Nonparametric Instrumental Variables Estimation Under Misspecification

Abstract

Nonparametric Instrumental Variables (NPIV) analysis is based on a conditional moment restriction. We show that if this moment condition is even slightly misspecified, say because instruments are not quite valid, then NPIV estimates can be subject to substantial asymptotic error and the identified set under a relaxed moment condition may be large. Imposing strong a priori smoothness restrictions mitigates the problem but induces bias if the restrictions are too strong. In order to manage this trade-off we develop a methods for empirical sensitivity analysis and apply them to the consumer demand data previously analyzed in Blundell et al., (2007) and Horowitz, (2011).

Instrumental validity can be difficult to defend. The assumption rules out not only confounding between outcomes and instruments, but also any direct causal effect of the instruments on outcomes. Thus instruments may not be valid even if they are assigned by an ideal randomized experiment. To justify the use of instrumental variables (IV) methods, applied researchers usually argue not that instrumental validity holds exactly, but that any deviation from validity is small.111See Conley et al., (2008) for further discussion. ‘Small’ does not imply ‘inconsequential’, and so it is important to assess the sensitivity of IV methods to a modest deviation from full instrumental validity.

In this work we consider the sensitivity of Nonparametric Instrumental Variables (NPIV) analysis (Newey & Powell, (2003), Ai & Chen, (2003)) to misspecification, particularly that which results from invalid instruments. NPIV generalizes the linear IV model to allow for a flexible, non-linear ‘structural function’. The structural function is the key object of interest and typically has a causal interpretation. Identification and estimation is based on a conditional moment restriction. If instruments are invalid then the moment condition generally does not hold.

We show that identification in NPIV models is fragile. If only weak a priori conditions are placed on the structural function, then the identified set can be very large under only a slight relaxation of the NPIV moment condition. Estimation in NPIV models can be highly non-robust to misspecification. For estimators that impose only weak restrictions on the structural function, an arbitrarily small deviation from instrumental validity can impart a large asymptotic bias. This sensitivity is a consequence of the ‘ill-posedness’ of the NPIV moment restriction.

If researchers place sufficiently strong restrictions (typically smoothness conditions) on the structural function, then robust identification is possible. Estimation that is robust to misspecification can be achieved by constraining the estimates so that they satisfy such smoothness conditions. In both cases, the sensitivity to misspecification is still greater in a certain sense than for standard nonparametric regression or parametric IV. Imposing strong smoothness restrictions in estimation carries a cost. If the true structural function does not obey these restrictions then an estimator that imposes them is necessarily inconsistent.

Two NPIV estimation methods which impose sufficient smoothness conditions are the procedures of Newey & Powell, (2003) and Blundell et al., (2007). A number of prominent NPIV procedures do not constrain the estimates to be smooth. For example, the methods described in Chen & Christensen, (2018), Darolles et al., (2011), Hall & Horowitz, (2005), and Horowitz, (2011).

Robust estimation is also possible if the researcher is interested in a continuous functional of the structural function rather than the function itself. We provide necessary and sufficient conditions under which such a functional can be estimated robustly without the need to impose smoothness.

Our results suggest that researchers face a trade-off: impose too little smoothness and NPIV estimates are non-robust to invalid instruments, impose too much smoothness and the estimates are inconsistent even if instruments are valid. In response, we supplement NPIV estimation with a method for empirical sensitivity analysis. Methods for sensitivity analysis are increasingly popular in applied economics and include local methods (e.g., Andrews et al., (2017), Armstrong & Kolesar, (2018), Bonhomme & Weidner, (2020)), and global methods (e.g., Altonji et al., (2005), Masten & Poirier, (2018), Oster, (2019))). We develop a technique for global sensitivity analysis in which the researcher estimates the identified set under relaxations of the NPIV moment condition and various smoothness assumptions. Thus researchers can assess which of their findings are robust to some misspecification of the NPIV moment condition and examine the trade-off between robustness and smoothness. Estimation of the identified set under weakened assumptions is used elsewhere for sensitivity analysis, for example in Masten & Poirier, (2018). The set estimation problem is well-posed, and we derive convergence rates under primitive conditions.

We apply our methods to the empirical setting shared by Blundell et al., (2007) and Horowitz, (2011) who use NPIV methods to estimate shape-invariant Engel curves using data from The British Family Expenditure Survey. We argue that in this setting instruments are unlikely to be fully exogenous, in which case the NPIV moment restriction will not hold exactly. We use our methodology to assess which features of the structural Engel curve for food can be inferred robustly.

A Note on Notation

For a random variable , the corresponding calligraphic letter denotes its support and its probability distribution. If and are random variables then statements of the form or should be understood to hold with probability . If is a random variable and a function on then is the essential supremum of , we refer to this as the ‘sup norm’. If is a subset of a topological space then is its closure and its interior. For an operator , if then is the image of under and if then is the pre-image of . If is a normed space then we denote its norm by . If is a set of functions with domain then contains all length- vectors of functions such that for all , where . For a real vector we let denote the norm of .

1 Analytical Sensitivity Results

1.1 Background and Assumptions

NPIV estimation is a flexible, nonparametric alternative to linear IV. It has been studied extensively, for example in Newey & Powell, (2003), Ai & Chen, (2003), Chen & Pouzo, (2012), Darolles et al., (2011), Hall & Horowitz, (2005), Horowitz, (2011), and Chen & Christensen, (2018). NPIV methods have been applied in empirical work by Blundell et al., (2007), Chen & Christensen, (2018), and Horowitz, (2011) among others.

NPIV models relax the linearity assumption of linear IV but retain additive separability. Let be an outcome of interest, an endogenous variable, and an instrument. NPIV analysis assumes where is a non-random ‘structural function’ and the structural residual satisfies . NPIV is ‘nonparametric’ because the structural function is not assumed to take any particular parametric form.

The structural function is the key object of interest and typically has a causal interpretation. The use of instrumental variables is motivated by the policy-relevance of . If is correlated with then standard nonparametric regression will not recover but rather a reduced-form parameter which may not be useful for analyzing the effects of a policy.

We can obtain an NPIV model by imposing an additive structure for potential outcomes and assuming instruments are valid in the sense of Angrist et al., (1996). In particular, instruments are valid if they have no direct causal effect on outcomes and they are randomly assigned. Let be the potential outcome from a counterfactual treatment level and counterfactual value of the instrument . An additive model for is given below.

| (1.1) |

The random variable captures all heterogeneity in potential outcomes and without loss of generality . The instrument has no direct effect on outcomes and so does not depend on , that is, . If the instrument is randomly assigned then . In this case the NPIV model holds with the average potential outcome from treatment level , that is .222In fact, we can allow for non-additive heterogeneity in potential outcomes so long as this heterogeneity is fully exogenous. Formally, suppose where is a non-random function, , and as before . Then the NPIV model holds with .

Assumption 1.1 below formally states the key NPIV identifying moment restriction. It is equivalent to the model with .

Assumption 1.1 (Correct Specification).

We sometimes wish to place a priori restrictions on the structural function. To achieve this we can assume belongs to a restrictive subset of the underlying space of functions .

Assumption 1.2 (Parameter Space).

.

Assumptions 1.1 and 1.2 are structural assumptions in the sense that one cannot confirm that they hold by looking at the joint distribution of the observables. The non-structural Assumptions 1.3 and 1.4 below are imposed throughout the NPIV literature. They restrict the joint distribution of and .

Assumption 1.3 (Completeness).

For any , if and only if .

Assumption 1.4 (Compactness).

Define the linear operator by the equation . is a compact infinite-dimensional linear operator from the Banach space into a Banach space .

Assumption 1.3 imposes a type of statistical completeness. Completeness plays a role analogous to the rank condition for identification in linear IV (Newey & Powell, (2003)).333For some work on statistical completeness see Andrews, (2017), Canay et al., (2013), Chen et al., (2014), D’Haultfoeuille, (2011), Freyberger, (2017), and Hu & Shiu, (2018). If Assumption 1.3 holds then Assumptions 1.1 point identifies .

Assumption 1.4 is a technical condition that allows us to apply powerful results from functional analysis to the NPIV estimation problem. For common choices of and , Assumption 1.4 holds under weak primitive conditions on the joint distribution of and (Florens, (2011), Horowitz, (2011)). However, the assumption rules out the case of which corresponds to standard non-parametric regression.444When and , is the identity and cannot be compact unless is finite-dimensional. See Theorem 2.20 in Kress, (2014).

As a leading example we consider and to be spaces of continuous functions equipped with the sup norm . In this case a sufficient condition for Assumption 1.4 is that and have compact supports and admit a strictly positive continuous joint probability density.555This implies the conditional density of given is continuous and so we can apply Theorem 2.21 in Kress, (2014).

