Weak comonotonicity

Ruodu Wang

Department of Statistics and Actuarial Science, University of Waterloo, Waterloo, Ontario, N2L 5A7, Canada. E-mail: wang@uwaterloo.ca

Ričardas Zitikis

School of Mathematical and Statistical Sciences, University of Western Ontario, London, Ontario N6A 5B7, Canada. E-mail: rzitikis@uwo.ca

This version: July 2019

Abstract. The classical notion of comonotonicity has played a pivotal role when solving diverse problems in economics, finance, and insurance. In various practical problems, however, this notion of extreme positive dependence structure is overly restrictive and sometimes unrealistic. In the present paper, we put forward a notion of weak comonotonicity, which contains the classical notion of comonotonicity as a special case, and gives rise to necessary and sufficient conditions for a number of optimization problems, such as those arising in portfolio diversification, risk aggregation, and premium calculation. In particular, we show that a combination of weak comonotonicity and weak antimonotonicity with respect to some choices of measures is sufficient for the maximization of Value-at-Risk aggregation, and weak comonotonicity is necessary and sufficient for the Expected Shortfall aggregation. Finally, with the help of weak comonotonicity acting as an intermediate notion of dependence between the extreme cases of no dependence and strong comonotonicity, we give a natural solution to a risk-sharing problem.

Key words and phrases: finance; comonotonicity; risk aggregation; conditional beta.

1 Introduction

Two functions are said to be comonotonic if the ups and downs of one function follows those of the other function. Hence, though geometric in nature, comonotonicity is also a kind of dependence notion between functions. It is not surprising, therefore, that comonotonicity has given rise to sufficient conditions when solving a variety of problems in economics, banking, and insurance, and in particular those that deal with portfolio diversification, risk aggregation, and premium calculation principles. Our search for necessary and sufficient conditions has revealed that a certain augmentation of the classical (and inherently point-wise) notion of comonotonicity with appropriately constructed measures achieves more advanced goals than those associated with sufficient conditions. As a by-product, the augmented notion of comonotonicity, which we call weak comonotonicity, provides a natural bridge between a host of concepts in the aforementioned areas of application, and also in statistics, including measures of association. In what follows, we methodically develop the notion of weak comonotonicity from first principles, establish its various properties, and demonstrate manifold uses.

Rigorously speaking, two functions and are comonotonic whenever the property

| (1.1) |

holds for all . This notion of comonotonicity (Schmeidler, 1986) has played a pivotal role in sorting out numerous applications and developing new theories (e.g., Yaari, 1987; Denneberg, 1994). Since then, these advances have been in the mainstream of quantitative finance and economics literature (e.g., Dhaene et al., 2002a, b; Föllmer and Schied, 2016). In this paper, we shall focus on dependence concepts between uni-dimensional functions (and random variables); for multivariate extensions and further references on comonotonicity, we refer to Puccetti and Scarsini (2010), Carlier et al. (2012), Ekland et al. (2012), and Rüschendorf (2013). Note that if non-negativity in property (1.1) is replaced by non-positivity, the functions and are said to be antimonotonic.

Comonotonicity of (Borel) functions and is a sufficient condition for non-negativity of the covariance , where is a random variable such that and have finite second moments. This is immediately seen from the equations

| (1.2) |

where is an independent copy of , and denotes the cumulative distribution function (cdf) of . The problem of determining the sign of covariances such as the one above has been of much interest in economics, insurance, banking, reliability engineering, and statistics. Several offshoots have arisen from this type of research, including quadrant dependence (Lehmann, 1966), measures of association (Esary et al., 1967), monotonic (Kimeldorf and Sampson, 1978) and supremum (Gebelein, 1941) correlation coefficients. The following example illustrates the need for such results.

Example 1.1.

Let be the severity of a risk, which could, for example, be a profit-and-loss variable. Let be the cost associated with the risk , and let be the so-called (knowledge-based) weighted cdf of the original random variable (e.g., Rao, 1997, and references therein). That is, is defined by the differential equation

| (1.3) |

where is a non-negative function such that . The role of the function is to modify the probabilities of the original random variable . For example, in insurance, it is usually designed to lower the left-hand tail of the pdf of and to lift its right-hand tail, thus making large insurance risks/losses more noticeable and the premiums loaded; we refer to, e.g., Deprez and Gerber (1985) for the Esscher principle of insurance premium calculation, where for some constant . Under the weighted cdf , the average cost is

which is not smaller than the average cost under the true cdf if and only if the covariance is non-negative. Several natural questions arise in this context: Under what conditions on the cost function and the probability weighting function is the covariance non-negative? Should the functions really be comonotonic, as our earlier arguments would suggest? It is important to note at this point that practical and theoretical considerations may or may not support the latter assumption, due to the complexity of economic agents’ behaviour (e.g., Markowitz, 1952; Pennings and Smidts, 2003; Gillen and Markowitz, 2009).

We have organized the rest of the paper as follows. In Section 2, we define, illustrate, and discuss the notion of weak comonotonicity, first for Borel functions and then for random variables (i.e., generic measurable functions). In Section 3 we elucidate the role of weak comonotonicity in risk aggregation. In particular, we show that a combination of weak comonotonicity and weak antimonotonicity with respect to some sets of measures is sufficient for the maximization of Value-at-Risk (VaR) aggregation, and weak comonotonicity is necessary and sufficient for the Expected Shortfall (ES) aggregation. Both the VaR and the ES aggregation problems have been popular in the recent risk management literature (e.g., Rüschendorf, 2013; McNeil et al., 2015; Embrechts et al., 2015). In Section 4, we explore some properties of weak comonotonicity and its relation to other dependence structures and measures of association. As most of this paper deals with weak comonotonicity with respect to product measures, in Section 5 we illuminate the special role of these measures within the general context of joint measures. With the help of the developed theory, in Section 6 we present a detailed solution to a risk-sharing problem by invoking a weak comonotonicity constraint, whose naturalness becomes clear upon noticing that the assumption of arbitrary dependence among admissible allocations might sometimes be too weak, and the assumption of strong comonotonicity might be too strong, and so an intermediate dependence assumption based on weak comonotonicity arises most naturally. Section 7 concludes the paper with a brief overview of main contributions.

