Smallest singular value and limit eigenvalue distribution

of a

class of non-Hermitian random matrices

with statistical application

Abstract

Suppose is an complex matrix whose entries are centered, independent, and identically distributed random variables with variance and whose fourth moment is of order . In the first part of the paper, we consider the non-Hermitian matrix , where is a deterministic matrix whose smallest and largest singular values are bounded below and above respectively, and is a complex number. Asymptotic probability bounds for the smallest singular value of this matrix are obtained in the large dimensional regime where and diverge to infinity at the same rate.

In the second part of the paper, we consider the special case where is a circulant matrix. Using the result of the first part, it is shown that the limit spectral distribution of exists in the large dimensional regime, and we determine this limit explicitly. A statistical application of this result devoted towards testing the presence of correlations within a multivariate time series is considered. Assuming that represents a -valued time series which is observed over a time window of length , the matrix represents the one-step sample autocovariance matrix of this time series. Guided by the result on the limit spectral distribution of this matrix, a whiteness test against an MA correlation model for the time series is introduced. Numerical simulations show the excellent performance of this test.

Keywords: Large non Hermitian matrix theory; Limit spectral distribution; Smallest singular value; Whiteness test in multivariate time series.

1 Introduction and the main results

Let be a sequence of positive integers, which diverges to as . Suppose is a sequence of complex random matrices whose entries satisfy the following assumptions:

Assumption 1.

For each , the complex random variables are i.i.d. with , , and .

Let be a sequence of deterministic matrices such that , and such that

Assumption 2.

where will refer hereinafter to the singular values of the matrix .

Suppose that , as . We shall first be interested in the behavior of the smallest singular value of the non-Hermitian matrix , where is an arbitrary non-zero complex number. We shall then use this result to obtain the limiting spectral behavior of the matrix where is given by Equation (1) below. Finally, we shall discuss a statistical application of this last result.

The behavior of the smallest singular value of large random matrices has recently aroused an intense research effort in the field of random matrix theory [36]. One of the main motivations for this interest is its close connections with the theory of the spectral behavior of large square non-Hermitian random matrices. It is indeed well-known that the probabilistic control of the smallest singular value of the matrix is a key step towards understanding the behavior of the spectral measure of the matrix [7, 36]. Starting with the fundamental model where has i.i.d. elements, most of the contributions dealing with the smallest singular value assume the independence between the entries of , as seen in [25, 33, 16, 37, 9]

among many others. More structured models, such as the one dealt with in this paper, have received comparatively much less attention.

Our results will be established under the following additional assumption on the elements of .

Assumption 3.

The random variables satisfy .

To understand the implication of Assumption 3, suppose it does not

hold. Drop the superscript (n), and write

. In that case,

.

Expanding the expectations, this implies that . Suppose for the moment, . Then clearly w.p.1 for some

constant . Thus,

, where is a real

random variable and is a constant. This amounts to being

real since the factor has no influence on . Thus,

Assumption 3 essentially says that the are not real.

We can now state our first result. We denote as the spectral norm of a matrix. Events are expressed in the forms or .

Theorem 1.

To prove this theorem, the first step is to linearize the model by considering the matrix

By using, e.g., the inversion formula for partitioned matrices, it is easy to see that

(versions of this “linearization trick” have been used in many different

contexts, see, e.g., [19]).

Thus, the problem is reduced to controlling the smallest singular value of

. A similar problem was tackled in [40] and [28].

In this paper, we follow closely the approach of [40]. However,

there instead of , the author had a real symmetric matrix with

i.i.d. elements above the diagonal. Our matrix is more structured,

and this necessitates a suitable modification in the arguments.

Theorem 1 will be proven in Section 3.

Theorem 1 can be used to study the eigenvalue distribution of the matrix in the large dimensional regime (see [7] or Section 4 below for more explanations on this connection). Motivated by the statistical application described in Section 2, we shall restrict our study in this paper to the specific case where equals the circulant matrix

| (1) |

This matrix satisfies Assumption 2, since it is orthogonal. Let be the eigenvalues of the matrix , which are in general complex-valued. The spectral distribution or measure of this matrix is defined as the random probability measure:

Given a sequence of random probability measures on the space or and a deterministic probability measure on , we recall that is said to converge weakly in the almost sure sense (resp. in probability) if for each continuous and bounded real function on ,

This weak convergence will be denoted as a.s. (resp. in probability).

In the asymptotic regime where , , we shall identify a deterministic probability measure such that in probability. This limit is called the limiting spectral distribution or measure (LSD) of the sequence of matrices. To state our result regarding this LSD, we need the following function. For any , let

| (2) |

Then exists on the interval and maps it to . It is an analytic increasing function on the interior of the interval.

Theorem 2.

Suppose Assumptions 1 and 3 hold. Then, there exists a deterministic probability measure such that in probability. The limit measure is rotationally invariant on . Let be the distribution function of the radial component.

If , then

If , then

The theorem implies that the support of is the disc when , and when , it is the ring together with the point where there is a mass .

Moreover, has a positive and analytical density on the open interval . A closer inspection of shows that this density is bounded if . If , then the density is bounded everywhere except when . A cumbersome closed form expression for (and hence for ) can be obtained by calculating the root of a third degree polynomial. For the special case , is given by

As an illustration of these results, eigenvalue realizations corresponding to the cases where and are shown in Figure 1. Plots of the functions given in the statement of Theorem 2 are shown on Figure 2, along with their empirical counterparts.

2 Application to statistical hypothesis testing

Consider the high dimensional linear moving average time series model

| (3) |

where are deterministic parameter matrices, and are random vectors such that the random matrix is equal in distribution to . Such models have found increasing attention in, e.g., the fields of signal processing, wireless communications, Radar, Sonar, and wideband antenna array processing [20, 39]. The sample autocovariance matrices , ( is called the lag or the step) carry useful information about the model (3), specially through their spectral distributions. Some of the works that deal with limit spectral distributions, mostly for high-dimensional real-valued time series, and their use in statistical inference are, [2, 3, 4, 5, 26, 41, 24, 23, 6].

The -step sample autocovariance matrices, except for the order , are non-Hermitian. LSD results are so far known only for certain symmetrized versions of these matrices. All the references cited above rely on this idea of symmetrization. To the best of our knowledge, no LSD results are known for the non-Hermitian sample autocovariance matrices. The result of Theorem 2 above is a beginning towards deriving the LSD of the sample autocovariance matrices in the general model (3) by considering the simplest case where and . This will be called the white noise model.

Consider the problem of testing the white noise model against an MA correlated model. To this end, we explore the idea of designing a test which is based on the eigenvalue distribution of the one-step sample autocovariance matrix, in contrast to more classical tests that are based on its singular value distribution. A non-rigorous justification of this idea is that when performing an eigenvalue-based test, we take advantage of the higher sensitivity of the eigenvalues of a matrix with respect to perturbations as compared to its singular values.

