Optimal Covariance Matrix Estimation for High-dimensional Noise in High-frequency Data

Abstract

We consider high-dimensional measurement errors with high-frequency data. Our objective is on recovering the high-dimensional cross-sectional covariance matrix of the random errors with optimality. In this problem, not all components of the random vector are observed at the same time and the measurement errors are latent variables, leading to major challenges besides high data dimensionality. We propose a new covariance matrix estimator in this context with appropriate localization and thresholding, and then conduct a series of comprehensive theoretical investigations of the proposed estimator. By developing a new technical device integrating the high-frequency data feature with the conventional notion of -mixing, our analysis successfully accommodates the challenging serial dependence in the measurement errors. Our theoretical analysis establishes the minimax optimal convergence rates associated with two commonly used loss functions; and we demonstrate with concrete cases when the proposed localized estimator with thresholding achieves the minimax optimal convergence rates. Considering that the variances and covariances can be small in reality, we conduct a second-order theoretical analysis that further disentangles the dominating bias in the estimator. A bias-corrected estimator is then proposed to ensure its practical finite sample performance. We also extensively analyze our estimator in the setting with jumps, and show that its performance is reasonably robust. We illustrate the promising empirical performance of the proposed estimator with extensive simulation studies and a real data analysis.

Keywords: High-dimensional covariance matrix; High-frequency data analysis; Measurement error; Minimax optimality; Thresholding.

JEL code: C13, C55, C58

1 Introduction

High-frequency data broadly refer to those collected at time points with very small time intervals between consecutive observations. Exemplary scenarios with high-frequency data include longitudinal observations with intensive repeated measurements (Bolger and Laurenceau, 2013), the tick-by-tick trading data in finance (Zhang et al., 2005), and functional data with dense observations (Zhang and Wang, 2016). High-frequency data are commonly contaminated by some noise, broadly termed as the measurement errors. For measurement errors in the context of functional data analysis, we refer to the review article Wang et al. (2016) and reference therein. In high-frequency financial data, as another example, the microstructure noise is well known; see the monograph Aït-Sahalia and Jacod (2014) for an overview.

Despite the central interests on recovering the signals contaminated by the noise, the properties of the noise themselves are of their own great interests. Recently, Jacod et al. (2017) highlighted the importance of statistical properties of the microstructure noise and studied the estimation of its moments; see the recent study of Li and Linton (2022) on the limiting distributions in a broad setting. Chang et al. (2018) investigated recovering the distribution of the noise with some frequency-domain analysis. In a simultaneous and independent work of ours, Da and Xiu (2021) investigated the auto-covariance of the measurement errors with a semiparametric approach that utilizing a working moving-average model. These aforementioned studies aimed on univariate cases. Ubukata and Oya (2009) considered the covariance estimation and testing for measurement errors in a bivariate case. Christensen et al. (2013) proposed an estimator for the covariance matrix of the noise vector in high-frequency finance data. Both Ubukata and Oya (2009) and Christensen et al. (2013) handled fixed dimensional cases with -dependent or independent measurement errors.

We are motivated to concentrate on high-dimensional cases in this study that shed light on influential practical applications where covariances between different components of the noise could bring us useful information in solving various problems. For example, for functional-type observations, the covariations between the measurement errors may help identifying the common source or reasons of contaminations so that improvement can be developed in designing future investigations. For financial data, such covariations in the high-dimensional microstructure noise may help in better understanding the trading behaviors that may show substantial different pattern between equities. Indeed, Li et al. (2016) found that a parametric function incorporating the market information may account for a substantial contribution to the variations in the microstructure noise. Nevertheless, studying the covariance between different components of the high-dimensional noise in high-frequency data remains little explored.

Our primary interests in this study are on the validity and optimality of the covariance matrix estimation procedure for the high-dimensional noise in high-frequency data. This problem has unique challenges from multiple aspects. First, since the noise of interest are not directly observable, the targeted random vectors are latent. Second, the latency arises together with high data dimensionality and high sampling frequency, two challenging features that interrelates to each other in this investigation. The high-dimensional noise sequence is expected to contain serial dependence, posing a major methodological and theoretical challenge. The properties of high-dimensional covariance matrix estimation have not yet been explored in this important scenario. Third, the high-dimensional observations may not be synchronous, i.e. different components of the contaminated observation for the high-dimensional noise may be observed at different time points. How these data features affect the statistical properties on the validity and optimality of the covariance matrix estimation remains unclear.

High-dimensional covariance matrix estimation is an important problem in the current state of knowledge, and has received intensive attentions in the past decade; see, among others, Bickel and Levina (2008a, b), Lam and Fan (2009), Rothman et al. (2009), Cai et al. (2010), Cai and Liu (2011) and Cai and Zhou (2012a, b). For high-dimensional sparse covariance matrices, the minimax optimality of the estimations were investigated in-depth in Cai and Zhou (2012a, b). We note that the existing estimation methods for high-dimensional sparse covariance matrices are developed when the underlying data of interest are fully observed; hence they are not applicable for the covariance matrix estimation of the noise in high-frequency data with latency and asynchronous observations. In the literature on multivariate and high-dimensional high-frequency data analysis, existing studies mainly concern the estimations of the so-called realized covariance matrix. Specifically, the major objective is on the signal part, attempting to eliminate the impact from the noise; see, for example, Aït-Sahalia et al. (2010), Fan et al. (2012), Tao et al. (2013), Liu and Tang (2014), Lam et al. (2017), and Xia and Zheng (2018). However, it remains little explored on the high-dimensional covariance matrix of the noises in high-frequency data, accommondating all aforementioned challenging features.

Our study makes several contributions to the area. To our best knowledge, our method is the first handling covariance matrix estimation of the serially dependent high-dimensional noises in high-frequency data. Methodologically, to overcome the difficulties due to the latency, asynchronicity, and serially dependent observations, we propose a new approach with appropriate localization and thresholding. Theoretically, to our best knowledge, our technical device integrating high-frequency serial dependence with the -mixing is a new development of the current state of knowledge; and it can be more broadly applied for solving this class of problems. Meanwhile, our theoretical analysis establishes the minimax optimal convergence rates associated with two commonly used loss functions for the covariance matrix estimations of the high-dimensional noise in high-frequency data. The minimax optimal rates in this setting are our new theoretical discoveries, and we establish cases when the proposed estimator achieves such rates. Our result also reveals that the optimal convergence rates reflect the impact due to the asynchronous data, which are slower than those with synchronous data. The higher the level of the data asynchronicity is, the slower the convergence rates are expected. We show that the proposed localized estimator has the same accuracy as if the high-dimensional noise are directly observed in the sense of the same convergence rates. Furthermore, our theory includes a second-order analysis revealing the dominating bias of the estimator. We then propose a bias-corrected estimator and show that removing such a bias leads to more promising performance, especially when components in the covariance matrix are small. Our analysis also indicates that the proposed localized estimator is robust to the setting with jumps.

The rest of this paper is organized as follows. The methodology is outlined in Section 2, followed by theoretical development in Section 3. Section 4 presents the theory and method handling situation when the level of the noises is small. Section 5 investigates the robustness of our method in the setting with jumps. Numerical studies with simulation and a real data analysis are presented in Section 6. Section 7 includes some discussions. All technical proofs are given in Section 8. Some additional numerical results are presented in the supplementary material.

2 Methodology

2.1 Model and data

We introduce some notations first. For any positive integer , we write . For a matrix , let , , , and , where denotes the largest eigenvalue of . Denote by the indicator function. For a countable set , we use to denote its cardinality. For two sequences of positive numbers and , we write or if there exist a positive constant and a large enough integer such that for all . We write if and only if and hold simultaneously.

The setting of our study contains the signal part – a -dimensional continuous-time process , where, without loss of generality, is the time frame in which the high-frequency data are observed. We begin with a setting that satisfies:

| (1) |

where and are progressively measurable processes, and are univariate standard Brownian motions. Here and are, respectively, governing the volatilities and correlations, where both of them may be dynamic over time. A theoretical study of our method in the setting with jumps will be considered in Section 5.

For each , we use to denote the grid of time points at which we observe the noisy data of the th component process , where . The subject-specific set reflects the asynchronous nature of the problem. For the special case with synchronous data, all ’s are the same. However, ’s are typically different in many practical high-frequency data. Let be the number of different time points in , and we denote the different time points in by . For any , we define

where evaluates how many time points ’s at which we observe the noisy data of the th and th component processes and simultaneously. Clearly, for any .

We consider that the actual observed data are contaminated by additive measurement errors in the sense that

with for each and . The additive noise assumption is common in the literature; see Aït-Sahalia and Jacod (2014). Formally, we can write

| (2) |

and assume the measurement errors are independent of the process . At each time point , we only observe components of .

Besides the cross-sectional dependence, serial dependence is expected to be the case for ; our study accommodates such a feature with an innovative device. Denote by and the -fields generated by and , respectively, the -mixing coefficients are defined as

| (3) |

Then is an -mixing sequence if as . The notion of -mixing is a conventional foundation for broadly characterizing the serial dependence. Among others, causal ARMA processes with continuous innovation distributions are -mixing with exponentially decaying -mixing coefficients, so are stationary Markov chains satisfying certain conditions; see Section 2.6.1 of Fan and Yao (2003). Stationary GARCH models with finite second moments and continuous innovation distributions are also -mixing with exponentially decaying -mixing coefficients; see Proposition 12 of Carrasco and Chen (2002). Under certain conditions, vector auto-regressive (VAR) processes, multivariate ARCH processes, and multivariate GARCH processes are all -mixing with exponentially decaying -mixing coefficients; see Hafner and Preminger (2009), Boussama et al. (2011) and Wong et al. (2020).

In (3), we highlight the necessary inclusion of , the frequency related sample size, in the -mixing coefficient. The reason is that in a high-dimensional data setting, is commonly specified as a function of the sample size . Such an intrinsic dependence makes characterizing the serial dependence substantially more challenging. To handle it in our study, we impose the following assumption on defined in (3).

Assumption 1.

There exist some universal constants , and such that for any , where may diverge with .

