A stochastic approximation method for approximating the efficient frontier of chance-constrained nonlinear programs††thanks: This research is supported by the Department of Energy, Office of Science, Office of Advanced Scientific Computing Research, Applied Mathematics program under Contract Number DE-AC02-06CH11347.

Version 2: November 8, 2019

Version 1: December 17, 2018)

Abstract

We propose a stochastic approximation method for approximating the efficient frontier of chance-constrained nonlinear programs.

Our approach is based on a bi-objective viewpoint of chance-constrained programs that seeks solutions on the efficient frontier of optimal objective value versus risk of constraint violation.

To this end, we construct a reformulated problem whose objective is to minimize the probability of constraints violation subject to deterministic convex constraints (which includes a bound on the objective function value).

We adapt existing smoothing-based approaches for chance-constrained problems to derive a convergent sequence of smooth approximations of our reformulated problem, and apply a projected stochastic subgradient algorithm to solve it.

In contrast with exterior sampling-based approaches (such as sample average approximation) that approximate the original chance-constrained program with one having finite support, our proposal converges to stationary solutions of a smooth approximation of the original problem, thereby avoiding poor local solutions that may be an artefact of a fixed sample.

Our proposal also includes a tailored implementation of the smoothing-based approach that chooses key algorithmic parameters based on problem data.

Computational results on four test problems from the literature indicate that our proposed approach can

efficiently determine good approximations of the efficient frontier.

Key words: stochastic approximation, chance constraints, efficient frontier, stochastic subgradient

1 Introduction

Consider the following chance-constrained nonlinear program (NLP):

| (CCP) | |||||

| s.t. |

where is a nonempty closed convex set, is a random vector with probability distribution supported on , is a continuous quasiconvex function, is continuously differentiable, and the constant is a user-defined acceptable level of constraint violation. We explore a stochastic approximation algorithm for approximating the efficient frontier of optimal objective value for varying levels of the risk tolerance in (CCP), i.e., to find a collection of solutions which have varying probability of constraint violation, and where for each such solution the objective function value is (approximately) minimal among solutions having that probability of constraint violation or smaller (see also [52, 40]). Most of our results only require mild assumptions on the data defining the above problem, such as regularity conditions on the functions and the ability to draw independent and identically distributed (i.i.d.) samples of from , and do not assume Gaussianity of the distribution or make structural assumptions on the functions (see Section 3). Our result regarding ‘convergence to stationary solutions’ of (CCP) additionally requires to be a continuous random variable satisfying some mild distributional assumptions. We note that Problem (CCP) can model joint nonconvex chance constraints, nonconvex deterministic constraints (by incorporating them in ), and even some recourse structure (by defining through the solution of auxiliary optimization problems, see Appendix C).

Chance-constrained programming was introduced as a modeling framework for optimization under uncertainty by Charnes et al. [15], and was soon after generalized to the joint chance-constrained case by Miller and Wagner [42] and to the nonlinear case by Prékopa [49]. Apart from a few known tractable cases, e.g., see Prékopa [50] and Lagoa et al. [37], solving chance-constrained NLPs to optimality is in general hard since the feasible region is not guaranteed to be convex and evaluating feasibility of the probabilistic constraint involves multi-dimensional integration. Motivated by a diverse array of applications [11, 32, 39, 64], many numerical approaches for chance-constrained NLPs attempt to determine good-quality feasible solutions in reasonable computation times (see Section 2 for a brief review).

Rather than solving (CCP) for a fixed , we are interested in approximating the efficient frontier between risk of constraint violation and objective value since this efficient frontier provides decision-makers with a tool for choosing the parameter in (CCP). An added advantage of estimating the efficient frontier of (CCP) is that we automatically obtain an estimate of the efficient frontier of a family of distributionally robust counterparts [36]. In this work, we investigate the potential of a stochastic subgradient algorithm [20, 30, 47] for approximating the efficient frontier of (CCP). While our proposal is more naturally applicable for approximating the efficient frontier, we also present a bisection strategy for solving (CCP) for a fixed risk level .

We begin by observing that the efficient frontier can be recovered by solving the following stochastic optimization problem [52]:

| (1) | |||||

| s.t. |

where the above formulation determines the minimum probability of constraints violation given an upper bound on the objective function value. The reformulation in (1) crucially enables the use of stochastic subgradient algorithms for its approximate solution. Assuming that (CCP) is feasible for risk levels of interest, solving (1) using varying values of the bound yields the same efficient frontier as solving (CCP) using varying values of [52].

Let , defined by if and if , denote the characteristic function of the set , and denote . Note that the following problem is equivalent to (1):

where denotes the closed convex set . The above formulation is almost in the form that stochastic gradient-type algorithms can solve [21], but poses two challenges that prevent immediate application of such algorithms: the step function is discontinuous and the function is nondifferentiable. We propose to solve a partially-smoothened approximation of the above formulation using the projected stochastic subgradient algorithm of Nurminskii [47] and Ermoliev and Norkin [26]. In particular, we use the procedure outlined in Davis and Drusvyatskiy [20] to solve our approximation (also see the closely-related proposals of Ermoliev [25], Ghadimi et al. [30], and the references in these works). To enable this, we replace the discontinuous step functions in the above formulation using smooth approximations , , to obtain the following approximation to (1):

| () |

where is shorthand for the composite function . Section 3.2 presents some options for the smooth approximations .

Our first primary contribution is to analyze the convergence of optimal solutions and stationary points of () to those of problem (1). This analysis closely follows previous work on the use of similar approximations for the chance-constrained problem (CCP) (cf. Norkin [46], Hong et al. [34], Shan et al. [57, 56], Hu et al. [35], and Geletu et al. [29]). Our analysis is required because: i. our approximations () involve a convergent sequence of approximations of the objective function of (1) rather than a convergent sequence of approximations of the feasible region of (CCP), ii. we handle joint chance-constrained NLPs directly without reducing them to the case of individual chance-constrained programs, and iii. our computational results rely on a slight generalization of existing frameworks for smooth approximation of the step function. Related to the first point, Norkin [46] analyzes smooth approximations in the probability maximization context, but their analysis is restricted to the case when the probability function being maximized is concave (see also Ermoliev et al. [28, Example 5.6], Shapiro et al. [58, Section 4.4.2], Lepp [38], and the references in Norkin [46] for related work).

Our second primary contribution is to propose a practical implementation of a method based on the projected stochastic subgradient algorithm of Nurminskii [47] and Ermoliev and Norkin [26] (we use the specific version proposed in Davis and Drusvyatskiy [20]) to obtain stationary points for problem () for varying levels of , and thus obtain an approximation of the efficient frontier. For each fixed this method yields convergence to a neighborhood of an approximately stationary solution since the objective function of () is weakly convex under mild assumptions [23, 47]. A similar approach has been proposed in Norkin [46]. In particular, Norkin [46] considers the case when the function is jointly convex with respect to and , uses Steklov-Sobolev averaging for constructing () from (1), assumes that the negative of the objective of (1) and the negative of the objective of () are ‘-concave functions’ (see Definition 2.3 of Norkin [46] or Definition 4.7 of Shapiro et al. [58]), and establishes the rate of convergence of the stochastic quasigradient method of Ermoliev [25], Nemirovsky and Yudin [45] for solving () to global optimality in this setting. Our contributions differ from those of Norkin [46] in two main respects: we present theory for the case when () may not be solved to global optimality (see Lepp [38] for a related approach), and we design and empirically test a practical implementation of a stochastic approximation algorithm for approximating the solution of (1).

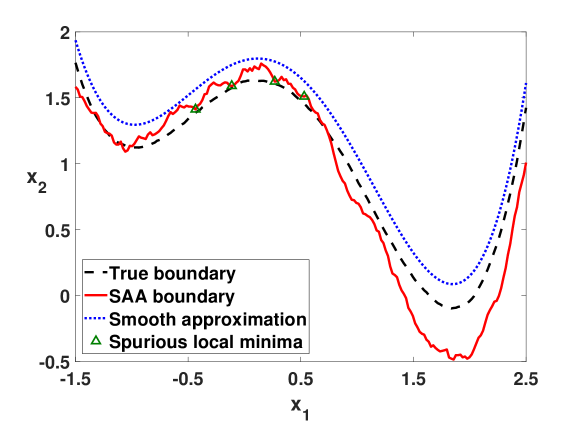

A major motivation for this study is the fact that sample average approximations [41] of (CCP) may introduce “spurious local optima” as a byproduct of sampling as illustrated by the following example from Section 5.2 of Curtis et al. [19] (see also the discussion in Ermoliev and Norkin [27, 26]).

Example 1.

Consider the instance of (CCP) with , , , , , , and with . Figure 1 plots the (lower) boundary of the feasible region defined by the chance constraint in a neighborhood of the optimal solution along with the boundaries of the feasible region generated by a ten thousand sample average approximation (SAA) of the chance constraint and the feasible region generated by the smooth approximation of the step function adopted in this work. The points highlighted by triangles in Figure 1 are local minima of the SAA approximation, but are not near any local minimia of the true problem. We refer to these as spurious local minima.

Example 1 illustrates that obtaining a local optimal solution of an accurate SAA of (CCP) may not necessarily yield a good solution even when is a ‘well-behaved’ continuous random variable that makes the probability function ‘well behaved’ (even though it might be nonconvex). While smoothing the chance constraint helps mitigate this issue (cf. Figure 1), existing algorithms [57, 29] still use SAA to solve the resulting smooth approximation. By employing a stochastic subgradient algorithm, we do not restrict ourselves to a single fixed batch of samples of the random variables, and can therefore hope to converge to truly locally optimal solutions of (). Our proposal leverages well-known advantages of stochastic subgradient-type approaches, including a low per-iteration cost, low memory requirement, good scaling with number of random variables and the number of joint chance constraints, and reasonable scaling with the number of decision variables (cf. the discussion in Nemirovski et al. [44]).

