Generative Adversarial Networks for Financial

Trading Strategies Fine-Tuning and Combination

Abstract

Systematic trading strategies are algorithmic procedures that allocate assets aiming to optimize a certain performance criterion. To obtain an edge in a highly competitive environment, the analyst needs to proper fine-tune its strategy, or discover how to combine weak signals in novel alpha creating manners. Both aspects, namely fine-tuning and combination, have been extensively researched using several methods, but emerging techniques such as Generative Adversarial Networks can have an impact into such aspects. Therefore, our work proposes the use of Conditional Generative Adversarial Networks (cGANs) for trading strategies calibration and aggregation. To this purpose, we provide a full methodology on: (i) the training and selection of a cGAN for time series data; (ii) how each sample is used for strategies calibration; and (iii) how all generated samples can be used for ensemble modelling. To provide evidence that our approach is well grounded, we have designed an experiment with multiple trading strategies, encompassing 579 assets. We compared cGAN with an ensemble scheme and model validation methods, both suited for time series. Our results suggest that cGANs are a suitable alternative for strategies calibration and combination, providing outperformance when the traditional techniques fail to generate any alpha.

Keywords: Conditional Generative Adversarial Networks, Trading Strategies, Ensemble, Model Tuning, Finance

1 Introduction

Systematic trading strategies are algorithmic procedures that allocate assets aiming to optimize a certain performance criterion. To obtain an edge in a highly competitive environment, the analyst needs to proper fine-tune its strategy, or discover how to combine weak signals in novel alpha creating manners. Both aspects, fine-tuning and combination, have been extensively researched in different domains, with distinct emphasis and assumptions:

-

•

Forecasting and Financial Econometrics: proper model fine-tuning is also known as preventing Backtesting Overfitting: partly due to the endemic abuse of backtested results, there is an increasing interest in devising procedures for the assessment and comparison of strategies [20, 33, 4]. Model/Forecasting combination is an established area of research [36], starting with the seminar work of [5] in the 60s, and still active [21].

-

•

Computational Statistics and Machine Learning: model tuning falls under the guise of Hyperparameter Optimization [13, 25] and Model Validation schemes [3, 24]; research on their interaction is scarce, and dealing with dependent data scenarios is still an open area of research [23, 6]. Forming ensembles is a modelling strategy widely adopted by this community, being Random Forest and Gradient Boosting Trees the two main workhorses of Bagging and Boosting strategies [17, 12].

In summary, proper model tuning and combination are still an active area of research, in particular to dependent data scenarios (e.g., time series). Emerging techniques such as Conditional Generative Adversarial Networks [29] can have an impact into aspects of trading strategies, specifically fine-tuning and to form ensembles. Also, we can list a few advantages of such method, like: (i) generating more diverse training and testing sets, compared to traditional resampling techniques; (ii) able to draw samples specifically about stressful events, ideal for model checking and stress testing; and (iii) providing a level of anonymization to the dataset, differently from other techniques that (re)shuffle/resample data.

The price paid is having to fit this generative model for a given time series. In this work we show how the training and selection of the generator is made; overall, this part tends to be less costly than the whole backtesting or ensemble modelling process. Therefore, our work proposes the use of Conditional Generative Adversarial Networks (cGANs) for trading strategies calibration and aggregation. We provide evidence that cGANs can be used as tools for model fine-tuning, as well as on setting up ensemble of strategies. Hence, we can summarize the main highlights of this work:

-

•

We have considered 579 assets, mainly equities, but we have also included swaps and equity indices, and currencies data.

-

•

Our findings suggest that cGAN can be an alternative to Bagging via Stationary Bootstrap, that is, when bootstrap approaches have failed to outperform, cGAN can be employed for Stochastic Gradient Boosting or Random Forest.

-

•

For model fine-tuning, we have evidence that cGAN is a viable procedure, comparable to many other well established techniques. Therefore, it should be considered part of the quantitative strategist toolkit of validation schemes for time series modelling.

-

•

A side outcome of our work is the wealth of results and comparisons: to the best of our knowledge most of the applied model validation strategies have not yet been cross compared using real datasets and different models.

Therefore, in addition to this introductory section, we structured this paper with other four sections. Next section provides background information about GANs and cGANs, how the training and selection of cGANs for time series was performed, as well as their application to fine-tuning and ensemble modelling of trading strategies. Third section outlines the experimental setting (scenario, parameters, etc.) used for two case studies: fine-tuning and combination of trading strategies. After this, section IV presents the results and discussion of both case studies, with section V exhibiting our concluding remarks and potential future works.

2 Generative Adversarial Networks

2.1 Background

Generative Adversarial Networks (GANs) [18] is a modelling strategy that employ two Neural Networks: a Generator () and a Discriminator (). The Generator is responsible to produce a rich, high dimensional vector attempting to replicate a given data generation process; the Discriminator acts to separate the input created by the Generator and of the real/observed data generation process. They are trained jointly, with benefiting from incapability to recognise true from generated data, whilst loss is minimized when it is able to classify correctly inputs coming from as fake and the dataset as true. Competition drive both Networks to improve their performance until the genuine data is indistinguishable from the generated one.

From a mathematical perspective, we start by defining a prior on input noise variables , which will be used by the Generator, denoted as a neural network with parameters , that maps noise to the data/input space . We also need to set the Discriminator, represented as a neural network , that scores how likely is that was sampled from the dataset ( – ). As outlined before, is trained to maximize correct labelling, whilst , in the original formulation, is trained to minimize . It follows from [18] that and play the following two-player minimax game with value function :

| (1) |

Overall, GANs have been successfully applied to image and text generation [9]. However, some issues linked to its training and applications to special cases [34, 19] have fostered a substantial amount of research in newer architectures, loss functions, training, etc. We can classify and summarise these new methods as of belonging to:

-

•

Ensemble Strategies: train multiple GANs, with different initial conditions, slices of data and tasks to attain; orchestrate the generator output by employing an aggregation operator (summing, weighted averaging, etc.), from multiple checkpoints or at the end of the training. Notorious instantiations of these steps are the Stacked GANs [22], Ensembles of GANs [39] and AdaGANs [37].

-

•

Loss Function Reshaping: reshape the original loss function (a lower-bound on the Jensen-Shannon divergence) so that issues linked to training instability can be circumvented. Typical examples are: employing Wasserstein-1 Distance with a Gradient Penalty [2, 19]; using a quantile regression loss function to implicitly push to learn the inverse of a cumulative density function [30]; rewriting the objective function with a mean squared error form – now minimizing the -distance [28]; or even view the discriminator as an energy function that assigned low energy values to the regions of high data density, guiding the generator to sample from those regions [41].

-

•

Adjusting Architecture and Training Process: we can mention Deep Convolutional GAN [32], in which a set of constraints on the architectural topology of Convolutional GANs are put in place to make the training more stable. Also, Evolutionary GANs [38] that adds to the training loop of a GAN different metrics to jointly optimize the generator, as well as employing a population of Generators, created by introducing novel mutation operators.

Another issue, more associated to our work, is the handling of time series since learning an unconditional model, similar to the original formulation, works for image and text creation/discovery. However, when the goal is to use it for time series modelling, a sampling process that can take into account the previous state space is required to preserve the time series statistical properties (autocorrelation structure, trends, seasonality, etc.). In this sense, next subsection deals with Conditional GANs [29], a more appropriate modelling strategy to handle dependent data generation.

2.2 Conditional GANs

As the name implies, Conditional GANs (cGANs) are an extension of a traditional GAN, when both and decision is based not only in noise or generated inputs, but include an additional information set . For example, can represent a class label, a certain categorical feature, or even a current/expected market condition; hence, cGAN attempts to learn an implicit conditional generative model. Such application is more appropriate in cases where the data follows a sequence (time series, text, etc.) or when the user wants to build ”what-if” scenarios (given that S&P 500 has fallen 1%, how much should I expect in basis points change of a US 10 year treasury?).

Most of the applications of cGANs related to our work have centred in synthesizing data to improve supervised learning models. The only exception is [42], where the authors use a cGAN to perform direction prediction in stock markets. Works [16, 11] deal with the problem of imbalanced classification, in particular to fraud detection; they are able to show that cGANs compare favourably to other traditional techniques for oversampling. In [15], the one that is closest to our work, the authors propose to use cGANs for medical time series generation and anonymization. They used cGANs to generate realistic synthetic medical data, so that this data could be shared and published without privacy concerns, or even used to augment or enrich similar datasets collected in different or smaller cohorts of patients.

Formally, we can define a cGAN by including the conditional variable in the original formulation. Therefore, now and , as before is trained to maximize correct labelling, whilst , in the original formulation, is trained to minimize . Similarly, it follows from [29] that and play the following two-player minimax game with value function :

| (2) |

in our case, given a time series , our conditional set is and what we are aiming to sample/discriminate is (with ). In this sense, sets the amount of past information that is considered in the implicit conditional generative model. If , then a traditional GAN will be trained; if is large, than the Neural Network have a larger memory, but it will need bigger capacity to model and deal with selecting the right past values and dealing with noise vector ; experimental setting section outline the values we have used during our experiments.

2.3 Training and Selecting Generators for Time Series

With the addition of the conditional vector , training cGANs is akin to GANs; what substantially change is how the right architecture is chosen across the training. Algorithm 1 detail a minibatch stochastic gradient descent Training and Selecting of cGANs.

represents a set of hyperparameters that the user has to define before running cGAN Training. It mainly encompasses: and architectures, number of lags , noise vector size and prior distribution, minibatch size , number of epochs, snapshot frequency (), number of samples , and parameters associated to the stochastic gradient optimizer; all of them are specified in the Experimental Setting section (see Table 2).