Assumption 1 is our new dedicated device for characterizing the serial dependence of in the context of high-frequency high-dimensional data. Here is introduced as a parameter to handle the aforementioned challenge due to the high data dimensionality, together with the conventional as in the -mixing settings for analyzing time series. As a development of its own interests, the synthetic device in Assumption 1 successfully integrates the considerations of high-frequency and high-dimensional data, where the usual interpretation of the -mixing remains: the between-observation dependence is still getting weaker when they are further away in the serial data, as characterized by both and . Intuitively, the rationale is that , as a standalone parameter, may diverge together with the sampling frequency and data dimensionality in a synthetic manner. Such a divergence reflects the nature of this more challenging problem due to relatively limited data information, in the sense that the serial dependence in the measurement errors will become stronger as increases.

More specifically, Assumption 1 does not require to be strictly stationary, and it includes several commonly used models for as special cases. For an independent sequence , we can select and in Assumption 1. For an -dependent sequence , we can select in Assumption 1. If follows VAR model, multivariate ARCH model or multivariate GARCH model with certain conditions, we can select in Assumption 1. We provide a concrete example here with a diverging . For each , let satisfy the diffusion process , where is a univariate standard Brownian motion, and are two functions of with some parameters and , respectively. Write with independent processes . Letting for some known loading matrix and some , we can select and when and satisfy certain conditions111For each , Lemma 4 of Aït-Sahalia and Mykland (2004) indicates that is a -mixing process with -mixing coefficient for any integer , where is a constant depending on the properties of and (see Assumption 1 of Aït-Sahalia and Mykland (2004)). Theorem 5.1 of Bradley (2005) implies is also a -mixing process with -mixing coefficient for any integer , where . Since -mixing implies -mixing, then defined in (3) satisfies for any integer ., where will diverge with if as . Here is also allowed to depend directly on , the dimension of . As an example, if each univariate sequence is -mixing with exponentially decaying -mixing coefficients, with the independent assumption imposed on the sequences , Theorem 5.1 of Bradley (2005) indicates that defined in (3) satisfies for some universal constant , which implies Assumption 1 holds for and .

To our best knowledge, there is no alternative assumption in the literature that is capable of handling the setting of our study. In existing studies, some serial dependence assumptions have been imposed on the measurement errors, with a primary objective recovering its auto-covariance. When , Jacod et al. (2017) assumes for some nonnegative semimartingale and a -mixing stationary sequence , where is independent of the process ; see also the setting of Li and Linton (2022) that covers serially dependent, endogenous, and nonstationary noises. If is the solution of some stochastic differential equations, is also -mixing. See, for example, Lemma 4 of Aït-Sahalia and Mykland (2004). Based on the independence between and , Theorem 5.2 of Bradley (2005) implies the sequence is also -mixing. Since -mixing implies -mixing, we know is also -mixing. Varneskov (2017) relaxes the -mixing assumption on to the weaker -mixing condition. In a recent study, Da and Xiu (2021) assume instead a working moving average structure for the measurement errors.

For (2), we assume for each . Our main goal in this study is to estimate , the covariance matrix that contains information on the between-component relationship of the unobserved noise . Clearly, is a latent vector. To estimate its covariance matrix, eliminating the impact due to the process is required, which means that now performs like ‘signal’ and is ‘noise’. Our strategy is to perform a dedicated localization: focusing on observations that are in a specific neighborhood mentioned later. For any , we write with . Let for any . In this paper, we consider the scenario with being fixed but as . Formally, we make the following assumption:

Assumption 2.

(i) As , is uniformly bounded away from zero. (ii) As , we have each , and is uniformly bounded away from zero. (iii) .

The setting with Assumption 2 is broad and general. The first part is a standard setting for studying high-frequency data. The second part requires enough number of pairwise synchronous observations. This is a reasonable practical setting; see also Aït-Sahalia et al. (2010) for a pairwise approach for estimating the realized covariance matrix for . Based on part (ii) of Assumption 2, we write

| (4) |

where as . As we will show in Theorems 1–4, the convergence rates for the estimates of the covariance matrix will depend on instead of . In the special case with synchronous observations, we have for any and we can set . Then all our results also apply to the setting with synchronous data. Assumption 2 is not necessary for our theoretical analysis which is just imposed for simplicity and can be removed at the expenses of lengthier proofs. Our theoretical analysis essentially only requires the assumption that and as . With such assumption, both and can decay to zero as . We will discuss in Section 7 how this assumption affects the convergence rates for the estimates of the covariance matrix .

2.2 Covariance matrix estimation of

Write and . Here the subscript in indicates that it is a quantity associated with the noise so as to differentiate it from the volatility process in (1). We know for any . By Assumption 1 and Davydov’s inequality (Davydov, 1968), for some constant , provided that and are uniformly bounded away from infinity for some universal constant . Notice that and each component process is a continuous-time and continuous-path stochastic process. We have considerations from two ends. First, due to almost surely as , in a small neighborhood of , the difference between the high-frequency observations and , for , can be approximately viewed as . Second, to avoid excessive impact from aggregating , we cannot choose and too close. Putting these two considerations together, we propose to estimate by

| (5) |

where for some integers and , and . Here the set is designed to meet the aforementioned two considerations – ensuring data in an appropriate range are incorporated for estimating .

Our estimator (5) with is generally applicable. For an independent sequence , we can select and then for any due to in Assumption 1. For an -dependent sequence , we can select due to in Assumption 1 and then for any . For general case with , with selecting for some sufficiently large constant , , which is negligible in comparison to the bias from approximating by . To simplify our presentation, we assume is a fixed integer in this paper. Our theoretical results can be parallel extended to the scenario with diverging .

For a fixed , (4) and Assumption 2 imply that

Let

| (6) |

for defined as (5). Theorem 1 in Section 3 shows that the elements of are uniformly consistent to the corresponding elements of with a suitable selection of , i.e.

Theorem 2 in Section 3 shows that is the minimax optimal rate in the maximum element-wise loss for the covariance matrix estimations of the high-dimensional noise in high-frequency data. If is an independent or -dependent sequence with fixed , we can select as a fixed integer and then the associated convergence rate of is minimax optimal. For general cases with and fixed , with selecting for some , the convergence rate of is nearly optimal with an additional logarithm factor . More importantly, as we will discuss below Remark 3 in Section 3, is also the minimax optimal rate in the maximum element-wise loss for the covariance matrix estimations of if we have observations of the noise, which indicates that our estimator shares some oracle property and the proposed localization actually makes the impact of the latent process be negligible.

However, the aforementioned element-wise consistency and optimality do not imply their counterparts for the covariance matrix estimation with high-dimensional data. That is, the estimator may not be consistent to under the spectral norm when . This is a well-known phenomenon in high-dimensional covariance matrix estimation; see, among other, Bickel and Levina (2008a). For high-dimensional covariance matrix estimations, one often resorts to some classes of the target with extra information. With the extra information, the consistency under the spectral norm and other properties associated with the covariance matrix estimations can be well established. In this paper, we focus on the following class – the sparse covariance matrices considered in Bickel and Levina (2008b):

| (7) |

where and are two prescribed constants, and may diverge with . Here can be viewed as a parameter that characterizes the sparsity of , i.e., if is smaller, then is more sparse. If , we have

where evaluates the number of nonzero components in each row of .

For , we propose the following thresholding estimator based on the element-wise estimation given in (6):

| (8) |

where is a fixed constant for the thresholding level. Theorem 3 in Section 3 shows that such defined thresholding estimator is consistent to under the spectral norm with suitable selections of and , i.e.

| (9) |

Furthermore, Theorem 4 in Section 3 indicates that is the minimax optimal convergence rate with the spectral norm loss function for the covariance matrix estimations of the high-dimensional noise in high-frequency data, which is also the minimax optimal convergence rate in the spectral norm loss if we have observations of the noise directly. If is an independent or -dependent sequence with fixed , we can select as a fixed integer and then the associated convergence rate of is minimax optimal. For general cases with and fixed , with selecting for some , the convergence rate of is nearly optimal with an additional logarithm factor .

Remark 1.

In finite samples, the thresholding estimator given in (8) may not be positive definite in general. We can first apply the singular value decomposition to : , where are the eigenvalues of , and is an orthogonal matrix. If there are negative eigenvalues, we can use as the estimate of for some . Write and let be the eigenvalues of . Since , if is uniformly bounded away from zero and we select when , such defined is positive definite and also satisfies (9).

3 Theoretical analysis

In this section, we establish the theoretical properties of the proposed estimators. To mimic the high-dimensional scenario, we always assume for some universal constant in this paper. We also require the following assumptions.

Assumption 3.

Write . There exist some universal constants and such that for any , and .

Assumption 4.

There exist some universal constants , and such that (i) and for any , and ; (ii) and for any and .

Assumption 5.

There exist some universal constants , and such that for any and .

All assumptions are mild for studying high-dimensional covariance matrix estimations with high-frequency data. Assumption 3 requires that each component of is sub-Gaussian. Following Lemma 2.2 of Petrov (1995), we know that part (i) of Assumption 4 holds if there exist two positive constants and such that and for any , and . Assumption 5 describes the behavior of the tail probability of . If the spot volatility process is uniformly bounded away from infinity over and , we can select in Assumption 5. Then we have the following result.

Theorem 1.

Let denote the collections of models for such that , where the noises satisfy Assumption 3, follows model (1) with each and satisfying Assumptions 4 and 5, and the grids of time points satisfy Assumption 2. Let for some constant . Under Assumption 1, it holds that

provided that and , where is specified in (4) and .

Remark 2.

Theorem 1 gives the convergence rate of .

(i) For an independent sequence , due to and , provided that . For fixed , .

(ii) For an -dependent sequence , due to and , provided that . For fixed , with selecting a fixed . For diverging , with selecting and .

(iii) For the general cases with and fixed , to make , we need to select . If we select for some , .

Furthermore, Theorem 2 below shows that the convergence rate is minimax optimal in the maximum element-wise loss for the covariance matrix estimations of the high-dimensional noise in high-frequency data.

Theorem 2.

Let . Denote by the class of all measurable functionals of the data. Then

where is defined in Theorem 1.

Remark 3.

(i) If is an independent sequence or -dependent sequence with fixed , Remarks 2(i) and 2(ii) indicate that our proposed estimate is minimax optimal under the maximum element-wise loss.

(ii) For the general cases with and fixed , Remark 2(iii) indicates our proposed estimate is nearly minimax optimal under the maximum element-wise loss with an additional logarithm factor .