This article is organized as follows. Section 2 reviews related approaches for solving chance-constrained NLPs. Section 3 establishes consistency of the smoothing approach in the limit of its parameter values, and discusses some choices for smooth approximation of the step function. Section 4 outlines our proposal for approximating the efficient frontier of (CCP) and lists some practical considerations for its implementation. Section 5 summarizes implementation details and presents computational experiments on four test problems that illustrate the strength of our approach. We close with a summary of our contributions and some avenues for future work in Section 6. The appendices present auxiliary algorithms, omitted proofs, and computational results, and provide technical and implementation-related details for problems with recourse structure.

Notation. We use to denote a vector of ones of suitable dimension, to denote the l.s.c. step function, , , , where denotes the Euclidean norm, and ‘a.e.’ for the quantifier ‘almost everywhere’ with respect to the probability measure . Given functions and , , we write to denote and to denote the element-wise composition . Given a set , we let denote its convex hull, denote its indicator function, i.e., if , and zero otherwise, denote its normal cone at a vector and to denote the projection of onto (we abuse notation to write when is a nonempty closed convex set), and denote its cardinality when it is a finite set. Given a twice differentiable function , we write and to denote its first and second derivatives at . Given a locally Lipschitz continuous function , we write to denote its Clarke generalized gradient at a point [17] and to denote its -subdifferential (note: ). We assume measurability of random functions throughout.

2 Review of related work

We restrict our attention in this brief review to algorithms that attempt to generate good-quality feasible solutions to chance-constrained nonlinear programs.

In the scenario approximation approach, a fixed sample of the random variables from the distribution is taken and the sampled constraints , , are enforced in lieu of the chance constraint . The advantage of this approach is that the scenario problem is a standard NLP that can be solved using off-the-shelf solvers. Calafiore, Campi, and Garatti [10, 12] present upper bounds on the sample size required to ensure that the solution of the scenario problem is feasible for (CCP) with a given probability when the functions are convex for each fixed . When the functions do not possess the above convexity property but instead satisfy alternative Lipschitz assumptions, Luedtke and Ahmed [41, Section 2.2.3] determine an upper bound on that provides similar theoretical guarantees for a slightly perturbed version of the scenario problem. A major limitation of scenario approximation is that it lacks strong guarantees on solution quality [41, 52]. A related approach for obtaining feasible solutions to (CCP) constructs convex approximations of the feasible region using conservative convex approximations of the step function [43, 53, 16]. Such approximations again may result in overly conservative solutions, e.g., see Hong et al. [34] and Cao and Zavala [13].

There has been a recent surge of interest in iterative smoothing-based NLP approaches in which the chance constraint is replaced by a convergent sequence of smooth approximations. To illustrate these approaches, consider first the case when we only have an individual chance constraint (i.e., ), and suppose is approximated by , where is a monotonic sequence of smooth approximations converging to the step function. If each element of is chosen to overestimate the step function, then solving the sequence of smooth approximations furnishes feasible solutions to (CCP) of improving quality. Due to the difficulty in evaluating high-dimensional expectations in general, the smooth approximation is typically applied to a scenario-based approximation. Joint chance constraints have been accommodated either by replacing the function in with its own convergent sequence of smooth approximations [35, 56], or by conservatively approximating (CCP) using a Bonferroni-type approximation [43].

Lepp (see [38] and the references therein) proposes a stochastic version of a modified Lagrangian algorithm for solving progressively refined smooth approximations of individual chance-constrained NLPs with a differentiable probability function , and establishes almost sure convergence to stationary solutions of (CCP). A key difference between our proposal and Lepp’s [38] is that the latter requires a diverging sequence of mini-batch sizes to ensure convergence. Andrieu et al. [5] propose smoothing and finite difference-based stochastic Arrow-Hurwicz algorithms for individual chance-constrained NLPs with continuous random variables, and establish local convergence to stationary solutions under relatively strong assumptions.

Hong et al. [34] propose a sequence of conservative nonsmooth difference-of-convex (DC) approximations of the step function and use it to solve joint chance-constrained convex programs. They establish convergence of any stationary/optimal solution of the DC approximation scheme to the set of stationary/optimal solutions of (CCP) in the limit under certain assumptions. Hu et al. [35] build on this work by developing a sequence of conservative smooth approximations of joint chance-constrained convex programs (using log-sum-exp approximations of the function), and use a sequential convex approximation algorithm to solve their smooth approximation of a SAA of (CCP). Shan et al. [57, 56] develop a family of conservative smooth DC approximations of the step function, also employ conservative log-sum-exp approximations of the function to construct smooth approximations of (CCP), and provide similar theoretical guarantees as Hong et al. [34] under slightly weaker assumptions. Geletu et al. [29] propose a framework for conservative analytic approximations of the step function, provide similar theoretical guarantees as these works, and illustrate the applicability of their framework for individual chance-constrained NLPs using a class of sigmoid-like smoothing functions. They also propose smooth outer-approximations of (CCP) for generating lower bounds. Adam et al. [1, 3] develop a continuous relaxation of SAAs of (CCP), and propose to use smooth approximations of the step function that are borrowed from the literature on mathematical programs with complementarity constraints along with Benders’ decomposition [7] to determine stationary points. Cao and Zavala [13] propose a nonsmooth sigmoidal approximation of the step function, and use it to solve a smooth approximation of a SAA of individual chance-constrained NLPs. They propose to initialize their algorithm using the solution of a SAA of a conservative approximation of (CCP) obtained by replacing the step function with a convex overestimate [53]. Finally, Peña-Ordieres et al. [48] also consider using a smooth approximation on an SAA of (CCP), analyze the joint convergence with respect to sample size and sequence of smooth approximations, propose to solve a quantile-based approximation, and devise a trust-region method to solve the approximation when applied to a joint chance constraint.

An alternative to smoothing the chance constraint is to solve a SAA problem directly using mixed-integer NLP techniques, which may be computationally challenging, especially when the constraint functions are not convex with respect to the decisions . Several tailored approaches [40, 61] have been proposed for solving SAAs of chance-constrained convex programs. Curtis et al. [19] attempt to directly solve a SAA of (CCP) using NLP techniques. They develop an exact penalty function for the SAA, and propose a trust region algorithm that solves quadratic programs with linear cardinality constraints to converge to stationary points of (CCP).

Another important body of work by van Ackooij and Henrion [59, 60] establishes (sub)gradient formulae for the probability function when the function possesses special structure and is a Gaussian or Gaussian-like distribution. These approaches employ internal sampling to numerically evaluate (sub)gradients, and can be used within a NLP framework for computing stationary point solutions to (CCP). When Problem (CCP) possesses certain special structures, NLP approaches based on ‘-efficient points’ [22, 62] can also be employed for its solution.

The recent independent work of Adam and Branda [2] also considers a stochastic approximation method for chance-constrained NLPs. They consider the case when the random vector has a discrete distribution with finite (but potentially large) support, rewrite the chance constraint in (CCP) using a quantile-based constraint, develop a penalty-based approach to transfer this constraint to the objective, and employ a mini-batch projected stochastic subgradient method to determine an approximately stationary solution to (CCP) for a given risk level. This work does not include a analysis that shows the method converges to a stationary solution.

3 The smoothing approach

In the first part of this section, we establish conditions under which global/stationary solutions of convergent sequences of smooth approximations () converge to a global/stationary solution of (1). We then present some concrete examples of sequences of smooth approximations that can be accommodated within this framework.

3.1 Consistency

We establish sufficient conditions under which solving a sequence of smooth approximations () of the stochastic program (1) yields a point on the efficient frontier of (CCP). The techniques in this section follow closely those in previous work that analyzed similar convergence for (CCP) (cf. Hong et al. [34], Shan et al. [57, 56], Hu et al. [35], and Geletu et al. [29]). We use the following assumptions on Problem (1) in our analysis. Not all results we present require all these assumptions; the required assumptions are included in the statements of our results.

Assumption 1.

The convex set is nonempty and compact.

Assumption 2.

For each , .

Assumption 3.

The following conditions on the functions hold for each and :

-

A.

The function is Lipschitz continuous on with a nonnegative measurable Lipschitz constant satisfying .

-

B.

The gradient function is Lipschitz continuous on with a measurable Lipschitz constant satisfying .

-

C.

There exist positive constants satisfying , .

Assumption 1 is used to ensure that Problem (1) is well defined (see Lemma 1). Assumption 2 guarantees that the family of approximations of the function considered converge pointwise to it on in the limit of their parameter values (see Proposition 1). This assumption, when enforced, essentially restricts to be a continuous random variable (see Lemma 1 for a consequence of this assumption). Assumption 3 is a standard assumption required for the analysis of stochastic approximation algorithms that serves two purposes: it ensures that the approximations of the function possess important regularity properties (see Lemma 2), and it enables the use of the projected stochastic subgradient algorithm for solving the sequence of approximations (). Note that Assumption 2 is implied by Assumption 6B, which we introduce later, and that Assumption 3A implies .

Lemma 1.

The probability function is lower semicontinuous. Under Assumption 2, we additionally have that is continuous on .

Proof.

Follows from Theorem 10.1.1 of Prékopa [50]. ∎

A natural approach to approximating the solution of Problem (1) is to construct a sequence of approximations () based on an associated sequence of smooth approximations that converge to the step function (cf. Section 2). In what follows, we use to denote a sequence of smooth approximations of the step function, where corresponds to a vector of approximating functions for the constraints defined by the function . Since we are mainly interested in employing sequences of approximations that depend on associated sequences of smoothing parameters (with ‘converging’ to the step function as the smoothing parameter converges to zero), we sometimes write , where , instead of to make this parametric dependence explicit. For ease of exposition, we make the following (mild) blanket assumptions on each element of the sequence of smoothing functions throughout this work. Section 3.2 lists some examples that satisfy these assumptions.

Assumption 4.

The following conditions hold for each and :

-

A.

The functions are continuously differentiable.

-

B.

Each function is nondecreasing, i.e., .

-

C.

The functions are equibounded, i.e., there exists a universal constant (independent of indices and ) such that , .

