Abstract.

This paper studies the income fluctuation problem with capital income risk (i.e., dispersion in the rate of return to wealth). Wealth returns and labor earnings are allowed to be serially correlated and mutually dependent. Rewards can be bounded or unbounded. Under rather general conditions, we develop a set of new results on the existence and uniqueness of solutions, stochastic stability of the model economy, as well as efficient computation of the ergodic wealth distribution. A variety of applications are discussed. Quantitative analysis shows that both stochastic volatility and mean persistence in wealth returns have nontrivial impact on wealth inequality.

Keywords: Income fluctuation, optimality, stochastic stability, wealth distribution.

The Income Fluctuation Problem with Capital Income Risk:

Optimality and Stability111We thank Jess Benhabib, Christopher Carroll, Fedor Iskhakov, Larry Liu, Ronald Stauber and Chung Tran for valuable feedback and suggestions, as well as audience members at the RSE seminar at the Australian National University in 2017.

Email addresses: qingyin.ma@anu.edu.au, john.stachurski@anu.edu.au,

atoda@ucsd.edu.

Qingyin Maa, John Stachurskib and Alexis Akira Todac

a, bResearch School of Economics, The Australian National University

cDepartment of Economics, University of California, San Diego

November 15, 2018

1. Introduction

The income fluctuation problem refers to the broad class of decision problems that characterize the optimal consumption-saving behavior for agents facing stochastic income streams. In most cases, agents are subject to idiosyncratic shocks and borrowing constraints. Markets are incomplete so idiosyncratic risks cannot be fully diversified or hedged. The model represents one of the fundamental workhorses of modern macroeconomics, and has been adopted to study a large variety of important topics, ranging from asset pricing, life-cycle choice, fiscal policy, social security, to income and wealth inequality, among many others. See, for example, Schechtman (1976), Deaton and Laroque (1992), Huggett (1993), Aiyagari (1994), Carroll (1997), Chamberlain and Wilson (2000), Cagetti and De Nardi (2008), De Nardi et al. (2010), Guner et al. (2011), Guvenen (2011), Meghir and Pistaferri (2011), Meyer and Sullivan (2013), Guvenen and Smith (2014) and Heathcote et al. (2014).

In recent years, researchers have come to investigate an important mechanism in the income fluctuation framework—the dispersion in rates of return to wealth, referred to below as the capital income risk. Early studies are provided by Angeletos and Calvet (2005) and Angeletos (2007). These works highlight that the macroeconomic effects of idiosyncratic capital income risk can be both qualitatively distinct from those of idiosyncratic labor income risk and quantitatively significant.

An especially important set of applications concerns wealth inequality. As is well known in the literature, the classic income fluctuation frameworks of Huggett (1993) and Aiyagari (1994), in which returns to wealth are homogeneous across agents, fail to reproduce the high inequality and the fat upper tail of wealth distributions in many economies. Such empirical failure has prompted researchers to investigate models with uninsured capital income risk. Entrepreneurial risk, a representative example of capital income risk, is studied by Quadrini (2000) and Cagetti and De Nardi (2006). By introducing heterogeneity across agents in their work and entrepreneurial ability, these studies successfully generate skewed wealth distributions that are more similar to those observed in the U.S. data.

Moreover, in an OLG economy with intergenerational transmission of wealth, Benhabib et al. (2011) show that capital income risk is the driving force of the heavy-tail properties of the stationary wealth distribution. In a Blanchard-Yaari style economy, Benhabib et al. (2016) show that idiosyncratic investment risk has a big impact on generating a double Pareto stationary wealth distribution. In another important contribution, Gabaix et al. (2016) point out that a positive correlation of returns with wealth (“scale dependence”) in addition to persistent heterogeneity in returns (“type dependence”) can well explain the speed of changes in the tail inequality observed in the data. An important work that is highly pertinent to the present paper is Benhabib et al. (2015). In a stylized infinite horizon income fluctuation problem with capital income risk, the authors prove that there exists a unique stationary wealth distribution that displays fat tail.

On the empirical side, using twelve years of population data from Norway’s administrative tax records, Fagereng et al. (2016a, b) document that individuals earn markedly different average returns to both their financial assets (a standard deviation of ) and net worth (a standard deviation of ). Wealth returns are heterogeneous both within and across asset classes. Returns are positively correlated with the wealth level and highly persistent over time. In addition, wealth returns are (mildly) correlated across generations.

