On Positive Solutions of a Delay Equation

Arising When Trading in Financial Markets

Abstract

We consider a discrete-time, linear state equation with delay which arises as a model for a trader’s account value when buying and selling a risky asset in a financial market. The state equation includes a nonnegative feedback gain and a sequence which models asset returns which are within known bounds but otherwise arbitrary. We introduce two thresholds, and , depending on these bounds, and prove that for , state positivity is guaranteed for all time and all asset-return sequences; i.e., bankruptcy is ruled out and positive solutions of the state equation are continuable indefinitely. On the other hand, for , we show that there is always a sequence of asset returns for which the state fails to be positive for all time; i.e., along this sequence, bankruptcy occurs and the solution of the state equation ceases to be meaningful after some finite time. Finally, this paper also includes a conjecture which says that for the “gap” interval state positivity is also guaranteed for all time. Support for the conjecture, both theoretical and computational, is provided.

I Introduction

The motivation for this paper is derived from an emerging line of research involving the use of system-theoretic ideas to trade in financial markets; e.g., see [1]–[8]. Similar to previous work, in this paper, we operate in an idealized market with no transaction costs such as brokerage commission or fees and with perfect liquidity; i.e., there is no gap between the bid and ask prices, and the trader has the ability to buy or sell any number of shares, including fractions, at the market price. These assumptions arise in the finance literature in the context of “frictionless” markets; e.g., see [9].

With the above providing the backdrop, this paper concentrates on a difference equation with delay and establishes conditions under which all solutions are positive for all . We refer to this as “all-time positivity.” Related to this work on all-time positivity are papers in the mathematics literature which deal with difference equations with multiple delays and provide conditions under which solutions are either eventually positive or eventually negative; i.e., has one sign for suitably large; e.g., see [10] and [11] and their bibliographies. As noted in Section IV, conditions in the aforementioned literature under which eventual positivity and negativity fail can be viewed as a special case of our theorem which provides a necessary condition for all-time positivity.

Problem Formulation: To formulate the problem at hand, we use to represent the unpredictable returns of a risky asset such as a stock or a foreign currency at stage . Our state-equation model for the account value includes a delay due to the fact that a trader’s interactions with the market are not instantaneous. Specifically, at stage , we take to be a feedback gain representing the targeted percentage of a trader’s account to be invested in the risky asset. Then, at stage , order transmission and execution delay are accounted for by the realized control representing the dollar level of investment at . We begin with , and for ,

to account for the delay. Accordingly, the closed-loop state equation is

with positive initial conditions

In the sequel, a time-varying sequence of risky asset returns

is called a path, and is said to be admissible if it stays within known bounds

where

The assumption excludes the case that the underlying asset price can reach zero. We take to be the set of all admissible paths and often emphasize the state dependence on by writing instead of . Additionally, we take to be the set of all such that for , stays within the known bounds above. Elements of are called admissible partial paths, or simply admissible paths when there is no confusion.

As is typical in control theory, it is convenient to eliminate the delay term in the state equation above and work with a two-state system. That is, defining the state vector

we obtain the linear time-varying system

where

As mentioned previously, we work with the specific initial conditions . Although our goal, state positivity, is the same as in existing positive system theory, for example, see [12] and [13], this body of work is not in play because the matrix can have a negative entry.

All-Time Positivity: Although the solution to the state equation exists for all , since bankruptcy precludes future trading, the analysis ceases to be meaningful once . With this as motivation, the focal point in this paper is the issue of all-time positivity. In a sense, we are addressing a question about existence and continuability of positive solutions for infinitely many stages. Indeed, for a given feedback gain , we say that the all-time positivity condition holds if

for all and all

It is also worth mentioning that is guaranteed when all-time positivity holds. In finance, the condition is interpreted to mean that the trader holds a long position and no short selling occurs. Finally, we mention that traders in financial markets often have their orders restricted by leverage constraints imposed by the broker. That is, letting

a maximum allowed leverage is specified, and the trader’s account is securitized by a requirement that . For markets involving stock, is rather typical, and for foreign currency trading, can easily be the case. Leverage imposes a restriction on . However, since our criteria and conjecture on all-time positivity apply for all , leverage bounds are ignored since they have no effect on the analysis to follow.

