Semi-Explicit Solutions to some Non-Linear Non-Quadratic Mean-Field-Type Games:

A Direct Method

Abstract

This article examines mean-field-type game problems by means of a direct method. We provide various solvable examples beyond the classical linear-quadratic game problems. These include quadratic-quadratic games and games with power, logarithmic, sine square, hyperbolic sine square payoffs. Non-linear state dynamics such as log-state, control-dependent regime switching, quadratic state, cotangent state and hyperbolic cotangent state are considered. We identify equilibrium strategies and equilibrium payoffs in state-and-conditional mean-field type feedback form. It is shown that a simple direct method can be used to solve broader classes of non-quadratic mean-field-type games under jump-diffusion-regime switching Gauss-Volterra processes which include fractional Brownian motions and multi-fractional Brownian motions. We provide semi-explicit solutions to the fully cooperative, noncooperative nonzero-sum, and adversarial game problems.

Keywords : Non-Linear, non-quadratic systems, mean-field-type games, risk-awareness, direct method.

1 Introduction

Mean-field-type game theory studies a class of games in which the payoffs and or state dynamics depend not only on the state-action pairs but also the distribution of them. In mean-field-type games, (i) a single decision-maker can have a strong impact on the mean-field terms, (ii) the expected payoffs are not necessarily linear with respect to the state distribution, (iii) the number of decision-makers (“true decision-makers”) is not necessarily infinite.

Games with non-linearly distribution-dependent quantity-of-interest [1, 2, 3] are very attractive in terms of applications because the non-linear dependence of the payoff functions in terms of state distribution allow us to capture risk measures which are functionals of variance, inverse quantiles, and or higher moments. During the past, a significant amount of research on mean-field-type games has been performed [4, 5, 6, 8, 9, 10]. In the time-dependent case, the analysis of mean-field-type games has several challenges. Previous works have devoted tremendous effort in terms of partial integro-differential system of equations (PIDEs), in infinite dimensions, of conditional Liouville, Boltzmann, Kolmogorov or McKean-Vlasov type. At the same time, an important set of numerical tools have been developed to address the master equilibrium system. However, the current state-of-the-art of numerical schemes is problem-specific and needs to be adjusted properly depending on the underlying problem. To date, the question of computation of the master system in the general setting remains open. This work provides explicit solutions of a class of master systems. These explicit solutions can be used to build reference trajectories and several numerical schemes developed to solve PIDEs can be tested beyond the linear-quadratic setting.

1.1 Direct Method for LQ-MFTG

In the current literature, only relatively few examples of explicitly solvable mean-field-type game problems are available. The most notable examples are (i) linear-quadratic mean-field-type games (LQ-MFTG) [6], (ii) linear-exponentiated quadratic mean-field-type games (LEQ-MFTG) [7] , (ii) adversarial linear-quadratic mean-field-type games (minmax LQ, minmax LEQ-MFTG) [6]. In LQ-MFTG the base state dynamics has two components: drift and noise.

-

•

the drift is an affine function of the state, expected value of the state, control action and expected value of the control actions of all decision-makers. The coefficients are regime switching dependent.

-

•

the noises are combination of diffusion, Gauss-Volterra, jump, regime-switching process where the noise coefficients are affine functions of the state, expected value of the state, control action and expected value of the control actions of all decision-makers. The coefficients are regime switching and jump dependent.

To the state dynamics, one can add a common noise which is a diffusion-Gauss-Volterra-jump-regime-switching process. The cost functions are polynomial of degree two and include the weighted conditional variances, co-variances between state and control actions of all decision-makers. In addition, the cost functional is not measured perfectly. Only a noisy cost is available.

This basic model of LQ mean-field-type games captures several interesting features such as heterogeneity, risk-awareness and empathy of the decision-makers.

To solve LQ-MFTG problems one can use the direct method proposed in Figure 3. This solution approach does not require solving the Bellman-Kolmogorov equations or backward-forward stochastic differential equations of Pontryagin’s type. The proposed direct method can be easily implemented by beginners and engineers who are new to the emerging field of mean-field-type game theory.

For this broader class of LQ-MFTG problem one can derive a semi-explicit solution under sufficient conditions. The existence of solution to the master system corresponding to the LQ-MFTG problem can be converted into an existence of solution to a system of ordinary differential equations driven by common noises. In some particular cases, these systems are stochastic Riccati systems and extensions of Riccati to include some fractional order terms.

1.2 Direct Method beyond LQ-MFTG

The direct method is not limited to the linear-quadratic case. The direct method can be extended to a class of LEQ-MFTG, minmax LQ-MFTG and minmax LEQ-MFTG. In this article, we present several examples to illustrate how the direct method addresses non-linear and/or non-quadratic mean-field-type games. The examples below go beyond LQ-MFTG, LEQ-MFTG and minmax LQ problems.