Although theoretical, empirical and quantitative studies all reveal the significant economic impact of capital income risk, existing models of capital income risk in the income fluctuation framework are highly stylized. For example, the assumptions of iid labor income process, iid wealth return process and their mutual independence made by Benhabib et al. (2015) are rejected by the empirical data in several economies (see, e.g., Kaplan and Violante (2010), Guvenen and Smith (2010) and Fagereng et al. (2016a, b)). As Benhabib et al. (2015) point out, adding positive correlations in labor earnings and wealth returns enriches model dynamics in that it captures economic environments with limited social mobility.

To our best knowledge, a general theory of capital income risk in the income fluctuation framework has been missing in the literature. This raises concerns about whether or not existing views on the economic impact of capital income risk hold in general, as well as whether or not modeling capital income risk in more generic and realistic settings is technically achievable. To be specific, several important questions are:

-

•

Do correlations in the wealth return process (e.g., those caused by mean persistence or stochastic volatility of wealth returns) enhance or dampen the macroeconomic impact of capital income risk?

-

•

What if, in addition to serial correlation, the wealth return process and the labor earnings process are mutually correlated?

-

•

Does an optimal policy always exist in these generalized settings? If it does, is it unique?

-

•

Does the stochastic law of motion for optimal wealth accumulation yield a stationary distribution of wealth?

-

•

If it does, is the model economy globally stable, in the sense that the stationary distribution is unique and can be approached by the distributional path from any starting point?

-

•

How do we compute the optimal policy and the stationary wealth distribution in practice?

These questions are highly significant, in the sense that a negative answer to any of them will pose a threat to the existing findings concerning capital income risk. However, due to technical limitations, these questions have not been investigated in a general income fluctuation framework. In this paper, we attempt to fill this gap. To this end, we extend the standard income fluctuation problem by characterizing the following essential features.

-

•

Agents face idiosyncratic rate of return to wealth (capital income risk) and idiosyncratic labor earnings (labor income risk), both of which are affected by a generic, exogenous Markov process .

-

•

Supports of and are bounded or unbounded, and, in either case, allowed to contain zero.

-

•

The reward (utility) function is bounded or unbounded, and no specific structure is imposed beyond differentiability, concavity and the usual slope conditions.

As can be seen, general and processes that are serially correlated and mutually dependent are covered by our framework. Moreover, consumption can become either arbitrarily small or arbitrarily large, so that agents are allowed to borrow up to the highest sustainable level of debt, creating rich and substantial model dynamics reflecting agents’ borrowing activity.222See the discussion of Rabault (2002).

We make several tightly connected contributions on optimality, stochastic stability and computation of this generalized income fluctuation problem.

First, we prove that the Coleman operator adapted to this framework is indeed an “-step” contraction mapping in a complete metric space of candidate consumption policies, even when rewards are unbounded. The unique fixed point is shown to be the optimal policy (also unique in the candidate space), and several important properties (e.g., continuity and monotonicity) are derived. To tackle unboundedness, we draw on and extend Li and Stachurski (2014) by adding capital income risk and constructing a metric that evaluates consumption differences in terms of marginal utility. To obtain contractions under a minimal level of restriction, we focus our key assumption on bounding the long-run growth rate of wealth returns.

We show that this assumption is indeed equivalent to bounding the spectral radius of an expected wealth return operator (a bounded linear operator) by . As a result, it is similar to the assumptions made by recent literature regarding the operator theoretic method, which have been proven both necessary and sufficient for the existence and uniqueness of solutions in a variety of models (see, e.g., Hansen and Scheinkman (2009, 2012), Borovička and Stachurski (2017) and Toda (2018)). Our assumption is easy to verify numerically. For example, when the state space for the exogenous Markov process is finite, verifying this assumption is as convenient as finding the largest modulus of the set of eigenvalues for a given matrix.

Second, as our most significant contribution, we show that the model economy is globally stable, even in the presence of capital income risk. Specifically, there exists a unique stationary distribution for the state process (including wealth and the exogenous Markov state), and, given any initial state, the distributional path of the state process generated via optimal consumption and wealth accumulation converges to the stationary distribution as time iterates forward. The idea of proof goes as follows. Based on the optimality results established in the previous step, existence of a stationary distribution is guaranteed under some further restrictions on agents’ level of patience, plus some mild assumptions on the stochastic properties of the exogenous state and the labor income processes. The key is to show that the wealth process is bounded in probability.

The proof of global stability is more tricky and separated into two scenarios.