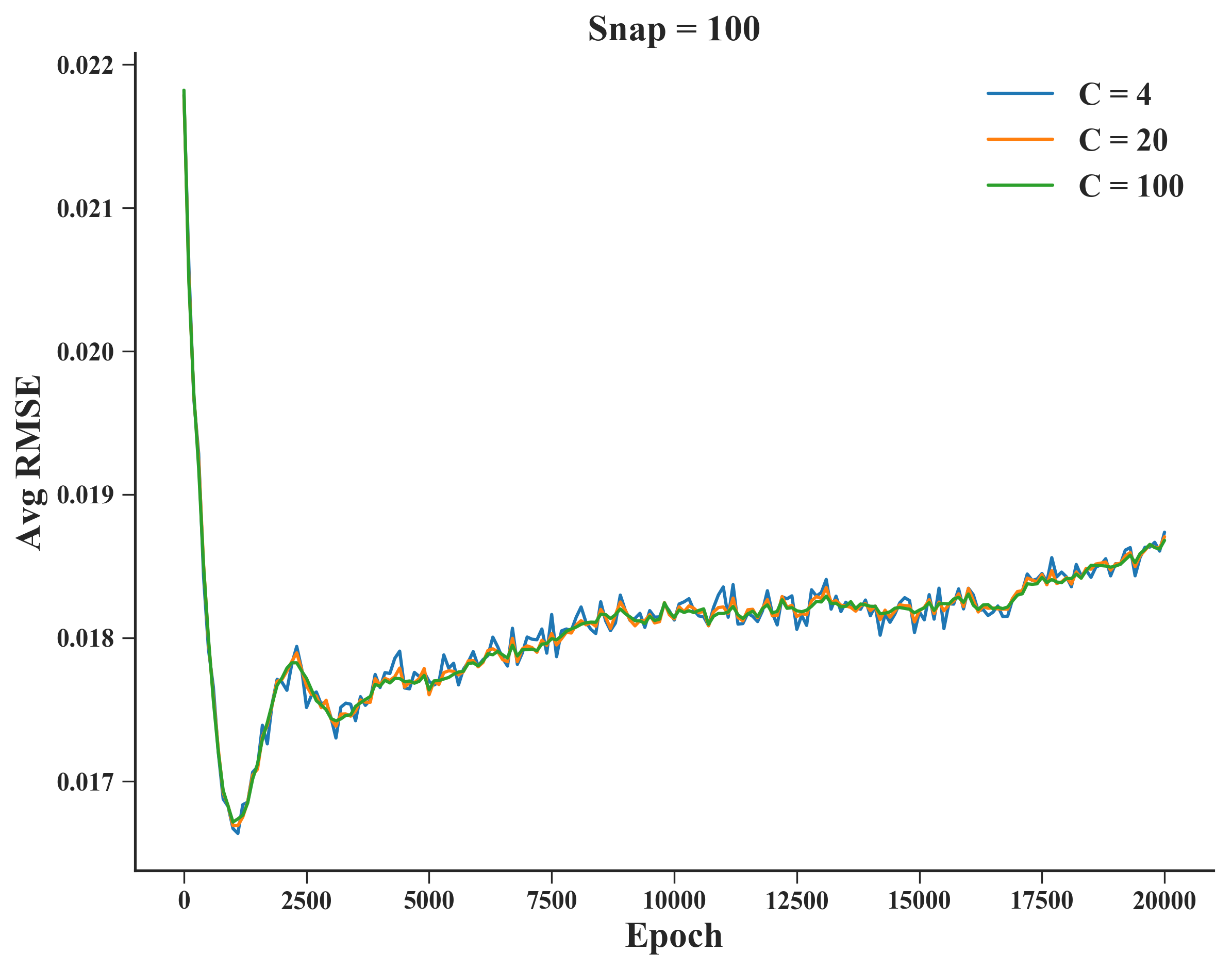

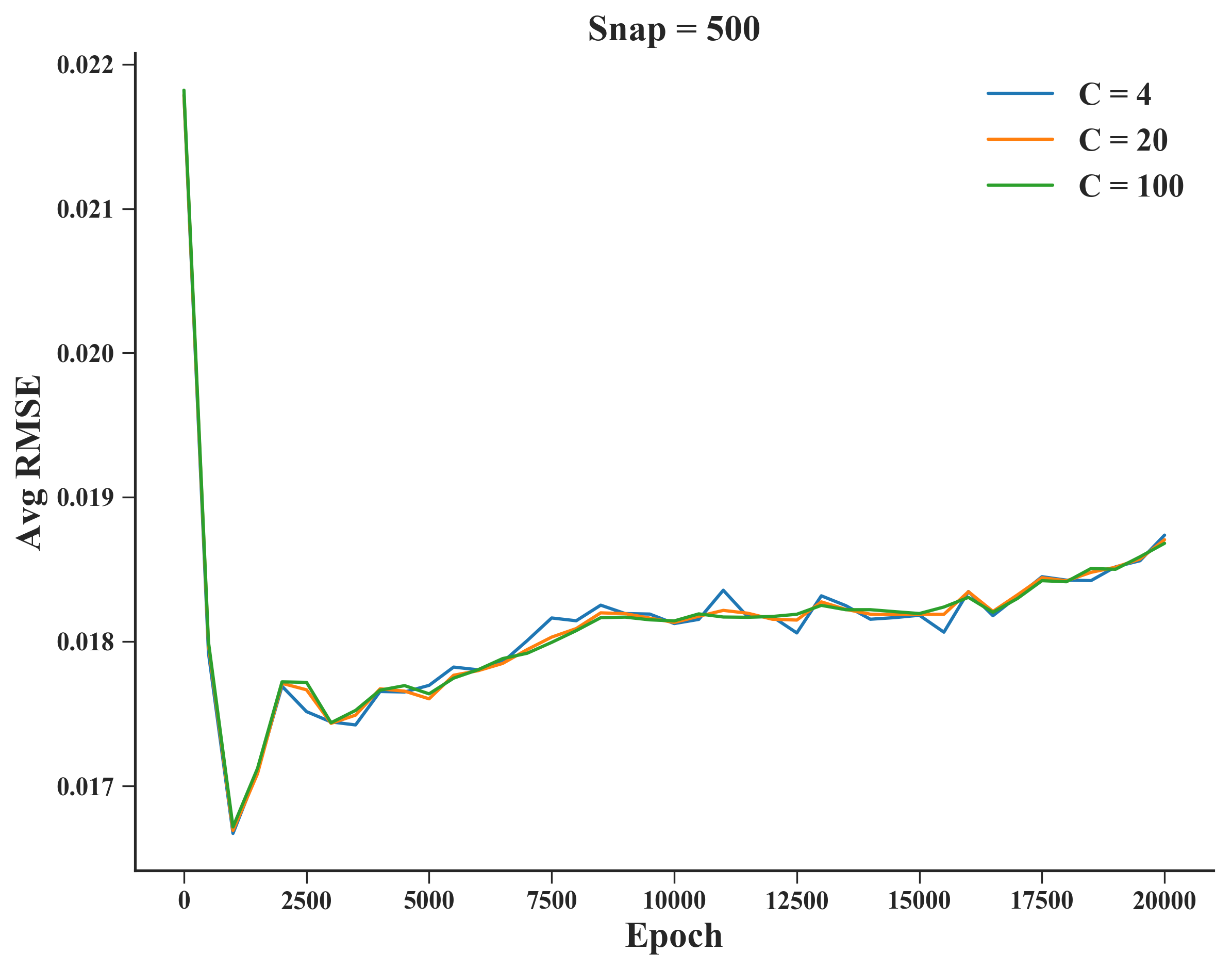

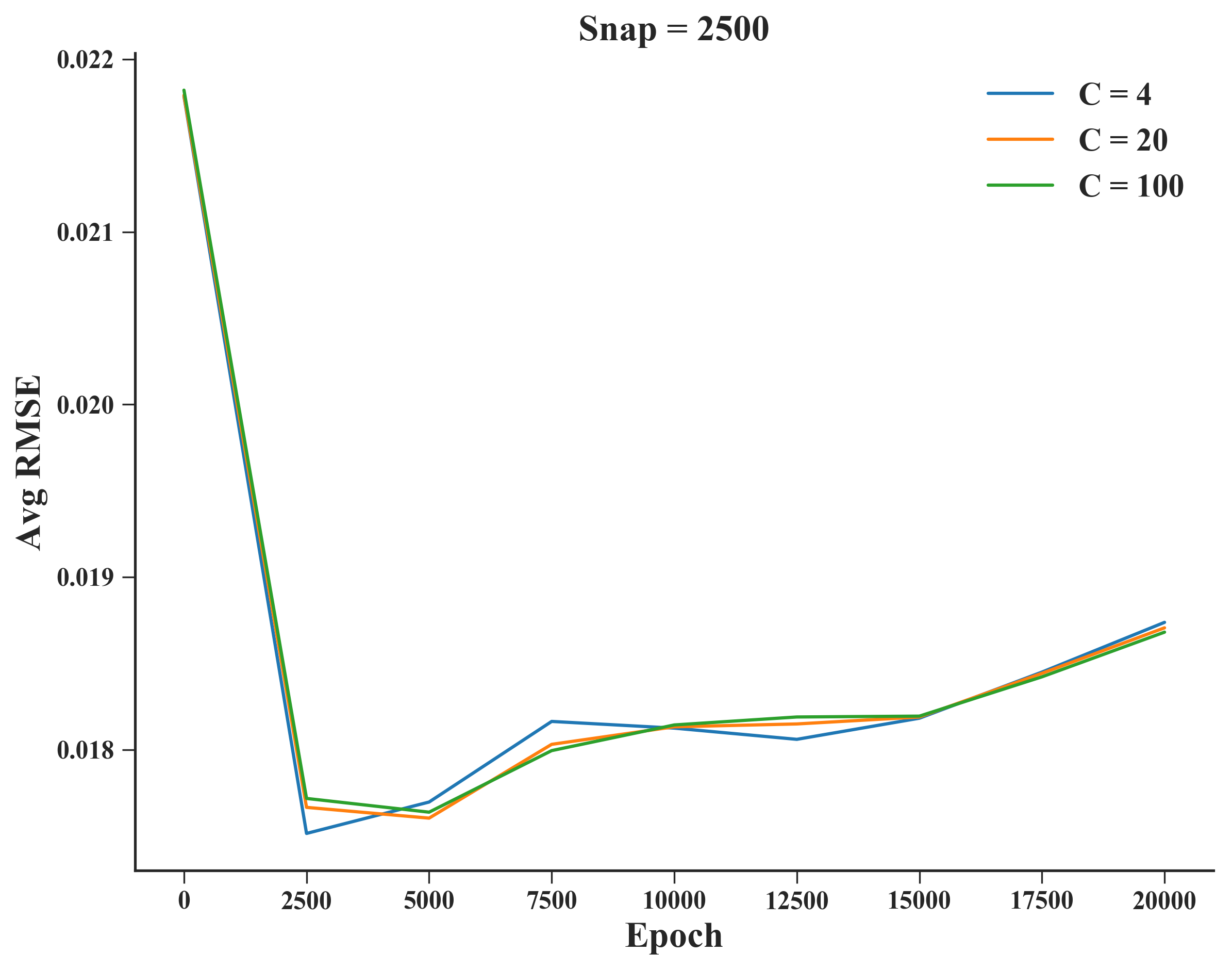

Selecting the right cGAN during the training is a difficult task, since it is computationally expensive to every iteration draw multiple samples and evaluate them. An approximation that we considered was to add a snapshot frequency in which every iterations and weights are store. This parameter plays a relevant role in regulating the available number of cGANs to draw samples, evaluate and select. To illustrate the selection part of Algorithm 1, Figure 1 presents a sensibility analysis of it to SPX Index.

