On the estimation of the Lorenz curve

under complex sampling designs

Pier Luigi Conti111Pier Luigi Conti. Dipartimento di Scienze Statistiche; Sapienza Università di Roma; P.le A. Moro, 5; 00185 Roma; Italy. E-mail pierluigi.conti@uniroma1.it

Alberto Di Iorio222Alberto Di Iorio. Dipartimento di Scienze Statistiche; Sapienza Università di Roma; P.le A. Moro, 5; 00185 Roma; Italy. E-mail alberto.diiorio@uniroma1.it

Alessio Guandalini333Alessio Guandalini. ISTAT, Via Cesare Balbo, 16; 00184 Roma; Italy. E-mail alessio.guandalini@istat.com

Daniela Marella444Daniela Marella. Dipartimento di Scienze della Formazione, Università Roma Tre, via del Castro Pretorio 20; 00185 Roma; Italy. E-mail daniela.marella@uniroma3.it

Paola Vicard555Paola Vicard. Dipartimento di Economia, Università Roma Tre, Via Silvio D’Amico, 77; 00145 Roma; Italy. E-mail paola.vicard@uniroma3.it

Vincenzina Vitale666Vincenzina Vitale. Dipartimento di Economia, Università Roma Tre, Via Silvio D’Amico, 77; 00145 Roma; Italy. E-mail vincenzina.vitale@uniroma3.it

Abstract

This paper focuses on the estimation of the concentration curve of a finite population, when data are collected according to a complex sampling design with different inclusion probabilities. A (design-based) Hájek type estimator for the Lorenz curve is proposed, and its asymptotic properties are studied. Then, a resampling scheme able to approximate the asymptotic law of the Lorenz curve estimator is constructed. Applications are given to the construction of a confidence band for the Lorenz curve, confidence intervals for the Gini concentration ratio, and a test for Lorenz dominance. The merits of the proposed resampling procedure are evaluated through a simulation study.

Keywords. Concentration, resampling, bootstrap, finite population, superpopulation.

1 Introduction

The analysis of income data is fundamental in both theoretical and applied research. In particular, a crucial role is played by the Lorenz curve, that essentially consists in plotting cumulative income shares against cumulative population shares. The Lorenz curve is a basic tool to construct inequality measures, including the popular Gini coefficient. Furthermore, the comparison of wealth and earnings distributions is a fundamental part of income, wealth, and poverty studies, as well as an important tool for public economics.

This justifies statistical inference for Lorenz curve and related quantities. In the literature, since the paper by [Gastwirth(1972)], several papers have been devoted to the subject. Good reviews are in [Giorgi(1999)], [Giorgi and Gigliarano(2017)]; cfr. also [Csörgő et al.(1986)], [Zheng(2002)], [Bhattacharya(2007)], [Davidson(2009)].

A basic condition common to many papers is that sampling observations are independent and identically distributed. Unfortunately, this condition is hardly ever met in practice (cfr. [Giorgi(1999)], [Zheng(2002)]).

The estimation of inequality measures (mainly Gini’s index), when data are collected according to a variable probability sampling design from a finite population, is widely studied in the literature: cfr. [Langel and Tillé(2013)], [Barabesi et al.(2016)], and references therein. However, the same is not true with regard to the estimation of the whole Lorenz curve. In [Zheng(2002)], the asymptotic law of the sample Lorenz curve (computed at a finite number of points) is obtained under stratified, cluster and multi-stage sampling plans; the sampling fractions within strata are assumed “small”, so that the finite population correction term is essentially negligible. This is equivalent, of course, to assume that sampling within strata is simple with replacement, so that sample data are essentially i.i.d.. A step forward is in a couple of papers by Bhattacharya (cfr. [Bhattacharya(2005)], [Bhattacharya(2007)]), where asymptotic results for whole Lorenz curve (estimated via the generalized moment method), under a multi-stage sample design, are obtained. At each stage, units (either primary or secondary) are drawn by simple random sampling with replacement. As a consequence, sample data are independent, although not necessarily identically distributed.