(Scenario \@slowromancapi@) When the exogenous state process is independent and identically distributed, so are and , and wealth is the only state variable remaining. We show that, with some additional concavity structure imposed, the model economy is monotone, allowing us to use some new results in the field of stochastic stability (due to Kamihigashi and Stachurski (2014, 2016)). Based on these results, both global stability and the Law of Large Numbers are established. In this case, convergence of the distributional path to its stationarity is in the form of weak convergence. Moreover, the added concavity assumption holds for standard utilities such as CRRA or the logarithm utility. Notably, even in the current case, our theory extends the stability theory of Benhabib et al. (2015), since we allow and to be dependent on each other (a more detailed comparison is given below).

(Scenario \@slowromancapii@) When the exogenous state process is Markovian, and are in general autocorrelated and mutually dependent, and the structure of monotone economy is lost due to the added exogenous state. As a result, the order theoretic approach used in the previous case is no longer applicable. In response to that, we aim to exploit the traditional theory of stochastic stability (see, e.g., Meyn and Tweedie (2009)). Specifically, we provide sufficient conditions for the state process to be -irreducible, strongly aperiodic and a positive Harris chain, which in turn guarantee global stability and the Law of Large Numbers. Convergence here is in total variation norm distance, which is stronger than weak convergence. Our sufficient conditions are easy to verify in applications, and centered around existence of density representations for the exogenous state process and the labor earnings process. We only require that supports of the two densities contain respectively a nontrivial compact subset and a certain “small” interval. Importantly, no further concavity structure is required.

Moreover, we show in this scenario that if we add the same concavity structure as we do in scenario \@slowromancapi@ and some other mild assumptions (e.g., existence of densities for the wealth return process and geometric drift property of the labor earnings process), then the model economy is indeed -geometrically ergodic. As a result, convergence to the stationary distribution occurs at a geometric speed.

Since an iid process is a special Markov process, as a byproduct, the theory in scenario \@slowromancapii@ serves as an alternative stability theory when the exogenous state process is iid. As can be seen from the discussion above, neither of the two theories is “stronger” than the other in this circumstance. On the one hand, global stability in scenario \@slowromancapi@ is established under an additional concavity assumption, which is not required for global stability in scenario \@slowromancapii@. On the other hand, we make no assumptions on the density structure of the key stochastic processes in scenario \@slowromancapi@ as we do in scenario \@slowromancapii@.

Based on the established stability and ergodicity results, the unique stationary distribution can be approximated via tracking a single state process simulated according to the optimal consumption and wealth accumulation rules, which is highly efficient. The real caveat is that, in presence of capital income risk, there can be very large realized values of wealth (and consumption), causing serious problems to numerical computation of the optimal policy. However, this problem is alleviated in our setting. We show that, under our maintained assumptions, the optimal policy is concave and asymptotically linear with respect to the wealth level. Hence, at large levels of wealth, the optimal consumption rule can be well approximated via linear extrapolation.

We provide several important applications. First, we illustrate how our theory can be applied to modeling capital income risk in different scenarios. Then, we provide a numerical example in which we explore the quantitative effect of stochastic volatility and mean persistence of the wealth return process on wealth inequality. In the calibrated economy, our quantitative analysis shows that both these two factors lead to lower tail exponents of the stationary wealth distribution and higher Gini coefficients, and thus a higher level of wealth inequality.

In terms of connections to the existing literature, the most closely related results are those found in the recent paper Benhabib et al. (2015). Like us, the authors study capital income risk in an income fluctuation framework. On the one hand, their paper proves an important theoretical result—the stationary wealth distribution has a fat tail, a topic not treated by the present paper (tail properties are only studied by us numerically).

On the other hand, our theory of optimality and stochastic stability is considerably sharper and covers a much broader range of applications. Specifically, to avoid technical complication, Benhabib et al. (2015) assume that and are iid, mutually independent, supported on bounded closed intervals with strictly positive lower bounds, and that their distributions are represented by densities. Albeit helpful for simplifying analysis and deriving tail properties, these assumptions rule out important features observed in the real economy (e.g., mean persistence and stochastic volatility in the empirical labor earnings and wealth return processes, as discussed). Moreover, the strictly positive lower bound for prevents agents from borrowing up to the highest sustainable level of debt, hiding substantial model dynamics.333As discussed in Rabault (2002), in this case, agents are guaranteed a strictly positive minimum level of consumption, so the marginal value of consumption is bounded, and the problem can be easily solved by constructing supremum norm contractions. However, relaxing this assumption allows agents to systematically avoid exhausting their borrowing capacity. As described above, all these assumptions are relaxed in our framework.