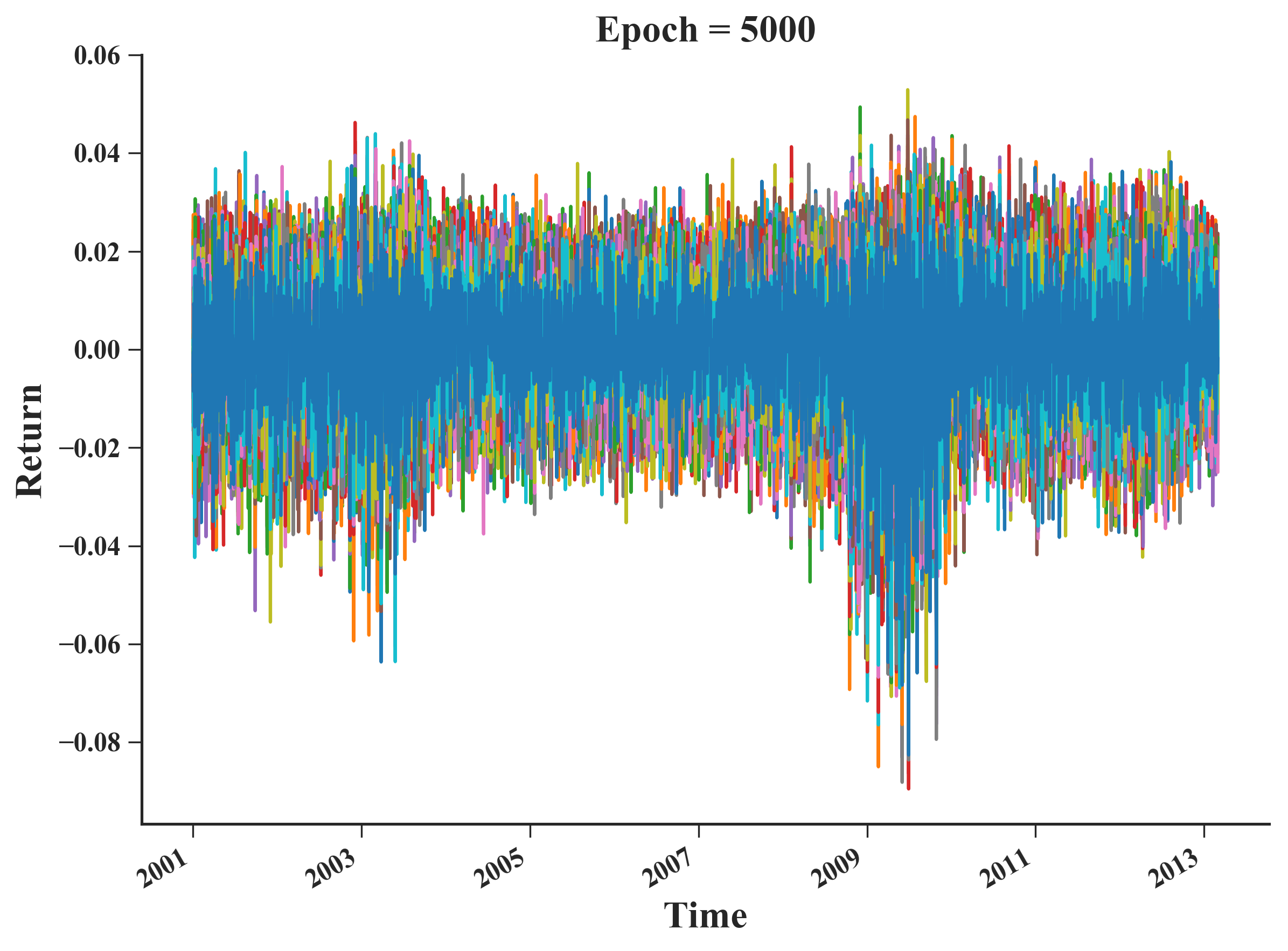

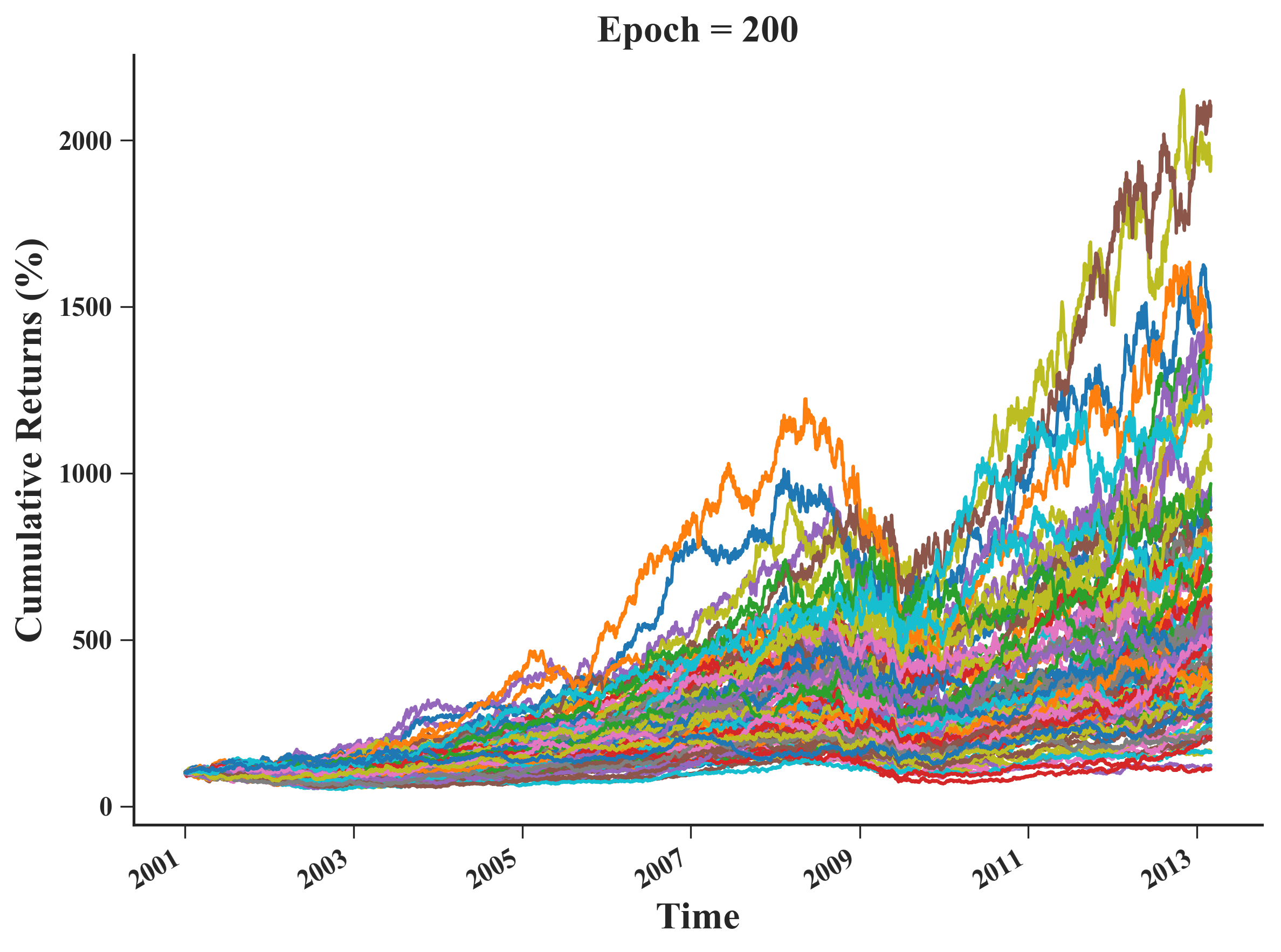

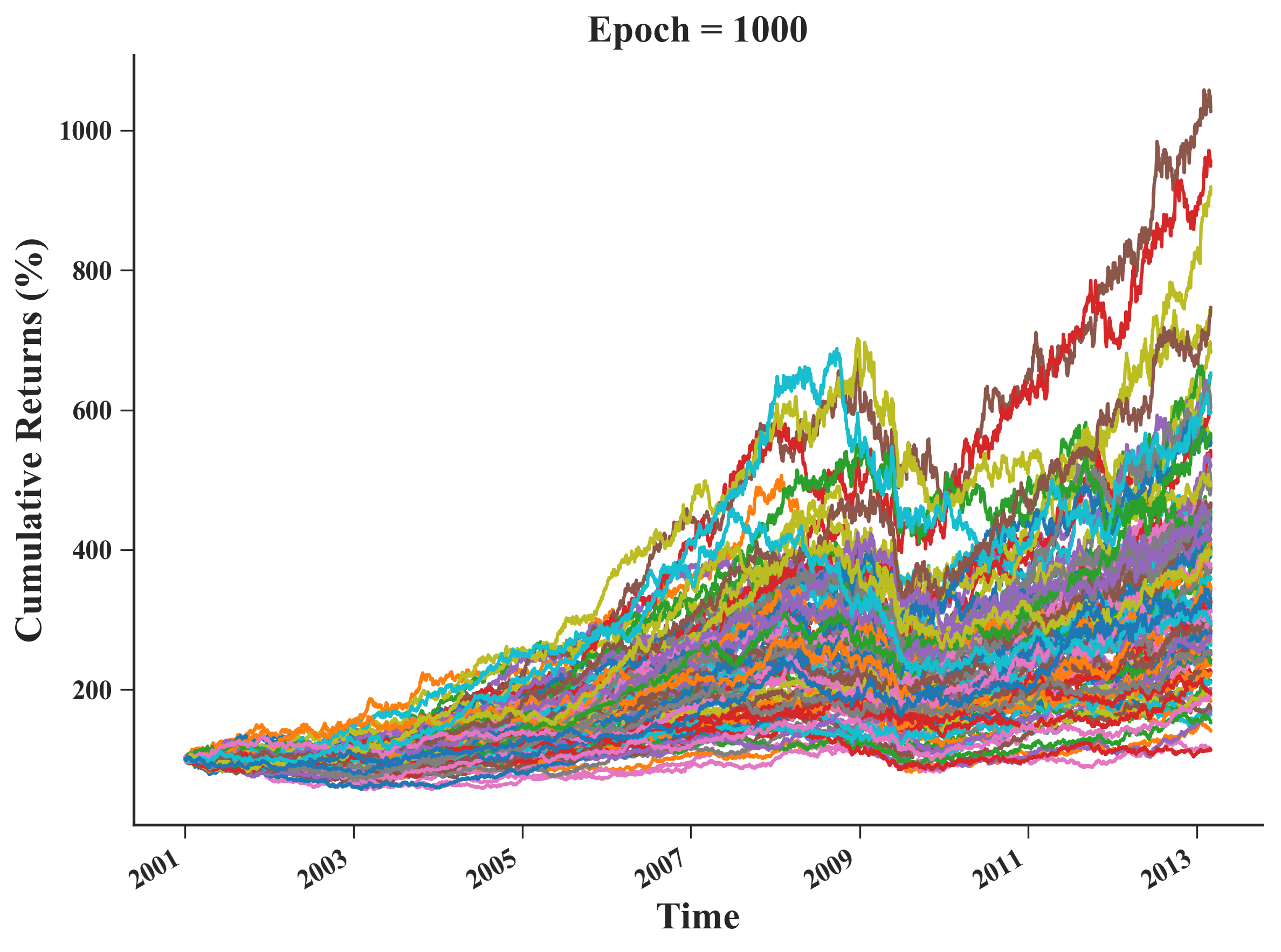

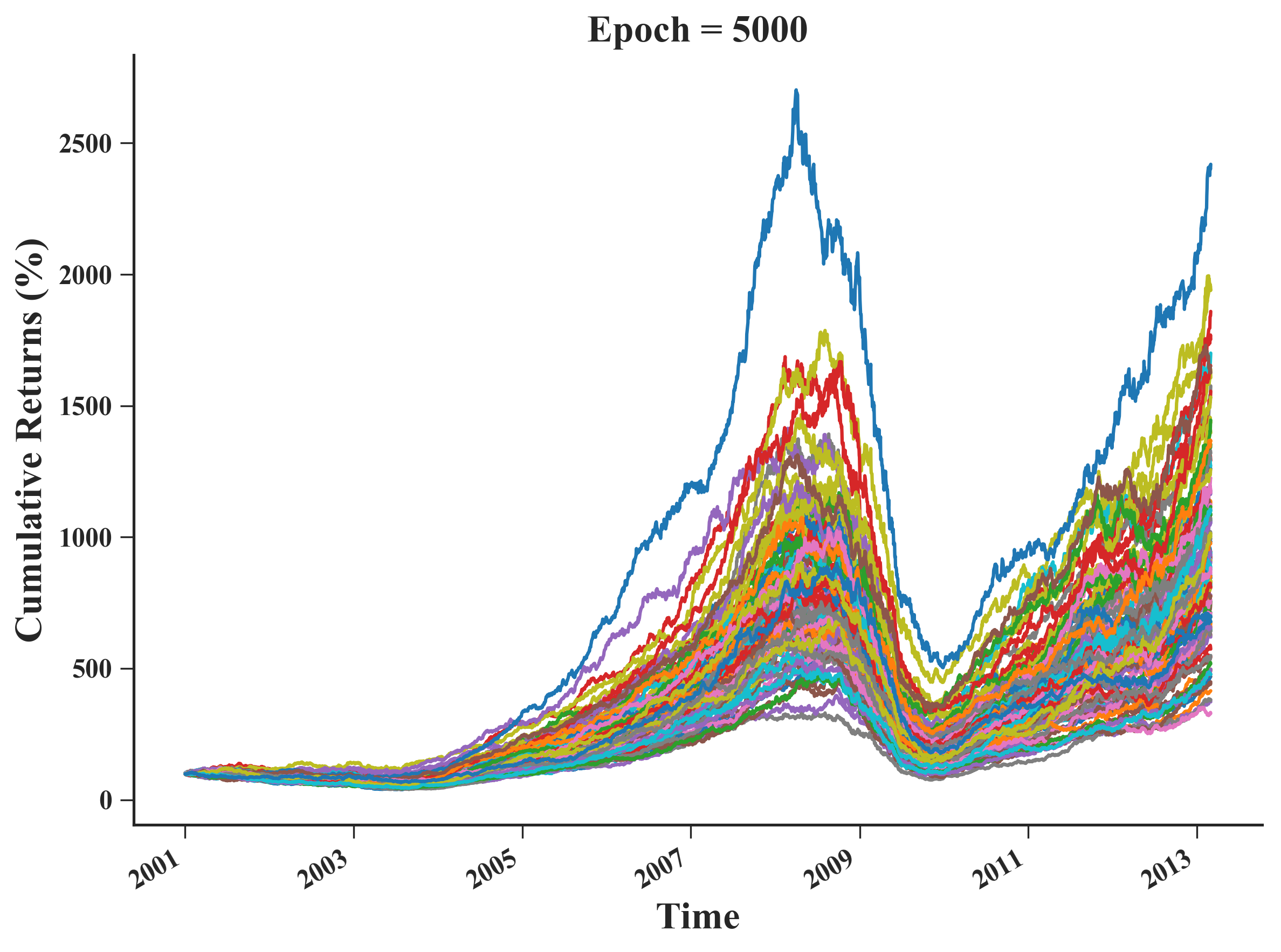

Overall, after a sharp decrease in the first 2000 epochs we observe a stabilization of RMSE to the 0.018 level. Drawing more samples improve estimation, but the gain is almost imperceptible from 20 to 100 samples. Snapshot frequency is an important parameter, with a noticeable difference between 100 to 2500, but without much change moving from 100 to 500. Number of samples draw from and the snapshot frequency are also reported in the Experimental Setting section. Figure 2 presents SPX Index samples (a-c) from cGAN and their respective cumulative returns (d-e)111We are highlighting this period in particular because our analyses and results concentrated on taking samples from 2001-2013. in different stages of training: 200, 1000 and 5000 epochs.

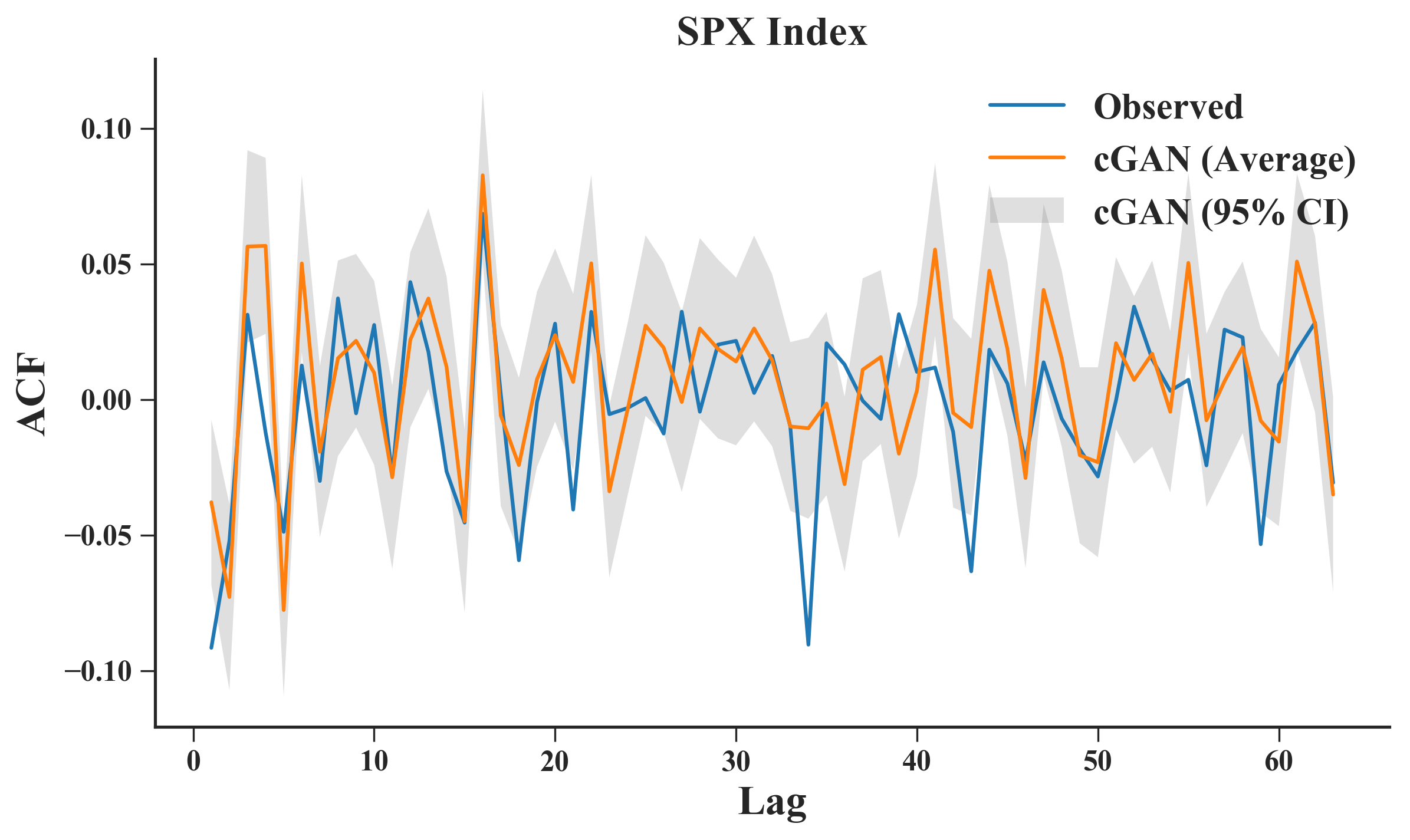

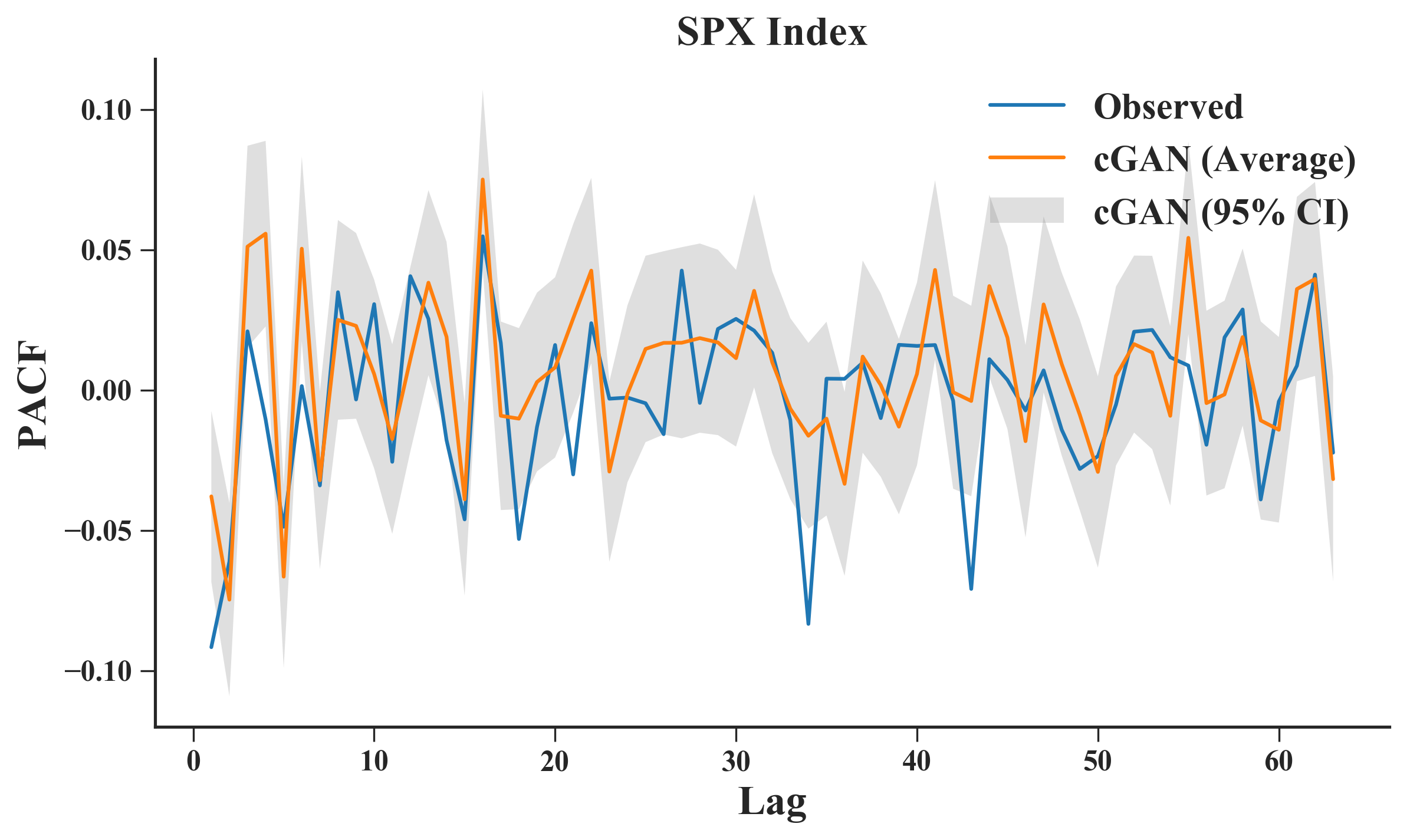

Clearly, with just a 200 epochs the samples generated do not resemble well the index, whilst with 1000 the results are closer. For SPX Index, not much improvement was observed after 1000-2000 epochs. Although the samples still appear similar to the index, some issues related to scaling and presence of overshoots in the prediction damaged the RMSE values. Figure 3 look into the estimated autocorrelations (ACF) and partial autocorrelations (PACF) functions using samples of cGAN with 1000 epochs. With few exceptions, most of the observed ACF and PACF values were in the neighbourhood of the average of several cGAN samples, with the confidence interval (CI) covering most of the 63 lags; this anecdotal evidence suggest that our cGAN Training and Selection Algorithm is able to replicate to a certain extent some statistical properties of a time series, in particular its ACF and PACF. The proper evidence toward this last assertion are provided in our case studies.

A final note: we have adopted the Root Mean Square Error as the loss function between the generator samples and the actual data, however nothing limits the user to use another type of loss function. In the next two subsections we outline new applications that can be made using the cGAN generator: fine-tuning and combination of trading strategies.

2.4 cGAN: Fine-Tuning of Trading Strategies

Fine-tuning of trading strategies consists of identifying a suitable set of hyperparameters such that a desired goal is attained. This goal depends on what is the utility function that the quantitative analyst is targeting: outperformance during active trading, hedging a specific risk, reaching a certain level of risk-adjusted returns, and so on. This problem can be decomposed into two tasks – model validation and hyperparameter optimization – that are strongly connected. Using [7] as the initial step, given a(n):

-

•

finite set of examples draw from a probability distribution

-

•

set of hyperparameters , such as number of neurons, activation function of layer , etc.

-

•

utility function to measure a trading strategy performance in face of new samples from

-

•

trading strategy with parameters identifiable by an optimization of a training criterion, but only spotted after a certain is fixed

mathematically, a trading strategy is fine-tuned properly if we are able to identify:

| (3) |

that is, the optimal configuration for that maximizes the generalization of utility . In reality, since drawing new examples from is hard, and could be extremely large, most of the work in hyperparameter optimization and model validation is done by a double approximation:

| (4) | |||

| (5) |

the first approximation (eq. 4) is discretizing the search space of (hopefully including ) due to finite amount of computation. There are better ways to do this search, such as using Evolution Strategies [25] or Bayesian Optimization [13], but this is not the focus of our work. The second approximation (eq. 4) replaces the expectation over sampling from , by an average over validation sets . Creating proper validation sets have been the focus of a substantial amount of research:

- •

-

•

when are not iid, then modifications have to be employed in order to create and adequately. In itself, it is an ongoing research topic, but we can mention the block-cross-validation and -block-cross-validation [31], sliding window [3], one-split (single holdout) [3], stationary bootstrap [24], as potential candidates.

in this work we follow a different thread: we attempt to build an approximation of drawing new examples from using a cGAN. Algorithm 2 outlines the steps followed to fine-tune a trading strategy using a cGAN generator.

