Path Dependent Optimal Transport and Model Calibration on Exotic Derivatives

Abstract

In this paper, we introduce and develop the theory of semimartingale optimal transport in a path dependent setting. Instead of the classical constraints on marginal distributions, we consider a general framework of path dependent constraints. Duality results are established, representing the solution in terms of path dependent partial differential equations (PPDEs). Moreover, we provide a dimension reduction result based on the new notion of “semifiltrations”, which identifies appropriate Markovian state variables based on the constraints and the cost function. Our technique is then applied to the exact calibration of volatility models to the prices of general path dependent derivatives.

Mathematics Subject Classification (2010): 60H30, 91G80, 93E20

Keywords: optimal transport, path dependent PDE, volatility calibration

1 Introduction

Inspired by the seminal work on optimal transport by Benamou and Brenier [3], and the duality theory developed in [4] and later [25], we examine the problem of optimal transport by semimartingales in continuous time settings. The semimartingale optimal transport problem with constraints on marginals at given times has been studied by Tan and Touzi in [34], extending the work of Mikami and Thieullen [26]. Other related works include [23, 35]. The main goal of our study is to extend this work by considering a much wider range of constraints. As shown in our abstract formulation, the constraints considered can be defined by any arbitrary closed and convex set of probability measures. In particular, this encompasses the constraints on marginals of the classical optimal transport problem. Furthermore, it can include constraints such as bounds on the distributions as well as expectations of path dependent functions.

One of the outcomes of the duality techniques developed in [4, 25] is that it bypasses the need to establish the dynamic programming principle, as the Hamilton-Jacobi-Bellman equation arises directly from the dual formulation. Our study establishes a natural connection between this optimal transport problem and the recent theory of path dependent partial differential equations (PPDEs) as developed in [7, 8, 11, 13, 14, 30]. We also provide a formalisation of the dimension reduction technique used in numerical methods for BSDEs (see e.g., [16, 37]) and path-dependent stochastic control problems (see e.g., [33]) that reduces the complexity of the PPDE into a more tractable PDE by identifying relevant state variables from the cost function and the constraints. This is achieved via the introduction of semifiltrations, which facilitates measurability results for both the solution of the optimal transport problem as well as the optimal drift and diffusion characteristics.

Recently, optimal transport has found applications in mathematical finance, particularly in the areas of robust hedging. For example, it is used to obtain model-free bounds for exotics derivatives in [21] and robust hedging strategies in [9, 22]. As shown in Remark 3.9, the so-called robust pricing hedging duality in continuous time is also a corollary of our duality results. Connections between optimal transport and stochastic portfolio theory [27] have also been observed. In this paper, we focus on applications to model calibration, which is a crucial problem in financial modelling. The celebrated Dupire’s formula [12] provides a unique way to recover a local volatility model from the knowledge of vanilla options for all strikes and maturities. However, it requires some form of price interpolation as only a finite number of options are available. Moreover, calibration to more sophisticated (path dependent) products cannot be achieved through this method. Beyond this analytical result, there are few theoretical advances that address the problem of calibration. Practitioners therefore often rely on parametric models, which they fine-tune to match observable instruments as much as possible.

The duality theory developed in this paper is used to exactly calibrate to any number of path dependent derivatives, without the need to perform any price interpolation. The idea of using optimal transport to calibrate local volatility models to European options was explored in [19], which is an adaptation of the numerical method of [3]. A similar numerical algorithm for discrete option prices was also studied in [2] in the context of entropy minimisation. In this paper, we extend the approach to the calibration of path dependent derivatives, resulting in a path dependent volatility function, a notion also explored in [20]. Despite the complex path dependent nature of the problem, efficient numerical algorithms are still possible via our dimension reduction result, where the optimal volatility function is Markovian in the state variables driving the derivatives. This is somewhat analogous to the fact that that European option prices can always be calibrated to local volatility models. Our method can also be used to refine stochastic volatility models to exactly match a set of given payoffs, while remaining close to a reference stochastic volatility model. This therefore is a generalisation of the calibration of so-called local-stochastic volatility (LSV) models (see [1, 18] and the references therein). Recently, our duality results have also been used in [17] for the joint calibration of stock and VIX options, which has been an extremely difficulty problem eluding researchers for many years.

The paper is organised as follows. Section 2 introduces the basic notations used throughout the paper as well as the abstract formulation of the problem, including some examples. Section 3 contains the main results and their proofs. A summary of the main results is found in Theorem 3.1. Section 4 includes the application of our results to volatility calibration, demonstrating numerical examples that calibrate to a large number of European, barrier and lookback options.

2 Optimal transport under path dependent constraints

2.1 Preliminaries

Let be the set of continuous paths, be the canonical process and be the canonical filtration generated by . For each , let be the set of paths stopped at time and let . Next, let and be the set of paths that stay at on . The spaces , and are equipped the with the norm , while the spaces and are equipped with the metric . Note that we have the relation . This also induces a natural isomorphism between and the product , as well as their -algebras, .

Given a Polish space equipped with its Borel -algebra, let be the set of continuous functions on , be the set of bounded continuous functions and be the set of signed finite Borel measures on . On , let denote the topology of uniform convergence on compact sets of . Denote by the finest locally convex topology on which agrees with on closed balls of (via the uniform norm). The topology was introduced by Le Cam [24] and is also known as the “mixed topology” [15] or the “substrict topology” [32]. For this paper, we will make use the following key result (see, e.g., [15, 32]).

Proposition 2.1.

The dual of can be identified with .

Remark 2.2.

The choice of topology will allow the applications of our duality argument in non-locally compact settings, and to avoid the issue of being identified with the set of all regular, signed, finite and finitely additive Borel measures ([10] Theorem IV.6.2) under the usual uniform norm topology.

Let denote subset of positive measures. For any , let be the set of -integrable functions. Also let , , and so on be their respective vector valued versions. In this paper, the typical choices of are as well as their various subspaces.

Let be the set of Borel probability measures on . For each , let be a subset of measures such that, for each , is an -semimartingale on given by

where is an -martingale on and is -adapted and -a.s. absolutely continuous with respect to time. In particular, is said to be have characteristics , which are defined by

Note that is -adapted and determined up to , almost everywhere. In general, takes values in the space . Note that and denote the sets of symmetric matrices, positive semidefinite matrices and positive definite matrices, respectively. For any , let us define . Denote by the set of probability measures whose characteristics are -integrable on the interval . In other words,

where denotes the -norm.

Remark 2.3.

One can define for every each path as the quadratic variation of and it would be compatible to every semimartingale measure . However, this choice of is highly pathological. Since, for each , the characteristic is determined up to , it is usually more practical to work with versions of that have more regularity.

For each and any probability measure on , define to be the set of consistent with on .

Furthermore, let and .