Regarding earlier literature, specific types of capital income risk are modeled by Quadrini (2000), Angeletos and Calvet (2005), Cagetti and De Nardi (2006) and Angeletos (2007) in general equilibrium frameworks. In comparison, the present paper focuses on constructing a “more general” one-sector framework and deriving sharper theoretical results, which, of course, could potentially benefit “more general” general equilibrium analysis.

Moreover, since we tackle unbounded rewards and the associated technical complication, our paper is also related to Rabault (2002), Carroll (2004), Kuhn (2013) and Li and Stachurski (2014). These works develop different methods to handle the issue of unboundedness in standard income fluctuation problems (ones without capital income risk). While Carroll (2004) constructs a weighted supremum norm contraction and works with the Bellman operator, the other three works focus on the Coleman operator. In particular, Rabault (2002) exploits the monotonicity structure, Kuhn (2013) applies a version of the Tarski’s fixed point theorem, while Li and Stachurski (2014) constructs a contraction mapping based on a metric that evaluates consumption differences in marginal values. As discussed above, the present paper draws on and extends Li and Stachurski (2014) by incorporating capital income risk.

The rest of this paper is structured as follows. Section 2 formulates the problem. Section 3 establishes optimality results. Sufficient conditions for the existence and uniqueness of optimal policies are discussed. Section 4 focuses on stochastic stability. Global stability and some further properties are studied. Section 5 provides a set of applications. All proofs are deferred to the appendix.

2. Set up

This section sets up the income fluctuation problem to be studied. As a first step, we introduce some mathematical techniques and notation used in this paper.

2.1. Preliminaries

Let , and be the natural, real and nonnegative real numbers respectively. Given topological space , let be the Borel -algebra and let be the set of probability measures on . A stochastic kernel on is a map such that

-

•

is -measurable for each and

-

•

is a probability measure on for each .

Let be the set of bounded continuous functions on . A stochastic kernel is called Feller if is in whenever .

For all , we define the -th order kernel as

The value represents the probability of transitioning from to in steps. Furthermore, for all , we define as

A sequence is called tight, if, for all , there exists a compact such that for all . We say that converges to weakly and write if and for all bounded continuous .

A stochastic kernel is called bounded in probability if the sequence is tight for all . We call stationary for if . We say that is globally stable if there exists a unique stationary distribution in and for all .

Let be a bounded linear operator from to itself and be the supremum norm on . The operator norm and spectral radius of are defined by

In particular, when is finite, becomes a square matrix, and the spectral radius reduces to , where ranges over the set of eigenvalues of . (See, e.g., page 663 of Aliprantis and Border (2006)).

In what follows, is a fixed probability space on which all random variables are defined, while is expectations with respect to .

2.2. The income fluctuation problem

We introduce capital income risk and consider a generalized income fluctuation problem as follows

| s.t. | (1) | |||

where is a state-independent discount factor, is the utility function, the control process is consumption, is a gross rate of return on wealth and is labor income. The return and income processes obey

| (2) |

where and are nonnegative real-valued measurable functions, and are innovations, and is a time-homogeneous -valued Markov process with Feller stochastic kernel , where is a Borel subset of paired with the usual relative topology.

Throughout we make the following assumption on the agent’s utility.

Assumption 2.1.

The utility function is twice differentiable on and satisfies

-

(1)

and everywhere on , and

-

(2)

as and as .

Example 2.1.

A typical example that meets assumption 2.1 is the CRRA utility

| (3) |

where is the coefficient of relative risk aversion.

2.3. Further notation

We use and to denote respectively the current and next period random variables. In addition,

| (4) |

In particular, for any integrable function ,

| (5) |

3. Optimality Results

In this section, we show that, with bounded or unbounded rewards, the Coleman operator adapted to the income fluctuation problem above is an -step contraction mapping on a complete metric space of candidate policies, and that the unique fixed point is the optimal policy. To that end, we make the following assumptions.

Assumption 3.1.

There exists such that .

Assumption 3.2.

For all , we have .

Assumption 3.3.

, and .

Assumption 3.4.

The functions , , and are continuous.

Example 3.1.

Example 3.2.

Let be a finite-state Markov chain on with transition matrix (a “discrete” stochastic kernel). Let denote the diagonal matrix generated by elements in the bracket, and, with slight abuse of notation, let

In this case, the operator in example 3.1 reduces to the matrix . Therefore, assumption 3.1 holds if and only if . In particular, equals the largest modulus of all the eigenvalues of .