Hence, we train a cGAN and use the generator to draw samples from the time series. For every sample, we perform an one-split to create and , so that we are able to identify parameters and assess a set of hyperparameters . Following eq. (5), we return the hyperparameter that maximize the average performance across the cGAN samples. The one-split method has one parameter which sets the holdout set size; its value is specified in the experimental setting section. We compared our methodology results with other schemes that produce and from a given dataset. Next subsection outline another use of the cGAN generator: ensemble modelling.

2.5 cGAN: Sampling and Aggregation

Another potential use of cGAN is to build an ensemble of trading strategies, that is, using base learners that are individually ”weak” (e.g. Classification and Regression Tree), but when aggregated can outcompete other ”strong” learners (e.g., Support Vector Machines). Notorious instantiations of this principle are Random Forest, Gradient Boosting Trees, etc., techniques that make use of Bagging, Boosting or Stacking [17, 12]. In our case, the closest parallel we can draw to cGAN Sampling and Aggregation is Bagging. Algorithm 3 shows this method. After have trained and selected a cGAN, we repeatedly draw a cGAN sample and train a base learner; having proceed this way for steps we return the whole set of base models as an ensemble.

An argument that is often used to show why this scheme work is the variance reduction lemma [17]: let be a set of base learners, each one trained using distinct samples draw repeatedly from the cGAN generator. Then, if we average their predictions and analyse its variance we have:

| (6) |

if we assume, for analytical purpose, that and for all , that is, equal variance and average correlation , this expression simplifies to:

| (7) |

hence, we are able to reduce a base learner variance by averaging many slightly correlated predictors. By Bias-Variance trade-off [17, 12], the ensemble Mean Squared Error tend to be minimized, particularly when low bias and high variance base learners are used, such as deep Decision Trees. Diversification in the pool of predictors is the key factor; commonly it is implemented by taking iid bootstrap samples from a dataset. When dealing with time series, iid bootstrap can corrupt its autocorrelation structure, and taking stationary bootstrap samples [24] is preferred. Bagging predictors using stationary bootstrap is, therefore, the appropriate benchmark to compare cGAN Sampling and Aggregation. The method that is able to produce and with low and as slightly correlated as possible, will tend to outperform out-of-sample. A final note: one potential risk is that cGAN is unable to replicate well . Therefore, thought the samples are more diverse they are also more ”biased”. This can make the base learners to miss patterns displayed in the real dataset, or even spot ones that did not existed in the first place.

3 Experimental Setting

3.1 Datasets and Holdout Set

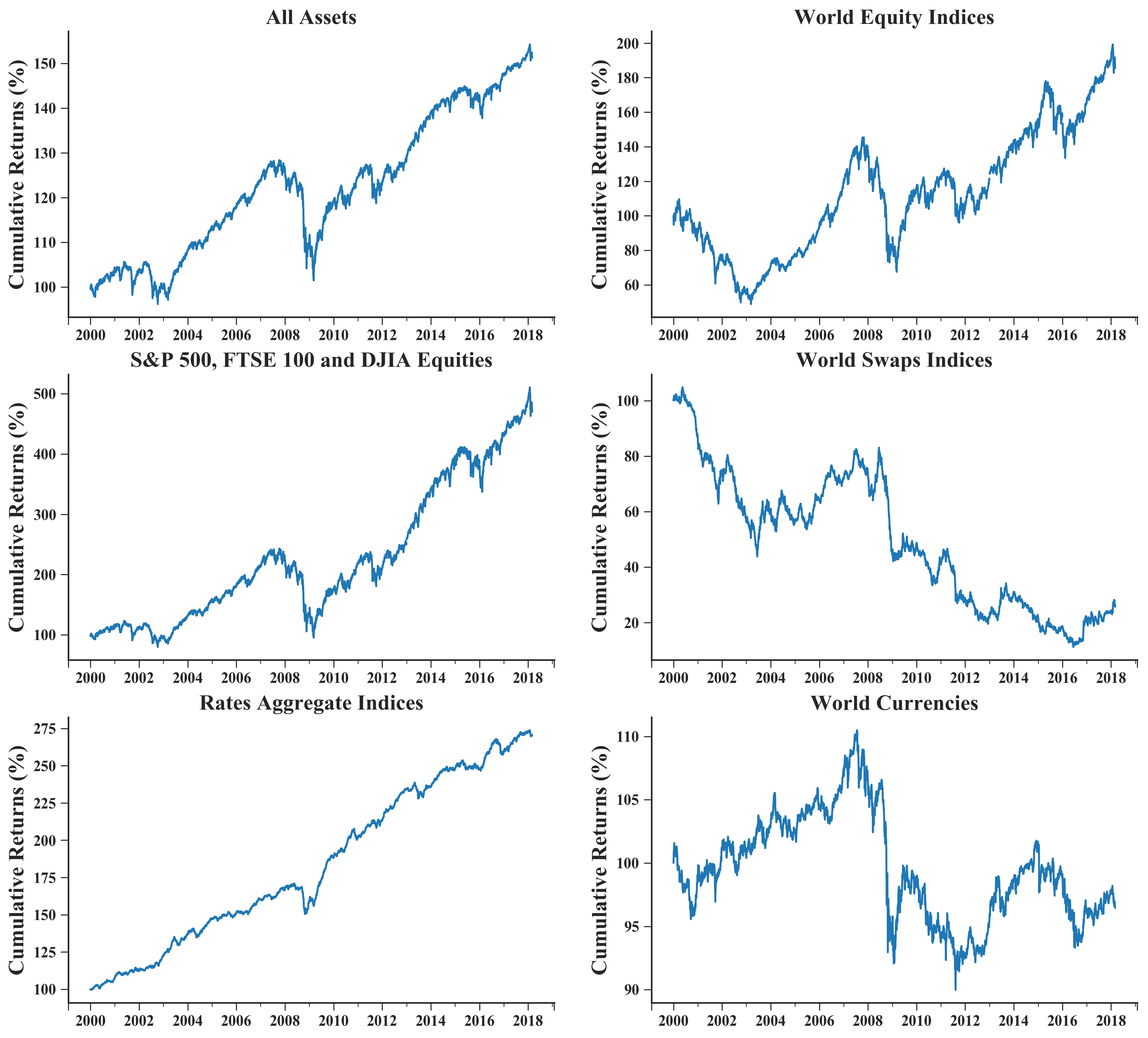

Table 1 presents aggregated statistics associated to the datasets used, whilst Figure 4 illustrates the cumulative returns per asset pool. We have considered three main asset classes during our evaluation: equities, currencies, and fixed income. The data was obtained from Bloomberg, with the full list of 579 assets tickers and period available at https://www.dropbox.com/s/08mjq7z49ybftqg/cgan_data_list.csv?dl=0. The typical time series started on 03/01/2000 and finished at 02/03/2018, with an average length of 4565 data points. We converted the raw prices in excess log returns, using a 3-month Libor rate as the benchmark rate.

| Asset Pool* | N | Avg Return | Volatility | Sharpe ratio | Calmar ratio | Monthly skewness | VaR 95% |

|---|---|---|---|---|---|---|---|

| All Assets | 579 | 0.0220 | 0.0453 | 0.4854 | 0.1051 | -1.2169 | -0.9443 |

| World Equity Indices | 18 | 0.0152 | 0.0717 | 0.2114 | 0.0504 | -0.8170 | -1.0048 |

| S&P 500, FTSE 100 and DJIA Equities | 491 | 0.0251 | 0.0525 | 0.4785 | 0.1127 | -1.1133 | -0.9517 |

| World Swaps Indices | 48 | -0.0191 | 0.0446 | -0.4295 | -0.0458 | 0.0275 | -0.9753 |

| Rates Aggregate Indices | 16 | 0.1220 | 0.0637 | 1.9135 | 0.5504 | -0.8227 | -0.9440 |

| World Currencies | 24 | -0.0025 | 0.0315 | -0.0798 | -0.0157 | -1.0052 | -0.8856 |

* Before being averaged, each individual asset was volatility scaled to 10%

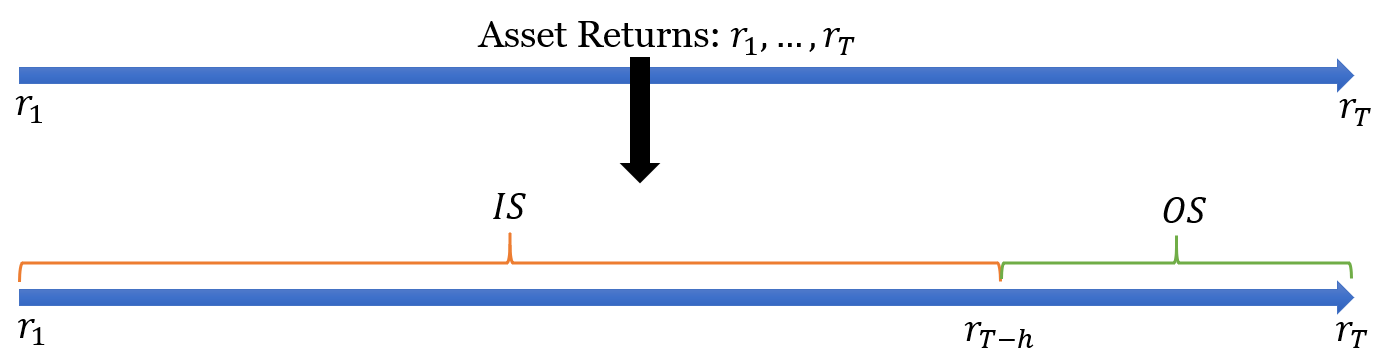

We have established a testing procedure to assess all the different approaches spanned in this research. Figure 5 summarize the whole procedure. The process start by splitting a sequence of returns in a single in-sample/training () and out-sample/testing/holdout () set, with both sets sizes being determined by the trading horizon . During our experiments we have fixed days years. Every method used or cGAN trained tap only into the data. Some methods, such as the other Model Validation schemes will create training and validation sequences, but all of them only based on set. However, the data used to measure their success is the same: by computing a set of metrics using the fixed set.

3.2 Performance Metrics

This subsection outline the utility function employed. We opted for a financial performance metric, instead of a generic metric based in prediction error. Low prediction error is a necessary, but not a sufficient condition to construct alpha-generating trading strategies [1]. In this sense, we mainly reported Sharpe and Calmar ratios: metrics that combine risk and reward measures, and make different investment strategies comparable [40, 35, 14]. These metrics can be defined as:

| (8) |

where is the strategy average annualized excess returns, is it volatility, and is the strategy maximum drawdown. All of them are calculated using the strategy instantaneous returns as the building block. In this case, is our trading signal, a transformation of the estimated returns outputted by a predictive model. We opted to use an identity function for so we can avoid having another layer of hyperparameters; in practice an user can select another transformation.

Finally, it should be mentioned that most of our reported results are aggregated across all 579 assets. Although the ratios provide a common basis to compare strategies with different risk profiles, still, the asset pool is quite diverse and is affected by outliers. Hence, we opted for robust statistics (median, mean absolute deviation, quantiles, ranks, etc.) to compare and statistically test the different hypothesis222The readers interested to understand more about the nonparametric statistical tests used in this work – Friedman, Holm Correction and Wilcoxon rank-sum test – should consult this reference [10]..

3.3 cGAN Configuration

Table 2 outlines the three different architectures used for and of a cGAN. Since the main variation is the number of neurons used, we abbreviated their names across the cases as cGAN-Small, cGAN-Medium and cGAN-Large. This variation will allow us to check how different architecture sizes perform across the benchmarks.

| Abbreviation | Individual Configuration |

| cGAN-Small (, ) | number of neurons = (5, 5) |

| cGAN-Medium (, ) | number of neurons = (100, 100) |

| cGAN-Large (, ) | number of neurons = (500, 500) |

| Other Configuration | Values |

| Architecture | Multilayer Perceptron |

| Number of hidden layers | 1 |

| Hidden layer activation function | rectified linear |

| Output layer activation function | linear |

| Output layer activation function | sigmoid |

| Epochs | 20000 |

| Batch Size | 252 |

| Solver | Stochastic Gradient Descent |

| Solver Parameters | learning rate = 0.01 |

| Conditional info | () |

| Noise prior | |

| Noise dimension | 252 |

| Snapshot frequency () | 200 |

| Number of samples for evaluation | 50 |

| Input features scaling function | -score (standardization) |

| Target scaling function | -score (standardization) |

After a few initial runs, we opted for Stochastic Gradient Descent with learning rate of 0.01 and batch size of 252 as the optimization algorithm. Input features and target were scaled using a z-score function to ease the training process. We selected the right cGAN to use by taking snapshots every 200 iterations (), drawing and evaluating 50 samples per generator along 20000 epochs. Finally, we used 252 consecutive lags as conditional information (around one year) with the noise prior (Standard Normal - ) wielding the same dimension of the conditional input; we did it to increase the chance to create a more diverse pool of examples, as well as to make it harder for the generator to omit/nullify the weights associated with this part of the input layer.

3.4 Case I: Combination of Trading Strategies

3.4.1 Overview

This case evaluates the success of different combination of trading strategies. In this sense, Algorithm 4 presents the main loop used for cGANs and Stationary Bootstrap. First step is to resample the actual returns using Stationary Bootstrap or cGAN, creating a new sequence of returns set. We then proceed as usual: use to train a base learner , and add it to the ensemble set All of these steps are repeated times. Finally, we can propagate the feature set through the ensemble , get the aggregated prediction, and compute its performance within this holdout set.

3.4.2 Methods and Parameters

Table 3 presents the instantiations of , , and of Algorithm 4. The main competing method is the Stationary Bootstrap; for all schemes, we have taken different number of resamples , so that we could compare the efficiency for different sizes of the ensemble. We used two main base learners: a deep Regression Tree and a large Multilayer Perceptron. The main idea was to follow the usual principle of using low bias and high variance base learners. We employed a fixed feature set of 252 consecutive lags, and averaged the prediction of all members. Therefore, we can describe the main hypothesis as: which resampling scheme is able to create a set of trading strategies that in aggregate manage to outcompete during the period?

| Resampling Scheme () | Parameters |

| Stationary Bootstrap [24] | samples and block size = 20 |

| cGAN-Small | samples |

| cGAN-Medium | samples |

| cGAN-Large | samples |

| Trading Strategy () | Hyperparameters () |

| Regression Tree (Reg Tree) [12] | unlimited depth, with minimum number of samples required to split an internal node of 2 |

| Multilayer Perceptron (MLP) [12] | number of neurons = , weight decay = and activation function = |

| Other details | Values |

| Number of lags used as features | |

| Aggregation function () | Mean |

3.5 Case II: Fine-tuning of Trading Strategies

3.5.1 Overview

This case evaluates the success of different fine-tuning strategies, in particular those that create and sets for time series. In this sense, Algorithm 5 presents an unified loop used regardless of the methodology employed: from data splitting, hyperparameter selection, and performance calculation.

It start by splitting the set in and using a Model Validation methodology – one-split, stationary bootstrap, cGAN, etc. Then, for every hyperparameter , we fit a trading strategy (e.g., Multi-layer Perceptron - ) that aims to predict using lagged information as the feature set. We check the strategy performance using a validation set and an utility function (e.g., Sharpe ratio). This process is repeated for all training and validation sets (). Then, we measure the worthiness of a hyperparameter (e.g., (number of neurons, weight decay) = (20, 0.05)) by averaging its performance across the validation folds ; the optimal configuration is the one that maximizes the expected utility. Using this hyperparameter, a final model is fitted and tested using set.