While our results apply for quite general choices of the underlying function spaces and , Assumption 1.5 below places some mild restrictions on these spaces. The condition ensures that means of functions in these spaces are finite. We also assume that the outcome has a finite mean.

Assumption 1.5 (First Moments).

, , and . The mapping from an element to its mean is continuous.

Let us define a function by . Using defined in Assumption 1.4, we can rewrite the moment condition in Assumption 1.1 as an equation . If Assumption 1.3 holds then this equation has a unique solution . The quantity on the right-hand side depends only on the distribution of the observables, and so is identified. If the NPIV moment condition is misspecified then need not equal , and so we refer to the latter as the ‘pseudo-solution’.

NPIV estimation is often said to be ‘ill-posed’. This refers to the fact that under Assumptions 1.3 and 1.4, the pseudo-solution varies discontinuously with . In fact, if we perturb by some arbitrarily small amount, this can induce an arbitrarily large change in the pseudo-solution. This is problematic for estimation because and must be empirically estimated, and thus are subject to error. If we substitute these estimates into the pseudo-solution then ill-posedness suggests the resulting estimate of can be highly inaccurate, even if and are precisely estimated.

To tackle this problem researchers have proposed numerous ‘regularization’ methods. Regularization involves replacing the discontinuous operator in the pseudo-solution with a continuous approximation. This generally imparts bias and so the degree of regularization is reduced as the sample size grows.666Available regularization methods including Tikhonov regularization, projection onto a finite-dimensional sieve space, and many others. See Darolles et al., (2011) for discussion. Reducing the strength of regularization increases sensitivity to error in the estimates of and , but this error typically decreases with the sample size. If the regularization is relaxed sufficiently slowly then the reduction in error more than offsets the increased sensitivity.

A key insight in this work is that misspecification, due to say invalid instruments, perturbs away from the value it would take under correct specification. The pseudo-solution is highly sensitive to perturbations due to misspecification just as it is to estimation error. NPIV estimators are typically designed to converge in probability to the pseudo-solution (Ai & Chen, (2007)), estimates that converge to the pseudo-solution under weak conditions are thus highly sensitive to misspecification, at least asymptotically. A similar sensitivity result applies for the identified set under a slight relaxation of the NPIV moment condition. To the best of our knowledge this point is entirely absent from the rest of the NPIV literature. The precise consequences for identification and estimation depend crucially on whether or not strong a priori conditions are imposed on the structural function. Strong restrictions can shrink the identified set and limit the conditions under which an NPIV estimator converges to the pseudo-solution.

1.2 Introducing Misspecification

The NPIV model is misspecified if Assumption 1.1 does not hold. That is, defined below is non-zero with positive probability:

| (1.2) |

Example 1: Direct Effect of the Instrument.

Suppose we relax the model for potential outcomes (1.1) so that the instrument may have a direct and additively separable effect on outcomes:

Without loss of generality we suppose and so that . We assume as before that the instrument is randomly assigned so that . This model implies (1.2).

Example 2: Confounded Instrument.

Suppose that (1.1) holds with , but the instrument is not randomly assigned. Instead, and are statistically associated due to their shared dependence on a latent factor and assume . Let and be the conditional probability densities of given , and of given respectively. In this case (1.2) holds with and given below:

Example 3: Nonseparable IV Model.

Consider the fully nonseparable potential outcomes model . As before, instruments have no direct effect on outcomes. Let be the potential treatment from a counterfactual level of the instrument . In this nonseparable model random assignment of the instrument can be formalized as . Suppose and admit a joint density and marginal densities and . Let then (1.2) holds with given below:

Assumption (Nearly Correct Specification).

where and .

The scalar in Assumption controls the degree of misspecification. If then Assumption 1.1 holds and so the NPIV moment condition is correctly specified. If is small but non-zero then the two sides of the moment condition in Assumption 1.1 need not be equal, but they must be close to equal, with the distance between them measured by . If is equipped with the sup norm then is equivalent to .

Other choices of norms correspond to stronger or weaker notions of misspecification. For example if we take to be the norm then we restrict the second moment of to be less than , which is weaker than the corresponding restriction on the sup norm.

Bounds on the norm of can be derived from more primitive conditions. Consider Example 1 above and let be a set of continuous functions equipped the sup norm. The direct causal effect of changing the instrument from to is . Suppose that for all the magnitude of this effect is at most , given it follows that . Conversely, must be bounded above by . Thus the norm of is small if and only if the instrument has at most a small direct impact on outcomes.

In Example 2 one can show the sup norm of must be less than the essential supremum of . This quantity measures the strength of the dependence between the structural residual and the unobserved confounder . In Example 3 one can derive the following bound:

The expression on the right-hand side measures how closely can be approximated by an additively separable function. Thus a bound the approximation error implies a bound on the norm of .

The restriction that allows us to incorporate additional conditions on . In Examples 1 and 2, but not necessarily Example 3, by construction, and so we may take to contain only functions with zero-mean. can also incorporate smoothness restrictions. In Example 1 is smooth if, loosely speaking, small changes in have small direct causal effects on the outcome.

In order to accommodate cases in which contains only zero-mean functions it is helpful to define the subspaces and so that contains all with and contains all with .

Our first result concerns the size of the identified set under the a priori assumptions and . The identified set is the set of functions that are consistent with these two assumptions:

| (1.3) |

Theorem 1.1 concerns the diameter of the identified set. The diameter, denoted is defined as follows:

Theorem 1.1.

Suppose Assumptions 1.3-1.5 hold and contains an open -ball centered at zero of radius .777An open -ball of radius is the intersection of and an open ball in of radius .

a. If then . More precisely, for all , , where is the radius of the largest open ball in centered at .

b. If is compact and , then . If in addition is absolutely convex and infinite-dimensional, and for some , then .888A subset of a real vector space is ‘absolutely convex’ if for any and , implies .

Theorem 1.1 examines the diameter of the identified under different degrees of misspecification. The behavior of the set for small values of depends crucially on the strength of the a priori restrictions on the structural function, as captured in . Part a. of the theorem requires that the pseudo-solution lies in the interior of the closure of . Some spaces of smooth functions are sufficiently restrictive that they are compact, in which case the interior is empty and part a. cannot apply.999A compact subset of an infinite-dimensional Banach space must be closed and have an empty interior. Part b. provides results for these more restrictive parameter spaces.

Under the conditions of part a., the diameter of the identified set does not shrink to zero with . Instead it remains bounded below by a constant that depends on and . Consider the extreme case in which is dense in and contains an open ball centered at zero. Then diameter of the identified set is infinite, regardless of how small we make the bound .101010If contains an open -ball at zero then for sufficiently small we can replace with (so ) and the resulting identified set contains the original as a subset. Under the conditions of part b., the identified set shrinks to a point as the degree of misspecification is reduced. However, the diameter of the identified set shrinks to zero strictly more slowly than the bound .

Let us compare to standard non-parametric regression. This case corresponds to the NPIV moment condition with . Let . Recall that Assumption 1.4 cannot hold in this setting and so Theorem 1.1 does not apply. In this case the identified set has diameter at most , regardless of the choice of and . The identified set shrinks to zero at exactly the same rate as . This is strictly faster than the rate at which the identified set shrinks in the NPIV case, even under the strong restrictions on imposed by part b. of Theorem 1.1.

We now specify spaces and compatible with parts a. and b. of the theorem. For concreteness let be the set of continuous functions with the sup norm and assume has compact support.

First take to be the set of Lipschitz continuous functions whose magnitude is bounded by a known constant :

| (1.4) |

By the Stone-Weirstrauss theorem the set of Lipschitz functions is dense . Thus this set satisfies the conditions in part a. of Theorem 1.1 with .

Now suppose we further restrict so that it contains only Lipschitz continuous functions with Lipschitz constant less than :

| (1.5) |

The closure of this set does not contain an open ball so we cannot apply part a. of Theorem 1.1. In fact, the set is compact (see Freyberger & Masten, (2019)) and it is absolutely convex and infinite-dimensional. Thus this choice of satisfies the restriction in part b. of Theorem 1.1. Part b. also requires that the pseudo-solution be in and that for some . Given the choice of above, this holds if and only if is Lipschitz with constant strictly less than and bounded in magnitude by a constant strictly less than .

Compact parameter spaces like (1.5) are employed in many NPIV papers. For example they appear in Newey & Powell, (2003), Ai & Chen, (2003), Blundell et al., (2007), Freyberger, (2017), and Santos, (2012).

The distinction between the sets (1.4) and (1.5) may seem subtle. However, (1.5) encodes much stronger knowledge about the structural function . Not only do we know is Lipschitz continuous, we know it is Lipschitz continuous with a Lipschitz constant smaller than a known scalar . A similar distinction holds for other smoothness conditions. For example, in Section 2 we consider a space of functions whose second derivatives are bounded. In order to achieve an identified set that shrinks to zero with we must be willing to assume a specific bound on the second derivatives of . It is not enough to simply assume that there exists some unknown finite bound on the second derivatives.111111For more examples of infinite-dimensional sets of compact functions see Freyberger & Masten, (2019). All examples in that paper also satisfy the absolute convexity requirement.