Assuming for simplicity that , our purpose is to test the null (white noise) hypothesis H0: against the alternative H1: . Consider the one-step sample autocovariance matrix

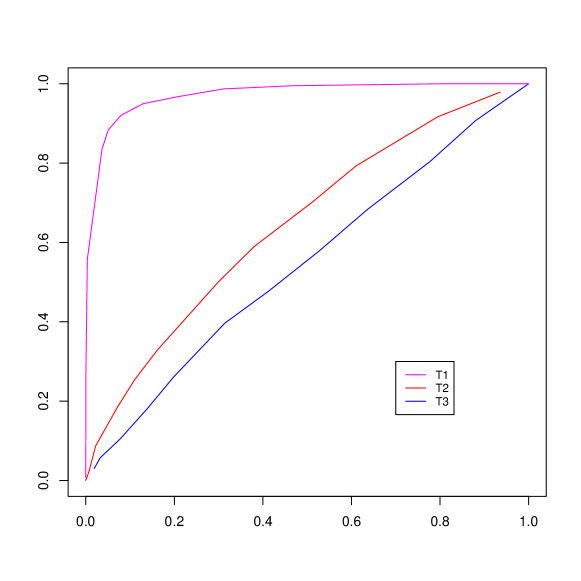

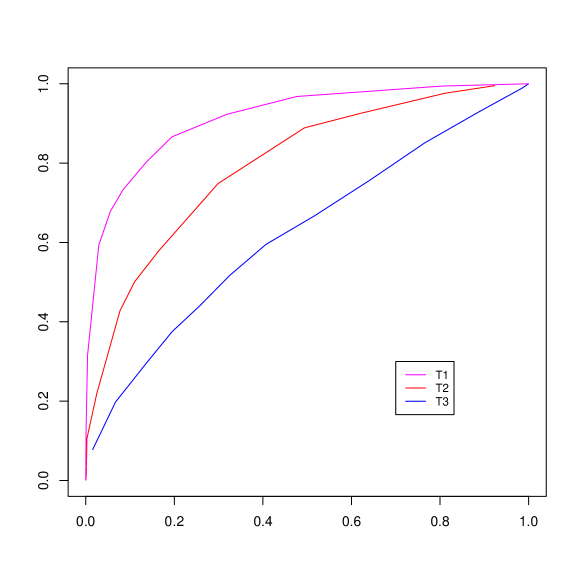

where the sum is taken modulo , and observe that under H0, this matrix coincides with . We shall consider the asymptotic regime where and . By Theorem 2, the spectral measure of converges weakly in probability to the measure . This suggests the use of a white noise test based on a distance between the spectral measure of and . We consider herein a test based on the -Wasserstein distance between these two distributions. For the sake of comparison, we also considered the more classical singular value based test which consists in comparing to a threshold. We denote these two tests as T1 and T2 respectively.

To get a more complete picture of the problem, we also considered a third test which is based on the eigenvalue distribution of the Hermitian sample covariance matrix

Its spectral distribution is known to converge weakly almost surely under H0 to the Marchenko-Pastur distribution with parameter (see [27], which deals with the Gaussian case). This suggests the use of the -Wasserstein distance between the spectral measure of and . We denote the resulting test as T3.

Figures 3 and 4 represent the ROC curves obtained for these three tests. The tests T1 and T3 were implemented by sampling and from the spectra of two large random matrices and by using the transport library of the R software. For Figure 3, , while for Figure 4, the elements of are chosen as , where and are non-zero real numbers.

These figures clearly show that T1 outperforms T2 and T3. This tends to corroborate the intuition that the eigenvalue sensitivity alluded to earlier, can be beneficial when it comes to designing white noise tests.

To better understand the behavior of the eigenvalue-based tests, the next step would be to study the large dimensional behavior of the spectral distribution of under H1. This appears to be quite non-trivial and is left for future research.

Notations

The notations and will refer to the dimension of the vector subspace , and the subspace orthogonal to respectively. The column span of a matrix will be denoted as . Similarly, is the span of the vector space and the vector .

The indices of the elements of a vector or a matrix start from zero. Given a positive integer , we write . For , we denote as the canonical vector of , with at the th place and elsewhere. Given a matrix and two sets and , we denote as the submatrix of that is obtained by retaining the rows of whose indices belong to and the columns whose indices belong to . We also write and . We define as the projection operator such that is the vector obtained by setting to zero the elements of whose indices are in . We also denote as the vector of obtained by removing the elements of whose indices are in . When is a matrix, refers to the orthogonal projector on .

As mentioned above, denotes the spectral norm. It will also denote the Euclidean norm of a vector. The Hilbert-Schmidt norm of a matrix will be denoted as . The unit-sphere of will be denoted as .

The notations and will refer respectively to the probability and the expectation with respect to the law of the vector .

3 Proof of Theorem 1: smallest singular value

To simplify the notations, from now on, we omit the superscript (n). We shall mostly work on the matrix instead of working on . Writing and , Assumption 2 is rewritten as . We also assume that without further mention.

3.1 General context and outline of proof

We first observe that if we establish Theorem 1 under the assumption that the entries have densities, then it continues to hold in the general case. This is because we can replace the matrix with, say, the independent sum where is a properly chosen matrix whose elements have densities, and use a standard perturbation argument. Hence, we assume throughout this section that the elements of have densities. It may be noted that instead of 20, any other positive number could be used and that would sharpen some of the bounds obtained later. However, it was not our goal to achieve sharp bounds.

Suppose is such that . Then . This implies that the multivariate polynomial in the variables is not identically zero. Since has a density, we conclude that is invertible w.p. 1.

Define the matrix

By the well-known inversion formula for partitioned matrices [21, §0.7.3], we have

which shows that

Therefore, to obtain Theorem 1, it is enough to prove that

| (4) |

where depends on , , and only.

As we mentioned in the introduction, a similar problem was considered in [40] and [28]. We shall follow here the argument of [40]. However, since our matrix is more structured than the one considered in this reference, a substantial adaptation of the proof is required. Here is a description of the general approach.

First recall that

Invoking an idea that has been frequently used in the literature since [25, 33], we partition into two sets of compressible and incompressible vectors as follows.

Let be fixed. A vector in is said to be -sparse if it does not have more than non-zero elements. Let be the set of vectors of that are supported by the (index) set . Given , let denote the -neighborhood of in in the Euclidean metric.

Given , we define the set of -compressible vectors as

Note that this is the set of all unit vectors at a distance less or equal to from the set of the -sparse unit vectors. The set of -incompressible vectors is the complementary set .

With these notations, we write

| (5) |

for judiciously chosen .

The infimum over is relatively easier to handle. Given a fixed vector , we first show that for some is exponentially small in . Recall that an -net is a set of points that are separated from each other by a distance of at most . Now, since the vectors of are close to being sparse, it has an -net of controlled cardinality for a well-chosen . Using this, along with a simple union bound, we will be able to infer the smallness of the probability that is small.

The infimum over the set of incompressible vectors poses a much bigger challenge since the -net argument fails. In this case the argument is more geometric. Observe that when is incompressible, is close to a sum of columns of with comparable weights. This helps to reduce the problem of controlling to the problem of controlling the distance between an arbitrary column of and the subspace generated by the other columns.