3.5.2 Methods and Parameters

| Model Validation () | Parameters |

| Naive () | - |

| Sliding window [3] | stride and window sizes days |

| Block cross-validation [31] | block size days |

| hv-Block cross-validation [31] | block size = 252 days and gap size = 10 days |

| One-split/Holdout/Single split [3] | = last 1260 days |

| k-fold cross-validation [6] | = 10 folds |

| Stationary Bootstrap [24] | = 100 samples and block size = 20 |

| cGAN-Small | 100 samples |

| cGAN-Medium | 100 samples |

| cGAN-Large | 100 samples |

| Trading Strategy () | Hyperparameters () |

| Gradient Boosting Trees (GBT) [12] | number of trees = , learning rate = , and maximum depth = |

| Multilayer Perceptron (MLP) [12] | neurons = , weight decay = , and activation function = |

| Ridge Regression (Ridge) [12] | shrinkage = , , , , |

| Other details | Values |

| Number of lags used as features | |

| Hyperparameter search | Grid-search or Exhaustive search |

| Utility function | Sharpe ratio |

Apart from the three different architectures of cGANs, the competing methods to cGAN for fine-tuning trading strategies are: naive (training and validation sets are equal), one-split and sliding window; block, hv-block and k-fold cross-validation; stationary bootstrap. Hence, the main hypothesis is: given a trading strategy , which mechanism is able to uncover the best configuration to apply during the period? We search for an answer to this hypothesis using linear and nonlinear trading strategies (Ridge Regression, Gradient Boosting Trees and Multilayer Perceptron). We used the Sharpe ratio as the utility function, grid-search as the hyperparameter search method, and a fixed feature set consisting of 252 consecutive lags.

4 Case Studies

4.1 Case I: Combination of Trading Strategies

Table 5 presents the median and mean absolute deviation (MAD - in brackets) results of ensemble strategies in the set. Starting with Regression Tree (Reg Tree), we observe that the median Sharpe and Calmar ratios of cGAN-Large was higher across distinct number of base learners (). In fact, it was already twice as much of Stationary Bootstrap (Stat Boot), even when the number of samples was smaller (); after this point some gain can still be obtained, but it seems that most of the diversification effect had already been realised. A different picture can be draw for Multilayer Perceptron (MLP): in this case Stat Boot produced better median Sharpe and Calmar ratios across the assets, with some exceptions when .

Looking into cGAN results, often the configuration cGAN-Large performed better, whilst in the other side of the spectrum cGAN-Small underperforming. Overall, our results suggest that using a high capacity MLP as the Generator/Discriminator helps to produce a Resampling Strategy that favours the training of base learners. We also reported the Root Mean Square Error (RMSE) since it is usual to report it for Ensemble Strategy. Numerically, they were very similar, nevertheless cGAN-Medium obtained the best values across and trading strategies.

| Trad Strat | Metric | Ensemble Strategy | ||||

| Stat Boot | cGAN-Small | cGAN-Medium | cGAN-Large | |||

| Reg Tree | Sharpe | 20 | 0.042560 (0.380039) | 0.053867 (0.378896) | 0.044741 (0.380228) | 0.080540 (0.360695) |

| 100 | 0.062837 (0.378920) | 0.058820 (0.387749) | 0.030588 (0.390575) | 0.086423 (0.406171) | ||

| 500 | 0.074116 (0.397212) | 0.067905 (0.392788) | 0.072071 (0.392382) | 0.098094 (0.424621) | ||

| Calmar | 20 | 0.019442 (0.230641) | 0.022619 (0.201044) | 0.018987 (0.200625) | 0.035473 (0.191353) | |

| 100 | 0.027235 (0.241023) | 0.024254 (0.209783) | 0.011890 (0.201523) | 0.036523 (0.239046) | ||

| 500 | 0.034422 (0.266419) | 0.031174 (0.212710) | 0.032761 (0.221514) | 0.042232 (0.251194) | ||

| RMSE | 20 | 0.014397 (0.005570) | 0.014561 (0.005604) | 0.014289 (0.005414) | 0.014411 (0.005432) | |

| 100 | 0.014096 (0.005486) | 0.014281 (0.005545) | 0.013988 (0.005357) | 0.014099 (0.005373) | ||

| 500 | 0.014035 (0.005470) | 0.014203 (0.005531) | 0.013912 (0.005346) | 0.014033 (0.005361) | ||

| MLP | Sharpe | 20 | 0.080722 (0.390515) | 0.079428 (0.416847) | 0.087960 (0.393913) | 0.069866 (0.398197) |

| 100 | 0.097576 (0.382028) | 0.063012 (0.415537) | 0.091344 (0.397506) | 0.087216 (0.414697) | ||

| 500 | 0.092262 (0.390161) | 0.059344 (0.415700) | 0.073652 (0.389588) | 0.085333 (0.414096) | ||

| Calmar | 20 | 0.035525 (0.223141) | 0.030805 (0.217727) | 0.037877 (0.219139) | 0.031145 (0.214533) | |

| 100 | 0.045916 (0.227827) | 0.023479 (0.223602) | 0.040718 (0.217648) | 0.040572 (0.223359) | ||

| 500 | 0.038678 (0.237459) | 0.024014 (0.225413) | 0.035688 (0.215691) | 0.035885 (0.222552) | ||

| RMSE | 20 | 0.014030 (0.005416) | 0.013999 (0.005408) | 0.013910 (0.005345) | 0.014055 (0.005369) | |

| 100 | 0.013924 (0.005399) | 0.013973 (0.005403) | 0.013878 (0.005339) | 0.014028 (0.005363) | ||

| 500 | 0.013924 (0.005400) | 0.013974 (0.005402) | 0.013887 (0.005337) | 0.014033 (0.005362) | ||

Except for RMSE, MAD values were high for Sharpe and Calmar ratios across the different combinations. Hence in aggregate, any numerical difference can become imperceptible from statistical lens. Table 6 shows if some of the differences raised about the values in Table 5, only between cGAN-Large and Stat Boot, are statistically significant or not. Overall, apart from RMSE, p-values of Wilcoxon rank-sum test were in general above 0.05 (significance level adopted), meaning that the differences observed were not substantial across models, number of samples, and Sharpe or Calmar ratios.

| Trad Strat | Metric | |||

|---|---|---|---|---|

| 20 | 100 | 500 | ||

| Reg Tree | Sharpe | 0.2440 | 0.3432 | 0.7832 |

| Calmar | 0.8495 | 0.2958 | 0.9106 | |

| RMSE | 0.0456 | 0.0001 | 0.0001 | |

| MLP | Sharpe | 0.7941 | 0.3994 | 0.4295 |

| Calmar | 0.8119 | 0.4805 | 0.4053 | |

| RMSE | 0.7973 | 0.0043 | 0.0007 | |

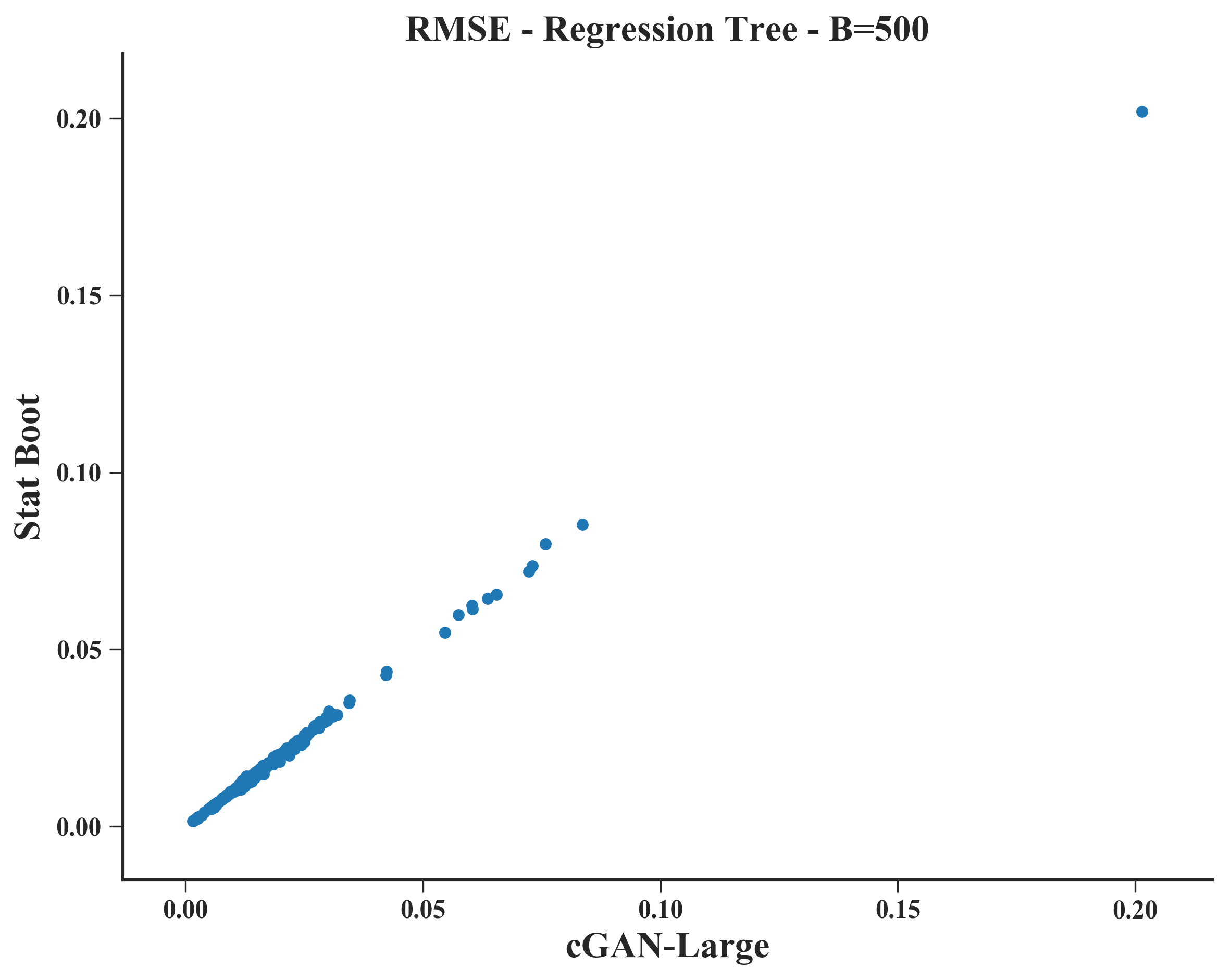

In principle, so far it seems that there is little difference between cGAN-Large and Stat Boot, across models, metrics and number of samples. However, this equivalence in aggregate often do not manifest itself at the micro level. Figure 6 presents this analysis: plotting the Sharpe ratio and RMSE obtained for every asset using cGAN-Large and Stat Boot (). For RMSE there is an almost perfect correlation – when cGAN-Large thrives, Stationary Bootstrap also do, with the converse also holding. However, a different phenomena occurs for Sharpe ratio: apart from a few outliers that skewed the correlation (0.407733), when Stat Boot fails to deliver reasonable results, cGAN-Large can provide a feasible alternative for combining weak signals. This complementarity, not perceived when looked in aggregate, can be an asset for the quantitative analyst in its pursuit to build alpha generating strategies.