2 Weak comonotonicity

Our efforts to tackle problems like those in the previous section, and in particular those related to risk aggregation (Section 3), have naturally led us to a notion of weak comonotonicity (to be defined in a moment) which naturally bridges the arguments around quantities in (1.1) and (1.2) in the following way: First, note the equation

| (2.1) |

where and are point masses at the points and , respectively. It now becomes obvious that by choosing various product measures instead of , we can seamlessly move from classical comonotonicity (1.1) to covariance non-negativity (1.2). Formalizing this flexibility gives rise to a general definition of weak comonotonicity, which is the topic of Section 2.1.

2.1 Weak comonotonicity of Borel functions

In what follows, we use to denote the Borel measurable space, where is the Borel -algebra, and we also work with the measurable space , where .

Definition 2.1.

Let be any subset of product measures on . We say that two functions and are weakly comonotonic with respect to whenever

| (2.2) |

for every . In case is a singleton, we also say that and are weakly comonotonic with respect to if (2.2) holds.

We also speak of weak antimonotonicity if non-negativity in (2.2) is replaced by non-positivity. Property (2.2) gives rise to a whole spectrum of comonotonicity notions, at one end of which is the classical notion of comonotonicity (i.e., property (1.1)), which can be viewed as and being weakly comonotonic with respect to . In other words, the classical notion of comonotonicity can be thought of as the point-wise or strong comonotonicity. On the other hand, Definition 2.1 and equation (1.2) imply that the covariance is non-negative if and only if the functions and are weakly comonotonic with respect to , where is the cdf of . By choosing various product measures, we thus arrive at a large array of comonotonicity notions. The following example is designed to illustrate, and in particular enhance our intuitive understanding of, the notion of weak comonotonicity.

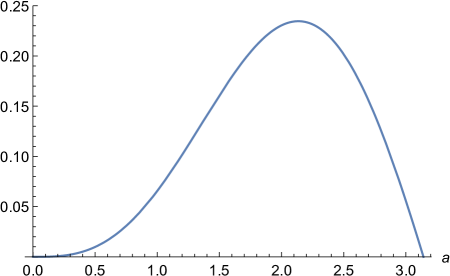

Example 2.1.

Let and . In the classical sense, the two functions are neither comonotonic nor antimonotonic on the interval , but they are antimonotonic on and comonotonic on . As to their weak comonotonicity, consider the integral

with respect to the following three uniform distributions , , and on the noted intervals, where in every case. We have

When , we depict as a function of in Figure 2.1.

It is non-negative for every , thus implying that the functions and , which are neither comonotonic nor antimonotonic on in the classical sense, are nevertheless weakly comonotonic with respect to . On the other hand, when , the function is non-positive for every , and thus and are weakly antimonotonic with respect to . Finally, under the distribution , the two functions are both weakly comonotonic and weakly antimonotonic. This concludes Example 2.1.

It is useful to reflect upon Example 2.1 from a general perspective, for which we employ Bayesian terminology. Namely, we first impose the (improper) uniform prior on the entire real line. Then we weight the prior using the indicator function , where can be any compact interval. This gives rise to the uniform distribution defined by the differential equation

| (2.3) |

(compare it with equation (1.3)). This uniform distribution, whose density (pdf) takes the form , can be thought of as a magnifying glass over the window : by sliding it over the domain of definition of functions, we explore weak comonotonicity of the functions, as we have done in Example 2.1.

2.2 Weak comonotonicity of random variables

Note that the moment we had shifted our focus from non-decreasing functions to comonotonic ones, we lost the need for having order relationship in the underlying measurable space. Hence, we can work with abstract measurable space , in which case -measurable functions like are called random variables, and this is the general framework within which we work next. Namely, and are said to be comonotonic whenever

for all . The definition is independent of any choice of measure.

Definition 2.2.

Let be any subset of probability product measures on . We say that two random variables and are weakly comonotonic with respect to whenever

| (2.4) |

for every .

Again, we also speak of weak antimonotonicity if non-negativity in (2.4) is replaced by non-positivity. This definition not only generalizes Definition 2.1 but also paves a path toward the notion of conditional correlation, and thus, in turn, toward conditional beta that has prominently featured in problems such as dynamic asset pricing and risk estimation with non-synchronous prices (Engle, 2016, see also references therein). The next example elucidates the connection.

Example 2.2.

Let be a probability space of financial scenarios , and let be, for example, risk severities of two financial instruments. Quite often, it is of interest to measure association between the two instruments over certain events of positive probabilities. In this case, the original probability is re-weighted

thus reducing property (2.4) via to

| (2.5) |

Property (2.5) can in turn be rewritten as , which can equivalently be interpreted as the non-negativity requirement on the conditional beta (Engle, 2016) over the events of interest, which could, for example, make up the -field of historical events (see, e.g., Box et al. (2015) for a time series context; and Pflug and Römisch (2007), Föllmer and Schied (2016) for risk measurement and management contexts).

