Estimation of multivariate asymmetric power GARCH models

Abstract

It is now widely accepted that volatility models have to incorporate the so-called leverage effect in order to model the dynamics of daily financial returns. We suggest a new class of multivariate power transformed asymmetric models. It includes several functional forms of multivariate GARCH models which are of great interest in financial modeling and time series literature. We provide an explicit necessary and sufficient condition to establish the strict stationarity of the model. We derive the asymptotic properties of the quasi-maximum likelihood estimator of the parameters. These properties are established both when the power of the transformation is known or is unknown. The asymptotic results are illustrated by Monte Carlo experiments. An application to real financial data is also proposed.

keywords:

Constant conditional correlation, multivariate asymmetric power GARCH models, quasi-maximum likelihood, threshold models1 Introduction

The ARCH (AutoRegressive Conditional Heteroscedastic) model has been introduced by Engle, (1982) in an univariate context. Since this work a lot of extensions have been proposed. A first one has been suggested four years later, namely the GARCH (Generalised ARCH) model by Bollerslev, (1986). This model had for goal to improve modeling by considering the past conditional variance (volatility). Their concept are based on the past conditional heteroscedasticity which depends on the past values of the return. A consequence is the volatility has the same magnitude for a negative or positive return.

Financial series have their own characteristics which are usually difficult to reproduce artificially. An important characteristic is the leverage effect which considers negative returns differently than the positive returns. This is in contradiction with the construction of the GARCH model, because it cannot consider the asymmetry. The TGARCH (Threshold GARCH) model introduced by Rabemananjara and Zakoïan, (1993) improves the modeling because it considers the asymmetry since the volatility is determined by the past negative observations and the past positive observations with different weights. Various asymmetric GARCH processes are introduced in the econometrics literature, for instance the EGARCH (Exponential GARCH) and the GARCH models (see Francq et al., (2013) who studied the asymptotic properties of the estimators for an EGARCH models).

The standard GARCH model is based on the concept that the conditional variance is a linear function of the squared past innovations whereas the TGARCH model is based on the concept of conditional standard deviation (also called volatility). In reality, as mentioned by Engle, (1982), other formulations (or several functional forms) of the volatility can be more appropriate. Motivated by Box-Cox power transformations, Higgins and Bera, (1992) proposed a general functional form for the ARCH model, the so-called PARCH (power-transformed ARCH) models in which the conditional variance is modeled by a power (see also Ding et al., (1993)). Hwang and Kim, (2004) extend the PARCH models to the class of asymmetric models: the power transformed asymmetric (threshold) ARCH (APARCH for short) model. Pan et al., (2008) generalized the APARCH (APGARCH) model by adding the past realizations of the volatility. Hamadeh and Zakoïan, (2011) studied the asymptotic properties of the APGARCH models.

When one uses an APGARCH model on real data, we often obtain interesting results on the power. In fact, as we can see on the Table 1, the power is not necessary equal to or and is different for each series.

| Exchange rates | |||||

|---|---|---|---|---|---|

| USD | 0.00279 | 0.02618 | 0.04063 | 0.96978 | 1.04728 |

| JPY | 0.00740 | 0.05331 | 0.08616 | 0.93580 | 1.12923 |

| GBP | 0.00240 | 0.06078 | 0.06337 | 0.94330 | 1.41851 |

| CAD | 0.00416 | 0.04054 | 0.03111 | 0.96114 | 1.56085 |

In the econometric applications, the univariate APGARCH framework is very restrictive. Despite the fact that the volatility of univariate series has been widely studied in the literature, modeling the realizations of several series is of great practical importance. When several series displaying temporal dependencies are available, it is useful to analyze them jointly, by viewing them as the components of a vector-valued (multivariate) process. Contrarily to the class of Vector Auto Regressive Moving Average (VARMA), there is no natural extension of GARCH models for vector series, and many MGARCH (multivariate GARCH) formulations are presented in the literature (see for instance Nelson, (1991), Engle and Kroner, (1995), Engle, (2002) and McAleer et al., (2008)). See also Bauwens et al., (2006), Silvennoinen and Teräsvirta, (2009) and Bauwens et al., (2012) for recent surveys on MGARCH processes. These extensions present numerous specific problems such that identifiabily conditions, estimation. Among the numerous specifications of MGARCH models, the most popular seems to be the Constant Conditional Correlations (CCC) model introduced by Bollerslev, (1990) and extended by Jeantheau, (1998) (denoted CCC-GARCH, in the sequel).

As mentioned before, to model the dynamics of daily financial returns, we need to incorporate the leverage effect to volatility models. Many asymmetric univariate GARCH models have been considered in the literature to capture the leverage effect, extensions to the multivariate setting have not been much developed. To our knowledge, notable exceptions are McAleer et al., (2009) who extend the GJR model (see Glosten et al., (1993)) to the CCC Asymmetric GARCH. Another extension is the Generalized Autoregressive Conditional Correlation (GARCC) model proposed by McAleer et al., (2008). Recently Francq and Zakoïan, (2012) proposed an asymmetric CCC-GARCH (CCC-AGARCH) model that includes the CCC-GARCH introduced by Bollerslev, (1990) and its generalization by Jeantheau, (1998). The attractiveness of the CCC-AGARCH models follows from their tractability (see Francq and Zakoïan, (2012)). Sucarrat et al., (2016) proposed a general framework for the estimation and inference in univariate and multivariate GARCH-X models (when covariates or other conditioning variables ”” are added to the volatility equation) with Dynamic Conditional Correlations of unknown form via the VARMA-X representation (Vector Auto Regressive Moving Average).

The main purpose of this paper is to introduce and study a multivariate version of the APGARCH models. In view of the results summarized in Table 1, it appears to be inadequate to consider a unique power for all the series. Hence we propose the CCC power transformed asymmetric (threshold) GARCH (denoted CCC-APGARCH or CCC-GARCH, where is a vector of powers and is the number of series considered). Our model includes for examples the CCC-AGARCH developed by Francq and Zakoïan, (2012) and of course, the most classical MGARCH model, the CCC-GARCH introduced by Bollerslev, (1990). An important feature in this family of models is that the interpretation of the coefficients and the conditional variance is simpler and explicit. We shall give a necessary and sufficient condition for the existence of a strictly stationary solution of the proposed model and we study the problem of estimation of the CCC-APGARCH.

For the estimation of GARCH and MGARCH models, the commonly used estimation method is the quasi-maximum likelihood estimation (QMLE for short). The asymptotic distribution of the Gaussian QMLE is obtained for a wide class of asymmetric GARCH models with exogenous covariates by Francq and Thieu, (2018). The asymptotic theory of MGARCH models are well-known in the literature. For instance Jeantheau, (1998) gave general conditions for the strong consistency of the QMLE for multivariate GARCH models. Comte and Lieberman, (2003) (see also Hafner and Preminger, (2009)) have proved the consistency and the asymptotic normality of the QMLE for the BEKK formulation (the acronym comes from synthesized work on multivariate models by Baba, Engle, Kraft and Kroner). Asymptotic results were established by Ling and McAleer, (2003) for the CCC formulation of an ARMA-GARCH. See also Bardet and Wintenberger, (2009) who studied the asymptotic behavior of the QMLE in a general class of multidimensional causal processes allowing asymmetries. Recently, the quasi-maximum likelihood (QML) results have been established for a MGARCH with stochastic correlations by Francq and Zakoïan, (2016) under the assumption that the system is estimable equation-by-equation. See also Darolles et al., (2018), who proved the asymptotic properties of the QML equation-by-equation estimator of Cholesky GARCH models and time-varying conditional betas. Francq and Sucarrat, (2017) prove the consistency and asymptotic normality of a least squares equation-by-equation estimator of a multivariate GARCH-X model with Dynamic Conditional Correlations by using the VARMA-X representation. Strong consistency and asymptotic normality of CCC-Periodic-GARCH models are established by Bibi, (2018). The asymptotic normality of maximum-likelihood estimator of Dynamic Conditional Beta is proved by Engle, (2016). In our context, we use the quasi-maximum likelihood estimation. The proofs of our results are quite technical. These are adaptations of the arguments used in Francq and Zakoïan, (2012) when the power is known, Hamadeh and Zakoïan, (2011) and Pan et al., (2008) when the power is unknown. We strength the fact that new techniques and arguments are applied in the proof of of the identifiability (see Subsection A.4.2 and in the proof of the invertibility of the Fisher information matrix (see Subsection A.5.5).

This paper is organized as follows. In Section 2 we introduce the CCC-APGARCH model and show that it includes some class of (M)GARCH models. We established the strict stationarity condition and we give an identifiability condition. Section 3 is devoted to the asymptotic properties of the quasi-maximum likelihood estimation when the power is known. In Section 4, we consider the estimation of . Wald test is developed in Section 5 in order to test the classical MGARCH model against a class of asymetric MGARCH models. The test can also be used to test the equality between the components of . Simulation studies and an illustrative application on real data are presented in Section 6 and we provide a conclusion in Section 7. The proofs of the main results are collected in the Appendix A.