Although the above mentioned papers are of the highest importance, the considered sampling designs do not cover several real cases. For instance, in Italy reliable income and wealth data come from the Survey on Household Income and Wealth (SHIW), conducted by Banca d’Italia (the Italian central bank) every two years. The sampling design is two-stage, with municipalities and households as primary and secondary sampling units, respectively. Primary units are stratified by administrative region and population size (less than 20,000 inhabitants; in between 20,000 and 40,000; 40,000 or more). Within each stratum, primary units are selected to include all municipalities with a population of 40,000 inhabitants or more; smaller municipalities are selected by using inclusion probability proportional to size sampling (without replacement). Individual households are then randomly selected, via simple random sampling without replacement, from administrative registers. Similar considerations hold for the EU-SILC (Statistics on Income and Living Conditions) survey.

Generally speaking, the sampling design can be dropped whenever the sampling design is ignorable; cfr. [Pfeffermann(1993)] and references therein. In general, a sampling design is ignorable provided that two conditions are met:

-

Ig 1.

the sampling design is non-informative, i.e. the probability of drawing a sample only depends on the values of design variables, but not on the variable of interest;

-

Ig 2.

the values of the design variables are known for all population units.

Now, condition Ig 1 is usually satisfied, whilst condition Ig 2 is not, at least for final users of data produced by Official Statistics, since micro-data are usually released together with sampling weights (i.e. reciprocals of inclusion probabilities) for sample units only. For instance, this is exactly what happens in SHIW and EU-SILC. Ignoring the sample design when it is not ignorable can produce severely biased inference; cfr. the illuminating remarks in [Pfeffermann(1993)].

In the present paper, in view of their importance in applications, we focus on sampling designs with first inclusion probabilities proportional to a size measure (ps designs). Furthermore, the primary interest is in making inference on the Lorenz curve at a “superpopulation level”. The results are of asymptotic nature, with both the population and the sample size increasing. They can be viewed as an extension of results on the Lorenz curve estimation that are valid in case of i.i.d. data.

The paper is organized as follows. In Section 2 the problem is described, and the main assumptions are listed. In Section 3, the main asymptotic results are provided. Section 4 is devoted to defining the multinomial resampling scheme, and to establish its properties. Section 5 is devoted to the construction of a confidence band for the Lorenz curve. Section 6 focuses on statistical inference for Gini concentration index, and Section 7 on the construction of a test for Lorenz dominance. Finally, in Section 8 a simulation study is performed.

2 The problem

2.1 Superpopulation model

Let be a finite population of size . If denotes a non-negative character of interest, let be the value of character for unit (). Each value is assumed to be a realization of a random variable (r.v.) ; the -variate r.v. is the superpopulation.

In the sequel, the r.v.s are assumed to be independent and identically distributed (i.i.d.), and their distribution function (d.f.) is denoted by

| (1) |

The superpopulation quantile of order , with , is defined as

| (2) |

The superpopulation generalized Lorenz curve is obtained by integrating the quantile function . In symbols

| (3) |

The curve is continuous, increasing, convex, with and

| (4) |

the superpopulation mean.

The superpopulation Lorenz curve is the normalized version of , namely

| (5) |

Of course, is convex, continuous, increasing, with , .

In the sequel, attention is devoted to the estimation of . Due to the effect of the sampling design, even if the r.v.s s are i.i.d. at a (super)population level, they are not i.i.d. at a sample level (except very special cases); cfr. [Pfeffermann(1993)].

Alongside -, one may define the corresponding finite population counterparts. The finite population distribution function (p.d.f., for short) is defined as

| (6) |

where

Clearly, is the expectation of w.r.t. the superpopulation probability distribution: .

The finite population quantile of order is

| (7) |

Next, the finite population generalized Lorenz curve is defined as

| (8) |

Clearly, is continuous, increasing, and convex, with and

| (9) |

being the finite population mean.

The Lorenz curve, in its turn, is the normalized version of , namely

| (10) |

Of course, is increasing, continuous, convex, with , .

As already said, our main interest is in estimating the Lorenz curve at a superpopulation level. However, the estimation of - will play an important, although indirect, role.

2.2 Sampling design and superpopulation model: basic aspects

In general, a sample is a subset of the population . For each unit , define a Bernoulli random variable (r.v.) such that is (is not) in the sample whenever (); denote further by the -dimensional vector of components , , . A (unordered, without replacement) sampling design is the probability distribution of the random vector . The expectations and are the first and second order inclusion probabilities, respectively. The suffix denotes the sampling design used to select population units. The sample size is . In the present paper we focus on fixed size sampling designs, such that .