The notions of path derivatives and functional Itô calculus were originally introduced in Dupire [11] and Cont and Fournie [8] for càdlàg paths. Here we choose a version of the definition that focuses on the space of continuous paths, as it is more suitable for the study of semimartingale optimal transport. Specifically, we use a slight variation of the definitions found in [7, 13, 14].

Definition 2.4 (Path derivatives and functional Itô formula).

For each , we say if and there exist functions such that, for any and , the following functional Itô formula holds:

The functions are known as the time derivative, first order space derivative and second order space derivative of , respectively.

Remark 2.5.

The definition of in Definition 2.4 is more restrictive than the corresponding version from [13, 14] in the following ways. We require the set to contain all measures with integrable characteristics , as opposed to bounded characteristics. Moreover, we also require the function and its derivatives to be bounded. The path derivatives are unique whenever they exist. We refer to [7, 13, 14] for more discussions on the different definitions of path derivatives, as well as comparisons to the original definitions of [11, 8].

2.2 Problem formulation

Now let us define the semimartingale optimal transport problem under path dependent constraints.

Denote by a cost function. Define so that is the convex conjugate of . When there is no ambiguity, we will simply write and . We impose the following global assumption on .

Assumption 2.6.

(i) For each , is a lower semi-continuous, proper convex function and is uniformly bounded.

(ii) If then .

(iii) The cost function is coercive in the sense that there exist constants and such that

In order to characterise the constraints, let be a convex set of measures. Assume that is closed under the weak-* topology, that is, the coarsest topology under which is continuous for all . In our problem, we would like to restrict the probability measures to the set .

Definition 2.7.

Given and , we define the semimartingale optimal transport problem under path dependent constraints to be the following minimisation problem

The problem is said to be admissible if and the infimum above is finite.

To handle the constraint, consider the convex function defined by

Since is closed, the convex conjugate of has the following representation: for any ,

| (1) |

In many cases, it is possible to further restrict the choice of in the definition of to some convex subset . This occurs whenever the supremum in (1) is always achieved by the elements of , so

| (2) |

For example, if is the subspace of defined by where is a fixed function, then we may choose . More examples can be found in the next subsection. In general, suitable choices of cannot always be easily identified. However, when it is possible, the reduction of to can greatly simplify the problem.

The formulation of in (2) indicates that it is, in fact, a suitable function for the penalisation of measures outside . Hence, the problem can be reformulated as the following saddle point problem:

| (3) |

2.3 Examples

The constraint on measures in our formulation is very general and allows a wide range of problems, including many existing formulations of continuous time optimal transport problems in literature. Here are some examples.

Example 2.8 (Deterministic optimal transport).

If the cost function satisfies

then we recover the classical deterministic optimal transport problem of Benamou-Brenier [3].

Example 2.9 (Semimartingale optimal transport).

Consider the problem on with the initial measure . Let be a probability measure on and consider the time constraint . Then by setting

we recover the semimartingale optimal transport problem studied in [34]. In particular

and the saddle point problem is given by

Furthermore, if the cost function is given by if , and otherwise, then we recover the stochastic optimal control problem in [26]. Alternatively, if the cost function is of the form if , and otherwise, then we recover the martingale optimal transport problem from [23]. Finally, if and if for some constant , and otherwise, then our formulation is equivalent to the one-dimensional case in [35].

Example 2.10.

Further generalising the previous example, let be any continuous function and be a target distribution. We would like to impose the constraint . In this case the constraint is characterised by

and

The saddle point problem is given by

Example 2.11.

Fix and consider the constraint . This corresponds to

In this case,

Then the saddle point problem is given by

Example 2.12.

Let be a function that is lower semi-continuous in each component. Consider the constraint for some , where the inequality is taken element-wise. This corresponds to . One can check that this set is in fact closed under the weak-* topology111Let be a sequence of measures converging to . Let be an increasing sequence of functions converging to . Then by Fatou’s lemma, .. In this case

Using the density of in , the saddle point problem is given by

Via a suitable translation, the condition can be relaxed so that is bounded from below.

3 Main results

3.1 Summary of main results

Theorem 3.1.

Let be a convex subset that is closed with respect to the weak-* topology. Define and by

| (4) |

Let be a function satisfying Assumption 2.6 and let denote the convex conjugates of .

Given and a probability measure on , recall that the semimartingale optimal transport problem with path dependent constraints refers to the following minimisation problem,

| (5) |

(i) Duality: If the problem is admissible, then the infimum in (5) is attained and it equals

| (6) |

where is given by

| (7) | ||||

| subject to |

Let denote the Dirac measure with a singular mass at . Then the function also satisfies

| (8) |

Moreover, if the set can be replaced by a convex subset in (4), then the same replacement can be made in (6).

(ii) Optimal solution: Suppose that is an optimal probability measure for the optimal transport problem and has characteristics on . Let be an optimising sequence of (6) and (7). Then we have the following convergences in probability on :

Moreover, suppose that is strongly convex, i.e., there exists a constant such that for all and any subderivative , if is finite then

where is the norm on and . Then the following holds on ,

(iii) PPDE characterisation: Suppose that Assumptions 2.6 and 3.14 are satisfied. Then has the representation

| (9) |

where is a viscosity solution of the following path dependent PDE:

| (10) |

Moreover, if Assumption 3.16 is also satisfied, then is the unique viscosity solution of the PPDE (10).

(iv) Dimension reduction: Fix and . Suppose that Assumptions 2.6 and 3.14 are satisfied. Let be a semifiltration (see Definition 3.19) such that is adapted to . Then the map defined by

is -measurable.

Moreover, if is a classical solution of the PPDE (10) and is strictly convex in , then is also -measurable.

Remark 3.2.

By dimension reduction, we mean the following. In general, the optimal are path dependent, -adapted processes. For practical applications, this is not very helpful as path dependent functions are difficult to compute in general. However, in many problems, we can show that the solution in fact only depends on a few state variables which can be usually identified from the constraint and the cost function. In essence, is generated by these state variables at time .

For instance, consider Example 2.9 (also found in [34]), where the constraints are on the initial density of and the final density of , while the cost function at time is not path dependent and only depends on . In this case, the optimal at time only depend on . So it suffices to solve a finite dimensional classical PDE, as opposed to an infinite dimensional PPDE.

Consider another example, where the constraint is on the expectation of for some fixed (for financial applications this would correspond to a so-called cliquet or ratchet options), then the optimal would simply depend on for and for .

Remark 3.3.

Theorem 3.1 is a generalisation of many existing continuous time optimal transport results (see the examples in Subsection 2.3). Here we will further highlight some technical differences between our technique and other works.