-

D.

Each approximation converges pointwise to the step function except possibly at , i.e., , or, equivalently, .

We say that ‘the strong form of Assumption 4’ holds if Assumption 4D is replaced with the stronger condition of pointwise convergence everywhere, i.e., . Note that a sequence of conservative smooth approximations of the step function (which overestimate the step function everywhere) cannot satisfy the strong form of Assumption 4, whereas sequences of underestimating smooth approximations of the step function may satisfy it (see Section 3.2). In the rest of this paper, we use to denote the approximation (again, we sometimes write instead of to make its dependence on the smoothing parameters explicit). Note that is continuous under Assumption 4, see Shapiro et al. [58, Theorem 7.43]. The following result establishes sufficient conditions under which pointwise on .

Proof.

Define by for each , and note that is continuous by virtue of Assumption 4A. Additionally, Assumption 4C implies that for each , and . By noting that for each ,

for a.e. due to Assumptions 2 and 4 (or just the strong form of Assumption 4), we obtain the stated result by Lebesgue’s dominated convergence theorem [58, Theorem 7.31]. ∎

The next two results show that a global solution of (1) can be obtained by solving a sequence of approximations () to global optimality. To achieve this, we rely on the concept of epi-convergence of sequences of extended real-valued functions (see Rockafellar and Wets [54, Chapter 7] for a comprehensive introduction).

Proposition 2.

Proof.

Define and by and , respectively. From Proposition 7.2 of Rockafellar and Wets [54], we have that epi-converges to if and only if at each

Consider the constant sequence with for each . We have

as a result of Proposition 1, which establishes the latter inequality.

To see the former inequality, consider an arbitrary sequence in converging to . By noting that the indicator function is lower semicontinuous (since is closed) and

it suffices to show to establish epi-converges to . In fact, it suffices to show the above inequality holds for any since the former inequality holds trivially for .

Define by , and note that is -integrable by virtue of Assumption 4. By Fatou’s lemma [58, Theorem 7.30], we have that

where is defined as

Therefore, it suffices to show that a.e. for each to establish the former inequality. (Note that this result holds with Assumption 2 if the strong form of Assumption 4 is made.)

Fix . Let denote an index at which the maximum in is attained, i.e., . Consider first the case when . By the continuity of the functions , for any there exists such that . Therefore

where the first inequality follows from Assumption 4B. Choosing yields

by virtue of Assumption 4D. The case when follows more directly since

where the second equality follows from Assumption 4. Since a.e. by Assumption 2, we have that a.e. for each , which concludes the proof. ∎

A consequence of the above proposition is the following key result (cf. Hong et al. [34, Theorem 2], Shan et al. [57, Theorem 4.1], Geletu et al. [29, Corollary 3.7], and Cao and Zavala [13, Theorem 5]), which establishes convergence of the optimal solutions and objective values of the sequence of approximating problems () to those of the true problem (1).

Theorem 1 has a couple of practical limitations. First, it is not applicable to situations where is a discrete random variable since it relies crucially on Assumption 2. Second, it only establishes that any accumulation point of a sequence of global minimizers of () is a global minimizer of (1). Since () involves minimizing a nonsmooth nonconvex expected-value function, obtaining a global minimizer of () is itself challenging. The next result circumvents the first limitation when the smoothing function is chosen judiciously (cf. the outer-approximations of Geletu et al. [29] and Section 3.2). Proposition 4 shows that strict local minimizers of (1) can be approximated using sequences of local minimizers of (). While this doesn’t fully address the second limitation, it provides some hope that strict local minimizers of (1) may be approximated by solving a sequence of approximations () to local optimality. Theorem 2 establishes that accumulation points of sequences of stationary solutions to the approximations () yield stationary solutions to (1) under additional assumptions.

Proposition 3.

Proof.

In fact, the proof of Proposition 3 becomes straightforward if we impose the additional (mild) condition (assumed by Geletu et al. [29]) that the sequence of smooth approximations is monotone nondecreasing, i.e., , , and . Under this additional assumption, the conclusions of Proposition 3 follow from Proposition 7.4(d) and Theorem 7.33 of Rockafellar and Wets [54].

The next result, in the spirit of Proposition 3.9 of Geletu et al. [29], shows that strict local minimizers of (1) can be approximated using local minimizers of ().

Proposition 4.

Proof.

Since is assumed to be a strict local minimizer of (1), there exists such that , . Since is compact, has a global minimum, say , due to Assumption 4A. Furthermore, has a convergent subsequence in .

Assume without loss of generality that itself converges to . Applying Theorem 1 to the above sequence of restricted minimization problems yields the conclusion that is a global minimizer of on , i.e., , . Since is a strict local minimizer of (1), this implies . Since , this implies that belongs to the open ball for sufficiently large. Therefore, is a local minimizer of for sufficiently large since it is a global minimizer of the above problem on . ∎

We are unable to establish the more desirable statement that a convergent sequence of local minimizers of approximations () converges to a local minimizer of (1) without additional assumptions (cf. Theorem 2).

The next few results work towards establishing conditions under which a convergent sequence of stationary solutions to the sequence of approximating problems () converges to a stationary point of (1). We make the following additional assumptions on each element of the sequence of smoothing functions for this purpose.

Assumption 5.

The following conditions hold for each and :

-

A.

The derivative mapping is bounded by on , i.e., , .

-

B.

The derivative mapping is Lipschitz continuous on with Lipschitz constant .

The above assumptions are mild since we let the constants and depend on the sequence index . Note that in light of Assumption 4A, Assumption 5A is equivalent to the assumption that is Lipschitz continuous on with Lipschitz constant . We make the following assumptions on the cumulative distribution function of a ‘scaled version’ of the constraint functions and on the sequence of smoothing functions to establish Proposition 6 and Theorem 2.

Assumption 6.

The following conditions on the constraint functions , the distribution of , and the sequences of smoothing functions hold for each and of interest:

-

A.

The sequence of smoothing parameters satisfies

(2) for some constant factor , i.e., for each , the smoothing parameters are chosen from a monotonically decreasing geometric sequence (with limit zero). Furthermore, the underlying smoothing function is homogeneous of degree zero, i.e.,

-

B.

For each , let be defined by , . Let denote the cumulative distribution function of , i.e., . There exists a constant such that distribution function is continuously differentiable on , where is an open subset of . Furthermore, for each , is Lipschitz continuous on with a measurable Lipschitz constant that is also Lebesgue integrable, i.e., .

-

C.

There exists a sequence of positive constants such that

Assumption 6A is a mild assumption on the choice of the smoothing functions that is satisfied by all three examples in Section 3.2. When this assumption is made in conjunction with Assumption 4B, the approximation can be rewritten as , which lends the following interpretation: the sequence of approximations can be thought of as having been constructed using the same sequence of smoothing parameter values for each constraint on a rescaled version of the constraint function . The Lipschitz continuity assumption in Assumption 6B is mild (and is similar to Assumption 4 of Shan et al. [57]). The assumption of local continuous differentiability of the distribution function in Assumption 6B is quite strong (this assumption is similar to Assumption 4 of Hong et al. [34]). A consequence of this assumption is that the function is continuously differentiable on . Finally, note that Assumption 6C is mild, see Section 3.2 for examples that (trivially) satisfy it. When made along with Assumption 4, the first part of this assumption ensures that the mapping approaches the ‘Dirac delta function’ sufficiently rapidly (cf. Remark 3.14 of Ermoliev et al. [28]).

The following result ensures that the Clarke gradient of the approximation is well defined.

Lemma 2.

Proof.

The next result characterizes the Clarke generalized gradient of the approximating objectives .

Proposition 5.

Proof.

From the corollary to Proposition 2.2.1 of Clarke [17], we have that is strictly differentiable. Theorem 2.3.9 of Clarke [17] then implies that is Clarke regular. The stronger assumptions of Theorem 2.7.2 of Clarke [17] are satisfied because of Assumption 4, Lemma 2, and the regularity of , which then yields

Noting that is Clarke regular from Proposition 2.3.6 of Clarke [17], the stated equality then follows from Proposition 2.3.12 of Clarke [17]. ∎

The next result, similar to Lemma 4.2 of Shan et al. [57], helps characterize the accumulation points of stationary solutions to the sequence of approximations ().

Proof.

See Appendix B. ∎

The following key result is an immediate consequence of the above proposition (cf. Shan et al. [57, Theorem 4.2]), and establishes convergence of Clarke stationary solutions of the sequence of approximating problems () to those of the true problem (1).

Theorem 2.

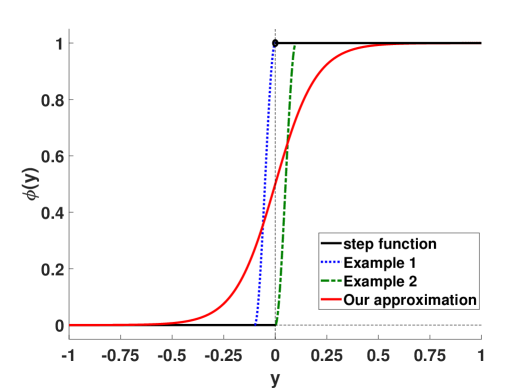

3.2 Examples of smooth approximations

We present a few examples of sequences of smooth approximations of the step function that satisfy Assumptions 4, 5, and 6. Throughout this section, we let , , denote sequences of positive reals satisfying (2).

Example 2.

Example 3.

The next example is the sequence of smooth approximations that we adopt in this work.

Example 4.

Figure 2 illustrates the above smoothing functions with the common smoothing parameter . We refer the reader to the works of Shan et al. [57], Geletu et al. [29], and Cao and Zavala [13] for other examples of ‘smooth’ approximations that can be accommodated within our framework. The next result estimates some important constants related to our smooth approximation in Example 4.

Proposition 7.

Proof.