In practice, the sampling design is constructed on the basis of the value of the design variables, i.e. auxiliary variables known for all population units (cfr. [Pfeffermann(1993)]). In particular, the first order inclusion probabilities are frequently chosen to be proportional to an auxiliary variable , depending itself on the design variables: , . A special case is the stratified sampling design, where is proportional to the weight of the stratum containing unit . The rationale of the choice is simple: if the values of the variable of interest are positively correlated with (or, even better, approximately proportional to) the values of , then the Horvitz-Thompson estimator of the population mean will be highly efficient.

For each unit , let be a positive number, with . The Poisson sampling design (, for short) with parameters , , is characterized by the independence of the r.v.s s, with . In symbols

The rejective sampling (), or normalized conditional Poisson sampling ([Hájek(1964)], [Tillé(2006)]) corresponds to the probability distribution of the random vector , under Poisson design, conditionally on .

The Hellinger distance between a sampling design and the rejective design is defined as

| (11) |

For each , , are realizations of a superpopulation composed by i.i.d. -dimensional r.v.s. In the sequel, the symbol will denote the (superpopulation) probability distribution of r.v.s s, and , are the corresponding operators of mean and variance, respectively.

It is important to observe that s are assumed marginally i.i.d.. Conditionally on , s are still independent, but not necessarily identically distributed. This covers, among others, the important case of stratified populations.

2.3 Assumptions

Our assumptions on both the superpopulation model and sampling design are listed below.

-

A1.

is a sequence of finite populations of increasing size .

-

A2.

For each , , are realizations of a superpopulation composed by i.i.d. -dimensional r.v.s, with almost surely.

-

A3.

The d.f. is continuously differentiable, with density function strictly positive of every interval with , . Furthermore, and:

(12) for some .

-

A4.

For each population , sample units are selected according to a fixed size sample design with positive first order inclusion probabilities , , , and sample size . The first order inclusion probabilities are taken proportional to , , being an arbitrary (positive) function. To avoid complications in the notation, we will assume that for each unit . It is also assumed that

(13) Furthermore, the notation is used.

-

A5.

The sample size increases as the population size does, with

-

A6.

For each population , let be the rejective sampling design with inclusion probabilities , , , and let be the actual sampling design (with the same inclusion probabilities). Then

-

A7.

, so that the quantity in is equal to:

(14)

3 Basic asymptotic results

Due to the effect of the sampling design, the empirical distribution function (e.d.f.)

| (15) |

is inconsistent. In fact, in view of the law of large numbers,

unless and are independent. As a consequence, the empirical Lorenz curve studied, for instance, in [Csörgő et al.(1986)], is inconsistent, too.

The first, basic step consists in constructing a consistent estimator of , and then in studying the asymptotic distribution of the corresponding estimate of . The d.f. is estimated by using the (design-based) Hájek estimator

| (16) |

that generates the corresponding “empirical process”

| (17) |

The weak convergence properties of are studied in [Conti and Di Iorio(2018)], [Boistard et al.(2017)].

Denote by

| (18) |

the joint superpopulation d.f. of , and by

| (19) |

the marginal superpopulation d.f.s of and , respectively. Furthermore, from now on the notation

| (20) |

will be used. Note that .

Proposition 1.

Assume that conditions A1-A7 are satisfied, and define

| (21) | |||

| (22) |

so that . Define further

| (23) |

with given by , and

| (24) |

Then, the following statements hold.

-

•

The sequence converges weakly, in equipped with the Skorokhod topology, to a Gaussian process with zero mean function and covariance kernel .

-

•

The sequence converges weakly, in equipped with the Skorokhod topology, to a Gaussian process with zero mean function and covariance kernel .

-

•

The two sequences , are asymptotically independent, so that the sequence , converges weakly, in equipped with the Skorokhod topology, to a Gaussian process with zero mean function and covariance kernel

(25)

Proof.

See [Conti and Di Iorio(2018)] or [Boistard et al.(2017)]. ∎

In particular, if is continuous and the sampling design is simple random sampling without replacement of size , the Hájek estimator reduces to the empirical d.f. . Furthermore, in this case . Hence, if is continuous and the sampling design is simple random sampling without replacement, , and the limiting process can be represented as , being a Brownian bridge.