Coming now back to Definition 2.2, we check that the following four statements are equivalent:

-

(i)

and are (strongly, or point-wise) comonotonic;

-

(ii)

and are weakly comonotonic with respect to every probability product measures on ;

-

(iii)

and are weakly comonotonic with respect to ;

-

(iv)

there exist non-decreasing functions and and a random variable such that and ; according to Denneberg’s Lemma (Denneberg, 1994, Proposition 4.5), we can set .

We are now ready to elucidate the fundamental role of weak comonotonicity in problems associated with risk aggregation.

3 Risk aggregation and weak comonotonicity

Two of the most popular classes of risk measures used in banking and insurance practice are the Value-at-Risk (VaR) and the Expected Shortfall (ES, also known as TVaR, CTE, CVaR, AVaR). We fix an atomless probability space . For a random variable , the VaR at level is defined as

and the ES at level is defined as

A classic problem in the field of risk management is risk aggregation with given marginal distributions (e.g., McNeil et al., 2015, Section 8.4). Let and be two integrable random variables. For , we say that maximizes the aggregation, if

and similarly for the ES aggregation, where “” stands for equality in distribution.

It is well-known (e.g., McNeil et al., 2015, Section 8.4.4) that the maximization of ES aggregation is achieved by (strong) comonotonicity, that is, maximizes the aggregation if they are strongly comonotonic. A similar statement holds for all convex-order consistent risk measures, or variability measures, such as the variance, the standard deviation, convex and coherent risk measures, and the Gini Shortfall (Furman et al., 2017), and this is because of the well-known fact (e.g., Puccetti and Wang, 2015) that comonotonicity maximizes convex order of the sum. Note that for a specific , (strong) comonotonicity is a sufficient condition for to maximize the aggregation, but it is not necessary.

Another well-known phenomenon (e.g., McNeil et al., 2015, Proposition 8.31), which is in sharp contrast to the above situation, is that the maximization of VaR aggregation is not achieved by comonotonicity. This is due to the fact that is generally not subadditive. The calculation of the worst-case VaR aggregation is technically very challenging and the corresponding dependence structure is quite complicated. For recent analytical and numerical results, we refer to Wang et al. (2013) and Embrechts et al. (2013, 2014, 2015). Fortunately, the case of admits an analytical solution, which is originally due to Makarov (1981) and Rüschendorf (1982).

To summarize, strong comonotonicity is sufficient but not necessary for the maximization of ES aggregation, and it is neither sufficient nor necessary for the maximization of VaR aggregation. This calls for weaker and alternative dependence notions compared to strong comonotonicity. We shall see later in Theorem 3.1 that the notion of weak comonotonicity serves this purpose very well, as it gives a sufficient condition for the maximum aggregation, as well as a necessary and sufficient condition for the maximum aggregation.

To prepare for Theorem 3.1, we need some notation and a lemma. For a random variable and for any , we write

Note that if is continuously distributed. In this case, is the event of probability on which takes its largest possible values. Further, let

where stands for the complement of a subset of , and let

In what follows, we treat -a.s. equal random variables as identical, and thus statements like “ and are weakly comonotonic with respect to ” should be interpreted as they hold for a representative pair of the random variables and .

Lemma 3.1.

Let and be two continuously distributed random variables, and let . The following three statements are equivalent:

-

(i)

and are weakly comonotonic with respect to ;

-

(ii)

and are weakly comonotonic with respect to ;

-

(iii)

a.s. with respect to .

Proof.

We only show (i)(iii) since (ii)(iii) holds by symmetry. First, we assume that statement (i) holds. For and , we have . By definition of weak comonotonicity, this implies . Therefore, takes its largest values on . Since , we have a.s. Next, we assume that statement (iii) holds. Then, for a.s. and , we have and . This gives the weak comonotonicity of and ; more precisely, of a representative version of . ∎

We are now ready to state our main result on the relationship between risk aggregation and weak comonotonicity.

Theorem 3.1.

Let and be two continuously distributed and integrable random variables, and let . We have the following two statements:

-

(i)

If and are weakly comonotonic with respect to , and and are weakly antimonotonic with respect to , then maximizes the aggregation;

-

(ii)

and are weakly comonotonic with respect to if and only if maximizes the aggregation.

Proof.

First, we prove statement (i). By Lemma 3.1, a.s. Also note that and are (strongly) antimonotonic on the set . Let , which is uniformly distributed on , and we know that and are strongly comonotonic. As a consequence, a.s., and the sets , and are a.s. equal. Because and are antimonotonic on the set , if takes value , then takes the value a.s., and hence a.s. on . Further, note that if , then a.s. and if , then a.s. As a consequence, by definition of the -quantile , is the smallest value (-a.s.) takes on the set , which is the smallest value of for . Therefore,

This gives the maximum value of the aggregation according to Makarov (1981, equation (2)) or McNeil et al. (2015, Proposition 8.31), thus concluding the proof of statement (i).

To prove statement (ii), we need some preliminaries. Namely, we use the dual representation of in the form

| (3.1) |

for any random variable , and attains the maximum in (3.1) if is continuously distributed (e.g., Embrechts and Wang, 2015, Lemma 3.1). Because of subadditivity of , we have

Hence, maximizes the aggregation if and only if . Note that always holds. Now we are able to establish the “if and only if” statement (ii).

