On the generalized low rank approximation of the correlation matrices arising in the asset portfolio

††thanks: The work was supported by National Natural Science Foundation of China (Nos. 11101100; 11261014;

11301107; 61362021), Natural Science Foundation of Guangxi Province (No. 2012GXNSFBA053006;

2013GXNSFBA019009; 2013GXNSFBB053005; 2013GXNSFDA019030), the Fund for Guangxi Experiment

Center of Information Science (20130103), Innovation Project of GUET Graduate Education

(GDYCSZ201473), Innovation Project of Guangxi Graduate Education (YCSZ2014137), and Guangxi Key

Lab of Wireless Wideband Communication and Signal Processing open grant 2012.

Xuefeng Duan 111Corresponding author.E-mail address:duanxuefenghd@aliyun.com(X. Duan), baijianchaok@126.com(J. Bai).

Jianchao Bai

Maojun Zhang

Xinjun Zhang

College of Mathematics and Computational Science,

Guilin University of

Electronic Technology, Guilin 541004, P.R. China

AbstractIn this paper, we consider the generalized low rank approximation of the correlation matrices problem

which arises in the asset portfolio. We first characterize the feasible set by using

the Gramian representation together with a special trigonometric function transform, and then transform

the generalized low rank approximation of the correlation matrices problem into an unconstrained

optimization problem. Finally, we use the conjugate gradient algorithm with the strong Wolfe line

search to solve the unconstrained optimization problem. Numerical examples show that

our new method is feasible and effective.

Throughout this paper, we use and to denote the set of real matrices

and symmetric positive semidefinite matrices, respectively. We use and to represent the

transpose and trace of the matrix , respectively. The symbols and denote the Frobenius norm

and the rank of the matrix respectively. The symbol stands for the vector whose elements lie

in the diagonal line of the matrix and the symbol stands for the vector whose elements are of all

ones, i.e.,

In this paper, we consider the following problem named generalized low rank

approximation of the correlation matrices.

Problem 1.1. Given some correlation matrices ,

and a positive integer , find a correlation matrix whose rank is less than

and equal to such that

Problem (1.1) arises in the asset portfolio (see [10] for more details), which can be stated as follows.

Suppose that is the covariance matrix of assets, where is a correlation matrix

and is a diagonal matrix with positive variances which are specially used to describe

the risk of assets. In practice, the covariance matrix is usually estimated by the

historical data of the return of each asset, that is, an approximation covariance is obtained

by statistics method. Let

be the approximation covariance with th sampling some data,

where and are the th approximation diagonal matrix and correlation matrix, respectively.

Higham [4] proposed a method for finding the nearest low rank approximation of a correlation matrix by only one

sampling(i.e., ). However, it is difficult for the decision maker to choose the best approximation covariance

matrix with only one sampling because there is always a noise in the data on the prices of assets. Thus, we develop

a repeated sampling method to get a series of approximation covariance matrices, that is, comes from to .

Obviously, it is very easy to obtain the optimal diagonal matrix by a series of .

The major obstacle to finding the optimal covariance matrix is conducting the optimal correlation

matrix from a series of . The above consideration leads to solving the following problem:

given some correlation matrices , find a correlation

matrix such that

Meanwhile, for the large financial correlation matrices, usually almost all variances can be attributed to some

stochastic Brownian factors. Therefore, instead of taking into account all Brownian motions, we would wish to

simulate with a smaller number of factors, i.e., and typically is from 1 to . Then the

problem (1.2) with rank constraint becomes problem (1.1).

Noting that the matrix in problem (1.1) is not only positive semidefinite but also satisfies ,

so problem (1.1) belongs to the structured low rank approximation problem. As Gillard-Zhigljavsky [3] said, the

structured low rank approximation is a difficult optimization problem, so there is much work to be done.

