Ladder Chains: A Variation of Random Walks

Chenhe Zhang111Department of Mathematics, Zhejiang University, Hangzhou 310027, P.R.China; 3150104161@zju.edu.cn and Xiang Fang222Department of Mathematics, Zhejiang University, Hangzhou 310027, P.R.China; 3150103685@zju.edu.cn

Abstract. The authors propose a new variation of random walks called ladder chains . We extend concepts such as ruin probability, hitting time, transience and recurrence of random walks to ladder chain. Take for instance, we find the linear difference equations that the ruin probability and the hitting time satisfy. We also prove the recurrence of a critical case . All approaches of these results can be generalized to solve similar problems for other ladder chains.

AMS 2010 subject classification: 60G40, 60J75.

Keywords: random walks, probabilities of ruin, mean duration, ladder chains, transience and recurrence.

1 Introduction

Research on random walks has a long history. The random walk problem was first formally proposed by Pearson in 1905 [9]. At the same year, Rayleigh solved it and extended the problem to 2-dimensions [11]. Later on, Pólya discussed the recurrence of random walks of several dimensions in his paper [10]. After that, Erdős and Rényi initiated the study of random graphs in [4, 6] and greatly advanced the research on graph theory. There is also much research on discrete variations of random walks such as Lévy flight, random walks on Riemannian manifolds, and random walks on finite groups (see [12, 1]). In the past several decades, the related theoretical work has made a tremendous success in various fields, including but not limited to, physics, psychology, computer science, and solving Laplace’s equation (see [13, 8, 2, 7]).

However, to the best knowledge of the authors, there is little mature research on the variation of random walks as follows. Suppose is a sequence of independent and identically distributed random variables and is a stochastic process, where is a simple function of unrelated to . Define . Then it is natural to ask the three questions as below.

-

(Q-1)

What is the ruin probability for ?

-

(Q-2)

How to calculate the mean duration of this case?

-

(Q-3)

Can we define the transience and recurrence about similarly to Markov chains, along with an easy criterion?

Although it is easy to see that is a second order Markov chain, we cannot directly apply the properties of higher order Markov chain to answer the above questions. Therefore, we start from a new perspective and solve these kinds of problems using the methods for random walks in [14].

The rest of the paper is organized as follows. In Section 2, we give and prove the linear differential equation that the ruin probability satisfies, using reflection principle. This is followed in Section 3 by proving the existence of the mean duration and the linear difference equation it satisfies. Finally, we compute the “absorption probability” for a critical case and derive the recurrence of this case in Section 4.

2 How likely is the gambler ruin?

Think about such a question. Suppose two gambler A and B are gambling under the rule as follows. If A wins B, B gives A a coin; otherwise, A gives B a coin. Specially, if A wins B both this round and previous round, B has to give A an extra coin. We already know that the probability that A wins B is and they have and coins respectively. How likely is A before B to ruin within finite rounds? It is easy to find that this problem is a variation of the gambler’s ruin problem. To solve it, we first introduce some notations.

Consider the Bernoulli scheme , where

Let and . Define

| (2.1) |

and . For any and starting point , define and stopping time

| (2.2) |

where are two integers. Let

| (2.3) |

and

| (2.4) |

Obviously we have for any positive integer ,

| (2.5) |

as the boundary conditions.

Theorem 2.1.

For any integer , there exists and such that

Proof.

It is easy to see that is a sequence of increasing events. Therefore,

The monotone convergence theorem promises the convergence of , that is exists and is in . Similarly, we know exists and is in . ∎

The following theorem gives the values of and .

Theorem 2.2.

Suppose , then the defined above are the unique solution of the linear difference equation

| (2.6) |

And the defined above are the unique solution of the linear difference equation

| (2.7) |

Proof.