To establish the lower bound stated in Theorem 2, we essentially focus on a model belonging to with and for any and . Let for any . In this specific model, the latent process for any and thus the data we observed are . Here denotes the subvector of with components indexed by . Hence, is also the minimax optimal rate in the maximum element-wise loss for the covariance matrix estimations of with data , which indicates that the estimator shares some oracle property and the proposed localization actually makes the impact of the latent process be negligible.

Regarding the loss function under the spectral norm for the whole covariance matrix estimation, Theorem 3 establishes the convergence rate of the thresholding estimator defined as (8).

Theorem 3.

Let denote the collections of models for such that , where the noises satisfy Assumption 3 with the covariance matrix , follows model (1) with each and satisfying Assumptions 4 and 5, and the grids of time points satisfy Assumption 2. Let for some constant . Under Assumption 1, with sufficiently large constant in (8), it holds that

provided that and , where is specified in (4) and .

Our result in the following Theorem 4 justifies that the convergence rate is minimax optimal under the spectral norm loss function for the covariance matrix estimations of with the sparsity structure (7). Again, this rate is also the minimax optimal rate in the spectral norm loss for the covariance matrix estimations of with data .

Theorem 4.

Let . Denote by the class of all measurable functionals of the data. Then

provided that , where is defined in Theorem 3.

Remark 4.

In summary, we conclude that it is – the effective sample size of the pairwise synchronous observations – determining the convergence rate of the covariance matrix estimation of the noise . Practically, is expected to be smaller than – the total number of observation times. Hence, the accuracy of the covariance matrix estimation is affected by the level of data asynchronicity – the more asynchronous the data are, the more difficult it is to estimate . Another finding from our theoretical analysis is that although the noise are not directly observable, the localized estimator in some scenarios has the (nearly) same accuracy as the one when the noise are observed in the sense of the (nearly) same convergence rates for estimating with high-frequency data. From the practical perspective, it can be viewed as a bless from the high-frequency data with adequate amount of data information locally, so that the statistical properties of the noise can be accurately revealed.

4 The effect of the smallness of the noise

Our results in Section 3 assume that with fixed. Empirically, as pointed out in Hansen and Lund (2006), the magnitude of may be small; see also Christensen et al. (2014). To address this issue, we study the second-order property of our estimator concerning its bias.

For defined as (5), since is independent of , we have that

| (10) |

which indicates that the bias in includes three parts: , and . Proposition 2 in Section 8 shows that , but , causing a bias of order that summarized in Theorem 5. Under Assumptions 1 and 3, it follows from Davydov’s inequality that for some universal constant . If is an independent sequence or -dependent sequence, we know and then with . If , with selecting for some sufficiently large constant , will be negligible in comparison to .

From (4) and Theorem 5, we have that

| (11) |

provided that for some sufficiently large constant . Since , the second term on the right-hand side of (11) is asymptotically negligible if is not vanishing; our Theorem 5 implies that it is the leading term in the bias. Impact from the bias on could be empirically substantial, especially when is relatively small.

For any , let . As a remedy, we propose a bias-correction for as follows:

| (12) |

where is given in (5), and is an estimate of . Since is an integrated covariance, it can be estimated by existing approaches, for example, the polarization method (Aït-Sahalia et al., 2010), the two time scales approach (Zhang, 2011), the pre-averaging method (Jacod et al., 2009; Christensen et al., 2010), and the quasi-maximum likelihood approach (Liu and Tang, 2014). Section 6.1.2 gives details for calculating by the two time scales approach. Based on given in (12), we can obtain and , the bias-corrected version of defined as (6) and defined as (8), respectively, by replacing by . Theorem 6 indicates that and share the same convergence rates of and , respectively.

5 Impact from jumps and the robustness of our methods

We now consider the setting with jumps in the underlying process . Assume satisfies the following model:

| (13) |

where ’s, ’s, ’s and ’s are same as those in (1), ’s are the jump sizes, and ’s are counting processes. Our analysis reveals that our estimators proposed in Section 2.2 for are reasonably robust against jumps. In our theoretical analysis, we impose Assumptions 6 and 7 on the counting process and the jump size , respectively.

Assumption 6.

Let for any . There exist and some universal constants such that (i) for any and ; (ii) for any .

Assumption 7.

There exist some universal constants and such that for any and .

If is a Poisson process with intensity , then follows the Poisson distribution with parameter and Assumption 6 holds for . Assumption 7 controls the tail behavior of the random jump size . If the jump size is bounded from above uniformly for and , we can select in Assumption 7.

Recall for some integers and , and . For any , define

| (14) |

Let and

where is defined as (6). Analogous to (8), we define the thresholding version of as

| (15) |

where is a fixed constant for the thresholding level.

Our theory has two parts. As the first part, parallel to Theorems 1 and 3, we have the next theorem for the convergence rates of and .

Theorem 7.

Assume Assumptions 1–7 hold. Let and for some constant . If , and , where is specified in (4) and , then the following two assertions are satisfied:

Theorems 7(i) and 7(ii) can be viewed as the generalization of Theorems 1 and 3, respectively. If there are no jumps in , we have for any and , and then and . In this scenario, we can set for any and in Assumptions 6 and 7, respectively, which implies holds automatically and . Hence, the results of Theorems 7(i) and 7(ii) in this scenario are identical to Theorems 1 and 3, respectively.

In the second part of our theory, we establish the properties of itself. Since where with defined as (14), the gap between and is seen determined by an extra ‘bias’. We assume the following condition for controlling the tail probability of .

Assumption 8.

Each has independent increments. Let for any and . There exist and some universal constants such that (i) for any and ; (ii) for any .

Assumption 6 holds automatically under Assumption 8. If is a Poisson process with intensity , then follows the Poisson distribution with parameter and Assumption 8 holds for . Given Assumptions 7 and 8, we have the following theorem for the tail probability of .

Theorem 8.

Theorem 8 implies if , which leads to the robustness of our proposed estimators against possible jumps in the underlying process , as established in the following theorem.

6 Numerical studies

6.1 Simulations

6.1.1 Data generating procedure

We set , where with . For , we generated each from the following stochastic volatility model:

| (16) |

where are independent Poisson processes with intensity , and are univariate standard Brownian motions such that (i) are independent Brownian motions, and (ii) and . We considered two settings – with or without jumps: (i) which are independent of , and (ii) for and . We set , the same as that in the numerical studies of Aït-Sahalia et al. (2013) that mimics the empirical features of financial data (Aït-Sahalia and Kimmel, 2007). This setting is reasonable; comparable settings are found in existing studies (Aït-Sahalia and Yu, 2009; Aït-Sahalia et al., 2010; Liu and Tang, 2014; Aït-Sahalia and Xiu, 2017). The initial observations of were generated from a Gamma distribution . In our simulation, we set .

We took with ; here 1 unit of means one year, so is corresponding to a trading day. We first generated high-frequency data available at each second in a -hour period; this setting results in observations. By letting , we generated with from (16), and each element of from a stationary GARCH(1,1) model:

where is independently generated from ; the settings of will be described later. In this model, upon observing for each , we considered different settings for the signal-to-noise ratios by varying . Since the signal-to-noise ratio can be approximated by with in (16), we specified two selections of : (i) such that , and (ii) such that . In Part S1 of the supplementary material, we have also investigated the finite-sample performance of the proposed estimators when with and .

We studied the following three models for that controls the correlations:

-

Model 1: is a banded matrix, where , , , and for .

-

Model 2: , where , is the identity matrix of order , is the smallest eigenvalue of , and satisfies that , ’s are independently generated from the uniform distribution , ’s are independently generated from the Bernoulli distribution with successful probability 0.04.

-

Model 3: is a bandable matrix with .

We considered both synchronous and asynchronous high-frequency data in our simulation. To model the synchronous data setting, we took as the observed data where is the floor function; by varying , we simulated data sets of different sizes: larger means fewer observations. Then the time points where we observed the noisy data are with . In our numerical studies, we set . To model the asynchronous data setting, for each , we applied the Poisson process sampling scheme with intensity to for generating , the grid of time points at which we actually observed . The Poisson process sampling schemes for different ’s are independent. Based on this setting for asynchronous data, on average there were observations for each . We selected in our simulation.

6.1.2 Implementation of bias-correction

To obtain the bias-corrected estimator in (12), we need to calculate , the estimate of the integrated covariance . In the simulation, we applied the two time scales approach (Zhang, 2011) to estimate . Recall is the grid of time points we observed . For given , we first used the refresh time procedure (Barndorff-Nielsen et al., 2011) to synchronize the data if . More specifically, let the first refresh time point be , and then define the other refresh time points with as iteratively. Denoted by the resulting refresh time points for and , and write and for each . If , the refresh time points based on above procedure are identical to , and thus the associated . For given positive integers and , the two time scales estimator for is given by

| (17) |

where for any positive integer . Following Aït-Sahalia and Yu (2009), we set in our simulation.

6.1.3 Selections of and the thresholding level

To obtain defined as (5) in practice, we need to select the tuning parameters and . If each univariate sequence is -mixing with exponentially decaying -mixing coefficients222Such requirement can be easily satisfied in most commonly used univariate time series models. See our discussion below (3)., with the independent assumption imposed on the sequences , Theorem 5.1 of Bradley (2005) indicates that defined in (3) satisfies for some universal constant , which provides a rough upper bound for . Hence, Assumption 1 holds for and for some sufficiently small constant . Our theoretical results require and for some constant . To match these requirements, when we estimate , we can select for some small constant . In our simulation, we have tried and the associated results are similar. We suggest to select in practice. Since we use to approximate for , the bias issue caused by and will impact the performance of our estimators. Notice that a smaller results in a smaller bias. We need to select as some small positive integers. Table 1 shows that (i) the estimators with perform quite well, and (ii) the estimators with work best in most cases and perform quite close to the best ones in other cases. This verifies our claim that should be selected as some small integers. We suggest to select in practice.

Based on and , to derive their thresholding version and , we need to determine the thresholding level. Our theoretical analysis shows that the thresholding level should have the order . Notice that with . Since has the order , the long-run variance of the sequence has the order . To incorporate the heterogeneity of the estimators , we implemented the thresholding estimators in practice as

| (18) |

where is a constant, and is an estimate for the long-run variance of the sequence . Write . We chose in (18) as

where is a symmetric kernel function, is the bandwidth, for and otherwise. Andrews (1991) suggested the quadratic spectral kernel

with optimal bandwidth , where is the estimated autoregressive coefficient in the fitted AR(1) model for the sequence . In our simulation, we have tried and the associated results are similar. We suggest to select in practice.

