Principal components analysis of regularly varying functions

Abstract

The paper is concerned with asymptotic properties of the principal components analysis of functional data. The currently available results assume the existence of the fourth moment. We develop analogous results in a setting which does not require this assumption. Instead, we assume that the observed functions are regularly varying. We derive the asymptotic distribution of the sample covariance operator and of the sample functional principal components. We obtain a number of results on the convergence of moments and almost sure convergence. We apply the new theory to establish the consistency of the regression operator in a functional linear model.

Key words: Functional data, Principal components, Regular variation

1 Introduction

A fundamental technique of functional data analysis is to replace infinite dimensional curves by coefficients of their projections onto suitable, fixed or data–driven, systems, e.g. [bosq:2000], [ramsay:silverman:2005], [HKbook], [hsing:eubank:2015]. A finite number of these coefficients encode the shape of the curves and are amenable to various statistical procedures. The best systems are those that lead to low dimensional representations, and so provide the most efficient dimension reduction. Of these, the functional principal components (FPCs) have been most extensively used, with hundreds of papers dedicated to the various aspects of their theory and applications.

If are mean zero iid functions in with , then

| (1.1) |

The FPCs and the eigenvalues are, respectively, the eigenfunctions and the eigenvalues of the covariance operator defined by As such, the are orthogonal. We assume they are normalized to unit norm. The form an optimal orthonormal basis for dimension reduction measured by the norm, see e.g. Theorem 11.4.1 in [KRbook].

The and the are estimated by and defined by

| (1.2) |

where

| (1.3) |

Like the , the are defined only up to a sign. Thus, strictly speaking, in the formulas that follow, the would need to be replaced with , where . As is customary, to lighten the notation, we assume that the orientations of and match, i.e. .

Under the existence of the fourth moment,

| (1.4) |

and assuming , it has been shown that for each ,

| (1.5) |

| (1.6) |

| (1.7) |

for a suitably defined variance and a covariance operator . The above relations, especially (1.5), have been used to derive large sample justifications of inferential procedures based on the estimated FPCs . In most scenarios, one can show that replacing the by the and the by the is asymptotically negligible. Relations (1.5) were established by [dauxois:1982] and extended to weakly dependent functional time series by [hormann:kokoszka:2010]. Relations (1.6) and (1.7) follow from the results of [kokoszka:reimherr:2013]. In case of continuous functions satisfying regularity conditions, they follow from the results of [hall:h-n:2006].

A crucial assumption for the relations (1.5)–(1.7) to hold is the existence of the fourth moment, i.e. (1.4), the iid assumption can be relaxed in many ways. Nothing is at present known about the asymptotic properties of the FPCs and their eigenvalues if (1.4) does not hold. Our objective is to explore what can be said about the asymptotic behavior of , and if (1.4) fails. We would thus like to consider the case of and . Such an assumption is however too general. From mid 1980s to mid 1990s similar questions were posed for scalar time series for which the fourth or even second moment does not exist. A number of results pertaining to the convergence of sample covariances and the periodogram have been derived under the assumption of regularly varying tails, e.g. Davis and Resnick (?, ?), [kluppelberg:mikosch:1994], [mikosch:gka:1995], [kokoszka:taqqu:1996], [anderson:meerschaert:1997]; many others are summarized in the monograph of [embrechts:kluppelberg:mikosch:1997]. The assumption of regular variation is natural because non–normal stable limits can be derived by establishing a connection to random variables in a stable domain of attraction, which is characterized by regular variation. This is the approach we take. We assume that the functions are regularly varying in the space with the index , which implies and . Suitable definitions and assumptions are presented in Section 2.

The paper is organized as follows. The remainder of the introduction provides a practical motivation for the theory we develop. It is not necessary to understand the contribution of the paper, but, we think, it gives a good feel for what is being studied. The formal exposition begins in Section 2, in which notation and assumptions are specified. Section 3 is dedicated to the convergence of the sample covariance operator (the integral operator with kernel (1.3)). These results are then used in Section 4 to derive various convergence results for the sample FPCs and their eigenvalues. Section 5 shows how the results derived in previous sections can be used in a context of a functional regression model. Its objective is to illustrate the applicability of our theory in a well–known and extensively studied setting. It is hoped that it will motivate and guide applications to other problems of functional data analysis. All proofs which go beyond simple arguments are presented in Online material.