The contributions of this article can be summarized as follows. We provide semi-explicit solution for classes of mean-field-type game problems presented in Table 1. Several noises are examined: Brownian motion , regime switching , jump process , and Gauss-Volterra process . The Gauss-Volterra noise processes are obtained from the integral of a Brownian motion with a suitable kernel function. In addition, several type of common noises are considered: . We limit ourselves to the class of state-and-conditional mean-field type feedback strategies. The analysis for more general class of strategies is beyond the scope of this article.

| Problem | State | Cost | Noise |

|---|---|---|---|

| Prop. 1 | |||

| Prop. 2 | |||

| Prop. 3 | |||

| Prop. 4 | |||

| Prop. 5 | |||

| Prop. 6 | |||

| Prop. 7 | |||

| Prop. 8 | |||

| Prop. 9 | |||

| Prop. 10 |

To the best of the authors’ knowledge this is the first work to provide semi-explicit solutions of mean-field-type games beyond LQ and under Gauss-Volterra processes.

Structure

The rest of the article is structured as follows. Section 2 presents semi-explicit solutions to some non-linear non-quadratic stochastic differential games. In Section 3 we formulate and solve various mean-field-type games with non-quadratic quantity-of-interest and provide semi-explicit solutions using a direct method. Section 4 presents semi-explicit solutions to some non-quadratic mean-field-type games driven by Gauss-Volterra processes. Numerical examples are presented in Section 5. The last section summarizes the work.

| Notation | Description |

|---|---|

| Brownian motion | |

| common Brownian motion | |

| Common Gauss-Volterra process | |

| Gauss-Volterra process | |

| set of jump sizes | |

| Radon measure over | |

| compensated jump process | |

| common compensated jump process | |

| state | |

| trend | |

| delayed state | |

| conditional state | |

| regime switching process | |

| set of decision-makers | |

| control action of decision-maker | |

| conditional control action of |

Preliminary

We introduce the following notations (see Table 2). Let be a fixed time horizon and be a given filtered probability space. The filtration is the natural filtration of the union of the family augmented by null sets of In practice, is used to capture smaller disturbance, is used for larger jumps of the system, is used for Gauss-Volterra processes (including sub- or super diffusion). Let is the set of measurable functions such that . is the set of -adapted -valued processes such that The stochastic quantity denotes the conditional expectation of the random variable with respect to the filtration Note that is a random process. Below, by abuse of notation we use for the values inside the jump processes or the regime-switching process . The set of decision-makers is denoted by An admissible control strategy of the decision-maker is an -adapted. We denote the set of all admissible controls by : Decision-maker chooses a control strategy to optimize its performance functional. The information structure of the problem under perfect state observation and under common noise observation

1.3 Conditional dynamics of mean-field type

Consider the following state dynamics of conditional McKean-Vlasov type with time delays, trend, diffusion, jump, regime switching, Gauss-Volterra and common noises.

| (1) |

where

-

•

is the set of decision-makers.

-

•

is the basic state at time of the decision-maker

-

•

represents a time delay,

-

•

is a dimensional delayed state vector,

-

•

is the integral state vector of the recent past state over The trend of the state of decision-maker is its latest moving averages. represents the trend of the state of . The process is an adapted locally bounded process, is a positive and finite measure on .

-

•

is the distribution states of all the other decision-makers,

-

•

the distribution of actions of all other decision-makers,

-

•

is a initial deterministic function of state of defined on

-

•

be a Brownian motion on with suitable dimension. be a Brownian motion observed by all decision-makers.

-

•

be a Gauss-Volterra process on with suitable dimension and with integrable kernel be a Gauss-Volterra process observed by all decision-makers

-

•

be a jump process with suitable dimension on with compensated jump , is a Radon measure over is a common jump process observed by all decision-makers.

-

•

is a regime switching process defined over the finite set with switching rate satisfying and We use to denote the indicator function on the condition

-

•

is the control strategy profile of all decision-makers. An admissible control strategy of the decision-maker is an -adapted process.

-

•

The processes , are defined in a given filtered probability space The processes are common noises assumed to be observable by all decision-makers. All the processes are assumed to be mutually independent.

-

•

The coefficient functionals are of compatible dimensions with

-

•

The quantity denotes the conditional expectation of the random variable with respect to the filtration Note that is a random process. We take By abuse of notation we use for the values inside the jump processes or the regime-switching process .

Let be a twice continuously differentiable function in and continuously differentiable in time for each regime Using [34] and [33, Theorem 4.1], the stochastic integration formula, which is an extended Itô’s formula, yields

| (2) |

Notice that (2) applies to a one-dimensional state as well as to a vector, matrix, tensor, lattice or another object in a Hilbert space. For vectors in an Euclidean space, the inner product is for matrices, where is the transpose of

1.4 Direct Method

Consider decision-makers under perfect state observation and common noise observation Given cost functionals associated with (1), we use (2) in the direct method described as follows. The direct method consists of five elementary steps (see Figure 3).

[bubble diagram] Direct Method, 1) MFTG

Problem, 2) Guess

Functional, 3) Stochastic

Integration

, 4) Terms

Completion, 5) Process

Identification

-

•

The first step starts by setting the mean-field terms of the problem.