In the last few years, there has been a constantly increasing interest in developing the theory and numerical

methods for the nearest low rank approximation of a correlation matrix, due to their wide applications in the

fiance and risk management [6], machine learning [15], stress testing of bank [13], industrial process

monitoring [7] and image processing [5]. Recently, problem (1.1) with has been extensively studied,

and the research results mainly concentrate on the following two cases. One is without the rank constraint

and the other is with the rank constraint.

For the case without the rank constraint, Higham [4] proposed an alternative projection

algorithm to solve the nearest correlation matrix problem by defining two projection operators.

Under some proper assumptions, Li-Li [8] developed a projected semismooth Newton method to solve the problem

of calibrating least squares covariance matrix. Qi and Sun [12] proposed a Newton-type method for the nearest

correlation matrix problem, and the quadratic convergence of the new method was proved. An unconstrained convex

optimization approach was proposed to find the nearest correlation matrix to the target matrix with the

fixed correlations unaltered in [13]. Besides, Qi-Sun [14] introduced an augmented Lagrangian dual method

for for the H-weighted nearest correlation matrix problem. This method solves a sequence of unconstrained strongly convex optimization

problems, each of which can be solved by a semismooth Newton method combined with the conjugate gradient method.

Recently, Yin, etc [18, 20] developed two new alternative gradient algorithms to compute the nearest correlation

matrix by making use of the alternative gradient method.

For the case with the rank constraint, by making use of the fact that

Gao and Sun [2] proposed a majorized penalty approach for solving the rank constrained correlation matrix problem.

It is noted that Gao and Sun’s majorized penalty approach can deal with some large scale problems ().

Motivated by the method in [12] and based on a well-known result that the sum of the largest

eigenvalues of a symmetric matrix can be represented as a semidefinite programming problem,

Li-Qi [9] proposed a novel sequential semismooth Newton method to solve problem (1.1) with .

They formulate the problem as a bi-affine semidefinite programming and then use an augmented

Lagrange method to solve a sequence of least squares problems.

Both Simon-Abell [16] and Pietersz-Groenen [11] used majorization approach

to solve the low rank approximation of a correlation matrix. The difference lies in that the former solved

the problem with any weighted norm while the latter only settled it with Frobenius norm.

By constructing a Lagrange function, Zhang-Wu [21] transformed the

low rank approximation of a correlation matrix into a min-max problem, where the inner maximization problem

was solved with closed form spectral decomposition and the outer minimization problem was solved with

gradient-based methods. In [1], Grubisic and Pietersz introduced a geometric programming approach

to solve the low rank nearest correlation matrix problem. The method could be used to minimize any sufficiently

smooth objective function.

However, the research results of problem (1.1) with are very few as far as we know. The greatest

difficulties to solve problem (1.1) are how to characterize the feasible set and deal with the complex

structure. In this paper, we overcome these difficulties by using the Gramian representation together

with a special trigonometric function transform. Then problem (1.1) is transformed into an unconstrained

optimization problem. Finally, the conjugate gradient method with the strong Wolfe line search is

given to solve the unconstrained optimization problem. Numerical examples show that our

new method is feasible and effective.

2. Main results

In this section, we first transform problem (1.1) into an unconstrained optimization problem

by making use of the Gramian representation together with a special trigonometric function transform.

Then we use the conjugate gradient algorithm with the strong Wolfe line search to solve it.

We first define the following set

It is easy to characterize the set by using the Gramian representation (see [17]), i.e.,

Set

It is easy to verify that the feasible

set of problem (1.1) is . The most difficulty to solve problem (1.1) is how to

characterize the feasible set. Now we begin to use the Gramian representation together with a

special trigonometric function transform to characterize the feasible set .

Theorem 2.1. Let the matrix be

Suppose

where

then the matrix is not only symmetric positive semidefinite,

but also satisfies and

Proof. By using the Gramian representation, it is easy to verify that the

matrix is symmetric positive semidefinite and satisfies . Hence, we only need to prove .

Consider the matrix with . According to the assumptions, we have

Let be the th row of the matrix , that is,

By multiplying and ,

we get the element of the matrix , that is,

That is to say, . Hence, Theorem 2.1 holds when .