Plan for the Remainder of the Paper: In Section II, we present our main results. To this end, the section is centered around two critical thresholds, and with , which we define. We first provide a result, called the Sufficiency Theorem, which tells us that is sufficient for all-time positivity. Our next result, called the Necessity Theorem, gives a necessary condition for all-time positivity. Specifically, for , we prove that there is a sequence of asset returns, called the distinguished path and denoted by , for which the state fails to be positive for all . In Section III, we state two preliminary technical results regarding the state along this path. Next, in Section IV, the proofs of the preliminary and main results are provided. In Section V, we provide a conjecture which says that all-time positivity is guaranteed for the “gap” interval . The section includes both theoretical and computational support for the conjecture. Finally, in Section VI, some concluding remarks are given, and possible directions for future research are indicated.

II Main Results

The main results to follow involve two critical thresholds, and . The first of these, , is motivated by considering and noting that

This lower bound is positive if and only if

To show for all rather than just , the theorem below, proved in Section IV, requires the stronger assumption that , where

Sufficiency Theorem 0:

The condition is sufficient for all-time positivity. That is, if , given any admissible path , it follows that for all .

Necessary Condition for All-Time Positivity: As mentioned in the introduction, our necessary condition for all-time positivity is motivated by studying the state equation in response to a distinguished path of returns . This path is defined by and for . Along this path, since the first trade is executed at stage , the return can be viewed as “baiting” the trader with a large positive return and then, a worst-case scenario of sorts occurs because the account loses value on every subsequent trade. To motivate the definition of the threshold entering into our analysis of necessity, let

Then with consistent with the fact that the matrix

has a pair of complex eigenvalues, the state is oscillatory about zero. Hence the value of state can be negative. This becomes a special case of the theorem to follow. For , the solution is nonoscillatory, and our analysis shows that the state is negative for large when and , where

The theorem below, whose proof is relegated to Section IV, brings these ideas to fruition. The threshold defined next is readily verified to exceed

Necessity Theorem 0:

With

the condition is necessary for all-time positivity. Equivalently, if then there exists an admissible path such that for some .

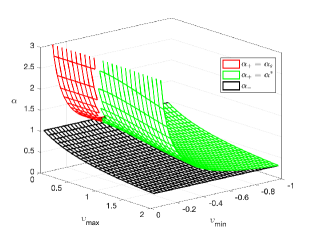

Graphical Depiction of Bounds: In Figure II, the dependencies of and on and are displayed over the range The lower surface (black) is obtained by using the formula for , the red part of the upper surface is obtained by using the formula for , and the larger green part of the upper surface is obtained using the formula for .

Figure II can be used to better understand which triples lead to all-time positivity. If the triple falls below the surface given by , then, according to the Sufficiency Theorem, all-time positivity holds. Alternatively, if the triple lies above the surface given by , then, according to the Necessity Theorem, all-time positivity fails. Finally, when the triple lies between the two surfaces, we conjecture in Section V that all-time positivity also holds.

III Preliminary Technical Results

This section provides the technical lemmas underlying the main results. In the previous section, we saw that the distinguished path plays an important role in the motivation of the Necessity Theorem. In this section, we provide two preliminary results whose proofs are relegated to Section IV. These preliminaries, involving the behavior of the state along the path , are essential to the proof of the main results to follow. In addition, later in the paper, these results are seen to provide support for our conjecture regarding all-time positivity.

Lemma 3.1 (Closed-Form for ):

If , for , the state along the distinguished path is given by

where

and

are the eigenvalues of . For the singular case, , the state solution is given by

Lemma 3.2 (Distinguished Path Properties):

(a) If , then is oscillatory about zero and is therefore negative for some values of .

(b) If and , then is negative for sufficiently large .

(c) If and , then is positive for all .

(d) If

, then is positive for all .