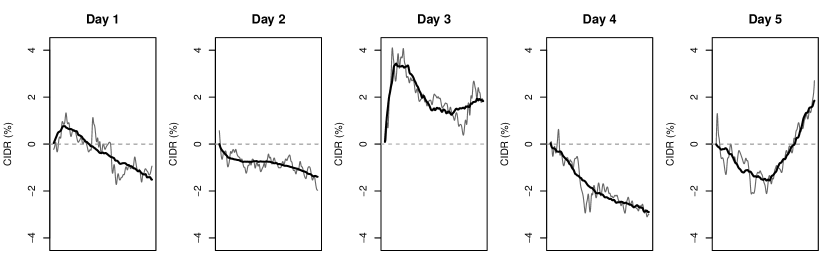

We conclude this introduction by presenting a specific data context. Denote by the price of an asset at time of trading day . For the assets we consider in our illustration, is time in minutes between 9:30 and and 16:00 EST (NYSE opening times) rescaled to the unit interval . The intraday return curve on day is defined by . In practice, is the price after the first minute of trading. The curves show how the return accumulates over the trading day, see e.g. [lucca:moench:2015]; examples of are shown in Figure 1.

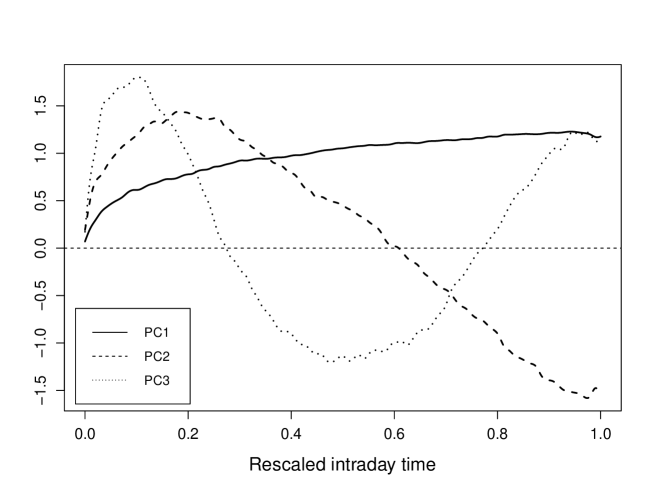

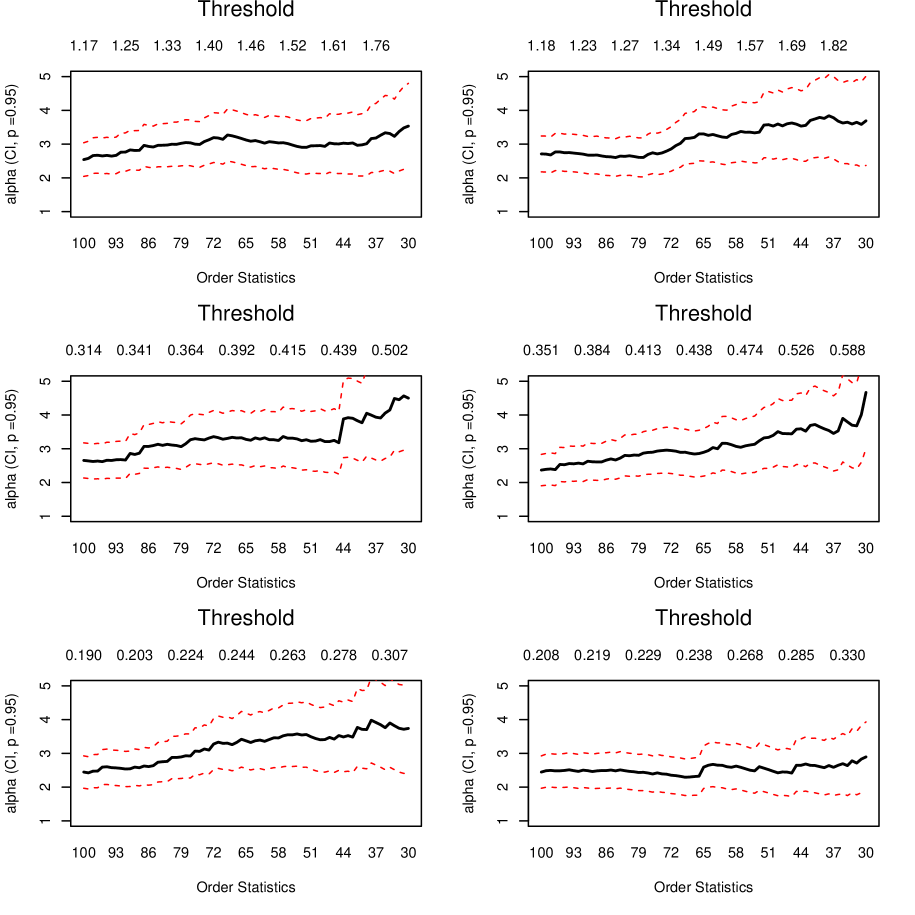

The first three sample FPCs, , are shown in Figure 2. They are computed, using (1.2), from minute-by-minute Walmart returns form July 05, 2006 to Dec 30, 2011, trading days. (This time interval is used for the other assets we consider.) The curves , with the scores , visually approximate the curves well. One can thus expect that the (with properly adjusted sign) are good estimators of the population FPCs in (1.1). Relations (1.5) and (1.7) show that this is indeed the case, if . (The curves can be assumed to form a stationary time series in , see [horvath:kokoszka:rice:2014].) We will now argue that the assumption of the finite fourth moment is not realistic, so, with the currently available theory, it is not clear if the are good estimators of the . If , then for every . Figure 3 shows the Hill plots of the sample score for two stocks and for . Hill plots for other blue chip stocks look similar. These plots illustrate several properties. 1) It is reasonable to assume that the scores have Pareto tails. 2) The tail index is smaller than 4, implying that the fourth moment does not exist. 3) It is reasonable to assume that the tail index does not depend on and is between 2 and 4. With such a motivation, we are now able to formalize in the next section the setting of this paper.

2 Preliminaries

The functions are assumed to be independent and identically distributed in , with the same distribution as , which is regularly varying with index . By , we denote the usual separable Hilbert space of square integrable functions on some compact subset of an Euclidean space. In a typical FDA framework, , e.g. Chapter 2 of [HKbook]. Regular variation in finite–dimensional spaces has been a topic of extensive research for decades, see e.g. Resnick (?, ?) and [meerschaert:scheffler:2001book]. We shall need the concept of regular variation of measures on infinitely-dimensional function spaces. To this end, we start by recalling some terminology and fundamental facts about regularly varying functions.

A measurable function is said to be slowly varying (at infinity) if, for all ,

Functions of the form are said to be regularly varying with exponent .

The notion of regular variation extends to measures and provides an elegant and powerful framework for establishing limit theorems. It was first introduced by [meerschaert:1984] and has been since extended to Banach and even metric spaces using the notion of convergence (see e.g. [hult:lindskog:2006]). Even though we will work only with Hilbert spaces, we review the theory in a more general context.

