Duesenberry’s Theory of Consumption: Habit, Learning, and Ratcheting111We thank participants of the JAFEE-Columbia-NUS Conference, Tokyo, Japan, the Asian Finance Quantitative Finance Conference, Guangzhou, China and the Quantitative Methods in Finance Conference 2018 in Sydney for helpful and encouraging comments. We thank Philip Dybvig for his inspiring work and discussions which provided motivation for this work.

Abstract

This paper investigates the consumption and risk taking decision of an economic agent with partial irreversibility of consumption decision by formalizing the theory proposed by Duesenberry (1949). The optimal policies exhibit a type of the (s, S) policy: there are two wealth thresholds within which consumption stays constant. Consumption increases or decreases at the thresholds and after the adjustment new thresholds are set. The share of risky investment in the agent’s total investment is inversely U-shaped within the (s, S) band, which generates time-varying risk aversion that can fluctuate widely over time. This property can explain puzzles and questions on asset pricing and households’ portfolio choices, e.g., why aggregate consumption is so smooth whereas the high equity premium is high and the equity return has high volatility, why the risky share is so low whereas the estimated risk aversion by the micro-level data is small, and whether and when an increase in wealth has an impact on the risky share. Also, the partial irreversibility model can explain both the excess sensitivity and the excess smoothness of consumption.

JEL Classification Codes: D11, E21, G11

Keywords: Duesenberry, consumption, portfolio choice, adjustment costs, time-varying risk aversion, habit formation, permanent income hypothesis, excess sensitivity, excess smoothness

1 Introduction

This critique is based on a demonstration that two fundamental assumptions of aggregate demand theory are invalid. These assumptions are (1) that every individual’s consumption behaviour is independent of that of every other individual, and (2) that consumption relations are reversible in time (Duesenberry, 1949).

This paper analyzes a model of consumption and portfolio choice decision. Building on the second part of the quote by Duesenberry (1949) as a critique of the Keynesian consumption function, we aim to model the irreversibility of consumption decision. However, we are also aware that each consumption decision is not fully irreversible, but partially irreversible. Thus, we model the partial irreversibility by introducing proportional costs for each consumption adjustment. The partial irreversibility makes consumption a non-smooth function of wealth and change infrequently over time, demonstrating the excess sensitivity and the excess smoothness for moderate shocks. The risky share of the household is U-shaped, which can reconcile several conflicting views in the literature, regarding time-varying risk aversion and the impact of a wealth change on risky investments.

In our model, conditional on consumption never changing, the household has the von-Neuman Morgenstern preference such as the constant relative risk aversion (CRRA) preference. However, there is a utility cost proportional to the current level of marginal utility whenever the household increases or decreases the consumption level. The former is a learning cost in increasing the consumption level555For example, consider a household who lives in Chicago and goes for a vacation within the U.S. once per year. Suppose the family has a permanent increase in income and decides to visit Europe for a regular vacation from this year. Our assumption implies that the household incurs search or learning costs when preparing to visit a new place. We do not consider a monetary cost of search that should follow every consumption decision. Rather, our model assumes that there is one time utility cost of searching or learning the new consumption pattern when they increase the consumption level. and the latter represents consumption ratcheting. Note that the existence of the utility cost from decreasing consumption is important in our model since the model can generate all the properties derived in our model only with the cost of downward adjustment.666In addition, the cost of upward adjustment is usually very small in our calibration exercise. We can set it to be zero and generate the same resultf by slightly changing values of other variables.

The optimal polices exhibit a (s, S) type of policy as follows. Suppose the current consumption level is . Then, there are two wealth thresholds and , where and are constants, i.e., the current (s, S) band is interval . In this case, consumption increases and decreases if and only if the wealth level hits and , respectively. Otherwise, consumption stays constant inside the band. Once a boundary is reached, the new consumption level, is set and the next new (s, S) band is updated as . The adjustment is made whenever there is a change in consumption. We describe how each new consumption level is determined in more detail in the main body of the paper.

The optimal risky share is U-shaped in wealth for each (s, S) band. The risky asset holdings consist of two components: the myopic component and the hedging component. Noticing the minus sign in this decomposition, the hedging demand takes zero at the boundaries of each (s, S) interval and the maximum value inside the interval. The reason is to avoid a high utility cost that would be incurred if the household frequently adjusted its consumption. Therefore, the risky share is U-shaped with the maximum at the one of the boundaries, the minimum somewhere inside the interval. On the other hand, naturally there is heterogeneity among households in utility costs as well as risk aversion. Naturally arises the question of how to infer risk aversion of a certain household. We define RCRRA (revealed coefficient of relative risk aversion) by risk aversion inferred by the outsider observing the risky asset holdings of a household over time. Since the risky share is time-varying, the RCRRA is time-varying. Moreover, the RCRRA is inverse U-shaped inside the (s, S) boundary since the risky share is U-shaped.

Having the above properties in mind, our model can explain a number of interesting implications for the household consumption and risky investment decisions. First, our model can fill a gap between different views on risk aversion in the literature on decision theory, structural estimation, behavioral, and asset pricing. Note that most asset pricing models use the relative risk aversion coefficient of around 10 or higher for calibration exercises to match asset pricing moments (e.g., Bansal et al. (2012), Cocco et al. (2005), and references therein777There are many other asset pricing models to suggest even much higher value than 10. For example, Kandel and Stambaugh (1991) argues .). Along the similar lines, households usually hold in equity (conditional on participation, up to 40 %), which implies relative risk aversion is at least 10 or larger following calibration according to the standard models with widely accepted market parameter values. On the contrary, the estimated individual relative risk aversion takes values between 0.7 and 2 in decision theory, structural estimation, or behavioral literature such as Bombardini and Trebbi (2012), Campo et al. (2011), Chetty (2006), Gandelman and Hernández-Murillo (2013, 2015), Hansen and Singleton (1982), Layard, Mayraz, and Nickel (2008), and Szpiro (1986), among which more recent ones tend to claim that risk aversion is less than 1 or around 1.

We show that time-varying risk aversion, i.e., RCRRA in our model is the same as actual risk aversion only when the wealth process hits either one of (s, S) boundaries. The set of these events, however, has measure zero for any stock price sample path. The RCRRA is greater than actual risk aversion for most of times. We note that the maximum value of RCRRA increases with the consumption adjustment costs (RCRRA is always equal to risk aversion if there is no such cost). We show that the RCRRA takes fairly high values closer to its maximum than actual risk aversion during the times when the wealth process stays in the middle range of the (s, S) band and does not have high fluctuation: These are times when the market is neither bullish nor bearish, rather has small volatility for a while. This feature is in sharp contrast with that from traditional habit models since risk aversion in the habit models becomes higher only in downturns. For example, Otrok et al. (2002) show that the size of equity premium in the traditional habit model is determined by a relatively insignificant amount of high-frequency volatility in US aggregate consumption. Moderate shocks have occurred in the world financial markets over substantial time periods when the RCRRA takes high values in our model. Therefore, our model can generate the average value of RCRRA consistent with that often used in the asset pricing literature, while the coefficient of relative risk aversion is close to that suggested by the behavioral or experimental literature.

Second, but more important is that the U-shaped risky share resulted from our model has an interesting implication for the effect of the change of wealth on the risky share on which the empirical literature looks inclusive. For example, Calvet et al. (2009) and Calvet and Sodini (2014) favor habit, commitment, or DARA (decreasing relative risk aversion) models predicting that the impact is positive, i.e., the risky share increases with an increase in financial wealth. Brunnermeier and Nagel (2008) and Chiappori and Paiella (2011), however, show no relationship (or slightly positive relationship, if any) between the financial (liquid) wealth change and the risky share. We argue that both can happen depending on which time-series is chosen. The U-shape implies that the risky share is decreasing in wealth in the left side of (s, S) band and increasing in wealth in the right side of (s, S) band (see Figure 10). The optimal wealth process tends to stay longer in the increasing (decreasing) regions of each (s, S) interval over time if the market is such that good shocks are more frequent than bad shocks (see Figure 3 and its description). Thus, if good shocks occurred more frequently in the stock market during the data period, the relationship tends to be positive. By using this intuition, we simulate four types of sample paths: (a) bullish, (b) intermediate, (c) bearish, and (d) highly fluctuating. Then, we regress the change of risky share on the change of financial wealth within each sample. For cases (a) and (b), we find a significant positive impact of the wealth increase on the risky share. Moreover, we find no or slightly negative relationship for cases (c) and (d). Thus, our model can reconcile the discrepancy in the empirical literature.