6.1.4 Simulation results

For given estimator , we evaluated its relative estimation error in different settings. Table 1 summarizes the averages of the relative estimation errors based on 1000 repetitions. We have several observations. First, we find that in general, performs quite well for all cases with satisfactorily small relative estimation errors compared with . Further, performs quite well when but poorly when . This suggests that when the noise is quite small, the bias-correction is necessary. Second, as the dimension increases, the relative estimation errors worsen a bit, but at a very slow pace growing with . This demonstrates the promising performance of the thresholding method for handling high-dimensional covariance estimations. Third, as the sampling frequency becomes higher (smaller or ), the performance is improved by observing smaller relative estimation errors, reflecting the blessing to the covariance estimations with more high-frequency data. This is actually the reason why the performance of the estimator with synchronous data is better than that with asynchronous data when and are the same. Fourth, we find that the differences are small among the performances with different , especially when the data are synchronous. Fifth, we find that the empirical performance of the proposed estimators is robust to jumps, confirming our finding in Theorem 9.

In addition, for given estimator , we also calculated in Tables 2 and 3 the true positive rate (TPR) and the false positive rate (FPR) defined as

Since the covariance matrix considered in Model 3 has no exact zero element, we omit reporting the TPR and FPR in this case. Results in Tables 2 and 3 show that the TPRs of our proposed estimators for all cases are equal to 1 or quite close to 1, and the FPRs for all cases are almost 0. This indicates that our proposed thresholding method can recover the non-zero elements of the covariance matrix very accurately. From the results in Table 3 when the data are asynchronous with and 3, we find that performs a bit better than , and both and have lower TPRs when , which is reasonable as the signal-to-noise ratio in term of estimating the covariance matrix of noises is lower in this case. For the FPRs, we find that there is no big difference between the FPRs of with different values for . However, the FPRs of when are much higher than those when , showing the impact from weaker signal. This again suggests that the bias-correction is very helpful, especially for handling relatively weaker signals.

| Synchronous Data | Model 1 | Model 2 | Model 3 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Estimators | ||||||||||||

| 0.063 | 50 | 1 | 4.5(4.5) | 4.0(4.0) | 3.2(3.2) | 5.2(5.5) | 4.6(4.9) | 3.3(3.4) | 6.3(6.3) | 5.3(5.3) | 4.3(4.3) | |

| 2 | 4.5(4.5) | 4.0(4.0) | 3.2(3.2) | 5.3(5.6) | 4.7(4.9) | 3.3(3.5) | 6.1(6.0) | 5.2(5.1) | 4.2(4.2) | |||

| 3 | 4.6(4.6) | 4.1(4.1) | 3.2(3.3) | 5.6(5.9) | 4.8(5.1) | 3.4(3.6) | 5.9(5.9) | 5.0(5.0) | 4.1(4.1) | |||

| 1 | 4.6(4.6) | 4.1(4.2) | 3.3(3.3) | 5.3(5.5) | 4.7(4.9) | 3.4(3.5) | 6.4(6.4) | 5.4(5.4) | 4.4(4.3) | |||

| 2 | 4.6(4.6) | 4.2(4.2) | 3.3(3.3) | 5.3(5.6) | 4.7(5.0) | 3.4(3.6) | 6.1(6.1) | 5.2(5.2) | 4.2(4.2) | |||

| 3 | 4.7(4.7) | 4.2(4.3) | 3.3(3.4) | 5.6(5.9) | 4.9(5.2) | 3.5(3.7) | 6.0(6.0) | 5.1(5.1) | 4.1(4.1) | |||

| 100 | 1 | 5.2(5.2) | 4.4(4.4) | 3.6(3.6) | 5.7(5.9) | 4.6(4.7) | 3.5(3.5) | 7.0(6.9) | 6.0(6.0) | 4.8(4.7) | ||

| 2 | 5.2(5.2) | 4.4(4.4) | 3.6(3.6) | 5.8(5.9) | 4.6(4.7) | 3.5(3.6) | 6.7(6.7) | 5.8(5.8) | 4.6(4.6) | |||

| 3 | 5.3(5.3) | 4.5(4.5) | 3.6(3.7) | 6.0(6.1) | 4.8(4.9) | 3.6(3.7) | 6.6(6.5) | 5.7(5.7) | 4.6(4.5) | |||

| 1 | 5.3(5.4) | 4.5(4.5) | 3.7(3.7) | 5.8(6.0) | 4.7(4.8) | 3.6(3.7) | 7.1(7.0) | 6.1(6.1) | 4.8(4.8) | |||

| 2 | 5.4(5.4) | 4.5(4.6) | 3.7(3.7) | 5.9(6.1) | 4.8(4.9) | 3.7(3.7) | 6.9(6.8) | 5.9(5.9) | 4.7(4.6) | |||

| 3 | 5.5(5.5) | 4.6(4.7) | 3.8(3.8) | 6.1(6.3) | 5.0(5.1) | 3.8(3.9) | 6.8(6.7) | 5.8(5.8) | 4.6(4.6) | |||

| 200 | 1 | 6.0(6.0) | 5.0(5.0) | 4.0(4.0) | 5.5(5.5) | 4.4(4.5) | 3.3(3.4) | 7.5(7.6) | 6.5(6.5) | 5.2(5.1) | ||

| 2 | 5.9(5.9) | 5.0(5.0) | 4.0(4.0) | 5.4(5.5) | 4.4(4.5) | 3.3(3.3) | 7.3(7.3) | 6.3(6.3) | 5.0(5.0) | |||

| 3 | 5.9(5.9) | 5.0(5.0) | 4.0(4.0) | 5.4(5.5) | 4.5(4.5) | 3.3(3.3) | 7.2(7.2) | 6.3(6.2) | 5.0(4.9) | |||

| 1 | 6.2(6.2) | 5.2(5.2) | 4.2(4.2) | 5.7(5.7) | 4.6(4.7) | 3.6(3.6) | 7.7(7.8) | 6.6(6.6) | 5.3(5.2) | |||

| 2 | 6.3(6.3) | 5.3(5.3) | 4.2(4.2) | 5.7(5.7) | 4.7(4.7) | 3.6(3.6) | 7.5(7.6) | 6.5(6.5) | 5.1(5.1) | |||

| 3 | 6.3(6.3) | 5.4(5.4) | 4.3(4.3) | 5.8(5.8) | 4.8(4.8) | 3.6(3.7) | 7.5(7.5) | 6.4(6.4) | 5.1(5.1) | |||

| 0.00252 | 50 | 1 | 23.5(18.6) | 21.0(16.6) | 9.9(8.0) | 40.6(34.8) | 36.4(30.9) | 16.5(14.2) | 19.9(16.3) | 17.1(14.1) | 9.0(7.5) | |

| 2 | 28.2(22.1) | 24.3(19.0) | 11.5(9.1) | 49.0(41.6) | 42.1(35.7) | 19.4(16.6) | 22.7(18.6) | 19.0(15.7) | 10.0(8.3) | |||

| 3 | 33.0(25.9) | 27.5(21.6) | 13.1(10.4) | 57.4(49.0) | 47.6(40.7) | 22.4(19.0) | 25.5(20.9) | 20.9(17.3) | 10.9(9.1) | |||

| 1 | 4.6(4.6) | 4.1(4.1) | 3.3(3.3) | 5.7(5.8) | 4.9(5.1) | 3.4(3.5) | 6.7(6.7) | 5.6(5.5) | 4.4(4.4) | |||

| 2 | 4.7(4.6) | 4.1(4.1) | 3.3(3.3) | 5.9(6.1) | 5.0(5.2) | 3.4(3.6) | 6.5(6.4) | 5.4(5.4) | 4.3(4.3) | |||

| 3 | 4.8(4.7) | 4.2(4.2) | 3.3(3.3) | 6.3(6.5) | 5.2(5.4) | 3.6(3.7) | 6.3(6.3) | 5.3(5.3) | 4.2(4.2) | |||

| 100 | 1 | 31.9(32.1) | 20.5(20.8) | 12.6(12.8) | 46.7(48.9) | 29.8(31.4) | 18.0(19.0) | 25.5(25.3) | 17.1(17.2) | 11.0(10.9) | ||

| 2 | 36.7(36.6) | 23.8(23.9) | 14.2(14.3) | 53.7(56.0) | 34.7(36.2) | 20.5(21.5) | 28.2(28.0) | 19.0(19.1) | 11.9(11.9) | |||

| 3 | 41.5(41.3) | 27.1(27.0) | 15.9(16.0) | 60.7(63.0) | 39.5(41.0) | 23.0(24.0) | 31.1(30.7) | 21.0(21.0) | 12.9(12.8) | |||

| 1 | 5.4(5.4) | 4.5(4.5) | 3.7(3.7) | 6.4(6.5) | 4.9(4.9) | 3.7(3.7) | 7.5(7.4) | 6.3(6.3) | 4.9(4.8) | |||

| 2 | 5.4(5.4) | 4.5(4.5) | 3.7(3.7) | 6.6(6.7) | 5.0(5.1) | 3.7(3.8) | 7.3(7.2) | 6.1(6.1) | 4.8(4.7) | |||

| 3 | 5.6(5.6) | 4.6(4.7) | 3.7(3.8) | 6.9(7.0) | 5.2(5.3) | 3.8(3.9) | 7.2(7.1) | 6.0(6.0) | 4.7(4.6) | |||

| 200 | 1 | 40.8(40.9) | 26.5(26.6) | 15.5(15.6) | 44.7(45.4) | 29.0(29.4) | 16.8(17.1) | 31.0(30.9) | 21.0(21.1) | 12.8(12.9) | ||

| 2 | 45.4(45.5) | 29.7(29.7) | 17.2(17.2) | 49.8(50.5) | 32.5(32.9) | 18.6(18.9) | 33.8(33.6) | 22.9(22.9) | 13.8(13.8) | |||

| 3 | 50.1(50.1) | 32.9(32.8) | 18.8(18.8) | 55.0(55.6) | 35.9(36.3) | 20.4(20.6) | 36.7(36.5) | 24.8(24.8) | 14.7(14.8) | |||

| 1 | 7.5(6.2) | 5.4(5.1) | 4.2(4.1) | 8.3(6.4) | 5.7(4.8) | 3.8(3.6) | 8.2(8.2) | 6.9(6.9) | 5.3(5.3) | |||