Consider a separable Banach space and let be the open ball of radius , centered at the origin. A Borel measure defined on is said to be boundedly finite if , for all Borel sets that are bounded away from , that is, such that , for some . Let be the collection of all such measures. For , we say that the converge to in the topology, if , for all bounded away from , -continuity Borel sets , i.e., such that , where denotes the boundary of . The convergence can be metrized such that becomes a complete separable metric space (Theorem 2.3 in [hult:lindskog:2006] and also Section 2.2. of [meinguet:2010]). The following result is known, see e.g. Chapter 2 of [meinguet:2010] and references therein.

Proposition 2.1

Let be a random element in a separable Banach space and . The following three statements are equivalent:

-

(i)

For some slowly varying function ,

(2.1) and

(2.2) where is a non-null measure on the Borel -field of .

-

(ii)

There exists a probability measure on the unit sphere in such that, for every ,

-

(iii)

Relation (2.1) holds, and for the same spectral measure in (ii),

Definition 2.1.

If any one of the equivalent conditions in Proposition 2.1 hold, we shall say that is regularly varying with index . The measures and will be referred to as exponent and angular measures of , respectively.

The measure is sometimes called the spectral measure, but we will use the adjective “spectral” in the context of stable measures which appear in Section 3. It is important to distinguish the angular measure of a regularly varying random function and a spectral measure of a stable distribution, although they are related. We also note that we call the tail index, and the tail exponent.

We will work under the following assumption.

Assumption 2.1

The random element in the separable Hilbert space has mean zero and is regularly varying with index . The observations are independent copies of .

Assumption 2.1 is a coordinate free condition not related in any way to functional principal components. The next assumption relates the asymptotic behavior of the FPC scores to the assumed regular variation. It implies, in particular, that the expansion contains infinitely many terms, so that we study infinite dimensional objects. We will see in the proofs of Proposition 3.3 and Theorem 3.6 that under Assumption 2.1 the limit

exists and is finite. We impose the following assumption related to condition (2.2).

Assumption 2.2

For every , .

Assumption 2.2 postulates, intuitively, that the tail sums must have extreme probability tails comparable to that of .

We now collect several useful facts that will be used in the following. The exponent measure satisfies

| (2.3) |

It admits the polar coordinate representation via the angular measure . That is, if , where and for , we have

| (2.4) |

This means that for every bounded measurable function that vanishes on a neighborhood of , we have

There exists a sequence such that

| (2.5) |

for any set in with . One can take, for example,

| (2.6) |

with a slowly varying function satisfying .