The term can be equivalently re-written as:

| (26) |

where

| (27) |

The map is monotone non-decreasing, right continuous, with as and as . Hence, induces a finite measure on the real line (equipped with the Borel -field). In view of , such a measure is absolutely continuous w.r.t. the probability measure induced by , and is the corresponding Radon-Nikodym derivative. In symbols:

| (28) |

Next assumption C1 ensures that the trajectories of the limiting process behave regularly, i.e. that they are (uniformly) continuous and bounded over the real line.

-

C1.

The conditional expectation is bounded w.r.t. :

(29)

Proposition 2.

Define the Gaussian process , with . If is continuous, then the process possesses with probability 1 trajectories that are continuous (and bounded) in .

Proof.

See Appendix. ∎

The process shares several properties with the Brownian bridge: it is a Gaussian process with a.s. continuous trajectories, and with with probability 1.

Next assumption D1 is essentially the same as in [Bhattacharya(2007)].

-

D1.

The density exists, is positive, and satisfies the relationships as and as , for some . Furthermore, for some positive .

Proposition 2 and assumption D1 allow one to use the same reasoning as in [Bhattacharya(2007)], and to show that the map is Hadamard differentiable at tangentially to the space of the trajectories of the limiting process . The Hadamard derivative (computed at “point” ) is equal to:

| (30) |

As an application of Theorem 20.8 in [van der Vaart(1998)], we are now in a position to obtain the following result.

Proposition 3.

Under assumptions A1-A6, C1, D1, the following weak convergence results hold:

| (31) | |||||

| (32) |

where , are Gaussian processes that can be represented as:

| (33) | |||||

| (34) |

respectively.

The process is, in a sense, the finite population counterpart of the concentration process studied, in case of i.i.d. data, in [Goldie(1977)], [Csörgő et al.(1986)].

The limiting Gaussian processes , , are quite non-standard. Their covariance kernels are complicate, and, ever worse, they depend on the unknown quantities , , , , . For this reason, in the subsequent section a resampling procedure to approximate the probability law of the processes , is developed.

Before ending this section, we note in passing that from Proposition 3 it is also possible to obtain, virtually with no additional effort, the limiting distribution of the Gini concentration index

| (35) |

Consider in fact its estimator

| (36) |

From it appears that is a linear functional of , so that it is Hadamard differentiable. As a consequence of the chain rule for Hadamard derivatives (see, e.g., [van der Vaart(1998)]), the map is Hadamard differentiable, too, with Hadamard derivative (computed at ‘point” ):

Taking into account that linear functionals of Gaussian processes possess normal distribution, from Proposition 3 the following result follows.

Proposition 4.

Under the assumptions of Proposition 3 the limiting distribution, as , tend to infinity, of can be represented as

| (37) |

The probability law of turns out to be normal with zero expectation and variance

| (38) |

4 The resampling procedure

In the present section we develop a resampling procedure to approximate the distribution of and . The basic requirement is to recover the limiting laws obtained in Propositions 1, 3. In other words, we aim at constructing a resampling procedure that is asymptotically exact. This is in fact the main justification of classical Efron’s bootstrap for i.i.d. data; see, e.g., [Bickel and Freedman(1981)]. Unfortunately, in the present case classical bootstrap does not work, because of the dependence among units due to the sampling design. This fact is well-known in the literature on sampling finite populations: cfr. [Antal and Tillé(2011)], [Chauvet(2007)], [Conti and Marella(2015)] and references therein.

In sampling finite populations several different resampling techniques exist, but none of them possesses a true asymptotic justification. The only exception is the method developed in [Conti and Marella(2015)], that unfortunately is not suitable in the case under examination, because it assumes the absence of relationships between the sampling weights and the values s of the variable of interest.

The resampling procedure we consider here has been proposed in [Conti and Di Iorio(2018)], and exploited in [Marella and Vicard(2018)]. It is composed by two phases. In the first one, on the basis of the sampling data a pseudo-population, consisting in a prediction of the “true” population, is constructed. The prediction process is based on the sampling design, and does not essentially involve the superpopulation model. In the second phase, a sample of size (the same as the “original” one) is drawn from the pseudo-population, according to a sample design (the resampling design) with inclusion probabilities appropriately chosen and satisfying the entropy condition A5.

