¯b \DeclareBoldMathCommand¸c \DeclareBoldMathCommand.d \DeclareBoldMathCommand\ee \DeclareBoldMathCommand\ff \DeclareBoldMathCommand\gg \DeclareBoldMathCommand\nn \DeclareBoldMathCommand\mm \DeclareBoldMathCommand\pp \DeclareBoldMathCommand\qq \DeclareBoldMathCommandor \DeclareBoldMathCommand\ss \DeclareBoldMathCommandˇv \DeclareBoldMathCommand\ww \DeclareBoldMathCommand\zz \DeclareBoldMathCommand\AA \DeclareBoldMathCommand\BB \DeclareBoldMathCommand\CC \DeclareBoldMathCommand\DD \DeclareBoldMathCommand\FF \DeclareBoldMathCommand\GG \DeclareBoldMathCommand˝H \DeclareBoldMathCommand\II \DeclareBoldMathCommand\JJ \DeclareBoldMathCommand\KK \DeclareBoldMathCommandŁL \DeclareBoldMathCommand\MM \DeclareBoldMathCommand¶P \DeclareBoldMathCommand\QQ \DeclareBoldMathCommand\RR \DeclareBoldMathCommand§S \DeclareBoldMathCommand\VV \DeclareBoldMathCommand\UU \DeclareBoldMathCommand\WW \DeclareBoldMathCommand\XX \DeclareBoldMathCommand\YY \DeclareBoldMathCommand\ZZ \DeclareBoldMathCommand\ssigmaσ \DeclareBoldMathCommand\SSigmaΣ \DeclareBoldMathCommand\OOmegaΩ \DeclareBoldMathCommand\mmuμ \DeclareBoldMathCommand\ones1 \DeclareBoldMathCommand\zeros0

Large-Scale Markov Decision Problems via the Linear Programming Dual

Abstract

We consider the problem of controlling a fully specified Markov decision process (MDP), also known as the planning problem, when the state space is very large and calculating the optimal policy is intractable. Instead, we pursue the more modest goal of optimizing over some small family of policies. Specifically, we show that the family of policies associated with a low-dimensional approximation of occupancy measures yields a tractable optimization. Moreover, we propose an efficient algorithm, scaling with the size of the subspace but not the state space, that is able to find a policy with low excess loss relative to the best policy in this class. To the best of our knowledge, such results did not exist in the literature previously. We bound excess loss in the average cost and discounted cost cases, which are treated separately. Preliminary experiments show the effectiveness of the proposed algorithms in a queueing application.

1 Introduction

The Markov Decision Process planning problem is to find a good policy given complete knowledge of the transition dynamics and loss function. Much work has been done by the reinforcement learning community; the earliest approaches with convergence guarantees date back to value iteration [Bellman, 1957], policy iteration [Howard, 1960], and other dynamic programming ideas. Another thread has been the linear programming formulation [Manne, 1960]. In general, the planning problem is well understood for state-spaces small enough to permit computation of the value function [Bertsekas, 2007]. However, in large state space problems, both the dynamic programming and linear program approaches are computationally infeasible as complexity scales quadratically with the number of states.

A popular approach to large-scale problems is to search for the optimal value function within the linear span of a small number of features with the hope that the optimal value function will be well approximated and will lead to a near optimal policy. Two popular methods are Approximate Dynamic Programming (ADP) and Approximate Linear Programming (ALP). For a survey on theoretical results for ADP, see [Bertsekas and Tsitsiklis, 1996], [Bertsekas, 2007, Vol. 2, Chapter 6], and more recent papers [Sutton et al., 2009b, a, Maei et al., 2009, 2010].

Our goal is to find an almost-optimal policy in some low dimensional space such that the complexity scales with the low dimensional space but is sublinear in the size of the state space. In contrast, all prior work on ALP either scales badly or requires access to samples from a distribution that depends on the optimal policy. To accomplish this, we will use randomized algorithms to optimize policies that are parameterized by linear functions in the dual LP. We provide performance bounds in the average loss and discounted loss cases. In particular, we introduce new proof techniques and tools for average cost and discounted cost MDP problems and use these techniques to derive a reduction to stochastic convex optimization with accompanying error bounds.

1.1 Markov Decision Process

Markov decision processes have become a popular approach to modeling an agent interacting with an environment, and, most notably, are the model assumed by reinforcement learning. Using , an MDP is parameterized by:

-

1.

a discrete state space ,

-

2.

a discrete action space ,

-

3.

transition dynamics that describes the distribution of the next states given a current state and action , and

-

4.

loss function that provides the cost of taking an action in a given state.

The (fully observed) state encapsulates all the persistent information of the environment, and the influence of the agent is captured through the transition distribution, which is a function of the current state and the current action.

A policy gives a distribution over actions for every possible state, and the goal of the learner is to identify a policy with small loss. Throughout, we will use and to refer to specific states and actions, respectively. Given some random variable for the starting distribution and some fixed policy , the distribution of the random variable of the initial action is fixed. Then, given the transition dynamics and , we can calculate the random trajectory . The random variables and will always refer to the random state and actions induced by a fixed policy , the transition dynamics, and initial distribution of . Using this random variable notation, we will write to refer to the th entry of , i.e. the probability of transitioning to state from state when action is taken.

How can we evaluate a policy? The two most common metrics are average cost and discounted cost. Average cost is roughly the expected loss of the policy once the Markov chain has reached stationarity and disregards the transient dynamics. Discounted cost minimizes the cost where future losses rounds into the future are discounted by , where is some discounting factor. Therefore, discounted cost emphasized the short-term cost and roughly only considers rounds into the future. Precisely,

| (average cost), and | (1) | ||||

| (discounted cost) | (2) |

The initial state is very relevant for but irrelevant for under the usual regularity (it is sufficient to assume that the induced Markov chain is recurrent [Puterman, 1994]). We study the average cost in Section 2 and the discounted cost in Section 4.

1.2 Notation

It will be convenient to be able to write the transition dynamics as a matrix multiplication. For vectors over state-action pairs, we will write for the element corresponding to state and action . The specific mapping from to is irrelevant, so just pick one and fix your favorite. We can then define the matrix to have row in the position; therefore, if is a probability distribution over , then is the distribution over . We can also define the vector of losses to have value in position .

Given a vector and a matrix , we will use for the th component of vector and , , and for the the th row, th column, and element in the position of , respectively. For matrices , where the first index is over state-action pairs, we will define to be the row corresponding to and to be the column, over state-action pairs, corresponding to the th column.

Any distribution over state-action pairs defines a policy with

| (3) |

with if for all . This is simply the conditional distribution of given . We will also define the marginalization matrix to be the binary matrix such that the th coordinate of is . If is a probability distribution over , then is the marginal of .

For some fixed policy , we would also like to refer to the induced state transition matrix, , defined by

so that if , then if policy is used.

We will use the norms and (for a positive vector ). The constant one and zero vector are and , and and refer to the element-wise minimum and maximum. We can then compactly define and as the negative and positive parts of a vector , respectively. Finally, for two vectors means element-wise inequality, i.e. for all .