Remarks on State Along Distinguished Path : It is interesting in its own right to study the asymptotic behavior of , since its tending to zero signifies “practical bankruptcy,” even for cases when all-time positivity is assured. For the case in Lemma 3.1, it is clear that , which implies . Thus, by the well-known unit-circle stability criterion, for example see [15], as . The closed-form solution for the singular case also tends to zero, and it is also readily verified, using l’Hôpital’s rule, that the closed-form expression of the state solution is continuous at .

IV Proofs of Preliminary and Main Results

This section may be skipped by readers who are not interested in the technical details of the proofs.

Proof of Sufficiency Theorem: Since the case is trivial, we assume and note that it suffices to prove all-time positivity with returns allowed to range over the larger interval . We proceed by induction on . First recall that was shown to guarantee positivity of in Section II. Next, for we assume for and all . Then for arbitrary , we must show . Indeed, noting and by the induction hypothesis, we obtain lower bound

To further lower bound the right hand side above, for , let be the value of with replaced by . With this notation, we can write

Since the function to be minimized on the right-hand side above is affine linear in , its minimum value is achieved by or . We now analyze what happens to the minimum in each of case.

For , the preceding lower bound of leads to

by the induction hypothesis. For , we obtain

Since using the facts that , , and is positive by the induction hypothesis, it follows that

where last inequality holds by induction hypothesis again. Hence, is further lower bounded as

Now, applying the assumed inequality and the fact that by the induction hypothesis, we obtain .

Proof of Lemma 3.1: Recall the state space representation introduced in Section I. Using the standard state augmentation

we obtain the linear time-varying system

where is the matrix defined in Section I. Starting from initial conditions and , in state-space form, we have for ,

and we obtain

We consider two cases: For the generic case, , a lengthy but straightforward computation leads to

Another lengthy but straightforward computation shows that are the eigenvalues of . For the singular case, , we find that

which, again, following a third lengthy but straightforward computation, results in

Proof of Lemma 3.2: A proof of part (a) that does not use the closed-form of can be given immediately by applying Theorem 2.2 in [10]. However, for the sake of self-containment, we provide a first-principles proof here. Assuming that , we must show the state is oscillatory about zero and is negative for some values of . By Lemma 3.1, we have

for . With , it is readily shown that , which implies that the two eigenvalues are complex conjugates. It follows that these eigenvalues can be written in polar form as and , where and

Next, substituting the polar form of into above, a lengthy but straightforward calculation shows that

where and are constants, with . Since , it is straightforward to find a value of such that the argument of the cosine lies in thus making the cosine negative. This completes the proof of part (a).

To prove part (b), we first consider the case . Then using the formula

for the singular case in Lemma 3.1, for and sufficiently large, . Next, for the case , we assume again . Since , the state will be negative for sufficiently large if we can show that where

To establish this, since , we have

Since the square root is an increasing function, the inequality on above implies that

In addition, we also have

Thus, it follows that

Hence, the proof of part (b) is complete.

To prove part (c), we first note that the desired positivity holds trivially for . For , assuming that and , the singular case formula given in Lemma 3.1 leads that

which is positive for all because , and . It remains to treat the case and . To show for all substitute and into and note that . Then the formula for reduces to

Since and , we obtain

Since , and

for all , it follows that This completes the proof of part (c).

Finally, to prove part (d), since the result trivially follows for , we assume Note that the inequality is readily shown to be equivalent to

Furthermore the above inequalities are both strict if and only if . Suppose Then implies , and so in Lemma 3.1, we have and It suffices to prove that and that one of or is strictly positive. In the formula for , the quantity is either negative or nonnegative. If it is nonnegative, then , and on account of the fact that is equivalent to

Similarly, if the quantity above is negative, then while on account of the fact that again.

Suppose Then for the case , the state for this singular case given in Lemma 3.1 applies and is clearly positive for all . Alternatively, for the case , we argue as in the preceding paragraph and obtain , . Moreover, since , we have , which leads to

This completes the proof of part (d).