Third, the optimal consumption process in our model features two well-documented empirical regularities: the excess smoothness (Deaton, 1987) and the excess sensitivity (Flavin, 1981). First, consumption tends not to respond to a permanent shock as long as the shock does not push up or down the wealth level to one of the (s, S) boundaries, which implies the excess smoothness. Second, suppose there is a good shock in the permanent income. While this shock may not increase the current consumption level, it increases the probability that consumption will increase in the future, by which the excess sensitivity of consumption appears in our model. By the same reason, however, both the excess smoothness and the excess sensitivity vanish for a large shock that immediately pushes the wealth process up or down to either of the (s, S) boundaries. In other words, the partial irreversibility of consumption in our model implies that consumption responds to a large shock consistent with the permanent income hypothesis (Jappelli and Pistaferri (2010)).

Fourth, we explore asset pricing implications and find that our partial reversibility model has a potential to well the U.S. data well. We follow Constantinides (1990) and Marshall and Parekh (1999), simulate optimal consumption of individuals, and obtain a simulated series of monthly aggregate consumption. We compute several moments such as the consumption growth rate, the standard deviation of marginal rate of intertemporal substitution, and the autocorrelation of consumption growth rate. We find that our model matches better the US data than the traditional habit models.

Finally, our paper also makes a theoretical contribution to the literature of dynamic optimization. We first transform the dynamic consumption and portfolio selection problem into a static one, and then derive the dual Lagrangian problem. The advantage of solving the dual Lagrangian problem is that we do not need to consider the portfolio choice and we are left to analyze two sided singular control problem (of consumption). After each adjustment of consumption, the problem is to decide whether to increase or to decrease consumption and if so, how much to change. Then, the original value function is obtained from the convex duality relation. We characterize the full analytic solution. The optimal portfolio can be derived from the dual value function by the convex duality and Itó’s lemma. The detail for each step is presented in the appendix.

1.1 Literature Review

Our paper is motivated from Duesenberry (1949). On one hand, the first part of his critique quoted in the beginning of our introduction is closely related to external habit formation and thus has significantly contributed to developing the modern habit models such as Abel (1990), Constantinides (1990), and Campbell and Cochrane (1999). Some of our results resemble those from habit model. For example, our model generates time-varying risk aversion. However, ours are fundamentally different from habit models in that the agent in habit models becomes more conservative when the current consumption level gets closer to the habit stock (e.g., in downturns) while RCRRA in our model becomes higher in times when the stock market is neither bullish nor bearis, but rather flat and has low volatility. On the other hand, there is a handful of previous literature that grew out from the second part of the critique such as Dybvig (1995) and Jeon et al. (2018).888Note that the second part of critique is well described as follows: At any moment a consumer already has a well-established set of consumption habits… Suppose a man suffers a 50 per cent reduction in his income and expects this reduction to be permanent. Immediately after the change he will tend to act in the same way as before… In retrospect he will regret some of his expenditures. In the ensuing periods the same stimuli as before will arise, but eventually he will learn to reject some expenditures and respond by buying cheap substitutes for the goods formerly purchased (Dusenberry 1949, p. 24). However, Dybvig (1995) and Jeon et al. (2018) assume that consumption decision is fully irreversible (other than allowing a predetermined depreciation). Therefore, they are an extreme special case of our model.999More precisely, Dybvig (1995) and Jeon et al. (2018) assume that consumption is not allowed to decrease. The model converges to those of Dybvig (1995) and Jeon et al. (2018) if the cost of decreasing consumption goes to infinite and the cost of increasing consumption is equal to zero in our model. We better formulate the ratchet effect with partial irreversibility by allowing costly downward adjustment, which generates the U-shape risky share and its novel implications that Dybvig (1995) and Jeon et al. (2018) do not.

Our model is also related to dynamic consumption and investment models with durable consumption or consumption commitment such as Grossman and Laroque (1990), Hindy and Huang (1992, 1993), Hindy et al. (1997), Flavin and Nakagawa (2008), and Chetty and Szeidl (2007, 2016). We view our model as complement to the consumption commitment literature. For example, Chetty and Szeidl (2016) show in the commitment model that the excess smoothness and excess sensitivity arise for moderate shocks and they vanish for large shocks. The same result holds from a different channel in our model, namely through learning or adjustment costs. In our model there exist two different adjustment costs, downward and upward adjustment costs. Thus magnitude of large shocks which make immediate adjustment and individuals aggressive in risk taking is in general different for good shock and for bad shocks. This paves a way for empirical test whether the effects of large shock on consumption and risk taking are different for these two different shocks. Furthermore, our model generalizes the models of consumption and portfolio selection with durability and local substitution by Hindy and Huang (1992) and Hindy et al. (1997) via the isomorphism discovered by Schroder and Skiadas (2002).

2 Model

We consider a simple and standard continuous-time financial market. The financial market consists of two assets: a riskless asset and a risky asset. We assume that the risk-free rate, the rate of return on the riskless asset, is constant and equal to . The price of the risky asset or the market Index evolves as follows:

where are constants, , and is a Brownian motion on a standard probability space 101010See Karatzas and Shreve (1998) for details of mathematics and the probability theory. endowed with an augmented filtration generated by the Brownian motion .

The agent’s wealth process evolves according to the following dynamics:

| (1) |

where and are the consumption rate and the dollar amount invested in the risky asset, respectively, at time .

For non-negative constants and , the agent’s utility function is given by

| (2) |

where is the subjective discount rate and is a twice-continuously differentiable, strictly concave, and strictly increasing function. We decompose

where and are non-decreasing processes. This decomposition is well-defined if the consumption process is admissible (See Definition 2.1 and equation (4)). (2) implies that the agent instantaneously loses the or unit of utility whenever there is one unit increase or decrease in the marginal utility. The example of the first kind is the utility cost of learning how to spend and that of the second is the point made by models with “catching up with Joneses” such as Abel (1990), Constantinides (1990), Gali (1994) and Campbell and Cochrane (1999).

In this paper, we assume the constant relative risk aversion(CRRA) utility function:

| (3) |

where is the agent’s risk coefficient of relative risk aversion.

To define the strategy set, we denote by the family of all cáglád, -adapted, non-decreasing process with starting at and assume that there exist such that the agent’s consumption can be expressed by

| (4) |

where is the agent’s initial consumption rate. Then, the agent’s objective (2) is rewritten as

| (5) |

We define the set of consumption and risky investment strategies as follows.

Definition 2.1.

We call a consumption-portfolio plans admissible if

-

(a)

A consumption strategy satisfies

(6) We denote by the class of all consumption strategies satisfying the condition (6).

-

(b)

For all , is measurable process with repsect to satisfying

(7) -

(c)

For all , the wealth process is non-negative, i.e.,

(8)

The following assumption should be satisfied in order to guarantee the existence of the special case of , i.e., the classical Merton problem.

Assumption 1.

If the agent instantaneously increases her consumption by a small amount, from to between and , the intertemporal utility gain from the additional consumption is On the other hand, the utility loss from the consumption increase is . The gain should be greater than the loss. Otherwise, the agent will never increase consumption in our model. This observation leads to the following assumption.

Assumption 2.

There is no parameter restriction for . The problem studied by Dybvig (1995) is an extreme case of ours. Dybvig (1995) consider the case when and , which means there is no utility cost of increasing consumption and infinity utility loss from decreasing consumption (i.e., ratcheting of consumption).

Now we state the problem as follows.

Problem 1 (Primal Problem (Dynamic Version)).

Given and , we consider the following utility maximization problem:

| (9) |

where the supremum is taken over all admissible consumption/portfolio plans subject to the wealth process (1).

Note that Problem 1 is subject to the dynamics budget constraint (1). In Section 3.1, we first transform Problem 1 into a static problem (Problem 2) by the well-known method of linearizing the budget constraint suggested by Karatzas et al. (1987) and Cox and Huang (1989). Finally we transform that static problem to a singular control problem (Problem 3). Theorem 3.1 shows that the solution to Problem 1 is recovered from the solution to Problem 3 by the duality relationship. We will obtain the solution to Problem 3 and characterize optimal policies by using it in later sections. Note that the advantages of dealing with the singular control problem in Problem 3 are described right below the problem statement.