Let be the first column of , and let be the submatrix left after extracting this column. Partition accordingly as

with and . Then, the distance between and the column span of equals ( will be shown to exist)

| (6) |

Our purpose is to bound the probability that this distance is small. If we write

where , and is the first column of , then

| (7) |

Assuming inverse exists, partition as

| (8) |

Then using Equation (6), we have

| (9) |

where

| (10) | ||||

To control the behavior of Num, we need an anti-concentration result. Loosely speaking, we show that conditionally on the matrix and for most of these matrices, the probability that a properly normalized version of the random variable lives in an arbitrary ball of of small radius is itself small.

Small ball probabilities are captured by the so-called Lévy’s concentration function. Given a constant vector and a random vector , Lévy’s concentration function of the inner product at is

When the elements of are i.i.d. random variables with finite third moment, the behavior of can be controlled by the Berry-Esséen theorem, whose use in random matrix theory dates back to [25]. Berry-Esséen theorem is a refinement of the Central Limit Theorem and implies that when has elements with magnitudes of order , it holds that .

Our plan now is to apply this theorem after replacing with the random vector . Unfortunately, this theorem cannot be used as is on the random variable because of the presence of the quadratic form . To circumvent this problem, we use a decoupling argument that replaces with an inner product that can be processed by the Berry-Esséen theorem. This decoupling idea that dates back to [15] has also been used in [40].

3.2 Technical results

The following proposition is a variation of [37, Prop. 5.1], see also [7, Lem. A2] and [17]. This variation is needed because we want the constants and to depend on the law of the ’s via and . For completeness, we provide the modified proof in Appendix A.1.

Proposition 3 (Distance of a random vector to a constant subspace).

Let be a vector of i.i.d. centered unit-variance random variables such that for some , . Then, there exist and that depend only on and and that satisfy the following property. For all , and for any deterministic subspace of such that ,

We shall also make use of:

Lemma 4 (Rosenthal’s inequality [32]).

Let be independent random variables such that and for . Then there exists a universal constant such that

These results easily lead to the following lemma:

Lemma 5.

Let the matrix satisfy Assumption 1. Then, there exist constants and a constant that depend on only and that satisfy the following property. For each deterministic vector and each deterministic subspace with ,

| (11) |

In particular, for each deterministic vector , it holds that . Similar conclusions hold if is replaced with .

Proof.

Let be the rows of , and define the random variables for . These random variables are i.i.d., centered, and have unit-variance. Furthermore, writing , we get by Rosenthal’s inequality that for some universal constant ,

Writing , we note that . Applying Proposition 3 with , we obtain (11). The rest of the claims follow immediately. ∎

The -net argument alluded to above will use the following lemma.

Lemma 6 (Metric entropy of a complex sphere, Lemma 2.2 of [9]).

Let be a -dimensional subspace, and let . Given , the set has an -net of cardinality bounded by .

The two following results regarding Lévy’s concentration functions will be needed.

Lemma 7 (Restriction of the concentration function, Lemma 2.1 of [33]).

Let be a vector of independent random variables. Then, for each non-empty , we have .

Proposition 8 (Anti-concentration via the Berry-Esséen theorem).

There exists a constant such that for any vector of complex centered independent random variables with finite third moments,

For a proof, see [36, Chap. 2] or [7, Lem. A6]. In particular, if there exist two positive constants and such that and for each , then

| (12) |

where and .

We now enter the proof of Theorem 1 via proving Inequality (4). Recall that we have written where is the first column of . Given , we denote as the event

In the remainder of this section, the constants that do not depend on will be referred to by the letter , possibly with primes or numerical indices. In all statements of the type

where or , the constants such as , , or depend on , , and at most.

3.3 Compressible vectors

Recalling (5), we start with the compressible vectors. The probability bound for these vectors is provided by the following proposition:

Proposition 9.

Let Assumption 1 hold true. Then, there exists , , and such that

Proof.

We first show that there exist such that for each deterministic vector ,

| (13) |

Let us partition as , where and . Since , either or . Assume that , and note that . Writing , we have

by applying Lemma 5 and choosing and judiciously. When , we can use a similar argument (with possibly different and ) after observing that . This establishes (13).

Now, on the event , we have

On this event, assume that there exists such that . Then . In other words,

Now, let to be fixed in a moment, and choose in such a way that . By Lemma 6, the unit-sphere of the subspace of the vectors of that are supported by has a -net of cardinality bounded by . Applying the previous results and making use of the union bound, we get that

Finally, considering all the sets such that , recalling the elementary bound on the binomial coefficients , and using the union bound, we get that

A small calculation shows that the right hand side is of the form for large enough when is chosen small enough. By taking , the proposition is proven. ∎

3.4 Incompressible vectors

3.4.1 Tools

One main feature of incompressible vectors of is that they contain elements of absolute values of order , as shown in [33, Lem. 3.4]. A slightly stronger version of this lemma will be needed in this paper:

Lemma 10.

Let , and let . Then the set

satisfies .

Proof.

Let

Since , we get by Tchebychev’s inequality that . Moreover, by the definition of . Recalling the definition of incompressibility, we get that . Thus, . ∎

One consequence of [33, Lem. 3.4] is the following lemma, which implies that the infimum of over a set of incompressible vectors can be handled by controlling the distance between an arbitrary column of and the subspace generated by the other columns:

Lemma 11 (Invertibility via mean distance, Lemma 3.5 of [33]).

Let be a random matrix. Let be the th column of and let be the submatrix left after removing this column. Then,

An expression for these distances is provided next.

Lemma 12.

Let , and partition this matrix as

where and are as in Lemma 11, is the first element of the vector , and is the bottom submatrix of . Assume that is invertible. Then,

Proof.

We develop the expression , where

is the orthogonal projector on . Using the Sherman-Morrison-Woodbury formula,

where . We thus obtain after a small calculation that

Since , we then get that , which is the required result. ∎

3.4.2 Distance control

Using Lemma 11, we need to control the distance between a column of and the subspace generated by the other columns.

Denote as the column of (thus, ). Let and denote the column of and the row of respectively. Then the columns of are one of the two types: , or . Due to the fact that is not necessarily a diagonal matrix, it will be more difficult to control the distances involving columns of the first type.

Partitioning as , where is the first column of , we have

Since is obviously included in , it will be enough to establish the inequality

to obtain Proposition 13. Replacing with will be more convenient due to the independence of and . The remainder of this section is devoted towards proving this inequality. Recall the formula for given in (6). To be able to use Lemma 12, we need to check that defined in (7) is invertible. Recall that is assumed to have a density.

Lemma 14.

The matrix is invertible with probability one.

Proof.

Since , the matrix is invertible. Thus, to show that is invertible with the probability one, we need to show that the Schur complement of in is invertible with probability one.

Since , it holds that . Thus, either is invertible or .

Assume it is invertible. Then on the set , it holds that . Thus, is a non-zero multivariate polynomial in the real and imaginary parts of the elements of . Since has a density, w.p. 1.

Assume now that . Then we can write where are full column-rank matrices. Writing where , we get that

Given a vector , the inner product is a continuous random variable, thus w.p. 1. Consequently, w.p. 1., which implies that is invertible w.p. 1. The same argument holds for , and thus the matrix is invertible w.p. 1. To obtain that is invertible, it remains to apply the previous argument after replacing with and with , and making use of the independence of and along with the Fubini-Tonelli theorem. ∎

Using Lemmas 12 and 14, we get that on a probability one set, Equation (6) holds. On the probability one set where is invertible, write as in (8). Then, from (6), where Num and Den are as given in (10).