2 Model and strict stationarity condition

In all this work, we use the following notation for .

2.1 Model presentation

The -dimensional process is called a CCC-APGARCH if it verifies

| (2.1) |

where and with and

and are vectors of size with strictly positive coefficients, and are matrices of size with positive coefficients and is a correlation matrix. The parameters of the model are the coefficients of the vectors , , the coefficients of the matrices and the coefficients in the lower triangular part excluding the diagonal of the matrix . The number of unknown parameters is

The innovation process is a vector of size and satisfies the assumption:

is an independent and identically distributed (iid for short) sequence of variables on with identity covariance matrix and .

With this assumption, the matrix is interpreted as the conditional variance (volatility) of .

The representation (2.1) includes various MGARCH models.

For instance, if we assume that , the model (2.1) can be viewed as a multivariate extension and generalization of the

the so-called PARCH (power-transformed ARCH) models introduced by Higgins and Bera, (1992) (denoted CCC-PGARCH, in the sequel). Moreover, if we also fixed the power vector we obtain the CCC-GARCH model proposed by Jeantheau, (1998). Now, if we assume that , the model CCC-AGARCH of Francq and Zakoïan, (2012) is retrieved. If we also fixed (the univariate case, we retrieve the APGARCH introduced by Pan et al., (2008).

As remarked by Francq and Zakoïan, (2012), the interest of the APGARCH model (2.1) is to consider the leverage effect observed for most of financial series. It is well known that a negative return has more effect on the volatility as a positive return. In fact, for the same magnitude, the volatility increases more if the return is negative than if it is positive. In general, the estimation of the coefficients of the model suggests that one may think that for some component by component.

Bollerslev, (1990) introduced the CCC-GARCH model with the assumption that the coefficients matrices and are diagonal. This assumption implies that the conditional variance of the -th component of depends only on their own past values and not on the past values of the other components. By contrast, in the model (2.1) (including the CCC-GARCH) the conditional variance of the -th component of depends not only on its past values but also on the past values of the other components. For this reason, Model (2.1) is referred to as the Extended CCC model by He and Teräsvirta, (2004).

2.2 Strict stationarity condition

A sufficient condition for strict stationarity of the CCC-AGARCH() is given by Francq and Zakoïan, (2012). For the model (2.1) the strict stationarity condition is established in the same way. For that sake we rewrite the first equation of (2.1) as

| (2.2) |

Using the third equation of model (2.1), we may write

| (2.3) |

where . To study the strict stationarity condition, we introduce the matrix expression for the model (2.1)

where

and

| (2.4) |

We have denoted , and (they are and matrices). The matrix is of size .

Let the top Lyapunov exponent of the sequence . It is defined by

Now we can state the following results. Their proofs are the same than the one in Francq and Zakoïan, (2012) so they are omitted.

Theorem 1

(Strict stationarity)

A necessary and sufficient condition for the existence of a strictly stationary and non anticipative solution process to model (2.1) is .

When , the stationary and non anticipative solution is unique and ergodic.

The two following corollaries are consequences of the necessary condition for strict stationarity. For a square matrix, denotes its spectral radius (i.e. the greatest modulus of its eigenvalues).

Corollary 1

Let be the matrix polynomial defined by for and define

Then, if the following equivalent properties hold:

-

The roots of are outside the unit disk,

-

.

Corollary 2

Suppose . Let be the strictly stationary and non anticipative solution of model (2.1). There exists such that and .

2.3 Identifiability condition

In this part, we are interested in the identifiability condition to ensure the uniqueness of the parameters in the CCC-APGARCH representation. This is a crucial step before the estimation.

The parameter is defined by

where and are defined by for , for , is the vector of powers and such that the ’s are the components of the matrix . The parameter belongs to the parameter space

The unknown true parameter value is denoted by

We adopt the following notation. For a matrix (which has to be seen as a parameter of the model), we write when the coefficients of the matrix are evaluated in the true value .

Let , and where is the backshift operator. By convention if and if .

If the roots of are outside the unit disk, we have from the compact expression:

| (2.5) |

The parameter is said to be identifiable if (2.5) does not hold true when is replaced by belonging to .

The assumption that the polynomials and have no common roots is not sufficient to consider that there is not another triple such that

| (2.6) |

This condition is equivalent as the existence of an operator such that

The matrix is unimodular if is a constant not equal to zero. If the common factor to both polynomials is unimodular,

the polynomials and are left-coprimes.

But in the vectorial case, suppose that , and are left-coprimes is not sufficient to consider that (2.6) have no solution for (see Francq and Zakoïan, (2012)).

To obtain a mild condition, for any column of the matrix operators , and , we denote by , , and their maximal degrees. We suppose that the maximal values of the orders are imposed:

| (2.7) |

where and are fixed integers.

We denote the column vector of the coefficients , the column vector of the coefficients in the column of , respectively and the column vector of the coefficients in the column of .

Proposition 1

(Identifiability condition)

If the matrix polynomials and are left-coprime, and if the matrix

has full rank , under the constraints (2.7) with and for any value of , then

3 Estimation when the power is known

In this section, we assume that is known. We write in order to simplify the writings. For the estimation of GARCH and MGARCH models, the commonly used estimation method is the QMLE, which can also be viewed as a nonlinear least squares estimation (LSE). The QML method is particularly relevant for GARCH models because it provides consistent and asymptotically normal estimators for strictly stationary GARCH processes under mild regularity conditions. For example, no moment assumptions on the observed process are required (see for instance Francq and Zakoïan, (2004) or Francq and Zakoïan, (2010)).

As remarked in Section 2, some particular cases of Model (2.1) are obtained for : the CCC-AGARCH introduced by Francq and Zakoïan, (2012) and the CCC model introduced by He and Teräsvirta, (2004) with . This section provides asymptotic results which can, in particular, be applied to those models.

3.1 QML estimation

The procedure of estimation and the asymptotic properties are similar to those of the model CCC-AGARCH introduced by Francq and Zakoïan, (2012).

The parameters are the coefficients of the vector , the matrices and , and the coefficients of the lower triangular part without the diagonal of the correlation matrix . The number of parameters is

The goal is to estimate the coefficients of the model (2.1). In this section, we note the parameter

where and are define by for for and . The parameter belongs to the parameter space

The unknown true value of the parameter is denoted by

The determinant of a square matrix is denoted by or .

Let be a realization of length of the unique non-anticipative strictly stationary solution of Model (2.1). Conditionally to nonnegative initial values , the Gaussian quasi-likelihood writes

where the are recursively defined, for , by

A quasi-likelihood estimator of is defined as any measurable solution of

| (3.1) |

where

3.2 Asymptotic properties

To establish the strong consistency, we need the following assumptions borrowed from Francq and Zakoïan, (2012):

and is compact,

and ,

For the distribution of is not concentrated on 2 points and .

if and are left-coprime and the matrix has full rank .

If the space is constrained by (2.7), Assumption A4 can be replaced by the more general condition

A4 with replaced by .

is a positive-definite correlation matrix for all .

To ensure the strong consistency of the QMLE, a compactness assumption is required (i.e A1). The assumption A2 makes reference to the condition of strict stationarity for the model (2.1). This assumption implies that for the true parameter , Model (2.1) admits a strictly stationary solution but is less restrictive concerning the other values . The second part of Assumption A2 implies that the roots of are outside the unit disk. Assumptions A3 and A4 or A4’

are made for identifiability reasons. In particular ensures that the process (for ) takes positive and negative values with a positive probability (if, for instance, the were

a.s. positive, the parameters for could not be identified).

We are now able to state the following strong consistency theorem.

Theorem 2

Let be a sequence of QMLE satisfying (3.1). Then, under or and A5, we have almost surely as

It will be useful to approximate the sequence by an ergodic and stationary sequence. Under Assumption A2 there exists a strictly stationary, non anticipative and ergodic solution of

| (3.2) |

We denote and and we define

To establish the asymptotic normality, the following additional assumptions are required:

, where is the interior of .

.

Assumption A6 prevents the situation where certain components of are equal to zero (more precisely the coefficients of the matrices in our model). One refers to Section 8.2 of Francq and Zakoïan, (2010) and Pedersen, (2017) for a discussion on this topic.

The second main result of this section is the following asymptotic normality theorem.

Theorem 3

Under the assumptions of Theorem 2 and A6–A7, when , we have

where is a positive-definite matrix and is a positive semi-definite matrix, defined by

Remark 1

In the one dimensional case (when ), we have with

This expression is in accordance with the one of Theorem 2.2 in Hamadeh and Zakoïan, (2011).

4 Estimation when the power is unknown

In this section, it is assumed that is unknown.

4.1 QML estimation

Now we consider the case when the power is unknown. Thus we consider joint estimation of and . In practice is difficult to identified, as it was remarked in Hamadeh and Zakoïan, (2011) for the APGARCH model. In line with Hamadeh and Zakoïan, (2011) we make the following assumption which is used to ensure that is identified. One refers to Remark 3.2 of Hamadeh and Zakoïan, (2011) for a discussion on how the following assumption differs from the one given in Pan et al., (2008).

has a positive density on some neighbourhood of zero.