The condition on is the same for both parts of the Theorem, it states that contains an open -ball centered at zero of radius . This condition is relatively weak in that it can hold even if contains only very smooth functions. Suppose we impose the same strong Lipschitz condition on as in (1.5):

| (1.6) |

Although this set is restrictive, can contain an open ball at zero. The following is a sufficient (but not necessary) condition for such a ball to exist given the choice of above. Let be the conditional probability density of given . Suppose is well-defined and Lipschitz continuous in its argument:

Denote the quantity on the right-hand side above by . Then contains an open -ball of radius .

The Sensitivity of Estimators of the Structural Function

The sensitivity of a given NPIV estimator to misspecification may be substantially worse than is suggested by Theorem 1.1. The reason for this is that under misspecification the probability limit of a particular NPIV estimate may be outside of the identified set. We show below that the sensitivity of an NPIV estimator to misspecification depends crucially on the conditions under which it is consistent under correct specification. In particular, an NPIV estimator that achieves consistency under only weak a priori conditions on the structural function is necessarily very sensitive to misspecification. Thus in order to obtain estimates that are robust to misspecification, one must forgo consistent estimation whenever the true structural function lies outside a restrictive parameter space.

In order to capture this formally we introduce a notion of asymptotic bias. In particular, we consider the largest possible (un-scaled) asymptotic bias under Assumptions , 1.2, 1.3, and 1.4. We fix parameters that are not directly related to misspecification. That is, we fix the structural function and the joint probability distribution of , , and . The worst-case asymptotic bias of an estimator for a given is then:

The above is a version of the ‘maximum bias’ discussed in Huber, (2011). The definition above does not require that has a probability limit.121212The existence of a probability limit for an NPIV estimator is difficult to establish under misspecification, sufficient conditions for the existence of a probability limit for misspecified sieve minimum distance estimators can be found in Ai & Chen, (2007). If converges in probability to a limit then the infimum in the definition above is equal to .

Theorem 1.2.

Fix so that Assumptions 1.3-1.5 hold. Let be the set of all functions so that if and Assumption 1.1 holds then . Suppose contains an open ball centered at of radius and contains an open -ball centered at zero of radius .

Then . More precisely, for all , .

Theorem 1.2 shows that there is a trade-off between consistency under correct specification and robustness to misspecification. Suppose that under correct specification and some restrictions on the distribution of observables, an NPIV estimator is consistent whenever . Ideally would be large so that consistency does not require strong a priori assumptions on the structural function. However, if is large (in the sense given in the theorem), then the estimator must be very sensitive to certain kinds of misspecification. This is true even if the structural function in fact lies in a set that is much more restrictive than .

Theorem 1.2 can be used to derive the sensitivity properties of particular NPIV estimators. To apply the theorem we can use existing asymptotic results to establish consistency over a sufficiently large space . In Appendix A1 we verify the key conditions of the theorem for some highly-cited NPIV estimators.

Some NPIV estimators are constructed in such a way that Theorem 1.2 cannot apply. These estimators are constrained so that is always an element of a restrictive parameter space like (1.5) whose closure has an empty interior. For example, let be an empirical objective function that may change with the sample size (for example, to incorporate a penalty function with decreasing strength) and let be a finite-dimensional subset of that can grow with the sample size. Many NPIV estimators take the form below, including those in Newey & Powell, (2003) and Blundell et al., (2007).

Because is a subset of , the estimate above must be an element of for all . Such an estimator is necessarily inconsistent if . If is sufficiently restrictive, for example if it takes the form (1.4), then the sensitivity result in Theorem 1.2 cannot apply. Thus such estimators forgo consistency outside of a restrictive parameter space but have the advantage that they potentially avoid the non-robustness to misspecification suggested by the theorem. If the researcher is certain that really does satisfy the restrictions imposed by inclusion in , then there is no cost to inconsistency outside of .

Our next result establishes conditions on an estimator that ensure it is robust in the sense that . However, analogous to Theorem 1.1, the rate at which the bias goes to zero must be strictly slower than the rate at which the degree of misspecification shrinks to zero

The key condition is that converges in probability to a function . is a projection onto . That is, a possibly non-linear operator that maps functions into and leaves those already in this set unchanged. This condition implies the estimator has a probability limit in . Thus if is not in then the estimator is necessarily inconsistent, even under correct specification. Conversely, if Assumption 1.1 holds and , then and so is consistent.

Theorem 1.3.

Fix so Assumptions 1.3-1.5 hold and suppose contains an open -ball centered at zero of radius .

Let be a compact subset of and let be a continuous projection onto . Suppose satisfies .

If then . If in addition is absolutely convex and infinite-dimensional, and for some , then .

Let us compare again with the case of standard nonparametric regression (where ). Suppose that under some conditions on a nonparametric regression estimator converges to the condition mean . If Assumption 1.1 holds then and so the estimator is consistent under correct specification. Under misspecification, the difference between the conditional mean and the structural function is simply . If we use the same norm to measure the degree of misspecification (i.e, the magnitude of ) and the worst-case bias, then this estimator has worst-case bias . Thus the estimator is robust and has worst-case bias that shrinks at the same rate as the degree of misspecification. This does not require projection onto some restricted parameter space .

1.3 Continuous Linear Functionals

The sensitivity results in Theorems 1.1-1.3 apply to the identified set for the structural function itself and estimators of the structural function. If the object of interest is instead a smooth linear functional of the structural function then the identified set may shrink to zero with the degree of misspecification, even without any strong a priori smoothness restrictions. Moreover, it may be possible to construct estimates that a) are consistent under correct specification of the NPIV moment condition without any a priori restrictions on the true structural function and also b) are robust to the failure of instrumental validity.

The estimation of functionals of the structural function in NPIV models is analyzed extensively in the literature (Ai & Chen, (2003), Severini & Tripathi, (2012), Ichimura & Newey, (2017), and others). Following Severini & Tripathi, (2012), we let and similarly . These choices of function spaces have the advantage that any continuous linear functional takes the form where . This characterization follows by the Reisz representation theorem.

The identified set for the linear functional is simply . Let be an estimator of and fix and . The worst-case asymptotic bias of is defined below.

Severini & Tripathi, (2012) show that is estimable at rate only if there exists a function so that . Theorem 1.4 shows that this condition is necessary and sufficient for robust estimation of to be possible without restricting the parameter space.

Theorem 1.4.

Fix so Assumptions 1.3-1.5 hold. Take and . Suppose that for any if Assumption 1.1 holds then .

a. If there exists with , then and are bounded above by for all .

b. If no such exists, and for all .

Theorem 1.4.a suggests that robust estimation of a continuous linear functional is possible without imposing any strong conditions on the NPIV estimates. However, the condition that for some may be hard to verify. In fact, we conjecture that for a given function , it is not possible to empirically verify this condition.131313More precisely, we conjecture that given a function any test of the null hypothesis that there is no with has power no greater than size against any alternative.

2 Empirical Sensitivity Analysis

The results in Section 1 show that identification and estimation in NPIV models entails a trade-off. Strong a priori restrictions allow for identification and estimation that is somewhat robust to misspecification. However, if the true structural function violates these restrictions then it will not lie in the corresponding identified set and an estimator that imposes the conditions will be inconsistent, even if the NPIV moment condition holds.

To help researchers assess the robustness of their findings, and to better assess the trade-off between robustness and strong smoothness conditions, we present a method for empirical sensitivity analysis in NPIV models. Our procedure is based on estimation of the identified set under the weakened instrumental validity condition in Assumption and Assumption 1.2. We estimate the identified set for a range of bounds on the degree of misspecification and a range of smoothness restrictions. The approach is similar in spirit to Masten & Poirier, (2018) who analyze the sensitivity of treatment effect estimates to a small failure of unconfoundedness by weakening the assumptions used for point identification. More precisely, we estimate the identified set for linear functionals of . An important special case is the identified set for at some in the support of .

Note that our approach assesses the robustness of empirical findings to deviations from instrumental validity and weakened smoothness conditions, it does not assess the sensitivity of any particular NPIV estimator. In Appendix A3 we also provide a method to directly assess the finite-sample sensitivity of specific NPIV point-estimates to invalid instruments.

Let be the identified set as defined in (1.3). We only restrict the degree of misspecification and thus we take to be the whole space . Recall that the identified set for a linear functional is . Unlike in the previous section we do not restrict ourselves to only continuous linear functionals. Of particular interest is the identified set for the value of at a point , this is the set and corresponds to .