-

•

The second step consists of the identification of a partial guess functional where the coefficient functionals are random and regime switching dependent. For each decision-maker , one needs to identify a guess functional

-

•

In the third step we compute the difference using the stochastic integration formula (2).

-

•

In the fourth step, we use completion of terms in one-shot optimization for both control actions and conditional mean-field of the control actions of all decision-makers. Terms completion make by matching coefficients. The latter inequality becomes equality iff the optimal control strategies are used.

-

•

The fifth and last step uses an algebraic basis of linearly independent processes to identify the coefficients. The identification leads to a (possibly stochastic) differential system of equations, providing a semi-explicit representation of the solution. The matched coefficients provide simpler differential systems that are uncoupled with the state.

2 Some Solvable Mean-Field-Free Games

We start with mean-field-free settings where logarithm, logarithm square, Legendre-Fenchel duality, and power payoffs are presented. The cost functions are not necessarily quadratic and the state dynamics is not necessarily linear.

2.1 Logarithmic Scale

Consider a set of decision makers interacting in the following non-linear non-quadratic mean-field-free game:

| (3) |

and with a given initial condition is an integer, and and

Proposition 1

Assume that The non-linear non-quadratic mean-field-free Nash equilibrium and the corresponding equilibrium cost are given by:

where and satisfies the following differential equations:

| (4) |

where , and .

.

Proof. Consider the following guess functional:

By applying Itô’s formula for jump-diffusion-regime switching processes, the gap between the cost and the guess functional can be computed and it is given by

| (5) |

Noting that

with equality iff the announced result follows.

Notice that the differential system (4) has a unique solution: the system in is linear and the system in is obtained by integration. is well-defined because the state stays positive in almost surely if one starts at

Remark 1

For the system reduces to the following ordinary differential equations:

| (6) |

2.2 Logarithm square

Consider the following non-linear non-quadratic mean-field-free game:

| (7) |

Proposition 2

Assume that and The non-linear non-quadratic mean-field-free Nash equilibrium and corresponding optimal cost are given by:

where satisfies the following differential equation:

Proof. Consider the following guess functional:

Applying the Itô’s formula yields

Thus, the gap is given by

By performing square completion one obtains

then,

Finally, the announced result is obtained by minimizing the terms.

2.3 Legendre-Fenchel

We consider a convex running loss functions

| (8) |

where and Recall that the Legendre-Fenchel transform of is given by

Proposition 3

Assume that are positive. Then, the game problem (8) has a solution:

| (9) |

with

| (10) |

where

| (11) |

These conditions are fulfilled by choosing for example

Proof Step 1: we observe that the structure of the problem is mainly driven by the evolution of the function

Step 2: Inspired the nature of the problem, we propose a guess functional in the form of with deterministic coefficients Let

Step 3: We apply stochastic integration formula for diffusion-regime switching to obtain the difference between the cost and the guess functional as

| (12) |

Step 4: Observing that

with equality iff the one-shot optimization provides

Step 5: By identification of processes, the announced result follows. This completes the proof.

2.4 Geometric Gauss-Volterra Game

The Gauss-Volterra processes are singular integrals of a standard Brownian motion and include (i) fractional Brownian motions, (ii) Liouville fractional Brownian motions, and (iii) multi-fractional Brownian motions. The difficulty of finding semi-explicit solution is significantly increased if the noise process and thereby the state process is driven by non-Markov processes or non-martingales. Let be a Gauss-Volterra process with zero mean and covariance

The kernel is assumed to have causality, continuity and integrability properties as in [27]. The variance of the process is given by

Consider the following geometric Gauss-Volterra game with unobserved processes which are assumed to be independent.

| (19) |

where and , , , , , and are real valued and regime-switching dependent functions with and

Proposition 4

Assume that The mean-field-free equilibrium for the Geometric Gauss-Volterra Game in (19) is given by

where satisfies the following differential equation:

| (20) |

Proof. This proof is developed following a direct method.

Step 1: Observe that the problem is a mean-field free problem driven by .

Step 2: Based on the structure of the problem we propose the following guess functional:

Step 3: We apply stochastic integration formula for jump-diffusion-regime-switching Gauss-Volterra and common noises to compute the difference between the costs and the guess functionals, i.e.,

Step 4: we perform terms completion:

Step 5: We perform process identification after having replaced back the optimal control inputs in the gap , i.e.,

Finally, the announced result is obtained by minimizing terms, which completes the proof.

Notice that under the conditions: the differential system (20) has a positive solution.

When are noises observed by all decision-makers (observed common noises), the ordinary differential system in becomes a stochastic differential system driven by the union of events with

| (21) |

with the terminal condition being -measurable random coefficient.

3 Some Solvable Mean-Field-Type Games

3.1 Control-dependent switching MFTG

In most continuous time MFTG models with regime switching considered in the literature it is assumed that the switching rate is control-independent. In this subsection, we provide an example with control-dependent switching rate in which the MFTG problem can be solved semi-explicitly.

| (22) |

where for and

Proposition 5

Assume that The equilibrium strategy is

| (23) |

and the equilibrium cost is which satisfies the following ordinary differential system:

| (24) |

Proof.