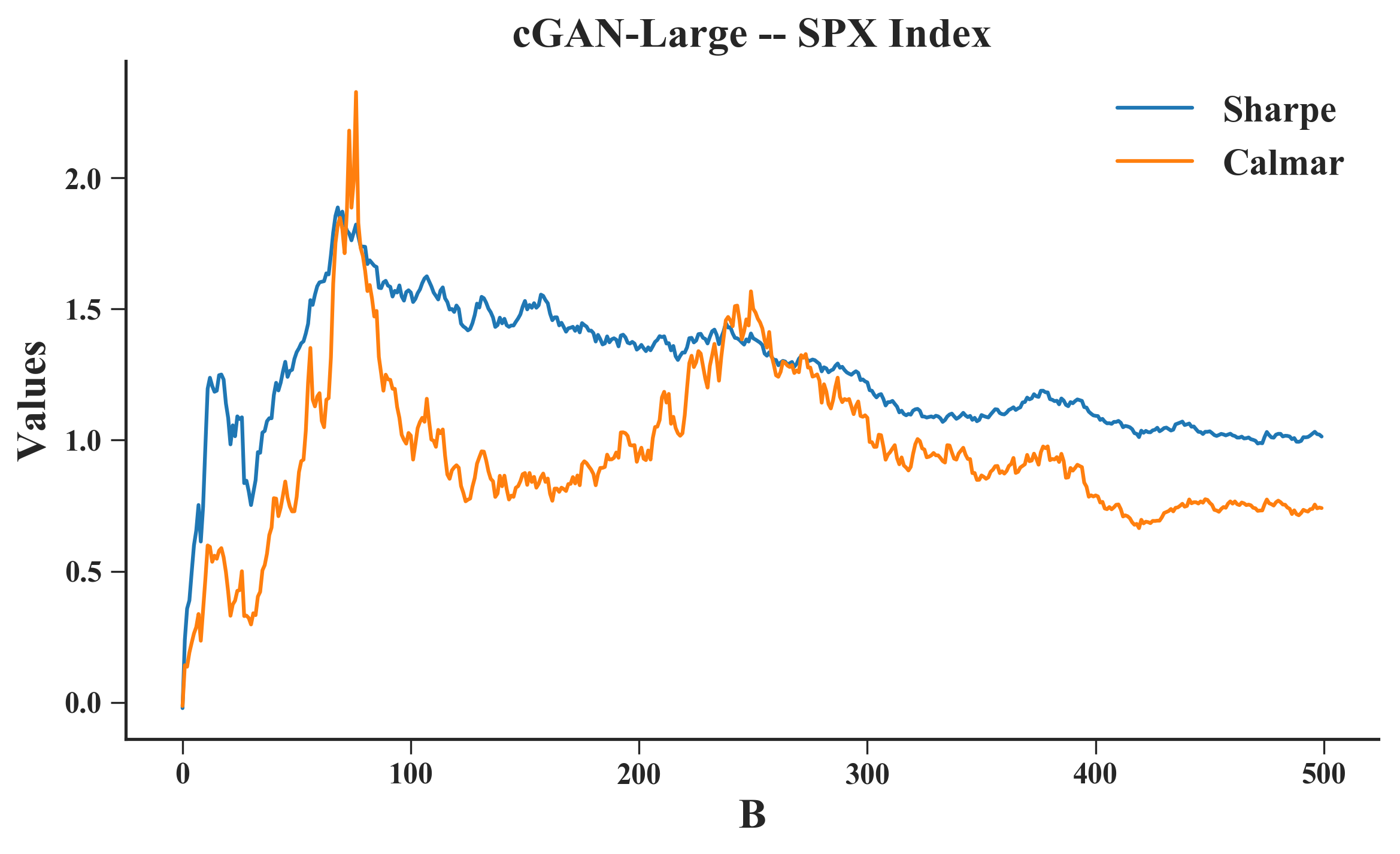

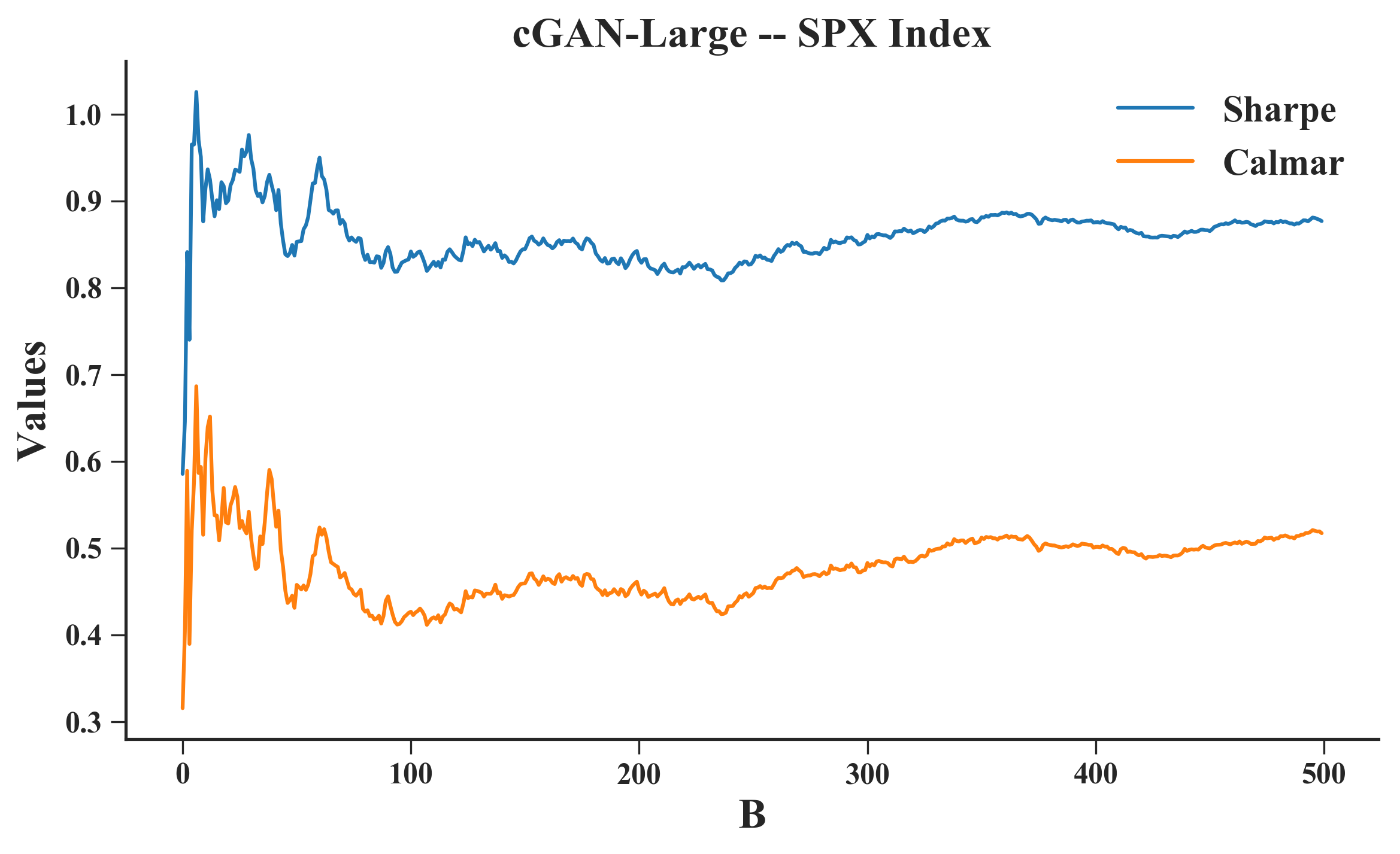

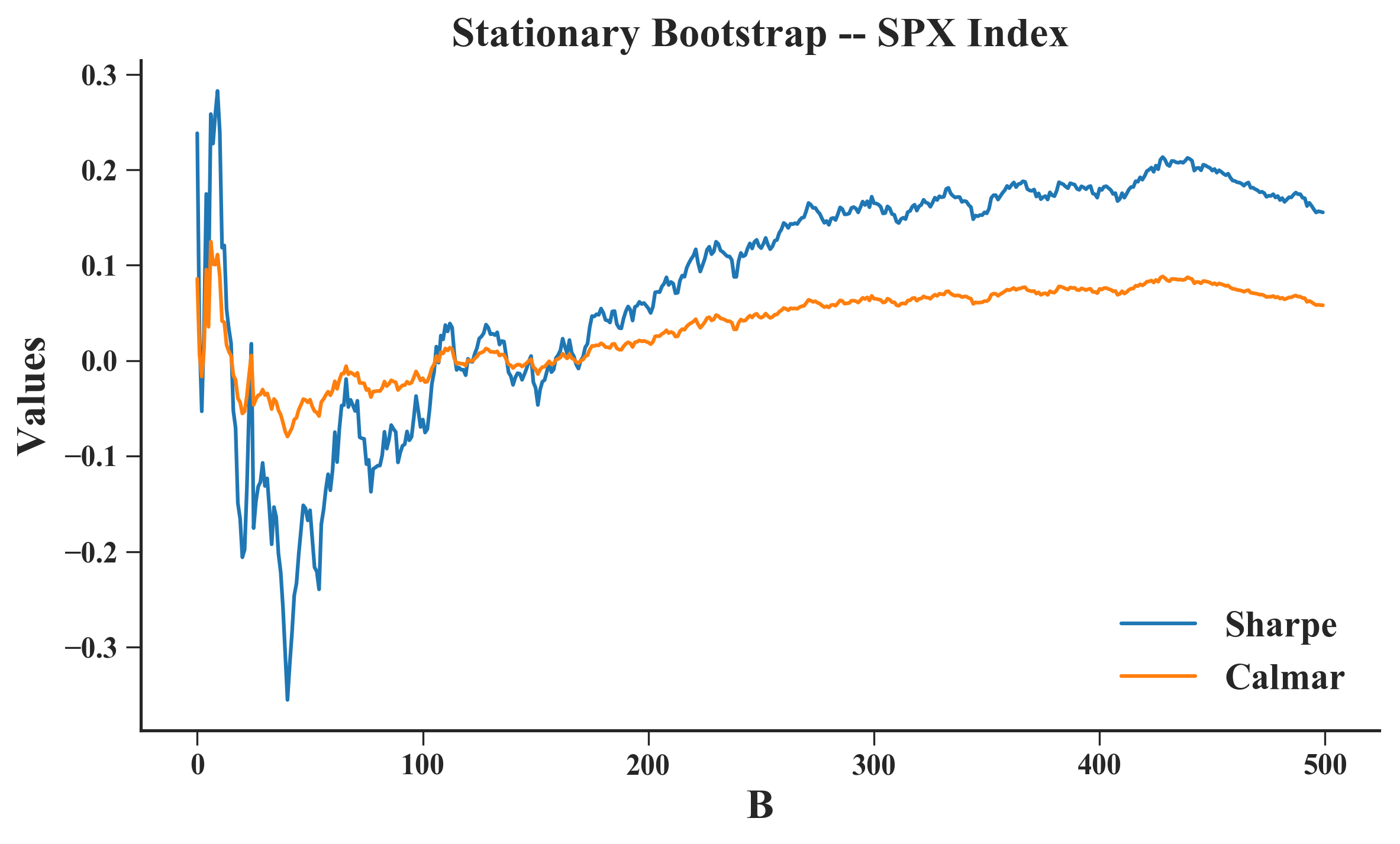

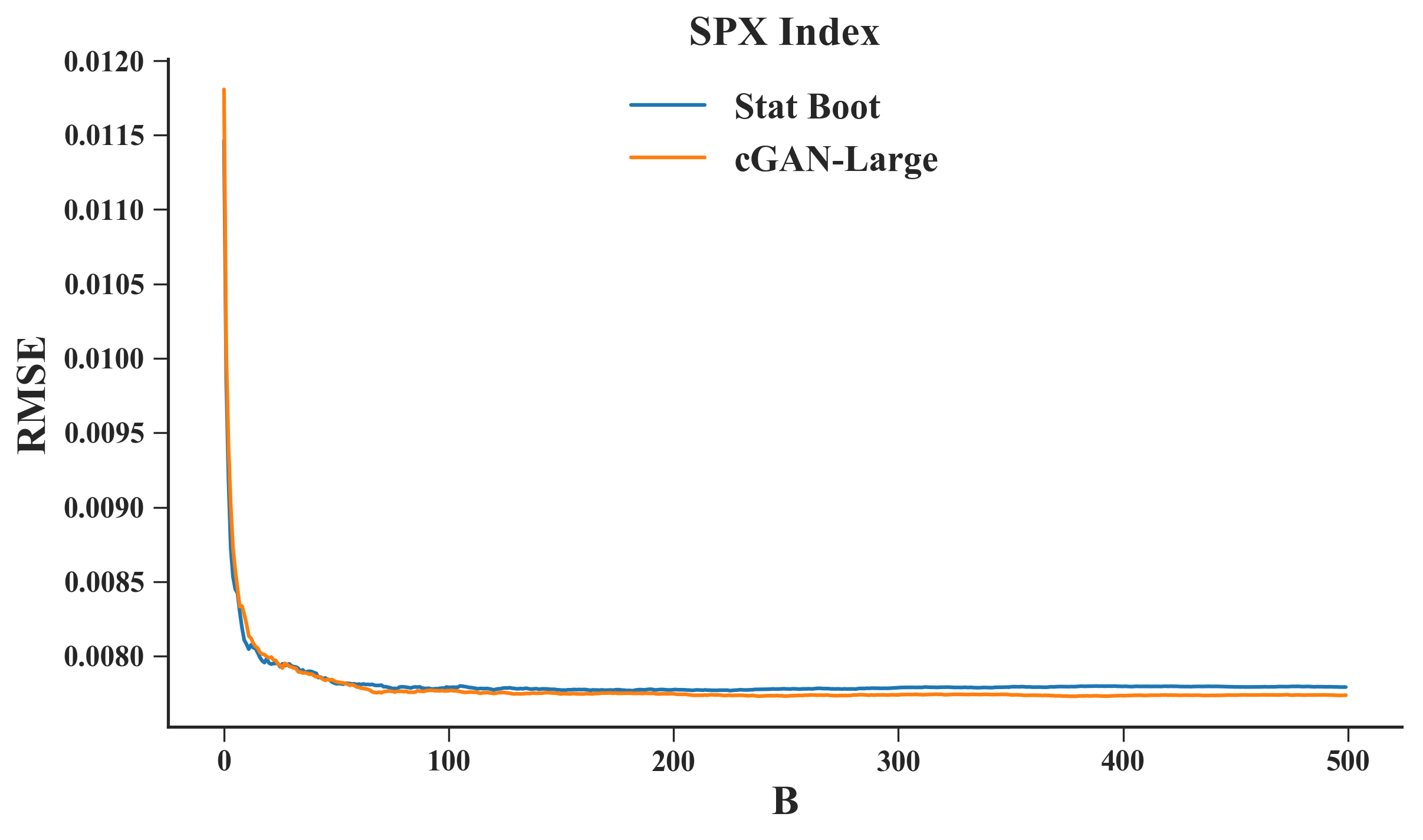

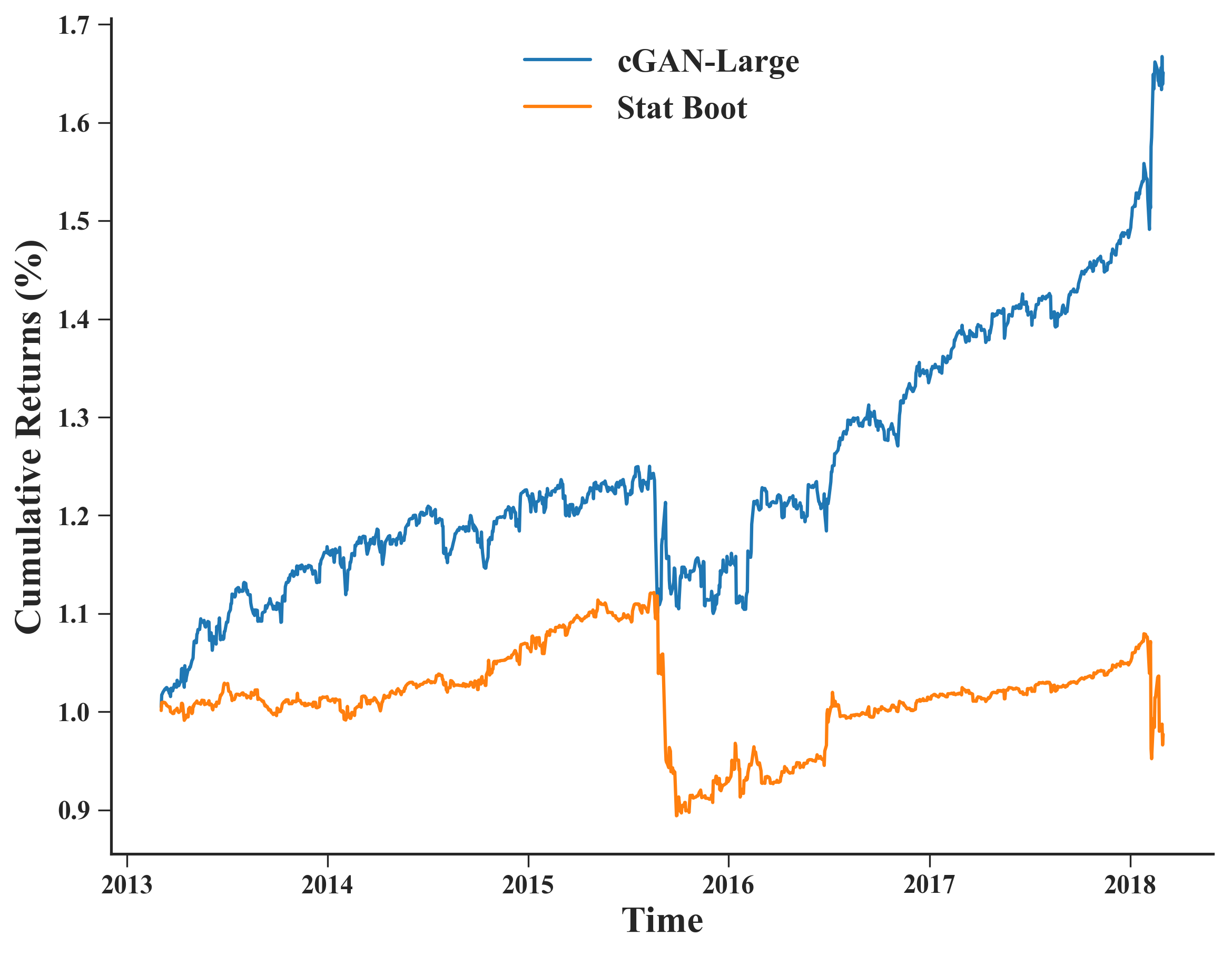

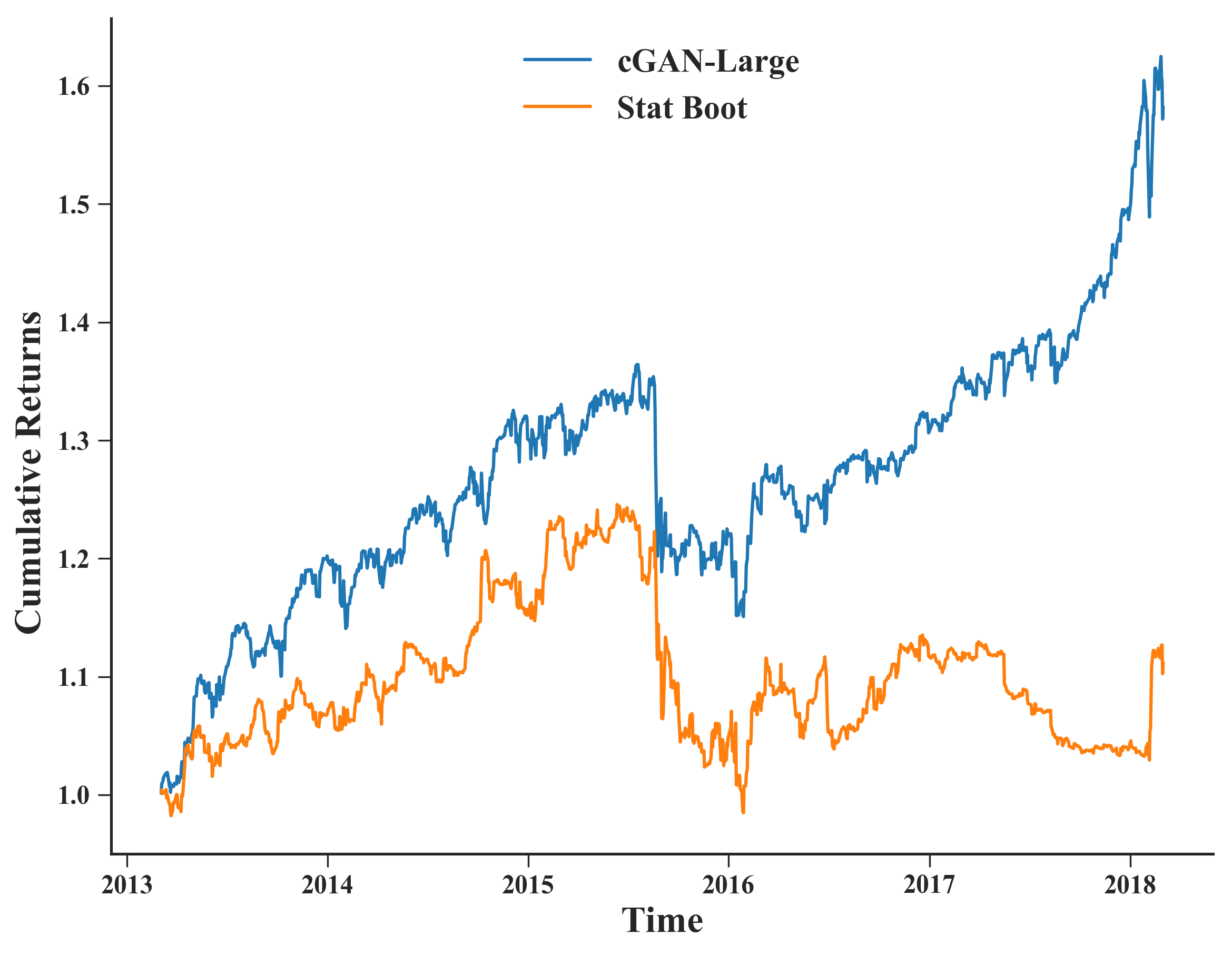

To give a more concrete example of this complementarity, Figure 7 presents the main findings obtained for SPX Index. Figures 7a and 7b show cGAN-Large as the ensemble strategy using Regression Tree and Multilayer Perceptron as the base learners, respectively. Regression Trees seemed more successful, obtaining a Sharpe and Calmar ratios of 1.00 and 0.75 approximately; but for both methods, cGAN-Large managed to produce positive Sharpe and Calmar ratios. Conversely, Stat Boot failed in both cases, scoring a Sharpe ratio near to 0.0 (Figures 7c and 7d). This outperformance manifested in a substantial gap between the cumulative returns of the different approaches (Figures 7g and 7h). Finally, although both methods similarly minimized RMSE (Figures 7e and 7f), this minimization manifested itself very differently from a Sharpe/Calmar ratio points of view. As a side note, this suggest that minimizing RMSE (a predictive metric) is not an ideal criteria when Sharpe ratio (a financial metric) is the metric that will decide which strategy to be implemented.

Regression Tree Multilayer Perceptron

4.2 Case II: Fine-tuning of Trading Strategies

Table 7 presents the quantiles of Sharpe and Calmar ratios in the set across the 579 assets for different trading strategies and model validation schemes. Starting from Ridge, we can spot that there not much differences between the model validation schemes, with Naive yielding the worst median (50%) values (0.121), and hv-Block, Block and cGAN-Medium with the best median (0.138); same can be said with respect to Calmar ratios.

| Trad Strat | Metric | Quant | Model Validation Scheme | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Naive | One-Split | Sliding | hv-Block | Block | k-Fold | Stat Boot | cGAN-Small | cGAN-Medium | cGAN-Large | |||

| Ridge | Sharpe | 0% | -1.594 | -1.594 | -1.594 | -1.594 | -1.594 | -1.493 | -1.594 | -1.493 | -1.493 | -1.493 |

| 25% | -0.215 | -0.212 | -0.213 | -0.201 | -0.201 | -0.214 | -0.213 | -0.197 | -0.197 | -0.197 | ||

| 50% | 0.121 | 0.134 | 0.122 | 0.138 | 0.138 | 0.135 | 0.135 | 0.135 | 0.138 | 0.136 | ||

| 75% | 0.403 | 0.418 | 0.409 | 0.409 | 0.409 | 0.424 | 0.410 | 0.424 | 0.419 | 0.419 | ||

| 100% | 3.156 | 3.177 | 3.238 | 3.226 | 3.226 | 3.177 | 3.203 | 3.226 | 3.226 | 3.226 | ||

| Calmar | 0% | -0.290 | -0.290 | -0.218 | -0.290 | -0.290 | -0.290 | -0.209 | -0.218 | -0.203 | -0.203 | |

| 25% | -0.075 | -0.071 | -0.071 | -0.071 | -0.071 | -0.071 | -0.071 | -0.071 | -0.071 | -0.071 | ||

| 50% | 0.055 | 0.063 | 0.060 | 0.064 | 0.064 | 0.063 | 0.064 | 0.063 | 0.064 | 0.064 | ||

| 75% | 0.236 | 0.251 | 0.232 | 0.239 | 0.241 | 0.241 | 0.241 | 0.241 | 0.244 | 0.244 | ||

| 100% | 5.074 | 4.561 | 4.561 | 4.561 | 4.561 | 4.561 | 4.561 | 4.561 | 4.561 | 4.561 | ||

| MLP | Sharpe | 0% | -1.362 | -1.583 | -1.554 | -1.291 | -1.297 | -1.389 | -1.062 | -1.150 | -1.212 | -1.176 |

| 25% | -0.310 | -0.280 | -0.263 | -0.246 | -0.254 | -0.207 | -0.226 | -0.290 | -0.241 | -0.247 | ||

| 50% | 0.020 | 0.061 | 0.073 | 0.086 | 0.097 | 0.112 | 0.115 | 0.059 | 0.061 | 0.067 | ||

| 75% | 0.352 | 0.390 | 0.400 | 0.396 | 0.416 | 0.406 | 0.429 | 0.380 | 0.396 | 0.416 | ||

| 100% | 1.249 | 1.579 | 1.390 | 1.564 | 1.903 | 1.663 | 1.896 | 1.733 | 1.757 | 1.464 | ||

| Calmar | 0% | -0.330 | -0.324 | -0.254 | -0.264 | -0.266 | -0.328 | -0.213 | -0.286 | -0.238 | -0.276 | |

| 25% | -0.099 | -0.095 | -0.089 | -0.081 | -0.090 | -0.073 | -0.073 | -0.093 | -0.087 | -0.093 | ||

| 50% | 0.008 | 0.026 | 0.031 | 0.039 | 0.046 | 0.050 | 0.056 | 0.022 | 0.028 | 0.032 | ||

| 75% | 0.194 | 0.213 | 0.212 | 0.214 | 0.242 | 0.229 | 0.235 | 0.211 | 0.229 | 0.224 | ||

| 100% | 1.565 | 1.981 | 1.738 | 2.399 | 2.381 | 1.724 | 1.586 | 2.209 | 1.554 | 1.579 | ||

| GBT | Sharpe | 0% | -1.197 | -1.171 | -1.155 | -1.289 | -1.143 | -1.038 | -1.073 | -1.157 | -1.275 | -1.157 |

| 25% | -0.233 | -0.192 | -0.208 | -0.167 | -0.143 | -0.212 | -0.214 | -0.239 | -0.209 | -0.224 | ||

| 50% | 0.088 | 0.159 | 0.142 | 0.175 | 0.211 | 0.174 | 0.162 | 0.123 | 0.150 | 0.133 | ||

| 75% | 0.391 | 0.503 | 0.488 | 0.537 | 0.546 | 0.534 | 0.527 | 0.446 | 0.531 | 0.473 | ||

| 100% | 5.174 | 5.174 | 4.411 | 5.174 | 5.174 | 5.174 | 5.174 | 3.443 | 1.929 | 5.174 | ||

| Calmar | 0% | -0.665 | -0.218 | -0.251 | -0.300 | -0.346 | -0.393 | -0.198 | -0.246 | -0.471 | -0.222 | |

| 25% | -0.080 | -0.070 | -0.078 | -0.058 | -0.060 | -0.076 | -0.077 | -0.084 | -0.076 | -0.084 | ||

| 50% | 0.038 | 0.071 | 0.066 | 0.081 | 0.105 | 0.077 | 0.072 | 0.053 | 0.067 | 0.064 | ||

| 75% | 0.232 | 0.325 | 0.299 | 0.348 | 0.385 | 0.331 | 0.333 | 0.295 | 0.325 | 0.306 | ||

| 100% | 7.492 | 7.492 | 6.454 | 7.492 | 7.492 | 7.492 | 7.492 | 3.782 | 2.845 | 7.492 | ||

Regarding Multilayer Perceptron (MLP) Sharpe ratio results, we can spot a bigger contrast in median terms: Naive fared worst as expected (0.020), with Stationary Bootstrap (Stat Boot) obtaining a median value six fold bigger than Naive. In this case, cGAN-Large (0.067) fared better across the cGANs, but still far from the top median values. For Gradient Boosting Trees (GBT), cGAN-Medium was the best of all cGAN approaches, obtaining better results than Sliding window scheme. However, these figures fell short to those of Block and hv-Block schemes, both faring 0.211 and 0.175 median Sharpe ratios, respectively.