1.3 Linear Programming for Average Cost

For the average cost, let be a vector and a scalar. The Bellman operator for average cost is

and and correspond to an optimal policy if they satisfy the Bellman optimality equation,

We will call such an and the differential value function and the average cost, respectively. When the Bellman optimality equation is satisfied, the greedy policy (taking the action that achieves the minimum in the operator with probability 1) achieves the optimal loss [Puterman, 1994].

The Bellman optimality equation was first recast as a linear program by Manne [1960], who noted that, if and satisfy , then we must have , where is the average cost of the optimal policy. Therefore, the optimal and are the solution to

Now, notice that is equivalent to requiring for all and . In our matrix notation, this is precisely . Hence, the Bellman optimality equation is equivalent to the linear program

| (4) | ||||

A standard computation shows that the dual of LP (4) has the form of

| (5) | ||||

The dual variable, , has an important interpretation: it is a stationary distribution over state-action pairs under its implied policy.

The first two constraints ensure that is a probability distribution over state-action space and the third constraint forces to be a stationary distribution under . Intuitively, if , then is the distribution of under policy ; hence, the third constraint implies that and have the same distribution. If is a stationary distribution, then the average loss under is exactly .

1.4 Linear Programming for Discounted Cost

There are analogous notions for the discounted cost setting. We define a value function as a mapping from states to discounted costs. The hope is to find , where is the discounted cost starting in state if the optimal policy is used.

We define the Bellman operator for discounted cost

and the optimal value function will be the fixed point of the Bellman operator,

It is easy to check that implies , and therefore, for any strictly positive vector , the optimal value function is the solution to the linear program

| (6) | ||||

We also have an interpretable dual LP. Let be such that and . The linear program for discounted MDPs in the dual space has the form of

| (7) | ||||

Unlike the average cost case, the dual variable cannot be interpreted as a stationary distribution. However, it can be thought of as the discounted number of visits, as made explicit in the following theorem from Puterman [1994]:

Theorem 1.

-

1.

For each randomized Markovian policy and state and action , define by

Then is a feasible solution to the dual problem.

-

2.

Suppose is a feasible solution to the dual problem, then, for each , . Define the randomized stationary policy by

Then, is a feasible solution to the dual LP and .

Thus, we can approximately solve the planning problem if we find a vector such that the discounted cost of the policy defined by , namely , is small. To handle possibly negative entries of , we more generally define

In this case, the precise relationship between and the value function can be found in Puterman [1994]: for any vector ,

| (8) |

where is the value function corresponding to policy .

1.5 Approximate Linear Programming

If we ignore computational constraints, we can solve the planning problem by solving the linear programs (5) and (7). Unfortunately, state spaces are frequently very large and often grow exponentially with the complexity of the system (e.g. number of queues in the queuing network), and therefore any method polynomial in becomes intractable. The general method of solving the planning problem with an approximate solution to the linear program is called Approximate Linear Programming (ALP). As any general optimality guarantee is impossible with computation sublinear in without special knowledge of the problem, we instead aim for optimality with respect to some smaller policy class.

We take the less common approach of reducing the dimensionality by placing a subspace restriction of the dual variables. Let by a feature matrix and some known stationary distribution (that can be taken to be zero but allows a user to start with a good policy). For the average cost case, we will limit our search to for ; that is, we will study the approximate average cost dual LP,

| (9) | ||||

we will only consider that sum to 1 and will restrict to lie in . This restriction is without loss of generality, since we may always renormalize .

For every , we associate a policy

| (10) |

and a stationary distribution the actual stationary distribution of running policy . Thus, the average cost corresponding to the policy is .

For the discounted cost case with feature matrix , we restrict the dual variable to and define the approximate discounted cost dual LP

For every , we define a policy

| (11) |

and let be the corresponding dual variable (i.e. the discounted number of visits); hence, is the discounted cost as in (8). In the discounted case, we will restrict to lie in .

1.6 Problem Definition

The goal of the paper is to find a such that the associated policy is close to the policy corresponding with the best in an efficient manner and while avoiding complexity proportional to . This goal is formalized by the following definition.

Definition 1 (Efficient Large-Scale Dual ALP).

For an MDP specified by and with the dual variables corresponding to , the efficient large-scale dual ALP problem is to find a such that

| (12) |

in time polynomial in and . The model of computation allows access to arbitrary entries of , , , , , and in unit time.

The computational complexity cannot scale with and we do not assume any knowledge of the optimal policy. In fact, as we shall see, we solve a harder problem, which we define as follows.

Definition 2 (Expanded Efficient Large-Scale Dual ALP).

Let be some “violation function” that represents how far is from satisfying the constraints of (5) or (7) and has if is feasible.

The expanded efficient large-scale dual ALP problem is to produce parameters such that

| (13) |

in time polynomial in and , under the same model of computation as in Definition 1.

Note that the expanded problem is strictly more general as guarantee (13) implies guarantee (12). Also, many feature vectors may not admit any feasible points. In this case, the dual ALP problem is trivial, but the expanded problem is still meaningful.

In particular, we desire an agnostic learning guarantee, where the true average cost of running the policy corresponding to to be close to the true average cost of the best policy in the class, regardless of how well the policy class models the optimal value function. To the best of our knowledge, such a guarantee does not exist in the literature.

Having access to arbitrary entries of the quantities in Definition 1 arises naturally in many situations. In many cases, entries of are easy to compute. For example, suppose that for any state there are a small number of state-action pairs such that . Consider Tetris; although the number of board configurations is large, each state has a small number of possible neighbors. Dynamics specified by graphical models with small connectivity also satisfy this constraint. Computing entries of is also feasible given reasonable features. If a feature is a stationary distribution, then . Otherwise, it is our prerogative to design sparse feature vectors, hence making the multiplication easy. We shall see an example of this setting later.

1.7 Related Work

Approximate linear programming, proposed by Schweitzer and Seidmann [1985], constrained the value function in the linear program to a low-dimensional subspace. In the discounted cost setting, the first theoretical analysis of ALP methods, by de Farias and Van Roy [2003a], analyzed the discounted primal LP (7) performance when only value functions of the form , for some feature matrix , are considered. Roughly, they show that the ALP solution has the family of error bound indexed by a vector

where is a “state-relevance” vector and is a “goodness-of-fit” parameter that measures how well represents a stationary distribution. Unfortunately, and are typically hard to choose (for example, a good choice of would be the stationary distribution under , which we do not know); but more importantly, the bound can be vacuous if does not model the optimal value function well and is always large. In particular, the problem we are considering in Definition 2 requires an additive bound with respect to the optimal parameter.

There are also computational concerns with the ALP, as the number of constraints remains . One solution, proposed by de Farias and Van Roy [2004], was to sample a small number of constraints and solve the resulting LP; this resulted in an error bound of the form

but the required number of sampled constraints needs to be a function of the stationary distribution of the optimal policy.