The bounds follow by noting that for each :

where the final inequality is obtained by maximizing the function on . ∎

4 Proposed algorithm

Our proposal for approximating the efficient frontier of (CCP) involves solving a sequence of approximations () constructed using the sequence of smooth approximations of the step function introduced in Example 4. We use the projected stochastic subgradient algorithm of Davis and Drusvyatskiy [20] to obtain an approximately stationary solution to () for each value of the objective bound and each element of the sequence of smoothing parameters (note that we suppress the constraint index in our notation from here on unless necessary). Section 4.1 outlines a conceptual algorithm for approximating the efficient frontier of (CCP) using the projected stochastic subgradient algorithm, and Sections 4.2 and 4.3 outline our proposal for estimating some parameters of the algorithm in Section 4.1 that are important for a good practical implementation.

4.1 Outline of the algorithm

Algorithm 1 presents a prototype of our approach for constructing an approximation of the efficient frontier of (CCP). It takes as input an initial guess , a sequence of objective bounds , the maximum number of ‘runs’, , of the projected stochastic subgradient method, and the maximum number of iterations of the method in each run, . For each objective bound , we first determine a sequence of smoothing parameters and step lengths for the sequence of approximations (). The middle loop of Algorithm 1 then iteratively solves the sequence of approximations () with and smoothing parameters by using the solution from the previous approximation as its initial guess. The innermost loop of Algorithm 1 monitors the progress of the stochastic subgradient method over several ‘runs’. Each run generates a candidate solution with risk level (we omit the superscript in Algorithm 1 for simplicity), and we move on to the next approximation in the sequence either if insufficient progress is made over the last few runs, or if the number of runs exceeds its limit. Since the choice of the smoothing parameters , step lengths , and the termination criteria employed within Algorithm 1 are important for its practical performance, we present our proposal for estimating/setting these algorithmic parameters from the problem data in Section 4.2. First, we split Algorithm 1 into several component algorithms so that it is easier to parse.

Algorithm 2 outlines our proposal for approximating the efficient frontier of (CCP). This algorithm takes as its inputs an initial guess , an initial objective bound of interest, an objective spacing for discretizing the efficient frontier, and a lower bound on risk levels of interest that is used as a termination criterion. Section 4.2 prescribes ways to determine a good initial guess and initial bound , whereas Section 5.1 lists our setting for , , and other algorithmic parameters. The preprocessing step uses Algorithm 4 to determine a suitable initial sequence of smoothing parameters based on the problem data, and uses this choice of to determine an initial sequence of step lengths for the stochastic subgradient algorithm (see Section 4.2). Good choices of both parameters are critical for our proposal to work well. The optimization phase of Algorithm 2 uses Algorithm 3 to solve the sequence of approximations () for different choices of the objective bound (note that Algorithm 3 rescales its input smoothing parameters at the initial guess for each bound ). Finally, Algorithm 8 in the appendix adapts Algorithm 2 to solve (CCP) approximately for a given risk level .

Algorithm 3 solves a sequence of approximations () for a given objective bound using the projected stochastic subgradient algorithm of Davis and Drusvyatskiy [20] and an adaptation of the two-phase randomized stochastic projected gradient method of Ghadimi et al. [30]. This algorithm begins by rescaling the smoothing parameters at the initial guess using Algorithm 4 to ensure that the sequence of approximations () are ‘well-scaled’111We make this notion more precise in Section 4.2. at . The optimization phase then solves each element of the sequence of approximations () using two loops: the inner loop employs a mini-batch version222Although Davis and Drusvyatskiy [20] establish that mini-batching is not necessary for the convergence of the projected stochastic subgradient algorithm, a small mini-batch can greatly enhance the performance of the algorithm in practice. of the algorithm of Davis and Drusvyatskiy [20] to solve () for a given smoothing parameter , and the outer loop assesses the progress of the inner loop across multiple ‘runs/replicates’ (the initialization strategy for each run is based on Algorithm 2-RSPG-V of Ghadimi et al. [30]). Finally, the initial guess for the next approximating problem () is set to be a solution corresponding to the smallest estimate of the risk level determined thus far. This initialization step is important for the next approximating problem in the sequence to be well-scaled at its initial guess - this is why we do not solve a ‘single tight approximating problem’ () that can be hard to initialize (cf. Figure 2), but instead solve a sequence of approximations to approximate the solution of (1). Note that while the number of iterations of the inner projected stochastic subgradient loop is chosen at random as required by the theory in Davis and Drusvyatskiy [20], a practical alternative is to choose a deterministic number of iterations and set to be the solution at the final iterate. Line 17 of Algorithm 3 heuristically updates the step length to ensure good practical performance. Additionally, in contrast with the proposal of Algorithm 2-RSPG-V of Ghadimi et al. [30] that chooses the solution over the multiple runs that is closest to stationarity, motivated by practical application, we return the solution corresponding to the smallest found risk level. Because of these heuristic steps, the algorithm would require slight modification (removal of the heuristic step-size update method and different choice of the solution from multiple runs) to be assured to have the convergence guarantees of Davis and Drusvyatskiy [20]. However, as our emphasis in this paper is on deriving a practical algorithm and testing it empirically, we keep the algorithm description matching what we have implemented.

In the remainder of this section, we verify that the assumptions of Davis and Drusvyatskiy [20] hold to justify the use of their projected stochastic subgradient method for solving the sequence of approximations (). First, we verify that the objective function of () with smoothing parameter is a weakly convex function on . Next, we verify that Assumption (A3) of Davis and Drusvyatskiy [20] holds. Note that a function is said to be -weakly convex (for some ) if is convex on (see Definition 4.1 of Drusvyatskiy and Paquette [23] and the surrounding discussion).

Proposition 8.

Proof.

Follows from Lemma 4.2 of Drusvyatskiy and Paquette [23]. ∎

The following result is useful for bounding ’s weak convexity parameter in terms of known constants.

Proposition 9.

Proof.

- 1.

-

2.

From part one of Lemma 2 and Theorem 7.44 of Shapiro et al. [58], we have , . The stated result then follows from the first part of this proposition and the fact that the Frobenius norm of a matrix provides an upper bound on its spectral norm, where the existence of the quantity follows from the fact that , Assumptions 3A and 3B, and Lebesgue’s dominated convergence theorem.

∎

We derive alternative results regarding the weak convexity parameter of the approximation when (CCP) is used to model recourse formulations in Appendix C. We now establish that Assumption (A3) of Davis and Drusvyatskiy [20] holds.

Proposition 10.

4.2 Estimating the parameters of Algorithm 2

This section outlines our proposal for estimating some key parameters of Algorithm 2. We present pseudocode for determining suitable smoothing parameters and step lengths, and for deciding when to terminate Algorithm 3 with a point on our approximation of the efficient frontier.

Algorithm 4 rescales the sequence of smoothing parameters based on the values assumed by the constraints at a reference point and a Monte Carlo sample of the random vector . The purpose of this rescaling step is to ensure that the initial approximation () with smoothing parameter is ‘well-scaled’ at the initial guess . By ‘well-scaled’, we mean that the smoothing parameter is chosen (neither too large, nor too small) such that the realizations of the scaled constraint functions , , are mostly supported on the interval but not concentrated at zero. This rescaling ensures that stochastic subgradients at are not too small in magnitude. If is ‘near’ a stationary solution, then we can hope that the approximation remains well-scaled over a region of interest and that our ‘first-order algorithm’ makes good progress in a reasonable number of iterations. Note that the form of the scaling factor in Algorithm 4 is influenced by our choice of the smoothing functions in Example 4. Algorithm 5 uses the step length rule in Davis and Drusvyatskiy [20, Page 6] with the trivial bound ‘’ and sample estimates of the weak convexity parameter of and the parameter related to its stochastic subgradient. Since stochastic approximation algorithms are infamous for their sensitivity to the choice of step lengths (see Section 2.1 of Nemirovski et al. [44], for instance), Algorithm 6 prescribes heuristics for updating the step length based on the progress of Algorithm 3 over multiple runs. These rules increase the step length if insufficient progress has been made, and decrease the step length if the risk level has increased too significantly. Algorithm 6 also suggests the following heuristic for terminating the ‘runs loop’ within Algorithm 3: terminate either if the upper limit on the number of runs is hit, or if insufficient progress has been made over the last few runs.

4.3 Other practical considerations

We list some other practical considerations for implementing Algorithm 2 below.

Setting an initial guess:

The choice of the initial point for Algorithm 2 is important especially because Algorithm 3 does not guarantee finding global solutions to (). Additionally, a poor choice of the initial bound can lead to excessive effort expended on uninteresting regions of the efficient frontier. We propose to initialize and by solving a set of tuned scenario approximation problems. For instance, Algorithm 7 in the appendix can be solved with , , and a tuned sample size (tuned such that the output of this algorithm corresponds to an interesting region of the efficient frontier) to yield the initial guess and . Note that it may be worthwhile to solve the scenario approximation problems to global optimality to obtain a good initialization , e.g., when the number of scenarios is not too large (in which case they may be solved using off-the-shelf solvers/tailored decomposition techniques in acceptable computation times). Case study 4 in Section 5 provides an example where globally optimizing the scenario approximation problems to obtain an initial guess yields a significantly better approximation of the efficient frontier.

Computing projections:

Algorithm 2 requires projecting onto the sets for some multiple times while executing Algorithm 3. Thus, it may be beneficial to implement tailored projection subroutines [14], especially for sets with special structures [18] (also see Case study 2 in Section 5). If the set is a polyhedron, then projection onto may be carried out by solving a quadratic program.

Computing stochastic subgradients:

Given a point and a mini-batch of the random vector , a stochastic element of the -subdifferential of the objective of () with smoothing parameter at can be obtained as

where for each , denotes a constraint index satisfying . Note that sparse computation of stochastic subgradients can speed Algorithm 2 up significantly.