Proof of Necessity Theorem: Given , it suffices to exhibit a path for which the state is not positive for some . We claim that the distinguished path is such a path. To establish this, we split our analysis into two cases:

Case 1: For , we have . Thus, it suffices to prove for some when . Using part (a) of Lemma 3.2, we obtain that the state oscillates and takes negative values for some .

V All-Time Positivity Conjecture and Support

The conjecture to follow addresses the “gap” between the lower and upper bounds, and , for all-time positivity provided by the theorems in Section II. Subsequently, we support the conjecture with analysis and simulations for various cases involving a finite time horizon. As seen below, the notion of “extreme paths” plays an important role.

All-Time Positivity Conjecture: The all-time positivity condition holds for the gap interval

Extreme Paths: To study the conjecture, for given , we consider the extreme paths , defined by being either or for . For example, is an extreme path in . First noting that the positivity condition for all and all is equivalent to

for , we make use of the fact that is multilinear in ; i.e., affine linear in each component . For example,

is multilinear in and . We now use the well-known fact that the minimum of a multilinear function over a hypercube is attained at one of the vertices; e.g., see [14]. This implies that is minimized by one of the extreme paths . Hence, is positive for all and all if and only if

for . For small , checking this condition is feasible, but for large , the number of “checks,” namely , becomes too large. For example, in the stock market, we can easily have , but it is computationally prohibitive to check extreme paths.

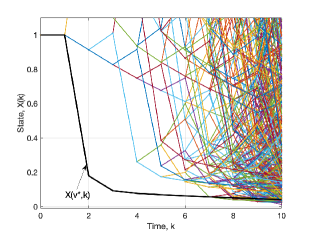

Examples for Various : Taking , , and , we have , and the gap interval is computed to be To support the conjecture, we took and chose equally-spaced values of from the gap interval and, for each , we used Matlab to check state positivity of each of the extreme paths. We found that state positivity held for all of them. In Figure V, the are shown for which lies within the gap interval above. We also ran many other simulations for various choices of , and , and consistently observed that state positivity held in the corresponding gap interval.

Given the motivation for the distinguished path in terms of a “worst-case” trading scenario in Section II, it is natural to ask if might be the minimum value of for all . However, as seen in Figure V, this proves not to be the case for .

To provide further support for the conjecture, we also studied , , and For equally spaced values of in the gap interval , we generated of the extreme paths for each . The positivity condition was seen to be satisfied in all cases. Finally, in support of the conjecture, we also ran other simulations for various choices of and , including smaller values of these bounds to more closely model values found in stock trading, and consistently observed that the desired state positivity held within the gap interval.

Theoretical Result for : In this subsection, we prove that if , then state positivity holds for all partial paths of length . We begin by noting that the cases and are immediate since are the initial conditions. Next, for , as shown in the beginning of Section II,

Thus, if and only if

Since it is also easily verified that , it follows that for and when . The case , per lemma below, requires a lengthier derivation to show that if and only if where

Then a straightforward calculation shows that

Lemma 5.1:

If then for all and all .

Proof: For any , we observe that

is minimized with . It follows that

Since the right-hand side is multilinear in and , the minimum must occur when they take the values or . If , then to minimize the right-hand side, must be . In this case, the right-hand side is lower bounded by

Similarly, if then must be which lower bounds the right-hand side by

It is easy to check that this second bound is strictly smaller than the first. Furthermore, the second bound is positive if and only if .

Finite-Time Positivity Set: Let denote the set of all feedback parameters assuring state positivity up to stage . Define

Then we have already seen above that and with readily verified. Beyond these two simple cases, one can in principle determine whether or not a given feedback parameter belongs to by checking all extreme paths. We also know, by the Sufficiency Theorem, that . If the All-Time Positivity Conjecture is true, we must have as well. Moreover, since for all , the are nonincreasing, and since they are bounded below by , they converge to a limit

It is also readily verified that otherwise, there would exist an assuring all-time positivity, which contradicts the Necessity Theorem. Finally, if the All-Time Positivity Conjecture is true, then in which case it would follow that

VI Conclusion and Future Work

In this paper, we considered a state positivity problem motivated by trading risky assets in the presence of delay. The desired positivity of the state was studied in terms of two critical thresholds, and with . First we proved that is sufficient for all-time positivity. Then we proved that is necessary for all-time positivity. Finally, we conjectured that state positivity is guaranteed for the “gap” interval Support for this conjecture, both theoretical and computational, was also provided.