Step 1: We observe that the structure of the problem does not have a drift and is driven by regime switching.

Step 2: Based on step 1, we propose guess in the following form:

Step 3: we use the stochastic integration formula for regime-switching to compute the difference between the cost and the guess functional as:

| (25) |

Step 4: Assuming that and the terms completion lead to a one-shot optimization of a strictly convex and coercive function.

Step 5: the minimization and the identification of the processes provides the announced result.

3.2 Quadratic-Quadratic MFTG

This example examines a class of Quadratic-Quadratic Mean-Field-Type Game (QQ-MFTG) problem. The state is non-linear in A semi-explicit solution is derived.

| (26) |

where the coefficients are regime-switching dependent with switching rate matrix

Proposition 6

Assume that The QQ-MFTG problem (26) has unique solution and it is given by

| (27) |

Note that the semi-explicit solution is in fact an explicit solution. Let , and , then is explicitly given by

in particular .

Proof. Let us consider the following guess functional: . Then,

Itô’s formula yields

| (28) |

Thus, the difference is given by

| (29) |

Performing square completion yields

| (30) |

| (31) |

Minimizing terms it yields

completing the proof.

Remark 2

Notice that using the result presented in Proposition 6, the following Quadratic-Exponential-Quadratic Mean-Field-Type Game (QEQ-MFTG) problem:

| (32) |

can be solved explicitly.

3.3 Quadratic State and Power Utility

This subsection examines a class of mean-field-type games with power payoffs and a non-linear state. The model is inspired from the modern portfolio optimization under shared asset platform by several decision-makers. The state is the total amount of money. Decision-maker can decide to consume certain amount and re-allocate the remaining between less-risky assets and more risky assets The coefficients depend on time and on the switching regime which takes values in The set is non-empty and finite. We have modified the model to include mean-field terms, a function of the expected value of the state and a function of the expected value of the control action.

| (33) |

where the coefficients are regime-switching dependent, and The coefficients are positive. The state dynamics (33) is not linear in

Following the same method as in the problem (33), a semi-explicit solution can be derived.

Note that a similar method can be used to derive semi-explicit solution to the following game problem in which decision-makers minimize with

| (34) |

This can be easily extended to include multi-type power utilities in the following form:

| (35) |

In this case, the guess functional will be

with an ordinary differential system for and

3.4 Non-Linear State and Log-Utility

We consider the following logarithmic Cobb-Douglas utility.

| (36) |

where the coefficients are regime-switching dependent.

Note that the state dynamics (36) is not linear in

Following the same method as above, the problem (36) can be solved explicitly.

3.5 Cotangent Drift

This subsection we examine mean-field-type games with cotangent drift. This class of games is inspired from [11, 12, 13, 14, 15, 16, 17, 18, 19, 20]. We have modified the model to include mean-field terms. Using trigonometric relationships a semi-explicit equilibrium solution is derived.

| (37) |

where the coefficients are regime-switching dependent and

Proposition 7

Assume that The mean-field-type game problem with cotangent drift (37) has a unique equilibrium solution which is given by

| (38) |

whenever the following system

| (39) |

has a unique solution with positive which do not blow up within

Proof:

We prove the statement using a direct method. Step 1: We observe that

the mean-field-type problem is driven by functionals of and which are conditionally orthogonal processes.

Step 2: Given the structure of the problem, we propose the following guess functional:

be a guess functional.

Step 3: we apply Brownian with regime switching to obtain the difference between the cost functional and the guess functional as:

| (40) |

Step 4: Noting the terms completion leads to a strictly concave one-shot optimization with coercive function whenever

Step 5: By identification of processes one obtains the announced result. This completes the proof.

The mean-field term solves

| (41) |

which has a unique solution for

3.6 Hyperbolic coTangent Drift

Problem (37) can be modified to handle the hyperbolic cotangent drift case as specified below. The functions are replaced by respectively.

| (42) |

where the coefficients are regime-switching dependent and

Proposition 8

The equilibrium strategies and the equilibrium costs are given by

| (43) |

whenever the following system:

| (44) |

has unique solution with positive which do not blow up within

The system in (44) shares some similarities with the system in (39) of Problem (37). However, these two systems are different. In particular, the sign of the terms and have changed.

Proof.

We prove the statement on the hyperbolic game using a direct method. Let

be a guess functional combining hyperbolic functions.

| (45) |

By identification one obtains the announced result. This completes the proof.

The mean-field term solves

| (46) |

which has a unique global solution within

3.7 A Delayed and Trend-based MFTG

We present a cooperative MFTG with basic state dynamics , regime switching a trend on the time window the delayed state This class of examples plays an important role in real-world applications as the effects of actions are not instantaneous in general [28, 29, 30, 31]. It may take a certain time delay. This leads to delayed and trend-based stochastic differential equations of mean-field type.

| (47) |

where denotes the variance of the random variable and is the conditional expectation with respect to the common noises

Lemma 1

The conditional expected trend satisfies the following stochastic differential equation:

Proof:

Taking the conditional expected values one obtains

This completes the proof.