For the choices of and we consider, is an interval.141414See Proposition 2.1 in the Appendix B for a proof. Denote the lower and upper endpoints for the interval by and , for simplicity we suppress the subscript . We wish to estimate these end-points.

Assumption depends on the norm of the space and Assumption 1.2 on the choice of . We assume that these spaces are chosen so that the two assumptions can be written in terms of inequality constraints.

Assumption 2.1.

i. and is the sup norm. Thus Assumption states that if , then with probability :

| (2.1) |

ii. is the set of continuous bounded functions so that:

| (2.2) |

Where is a known linear functional from to , and is a known vector of functions.

Under Assumption 2.1 and are defined as follows:

Our statistical analysis applies for more general constraints than (2.1) and (2.2). We detail the more general framework in Appendix A2.

2.1 Calibrating

The bound in Assumption determines the size of the identified set. We suggest the researcher estimate the identified set for a range of choices for corresponding to mild, moderate, and severe misspecification. To determine whether corresponds to say, ‘mild’ misspecification, it is helpful to compare to an estimable reference quantity. This approach is common in the empirical sensitivity literature. For example, Masten & Poirier, (2018) compare the degree of selection on unobservables to selection on observables, which is estimable. See also Imbens, (2003), Altonji et al., (2005), and Oster, (2019).

We suggest calibrating of against the residual variation in the outcome. Consider the following decomposition:

In the context of Example 1 in Section 1, the first two terms on the right-hand side capture the additive indirect and direct effects of the instrument. The residual absorbs the effect of all other factors that influence . The variation in is a useful reference quantity against which to calibrate the bound on the magnitude of . We measure the variation using a difference in quantiles.

Let denote the quantile of . We say is small if it is equal to for a small . Suppose which corresponds to . In Example 1, this restricts the direct causal effect of the instrument to be less than twice the effect of shifting from its to its quantile. In our application we take , , and to correspond to mild, moderate, and severe misspecification respectively. Note that is a reduced-form residual and thus we can estimate and its quantiles in a first stage.

2.2 Set Estimation

To estimate and we must replace the optimization problems that define these quantities with feasible ones. Instead of optimizing over , we optimize over a finite-dimensional sieve space. We replace the conditional moment in (2.1) with a non-parametric estimate. Finally, we enforce the inequalities (2.1) and (2.2) only on finite grids.

Let be a length- column vector of basis functions on . In a first stage, we nonparametrically regress and on to obtain estimates and of and . Let and be finite grids in the supports of and . We replace the constraints (2.1) and (2.2) with:

| (2.3) | |||

| (2.4) |

Where be the -by- matrix whose column is where is the component of . Let be the column-vector whose entry is . The estimates of and are respectively:

These are linear programming problems with scalar parameters and constraints.

2.3 Consistency and Convergence Rates

A vector-valued function on a domain is of Hölder smoothness class with constant if and only if:

Let denote the largest integer less than . is of Hölder smoothness class with constant if and only if all the derivatives of each entry of of order weakly less than are uniformly bounded by and all the derivatives of order exactly are of Hölder smoothness class with constant . A function is Lipschitz continuous with constant if it is of Hölder smoothness class with constant .

Let and . Let .

Assumption 2.2.

implies for some , and for some , for all .

Assumption 2.3.

There is a sequence of positive scalars so that:

Assumption 2.4.

There is a sequence of positive scalars so that for any there exists with and:

Assumption 2.5.

i. , , and each row of are Lipschitz continuous with constant at most . ii. With probability approaching both and are Lipschitz continuous with constant at most . iii. , and .

Assumption 2.2 implies that is bounded and convex. Assumption 2.3 quantifies the estimation error in and . 2.4 quantifies the error from the replacing with a sieve space. Theorems 2.2 and 2.3 establish primitive conditions for Assumptions 2.3 and 2.4. Assumption 2.5 controls the error from the use of grids and .

Theorem 2.1.

Theorem 2.1 demonstrates the well-posedness of the set estimation problem. The first-stage rate is not premultiplied by some growing factor like a ‘sieve measure of ill-posedness’ (Blundell et al., (2007)).

and are small when the grids and are dense. and are independent of the grids, so if the grids grow dense quickly enough, the rates in the Theorem reduce to . This suggests the grids should be made as dense as computationally feasible.

If the dimension of the sieve space grows quickly then converges rapidly to zero. Theorem 2.2 establishes a rate that is independent of . This suggests that under the conditions of Theorem 2.2, should be made as large as is computational constraints allow.

We now provide primitive conditions for Assumption 2.3. Define series estimators and . Let be a length- column vector of basis functions on and define :

| (2.5) | ||||

| (2.6) |

In the Assumptions below is the smallest number of -balls of radius that can cover and is the dimension of .

Assumption 2.6.

i. The eigenvalues of are bounded uniformly above and away from zero. ii. is bounded and the distribution of given admits a conditional density so that , is of Hölder smoothness class with constant at most .

Assumption 2.7.

For any there is a sequence so that for any of Hölder smoothness class with constant :

ii. For all , . is Lipschitz continuous with constant . iii. . iv.

Assumption 2.8.

i. The function is of Hölder smoothness class . For , , , and . ii. , and for some function and .

Assumption 2.6.i is standard. Smoothness of the conditional density in 2.6.ii ensures that for any , is smooth. Assumptions 2.7.i and 2.7.ii. can be verified for common basis functions. 2.7.iii is a condition on the metric entropy of , such conditions are commonplace in the sieve estimation literature (see Chen, (2007)). Spaces of smooth functions like those used in our empirical application typically obey the condition (see Wainwright, (2019) Chapter 5). Assumption 2.7.iv allows us to apply Rudelson’s matrix law of large numbers (Rudelson, (1999)).

Assumption 2.8.i allows us to apply results from Belloni et al., (2015) to derive a convergence rate for . 2.8.ii can be verified for a given choice of basis functions, for example if , then the Assumption holds for the one-dimensional B-spline case in Section 3.

Theorem 2.2.

If the conditions of the theorem hold, then setting optimally Assumption 2.3 holds with .

Finally, we show Assumption 2.4 holds with for the setting in our empirical application.

Theorem 2.3.

Let contain functions that map from a closed interval to so that any is twice-differentiable with . Let be a vector of -order B-spline basis functions with knot points evenly spaced between . If , Assumption 2.4 holds with .

3 An Empirical Application

To demonstrate the usefulness of our methods we apply them to setting in Section 5.1 of Horowitz, (2011). Horowitz, (2011) estimates a shape-invariant Engel curve for food using data from the British Family Expenditure Survey.151515We made use of the data file that accompanies Horowitz, (2011) and adapted the accompanying code in order to evaluate Horowitz’s estimator and B-spline bases for our own methods. Horowitz’s application is in turn based on Blundell et al., (2007) who also carry out NPIV estimation of shape-invariant Engel curves and use the same data.

From Horowitz, (2011): “The data are 1655 household-level observations from the British Family Expenditure Survey. The households consist of married couples with an employed head-of-household between the ages of 25 and 55 years.”

Blundell et al., (2007) and Horowitz, (2011) aim to estimate ‘structural’ Engel curves. Suppose a researcher were to exogenously allocate to a household a particular budget for non-durable goods. A structural Engel curve measures the share of that budget the household would choose to allocate to a class of goods as a function of the budget size.

In observational settings, the share of household wealth allocated to nondurables is decided by the household. Therefore, the budget for nondurables depends on household preferences. These preferences also determine the allocation of the budget to classes of non-durable goods. Thus expenditure on non-durable goods is endogenous.

To tackle this problem Blundell et al., (2007) and Horowitz, (2011) use household income as an instrument for nondurables expenditure. There are many reasons to think that household income and preferences are correlated. Both tastes and income may depend on household size and socio-economic status, and those with expensive tastes may seek high-paying jobs. However, some shocks to household income may result from exogenous external factors like shocks to production costs in an employed householder’s firm. If one controls for a sufficiently rich set of household covariates this may absorb the endogenous variation in income leaving only the exogenous variation. If the data do not contain rich enough household observables, then some endogeneity likely remains and the income instrument is unlikely to be fully valid.

Blundell et al., (2007) and Horowitz, (2011) can only control for some coarse demographic variables.161616Both papers control for demographics by analyzing a homogeneous sub-sample. Blundell et al., (2007) incorporate additional dummy variable controls. Therefore, in this setting instrumental validity may not hold exactly and it is of interest to assess what empirical findings are robust to some failure of instrumental validity.

In this setting is the share of total expenditure on non-durables that a household spends on food. is the logarithm of the household’s total expenditure and is the logarithm of household income. We take to be the set of functions that map from to the unit interval and have second derivative bounded in magnitude by a constant . We present results for and , for comparison, the magnitude of the second derivatives of Horowitz’s estimated structural function never exceed .