Estimating risk levels:

Given a candidate solution and a sample of the random vector , a stochastic upper bound on the risk level can be obtained as

where is the cardinality of the set and is the required confidence level, see Nemirovski and Shapiro [43, Section 4]. Since checking the satisfaction of constraints at the end of each run in Algorithm 3 may be time consuming (especially for problems with recourse structure), we use a smaller sample size (determined based on the risk lower bound ) to estimate risk levels during the course of Algorithm 3 and only use all samples of to estimate the risk level of the final solutions in Algorithm 2. If our discretization of the efficient frontier obtained from Algorithm 2 consists of points each of whose risk levels is estimated using a confidence level of , then we may conclude that our approximation of the efficient frontier is ‘achievable’ with a confidence level of at least using Bonferroni’s inequality.

Estimating weak convexity parameters:

Proposition 8 shows that the Lipschitz constant of the Jacobian on provides a conservative estimate of the weak convexity parameter of on . Therefore, we use an estimate of the Lipschitz constant as an estimate of . To avoid overly conservative estimates, we restrict the estimation of to a neighborhood of the reference point in Algorithm 5 to get at the local Lipschitz constant of the Jacobian .

Estimating :

For each point sampled from , we compute multiple realizations of the mini-batch stochastic subdifferential element outlined above to estimate . Once again, we restrict the estimation of to a neighborhood of the reference point in Algorithm 5 to get at the local ‘variability’ of the stochastic subgradients.

Estimating initial step lengths:

Algorithm 5 estimates initial step lengths for the sequence of approximations () by estimating the parameters and , which in turn involve estimating subgradients and the Lipschitz constants of . Since the numerical conditioning of the approximating problems () deteriorates rapidly as the smoothing parameters approach zero (see Figure 2), obtaining good estimates of these constants via sampling becomes challenging when increases. To circumvent this difficulty, we only estimate the initial step length for the initial approximation () with smoothing parameter by sampling, and propose the conservative initialization for (see Propositions 7, 8, 9, and 10 for a justification).

5 Computational study

We present implementation details and results of our computational study in this section. We use the abbreviation ‘EF’ for the efficient frontier throughout this section.

5.1 Implementation details

The following parameter settings are used for testing our stochastic approximation method:

- •

-

•

Algorithm 4: , , and .

-

•

Algorithm 5: , , and (assuming that ).

-

•

Algorithm 6: , , , , and .

- •

- •

-

•

Case study 2:

- •

We compare the results of our proposed approach with a tuned application of scenario approximation that enforces a predetermined number of random constraints, solves the scenario problem to local/global optimality, and determines an a posteriori estimate of the risk level at the solution of the scenario problem using an independent Monte Carlo sample (see Section 4.3) to estimate a point on the EF of (CCP). Algorithm 7 in Appendix A presents pseudocode for approximating the EF of (CCP) by solving many scenario approximation problems using an iterative (cutting-plane) approach.

Our codes are written in Julia 0.6.2 [8], use Gurobi 7.5.2 [33] to solve linear, quadratic, and second-order cone programs, use IPOPT 3.12.8 [63] to solve nonlinear scenario approximation problems (with MUMPS [4] as the linear solver), and use SCIP 6.0.0 [31] to solve nonlinear scenario approximation problems to global optimality (if necessary). The above solvers were accessed through the JuMP 0.18.2 modeling interface [24]. All computational tests333The scenario approximation problems solved to global optimality using SCIP in Case study 4 were run on a different laptop running Ubuntu 16.04 with a 2.6 GHz four core Intel i7 CPU, 8 GB of RAM due to interfacing issues on Windows. were conducted on a Surface Book 2 laptop running Windows 10 Pro with a GHz four core Intel i7 CPU, GB of RAM.

5.2 Numerical experiments

We tested our approach on four test cases from the literature. We present basic details of the test instances below. The Julia code and data for the test instances are available at https://github.com/rohitkannan/SA-for-CCP. For each test case, we compared the EFs generated by the stochastic approximation method against the solutions obtained using the tuned scenario approximation method and, if available, the analytical EF. Because the output of our proposed approach is random, we present enclosures of the EF generated by our proposal over ten different replicates in Appendix D for each case study. These results indicate that the output of the proposed method does not vary significantly across the replicates.

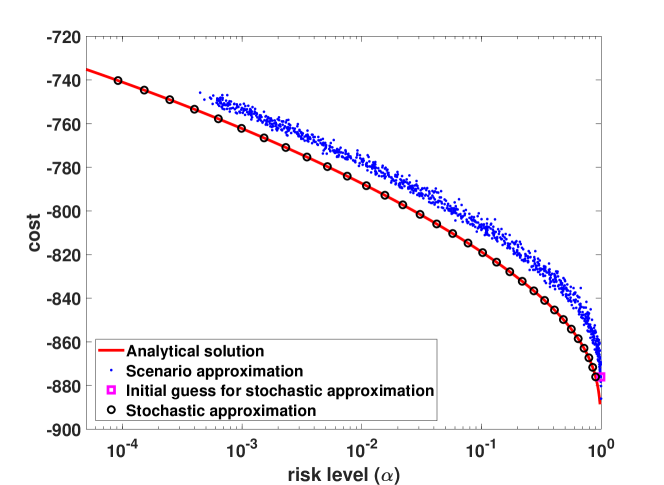

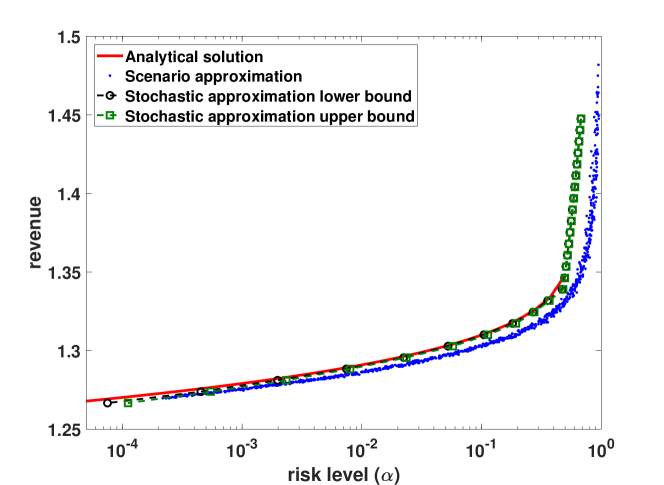

Case study 1.

This portfolio optimization instance is based on Example 2.3.6 in Ben-Tal et al. [6], and includes a single individual linear chance constraint:

| s.t. |

where is the standard simplex, denotes the fraction of investment in stock , is a random vector of returns with joint normal probability distribution, and , , and . We consider the instance with number of stocks . We assume the returns are normally distributed so that we can benchmark our approach against an analytical solution for the true EF when the risk level (e.g., see Prékopa [50, Theorem 10.4.1]).

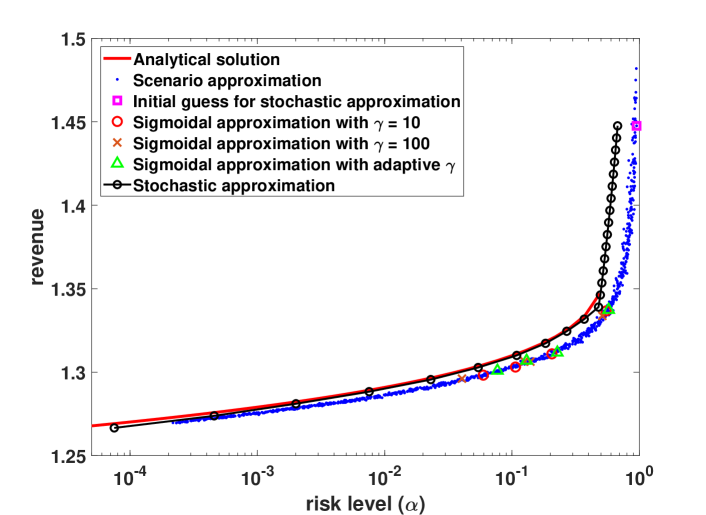

Figure 3 compares a typical EF obtained using our approach against the analytical EF and the solutions generated by the tuned scenario approximation algorithm. Our proposal is able to find a very good approximation of the true EF, whereas the scenario approximation method finds solutions that can be improved either in objective or risk. Our proposed approach took seconds on average (and a maximum of seconds) to approximate the EF using points, whereas the tuned scenario approximation method took a total of seconds to generate its points in Figure 3. Note that even though the above instance of (CCP) does not satisfy Assumption 1 as written (because is not compact), we can essentially incorporate the upper bound within the definition of the set because the solution to Problem () always satisfies .

Since existing smoothing-based approaches provide the most relevant comparison, we compare our results with one such approach from the literature. We choose the smoothing-based approach of Cao and Zavala [13] for comparison because: i. they report encouraging computational results in their work relative to other such approaches, and ii. they have made their implementation available. Table 1 summarizes typical results of the sigmoidal smoothing approach of Cao and Zavala [13] when applied to the above instance with a specified risk level of , with a varying number of scenarios, and with different settings for the scaling factor of the sigmoidal approximation method (see Algorithm SigVar-Alg of Cao and Zavala [13]). Appendix A.3 lists details of our implementation of this method. The second, third, and fourth columns of Table 1 present the overall solution time in seconds (or a failure status returned by IPOPT), the best objective value and the true risk level of the corresponding solution returned by the method over two replicates (we note that there was significant variability in solution times over the replicates; we report the results corresponding to the smaller solution times). Figure 3 plots the solutions returned by this method (using the values listed in Table 1). The relatively poor performance of Algorithm SigVar-Alg on this example is not surprising; even the instance of the sigmoidal approximation problem with only a hundred scenarios (which is small for ) has more than a thousand variables and a hundred thousand nonzero entries in the (dense) Jacobian. Therefore, tailored approaches have to be developed for solving these problems efficiently. Since our implementation of the proposal of Cao and Zavala [13] failed to perform well on this instance even for a single risk level, we do not compare against their approach for the rest of the case studies.