So far we have focused on mainly at the median values, and though we can spot some discrepancies across the methods, these become small when we take into account the average interquartile range333A measure of dispersion calculated by taking the difference between the 3rd quartile (75%) and 25% 1st quartile. of 0.4 units of Sharpe ratio, around 3-5 times the size of the median values. In this sense, to statistically assess whether some of the observed difference is substantial, Table 8 presents a statistical analysis using the average ranks444When we rank the model validation schemes for a given asset, it means that we sort all them in such way that the best performer is in the first place (receive value equal to 1), the second best is positioned in the second rank (receive value equal to 2), and so on. We can repeat this process for all assets and compute metrics, such as the average rank (e.g., 1.35 means that a particular scheme was placed mostly near to the first place)., Friedman test and Holm correction for multiple hypothesis testing of the different model validation schemes for Ridge, MLP and GBT based on the Sharpe ratio results.

| Ridge-Sharpe | MLP-Sharpe | GBT-Sharpe | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Method | Avg Rank | p-value | Method | Avg Rank | p-value | Method | Avg Rank | p-value | Holm Correction |

| Naive | 5.700 | 0.0022 | Naive | 5.900 | 0.0001 | Naive | 6.074 | 0.0001 | 0.0055 |

| Sliding | 5.630 | 0.0081 | One-Split | 5.718 | 0.0004 | cGAN-Large | 5.642 | 0.0001 | 0.0062 |

| Stat Boot | 5.605 | 0.0121 | cGAN-Small | 5.549 | 0.0114 | Sliding | 5.628 | 0.0001 | 0.0071 |

| k-Fold | 5.592 | 0.0148 | cGAN-Medium | 5.497 | 0.0254 | cGAN-Small | 5.597 | 0.0001 | 0.0083 |

| One-Split | 5.510 | 0.0481 | Sliding | 5.489 | 0.0287 | cGAN-Medium | 5.431 | 0.0032 | 0.0100 |

| cGAN-Small | 5.503 | 0.0531 | hv-Block | 5.449 | 0.0492 | k-Fold | 5.427 | 0.0034 | 0.0125 |

| cGAN-Large | 5.487 | 0.0644 | Block | 5.444 | 0.0525 | Stat Boot | 5.427 | 0.0034 | 0.0167 |

| cGAN-Medium | 5.477 | 0.0729 | cGAN-Large | 5.411 | 0.0783 | One-Split | 5.415 | 0.0043 | 0.0250 |

| hv-Block | 5.253 | 0.4743 | k-Fold | 5.359 | 0.1368 | Block | 5.359 | 0.0112 | 0.0500 |

| Block | 5.243 | - | Stat Boot | 5.183 | - | hv-Block | 4.992 | - | - |

| Friedman | 5715.01 | 0.0001 | Friedman | 2040.8 | 0.0001 | Friedman | 2865.34 | 0.0001 | |

For Ridge Regression, the lowest rank was obtained by Block cross-validation (Block), whilst the worst by Naive (5.700). cGANs methods were consecutively in the third, fourth and fifth places, beating other methods, such as Stat Boot, k-fold cross-validation, etc. The Friedman statistics of 5715.01 signal that the hypothesis of equal average rank across the approaches is not statistically credible (p-value 0.0001). By running a pairwise comparison between Block and the remaining approaches, we can spot that only Naive has stand out as a substantially worst approach, even when we control for multiple hypothesis testing (check Holm Correction column for the adjusted level of significance).

In respect to MLP ranking results, Naive performed worst as well (5.900), with Stat Boot being the top scheme in this case (5.183); cGAN-Large in the third position, comparing favourably to the other cGAN configurations, as well as hv-Block, Sliding window, etc. Apart from Naive and One-Split/Single holdout scheme, all the remaining approaches were not statistically different from Stat Boot. On the GBT case, we can spot that hv-Block outperformed all approaches, with the cGANs do not delivering reasonable results in this case.

Overall, apart from a few analyses and cases (e.g., GBT and Naive method), in aggregate the model validation schemes do not appear to be significantly distinct from each other. This can be interpreted that cGAN is a viable procedure to be part of the fine-tuning pipeline, since its results are statistically indistinguishable to well established methodologies. When we drill down into the results, in particular to the Sharpe ratios of the different approaches, we can spot a low correlation among the validation schemes; Figure 8555We decided to omit Ridge since all of the correlations were above 0.8. presents correlation matrices based on Sharpe ratios of model validation schemes for MLP (a) and GBT (b).

Though in median and rank terms the strategies look similar, at the micro-level they appear quite the opposite, in particular to the MLP case. Even the cGANs provide distinct Sharpe ratios, showing the importance of the underlying configuration of the Generator/Discriminator. In general, this outline that distinct model validation schemes are arriving with different hyperparameter combinations, incurring in distinct values for Sharpe and Calmar ratios in the set. Hence, it may be that in some assets cGAN outcompeted the remaining model validation schemes. To exemplify that, Table 9 presents a sample of Sharpe ratio results in the set for cases where cGAN-Large outcompeted the other methods.

| MV Scheme | ADSWAP2Q | CADJPY | ED UN | NKY | NZDUSD |

|---|---|---|---|---|---|

| CMPN | BGN | Equity | Index | BGN | |

| Curncy | Curncy | Curncy | |||

| Naive | -0.3477 | 0.2009 | -0.0343 | -0.5785 | 0.4503 |

| One-Split | -0.0184 | -0.4218 | 0.0108 | 0.0520 | -0.0809 |

| Sliding | 0.5600 | -0.8328 | -0.227 | 0.1083 | 0.1034 |

| k-Fold | 0.0505 | -0.2861 | 0.4068 | -0.3347 | -0.3104 |

| Block | 0.4344 | 0.2219 | -0.0971 | -0.8870 | 0.1215 |

| hv-Block | 0.1120 | -0.3932 | 0.5364 | -0.0244 | -0.272 |

| Stat Boot | 0.4296 | -0.19498 | 0.3107 | -0.3068 | -0.2616 |

| cGAN-Small | 0.5146 | -0.6222 | -0.0980 | 0.1095 | 0.3059 |

| cGAN-Medium | 0.84 | -0.0901 | 0.3443 | 0.0884 | 0.0582 |

| cGAN-Large | 1.4207 | 0.5885 | 1.1224 | 0.2263 | 0.6703 |

We can spot a few instances that cGAN-Large substantially fared better results, such as in a 2y Australian Dollar Swap, New Zealand Dollar vs US Dollar Currency, and Consolidated Edison Inc. Equity. This set of results suggest that cGAN-Large is a viable alternative for fine-tuning machine learning models when other methodologies provide poor results, and it should be considered in the portfolio of different validation schemes aside of the distinct trading strategies models.