To study the behavior of Num and Den, we first need to show that the image of each deterministic vector by the matrix at the right hand side of (8) is incompressible with high probability. This will be stated in the corollary of Proposition 16 below.

Lemma 15.

.

Proof.

The matrix is a principal submatrix of the Hermitian matrix . Using the variational representation of the eigenvalues of , we get that . By Weyl’s interlacing inequalities, , hence the result. ∎

Proposition 16.

There exist , , and such that for each ,

Proof.

Let and to be fixed later. Let such that . Fix an element of the unit-sphere . In this first part of the proof, we shall control the probability of the event

The event between brackets is included in the event

| (14) |

Let

| (15) |

be a singular value decomposition of , where (resp. ) is the last column of the unitary matrix (resp. ). Given any vector , we shall use in the remainder of the proof the notations and , making an orthogonal sum. As is well-known (see [31]), the vector where is the Moore-Penrose pseudo-inverse of , minimizes with respect to . Assume that there is a solution of the inequality in . Then, since is also a solution, we get that

and hence,

Noting that and are orthogonal, we get that . By Lemma 15, the smallest singular value of the restriction of the operator to the subspace is bounded below by . Hence we get that

The vector also satisfies the inequality for some . Thus,

which implies that on the event ,

Observing that is collinear with , we get at this stage of the proof that

| (16) |

To proceed, we need to control the Euclidean norm of . For , consider the event

Since , we get from Lemma 15 that . By Lemma 5, there exist and such that . We thus obtain

| (17) |

To bound the probability of the event at the right hand side of the inclusion (16), we consider separately the situations where is large and where is bounded above. Consider the event

On , it holds that

From Lemma 5, there exist such that . Writing , we have

Thus, setting , we get that

| (18) |

Now consider the case . We discretize this ball as follows. Consider the event

Given , define the event

For , let and . Then . Therefore,

Let us bound the probability of the event . Recalling that and that is supported by , we observe that and are independent. Writing and , we have

By Lemma 5 once again, . Thus, if we choose small enough so that , we get that

| (19) |

Putting things together, we get

where .

Now, let be a -net of . Given an element of , there exists such that , and there exists such that . Thus, by the triangle inequality. Assume that there exist and such that the inequality

holds true. Then on the set , we have

By Lemma 6, . Adjusting again in such a way that , we obtain that

Finally, considering all the sets such that , and using the bound along with the union bound, we get that

Choosing small enough, we get the result with and small enough. ∎

Corollary 17.

For each deterministic vector ,

3.5 Handling the denominator Den in (10)

Lemma 18.

There exist positive constants and such that

where , , or .

Proof.

We reuse here the notations of the singular value decomposition (15) of . For any matrix with rows, we also use the notations and . We first prove the result for .

From Lemma 5, we know that there exist such that . We shall show that on the event , there exists some , such that

This will establish that

| (20) |

Recall that

or equivalently,

| (21a) | ||||

| (21b) | ||||

Since , we get from Lemma 15 and (21a) that

Thus, on . Writing , Equation (21b) can be rewritten as , which gives that

on . Since , there exists such that , and the inequality (20) follows.

Our next step is to show that there exists a constant such that . It is then easy to deduce from (20) that with . We shall assume that on and obtain a contradiction if is chosen small enough. From the equation , we have

| (22a) | ||||

| (22b) | ||||

By Equation (22a), on . Writing and observing from (15) that and are orthogonal, we obtain that . Turning to (15) again and using Lemma 15, we also have

thus, . Now, rewriting Equation (22b) as and using the triangle inequality, we get that . Since is a rank-one matrix, the set of vectors such that is not empty. For any such vectors, we have

which raises a contradiction if we choose . The lemma is proven for .

The following lemma is very close to [40, Prop. 8.2], with the difference that the bound on the probability in Statement 3 is a Berry-Esséen type bound.

Lemma 19.

The following hold true:

-

1.

There exist such that

-

2.

Let be a random vector with independent elements such that and for all , and let be deterministic. Then for each ,

-

3.

There exists such that for each ,

Proof.

To prove the first statement, we write . By Lemma 5, there exist two constants such that with a probability larger than . Moreover, on , hence the result.

Turning to the third statement, we start by writing

| (23) |

Define . The idea of the proof is the following. By Corollary 17, is incompressible with high probability. Moreover, and are independent. Therefore, we can use the Berry-Esséen theorem (Proposition 8) to control the behavior of the inner products . We then use [40, Lemma 8.3] to pass from these inner products to the sum at the right hand side of (23). Indeed, this lemma shows that if are arbitrary non-negative random variables and if are non-negative numbers such that , then for each .

Specifically, define for each the set of indices

Using the independence of and , Lemma 7 and Proposition 8, we get after a small calculation that

where

and is the constant that appears in the statement of Proposition 8. Observing that and using [40, Lemma 8.3], we get that

Defining the event , we know from Corollary 17 that . Moreover, on for each by Lemma 10. Thus, by changing the value of the constant above we get that on for each . Putting things together, we conclude that

which leads to the required result after changing once again the value of . ∎

Lemma 20.

There exist positive constants and such that for each ,

Proof.

3.6 Handling the numerator Num in (10)

This is the only section where we shall need Assumption 3.

We shall use the idea of decoupling that will allow us to replace the term in the expression of this numerator with an inner product whose concentration function is manageable by means of the Berry-Esséen theorem. This decoupling idea that dates back to [15] has been used many times in the literature. The following lemma is found in [40] (see also [35]).

Lemma 21.

Let and be independent random vectors, and let be an independent copy of . Let be an event that depends on and . Then

Lemma 22.

Let , and be deterministic. Let . Then for each ,

where is an independent copy of (here we assume that the right hand side is equal to one if or ).

Proof.

Assume without loss of generality that . Write

Using Lemma 21 with , , and , we get

where the second inequality is due to the triangle inequality. Developing, we get that

∎

We now have all the ingredients to prove Proposition 13.

Proof of Proposition 13.

In the remainder, we write

where . Given , we have

and

Given an arbitrary , we denote as , , and three independent vectors, independent of everything else, such that and . Recalling the expression of Num in (10) and using Lemma 22, we get that for each ,

| (25) |

where the linear mapping such that if , then , where is at the position .

Let be a vector of i.i.d. Bernoulli random variables valued in such that , where the probability will be fixed below. This vector is assumed to be independent of everything else. Since (25) is true for each , we can randomize by setting . Setting , we obtain

| (26) |

where is a vector that has the same law as and that is independent of all other random variables.

Write

and let

For , let

Then the concentration function at the right hand side of (26) can be rewritten as

We wish to control this by using the Berry-Esséen theorem (Proposition 8). Recalling Proposition 16, define the set

By the restriction lemma 7, we have

Informally, we expect to be of order with high probability, the to be lower bounded with high probability, and the to be upper bounded with high probability for , in order to benefit from the effect of the Berry-Esséen theorem in a manner similar to Inequality (12).