3 Solution Analysis

3.1 The Problem Reformulation

In order to reformulate Problem 1, first we transform the wealth process satisfying (1) into a static budget constraint. For this purpose we define, for ,

Let us define an equivalent measure by setting

| (10) |

so that the process is a standard Brownian motion under the measure . Then, the wealth process (1) is changed by

| (11) |

Applying Fatou’s lemma and Bayes’ rule to , we get the following static budget constraint:

| (12) |

where is the initial wealth level, i.e., . Then, we restate Problem 1 as the following problem.

Problem 2 (Primal Problem (Static Version)).

Given and , we consider the following utility maximization problem:

| (13) |

where the supremum is taken over all admissible consumption/portfolio plans subject to the static budget constraint (12).

By following Cox and Huang (1989) and Karatzas et al. (1987), it is easy to see that the solution to Problem 1 is the same as that to Problem 2. Thus, henceforth the both problems are called the primal problem in this paper.

Using the static budget constraint (12), we consider the following Lagrangian:

| (14) |

where is the Lagrange multiplier for the budget constraint. We define the process

which plays the role of the Lagrange multiplier for the budget constraint at time , and thus represents the marginal utility(shadow price) of wealth process. We will describe how the marginal utility of wealth process is related to the agent’s optimal consumption policy.

Problem 3 (Dual problem).

Problem 3 is the optimization problem with singular controls over . There are two advantages in dealing with the dual problem. The first advantage is that we do not need to consider the portfolio choice. This property is, in fact, inherited from the formulation of Problem 2. The second advantage is that now the agent’s problem becomes a singular control problem of deciding either to increase or decrease the level of consumption given the current consumption . Therefore, we can apply a standard method of singular control problem developed by Davis and Norman (1990) or Fleming and Soner (2006).

3.2 Solution: Dual Value Function

The dual value function satisfies the following Hamilton-Jacobi-Bellman(HJB) equation:

| (16) |

where and the differential operator is given by

To solve the HJB equation (16), we define the increasing region IR, the decreasing region DR and the non-adjustment region NR as follows:

| (17) |

In what follows in this subsection we describe the explicit form of the dual value function in each region. First, as shown in Appendix A, the regions IR, NR and DR are rewritten by

respectively. See Figure 1 for the graphical representation of each region. It is important to characterize IR-, NR- and DR-regions in order to understand the optimal strategies, which will be investigated in great detail in Section 3.3. Here, and are given by

with . and are positive and negative roots of following quadratic equation:

Moreover, is a unique solution to the equation in , where

| (18) |

In the following proposition, we provide a solution to Problem 3.

Proposition 3.1.

Proof.

The proof is given in Appendix A. ∎

Finally we summarize the duality relationship between the value function of the primal problem and the dual value function of Problem 3 in the following theorem.

Theorem 3.1.

Proof.

The proof is given in Appendix B. ∎

3.3 Optimal strategies

Refer Figure 1 for the graphical representation of the optimal consumption behavior. If the initial consumption level is such that lies in the increasing region IR or the decreasing region DR, it jumps immediately to the non-adjustment region NR. Suppose the level of consumption is such that lies inside the NR-region. The level of consumption stays constant during the time -process lies inside the NR-region. Consumption jumps down if and only if process hits and it jumps up if and only if hits . In this case, the question is how much the consumption level jumps up or down. Proposition 3.2 explicitly characterizes the amount of the jump at each time when there is a consumption adjustment.

Proposition 3.2.

The optimal consumption for is given by

where and is the unique solution to the minimization problem (20) and

| (21) |

Proof.

The proof is given in Appendix C. ∎

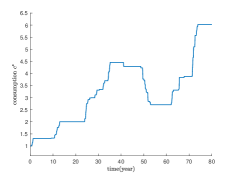

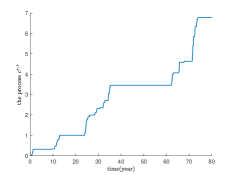

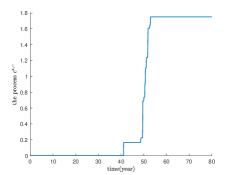

Processes and are non-decreasing regulators such that lies inside the -region. and stay mostly constant. Consumption increases whenever increases, but consumption decreases whenever increases. More precisely, as seen in Figure 1, the process stays constant within the non-adjustment region NR and increases if and only if hits the free boundary . Similarly, the process also stays constant within the non-adjustment region NR. increases if and only if hits the free boundary . Figure 2 plots sample paths of and together with those of and . See Figure 2 for simulated paths of , , , and .

Proposition 3.2 describes the consumption path according to the ratio of the shadow price of wealth to the marginal utility process. Then, how is the consumption process related to the agent’s wealth process? The following theorem provides the answer to this question.

Theorem 3.2.

Pick an arbitrary time and let be the optimal consumption at for some constant . For , the optimal consumption is fixed as during the time in which is inside the region (by Proposition 3.2). In this case, the optimal wealth process follows

| (22) |

In addition, there exist two positive numbers and such that for if and only if

| (23) |

The explicit forms of and are given in the proof.

Proof.

The proof is given in Appendix D. ∎

Suppose is the optimal consumption level at a certain time as in Theorem 3.2. Equation (22) explicitly describes the optimal wealth process during the times when the shadow value of wealth, -process stays inside the -region for .

The consumption level increases according to the first equation in (21) if and only if hits the lower threshold or touches the -region. The latter part of Theorem 3.2 tells that this condition is equivalent to the case when hits the upper threshold . Conversely, the consumption level decreases according to the second equation in (21) if and only if hits the upper threshold or touches the -region. This condition is equivalent to the case when hits the lower threshold .

The optimal consumption policy looks like a (s, S) policy over wealth. Note that the two threshold levels and depend on the market parameter values and ). Equation (23) implies that for a given consumption at a certain point of time, the thresholds are and . Once the agent’s wealth reaches either one of two thresholds of wealth, the new consumption level is determined by (21). Then, the two new thresholds levels are set as and .

Figure 3 describes a discrete-time version of the wealth and consumption movement. Assume that current wealth is and consumption is . Initially the wealth process lies in interval . Suppose hits (point ) after several good shocks. Then, a new consumption level is set as and the new (s, S) band is interval . At this instant, the wealth level is at point . If a positive shock arrives again at point , a new consumption level is immediately set as and the new (s, S) band is interval . If a negative shock arrives at point , however, moves inside and the consumption level stays at until hits either (point ) or (point ).

On the contrary, let us go back to the time when the wealth process lies in interval . Suppose hits (point ) after several bad shocks. Then, a new consumption level is set as and the new (s, S) band is interval . At this instant, the wealth level is at point . If a negative shock arrives again at point , a new consumption level is immediately set as and the new (s, S) band is interval . If a positive shock arrives at at point , however, moves inside and the consumption level stays at until hits either (point ) or (point ).

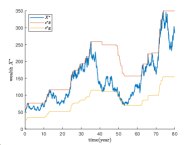

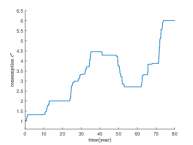

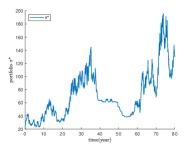

Now let us turn to the optimal risky investment, which is given in Proposition 3.3 below. The explicit form of the optimal portfolio in is easily obtained by applying Ito’s lemma to the optimal wealth process in (22) and drawing out the corresponding term. Figure 4 shows a simulated path of and plots its corresponding consumption and risky portfolio. Notice from the figure that the number of portfolio rebalances is far more than the number of consumption adjustment over time. In other words, the household keeps rebalancing risky stock holdings within the (s, S) band while consumption is adjusted only at the boundary.

Proposition 3.3.

Let be the optimal consumption level at time for some constant . The optimal portfolio is given by

| (24) |

for before the next consumption adjustment happens.

Proof.