| Num. scenarios | adaptive | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Time | Obj | Risk | Time | Obj | Risk | Time | Obj | Risk | |

| 100 | 34 | 1.337 | 0.548 | 23 | 1.334 | 0.513 | 29 | 1.337 | 0.575 |

| 500 | 508 | 1.311 | 0.206 | 106 | 1.306 | 0.139 | 59 | 1.312 | 0.227 |

| 1000 | 606 | 1.303 | 0.106 | 1203 | 1.306 | 0.125 | 1011 | 1.307 | 0.130 |

| 2000 | 1946 | 1.298 | 0.059 | 296 | 1.296 | 0.040 | 2787 | 1.301 | 0.077 |

| 5000 | 4050 | 1.226 | 6289 | 1.292 | 0.025 | infeas | |||

| 10000 | 2708 | 1.199 | tle | tle |

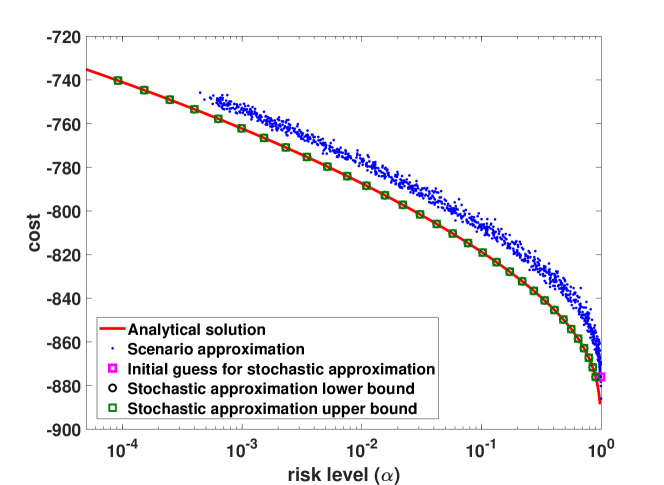

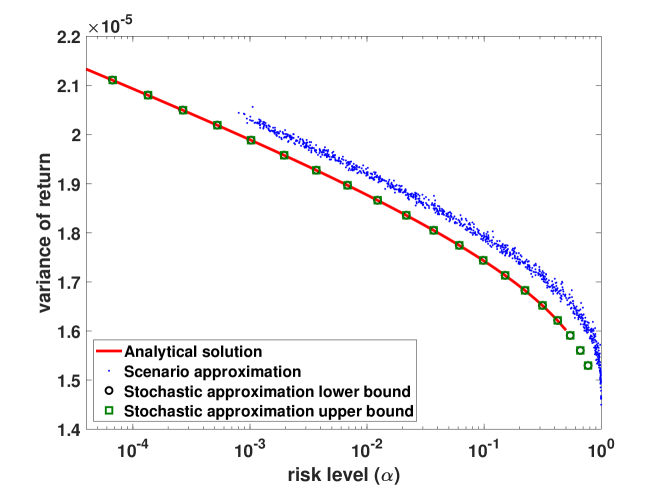

Case study 2.

We consider the following variant of Case study 1 where the variance of the portfolio is minimized subject to the constraint that the return is larger than a fixed threshold at least with a given probability:

| s.t. |

where we require that the percentile of the return is at least . Once again, we consider the instance with number of stocks , and assume the returns are normally distributed as in Case study 1 so that we can benchmark our approach against the analytical solution for the true EF.

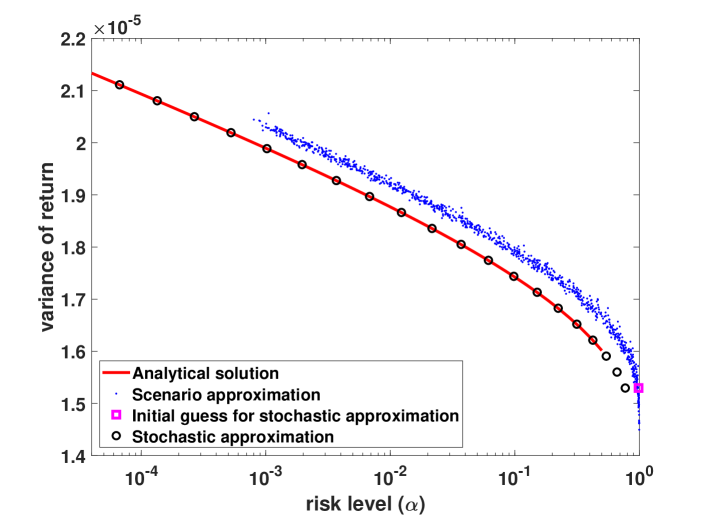

We found that using a general-purpose NLP solver to solve the quadratically-constrained quadratic program to compute projections onto the set during the course of Algorithm 2 was a bottleneck of the algorithm in this case. Thus, we implemented a tailored projection routine that exploits the structure of this projection problem. Appendix A.4 presents details of the projection routine. Figure 4 compares a typical EF obtained using our approach against the analytical EF and the solutions generated by the tuned scenario approximation algorithm. Our proposal is able to generate solutions that lie on or very close to the true EF, whereas the scenario approximation method finds solutions that can be improved either in objective or risk. Our proposed approach took seconds on average (and a maximum of seconds) to approximate the EF using points, whereas the tuned scenario approximation method took a total of seconds to generate its points in Figure 4.

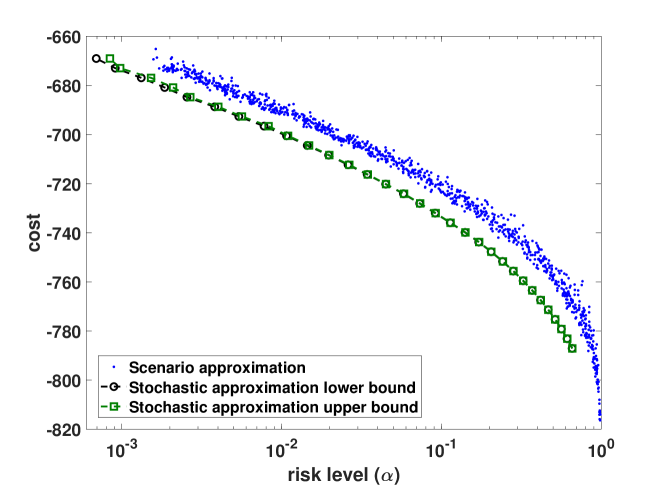

Case study 3.

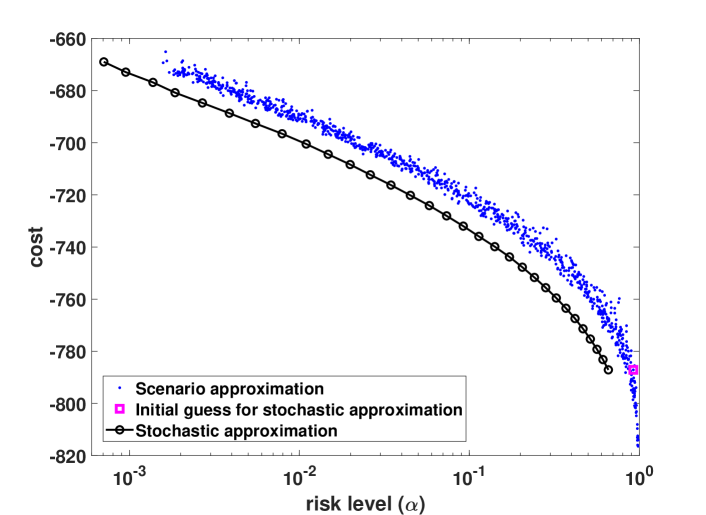

This norm optimization instance is based on Section 5.1.2 of Hong et al. [34], and includes a joint convex nonlinear chance constraint:

| s.t. |

where are dependent normal random variables with mean and variance , and cov if , cov if . We consider the instance with number of variables , number of constraints , and bound . Figure 5 compares a typical EF obtained using our approach against the solutions generated by the tuned scenario approximation algorithm. Once again, our proposed approach is able to find a significantly better approximation of the EF than the scenario approximation method, although it is unclear how our proposal fares compared to the true EF since it is unknown in this case. Our proposal took seconds on average (and a maximum of seconds) to approximate the EF using points, whereas it took tuned scenario approximation a total of seconds to generate its points in Figure 5. We note that more than of the reported times for our method is spent in generating random numbers because the random variable is high-dimensional and the covariance matrix of the random vector is full rank. A practical instance might have a covariance matrix rank that is at least a factor of ten smaller, which would reduce our overall computation times roughly by a factor of three (cf. the smaller computation times reported for the similar Case study 5 in the appendix). Appendix D benchmarks our approach against the true EF when the random variables are assumed to be i.i.d. in which case the analytical solution is known (see Section 5.1.1 of Hong et al. [34]). Once again, note that Assumption 1 does not hold because the set is not compact; however, we can easily deduce an upper bound on each , , that is required for feasibility of the chance constraint for the largest (initial) risk level of interest and incorporate this upper bound within the definition of without altering the EF.

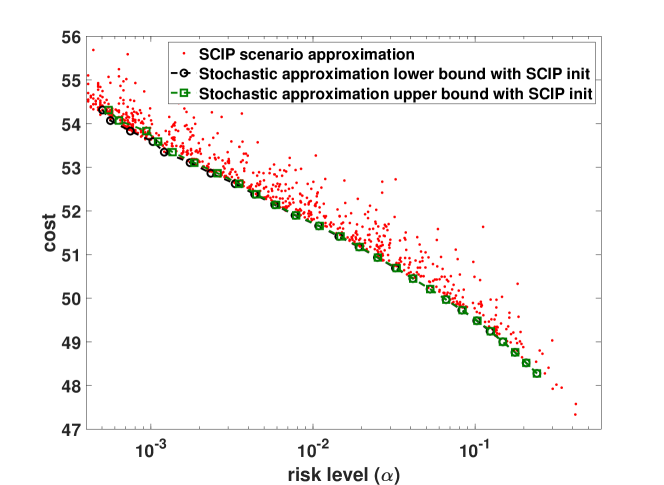

Case study 4.