| 2 | 8.1(6.3) | 5.7(5.2) | 4.2(4.1) | 8.9(6.5) | 6.1(4.9) | 3.9(3.6) | 8.1(8.1) | 6.7(6.7) | 5.2(5.2) | |||

| 3 | 8.8(6.5) | 6.0(5.3) | 4.3(4.2) | 9.6(6.7) | 6.6(5.0) | 4.1(3.7) | 8.0(8.0) | 6.7(6.6) | 5.2(5.1) | |||

| Asynchronous Data | Model 1 | Model 2 | Model 3 | |||||||||

| Estimators | ||||||||||||

| 0.063 | 50 | 1 | 6.3(6.3) | 5.1(5.1) | 3.7(3.7) | 9.8(10.1) | 7.3(7.6) | 4.4(4.7) | 9.8(9.7) | 7.3(7.2) | 5.5(5.5) | |

| 2 | 6.5(6.4) | 5.2(5.2) | 3.7(3.7) | 9.8(10.3) | 7.5(7.8) | 4.6(4.8) | 9.2(9.2) | 7.0(6.9) | 5.2(5.2) | |||

| 3 | 6.7(6.7) | 5.4(5.3) | 3.8(3.8) | 10.3(10.7) | 7.8(8.2) | 4.8(5.1) | 8.9(8.8) | 6.8(6.7) | 5.1(5.1) | |||

| 1 | 6.2(6.3) | 5.2(5.2) | 3.8(3.8) | 9.8(10.2) | 7.4(7.8) | 4.5(4.7) | 9.7(9.6) | 7.2(7.2) | 5.5(5.5) | |||

| 2 | 6.4(6.4) | 5.3(5.3) | 3.8(3.8) | 9.9(10.4) | 7.6(8.0) | 4.6(4.9) | 9.1(9.1) | 6.9(6.9) | 5.3(5.3) | |||

| 3 | 6.7(6.8) | 5.4(5.5) | 3.9(3.9) | 10.4(11.0) | 8.0(8.4) | 4.9(5.2) | 8.7(8.7) | 6.7(6.7) | 5.1(5.1) | |||

| 100 | 1 | 7.6(7.6) | 5.6(5.6) | 4.2(4.2) | 11.0(11.3) | 7.3(7.4) | 4.9(5.0) | 10.5(10.4) | 8.3(8.2) | 5.9(5.9) | ||

| 2 | 7.8(7.8) | 5.7(5.7) | 4.3(4.3) | 11.0(11.3) | 7.5(7.7) | 5.0(5.1) | 10.1(10.0) | 7.9(7.8) | 5.7(5.7) | |||

| 3 | 8.1(8.1) | 5.9(5.9) | 4.4(4.4) | 11.3(11.6) | 7.8(8.0) | 5.2(5.3) | 9.9(9.8) | 7.7(7.6) | 5.6(5.6) | |||

| 1 | 7.7(7.7) | 5.7(5.7) | 4.3(4.3) | 11.2(11.6) | 7.5(7.6) | 5.1(5.2) | 10.4(10.3) | 8.2(8.1) | 5.9(5.9) | |||

| 2 | 8.0(8.0) | 5.8(5.9) | 4.4(4.4) | 11.3(11.7) | 7.7(7.9) | 5.2(5.3) | 10.0(9.9) | 7.9(7.8) | 5.8(5.8) | |||

| 3 | 8.3(8.3) | 6.1(6.1) | 4.6(4.6) | 11.8(12.1) | 8.1(8.3) | 5.4(5.5) | 9.8(9.7) | 7.7(7.6) | 5.7(5.7) | |||

| 200 | 1 | 9.1(9.1) | 6.6(6.6) | 4.8(4.8) | 10.6(11.0) | 7.2(7.4) | 4.7(4.8) | 11.3(11.2) | 8.8(8.7) | 6.3(6.3) | ||

| 2 | 9.2(9.2) | 6.7(6.7) | 4.8(4.9) | 10.4(10.8) | 7.3(7.4) | 4.7(4.8) | 11.0(11.0) | 8.5(8.5) | 6.2(6.2) | |||

| 3 | 9.4(9.4) | 6.8(6.8) | 4.9(4.9) | 10.6(10.9) | 7.4(7.5) | 4.7(4.8) | 10.9(10.8) | 8.4(8.3) | 6.1(6.1) | |||

| 1 | 9.4(9.4) | 6.9(6.9) | 5.0(5.0) | 11.1(11.6) | 7.6(7.7) | 5.0(5.1) | 11.2(11.2) | 8.7(8.7) | 6.4(6.4) | |||

| 2 | 9.7(9.6) | 7.0(7.1) | 5.1(5.1) | 11.1(11.5) | 7.7(7.8) | 5.0(5.1) | 11.0(11.0) | 8.5(8.5) | 6.3(6.3) | |||

| 3 | 10.0(10.0) | 7.3(7.3) | 5.2(5.2) | 11.4(11.7) | 7.9(8.1) | 5.1(5.2) | 10.9(10.9) | 8.4(8.4) | 6.2(6.2) | |||

| 0.00252 | 50 | 1 | 61.8(49.2) | 46.7(36.8) | 18.4(14.7) | 109(93.2) | 81.8(69.6) | 31.5(27.0) | 48.2(40.4) | 36.7(30.3) | 16.1(13.3) | |

| 2 | 78.9(62.3) | 55.5(43.9) | 22.1(17.4) | 137(118) | 97.2(83.5) | 38.2(32.4) | 57.5(47.8) | 41.5(34.5) | 18.3(15.1) | |||

| 3 | 95.8(75.9) | 64.3(51.3) | 26.0(20.3) | 165(143) | 113(97.7) | 45.0(38.1) | 67.4(55.5) | 46.4(38.8) | 20.5(16.9) | |||

| 1 | 6.9(6.7) | 5.4(5.3) | 3.8(3.8) | 15.1(14.8) | 8.1(8.1) | 4.7(4.8) | 12.7(12.2) | 8.5(8.3) | 5.8(5.7) | |||

| 2 | 7.2(6.9) | 5.4(5.4) | 3.8(3.8) | 15.8(15.5) | 8.3(8.2) | 4.8(5.0) | 12.9(12.2) | 8.4(8.2) | 5.6(5.5) | |||

| 3 | 7.6(7.0) | 5.5(5.5) | 3.9(3.9) | 16.6(16.6) | 8.6(8.5) | 5.0(5.3) | 13.2(12.3) | 8.3(8.1) | 5.4(5.4) | |||

| 100 | 1 | 91.9(89.5) | 46.8(46.9) | 24.7(24.8) | 133(136) | 68.9(72.1) | 35.9(37.6) | 65.3(64.0) | 37.4(37.1) | 20.4(20.3) | ||

| 2 | 107(104) | 55.7(55.6) | 28.5(28.5) | 156(160) | 82.1(85.4) | 41.6(43.3) | 73.9(72.1) | 42.1(42.3) | 22.6(22.4) | |||

| 3 | 121(119) | 64.8(64.8) | 32.4(32.2) | 179(183) | 95.3(98.7) | 47.3(49.0) | 82.8(81.1) | 47.0(47.7) | 24.9(24.6) | |||

| 1 | 9.0(8.8) | 5.8(5.8) | 4.3(4.3) | 19.8(21.4) | 8.4(8.4) | 5.2(5.3) | 15.5(15.0) | 9.7(9.6) | 6.3(6.3) | |||

| 2 | 9.9(9.9) | 5.9(5.9) | 4.4(4.4) | 20.8(22.8) | 8.5(8.5) | 5.3(5.4) | 16.1(15.5) | 9.5(9.4) | 6.2(6.1) | |||

| 3 | 11.3(11.3) | 6.1(6.1) | 4.5(4.5) | 22.0(24.2) | 8.8(8.9) | 5.5(5.6) | 16.9(16.1) | 9.5(9.3) | 6.1(6.0) | |||

| 200 | 1 | 119(121) | 63.5(64.5) | 31.2(31.4) | 132(135) | 69.8(71.6) | 34.0(34.7) | 81.1(82.0) | 46.7(47.8) | 24.5(24.5) | ||

| 2 | 132(135) | 72.6(73.2) | 34.9(35.1) | 149(152) | 79.5(81.3) | 38.1(38.8) | 89.9(91.1) | 51.7(52.7) | 26.6(26.7) | |||

| 3 | 147(150) | 81.8(82.0) | 38.7(38.8) | 167(170) | 89.3(91.1) | 42.2(42.9) | 99.5(101) | 57.1(57.7) | 28.9(28.9) | |||

| 1 | 14.3(14.3) | 7.2(6.7) | 5.1(4.9) | 25.5(27.1) | 9.7(9.7) | 5.3(5.1) | 18.9(18.9) | 10.8(10.7) | 6.9(6.8) | |||

| 2 | 15.6(15.7) | 7.4(6.8) | 5.2(5.0) | 27.2(28.9) | 10.0(9.9) | 5.5(5.2) | 20.1(20.2) | 10.8(10.7) | 6.7(6.7) | |||

| 3 | 17.1(17.1) | 7.8(6.9) | 5.4(5.1) | 28.8(30.5) | 10.4(10.2) | 5.8(5.3) | 21.4(21.7) | 10.9(10.8) | 6.7(6.7) | |||

| Model 1 | Model 2 | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TPR | FPR | TPR | FPR | ||||||||||||

| Estimators | |||||||||||||||

| 0.063 | 50 | 1 | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.9(0.9) | 0.6(0.5) | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.9(0.9) | 0.5(0.5) | |

| 2 | 100(100) | 100(100) | 100(100) | 0.8(0.8) | 1.2(1.2) | 0.8(0.8) | 100(100) | 100(100) | 100(100) | 0.8(0.8) | 1.2(1.2) | 0.8(0.8) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.2(1.2) | 1.6(1.6) | 1.2(1.2) | 100(100) | 100(100) | 100(100) | 1.2(1.2) | 1.6(1.7) | 1.2(1.2) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.5(0.6) | 1.0(1.0) | 0.6(0.6) | 100(100) | 100(100) | 100(100) | 0.5(0.6) | 1.0(1.0) | 0.6(0.6) | |||