From now on, the following terminology will be used. The sampling design is the sampling procedure drawing units from the “original” population . The resampling design is the sampling procedure drawing units from the pseudo-population.

4.1 Pseudo-population

A design-based population predictor of is

| (39) |

where s are integer-valued r.v.s, with (joint) probability distribution . In practice, means that population units are predicted to have -value equal to and -value equal to , for each sample unit . In the sequel, the symbols , will be used to denote the -value and -value of unit of the pseudo-population, respectively. Of course units of the pseudo-population satisfy the relationships , , .

Although several pseudo-populations could be constructed, according to [Conti and Di Iorio(2018)] there is essentially only one pseudo-population that asymptotically works in a superpopulation perspective: the multinomial pseudo-population. In a non-asymptotic setting, it goes back to [Pfeffermann and Sverchkov(2004)].

Consider independent trials, where trial () consists in choosing a unit from the original sample ; unit is selected with probability . If at trial the unit is selected, define and , . Next, define a pseudo-population of units, such that unit possesses -value and -value , . Finally, let , , be the number of the pseudo-population units equal to unit of the sample . Of course, the pseudo-population has size .

4.2 Resampling scheme

The resampling procedure we consider is described below.

-

Ph 1.

Generate a pseudo-population of units. Denote by , the -value and -value of unit of the pseudo-population, respectively.

-

Ph 2.

Draw a sample of size from the pseudo-population defined in phase 1, on the basis of a resampling design with first order inclusion probabilities and satisfying assumption A5.

Consider now the resampling design, and let if the unit of the pseudo-population is drawn, and otherwise. The Hájek estimator of is equal to

| (40) |

Next, define the resampled version of the process , namely

| (41) |

The main property of the above resampling scheme is its asymptotic correctness.

Proposition 5.

Assume the sampling design and the resampling design both satisfy assumptions A1-A6, and that P1-P3 are fulfilled. Conditionally on , , , , the following statements hold.

-

.

The sequence , converges weakly, in equipped with the Skorokhod topology, to a Gaussian process with zero mean function and covariance kernel .

-

.

If is Hadamard differentiable at , then converges weakly to , as increases.

In both , weak convergence takes place for a set of s, s having -probability 1, and for a set of s and of probability tending to .

Proof.

See [Conti and Di Iorio(2018)]. ∎

In particular, denote by , the estimators of the generalized Lorenz curve and Lorenz curve, respectively, based on the sample drawn from the pseudo-population. Consider further the resampled processes

| (42) |

From Propositions 3 and 5 it is immediate to obtain the following corollary.

Corollary 1.

Corollary 1 provides an approximation scheme for the probability laws of , .

As a by-product, a similar result for Gini concentration ratio can be obtained. Let

| (44) |

be the resampled version of the Gini concentration ratio.

5 Construction of fixed-size confidence bands

Corollary 1 essentially offers a resampling scheme enabling one to approximate the actual (design-based) distribution of the estimator of the finite population Lorenz curve. In particular, we focus here on the construction of a confidence band for the superpopulation Lorenz curve, . For the sake of simplicity, we confine ourselves on fixed-size confidence bands. Let be the -quantile of the distribution of

| (45) |

If the covariance kernel of the Gaussian process is non-singular, then the r.v. is absolutely continuous with strictly positive density (cfr. [Lifshits(1982)]), so that the equality

| (46) |

holds. Relationship , in its turn, implies that the region

| (47) |

is a confidence band for the whole Lorenz curve of asymptotic level .

The quantile appearing in obviously depends on the law of the process , and hence cannot be computed in practice. The resampling scheme of Section 4 offers the following, simple procedure for its approximate evaluation.

-

1

Generate independent samples of size on the basis of the two-phase procedure described above.

-

2

For each generated sample, compute the corresponding Hajek estimator . They will be denoted by , .

-

3

Compute the corresponding estimates of the Lorenz curve:

with

-

4

Compute the quantities

(48)

Denote further by

| (49) |

the empirical distribution function of s, and by

| (50) |

the corresponding -quantile.

The empirical d.f. is essentially an approximation of the (resampling) distribution of .

In Proposition 6 it is stated that converges to the d.f. of , and that a similar result holds for the quantiles . Proof is in Appendix.