- ()

-

()

Suppose that maximizes the aggregation. Then, using equation (3.1), we have, for some ,

Therefore, . Since is continuously distributed and takes its largest values on , and , we conclude that a.s. Similarly, we conclude that a.s. Using Lemma 3.1 again, we obtain that and are weakly comonotonic with respect to

This finishes the proof of Theorem 3.1. ∎

Note that the weak comonotonicity condition on in Theorem 3.1 is truly weaker than strong comonotonicity, as it does not specify the copula of and . As discussed by Embrechts et al. (2014, Section 3), the typical worst-case scenario of VaR aggregation is a combination of positive dependence and negative dependence in some non-rigorous sense. Theorem 3.1(i) answers precisely what these non-rigorous positive and negative dependence structures mean: weak comonotonicity with respect to and weak antimonotonicity with respect to . Furthermore, Theorem 3.1(ii) gives a necessary and sufficient condition for the dependence structure maximizing the aggregation.

As a direct consequence of Theorem 3.1, there exists a dependence structure that maximizes the and aggregations simultaneously, as specified in Theorem 3.1(i). Note that the weak comonotonicity of and with respect to can be interpreted as a positive dependence in which the large values of and appear simultaneously; but they are not perfectly aligned as in strong comonotonicity. It is straightforward to see, however, that this dependence structure, although necessary and sufficient for the aggregation, is not necessary for the aggregation. For instance, if is positive and is large enough, say , then it does not matter what value takes because it does not affect the calculation of .

Remark 3.1.

Theorem 3.1(ii) is formulated for a specific . If one likes to maximize aggregation for all or, equivalently, maximize the convex order of the sum, then strong comonotonicity is the only dependence structure (e.g., Cheung, 2010, Theorem 3). This, in particular, highlights the lack of practical attractiveness of the classical notion of comonotonicity, as it is unnecessarily too strong, at least from the perspective of aggregation. Indeed, practical considerations place emphasis on special values of , usually specified by regulators, and they are, for example, close to 1 in banking and insurance (e.g., Basel IV and Solvency II; see McNeil et al. (2015)). More generally, we can think of examples when we would be concerned with ’s in certain subinterval of , but not in the entire interval . This serves yet another justification for the introduction and explorations of the notion of weak comonotonicity.

Remark 3.2.

The VaR aggregation problem is equivalent to the problem of maximizing or minimizing for a given and given marginal distributions of and . Indeed, this is the problem originally studied by Makarov (1981) and Rüschendorf (1982). It has become well known since then that comonotonicity does not maximize or minimize the probability , and hence it is not the right notion to describe the corresponding dependence structures.

4 Some properties of weak comonotonicity

In this section we explore some properties of weak comonotonicity, and its relation to notions of dependence structures and measures of association.

4.1 Point-masses and comonotonicity

We have already noted that point masses reduce weak comonotonicity to strong comonotonicity, but the class

depends, naturally, on the functions and . In a sense, we can circumvent this dependence by introducing certain classes of point masses. Define

and

Note that is the largest set of product measures with respect to which and are weakly comonotonic. The set is never empty because . Finally, we note that for any two functions and , the inclusions and always hold.

Theorem 4.1.

We have the following two statements:

-

(i)

if and only if and are strongly comonotonic.

-

(ii)

if and only if and are strongly antimonotonic and injective on .

Proof.

Statement (i) is trivial. To prove statement (ii), we first note that if , then for any two which are not identical, we have . Thus, , and the desired injectivity and antimonotonicity follow. Next, assume injectivity and antimonotonicity. Then, for all that are not identical. For any product measure , if condition (2.2) holds, then must be supported in the points where either or , and hence . Since is a product measure, we know that it has to be of the form for . This concludes the proof of Theorem 4.1. ∎

We now turn our attention to random variables and . Similarly to , let

In other words, is the largest set of product measures with respect to which and are weakly comonotonic. It is a symmetric set with respect to and , that is, we have . The validity of this symmetry easily follows from the equation

| (4.1) |

It also follows from the latter equation that if , then condition (2.4) means that the correlation of and under the measure is non-negative. Finally, we note that is invariant under all increasing linear marginal transforms, that is, the equation holds for all and .

Theorem 4.2.

Let and . We have the following two statements:

-

(i)

if and only if and are strongly comonotonic.

-

(ii)

if and only if and are strongly antimonotonic and injective on .

4.2 Set-masses and independence

We now go back to the integral, for a probability space ,

and distort, or rather weight, its probabilities. This gives rise to the integral

| (4.2) |

where, for two random variables and , the probability measure is defined via the equation

with defined analogously. We next explore the case when the weights and are the indicators and , respectively, where and are elements of the -field .

Let denote the -field generated by , and let

For any event , let be the conditional probability of on . We call these conditional probabilities set masses, which are natural extensions of the earlier explored point masses.

We shall next connect weak comonotonicity with (in)dependence of random variables and . It is instructive to start with the bivariate Gaussian case, and the following proposition is akin to the classical result which says that the equivalence of uncorrelatedness and independence characterizes Gaussian random variables.

Proposition 4.1.

Let be jointly Gaussian with standard margins and correlation . Then the following three statements are equivalent:

-

(i)

;

-

(ii)

;

-

(iii)

.

Proof.

We first write for some standard Gaussian independent of . For any , we have and . Therefore, the following holds if and only if :

Furthermore, we check that, for ,

This establishes the proposition. ∎

Generally, and are not equivalent conditions, although they are in the Gaussian case, as we have just seen in Proposition 4.1.

Proposition 4.2.

We have the following statements:

-

(i)

If and are independent, then and, by symmetry, .

-

(ii)

If , then, for , we have the property

which in the “diagonal” case reduces to non-negativity of the conditional correlation for every event .

Proof.