To define the QML estimator of , we replace by in the expression of the criterion defined in (3.1) and we obtain recursively , for ,

A quasi-maximum likelihood estimator of is defined as any mesurable solution of

| (4.1) |

where

4.2 Asymptotic properties

To establish the consistency and the asymptotic normality, we need some assumptions similar to those we assumed when the power is known. We will assume with the parameter which is replaced by and the space parameter is replaced by .

Theorem 4

(Strong consistency)

Let be a sequence of QMLE satisfying (3.1). Then, under

or , A5 and A8, we have

almost surely when

Theorem 5

(Asymptotic normality)

Under the assumptions of Theorem 4, A6, A7 and A8, when , we have

where is positive-definite matrix and is a positive semi-definite matrix, defined by

5 Linear tests

The asymptotic normality results from Theorem 3 and Theorem 5 are used to test linear constraints on the parameter. We thus consider a null hypothesis of the form

| (5.1) |

where is a known matrix of rank and is a known vector of size . The Wald test is a standard parametric test for testing and it is particularly appropriate in the context of financial series. Let and be weakly consistent estimators of and involved in the asymptotic normality of the QMLE. For instance, and can be estimated by their empirical or observable counterparts given by

Under the assumptions of Theorem 5, and the assumption that the matrix is invertible, the Wald test statistic is defined as follows

We reject the null hypothesis for large values of . If (here correspond to the quantile of the Khi2 distribution of asymptotic level ), we could conclude that the powers of the model (2.1) are equals. Thus we can consider a model with equal powers and so we are able to reduce the dimension of the parameter space.

We can also test the equality between the components of the power . For instance, in the bivariate case with the orders fixed at , we take and in (5.1) (remind that ).

Via this kind of test, we can also test the asymmetric property. If we reject the asymmetric assumption, we can consider the standard CCC-PGARCH model and reduce the dimension of the parameter space.

We strength the fact that our normality results can not be used in order to determine the orders of the model (2.1). Indeed, this can be usually done when one tests the nullity of the coefficients of the matrix . If they are all equal to zero, we can consider a smaller order (and similarly with the matrices and with the order ). Unfortunately, the assumption A6 excludes the case of vanishing coefficients so we can not apply our results in this situation. One refers to Section 8.2 of Francq and Zakoïan, (2010) and Pedersen, (2017) for a discussion on this topic.

6 Numerical illustrations

In this section, we make some simulations with and we compute the QML estimator to estimate the coefficients of the model (2.1). The simulations are made with the open source statistical software R (see R Development Core Team, 2017) or (see http://cran.r-project.org/). We use the function nlminb() to minimize the quasi-likelihood.

6.1 Estimation when the power is known

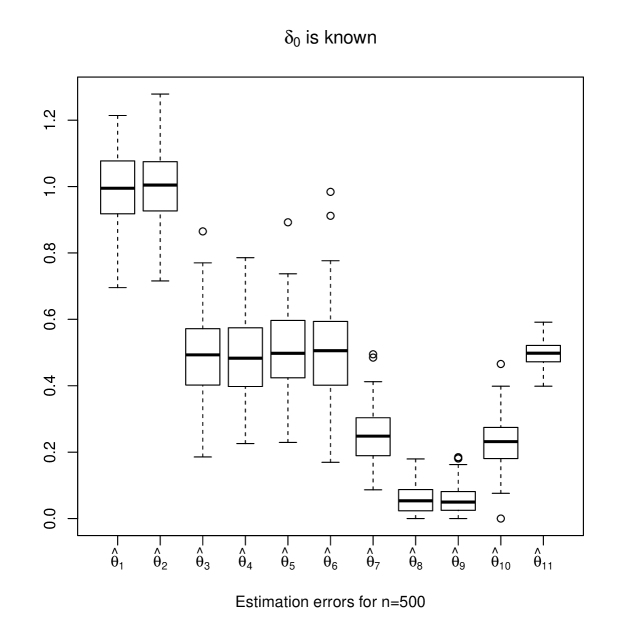

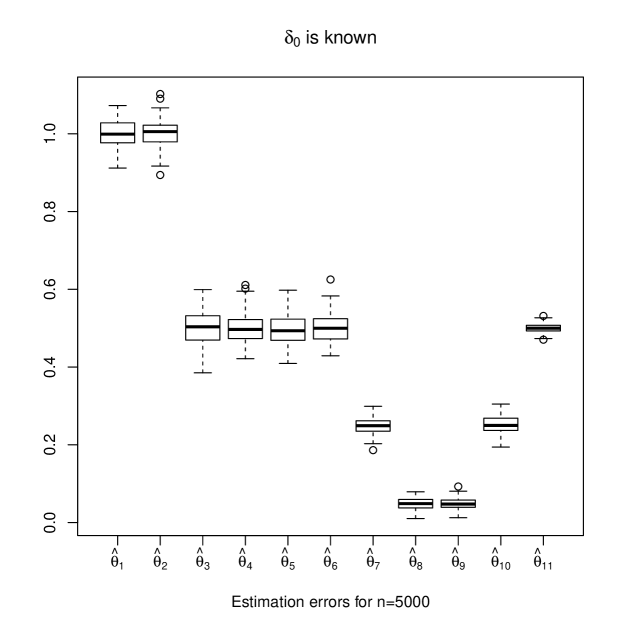

We fixed the orders of the model (2.1) at and . We computed the estimator on independent simulated trajectories to assess the performance of the QMLE in finite sample. The trajectories are made in dimension 2 with a length and .

The parameter used to simulate the trajectories are given in first row of the Table 2 and the space associated is chosen to satisfied the assumptions of Theorem 3. As expected, Table 2 shows that the bias and the RMSE decrease when the size of the sample increases. Figures 1 and 2 summarize via box-plot, the distribution of the QMLE for these simulations. Of course the precision around the estimated coefficients is better when the size of the sample increases (see Figures 1 and 2).

| Length | True val. | 1 | 0.25 | 0.05 | 0.5 | 0.5 | 0.5 |

| 1 | 0.05 | 0.25 | 0.5 | 0.5 | |||

| Bias | -0.00498 | 0.00180 | 0.00789 | -0.00525 | 0.00485 | -0.00471 | |

| -0.00090 | 0.00683 | -0.02083 | -0.01505 | 0.00122 | |||

| RMSE | 0.10714 | 0.08290 | 0.04520 | 0.12666 | 0.12379 | 0.03774 | |

| 0.12073 | 0.04308 | 0.07730 | 0.12738 | 0.15095 | |||

| Bias | 0.00105 | -0.00063 | -0.00024 | 0.00346 | -0.00324 | 0.00010 | |

| 0.00044 | -0.00175 | 0.00188 | 0.00175 | 0.00121 | |||

| RMSE | 0.03526 | 0.02129 | 0.01464 | 0.04219 | 0.03950 | 0.01143 | |

| 0.03745 | 0.01437 | 0.02220 | 0.03883 | 0.03890 | |||

6.2 Estimation when the power is unknown

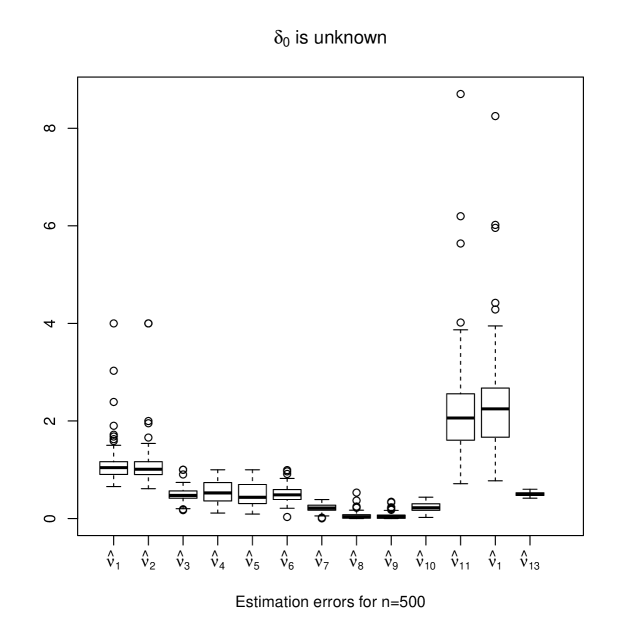

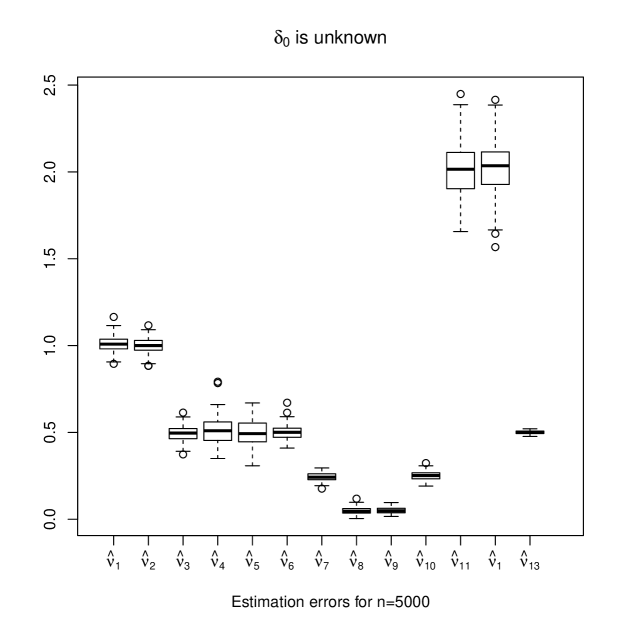

In this section, we also fixed the orders and of Model (2.1) and we estimate the parameter . We compute, as the previous section, the estimator on independent simulated trajectories in dimension 2 with sizes and . Table 3 presents the results of QMLE of the parameters including the powers . The results are satisfactory even for the parameter which is difficult to identify in practice (see Section 4.1 of Hamadeh and Zakoïan, (2011)) and which is more difficult to estimate than the others parameters. The conclusions are similar as in the case where is known. The dispersion around the parameter is much more precise when the sample size is . The bias and the RMSE decrease when the size of sample increases. Figure 3 shows the distribution of the parameter for the size . We remark that the estimation of the parameter has an important dispersion as regard to the other parameters. When the size of the sample is (see Figure 4), the estimation of the power is more accurate.