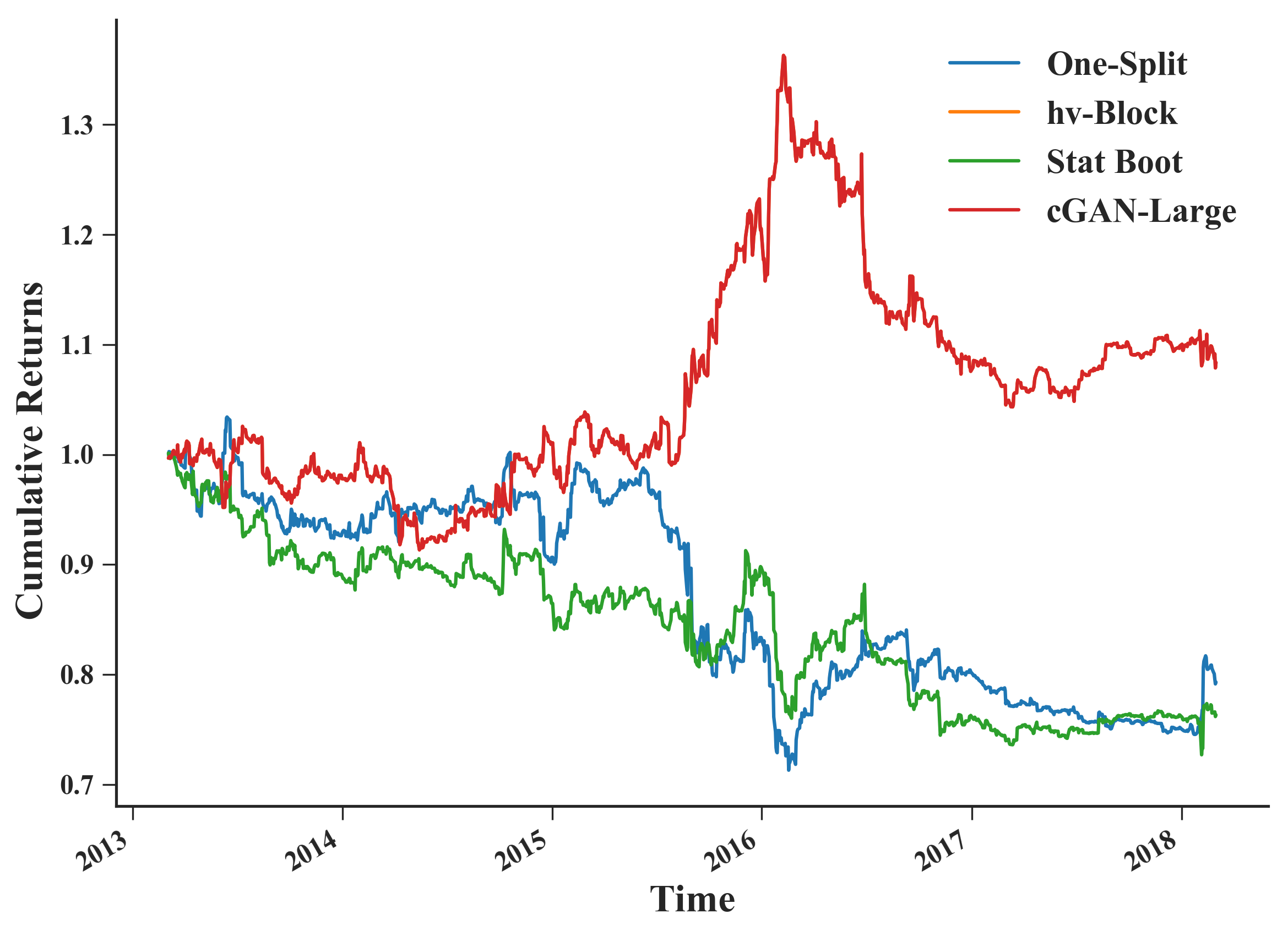

Finally, Figure 9 outlines the cumulative returns for SPX Index for a few of the different model validation schemes using MLP as the trading strategy. In this case, Stat Boot and One-Split were unable to produce a profit after five years of trading, whilst cGAN-Large and hv-Block produced around 10% of return for a given initial amount of investment (they both found out the same hyperparameters, therefore obtaining similar profiles). This is another example that demonstrate the relevance of having a set of model assessment schemes, as similar as the more common defensive posture of having a portfolio of trading strategies/models and hyperparameter optimization schemes.

5 Conclusion

This work has proposed the use of Conditional Generative Adversarial Networks (cGANs) for trading strategies calibration and aggregation. This emerging technique can have an impact into aspects of trading strategies, specifically fine-tuning and to form ensembles. Also, we can list a few advantages of such method, like: (i) generating more diverse training and testing sets, compared to traditional resampling techniques; (ii) able to draw samples specifically about stressful events, ideal for model checking and stress testing; and (iii) providing a level of anonymization to the dataset, differently from other techniques that (re)shuffle/resample data.

The price paid is having to fit this generative model for a given time series. To this purpose, we provided a full methodology on: (i) the training and selection of a cGAN for time series generation; (ii) how each sample is used for strategies calibration; and (iii) how all generated samples can be used for ensemble modelling. To provide evidence that our approach is well grounded, we have designed an experiment encompassing 579 assets, tested multiple trading strategies, and analysed different capacities for Generator/Discriminator. In summary, our main contributions were to show that our procedure to train and select cGANs is sound, as well as able to obtain competitive results against traditional methods for fine-tuning and ensemble modelling.

Being more specific, in the Case Study I: Combination of Trading Strategies, we compared cGAN Sampling and Aggregation with Stationary Bootstrap. Our results suggest that both approaches are equivalent in aggregate, with non-statistically significant advantage for cGAN when using Regression Trees, and for Stationary Bootstrap when using a shallow Multilayer Perceptron. But when Bagging via Stationary Bootstrap fails to perform properly, it is possible to use cGAN Sampling and Aggregation as a tool to combine weak signals in alpha generating strategies; SPX Index was an example where cGAN outcompeted Stationary Bootstrap by a wide margin.

In relation to the Case Study II: Fine-tuning of trading Strategies, we compared cGAN with a wide range of model validation strategies. All of these were techniques designed to handle time series scenarios: these ranged from window-based methods, to shuffling and reshuffling of a time series. We have evidence that cGANs can be used for model tuning, bearing better results in cases where traditional schemes fail. A side outcome of our work is the wealth of results and comparisons: to the best of our knowledge most of the applied model validation strategies have not yet been cross compared using real datasets and different models.

Finally, our work also open new avenues to future investigations. We list a few potential extensions and directions for further research:

-

•

cGANs for stress testing: a stress test examines the potential impact of a hypothetical adverse scenario on the health of a financial institution, or even a trading strategy. In doing so, stress tests allow the quantitative strategist to assess a strategy resilience to a range of adverse shocks and ensure they are sufficiently hedged to withstand those shocks. A proper benchmark can be model-based bootstrap, since it allows conditional variables which facilitates the process of generating resamples of crisis events.

-

•

Selection metrics for cGANs: we have adopted the Root Mean Square Error as the loss function between the generator samples and the actual data, however nothing limits the user to use another type of loss function. It could be a metric that take into account several moments and cross-moments of a time series. With financial time series, taking into account stylized facts [8] can be a feasible alternative to produce samples that are more meaningful and resemble more a financial asset return.

-

•

Combining cGAN with Stationary Bootstrap: in our results section, in particular to Figure 6, we observed the low correlation between the Sharpe ratios obtained in both approaches. This imply that a mixed approach, that is, combining resamples from cGAN and Stationary Bootstrap, can yield better results than opting for a single approach.

-

•

Extensions and other applications: a natural extension is to consider predicting directly multiple steps ahead, or considering modelling multiple financial time series. Both can improve our results, as well as, may reduce the time to train and select a cGAN. Another extension is to consider other architectures, such as AdaGANs [37] or Ensemble of GANs [39]. Also, other applications such as fine-tuning and combination of time series forecasting methods; a good benchmark are the M3 and M4 competitions [26, 27] that involve a large number of time series as well as results from a wide array of forecasting methods.

Acknowledgment

The authors would like to thank EO for his insightful suggestions and critical comments about our work. Adriano Koshiyama would like to acknowledge the National Research Council of Brazil for his PhD scholarship, and The Alan Turing Institute for providing infra-structure and environment to conclude this work.

References

- [1] Emmanuel Acar and Stephen Satchell. Advanced trading rules. Butterworth-Heinemann, 2002.

- [2] Martin Arjovsky, Soumith Chintala, and Léon Bottou. Wasserstein generative adversarial networks. In International Conference on Machine Learning, pages 214–223, 2017.

- [3] Sylvain Arlot, Alain Celisse, et al. A survey of cross-validation procedures for model selection. Statistics surveys, 4:40–79, 2010.

- [4] David H Bailey, Jonathan Borwein, Marcos Lopez de Prado, and Qiji Jim Zhu. The probability of backtest overfitting. Journal of Computational Finance (Risk Journals), 2015.

- [5] John M Bates and Clive WJ Granger. The combination of forecasts. Journal of the Operational Research Society, 20(4):451–468, 1969.

- [6] Christoph Bergmeir, Rob J Hyndman, and Bonsoo Koo. A note on the validity of cross-validation for evaluating autoregressive time series prediction. Computational Statistics & Data Analysis, 120:70–83, 2018.

- [7] James Bergstra and Yoshua Bengio. Random search for hyper-parameter optimization. Journal of Machine Learning Research, 13(Feb):281–305, 2012.

- [8] Rama Cont. Empirical properties of asset returns: stylized facts and statistical issues. 2001.

- [9] Antonia Creswell, Tom White, Vincent Dumoulin, Kai Arulkumaran, Biswa Sengupta, and Anil A Bharath. Generative adversarial networks: An overview. IEEE Signal Processing Magazine, 35(1):53–65, 2018.

- [10] Joaquín Derrac, Salvador García, Daniel Molina, and Francisco Herrera. A practical tutorial on the use of nonparametric statistical tests as a methodology for comparing evolutionary and swarm intelligence algorithms. Swarm and Evolutionary Computation, 1(1):3–18, 2011.

- [11] Georgios Douzas and Fernando Bacao. Effective data generation for imbalanced learning using conditional generative adversarial networks. Expert Systems with applications, 91:464–471, 2018.

- [12] Bradley Efron and Trevor Hastie. Computer age statistical inference, volume 5. Cambridge University Press, 2016.

- [13] Katharina Eggensperger, Matthias Feurer, Frank Hutter, James Bergstra, Jasper Snoek, Holger Hoos, and Kevin Leyton-Brown. Towards an empirical foundation for assessing bayesian optimization of hyperparameters. In NIPS workshop on Bayesian Optimization in Theory and Practice, volume 10, page 3, 2013.

- [14] Martin Eling and Frank Schuhmacher. Does the choice of performance measure influence the evaluation of hedge funds? Journal of Banking & Finance, 31(9):2632–2647, 2007.

- [15] Cristóbal Esteban, Stephanie L Hyland, and Gunnar Rätsch. Real-valued (medical) time series generation with recurrent conditional gans. arXiv preprint arXiv:1706.02633, 2017.

- [16] Ugo Fiore, Alfredo De Santis, Francesca Perla, Paolo Zanetti, and Francesco Palmieri. Using generative adversarial networks for improving classification effectiveness in credit card fraud detection. Information Sciences, 2017.

- [17] Jerome Friedman, Trevor Hastie, and Robert Tibshirani. The elements of statistical learning, volume 1. Springer series in statistics New York, NY, USA:, 2001.

- [18] Ian Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. Generative adversarial nets. In Advances in neural information processing systems, pages 2672–2680, 2014.

- [19] Ishaan Gulrajani, Faruk Ahmed, Martin Arjovsky, Vincent Dumoulin, and Aaron C Courville. Improved training of wasserstein gans. In Advances in Neural Information Processing Systems, pages 5767–5777, 2017.

- [20] Campbell R Harvey and Yan Liu. Backtesting. The Journal of Portfolio Management, pages 12–28, 2015.

- [21] Cheng Hsiao and Shui Ki Wan. Is there an optimal forecast combination? Journal of Econometrics, 178:294–309, 2014.

- [22] Xun Huang, Yixuan Li, Omid Poursaeed, John E Hopcroft, and Serge J Belongie. Stacked generative adversarial networks. In CVPR, volume 2, page 3, 2017.

- [23] Gaoxia Jiang and Wenjian Wang. Markov cross-validation for time series model evaluations. Information Sciences, 375:219–233, 2017.

- [24] Soumendra Nath Lahiri. Resampling methods for dependent data. Springer Science & Business Media, 2013.

- [25] Ilya Loshchilov and Frank Hutter. Cma-es for hyperparameter optimization of deep neural networks. arXiv preprint arXiv:1604.07269, 2016.

- [26] Spyros Makridakis and Michele Hibon. The m3-competition: results, conclusions and implications. International journal of forecasting, 16(4):451–476, 2000.

- [27] Spyros Makridakis, Evangelos Spiliotis, and Vassilios Assimakopoulos. The m4 competition: Results, findings, conclusion and way forward. International Journal of Forecasting, 2018.

- [28] Xudong Mao, Qing Li, Haoran Xie, Raymond YK Lau, Zhen Wang, and Stephen Paul Smolley. Least squares generative adversarial networks. In Computer Vision (ICCV), 2017 IEEE International Conference on, pages 2813–2821. IEEE, 2017.

- [29] Mehdi Mirza and Simon Osindero. Conditional generative adversarial networks. Manuscript: https://arxiv. org/abs/1709.02023, 2014.

- [30] Georg Ostrovski, Will Dabney, and Rémi Munos. Autoregressive quantile networks for generative modeling. arXiv preprint arXiv:1806.05575, 2018.

- [31] Jeff Racine. Consistent cross-validatory model-selection for dependent data: hv-block cross-validation. Journal of econometrics, 99(1):39–61, 2000.

- [32] Alec Radford, Luke Metz, and Soumith Chintala. Unsupervised representation learning with deep convolutional generative adversarial networks. arXiv preprint arXiv:1511.06434, 2015.

- [33] Joseph P Romano and Michael Wolf. Efficient computation of adjusted p-values for resampling-based stepdown multiple testing. Statistics & Probability Letters, 113:38–40, 2016.

- [34] Tim Salimans, Ian Goodfellow, Wojciech Zaremba, Vicki Cheung, Alec Radford, and Xi Chen. Improved techniques for training gans. In Advances in Neural Information Processing Systems, pages 2234–2242, 2016.

- [35] William F Sharpe. The sharpe ratio. Journal of portfolio management, 21(1):49–58, 1994.

- [36] Allan Timmermann. Forecast combinations. Handbook of economic forecasting, 1:135–196, 2006.

- [37] Ilya O Tolstikhin, Sylvain Gelly, Olivier Bousquet, Carl-Johann Simon-Gabriel, and Bernhard Schölkopf. Adagan: Boosting generative models. In Advances in Neural Information Processing Systems, pages 5424–5433, 2017.

- [38] Chaoyue Wang, Chang Xu, Xin Yao, and Dacheng Tao. Evolutionary generative adversarial networks. arXiv preprint arXiv:1803.00657, 2018.

- [39] Yaxing Wang, Lichao Zhang, and Joost van de Weijer. Ensembles of generative adversarial networks. arXiv preprint arXiv:1612.00991, 2016.

- [40] Terry W Young. Calmar ratio: A smoother tool. Futures, 20(1):40, 1991.

- [41] Junbo Zhao, Michael Mathieu, and Yann LeCun. Energy-based generative adversarial network. arXiv preprint arXiv:1609.03126, 2016.

- [42] Xingyu Zhou, Zhisong Pan, Guyu Hu, Siqi Tang, and Cheng Zhao. Stock market prediction on high-frequency data using generative adversarial nets. Mathematical Problems in Engineering, 2018, 2018.