Following Subsection 2.1 we set for different values of . is an estimate of and is calculated by taking empirical quantiles of . In particular we consider to correspond to mild, moderate, and severe misspecification. These values of correspond to .

Following Horowitz, (2011) we let be fourth-order (cubic) B-spline basis functions with evenly-spaced knot points.171717See de Boor, (2014) for a practical introduction to B-splines. We carry out our first-stage estimates using series regression onto cubic B-splines. Motivated by the results in Theorem 2.2 we set to be large, specifically we let . The grid consists of 100 evenly spaced points between the smallest and largest observed values of . The grid consists of 100 evenly spaced points between the and quantiles of .

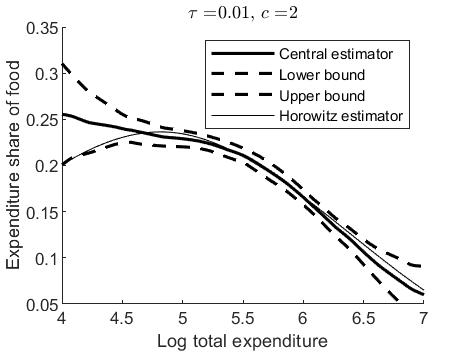

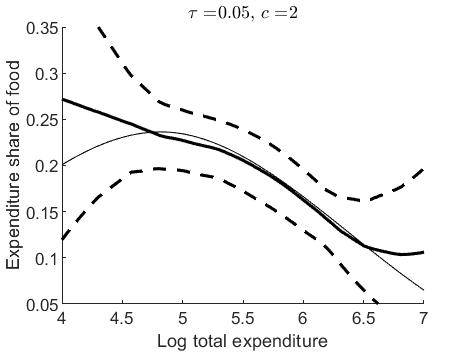

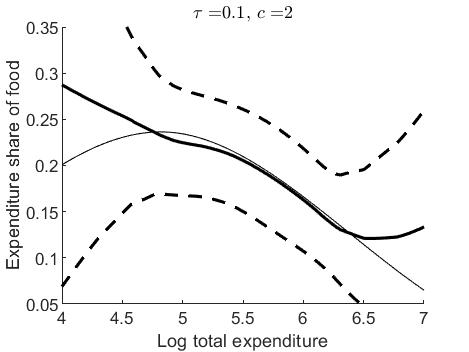

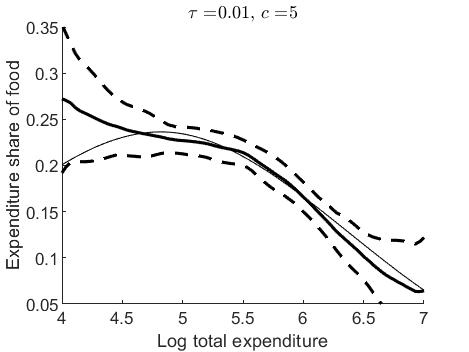

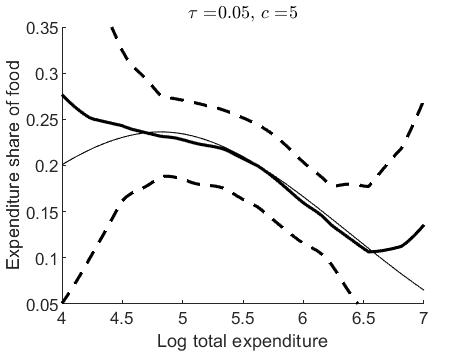

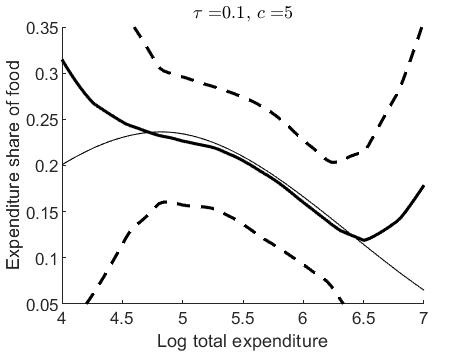

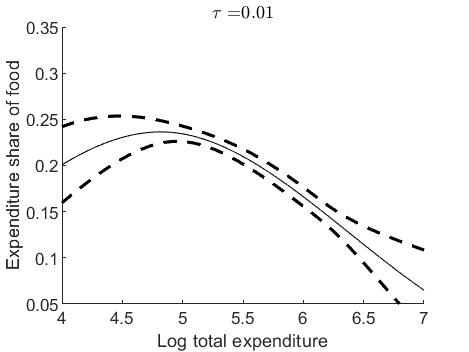

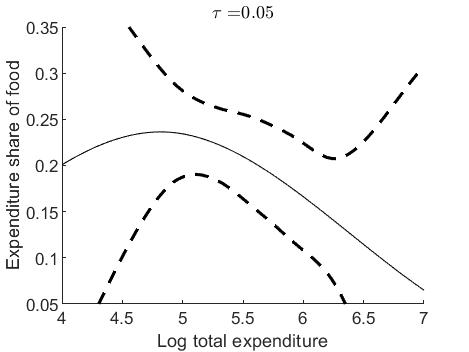

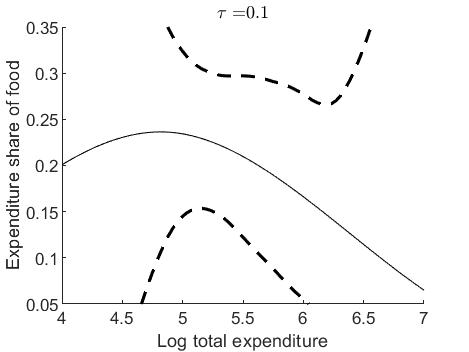

Figure 4.1 contains the results of our procedure. The figure contains six sub-figures each corresponding to a different set of values for and . The lower and upper dotted lines represent and , the upper and lower end points of the identified set for . The thick black line represents the half-way point between the end points, which is a point estimator with the smallest possible worst-case asymptotic bias under Assumptions and 1.2. The thin black line is the estimator from Horowitz, (2011).

Results for various and . Lower and upper dotted lines represent the end points of the identified set for for each . The thick black line is half-way between the dotted lines. The thin black line is the estimate in Horowitz, (2011).

The results in Section 1 suggest that if the bound on the second derivatives is loose then the identified set for will be large, even if (and hence ) is small. This is clear in Figure 4.1 which shows that for a given , the intervals are wider when than when .

Apart from in the severely misspecified case of (Sub-figures (c) and (f)), the figures suggest a general downward slope in the Engel curve for medium values of total expenditure. More precisely, the lower envelope at log-total expenditure of exceeds the upper envelope at , which implies the Engel curve has decreased between these two values. None of the results in Figure 4.1 provide evidence in favor of an upward sloping Engel curve for low values of total expenditure as found by Horowitz, (2011) and so we conclude then that this finding is not robust to even a mild failure of instrumental validity.

Conclusions

Our results show that identification and estimation in NPIV can be highly sensitive to misspecification, and that the sensitivity depends crucially upon the strength of a priori restrictions on the structural function. We develop a method for empirical sensitivity analysis in NPIV that allows researchers to better assess the relationship between the smoothness restrictions they impose and the robustness of their findings to misspecification.

We conjecture that our sensitivity results extend to a broader class of conditional moment restriction models. The non-robustness of NPIV estimators is tied to the ill-posedness of NPIV and a range of other nonparametric conditional moment restriction models are likewise ill-posed. It may be possible to adapt our empirical methods to these settings, although non-linearity of the conditional moment restriction would likely complicate estimation of the identified set. We leave these extensions for future work.

References

- Ai & Chen, (2003) Ai, Chunrong, & Chen, Xiaohong. 2003. Efficient estimation of models with conditional moment restrictions containing unknown functions. Econometrica, 71(6), 1795–1843.

- Ai & Chen, (2007) Ai, Chunrong, & Chen, Xiaohong. 2007. Estimation of possibly misspecified semiparametric conditional moment restriction models with different conditioning variables. Journal of Econometrics, 141, 5–43.

- Altonji et al., (2005) Altonji, Joseph G., Elder, Todd E., & Taber, Christopher R. 2005. Selection on Observed and Unobserved Variables: Assessing the Effectiveness of Catholic Schools. Journal of Political Economy, 113, 151–184.

- Andrews, (2017) Andrews, Donald WK. 2017. Examples of L2-complete and boundedly-complete distributions. Journal of Econometrics, 199(2), 213–220.

- Andrews et al., (2017) Andrews, Isaiah, Gentzkow, Matthew, & Shapiro, Jesse M. 2017. Measuring the Sensitivity of Parameter Estimates to Estimation Moments. The Quarterly Journal of Economics, 132, 1553–1592.

- Angrist et al., (1996) Angrist, Joshua, Imbens, Guido, & Rubin, D. B. 1996. Identification of Causal Effects Using Instrumental Variables. Journal of the American Statistical Association.