Desai et al. [2012] proposed a different relaxation by defining the Smoothed Approximate Linear Program, which only requires a soft feasibility and solves the linear program

which is exact LP (6) with , the Bellman optimality constraint relaxed with a slack variable , and additional bounds places on . Here, is the stationary distribution of the optimal policy and a violation budget, so the method requires some knowledge of the optimal policy. Despite this, the method remains computationally efficient and able to produce an agnostic approximation bound

However, their results do not easily extend to bounding the true error of running the policy associated with , , without choosing as a function of , which is itself a function of . Petrik and Zilberstein [2009] proposed two different constraint relaxations schemes for the ALP, but did not show better approximations to the true solution, but rather focused on the better empirical performance. Yet another relaxation of the primal LP was proposed by Lakshminarayanan et al. [2018], who generalized previous constraint sampling approaches. A bound for the discounted loss of the policy associated with the solution to this relaxed LP is presented and neatly decomposes into an estimation error that tends to zero and an approximation error between the optimal LP solution and the optimal relaxed LP solution.

In the average cost setting, largely thought to be more difficult, shares a similar history is that the first theoretical analysis for ALP was by de Farias and Van Roy [2003b]. They proposed a two stage LP. The first approximates the optimal average cost and the second uses this estimate to try and learn the differential cost function . The method suffers from the same problem as the discounted cost case is that we can only guarantee that , the excess loss of running the policy associated with , is small when we tune the LP with knowledge of , the stationary distribution.

Subsequent work in de Farias and Van Roy [2006] took a different approach by viewing the average cost LP as a perturbed discounted cost LP, which is easier to analyze. Again, the span of the feature vectors needs to approximate the optimal policy in order for the excess loss guarantee to be meaningful. More recently, Veatch [2013] proposed a relaxation, similar to the smoothed ALP but with the total constraint violation terms entering the objective instead of facing a hard constraint, and derived similar loss bounds.

Recently, Chen et al. [2018] analyzed a linearly parameterized ALP where the state and action spaces are both parameterized by linear features and the value function is assumed to be well approximated by linear function of the state features. They propose an efficient algorithm but suffer the same drawback and retain an error term of the form . Additionally, Banijamali et al. [2019] study the related problem of optimizing policies in the convex hull of base policies. This problem can be seen as a special case of the usual ALP formulation when all features correspond to the stationary distribution of policies.

To the best of our knowledge, no work has been able to show a bound of the form (13), as all the previous bounds are only meaningful when the approximate policy class can closely approximate the optimal policy. We are also the first to prove theoretical guarantees when the dual variables of the LP are restricted to a linear class, though such a parameterization appeared previously by Wang et al. [2008], albeit without theoretical guarantees. See Section D in the appendix for a more thorough literature review and precise statements of prior bounds.

1.8 Our Contributions

We prove that if we parameterize the policy space by using the approximate dual LPs, then we can solve the expanded efficient large-scale dual ALP problem for both average cost and discounted cost. In the average cost setting, we require a (standard) assumption that the distribution of states under any policy converges quickly to its stationary distribution, but no such assumption is needed in the discounted cost setting. We also show that it suffices to solve the approximate dual LPs by approximately minimizing a surrogate loss function equal to the sum of the objective and a scaled violation function.

We begin with the average cost in Section 2 and prove that, for some parameter , any and , the excess loss bound

holds with probability at least , where . The term is zero for feasible points (that is, points in the intersection of the feasible set of LP (9) and the span of the features). For points outside the feasible set, these terms measure the extent of constraint violations for the vector , which indicate how well stationary distributions can be represented by the chosen features.

However, optimizing the excess loss bound to obtain the guarantee of Definition 2 requires us to tune correctly (in particular, setting ). Unfortunately, the convex surrogate is not jointly convex in and . In Section 3, we present and analyze a meta-algorithm that solves the convex surrogate for a grid on values and returns a that has

We emphasize that this bound is on the loss of actually running the policy, which could differ from the surrogate used in the optimization, . The run-time, up to logarithmic factors, is for both algorithms; we essentially can tune for a small logarithmic cost.

As we have seen in the related works section, all previous guarantees for efficient ADP algorithms only had meaningful guarantees when the policy class closely approximates the true value function, and many algorithms required tuning (say, of the state relevance weights) with knowledge of the optimal policy or stationary distribution. These restrictions render previous guarantees meaningless in many modern reinforcement learning systems, where the optimal value function is completely unknown and it is hopeless to try to engineer features that can approximate it [Goodfellow et al., 2016]. Our algorithm have guarantees that are meaningful in this setting, as we can obtain near-optimal excess loss within the policy class; in fact, one can use the stationary distribution of existing policies (based on DQN, heuristics, etc.) as feature vectors and improve upon them.

We then turn to the discounted cost problem in Section 4. We propose an algorithm and show that it guarantees a bound on the discounted cost of the form

Furthermore, the meta-algorithm, with minimal modification, solves the Expanded Efficient Large-Scale Dual ALP problem by obtaining the bound

where the violation function for the discounted cost is .

Section 5 then demonstrates the effectiveness of our method on a well studied example from queuing theory, the Rybko-Stolyar queue. We show that using two simple heuristic policies with a small number of simple features provides good performance.

2 The Dual ALP for Average Cost

Is this section, we propose and analyze our solution to the Expanded large-scale MDP problem for average cost. As discussed in the introduction, there are two main challenges for solving the planning problem in its LP formulation: the optimization is in dimension , and there are constraints, which is intractable in the large state-space setting.

We solve the two challenges by projecting the dual LP onto a subspace and by approximately solving the optimization using stochastic gradient descent, respectively. Unlike previous approaches for the primal LP, we show that an approximate solution in the dual allows us to bound the excess loss, i.e. one that controls the error between our approximate solution and the best solution in some approximate policy class, and thereby solve Equation (13). We also provide some interpretation of the approximations we make.

Recall that, for a matrix and a known stationary distribution (which may be set to zero if no distribution is known), we defined the dual ALP

and associated every with the policy

We denote the stationary distribution of this policy , which is only equal to if is in the feasible set.

2.1 A Reduction to Stochastic Convex Optimization

Unfortunately, the ALP (9) still has constraints and cannot be solved exactly. Instead, we will use the penalty method to form an unconstrained convex optimization that will act as a surrogate for the original problem and show that it is a finite sum, e.g. equal to . Therefore, we can apply the extensive literature of solving finite sum problems with stochastic subgradient descent methods.

To this end, for a constant , define the following convex cost function by adding a multiple of the total constraint violations to the objective of the LP (9):

| (14) |

We justify using this surrogate function as follows. Suppose we find a near optimal vector such that . We will prove

-

1.

that and are small and is close to (Lemma 3), and

-

2.

that .

As we will show, these two facts imply that with high probability, for any ,

Unfortunately, calculating the gradients of is . Instead, we construct unbiased estimators and use stochastic subgradient descent. Let be the number of iterations of our algorithm, and be distributions over the state-action and state space, respectively (we will later discuss how to choose them), and and be i.i.d. samples from these distributions. At round , the algorithm estimates subgradient by

| (15) |

This estimate is fed to the projected subgradient method, which in turn generates a vector . After rounds, we average vectors and obtain the final solution . Vector defines a policy, which in turn defines a stationary distribution . The algorithm is shown in Figure 1.