More rigorously, for each , we have

for all large enough , where is positive by Assumption 3. Focusing on the set , we get that

| (27) |

Moreover,

Then, by the Berry-Esséen theorem,

(here, we assume that if ). The constant in the term after the second inequality is the one that appears in the statement of Proposition 8. In the remainder of the proof, the value of this constant may change without mention.

At this stage of the calculation, we have

| (28) |

Now, take , and consider the event

Since , we get by Hoeffding’s concentration inequality that

Consider also the event

By Corollary 17, there exists a constant such that

On , we have that by Lemma 10. Therefore, on , it holds that

It remains to control the terms and in the expression of . Given a small , consider the event

Note that and , thus on . Applying Lemma 19 after setting the vector in its statement to , we get that there exists a constant for which

3.7 Theorem 1: end of proof

First note that for any , Proposition 13 continues to hold when is replaced by , by the same proof. When , too, the proof continues to be valid once the roles of and are interchanged. Indeed, one can check that the argument is simpler and hence is omitted. Applying Lemma 11, we obtain that

Using Proposition 9 along with the characterization (5) of the smallest singular value, we obtain Theorem 1 with and .

Remark 1.

The proof of Proposition 13 shows that the origin of the slow decreasing term at the right hand side of the last inequality is the decay that is optimal while using the Berry-Esséen theorem, as shown by Inequality (12). To obtain a better decay rate of the concentration functions, one can use the so-called Littlewood-Offord theory instead. This was the approach of [33, 37, 38, 40] among others to solve small singular value problems.

4 Proof of Theorem 2

4.1 A general approach: log potential

A well established technique for studying the spectral behavior of large random non-Hermitian matrices is Girko’s so-called hermitization technique [13]. This is intimately tied to the logarithmic potential of their spectral measures.

Recall that the logarithmic potential of a probability measure on is the superharmonic function defined as

The measure can be recovered from in the following way. Let the space of Schwartz distributions on and let for be the Laplace operator defined on . Let

Note that . Then

| (29) |

in the sense that

It is also known that the convergence of the logarithmic potentials for Lebesgue almost all implies the weak convergence of the underlying measures under a tightness criterion (see, e.g., [7]).

Turning back to our matrix , the logarithmic potential of its spectral measure can be written as

where the probability measure is the singular value distribution of , given as

The above observation is at the heart of the hermitization technique. It transforms the eigenvalue problem into a problem of singular values. To study the asymptotic behavior of , we need to study the asymptotic behavior of for Lebesgue almost all . In the light of the above relations, this approach may be formalized as follows:

Proposition 23 (Lemma 4.3 of [7]).

Let be a sequence of random matrices with complex entries.

Let be its

spectral measure

and let be the

empirical singular value distribution of . Assume that

(i) for almost every , there exists a probability measure such that

in probability,

(ii) is uniformly integrable in probability with respect to the

sequence .

Then, there exists a probability measure such that in probability, and furthermore,

Note that to successfully apply Proposition 23 to , we need to establish that:

Step 1: for almost all , (a deterministic probability measure) in probability.

Step 2: the function is uniformly integrable with respect to the measure for almost all in probability. That is,

| (30) |

By achieving these two steps, we conclude that there exists a probability measure such that in probability, and such that -almost everywhere. It would then remain to identify the measure to complete the proof of Theorem 2.

The proofs of the results devoted to the asymptotic behavior of (mainly, Step 1) are provided in Section 5. Step 2 relies heavily on Theorem 1 above. The proofs of the results devoted to the identification of are provided in Section 6.

4.1.1 Step 1: Weak convergence of

Going a bit further than what Proposition 23 requires on , we shall show that for each , there exists a probability measure such that almost surely. As is usual in random matrix theory, this convergence will be established through the convergence of the associated Stieltjes transforms. For this, it will be convenient to consider the Hermitian matrix

whose spectral measure

is the symmetrized version of ( is symmetric in the sense that for each Borel set ). It is enough to show that converges weakly a.s. to a probability measure .

Given , let us write

| (31) |

which is the resolvent of in the complex variable .

The a.s. convergence is a consequence of the following theorem. Its proof will be provided in Section 5.1. By this theorem, the first assumption in the statement of Proposition 23 is satisfied when is replaced with . Note that the Stieltjes transform of a symmetric probability measure is purely imaginary with a positive imaginary part on the positive imaginary axis.

Theorem 24.

Let Assumption 1 hold true. Then

| (32) |

where for each , is a pair of holomorphic functions on such that is the Stieltjes transform of a symmetric probability measure, , and writing for , the pair uniquely solves the equations

| (33a) | ||||

| (33b) | ||||

where

| (34) |

4.1.2 Step 2: uniform integrability

It is equivalent to show the uniform integrability of with respect to . Note that is unbounded near both and . The following proposition will address uniform integrability near zero.

Proposition 25.

Let be a sequence of random matrices such that . Let , and assume that there exist three constants such that

| (35) |

Assume in addition that there exist a sequence of events such that , and two constants such that for large enough ,

| (36) |

Then, denoting as the empirical singular value distribution of ,

| (37) |

For a detailed proof, please refer to [18, Proposition 14] or to [10, Section 6.2]. We just point out that starting from (35) and making some elementary Stieltjes transform calculations, one can show that there exist constants such that . This so-called local Wegner estimate [42] on the number of intermediate singular values, used in conjunction with the control provided by (36) on the smallest singular value, leads to (37).

The validity of condition (35) in Proposition 25 is guaranteed by the next proposition. It is proven in Section 5.2. The rate can be improved but is adequate for our purposes.

Proposition 26.

Let Assumption 1 hold true, and assume that . Then, there exist two constants such that

Condition (36) on the smallest singular value of in Proposition 25 is a consequence of the following corollary to Theorem 1, whose proof is immediate.

Corollary 27 (Corollary to Theorem 1).

Invoking the boundedness of the fourth moment specified by Assumption 1, we know from [43] that

| (39) |

Thus, the probability of the event converges to by setting . By Proposition 26 and Corollary 27, the assumptions of Proposition 25 are satisfied for with . Therefore, the uniform integrability of the near zero specified by (37) is true when is replaced with , and .

Remark 3.

The proof of Theorem 1 showed that we can take . Recall Remark 1 in Section 3.7 above for more comments on this point. The consequent slow rate at the right hand side of (38) is the primary reason that we conclude the uniform integrability of the near zero only in probability. The convergence in probability stated in Theorem 2 is due to this.

To be able to apply Proposition 23, it only remains to establish the uniform integrability of near infinity, namely

But this result follows immediately from the identity , valid for .

4.2 Identification of

At this point, we know that there exists a probability measure such that in probability, and such that

We now aim to identify and establish its properties that are specified in Theorem 2. To that end, we rely on equation (29). We use an idea that dates back to [11] and that has been frequently used in the literature devoted to large non-Hermitian matrices. Define on the regularized versions of and respectively:

In parallel, let us get back to the resolvent defined in (31). By Jacobi’s formula,

Letting we know from Theorem 24 that a.s. At the same time, a.s. since . We can therefore assert that in , and then extract the properties of from the equation

This line of thought leads to the following proposition. Its proof is provided in Section 6.1.