Example 3.3.

Based on the Hölder’s inequality, to show assumption 3.3, it suffices to find some such that and

To establish the required results, we (temporarily) assume and set the asset space as . The state space for the state process is then444Note that the second condition of assumption 2.1 and assumption 3.3 imply that for all (although is allowed to be arbitrarilly close to zero). Hence, for all by the law of motion (2.2). It thus makes no difference to optimality to exclude zero from the asset space. Doing this simplifies analysis since and are finite away from zero. It actually allows us to propose a useful metric and apply the contraction approach, as to be shown later.

Consider the maximal asset path defined by

| (6) |

A feasible policy is a Borel measurable function with for all . Given any feasible policy and initial condition , the asset path generated by is the sequence in (2.2) when and . The lifetime value of any feasible policy is the function defined by

where is the asset path generated by . Notice that for any feasible and any . This is because, by assumption 2.1, there exists a constant such that , and hence

The last expression is finite by lemma 3.1.

A feasible policy is called optimal if on for any feasible policy . In the present setting, the finiteness of for each feasible policy, the strict concavity of , and the convexity of the set of feasible policies from each imply that for each given parameterization, at most one optimal policy exists.

A feasible policy is said to satisfy the first order optimality conditions if

| (7) |

for all , and equality holds when . Moreover, a feasible policy is said to satisfy the transversality condition if, for all ,

| (8) |

Theorem 3.1.

When does an optimal policy exist, and how can we compute it? To answer these questions, following Li and Stachurski (2014), we use a contraction argument, where the underlying function space is set to , the functions such that

-

(1)

is continuous,

-

(2)

is increasing in the first argument,

-

(3)

for all , and

-

(4)

.

To compare two policies, we pair with the distance

| (9) |

that evaluates the maximal difference in terms of marginal utility. Note that

| (10) |

Moreover, while elements of are not generally bounded, one can show that is a valid metric on . In particular, is finite on since , and the last two terms are finite by the definition of .

Proposition 3.1.

is a complete metric space.

Proposition 3.2.

Inspired by proposition 3.2, we aim to characterize the optimal policy as the fixed point of the Coleman operator defined as follows: for fixed and , the value of the image at is defined as the that solves

| (12) |

where is the function on

| (13) |

defined by

| (14) |

The following propositions show that the Coleman operator is a well-defined self-map from the candidate space into itself.

Proposition 3.3.

Recall and defined in assumption 3.1. We now provide our key optimality result.

4. Stochastic Stability

This section focuses on stochastic stability of the generalized income fluctuation problem. We first provide sufficient conditions for the existence of a stationary distribution and then explore conditions for uniqueness and ergodicity.

Now we add zero back into the asset space, and consider a larger state space for the state process , denoted by

We extend to by setting for all . Together, and the transition functions for , and determine a Markov process with state vector taking values in the state space . Let denote the corresponding stochastic kernel. The law of motion of is

| (15) |

4.1. Existence of a stationary distribution

To obtain existence of a stationary distribution, we make the following assumptions.

Assumption 4.1.

There exists such that

-

(1)

for all ,555Here we adopt the convention that so that assumption 4.1 does not rule out the case . Indeed, as would be shown in proofs, all the conclusions of this paper still hold if we replace this condition by the weaker alternative: for all , while maintaining the second part of assumption 4.1. and

-

(2)

there exists such that .

Assumption 4.2.

for all .

Assumption 4.3.

The stochastic kernel is bounded in probability.

Example 4.1.

For homogeneous utility functions (e.g., CRRA), if the first condition of assumption 4.1 holds for some , then it must hold for all . To see this, let be the degree of homogeneity. Then we have

The right hand side is constant in .

Example 4.2.

Recall example 3.2, where is a finite-state Markov chain. Consider the CRRA utility defined in (3). Define further the column vector

Then, assumption 4.1 holds whenever

| (16) |

To see this, the first condition of assumption 4.1 holds if there exists such that for all . Since is finite, this is equivalent to the existence of an such that . Similar to example 3.2, the second condition of assumption 4.1 holds if for the same . Together, these requirements are equivalent to (16).

Example 4.3.

Benhabib et al. (2015) consider the CRRA utility and assume that and are iid, mutually independent, supported on bounded closed intervals of strictly positive real numbers with their distributions represented by densities, and that and . Under these conditions, assumptions 4.2–4.3 obviously hold. Assumption 4.1 is satisfied by letting and . The first condition of assumption 4.1 holds since and

while the second condition holds for since

Let be the unique optimal policy obtained from theorem 3.2 and be defined as in assumption 4.1. The next proposition establishes a strictly positive lower bound on the optimal consumption rate.