To prove part (i), we use equation (4.1) and have

Hence . The other half of (i) is by symmetry. The proof of statement (ii) is a straightforward verification. ∎

4.3 Weak comonotonicity and measures of association

The notion of weak comonotonicity has enabled us to establish a whole spectrum of comonotonicity notions, ranging from the classical (strong) comonotonicity under the pairs of all point masses to weaker comonotonicity notions under the pairs of more elaborate measures. As we shall see next, this flexibility enables us to capture a whole array of measures of association.

-

(S1)

The Pearson correlation is non-negative if and only if and are weakly comonotonic with respect to .

-

(S2)

Two random variables and are positively associated (also called positively function dependent; see Joe (1997) for details) if and only if for all non-decreasing functions and , the random variables and are weakly comonotonic with respect to .

-

(S3)

Assuming that and have continuous cdf’s and , respectively, the Spearman correlation is non-negative if and only if and are weakly comonotonic with respect to the product .

-

(S4)

Two random variables and are independent if and only if, for all , the indicators and are weakly comonotonic with respect to . The same statement holds if we replace weak comonotonicity by weak antimonotonicity.

All the above statements are straightforward and follow from the equivalence of weak comonotonicity (with respect to ) and covariance non-negativity. The fourth property, however, warrants a simple comment-like proof.

Proof of (S4).

It is obvious that independence implies weak comonotonicity, as well as weak antimonotonicity, of and . For the other direction, let be an independent copy of . For all , we have

which is non-negative. Likewise, we have

which is also non-negative. Adding the left-hand sides of the two equations gives zero, which, due to the just established non-negativity statements, implies that the right-hand sides are also zeros, which implies independence. ∎

It is convenient to have probability-based quantities expressed in terms of distribution functions, and we next do so expressly for the purpose of checking whether or not the random variables and are weakly comonotonic with respect to . To this end, we write the equations

| (4.3) |

where

Consequently, and are weakly comonotonic with respect to if and only if the functions and are weakly comonotonic with respect to , that is,

| (4.4) |

From this we arrive at the following interpretation of positive association in terms of weak comonotonicity.

Proposition 4.3.

The following two statements are equivalent:

-

(1)

The random variables and are positively associated.

-

(2)

For all non-decreasing Borel functions and , the functions and are weakly comonotonic with respect to .

From Proposition 4.3 we see that if we require the functions and to be weakly comonotonic with respect to all product measures , and thus in particular with respect to the products for all , then this is tantamount to the functions and being strongly comonotonic. The next theorem connects the notion of weak comonotonicity of and with the notion of positive regression dependence (Lehmann, 1966).

Proposition 4.4.

The following two statements are equivalent:

-

(i)

For all non-decreasing Borel functions and , the functions and are weakly comonotonic with respect to all product measures .

-

(ii)

The random variable is positively regression dependent on , that is, for every , the function is non-increasing.

Proof.

Statement (i) means that and are strongly comonotonic for all non-decreasing Borel functions and . With this in mind, the equivalence of statements (i) and (ii) follows by noting that and are equal to and , respectively, where and . It now remains to recall that the class of all non-decreasing functions and the class , give rise to two equivalent ways for defining stochastic ordering (e.g., Pflug and Römisch, 2007; Rüschendorf, 2013; Föllmer and Schied, 2016). ∎

5 Maximality of product measures

Definition 2.2 is based on the product measure , which is a natural choice in view of the examples that have given rise to the notion of weak comonotonicity. There are, however, situations when the need for more generality arises, and for this we introduce an extension of integral (2.4):

| (5.1) |

where, is a measure on , and for any random variable on ,

Definition 5.1.

We say that random variables and are weakly comonotonic with respect to a set of (not necessarily product) measures on whenever

for all .

This generalization provides a context within which we can better understand the role of the product measure , which happens to enjoy the following maximality property:

| (5.2) |

provided that

| (5.3) |

where and . If the measure is symmetric, that is, for all , then . Note also that the covariance-looking quantities inside the first braces and inside the second braces are not, in general, symmetric with respect to and , but their sum is always symmetric, irrespective of the measure . Finally, we note that in the “diagonal” case , we have

To get a deeper insight into the above notion, and to also connect it to weak comonotonicity and positive association, we shift our focus to 1) the measurable space , 2) Borel functions and , and 3) the joint cdf generated by two random variables and , whose marginal cdf’s we denote by and , respectively. Under this scenario, bound (5.2) takes on the following form

| (5.4) |

which holds (cf. condition (5.3)) if and only if

| (5.5) |

where . Obviously, irrespective of the measure , and we also have the equation .

From the above notes we conclude that within the class of measures generated by positively-associated random variables and , the product measure is maximal in the sense of bound (5.4) within the class of all pairs of non-decreasing Borel functions and . But the assumptions that 1) and are positively associated and 2) and are non-decreasing are rather strong: they ensure non-negativity of the two covariances on the right-hand side of equation (5.5) and thus, in turn, imply the required non-negativity of .

Due to the notion of weak comonotonicity, we can specify necessary and sufficient conditions for non-negativity of the two covariances on the right-hand side of equation (5.5). For this, we write

| (5.6) |

where and . The two covariances on the right-hand side of equation (5.6) are non-negative if and only if the two pairs and are weakly comonotonic with respect to the measure .

Note, however, that the covariance can be non-negative without making the two covariances on the right-hand side of equation (5.6) non-negative. To show this, we next construct an example when one of the two covariances is negative but is positive.

Example 5.1.

Let and . Furthermore, let and be random variables whose marginal distributions are

and

and let the dependence structure be given by the matrix

with Archimedes’ constant not be confused with the earlier used notation for measures. We have

and thus

This concludes Example 5.1.