There are some similarities between our approach and [23], since both works make use of the Fenchel-Rockafellar duality theorem 3.5. In [23] the problem is posed in Markovian settings and restricted to martingales. The duality theorem is applied first to a compact domain, then extended to an unbounded domain via verification arguments. On the other hand, our formulation is in a non-Markovian, semimartingale setting with more general constraints. The lack of local compactness leads to additional technical challenges in the formulation of the underlying topological spaces and the application of the duality result. Unlike [23], we cannot encode our semimartingale condition in the form of a Fokker-Planck equation. Instead, we identify semimartingale measures via the functional Itô formula in the form of Lemma 3.4.

Our work also generalises the results of [34] to non-Markovian constraints. The approach of [34] involves proving the convexity and lower-semicontinuity of the objective function and applying the Fenchel-Moreau theorem on the measure-function duality pairing. The resulting PDE representation is derived via classical measurable selection and dynamic programming arguments. Our approach uses the Fenchel-Rockafellar duality theorem on the function-measure duality pairing and directly obtains the dual problem in terms of path dependent PDEs while bypassing dynamic programming. In fact, our duality result would also implies the dynamic programming principle without needing to invoke measurable selection arguments.

To simplify our notations, the proof of the main duality result will focus on the case . In other words, this corresponds to the class of optimal transport problem starting at time 0 with initial distribution . The general case can be dealt with using similar arguments.

3.2 Characterising suitable measures

The function was used to penalise measures outside of , a constraint of the problem. In this subsection, we aim to find a suitable function that penalises measures outside of , the set of semimartingale measures.

A key step in our argument is to extend measures in to measures on the stopped paths , then to utilise the Fenchel-Rockafellar duality theorem 3.5 (see, e.g., [31]) on that space. The following lemma provides a condition for the identification of measures in as well as a suitable corresponding measure in .

Lemma 3.4.

Let be a probability measure on . Suppose that and induces the measure via

Let and .

The equality

holds for all if and only if and has characteristics .

Proof.

See Appendix. ∎

3.3 Duality

In this subsection, we will prove Theorem 3.1 (i), the main duality result of the paper. In fact, we will prove a slightly stronger statement in Theorem 3.6, which allows to be an arbitrary convex function, rather than one defined using the set .

Recall that, at time , the saddle point problem is given by

The key step is to encode the condition using Lemma 3.4 and reformulate the problem with respect to the measures and ,

Then duality (swapping the infimum and the supremum) is established via the Fenchel-Rockafellar duality theorem 3.5. We will state the version of the theorem found in [31]. Variants of the theorem can also be found in, e.g., the beginning of [5], or Theorem 1.9 in [36].

Theorem 3.5 (Fenchel-Rockafellar).

Let be a locally convex Hausdorff topological vector space over with dual . Let be a proper convex function, be a proper concave function, and , be their respective conjugates. If either or is continuous at some point where both functions are finite, then

Roughly speaking, the duality pairings used in the current context are of the form and , where and . The dual formulation will be characterised using path dependent PDEs (PPDEs).

Theorem 3.6.

Let be a convex function and be a convex set such that . Define the function by222In this set up, unless , is not necessarily the convex conjugate of . Instead, would be the convex conjugate of .

Let satisfy Assumption 2.6 and be the convex conjugate of . Define

| (11) | ||||

| (12) | ||||

| subject to | (13) |

Then . Moreover, if is finite, then the infimum in (11) is attained.

Proof.

For convenience, let us use instead of . Recall that is induced by via . Under Assumption 2.6, it suffices to only consider the set of probability measures in (11).

The direction can be easily shown as follows. Applying Fubini’s theorem and Lemma 3.4, we have

| s.t. . | ||

Now let us focus on the opposite direction, , which is significantly more difficult. The main technical issue is that, in order to use the Fenchel-Rockafellar duality theorem 3.5, we require the effective domain of a particular convex function to have a non-empty interior. This is achieved by introducing two additional slack terms of , in both and . This is similar to the technique in [36], Section 1.3, for the proof of Kantorovich duality in Proposition 1.22.

By the conditions on and , there exists some such that . Throughout the remainder of the proof, let be a fixed constant such that .

For the next part of the proof, introduce the measures via and , so that we can write

where

and the inner product is defined by

Note that both and are convex sets.

Next, define the convex function and its convex conjugate according to Lemma A.1. They are given by the following expressions:

Furthermore define the concave function and its concave conjugate in the following way

Note that we do not need to compute explicitly. Hence can be written as

In order to apply the Fenchel-Rockafellar duality theorem 3.5, we require . Recall that , and . The required condition is fulfilled at . The duality theorem implies that

| s.t. , , |

Translating by yields

| s.t. and . | (14) |

In order to eliminate in (14), we will use the fact that one can arbitrarily modified the time derivative of a path dependent function without altering the space derivatives (see Remark 3.8). For each satisfying (14), we can construct via

It is straightforward to check that

Therefore

| s.t. and | |||

Thus we may conclude . The fact that the infimum in (11) is attained if is a direct consequence of the Fenchel-Rockafellar duality theorem 3.5. This completes the proof of Theorem 3.6. ∎

Corollary 3.7.

The analogous result for time is given below.

| (15) |

Remark 3.8.

By adding to any function in , it is possible to change the time derivative by an arbitrary function without altering the space derivatives. This is a useful yet peculiar property of path dependent derivatives and it is somewhat counter-intuitive when compared to conventional differentiable functions. By applying this idea and increasing appropriately, we can replace the inequality in the PPDE by an equality. However, the inequality in the terminal condition remains.

Remark 3.9.

Theorem 3.6 provides a slightly more general set up than Theorem 3.1 (i), due to the additional flexibility in . Beyond the examples in Subsection 2.3, this allows for an even wider range of applications, e.g., the inclusion of a terminal objective function in the primal problem. A noteworthy example is the application to the robust hedging of path dependent options in continuous time settings (see, e.g., [9, 22]). As shown below, Theorem 3.6 immediately implies the so-called robust pricing hedging duality.

Consider the problem of robust hedging a European payoff with respect to a set of models which are represented by the martingale measures whose diffusion characteristic is bounded lines in some compact and convex set . Suppose there are additional model constraints in the form of European payoffs with the known price of 0. Let us set , , and if or otherwise. Then the robust model price is equal to the primal problem,

The dual formulation is given by

| (16) |

By the functional Itô formula, for each satisfying (16), the following inequality holds -a.s. for every candidate model ,

Hence the trading strategy with a starting cost of , holding a dynamic portfolio in and a static position in , is a superhedging strategy for . Since this is true for all satisfying (16), the dual value must be an upper bound for the superhedging price, which is easily shown to be at least the robust model price. By Theorem 3.6, we must have equality between the robust model price and the superhedging price.

To complete the proof of Theorem 3.1 (i), we need to express the solution of the path dependent optimal transport problem in terms of the function , which reaffirms the link between optimal control problems and PPDEs.

Proposition 3.10.

Fix . Define by

| (17) |

(i) Then can be written as

(ii) The function also satisfies

Proof.

(i) This is an immediate consequence of Theorem 3.6 after setting and .

