures of dependence for random variables,” The annals of statistics, vol. 9, no. 4, pp. 879–885, 1981.

- [18] H. Voss and J. Kurths, “Reconstruction of non-linear time delay models from data by the use of optimal transformations,” Physics Letters A, vol. 234, no. 5, pp. 336–344, 1997.