Proposition 9

The equilibrium strategies and the equilibrium payoff of the delayed MFTG (47) are given by

| (48) |

whenever the following system:

| (49) |

has a unique solution

Note that the system in has a positive solution if With single regime the equation yields

| (50) |

This is completely solvable with an explicit solution given by

where

Proof:

Let be a guess functional.

| (51) |

with the following careful matching The joint optimization over together with the mean-field terms gives the announced result provided that

3.8 Mean-Field of MFTG

This subsection we examine a class of mean-field of mean-field-type games.

In view of the delayed mean-field-type game (47), we have modified to be where is the conditional total consumption of the large population. Then, is obtained as

where is the conditional distribution of all players’ states and trends in the large population under which reduces to the fixed-point problem

Now consider the following modified Cournot-Ross game with producers and a large population of potential consumers. The mean-field-type version of the game under common noise is analyzed in [21].

| (52) |

Let be the demand generated by a large population of consumers. Given a demand each macro-player has a certain utility of mean-field type. The payoff function in the Cournot game is modified to be and some extra mean-field dependent terms.

By means of a direct method one can fully characterize the mean-field equilibrium of (52). It is given by following set of equations:

| (53) |

where solve a system of ordinary differential equations.

4 MFTG beyond Brownian motions and Poisson

In this section class of mean-field-type games with a state dependent Gauss-Volterra noise is formulated and solved with a polynomial and mean-field dependent payoff for an arbitrary number of players and a finite time horizon. The control strategies are linear state and mean-field feedbacks. A mean-field-type Nash equilibrium is verified for the game and the optimal strategies are obtained using a direct method that does not require solving nonlinear partial integro-differential equations or forward-backward stochastic differential equations. The example below is inspired from [22, 23, 24, 25, 26, 27]. We add mean-field terms to these previous works. This will allow us to solve variance or higher moment reduction problems.

4.1 Noncooperative MFTG under Gauss-Volterra processes

This section examines a class of noncooperative mean-field-type games with non-quadratic cost and state driven by Gauss-Volterra processes.

| (54) |

where are natural numbers, the coefficients are time and switching dependent,

Remark 3

The cost functional is clearly non-quadratic for or For the equilibrium of the variance reduction game (54) under Gauss-Volterra processes is obtained.

Proposition 10

Assume and The mean-field Nash equilibrium of the mean-field type game (54) under Gauss-Volterra process is given by

| (55) |

whenever the following system of ordinary differential equations admit a positive solution which does not blowup within

| (56) |

Proof:

Consider the guess functional

| (57) |

We complete the following term:

| (58) |

A similar completion is done for the terms in Thus,

| (59) |

Noting for one has:

| (60) |

with equalities in (60) iff

By identification, one obtains the announced result.

The derived system of equations (56) are inhomogeneous differential system where it is known that existence and uniqueness, nonexistence or nonuniqueness may occur.

Existence

Some results on sufficient conditions for the existence of trajectories satisfying the associated set of non-linear differential equations (56) are outlined. Below we present Carathéodory conditions for existence of a solution.

Here, the non-linear differential system (56) can be written as

| (61) |

Assume that

-

•

For each fixed time is continuous in

-

•

For each fixed is measurable in

-

•

Given a nonempty compact and interval there is an integrable positive function on the time interval such that for all

Uniqueness

It is a well-known result that not every non-linear differential system has a unique solution. Therefore, the uniqueness issue is dealt with in a separate result. We provide two sufficient conditions for having at most one solution:

-

•

If is continuously differentiable in and on then there is at most one solution on

-

•

If on then there is at most one solution on

It is important the notice that the function is not necessarily globally Lipschitz in For example, for is not necessarily globally Lipschitz. Therefore we need estimates of We rely on the original dynamic optimization problem to derive lower and upper bounds on Since by assumption, lower bound for is zero. This can also be obtained directly from the problem formulation as the cost is positive. By summing up (56) over an upper bound is obtained as is bounded subject to integrability condition of the coefficients.

Note, however, that the stationary system may have multiple solutions, depending on the parameters.

Admissibility of the coefficient solution

As in the Carathéodory existence result depends on the maximal interval in which the solution is defined may depend on Thus, we need to examine the singularity of in (56). In order for the control strategies to be admissible, we seek sufficient conditions for non-blow-up (no escape) within If and all coefficients continuous, then there is no escape within If in addition the coefficient functions and are all integrable within , then there is no escape of within the entire as the estimates of is finite in

Similar reasoning works for when and the coefficient functions are integrable within

At equilibrium, the mean-field term in Proposition 10 solves

| (62) |

which admits a unique solution within subject to the integrability of the regime switching dependent coefficient over

4.2 Fully Cooperative MFTG under Gauss-Volterra Noise

In this subsection we choose and assume that the decision-makers are fully cooperative. They jointly decide and solve the following problem:

| (63) |

Proposition 11

The global optimum of the fully cooperative mean-field type game (63) under Gauss-Volterra process is given by

| (64) |

whenever the following system of ordinary differential equations admit a positive solution which does not blowup within

| (65) |

Proof: The proof follows similar steps as in Proposition 10.