(ii) Define the set

From part (i), we immediately have

For the other direction, for any , let us disintegrate with respect to the map . Hence there exists a -a.s.unique map such that, for all ,

Recall that is an -semimartingale with characteristics . Then it follows that, -a.s., is an -semimartingale also with characteristics . Hence

Since this holds for any , by definition of , we obtain the required result. ∎

Remark 3.11.

The argument used in Proposition 3.10 can be extended to obtain the well-known dynamic programming principle for . To briefly outline the argument, for any stopping time , we have the following chain of inequalities,

where the first inequality follows from the disintegration argument of Proposition 3.10 (ii), the middle equality follows from the duality result of Proposition 3.10 (i), and the final inequality follows from the functional Itô formula and the PPDE. Applying the duality result again implies there must be equality throughout.

3.4 Optimal probability measure

If the optimum of the dual problem is attained, we can characterise the optimal probability measure using Theorem 3.1 (ii), which is restated as Proposition 3.12 below.

Proposition 3.12.

Let be an optimal probability measure for the optimal transport problem, with characteristics on . Let be an optimising sequence of (6) and (7). Then we have the following convergences in probability on :

| (18) |

Moreover, suppose that is strongly convex, i.e., there exists a constant such that for all and any subderivative , if is finite then

where is the norm on and . Then the following holds on ,

Proof.

For each , we have the following inequality for all large enough

Applying the functional Itô formula and rearranging, this yields

| (19) | |||

By Fenchel’s inequality, as well as the conditions,

| (20) |

each of the four terms in (19) (in particular, terms inside the expectations and integrals) are non-negative. Hence they must all be bounded by , which implies the required convergences (18), as well as

| (21) |

If is strongly convex333Note that our definition of strongly convex does not require to be differentiable, since only subderivatives are used. Nevertheless, it implies that is strictly convex and thus is differentiable, then is differentiable and we can define such that

Hence, by the definition of convex conjugate and the strong convexity of ,

| (22) |

Combining (21) and (22) implies that in , completing the proof. ∎

Remark 3.13.

If the optimum of the dual problem is obtained by a pair , then all convergence results in Proposition 3.12 can be replaced by equalities.

3.5 Path dependent PDE

For this subsection as well as the next, we impose additional assumptions on and , which is required for the well-posedness of the PPDE.

Assumption 3.14.

(i) For each , is -progressively measurable.

(ii) The effective domain of is given by

, where is compact. In other words, for all , if and only if .

(iii) Furthermore, is bounded and uniformly continuous within its effective domain.

(iv) The function is bounded and uniformly continuous and has a common modulus of continuity with .

Remark 3.15.

Assumptions 2.6 and 3.14 have the following implications on :

(a) For fixed , is -progressively measurable and is bounded;

(b) is uniformly elliptic, i.e., there exists a constant such that for any ;

(c) is uniformly Lipschitz continuous in ;

(d) is uniformly continuous in .

Condition (a) is satisfied since is progressively measurable and can be written as the supremum of a countable family of progressively measurable functions. Also note that is bounded. For (b), is indeed uniformly elliptic since is finite only if the eigenvalues of are uniformly bounded below by a positive constant. For (c), since the effective domain of is a bounded set , must also be bounded. Finally, (d) holds because is uniformly continuous on .

In order to obtain the uniqueness of viscosity solutions, we require an additional technical assumption (see [14], Assumption 3.5). For all , and , denote

For all , let denote the linear interpolation of

Assumption 3.16.

There exists such that the following holds for each . For any , and , the functions and are uniformly continuous in .

Now we will present Proposition 3.1 (iii), which is restated here.

Proposition 3.17.

Proof.

Following Proposition 3.10, it suffices to show that the solution the control problem

is a viscosity solution of the PPDE (24). This can be proven by following the same argument of [13], Proposition 4.7, which is an adaptation of the standard argument for deriving HJB equations in the PPDE settings. If Assumption 3.16 also holds, then we have the full comparison principle for the PPDE (24) and must be the unique viscosity solution (see [14], Theorem 4.1). ∎

Remark 3.18.

As mentioned in [14] Section 8.3, Assumption 3.16 is a technical assumption only used for the construction of a family of viscosity solutions to an approximating family of path-frozen PDEs. It is likely that in control problems such as the one in Proposition 3.17, one can directly construct the required family of viscosity solutions via a sequence of approximating control problems and their HJB equations, without the need for Assumption 3.16.

Another approach would be to utilise the comparison principle result of [30], which requires a different metric on in the definition of uniform continuity. It also does not require Assumption 3.16. We will defer these potential approaches to future research, and refer the interested readers to [13, 14, 30] for detailed discussions of viscosity solutions to fully nonlinear PPDEs and various versions of regularity assumptions.

3.6 Dimension reduction

One particular interesting case is when is a Dirac measure, i.e., . Then

| (25) | |||

| (26) |

For , let us use the shorthand .

In general, only depends on the path up to time and can be shown to be -measurable. But in all practical examples, both the payoff function and the cost function only depend on certain features of the path rather than the entire path, and can often be parametrised by a finite number of state variables. Intuitively, the solution should be Markovian with respect to in terms of those state variables. This is useful in practice since it allows us to identify the state variables driving the relevant features of the path, and reduces an infinite dimensional PPDE to a finite dimensional PDE.

This idea of dimension reduction is well-known in numerical methods for BSDEs (see e.g., [16, 37]) and path-dependent stochastic control problems (see e.g., [33]). The usual approach is to identify an “updating function” [6] or equivalent which updates the state variables according the evolution of the paths. In this paper, we will formalise this notion in a slightly different approach. Here, we introduce a so-called “semifiltration”, which is an appropriate class of -algebra smaller than that captures the information required for the solution. Typically, this can simply be the -algebras generated by the state variables, but our construction also allows for more general cases. Moreover, as shown in Remark 3.22, our approach enables the explicit construction of the “minimal” semifiltration for an arbitrary problem.

Definition 3.19 (Semifiltration).

(i) A collection of -algebras is called a semifiltration if the following properties hold:

-

•

for every , ;

-

•

for all , , where is a -algebra defined by

(ii) A pair of functions is said to be adapted to a semifiltration if is -measurable and for every , is -measurable.

In general, a semifiltration is not a filtration. It has the following interpretation. As we move forward in time, collects more information about the canonical process , in the same way that does. At the same time, is also allowed to “forget” information, which occurs whenever the inclusion is strict. Moreover, is not allowed to “recall” information once it is “forgotten”.

For the numerical implementation of many practical problems, has the advantage of being much smaller than . For example, if the problem is known to be Markovian, then it suffices to keep track of the current value of the state variable , as opposed to the history of the entire path . Ideally, we would choose to be as small as possible, while still retaining all dependent variables required for the solution.