From this result the existence of a stationary distribution is not difficult to verify.

4.2. Further Optimality Properties

Slightly digressed from our main topics, we show that the optimal policy satisifies several other important properties under the following assumption.

Assumption 4.4.

The map is concave on for each fixed and that is concave in its first argument.

Example 4.4.

Assumption 4.4 imposes some concavity structure on the utility function. It holds for CRRA and logarithmic utilities, as shown in appendix B.

The next proposition implies that, with this added concavity structure, the optimal policy is concave and asymptotically linear with respect to the wealth level.

Proposition 4.2.

-

(1)

is concave for all , and

-

(2)

for all , there exists such that .666 Here we rule out the trivial situation , in which case .

By proposition 4.2, as gets large, for some function , which is helpful for numerical computation. In the presence of capital income risk, there can be large realized values of wealth and consumption. This proposition then provides a justification for the linear extrapolation technology adopted when computing the optimal policy at large wealth levels.

4.3. Global stability

We start with the case of iid process, which allows us to exploit the monotonicity structure of the stochastic kernel . We then discuss general Markov processes. Since is not generally monotone in these settings,777Since the optimal policy is not generally monotone in , we cannot conclude from (4) that is monotone in . Hence, is not necessarily increasing in and monotonicity might fail. global stability is established via a different approach.

4.3.1. Case I: iid process

In this case, both and are iid processes, though dependence between and are allowed. The optimal policy is then a function of asset only, and the transition function (4) reduces to

| (17) |

In particular, we have a Markov process taking values in . The next result extends theorem 3 of Benhabib et al. (2015).

Theorem 4.2.

Let be the unique stationary distribution of , obtained in theorem 4.2. Let be the linear span of the set of increasing -integrable functions .999In other words, is the set of all such that for some scalars and increasing measurable with . Recall that is the set of continuous bounded functions . The following theorem shows that the Law of Large Numbers holds in this framework.

Theorem 4.3.

If the assumptions of theorem 4.2 hold, then the following statements hold:

-

(1)

For all and , we have

-

(2)

For all , we have

4.3.2. Case II: Markovian process

In this case, and are in general non-iid and mutually dependent processes.101010Since this framework encorporates the iid structure as a special case, this section provides an alternative ergodic theory for the iid framework as a byproduct. By comparing the assumptions of theorem 4.2 and those of theorem 4.4 below, we see that the latter holds without assumption 4.4, so neither of the two theories is more powerful than the other.

We assume that the stochastic processes and admit density representations denoted respectively by and . Specifically, there exists a nontrivial measure on such that

and for , where is the Lebesgue measure,

Assumption 4.5.

The following conditions hold:

-

(1)

the support of contains a compact subset that has nonempty interior,111111The support of the measure is defined as the set of points for which every open neighborhood of has positive measure.

-

(2)

is strictly positive on and continuous in , and

-

(3)

there exists such that is strictly positive on .

Assumption 4.5 is easy to verify in applications. The following examples are some simple illustrations, while more complicated applications are treated in section 5.

Example 4.5.

If is a countable subset of , then is a countable state Markov chain, in which case is the counting measure and reduces to a transition matrix . In particular, each single point in is a compact subset in the support of that has nonempty interior (itself), and is continuous in by definition. Hence, conditions (1)–(2) of assumption 4.5 hold as long as at least one column of is strictly positive (i.e., each element of that column is positive).

Example 4.6.

Since is a Borel subset of , if can be chosen as the Lebesgue measure, then condition (1) of assumption 4.5 holds trivially. Indeed, since , the support of must contain a nonempty open box (i.e., sets of the form with , ), inside which a compact subset with nonempty interior can be found.

For all measurable map and , we define

We say that the stochastic kernel corresponding to is -ergodic if

-

(a)

there exists a unique stationary distribution such that ,

-

(b)

, , and, for all ,

We say that is -geometrically ergodic if, in addition, there exist constants and such that, for all ,

In particular, if , then is called ergodic/geometrically ergodic.

The following theorem establishes ergodicity and the Law of Large Numbers. Notably, assumption 4.4 is not required for these results.

Theorem 4.4.

We next show that geometric ergodicity is guaranteed under some further assumptions. Suppose admits a density representation , in other words,

where . Recall the iid innovations and defined by (2.2) and the compact subset defined by assumption 4.5.

Assumption 4.6.