| 2 | 100(100) | 100(100) | 100(100) | 0.8(0.9) | 1.4(1.3) | 0.9(0.9) | 100(100) | 100(100) | 100(100) | 0.8(0.9) | 1.3(1.4) | 0.9(0.9) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.3(1.3) | 1.8(1.8) | 1.4(1.4) | 100(100) | 100(100) | 100(100) | 1.3(1.4) | 1.8(1.9) | 1.4(1.4) | |||

| 100 | 1 | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.5(0.4) | 0.6(0.5) | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.5(0.5) | 0.6(0.6) | ||

| 2 | 100(100) | 100(100) | 100(100) | 0.8(0.8) | 0.6(0.6) | 0.7(0.7) | 100(100) | 100(100) | 100(100) | 0.8(0.8) | 0.7(0.6) | 0.7(0.7) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.0(1.0) | 0.9(0.9) | 1.0(1.0) | 100(100) | 100(100) | 100(100) | 1.0(1.0) | 0.9(0.9) | 1.0(1.0) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.5(0.5) | 0.7(0.6) | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.5(0.5) | 0.7(0.7) | |||

| 2 | 100(100) | 100(100) | 100(100) | 0.9(0.9) | 0.7(0.7) | 0.9(0.9) | 100(100) | 100(100) | 100(100) | 0.9(0.9) | 0.7(0.7) | 0.9(0.9) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.2(1.2) | 1.1(1.1) | 1.2(1.2) | 100(100) | 100(100) | 100(100) | 1.2(1.2) | 1.1(1.1) | 1.2(1.2) | |||

| 200 | 1 | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.5(0.5) | 0.5(0.5) | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.5(0.5) | 0.5(0.5) | ||

| 2 | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.6(0.6) | 0.6(0.6) | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.6(0.6) | 0.6(0.6) | |||

| 3 | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.7(0.7) | 0.7(0.7) | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.7(0.7) | 0.7(0.7) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.5(0.5) | 0.6(0.6) | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.6(0.5) | 0.6(0.6) | |||

| 2 | 100(100) | 100(100) | 100(100) | 0.7(0.8) | 0.7(0.7) | 0.8(0.8) | 100(100) | 100(100) | 100(100) | 0.8(0.8) | 0.7(0.7) | 0.8(0.8) | |||

| 3 | 100(100) | 100(100) | 100(100) | 0.9(0.9) | 0.8(0.8) | 0.9(0.9) | 100(100) | 100(100) | 100(100) | 0.9(0.9) | 0.9(0.8) | 0.9(0.9) | |||

| 0.00252 | 50 | 1 | 100(100) | 100(100) | 100(100) | 5.6(4.4) | 7.6(6.2) | 4.0(3.0) | 100(100) | 100(100) | 100(100) | 11.0(9.8) | 13.4(12.1) | 8.3(7.0) | |

| 2 | 100(100) | 100(100) | 100(100) | 8.2(6.8) | 10.0(8.6) | 5.8(4.5) | 100(100) | 100(100) | 100(100) | 14.2(13.1) | 16.1(15.0) | 10.9(9.5) | |||

| 3 | 100(100) | 100(100) | 100(100) | 10.9(9.7) | 12.5(11.1) | 8.0(6.6) | 100(100) | 100(100) | 100(100) | 17.2(16.4) | 18.7(17.8) | 13.6(12.4) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.8(0.8) | 0.5(0.5) | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.8(0.8) | 0.5(0.5) | |||

| 2 | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 1.1(1.1) | 0.8(0.8) | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 1.0(1.1) | 0.7(0.8) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.1(1.1) | 1.5(1.5) | 1.2(1.2) | 100(100) | 100(100) | 100(100) | 1.1(1.1) | 1.5(1.5) | 1.1(1.2) | |||

| 100 | 1 | 100(100) | 100(100) | 100(100) | 4.1(4.0) | 3.0(2.8) | 2.8(2.7) | 100(100) | 100(100) | 100(100) | 7.5(7.3) | 6.0(5.8) | 5.6(5.3) | ||

| 2 | 100(100) | 100(100) | 100(100) | 5.4(5.2) | 4.2(4.0) | 3.8(3.6) | 100(99.9) | 100(100) | 100(100) | 8.9(8.8) | 7.5(7.2) | 6.9(6.6) | |||

| 3 | 100(100) | 100(100) | 100(100) | 6.7(6.6) | 5.5(5.3) | 4.9(4.7) | 99.9(99.8) | 100(100) | 100(100) | 10.3(10.2) | 9.0(8.7) | 8.2(8.0) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.4(0.4) | 0.5(0.5) | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.4(0.4) | 0.5(0.5) | |||

| 2 | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.6(0.6) | 0.7(0.7) | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.6(0.6) | 0.7(0.7) | |||

| 3 | 100(100) | 100(100) | 100(100) | 0.9(0.9) | 0.8(0.8) | 1.0(1.0) | 100(100) | 100(100) | 100(100) | 0.9(0.9) | 0.8(0.8) | 1.0(1.0) | |||

| 200 | 1 | 100(100) | 100(100) | 100(100) | 2.8(2.8) | 2.2(2.2) | 2.0(2.0) | 99.8(99.8) | 100(100) | 100(100) | 4.6(4.7) | 3.9(4.0) | 3.6(3.6) | ||

| 2 | 100(100) | 100(100) | 100(100) | 3.3(3.4) | 2.7(2.8) | 2.4(2.5) | 99.8(99.7) | 100(100) | 100(100) | 5.2(5.3) | 4.6(4.6) | 4.1(4.2) | |||

| 3 | 100(100) | 100(100) | 100(100) | 3.9(3.9) | 3.3(3.4) | 2.9(3.0) | 99.6(99.6) | 100(99.9) | 100(100) | 5.8(5.8) | 5.2(5.2) | 4.7(4.7) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.4(0.4) | 0.5(0.5) | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.4(0.4) | 0.5(0.5) | |||

| 2 | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.5(0.5) | 0.6(0.6) | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.5(0.5) | 0.6(0.6) | |||

| 3 | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.7(0.7) | 0.8(0.8) | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.7(0.7) | 0.8(0.8) | |||

| Model 1 | Model 2 | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TPR | FPR | TPR | FPR | ||||||||||||

| Estimators | |||||||||||||||

| 0.063 | 50 | 1 | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.9(0.9) | 0.4(0.4) | 99.3(98.9) | 100(100) | 100(100) | 0.6(0.6) | 0.9(0.9) | 0.5(0.4) | |

| 2 | 100(100) | 100(100) | 100(100) | 0.9(0.9) | 1.2(1.2) | 0.7(0.7) | 99.7(99.5) | 100(100) | 100(100) | 0.9(0.9) | 1.3(1.2) | 0.7(0.7) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.3(1.3) | 1.6(1.6) | 1.1(1.1) | 99.8(99.7) | 100(100) | 100(100) | 1.4(1.3) | 1.7(1.7) | 1.1(1.1) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 1.0(1.0) | 0.5(0.5) | 99.3(98.9) | 100(100) | 100(100) | 0.6(0.6) | 1.0(1.0) | 0.5(0.5) | |||

| 2 | 100(100) | 100(100) | 100(100) | 1.0(1.0) | 1.4(1.4) | 0.8(0.8) | 99.7(99.4) | 100(100) | 100(100) | 1.0(1.0) | 1.4(1.4) | 0.8(0.8) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.5(1.5) | 1.9(1.9) | 1.3(1.3) | 99.8(99.7) | 100(100) | 100(100) | 1.5(1.5) | 1.9(1.9) | 1.3(1.3) | |||

| 100 | 1 | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.4(0.4) | 0.5(0.5) | 99.4(99.1) | 100(100) | 100(100) | 0.6(0.6) | 0.4(0.4) | 0.5(0.5) | ||

| 2 | 100(100) | 100(100) | 100(100) | 0.8(0.8) | 0.6(0.6) | 0.7(0.7) | 99.7(99.5) | 100(100) | 100(100) | 0.9(0.9) | 0.7(0.7) | 0.7(0.7) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.1(1.1) | 0.9(0.9) | 1.0(1.0) | 99.8(99.7) | 100(100) | 100(100) | 1.1(1.1) | 0.9(0.9) | 1.0(1.0) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.5(0.5) | 0.6(0.6) | 99.4(99.0) | 100(100) | 100(100) | 0.7(0.7) | 0.5(0.5) | 0.6(0.6) | |||

| 2 | 100(100) | 100(100) | 100(100) | 1.0(1.0) | 0.8(0.8) | 0.9(0.9) | 99.7(99.4) | 100(100) | 100(100) | 1.0(1.0) | 0.8(0.8) | 0.9(0.8) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.3(1.3) | 1.1(1.1) | 1.2(1.2) | 99.8(99.6) | 100(100) | 100(100) | 1.3(1.3) | 1.1(1.1) | 1.2(1.2) | |||

| 200 | 1 | 100(100) | 100(100) | 100(100) | 0.5(0.5) | 0.5(0.5) | 0.5(0.5) | 99.4(98.8) | 100(100) | 100(100) | 0.5(0.5) | 0.5(0.5) | 0.5(0.5) | ||

| 2 | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.6(0.6) | 0.6(0.6) | 99.6(99.2) | 100(100) | 100(100) | 0.6(0.6) | 0.6(0.6) | 0.6(0.6) | |||

| 3 | 100(100) | 100(100) | 100(100) | 0.7(0.7) | 0.7(0.7) | 0.7(0.7) | 99.7(99.4) | 100(100) | 100(100) | 0.7(0.7) | 0.7(0.7) | 0.7(0.7) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.6(0.6) | 0.6(0.6) | 0.6(0.6) | 99.3(98.6) | 100(100) | 100(100) | 0.6(0.6) | 0.6(0.6) | 0.6(0.6) | |||

| 2 | 100(100) | 100(100) | 100(100) | 0.8(0.8) | 0.7(0.7) | 0.8(0.8) | 99.6(99.1) | 100(100) | 100(100) | 0.8(0.8) | 0.7(0.7) | 0.8(0.8) | |||

| 3 | 100(100) | 100(100) | 100(100) | 1.0(1.0) | 0.9(0.9) | 0.9(0.9) | 99.7(99.3) | 100(100) | 100(100) | 1.0(1.0) | 0.9(0.9) | 0.9(0.9) | |||

| 0.00252 | 50 | 1 | 99.8(100) | 100(100) | 100(100) | 6.6(5.6) | 8.9(7.9) | 4.7(3.6) | 88.4(89.8) | 97.0(97.9) | 100(100) | 12.7(12.0) | 15.3(14.6) | 9.8(8.5) | |