The condition can be interpreted as a time consistency condition on semifiltrations. Given and all possible information on the time period , we have enough to construct . This notion is formalised in the following crucial lemma.

Lemma 3.20.

Let be a semifiltration and be Polish spaces. Fix and consider a function that is -measurable. Define the map via

Then is -measurable.

Proof.

Note that the space is endowed with the supremum norm and the associated Borel -algebra.

For any open ball with centre and radius , we have to check that . Due to the separability of , we can write

| (27) |

where is a countable dense subset of , the map is defined by

and is an open ball with centre and radius . By (27), it suffices to check that for all .

Now since , by taking the -section of this set, we have . Then we have the following implications

| (28) | ||||

| (29) |

The last implication relies on the fact that there is a natural isomorphism

where is a -algebra on . Since does not depend on the path after time , (29) is obtained by sectioning (28) by . Since (29) is equivalent to , this completes the proof. ∎

Proposition 3.21.

Proof.

(i) First note that, since is bounded, continuous and adapted to , the map where is bounded, continuous and measurable. Hence by Lemma 3.20, the map defined by

is -measurable.

After a suitable translation can be written as

Hence can be written as the composition

We have already established that is -measurable. The second map is continuous, since both and are Lipschitz continuous functionals. Therefore is -measurable.

(ii) First, the -measurability of follows immediately from Proposition 3.17. By the functional Itô formula, for

| (30) |

holds for all . Consider the probability whose characteristics is constant on . Then the infinitesimal generator of is given by

| (31) |

By Lemma 3.20 and Proposition 3.21 (i), the left hand side of (31), as a function of , is -measurable. Since (31) holds for all , must also be -measurable. Finally, being strictly convex on implies that is continuous. Thus is also -measurable. ∎

Remark 3.22.

In fact, there exists a “minimal” semifiltration to which is adapted. For each , we can define a -algebra , where is the map defined by,

From the proof of Proposition 3.21, we have seen that for every semifiltration to which is adapted. So it suffices to show that is indeed a semifiltration. This reduces to checking that is -measurable for , which follows from the continuity of the map .

4 Volatility calibration

The results of this paper can be applied to the problem of calibrating a volatility model to complex path dependent derivatives. Without loss of generality, let us assume that the interest rate is 0. Suppose that some derivative prices are known, the goal is to find a martingale diffusion for the underlying asset which attains those prices. As far as the authors are aware of, exact calibration techniques are only available on vanilla products (European options). The path dependent nature of the results presented allows us to include path dependent products such as Asian options, barrier options and lookback options.

Let the canonical process be the logarithm of the underlying stock price. Note that the logarithm transform is purely chosen for notational and numerical convenience, and is not at all necessary. We are interested in finding a probability measure with characteristics where is some -adapted process. In other words, we want to be an -semimartingale in the form of

Next let denote a vector of (path dependent) discounted option payoff functions. We further restrict so that the options have known prices for some . It is immediate that this problem is a special case of the general problem we introduced in Section 2, specifically in Example 2.11. In particular, we want to solve

where is any suitable convex cost function whose effective domain is within the set . In the examples of this Section, we consider a cost function of the form

where is some reference volatility level, are constants greater than 1, and are constants chosen so that the function reaches its minimum at with . The basic idea is to keep positive and penalise any large deviations from .444The results from Sections 3.6 and 3.5 required the cost function to have a compact effective domain, this can be achieved by truncating at extreme values of and setting to infinity outside of these values.

As mentioned in Example 2.11, the corresponding saddle point problem is

Applying Theorem 3.1 and assuming sufficient regularity on the payoff functions, the dual formulation of the problem is

| (32) |

where is a solution to the PPDE

| (33) |

Numerically, the difficult part is to solve the PPDE (33) to find . The key idea is to use Theorem 3.1 (iv) to effectively reduce the dimensionality of to a manageable size. For many examples, instead of being dependent on the whole path of , the solution is in fact Markovian with respect to a few state variables. The general abstract result is described in Definition 3.21. But for most practical cases, it is straightforward to identify the relevant state variables by inspection and they are the familiar variable from standard option pricing techniques. Here are some examples of relevant state variables:

-

•

European options: the spot price ;

-

•

Asian options: the spot price and the running average ;

-

•

Continuous barrier options: the spot price and the indicator variable for lower barriers or for upper barriers;

-

•

Lookback options: the spot price and either the running minimum or running maximum .

In each case, the relevant semifiltration at time is the -algebra generated by each set of state variables at time . Then the PPDE reduces to a PDE which depends on the spot price as well as an additional path dependent variable and can be solved via conventional methods.

The supremum in (32) over is computed by a standard optimisation routine. This process can be further aided by numerically computing the gradient of the objective with respect to in the following way. From (33), is also a function a via the terminal condition. Writing and differentiating the PPDE with respect to , we obtain

| (34) |

where . Hence the gradient of the objective function is given by where satisfies and (34). Once the optimal and have been found, the optimal volatility is given by where .

Remark 4.1.

(i) The gradient of the objective function with respect to has a natural financial interpretation. Since where has characteristics , the gradient is in fact , or the difference between the option prices given by the current optimisation iteration and the target option prices. The optimum is reached when that difference is zero, in other words, the target option prices are attained exactly.

(ii) Recall that in our original formulation, is required to be a bounded and uniformly continuous function. In practice, many options do not have bounded payoffs (e.g., call options). This can be fixed by either converting them into options with bounded payoffs via arbitrage arguments (e.g., put options via put-call parity), or by truncating the domain at some extremely large value. Option that do not have continuous payoffs (e.g., digital options, barrier options) can be approximated by uniformly continuous functions.

(iii) By increasing the dimension of the canonical process to include other features such as the variance process, the same technique can be used to calibrate local stochastic volatility (LSV) models. See [18] for more details.

(iv) Based on the result of this paper, similar methods have been developed for the calibration of LSV models [18] and the joint calibration of stock and VIX options [17].

(v) Our results here are limited to non-callable products, hence excluding the calibration of Bermudan and American options. Callable products involve incorporating stopping times into the duality spaces, which requires additional techniques beyond the scope of the current work. This problem is under current research and will be addressed in a forthcoming paper.

In the following subsections, we will demonstrate a few numerical examples that involve calibrating volatility functions to European, Barrier and Lookback options. Since each of the payoff functions considered satisfies Assumption 3.16 (see also, [14] Lemma 3.6), the corresponding PPDE (33) has a unique viscosity solution. For the the convergence of the numerical schemes for viscosity solutions to PPDEs, we refer to [29, 38].