Table 4 displays the relative percentages of rejection of the Wald test proposed in Section 5 for testing the null hypothesis in the case of bivariate CCC-APGARCH, where is a matrix with 1 in positions and and 0 elsewhere and . We simulated independent trajectories of size and of Model (2.1) with , and . The nominal asymptotic level of the tests is . The values in bold correspond to the null hypothesis . We remark that the relative rejection frequencies of the Wald test are close to the nominal 5% level under the null, and are close to 100% under the alternative. We draw the conclusion that the proposed test well controls the error of first kind.

| Length | True val. | 1 | 0.25 | 0.05 | 0.5 | 0.5 | 2 | 0.5 |

| 1 | 0.05 | 0.25 | 0.5 | 0.5 | 2 | |||

| Bias | 0.12600 | -0.03211 | 0.00370 | -0.00853 | -0.00155 | 0.27015 | -0.00112 | |

| 0.11629 | 0.00937 | -0.02054 | 0.04720 | 0.00177 | 0.33354 | |||

| RMSE | 0.45385 | 0.08449 | 0.06808 | 0.14385 | 0.27142 | 1.13662 | 0.03772 | |

| 0.48839 | 0.07917 | 0.09275 | 0.26265 | 0.16417 | 1.14144 | |||

| Bias | 0.00921 | -0.00490 | 0.00082 | -0.00526 | -0.00574 | 0.00000 | -0.00013 | |

| 0.00072 | -0.00052 | 0.00183 | 0.01204 | 0.00196 | 0.00000 | |||

| RMSE | 0.05023 | 0.02434 | 0.01783 | 0.04278 | 0.07725 | 0.16761 | 0.01067 | |

| 0.04825 | 0.01935 | 0.02661 | 0.08433 | 0.04402 | 0.16004 | |||

| Length | |||||||

| 100.0 | 100.0 | 100.0 | 100.0 | 6.0 | 5.0 | ||

| Length | |||||||

| 100.0 | 100.0 | 83.0 | 100.0 | 80.0 | 100.0 | ||

6.3 Estimation on a real dataset

In this section, we propose to estimate the bivariate series returns of the daily exchange rates between the Dollar (USD) and the Yen (JPY) against the Euro (EUR). The observations cover the period from January 4, 1999 to July 13, 2017 which correspond to 4746 observations. The data were obtained from the website of the National Bank of Belgium (https://www.nbb.be). We divide the full period in three subperiods with equal length (): the first period runs from 1999-01-04 to 2005-03-02, the second from 2005-03-03 to 2011-05-05 and the last one from 2011-05-06 to 2017-07-13.

First, we consider the univariate case and an APGARCH model is estimated by QML on the full period and the three subperiods. Tables 5 and 6 show the univariate analysis of the two series (when is known and estimated, respectively) and give an idea of the behaviour of the modeling. We observe:

-

1.

a strong leverage effect (resp. no leverage effect) of the JPY with respect to its own past return for the full, first and second periods (resp. for the third periods) confirmed by the Wald test proposed in Section 5.

-

2.

almost no leverage effect is also confirmed by Wald test in the volatility of the USD for some periods

-

3.

a strong persistence of past volatility for the USD and JPY

-

4.

different values of the power for the USD in the three subperiods.

To give an idea of the reliability of the parameter estimates (in the bivariate case) obtained from the full period (4746 observations), the period has been divided into 3 subperiods as in the univariate analysis (see Tables 5 and 6). Tables 7 and 8 present the estimation of the model (2.1) for the bivariate series when is known and estimated, respectively. The conclusion is the same as in Tables 5 and 6. But we also remark a strong correlation between the two exchange rates. The power is equivalent to the univariate case and differs for each subperiod. We also note that none is equal to the others. The persistence matrix has a diagonal form and the persistence of past volatility is strong as in the univariate case. The coefficients corresponding to the negative returns are generally bigger than those for the positive returns and some of them are equal to zero. Since we obtain null estimated coefficients, we think that the assumption A6 is not satisfied and thus our asymptotic normality theorems do not apply. In future works we intent to study how the identification (orders and selection) procedure should be adapted in the CCC-APGARCH framework considered in the present paper by extending Section 8.2 of Francq and Zakoïan, (2010).

| Parameters | Full Period | First Period | Second Period | Third Period | |||||

|---|---|---|---|---|---|---|---|---|---|

| USD | JPY | USD | JPY | USD | JPY | USD | JPY | ||

| 0.00492 | 0.01107 | 0.01098 | 0.01245 | 0.00245 | 0.01192 | 0.00363 | 0.01115 | ||

| 0.5 | 0.02573 | 0.05211 | 0.02132 | 0.05832 | 0.03822 | 0.03087 | 0.00984 | 0.05656 | |

| 0.03512 | 0.06995 | 0.02919 | 0.07707 | 0.04447 | 0.06687 | 0.02780 | 0.06050 | ||

| 0.96960 | 0.93866 | 0.96626 | 0.93106 | 0.96405 | 0.94787 | 0.98016 | 0.94095 | ||

| 0.00293 | 0.00803 | 0.00803 | 0.00993 | 0.00184 | 0.00826 | 0.00176 | 0.00826 | ||

| 1 | 0.02628 | 0.05377 | 0.02205 | 0.06009 | 0.04306 | 0.02422 | 0.00127 | 0.06211 | |

| 0.04059 | 0.08504 | 0.03498 | 0.09537 | 0.04933 | 0.08989 | 0.03315 | 0.06808 | ||

| 0.96972 | 0.93620 | 0.96588 | 0.92635 | 0.96180 | 0.94543 | 0.98318 | 0.93977 | ||

| 0.00177 | 0.00597 | 0.00600 | 0.00815 | 0.00149 | 0.00564 | 0.00103 | 0.00637 | ||

| 1.5 | 0.02447 | 0.05075 | 0.02048 | 0.05620 | 0.04050 | 0.01979 | 0.00205 | 0.05886 | |

| 0.03803 | 0.08468 | 0.03274 | 0.09880 | 0.04617 | 0.09510 | 0.03102 | 0.06150 | ||

| 0.97041 | 0.93463 | 0.96675 | 0.92254 | 0.96131 | 0.94293 | 0.98273 | 0.94044 | ||

| 0.00113 | 0.00466 | 0.00456 | 0.00693 | 0.00120 | 0.00396 | 0.00064 | 0.00509 | ||

| 2 | 0.02100 | 0.04517 | 0.01672 | 0.04936 | 0.03408 | 0.01669 | 0.00406 | 0.05209 | |

| 0.03156 | 0.07586 | 0.02646 | 0.08730 | 0.03970 | 0.08730 | 0.02402 | 0.04845 | ||

| 0.97110 | 0.93242 | 0.96856 | 0.94046 | 0.96131 | 0.94046 | 0.98233 | 0.94082 | ||

| 0.00078 | 0.00378 | 0.00347 | 0.00597 | 0.00096 | 0.00285 | 0.00044 | 0.00425 | ||

| 2.5 | 0.01652 | 0.03838 | 0.01164 | 0.04137 | 0.02680 | 0.01340 | 0.00386 | 0.04405 | |

| 0.02438 | 0.06435 | 0.01945 | 0.08541 | 0.03246 | 0.07338 | 0.01624 | 0.03406 | ||

| 0.97161 | 0.92895 | 0.97126 | 0.91149 | 0.96114 | 0.93840 | 0.98284 | 0.94060 | ||

| Parameters | Full Period | First Period | Second Period | Third Period | ||||

|---|---|---|---|---|---|---|---|---|

| USD | JPY | USD | JPY | USD | JPY | USD | JPY | |

| 0.00279 | 0.00740 | 0.01070 | 0.00896 | 0.00127 | 0.00810 | 0.00185 | 0.00777 | |