The following conditions hold:

-

(1)

there exists such that is strictly positive on ,

-

(2)

there exist and such that for all ,

-

(3)

the innovations and are mutually independent.

Example 4.7.

Let the measurable map be defined by

| (18) |

where is a sufficiently large constant defined in the proof of theorem 4.5 below.

5. Applications

We now turn to several substantial applications of the theory described above. We first illustrate how our theory can be applied to modeling capital income risk in different situations. We then provide a numerical example and study the quantitative effect of stochastic volatility and mean persistence of the wealth return process on wealth inequality.

Throughout this section, we work with the CRRA utility function defined by (3). Recall that is the coefficient of relative risk aversion.

5.1. Modeling Capital Income Risk

Suppose the income process contains both persistent and transient components (see, e.g., Blundell et al. (2008), Browning et al. (2010), Heathcote et al. (2010), Kaplan and Violante (2010), Kaplan (2012), DeBacker et al. (2013), and Carroll et al. (2017)). In particular, we consider

where the persistent component is a finite-state Markov chain with transition matrix , and the transient component is an iid sequence with and . Moreover, and are mutually independent.

As a natural extension of the iid financial return process assumed by Benhabib et al. (2015), we consider taking form of

where , and are respectively finite-state Markov chains with transition matrices and , is positive, and , and are mutually independent.121212Note that and are allowed to be dependent on each other since, for example, we allow and to be mutually dependent, as we do for and , etc. Such a setup, as it appears, allows us to capture both mean persistence and stochastic volatility.

The state spaces of and are respectively (sorted in increasing order)

Let be the diagonal matrix created by elements in the bracket, and let

Furthermore, we define the column vectors

For any square matrix , let be its spectral radius. We assume that

| (19) |

| (20) |

This problem can be placed in our framework by setting

To simplify notation, we denote and .

5.1.1. Optimality Results

Since , by the Fubini theorem,

For all bounded functions on and on , we define

Similar to example 3.1, for some if and only if .131313As in example 3.1, we have and . Then iff for some iff for some iff for some . The latter obviously holds since (19) holds, and, similar to example 3.2, and . Assumption 3.1 is verified.

Using the fact that is a finite space, we have

| (21) |

Since in addition is iid with , we have

Hence, assumption 3.2 holds. As a byproduct, we have also verified assumptions 4.2 and 4.6-(2) (recall example 4.7). Similarly, since and , we have

| (22) |

Moreover, for all , based on the Fubini theorem,

Hence, assumption 3.3 holds (see example 3.3). Since is a finite space, this in turn implies that must be continuous, so assumption 3.4 holds.

In summary, we have verified all the assumptions of section 3. All the related optimality results have been established.

5.1.2. Existence of Stationary Distributions

Similar to examples 4.1–4.2, assumption 4.1-(1) holds if for all . Since

it suffices to show that . Moreover, similar to verifying assumption 3.1, assumption 4.1-(2) holds as long as . In summary, assumption 4.1 holds whenever there exists that satisfies

This is guaranteed by (20). Moreover, assumption 4.2 has been verified in the previous section, assumption 4.3 is trivial since is finite, and assumption 4.4 has been verified in example 4.4.

5.1.3. Global Stability

Regarding ergodicity and the Law of Large Numbers (theorem 4.4), it remains to verify assumption 4.5. This is true if we assume further

-

•

there are strictly positive columns in each of the matrices , and (recall example 4.5), and

-

•

has a density that is strictly positive on for some .

Regarding geometric ergodicity (theorem 4.5), it remains to verify assumption 4.6. Condition (1) is trivial since . Condition (2) has been verified in previous sections. Hence, the model is -geometrically ergodic as long as the innovations and are mutually independent.

5.2. Modeling Generic Stochastic Returns

Indeed, our theory works for more general setups. To illustrate, consider the following labor income process141414Similar extensions can be made to the process.

| (23) |

where and are given, , and are positive iid sequences with finite second moments, and . Moreover, , and are mutually independent. Similar setups appear in a lot of applied literature. See, for example, Heathcote et al. (2010), Kaplan and Violante (2010), Huggett et al. (2011), Kaplan (2012) and DeBacker et al. (2013).

This setup can be placed in our framework by setting . Next, we aim to verify all the assumptions related to .

Based on (23), for all , the distribution of given follows

We denote for simplicity. Then for all and , we have151515Recall that for and , we have .