When , without loss of generality, we take the th row of the matrix and write

it as , then

By multiplying and , we get the element of the matrix , that is,

Hence, for any , we have , that is,

Remark 2.1. As Simon and Abell [16] said, a correlation matrix is a symmetric

positive semidefinite matrix with unit diagonal, and any symmetric positive semidefinite matrix with unit

diagonal is a correlation matrix. In Theorem 2.1, the matrix must be a correlation matrix, and noting that

are arbitrary real number, so the matrix

can be represented all the correlation matrices.

Remark 2.2. To explain Theorem 2.1, we take a matrix for example. Set

By a simple calculation, we can obtain that

Obviously, the matrix is not only symmetric positive semidefinite , but also satisfies and

By using the similar way in the proof of Theorem 2.1, we can obtain the other elements of the

matrix , that is,

Substituting into problem (1.1), it is easy to obtain that problem (1.1) can be

written as the following unconstrained optimization problem.

Problem 2.1. Given some correlation matrices ,

and a positive integer , find the solution of the following optimization problem

where

Nextly, we will use the conjugate gradient algorithm with the strong Wolfe line search to solve the

unconstrained optimization problem. The most difficulty to solve problem (2.1) is how to

compute the gradient of the objective function . Now we begin to compute the

gradient of the objective function.

Theorem 2.2. The gradient of the objective function of problem (2.1) is

where

here .

Proof. To prove Theorem 2.2, we only need to prove (2.3) holds when ,

because the forms of the expression of the gradient of the objective function

with are the same as that with .

For , noting that the total numbers including in are

Hence, the derivative of at is

Because , we turn to and conclude that

where .

Consequently, the conjugate gradient algorithm with the strong Wolfe line search to solve the

minimization problem (2.1) can be described in Algorithm 2.1.

Algorithm 2.1 (This algorithm attempts to solve problem (2.1))

Step 1. Given parameters ,

and tolerance error . Choose an initial iterative matrix . Set .

Step 2. Calculate . If , stop

and output .

Step 3. Determine the search direction , where

Step 4. Confirm the step length by applying the strong Wolfe line search, i.e.,

Set

Step 5. Set . Go to step 2.

Remark 2.3. To implement Algorithm 2.1, we first need to create three matlab files,

fun file, gfun file and frac file, where the fun file is used to compute

, the gfun file is used to calculate , and the frac

file is used to minimize . In addition, the function returns the

by vector whose elements are taken column-wise from the matrix ,

and the function returns the by matrix

whose elements are taken column-wise from .

By Theorem 4.3.5 [19, P.203], we can establish the global convergence theorem for Algorithm 2.1.

Theorem 2.3. Suppose the function is twice continuous and differentiable,

the level set

is

bounded, and the step length is generated by (2.4), where . Then the

sequence generated by Algorithm 2.1 is guaranteed to globally converge, that is,

3. Numerical Experiments

In this section, we use two numerical examples to illustrate that Algorithm 2.1 is feasible to

solve problem (2.1). All experiments are tested in Matlab R2010a. We denote the relative residual error