Input: Constants and , number of rounds , step size . Let be the Euclidean projection onto . Initialize . for do Sample and . Compute subgradient estimate (15). Update . end for . Return policy .

2.2 Excess Loss bound

We now turn towards proving the main result of this section, Theorem 2, which requires a (standard) assumption that any policy quickly converges to its stationary distribution.

-

Assumption A1 (Fast Mixing) For any policy , there exists a constant such that for all distributions and over the state space, .

Define

These constants appear in our excess loss bounds, so we would like to choose distributions and such that and are small. Several common scenarios permit convenient and :

-

•

Sparseness of If there is such that for any and , and each column of has only non-zero elements, then we can simply choose and to be uniform distributions and

-

•

Features as stationary distributions If every feature is the stationary distribution of some policy, then we can choose and vanishes.

-

•

Exponential distributions If are exponential distributions and feature values at neighboring states are close to each other, then we can choose and to be appropriate exponential distributions so that and are always bounded.

-

•

One step look-ahead When the columns of are close to their one step look-ahead, there exists a constant such that for any , . If we are also able to compute and , then it is natural to take and .

In what follows, we assume that such distributions and are known.

Minimizing the convex surrogate function does not guarantee a feasible solution to the original dual LP. Therefore, we define the following non-feasibility penalties which roughly correspond to how far is from the simplex and how far is from a stationary distribution, respectively:

The rest of the section proves the following theorem, our main guarantee for the stochastic subgradient method.

Theorem 2.

Consider an expanded efficient large-scale dual ALP problem and some error tolerance and desired maximum probability of error . Then running the stochastic subgradient method (shown in Figure 1) with

yields a where

holds with probability at least . In particular, for the choice of , the bound becomes

| (16) |

Constants hidden in the big-O notation are polynomials in , , , , , , , and .

Functions and are bounded by small constants for any set of normalized features: for any ,

Thus and can be very small given a carefully designed set of features. The output is a random vector as the algorithm is based on a stochastic convex optimization method. The above theorem shows that with high probability the policy implied by this output is near optimal.

The optimal choice for is , where is the minimizer of RHS of (16) and not known in advance. One could think of parameterizing the optimization problem by , but the problem is not jointly convex in and . Nevertheless, we present methods that recover a error bound using a grid based method in Section 3.

2.3 Analysis

This section provides the necessary technical tools and a proof of the main result. We break the proof into two main ingredients. First, we demonstrate that a good approximation to the surrogate loss gives a feature vector that is almost a stationary distribution; this is Lemma 3. Second, we justify the use of unbiased gradients in Theorem 4 and Lemma 6. The section concludes with the proof of Theorem 2. Long, technical proofs have been moved to Section A when we felt that their inclusion did not add much insight.

The first ingredient shows that we can relate the magnitude of the constraint violation of to the difference between and , which quantifies how far is from a stationary distribution.

Lemma 3.

Let be a vector, be the set of points where , and be the complement of . Assume

The vector defines a policy, which in turn defines a stationary distribution . We have that

The second ingredient is the validity of the subgradient estimates. We assume access to estimates of the subgradient of a convex cost function. Error bounds can be obtained from results in the stochastic convex optimization literature; the following theorem, a high-probability version of Lemma 3.1 of Flaxman et al. [2005] for stochastic convex optimization, is sufficient. We note that the variance reduced stochastic gradient descent literature (e.g. SAGA or SVGR) cannot be directly applied since a full gradient calculation is impossible, and most complexity upper bounds are at least [Xiao and Zhang, 2014], which is inappropriate for our setting.

Theorem 4.

Consider a bounded set of radius (i.e. for all and a sequence of real-valued convex cost functions . Let be the stochastic gradient decent path defined by defined by and , where is the Euclidean projection onto , is a learning rate, and are bounded unbiased subgradient estimates; that is, and for some . Then, for and any ,

| (17) |

with probability at least .

Proof.

Remark 5.

Let denote the RHS of (17). If all cost functions are equal to , then by convexity of and an application of Jensen’s inequality, we obtain that .

The last step before giving the proof of Theorem 2 is to apply Theorem 4 to our convex surrogate function, .

Lemma 6.

The proof (in the appendix) consists of checking that conditions of Theorem 4 are satisfied

With both ingredients in place, we can prove our main result.

Proof of Theorem 2.

Let be the RHS of (18). Using the trivial fact that , we can easily derive

| (19) |

Lemma 6 implies that with high probability for any ,

| (20) |

From (20), we get that

| (21) | ||||

| (22) |

Inequalities (21) and (22) and Lemma 3 give the following bound:

| (23) |

and we can similarly bound

| (24) |

Combining these two equations with (20) gives the final result:

Using the form of above, we find the excess loss bound

| (25) | ||||

| (26) |

Now, recall that we set

which finally yields that with high probability, for any ,

as claimed. ∎

2.4 Comparison with Previous results

With a precise statement of our main result, we return to compare Theorem 2 from de Farias and Van Roy [2006]. Their approach is to relate the original MDP to a perturbed version 111In a perturbed MDP, the state process restarts with a certain probability to a restart distribution. Such perturbed MDPs are closely related to discounted MDPs. and then analyze the corresponding ALP. Let be a feature matrix that is used to estimate value functions. Recall that is the average loss of the optimal policy and is the average loss of the greedy policy with respect to value function . Let be the differential value function when the restart probability in the perturbed MDP is . For vector and positive vector , define the weighted maximum norm . de Farias and Van Roy [2006] prove that for appropriate constants and weight vector ,

| (27) |

This bound has similarities to bound (16): tightness of both bounds depends on the quality of feature vectors in representing the relevant quantities (stationary distributions in (16) and value functions in (27)). Once again, we emphasize that the algorithm proposed by de Farias and Van Roy [2006] is computationally expensive and requires access to a distribution that depends on optimal policy.

3 Average Cost Meta-Algorithm

The previous section proved that Algorithm 1 found a with

where is a hyperparameter and is some error tolerance. If one has reason to believe that the violation terms are negligible (for example, if the features are close to stationary distributions), then one can set . However, we wish to be adaptive to the size of the constrain violations around the optimum , and ideally obtain the excess loss bound

which would imply that we have solved the Expanded Efficient Large-Scale Dual ALP problem (Definition 2) with violation .

Unfortunately, we must jointly optimize over and and the objective is not jointly convex. We avoid this difficulty with a meta-algorithm, proposed and analyzed in this section.

This meta-algorithm, detailed in Figure 2, uses Algorithm 1 to approximate over a grid of values. It takes as inputs a bound on the violation function , a desired error tolerance , and desired probability tolerance . The algorithm then carefully chooses a grid , and, for each , computes , the output of Algorithm 1 with parameter , and , an approximation to . It then returns , where

Intuitively, this two-step procedure approximately computes

| (28) |

which produces a bound that satisfies Definition 2.

Throughout this section, we use the following notation. We define , , and . Hence, the optimization (28) is equal to .