We will work with Hilbert–Schmidt operators. A linear operator is Hilbert–Schmidt if , where is any orthonormal basis of . Every Hilbert–Schmidt operator is bounded. The space of Hilbert–Schmidt operators will be denoted by . It is itself a separable Hilbert space with the inner product

If is an integral operator defined by , then .

Relations (1.5) essentially follow from the bound

where the subscript indicates the Hilbert–Schmidt norm. Under Assumption 2.1 such a bound is useless because, by (2.1), . In fact, one can show that under Assumption 2.1, , so no other bound on can be expected. The following Proposition 2.2 implies however that under Assumption 2.1 the population covariance operator is a Hilbert-Schmidt operator, and with probability 1. This means that the space does provide a convenient framework.

Proposition 2.2.

Suppose is a random element of with and is the sample covariance operator based on iid copies of . Then and with probability 1.

Like all proofs, the proof of Proposition 2.2 is presented in the on-line material.

3 Limit distribution of

We will show that converges to an –stable Hilbert–Schmidt operator, for an appropriately defined regularly varying sequence . Unless stated otherwise, all limits in the following are taken as .

Observe that for any ,

| (3.1) | ||||

where . Since the are Hilbert–Schmidt operators, the last expression shows a connection between the asymptotic distribution of and convergence to a stable limit in the Hilbert space of Hilbert–Schmidt operators. We therefore restate below, as Theorem 3.1, Theorem 4.11 of [kuelbs:mandrekar:1974] which provides conditions for the stable domain of attraction in a separable Hilbert space. The Hilbert space we will consider in the following will be and the stability index will be . However, when stating the result of Kuelbs and Mandrekar, we will use a generic Hilbert space and the generic stability index . Recall that for a stable random element with index , there exists a spectral measure defined on the unit sphere , such that the characteristic functional of is given by

| (3.2) |

where

We denote the above representation by . The -stable random element is necessarily regularly varying with index . In fact, its angular measure is precisely the normalized spectral measure appearing in (3.2), i.e.,

[kuelbs:mandrekar:1974] derived sufficient and necessary conditions on the distribution of under which

| (3.3) |

where the are iid copies of . They assume that the support of the distribution of , equivalently of the distribution of , spans the whole Hilbert space . In our context, we will need to work with whose distribution is not supported on the whole space. Denote by the smallest closed subspace which contains the support of the distribution of . Then is a Hilbert space itself with the inner product inherited from . Denote by an orthonormal basis of . We assume that this is an infinite basis because we consider infinite dimensional data. (The finite dimensional case has already been dealt with by [rvaceva:1962].) Introduce the projections

Theorem 3.1.

Let , , be iid random elements in a separable Hilbert space with the same distribution as . Let be an orthonormal basis of . There exist normalizing constants and such that (3.3) holds if and only if

| (3.4) |

where for each , , and , and where

| (3.5) |

for all continuity sets , with .

If (3.3) holds, the sequence must satisfy

| (3.6) |

where

| (3.7) |

and is the Euler gamma function. Furthermore, the may be chosen as

| (3.8) |

Remark 3.2.

The origin of the constant appearing in (3.6) can be understood as follows. Consider the simple scalar case Let be symmetric -stable with , where in this case, . Consider iid copies of and observe that by the -stability property

and hence (3.3) holds trivially with and .

On the other hand, by Proposition 1.2.15 on page 16 in [samorodnitsky:taqqu:1994], we have

This along with an integration by parts and an application of Karamata’s theorem yield , giving the constant in (3.6).

Proposition 3.3.

Our next objective is to show that if is a regularly varying element of a separable Hilbert space whose index is , then the operator is regularly varying with index , in the space of Hilbert–Schmidt operators. If , then is an element of defined by . It is easy to check that . If , we denote by the subset of defined as the set of operators of the form , with . Denote by the unit sphere in centered at the origin, and by such a sphere in .

The next result is valid for all .

Proposition 3.4.

Suppose is a regularly varying element with index of a separable Hilbert space . Then the operator is a regularly varying element with index of the space of Hilbert-Schmidt operators.

Remark 3.5.

The proof of Proposition 3.4 shows that the angular measure of is supported on the diagonal and that

The next result specifies the limit distribution of the sums of the based on the results derived so far.

Theorem 3.6.

The final result of this section specifies the asymptotic distribution of .

Theorem 3.7.