| 2 | 98.4(99.6) | 100(100) | 100(100) | 9.3(8.4) | 11.6(10.7) | 7.1(5.7) | 87.8(89.9) | 96.6(97.4) | 100(100) | 15.8(15.4) | 18.1(17.6) | 12.9(11.7) | |||

| 3 | 95.5(98.7) | 100(100) | 100(100) | 11.8(11.2) | 14.1(13.4) | 9.8(8.4) | 87.1(89.7) | 96.3(97.0) | 100(100) | 18.4(18.3) | 20.5(20.4) | 15.9(14.9) | |||

| 1 | 100(100) | 100(100) | 100(100) | 0.2(0.2) | 0.5(0.5) | 0.4(0.4) | 91.8(92.9) | 99.8(99.8) | 100(100) | 0.2(0.2) | 0.4(0.5) | 0.4(0.4) | |||

| 2 | 100(100) | 100(100) | 100(100) | 0.3(0.3) | 0.6(0.6) | 0.6(0.6) | 91.2(92.7) | 99.8(99.8) | 100(100) | 0.3(0.3) | 0.6(0.6) | 0.6(0.6) | |||

| 3 | 99.9(100) | 100(100) | 100(100) | 0.3(0.4) | 0.7(0.8) | 0.9(0.9) | 90.0(92.3) | 99.7(99.8) | 100(100) | 0.3(0.4) | 0.7(0.8) | 0.9(0.9) | |||

| 100 | 1 | 96.2(97.4) | 100(100) | 100(100) | 4.5(4.4) | 3.6(3.5) | 3.6(3.4) | 86.1(80.9) | 98.1(97.4) | 100(100) | 8.2(8.1) | 7.0(6.9) | 6.8(6.6) | ||

| 2 | 93.4(94.8) | 100(100) | 100(100) | 5.6(5.6) | 5.0(4.9) | 4.8(4.6) | 85.4(80.2) | 97.9(97.0) | 100(100) | 9.3(9.3) | 8.6(8.4) | 8.2(8.1) | |||

| 3 | 89.9(91.8) | 100(99.8) | 100(100) | 6.6(6.6) | 6.3(6.2) | 6.1(6.0) | 84.3(79.3) | 97.7(96.6) | 100(100) | 10.3(10.3) | 10.0(9.9) | 9.7(9.5) | |||

| 1 | 99.9(99.9) | 100(100) | 100(100) | 0.2(0.2) | 0.2(0.2) | 0.4(0.4) | 87.5(84.5) | 99.8(99.6) | 100(100) | 0.2(0.2) | 0.2(0.2) | 0.4(0.4) | |||

| 2 | 99.8(99.8) | 100(100) | 100(100) | 0.2(0.2) | 0.3(0.3) | 0.6(0.6) | 86.5(83.4) | 99.8(99.7) | 100(100) | 0.2(0.2) | 0.3(0.3) | 0.6(0.6) | |||

| 3 | 99.5(99.5) | 100(100) | 100(100) | 0.2(0.2) | 0.4(0.4) | 0.8(0.8) | 85.1(82.0) | 99.8(99.7) | 100(100) | 0.2(0.2) | 0.4(0.4) | 0.8(0.8) | |||

| 200 | 1 | 89.3(89.6) | 100(99.9) | 100(100) | 2.7(2.8) | 2.6(2.6) | 2.5(2.6) | 76.1(70.5) | 98.0(97.0) | 100(99.9) | 4.7(4.7) | 4.4(4.5) | 4.3(4.4) | ||

| 2 | 85.6(86.0) | 99.9(99.8) | 100(100) | 3.1(3.2) | 3.1(3.2) | 3.0(3.1) | 73.9(68.4) | 97.9(96.9) | 100(99.9) | 5.0(5.1) | 5.0(5.1) | 4.9(5.0) | |||

| 3 | 82.4(82.7) | 99.5(99.7) | 100(100) | 3.5(3.5) | 3.6(3.7) | 3.6(3.7) | 71.9(66.6) | 97.7(96.7) | 99.9(99.8) | 5.4(5.5) | 5.6(5.6) | 5.5(5.6) | |||

| 1 | 99.1(99.1) | 100(100) | 100(100) | 0.1(0.1) | 0.2(0.2) | 0.4(0.4) | 76.1(70.9) | 99.2(98.6) | 100(100) | 0.1(0.1) | 0.2(0.2) | 0.4(0.4) | |||

| 2 | 98.4(98.3) | 100(100) | 100(100) | 0.1(0.1) | 0.2(0.2) | 0.5(0.5) | 73.7(68.5) | 99.2(98.5) | 100(100) | 0.1(0.1) | 0.2(0.2) | 0.5(0.5) | |||

| 3 | 97.4(97.3) | 100(100) | 100(100) | 0.1(0.1) | 0.3(0.3) | 0.6(0.6) | 71.4(66.3) | 99.1(98.4) | 100(100) | 0.1(0.1) | 0.3(0.3) | 0.6(0.6) | |||

6.2 Real data analysis

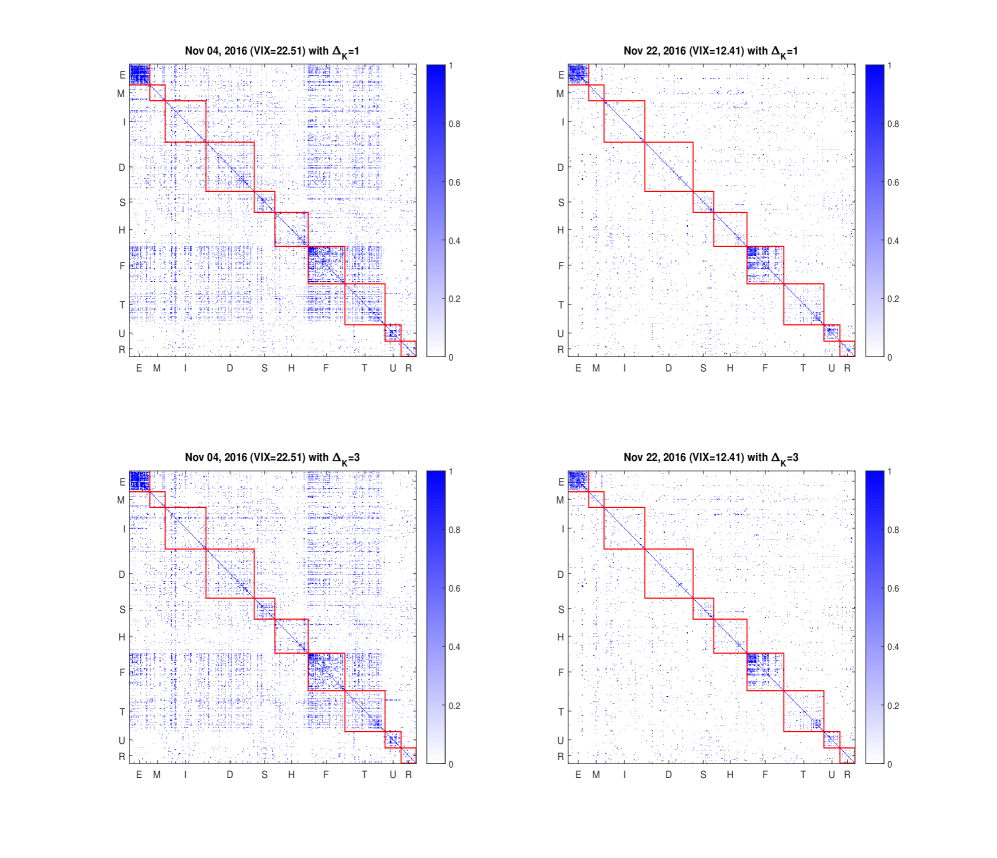

We analyzed a real high-dimensional data set, studying the statistical properties of microstructure noises that contaminate the trading prices (log-prices) of the constituent stocks of S&P 500. Intra-day tick-by-tick trading data on two days, November 4 and 22, 2016, were downloaded from the TAQ database.

Besides the prices themselves, the Global Industry Classification Standard (GICS) codes are available to classify the companies in S&P 500333The code is 8-digits and each company has its unique code. Digits 1-2 of the code describe the company’s sector; digits 3-4 describe the industry group; digits 5-6 describe the industry; digits 7-8 describe the sub-industry.. Based on the GICS codes, there are 36, 27, 71, 84, 36, 58, 64, 65, 5, 28, and 26 companies respectively belonging to the 11 different sectors – Energy (E), Materials (M), Industrials (I), Consumer Discretionary (D), Consumer Staples (S), Health Care (H), Financial (F), Information Technology (T), Telecommunication Services (C), Utilities (U), and Real Estate (R). Since there are only 5 companies belonging to Telecommunication Services, we therefore combined the companies belonging to the Information Technology and Telecommunication Services together and denoted them as ‘T’. Our analysis does not assume any information from the GICS classifications; we use it for validating and interpreting the outcomes from applying the proposed method.

Upon applying the proposed methods, we report in Figure 1 the magnitudes of the elements in the correlation matrices of the microstructure noises estimated from in (18), respectively for November 4 and 22, 2016 with tuning parameters suggested in Section 6.1.3. Here the companies are sorted by the categories defined by the GICS codes. The red blocks along the diagonal in Figure 1 represent the industrial classifications according to the digits 1-2 of GICS codes. Hence, we can examine both the within- and between-block correlations as revealed by our estimator.

We remark with some interesting findings from Figure 1. Overall, we can see that the estimated correlation matrices is sparse with many components estimated as zero, indicating that our approach achieved the goal of parsimonious covariance estimations that can (i) effectively identify nonzero components, and (ii) support providing meaningful interpretations. More specifically, we see that the correlations differ substantially on these two days; and such difference is related to the level of the Chicago Board Options Exchange Volatility Index (VIX), a popular measure of the stock market’s expectation of volatility implied by S&P 500 index options. On November 4 when the VIX level was higher, and the overall correlation level between different components of the microstructure noise is also found to be higher than that on November 22. Upon examining the within- and between- category correlations with categories defined by the GICS codes, we see that the correlations within each industrial sector are clear, especially for the Energy and Financial sectors. In contrast, the correlations between different industrial sector are much weaker. Meanwhile, we observe that the correlation estimations have no substantial difference between the cases with and 3, an indication that our method is not sensitive for the choice of .