| 0.02618 | 0.05331 | 0.02150 | 0.05864 | 0.03599 | 0.02394 | 0.00161 | 0.06189 | |

| 0.04063 | 0.08616 | 0.02992 | 0.09854 | 0.04158 | 0.09056 | 0.03302 | 0.06754 | |

| 0.96978 | 0.93580 | 0.96620 | 0.92450 | 0.96130 | 0.94531 | 0.98309 | 0.93990 | |

| 1.04728 | 1.12923 | 0.53666 | 1.24883 | 1.86581 | 1.02499 | 0.96029 | 1.10951 | |

| Parameters | Full Period | First Period | Second Period | Third Period | |

| 0.00535 | 0.33950 | 0.01813 | 0.06369 | ||

| 0.14680 | 0.33068 | 0.08347 | 0.09406 | ||

| 0.04265 | 0.01283 | 0.10252 | 0.14253 | ||

| 0.00000 | 0.00000 | 0.04520 | 0.00361 | ||

| 0.00484 | 0.11529 | 0.06218 | 0.02385 | ||

| 0.04232 | 0.03573 | 0.00000 | 0.07928 | ||

| 0.02825 | 0.00000 | 0.05721 | 0.02225 | ||

| 0.00000 | 0.00000 | 0.00000 | 0.00000 | ||

| 0.02203 | 0.03164 | 0.00000 | 0.06317 | ||

| 0.11239 | 0.17432 | 0.08536 | 0.04928 | ||

| 0.94718 | 0.37445 | 0.86761 | 0.73823 | ||

| 0.04727 | 0.00000 | 0.02670 | 0.00000 | ||

| 0.00000 | 0.00000 | 0.00000 | 0.00000 | ||

| 0.79038 | 0.63165 | 0.86991 | 0.87176 | ||

| 0.68316 | 0.74252 | 0.66079 | 0.69230 | ||

| 0.00600 | 0.06562 | 0.01928 | 0.04892 | ||

| 0.04538 | 0.12019 | 0.01354 | 0.02421 | ||

| 0.03022 | 0.02592 | 0.07476 | 0.09216 | ||

| 0.00526 | 0.00000 | 0.06385 | 0.00262 | ||

| 0.00000 | 0.00000 | 0.02459 | 0.00734 | ||

| 0.06315 | 0.04730 | 0.00443 | 0.07986 | ||

| 0.02421 | 0.02062 | 0.03516 | 0.03387 | ||

| 0.00000 | 0.0000 | 0.00000 | 0.00000 | ||

| 0.00808 | 0.00986 | 0.00000 | 0.01241 | ||

| 0.14923 | 0.25040 | 0.13401 | 0.05892 | ||

| 0.95080 | 0.82370 | 0.87099 | 0.77251 | ||

| 0.00000 | 0.00000 | 0.00000 | 0.00000 | ||

| 0.00000 | 0.00000 | 0.00528 | 0.00000 | ||

| 0.81186 | 0.65577 | 0.88146 | 0.88318 | ||

| 0.55335 | 0.61313 | 0.52596 | 0.56145 |

| Parameters | Full Period | First Period | Second Period | Third Period |

|---|---|---|---|---|

| 0.00136 | 0.00117 | 0.02407 | 0.11245 | |

| 0.06124 | 0.15275 | 0.01453 | 0.07930 | |

| 0.03050 | 0.00719 | 0.06434 | 0.04457 | |

| 0.00000 | 0.00000 | 0.06129 | 0.01818 | |

| 0.00000 | 0.05530 | 0.01975 | 0.00000 | |

| 0.05368 | 0.04459 | 0.00292 | 0.05135 | |

| 0.02351 | 0.00000 | 0.03112 | 0.02393 | |

| 0.00000 | 0.00613 | 0.00000 | 0.00000 | |

| 0.01072 | 0.00994 | 0.00000 | 0.00000 | |

| 0.12207 | 0.15270 | 0.12752 | 0.01499 | |

| 0.95326 | 0.41630 | 0.89072 | 0.90158 | |

| 0.03182 | 0.00000 | 0.00000 | 0.00000 | |

| 0.00000 | 0.00000 | 0.00382 | 0.00410 | |

| 0.80512 | 0.70082 | 0.88657 | 0.87580 | |

| 0.55106 | 0.61076 | 0.52380 | 0.57556 | |

| 2.01916 | 3.93035 | 1.95333 | 1.53699 | |

| 1.88965 | 1.72984 | 1.98917 | 1.77340 |

7 Conclusion

In this paper we propose a class of multivariate asymmetric GARCH models which includes numerous functional forms of MGARCH. We provide an explicit necessary and sufficient condition to the strict stationary of the proposed model. In addition the asymptotic properties of the QMLE are investigated in the two cases of known and unknown). We remark that moment conditions on the observed process are not needed. A Wald test is proposed to test linear constraints on the parameter. In Monte Carlo experiments we demonstrated that the QMLE of the CCC-APGARCH models provide some satisfactory results, at least for the models considered in our study.

Appendix A Appendix : Proofs of the main results

The proofs of our results are quite technical. These are adaptations of the arguments used in Francq and Zakoïan, (2012) when the power is known, Hamadeh and Zakoïan, (2011) and Pan et al., (2008) when the power is unknown. We strength the fact that new techniques and arguments are applied in the proof of of the identifiability (see Subsection A.4.2 and in the proof of the invertibility of the Fisher information matrix (see Subsection A.5.5).

A.1 Preliminaries

In the following technical proofs we will use the following notations. We will use the multiplicative norm defined as:

where is a matrix of size and is the Euclidian norm of vector and is the spectral radius. We recall that this norm satisfies

Moreover we have the following relation

as long as the matrix product is well defined (actually is a matrix).

We recall some useful derivation rules for matrix valued functions. If we consider a scalar function of a matrix , where all the are considered as a function of an one real variable , we have

| (A.1) |

For a non singular matrix , we have the following relations:

| (A.2) |

| (A.3) |

| (A.4) |

| (A.5) |

| (A.6) |

| (A.7) |

A.2 Proof of Theorem 2

We prove the consistency of the QMLE result when known following the same lines as in Francq and Zakoïan, (2012).

We first rewrite Equation (3.2) in the matrix form as follows:

| (A.8) |

with

and

For simplicity, one writes instead of when there is no possible confusion (and analogously one writes and ). We iterate the expression (A.8) and we obtain

| (A.9) |

The proof is decomposed in the four following points which will be treated in separate subsections.

-

Initial values do not influence quasi-likelihood: , almost surely.

-

Identifiability: if there exists such that almost surely and , then

-

Minimization of the quasi-likelihood on the true value: and if , .

-

For any there exists a neighborhood such that

(A.10)

A.2.1 Initial values do not influence quasi-likelihood

We define the vectors by replacing the variables , , in by and we have

| (A.11) |

where the vector is obtained by replacing in by the initial values.

From the Assumption A2 and Corollary 1, we have and we deduce from the compactness of that we have . Using the two iterative equations (A.8) and (A.11), we obtain almost surely that for any :

| (A.12) |

where is a random constant that depends on the past values of . We may write (A.12) as

| (A.13) |

Thus, for , since , the mean-value theorem implies that

| (A.14) |

and similarly

| (A.15) |

From (A.2.1) we can deduce that, almost surely, we have

| (A.16) |

Since is the inverse of the eigenvalue of smaller module of and , we have

| (A.17) |

by using the fact that is a positive-definite matrix (see assumption A5), the compactness of and the strict positivity of the components of . Similarly, we have

| (A.18) |

One may writes

We can rewrite the first term in the right hand side of the above inequality as

where we have used (A.16), (A.17) and (A.18). Using the Borel-Cantelli lemma and Corollary 2, we deduce that goes to zero almost surely. Consequently, the Cesáro lemma implies that when goes to infinity.

For the second term we use for and the inequality and we obtain

and, by symmetry, we have

Using (A.16), (A.17) and (A.18), we have

Using the same arguments as for , we conclude that goes to . We have shown that almost surely and thus is proved.

A.2.2 Identifiability

We suppose that for some we have

So we have . Remind that by (2.5) we have

We have a similar expression with the parameter :

Consequently we have

and

where

| (A.19) |

We remark that by the identifiability conditions. Using (2.2) and (2.3) we can write

where is measurable with respect to the -field generated by . Hence we have

where is another -measurable random matrix. Since is independent from and since , for some constant matrix . Since the matrices- are diagonal (see (2.3)), the element of the matrix satisfies

If , then takes at most two different values, which is in contradiction with A3. If and , then which entails , since , and then , a.s., which is also in contradiction with A3. We thus have . We argue similarly for for and by (A.19) we obtain that . Therefore, in view of (A.19), we may apply Proposition 1 because we assumed A4 (or A4’). Thus we have . We have thus established .

A.3 Proof of Theorem 3

Here, we prove the asymptotic normality result when is known. The prove is based on the standard Taylor expansion. We have

where the parameter is between and . To establish the asymptotic normality result when the power is known, we will decomposed the proof in six intermediate points as in Francq and Zakoïan, (2012).