If the are scalars, then the angular measure is concentrated on , with , in the notation of [davis:resnick:1986]. Thus , and we recover the centering in Theorem 2.2 of [davis:resnick:1986]. Relation (3.12) explains the structure of this centering in a much more general context.

Theorem 3.7 readily leads to a strong law of large numbers which can be derived by an application of the following result, a consequence of Theorem 3.1 of [acosta:1981].

Theorem 3.8.

Suppose are iid mean zero elements of a separable Hilbert space with , for some . Then,

4 Convergence of eigenfunctions and eigenvalues

We first formulate and prove a general result which allows us to derive the asymptotic distributions of the eigenfunctions and eigenvalues of an estimator of the covariance operator from the asymptotic distribution of the operator itself. The proof of this result is implicit in the proofs of the results of Section 2 of [kokoszka:reimherr:2013], which pertain to the asymptotic normality of the sample covariance operator if . The result and the technique of proof are however more general, and can be used in different contexts, so we state and prove it in detail.

Assumption 4.1

Suppose is the covariance operator of a random function taking values in such that . Suppose is an estimator of which is a.s. symmetric, nonnegative–definite and Hilbert–Schmidt. Assume that for some random operator , and for some ,

In our setting, is specified in (3.12), and for some . More precisely,

We will work with the eigenfunctions and eigenvalues defined by

Assumption 4.1 implies that and the are orthogonal with probability 1. We assume that, like the , the have unit norms. To lighten the notation, we assume that sign = 1. This sign does not appear in any of our final results, it cancels in the proofs. We assume that both sets of eigenvalues are ordered in decreasing order. The next assumption is standard, it ensures that the population eigenspaces are one dimensional.

Assumption 4.2

If is an –stable random operator in , then the are jointly –stable random functions in , and are jointly –stable random variables. This follows directly from the definition of a stable distribution, e.g. Section 6.2 of [linde:1986]. Under Assumption 2.1, . Theorem 4.1 thus leads to the following corollary.

Corollary 4.2.

Corollary 4.2 implies the rates in probability and , with . This means, that the distances between and and the corresponding population parameters are approximately of the order , i.e. are asymptotically larger that these distances in the case of , which are of the order . Note that , as .

It is often useful to have some bounds on moments, analogous to relations (1.5). Since the tails of and behave like , e.g. Section 6.7 of [linde:1986], , with an analogous relation for . We can thus expect convergence of moments of order . The following theorem specifies the corresponding results.

Theorem 4.3.

Several cruder bounds can be derived from Theorem 4.3. In applications, it is often convenient to take . Then . By Potter bounds, e.g. Proposition 2.6 (ii) in [resnick:2006], for any there is a constant such that for . For each , we can choose so small that . This leads to the following corollary.

Corollary 4.4.

Corollary 4.4 implies that , and tend to zero, for any .

5 An application: functional linear regression

One of the most widely used tools of functional data analysis is the functional regression model, e.g. [ramsay:silverman:2005], [HKbook], [KRbook]. Suppose are explanatory functions, are response functions, and assume that

| (5.1) |

where is the kernel of . The are mean zero iid functions in , and so are the error functions . Consequently, the are iid in . A question that has been investigated from many angles is how to consistently estimate the regression kernel . An estimator that has become popular following the work of [yao:muller:wang:2005AS] can be constructed as follows.

The population version of (5.1) is . Denote by the FPCs of and by those of , so that

If is independent of , then, with ,

with the series converging in , equivalently in , see Lemma 8.1 in [HKbook]. This motivates the estimator

where are the eigenfunctions of and is an estimator of . [yao:muller:wang:2005AS] study the above estimator under the assumption that data are observed sparsely and with measurement errors. This requires two-stage smoothing, so their assumptions focus on conditions on the various smoothing parameters and the random mechanism that generates the sparse observations. Like in all work of this type, they assume that the underlying functions have finite fourth moments: , , and so . Our objective is to show that if the satisfy the assumptions of Section 2, then

| (5.2) |

as , and at suitable rates determined by the rate of decay of the eigenvalues. The norm is the usual operator norm. The integral operators and are defined by their kernels and , respectively. We focus on moment conditions, so we assume that the functions are fully observed, and use the estimator

Since the regression operator is infinitely dimensional, we strengthen Assumption 4.2 to the following assumption.

Assumption 5.1

The eigenvalues and satisfy

Many issues related to the infinite dimension of the functional data in model (5.1) are already present when considering projections on the unobservable subspaces

Therefore we first consider the convergence of the operator with the kernel

Set and observe that

Therefore

| (5.3) |

The condition

| (5.4) |

which is Assumption (A1) of [yao:muller:wang:2005AS], implies that the remainder term is asymptotically negligible. It is instructive to rewrite condition (5.4) in a different form. Observe that

| (5.5) |

Therefore

| (5.6) |

We see that condition (5.4) simply means that is a Hilbert–Schmidt operator, and so it holds under our general assumptions on model (5.1).