Proposition 28.

As , the function converges to in .

The following lemma specifies the properties of the function defined in (2), that we shall need. Its proof is straight-forward and is omitted.

Lemma 29.

Consider the function on the interval . It is analytical and increasing on . Moreover, , and .

By this lemma, has an inverse on that takes this interval to . On , the function is analytical and increasing.

By showing that converges as point-wise for each and by identifying the limit function , we get the following proposition whose proof is given in Section 6.2.

Proposition 30.

Let be the function defined on as follows:

If , then

If , then

Then in .

By Lemma 29, defined in the statement of Proposition 30 is continuously differentiable as a function of on the open set

Therefore, coincides with in , where is the pointwise derivative of w.r.t. . Specifically, for each test function , we have

where, by Proposition 30, the density of on is given by

| (40) |

Hence the density depends on through only, and thus is rotationally invariant on .

Now we consider on the boundary . We deal separately with the cases and .

First suppose . Let . Changing to polar co-ordinates, we get

But since and , we get that

establishing the formula in Theorem 2 for .

Now suppose . Put .

If we set , we obtain from (40) that .

If , then by the same derivation as for .

Now we claim that . To show this, let be a smooth function such that and . Given , define the function

which is supported on the ring . It is then enough to show that as . Indeed, by an integration by parts, we get that

where the function for is a real bounded function near that satisfies by Proposition 30. Making a cartesian to polar variable change, we get that

by the dominated convergence theorem.

Since , we can infer now that for each and each . Letting and , and recalling that , we get that

Similarly to , we can show that . We therefore get that , and hence the formula in Theorem 2 is verified also for .

This completes the proof of Theorem 2.

5 Limit singular value distribution

Given , , and a sequence of complex numbers, the notation (or when ) will refer in this section to the existence of a constant and two non-negative integers and such that

The constants , , and may depend on but not on or . If is a matrix, then the notations and , are to be understood in a uniform entry-wise sense.

5.1 Proof of Theorem 24

We start by showing that for each , the bulk behavior of the singular values of is completely specified by Assumption 1 and does not depend on the particular distribution of the elements of .

Our first result is a standard concentration result which helps to replace the traces by their expectations. The proof uses well-known methods, see [1], and we omit it.

Proposition 31.

Under Assumption 1, for each ,

The above expectations are easier to compute when the entries are Gaussian. The next result establishes that we can assume this without any loss. Let , where and are real independent standard Gaussian random variables. Define , where the are independent copies of . Clearly, these entries satisfy Assumption 1. Let be the analogues of the , obtained by replacing the matrix with . The proof of the following proposition proceeds along standard lines and uses the boundedness of the fourth moment in Assumption 1 and the fact that the first two moments of the two sets of variables agree. We omit the details.

Proposition 32.

Under Assumption 1, for each ,

Hence, in the rest of this subsection we assume that the elements of are distributed as . This enables us to study with the help of two Gaussian tools that are frequently used in random matrix theory. The first is the Integration by Parts (IP) formula [14], [22], and the second is the Poincaré-Nash (PN) inequality [8], [29], which is also a particular case of the Brascamp-Lieb inequality. A detailed account of the use of these tools in random matrix theory can be found in the treatise [30].

Let be a complex Gaussian random vector with , , and . Let be a complex function which is polynomially bounded together with its derivatives. Then, the IP formula reads as

| (41) |

Furthermore, writing

the PN inequality is

| (42) |

We shall apply (41) to the case and where is the resolvent given by Eq. (31) (seen as a function of ), and and are deterministic vectors in . If we disregard and write to emphasize the dependence of the resolvent on , then, given a matrix , the resolvent identity implies that

Using this equation, we can obtain the expression of , where and . Taking we get that

In particular, by taking and for , we obtain from these equations that

| (43) |

and by taking and for , we get

| (44) |

Given , we shall also use the trivial relations

where both the sum and the difference are taken modulo-.

We can now start our calculations. Recalling that refers to the column of for , our first task is to study quadratic forms of the type and . Define the matrices

It is obvious that for each . Thus, given a measurable function and the integers , it holds that

where the index summations are taken modulo-. As a consequence, the matrices and are circulant matrices, a fact very useful to us.

In right side of the above two expressions we have terms of the type . We can use the PN inequality (42) to decouple from . Specifically, we have the following lemma, which is proven in Appendix A.2.

Lemma 33.

For each and each ,

Let us write for . Using the lemma, and applying the Cauchy-Schwartz inequality, it is easy to see that

Since is a square matrix, we see from (31) that . Thus, the equations above can be written in a matrix form as

| (45) | ||||

| (46) |

Let us give these equations a more symmetric form. Developing , we get that

| (47) |

Similarly, taking , we get

| (48) |

Now, by using the obvious identity we obtain

(the similar equations involving the terms and will not be used). Taking the traces of the expectations, we get

| (49) | ||||

| (50) |

where .

Recalling that , the function is the Stieltjes transform of the probability measure . Hence, . So, is a normal family of holomorphic functions on . Similarly, and are holomorphic functions in whose absolute values are bounded by .

Using the normal family theorem, let us extract from the sequence a subsequence (still denoted as ) such that , , and converge to holomorphic functions in the sense of uniform convergence on the compact subsets of . Denote these functions respectively as , and . We shall show that they uniquely solve a system of equations on the line segment of the positive imaginary axis, where is some positive constant. This will show that is uniquely defined on , and that and on . We then show that as . This will lead to the fact that is the Stieltjes transform of a symmetric probability measure .

Assume that where . Then, since the measure is symmetric, with . Moreover, we notice from the expressions of and in (31) that .

Recall that and are circulant matrices. Define the so-called Fourier matrix

Then the circulant matrix can be written as

Notice that the matrices , and commute, since they are circulant.

Now Equation (47) can be rewritten as where is a circulant matrix, and

| (51) |

If , then , and thus, the positive definite matrix satisfies in the semi-definite positive ordering. In view of Equation (50), we need an expression for . We can write

| (52) |

Given two square matrices and of the same size, it is well known that . Thus, since , we get that

By a similar derivation, and in view of Equation (49), we also get from Equation (48) that

| (53) |

Now, taking to infinity along the subsequence in Equations (49), (50), (52), and (53), writing where , and noting that , the pair satisfies the system of Equations (33) of the statement of Theorem 24 for .

Let us consider the system of equations in

| (54a) | ||||

| (54b) | ||||

where and are given by Equations (34). Writing

the system (54) can be rewritten as

| (55a) | ||||

| (55b) | ||||

By using the residue theorem (derivations omitted), we know that the integrals are given by the expressions

| (56) |

for each and such that or .

Lemma 34.

There exists (depending on and ) such that for each , the system (54) has a unique solution such that and .

Proof.

Equation (55b) can be written equivalently as . Note that and are both real and depend on through only. Thus, , and if we write , then is a solution for this if and only if is a solution for , where . Consequently, we can assume without loss of generality that and belong to in the system (54).

This system can be written equivalently as , where

We shall show if is large, is a Banach contraction on the space .

If is large enough, we get from the integral expressions of and that

Hence, writing , (and recalling that is real), we get that , thus , and moreover,

for large enough . Thus, when .