Input: Upper bound on , error tolerance , error probability , constraint estimation distributions and Initialize and while do Set Set end while Set for do Obtain from Algorithm 1 with Set Sample and Set end for Set Return policy

3.1 Estimating the Error Functions

To run the Grid Algorithm, we need to be able to estimate the constraint violations . Similar to the gradient estimate, we estimate by importance-weighted sampling. For some and samples and , define

| (29) |

Since and , this estimate is clearly unbiased. Also, we earlier assumed the existence of constants and , and so we can bound

which gives us concentration of around . In particular, applying Hoeffding’s inequality yields:

Lemma 7.

Given and , for any , the violation function estimate has

with probability at least as long as we choose

3.2 Choosing the Coarseness of the Grid

We wish to construct the sequence such that is always , and hence we need control of the smoothness of . Recall that we will choose to approximately balance the two terms , and so it suffices to only search for . The maximum will be determined by .

Lemma 8.

Let be some desired error tolerance and be some upper bound on ; we can always take . Consider the sequence defined in Algorithm 2 by the base case , induction step , and terminal condition . The grid has the property that

| (30) |

Additionally, we have .

Proof.

Our first goal is to bound . We first note that , which is a function of only, is increasing since

We also note that is sublinear in , and indeed

The two observations imply that

and hence we may bound

We now check that the grid has the property that

for all . Defining , we see that for all . The left hand side of the above condition is equal to

giving us the desired condition.

Lastly, we calculate an upper bound on , the number of grid points needed. We can write

and using the bounds and , we have that , which implies that

Since we defined , we conclude that , where is the smallest index such that

leading to the conclusion that . ∎

3.3 Meta-Algorithm Excess Loss Bound

Combining the results from the last two section yields the following theorem.

Theorem 9.

For some and , the Meta-Algorithm specified in Figure 2 has excess loss

| (31) |

with probability at least . It requires subgradient steps and samples to estimate the constraint violations.

In particular, adapting to the optimal only introduces logarithmic terms to the run time.

4 The Dual ALP for Discounted Cost

We now change settings to discounted cost and try to find a policy with discounted cost almost as low as the best in the class. Most of the tools from the average cost carry over with small modifications, and we will focus on presenting the results in this section with most of the theorem proofs presented in the appendix.

Recall that the LP we intend to approximately solve is

This LP has another interpretation. The dual of the approximate dual is

which can be viewed as the original primal with constraint aggregation.

Approximately solving the LP

Analogous to and , we define, relative to a feature matrix , the constraint violation functions

so that we can approximate the solution of the LP by minimizing the convex surrogate

| (32) | ||||

with some constant and the constraint set .

We will minimize (32) through stochastic subgradient descent by sampling and and calculating the unbiased estimator of the subgradient,

| (33) |

The algorithm for the average cost case is exactly the same as Figure 1 with instead of . Recall that we are using the shorthand

Thus, our objective is to show that is small.

A key difference between the average and discounted cases is the interpretation for the dual variables, and . In the average case, the feasible exactly corresponded to stationary distributions and therefore the average loss was precisely . However, in the discounted case, the dual variables correspond to the expected discounted number of visits to each state and , where is the value function corresponding to policy .

4.1 A Excess Loss Bound for a Fixed

Unlike the average cost case, the discounted cost case does not need a fast mixing assumption. Instead, we assume that the operator 1-norm of is upper bounded by some constant :

| (34) |

We also need to assume coverage of the constraint sampling distribution, analogously to the average cost case. We assume existence of constants and such that

Special structure may suggest natural choices of sampling distributions to ensure small and . For example, if is sparse with support on only elements and if there is such that for any and , and each column of has only non-zero elements, we can choose and to be uniform distributions and we can bound

Finally, note that we can always upper bound the constraint violation functions. For any ,

We can combine both statements and obtain

| (35) |

as long as and .

The method we propose for optimizing in the discounted cost setting is to apply stochastic subgradient descent (from Figure 1) to subgradients defined in (33). Our algorithm for optimizing discounted cost MDPs is just Figure 1 run with subgradient (defined in (33)) instead of .

We now present the excess loss bound for discounted cost and a fixed .

Theorem 10.

Consider an expanded efficient large-scale dual ALP problem and some error tolerance , desired maximum probability of error , and parameter . Running the stochastic subgradient method (Figure 1 with ) with

| (36) |

and constant learning rate , where , yields a with

Constants hidden in the big-O notation are polynomials in , , , , and .

Because the proof is very similar to the average cost section, it has been deferred to Section B.

4.2 Error Bound

Previous ADP literature concentrated on showing that the optimal value is well approximated if the feature space contains elements close to the optimum; i.e. was bounded in terms of . Theorem 10 is certainly more general, as it remains non-trivial even if is large. For completeness, we provide a corollary of this form.

Corollary 11.

Under the same conditions as Theorem 10,

| (37) |

Proof of Corollary 11.

Let be one of the vectors minimizing . Theorem 10 gives

Since and by the simple fact that for any , we have

| (38) |

For the term , since is feasible (i.e., )

| (39) |

where is the matrix operator 1-norm. Therefore, we have,

Next, we bound . Since and and by Lemma 13,

where the last inequality is due to (38) and (39). The theorem statement follows from combining these two results. ∎

4.3 The Meta-Algorithm for Discounted Cost

Input: Upper bound on , error tolerance , error probability , constraint estimation distributions and Initialize and while do Set Set end while for do Obtain from Algorithm 1 with set by (36) Set Sample and Set end for Set Return policy

Analogously to the average cost case, setting correctly yields a excess loss bound of . The excess loss bound from Theorem 10 suggests that we want and to optimize

where we have defined . The Meta-Algorithm for discounted cost, presented in Figure 3, operates in a manner very similar to the average cost case: a grid is chosen, the corresponding are computer, then , where

is returned. We can prove the following bound for the meta-algorithm.

Theorem 12.

For some and , the Meta-Algorithm for discounted cost (Figure 3 has excess loss

with probability at least . It requires subgradient steps and samples to estimate the constraint violations.

For the proof and technical details, please see Section C.

5 Experiments

In this section, we apply both algorithms to the four-dimensional discrete-time queuing network illustrated in Figure 4. This network has a relatively long history; see, e.g. Rybko and Stolyar [1992] and more recently de Farias and Van Roy [2003a] (c.f. Section 6.2). There are four queues, , each with state . Since the cardinality of the state space is , even a modest results in huge state-spaces. For time , let be the state and , denote whether queue is being served. Server 1 only serves queue 1 or 4, server 2 only serves queue 2 or 3, and neither server can idle. Thus, and . The dynamics are as follows. At each time , the following random variables are sampled independently: , , and for . Using to denote the standard basis vectors, the dynamics are:

and (i.e. all four states are thresholded from below by 0 and above by ). The loss function is the total queue size: . We compared our method against two common heuristics. In the first, denoted LONGER, each server operates on the queue that is longer with ties broken uniformly at random (e.g. if queue 1 and 4 had the same size, they are equally likely to be served). In the second, denoted LBFS (last buffer first served), the downstream queues always have priority (server 1 will serve queue 4 unless it has length 0, and server 2 will serve queue 2 unless it has length 0). These heuristics are common and have been used as benchmarks for queuing networks (e.g. de Farias and Van Roy [2003a]).