The last assumption implicitly restricts the rates at which and tend to infinity with . Under Assumption 5.1, the following quantities are well defined

| (5.7) |

| (5.8) |

Assumption 5.2

The truncation levels and tend to infinity with in such a way that for some ,

| (5.9) | |||

| (5.10) | |||

| (5.11) | |||

| (5.12) |

The conditions in Assumption 5.2 could be restated or unified; and could be replaced by slightly different conditions by modifying the technique of proof. The essence of this assumption is that and must tend to infinity sufficiently slowly, and the rate is influenced by index ; the closer is to 4, the larger can be taken, so and can be larger.

Theorem 5.1.

Acknowledgements: The authors have been supported by NSF grant “FRG: Collaborative Research: Extreme Value Theory for Spatially Indexed Functional Data” (1462067 CSU, 1462368 Michigan). We thank Professor Jan Rosiński for directing us to the work of [acosta:gine:1979], and Mr. Ben Zheng for preparing the figures.

Online material

6 Proofs of the results stated in the paper

Throughout the proofs, we will use relatively well–known properties of slowly varying functions, which we collect in Lemma 6.1 for ease of reference. For the proofs and many more details, see e.g., [resnick:1987] and [bingham:goldie:teugels:1987].

Lemma 6.1.

If is a slowly varying function, then:

(i) and are slowly varying.

(ii) (Potter bounds) For all , we have as .

(iii) (Karamata’s Theorem) For all and , as , we have

where means , as .

6.1 Proofs of Proposition 2.2 and of the results of Section 3

Proof of Proposition 2.2

Since is a covariance operator, it is nuclear (), e.g. Theorem 11.2.2 of [KRbook], and so it is Hilbert–Schmidt ().

We now verify that is a.s. a Hilbert-Schmidt operator. Observe that

It thus suffices to show that

where

Observe that

Therefore, by the orthonormality by the ,

Finally, observe that

because is a random element of .

Proof of Proposition 3.3

Set

| (6.1) |

Recall that (6.1) specifies the relationship between the stable spectral measure and the angular measure of a regularly varying distribution appearing in Proposition 2.1.

First we assume (3.4) and (3.5) hold. Take in (3.4) and in (3.5), we then have for every ,

for any continuity set of (equivalently, of ). Thus condition (ii) in Proposition 2.1 holds, which implies that is regularly varying with index .

Next we assume that is regularly varying with index , and show that (3.4) and (3.5) will hold. Using condition (ii) in Proposition 2.1, we have

for all continuity sets , with . Then, with the set defined by (3.9),

where the above convergence follows from (2.2) provided we can show that are continuity sets of the measure . We do that next.

By the definition of in (3.9) and since is continuous and homogeneous, we have

Furthermore, we have that for all . This implies that , where the sets are all disjoint in . By the homogeneity of , however, (recall (2.3)) it follows that . In particular,

for any sequence . If , then by taking ’s such that , we obtain , which is not possible since is bounded away from zero. We have thus shown that , i.e., is a continuity set of for all .

To complete the proof of (3.4), it remains is to show that , as . Notice that and thus since . It is easy to see that . Indeed, for each , we have and therefore

If , then for each , which is impossible.

Proof of Proposition 3.4

Since and , we conclude that

Notice that is a slowly varying function. Thus, by Proposition 2.1 (iii), to establish the regular variation of it remains to show that there must exist a probability measure on such that

for every -continuity set . The operator takes values only in a small subset of , namely in

| (6.2) |

The set is closed in and its Borel subsets have the form , where is a Borel subset of . We know that

for every -continuity set . Denote by a random element of taking values in whose distribution is . Then we have

| (6.3) |

where has distribution . Furthermore, denote by a random element of taking values in whose distribution is

We want to identify a random element such that

| (6.4) |

whose distribution will be the desired measure .

We first verify that

| (6.5) |

Relation (6.5) is equivalent to

| (6.6) |

Set . Since , the left–hand side of (6.6) is

while the right–hand side of (6.6) is

| (6.7) |

Therefore, (6.5) holds. It remains to show that

The above relation holds because by (6.7) and (6.3),

provided is a continuity set of . Using the relation , it is easy to check that in if and only if in . Hence, , so the continuity sets of the distribution of have the form with .

Proof of Theorem 3.6

By Proposition 3.4, the operators are iid regularly varying elements of , whose index of regular variation is . In order to use Theorem 3.1, we first verify that , cf. Proposition 3.3. This is where Assumption 2.2 comes into play. An orthonormal basis of is , where the are the FPCs of . Set

We must thus verify that . By (2.2),

Clearly

which is the denominator of in Assumption 2.2. Turning to the numerator, observe that iff

Direct verification, which uses the definition of the inner product in and the orthonormality of the , shows that It follows that iff

Using the definition of the Hilbert–Schmidt norm and the orthogonality of the again, we see that the above inequality is equivalent to so is equal to the numerator of .

It remains to show that the normalizing sequences can be chosen as specified in (3.11). It is easy to check that and . We will show that

| (6.8) |

which in view of (3.6) would yield (3.10), where the spectral measure of the limit is normalized so that with in (3.7).

Observe that by the Tonelli-Fubini Theorem, we have

where we used the fact that . Now, by applying Karamata’s theorem (Lemma 6.1 (iii)) to the integral in the last expression, we obtain

| (6.9) |

as , where means that .

In view of (2.5) by taking , we obtain

| (6.10) |

since is normalized so that and by Proposition 2.2.2 of [meinguet:2010]. Thus, multiplying (6.1) by and recalling (3.11), we obtain

where . Since is a slowly varying function, we have as , and therefore by (6.10), we obtain (6.8). This completes the proof.

Proof of Theorem 3.7

Observe that by (3.1),

| (6.11) |

with and as in Theorem 3.6. The first term converges to , so we must verify the existence of the second term, show that it converges, and describe its limit. The issue is subtle because implies that with probability 1, yet the expected value does not tend to zero even in the case of scalar observations, see Theorem 2.2 of [davis:resnick:1986]. It is convenient to approach the problem in a slightly more general setting.

Suppose is a regularly varying element of a separable Hilbert space whose index of regular variation is . In our application, , the Hilbert space is and . Denote by the exponent measure of and by a regularly varying sequence such that , so that

| (6.12) |

with the usual restrictions on the set , cf. Proposition 2.1. Set

and observe that exists in the sense of Bochner. Indeed, by (2.1) and the Potter bounds (Lemma 6.1), we have

for an arbitrarily small . Since , by taking , we obtain and the expectation of and hence is well-defined.

Now set . We want to identify such that . We will show that the above convergence holds with

| (6.13) |

where . Recall that is regularly varying and by (2.4) its exponent and angular measures are related as follows

| (6.14) |

where and are polar coordinates in . Thus, in polar coordinates, we obtain

| (6.15) | ||||

This shows that the Bochner integral in (6.13) is well defined and in fact equals

In view of Remark 3.5, by taking and , we then obtain

which is the expression for the offset in (3.12).

Observe that by the definition (6.12) of , since , for any Bochner integrable mapping of the Hilbert space into itself, or to the real line,

| (6.16) |

Therefore,

Observe that , and by (6.14),

Thus and are probability measures on , and we want to show that

Since converges weakly to , it suffices to verify that

| (6.17) |

for some (this implies strong uniform integrability). Observe that by (6.16),

| (6.18) |

where

By the Tonelli–Fubini theorem, we have

Now, by picking such that and applying the Karamata Theorem (Lemma 6.1(iii)), for the right-hand side of (6.1), we obtain

where the last convergence follows from the definition of the sequence . This shows that the supremum in (6.17) is finite, which completes the proof.

6.2 Proofs of the results of Section 4

Proof of Theorem 4.1

Before stating Theorem 4.1, we referred to Lemma 6.2 which ensures that the the series

converge a.s. in . These series play a fundamental role in our arguments.

Lemma 6.2.

Suppose . For , set

Then, the series defining converges in .

Proof 6.3.

Since the are orthonormal, it is enough to check that

Since the system forms an orthonormal basis in

Therefore,

withe defined in (5.7).

We will use the following lemma, which is analogous to Lemma 1 in [kokoszka:reimherr:2013], whose fully analogous proof, based on algebraic manipulations, is omitted.

Lemma 6.4.

For any ,

For any such that and ,

By Assumption 4.1, . Using the well–known inequalities

(see e.g. Lemmas 2.2 and 2.3 in [HKbook]), we obtain the following Lemma.

Lemma 6.5.

For ,

Lemma 6.6.

For ,

Proof 6.7.

The same arguments apply to any fixed , so to reduce the number of indexes used, we present them for . Set

where

By Parseval’s identity,

Focusing on the first term, , observe that

We conclude that , and it remain to show that

| (6.19) |

In the remainder of the proof it is assumed that . Since

by Lemma 6.4,

Using a common denominator and rearranging the numerator, we obtain

It is convenient to decompose the sum in (6.19) as

where

Since , by Parseval’s identity,

By Lemma 6.5, the denominator converges in probability to , and the numerator is bounded above by .

A similar argument shows that

The denominator again converges to a positive constant. By the Cauchy–Schwarz inequality,

We see that .

The above method also shows that .

Proof of Theorem 4.1: To prove the first relation, we use the decomposition

By Lemma 6.6, it suffices to show that the converge jointly in distribution to the . Consider the operator defined by

with the functions defined in Lemma 6.2. The proof of Lemma 6.2 shows that , so each is a continuous linear operator. Hence is continuous, and so . Since, and , the required convergence follows.

Now we turn to the convergence of the eigenvalues. We will derive an analogous decomposition,

| (6.20) |

and show that for each , . Since the projections

are continuous, the claim will follow.

Proof of Theorem 4.3

We start with a simple lemma, custom formulated for our needs.

Lemma 6.8.

Suppose and are sequences of nonnegative random variables and is a convergent sequence of nonnegative numbers. Suppose . If the are uniformly integrable, then so are the .

Proof 6.9.

We will establish a more general result under the assumption that . Recall that a sequence is uniformly integrable if and only if the following two conditions hold

(i) We have .

(ii) For all , there exists a , such that

for all events such that (see, e.g., Theorem 6.5.1 on page 184 in [resnick:1999]).

Since is uniformly integrable, we have and Condition (i) above follows from the triangle inequality and the boundedness of the sequence . To show that Condition (ii) holds, observe that by the triangle inequality

| (6.21) |

Using the uniform integrability of , for every , one can find such that the first term in the right-hand side of (6.21) is less than , provided . By setting , we also ensure that the second term therein is less than for all . This completes the proof of the uniform integrability of .

In the following, we assume that is a fixed number in . Theorem 6.1 of [acosta:gine:1979] implies that, in the notation of Theorem 3.1, cf. (3.3),

Applying the above result to (3.10), we obtain

| (6.22) |

where

In the framework of Theorem 3.7, set

and

so that (6.11) becomes

with and . We now explain why we can conclude that

| (6.23) |

Since in , in . Convergence (6.23) will follow if we can assert that the nonnegative random variables are uniformly integrable. Since and (6.22) holds, Theorem 3.6 in [billingsley:1999] implies that the random variables are uniformly integrable. Relation (6.23) thus follows from the inequality

and Lemma 6.8. Relation (6.23) implies the first relation in Theorem 4.3 with .

Since (see e.g. Lemma 2.2 in [HKbook]), the second relation follows from the first. Under Assumption 4.2, (see e.g. Lemma 2.3 in [HKbook] or Lemma 4.3 in [bosq:2000]), so the third relation also follows from the first.

6.3 Proof of Theorem 5.1

Since by (5.3) and (5.4), it is enough to show that

| (6.24) |

The operators and have the following expansions:

Introduce the sample analogs of the subspaces and ,

and consider the following projections:

Observe that

where

and

Notice that for any or , and exist.

For , consider the decomposition

where

Relation (6.24) will follow from Lemmas 6.12, 6.14, 6.16 and 6.22. The first two of these lemmas use the following result.

Lemma 6.10.

Under the assumptions of Theorem 5.1,

Proof 6.11.

For each integer , we have

Therefore,

and

Hence the claim holds.

Lemma 6.12.

Under the assumptions of Theorem 5.1, .

Proof 6.13.

Lemma 6.14.

Under the assumptions of Theorem 5.1, .

Proof 6.15.

Lemma 6.16.

Under the assumptions of Theorem 5.1, .

Proof 6.17.

Observe that

Therefore,

Since, by the law of large numbers, , the claim follows from condition (5.10).

To deal with the last term, we need additional lemmas.

Lemma 6.18.

Under the assumptions of Theorem 5.1, .

Proof 6.19.

The decomposition

and the identities

imply that

For any ,

The above convergence follows from Theorem 4.1 of [acosta:1981] which implies that in any separable Banach space of Rademacher type , , , provided the are iid with and . In our case, the Banach space is the Hilbert space (a Hilbert space has Rademacher type for any , see e.g. Theorems 3.5.2 and 3.5.7 of [linde:1986]). Clearly, and . Another application of Corollary 3.9 completes the proof.

Lemma 6.20.

Under the assumptions of Theorem 5.1, .

Proof 6.21.

Turning to the second term, observe first that

Setting we thus have

Consequently, , where

Next,

and

We see that condition (5.12) implies that .

Lemma 6.22.

Under the assumptions of Theorem 5.1, .