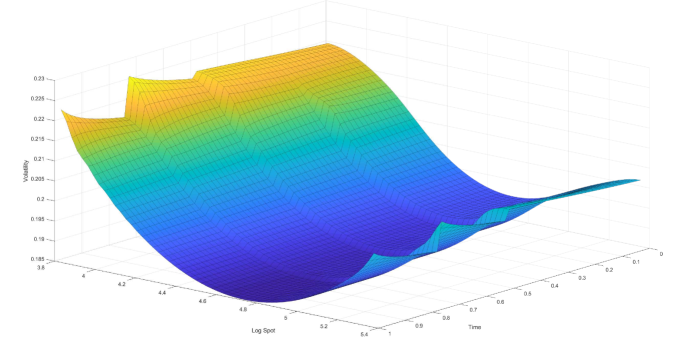

4.1 European options

European options have payoff functions of the form where each option depends on the value of the underlying at a fixed maturity . In this case, the function and the optimal volatility only depend on the state variable and . In other words, we recover a local volatility model. This is consistent with classical approaches such as Dupire’s formula [12]. In some sense, local volatility models are the “simplest” models that can calibrate to all European products. Unlike Dupire’s formula, our approach does not require the interpolation of option prices between discrete strikes and maturities. The functional derivatives in the PPDE simply reduces to the usual partial derivatives,

| (35) |

Figure 1 shows an example of a volatility calibrated to European options at all strikes and four different maturities.

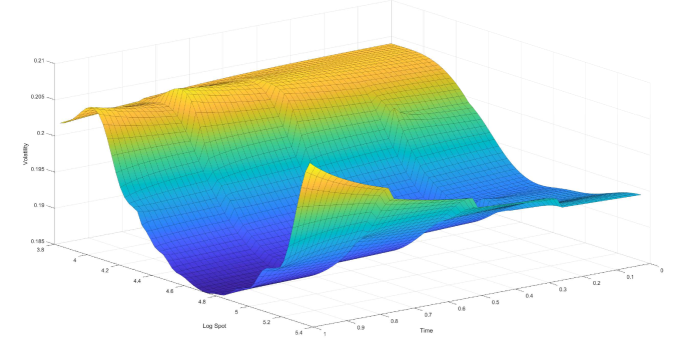

4.2 Barrier options

Formally speaking, a barrier is a closed subset whose complement is a connected region containing . The payoff of a barrier product expiring at time is a function of and the indicator variable , checking whether the path of the underlying has hit the barrier. When calibrating to a collection of barrier products with a single fixed barrier, the required state variables are and . Then the function can be effectively split into two functions, and , corresponding to the cases and , respectively. The PDE is then given by

Similarly, the optimal volatility will be switching between two local volatilities and , conditional to whether the underlying has hit or not. The PDE for will be used to compute the volatility function prior to the stock hitting the barrier, while the PDE for will be used to compute the volatility function after the barrier has been hit.

If we calibrate to options with distinct barriers, then a similar approach applies but with indicator variables. In this case and will be split into functions, conditioning on the subset of the barriers that has been reached. The number can be reduced in many cases by eliminating combinations of barrier events are not reachable. For example, if the barriers are nested, then only functions are needed.

As an example, let us consider barrier products with respect to a continuous lower barrier where is a constant. In particular, we will be calibrating to all down-and-in and down-and-out puts at all strikes and four different maturities. The top half of Figure 2 shows the calibrated volatility function (before hitting the barrier) and the bottom half shows (after hitting the barrier). Even though is only defined for , for the purpose of visualisation, we set for .

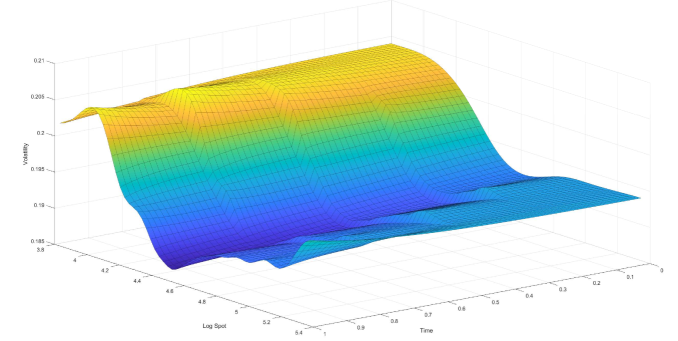

4.3 Lookback options

The payoff of lookback products expiring at time depends on as well as either or . Here we will focus on cases involving the minimum . For example, the payoff of a fixed strike lookback put with strike is given by . In this case, the state variables for and will be and . Note that European options and barrier options with lower barriers are also special cases of lookback products. The PDE is then given by

| (36) | ||||

| (37) |

The boundary condition (37) can be obtained in the following way. First, via standard arguments using the dynamic programming principle, and the fact that has finite variation, we derive the following equation

Then, by using the argument from [28] Proposition 8.5., the required boundary condition (37) follows from the fact that and are mutually singular.

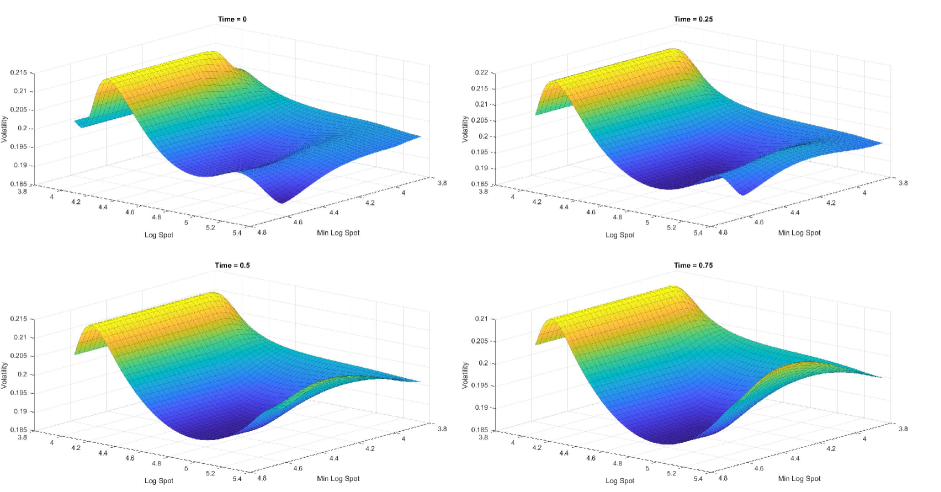

In Figure 3, we show the resulting volatility function calibrated to European puts, all lower barrier down-and-out puts and fixed strike lookback puts at all strikes and four different maturities. The top half of the figure shows cross sections at different values of while the bottom half shows cross sections at different values of . Even though is only defined for , for the purpose of visualisation, we set for .