We used , , and , and buffer sizes , as the parameters of the network.. The asymmetric size was chosen because server 1 is the bottleneck and tend to have longer queues. The first two features are features of the stationary distributions corresponding to two heuristics. We also included two types of non-stationary-distribution features. For every interval and action , we added a feature with if is in the interval and . To define the second type, consider the three intervals , , and . For every 4-tuple of intervals and action , we created a feature with only if and . Every feature was normalized to sum to 1. In total, we had 372 features which is about a reduction in dimension from the original problem.

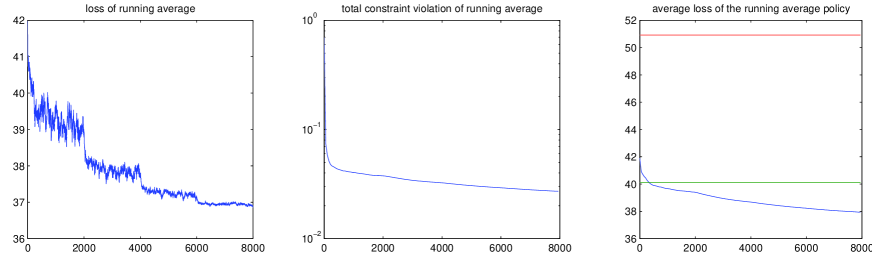

We ran our stochastic subgradient descent algorithm with sampled constraints and constraint gain . Our learning rate began at and halved every iterations. The results of our algorithm are plotted in Figure 5, where denotes the running average of . The left plot is of the LP objective, . The middle plot is of the sum of the constraint violations, . Thus, is a scaled sum of the first two plots. Finally, the right plot is of the average losses, and the two horizontal lines correspond to the loss of the two heuristics, LONGER and LBFS. The right plot demonstrates that, as predicted by our theory, minimizing the surrogate loss does lead to lower average losses.

All previous algorithms (including de Farias and Van Roy [2003a]) work with value functions, while our algorithm works with stationary distributions. Due to this difference, we cannot use the same feature vectors to make a direct comparison. The solution that we find in this different approximating set is slightly worse than the solution of de Farias and Van Roy [2003a].

6 Conclusion

This paper demonstrated the feasibility of solving the MDP planning problem with a parametric policy class based on an approximate dual LP. Unlike previous approaches, we were able to prove excess loss bounds, that is, bounds relative to the best policy in our parametric class. We obtained results for both the average cost and discounted cost settings as well as empirical justification.

There are several promising directions. First, are such excess loss bounds possible in the primal formulation?

Another drawback to our methods is that we need a backwards simulator, that is, access to every state with positive probability of transitioning into a state . Are there alternative formulations that remove this requirement?

References

- Abbasi-Yadkori [2012] Y. Abbasi-Yadkori. Online Learning for Linearly Parametrized Control Problems. PhD thesis, University of Alberta, 2012.

- Banijamali et al. [2019] Ershad Banijamali, Yasin Abbasi-Yadkori, Mohammad Ghavamzadeh, and Nikos Vlassis. Optimizing over a restricted policy class in Markov decision processes. In AISTATS, 2019.

- Bellman [1957] R. Bellman. Dynamic Programming. Princeton University Press, 1957.

- Bertsekas [2007] D. P. Bertsekas. Dynamic Programming and Optimal Control. Athena Scientific, 2007.

- Bertsekas and Tsitsiklis [1996] D. P. Bertsekas and J. Tsitsiklis. Neuro-Dynamic Programming. Athena scientific optimization and computation series. Athena Scientific, 1996.

- Chen et al. [2018] Yichen Chen, Lihong Li, and Mengdi Wang. Scalable bilinear learning using state and action features. arXiv preprint arXiv:1804.10328, 2018.

- de Farias and Van Roy [2003a] D. P. de Farias and B. Van Roy. The linear programming approach to approximate dynamic programming. Operations Research, 51, 2003a.

- de Farias and Van Roy [2003b] D. P. de Farias and B. Van Roy. Approximate linear programming for average-cost dynamic programming. In Advances in Neural Information Processing Systems (NIPS), 2003b.

- de Farias and Van Roy [2004] D. P. de Farias and B. Van Roy. On constraint sampling in the linear programming approach to approximate dynamic programming. Mathematics of Operations Research, 29, 2004.

- de Farias and Van Roy [2006] D. P. de Farias and B. Van Roy. A cost-shaping linear program for average-cost approximate dynamic programming with performance guarantees. Mathematics of Operations Research, 31, 2006.

- de la Peña et al. [2009] V. H. de la Peña, T. L. Lai, and Q-M. Shao. Self-normalized processes: Limit theory and Statistical Applications. Springer, 2009.

- Desai et al. [2012] V. V. Desai, V. F. Farias, and C. C. Moallemi. Approximate dynamic programming via a smoothed linear program. Operations Research, 60(3):655–674, 2012.

- Flaxman et al. [2005] A. D. Flaxman, A. T. Kalai, and H. B. McMahan. Online convex optimization in the bandit setting: gradient descent without a gradient. In Proceedings of the sixteenth annual ACM-SIAM symposium on Discrete algorithms, 2005.

- Goodfellow et al. [2016] Ian Goodfellow, Yoshua Bengio, Aaron Courville, and Yoshua Bengio. Deep learning, volume 1. MIT press Cambridge, 2016.

- Guestrin et al. [2004] C. Guestrin, M. Hauskrecht, and B. Kveton. Solving factored mdps with continuous and discrete variables. In Twentieth Conf. Uncertainty in Artificial Intelligence, 2004.

- Hauskrecht and Kveton [2003] M. Hauskrecht and B. Kveton. Linear program approximations to factored continuous-state markov decision processes. In Advances in Neural Information Processing Systems, 2003.

- Howard [1960] R. A. Howard. Dynamic Programming and Markov Processes. MIT, 1960.

- Lakshminarayanan et al. [2018] Chandrashekar Lakshminarayanan, Shalabh Bhatnagar, and Csaba Szepesvári. A linearly relaxed approximate linear program for markov decision processes. IEEE Transactions on Automatic Control, 63(4):1185–1191, 2018.

- Maei et al. [2009] H. R. Maei, Cs. Szepesvári, S. Bhatnagar, D. Precup, D. Silver, and R. S. Sutton. Convergent temporal-difference learning with arbitrary smooth function approximation. In Advances in Neural Information Processing Systems, 2009.

- Maei et al. [2010] H. R. Maei, Cs. Szepesvári, S. Bhatnagar, and R. S. Sutton. Toward off-policy learning control with function approximation. In Proceedings of the 27th International Conference on Machine Learning, 2010.

- Manne [1960] A. S. Manne. Linear programming and sequential decisions. Management Science, 6(3):259–267, 1960.

- Petrik and Zilberstein [2009] M. Petrik and S. Zilberstein. Constraint relaxation in approximate linear programs. In Proc. 26th Internat. Conf. Machine Learning (ICML), 2009.