and the gradient norm

where is the th iterative matrix of Algorithm 2.1. We use the stopping criterion

And we choose the random matrix as the initial value in the

following examples, where the random matrix is generated by the Matlab function

Example 3.1. Consider problem (2.1) with and

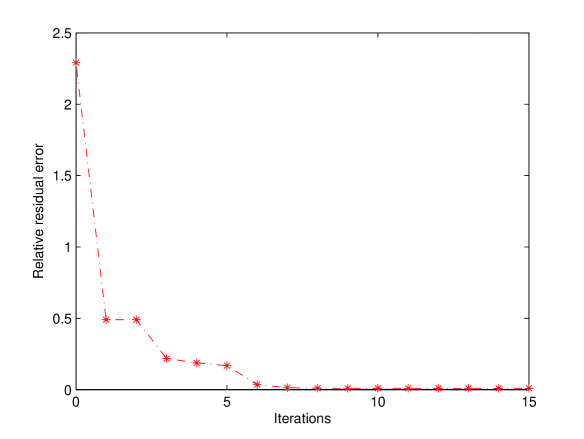

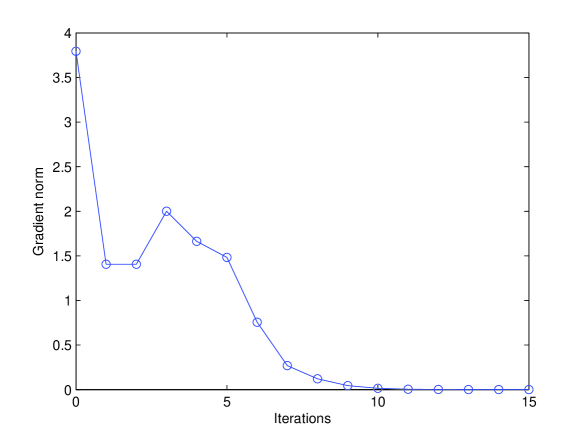

Case I: Set k=3. We use Algorithm 2.1 with the initial value

to solve problem (2.1). After 15 iterations, we get the solution of problem (2.1)

Hence, the solution of problem (1.1) is

And the curves of the relative residual error and the gradient norm

are in Fig. 1.

Fig. 1: Convergence curves of the relative residual error

and the gradient norm .

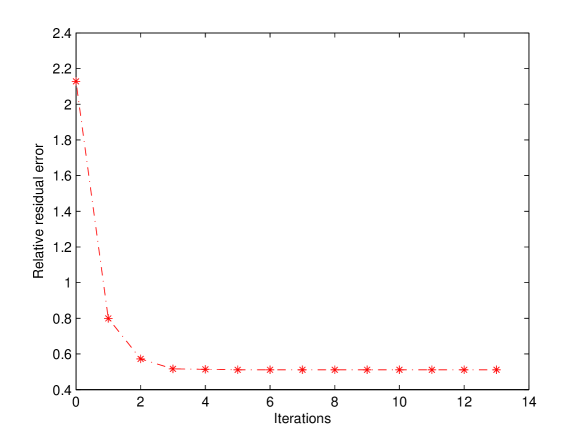

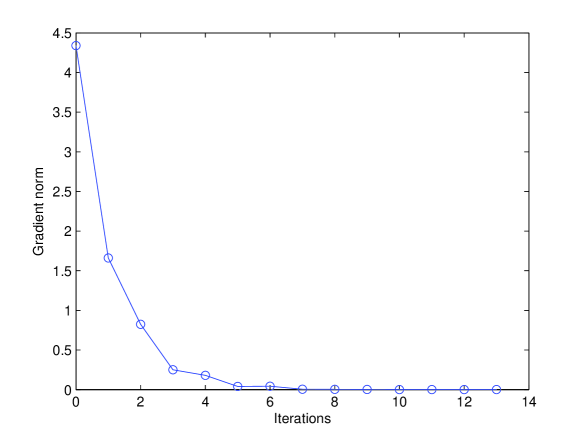

Case II: Set k=2. We use Algorithm 2.1 with the initial value

to solve problem (2.1). After 13 iterations, we get the solution of problem (2.1)

Hence, the solution of problem (1.1) is

And the curves of the relative residual error and the gradient norm

are in Fig. 2.

Fig. 2: Convergence curves of the relative residual error

and the gradient norm .

In order to compare our algorithm with the Major algorithm in [11], we use them to solve

problem (2.1) with the same initial value. We list the number of iteration (denoted by ”IT”),

CPU time (denoted by ”CPU”), the gradient norm (denoted by ”GN”) and the relative

residual error (denoted by ”ERR”) in Table 1.

Example 3.1 shows that Algorithm 2.1 is feasible to solve problem (1.1). Especially, Table 1

shows that our algorithm outperforms the Major algorithm [11] in both iterations and CPU time,

which indicates that our algorithm has faster convergence rate than the Major algorithm.