The proof is given in Appendix E. ∎

Based on the classical portfolio selection results, we can easily see that the optimal risky portfolio in Equation (24) in Proposition 3.3 (a) will be decomposed as follows:

| (25) |

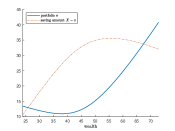

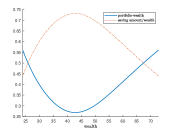

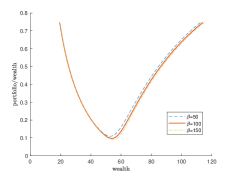

The first term is a myopic term and the remaining term is a hedging term. Note the minus sign in front of the second term. Intuitively, the second term in (25) is the demand that crows out the myopic demand, in order to maintain the current consumption level since frequent changes of the consumption level incur high utility cost. In this sense, the second term itself is positive. As seen in Panel (b) of Figure 5, the risky share is U-shaped and the ratio of the hedging demand takes the largest value at the certain point inside the (s, S) band at which the total risky share takes the minimum value, which generates interesting implications. We will discuss the implications of the U-shaped risky share over time in Section 4 (e).

While decomposition (25) is intuitive, putting (24) into (25) is complicated and thus it is not much informative. In order to better understand risky investment pattern, we define the revealed coefficient of relative risk aversion (RCRRA) as follows:

| (26) |

The RCRRA is the level of relative risk aversion inferred from the agent’s portfolio allocation at time by outsiders who does not know the agent’s actual risk aversion. If the agent is unconstrained (, i.e., the Merton case), the RCRRA is always the same as the agent’s true relative risk aversion . However, in general RCRRA is time-varying. In fact, it has maximum and minimum values as shown in Theorem 3.3. The next theorem provides the properties of RCRRA and confirms the above intuition regarding the hedging demand.

Theorem 3.3.

-

(a)

for all .

-

(b)

Pick any . Consider the wealth process for , where is the optimal consumption level at time for some constant . Then, RCRRA approaches as approaches either or . Moreover, there exist such that RCRRA attains the maximum at . RCRRA decreases in wealth for and increases in wealth for .

Proof.

The proof is given in Appendix F. ∎

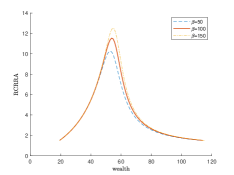

Panle (c) of Figure 5 plots a typical RCRRA as a function of wealth. RCRRA is hump-shaped, which is opposite to the U-shaped risky share in Panel (b). It attains the minimum value at the two ends of interval and the maximum value at . As described in Theorem 3.3(b), RCRRA increases in wealth when the wealth level is smaller than and it decreases in wealth when the wealth level is greater than .

4 Risk Attitude and Risky Share

This section investigate the properties of the optimal risky investment policy obtained in Section 3.3 in detail.

4.1 The consumption partial irreversibility model can explain the puzzle why the risky share of households is low

A puzzle in the classical dynamic portfolio selection literature is that while households usually hold in equity (conditional on participation, up to 40%), standard models predicts much higher values. For example, see the first row of Table 1 that is the Merton case with CRRA preference with about risk premium and volatility. The risky share is fairly high such as 124% and 75% when and , respectively, while these values fall into the reasonable range of risk aversion estimated by the recent literature (see the first paragraph of Section 4.2).

| 124% | 75% | 32% | 19% | 11% | |

| 100% – 124% | 55% – 75% | 24% – 32% | 11% – 19% | 9% – 11% | |

| 48% – 124% | 27% – 75% | 14% – 32% | 9% – 19% | 6% – 11% | |

| 15% – 124% | 9% – 75% | 6% – 32% | 4% – 19% | 2% – 11% |

The optimal risky share in our case is not constant, but is U-shaped (or V-shaped) (see Panel (b) in Figure 5 or Panels (b) and (d) in Figure 6). The maximum value of the ratio of risky asset holdings is the same as that of the Merton case only when the wealth process hits the boundary. But, it is a measure zero event in a sample path. In most of times, the risky share is strictly smaller as seen in Figure 5(b). As we will discuss in Section 4.4, the ratio of risky asset holdings tends to be close to the minimum levels in times when there are moderate shocks and the wealth fluctuation is also moderate (equivalently, the RCRRA tends to be high for those times). For example, a household with and may keep the risky share close to 9% for a long time if only moderate good and bad shocks alternates in the market for the same period time. The ratio gradually increases as the wealth process gradually increases since the equity premium is positive. However, as mentioned before, 75% ratio happens fairly infrequently and the ratio should be much lower than 75% for most of times. This means that the utility cost model can generate the household portfolio holdings consistent with the data from a plausible level of risk aversion (on which will be discussed in Section 4.2 below).

4.2 Time-varying risk attitude in our model can reconcile the gap among the risk aversion parameter values widely used in different literature

There is a vast literature on measuring risk aversion. The most widely accepted values are between 0.7 and 2. More recent literature tends to argue that risk aversion is close to 1 or even less than 1 (For example, see Chetty (2006), Layard, Mayraz, and Nickel (2008), Bombardini and Trebbi (2012), and Gandelman and Hernández-Murillo (2015)).

| Actual Risk aversion | |||||

|---|---|---|---|---|---|

| (, ) | (40,10000) | (40,6000) | (40,4500) | (40,3200) | (40, 2200) |

| (, ) | (45,5000) | (45,3000) | (45,2200) | (45,1500) | (45, 1100) |

| (, ) | (49,1000) | (49,500) | (49,400) | (49,260) | (49, 180) |

However, most of asset pricing literature takes the level of risk aversion as about 10 or higher for the calibration analysis (e.g., Bansal et al. (2012), and Cocco et al. (2005)). If we consider the investment aspect of these asset pricing models, it is related to the point made in Section 4.1 in the sense that results in the risky share consistent with the empirical observation for households’ stock holdings (see the column for when in Table 1).

In summary, the estimated results directly tell that risk aversion is small around unity while the calibration exercise in asset pricing indicates that the plausible level of risk aversion should be much higher. Our model can reconcile the gap in these two lines of literature. Table 2 shows our numerical exercises. It calibrates values that generate 13 as the maximum RCRRA for each risk aversion around unity with other widely accepted market parameter values given in the table.

Note that the conventional habit model can also generate time-varying risk aversion. However, it requires to define a internal or external habit stock process, which are usually ad hoc. Our model can perform a precise calibration analysis that can fit the maximum and minimum values of risk aversion.

4.3 RCRRA can be very large while actual risk aversion is small

| (, ) | ||||

|---|---|---|---|---|

| (5, 10) | 1.116 | 1.164 | 1.208 | 1.249 |

| (5, 100) | 1.782 | 1.974 | 2.164 | 2.358 |

| (29, 100) | 2.502 | 2.866 | 3.250 | 3.668 |

| (49, 100) | 7.459 | 9.607 | 12.40 | 16.07 |

| (49, 1000) | 13.18 | 18.48 | 26.20 | 37.46 |

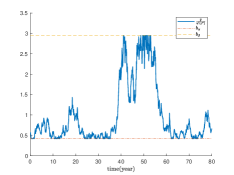

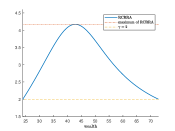

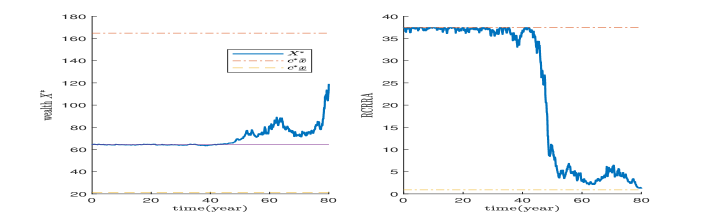

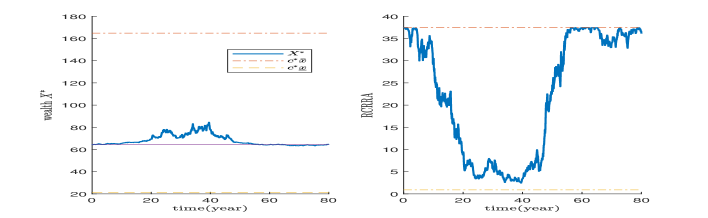

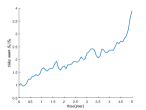

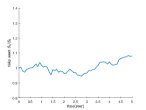

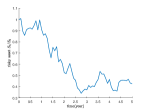

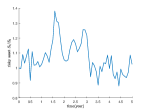

In Figure 5(c), the actual risk aversion is and the maximum value of RCRRA is about 5.32. This difference does not seem large. However, the difference between the actual level of risk aversion and the RCRRA value can be dramatically large. Figures 7 and 8 plot a sample path of RCRRA. While the actual risk aversion level is in these figures, RCRRA can take more than 38. The optimal wealth path touches neither nor (See the left panel in each figure), which means that the consumption path stays constant in Figures 7 and 8.

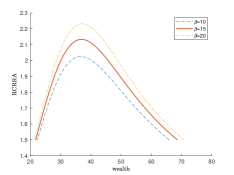

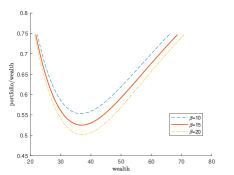

The maximum value of RCRRA increases in and , respectively111111Note that is more important since cannot exceed because of Assumption 2. (see Table 3). A high or implies a high cost when the agent changes the consumption level. Therefore, the intertemporal hedging deman become large (with negative sign) to crow out the myopic demand (see Eq. (25) and explanation below the equation), which makes the RCRRA level higher. In addition, a high risk, i.e., a high volatility increase the maximum level of RCRRA by the same token.

4.4 RCRRA tends to be large during the times when moderate shocks continuously arrive. RCRRA becomes small for the times with large shocks.

We know that RCRRA can be very large while the given risk aversion is very small. Then, when does it happen? In habit models, it happens in the downturns, in particular, when the current consumption level is very close to the habit stock. The mechanism to induce the difference between the actual risk aversion and the RCRRA in our model is very different from that of habit models.

Notice in our model that RCRRA tends to be small during the times when there are consecutive large shocks and thus in these times there are high fluctuations in wealth. For example, those times are between and in Figure 7 and between and in Figure 8. On the other hand, it tends to be high during the time when there are little or modest fluctuations in wealth due to moderately alternating good and bad shocks. For example, those times are before in Figure 7 and after in Figure 8. There are other examples in the Appendix.

In other words, high cost for consumption adjustment amplifies risk aversion over small or moderate shocks (particularly during the times when the wealth level stays in the mid range of (s, S) band), making the household look very conservative. However, the household may look very aggressive (if her actual risk aversion is very low), showing RCRRA close to her actual risk aversion, during the time when there are large shocks. Notably, if the household has a long sequence of moderate good shocks, then the risk aversion gradually decreases (equivalently the household gradually increases risky asset holdings). This pattern looks like that the household gains more confidence due to the success in the stock market.

In this sense, our utility cost model can generate substantial risk aversion in times of moderate risk events and great risk-taking in times of large risk events. This result is quite consistent with the puzzle reported in the behavioral literature.

4.5 Change in risky share relative to change in wealth

Here we investigate how the risky share changes relative to an increase in wealth. Note that models with habit, commitment, or DRRA (decreasing relative risk aversion) often predict that the relationship is positive while standard models with CRRA preference predicts no relationship. The empirical literature, however, seems rather inconclusive. For example, Calvet et al. (2009) and Calvet and Sodini (2014) favor the habit or commitment or DRRA models, and Chiappori and Paiella (2011) and Brunnermeier and Nagel (2008) favor the classical CRRA model and show even slightly negative relationship. We shed on light on the debate in the literature. We argue that whether the change in wealth has positive, negative, or no impact on the risky share depends on what kind of a sample path (time-series of the stock market data) researchers use although the data generating process is fixed.

Figure 9 shows the four types of sample paths we consider. Panel (a) is a typical long-term bull market, , Panel (b) is intermediate, Panel (c) is a typical bear market, and Panel (d) is the highly-fluctuating market over time. We will show that the impact of an wealth change on the risky share is different for each sample path. To do so, we generate the population with random and simulate their wealth and risky share over time.

Basically our estimation analysis follows that of Brunnermeier and Nagel (2008). Consider the following equation

| (27) |

where denotes a -period(year) first-difference operator, . Below we briefly explain how we regress Eq. (27).

(Step 1) Generate initial consumption/wealth distributions of individuals.

-

•

We divide the interval into subintervals with end points . (Here, we assume that is a positive integer)

-

•

We set equal initial consumption, for each individual and generate each individual’s initial consumption randomly according to a uniform distribution over .

-

•

For each and given pairs , , we generate log-normally distributed random variables and whose the mean and variance are and , respectively.121212The log-normal distribution implies that there are households having fairly large values of ’s although their density in the population is very small. We drop those household whose values violates Assumption 2.

-

•

Generate a random vector that follows a standard normal distribution. Using this vector , we generate the process of the risky asset returns , and the dual process in Proposition 3.2 for all the individuals. By Proposition 3.2, we can simulate the optimal wealth and portfolio processes of individuals.

(Step 2) Compute changes in the ratio of risk asset holdings and changes in wealth.

-

•

Let be the simulated wealth/portfolio processes for individuals in our utility cost model obtained in (Step 1). (Note that and are random vectors for ).

-

•

For given and , there are numbers of .

For and

-

•

We regress Eq. (27) with using the simulate results and .

| bull markets | intermediate | bear markets | highly fluctuating | ||

|---|---|---|---|---|---|

| (5, ) | (50, ) | 0.0208 (0.22) | |||

| (10, ) | (100, ) | ||||

| (10, ) | (150, ) | -0.0478 (0.01) | -0.0271 (0.26) | ||

| (15, ) | (150, ) | -0.0387 (0.04) | -0.0341 (0.17) | ||

| (15, ) | (200, ) | -0.0164 (0.43) | -0.0379 (0.14) | ||

| , | , . |

The results are summarized in Table 4. The regression results show the positive impact of the wealth increase on the risky share when the market is generally going up (Panel (a)) or intermediate with moderate up-and-downs. There is no wealth impact on the risky share or slightly negative (if any) when the market is generally going down (Panel (c)) or has a huge volatility (Panel (d)).

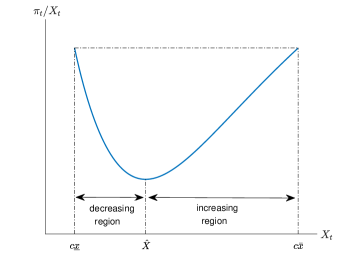

The intuition behind these results originates from the ratio of risky asset holding dynamics and wealth process. The risky share is hump-shaped in each (s, S) band, which implies that there are two regions with the band: the one is the decreasing region in which the risky share decreases with wealth and the other is the increasing region in which the risky share increases with wealth (see Figure 10). The decreasing region is in the left part of the (s, S) band and the increasing region is in the right part of the (s, S) band. In general, the increasing region longer than the decreasing region since the risk premium is positive. In addition, recall Figure 3 and its description below Theorem 3.2. In Figure 3, if there are consecutive good shocks, the wealth process tends to move in the following way: . During the times of this journey, the wealth process will stay longer in the increasing region of each (s, S) band since there are more good shocks than bad shocks in size and amount. On the other hand, if there are consecutive bad shocks, the wealth process tends to move in the other way: . During the times of this journey, the wealth process will stay longer in the decreasing region of each (s, S) band since there are more bad shocks than good shocks.

Having the above property in mind, if the market is doing well in the long-run as in Panel (a) of Figure 9), over time the wealth process is more likely to stay in the increasing region of each (s, S) band. Thus, the risky share tends to increase with wealth during these times. On the other hand, if the market is doing poorly for a while as in Panel (c) of Figure 9), the wealth process is more likely to stay in the decreasing region of each (s, S) interval. Thus, the risky share decreases with wealth during these times.

The intermediate case (Panel (b) of Figure 3) tends to be closer to the case of the bull market and the highly fluctuating period (Panel (d)) of 3) tends to be closer to the case of the bear market. It is because, as mentioned above, the right half part of the (s, S) band (increasing region) is generally longer than left half part of the (s, S) band (decreasing region).

5 Consumption and Asset Pricing Moments

Here we provide two implications of optimal consumption. Our model can explain the excess sensitivity and excess smoothness puzzles. In addition, our model can generate the reasonable asset pricing moments such as auto-correlation coefficient of consumption, which is often pointed out as a weakness of habit models.

5.1 Excess Sensitivity and Excess Smoothness

The optimal consumption level is infrequently adjusted in our model (see, for example, Figures 4 and 5). The excess smoothness appears since consumption in our model does not immediately respond to a permanent shock with a moderate level when the wealth level after the shock does not reach the (s, S) boundary. In other words, the household is less likely to change a consumption level with response to a small unexpected permanent shock (income), while they do increase or decrease the ratio of risky asset holdings for a positive (negative) shock.

The excess sensitivity also arises in our model by a similar reason. After a moderate good shock, the wealth level becomes higher than before. Although consumption does not immediately respond, it is more likely to increase later since the probability of increasing consumption in the next period becomes higher after the good shock. Therefore, our model can explain the excess sensitivity puzzle.

However, all the above arguments do not really work if the size of shock is large enough. For a large good shock, the wealth level immediately reaches the upper threshold, which makes consumption increase immediately. By the same token, the consumption level decreases immediately after a large bad shock. So, the consumption moves in the large shock events, following the permanent income hypothesis.

5.2 Auto-correlation

| EP | Std of IMRS | AC1 | |||||

|---|---|---|---|---|---|---|---|

| Data | 0.0192 | 0.0212 | – | – | 0.4600 | ||

| Our Model | 0.0181 | 0.0236 | 0.0052 | 0.0775 | 0.4900 | ||

|

0.0200 | 0.0858 | 0.0526 | 0.2996 | 0.1677 |

Here we provide how the model can generate consumption data and try to match several asset pricing moments. By using the time series of aggregate consumption we compute the mean and standard deviation of consumption growth rates, the intertemporal marginal rate of substitution(IMRS) and the theoretical equity premium(EP). Based on our consumption model, we simulate optimal consumption processes for individuals following three steps:

| EP | Std of IMRS | AC1 | ||||||

| 0.015 | 3.5 | 5 | 10 | 0.0181 | 0.0236 | 0.0052 | 0.0775 | 0.4900 |

| 15 | 0.0182 | 0.0232 | 0.0050 | 0.0758 | 0.4888 | |||

| 20 | 0.0183 | 0.0229 | 0.0049 | 0.0747 | 0.4881 | |||

| 0.015 | 3.5 | 0 | 20 | 0.0182 | 0.0233 | 0.0050 | 0.0762 | 0.4889 |

| 5 | 0.0183 | 0.0229 | 0.0049 | 0.0747 | 0.4881 | |||

| 10 | 0.0184 | 0.0226 | 0.0048 | 0.0736 | 0.4869 | |||

| 0.015 | 3.5 | 30 | 100 | 0.0191 | 0.0217 | 0.0044 | 0.0699 | 0.4825 |

| 50 | 100 | 0.0192 | 0.0215 | 0.0044 | 0.0693 | 0.4808 | ||

| 50 | 1000 | 0.0192 | 0.0215 | 0.0044 | 0.0691 | 0.4802 | ||

| 0.010 | 3.5 | 5 | 10 | 0.0194 | 0.0242 | 0.0054 | 0.0791 | 0.4888 |

| 0.015 | 0.0181 | 0.0236 | 0.0052 | 0.0775 | 0.4900 | |||

| 0.050 | 0.0093 | 0.0204 | 0.0039 | 0.0683 | 0.4953 | |||

| 0.015 | 0.9 | 5 | 10 | 0.0738 | 0.0963 | 0.0052 | 0.0775 | 0.4889 |

| 1.5 | 0.0431 | 0.0563 | 0.0052 | 0.0775 | 0.4898 | |||

| 3.5 | 0.0181 | 0.0236 | 0.0052 | 0.0775 | 0.4900 | |||

| 10 | 0.0063 | 0.0082 | 0.0052 | 0.0775 | 0.4900 |

(Step 1) Generate initial consumption/wealth distributions of individuals.

-

•

We divide the interval into subintervals with end points .

-

•

Similar to Marshall and Parekh (1999), we set equal initial consumption, for each individual and generate each individual’s initial consumption randomly according to a uniform distribution over .

- •

(Step 2) Aggregation of Consumption

-

•

Let be the simulated consumption processes for individuals in our utility cost model obtained in (Step 1).

-

•

(Cross sectional aggregation) The cross sectionally aggregated consumption process of is defined as follows:

For ,

-

•

(Temporal aggregation) We temporally aggregate the cross sectionally aggregated series to create monthly (that is, ) as follows:

For ,

(Step 3) Compute the consumption growth rate, IMRS, and theoretical EP of aggregated consumption

-

•

We use the simulated returns on the risky asset .

-

•

We derive the following time-series

,

Using these time-series, we obtain desired statistics(the mean and the standard derivation of consumption growth, the IMRS, the theoretical EP and the auto-correlation of aggregated consumption ).

Since each time-series depends on the random vector , repeat (Step 1)–(Step 3) 1000 times.

The baseline results are summarized in Table 5. The model fits the consumption data well with reasonable values for the market and preference parameters. In particular, the auto-correlation simulated by our model is well matched with the data, which is not possible with the standard Merton case. It is surprising that a fairly small values of can generate the autocorrelation value close to its historical data. Table 6 confirms this result.

6 Concluding Remarks

We model the partial irreversibility of consumption decision motivated by Duesenberry (1949). In order to do so, we introduce the adjustment cost of consumption. We show that the consumption partial irreversibility model can generate a number of novel implications. Some of our results are similar to those derived from habit formation or consumption commitment models. However, the mechanism to generate time-varying risk aversion or the excess sensitivity and excess smoothness consumption is very different from that from these literature. In this sense, we view that our model as complement to the existing literature. In addition to these results, we find that the consumption adjustment cost can reconcile the gap between the asset pricing literature and the literature on estimating risk aversion. Also, we shed light on the debate on how the wealth change has impact on the households risky share.

We believe that the (partial) irreversibility is a very realistic and important aspect of consumption decision. While we model it by introducing the adjustment cost, we admit that there would be other ways to model it. We hope that our model contributes to building other works toward this direction. One of important future works will be building a general equilibrium model with the partial irreversibility of consumption decision that can investigate further asset pricing implications (e.g., Choi et al. (2018)). This type of extension will help to provide the microfoundation for the relative income hypothesis by Duesenberry (1949).

References

- Abel (1990) Abel, A. B., 1990, Asset Prices under Habit Formation and Catching up with the Joneses, American Economic Review, 80(2), 38–42.

- Bansal et al. (2012) Bansal, R., Kiku, D., Yaron, A., 2012, An empirical evaluation of the longrun risks model for asset prices, Critical Finance Review, 1, 183–221.

- Bombardini and Trebbi (2012) Bombardini, M., Trebbi, F. , 2012, Risk Aversion and Expected Utility Theory: An Experiment with Large and Small Stakes, Journal of the European Economic Association, 2012, 10(6), 1348–99.

- Brunnermeier and Nagel (2008) Brunnermeier, M., Nagel, S., 2008, Do wealth fluctuations generate time-varying risk aversion? Micro-evidence on individuals’ asset allocation, American Economic Review 98, 713–736.

- Calvet and Sodini (2014) Calvet, L. E., Sodini, P., 2014, Twin Picks: Disentangling the Determinants of Risk-Taking in Household Portfolios, Journal of Finance, 69(2), 867–906

- Calvet et al. (2009) Calvet, L. E., Campbell, J. Y., Sodini, P., 2009, Fight or flight? Portfolio rebalancing by individual investors, Quarterly Journal of Economics, 124, 301–348.

- Campbell and Cochrane (1999) Campbell, J. Y., Cochrane, J. H., 1999, By force of habit: a consumption-based explanation of aggregate stock market behavior, Journal of Political Economy, 107, 205–251.

- Campo et al. (2011) Campo, S., Guerre, E., Perrigne, I., Quang, V., 2011, Semiparametric Estimation of First-Price Auctions with Risk-Averse Bidders, Review of Economic Studies, 78(1), 112–47.

- Chetty (2006) Chetty, R., 2006, A New Method of Estimating Risk Aversion, American Economic Review, 96(5), 1821–34.

- Chetty and Szeidl (2007) Chetty, R., Szeidl, A., 2007, Consumption Commitments and Risk Preferences, Quarterly Journal of Economics, 122 (2), 831–877.

- Chetty and Szeidl (2016) Chetty, R., Szeidl, A., 2016,Consumption Commitments and and Habit Formation, Econometrica, 84(2), 855–890.

- Chiappori and Paiella (2011) Chiappori, P., Paiella, M., 2011, Relative Risk Aversion is Constant: Evidence From Panel Data, Journal of the European Economic Association, 9(6), 1021–2052.

- Choi et al. (2018) Choi, K. J., Jeon, J., Koo, H.K., 2018, Duesenberry’s Theory of Consumption: An Equilibrium Model of (Partial) Consumption Irreversibility, working paper

- Cocco et al. (2005) Cocco, J.F., Gomes, F.J, Maenhout, P.J., 2005, Consumption and Portfolio Choice over the Life Cycle, Review of Financial Studies, 18(2), 491-533.

- Constantinides (1990) Constantinides, G. M., 1990, Habit Formation: A Resolution of the Equity Premium Puzzle, Journal of Political Economy, 98, 519–543.

- Cox and Huang (1989) Cox, J., Huang, C., 1989, Optimal Consumption and Portfolio Polices when Asset Prices Follow a Diffusion Process, Journal of Economic Theory, 49(1), 33–83.

- Dai and Yi (2009) Dai, M., Yi, F., 2009, Finite-horizon optimal investment with transaction costs: A parabolic double obstacle problem, Journal of Differential Equations, 246(4), 1445-1469.

- Davis and Norman (1990) Davis, M.H.A., Norman A.R., 1990, Portfolio selection with transaction costs, Mathematics of Operations Research 15, 676–713.

- Deaton (1987) Deaton, A., 1987, Life-Cycle Models of Consumption: Is the Evidence Consistent With the Theory, Advances in Econometrics, Fifth World Congress, Vol. 2, ed. by B. Truman. Cambridge: Cambridge University Press

- Duesenberry (1949) Duesenberry, J. S., 1949, ‘Income, Saving, and the Theory of Consumer Behavior, Cambridge, Mass.: Harvard University Press.

- Dybvig (1995) Dybvig, P. H., 1995, Dusenberry’s Racheting of Consumption: Optimal Dynamic Consumption and InvestmentGiven Intolerance for any Decline in Standard of Living, Review of Economic Studies, 62(2), 287–313.

- Flavin (1981) Flavin, M., 1981, The Adjustment of Consumption to Changing Expectations About Future Income, Journal of Political Economy, 89, 974–1009

- Flavin and Nakagawa (2008) Flavin, M., Nakagawa, S., 2008, “A Model of Housing in the Presence of Adjustment Costs: A Structural Interpretation of Habit Persistence, American Economic Review, 98, 474–495.

- Fleming and Soner (2006) Fleming, W.H., Soner, H.M., 2006, Controlled Markov Processes and Viscosity Solutions, (Springer-Verlag), New York.

- Gali (1994) Gali, J. (1994), Keeping up with the Joneses: Consumption Externalities, Portfolio Choice, and Asset Prices, Journal of Money, Credit, and Banking, 26, 1–8.

- Gandelman and Hernández-Murillo (2013) Gandelman, N, Hernández-Murillo, R., 2013, What Do Happiness and Health Satisfaction Data Tell Us About Relative Risk Aversion? Journal of Economic Psychology 39, 301–12.

- Gandelman and Hernández-Murillo (2015) Gandelman, N., Hernández-Murillo, R., 2015 Risk Aversion at the Country Level, Federal Reserve Bank of St. Louis Review, 97(1), 53–66.

- Grossman and Laroque (1990) Grossman, S. J., Laroque, G., 1990, Asset Pricing and Optimal Portfolio Choice in the Presence of Illiquid Durable Consumption Goods, Econometrica, 58, 25–51.

- Hansen and Singleton (1982) Hansen, L P., Singleton, K., Generalized Instrumental Variables Estimation of Nonlinear Rational Expectations Models, Econometrica, 50(5), 1269–86.

- Harrison (1985) Harrison, M., 1985, Brownian Motion and Stochastic Flow Systems, Wiley, New York.

- Hindy and Huang (1992) Hindy, A. and C. Huang “Intertemporal Preferences for Uncertain Consumption: A Continuous Time Approach,” Econometrica 60(4), 781-801.

- Hindy and Huang (1993) Hindy, A. and C. Huang “Optimal Consumption and Portfolio Rules with Durability and Local Substitution,” Econometrica 61(1), 85-121.

- Hindy et al. (1997) Hindy, A. C. Huang, and S. Zhu “Optimal consumption and portfolio rules with durability and habit formation,” Journal of Economic Dynamics and Control 21(2-3), 525-550.

- Jappelli and Pistaferri (2010) Jappelli, T., Pistaferri, L., 2010, The Consumption Response to Income Changes, Annual Review of Economics, 2, 479-506.

- Jeon et al. (2018) Jeon, J., Koo, H. K., Shin, Y. H., 2018, Portfolio selection with consumption ratcheting, Journal of Economic Dynamics and Control, 92, 153–182.

- Kandel and Stambaugh (1991) Kandel, S., Stambaugh, R., 1991, Asset Returns, Investment Horizons and Intertemporal Preferences, Journal of Monetary Economics 27, 39-71

- Karatzas et al. (1987) Karatzas, I., Lehoczky, J., Shreve, S.E., 1987, “Optimal Portfolio and Consumption Decisions for a ”Small Investor” on a Finite Horizon,” SIAM Journal on Control and Optimization, 25(6), 1557-1586.

- Karatzas and Shreve (1998) Karatzas, I., Shreve, S.E., 1998. Methods of Mathematical Finance, Springer-Verlag, New York.

- Layard, Mayraz, and Nickel (2008) Layard, R., Mayraz, G., Nickell, S., 2008, The Marginal Utility of Income., Journal of Public Economics, 92, 1846-57.

- Lieberman (1996) Lieberman, G., 1996, Second Order Parabolic Differential Equations. World Scientific, Singapore.

- Marshall and Parekh (1999) Marshall, D., Parekh, N., 1999, Can costs of consumption adjustment explain asset pricing puzzles, Journal of Finance, 54(2), 623-654.

- Oksendal (2005) Oksendal, B., 2005, Stochastic Differential Equations, 6th ed. Springer.

- Otrok et al. (2002) Otrok, C., Ravikumar, B., Whiteman, C., 2002, Habit formation: a resolution of the equity premium puzzle, Journal of Monetary Economics, 49, 1261–1288.

- Schroder and Skiadas (2002) Szpiro, G., 2002, “An Isomorphism Between Asset Pricing Models With and Without Linear Habit Formation” Review of Financial Studies, 15(4), 1189-1221.

- Szpiro (1986) Szpiro, G., 1986, “Relative Risk Aversion Around the World.” Economics Letters, 20(1), 19–21.

Appendix

Appendix A Derivation of the dual value function

The following theorem guarantees that the solution to the HJB equation (16) is the solution to the dual problem.

Theorem A.1 (Verification Theorem).

1. Suppose that the HJB equation (16) has a twice continuously differentiable solution satisfying the following conditions:

-

(1)

For any admissible consumption strategy , the process defined by

is a martingale.

-

(2)

For any admissible consumption strategy ,

Then, for initial condition and any admissible consumption strategy ,

2. Given any initial condition , suppose that there exist an admissible consumption strategy such that, if is the associated consumption process, then

Lebesgue-a.e., -a.s.,

| (28) |

and

Then, is the dual value function for Problem 3 and is the optimal consumption strategy.

Proof.

(Proof of 1.)

For given consumption process , define a process

| (29) |

By the generalized Itó’s lemma (See Harrison (1985)),

| (30) |

where and are the continuous parts of and , respectively.

Hence, for any fixed ,

| (31) |

Since

we deduce that

Moreover,

| (32) |

and by assumption, .

Thus, we can conclude that

and is a super-martingale.

This implies that and

| (33) |

By assumption

and Fatou’s lemma, we deduce that

| (34) |

The relation (34) holds for any admissible consumption strategy , we obtain

(Proof of 2.)

By assumption, we can show that in (31)

This implies that is a martingale and

| (35) |

The transversality condition leads to

| (36) |

Thus,

and the consumption strategy attains the maximum. Hence is the optimal.

∎

Now, we will obtain the analytic characterization of the dual value function by using the the variational inequality (16).

As Dai and Yi (2009), we consider the double obstacle problem arising from variational inequality (16) as follows:

| (37) |

Consider the following substitution:

Then, the double obstacle problem (37) can be changed by

| (38) |

The following proposition provides the exact solution of the double obstacle problem (38).

Proposition A.1.

The variational inequality (38) has a unique -solution, which is

| (39) |

where

and , are positive and negative roots of following quadratic equation:

and , are defined as

with .

Here, is the unique root to the equation in , where

| (40) |

Also,

and attains minimum at defined by

Proof.

The uniqueness of the solution is guaranteed due to the maximum principle of the partial differential equation theory(see Lieberman (1996)).

Now, we will prove the remain part of proposition in the following steps.

(Step 1) We first consider the following free boundary problem:

| (41) |

Then we can extend the solution onto by

| (42) |

Next, we show that is the solution to variational inequality (38). We can let the general solution for (41) in the form of

From the smooth-pasting condition and ,

| (43) |

Therefore, and are given by

| (44) |

Similarly,

| (45) |

and

| (46) |

| (47) |

Let us define

From (47),

| (48) |

(Step 2) has a unique solution and .

For ,

| (49) |

On the other hand,

| (50) |

By the Intermediate Value Theorem, there exists such that . To show “uniqueness”, it is suffice to show that

Then,

| (51) |

and

| (52) |

Let us temporarily denote

Since

| (53) |

Let us temporarily denote

Since

| (54) |

By (52), (53) and (54), we can conclude that

and has a unique solution on with .

(Step 3) The two free boundaries and are uniquely determined. Moreover, and .

Let us temporarily denote

Since

we deduce that

This leads to

and .

Let us also temporarily denote

Since

we deduce that

This leads to

and .

(Step 4) In , and attains minimum at .

First, we will show that

Since

| (55) |

Similarly, we can deduce that .

We know that and

Since , it is enough to show that

By the definition of ,

Since

we can easily check that

Also, we know that

This implies that

Thus, we deduce that

and

Hence, attains minimum at and on .

(Step 4) satisfies the variational inequality (38).

-

•

For . it is clear that

(56) Since and is strictly decreasing function on ,

-

•

For , and

-

•

For , and

From (Step 1) (Step 4), we have proved the desired result.

∎

Using the in the equation (57), we construct the dual value function as follows:

(i) For ,

| (58) |

(ii) For ,

| (59) |

(iii) For ,

| (60) |

where the function is defined by

Remark A.1.

Proposition A.2.

For the function defined in (58), (59) and (60), the following statements are true:

-

1.

is a twice continuously differentiable and satisfies the HJB equaton (16). Moreover, the regions , and are represented by

respectively.

-

2.

For any admissible consumption strategy ,

is a martingale.

-

3.

For any admissible consumption strategy ,

Proof.

(Proof of 1.)

First, with reference to the construction of the dual value function , we will show that is a continuously differentiable if we prove that , and are continuous along the free boundaries and .

Then, we can compute

| (61) |

and

| (62) |

Thus, is continuous along the free boundaries.

Similarly, we can obtain

| (63) |

and hence is continuous along the free boundaries.

We know that and is -function. Thus, it is clear that is continuous function and we conclude that is -function.

Next, we will show that satisfies the HJB-equation (16).

-

•

The region NR:

Since ,Also, we can easily confirm that

-

•

The region IR:

We deduce thatClearly,

Since and on IR,

(64) -

•

The region DR:

Similarly,and

Since and on IR,

(65) Thus, satisfies the HJB-equation

(Proof of 2.)

Let

To show the process is a martingale, it is suffice to prove that

(see Chapter 3 in Oksendal (2005))

First, we consider the case when . Then,

Since

there exist constants such that

| (66) |

When , we know that

In this case,

Thus, there exist constants such that

| (67) |

Similarly, when , there exist constants such that

| (68) |

By (66), (67) and (68), for any ,

for some constant .

Hence

| (69) |

This implies that is a martingale for .

(Proof of 3.)

If , then

Since,

| (70) |

there exists a constant such that

| (71) |

When , we know that

| (72) |

Thus, there exits a constant such that

| (73) |

Similarly, for , there exists a constant such that

| (74) |

By (71), (73) and (74), for any , there exist a constant such that

| (75) |

By the admissibility of the consumption strategy,

Since is a finite variation process, its sample paths can have at most countable discontinuities. Hence, applying Fubini’s theorem, we deduce that

and

From (75),

| (76) |

Thus, we can conclude that for any admissible consumption strategy and its associated consumption process ,

∎

Appendix B Proof of Theorem 3.1

We will show that the duality relationship in the following steps:

(Step 1) First, we will prove that the dual value function is strictly convex in :

By direct computation,

| (77) |

Since

we deuce that

and thus is strictly convex in .

Let us denote the Lagrangian L defined in (14) by for the Lagrangian multiplier and consumption profile .

(Step 2) We will show that there exist a unique solution such that and the optimal consumption maximize the Lagrangian .

From Proposition 3.1, we deduce that

| (78) |

For a sufficiently small ,

and for a sufficiently large ,

This implies that

| (79) |

Since is strictly convex in , for given , there exists a unique such that

| (80) |

Thus, there exist optimal consumption strategy such that

| (81) |

where , and .

This means that since the Lagrangian is concave, and are maximizers of the Lagrangian.

(Step 3) satisfies the budget constraint with equality.

Define and with (For convenience of notation we drop the time subscript ). Then,

Since maximizers of the Lagrangian , we have

and thus we deduce

This leads to

This implies that satisfies the budget constraint with equality.

(Step 4) is optimal consumption.

Let be a feasible consumption strategy, i.e., it is admissible and satisfies the budget constraint.

Since satisfies the budget constraint,

| (82) |

where is defined in (Step 2).

Since and maximize the Lagrangian and satisfies the budget constraint with equality,

| (83) |

Therefore, is optimal.

Step 5) Proof of duality-relationship in (20)

Since is optimal consumption, for , we deduce

where is the optimal consumption process for Problem 3 for . This implies that

However, we know that

Thus,

This completes the proof.

Appendix C Proof of Proposition 3.2

First, we show that the optimal consumption strategy given in (21) is admissible. We can see that for optimal consumption strategy and its associated consumption ,

| (84) |

Then, there exist constants such that

| (85) |

for all .

Thus,

Since is the optimal strategy, it is clear that

Above two inequalities imply is admissible consumption strategy.

Appendix D Proof of Theorem 3.2

From Theorem 3.1, we know that there exists a unique solution for the minimization problem (20). The first-order condition implies that

| (89) |

Since Problem 3 is time-consistent, is the minimizer for the duality relationship starting at . Thus, for optimal wealth at time , we have

| (90) |

During the time in which is inside the NR, the optimal consumption is constant, i.e., and thus the optimal wealth for is given by

| (91) |

By Proposition 3.2, we know that the agent does not increase or decrease his/her consumption in the region

Let us define , as follows:

where is

Since

and , is strictly increasing function of .

This means that the consumption stays for constant if and only if

This completes the proof.

Appendix E Proof of Proposition 3.3

Proof of (a).

By applying the generalized Itó’s lemma(see Harrison (1985)) to the optimal wealth process ,

| (92) |

If , the agent does not adjust his/her consumption. This means that and thus

If , the agent should increase his/her consumption. This implies that

and hence

Similarly, we also obtain

when .

Appendix F Proof of Theorem 3.3

For , for , the consumption stays constant. Thus, for simplicity, we can assume .

Then,

| (96) |

Since ,

We will show that there exists a unique such that is a strictly decreasing function on and strictly decreasing function on .

| (97) |

(For convenience of notation we drop the time subscript and the optimal subscript .)

Let us define the numerator of as , i.e.,

| (98) |

By the proof in Proposition A.1, we know that

Thus,

Since

we have

Hence,

We know that

thus, is a strictly increasing function of .

Since , we deduce that

Thus, there exists a unique such that

This implies that

To sum up, we conclude that RCRRA is a strictly increasing for and a strictly decreasing for . Moreover, RCRRA approaches when approaches or . (Here, and is a unique solution of the following algebraic equation:

| (99) |