6 An application to quantile-based risk sharing

In this section, we illustrate the above developed theory by studying an optimization problem arising in the context of risk sharing, where weak comonotonicity provides a natural constraint on the dependence structure of admissible risk allocations. We follow the framework of Embrechts et al. (2018, 2019), who studied risk sharing problems with quantile-based risk measures.

Let be the set of all random variables in an atomless probability space. The random variable represents a total random loss, and are risk measures (e.g., VaR or ES) used by economic agents (e.g., firms or investors). Denote

| (6.1) |

which is the set of all possible allocations of losses to the agents, summing up to at least the total loss . By Embrechts et al. (2018, Proposition 1), Pareto-optimal allocations for the risk sharing problem are solutions to the following optimization problem

| (6.2) |

In problem (6.2), the dependence structure among the allocation is arbitrary. Embrechts et al. (2018) also consider the constrained problem

| (6.3) |

where means that and are strongly comonotonic.

For a practical situation, the assumption of arbitrary dependence in the admissible allocations as in problem (6.2) may be too weak, and the assumption of strongly comonotonic allocations in problem (6.3) may be too strong. Therefore, we can consider an intermediate assumption on the dependence structure of the admissible allocations in the risk sharing problem, which is modelled by weak comonotonicity.

To this end, we construct a spectrum of weak comonotonicity indexed by , such that corresponds to no dependence constraint and corresponds to strong comonotonicity. For this purpose, recall that in Section 3 above, for a random variable and for any , we defined

and

In what follows, for two random variables and , we shall use the notation when and are weakly comonotonic with respect to .

The interpretation of is that and are comonotonic and both take large values on the event , and there is no dependence assumption on . Note also that the requirement gets stronger when increases. In particular, assuming that is continuously distributed, for , imposes no dependence assumption, and for , it means that and are strongly comonotonic. Using this connection, we will impose , as a constraint on the admissible allocations in our risk sharing problem, so that corresponds to (6.2) and corresponds to (6.3).

For the purpose of illustration, we focus on an important special case studied by Embrechts et al. (2018), when the risk measures are quantiles at different levels. Following the setup of Embrechts et al. (2018), for and , we define

Remark 6.1.

Note that is the left -quantile, which is different from the VaR (right quantile) defined in Section 3. The choice of the left quantile here and in Embrechts et al. (2018, 2019) is intentional. For minimization problems, we need to work with left quantiles to guarantee the existence of optimal allocations. Recall that in Section 3 we study maximization problems, and hence right quantiles are natural choices there. On the other hand, using -quantile instead of -quantile leads to concise statements of the results; this will be clear from statements (6.4)–(6.5) below.

Let , , where are positive constants such that . For this choice of risk measures, both problems (6.2) and (6.3) admit analytical solutions, given in Theorem 2 and Proposition 5 of Embrechts et al. (2018), respectively. These results imply

| (6.4) |

and

| (6.5) |

and the corresponding optimal allocations can be explicitly constructed as well. Note that result (6.4) implies

| (6.6) |

for all (Embrechts et al., 2018, Corollary 1), which will be useful in our analysis below.

Remark 6.2.

Embrechts et al. (2018) formulate the admissible allocations in (6.1) using instead of . It is easy to see that in problems (6.2) and (6.3), these two setups are equivalent for monotone risk measures such as the quantiles. In this paper, we use inequality in definition (6.1) because our dependence constraint would make the two formulations generally no longer equivalent, and analytical solutions are found for the current formulation.

For a continuously distributed and a parameter , we consider the optimization problem

| (6.7) |

It is clear that corresponds to problem (6.2) and corresponds to problem (6.3). Therefore, the use of weak comonotonicity yields a bridge between the two risk sharing problems (6.2) and (6.3) considered by Embrechts et al. (2018), and it offers more flexibility as one can impose a partial dependence constraint on the admissible allocations.

Similarly to many other optimization problems involving quantiles (or VaR), problem (6.7) is not convex as is generally not convex, and thus a specialized analysis of the problem is needed. Nevertheless, via some auxiliary technical results, we will show below that problem (6.7) admits an analytical solution, and an optimal allocation will be obtained in explicit form.

Theorem 6.1.

Suppose that is a continuously distributed random variable, , , and . We have

where

Proof.

We first note that if , and if , corresponding to statements (6.4) and (6.5), respectively. Thus, it suffices to consider . To proceed, we need the following lemma, whose proof will be given in the appendix.

Lemma 6.1.

Let and . Denote . We have the statements:

-

(i)

and a.s.

-

(ii)

If , then for all .

-

(iii)

If , then for all .

-

(iv)

If , then for all .

-

(v)

If , then for all and .

We can now continue the proof of Theorem 6.1. Let and take an arbitrary admissible allocation such that , . We need additional notation: , , and . Moreover, let , , , , , , and .

By Lemma 6.1(i), we have (all statements are in the sense of a.s.)

| (6.8) |

Using statements (6.8), we see that the random vector is strongly comonotonic, because is strongly comonotonic on the event by assumption. Hence, using for , Lemma 6.1(iv) and statement (6.5), we get

| (6.9) |

Further, statements (6.8) also imply

| (6.10) |

We split the following considerations into two cases.

Case 1.

Case 2.

Assume , which means , and . Using Lemma 6.1(ii) and (v), and bound (6.6), we get

| (6.11) |

Therefore, and are strongly comonotonic. Putting inequalities (6.9) and (6.11) together, and using statements (6.5) and (6.10), we obtain

| (6.12) |

Note that is continuously distributed, implying . Moreover, on , and by Lemma 6.1(i), we have

This shows . Using Lemma 6.1(iii) and bounds (6.12), we obtain

This proves .

Next, we show by an explicit construction of an optimal allocation. Let and . Without loss of generality, assume . Recall that

and hence we can find a partition of such that for each . Define

| (6.16) |

We easily verify that and , . Hence, is an admissible allocation for problem (6.7). Furthermore, we check that and for . Therefore,

showing that .

With this, we finish the proof of Theorem 6.1.∎

An explicit construction of an optimal allocation to problem (6.7) has been obtained in the proof of Theorem 6.1. Specifically, and without loss of generality, let . If , then an optimal allocation is given by equation (6.16). On the other hand, if , then an optimal allocation is trivially given by and for . The optimal allocations are generally not unique, similarly to the case of problems (6.2) and (6.3) in Embrechts et al. (2018).

Finally, we discuss the implication of the values of the parameter in problem (6.7). Recall that represents the smallest total risk measure after risk redistribution. In Theorem 6.1, is a piece-wise linear decreasing function of , with and if . Thus, if there is no dependence constraint, we arrive at (6.4), the minimum possible total risk measure obtained by Embrechts et al. (2018, Theorem 2). If the dependence constraint is strong enough (i.e., ), then we arrive at the same value of the minimum total risk measure to (6.5), obtained by Embrechts et al. (2018, Proposition 5). If the dependence constraint is intermediate, then the total risk measure varies between the two values, decreasing in . This suggests that the use of weak comonotonicity as a dependence constraint yields a spectrum of flexible formulations of the risk sharing problem.

7 Summary and concluding notes

In this paper, we introduced the notion of weak comonotonicity. Via the analysis of several properties and applications, we show the encompassing nature of weak comonotonicity, which contains – as a special case – the classical notion of comonotonicity. The new notion serves a bridge that connects the classical notion of comonotonicity of random variables with a number of well-known notions of (in)dependence and association (e.g., Joe, 2014; Durante and Sempi, 2015, and references therein). More importantly, we illustrate that introduced weak comonotonicity provides necessary and sufficient conditions for a number of problems in economics, banking, and insurance, and in particular to those dealing with risk aggregation and risk sharing. Specifically, it is shown that the notion of weak comonotonicity yields a sufficient condition for the maximum aggregation, and a necessary and sufficient condition for the maximum aggregation. As far as we are aware of, such conditions have been elusive. In addition, we provided analytical solutions to a risk sharing problem whose constraint on the dependence structure of admissible allocations has been most naturally described by weak comonotonicity, bridging the gap between strong comonotonicity and no dependence assumption studied in the literature. We finally remark that, as weak comonotonicity depends on the set of product measures, its spectrum is very wide, including many types of dependence.

Acknowledgements

The authors thank the Editor Emanuele Borgonovo and four anonymous referees for various helpful comments on an early version of the paper. The authors have been supported by their individual research grants from the Natural Sciences and Engineering Research Council (NSERC) of Canada (RGPIN-2018-03823, RGPAS-2018-522590, RGPIN-2016-427216), as well as by the National Research Organization “Mathematics of Information Technology and Complex Systems” (MITACS) of Canada.

Appendix A Appendix: Proof of Lemma 6.1

Proof of statement (i).

By definition of , for a.s. all and , we have . Therefore, there exists a constant such that and a.s. It is easy to see that this constant can be chosen as because and .

Proof of statement (ii).

Proof of statement (iii).

Note that

This shows

| (A.2) |

For the other direction, we consider two cases, similarly to statement (ii). If , then by statement (i). In this case,

If , then by statement (i). In this case,

In both cases,

which implies . By bound (A.2), we get .

Proof of statement (iv).

If , then for all . Note that

This shows

| (A.3) |

For the other direction, we again consider two cases. If , then by statement (i). In this case,

If , then by statement (i). In this case,

In both cases,

which implies . By bound (A.3), we get .

Proof of statement (v).

References

- Box et al. (2015) Box, G.E.P., Jenkins, G.M., Reinsel, G.C. and Ljung, G.M. (2015). Time Series Analysis: Forecasting and Control. (Fifth edition.) Wiley, New York.

- Carlier et al. (2012) Carlier, G., Dana, R.-A. and Galichon, A. (2012). Pareto efficiency for the concave order and multivariate comonotonicity. Journal of Economic Theory, 147, 207–229.

- Cheung (2010) Cheung, K. C. (2010). Characterizing a comonotonic random vector by the distribution of the sum of its components. Insurance: Mathematics and Economics, 47, 130–136.

- Dhaene et al. (2002a) Dhaene, J., Denuit, M., Goovaerts, M.J. and Vyncke, D. (2002a). The concept of comonotonicity in actuarial science and finance: theory. Insurance: Mathematics and Economics, 31, 3–33.

- Dhaene et al. (2002b) Dhaene, J., Denuit, M., Goovaerts, M.J. and Vyncke, D. (2002b). The concept of comonotonicity in actuarial science and finance: applications. Insurance: Mathematics and Economics, 31, 133–161.

- Denneberg (1994) Denneberg, D. (1994). Non-additive Measure and Integral. Kluwer, Dordrecht.

- Deprez and Gerber (1985) Deprez, O. and Gerber, H.U. (1985). On convex principles of premium calculation. Insurance: Mathematics and Economics, 4(3), 179–189.

- Durante and Sempi (2015) Durante, F. and Sempi, C. (2015). Principles of Copula Theory. Chapman and Hall/CRC, Boca Raton, FL.