Proposition 6.

For almost all s, s values, and in probability w.r.t. , , conditionally on , , , , the following results hold:

| (51) | |||||

| (52) |

as , go to infinity.

As a consequence of Proposition 6, the region

| (53) |

is a confidence band for with asymptotic level as and increase.

6 Gini concentration index

The results of the above Section also allow us to construct confidence intervals of asymptotic level for the Gini concentration index . Using the same notation as in Section 5, let , the replicates of generated according to the resampling procedure of Section 5, and let

Let further

| (54) | |||||

| (55) | |||||

| (56) |

where

Denote now by the d.f. of a normal distribution with expectation and variance .

Proposition 7.

Under the assumptions of Proposition 6, the following results hold:

| (57) | |||||

| (58) |

as , go to infinity. If, in addition, the sequence is dominated by a r.v. with finite expectation, then

| (59) |

where convergence in is in probability w.r.t. resampling replications.

The main consequences of Proposition 7 are two. First of all, the estimator is a consistent estimator of the variance of ; variance estimation based on linearization techniques is dealt with, for instance, in [Barabesi et al.(2016)]. In the second place, the confidence intervals

| (60) | |||||

| (61) |

both possess asymptotic confidence level as , and increase.

7 Testing for Lorenz dominance

Consider two finite populations of size , . In the sequel, we will essentially use the same notation as in Section 2, with the addition of the suffix (). Denote by

the Lorenz curve for population , , . The population (weakly) Lorenz dominates if

i.e. if

| (62) |

where

The goal of the present section is to construct a test for the Lorenz dominance hypothesis

-

:

-

:

.

The importance of the Lorenz ordering, and testing for Lorenz dominance is stressed, for instance, in [Anderson(1996)], [Barrett et al.(2014)].

From population a sample of size is drawn, according to a sampling design satisfying assumptions -. Assume further that all r.v.s s (, ) for the two populations are independent, and that the two sampling designs , independently select samples from , . The following proposition is an immediate consequence of Proposition 3.

Proposition 8.

Suppose assumptions A1-A6, C1, D1 hold for , , and that as , go to infinity, with . Let further , and

| (63) |

Then, as , tend to infinity, the sequence of stochastic processes converges weakly to a Gaussian process that can be represented as

where , , are two independent Gaussian processes having representation .

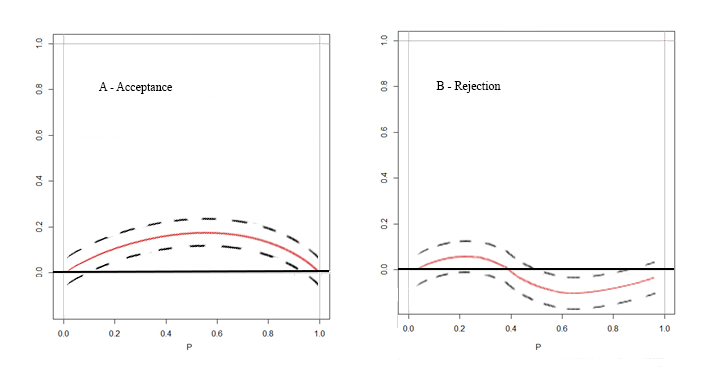

The idea pursued here to construct a test procedure for the hypothesis of Lorenz dominance is simple. It is summarized below.

-

-

Construct a confidence band of level for .

-

-

If, for at least a the confidence band is under the horizontal axis, reject the stochastic dominance hypothesis.

-

-

Otherwise, “accept” stochastic dominance hypothesis.

Clearly, the test procedure has significance level equal to . A graphical illustration of the procedure is in Fig. 1 A, B.

A confidence band for can be constructed by using the resampling procedure of Section 4.

-

1.

For sample drawn from population , generate independent samples of size on the basis of the two-phase procedure described in Section 4.

-

2.

For each generated sample, compute the corresponding estimates of the Lorenz curves:

-

3.

Compute the quantities

-

4.

Compute the quantities

(64)

Denote now by

| (65) |

the empirical distribution function of s, and by

| (66) |

the corresponding -quantile.

Using the same arguments as in Proposition 6, it is now possible to prove the following, further result.

Proposition 9.