Nextly, we will use an example to show that our algorithm can be used to solve the generalized

low rank approximation of correlation matrices arising in the asset portfolio.

Example 3.2. It is an important issue to calculate the more exact correlation matrix of assets in the portfolio selection.

For instance, suppose that an investor uses one unit money to buy a total of assets at the beginning of one period. There is a

relationship between any two assets of the portfolio because the price of each asset is related to some common factors in the financial market. The correlation matrix is one of the methods measuring the relation between assets. However, how to accurately compute the

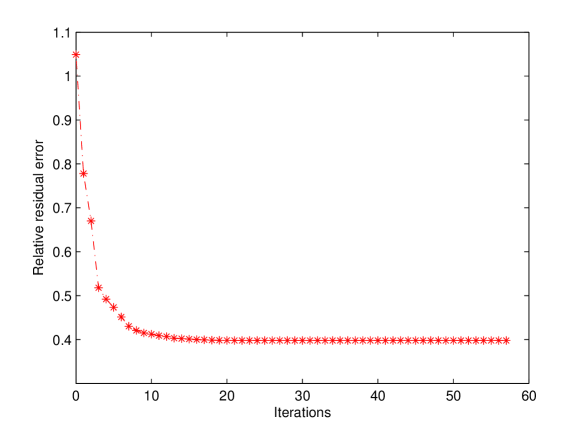

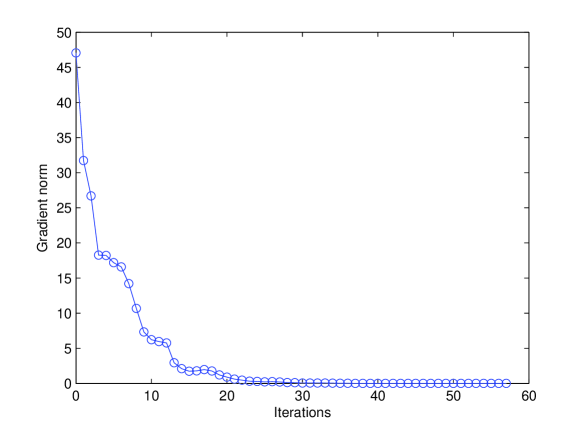

correlation matrix is the key problem for the investor since the optimal investment policies is affected by the uncertainty of parameters in the correlation matrix. The daily price data of each asset in the portfolio are taken from the Wind database, which is a Chinese financial database, in order to obtain the correlation matrix. Five sets of the daily data are got by the sampling based on five different periods of the data. Using the Matlab software, five correlation matrix of the eleven assets are given as follows.

Set k=3, and we use Algorithm 2.1 with the initial value

to solve problem (2.1). After 57 iterations, we get the solution of problem (2.1)

Hence, the solution of problem (1.1) is

And the curves of the relative residual error and the gradient norm are in Fig. 3.

Fig. 3: Convergence curves of the relative residual error

and the gradient norm .

For the above example, we use Algorithm 2.1 to solve problem (2.1) with different rank. We

list the number of iteration (denoted by ”IT”) , CPU time (denoted by ”CPU”),

the gradient norm (denoted by ”GN”) and the relative residual error (denoted by ”ERR”) in Table 2.

Fig. 3 and Table 2 show that Algorithm 2.1 can be used to solve the generalized low rank

approximation of correlation matrices arising in the asset portfolio. What is more important,

when the investor uses the matrix obtained by using Algorithm 2.1 to analyze the relationship

between any two assets, some noise in the data can be reduced because the correlation matrix of

assets is an important factor for selecting assets in portfolio.