- Ekland et al. (2012) Ekeland, I., Galichon, A. and Henry, M. (2012). Comonotonic measures of multivariate risks. Mathematical Finance, 22, 109–132.

- Embrechts et al. (2018) Embrechts, P., Liu, H. and Wang, R. (2018). Quantile-based risk sharing. Operations Research, 66, 936–949.

- Embrechts et al. (2019) Embrechts, P., Liu, H., Mao, T. and Wang, R. (2019). Quantile-based risk sharing with heterogeneous beliefs. Mathematical Programming Series B (in press). https://doi.org/10.1007/s10107-018-1313-1

- Embrechts et al. (2013) Embrechts, P., Puccetti, G. and Rüschendorf, L. (2013). Model uncertainty and VaR aggregation. Journal of Banking and Finance, 37, 2750–2764.

- Embrechts et al. (2014) Embrechts, P., Puccetti, G., Rüschendorf, L., Wang, R. and Beleraj, A. (2014). An academic response to Basel 3.5. Risks, 2, 25-48.

- Embrechts et al. (2015) Embrechts, P., Wang, B. and Wang, R. (2015). Aggregation-robustness and model uncertainty of regulatory risk measures. Finance and Stochastics, 19, 763–790.

- Embrechts and Wang (2015) Embrechts, P. and Wang, R. (2015). Seven proofs for the subadditivity of expected shortfall. Dependence Modeling, 3, 126–140.

- Engle (2016) Engle, R.F. (2016). Dynamic conditional beta. Journal of Financial Econometrics, 14, 643–667.

- Esary et al. (1967) Esary, J.D., Proschan, F., and Walkup, D.W. (1967). Association of random variables, with applications. Annals of Mathematical Statistics, 38, 1466–1474.

- Föllmer and Schied (2016) Föllmer, H. and Schied, A. (2016). Stochastic Finance: An Introduction in Discrete Time. (Fourth Edition.) Walter de Gruyter, Berlin.

- Furman and Zitikis (2009) Furman, E. and Zitikis, R. (2009). Weighted pricing functionals with applications to insurance: an overview. North American Actuarial Journal, 13, 483–496.

- Furman et al. (2017) Furman, E., Wang, R. and Zitikis, R. (2017). Gini-type measures of risk and variability: Gini shortfall, capital allocation and heavy-tailed risks. Journal of Banking and Finance, 83, 70–84.

- Gebelein (1941) Gebelein, H. (1941). Das statistische problem der korrelation als variations- und eigenwertproblem und sein zusammenhang mit der ausgleichsrechnung. Zeitschrift für Angewandte Mathematik und Mechanik, 21, 364–379.

- Gillen and Markowitz (2009) Gillen, B. and Markowitz, H.M. (2009). A taxonomy of utility functions. In: Variations in Economic Analysis: Essays in Honor of Eli Schwartz (Eds.: J.R. Aronson, H.L. Parmet, and R.J. Thornton). Springer, New York.

- Joe (1997) Joe, H. (1997). Multivariate Models and Multivariate Dependence Concepts. Springer, Dordrecht.

- Joe (2014) Joe, H. (2014). Dependence Modeling with Copulas. Chapman and Hall/CRC, Boca Raton, FL.

- Kimeldorf and Sampson (1978) Kimeldorf, G. and Sampson, A.R. (1978). Monotone dependence. Annals of Statistics, 6, 895–903.

- Lehmann (1966) Lehmann, E.L. (1966). Some concepts of dependence. Annals of Mathematical Statistics, 37, 1137–1153.

- Makarov (1981) Makarov, G. D. (1981). Estimates for the distribution function of the sum of two random variables with given marginal distributions. Theory of Probability and its Applications, 26, 803–806.

- Markowitz (1952) Markowitz, H. (1952). The utility of wealth. Journal of Political Economy, 60, 151–156.

- McNeil et al. (2015) McNeil, A. J., Frey, R. and Embrechts, P. (2015). Quantitative Risk Management: Concepts, Techniques and Tools. Revised Edition. Princeton, NJ: Princeton University Press.

- Pennings and Smidts (2003) Pennings, J.M.E., and Smidts, A. (2003). The shape of utility functions and organizational behavior. Management Science, 49, 1251–1263.

- Pflug and Römisch (2007) Pflug, G.C. and Römisch, W. (2007). Modelling, Managing and Measuring Risks. World Scientific Publishing, Singapore.

- Puccetti and Scarsini (2010) Puccetti, G. and Scarsini, M. (2010). Multivariate comonotonicity. Journal of Multivariate Analysis, 101, 291–304.

- Puccetti and Wang (2015) Puccetti, G. and Wang R. (2015). Extremal dependence concepts. Statistical Science, 30, 485–517.

- Rao (1997) Rao, C.R. (1997). Statistics and Truth: Putting Chance to Work. World Scientific, Singapore.

- Rüschendorf (1982) Rüschendorf, L. (1982). Random variables with maximum sums. Advances in Applied Probability, 14, 623–632.

- Rüschendorf (2013) Rüschendorf, L. (2013). Mathematical Risk Analysis. Dependence, Risk Bounds, Optimal Allocations and Portfolios. Springer, Heidelberg.

- Schmeidler (1986) Schmeidler, D. (1986). Integral representation without additivity. Proceedings of the American Mathematical Society, 97, 255–261.

- Wang et al. (2013) Wang, R., Peng, L. and Yang, J. (2013). Bounds for the sum of dependent risks and worst Value-at-Risk with monotone marginal densities. Finance and Stochastics, 17, 395–417.

- Yaari (1987) Yaari, M.E. (1987). The dual theory of choice under risk. Econometrica, 55, 95–115.