This probabilistic resource planning instance is based on Section 3 of Luedtke [40], and is modified to include a nonconvex recourse constraint:

| s.t. |

where denotes the quantity of resource , denotes the unit cost of resource ,

denotes the number of customer types, denote the amount of resource allocated to customer type , is a random variable that denotes the yield of resource , is a random variable that denotes the demand of customer type , and is a deterministic scalar that denotes the service rate of resource for customer type . Note that the nonlinear term in the definition of is a modification of the corresponding linear term in Luedtke [40]. This change could be interpreted as a reformulation of the instance in Luedtke [40] with concave objective costs (due to economies of scale). We consider the instance with number of resources and number of customer types . Details of how the parameters of the model are set (including details of the random variables) can be found in the electronic companion to Luedtke [40].

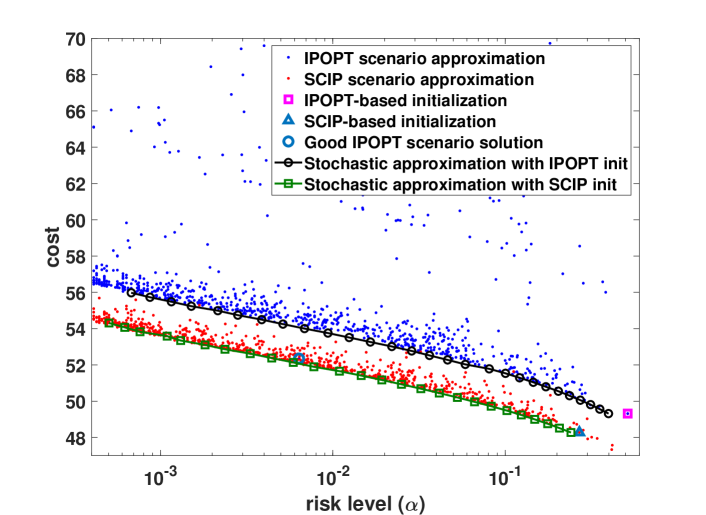

Figure 6 compares a typical EF obtained using our approach against the solutions generated by the tuned scenario approximation algorithm. The blue dots in the top part of Figure 6 correspond to the points obtained using the scenario approximation method when IPOPT is used to solve the scenario approximation problems. We mention that the vertical axis has been truncated for readability; the scenario approximation yields some solutions that are further away from the EF (with objective values up to for the risk levels of interest). The red dots in the bottom part of Figure 6 correspond to the points obtained by solving the scenario approximation problems to global optimality using SCIP. The top black curve (with circles) corresponds to the EF obtained using the stochastic approximation method when it is initialized using the IPOPT solution of a scenario approximation problem. When a better initial point obtained by solving a scenario approximation problem using SCIP is used, the stochastic approximation method generates the bottom green curve (with squares) as its approximation of the EF.

Several remarks are in order. The scenario approximation solutions generated using the local solver IPOPT are very scattered possibly because IPOPT gets stuck at suboptimal local minima. However, the best solutions generated using IPOPT provide a comparable approximation of the EF as the stochastic approximation method that is denoted by the black curve with circles (which appears to avoid the poor local minima encountered by IPOPT). We note that IPOPT finds a good local solution at one of the scenario approximation runs (indicated by the blue circle). Solving the scenario approximation problems to global optimality using SCIP yields a much better approximation of the EF than the local solver IPOPT. Additionally, when the proposed approach is initialized using the global solution obtained from SCIP for a single scenario approximation problem (which took less than seconds to compute), it generates a significantly better approximation of the EF that performs comparably to the EF generated using the global solver SCIP. We also tried initializing the solution of IPOPT with the one global solution from SCIP, and this did not yield a better approximation of the EF. Our approach took seconds on average (and a maximum of seconds) to generate the green curve (with squares) approximation of the EF using points, whereas it took the blue scenario approximations (solved using IPOPT) and the red scenario approximations (solved using SCIP) a total of seconds and seconds, respectively, to generate their points in Figure 6.

6 Conclusion and future work

We proposed a stochastic approximation algorithm for estimating the efficient frontier of chance-constrained NLPs. Our proposal involves solving a sequence of partially smoothened stochastic optimization problems to local optimality using a projected stochastic subgradient algorithm. We established that every limit point of the sequence of stationary/global solutions of the above sequence of approximations yields a stationary/global solution of the original chance-constrained program with an appropriate risk level. A potential advantage of our proposal is that it can find truly stationary solutions of the chance-constrained NLP unlike scenario-based approaches that may get stuck at spurious local optima generated by sampling. Our computational experiments demonstrated that our proposed approach is consistently able to determine good approximations of the efficient frontier in reasonable computation times.

Extensions of our proposal that can handle multiple sets of joint chance constraints merit further investigation. One option is to minimize the maximum risk of constraints violation over the various sets of joint chance constraints, which can be formulated as a minimax stochastic program (cf. Section 3.2 of Nemirovski et al. [44]). This can in turn be reformulated as a weakly convex-concave saddle point problem that can be solved to stationarity using existing techniques [51]. Since our proposal relies on computing projections efficiently, approaches for reducing the computational effort spent on projections, such as random constraint projection techniques, could be explored. Additionally, extensions that incorporate deterministic nonconvex constraints in a more natural fashion provide an avenue for future work. The projected stochastic subgradient method of Davis and Drusvyatskiy [20] has recently been extended to the non-Euclidean case [65], which could accelerate convergence of our proposal in practice. Finally, because stochastic approximation algorithms are an active area of research, several auxiliary techniques, such as adaptive step sizes, parallelization, acceleration, etc., may be determined to be applicable (and practically useful) to our setting.

Acknowledgements

The authors thank the anonymous reviewers for suggestions that improved the paper. R.K. also thanks Rui Chen, Eli Towle, and Clément Royer for helpful discussions.

References

- Adam and Branda [2016] Lukáš Adam and Martin Branda. Nonlinear chance constrained problems: optimality conditions, regularization and solvers. Journal of Optimization Theory and Applications, 170(2):419–436, 2016.

- Adam and Branda [2018] Lukáš Adam and Martin Branda. Machine learning approach to chance-constrained problems: An algorithm based on the stochastic gradient descent. http://www.optimization-online.org/DB_HTML/2018/12/6983.html (Last accessed: April 1, 2019), 2018.

- Adam et al. [2018] Lukáš Adam, Martin Branda, Holger Heitsch, and René Henrion. Solving joint chance constrained problems using regularization and Benders’ decomposition. Annals of Operations Research, pages 1–27, 2018. doi: 10.1007/s10479-018-3091-9.

- Amestoy et al. [2000] Patrick R Amestoy, Iain S Duff, Jean-Yves L’Excellent, and Jacko Koster. MUMPS: a general purpose distributed memory sparse solver. In International Workshop on Applied Parallel Computing, pages 121–130. Springer, 2000.

- Andrieu et al. [2007] Laetitia Andrieu, Guy Cohen, and Felisa Vázquez-Abad. Stochastic programming with probability constraints. arXiv preprint arXiv:0708.0281, 2007.

- Ben-Tal et al. [2009] Aharon Ben-Tal, Laurent El Ghaoui, and Arkadi Nemirovski. Robust optimization. Princeton University Press, 2009.

- Benders [1962] Jacques F Benders. Partitioning procedures for solving mixed-variables programming problems. Numerische Mathematik, 4(1):238–252, 1962.

- Bezanson et al. [2017] Jeff Bezanson, Alan Edelman, Stefan Karpinski, and Viral B Shah. Julia: A fresh approach to numerical computing. SIAM Review, 59(1):65–98, 2017.

- Bienstock et al. [2014] Daniel Bienstock, Michael Chertkov, and Sean Harnett. Chance-constrained optimal power flow: Risk-aware network control under uncertainty. SIAM Review, 56(3):461–495, 2014.

- Calafiore and Campi [2005] Giuseppe Calafiore and Marco C Campi. Uncertain convex programs: randomized solutions and confidence levels. Mathematical Programming, 102(1):25–46, 2005.

- Calafiore et al. [2011] Giuseppe C Calafiore, Fabrizio Dabbene, and Roberto Tempo. Research on probabilistic methods for control system design. Automatica, 47(7):1279–1293, 2011.

- Campi and Garatti [2011] Marco C Campi and Simone Garatti. A sampling-and-discarding approach to chance-constrained optimization: feasibility and optimality. Journal of Optimization Theory and Applications, 148(2):257–280, 2011.

- Cao and Zavala [2017] Yankai Cao and Victor Zavala. A sigmoidal approximation for chance-constrained nonlinear programs. http://www.optimization-online.org/DB_FILE/2017/10/6236.pdf (Last accessed: April 1, 2019), 2017.

- Censor et al. [2012] Yair Censor, Wei Chen, Patrick L Combettes, Ran Davidi, and Gabor T Herman. On the effectiveness of projection methods for convex feasibility problems with linear inequality constraints. Computational Optimization and Applications, 51(3):1065–1088, 2012.

- Charnes et al. [1958] Abraham Charnes, William W Cooper, and Gifford H Symonds. Cost horizons and certainty equivalents: an approach to stochastic programming of heating oil. Management Science, 4(3):235–263, 1958.

- Chen et al. [2010] Wenqing Chen, Melvyn Sim, Jie Sun, and Chung-Piaw Teo. From CVaR to uncertainty set: Implications in joint chance-constrained optimization. Operations Research, 58(2):470–485, 2010.

- Clarke [1990] Frank H Clarke. Optimization and nonsmooth analysis, volume 5. SIAM, 1990.

- Condat [2016] Laurent Condat. Fast projection onto the simplex and the ball. Mathematical Programming, 158(1-2):575–585, 2016.

- Curtis et al. [2018] Frank E Curtis, Andreas Wächter, and Victor M Zavala. A sequential algorithm for solving nonlinear optimization problems with chance constraints. SIAM Journal on Optimization, 28(1):930–958, 2018.