- Armstrong & Kolesar, (2018) Armstrong, Timothy B., & Kolesar, Michal. 2018. Sensitivity Analysis using Approximate Moment Condition Models. Cowles Foundation Discussion Papers.

- Belloni et al., (2015) Belloni, Alexandre, Chernozhukov, Victor, Chetverikov, Denis, & Kato, Kengo. 2015. Some new asymptotic theory for least squares series: Pointwise and uniform results. Journal of Econometrics, 186, 345–366.

- Blundell et al., (2007) Blundell, Richard, Chen, Xiaohong, & Kristensen, Dennis. 2007. Semi-nonparametric IV estimation of shape-invariant Engel curves. Econometrica. Journal of the Econometric Society, 75(6), 1613–1669.

- Bonhomme & Weidner, (2020) Bonhomme, Stéphane, & Weidner, Martin. 2020. Minimizing Sensitivity to Model Misspecification.

- Canay et al., (2013) Canay, Ivan A., Santos, Andres, & Shaikh, Azeem M. 2013. On the testability of identification in some nonparametric models with endogeneity. Econometrica. Journal of the Econometric Society, 81(6), 2535–2559.

- Chen, (2007) Chen, Xiaohong. 2007. Large Sample Sieve Estimation of Semi-nonparametric Models. The Handbook of Econometrics, JJ Heckman and EE Leamer (eds.), 6B.

- Chen & Christensen, (2018) Chen, Xiaohong, & Christensen, Timothy M. 2018. Optimal sup-norm rates and uniform inference on nonlinear functionals of nonparametric IV regression. Quantitative Economics, 9, 39–84.

- Chen & Pouzo, (2012) Chen, Xiaohong, & Pouzo, Demian. 2012. Estimation of Nonparametric Conditional Moment Models with Possibly Nonsmooth Generalized Residuals. Econometrica.

- Chen et al., (2014) Chen, Xiaohong, Chernozhukov, Victor, Lee, Sokbae, & Newey, Whitney K. 2014. Local Identification of Nonparametric and Semiparametric Models. Econometrica.

- Conley et al., (2008) Conley, Timothy G., Hansen, Christian B., McCulloch, Robert E., & Rossi, Peter E. 2008. A semi-parametric Bayesian approach to the instrumental variable problem. Journal of Econometrics, 144(1), 276–305.

- Darolles et al., (2011) Darolles, Serge, Fan, Yanqin, Florens, Jean-Pierre, & Renault, Eric. 2011. Nonparametric Instrumental Regression. Econometrica.

- de Boor, (2014) de Boor, Carl. 2014. (B)asic-Spline Basics.

- DeVore & Lorentz, (1993) DeVore, Ronald A., & Lorentz, George G. 1993. Constructive Approximation. Springer-Verlag.

- D’Haultfoeuille, (2011) D’Haultfoeuille, Xavier. 2011. On the completeness condition in nonparametric instrumental problems. Econometric Theory, 27(3), 460–471.

- Dudley, (1967) Dudley, R. M. 1967. The sizes of compact subsets of Hilbert space and continuity of Gaussian processes. Journal of Functional Analysis, 1, 290–330.

- Florens, (2011) Florens, Jean-Pierre. 2011. Non-parametric Models with Instrumental Variables.

- Freyberger, (2017) Freyberger, Joachim. 2017. On completeness and consistency in nonparametric instrumental variable models. Econometrica. Journal of the Econometric Society, 85(5), 1629–1644.

- Freyberger & Masten, (2019) Freyberger, Joachim, & Masten, Matthew A. 2019. A Practical Guide to Compact Infinite Dimensional Parameter Spaces. Econometric Reviews.

- Hall & Horowitz, (2005) Hall, Peter, & Horowitz, Joel L. 2005. Nonparametric methods for inference in the presence of instrumental variables. The Annals of Statistics, 33, 2904–2929.

- Horowitz, (2011) Horowitz, Joel L. 2011. Applied nonparametric instrumental variables estimation. Econometrica. Journal of the Econometric Society, 79(2), 347–394.

- Horowitz, (2012) Horowitz, Joel L. 2012. Specification testing in nonparametric instrumental variable estimation. Journal of Econometrics, 167, 383–396.

- Hu & Shiu, (2018) Hu, Yingyao, & Shiu, Ji-Liang. 2018. Nonparametric identification using instrumental variables: sufficient conditions for completeness. Econometric Theory, 34(3), 659–693.

- Huber, (2011) Huber, Peter J. 2011. Robust Statistics.

- Ichimura & Newey, (2017) Ichimura, Hidehiko, & Newey, Whitney K. 2017. The influence function of semiparametric estimators.

- Imbens, (2003) Imbens, Guido W. 2003. Sensitivity to Exogeneity Assumptions in Program Evaluation. American Economics Review, P&P, 93, 126–132.

- Kress, (2014) Kress, Rainer. 2014. Linear Integral Equations.

- Masten & Poirier, (2018) Masten, Matthew A., & Poirier, Alexandre. 2018. Identification of Treatment Effects under Conditional Partial Independence. Econometrica.

- Newey & Powell, (2003) Newey, Whitney K., & Powell, James L. 2003. Instrumental Variable Estimation of Nonparametric Models. Econometrica, 71, 1565–1578.

- Oster, (2019) Oster, Emily. 2019. Unobservable Selection and Coefficient Stability: Theory and Evidence. Journal of Business & Economic Statistics, 37, 187–204.

- Rudelson, (1999) Rudelson, M. 1999. Random Vectors in the Isotropic Position. Journal of Functional Analysis, 164, 60–72.

- Santos, (2012) Santos, Andres. 2012. Inference in nonparametric instrumental variables with partial identification. Econometrica. Journal of the Econometric Society, 80(1), 213–275.

- Severini & Tripathi, (2012) Severini, Thomas A., & Tripathi, Gautam. 2012. Efficiency bounds for estimating linear functionals of nonparametric regression models with endogenous regressors. Journal of Econometrics, 170, 491–498.

- Wainwright, (2019) Wainwright, Martin J. 2019. High-Dimensional Statistics: A Non-Asymptotic Viewpoint. Cambridge University Press.

Appendix A Additional Materials

A.1 Applying Theorem 1.2 to Specific Estimators

We can apply Theorem 1.2 to assess the sensitivity of a particular NPIV estimator. Key is to find a set that satisfies the conditions of the theorem. We can leverage existing asymptotic results for an NPIV estimator in order to find such a set. As an example, consider the estimator of Horowitz, (2011) (whose results we replicate in our empirical example). The estimator in Horowitz, (2011) is based on an estimator in Horowitz, (2012).181818While this appears to contradict the chronology, the 2011 paper cites an earlier pre-print of the 2012 paper. The estimators in Horowitz, (2011) and Horowitz, (2012) differ in an important respect. While the latter constrains the estimate to be inside a Sobolev ball of fixed radius, the former does not. Theorem 1.2 applies for the unconstrained Horowitz, (2011) estimator but not the estimator in Horowitz, (2012).

Consistency of the estimator in Horowitz, (2011) follows from results in Horowitz, (2012). Horowitz, (2012) provides conditions on so that the estimator is consistent whenever has Sobolev norm below some bound . Consistency is defined using the -norm ( is transformed to lie in the unit interval). The unconstrained estimator in Horowitz, (2011) does not depend on the specific level of and it appears in no other conditions, thus consistency only requires that has a finite Sobolev norm. Thus we can take to be the space of functions with a finite Sobolev norm, and this is dense in . So in this case is the entire space . Thus if contains an open ball at zero and assumptions 1.3-1.5 hold for , the worst-case bias of Horowitz’s estimator is infinite for all .

As a second example, Darolles et al., (2011) prove consistency of their estimator when is in a space of functions that obey a ‘source condition’ (their Assumption A.2). Under statistical completeness, is dense in and so is the whole space .

Chen & Christensen, (2018) study the supremum-norm consistency of a more general series two-stage least-squares estimator than Horowitz, (2011). They suggest a Sobolev ball for the parameter space . The radius of the ball is left unspecified and the formula for the series two-stage least-squares estimator does not depend on this radius. Thus if the estimator is supremum-norm consistent when lies in one particular ball, it is consistent when lies in any ball. The space of all functions with finite Sobolev norm is dense in the set of continuous bounded functions on a compact support. So if is compact we have equal to the whole space of continuous bounded functions.

A.2 Extensions to the Set Estimator

The results in Section 2 extend to a more general set estimation problem. For let be a vector of instruments and let and be known functions. We can replace the supremum norm constraint with a set of constraints:

| (A.1) |

The supremum norm constraint in Section 2 is a special case of the above in which and . To estimate of and with the constraints above, we replace the corresponding constraint in the feasible problem with:

Where and are first-stage nonparametric estimates of and , and is a finite subset of the support of . Theorem 2.0 in the appendix provides a rate of convergence for and in this more general set estimation problem. Theorem 2.1 is a special case of the more general theorem.