These findings suggest us that it is practically meaningful by studying the high-dimensional statistical properties of the noises. For example, the between-day difference in correlations is helpful to understand the changes in the market sentiment under different market conditions. Furthermore, an interesting feature is the pattern found in the within- and between- industrial sector correlations, which is seen interrelated to the market conditions. Broad questions include how the correlations between noises vary associated with the prices and/or the volatility of different assets, how the sparse covariance matrix of the noises can help in solving practical problems, and so on. Supported by our new methods, we expect more future investigations along this line.

Note: The graph describes the magnitudes of the elements in the estimated correlation matrices of the microstructure noises. Different colors denote different values of the pairwise correlations. The red squares along the diagonal denote the sectors—Energy (E), Materials (M), Industrials (I), Consumer Discretionary (D), Consumer Staples (S), Health Care (H), Financial (F), Information Technology and Telecommunication Services (T), Utilities (U), and Real Estate (R).

7 Discussion

In this paper, we consider estimating the covariance matrix of the high-dimensional noise in high-frequency data. We propose an estimator with appropriate localization and thresholding to achieve the minimax optimal convergence rates under two kinds of loss. Although all theoretical properties of the proposed estimator are derived under the continuous-time model (1), the method developed in this paper could be applied to other types of process , such as the smooth ones typically encountered in the functional data literature. The key property that makes our method work is the continuity of the underlying process , but the convergence rate of the proposed estimator depends on more specific assumptions, such as those implied by the model (1). On the other hand, Assumption 2 can be replaced by a weaker assumption that and as . If we write and assume for some , with suitable selection of , Theorems 1 and 3 in Section 3 still hold with replacing by , where is a function of . More specifically, if , then . However, whether such rates are minimax optimal under the associated losses or not is unclear.

In the analysis of this study, we focus on noises with homoscedastic covariance matrix, so that our target is for each . As an interesting problem, our framework can be extensively developed to handle time-varying heteroscedastic noise where the target covariance is time-dependent at a given time point instead. Denote by the Hadamard product. Assume with and , where are nonnegative continuous-time processes, and each sequence is -mixing. Without loss of generality, we assume and for each and . Recall with for any . We outline a framework as follows.

Step 1. Given some , define and . For each , write and . We then define in the same manner as in (5) with replacing by . Under the independence between the process and the sequence , following our current technical arguments, we have in probability with suitable selection of .

Step 2. Given some integers and , if and are slowly varying with , we know with will provide a consistent estimator for under some regularity conditions with suitable selections of and .

Clearly, this problem differs substantially from our current investigation. The technical analysis of such estimator would require an extensive framework including additional assumptions on and which are beyond the scope of this study. We plan to carefully investigate this problem in a future project.

8 Proofs

In the sequel, we use to denote a generic positive finite universal constant that may be different in different uses.

8.1 Proof of Theorem 1

For any , let . For any , we have that

Define . To prove Theorem 1, we need the following three propositions whose proofs are given in Sections 8.2–8.4, respectively.

Proposition 1.

Remark 5.

As shown in Section 8.2, the upper bound stated in Proposition 1 holds for any . Since by Davydov’s inequality, we need the restriction in general settings.

Proposition 2.

Proposition 3.

Remark 6.

If , the upper bound stated in Proposition 3 can be refined as .

Write . We first consider the case with . Notice that for any and . By Propositions 1–3, if and , we have

| (19) | ||||

for any , and . Since and , then and . Given a sufficiently large constant , it holds that

It is easy to see that . By Cauchy-Schwarz inequality, we have

Let . Since , then it follows from (8.1) that

with some sufficiently large , where as . Due to , if with , then

Hence, provided that , , and .

Now we consider the case with . As we discussed in Remark 5(i), if is an independent sequence, we can select . Due to , we have in this case. Without loss of generality, we can always assume when . Based on Remark 5, it holds that for any and under either of the scenarios: (i) is an independent sequence, and (ii) is an -dependent sequence. Repeating the arguments for , we have provided that , and . We complete the proof of Theorem 1.

8.2 Proof of Proposition 1

Lemma 1.

Let be an -mixing sequence of real-valued and centered random variables with -mixing coefficients . Assume there exist some universal constants , , and such that (i) for any , (ii) for any integer , where and may diverge with . Let and . It holds that

for any and , where we adopt the convention for any .

Remark 7.

If , we have . Then the upper bound in Lemma 1 can be refined as .

Now we begin to prove Proposition 1. Recall that

| (20) |

In the sequel, we will bound the tail probabilities of , and , respectively.

For each , let . Then we have . Recall that with . Since and as , we then have for sufficiently large . Thus for sufficiently large , it holds that

| (21) |

which implies that and . Therefore, we have that holds uniformly over and . By Lemma 2 of Chang et al. (2013), Assumption 3 yields for any , which implies . It follows from Davydov’s inequality that . By Lemma 1 with and , we have

| (22) |

for any and .

Define . Then . Since

for sufficiently large , we know is uniformly bounded away from infinity due to the fact is a fixed constant. It follows from Assumption 3 that

for any . By Davydov’s inequality, we have . Write with . By Lemma 1 with and , for any and . Let and . Then . Applying Davydov’s inequality and Jensen’s inequality, it holds that . Analogously, we also have . Thus, it holds that , which implies . For any and , we have

Analogously, for any and . Note that . Together with (22), it holds that for any and .

8.3 Proof of Proposition 2

Notice that . Then

| (23) | ||||

Recall . In the sequel, we will bound the tail probabilities of , , and , respectively.

For any , define . Then we have . We will first bound for any , where is specified in Assumption 4. By Jensen’s inequality and Cauchy-Schwarz inequality,

| (24) | ||||

Recall that . By Assumption 4, for any . Therefore, by (8.3), for any . By Lemma 2 of Fan et al. (2012), it holds that

| (25) |

for any .

For any , define . Then we have . For any constant , define a stopping time . For any , by Jensen’s inequality and Cauchy-Schwarz inequality, it holds that

| (26) | ||||

Restricted on the event , we have . For any , it holds that

| (27) | ||||

Recall . Following the arguments of Equation (A.5) in Fan et al. (2012), we have that

| (28) |

for any , where and is the -field generated by . Thus, by (8.3) and (8.3), we have for any . By Lemma 2 of Fan et al. (2012), it holds that for any . Note that . Since , by Assumption 5, we have . Then

| (29) |

for any with .

Due to for any , we have

Identical to deriving (25) and (29), it holds that for any with . Such upper bound also holds for . Together with (25) and (29), we have

| (30) |

for any with . To make , it suffices to require , , , and . Due to , and , when . Thus, we need to restrict , which leads to and . It follows from that . Selecting sufficiently close to , we have . To make diverge as fast as possible, we can choose and . Note that . It follows from (30) that for any .

By (8.3), . Notice that for sufficiently large , and . Since is a fixed constant, by Assumption 4, for any fixed positive integer , Jensen’s inequality implies that

| (31) |

Meanwhile, by Assumption 4 and Burkholder-Davis-Gundy inequality, it holds that

| (32) |

Due to , together with (8.3) and (32), . Hence, . We complete the proof of Proposition 2.

8.4 Proof of Proposition 3

Lemma 2.

Let be an -mixing sequence of real-valued and centered random variables with -mixing coefficients . Assume there exist some universal constants , , and such that (i) for any integer , where may diverge with , (ii) for any integer , where may diverge with . Let . It holds that

for any , where .

Remark 8.

If , the upper bound in Lemma 2 holds with .

By the definition of , we can reformulate it as

For each and , define and . Recall .

We will first consider the tail probability . By Bonferroni inequality, we have

| (33) | ||||

For any , by Triangle inequality and Jensen’s inequality, similar to (8.3), it holds that . It follows from Assumption 4 that . Selecting and applying Markov’s inequality, we have

| (34) | |||

for any . For any constant , define a stopping time . By Cauchy-Schwarz inequality, , which implies that

| (35) |

for any . By Jensen’s inequality, . Same as (8.3) and (8.3), for any , it holds that . Selecting , together with (35), we have for any . It follows from Assumption 5 that

for any . Letting , together with (34), (8.4) implies that

| (36) |

for any . Let . For any integer , we have . By Lemma 2 with , for any , which implies that

for any . Therefore, from (36) with , it holds that

Analogously, we also have

Thus, it holds that for any . Recall that . To make , it suffices to require , and . In order to make diverge as fast as possible, we can select . If , then for any .

8.5 Proof of Theorem 2

To prove Theorem 2, we need the Le Cam’s lemma as stated in Lemma 3 below. Its proof can be found in Le Cam (1973) and Donoho and Liu (1991). Let be an observation from a distribution where belongs to a parameter space . For two distributions and with densities and with respect to any common dominating measure , the total variation affinity is given by . Let and denote by the loss function. Define and denote .

Lemma 3.

(Le Cam’s lemma) Let be any estimator of based on an observation from a distribution with , then .

For each , define where is the grid of time points where we observe the noisy data of the th component process. For any -dimensional vector and an index set , denote by the subvector of with components indexed by . The data we have is . Select the loss function for any and . Select , and

for any , where is a sufficiently small constant. For each , we write . Then

| (37) |

To prove the lower bound stated in Theorem 2, it suffices to construct a specific model which makes the stated lower bound be achievable. To do this, we select and for any . Then the associated for any . In this special case, . Given with , and , we define with each and . For each , we assume all component processes are observed. For any , we assume only one component process are observed. Without loss of generality, we assume . Let where and are two integers. We assume the th component process is observed at ’s with and . Then .

Let , and denote the joint density of by . Denote by the density of . Write . Then and for each . Here we adopt the convention if . We will show for some uniform constant .

For any two densities and , by Cauchy-Schwarz inequality, we have , which implies that . In order to show for some uniform constant , it suffices to show that , that is,

| (38) |

Notice that for any , then , which implies . For any , we have

which implies

Notice that for each . Therefore, for each . Due to , we know . Applying the inequality for any , we have

for sufficiently small . Then (38) holds. Hence for some uniform constant . Together with (37), we can obtain Theorem 2 by Lemma 3.

8.6 Proof of Theorem 3

We first consider the case with . Write . For each , we define the event with some , and . Write . Due to for any symmetric matrix , it holds that

| (39) |

For the second term on the right-hand side of (39), we have that . Due to , we then have and . Therefore, we have that holds uniformly over . It follows from (39) that

| (40) |