We now consider the Jacobian matrix of . After some easy derivations that we omit, we obtain that when is large, there exist a constant such that

Since

we get that on for large enough , and the result follows from Banach’s fixed point theorem. ∎

Lemma 35.

as .

Proof.

We now need to prove that satisfy the system of Equations (33) for each . By the convergence , we get that . In particular, is tight. Let be such that . Recalling that is symmetric, we have

Therefore, for each , the matrix defined in (51) satisfies in the semidefinite ordering for all large enough . By repeating the argument that follows Equation (51), we obtain that solve the system (33).

5.2 Proof of Proposition 26

We first assume that , where was defined before the statement of Proposition 32. Fixing , and writing , we first show that there exist constants such that

| (57) |

From Equations (49), (50), (52), and (53), we get that

| (58a) | ||||

| (58b) | ||||

where

We now show that for some constant . It is enough to focus on the case . Using

it is easy to see that . Since , we get from Equation (58a) that for some constant .

6 Properties of

6.1 Proof of Proposition 28

We first show that is continuous, and that there is a probability one set on which

| (59) |

Fix . From the almost sure weak convergence of to and (39), we get that for each . Furthermore, by the Hoffman-Wielandt theorem (see [21]), given , we have . Thus, , and taking to infinity, we get that is continuous.

Let be a compact set of . For , we have

| (60) |

On the underlying probability space , let be the probability one event where the convergence (39) takes place. For each , define the event

Since is measurable on the product space and is continuous, the function is measurable on . Moreover, for each ,

By the Fubini-Tonelli theorem, there exists a probability one set such that

Let be supported by , and let . We have

By (60) and the continuity of , the term is bounded. Thus, the first term at the right hand side converges to zero by the dominated convergence, while the second is zero for large enough . This proves (59).

Equation (59) implies that, almost surely. On the other hand, we know from Jacobi’s formula that the pointwise derivative of with respect to is . Moreover, this derivative coincides with the distributional derivative . By Theorem 24, for each . By an argument similar to the one used in the proof of (59), we can show that this convergence holds almost surely in . Thus,

| (61) |

We now show that

| (62) |

It is clear from the expressions of and that as . Therefore, for , and since is continuous hence locally integrable, we get (62) by the monotone convergence theorem.

6.2 Proof of Proposition 30

The following preliminary lemma is needed.

Lemma 36.

For each , the function is bounded for . Moreover, , where is a positive constant.

Proof.

Assume without loss that . Using

it is easily seen that . Observing that by the general properties of the Stieltjes transforms, we obtain from (54a) that for some .

Using the inequality along with (54b), we get that which shows that is bounded when . ∎

We now enter the proof of Proposition 30. Since is symmetric,

thus, on , the function

is lower-bounded by a positive constant.

In the proof, we shall use the fact that satisfies the system of equations (55). We rewrite Equation (55a) as , and Equation (55b) as , or equivalently, as . Since for , we can use the expressions (56) of the integrals and to obtain

| (63) |

where .

We now let . Here, each sequence satisfies one of two cases : either , or where is a positive number. Indeed, we have just shown that is excluded.

Case .

Using Lemma 36, and taking a further subsequence that we still denote as , we can assume that and . The pair satisfies the equations

| (64) | ||||

| (65) |

By Equation (65), the number is real and satisfies

| (66) |

Moreover, we have . Replacing in (64), we get

Reducing to the same denominator, we get after some simple manipulations that

where is the function given in the statement of Theorem 2. Let us delineate the domain of variation of . Equation shows that , thus or . By Equation (66),

We therefore get that and furthermore, by rearranging the terms of the inequality above, that . The last inequality implies that . In conclusion, we get that .

The case .

Here we get of course that . Taking a subsequence if necessary, we shall assume that . Getting back to the system (63) and taking to zero, we get that

The first equation implies that , and that

Replacing by its value in the second equation, we get after a simple calculation that

Here we need to consider two cases: either or . If , we get from the last equation that (thus, ). Plugging in the expression of , we get that

Since , this implies that .

If , we obtain that , thus, and

Using again that , we get after a small calculation that and .

Let us summarize our conclusions for clarity.

-

•

If , let be an arbitrary accumulation point of , and let .

-

–

If , then , and .

-

–

If , then , and .

-

–

-

•

If converges to a positive constant, let be an arbitrary accumulation point of .

-

–

If , then , and .

-

–

If , thein either in which case , or , in which case .

-

–

These statements show that given , the accumulation points reduce to a genuine limit. Moreover, the behavior of this limit is as described in the statement of Proposition 30.

Acknowledgements.

The visit of AB to France has been funded by the Indo-French Center for Applicable Mathematics project High Dimensional Random Matrix Models with Applications. This work has been partially supported by the French ANR grant HIDITSA (ANR-17-CE40-0003). The authors would like to thank Monika Bhattacharjee, Nicholas Cook, and David Renfrew for fruitful discussions.

Appendix A Supplementary proofs

A.1 Proof of Proposition 3

Given , we have by Markov’s inequality that . Let . By Hoeffding’s concentration inequality, we have

Given , let be the event

Then we just showed that

Let be such that . Assume without loss of generality that . To obtain the result, it is enough to prove that

| (67) |

where depend on and only.

Define , where the are independent copies of a random variable whose law is the distribution of conditionally on the event . Recalling that is the orthogonal projection on the subspace of the vectors that are supported by , we note that . Then, the inequality (67) will be established if we show that

Write , and define the subspace . Since , the claim can be reduced to

| (68) |

Consider the disc , and define the convex and -Lipschitz function

If we denote as the probability law of an element of , then (68) can be re-expressed as

| (69) |

We can now make use of Talagrand’s concentration inequality, which shows that

| (70) |

where is a median of under . This inequality shows that there exists a constant such that

| (71) |

Writing , we now have

Observe that . From the assumption on the -th moment, , and hence, . We can similarly show that . Thus, . Moreover, since , we have

Assuming that , and using (71), this leads to:

for above a value that depends on and only. Put . Observing that in this case, , we can apply (70) to obtain

and (69) follows after bounding and adjusting and in a straightforward manner. This concludes the proof of Proposition 3.

A.2 Proof of Lemma 33

We start by showing that , the proof for the other being similar. Applying the NP inequality to the function , we get that

| (72) |

We focus on the first term at the right hand side of this inequality, the other term being treated similarly. Using Equation (43),

Hence, using the inequality when the matrix is Hermitian and non-negative, we get

This shows that .

We now show that (proof is similar for other ). Writing this time , we also use the inequality (72) to bound . Here we have

thus,

| (73) |

We have . Moreover,

Using, e.g., [34, Prop. 2.3], we get that there exists a constant such that (we note here that [34, Prop 2.3] can be applied to the Gaussian real case. Extension to the complex Gaussian case is easy). Thus, . It is clear that , and hence, by the Cauchy-Schwarz inequality. The third term at the right hand side of Inequality (73) can be dealt with similarly, which shows that . The term involving at the right hand side of (72) can be bounded in a similar manner, leading to the bound . This concludes the proof.

References

- [1] Z. Bai and J. W. Silverstein. Spectral analysis of large dimensional random matrices. Springer Series in Statistics. Springer, New York, second edition, 2010.