For almost all s, s values , and in probability w.r.t. the sample designs, the following results hold:

| (67) | |||||

| (68) |

as , , go to infinity.

As a consequence of Proposition 9, the region

| (69) |

is a confidence band for with asymptotic level as and increase.

8 Simulation study

In this section a simulation study is performed, in order to evaluate the actual confidence level of the proposed confidence bands and intervals. The simulation scenario is similar to [Antal and Tillé(2011)]. In detail, a finite population of size has been generated from the model

| (70) |

where and , and . According to [Antal and Tillé(2011)], the regression parameters , and have been chosen. As far as the inclusion probabilities are concerned, they are taken proportional to the value of a variable , generated from the equation where has a lognormal distribution with parameters and . Three population sizes, , , , and one sampling fraction () have been considered. For each combination , samples of size have been generated according to two sampling schemes: Pareto design (PA) and Sampford design (SA), with inclusion probabilities proportional to s. Actual coverage probabilities for confidence bands for the superpopulation Lorenz curve , as well as for confidence intervals for the superpopulation Gini concentration ratio , have been computed. The nominal level was in all cases. Results are shown in Table 1.

| Pareto sampling design | Sampford sampling design | ||||

|---|---|---|---|---|---|

| Population () and sample () sizes | |||||

| () | () | () | () | () | () |

| Confidence band for Lorenz curve | |||||

| () | () | () | () | () | () |

| Confidence interval for Gini coefficient (Normal approximation) | |||||

| () | () | () | () | () | () |

| Confidence interval for Gini coefficient (Pivot percentile method) | |||||

| () | () | () | () | () | () |

As it appear from Table 1, the performance of the confidence band for the whole Lorenz curve is generally good, and the actual coverage probability is close to the nominal level , for both Pareto and Sampford sampling designs. Similar considerations hold for confidence intervals for Gini concentration ratio, . The method based on normal approximation and variance estimated by resampling performs slightly better than the pivot-percentile method . Again, results are virtually identical for both Pareto and Sampford designs.

Appendix

Proof of Proposition 2.

Suppose that . From it is not difficult to see that

| (71) |

Assumption C1 implies that

so that from it is not difficult to see that

| (72) |

being an appropriate constant. Inequality also holds when . Hence, in terms of the process introduced above we may write

| (73) |

Inequality and the Gaussianity of , in their turn, imply that

| (74) |

Observing that , Proposition 2 now follows from and [Leadbetter and Weissner(1969)]. ∎

Proof of Proposition 6.

Let

be the (resampling) d.f. of . By Dvoretzky-Kiefer-Wolfowitz inequality (cfr. [Massart(1990)]), we have first

| (75) |

Using the Borel-Cantelli first lemma, and taking into account that converges uniformly to , immediately follows. Statement follows from and the absolute continuity of the distribution of (cfr. [Lifshits(1982)]). ∎

Proof of Proposition 7.

Proof of and is similar to Proposition 6. As far as is concerned, it is a consequence of Th. 2.5.5. in [Sen and Singer(1993)] (pp. 90-91). ∎

References

- [Anderson(1996)] Anderson, G. (1996). Nonparametric Tests of Stochastic Dominance in Income Distribution. Econometrica, 64, 1183–1193.

- [Antal and Tillé(2011)] Antal, E. and Tillé, Y. (2011). A direct bootstrap method for complex sampling designs from a finite population. Journal of the American Statistical Association, 106(494), 534–543.

- [Barabesi et al.(2016)] Barabesi, L., Diana, G., and Perri, P. F. (2016). Linearization of inequality indices in the design-based framework. Statistics, 50, 1161–1172.

- [Barrett et al.(2014)] Barrett, G. F., Donald, S. G., and Bhattacharya, D. (2014). Consistent Nonparametric Tests for Lorenz Dominance. Journal of Business and Economic Statistics, 32, 1–13.

- [Bhattacharya(2005)] Bhattacharya, D. (2005). Asymptotic inference from multi-stage samples. Journal of Econometrics, 126, 145–171.

- [Bhattacharya(2007)] Bhattacharya, D. (2007). Inference on inequality from household survey data. Journal of Econometrics, 137, 674–707.

- [Bickel and Freedman(1981)] Bickel, P. J. and Freedman, D. (1981). Some asymptotic theory for the bootstrap. The Annals of Statistics, 9, 1196–1216.