Remark 4

A sufficient condition for existence and uniqueness of the global optimum of mean-field type is obtained for and all coefficients continuous. Then there is no escape within If in addition the coefficient functions and are all integrable within , then is no escape of within the entire interval Similar reasoning works for when and the coefficient functions are integrable within

At the global optimum, the mean-field term in Proposition 11 solves

| (66) |

which admits a unique solution within subject to the integrability of the regime switching dependent coefficient over

Remark 5

Notice that the differential equation

| (67) |

has a unique solution within Moreover, the unique solution is positive.

4.3 Adversarial Mean-Field-Type Game under Gauss-Volterra Noise

In this subsection we choose and assume that the decision-makers are divided into two teams and The decision-makers in team minimize the functional over The decision-makers in team maximize over This leads to a minmax game problem:

| (68) |

A mean-field-type risk-neutral saddle point is a strategy profile of the team of defenders and of the team of attackers such that

Proposition 12

Assume and Then, the minmax solution of the adversarial mean-field type game (68) under Gauss-Volterra process is given by

| (69) |

whenever the following system of ordinary differential equations admit a positive solution which does not blowup within the horizon

| (70) |

In this case, the minmax solution is also a maxmin solution, hence is a saddle point. Thus, the adversarial mean-field-type game has a value

The proof follows similar steps as above by exploiting the strict convex-concave and coercivity properties of the cost functional.

Remark 6

A sufficient condition for existence and uniqueness of the minmax point of mean-field type is obtained:

and the coefficient functions and are all integrable within , then is no escape of within the entire interval

Similar reasoning works for when

and the coefficient functions are integrable within

5 Numerical Examples

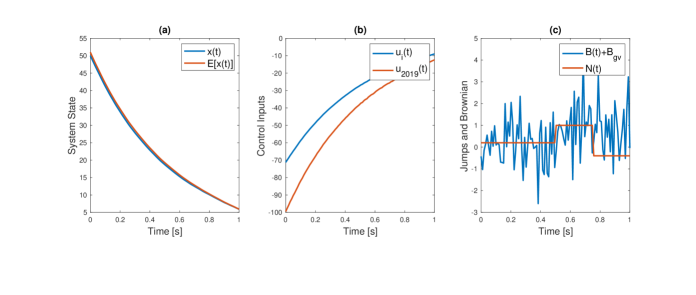

In this section, we present some numerical illustrations of Problem (54) by choosing Gauss-Volterra process with the following kernel

| (71) |

and is a normalizing constant, where is the gamma function

The Gauss-Volterra process with kernel is a fractional Brownian motion with the Hurst parameter The parameters of the numerical setting are displayed in Table 4.

| Numerical setting | Value |

|---|---|

| Kernel | |

| Switching | |

| if | |

| if | |

| if | |

| if | |

| if | |

| if | |

It is important to notice that under this setting the problem (54) is not Markov and the cost is not quadratic. From (10) we know that the mean-field Nash equilibrium of the mean-field type game (54) under Gauss-Volterra process is given by

| (72) |

Figure 5 plots (a) a sample path of the optimal state trajectory starting from (b) the optimal strategies of all decision-makers and 2019, and (c) sample noises. As expected the state is moving toward zero when the optimal strategies are employed.

6 Conclusion

In this article, we have shown that a mean-field equilibrium can be determined in a semi-explicit way for a broader class of non-linear, non-quadratic game problems with non-linearly distribution-dependent payoffs where the state dynamics is driven by conditional expected values of states, controls, Brownian motions, Gauss-Volterra processes, jump and regime-switching. The method does not require the sophisticated non-elementary extension to backward-forward systems. It does not need PIDEs. It does not need SMPs. It is basic and applies the stochastic integration formula. The use of this simple method may open the accessibility of the tool to a broader audience including beginners and engineers to this emerging field of mean-field-type game theory. Another direct application of the results presented this article is that the explicit solution provides a reference trajectory to the numerical schemes of the corresponding master system beyond the LQ setting.

Acknowledgements

Authors gratefully acknowledge support from U.S. Air Force Office of Scientific Research under grants number FA9550-17-1-0259 , FA9550-12-1-0384 and NSF grant DMS 1411412.

References

- [1] A. K. Cissé, H. Tembine: Cooperative Mean-Field Type Games, IFAC Proceedings Volumes Vol. 47, Issue 3, 2014, Pages 8995-9000.

- [2] H. Tembine: Risk-sensitive mean-field-type games with Lp-norm drifts. Automatica 59: 224-237 (2015)

- [3] H. Tembine: Uncertainty quantification in mean-field-type teams and games. CDC 2015: 4418-4423

- [4] B. Djehiche, A. Tcheukam, H. Tembine: Mean-Field-Type Games in Engineering, AIMS Electronics and Electrical Engineering, 2017, 1(1): 18-73

- [5] H. Tembine: Mean-field-type games: AIMS Mathematics, 2017, 2(4): 706-735.