- [2] M. Bhattacharjee and A. Bose. Estimation of autocovariance matrices for infinite dimensional vector linear process. J. Time Series Anal., 35(3):262–281, 2014.

- [3] M. Bhattacharjee and A. Bose. Large sample behaviour of high dimensional autocovariance matrices. Ann. Statist., 44(2):598–628, 2016.

- [4] M. Bhattacharjee and A. Bose. Polynomial generalizations of sample variance-covariance matrices when . Random Matrices: Theory and Applications, 5(4):1650014, 2016.

- [5] M. Bhattacharjee and A. Bose. Large Covariance and Autocovariance Matrices. Chapman & Hall/CRC, Boca Raton, London, New York, 2018.

- [6] M. Bhattacharjee and A. Bose. Joint convergence of sample autocovariance matrices when with application. Ann. Statist., 2019. To appear.

- [7] Ch. Bordenave and D. Chafaï. Around the circular law. Probab. Surv., 9:1–89, 2012.

- [8] S. Chatterjee and A. Bose. A new method for bounding rates of convergence of empirical spectral distributions. J. Theoret. Probab., 17(4):1003–1019, 2004.

- [9] N. Cook. Lower bounds for the smallest singular value of structured random matrices. Ann. Probab., 46(6):3442–3500, 11 2018.

- [10] N. Cook, W. Hachem, J. Najim, and D. Renfrew. Limiting spectral distribution for non-Hermitian random matrices with a variance profile. ArXiv e-prints, December 2016.

- [11] J. Feinberg and A. Zee. Non-Hermitian random matrix theory: method of Hermitian reduction. Nuclear Phys. B, 504(3):579–608, 1997.

- [12] J. S. Geronimo and T. P. Hill. Necessary and sufficient condition that the limit of Stieltjes transforms is a Stieltjes transform. J. Approx. Theory, 121(1):54–60, 2003.

- [13] V. L. Girko. The circular law. Teor. Veroyatnost. i Primenen., 29(4):669–679, 1984. English translation: Theory Probab. Appl. 29 (1984), no. 4, 694-706.

- [14] J. Glimm and A. Jaffe. Quantum Physics. A functional integral point of view. Springer-Verlag, New York, second edition, 1987.

- [15] F. Götze. Asymptotic expansions for bivariate von Mises functionals. Z. Wahrsch. Verw. Gebiete, 50(3):333–355, 1979.

- [16] F. Götze and A. Tikhomirov. The circular law for random matrices. Ann. Probab., 38(4):1444–1491, 07 2010.

- [17] F. Götze and A. Tikhomirov. On the asymptotic spectrum of products of independent random matrices. arXiv preprint arXiv:1012.2710, 2010.

- [18] A. Guionnet, M. Krishnapur, and O. Zeitouni. The single ring theorem. Ann. of Math. (2), 174(2):1189–1217, 2011.

- [19] U. Haagerup and S. Thorbjørnsen. A new application of random matrices: is not a group. Ann. of Math. (2), 162(2):711–775, 2005.

- [20] S. S. Haykin and A. O. Steinhardt. Adaptive radar detection and estimation, volume 11. Wiley-Interscience, 1992.

- [21] R. A. Horn and C. R. Johnson. Matrix Analysis. Cambridge University Press, Cambridge, 1990. Corrected reprint of the 1985 original.

- [22] A. M. Khorunzhy and L. A. Pastur. Limits of infinite interaction radius, dimensionality and the number of components for random operators with off-diagonal randomness. Comm. Math. Phys., 153(3):605–646, 1993.

- [23] W. Li, Z. Li, and J. Yao. Joint central limit theorem for eigenvalue statistics from several dependent large dimensional sample covariance matrices with application. Scandinavian Journal of Statistics, 45(3):699–728, 2018.

- [24] Z. Li, C. Lam, J. Yao, and Q. Yao. On testing for high-dimensional white noise. arXiv preprint arXiv:1808.03545, 2018.

- [25] A. E. Litvak, A. Pajor, M. Rudelson, and N. Tomczak-Jaegermann. Smallest singular value of random matrices and geometry of random polytopes. Adv. Math., 195(2):491–523, 2005.

- [26] H. Liu, A. Aue, and D. Paul. On the Marčenko-Pastur law for linear time series. Ann. Statist., 43(2):675–712, 2015.

- [27] Ph. Loubaton. On the almost sure location of the singular values of certain Gaussian block-Hankel large random matrices. J. Theoret. Probab., 29(4):1339–1443, 2016.

- [28] H. H. Nguyen. On the least singular value of random symmetric matrices. Electron. J. Probab., 17:no. 53, 19, 2012.

- [29] L. A. Pastur. A simple approach to the global regime of Gaussian ensembles of random matrices. Ukraïn. Mat. Zh., 57(6):790–817, 2005.

- [30] L. A. Pastur and M. Shcherbina. Eigenvalue Distribution of Large Random Matrices, volume 171 of Mathematical Surveys and Monographs. American Mathematical Society, Providence, RI, 2011.

- [31] C. R. Rao and S. K. Mitra. Generalized inverse of matrices and its applications. John Wiley & Sons, Inc., New York-London-Sydney, 1971.

- [32] H. P. Rosenthal. On the subspaces of () spanned by sequences of independent random variables. Israel Journal of Mathematics, 8(3):273–303, Sep 1970.

- [33] M. Rudelson and R. Vershynin. The Littlewood-Offord problem and invertibility of random matrices. Adv. Math., 218(2):600–633, 2008.

- [34] M. Rudelson and R. Vershynin. Smallest singular value of a random rectangular matrix. Comm. Pure Appl. Math., 62(12):1707–1739, 2009.

- [35] A. Sidorenko. A correlation inequality for bipartite graphs. Graphs Combin., 9(2):201–204, 1993.

- [36] T. Tao. Topics in Random Matrix Theory, volume 132 of Graduate Studies in Mathematics. American Mathematical Society, Providence, RI, 2012.

- [37] T. Tao and V. Vu. Random matrices: universality of ESDs and the circular law. Ann. Probab., 38(5):2023–2065, 2010. With an appendix by Manjunath Krishnapur.

- [38] T. Tao and V. H. Vu. Inverse Littlewood-Offord theorems and the condition number of random discrete matrices. Ann. of Math. (2), 169(2):595–632, 2009.

- [39] H. L. Van Trees. Optimum array processing: Part IV of detection, estimation, and modulation theory. John Wiley & Sons, 2002.

- [40] R. Vershynin. Invertibility of symmetric random matrices. Random Structures & Algorithms, 44(2):135–182, 2014.

- [41] L. Wang, A. Aue, and D. Paul. Spectral analysis of linear time series in moderately high dimensions. Bernoulli, 23(4A):2181–2209, 2017.

- [42] F. Wegner. Bounds on the density of states in disordered systems. Z. Phys. B, 44(1-2):9–15, 1981.

- [43] Y. Q. Yin, Z. D. Bai, and P. R. Krishnaiah. On the limit of the largest eigenvalue of the large-dimensional sample covariance matrix. Probab. Theory Related Fields, 78(4):509–521, 1988.