We only give the proof of . For we have

| (2.8) |

Similarly,

| (2.9) |

Notice that

| (2.10) |

and

| (2.11) |

so we have

| (2.12) |

For and positive integer , define

| (2.13) |

In other words, is the least positive number such that . Then we have

| (2.14) |

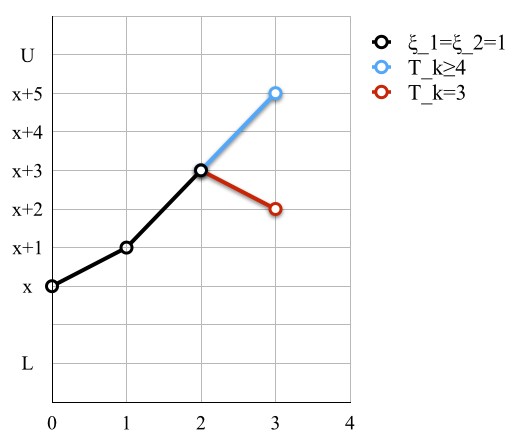

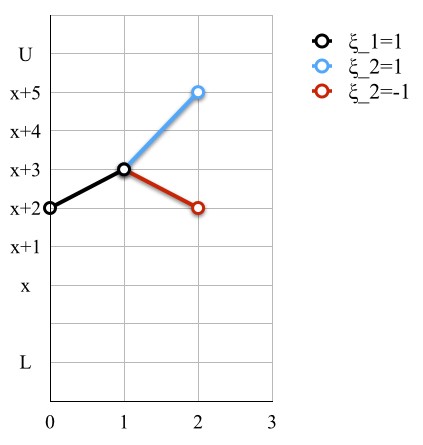

From the above two figures we can see that the paths

in satisfying are in one-to-one correspondence with the paths

in satisfying . By the reflection principle, we know

| (2.15) |

Furthermore,

| (2.16) |

which means that

| (2.17) |

| (2.18) |

and we get

| (2.19) |

According to Theorem 2.1 and (2.5), we finally find the linear difference equation that satisfies. According to the theory of linear difference equations, (2.7) has and only has one solution . By the same token, we can get the corresponding conclusion for . ∎

The answer to the question we asked at first is a direct corollary of the above theorem as follows.

Corollary 2.3.

Corollary 2.4.

For any integer , , where are two integers and follows Theorem 2.1.

Proof.

According to the Theorem 2.7 and its proof, whether or , and are integers or not, we always have the following corollary.

Corollary 2.5.

For any real number , there exists and such that

Furthermore, .

Hence, as the classic gambler’s ruin problem, we can conclude that there must be one of the two gamblers ruin within finite rounds.

3 When will a gambler ruin?

We have defined the as a stopping time from above. In this section, we will first give the linear difference equation that (obviously it exists because it is bounded) satisfies, and then prove the existence of for any integer and . For simplicity, we assume that and are two integers satisfying and is an integer between them in the rest of the paper.

Theorem 3.1.

The defined above are the unique solution of the linear difference equation

| (3.1) |

Proof.

For any given integer , define . Proceed as in the derivation of the recurrent relations for and we have

| (3.2) |

Furthermore,

| (3.3) |

Also,

| (3.4) |

Hence,

| (3.5) |

and

| (3.6) |

Combining the boundary conditions that

| (3.7) |

with (3.2) and (3.6) gives the linear difference equation showed in (3.1).

∎

Theorem 3.2.

For any integer and , there exists such that . The is called mean duration.

Proof.

See Appendix A. ∎

4 Ladder Chains

In this Section, we generalize the in the Section 2 to a specific -th order Markov Chain named ladder chain, denoted by , and prove the recurrence of .

4.1 Basic Concepts

Definition 4.1.

Suppose and is a positive integer. Define

| (4.1) |

and . Then we call the stochastic process a ladder chain with order , step , and probability , simply denoted by .

Similar to the transience and recurrence of a state of a Markov chain, we can define the transience and recurrence of a ladder chain here.

Definition 4.2.

A ladder chain is said to be transient if

| (4.2) |

Otherwise, the ladder chain is said to be recurrent.

4.2 Recurrence of

Before demonstrating the recurrence of the ladder chain , we first prove a rather intuitive theorem about the ruin probability when or are infinite.

Theorem 4.1.

Suppose and x is a given positive integer. Then for ,

| (4.3) |

Proof.

It is easy to see that the event

| (4.4) |

and

| (4.5) |

Therefore, we have

| (4.6) |

Solving the characteristic equation of (2.7) gives

| (4.7) |

Therefore, the general formula of is given by

| (4.8) |

where

| (4.9) |

Since for fixed ,

| (4.10) |

and for fixed ,

| (4.11) |

we know that

| (4.12) |

It suffices to apply for any and thus we have

| (4.13) |

which completes the proof. ∎

It is easy to see that the here is the probability such that of . We end the paper with a theorem about the transience and recurrence of the ladder chain . Since the corresponding properties of ladder chains with higher orders and steps can be derived by a similar method, we omit them in this paper.

Theorem 4.2.