- Davis and Drusvyatskiy [2018] Damek Davis and Dmitriy Drusvyatskiy. Stochastic subgradient method converges at the rate on weakly convex functions. arXiv preprint arXiv:1802.02988, 2018.

- Davis et al. [2018] Damek Davis, Dmitriy Drusvyatskiy, Sham Kakade, and Jason D Lee. Stochastic subgradient method converges on tame functions. arXiv preprint arXiv:1804.07795, 2018.

- Dentcheva and Martinez [2013] Darinka Dentcheva and Gabriela Martinez. Regularization methods for optimization problems with probabilistic constraints. Mathematical Programming, 138(1-2):223–251, 2013.

- Drusvyatskiy and Paquette [2018] Dmitriy Drusvyatskiy and Courtney Paquette. Efficiency of minimizing compositions of convex functions and smooth maps. Mathematical Programming, pages 1–56, 2018. doi: 10.1007/s10107-018-1311-3.

- Dunning et al. [2017] Iain Dunning, Joey Huchette, and Miles Lubin. JuMP: A modeling language for mathematical optimization. SIAM Review, 59(2):295–320, 2017.

- Ermoliev [1988] Yuri M Ermoliev. Stochastic quasigradient methods. In Yuri M Ermoliev and Roger JB Wets, editors, Numerical techniques for stochastic optimization, chapter 6, pages 141–185. Springer, 1988.

- Ermoliev and Norkin [1998] Yuri M Ermoliev and VI Norkin. Stochastic generalized gradient method for nonconvex nonsmooth stochastic optimization. Cybernetics and Systems Analysis, 34(2):196–215, 1998.

- Ermoliev and Norkin [1997] Yuri M Ermoliev and Vladimir I Norkin. On nonsmooth and discontinuous problems of stochastic systems optimization. European Journal of Operational Research, 101(2):230–244, 1997.

- Ermoliev et al. [1995] Yuri M Ermoliev, Vladimir I Norkin, and Roger JB Wets. The minimization of semicontinuous functions: mollifier subgradients. SIAM Journal on Control and Optimization, 33(1):149–167, 1995.

- Geletu et al. [2017] Abebe Geletu, Armin Hoffmann, Michael Kloppel, and Pu Li. An inner-outer approximation approach to chance constrained optimization. SIAM Journal on Optimization, 27(3):1834–1857, 2017.

- Ghadimi et al. [2016] Saeed Ghadimi, Guanghui Lan, and Hongchao Zhang. Mini-batch stochastic approximation methods for nonconvex stochastic composite optimization. Mathematical Programming, 155(1-2):267–305, 2016.

- Gleixner et al. [2018] Ambros Gleixner, Michael Bastubbe, Leon Eifler, Tristan Gally, Gerald Gamrath, Robert Lion Gottwald, Gregor Hendel, Christopher Hojny, Thorsten Koch, Marco E. Lübbecke, Stephen J. Maher, Matthias Miltenberger, Benjamin Müller, Marc E. Pfetsch, Christian Puchert, Daniel Rehfeldt, Franziska Schlösser, Christoph Schubert, Felipe Serrano, Yuji Shinano, Jan Merlin Viernickel, Matthias Walter, Fabian Wegscheider, Jonas T. Witt, and Jakob Witzig. The SCIP Optimization Suite 6.0. Technical report, Optimization Online, July 2018. URL http://www.optimization-online.org/DB_HTML/2018/07/6692.html.

- Gotzes et al. [2016] Claudia Gotzes, Holger Heitsch, René Henrion, and Rüdiger Schultz. On the quantification of nomination feasibility in stationary gas networks with random load. Mathematical Methods of Operations Research, 84(2):427–457, 2016.

- Gurobi Optimization LLC [2018] Gurobi Optimization LLC. Gurobi Optimizer Reference Manual, 2018. URL http://www.gurobi.com.

- Hong et al. [2011] L Jeff Hong, Yi Yang, and Liwei Zhang. Sequential convex approximations to joint chance constrained programs: A Monte Carlo approach. Operations Research, 59(3):617–630, 2011.

- Hu et al. [2013] Zhaolin Hu, L Jeff Hong, and Liwei Zhang. A smooth Monte Carlo approach to joint chance-constrained programs. IIE Transactions, 45(7):716–735, 2013.

- Jiang and Guan [2016] Ruiwei Jiang and Yongpei Guan. Data-driven chance constrained stochastic program. Mathematical Programming, 158(1-2):291–327, 2016.

- Lagoa et al. [2005] Constantino M Lagoa, Xiang Li, and Mario Sznaier. Probabilistically constrained linear programs and risk-adjusted controller design. SIAM Journal on Optimization, 15(3):938–951, 2005.

- Lepp [2009] Riho Lepp. Extremum problems with probability functions: Kernel type solution methods. In Christodoulos A. Floudas and Panos M. Pardalos, editors, Encyclopedia of Optimization, pages 969–973. Springer, 2009. URL https://doi.org/10.1007/978-0-387-74759-0_170.

- Li et al. [2008] Pu Li, Harvey Arellano-Garcia, and Günter Wozny. Chance constrained programming approach to process optimization under uncertainty. Computers & Chemical Engineering, 32(1-2):25–45, 2008.

- Luedtke [2014] James Luedtke. A branch-and-cut decomposition algorithm for solving chance-constrained mathematical programs with finite support. Mathematical Programming, 146(1-2):219–244, 2014.

- Luedtke and Ahmed [2008] James Luedtke and Shabbir Ahmed. A sample approximation approach for optimization with probabilistic constraints. SIAM Journal on Optimization, 19(2):674–699, 2008.

- Miller and Wagner [1965] Bruce L Miller and Harvey M Wagner. Chance constrained programming with joint constraints. Operations Research, 13(6):930–945, 1965.

- Nemirovski and Shapiro [2006] Arkadi Nemirovski and Alexander Shapiro. Convex approximations of chance constrained programs. SIAM Journal on Optimization, 17(4):969–996, 2006.

- Nemirovski et al. [2009] Arkadi Nemirovski, Anatoli Juditsky, Guanghui Lan, and Alexander Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on Optimization, 19(4):1574–1609, 2009.

- Nemirovsky and Yudin [1983] Arkadii Semenovich Nemirovsky and David Borisovich Yudin. Problem complexity and method efficiency in optimization. Wiley, 1983.

- Norkin [1993] Vladimir I Norkin. The analysis and optimization of probability functions. Technical report, IIASA Working Paper, WP-93-6, January 1993.

- Nurminskii [1973] EA Nurminskii. The quasigradient method for the solving of the nonlinear programming problems. Cybernetics, 9(1):145–150, 1973.

- Peña-Ordieres et al. [2019] Alejandra Peña-Ordieres, James R Luedtke, and Andreas Wächter. Solving chance-constrained problems via a smooth sample-based nonlinear approximation, 2019.

- Prékopa [1970] András Prékopa. On probabilistic constrained programming. In Proceedings of the Princeton symposium on mathematical programming, pages 113–138. Princeton, NJ, 1970.

- Prékopa [1995] András Prékopa. Stochastic programming, volume 324. Springer Science & Business Media, 1995.

- Rafique et al. [2018] Hassan Rafique, Mingrui Liu, Qihang Lin, and Tianbao Yang. Non-convex min-max optimization: Provable algorithms and applications in machine learning. arXiv preprint arXiv:1810.02060, 2018.

- Rengarajan and Morton [2009] Tara Rengarajan and David P Morton. Estimating the efficient frontier of a probabilistic bicriteria model. In Winter Simulation Conference, pages 494–504, 2009.

- Rockafellar and Uryasev [2000] R Tyrrell Rockafellar and Stanislav Uryasev. Optimization of conditional value-at-risk. Journal of Risk, 2:21–42, 2000.

- Rockafellar and Wets [2009] R Tyrrell Rockafellar and Roger J-B Wets. Variational analysis, volume 317. Springer Science & Business Media, 2009.

- Ruben [1962] Harold Ruben. Probability content of regions under spherical normal distributions, IV: The distribution of homogeneous and non-homogeneous quadratic functions of normal variables. The Annals of Mathematical Statistics, 33(2):542–570, 1962.

- Shan et al. [2016] F Shan, XT Xiao, and LW Zhang. Convergence analysis on a smoothing approach to joint chance constrained programs. Optimization, 65(12):2171–2193, 2016.

- Shan et al. [2014] Feng Shan, Liwei Zhang, and Xiantao Xiao. A smoothing function approach to joint chance-constrained programs. Journal of Optimization Theory and Applications, 163(1):181–199, 2014.

- Shapiro et al. [2009] Alexander Shapiro, Darinka Dentcheva, and Andrzej Ruszczyński. Lectures on stochastic programming: modeling and theory. SIAM, 2009.

- van Ackooij and Henrion [2014] Wim van Ackooij and René Henrion. Gradient formulae for nonlinear probabilistic constraints with Gaussian and Gaussian-like distributions. SIAM Journal on Optimization, 24(4):1864–1889, 2014.

- van Ackooij and Henrion [2017] Wim van Ackooij and René Henrion. (Sub-)Gradient formulae for probability functions of random inequality systems under Gaussian distribution. SIAM/ASA Journal on Uncertainty Quantification, 5(1):63–87, 2017.

- van Ackooij et al. [2016] Wim van Ackooij, Antonio Frangioni, and Welington de Oliveira. Inexact stabilized Benders’ decomposition approaches with application to chance-constrained problems with finite support. Computational Optimization and Applications, 65(3):637–669, 2016.

- van Ackooij et al. [2017] Wim van Ackooij, V Berge, Welington de Oliveira, and C Sagastizábal. Probabilistic optimization via approximate p-efficient points and bundle methods. Computers & Operations Research, 77:177–193, 2017.

- Wächter and Biegler [2006] Andreas Wächter and Lorenz T Biegler. On the implementation of an interior-point filter line-search algorithm for large-scale nonlinear programming. Mathematical programming, 106(1):25–57, 2006.