4. Conclusion

The generalized low rank approximation of correlation matrices is widely used in the asset

portfolio and risk management. It is a difficult matrix optimization problem, and the

difficulties lie in how to deal with its feasible set and complex structure. In this paper,

we use the Gramian representation together with special trigonometric function transform to

overcome these difficulties, and develop a new algorithm to solve it. Numerical examples

show that our new method is feasible and effective. Moreover, the theory and algorithm of

this paper can be extended to solve the low rank approximation in Li-Qi [9], that is, the

nearest low rank approximation of a correlation matrix to the given symmetric matrix.

Acknowledgements

The authors wish to thank Prof. Richard A Brualdi and the anonymous

referee for providing very useful suggestions for improving this

paper. The authors also thank Prof. Qingwen Wang for discussing

the properties of the objective function.

References

[1]

[2] I. Grubisic, R. Pietersz,

Efficient rank reduction of correlation matrices,

Linear Algebra Appl. 422 (2007) 629-653.

[3] Y. Gao, D. Sun,

A majorized penalty approach for calibrating rank constrained correlation matrix problems,

Technical Report, Department of Mathematics, National University of Singapore, March 2010.

[4] J. Gillard, A. Zhigljavsky,

Analysis of structured low rank approximation as an optimization problem,

Inform. 22 (2011) 489-505.

[5] N. Higham,

Computing the nearest correlation matrix - A problem from finance,

IMA J. Numer. Anal. 22 (2002) 329-343.

[6] W. Hoge,

A subspace identification extension to the phase correlation method,

IEEE Trans. Med. Imaging 22 (2003) 277-280.

[7] P.H. Kupiec,

Stress testing in a value at risk framework,

J. Derivatives 6 (1988) 7-24.

[8] T. Kourti,

Process analysis and abnormal situation detection: from theory to practice,

IEEE Control Syst. Mag. 22 (2002) 10-25.

[9] Q.N. Li , D.H. Li,

A projected semismooth Newton method for problems of calibrating least squares covariance matrix,

Oper. Res. Lett. 39 (2011) 103-108.

[10] Q.N. Li, H.D. Qi,

A Sequential Semismooth Newton Method for the Nearest Low-rank Correlation Matrix Problem,

SIAM J. Optim . 21 (2011) 1641-1666.

[11] H. Markowitz,

Portfolio selection,

J. Finance 7 (1952) 77-91.

[12] R. Pietersz, P. Groenen,

Rank reduction of correlation matrices by majorization,

Quant. Finance 4 (6) (2004) 649-662.

[13] H.D. Qi, D. Sun,

A quadratically convergent Newton method for computing the nearest correlation matrix,

SIAM J. Matrix Anal. Appl., 28 (2006) 360-385.

[14] H.D. Qi, D. Sun,

Correlation stress testing for value-at-risk: an unconstrained convex optimization approach,

Comput Optim. Appl. 45 (2010) 427-462.

[15] H.D. Qi, D. Sun,

An augmented Lagrangian dual approach for the H-weighted nearest correlation matrix problem,

IMA J. Numer. Anal. 31 (2011) 491-511.

[16] H.D. Qi, Z.H. Xia, G.M. Xing,

An application of the nearest correlation matrix on web document classification,

J. Ind. Manag. Optim. 3 (2007) 701-713.

[17] D. Simon , J. Abell,

A majorization algorithm for constrained correlation matrix approximation,

Linear Algebra Appl. 432 (2010) 1152-1164.

[18] S. Xu, L. Gao, P. Zhang,

Numerical linear algebra,

Peking university press, Beijing, 2010.

[19] J. Yin, Y. Huang,

Modified multiplicative update algorithms for computing the nearest correlation matrix,

J. Appl. Math. Inform. 30 (2012) 201-210.

[20] Y. Yuan, W. Sun,

Optimization theory and methods,

Science press, Beijing, 2010.

[21] J. Yin, Y. Zhang,

Alternative gradient algorithms for computing the nearest correlation matrix,

Appl. Math. Comput. 219 (2013) 7591-7599.

[22] Z. Zhang, L. Wu,

Optimal low-rank approximation to a correlation matrix,

Linear Algebra Appl. 364 (2003) 161-187.