A.3 Direct Finite-Sample Sensitivity

Our set estimation method is designed to analyze the sensitivity of one’s empirical findings to misspecification. It is not based on any particular estimator. In this subsection we suggest a method to assess the finite-sample sensitivity of a particular NPIV estimator and apply the method to the empirical setting in Section 3.

Consider a linear NPIV estimator of the form where may depend on the instruments and endogenous regressors but not the outcomes . Many NPIV estimators take this form, for example those of Horowitz, (2011) and Darolles et al., (2011). We can decompose the estimator as follows:

Under correct specification for all and keeping all else fixed we would instead attain the estimate given by:

Suppose we assume that . Then with probability the interval below contains the value the estimator would take under correct specification. This interval is not conservative, for each point in the interval there is a function that satisfies the constraint so that is equal to that point.

A wide interval suggests that the presence of misspecification (of norm below ) can have a large effect on the the estimate. Note the width scales linearly with and at each point the width is determined by the factor which we can take as a measure of the sensitivity to misspecification.

Below we apply the method above to analyze the sensitivity of the specific estimator in Horowitz, (2011). The results are given in Figure A1 below. For these bounds are wider than those based on the identified set, even though the bounds do not account for any bias due to excessive Tikhonov regularization or the finite number of series terms used.191919The estimates in Horowitz, (2011) employ a small degree of Tikhonov regularization although the description of the estimator in the paper omits this. The maximum width of each interval is approximately times the corresponding value of (in each case is around twice the corresponding value of ). This demonstrates the substantial sensitivity of this estimator to misspecification.

Results for various . Lower and upper dotted lines represent the end points of the interval for for each as detailed in Subsection 2.3. The thin black line is the estimate in Horowitz, (2011).

Appendix B Proofs

B.1 Proofs of Results in Section 1

Lemma 1.1.

Suppose Assumption 1.4 holds. Then is a Banach space with the norm and is a compact infinite-dimensional linear operator from to .

Proof.

First we show that is a Banach space with the norm , that is, a linear space that is complete with respect to . Recall that contains all elements of that have mean zero. Let and . Note that and . Since is a Banach space and thus linear, , and by linearity of the mean . Thus and so is a linear space. To show is complete, let be a Cauchy sequence in . Since is Banach and thus complete, this sequence converges (in the norm ) to an element . By Assumption 1.5 the mapping of a function in to its mean is continuous, and so implies and since for all , we must have . Thus and so is complete.

Finally we show that is a compact operator from to . By definition a compact operator maps bounded sets into relatively compact sets. Assumption 1.4 states that is a compact operator between and . Since any bounded set in is also a bounded set in we get that is compact between to . ∎

Lemma 1.2.

Suppose Assumption 1.4 holds, there is an open -ball centered at zero in of radius , and an open -ball centered at an element in a set of radius . Then for any there exist functions , so that for , , , , and .

Proof.

From Lemma 1.1 is a Banach space and is a compact infinite-dimensional operator from to . Thus we can apply Theorem 15.4 (or 2.20) in Kress, (2014) to get that is unbounded and so:

| (B.1) |

Let be the operator norm of , this must be finite because is compact and therefore bounded (see Theorem 2.14 in Kress, (2014)). By (B.1) for any there exists an element of so that and . By linearity of and the elementary properties of norms we also have and .

Because we have and similarly . Since is dense in there exists an so that in which case, by the triangle inequality:

The inequality above implies that and therefore . Also by the definition of the operator norm and the triangle equality:

So in all , , , and . Applying the same reasoning with replaced by we see that there exists an with , and , and . Now that note that by the triangle inequality:

And similarly . Moreover, by the triangle inequality:

∎

Lemma 1.3.

Suppose Assumptions 1.3 and 1.4 hold. If is a compact subset of then:

Proof.

Since Assumption 1.3 holds, is injective. Denote the restriction of to by and its inverse by . It is well-known that a continuous and injective function defined on a compact set has a continuous inverse. So by compactness of , is continuous. Continuity of implies:

The final result follows because and coincide for . ∎

Lemma 1.4.

Suppose Assumptions 1.3-1.5 hold, there is an open -ball centered at zero in , and the set is such that is absolutely convex and infinite dimensional. Let and suppose there exists so that . Then:

Proof.

Assume the contrary, then for some there exists a finite scalar so that for any with :

By definition of the operator norm of , , . Assumption 1.3 implies that . And so for any with we must have:

Recall that there is an open -ball centered at zero in , call the radius of this ball . If and it follows that . Let , we get that for any with :

We have for some and is convex. So for any , in which case . Thus any can be written as for some and and . Therefore, for any :

Let be the closed ball in of radius . Let . We have already shown that for any , . By linearity of and properties of norms, for any we have that .

Let be the closure of . For any there is a sequence in so that . For all , , so by the triangle inequality and the definition of the operator norm:

is continuous so , and so since we get . Thus the inverse (which exists by Assumption 1.3) is bounded on .

Now, is absolutely convex which implies is a linear space and therefore so is . Because is infinite-dimensional and absolutely convex, is infinite-dimensional and likewise . It is well-known that a closed subset of a complete space is complete, is a closed subset of by construction and is a Banach space (see Lemma 1.1) and thus complete in the norm . Thus is an infinite-dimensional, complete linear space, i.e., an infinite-dimensional Banach space. But the inverse of a compact injective operator on an infinite-dimensional Banach space cannot be bounded (see Theorem 15.4 in Kress, (2014)), and so we have a contradiction. ∎

Proof of Theorem 1.1.

We begin with part a. Apply Lemma 1.2 with and the element of so that contains an open ball of radius centered at this element. We see that for any there exists , with and for , , and . Thus for , . Since we make arbitrarily small, it follows that the diameter of satisfies:

Now consider part b. First we show that . It is well known that a continuous function maps compact sets into compact sets. By Assumption 1.4 is compact and therefore continuous. Thus is compact. It is also well-known that a compact set in a Hausdorff space is closed, and so is closed. Suppose , then by closedness of there exists an open ball centered at that does not intersect , in which case for sufficiently small, there is no so that and so the identified set is empty for sufficiently small and holds trivially. So it remains to consider the case of and thus we assume this for the remainder of the theorem.

Now, given and is injective by Assumption 1.3, we have:

Where the first inequality follows by the triangle inequality, the second because the set is a subset of , and the final inequality by a reparameterization. Note that is defined so that if and only if .

Finally, since is compact, it follows that is compact. Thus we can apply Lemma 1.4 with and we get the result.

Now we show that . Since :

Applying Lemma 1.4 with and then gives the result. ∎

Proof of Theorem 1.2.

Applying Lemma 1.2 with , there exists an so that , , and . Fix , then and . By Assumption 1.3 is singleton which implies , therefore we have . Since can be made arbitrarily small we get:

By supposition is consistent for under Assumptions 1.1 and 1.2 whenever . Under Assumption 1.1, and under Assumption 1.2, is singleton and thus . Therefore whenever , we have . Now, by definition of , and so:

By the triangle inequality we get:

Recall that for an . Thus we have and so . From the above we then get:

Recall that and so:

Since our choice of satisfies and we have:

Since we can set arbitrarily small we get:

Using the definition of the worst-case asymptotic bias then gives the result. ∎

Proof of Theorem 1.3.

It is well-known that a continuous and injective function defined on a compact set has a continuous inverse. So by compactness of , the restriction of to is continuous. is continuous by assumption, and maps into . Hence is continuous. By continuity, for any :

Set in the above. Since we have . Reparameterizing in terms of and using we get:

Further restrictions on can only decrease the supremum and so:

| (B.2) |

Now, by the triangle inequality:

Since it follows that:

| (B.3) |

Substituting the above into (B.2) and using the definition of the worst case asymptotic bias gives the result.

For the second part of the theorem we apply Lemma 1.4 with and reparameterize and use to get:

Note that and implies and so . Substituting we get:

The supremum in the above must be smaller than the supremum without the constraint , and so we have:

Substituting (B.3) and using the definition of the worst-case bias then gives the result. ∎

Proof of Theorem 1.4.

Let us introduce notation. Let the and inner products be and respectively. The linear functional of interest can then be written as . The adjoint of the operator , denoted is given by .

First we prove the following:

| (B.4) |

If instruments are valid then and . So consistency under instrumental validity, implies that if then:

Let . Using :

And so:

Applying the definition of the worst-case asymptotic bias then gives (B.4).

Next we show that :

| (B.5) |

First we note that by the triangle inequality:

| (B.6) |

Given our choice of and the identified set is symmetric around , thus implies . So (using linearity of ) the lower bound is equal to

Using the respresentation of and our choice of and we have:

Reparameterizing we get:

And thus:

Now, given our choice of and , the upper bound in (B.6) can be written as:

Reparameterizing and using (B.6) we get:

Thus we have (B.5).