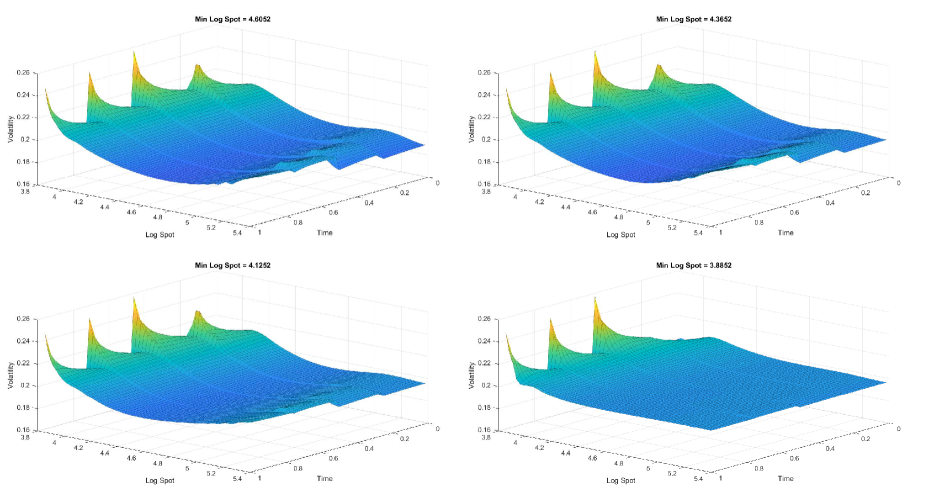

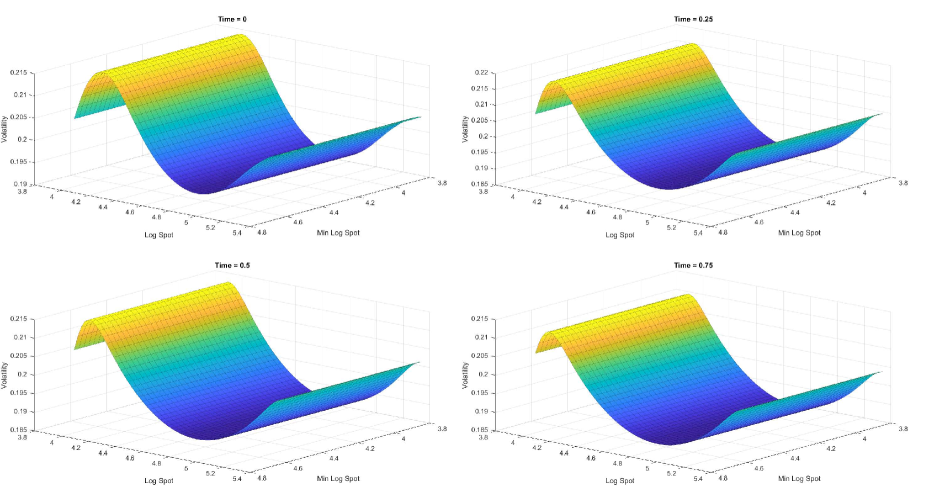

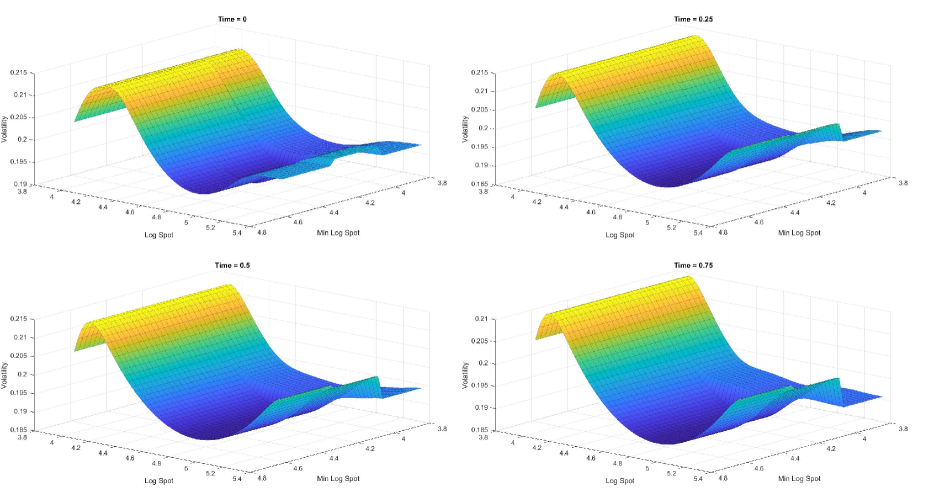

To further demonstrate the effect of dimension reduction, we repeat the same computation but removing some of the options. In the first test, we only calibrate to European options, while in the second test we calibrate to European options and barrier options at two different barriers . The results are shown in Figure 4. When only European options are used, only depends on but not . In the cases where some barrier options are added, the dependence of on can be divided into three regions, , and , corresponding to the number of barriers the underlying has hit. This behaviour is consistent with our dimension reduction results.

Appendix A Appendix

A.1 Proof of Lemma 3.4

Proof of Lemma 3.4.

The “if” direction follows immediately from the functional Itô formula, so we will focus only on the “only if” direction. First note that we can translate by any without altering the right hand side. This yields

for all . Therefore is a probability measure with .

Let be any function. Consider Then we have and . Applying Fubini’s theorem, we obtain Since is an arbitrary continuous function on , this implies that and we can rewrite our condition as

| (38) |

Fix and let be a sequence of increasing functions with for and for . Define the function by and let be a sequence of positive, bounded functions with uniformly bounded derivatives such that for . Set

It is clear that . Then the integral of can be bounded by

which converges to 1 as . The space derivatives of are uniformly bounded. Using Fatou’s lemma and the integrability of , we have

hence is -integrable for all .

Next, fix and let be a sequence of bounded functions with uniformly bounded derivatives satisfying for . Let be an arbitrary function and consider

Using arguments similar to before, . Furthermore, the space derivatives of are uniformly bounded and

By the integrability of and as well as the dominated convergence theorem, as ,

Recall that is arbitrary, which implies

Since this holds for all , and are integrable, must be a continuous -martingale.

Applying the functional Ito’s formula, our condition reduces to

Fix , let and consider

where and are defined as before. Once again, . In particular, takes value in , is uniformly bounded and satisfies

By the integrability of , Fatou’s lemma and the dominated convergence theorem, we have

Thus and we may apply the dominated convergence theorem again to change the first inequality to an equality, which yields

for all . Since is a martingale with , we must have

and so is an -martingale. Therefore must be a semimartingale measure with characteristics , completing the proof. ∎

A.2 Lemma A.1

Lemma A.1.

Define by

Its convex conjugate is given by

where

Proof.

Throughout the proof, we will use the fact that is dense in with respect to the topology. Let us identify the cases where . Using the definition of convex conjugates, we have

If , then , , and . To see why one can restrict to , suppose for some measurable set . Then there exists a sequence of non-positive functions that converge to in . By scaling arbitrarily and adding them to , the function becomes unbounded. A similar argument shows that . So our function reduces to

Next, since the function is linear in , if is finite, then the supremum must occur at the boundary

We claim that it is necessary to have . Suppose that there exists a measurable set such that but . Once again let us construct a sequence of continuous function in converging to in and add multiples of it (depending on the sign of ) to , which would allow to grow arbitrarily. Thus, we may write and bound in the following way,

Note that we have used the lower-semicontinuity of . Equality can be shown by choosing to be a sequence of continuous functions converging to , then applying the dominated convergence theorem and the fact that is continuous in .