The ladder chain is recurrent.

Proof.

Define , , and . Obviously, . On one hand,

| (4.14) |

By Theorem 4.3, we find for any and consequently

| (4.15) |

On the other hand,

| (4.16) |

For any satisfying , assume for contradiction that ; then it follows that and , which means that there exists some such that or 1 and .

| (4.17) |

For any , according to Theorem 4.3,

| (4.18) |

Substituting (4.18) into (4.17) and applying Theorem 4.3 again give

| (4.19) |

Therefore,

| (4.20) |

which completes the proof. ∎

Appendix A: Proof of Theorem 3.2

Theorem 3.2. For any integer and , there exists such that . The is called mean duration.

Proof.

We first prove that is bounded on for any , where and are two integers such that . We demonstrate it in two cases.

(Case a) .

The random variable describes the walk at the stopping time . Computing the expectation of both sides gives

| (4.21) |

From the definition of and , we can conclude that is only related with , and is only related with . Hence, by the independence among we know that and are mutually independent. It follows that

| (4.22) |

Besides, we have

| (4.23) |

and

| (4.24) |

If , then , which shows that

| (4.25) |

Similarly, if , then , which shows that

| (4.26) |

Substitute (4.22), (4.23), (4.24), (4.25), (4.26) into (4.21) and we find

| (4.27) |

Notice that in this case and Therefore, we have

| (4.28) |

is bounded on .

(Case b) .

| (4.29) |

In this case, we have . Simple computation gives

| (4.30) |

Then it follows that

| (4.31) |

Notice that

| (4.32) |

So we have

| (4.33) |

Besides,

| (4.34) |

First,

| (4.35) |

Also,

| (4.36) |

At last,

| (4.37) |

By (4.29), (4.31), (4.33), (4.34), (4.35), (4.36), (4.37), and the fact that we eventually find

| (4.38) |

which means that is bounded on . From the denifition of in (2.2), we can see obviously that , which means that is non-decreasing for any fixed . Hence, exists for any integer according to the monotone convergence theorem. ∎

Acknowledgements

We are grateful to Prof. Zhonggen Su and Prof. Qinghai Zhang for many useful discussions and suggestions on systemizing our ideas and polishing this paper.

References

- [1] Aldous, D. J. (1983). Random walks on finite groups and rapidly mixing Markov chains. Séminaire de probabilités 17 243-297

- [2] Bar-Yossefy, Z., Berg, A., Chienz, S., Fakcharoenpholx, J., and Weitz, D. (2000). Approximating Aggregate Queries about Web Pages via Random Walks. Proc Int Conf Very Large Data Bases 26 535-544

- [3] Cae̋r, G. L. (2011). A New Family of Solvable Pearson-Dirichlet Random Walks. Journal of Statistical Physics 144 23-45

- [4] Erdős, P. and Rényi, A. (1959). On random graphs I. Publicationes Mathematicae Debrecen 6 290-297

- [5] Erdős, P. and Rényi, A. (1960). On the Evolution of Random Graphs. The Mathematical Institute of the Hungarian Academy of Sciences 5 17-61

- [6] Gilbert, E. N. (1959). Random Graphs. The Annals of Mathematical Statistics 30(4) 1141-1144

- [7] Lawler, G. F. (2010). Random Walk and the Heat Equation. American Mathematical Society

- [8] Nosofsky, R. M. and Palmeri, T. J. (1997). An Exemplar-Based Random Walk Model of Speeded Classification. Psychological Review 104(2) 266-300

- [9] Pearson, K. (1905). The Problem of the Random Walk. Nature 72 294

- [10] Pólya, G. (1921). Űber eine Aufgabe der Wahrscheinlichkeitsrechnung betreffend die Irrfahrt im Strassennetz. Math. Ann. 84 149-160

- [11] Rayleigh, J. W. S. (1905). The Problem of the Random Walk. Nature 72 318

- [12] Roberts, P. H. and Ursell, H. D. (1960). Random Walk on a Sphere and on a Riemannian Manifold. Philosophical Transactions of the Royal Society of London. Series A, Mathematical and Physical Sciences 252 317-356

- [13] Sander, L. M. (2000). Diffusion-limited aggregation: a kinetic critical phenomenon? Contemporary Physics 41(4) 203-218

- [14] Shiryaev, A. N. (1995). Probability. Springer; 2nd edition

- [15] Stroock, D. W. (2005). An Introduction to Markov Processes. Springer