- [6] T.E. Duncan ; H. Tembine : Linear-Quadratic Mean-Field-Type Games: A Direct Method. Games 2018, 9, 7.

- [7] J. Barreiro-Gomez , T. E. Duncan and H. Tembine : Matrix-Valued Mean-Field-Type Games: Linear-Quadratic case with Common Noise, Preprint 2018.

- [8] A. Aurell: Mean-Field Type Games between Two Players Driven by Backward Stochastic Differential Equations Special Issue Mean-Field-Type Game Theory, Games Journal, 9(4), 88; 2018

- [9] S. Eddine Choutri and H.Tembine: A Stochastic Maximum Principle for Markov Chains of Mean-Field Type Special Issue Mean-Field-Type Game Theory, Games Journal, 2018, 9(4), 84;

- [10] S. Eddine Choutri, B. Djehiche, H. Tembine: Optimal Control and Zero-Sum Games for Markov Chains of Mean-Field Type. Mathematical Control & Related Fields, accepted and to appear, 2019.

- [11] T. E. Duncan, Dynamic programming optimality criteria for stochastic systems in Riemannian manifolds, Appl. Math. Optim. 3 (1977), 191-208.

- [12] T. E. Duncan, Stochastic systems in Riemannian manifolds, J. Optim. Theory Appl. 27 (1979), 399-426.

- [13] T. E. Duncan, A solvable stochastic control problem in hyerbolic three space, Systems Control Lett. 8 (1987), 435-439.

- [14] T. E. Duncan, A solvable stochastic control problem in spheres, in: Contemp. Math. 73, Amer. Math. Soc., 1988, 49-54

- [15] T. E. Duncan, Some solvable stochastic control problems in compact symmetric spaces of rank one, in: Contemp. Math. 97 Amer. Math. Soc., 1989, 79-96.

- [16] T. E. Duncan, Some solvable stochastic control problems in noncompact symmetric spaces of rank one, Stochastics and Stochastic Rep. 35 (1991), 129-142.

- [17] T. E. Duncan, A solvable stochastic control problem in the hyperbolic plane, J. Math. Sys. Estim. Control 2 (1992), 445-452.

- [18] T. E. Duncan, A solvable stochastic control problem in real hyperbolic three space II, Ulam Quart. 1 (1992), 13-18.

- [19] T. E. Duncan and H. Upmeier, Stochastic control problems in symmetric cones and spherical functions, in: Diffusion Processes and Related Problems in Analysis I, Birkhauser, 1990, 263-283.

- [20] T.E Duncan: Solvable optimal control of brownian motion in symmetric spaces and spherical polynomials, Geometry in nonlinear control and differential inclusions, Banach Center Publications, vol 32 Institute of Mathematics, Polish Academy of sciences, Warszawa,1995

- [21] B. Djehiche, J. Barreiro-Gomez, and H. Tembine. Electricity Price Dynamics in the Smart Grid: A Mean-Field-Type Game Perspective. 23rd International Symposium on Mathematical Theory of Networks and Systems (MTNS), 2018, Hong Kong, China, pp. 631-636.

- [22] P. Coupek, T. E. Duncan, B. Maslowski, and B. Pasik-Duncan, An infinite time horizon linear-quadratic control problem with a Rosenblatt process, Proc. 57th IEEE Conf. Decision and Control, Miami, Dec. 2018.

- [23] T. E. Duncan, Linear-quadratic stochastic differential games with general noise processes, Models and Methods in Economics and Management Science: Essays in Honor of Charles S. Tapiero, (eds. F. El Ouardighi and K. Kogan), Operations Research and Management Series, Springer Intern. Publishing, Switzerland, Vol. 198, 2014, 17-26.

- [24] T.E. Duncan and B. Pasik-Duncan, Linear-quadratic fractional Gaussian control, SIAM J. Control Optim., 51 (2013), 4604-4619.

- [25] T. E. Duncan and B. Pasik-Duncan, Explicit strategies for some linear and nonlinear stochastic differential games, J. Math. Engrg. Sci. Aerospace, 7 (2016), 83-92.

- [26] T.E. Duncan, B. Maslowski and B. Pasik-Duncan: Ergodic control of linear stochastic equations in a Hilbert space with fractional Brownian motion. Stochastic analysis, 91-102, Banach Center Publ., 105, Polish Acad. Sci. Inst. Math., Warsaw, 2015

- [27] T. E. Duncan, B. Maslowski and B. Pasik-Duncan, Linear stochastic differential equations driven by Gauss-Volterra processes and related linear-quadratic control problems, Appl. Math. Optim., 2018.