- [Boistard et al.(2017)] Boistard, H., Lopuhaä, R., and Ruiz-Gazen, A. (2017). Functional central limit theorems for single-stage sampling designs. The Annals of Statistics, 45, 1728–1758.

- [Chauvet(2007)] Chauvet, G. (2007). Méthodes de bootstrap en population finie. Ph.D. Dissertation, Laboratoire de statistique d’enquêtes, CREST-ENSAI, Universioté de Rennes 2.

- [Conti and Di Iorio(2018)] Conti, P. L. and Di Iorio, A. (2018). Analytic inference in finite populations via resampling, with applications to confidence intervals and testing for independence. Preprint arXiv:1809.08035 available at https://arxiv.org/abs/1809.08035 - Submitted for publication.

- [Conti and Marella(2015)] Conti, P. L. and Marella, D. (2015). Inference for quantiles of a finite population: asymptotic vs. resampling results. Scandinavian Journal of Statistics, 42, 545–561.

- [Csörgő et al.(1986)] Csörgő, M., Csörgő, S., and Horváth, L. (1986). An Asymptotic Theory for Empirical Reliability and Concentration Processes. Springer-Verlag, Berlin.

- [Davidson(2009)] Davidson, R. (2009). Reliable inference for the Gini index. Journal of Econometrics, 150, 30–40.

- [Gastwirth(1972)] Gastwirth, J. L. (1972). The estimation of Lorenz curve and Gini index. Review of Economics and Statistics, 54, 306–316.

- [Giorgi(1999)] Giorgi, G. M. (1999). Income Inequality Measurement: The Statistical Approach. In: Hanbdbook of Income Inequtality Measurement (J. Silber Ed.). Kluwer Academic Publishers, Boston.

- [Giorgi and Gigliarano(2017)] Giorgi, G. M. and Gigliarano, C. (2017). The Gini Concentration Index: a Review of the Inference Literature. Journal of Economic Surveys, 31, 1130–1148.

- [Goldie(1977)] Goldie, C. M. (1977). Convergence theorems for empirical Lorenz curve and their inverses. The Annals of Applied Probability, 9, 765–791.

- [Hájek(1964)] Hájek, J. (1964). Asymptotic theory of rejective sampling with varying probabilities from a finite population. The Annals of Mathematical Statistics, 35, 1491–1523.

- [Langel and Tillé(2013)] Langel, M. and Tillé, Y. (2013). Variance estimation of the Gini index: revisiting a result several times published. Journal of the Royal Statistical Society Series A, 176, 521 540.

- [Leadbetter and Weissner(1969)] Leadbetter, M. R. and Weissner, J. H. (1969). On continuity and other analytic properties of stochastic process sample functions. Proceedings of the American Mathematical Society, 22, 291–294.

- [Lifshits(1982)] Lifshits, M. A. (1982). On the absolute continuity of distributions of functionals of random processes. Theory of Probability and Its Applications, 27, 600–607.

- [Marella and Vicard(2018)] Marella, D. and Vicard, P. (2018). Pc complex: PC algorithm for complex survey data. Working Paper n. 240, Dipartimento di Economia - Università Roma Tre (ISSN: 2279-6916). Submitted for publication.

- [Massart(1990)] Massart, P. (1990). The tight constant in the Dvoretzky-Kiefer-Wolfowitz inequality. The Annals of Probability, 18, 1269–1283.

- [Pfeffermann(1993)] Pfeffermann, D. (1993). The role of sampling weights when modeling survey data. International Statistical Review, 61, 317–337.

- [Pfeffermann and Sverchkov(2004)] Pfeffermann, D. and Sverchkov, M. (2004). Prediction of finite population totals based on the sample distribution. Survey Methodology, 30, 79–92.

- [Sen and Singer(1993)] Sen, P. K. and Singer, J. (1993). Large Sample Methids in Statistics. Champam & Hall, London.

- [Tillé(2006)] Tillé, Y. (2006). Sampling Algorithms. Springer, New York.

- [van der Vaart(1998)] van der Vaart, A. (1998). Asymptotic Statistics. Cambridge University Press, Cambridge.

- [Zheng(2002)] Zheng, B. (2002). Testing Lorenz curves with non-simple random samples. Econometrica, 70, 1235–1243.