Finally, we see that the conditions , , , and are necessary for . Therefore, the claim is proven. ∎

References

- [1] Abergel, F., and Tachet, R. A nonlinear partial integro-differential equation from mathematical finance. Discrete Contin. Dyn. Syst. 27, 3 (2010), 907–917.

- [2] Avellaneda, M., Friedman, C., Holmes, R., and Samperi, D. Calibrating volatility surfaces via relative-entropy minimization. Applied Mathematical Finance 4, 1 (1997), 37–64.

- [3] Benamou, J.-D., and Brenier, Y. A computational fluid mechanics solution to the Monge-Kantorovich mass transfer problem. Numerische Mathematik 84, 3 (2000), 375–393.

- [4] Brenier, Y. Minimal geodesics on groups of volume-preserving maps and generalized solutions of the Euler equations. Comm. Pure Appl. Math. 52, 4 (1999), 411–452.

- [5] Brézis, H. Analyse fonctionnelle, théorie et applications,(1983), 1983.

- [6] Brunick, G., Shreve, S., et al. Mimicking an Itô process by a solution of a stochastic differential equation. The Annals of Applied Probability 23, 4 (2013), 1584–1628.

- [7] Buckdahn, R., Ma, J., and Zhang, J. Pathwise Taylor expansions for random fields on multiple dimensional paths. Stochastic Processes and their Applications 125, 7 (2015), 2820–2855.

- [8] Cont, R., Fournié, D.-A., et al. Functional Itô calculus and stochastic integral representation of martingales. The Annals of Probability 41, 1 (2013), 109–133.

- [9] Dolinsky, Y., and Soner, H. M. Martingale optimal transport and robust hedging in continuous time. Probability Theory and Related Fields 160, 1-2 (2014), 391–427.

- [10] Dunford, N., and Schwartz, J. T. Linear operators part I: general theory, vol. 7. Interscience publishers New York, 1958.

- [11] Dupire, B. Functional Itô calculus. papers.ssrn.com (2009).

- [12] Dupire, B., et al. Pricing with a smile. Risk 7, 1 (1994), 18–20.

- [13] Ekren, I., Touzi, N., Zhang, J., et al. Viscosity solutions of fully nonlinear parabolic path dependent PDEs: Part I. The Annals of Probability 44, 2 (2016), 1212–1253.

- [14] Ekren, I., Touzi, N., Zhang, J., et al. Viscosity solutions of fully nonlinear parabolic path dependent PDEs: Part II. The Annals of Probability 44, 4 (2016), 2507–2553.

- [15] Fremlin, D., Garling, D., and Haydon, R. Bounded measures on topological spaces. Proceedings of the London Mathematical Society 3, 1 (1972), 115–136.

- [16] Gobet, E., Lemor, J.-P., Warin, X., et al. A regression-based Monte Carlo method to solve backward stochastic differential equations. The Annals of Applied Probability 15, 3 (2005), 2172–2202.

- [17] Guo, I., Loeper, G., Obloj, J., and Wang, S. Joint modelling and calibration of spx and vix by optimal transport. arXiv preprint arXiv:2004.02198 (2020).

- [18] Guo, I., Loeper, G., and Wang, S. Calibration of local-stochastic volatility models by optimal transport. arXiv preprint (2019).

- [19] Guo, I., Loeper, G., and Wang, S. Local volatility calibration by optimal transport. In 2017 MATRIX Annals. Springer, 2019, pp. 51–64.

- [20] Guyon, J. Path-dependent volatility. https://ssrn.com/abstract=2425048 (2014).

- [21] Henry-Labordère, P., and Touzi, N. An explicit martingale version of the one-dimensional Brenier theorem. Finance Stoch. 20, 3 (2016), 635–668.

- [22] Hou, Z., and Obłój, J. Robust pricing–hedging dualities in continuous time. Finance and Stochastics 22, 3 (2018), 511–567.

- [23] Huesmann, M., Trevisan, D., et al. A benamou–brenier formulation of martingale optimal transport. Bernoulli 25, 4A (2019), 2729–2757.

- [24] LeCam, L. Convergence in distribution of stochastic processes. Univ. California Publ. Statist 2 (1957), 207–236.

- [25] Loeper, G. The reconstruction problem for the Euler-Poisson system in cosmology. Archive for rational mechanics and analysis 179, 2 (2006), 153–216.

- [26] Mikami, T., and Thieullen, M. Duality theorem for the stochastic optimal control problem. Stochastic processes and their applications 116, 12 (2006), 1815–1835.

- [27] Pal, S., Wong, T.-K. L., et al. Exponentially concave functions and a new information geometry. The Annals of Probability 46, 2 (2018), 1070–1113.

- [28] Privault, N. Stochastic finance: an introduction with market examples. Chapman and Hall/CRC, 2013.

- [29] Ren, Z., and Tan, X. On the convergence of monotone schemes for path-dependent PDEs. Stochastic Processes and their Applications 127, 6 (2017), 1738–1762.

- [30] Ren, Z., Touzi, N., and Zhang, J. Comparison of viscosity solutions of fully nonlinear degenerate parabolic path-dependent PDEs. SIAM Journal on Mathematical Analysis 49, 5 (2017), 4093–4116.

- [31] Rockafellar, R. T., et al. Extension of Fenchel duality theorem for convex functions. Duke mathematical journal 33, 1 (1966), 81–89.

- [32] Sentilles, F. D. Bounded continuous functions on a completely regular space. Transactions of the American Mathematical Society 168 (1972), 311–336.

- [33] Tan, X., et al. Discrete-time probabilistic approximation of path-dependent stochastic control problems. The Annals of Applied Probability 24, 5 (2014), 1803–1834.

- [34] Tan, X., Touzi, N., et al. Optimal transportation under controlled stochastic dynamics. The annals of probability 41, 5 (2013), 3201–3240.

- [35] Veraguas, J. B., Beiglböck, M., Huesmann, M., and Källblad, S. Martingale Benamou–Brenier: a probabilistic perspective. arXiv preprint arXiv:1708.04869 (2017).

- [36] Villani, C. Topics in optimal transportation. No. 58. American Mathematical Soc., 2003.

- [37] Zhang, J., et al. A numerical scheme for BSDEs. The annals of applied probability 14, 1 (2004), 459–488.

- [38] Zhang, J., and Zhuo, J. Monotone schemes for fully nonlinear parabolic path dependent PDEs. Journal of Financial Engineering 1, 01 (2014), 1450005.