Now let us now prove claim a. Suppose that for some , , equivalently . Then for any :

Which simply equals . Suppose , by Cauchy-Schwartz:

We now prove claim b. Given (B.4) and (B.5) it is enough to show that for any :

Suppose that for some the worst-case asymptotic bias is finite. That is, there exists a scalar so that:

Linearity of and the inner-product then implies that for all :

Also by linearity, the LHS above equals:

Define the function by . Then:

By the Hahn-Banach theorem we can extend to a bounded linear function defined on the whole space which then satisfies:

Since is a bounded linear functional defined on a Hilbert space, by the Reisz representation theorem there exists an element so that for all , . And so for any :

Where the final equality follows by the definition of .

Since the equality above holds for all , for all we have (using bi-linearity of the inner product) . But we can set and the above implies that the norm of equals zero and so we have that . Or equivalently . ∎

B.2 Proofs of Results in Section 2

Proposition 2.1.

Under Assumption 2.1, for any linear operator , is an interval.

Proof.

The constraints (2.1) and (2.2) are clearly convex and therefore so is . Suppose , then with , and . Since is convex for any . is linear, so we then have . So is a convex subset of , i.e., an interval. ∎

Lemma 2.1.

For each let be a linear operator from a vector space to the space of functions from to and let be a function from to .202020 denote the set of natural numbers from to . Let be a linear operator that maps from to . Define:

And is the infimum subject the same constraints.

Consider some so that for some and all , ,. Suppose there exists and so that for each , , . Then .

Proof.

Define by . By the linearity of , for :

So satisfies the constraints in the problems for and , so we must have . Substituting the definition of and using linearity of we get:

Subtracting from both sides and then dividing by we get . Noting gives the conclusion. ∎

Lemma 2.2.

For each let be a linear operator from a vector space with norm to the space of functions from to , and let be a function from to . Let be a linear operator from to . Define:

And let be the infimum subject to the same constraints.

Consider a subset . Suppose: i. There exists so that for any , if , then there exists so that and . ii. For each the linear operators of the form for each have operator norm less than . iii. There exists and so that for each , , . iv. is a continuous linear operator with operator norm .

Under conditions i., ii., and iv., there exists so that for each , , .

Define by:

Under conditions i. ii., iii., and iv., .

Proof.

By conditions i. and iii. there exists an so that and for , for each . By ii., for any and all , . Therefore for , . By the triangle inequality and :

So the first claim of the lemma holds, now we prove the second claim. By definition of the supremum, for any there must be some that satisfies the constraints in the problem for and achieves . By the same reasoning used to establish the first claim there must exist a with and for , and for , . Let . Since is linear . Moreover, by linearity of we have get that for and for :

So satisfies the constraints of the problems for and so . Now, by iv., for any , . Therefore using the definition of :

And so . Since and satisfy the constraints of the problems for and , and , and recall so (using linearity of ) we get . Since this holds for any we get . Finally, note that the constraints of the problem for are stronger than those for (because ) so . ∎

Lemma 2.3.

For each let be a linear operator from a vector space to the space of functions from to . Let be a linear operator that maps from to . Define:

And let be the infimum subject to the same constraints. For each let be a finite subset of and define:

Suppose there exists and so that for each we have , . Suppose for each , is a subset of Euclidean space, is Lipschitz continuous with constant at most , and that if satisfies the constraints in the problem for then is Lipschitz continuous with constant at most . Then , where .

Proof.

By definition of the supremum, for any there must be some that satisfies the constraints in the problem for and achieves . By supposition is Lipschitz continuous with constant at most and likewise for . Thus is Lipschitz with constant at most . This implies:

We know that for all , so from the above we get that , . Applying Lemma 2.1 we then get which implies . Since this holds for any we get . Finally, the constraints in the problem for are weaker than for , so . ∎

Theorem 2.0.

Let be the space of real valued functions on the support of equipped with the supremum norm. Define and as follows:

Define estimates and by:

Suppose Assumptions 2.1.i, 2.2, and 2.4 hold, and for each Assumption 2.3 holds with replaced by , by , by , and by . Suppose for each , and are Lipschitz continuous with constant at most . Finally suppose there exists that satisfies the constraints of the problem for with slack , that is for all and for all . Then uniformly over all linear functionals with operator norm less than :

And likewise for .

Proof.

Define by:

| (B.7) |

By Assumption 2.3, . We suppose, until stated otherwise, that , by Assumptions 2.3 and 2.4 this holds with probability approaching . We also suppose that is sufficiently large that , this must be true for sufficiently large by Assumption 2.5.iii.

Define , and as follows:

And let and be the respective infima subject to the same constraints. By the triangle inequality:

| (B.8) |

We use Lemma 2.2 to bound . To apply Lemma 2.2 let equipped with the supremum norm and we take to be the functions of the form . For let , let , and , where denotes the component of a vector . Then Assumption 2.4 implies condition i. of Lemma 2.2 with . To establish condition ii., of Lemma 2.2, note that the linear operators of the form and have operator norm of unity because . So condition ii., of the lemma holds with . Conditions iii. of Lemma 2.2 holds be supposition and iv. with . The second statement of Lemma 2.2 gives:

| (B.9) |

Moreover, the first statement in Lemma 2.2 tells us there exists so that for each , for all . We will use this when we employ Lemma 2.1 below.

We now use Lemma 2.1 to bound . By definition of the supremum we can find a and that respectively satisfy the constraints of the problems for and so that and . Because they satisfy the constraints we have that . Recall and . Since we get from (B.7) that:

And similarly:

We established earlier that there exists with for each and (where and were defined above). Because we have , so we can apply Lemma 2.1 to get and so . Because this holds for each :

| (B.10) |

Now, again using (B.7) we get see that satisfies the constraints of the problem for with slack for each and . Moreover, since we get from (B.7) that:

Recall and so , then by Lemma 2.1 . Using and we get:

Again, this holds for each , and so . Since , adding to both sides and then dividing both sides by we get: . Combining with (B.10) and using that we get:

| (B.11) |

Where the final inequality holds because the constraints of the problems for and are stronger than those for and .

Next, we apply Lemma 2.3 to bound . By Assumption 2.5.i, is Lipschitz continuous with constant , and so the function is Lipschitz continuous with constant at most . Therefore:

It follows that:

By the definition of :

So if we must have:

Where we used that . By Assumption 2.2, for any that satisfies the constraints in the problem for we have , and so for any such , . By Assumption 2.5.i, each row of is Lipschitz with constant at most and so is Lipschitz with constant at most . In all, if satisfies the constraints for the problem for then is Lipschitz with constant at most . Further, by Assumption 2.5.i is Lipschitz continuous with constant at most . Note that both and are less than

Now, by Assumption 2.5.ii, , , , and are Lipschitz with constant at most . So if satisfies the constraints for the problem for then and are both Lipschitz with constant at most , and both and are Lipschitz with constant at most . Note that and are less than .

So applying Lemma 2.3 we get:

Now, recall that . We can apply the same reasoning to get . To see this note that we can just replace with in the problems for , , and and then , , and are the respective suprema of the new problems. Then by the triangle inequality:

Where the second inequality follows because the problems for and have weaker constraints than for and so . Combining:

Where the second inequality uses . Combining the above with (B.9), (B.11), and (B.8) we get:

Note that linearity and boundedness of and Assumption 2.2 imply that so we get:

Now, and are the respective suprema of the problems for and with replaced by , and so we can repeat the same steps that bound to get:

Finally, recall we derived the above under the assumption that . By Assumptions 2.3 and 2.4 this holds with probability approaching . Further, by Assumption 2.3 and by construction . So in all we get:

And likewise for . Since the above is based on an inequality that depends on only through , the convergence in probability above must is uniform over all that have the same constant . ∎

Theorem 2.1.

In this case so both are Lipschitz continuous with constant . The first statement of the theorem then follows immediately from Theorem 2.0. For the final statement of the theorem note that the evaluation functionals all have operator norm of unity, because . ∎

For the proofs below, we refer to a functional defined as follows. Let , then for each let be the least squares estimator defined by . If is singular we take to be zero (under Assumption 2.5.i this event happens with probability approaching zero).

Lemma 2.3.

Suppose Assumptions 2.1.ii, 2.2, 2.6 and 2.7 hold. Then:

Proof.

The proof follows some steps of Belloni et al., (2015) Lemma 4.2 with alterations to achieve uniformity over . Recall . By Assumption 2.6.i we can normalize and the assumptions still hold with sequences and (that satisfy Assumption 2.6) changed only by a factor independent of . We maintain this normalization throughout. Define by , , and . Then:

By Assumption 2.2, contains functions bounded by , so: