Functional Sequential Treatment Allocation111 We are grateful to the Editor, the Associate Editor, and two referees for their comments and suggestions that helped to substantially improve the manuscript.

This version222Early versions of the paper have also contained results incorporating covariates, which are now available in the companion paper Kock et al. (2020a). : July 2020)

Abstract

Consider a setting in which a policy maker assigns subjects to treatments, observing each outcome before the next subject arrives. Initially, it is unknown which treatment is best, but the sequential nature of the problem permits learning about the effectiveness of the treatments. While the multi-armed-bandit literature has shed much light on the situation when the policy maker compares the effectiveness of the treatments through their mean, much less is known about other targets. This is restrictive, because a cautious decision maker may prefer to target a robust location measure such as a quantile or a trimmed mean. Furthermore, socio-economic decision making often requires targeting purpose specific characteristics of the outcome distribution, such as its inherent degree of inequality, welfare or poverty. In the present paper we introduce and study sequential learning algorithms when the distributional characteristic of interest is a general functional of the outcome distribution. Minimax expected regret optimality results are obtained within the subclass of explore-then-commit policies, and for the unrestricted class of all policies.

Keywords: Sequential Treatment Allocation, Distributional Characteristics, Randomized Controlled Trials, Minimax Optimal Expected Regret, Multi-Armed Bandits, Robustness.

1 Introduction

A fundamental question in statistical decision theory is how to optimally assign subjects to treatments. Important recent contributions include Chamberlain (2000), Manski (2004), Dehejia (2005), Hirano and Porter (2009), Stoye (2009), Bhattacharya and Dupas (2012), Stoye (2012), Tetenov (2012) Manski and Tetenov (2016), Athey and Wager (2017), Kitagawa and Tetenov (2018), and Manski (2019b); cf. also the overview in Hirano and Porter (2018). In the present paper we focus on assignment problems where the subjects to be treated arrive sequentially. Thus, in contrast to the above mentioned articles, the dataset is gradually constructed during the learning process. In this setting, a policy maker who seeks to assign subjects to the treatment with the highest expected outcome (but who initially does not know which treatment is best), can draw on a rich and rapidly expanding literature on “multi-armed bandits.” Important contributions include Thompson (1933), Robbins (1952), Gittins (1979), Lai and Robbins (1985), Agrawal (1995), Auer et al. (1995), Audibert and Bubeck (2009); cf. Bubeck and Cesa-Bianchi (2012) and Lattimore and Szepesvári (2020) for introductions to the subject and for further references. In many applications, however, the quality of treatments cannot successfully be compared according to the expectation of the outcome distribution: A cautious policy maker may prefer to use another (more robust) measure of location, e.g., a quantile or a trimmed mean; or may actually want to make assignments targeting a different distributional characteristic than its location. Examples falling into the latter category are encountered in many socio-economic decision problems, where one wants to target, e.g., a welfare measure that incorporates inequality or poverty implications of a treatment. Inference for such “distributional policy effects” has received a great deal of attention in non-sequential settings, e.g., Gastwirth (1974), Manski (1988), Thistle (1990), Mills and Zandvakili (1997), Davidson and Duclos (2000), Abadie et al. (2002), Abadie (2002), Chernozhukov and Hansen (2005), Davidson and Flachaire (2007), Barrett and Donald (2009), Hirano and Porter (2009), Schluter and van Garderen (2009), Rostek (2010), Rothe (2010, 2012), Chernozhukov et al. (2013), Kitagawa and Tetenov (2019) and Manski (2019a).333In contrast to much of the existing theoretical results concerning inference on inequality, welfare, or poverty measures, we do not investigate (first or higher-order) asymptotic approximations, but we establish exact finite sample results with explicit constants. To this end we cannot rely on classical asymptotic techniques, e.g., distributional approximations based on linearization arguments.

Motivated by robustness considerations and the general interest in distributional policy effects, we consider a decision maker who seeks to minimize regret compared to always assigning the unknown best treatment according to a functional of interest. In order to achieve a low regret, the policy maker must sequentially learn the distributional characteristic of interest for all available treatments, yet treat as many subjects as well as possible.

While most of the multi-armed bandit literature focuses on targeting the treatment with the highest expectation, there are articles going beyond the first moment. This previous work has focused on risk functionals: Maillard (2013) considers problems where one targets a coherent risk measure. Sani et al. (2012), Vakili and Zhao (2016) and Vakili et al. (2018) study a problem targeting the mean-variance functional, i.e., the variance minus a multiple of the expectation. Zimin et al. (2014), motivated by earlier results on problems targeting specific risk measures, and Kock and Thyrsgaard (2017) consider problems where one targets a functional that can be written as a function of the mean and the variance. Tran-Thanh and Yu (2014) and Cassel et al. (2018) do not restrict themselves to functionals of latter type, and consider bandit problems, where the target can be a general risk functional. These papers use various types of regret frameworks. Tran-Thanh and Yu (2014) consider a “pure-exploration” regret function into which the errors made during the assignment period do not enter. Maillard (2013), Zimin et al. (2014), Kock and Thyrsgaard (2017) and Vakili et al. (2018) consider a “cumulative” regret function that is closely related to the regret used in classical multi-armed bandit problems (i.e., where the expectation is targeted). Sani et al. (2012), Vakili and Zhao (2016) and Cassel et al. (2018) consider a “path-dependent” regret function. The just-mentioned articles have in common that pointwise regret upper bounds are derived for certain policies (and the regret considered). Except for Vakili and Zhao (2016) and Vakili et al. (2018), who exclusively consider the mean-variance functional, matching lower bounds are not established. Therefore, apart from the mean-variance functional, it remains unclear if the policies developed are optimal. The main goal of the present paper is to develop a minimax optimality theory for general functional targets. The regret function we work with is cumulative, and thus has the following important features which are relevant for many socio-economic assignment problems:

-

•

Every subject not assigned to the best treatment contributes to the regret.

-

•

A loss incurred for one subject cannot be compensated by future assignments.

The first bullet point is not satisfied by a “pure-exploration” regret; the second is violated by “path-dependent” regrets.

Our first contribution is to establish minimax expected regret optimality properties within the subclass of “explore-then-commit” policies (cf. Theorems 3.4 and 3.5). These are policies that strictly separate the exploration and exploitation phases: one first attempts to learn the best treatment, e.g., by conducting a randomized controlled trial (RCT), on an initial segment of subjects. Based on the outcome, one then assigns all remaining subjects to the inferred best treatment (which is not guaranteed to be the optimal one). Such policies are close to current practice in many socio-economic decision problems. Garivier et al. (2016) recently studied optimality properties of explore-then-commit policies in a 2-arm Gaussian setting targeting exclusively the expectation.

Our second contribution is to obtain lower bounds on maximal expected regret over the class of all policies (cf. Theorem 4.2), and to show that they are matched by uniform upper bounds for the following two policies: Firstly, the “F-UCB” policy (an extension of the UCB1 policy of Auer et al. (2002)), and secondly the “F-aMOSS” policy (an extension of the anytime MOSS policy of Degenne and Perchet (2016)), cf. Theorems 4.1 and 4.3.

Our lower bounds hold under very weak assumptions. Therefore, they settle firmly what can and cannot be achieved in a functional sequential treatment assignment problem.

As a corollary to our results, comparing the regret upper bounds derived for the F-UCB and the F-aMOSS policy to the lower bound obtained for explore-then-commit policies, we reveal that in terms of maximal expected regret all explore-then-commit policies are inferior to the F-UCB and the F-aMOSS policy, and therefore should not be used if it can be avoided. If an explore-then-commit policy has to be used, our results provide guidance on the optimal length of the exploration period.

In Sections 5 and 6 we provide numerical results (based on simulated and empirical data) comparing the regret-behavior of explore-then-commit policies with that of the F-UCB and the F-aMOSS policy. In this context we develop test-based and empirical-success-based explore-then-commit policies that might be of independent interest, because they provably possess desirable performance guarantees.

Concerning the functionals we permit our theory is very general. We verify in detail that it covers many inequality, welfare, and poverty measures, such as the Schutz coefficient, the Atkinson-, Gini- and Kolm-indices. This discussion can be found in Appendix D. We also show that our theory covers quantiles, U-functionals, generalized L-functionals, and trimmed means. These results can be found in Appendix F. The results in these appendices are of high practical relevance, because they allow the policy maker to choose the functional-dependent constants appearing in the optimal policies in such a way that the performance guarantees apply.

In the companion paper Kock et al. (2020a) we address the important but nontrivial question how to construct policies that optimally incorporate covariate information. The results in the present paper are crucial for obtaining those results.

2 Setting and assumptions

We consider a setting, where at each point in time a policy maker must assign a subject to one out of treatments. Each subject is only treated once.444We emphasize that the sequential setting is different from the “longitudinal” or “dynamic” one in, e.g., Robins (1997), Lavori et al. (2000), Murphy et al. (2001), Murphy (2003) and Murphy (2005), where the same subjects are treated repeatedly. Thus, the index can equivalently be thought of as indexing subjects instead of time. The observational structure is the one of a multi-armed bandit problem: After assigning a treatment, its outcome is observed, but the policy maker does not observe the counterfactuals. Having observed the outcomes of treatments , subject arrives, and must be assigned to a treatment. The assignment can be based on the information gathered from all previous assignments and their outcomes, and, potentially, randomization. Thus, the data set is gradually constructed in the course of the treatment program. Without knowing a priori the identity of the “best” treatment, the policy maker seeks to assign subjects to treatments so as to minimize maximal expected regret (which we introduce in Equation (3) further below).

This setting is a sequential version of the potential outcomes framework with multiple treatments. Note also that restricting attention to problems where only one out of the treatments can be assigned does not exclude that a treatment consists of a combination of several other treatments (for example a combination of several drugs) — one simply defines this combined treatment as a separate treatment at the expense of increasing the set of treatments.

The precise setup is as follows: let the random variable denote the potential outcome of assigning subject to treatment .555We do not explicitly consider the case of individuals arriving in batches. However, in our setup, one may also interpret as a summary statistic of the outcomes of batch , when all of its subjects were assigned to treatment . For a more sophisticated way of handling batched data in case of targeting the mean treatment outcome, we refer to Perchet et al. (2016). That is, the potential outcomes of subject are . We assume that , where are real numbers. Furthermore, for every , let be a random variable, which can be used for randomization in assigning the -th subject. Throughout, we assume that for are independent and identically distributed (i.i.d.); and we assume that the sequence is i.i.d., and is independent of the sequence . Note that no assumptions are imposed concerning the dependence between the components of each random vector . We think of the randomization measure, i.e., the distribution of , as being fixed, e.g., the uniform distribution on . We denote the cumulative distribution function (cdf) of by , where denotes the set of all cdfs such that and . The cdfs for are unknown to the policy maker.

A policy is a triangular array of (measurable) functions . Here denotes the assignment of the -th subject out of subjects. In each row of the array, i.e., for each , the assignment can depend only on previously observed treatment outcomes and randomizations (previous and current). Formally,

| (1) |

Given a policy and , the input to is denoted as . Here is defined recursively: The first treatment is a function of alone, as no treatment outcomes have been observed yet (we may interpret ). The second treatment is a function of , the outcome of the first treatment and the first randomization, and of . For we have

The -dimensional random vector can be interpreted as the information available after the -th treatment outcome was observed. We emphasize that depends on the policy via . In particular, also depends on , which we do not show in our notation. For convenience, the dependence of on and is often suppressed, i.e., we often abbreviate by if it is clear from the context that the actual assignment is meant, instead of the function defined in Equation (1).

Remark 2.1 (Concerning the dependence of on the horizon ).

We have chosen to allow the assignments to depend on , the total number of assignments to be made. Consequently, for it may be that does not coincide with the first elements of . This is crucial, as a policy maker who knows may choose different sequences of allocations for different . For example, one may wish to explore the efficacies of the available treatments in more detail if one knows that the total sample size is large, such that there is much opportunity to benefit from this knowledge later on. We emphasize that while our setup allows us to study policies that make use of , we devote much attention to policies that do not. The latter subclass of policies is important. For example, a policy maker may want to run a treatment program for a year, say, but it is unknown in advance how many subjects will arrive to be treated. In such a situation, one needs a policy that works well irrespective of the unknown horizon. Such policies are called “anytime policies,” as does not depend on .

The ideal solution of the policy maker would be to assign every subject to the “best” treatment. In the present paper, this is understood in the sense that the outcome distribution for the best treatment maximizes a given functional

| (2) |

We do not assume that the maximizer is unique, i.e., need not be a singleton. The specific functional chosen by the policy maker will depend on the application, and encodes the particular distributional characteristics the policy maker is interested in. For a streamlined presentation of our results it is helpful to keep the functional abstract at this point (see Section 2.1 below for an example, and a brief overview of examples we study in detail in appendices).

The ideal solution of the policy maker of assigning each subject to the best treatment is infeasible, simply because it is not known in advance which treatment is best. Therefore, every policy will make mistakes. To compare different policies, we define the (cumulative) regret of a policy at horizon as

| (3) |

i.e., for every individual subject that is not assigned to the best treatment one incurs a loss. One important feature of is that the losses incurred at time cannot be nullified by later assignments. As discussed in the introduction, cumulative regret functions have previously been used by Maillard (2013), Zimin et al. (2014), Kock and Thyrsgaard (2017) and Vakili et al. (2018), the latter explicitly emphasizing the practical relevance of this regret notion in the context of clinical trials where the loss in each individual assignment needs to be controlled.

The unknown outcome distributions are assumed to vary in a pre-specified class of cdfs. Following the minimax-paradigm, we evaluate policies according to their worst-case behavior over such classes. We refer to Manski and Tetenov (2016) for further details concerning the minimax point-of-view in the context of treatment assignment problems, and for a comparison with other approaches such as the Bayesian. Formally, we seek a policy that minimizes maximal expected regret, that is, a policy that minimizes

| (4) |

where is a subset of . The supremum is taken over all potential outcome vectors such that the marginals for have a cdf in . The set will typically be nonparametric, and corresponds to the assumptions one is willing to impose on the cdfs of each treatment outcome, i.e., on . Note that the maximal expected regret of a policy as defined in the previous display depends on the horizon . We will study this dependence on . In particular, we will study the rate at which the maximal expected regret increases in for a given policy ; furthermore, we will study the question of which kind of policy is optimal in the sense that the rate is optimal.

The following assumption is the main requirement we impose on the functional and the set . We denote the supremum metric on by , i.e., for cdfs and we let .

Assumption 2.2.

The functional and the non-empty set satisfy

| (5) |

for some .

Remark 2.3 (Restricted-Lipschitz continuity).

Assumption 2.2 implies that the functional is Lipschitz continuous when restricted to (the domain being equipped with ). We emphasize, however, that if , the functional is not necessarily required to be Lipschitz-continuous on all of . This is due to the asymmetry inherent in the condition imposed in Equation (5), where varies only in , but varies in all of .

Remark 2.4.

A simple approximation argument666 Let be such that as for a sequence , and let . Then, , which, by Assumption 2.2, is not greater than as . shows that if Assumption 2.2 is satisfied with and , then Assumption 2.2 is also satisfied with replaced by the closure of (the ambient space being equipped with the metric ) and the same constant .

Remark 2.5.

The set encodes assumptions imposed on the cdfs of each treatment outcome. In particular, the larger , the less restrictive is for . Ideally, one would thus like , which, however, is too much to ask for some functionals. Furthermore, there is a trade-off between the sizes of and , in the sense that a larger class typically requires a larger constant . The reader who wants to get an impression of some of the classes of cdfs we consider may want to consult Appendix D.1, where important classes of cdfs are defined.

2.1 Functionals that satisfy Assumption 2.2: A summary of results in Appendix D and Appendix F

In the present paper, we do not contribute to the construction of functionals for specific questions. Rather, we take the functional as given. To choose an appropriate functional, the policy maker can already draw on a very rich and still expanding body of literature; cf. Lambert (2001), Chakravarty (2009) or Cowell (2011) for textbook-treatments. To equip the reader with a specific and important example of a functional , one may think of the Gini-welfare measure (cf. Sen (1974))

| (6) |

Because all of our results impose Assumption 2.2, a natural question concerns its generality. To convince the reader that Assumption 2.2 is often satisfied, and to make the policies studied implementable (as they require knowledge of ), we show in Appendix D that Assumption 2.2 is satisfied for many important inequality, welfare, and poverty measures (together with formal results concerning the sets along with corresponding constants ). For example, it is shown that for the above Gini-welfare measure, Assumption 2.2 is satisfied with , i.e., without any restriction on the treatment cdfs (apart from having support ), and with constant . At this point we highlight some further functionals that satisfy Assumption 2.2:

-

1.

The inequality measures we discuss in Appendix D.2 include the Schutz-coefficient (Schutz (1951), Rosenbluth (1951)), the Gini-index, the class of linear inequality measures of Mehran (1976), the generalized entropy family of inequality indices including Theil’s index, the Atkinson family of inequality indices (Atkinson (1970)), and the family of Kolm-indices (Kolm (1976a)). In many cases, we discuss both relative and absolute versions of these measures.

-

2.

In Appendix D.3 we provide results for welfare measures based on inequality measures.

- 3.

The results in Appendices D.2, D.3, and D.4 mentioned above are obtained from and supplemented by a series of general results that we develop in Appendix F. These results verify Assumption 2.2 for U-functionals defined in Equation (151) (i.e., population versions of U-statistics, e.g., the mean or the variance), quantiles, generalized L-functionals due to Serfling (1984) defined in Equation (169), and trimmed U-functionals defined in Equation (176). These techniques are of particular interest in case one wants to apply our results to functionals that we do not explicitly discuss in Appendix D.

The results in Appendix D and Appendix F could also be of independent interest, because they immediately allow the construction of uniformly valid (over ) confidence intervals and tests in finite samples. To see this, observe that Assumption 2.2 together with the measurability Assumption 2.6 given further below and the Dvoretzky-Kiefer-Wolfowitz-Massart inequality in Massart (1990) implies that, uniformly over , the confidence interval covers with probability not smaller than ; here denotes the empirical cdf based on an i.i.d. sample of size from .

2.2 Further notation and an additional assumption

Before we consider maximal expected regret properties of certain classes of policies, we need to introduce some more notation: Given a policy and , we denote the number of times treatment has been assigned up to time by

| (7) |

and we abbreviate . Defining the loss incurred due to assigning treatment instead of an optimal one by , the regret , which was defined in Equation (3), can equivalently be written as

| (8) |

On the event we define the empirical cdf based on the outcomes of all subjects in that have been assigned to treatment

| (9) |

Note that the random sampling times such that depend on previously observed treatment outcomes.

We shall frequently need an assumption that guarantees that the functional evaluated at empirical cdfs, such as just defined in Equation (9), is measurable.

Assumption 2.6.

For every , the function on that is defined via i.e., evaluated at the empirical cdf corresponding to , is Borel measurable.

Assumption 2.6 is typically satisfied and imposes no practical restrictions.

Finally, and following up on the discussion in Remark 2.1, we shall introduce some notational simplifications in case a policy is such that is independent of , i.e., is an anytime policy. It is then easily seen that the random quantities and do not depend on (as long as and are such that ). Therefore, for such policies, we shall drop the index in these quantities.

3 Explore-then-commit policies

A natural approach to assigning subjects to treatments in our sequential setup would be to first conduct a randomized controlled trial (RCT) to study which treatment is best, and then to use the acquired knowledge to assign the inferred best treatment to all remaining subjects. Such policies are special cases of explore-then-commit policies, which we study in this section. Informally, an explore-then-commit policy deserves its name as it (i) uses the first subjects to explore, in the sense that every treatment is assigned, in expectation, at least proportionally to ; and (ii) then commits to a single (inferred best) treatment after the first treatments have been used for exploration. Here, may depend on the horizon .

Formally, we define an explore-then-commit policy as follows.

Definition 3.1 (Explore-then-commit policy).

A policy is an explore-then-commit policy, if there exists a function and an , such that for every we have that , and such that the following conditions hold for every :

-

1.

Exploration Condition: We have that

Here, the first infimum is taken over all potential outcome vectors such that the marginals for have a cdf in .

[That is, regardless of the (unknown) underlying marginal distributions of the potential outcomes, each treatment is assigned, in expectation, at least times among the first subjects.]

-

2.

Commitment Condition: There exists a function such that, for every , we have

(10) where is the vector of the last coordinates of .

[That is, the subjects are all assigned to the same treatment, which is selected based on the outcomes and randomizations observed during the exploration period.]

It would easily be possible to let the commitment rule depend on further external randomization. For simplicity, we omit formalizing such a generalization. We shall now discuss some important examples of explore-then-commit policies.

Example 3.2.

A policy that first conducts an RCT based on a sample of subjects, followed by any assignment rule for subjects that satisfies the commitment condition in Definition 3.1, is an explore-then-commit policy, provided the concrete randomization scheme used in the RCT encompasses sufficient exploration. In particular, with for every and every satisfies the exploration condition in Definition 3.1 with ; more generally, Definition 3.1 holds if . Alternatively, a policy that enforces balancedness in the exploration phase through assigning subjects to treatments “cyclically,” i.e., , satisfies the exploration condition in Definition 3.1 with if for every . Concrete choices for commitment rules for subjects include:

-

1.

In case , a typical approach is to assign the fall-back treatment if, according to some test, the alternative treatment is not significantly better, and to assign the alternative treatment if it is significantly better. The sample size used in the RCT is typically chosen to ensure that the specific test used achieves a desired power against a certain effect size. We refer to the description of the ETC-T policy in Section 5.1.1 for a specific example of a test and a corresponding rule for choosing , of which we establish that it achieves the desired power requirement (while holding the size).

-

2.

As an alternative to test-based commitment rules, one can use an empirical success rule as in Manski (2004), which in our general context amounts to assigning an element of to subjects . Specific examples of such a policy, together with concrete ways of choosing that come with certain performance guarantees, are discussed in Policy 1 below and in the description of the ETC-ES policy in Section 5.1.1.

We now establish regret lower bounds for the class of explore-then-commit policies. To exclude trivial cases, we assume that (which is typically convex) contains a line segment on which the functional is not everywhere constant.

Assumption 3.3.

The functional satisfies Assumption 2.2, and contains two elements and , such that

| (11) |

and such that .

Since there only have to exist two cdfs and as in Assumption 3.3, this is a condition that is practically always satisfied.

The next theorem considers general explore-then-commit policies, as well as the subclass of policies where holds for every for some . This subclass models situations, where the horizon is unknown or ignored in planning the experiment, and the envisioned number of subjects used for exploration is fixed in advance (here for every , and , else); the subclass also models situations where the sample size that can be used for experimentation is limited due to budget constraints.

Theorem 3.4.

Suppose and that Assumption 3.3 holds. Then the following statements hold:777The constants depend on properties of the function for . More specifically, the constants depend on the quantities and from Lemma A.4. The precise dependence is made explicit in the proof.

-

1.

There exists a constant , such that, for every explore-then-commit policy that satisfies the exploration condition with , and for any randomization measure, it holds that

-

2.

For every there exists a constant , such that, for every explore-then-commit policy that satisfies (i) the exploration condition with and (ii) , and for any randomization measure, it holds that

The first part of Theorem 3.4 shows that, under the minimal assumption of containing a line segment on which is not constant, any explore-then-commit policy must incur maximal expected regret that increases at least of order in the horizon .

The second part implies in particular that when is unknown, such that the exploration period cannot depend on it, any explore-then-commit policy must incur linear maximal expected regret. We note that this is the worst possible rate of regret, since by Assumption 2.2 no policy can have larger than linear maximal expected regret.

The lower bounds on maximal expected regret are obtained by taking the maximum only over all potential outcome vectors with marginal distributions in the line segment in Equation (11). This is a one-parametric subset of over which nevertheless varies sufficiently to obtain a good lower bound.

We now prove that a maximal expected regret of rate is attainable in the class of explore-then-commit policies, i.e., we show that the lower bound in the first part of Theorem 3.4 cannot be improved upon. In particular, we show that employing an empirical success type commitment rule after an RCT in the exploration phase as discussed in Example 3.2 yields a maximal expected regret of this order. To be precise, we consider the following policy, which in contrast to test-based commitment rules (which require the choice of a suitable test and taking into account multiple-comparison issues in case ) can be implemented seamlessly for any number of treatments:

Note that the policy is an explore-then-commit policy that requires knowledge of the horizon , which by Theorem 3.4 is necessary for obtaining a rate slower than . The outer minimum in the second for loop in the policy is just taken to break ties (if necessary). Our result concerning is as follows (an identical statement can be established for a version of with cyclical assignment during the exploration phase as discussed in Remark 3.2; the proof follows along the same lines, and we skip the details).

Theorem 3.5.

Theorems 3.4 and 3.5 together prove that within the class of explore-then-commit policies, the policy is rate optimal in . An upper bound as in Theorem 3.5 for the special case of the mean functional can be found in Chapter 6 of Lattimore and Szepesvári (2020). We shall next show that policies which do not separate the exploration and commitment phase can obtain lower maximal expected regret. In this sense, the natural idea of separating exploration and commitment phases turns out to be suboptimal from a decision-theoretic point-of-view in functional sequential treatment assignment problems.

The finding that for large classes of functional targets explore-then-commit policies are suboptimal in terms of maximal expected regret does, of course, by no means discredit RCTs and subsequent testing for other purposes. For example, RCTs are often used to test for a causal effect of a treatment, cf. Imbens and Wooldridge (2009) for an overview and further references. The goal of the present article is not to test for a causal effect, but to assist the policy maker in minimizing regret, i.e., to keep to a minimum the sum of all losses due to assigning subjects wrongly. This goal, as pointed out in, e.g., Manski (2004), Manski and Tetenov (2016) and Manski (2019b), is only weakly related to testing. For example, the policy maker may care about more than just controlling the probabilities of Type 1 and Type 2 errors. In particular the magnitude of the losses when errors occur are important components of regret.

4 Functional UCB-type policies and regret bounds

In this section we define and study two policies based on upper-confidence-bounds. We start with the Functional Upper Confidence Bound (F-UCB) policy. It is inspired by the UCB1 policy of Auer et al. (2002) for multi-armed bandit problems targeting the mean, which is derived from a policy in Agrawal (1995), building on Lai and Robbins (1985). Extensions of the UCB1 policy to targeting risk functionals have been considered by Sani et al. (2012), Maillard (2013), Zimin et al. (2014), Vakili and Zhao (2016), and Vakili et al. (2018). The F-UCB policy can target any functional (and reduces to the UCB1 policy of Auer et al. (2002) in case one targets the mean). It has the practical advantage of not needing to know the horizon , cf. Remark 2.1 (recall also the notation introduced in Section 2.2). Furthermore, no external randomization is required, which will therefore be notationally suppressed as an argument to the policy. The policy is defined as follows, where is the constant from Assumption 2.2.

After the initialization rounds, the F-UCB policy assigns a treatment that i) is promising, in the sense that is large, or ii) has not been well explored, in the sense that is small. The parameter is chosen by the researcher and indicates the weight put on assigning scarcely explored treatments, i.e., treatments with low . An optimal choice of , minimizing the upper bound on maximal expected regret, is given after Theorem 4.1 below. We use the notation for .

The upper bound on maximal expected regret just obtained is increasing in the number of available treatments . This is due to the fact that it becomes harder to find the best treatment as the number of available treatments increases. Note also that the choice minimizes and implies .

In case of the mean functional, an upper bound as in Theorem 4.1 can be obtained from Theorem 1 in Auer et al. (2002) as explained after Theorem 2 in Audibert and Bubeck (2009), cf. also the discussion in Section 2.4.3 of Bubeck and Cesa-Bianchi (2012).888High-probability bounds as in Theorem 8 in Audibert et al. (2009) can also be obtained for the F-UCB policy, cf. Theorem B.3 in Appendix B.2.3. The proof of Theorem 4.1 is inspired by their arguments. However, we cannot exploit the specific structure of the mean functional and related concentration inequalities. Instead we rely on the high-level condition of Assumption 2.2 and the Dvoretzky-Kiefer-Wolfowitz-Massart inequality as established by Massart (1990) to obtain suitable concentration inequalities, cf. Equation (149) in Appendix F. Since adaptive sampling introduces dependence, we also need to take care of the fact that the empirical cdfs defined in (9) are not directly based on a fixed number of i.i.d. random variables. This is done via the optional skipping theorem of Doob (1936), cf. Appendix B.2.1. For functionals that can be written as a Lipschitz-continuous function of the first and second moment (a situation where Assumption 2.2 holds), an upper bound of the same order as in Theorem 4.1 has been obtained in Kock and Thyrsgaard (2017) for a successive-elimination type policy.

The lower bound in Theorem 3.4 combined with the upper bound in Theorem 4.1 shows that the maximal expected regret incurred by any explore-then-commit policy grows much faster in than that of the F-UCB policy. What is more, the F-UCB policy achieves this without making use of the horizon . Thus, in particular when is unknown, a large improvement is obtained over any explore-then-commit policy, as the order of the regret decreases from to . Hence, in terms of maximal expected regret, the policy maker is not recommended to separate the exploration and commitment phases.

Theorem 4.1 leaves open the possibility that one can construct policies with even slower growth rates of maximal expected regret. We now turn to establishing a lower bound on maximal expected regret within the class of all policies. In particular, the theorem also applies to policies that incorporate the horizon .

Theorem 4.2.

Suppose and that Assumption 3.3 holds. Then there exists a constant , such that for any policy and any randomization measure, it holds that

| (14) |

Under the same assumptions used to establish the lower bound on maximal expected regret in the class of explore-then-commit policies, Theorem 4.2 shows that any policy must incur maximal expected regret of order at least . In combination with Theorem 4.1 this shows that, up to a multiplicative factor of , no policy exists that has a better dependence of maximal expected regret on than the F-UCB policy. In this sense the F-UCB policy is near minimax (rate-) optimal.

For the special case of the mean functional a lower bound as in Theorem 4.2 was given in Theorem 7.1 in Auer et al. (1995). Their proof is based on suitably chosen Bernoulli cdfs with parameters about , and thus provides a lower bound over all sets containing these cdfs, in particular over . Depending on the functional considered, however, Bernoulli cdfs may not create sufficient variation in the functional to get good lower bounds. Furthermore, Bernoulli cdfs may not be contained in , if, e.g., the latter does not contain discrete cdfs, in which case a lower bound derived for Bernoulli cdfs is not informative. For these two reasons, we have tailored the lower bound towards the functional and parameter space under consideration. As in the proof of Theorem 3.4 this is achieved by working with a suitably chosen one-parametric family of binary mixture cdfs of elements of the functional-specific line segment ; cf. Lemma A.4 in Appendix A.

It is natural to ask whether a policy exists, which avoids the factor of appearing in Theorem 4.1. In the special case of the mean functional, Audibert and Bubeck (2009) and Degenne and Perchet (2016) answered this question affirmatively for the MOSS policy and an anytime MOSS policy, respectively. As the second policy in this section, following the construction in Degenne and Perchet (2016), we now consider a Functional anytime MOSS (F-aMOSS) policy, and establish an upper bound on its maximal expected regret that matches the lower bound in Theorem 4.2. The policy is of UCB-type in the sense that it proceeds similarly as Policy 2, but uses a slightly different confidence bound; cf. Policy 3 where for we write ,

A regret upper bound for the F-aMOSS policy is given next.

Theorem 4.3.

To prove the result, we generalize to the functional setup a novel argument recently put forward by Garivier et al. (2018) for obtaining a regret upper bound for the anytime MOSS policy of Degenne and Perchet (2016). As in the proof of Theorem 4.1 we need to replace arguments relying on concentration inequalities for the mean, and rely heavily on optional skipping arguments. Furthermore, in contrast to Garivier et al. (2018), we do not only consider the case , but we show that the argument actually goes through for , also expanding the range considered in Degenne and Perchet (2016).999Interestingly, in the special case of the mean functional (with ), Theorem 4.3 shows that the multiplicative constant given in Theorem 3 of Degenne and Perchet (2016) for can be improved to . This establishes theoretical guarantees for parameter values close to , which turned out best in their numerical results (but for which no regret guarantees were provided). Finally, we note that while the upper bound just given is of the order , and improves on the upper bound for the F-UCB policy in this sense, this is bought at a price: the multiplicative constant appearing in the upper bound is larger than that obtained in Theorem 4.1.

5 Numerical illustrations

We now illustrate the theoretical results established in this article by means of simulation experiments. Throughout this section, the treatment outcome distributions will be taken from the Beta family, a parametric subset of , which has a long history in modeling income distributions; see, for example, Thurow (1970), McDonald (1984) and McDonald and Ransom (2008). An appealing characteristic of the Beta family is its ability to replicate many “shapes” of distributions. We emphasize that the policies investigated do not exploit that the unknown treatment outcome distributions are elements of the Beta family.

Our numerical results cover different functionals , with a focus on situations where the policy maker targets the distribution that maximizes welfare, and where we consider the case and . In all our examples the feasible set for the marginal distributions of the treatment outcomes .

The specific welfare measures we consider are as follows (and correspond to the Gini-, Schutz- and Atkinson- inequality measure, respectively, through the transformations detailed in Appendix D.3, to which we refer the reader for more background information):

-

1.

Gini-index-based welfare measure: , where denotes the mean of .

-

2.

Schutz-coefficient-based welfare measure: .

-

3.

Atkinson-index-based welfare measure: for a parameter .

In this section we consider two settings: (A) we compare the performance of explore-then-commit policies which do not incorporate with the F-UCB and the F-aMOSS policy (which also do not incorporate ); (B) as in (A) but where we now consider explore-then-commit policies that optimally incorporate . Throughout in this section, we consider the case of treatments. In the following, the symbol shall denote one of the welfare measures just defined in the above enumeration.

5.1 Numerical results in Setting A

In this setting the total number of assignments to be made is not known from the outset. Thus, the policies we study do not make use of the horizon . We consider explore-then-commit policies as in Section 3, the F-UCB policy, and the F-aMOSS policy. While the F-UCB policy is implemented as in Policy 2 of Section 4 with , and the F-aMOSS policy is implemented as in Policy 3 with , the concrete development of explore-then-commit policies with certain performance guarantees requires some additional work which we develop next.

5.1.1 Implementation details for explore-then-commit policies

In all explore-then-commit policies we consider, Treatments 1 and 2 are assigned cyclically in the exploration period. This ensures that the number of assignments to each treatment differs at most by (cf. also Example 3.2 in Section 3).101010Investigating policies with randomized assignment in the exploration phase would necessitate running the simulations repeatedly, averaging over different draws for the assignments in the exploration phase. The numerical results are already quite computationally intensive, which is why we only investigate a cyclical assignment scheme. This scheme already reflects to a good extent the average behavior of a randomized assignment with equal assignment probabilities. Given this specification, the policy maker must still choose i) the length of the exploration period , and ii) a commitment rule to be used after the exploration phase. The choice of (while independent of ) depends on the commitment rule, of which we now develop a test-based and an empirical-success-based variant:

-

1.

ETC-T: This policy is built around a test-based commitment rule. That is, one uses a test for the testing problem “equal welfare of treatments,” i.e., , in deciding which treatment to choose after the exploration phase.

Given a test that satisfies a pre-specified size requirement, the length of the exploration phase is chosen such that the power of the test against a certain deviation from the null (effect size) is at least of a desired magnitude. A typical desired amount of power against the deviation from the null of interest is 0.8 or 0.9.

The deviation from the null that one wishes to detect is clearly context dependent. We refer to Jacob (1988), Murphy et al. (2014) and Athey and Imbens (2017), as well as references therein, for in-depth treatments of power calculations.

To make this approach implementable, we need to construct an appropriate test. Given , and for , we shall consider the test that rejects if (and only if) with . Under the null, i.e., for every pair and in such that , this test has rejection probability at most (a proof of this statement is provided in Appendix B.3.1). Hence, the size of this test does not exceed .

For this test, in order to detect a deviation of with probability at least , where , it suffices that (for a proof of this statement, see Appendix B.3.2).

In our numerical studies we set . We consider , which amounts to a small and moderate desired detectable effect size, respectively. Note that while choosing small allows one to detect small differences in the functionals by the above test, this comes at the price of a larger . Thus, we shall see that neither nor dominates the other uniformly (over ) in terms of maximal expected regret. The commitment rule applied is to assign if the above test rejects, and to randomize the treatment assignment with equal probabilities otherwise. Finally, we sometimes make the dependence of ETC-T on explicit by writing ETC-T().

-

2.

ETC-ES: This policy assigns to subjects , which is an empirical success commitment rule inspired by Manski (2004) and Manski and Tetenov (2016). Here, given a , is chosen such that the maximal expected regret for every subject to be treated after the exploration phase is at most ; i.e., satisfies

We prove in Appendix B.3.3 that suffices.

In our numerical results, we consider , which should be contrasted to the treatment outcomes taking values in . Note that the required to guarantee a maximal expected regret of at most for every subject treated after the exploration phase is decreasing in . Thus, we shall see that it need not be the case that choosing smaller will result in lower overall maximal expected regret. Finally, we sometimes make the dependence of ETC-ES on explicit by writing ETC-ES().

The following display summarizes the numerical implementation.

Since maximizing expected regret over all Beta distributions would be numerically infeasible, we have chosen to maximize expected regret over a subset of all Beta distributions indexed by as defined in the previous display. We stress that since none of the three policies above needs to know , the numerical results also contain the maximal expected regret of the policies for any sample size less than .

5.1.2 Results

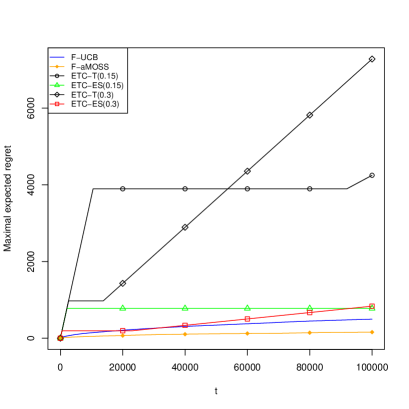

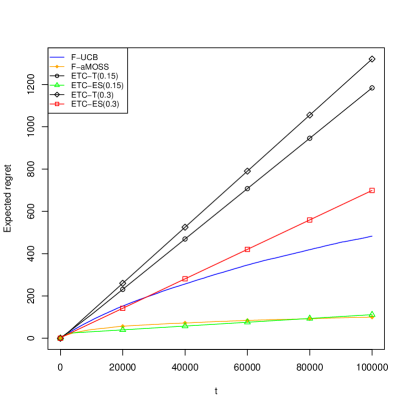

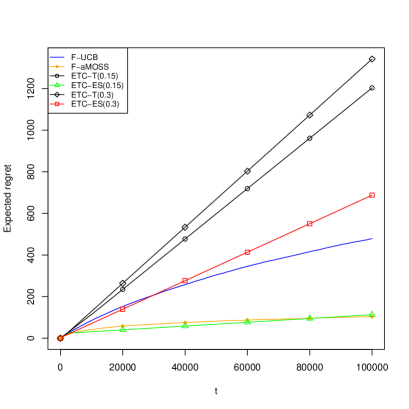

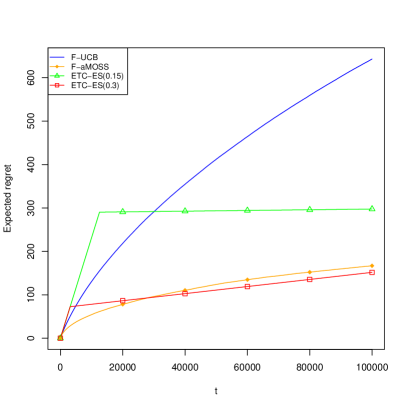

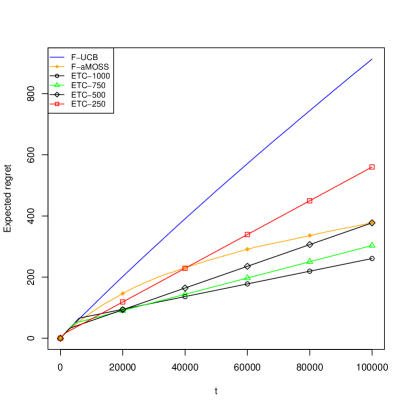

The left panel of Figure 1 illustrates the maximal expected regret for the F-UCB, F-aMOSS, ETC-T and ETC-ES policies in the case of Gini-welfare. Each point on the six graphs is the maximum of expected regret over the different distributions considered at a given . In accordance with Theorems 3.4, 4.1 and 4.3, the maximal expected regret of the policies in the explore-then-commit family is generally higher than the one of the F-UCB and the F-aMOSS policy. For , the maximal expected regret of F-UCB is , and for F-aMOSS, while the corresponding numbers for ETC-T(0.15), ETC-ES(0.15), ETC-T(0.30) and ETC-ES(0.30) are , , and , respectively. Note also that no matter the values of and , the maximal expected regret of ETC-ES() is much lower than the one of the ETC-T() policy.111111This result on the ranking of test-based vs. empirical success-based commitment rules is similar to an analogous finding in a non-sequential setting in Manski and Tetenov (2016). In fact, we shall see for all functionals considered that the F-aMOSS policy generally incurs the lowest maximal expected regret, followed by the F-UCB policy and subsequently by the ETC-ES policies, which in turn perform much better than ETC-T policies.

The shape of the graphs of the maximal expected regret of the explore-then-commit policies can be explained as follows: in the exploration phase maximal expected regret is attained by a distribution , say, for which the value of the Gini-welfare differs strongly at the marginals. However, such distributions are also relatively easy to distinguish, such that none of the commitment rules (testing or empirical success) assigns the suboptimal treatment after the exploration phase. This results in no more regret being incurred and thus a horizontal part on the maximal expected regret graph. For sufficiently large, however, maximal expected regret will be attained by a distribution , say, for which the marginals are sufficiently “close” to imply that the commitment rules occasionally assign the suboptimal treatment. For such a distribution, the expected regret curve will have a positive linear increase even after the commitment time and this curve will eventually cross the horizontal part of the expected regret curve pertaining to . This implies that maximal expected regret increases again (as seen for ETC-T(0.30) around and ETC-ES(0.30) around in the left panel of Figure 1). Such a kink also occurs for ETC-T(0.15) and eventually also for ETC-ES(0.15). Thus, the left panel of Figure 1 illustrates the tension between choosing small in order to avoid incurring high regret in the exploration phase and, on the other hand, choosing large in order to ensure making the correct decision at the commitment time.

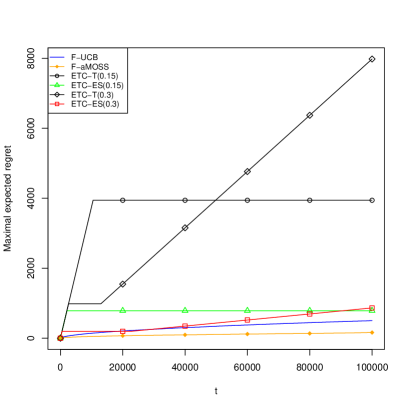

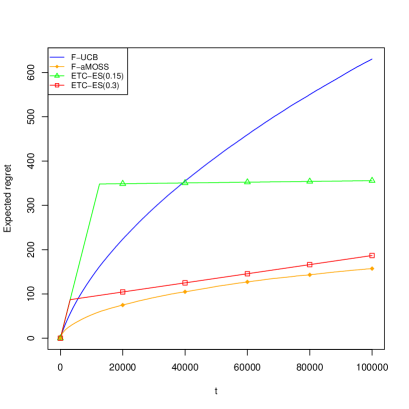

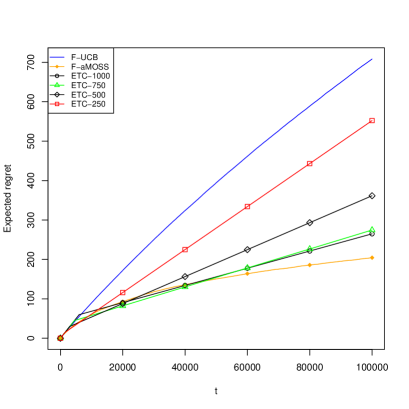

The right panel of Figure 1, which contains the maximal expected regret for the Schutz-welfare, yields results qualitatively similar to the ones for the Gini-welfare. The best explore-then-commit policy again has a terminal maximal expected regret that is more than times that of the F-aMOSS policy.

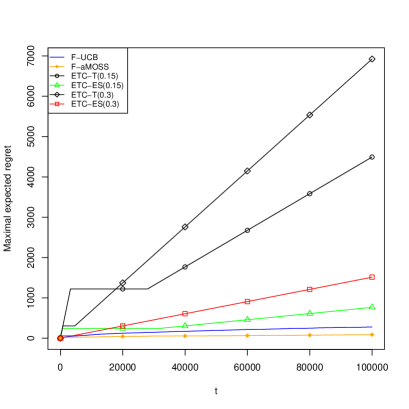

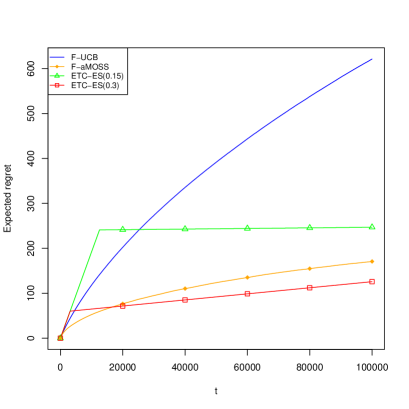

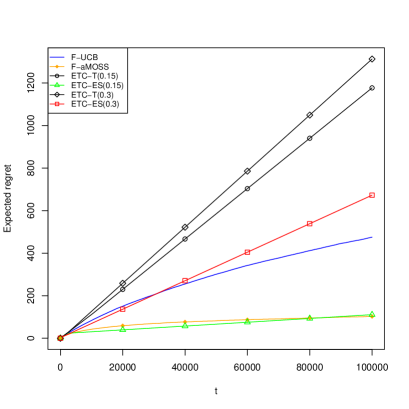

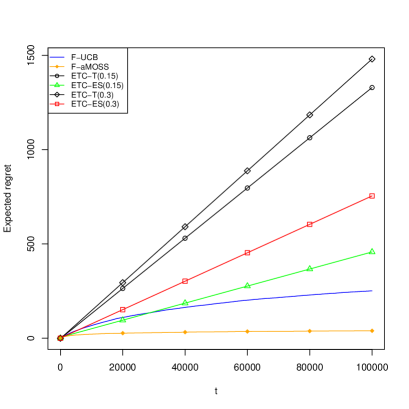

We next turn to the two welfare measures in the Atkinson family. The left panel of Figure 2 contains the results for the case of . While F-aMOSS incurs the lowest maximal expected regret uniformly over , the most remarkable feature of the figure is that maximal expected regret of all explore-then-commit policies is eventually increasing within the sample considered. The reason for this is that implies a low value of such that i) the steep increase in maximal expected regret becomes shorter and ii) more mistakes are made at the commitment time. The ranking of the families of polices is unaltered with F-UCB and F-aMOSS dominating ETC-ES, which in turn incurs much lower regret than ETC-T.

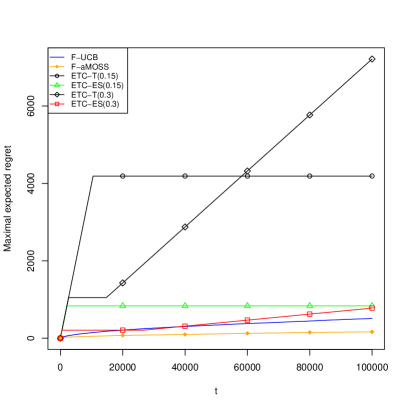

The right panel of Figure 2 considers the case of Atkinson welfare when . The findings are qualitatively similar to the ones for the Gini- and Schutz-based welfare measures.

5.2 Numerical results in Setting B

5.2.1 Implementation details

In this section we compare the explore-then-commit Policy 1 (but with cyclical assignment in the exploration phase, cf. Footnote 10) with the F-UCB policy as implemented as in the previous subsection. Note that Policy 1 depends on in an optimal way, cf. Theorem 3.5, while the F-UCB policy does not incorporate .

5.2.2 Results

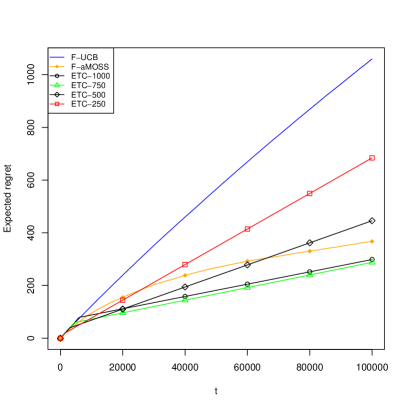

Table 1 contains maximal expected regret computations for Policy 1 relative to that of the F-UCB policy for . Thus, numbers larger than 1 indicate that the F-UCB policy has lower maximal expected regret. Since Policy 1 is not anytime, cf. Remark 2.1, to study its regret behavior it must be implemented and run anew for each ; i.e., for each we proceed as in the display describing the implementation details for Setting A, but only record the terminal value of the numerically determined maximal expected regret. Producing a plot analogous to Figure 1 but for a policy incorporating would require us to run the simulation 100,000 times, i.e., one simulation per terminal sample size , which would be extremely computationally intensive.121212To reduce the computational cost we set in the results reported in the present section. As can be seen from Table 1, the F-UCB policy achieves lower expected regret than Policy 1 at all considered horizons for all welfare measures even though the former policy does not make use of while the latter does. Note also that the relative improvement of the F-UCB policy over Policy 1 is increasing in as suggested by our theoretical results.

| 1,000 | 5,000 | 10,000 | 20,000 | 40,000 | 60,000 | |

|---|---|---|---|---|---|---|

| Gini | 1.96 | 2.30 | 2.49 | 2.64 | 2.89 | 3.10 |

| Schutz | 2.02 | 2.34 | 2.47 | 2.68 | 2.86 | 3.10 |

| Atkinson, | 3.46 | 3.94 | 4.16 | 4.77 | 5.34 | 5.20 |

| Atkinson, | 2.21 | 2.48 | 2.65 | 2.86 | 3.05 | 3.27 |

As shown by the simulation results reported in the previous section, using the F-aMOSS policy as a benchmark instead of the F-UCB policy would lead to even larger relative improvements over the explore-then-commit Policy 1.

6 Illustrations with empirical data

We here compare the performance of the policies using three (non-sequentially generated) empirical data sets, each containing the outcomes of a treatment program. From every data set we generate synthetic sequential data by sampling from the empirical cdfs corresponding to the treatment/control groups. That is, the empirical cdfs in the data sets are taken as the respective (unknown) treatment outcome distributions , from which observations are then drawn sequentially. This approach allows us to study the policies’ performance on cdfs resembling specific characteristics arising in large scale empirical applications. The data sets considered are as follows; cf. also Appendix C.

-

1.

The Cognitive Abilities program studied in Hardy et al. (2015). In this RCT, the participants were split into a treatment group who participated in an online training program targeting various cognitive capacities and an active control group solving crossword puzzles. Thus, . The outcome variable is a neuropsychological performance measure.

- 2.

-

3.

The Pennsylvania Reemployment Bonus program studied originally in Bilias (2000) and also in, e.g., Chernozhukov et al. (2018). The participants in the program are unemployed individuals who are either assigned to a control group, or to one of five treatment groups who receive a cash bonus if they find and retain a job within a given qualification period. Thus, . The size of the cash bonus and the length of the qualification period vary across the five treatment groups. The outcome variable is unemployment duration which varies from 1 to 52 weeks.

To facilitate the comparision with the other results in the previous section, all data were scaled to , and we consider the Gini-, Schutz- and two Atkinson-welfare measures. We focus on the Gini-based-welfare, and report the results for the remaining functionals in Appendix C. The reported expected regrets are averages over replications, with in each setup. When interpreting the results, it is important to keep in mind that in contrast to the maximal expected regret studied in Section 5, where for each the worst-case regret over a certain family of distributions is reported, the focus is now on three particular data sets, i.e., three instances of pointwise expected regret w.r.t. fixed distributions.

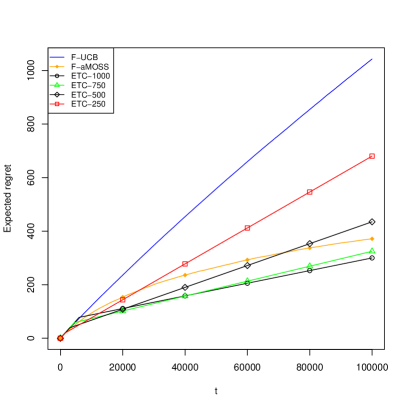

For the Detroit Work First Program, for which , the ETC-ES policies are implemented as in Section 5.1.1 with . For the Pennsylvania Reemployment Bonus experiment, where , this rule led to exploration periods exceeding . Hence, we instead considered exploration periods assigning and observations to each of the six arms, respectively. We only implemented the ETC-T policies for the cognitive ability program for which .131313This is justified by the fact that these policies were always inferior in Section 5. Furthermore, implementing the ETC-T policies when would require taking a stance on how to control the size of the (multiple) testing problem at the commitment time. The F-UCB and F-aMOSS policies are implemented as in Section 5.

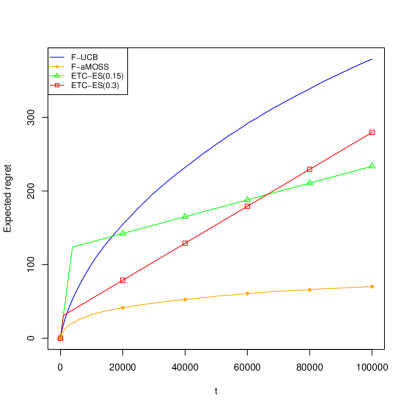

The results for the Gini-welfare measure are summarized in Figure 3. The main take-aways are: i) F-aMOSS performs solidly across all data sets. ii) Except for the cognitive training program data, the F-UCB policy is not among the best. Note that this is not in contradiction to the theoretical results of this paper (nor the simulations in Section 5) as these are concerned with the worst-case performance of the policies. iii) There always exists an exploration horizon such that an ETC-ES policy incurs a low expected regret (over the sample sizes considered). However, this horizon is data dependent: Note that for the cognitive and Pennsylvania data sets long exploration horizons are preferable, while for the Work First data the opposite is the case. From the Pennsylvania data it is also seen that the optimal length of the exploration horizon depends on the length of the program.

The figures containing the results for the remaining functionals are contained in Appendix C. For the Schutz- and Atkinson-welfare measure with the results are qualitatively similar to those of the Gini-based welfare. Regarding the Atkinson-based welfare with , F-aMOSS and F-UCB now even incur the lowest regret for the cognitive data. For the Work First and Pennsylvania data F-aMOSS remains best (at the end of the program). It is interesting that for the Work First data the ordering of the two ETC-ES policies is reversed at the end of the treatment period compared to the remaining functionals. The latter observation again underscores the difficulty in getting the length of the exploration period “right.” This echoes our theoretical results showing that there is no way of constructing an ETC-based rule that would uniformly dominate the UCB-type policies.

7 Conclusion

In this paper we have studied the problem of a policy maker who assigns sequentially arriving subjects to treatments. The quality of a treatment is measured through a functional of the potential outcome distributions. Drawing crucially on the results and the framework developed in the present paper, the companion paper Kock et al. (2020a) studies how the setting and regret notion can be adapted to allow for covariates, and explores how those can be optimally incorporated in the decision process.

References

- Abadie (2002) Abadie, A. (2002): “Bootstrap tests for distributional treatment effects in instrumental variable models,” Journal of the American Statistical Association, 97, 284–292.

- Abadie et al. (2002) Abadie, A., J. Angrist, and G. Imbens (2002): “Instrumental variables estimates of the effect of subsidized training on the quantiles of trainee earnings,” Econometrica, 70, 91–117.

- Agrawal (1995) Agrawal, R. (1995): “Sample mean based index policies with O (log n) regret for the multi-armed bandit problem,” Advances in Applied Probability, 1054–1078.

- Athey and Imbens (2017) Athey, S. and G. W. Imbens (2017): “The econometrics of randomized experiments,” in Handbook of Economic Field Experiments, Elsevier, vol. 1, 73–140.

- Athey and Wager (2017) Athey, S. and S. Wager (2017): “Efficient policy learning,” arXiv preprint arXiv:1702.02896.

- Atkinson (1970) Atkinson, A. B. (1970): “On the measurement of inequality,” Journal of Economic Theory, 2, 244–263.

- Audibert and Bubeck (2009) Audibert, J. and S. Bubeck (2009): “Minimax Policies for Adversarial and Stochastic Bandits,” in Proceedings of the 22nd Conference on Learning Theory, 217–226.

- Audibert et al. (2009) Audibert, J.-Y., R. Munos, and C. Szepesvári (2009): “Exploration–exploitation tradeoff using variance estimates in multi-armed bandits,” Theoretical Computer Science, 410, 1876–1902.

- Auer et al. (2002) Auer, P., N. Cesa-Bianchi, and P. Fischer (2002): “Finite-time analysis of the multiarmed bandit problem,” Machine Learning, 47, 235–256.

- Auer et al. (1995) Auer, P., N. Cesa-Bianchi, Y. Freund, and R. E. Schapire (1995): “Gambling in a rigged casino: The adversarial multi-armed bandit problem,” in Proceedings of IEEE 36th Annual Foundations of Computer Science, IEEE, 322–331.

- Autor et al. (2017) Autor, D. H., S. N. Houseman, and S. P. Kerr (2017): “The effect of Work First job placements on the distribution of earnings: An instrumental variable quantile regression approach,” Journal of Labor Economics, 35, 149–190.

- Autor and Houseman (2010) Autor, David, H. and S. N. Houseman (2010): “Do temporary-help jobs improve labor market outcomes for low-skilled workers? Evidence from ”Work First”,” American Economic Journal: Applied Economics, 2, 96–128.

- Barrett and Donald (2009) Barrett, G. F. and S. G. Donald (2009): “Statistical inference with generalized Gini indices of inequality, poverty, and welfare,” Journal of Business & Economic Statistics, 27, 1–17.

- Bhattacharya and Dupas (2012) Bhattacharya, D. and P. Dupas (2012): “Inferring welfare maximizing treatment assignment under budget constraints,” Journal of Econometrics, 167, 168–196.

- Bilias (2000) Bilias, Y. (2000): “Sequential testing of duration data: the case of the Pennsylvania ‘reemployment bonus’ experiment,” Journal of Applied Econometrics, 15, 575–594.

- Blackorby and Donaldson (1978) Blackorby, C. and D. Donaldson (1978): “Measures of relative equality and their meaning in terms of social welfare,” Journal of Economic Theory, 18, 59–80.

- Blackorby and Donaldson (1980) ——— (1980): “A theoretical treatment of indices of absolute inequality,” International Economic Review, 21, 107–136.

- Bubeck and Cesa-Bianchi (2012) Bubeck, S. and N. Cesa-Bianchi (2012): “Regret analysis of stochastic and nonstochastic multi-armed bandit problems,” Foundations and Trends® in Machine Learning, 5, 1–122.

- Burke (2003) Burke, M. R. (2003): “Borel measurability of separately continuous functions,” Topology and its Applications, 129, 29 – 65.

- Cassel et al. (2018) Cassel, A., S. Mannor, and A. Zeevi (2018): “A General Approach to Multi-Armed Bandits Under Risk Criteria,” in Proceedings of the 31st Conference On Learning Theory, ed. by S. Bubeck, V. Perchet, and P. Rigollet, vol. 75 of Proceedings of Machine Learning Research, 1295–1306.

- Chakravarty (1983) Chakravarty, S. R. (1983): “A new index of poverty,” Mathematical Social Sciences, 6, 307–313.

- Chakravarty (2009) ——— (2009): Inequality, Polarization and Poverty, New York: Springer.

- Chamberlain (2000) Chamberlain, G. (2000): “Econometrics and decision theory,” Journal of Econometrics, 95, 255–283.

- Chao and Strawderman (1972) Chao, M.-T. and W. Strawderman (1972): “Negative moments of positive random variables,” Journal of the American Statistical Association, 67, 429–431.

- Chernozhukov et al. (2018) Chernozhukov, V., D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins (2018): “Double/debiased machine learning for treatment and structural parameters,” The Econometrics Journal, 21, C1–C68.

- Chernozhukov et al. (2013) Chernozhukov, V., I. Fernández-Val, and B. Melly (2013): “Inference on counterfactual distributions,” Econometrica, 81, 2205–2268.

- Chernozhukov and Hansen (2005) Chernozhukov, V. and C. Hansen (2005): “An IV model of quantile treatment effects,” Econometrica, 73, 245–261.

- Cowell (2011) Cowell, F. (2011): Measuring Inequality, Oxford: Oxford University Press.

- Cowell (1980) Cowell, F. A. (1980): “Generalized entropy and the measurement of distributional change,” European Economic Review, 13, 147–159.

- Dagum (1990) Dagum, C. (1990): “On the relationship between income inequality measures and social welfare functions,” Journal of Econometrics, 43, 91–102.

- Dalton (1920) Dalton, H. (1920): “The measurement of the inequality of incomes,” Economic Journal, 30, 348–361.

- Davidson and Duclos (2000) Davidson, R. and J.-Y. Duclos (2000): “Statistical inference for stochastic dominance and for the measurement of poverty and inequality,” Econometrica, 68, 1435–1464.

- Davidson and Flachaire (2007) Davidson, R. and E. Flachaire (2007): “Asymptotic and bootstrap inference for inequality and poverty measures,” Journal of Econometrics, 141, 141 – 166.

- Degenne and Perchet (2016) Degenne, R. and V. Perchet (2016): “Anytime optimal algorithms in stochastic multi-armed bandits,” in International Conference on Machine Learning, 1587–1595.

- Dehejia (2005) Dehejia, R. H. (2005): “Program evaluation as a decision problem,” Journal of Econometrics, 125, 141–173.

- Doob (1936) Doob, J. (1936): “Note on probability,” Annals of Mathematics, 363–367.

- Dudley (2002) Dudley, R. M. (2002): Real Analysis and Probability, Cambridge University Press.

- Embrechts and Hofert (2013) Embrechts, P. and M. Hofert (2013): “A note on generalized inverses,” Mathematical Methods of Operations Research, 77, 423–432.

- Folland (1999) Folland, G. B. (1999): Real Analysis: Modern Techniques and their Applications, New York: Wiley.

- Foster et al. (1984) Foster, J., J. Greer, and E. Thorbecke (1984): “A class of decomposable poverty measures,” Econometrica, 52, 761–766.

- Foster et al. (2010) ——— (2010): “The Foster–Greer–Thorbecke (FGT) poverty measures: 25 years later,” Journal of Economic Inequality, 8, 491–524.

- Garivier et al. (2018) Garivier, A., H. Hadiji, P. Menard, and G. Stoltz (2018): “KL-UCB-switch: optimal regret bounds for stochastic bandits from both a distribution-dependent and a distribution-free viewpoints,” arXiv preprint arXiv:1805.05071.

- Garivier et al. (2016) Garivier, A., T. Lattimore, and E. Kaufmann (2016): “On explore-then-commit strategies,” in Advances in Neural Information Processing Systems, 784–792.

- Gastwirth (1971) Gastwirth, J. L. (1971): “A general definition of the Lorenz curve,” Econometrica, 39, 1037–1039.

- Gastwirth (1974) ——— (1974): “Large sample theory of some measures of income inequality,” Econometrica, 42, 191–196.

- Gittins (1979) Gittins, J. C. (1979): “Bandit processes and dynamic allocation indices,” Journal of the Royal Statistical Society: Series B, 41, 148–164.

- Hardy et al. (2015) Hardy, J. L., R. A. Nelson, M. E. Thomason, D. A. Sternberg, K. Katovich, F. Farzin, and M. Scanlon (2015): “Enhancing cognitive abilities with comprehensive training: a large, online, randomized, active-controlled trial,” PloS ONE, 10.

- Hirano and Porter (2009) Hirano, K. and J. R. Porter (2009): “Asymptotics for statistical treatment rules,” Econometrica, 77, 1683–1701.

- Hirano and Porter (2018) ——— (2018): “Statistical decision rules in econometrics,” Working paper.

- Imbens and Wooldridge (2009) Imbens, G. W. and J. M. Wooldridge (2009): “Recent developments in the econometrics of program evaluation,” Journal of Economic Literature, 47, 5–86.

- Jacob (1988) Jacob, C. (1988): Statistical Power for the Behavioral Sciences, Lawrence Erlbaum Associates, Publishers.

- Kakwani (1980) Kakwani, N. (1980): “On a class of poverty measures,” Econometrica, 437–446.

- Kakwani (1986) ——— (1986): Analyzing Redistribution Policies: A Study Using Australian Data, Cambridge: Cambridge University Press.

- Kallenberg (2005) Kallenberg, O. (2005): Probabilistic Symmetries and Invariance Principles, New York: Springer.

- Kitagawa and Tetenov (2018) Kitagawa, T. and A. Tetenov (2018): “Who should be treated? Empirical welfare maximization methods for treatment choice,” Econometrica, 86, 591–616.

- Kitagawa and Tetenov (2019) ——— (2019): “Equality-Minded Treatment Choice,” Journal of Business & Economic Statistics, 0, 1–14.

- Kock et al. (2020a) Kock, A. B., D. Preinerstorfer, and B. Veliyev (2020a): “Functional Sequential Treatment Allocation with Covariates,” arXiv preprint arXiv:2001.10996.

- Kock et al. (2020b) ——— (2020b): “Treatment recommendation with distributional targets,” arXiv preprint arXiv:2005.09717.

- Kock and Thyrsgaard (2017) Kock, A. B. and M. Thyrsgaard (2017): “Optimal sequential treatment allocation,” arXiv preprint arXiv:1705.09952.

- Kolm (1976a) Kolm, S.-C. (1976a): “Unequal inequalities. I,” Journal of Economic Theory, 12, 416–442.

- Kolm (1976b) ——— (1976b): “Unequal inequalities. II,” Journal of Economic Theory, 13, 82–111.

- Lai and Robbins (1985) Lai, T. L. and H. Robbins (1985): “Asymptotically efficient adaptive allocation rules,” Advances in Applied Mathematics, 6, 4–22.

- Lambert (2001) Lambert, P. J. (2001): The Distribution and Redistribution of Income, Manchester: Manchester University Press.

- Lattimore and Szepesvári (2020) Lattimore, T. and C. Szepesvári (2020): Bandit Algorithms, Cambridge: Cambridge University Press.

- Lavori et al. (2000) Lavori, P. W., R. Dawson, and A. J. Rush (2000): “Flexible treatment strategies in chronic disease: clinical and research implications,” Biological psychiatry, 48, 605–614.

- Liese and Miescke (2008) Liese, F. and K. J. Miescke (2008): Statistical Decision Theory, New York: Springer.

- Maillard (2013) Maillard, O.-A. (2013): “Robust Risk-Averse Stochastic Multi-armed Bandits,” in Algorithmic Learning Theory, ed. by S. Jain, R. Munos, F. Stephan, and T. Zeugmann, Berlin, Heidelberg: Springer Berlin Heidelberg, 218–233.

- Manski (1988) Manski, C. F. (1988): “Ordinal utility models of decision making under uncertainty,” Theory and Decision, 25, 79–104.

- Manski (2004) ——— (2004): “Statistical treatment rules for heterogeneous populations,” Econometrica, 72, 1221–1246.

- Manski (2019a) ——— (2019a): “Remarks on statistical inference for statistical decisions,” Tech. rep., Centre for Microdata Methods and Practice, Institute for Fiscal Studies.

- Manski (2019b) ——— (2019b): “Treatment choice with trial data: statistical decision theory should supplant hypothesis testing,” American Statistician, 73, 296–304.

- Manski and Tetenov (2016) Manski, C. F. and A. Tetenov (2016): “Sufficient trial size to inform clinical practice,” Proceedings of the National Academy of Sciences, 113, 10518–10523.

- Massart (1990) Massart, P. (1990): “The tight constant in the Dvoretzky-Kiefer-Wolfowitz inequality,” Annals of Probability, 18, 1269–1283.

- McDonald (1984) McDonald, J. B. (1984): “Some Generalized Functions for the Size Distribution of Income,” Econometrica, 52, 647–663.

- McDonald and Ransom (2008) McDonald, J. B. and M. Ransom (2008): “The generalized beta distribution as a model for the distribution of income: estimation of related measures of inequality,” in Modeling Income Distributions and Lorenz Curves, New York: Springer, 147–166.

- Mehran (1976) Mehran, F. (1976): “Linear measures of income inequality,” Econometrica, 44, 805–809.

- Mills and Zandvakili (1997) Mills, J. A. and S. Zandvakili (1997): “Statistical inference via bootstrapping for measures of inequality,” Journal of Applied Econometrics, 12, 133–150.

- Minassian (2007) Minassian, D. (2007): “A mean value theorem for one-sided derivatives,” American Mathematical Monthly, 114, 28.

- Murphy et al. (2014) Murphy, K. R., B. Myors, and A. Wolach (2014): Statistical Power Analysis: A Simple and General Model for Traditional and Modern Hypothesis Tests, New York: Routledge.

- Murphy (2003) Murphy, S. A. (2003): “Optimal dynamic treatment regimes,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 65, 331–355.

- Murphy (2005) ——— (2005): “An experimental design for the development of adaptive treatment strategies,” Statistics in medicine, 24, 1455–1481.

- Murphy et al. (2001) Murphy, S. A., M. J. van der Laan, and J. M. Robins (2001): “Marginal mean models for dynamic regimes,” Journal of the American Statistical Association, 96, 1410–1423.

- Perchet et al. (2016) Perchet, V., P. Rigollet, S. Chassang, and E. Snowberg (2016): “Batched bandit problems,” The Annals of Statistics, 44, 660–681.

- Robbins (1952) Robbins, H. (1952): “Some aspects of the sequential design of experiments,” Bulletin of the Americal Mathematical Society, 58, 527–535.

- Robins (1997) Robins, J. M. (1997): “Causal inference from complex longitudinal data,” in Latent variable modeling and applications to causality, ed. by M. Berkane, New York: Springer, 69–117.

- Rosenbluth (1951) Rosenbluth, G. (1951): “Note on Mr. Schutz’s measure of income inequality,” American Economic Review, 41, 935–937.

- Rostek (2010) Rostek, M. (2010): “Quantile maximization in decision theory,” Review of Economic Studies, 77, 339–371.

- Rothe (2010) Rothe, C. (2010): “Nonparametric estimation of distributional policy effects,” Journal of Econometrics, 155, 56–70.

- Rothe (2012) ——— (2012): “Partial distributional policy effects,” Econometrica, 80, 2269–2301.

- Sani et al. (2012) Sani, A., A. Lazaric, and R. Munos (2012): “Risk-Aversion in Multi-armed Bandits,” in Advances in Neural Information Processing Systems 25, ed. by F. Pereira, C. J. C. Burges, L. Bottou, and K. Q. Weinberger, Curran Associates, Inc., 3275–3283.

- Schluter and van Garderen (2009) Schluter, C. and K. J. van Garderen (2009): “Edgeworth expansions and normalizing transforms for inequality measures,” Journal of Econometrics, 150, 16 – 29.

- Schutz (1951) Schutz, R. R. (1951): “On the measurement of income inequality,” American Economic Review, 41, 107–122.

- Sen (1974) Sen, A. (1974): “Informational bases of alternative welfare approaches: Aggregation and income distribution,” Journal of Public Economics, 3, 387 – 403.

- Sen (1976) ——— (1976): “Poverty: an ordinal approach to measurement,” Econometrica, 219–231.

- Serfling (1984) Serfling, R. J. (1984): “Generalized L-, M-, and R-Statistics,” Annals of Statistics, 12, 76–86.

- Serfling (2009) ——— (2009): Approximation Theorems of Mathematical Statistics, vol. 162, New York: Wiley.

- Shorack and Wellner (2009) Shorack, G. R. and J. A. Wellner (2009): Empirical Processes with Applications to Statistics, Philadelphia: SIAM.

- Stoye (2009) Stoye, J. (2009): “Minimax regret treatment choice with finite samples,” Journal of Econometrics, 151, 70–81.

- Stoye (2012) ——— (2012): “Minimax regret treatment choice with covariates or with limited validity of experiments,” Journal of Econometrics, 166, 138–156.

- Tetenov (2012) Tetenov, A. (2012): “Statistical treatment choice based on asymmetric minimax regret criteria,” Journal of Econometrics, 166, 157–165.

- Theil (1967) Theil, H. (1967): Economics and Information Theory, Amsterdam: North-Holland.

- Thistle (1990) Thistle, P. D. (1990): “Large sample properties of two inequality indices,” Econometrica, 58, 725–728.

- Thompson (1933) Thompson, W. R. (1933): “On the likelihood that one unknown probability exceeds another in view of the evidence of two samples,” Biometrika, 25, 285–294.

- Thurow (1970) Thurow, L. C. (1970): “Analyzing the American income distribution,” American Economic Review, 60, 261–269.

- Tran-Thanh and Yu (2014) Tran-Thanh, L. and J. Y. Yu (2014): “Functional bandits,” arXiv preprint arXiv:1405.2432.

- Tsybakov (2009) Tsybakov, A. B. (2009): Introduction to Nonparametric Estimation, New York: Springer.

- Vakili et al. (2018) Vakili, S., A. Boukouvalas, and Q. Zhao (2018): “Decision Variance in Online Learning,” arXiv preprint arXiv:1807.09089.

- Vakili and Zhao (2016) Vakili, S. and Q. Zhao (2016): “Risk-Averse Multi-Armed Bandit Problems Under Mean-Variance Measure,” IEEE Journal of Selected Topics in Signal Processing, 10, 1093–1111.

- Witting and Müller-Funk (1995) Witting, H. and U. Müller-Funk (1995): Mathematische Statistik II, B.G. Teubner: Stuttgart.

- Zimin et al. (2014) Zimin, A., R. Ibsen-Jensen, and K. Chatterjee (2014): “Generalized risk-aversion in stochastic multi-armed bandits,” arXiv preprint arXiv:1405.0833.

Throughout the appendices, the (unique) probability measure on the Borel sets of corresponding to a cdf will be denoted by (cf., e.g., Folland (1999), p.35).

We shall freely use standard notation and terminology concerning stochastic kernels (also referred to as Markov kernels or probability kernels) and semi-direct products (i.e., the joint distribution corresponding to a stochastic kernel and a probability measure) see, e.g., Appendix A.3 of Liese and Miescke (2008) in particular their Equation A.3. Furthermore, the random variables and vectors appearing in the proofs are defined on an underlying probability space with corresponding expectation , which is (without loss of generality) assumed to be rich enough to support all random variables we work with. Furthermore, we shall denote by a generic element of .

We also recall from, e.g., Definition 2.5 in Tsybakov (2009), that the Kullback-Leibler divergence between two probability measures and on a measurable space is defined as

| (16) |

The integral appearing in this definition is well-defined, because the negative part of the integrand is -integrable. The positive part of the integrand is not necessarily -integrable. Therefore, might hold even in case . Furthermore, is non-negative, and equals if and only if . Proofs for the just-mentioned facts can be found in Section 2.4 of Tsybakov (2009). Note that the definition of does not depend on how one defines (for completeness, we set in the sequel).

Appendix A Auxiliary results

This section develops some auxiliary lemmas that will be used in Appendix B. The following result is a general “chain rule” for Kullback-Leibler divergences. Although well-documented under stronger assumptions, we could not find a reference containing a proof of the following general statement.

Lemma A.1 (“Chain rule” for Kullback-Leibler divergence).

Let and be measurable spaces. Suppose that is countably generated. Let be stochastic kernels, and let and be probability measures on . Then,

| (17) |

Remark A.2.