- Puterman [1994] Martin L. Puterman. Markov Decision Processes: Discrete Stochastic Dynamic Programming. John Wiley & Sons, Inc., New York, NY, USA, 1st edition, 1994.

- Rybko and Stolyar [1992] A. N. Rybko and A. L. Stolyar. Ergodicity of stochastic processes describing the operation of open queueing networks. Problemy Peredachi Informatsii, 28(3):3–26, 1992.

- Schweitzer and Seidmann [1985] P. Schweitzer and A. Seidmann. Generalized polynomial approximations in Markovian decision processes. Journal of Mathematical Analysis and Applications, 110:568–582, 1985.

- Sutton et al. [2009a] R. S. Sutton, H. R. Maei, D. Precup, S. Bhatnagar, D. Silver, Cs. Szepesvári, and E. Wiewiora. Fast gradient-descent methods for temporal-difference learning with linear function approximation. In Proceedings of the 26th International Conference on Machine Learning, 2009a.

- Sutton et al. [2009b] R. S. Sutton, Cs. Szepesvári, and H. R. Maei. A convergent O(n) algorithm for off-policy temporal-difference learning with linear function approximation. In Advances in Neural Information Processing Systems, 2009b.

- Veatch [2013] M. H. Veatch. Approximate linear programming for average cost mdps. Mathematics of Operations Research, 38(3), 2013.

- Wang et al. [2008] T. Wang, D. Lizotte, M. Bowling, and D. Schuurmans. Dual representations for dynamic programming. Journal of Machine Learning Research, pages 1–29, 2008.

- Xiao and Zhang [2014] Lin Xiao and Tong Zhang. A proximal stochastic gradient method with progressive variance reduction. SIAM Journal on Optimization, 24(4):2057–2075, 2014.

- Zinkevich [2003] M. Zinkevich. Online convex programming and generalized infinitesimal gradient ascent. In ICML, 2003.

7 Acknowledgments

We gratefully acknowledge the support of the NSF through grant CCF-1115788 and of the ARC through an Australian Research Council Australian Laureate Fellowship (FL110100281).

Appendix A Deferred Proofs for Average Cost

Proof of Lemma 3.

Let . From , we get that for any ,

such that . Let . Let . We write

Vector is almost a stationary distribution in the sense that

| (40) |

Let . First, we have that

Next we bound . Using as the initial state distribution, we will show that as we run policy (equivalently, policy ), the state distribution converges to and this vector is close to . From (40), we have , where is such that . Let be a matrix that encodes policy , . Other entries of this matrix are zero. We have

where we used the fact that . Let which is the state-action distribution after running policy for one step. Let and notice that as , we also have that . Thus,

By repeating this argument for rounds, we obtain

and it is easy to see that

Thus, . Now, notice that is the state-action distribution after rounds of policy . By the mixing assumption, , so the choice of yields .

∎

Proof of Lemma 6.

We prove the lemma by showing that conditions of Theorem 4 are satisfied. The assumptions allow an easy bound on the subgradient estimate:

Also, we show that the subgradient estimate is unbiased:

It is also convenient to bound the norm of the gradient. If , then . Otherwise, . Calculating,

| (41) |

where is the sign function. Let denote the plus or minus sign (the exact sign does not matter here). We have that

Thus,

where we used . ∎

Proof of Theorem 9.

By Theorem 2, running Algorithm 1 for a given with produces a with

where , and the probability of error for any single is guaranteed to be at most . Hence, the union bound implies that the total probability of error of any is at most . Similarly, with our choice of , Lemma 7 guarantees that holds for all simultaneously with probability at least

With these two observations, we can bound the suboptimality of the objective. Recalling that is the minimizer of , and using as the minimizer of , we have

| (Lemma 7) | ||||

| (Lemma 8) | ||||

One final application of the union bound guarantees that the statement holds with probability . Hence, the Meta-algorithm minimizes the objective to within .

We next relate the suboptimality of the objective optimization to the suboptimality of the true loss . Since all quantities are non-negative, this implies that . Finally, we can put together the excess loss bound. To apply Lemma 3 and bound the distance between and , we first need to bound and . Using the bounded suboptimality of as an optimizer of , we have

and can conclude that

Completely analogous reasoning gives the same bound on .

Then, applying Lemma 3, we have

Plugging in produces

The theorem statement follows by recalling that .

Let us turn to the complexity. The total number of subgradient descent steps is bounded by

and the total number of samples needed to estimate the violation function is

∎

Appendix B Discounted Cost Excess Loss Analysis

This section presents the necessary technical tools and the proof of Theorem 10. We begin by showing that if some vector is close to a feasible point of the LP, then it almost equals the expected frequencies of visits of the policy (when the system runs under the policy with the initial distribution ), i.e.,

| (42) |

Lemma 13.

For any vector , let be the set of points where and and define the constants and . Further assume that for each , there exists an such that . Then, for the policy define by

| (43) |

the expected frequencies of visits under the policy is close to :

Proof.

First, we notice that,

| (44) |

Let with according to the assumption. For any , we have,

Let , we have

| (45) |

with the upper bound

| (46) |

Let be a matrix that encodes the policy , where As a concrete example with state space and action space , we have

By the definition of in (43), it is easy to check that .

With , the defined in (42) can be written as,

| (47) |

Now, we are ready to bound . By the definition of (i.e., ), we have,

where the last equality is due to . Therefore,

By (47), we have,

| (48) |

Next, we need the analog of Lemma 6 for the discounted case, which is again a direct application of Theorem 4.

Lemma 14.

Given some error tolerance and desired maximum probability of error , running the stochastic subgradient method (shown in Figure 1) on with , , and constant learning rate produces a such that, with probability at least ,

| (51) |

Proof.

We (once again) prove the lemma by showing that conditions of Theorem 4 are satisfied. First, the subgradient norms have the easy bound

Finally, we show that the subgradient estimate is unbiased:

∎

With this lemma in hand, the proof of Theorem 10] proceeds in much the same way as the proof of Theorem 2].

Proof of Theorem 10.

Recall that the convex surrogate for the discounted cost is

with the constraint set .

Now, obtain from the stochastic subgradient descent algorithm. By Lemma 14, the error bound must be less than

Then with high probability, we have for any ,

Since we can bound

rearranging Equation (B) yields

Using these bounds on and with Lemma 13 gives

Lemma 13, applied to , implies that

and so

First, we simplify

Plugging in this expression and , we have

Thus, setting such that

or, more compactly, , yields

where, as usual, the hides log factors. This statement holds with probability at least and for any .

∎

Appendix C Analysis of the Discounted Cost Meta-Algorithm

It is important to note that the optimum need never be smaller than , where is some bound on . Even though we cannot compute this quantity, we may still restrict the domain of to

where the bound on is taken from (35).

For convenience, we will overload the notation from the average cost analysis. Define

where , and . The meta-algorithm for discounted cost takes as inputs a bound on the violation function , discount factor , an error tolerance , and desired probability tolerance . The algorithm then carefully chooses a grid , computes the corresponding , then returns where

C.1 Estimating the Violation Functions

Given some , we can estimate the violation function in much the same way as the average cost case. For some and samples and , define

| (52) |

Since and , this estimate is clearly unbiased. Also, we earlier assumed the existence of constants

and so we can bound

Therefore, we have concentration of around . The analogous result to Lemma 7 (also using Hoeffding’s inequality) is the following.