- [28] H. Tembine, E. Altman, R. El Azouzi, Y. Hayel: Bio-inspired delayed evolutionary game dynamics with networking applications. Telecommunication Systems 47(1-2): 137-152 (2011)

- [29] H. Tembine, E. Altman, R. El Azouzi, Y. Hayel: Evolutionary Games in Wireless Networks. IEEE Trans. Systems, Man, and Cybernetics, Part B 40(3): 634-646 (2010)

- [30] E. Altman, R. El Azouzi, Y. Hayel, H. Tembine: The evolution of transport protocols: An evolutionary game perspective. Computer Networks 53(10): 1751-1759 (2009)

- [31] H. Tembine, E. Altman, R. El Azouzi: Asymmetric delay in evolutionary games. Valuetools, 2007: 36

- [32] Coddington, Earl A.; Levinson, Norman (1955), Theory of Ordinary Differential Equations, New York: McGraw-Hill.

- [33] Zhang X, Elliott RJ, Siu TK (2012) A stochastic maximum principle for a Markov regime-switching jump-diffusion model and its application to finance. SIAM J Control Optim 50:964-990

- [34] P. E. Protter, Stochastic Integration and Differential Equations, second ed., Springer-Verlag, New York, 2005.

Julian Barreiro-Gomez received his B.S. degree (cum laude) in Electronics Engineering from Universidad Santo Tomas (USTA), Bogotá, Colombia, in 2011. He received the MSc. degree in Electrical Engineering and the Ph.D. degree in Engineering from Universidad de Los Andes (UAndes), Bogotá, Colombia, in 2013 and 2017, respectively. He received the Ph.D. degree (cum laude) in Automatic, Robotics and Computer Vision from the Technical University of Catalonia, Barcelona, Spain, in 2017, and the Best Ph.D. Thesis in Control Engineering 2017 award from the Spanish National Committee of Automatic Control and Springer. He is currently a Post-Doctoral Associate in the Learning & Game Theory Laboratory at New York University Abu Dhabi. His main research interests are evolutionary game dynamics, mean-field-type games, and distributed control and optimization.

Tyrone E. Duncan received the B.E.E. degree from Rensselaer Polytechnic Institute, Troy, NY, in 1963 and the M.S. and Ph.D. degrees from Stanford University, Stanford, CA, in 1964 and 1967, respectively. He has held regular positions with the University of Michigan, Ann Arbor (1967-1971), the State University of New York, Stony Brook (1971-1974), and the University of Kansas, Lawrence (1974- present), where he is Professor of Mathematics. He has held visiting positions with the University of California, Berkeley (1969-1970), the University of Bonn, Germany (1978-1979), and Harvard University, Cambridge, MA (1979-1980), and shorter visiting positions at numerous other institutions. Dr. Duncan is a member of the editorial boards of Communications on Stochastic Analysis, and Risk and Decision Analysis and was on the editorial board of SIAM Journal on Control and Optimization (1994-2007) as an Associate Editor and a Corresponding Editor. He is a member of AMS, MAA, and SIAM.

Bozenna Pasik-Duncan received M.S. degree in mathematics from University of Warsaw, and Ph.D. and D.Sc. (Habilitation) degrees from the Warsaw School of Economics, Poland. She is Professor of Mathematics; Courtesy Professor of EECS and AE; Investigator at ITTC; Affiliate Faculty at Center of Computational Biology, and Chancellors Club Teaching Professor at the University of Kansas (KU). She is strong advocate for STEM education and for women in STEM. She is IEEE WIE Chair, founder of CSS Women in Control, founder and faculty advisor of KU Student Chapters of AWM and SIAM, founder and coordinator of KU and CSS Outreach Programs. She has served in many capacities in several societies. Her current service includes Chair of IEEE WIE, member of IEEE CSS and IEEE SSIT Board of Governors, Deputy Chair of IEEE CSS TC on Control Education, Chair of AACC Education Committee, member of IFAC TB, and Award Committees of AWM and MAA. She is General Chair of IFAC ACE 2019 Symposium and member of Organizing Committee of SIAM CT19. She is Associate Editor of several Journals. Her research interests are primarily in stochastic systems and adaptive control and its applications to science and engineering, and in STEM education. She is a recipient of many awards that include IREX Fellowship, NSF Career Advancement Award, Louise Hay Award, Polish Ministry of Higher Education Award, H.O.P.E., Kemper Fellowship, IEEE EAB Meritorious Achievement Award, Service to Kansas and IFAC Outstanding Service Awards. She is Life Fellow of IEEE and Fellow of IFAC, a recipient of the IEEE Third Millennium Medal and IEEE CSS Distinguished Member Award. She is inducted to the KU Women’s Hall of Fame.

Hamidou Tembine received the M.S. degree in applied mathematics from Ecole Polytechnique, Palaiseau, France, in 2006 and the Ph.D. degree in computer science from the University of Avignon, France, in 2009. He holds over 150 scientific publications including magazines, letters, journals, and conferences. He is the author of the book on Distributed Strategic Learning for Engineers (CRC Press, Taylor & Francis 2012), and coauthor of the book Game Theory and Learning in Wireless Networks (Elsevier Academic Press).