-

First derivative of the quasi log-likelihood.

-

Existence of moments at any order of the score.

-

Asymptotic normality of the score vector:

(A.20) -

Convergence to :

(A.21) -

Invertibility of the matrix .

-

Asymptotic irrelevance of the initial values.

We shall need the following notations.

-

,

-

,

-

,

-

.

These notations will help us to point out the different entries of our parameter .

A.3.1 First derivative of log-likelihood

The aim of this subsection is to establish the expressions of the first order derivatives of the quasi log-likelihood. We shall use the following notations: ,

and , where with .

We recall the expression:

We differentiate with respect to for (that is with respect to ). We have

| (A.22) | ||||

| (A.23) |

We differentiate with respect to for (that is with respect to ). We have

| (A.24) | ||||

| (A.25) |

A.3.2 Existence of moments of any order of the score

-

(i)

For , in view of (A.23) we have

-

(ii)

For , in view of (A.25) we have

- (iii)

- (iv)

-

(v)

For , , in view of (A.25) we have,

To have the finiteness of the moments of the first derivative of the log-likelihood, it remains to treat the cases (i), (iii) and (iv) above. Thus, we have to control the term . Since

we can work component by component. We have for and

| (A.26) |

Control the term is equivalent to control in . So it is sufficient to prove that for any

| (A.27) |

For this purpose, we shall use the matrix expression (A.9). Three kinds of computations (listed (a), (b) and (c) below) are necessary according to the parameter with respect to which we differentiate.

-

(a)

We first differentiate with respect to and we obtain

and since (the vector composed with 0 and 1 at the th position for ), we have

where is the component of . So we have

(A.28) -

(b)

We differentiate with respect to . We have

with

where is a null matrix or a matrix whose entries are all zero except the one (equal to ) which is located at the same place of . Thus

and we have

(A.29) -

(c)

We now differentiate with respect to and we have

(A.30) The matrix is a matrix whose entries are all 0, apart from a 1 located at the same place as in . Thus and using (A.30), for all we obtain

Reasoning component by component, we have

(A.31) We use , with and the relation which is valid for all and . In view of (A.31), we obtain

with the constant which belongs to the interval . Since has moments of any order (see Corollary 2) we have proved that

(A.32)

Since (A.28) (as well as (A.29) and (A.32)) is an equivalent writing of (A.27) (as well as (A.29) and (A.32)), we deduce that (A.27) is true. By continuity of the functions that are involved on our estimations, the above inequalities are uniform on a neighborhood of : for all and all we have

| (A.33) |

A.3.3 Asymptotic normality of the score vector.

The proof is the same than the one in Francq and Zakoïan, (2012). It follows the following arguments:

-

1.

the process is stationary,

-

2.

is measurable with respect to the field generated by ,

-

3.

thus we have a martingale-difference sequence,

-

4.

Subsection A.3.2 implies that the matrix is well defined.

Using the central limit theorem from Billingsley, (1995) we obtain (A.20).

A.3.4 Convergence to

Expression of the second order derivatives of the log-likelihood

We start from the expression (A.22) and (A.24) in order to compute the second order derivatives of the log-likelihood. According to the index of , we have three cases:

- (i)

- (ii)

- (iii)

Thanks to the three above cases, we remark that to control the second order derivatives, it is sufficient to control the new term . Indeed, all the other terms in can be controlled thanks to the results from Subsection A.3.3.

Existence of the moments of the second order derivatives of the log-likelihood

We take derivatives in the expression (A.26) and we obtain

It only remains to control the last term in the right hand side of the above identity. We will prove that

| (A.37) |

By (A.8), we have for :

and we remark that

We also have

| (A.38) | ||||

| (A.39) |

and

| (A.40) |

We recall that the matrix is a matrix whose entries are all 0, apart from a 1 located at the same place as in .

Now we treat separately the three different expressions of the derivatives.

- (a)

- (b)

- (c)

We deduce from (A.41), (A.42) and (A.43) that (A.37) is true.

Once again, by continuity of the involved functions, the above inequalities are uniform on a neighborhood of : for all and all we have

| (A.44) |

Existence of the moments of the third order derivatives of the log-likelihood

First we write the quite heavy expressions of the third order derivatives derivatives with respect to the different parameters.

-

(i)

For , the derivatives with respect to , and will correspond to the derivatives with respect to the parameters , et . We obtain from (A.34) that

(A.45) with

-

(ii)

For which means that we differentiate with respect to the parameter , we differentiate (A.36) and we obtain

(A.46) with

-

(iii)

For (differentiation with respect to , and ) and for (differentiation with respect to ), we obtain from (A.35)

(A.47) where

- (iv)

In order to estimate the moments of order of the third order derivatives, we need to study the term which appears, for example, in the third term of namely . Indeed, using the fact that , we may write

| (A.49) |

Consequently we have to prove that for any ,

| (A.50) |

Letting , by (A.9) the component of equals

where is a strictly positive constant. For a sufficiently small neighborhood of , we have

for any and for all integer and all . Moreover, the coefficients et are bounded below by a constant uniformly in on . We thus obtain that

for some , all and all . We then deduce that

We distinguish two cases. If , the concavity of the function on implies, by the Jensen inequality, that

| (A.51) |

by using Corollary 2. Now, when , Corollary 2 entails that

| (A.52) |

In view of (A.51) and (A.52), for all , we deduce that

| (A.53) |

and (A.50) is true.

We also need to control the term . There are many other terms that involve derivatives of order one and two that we may control thanks our previous estimations. Moreover because .

The third order derivative of the matrix with respect to the parameters , and has the following expression for

The terms in which the first and second order derivatives of are involved are already controlled thanks to (A.33) and (A.44). Thus it remains to prove that

| (A.54) |

Starting from (A.9)

one may express the derivatives with respect to the different parameters. We only have to treat the derivatives

when and because the other derivatives vanish.

There are three cases.

-

(i)

For (this means that we differentiate with respect to the parameter ) and for fixed and , it holds

(A.55) Arguing as we did for the second order derivatives, we obtain

Consequently, it holds

(A.56) -

(ii)

For (corresponding to differentiation with respect to ) and for fixed and , we have

(A.57) and we write that

Hence we deduce that

(A.58) -

(iii)

For (that corresponds to the parameters ) and for fixed and such that , we have

(A.59) where denotes the th component of the matrix . By multiplying by , and we obtain

So we deduce that

(A.60)

The three above cases prove the existence of the moments of the third order derivatives. As before, our estimations are in fact uniform and we may write that on a neighborhood of , for all and , we have

| (A.61) |

These estimations imply that

| (A.62) |

By a Taylor expansion around , for all and it holds that

| (A.63) |

where lies between et . Using the almost sure convergence of to , the ergodic theorem and (A.62), we imply that almost-surely

Since , the second term in the right hand side of (A.63) converges to almost-surely. By the ergodic theorem and using the same arguments than in the proof of theorem 2.2 in Francq and Zakoïan, (2004) it follows that

| (A.64) |

A.3.5 Invertibility of the matrix

To prove the invertibility of the matrix we calculate the derivatives of the criterion and as functions of . We start from

and we have the first derivative

and the second derivative

Since

we compute the conditional expectation as follows (with the convention that ):

By the relation we have

where and . In view of we have with .

We define the matrices and ,

we have with .

Reasoning by contradiction, we suppose that is singular. There exists a non-zero vector , such that . Since almost surely, it means that , almost surely.

The matrix is definite-positive, then is too. This entails that is definite positive. This implies that is a definite-positive matrix with probability 1, and consequently with probability 1.

We write c as where and where (which is the dimension of the parameters ). The rows of the following equations

| dc | ||||

| (A.65) |

yield

| (A.66) |

by using (A.26). Differentiating the equation (2.1), we obtain that

where

Because Equation (A.66) is satisfied for all , we have

It follows that

Finally, we introduce the vector for which the first components are

One may obtain by choosing small enough in such a way that . If then . This is in contradiction with the identifiability assumption and thus . Consequently, Equation (A.65) becomes

and then

Since the vectors , are linearly independent, the vector is null and thus . This is in contradiction with almost-surely. Therefore the assumption that is not singular is absurd.

A.3.6 Asymptotic irrelevance of the initial values

To conclude the proof, we have to deduce (A.20) and (A.21) from (A.20) and (A.21). For this, we must show that the initial values have asymptotically no effect on the derivatives of the quasi likelihood. More precisely we may prove that

| (A.67) |

and

| (A.68) |

for some neighbourhood .

The arguments are the same than in Francq and Zakoïan, (2012).

By (A.22), it holds

with

The term is a sum of term which can be handled as and . Thus we need to prove that , , and . From (A.2.1), (A.16), (A.17) and (A.18), we deduce that for any

| (A.69) | ||||

We remark that . Thus the above estimations yield

| (A.70) |

By the matrix expressions (A.9) and (A.11), we have

where . Since, for all , we have

and

Since and (A.12) or (A.13), we obtain

or equivalently

| (A.71) |

By (A.26) we have the expression of the derivative of (and analogously for the derivative of ). Thus we may write, for that

Using, for , (A.13), (A.2.1), (A.69), (A.70), (A.71) and in view of (A.33), we obtain

| (A.72) |

where is a squared integrable variable. Using (2.2), from (A.53) and (A.69), we deduce

| (A.73) | ||||

| (A.74) |

where the random variable admits a fourth-order moment. Now, using (A.69)–(A.74) and the Cauchy-Schwarz inequality, we obtain

where is an integrable variable. From the Markov inequality, we have

which implies (A.67). By exactly the same arguments, we obtain

where is an integrable random variable. Using the Borel-Cantelli lemma and the Markov inequality, we deduce that goes to zero almost surely. Consequently, the Cesáro lemma implies that when goes to infinity, which entails (A.68).

The proof of Theorem 3 is completed.

A.4 Proof of Theorem 4

In the sequel, we will use the version of the matrix representation (A.8) when the parameter is unknown. We write

| (A.75) |

with

and

and we can iterate the expression and we have

| (A.76) |

We prove our consistency statement when is unknown. As in the case where was known (see Section A.2), the proof is decomposed in the four following points which will be treated in separate subsections.

-

A.4.1.

Initial values do not influence quasi-likelihood: a.s.

-

A.4.2.

Identifiability: If there exists such that almost surely and , then .

-

A.4.3.

Minimisation of the quasi log-likelihood on the true value: and if

-

A.4.4.

For any there exists a neighborhood such that

(A.77)

There are many similarities with the proof of Theorem 2. We only indicates where the fact that the power is estimated has an importance is our reasoning.

A.4.1 Initial values do not influence quasi-likelihood

The proof is the same than the one done in Subsection A.2.1 when the power is assumed to be known.

A.4.2 Identifiability

As regard to the proof of identifiability from Subsection A.2.2, it only remains to prove that if for , , a.s, then . Let (resp. ) the element of (resp. of ). We denote and . Under Assumption A4, by Proposition 1, for any , one may find and such that . Since the coefficients of the matrix are positive, we denote by the position of a non zero element, for . By (2.3) and (2.5) we have

where the quantities indexed by are measurable. In the same way we have

Since , a.s, we have

| (A.78) |

We denote and we introduce the function

By (A.78), almost-surely hence is almost surely constant on some neighborhood of zero (see Assumption A8). Hence for any :

almost-surely. Since the coefficients , , and are positive, we deduce that after differentiate twice the above equation. Starting now from

we can deduce by differentiating twice again, as in Hamadeh and Zakoïan, (2011), that . Hence we have . This is done for any so the result is proved.

A.4.3 Minimisation of the likelihood on the true value

Replacing by , the proof is the same than the one when the power is assumed to be known.

A.4.4 Proof of (A.77)

Once again, the proof is the same than the one when the power is assumed to be known.

A.4.5 Conclusion

A.5 Proof of Theorem 5

Now we deal with the asymptotic normality result when is unknown. We follow the arguments and the different steps that we used in the proof of Theorem 3 in Section A.3. To establish the asymptotic normality result when the power is known, the proof is again decomposed in six intermediates points.

-

A.5.1.

First derivative of the quasi log-likelihood

-

A.5.2.

Existence of moments at any order of the score

-

A.5.3.

Asymptotic normality of the score vector:

(A.79) -

A.5.4.

Convergence to :

(A.80) -

A.5.5.

Invertibility of the matrix

-

A.5.6.

Asymptotic irrelevance of the initial values

We introduce the following notations:

-

,

-

,

-

,

-

,

-

.

A.5.1 First derivative of the quasi log-likelihood

The aim of this subsection is to establish the expressions of the first order derivatives of the quasi log-likelihood. We may argue as in subsection A.3.1.

We denote ,

and , where with .

When we differentiate with respect to for (that is with respect to ) we obtain:

| (A.81) | ||||

| (A.82) |

We differentiate with respect to for (that is with respect to ). We have

| (A.83) | ||||

| (A.84) |

A.5.2 Existence of moments at any order for the score

Arguing as in the beginnig of Subsection A.3.2 we have:

-

(i)

for

-

(ii)

for

-

(iii)

for

-

(iv)

for and

-

(v)

and finally for , we have

To have the finiteness of the moments of the first derivative of the quasi log-likelihood, it remains to treat the cases (i), (iii) and (iv) above. Thus, we have to control the term . Since

we can work component wise.

All the computations that we have done in Subsection A.3.2 are valid. This means that we have the same estimations on the derivatives as long as we differentiate with respect to for (that is when we do not differentiate with respect to for ). Indeed, for and , we have

| (A.85) |

and the reasonings are unchanged.

So we can focus ourselves on the derivatives with respect to :

| (A.86) |

where denotes the Kronecker symbol. Using the matrix expression (A.76), we calculate the derivatives for (with ) and for :

with

Differentiating with respect to corresponds to a differentiation with respect to for an index . In the following computations, it is easy to work with an arbitrary order of derivation. So we write, for an order of derivation , that

and we have

By convention, we consider when is negative and when is positive.

Using the inequality

valid for any where , and the fact that for all , we obtain

We have , for all (see Corollary 2). So we obtain

with for :

By stationarity, we treat only the terms and the computations are identical when one replaces by so we will only to treat . We have for any

It follows that

| (A.87) |

with obvious notations. Using the Markov inequality one has

| (A.88) |

The second term is more difficult. One has to use the property

| (A.89) |

This is the Assumption A1 in Pan et al., (2008) and in our case, it is a consequence of the fact that has a positive density on some neighborhood of zero (see Assumption A8). We apply this property to . Indeed one may find some such that is small. Thus for any :

| (A.90) |

Hence, the second term satisfies

| (A.91) |

We use (A.88) and (A.91) in (A.5.2) and we obtain that

This yields

and it can be similarly be shown that, for any :

| (A.92) |

or equivalently that for any

| (A.93) |

A.5.3 Asymptotic normality of the score vector

The arguments are the same than in the case of known power (see subsection A.3.3).

A.5.4 Convergence to

Expression of the second order derivatives of the log-likelihood

First one may remark that the algebraic expressions of the second order derivatives (A.34), (A.35) and (A.36) are unchanged (even if the values of and take into account the parameter ). To control the derivates at the second order it is sufficient to control the term . For this, it necessary to calculate the second order derivatives of .

Existence of the moments of the second order derivatives of the log-likelihood

We give now the expressions of the second order derivatives of .

-

(i)

For , we have

-

(ii)

for and , we obtain

-

(iii)

for , and such that , we have

-

(iv)

for , we have

-

(v)

finally for , we obtain

Since the first order derivatives are already controlled, and since the estimations done in the case with known power, it remains to prove that

| (A.94) |

By (A.76), we have

It is easy to notice that

and for

It remains to treat three cases to prove (A.94).

-

(a)

For we have

where is a matrix with only one non null element equal 1 at the place of . It follows that

Using the same techniques used to prove (A.93) with , we obtain that

-

(b)

For it holds

Consequently

and we proceed as in the previous case to conclude that

- (c)

The above arguments can be generalized on a neighborhood of of . So we have for all and all :

Using the same arguments as in Subsection A.3.4 combined with the previous modification taking into account that the power is unknown (especially the estimation (A.93) with ) we obtain that for and , it holds

A.5.5 Invertibility of the matrix

Replacing by in the arguments that lead to (A.65), one obtains that the rows of the following equations

| dc | (A.95) |

yield

| (A.96) | ||||

| (A.97) |

Under A8, Equation (A.97) is equivalent to

Since the vectors , are linearly independent, the vector is null. Consequently, Equation (A.95) becomes

or equivalently

| (A.98) |

In view of (2.1), the component of is

| (A.99) | ||||

For , from (A.85) and (A.86), Equation (A.98) reduces as

| (A.100) |

From (A.99), the derivatives are defined recursively by

for , where is defined by

| (A.101) | ||||

Let a random variable measurable with respect to .

We restrict ourselves to the particular case of a CCC-APGARCH (see (2.1)). The general case can be easily deduced from the following arguments. We thus have

Combining the above expressions and (A.101), under A8, Equation (A.100) becomes

which is equivalent, almost surely, to the following two equations

| (A.102) | ||||

| (A.103) | ||||

It follows from A8 that, for some ,

| (A.104) | ||||

| (A.105) | ||||

for any . Differentiating three times Equations (A.104) and (A.105) with respect to , for , we obtain that

Under Assumption if it is impossible to have , for all . Then there exists such that and then we have . Equations (A.104) and (A.105) become

| (A.106) | ||||

| (A.107) | ||||

Differentiating twice again Equations (A.106) and (A.107) with respect to , we find that

Since the law of is non degenerated (see Assumption A3), we deduce that

So . Since is arbitrary, we deduce that for any , or equivalently that .

Thus the vector is null. We recall that is null, the invertibility of the matrix is thus shown in this case of a CCC-APGARCH.

In the general case of a CCC-APGARCH, we show by induction that (A.98) entails necessarily

which is impossible under Assumption A4 and thus .

This is in contradiction with almost-surely. Therefore the assumption that is not singular is absurd.