Lemma 15.

Given and , for any , the violation function estimate has

with probability at least as long as we choose

C.2 Defining the Grid

As before, let be some desired error tolerance and be some upper bound on ; we can always take . As we shall see, the sequence can be taken to be identical to the average cost case as long an appropriate and are used. Recall that is chosen to approximately minimize , and so limiting to suffices in the discounted case as well.

Lemma 16.

Let be some desired error tolerance and be some upper bound on ; we can always take . Consider the sequence defined in Algorithm 2 by the base case , induction step , and terminal condition . The grid has the property that

| (53) |

Additionally, we have .

Proof.

Our first goal is to bound . We first note that , which is a function of only, is increasing since

We also note that is sublinear in , and indeed

The two observations imply that

and hence we may bound

which is exactly the same bound as in the average cost case. Therefore, the same analysis shows that

for all and that we may bound

leading to the conclusion that .

∎

Proof of Theorem 12.

Running the discounted SGD Algorithm (Figure 1 with subgradient ) for

with steps, where is set as in Theorem 10, produces a sequence such that

holds for all simultaneously with probability at least , which is easily argued by noting that the probability of error for any single is and applying the union bound.

Lemma 15, along with our choice of

guarantees that holds with probability at least , and hence the statement holds for all with probability at most .

We now turn to bounding the suboptimality of the objective. Recalling that is the minimizer of , and using as the minimizer of , we have

| (Lemma 15) | ||||

| (Theorem 10) | ||||

The statement holds with probability at least , where the first term is from estimating (Lemma 15) and the second term is from bounding the SGD error (Theorem 10). Hence, the Meta-algorithm minimizes the objective to within .

Next, we use Lemma 13 to bound the discrepancy between and . Therefore, we need to bound and . Since all quantities are non-negative, this implies that . Using the bounded suboptimality of as an optimizer of , we have

Next, we crudely bound and use to obtain

Then, applying Lemma 13, we have

All in all, this simplifies to

Using our assumption that , we obtain the theorem statement.

We now turn towards bounding the subgradient steps and number of samples. Since the are equal to the average cost case, we can still bound . Theorem 10 requires we use

and so the total number of gradient descent steps can be bounded by

with the same number of samples as in the average cost case. ∎

Appendix D Related Work

One of the approximate linear programming methods, proposed by Schweitzer and Seidmann [1985], was to project the primal LP into a subspace. These ideas have seen lots of recent work [de Farias and Van Roy, 2003a, de Farias and Van Roy, 2003b, Hauskrecht and Kveton, 2003, Guestrin et al., 2004, Petrik and Zilberstein, 2009, Desai et al., 2012]. As noted by Desai et al. [2012], the prior work on ALP either requires access to samples from a distribution that depends on optimal policy or assumes the ability to solve an LP with as many constraints as states.

The first theoretical analysis of ALP methods, by de Farias and Van Roy [2003a], analyzed the discounted primal LP (7) performance when only value functions of the form , for some feature matrix , are considered. Roughly, they show that the ALP solution has the family of error bound indexed by a vector

| (54) |

where is a “state-relevance” vector and is a “goodness-of-fit” parameter that measures how well represents a stationary distribution. Unfortunately, and are typically hard to choose (for example, a good choice of would be the stationary distribution under , which we do not know); but more importantly, the bound can be vacuous if does not model the optimal value function well and is always large. In particular, the problem we are considering in Definition 2 requires an additive bound with respect to the optimal parameter.

This result has some limitations. We need to specify , but a good choice is usually not known a priori. The authors show that, if the ALP is solved iteratively using the from the last iteration, then for an arbitrary probability distribution and accompanying , we must have

where is the discounted cost of the optimal policy. This suggests that we should choose , which is impossible as is not known a priori.

A second limitation is that the ALP remains computationally expensive if the number of constraints is large and was addressed in de Farias and Van Roy [2004] by reducing the number of constraints by sampling them. The idea is to sample a relatively small number of constraints and solve the resulting LP. Let be a known set that contains (solution of ALP). Let and define the distribution . Let and . Let and

Let be a set of random state-action pairs sampled under . Let be a solution of the following sampled LP:

de Farias and Van Roy [2004] prove that with probability at least , we have

Unfortunately, (which was used in the definition of ) depends on the optimal policy, which is obviously unknown, which makes this method difficult to implement.

In the primal form (4), an extra constraint is added to obtain

| (55) | ||||

Let be the average loss of the optimal policy and be the solution of this LP. It turns out that the greedy policy with respect to can be arbitrarily bad even if was small [de Farias and Van Roy, 2003b]. de Farias and Van Roy [2003b] propose a two stage procedure, where the above LP is the first stage and the second stage is

| (56) |

where is a user specified weight vector. Let be the solution of the second stage. Let and be the average loss and the stationary distribution of the greedy policy with respect to . de Farias and Van Roy [2003b] prove that

Further, it is shown that minimizes and that

which implies that is small. To get that is small, we need to use . Value of is obtained only after solving the optimization problem (D). To fix this problem, de Farias and Van Roy [2003b] propose to solve (D) iteratively, using from the solution of the last round.

The above approach has two problems. First, it is still not clear if the average loss of the resultant policy is close to (or the best policy in the policy class). Second, iteratively solving (D) is computationally expensive. Similar results are also obtained by Desai et al. [2012] who also show that if we were able to sample from the stationary distribution of the optimal policy, then LP (55) can be solved efficiently.

Desai et al. [2012] study a smoothed version of ALP, in which slack variables are introduced that allow for some violation of the constraints. Let be a violation budget. The smoothed ALP (SALP) has the form of

| s.t. |

The ALP on RHS is equivalent to LHS with a specific choice of . Let be a set of weight vectors. Desai et al. [2012] prove that if is a solution to above problem, then

The above bound improves (54) as is larger than and RHS in the above bound is smaller than RHS of (54). Further, they prove that if is a distribution and we choose , then

Similar methods are also proposed by Petrik and Zilberstein [2009]. One problem with this result is that is defined in terms of , which itself depends on . Also, the smoothed ALP formulation uses which is not known. Desai et al. [2012] also propose a computationally efficient algorithm. Let be a set of random states drawn under distribution . Let be a known set that contains the solution of SALP. The algorithm solves the following LP:

Let be the solution of this problem. Desai et al. [2012] prove high probability bounds on the approximation error . However, it is no longer clear if a performance bound on can be obtained from this approximation.

Next, we turn our attention to average cost ALP. Let be a distribution over states, , , , , and . de Farias and Van Roy [2006] propose the following optimization problem:

| (57) | ||||

Let be the solution of this problem. Define the mixing time of policy by

Let . Let be the optimal policy when discount factor is . Let be the greedy policy with respect to when discount factor is , and . de Farias and Van Roy [2006] prove that if ,

where , and . Similar results are obtained more recently by Veatch [2013].