Regarding further research, we mention two attractive directions. The first is obviously to pursue a proof of the conjecture. Based on many simulations, we consistently observed the following phenomenon: If for , it follows that for and all ; e.g., see Figure V where is positive and the other states are positive too, which implies for . If this observation is true for all , then parts (c) and (d) of Lemma 3.2 give us all-time positivity for .

A second direction for future research involves studying the state positivity problem when is vector-valued rather than a scalar. That is, if with being the th component satisfying with for , then, motivated by portfolio rebalancing problems with delay, the more general state equation

arises where the are scalar constant feedback parameters. In this case, generalization of the theory in this paper would be of interest. To this end, one result along these lines is that the condition

leads to oscillation and failure of all-time positivity. This can be established using arguments similar to those given in the proof of Lemma 3.2 and the related literature.

References

- [1] T. M. Cover and E. Ordentlich, “Universal Portfolios with Side Information,” IEEE Transactions on Information Theory, IT-42. pp. 348–363, 1996.

- [2] B. R. Barmish and J. A. Primbs, “On a New Paradigm for Stock Trading Via a Model-Free Feedback Controller,” IEEE Transactions on Automatic Control, AC-61, pp. 662–676, 2016.

- [3] Q. Zhang, “Stock Trading: An Optimal Selling Rule,” SIAM Journal of Control and Optimization, vol. 40, pp. 64–87, 2001.

- [4] J. A. Primbs, “Portfolio Optimization Applications of Stochastic Receding Horizon Control,” Proceedings of the American Control Conference, pp. 1811–1816, New York, 2007.

- [5] C. H. Hsieh, B. R. Barmish, and J. A. Gubner, “Kelly Betting Can Be Too Conservative,” Proceedings of the IEEE Conference on Decision and Control, pp. 3695–3701, Las Vegas, 2016.

- [6] C. H. Hsieh and B. R. Barmish, “On Drawdown-Modulated Feedback in Stock Trading,” IFAC-PapersOnline, vol. 50, pp. 952–958, 2017.

- [7] C. H. Hsieh, B. R. Barmish, and J. A. Gubner, “At What Frequency Should the Kelly Bettor Bet,” Proceedings of the American Control Conference, pp. 5485–5490, Milwaukee, 2018.

- [8] C. H. Hsieh, J. A. Gubner, and B. R. Barmish, “Rebalancing Frequency Considerations for Kelly-Optimal Stock Portfolios in a Control-Theoretic Framework,” Proceedings of the IEEE Conference on Decision and Control, pp. 5820–5825, Miami Beach, 2018.

- [9] R. C. Merton, Continuous Time Finance, Wiley-Blackwell, 1992.

- [10] L. H. Erbe and B. G. Zhang, “Oscillation of Discrete Analogues of Delay Equations,” Differential and Integral Equations, vol. 2, pp. 300–309, 1989.

- [11] L. Berezansky and E. Braverman, “On Existence of Positive Solutions for Linear Difference Equations with Several Delays,” Advances in Dynamical Systems and Applications, vol. 1, pp. 29–47, 2006.

- [12] L. Farina, “Positive Systems in the State Space Approach: Main Issues and Recent Results,” Proceedings of International Symposium on Mathematical Theory of Networks and Systems, Notre Dame, 2002.

- [13] T. Kaczorek, “Positivity and Stability of Time-Varying Discrete-Time Linear Systems,” Intelligent Information and Database Systems, Lecture Notes in Computer Science, pp. 295–303, 2015.

- [14] B. R. Barmish, New Tools for Robustness of Linear Systems, Macmillan Publishing Company, 1994.

- [15] E. I. Jury, Theory and Application of The z-Transform Method, Huntington, Krieger Publishing Company, 1973.