A.5.6 Asymptotic irrelevance of the initial values

It suffices to adapt the arguments used in Subsection A.3.6 when the power is known.

References

- Bardet and Wintenberger, (2009) Bardet, J.-M. and Wintenberger, O. (2009). Asymptotic normality of the quasi-maximum likelihood estimator for multidimensional causal processes. Ann. Statist., 37(5B):2730–2759.

- Bauwens et al., (2012) Bauwens, L., Hafner, C. M., and Laurent, S. (2012). Handbook of volatility models and their applications, volume 3. John Wiley & Sons.

- Bauwens et al., (2006) Bauwens, L., Laurent, S., and Rombouts, J. V. K. (2006). Multivariate GARCH models: a survey. J. Appl. Econometrics, 21(1):79–109.

- Bibi, (2018) Bibi, A. (2018). Asymptotic Properties of QML Estimation of Multivariate Periodic CCC – GARCH Models. Math. Methods Statist., 27(3):184–204.

- Billingsley, (1995) Billingsley, P. (1995). Probability and measure. Wiley Series in Probability and Mathematical Statistics. John Wiley & Sons, Inc., New York, third edition. A Wiley-Interscience Publication.

- Bollerslev, (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31:307–327.

- Bollerslev, (1990) Bollerslev, T. (1990). Modelling the coherence in short-run nominal exchange rates: a multivariate generalized arch model. The review of economics and statistics, pages 498–505.

- Comte and Lieberman, (2003) Comte, F. and Lieberman, O. (2003). Asymptotic theory for multivariate GARCH processes. J. Multivariate Anal., 84(1):61–84.

- Darolles et al., (2018) Darolles, S., Francq, C., and Laurent, S. (2018). Asymptotics of Cholesky GARCH models and time-varying conditional betas. J. Econometrics, 204(2):223–247.

- Ding et al., (1993) Ding, Z., Granger, C. W., and Engle, R. F. (1993). A long memory property of stock market returns and a new model. Journal of empirical finance, 1:83–106.

- Engle, (2002) Engle, R. (2002). Dynamic conditional correlation: a simple class of multivariate generalized autoregressive conditional heteroskedasticity models. J. Bus. Econom. Statist., 20(3):339–350.

- Engle, (1982) Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica: Journal of the Econometric Society, pages 987–1007.

- Engle, (2016) Engle, R. F. (2016). Dynamic conditional beta. Journal of Financial Econometrics, 14(4):643–667.

- Engle and Kroner, (1995) Engle, R. F. and Kroner, K. F. (1995). Multivariate simultaneous generalized arch. Econometric Theory, 11(1):122–150.

- Francq and Sucarrat, (2017) Francq, C. and Sucarrat, G. (2017). An equation-by-equation estimator of a multivariate log-GARCH-X model of financial returns. J. Multivariate Anal., 153:16–32.

- Francq and Thieu, (2018) Francq, C. and Thieu, L. Q. (2018). Qml inference for volatility models with covariates. Econometric Theory, pages 1–36.

- Francq et al., (2013) Francq, C., Wintenberger, O., and Zakoïan, J.-M. (2013). GARCH models without positivity constraints: exponential or log GARCH? J. Econometrics, 177(1):34–46.

- Francq and Zakoïan, (2004) Francq, C. and Zakoïan, J.-M. (2004). Maximum likelihood estimation of pure GARCH and ARMA-GARCH processes. Bernoulli, 10(4):605–637.

- Francq and Zakoïan, (2010) Francq, C. and Zakoïan, J.-M. (2010). GARCH Models: Structure, Statistical Inference and Financial Applications. Wiley.

- Francq and Zakoïan, (2012) Francq, C. and Zakoïan, J.-M. (2012). QML estimation of a class of multivariate asymmetric GARCH models. Econometric Theory, 28:179–206.

- Francq and Zakoïan, (2016) Francq, C. and Zakoïan, J.-M. (2016). Estimating multivariate volatility models equation by equation. J. R. Stat. Soc. Ser. B. Stat. Methodol., 78(3):613–635.

- Glosten et al., (1993) Glosten, L. R., Jagannathan, R., and Runkle, D. E. (1993). On the relation between the expected value and the volatility of the nominal excess return on stocks. The journal of finance, 48:1779–1801.

- Hafner and Preminger, (2009) Hafner, C. M. and Preminger, A. (2009). On asymptotic theory for multivariate GARCH models. J. Multivariate Anal., 100(9):2044–2054.

- Hamadeh and Zakoïan, (2011) Hamadeh, T. and Zakoïan, J.-M. (2011). Asymptotic properties of LS and QML estimators for a class of nonlinear GARCH processes. Journal of Statistical Planning and Inference, 141:488–507.

- He and Teräsvirta, (2004) He, C. and Teräsvirta, T. (2004). An extended constant conditional correlation garch model and its fourth-moment structure. Econometric Theory, 20(5):904–926.

- Higgins and Bera, (1992) Higgins, M. L. and Bera, A. K. (1992). A class of nonlinear ARCH models. Internat. Econom. Rev., 33(1):137–158.

- Hwang and Kim, (2004) Hwang, S. Y. and Kim, T. Y. (2004). Power transformation and threshold modeling for ARCH innovations with applications to tests for ARCH structure. Stochastic Process. Appl., 110(2):295–314.

- Jeantheau, (1998) Jeantheau, T. (1998). Strong consistency of estimators for multivariate ARCH models. Econometric Theory, 14(1):70–86.

- Ling and McAleer, (2003) Ling, S. and McAleer, M. (2003). Asymptotic theory for a vector ARMA-GARCH model. Econometric Theory, 19(2):280–310.

- McAleer et al., (2008) McAleer, M., Chan, F., Hoti, S., and Lieberman, O. (2008). Generalized autoregressive conditional correlation. Econometric Theory, 24(6):1554–1583.

- McAleer et al., (2009) McAleer, M., Hoti, S., and Chan, F. (2009). Structure and asymptotic theory for multivariate asymmetric conditional volatility. Econometric Rev., 28(5):422–440.

- Nelson, (1991) Nelson, D. B. (1991). Conditional heteroskedasticity in asset returns: a new approach. Econometrica, 59(2):347–370.

- Pan et al., (2008) Pan, J., Wang, H., and Tong, H. (2008). Estimation and tests for power-transformed and threshold GARCH models. J. Econometrics, 142(1):352–378.

- Pedersen, (2017) Pedersen, R. S. n. (2017). Inference and testing on the boundary in extended constant conditional correlation GARCH models. J. Econometrics, 196(1):23–36.

- Rabemananjara and Zakoïan, (1993) Rabemananjara, R. and Zakoïan, J.-M. (1993). Threshold ARCH models and asymmetries in volatility. Journal of Applied Econometrics, 8:31–49.

- Silvennoinen and Teräsvirta, (2009) Silvennoinen, A. and Teräsvirta, T. (2009). Multivariate GARCH Models, pages 201–229. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Sucarrat et al., (2016) Sucarrat, G., Grønneberg, S., and Escribano, A. (2016). Estimation and inference in univariate and multivariate log-GARCH-X models when the conditional density is unknown. Comput. Statist. Data Anal., 100:582–594.

Estimation of multivariate asymmetric power GARCH models:

Complementary results that are not submitted for publication

Appendix B Details on the proof of Theorem 2

B.1 Minimization of the quasi-likelihood on the true value

The criterion is not integrable on all point, but we first prove that is well defined on for all . Indeed we have

Now we show that is well defined on . We use , the Jensen inequality and the Corollary 2

Therefore we have

Since for any , and we deduce that is well defined in . So, when one studies the function , we can restrict our study to the values of such that .

We denote the positive eigenvalues of . We have

where we have used the inequality , for all . But, if , , then the inequality is strict, except if for all , a.s. This condition means that a.s. It follows a.s. and . By the identifiability proved in subsection A.2.2, we deduce that .

B.2 Proof of (A.10)

We recall that

For and an integer , we denote the open ball of radius centered on . We have

Then

and by subsection A.2.1 we deduce that

| (B.1) |

We can not apply the classical ergodic theorem to because of the lack of integrability mentioned in Subsection B.1. So we use an extension of the classical ergodic theorem (see Billingsley, (1995) pages 284 and 495) and we have

By Beppo-Levi’s theorem we have, when goes to infinity

Hence (B.2) implies that

and (A.10) follows from the result stated in Subsection B.1.

B.3 Conclusion: proof of Theorem 2

By Subsection A.2.1, and by the ergodic theorem, we have . Consequently, exists and is . Since , we have

Then for a small neighborhood of

| (B.2) |

The parameter space can be covered as

with is a neighborhood of verifying . By the compactness of , there exists a finite covering of

and then

| (B.3) |

Suppose that for all , there exist such that with . Let , we have by (B.2) that there exists such that for all ,

and by (A.10), for , we obtain the existence of such that for all ,

We can suppose that and by the two latter relations and (B.3), we have for

Then we will have

then

| (B.4) |

But by (A.10) we have and this is in contradiction to (B.4).

For large enough, we conclude that belongs to .