In particular, since , this implies that for all and . Hence,

for all , and assumptions 3.2 and 4.2 hold. Moreover, since ,

and the second part of assumption 3.3 holds. Regarding assumption 4.6-(2), since , we can choose such that

Then for , we have , and for , we have

Hence, for all . Since in addition , and

assumption 4.6-(2) follows immediately.

Finally, assumption 4.5-(3) holds as long as the distributions of and have densities that are strictly positive on for some .

5.3. Numerical Example

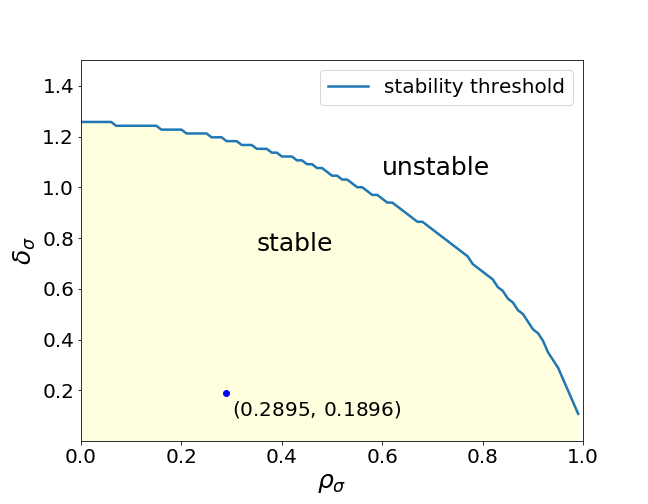

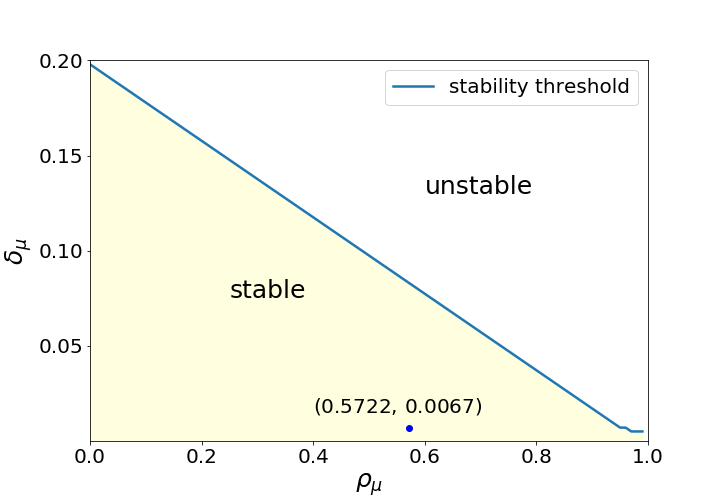

What are the “wealth inequality effects” of mean persistence and stochastic volatility in the rate of return to wealth? This is an important question that is rarely explored by the existing literature. In what follows we attempt to provide an answer via simulation. In doing this, we will also explore the generality of our theory by testing the stability properties of the economy for a broad range of parameters. Our study is based on the model of section 5.1.

Regarding the finite-state Markov chains , and , we use the method of Tauchen and Hussey (1991) and discretize the following AR(1) processes

into , and states, respectively.

Regarding the parameters of the process, we set to be a normal distribution with mean and variance . In addition, we set and . These values are chosen broadly in line with the existing literature. See, for example, Heathcote et al. (2010), Kaplan and Violante (2010), and DeBacker et al. (2013).

Our calibration of the process is based on Fagereng et al. (2016a), in which the authors report the average and standard deviation of the financial return process of Norway from 1993–2013.161616This is the only data source we can find that has a full record of financial returns. Although our calibration is based on this dataset, we have conducted sensitivity analysis for different groups of parameters. The results show that their qualitative effects are broadly the same, although their quantitative effects vary, as one would expect. We transform the two series to match our model and run first-order autoregressions, which yield , , , , and . Based on this parameterization, the stationary mean and standard deviation of the process are approximately and , respectively.

However, to distinguish the different effect of stochastic volatility and mean persistence, as well as to mitigate the computational burden caused by high state dimensionality, we consider two subsidiary model economies. The first model reduces to its stationary mean , while the second model reduces to its stationary mean . In summary, satisfies

To test the stability properties of the economy, we set , and consider respectively and . Furthermore, in model \@slowromancapi@, we set and consider a broad neighborhood of the calibrated pairs, and in model \@slowromancapii@, we set and consider a large neighborhood around the calibrated values. Each scenario, we hold the rest of the parameters as in the benchmark. The results are shown in figure 1 and figure 2.

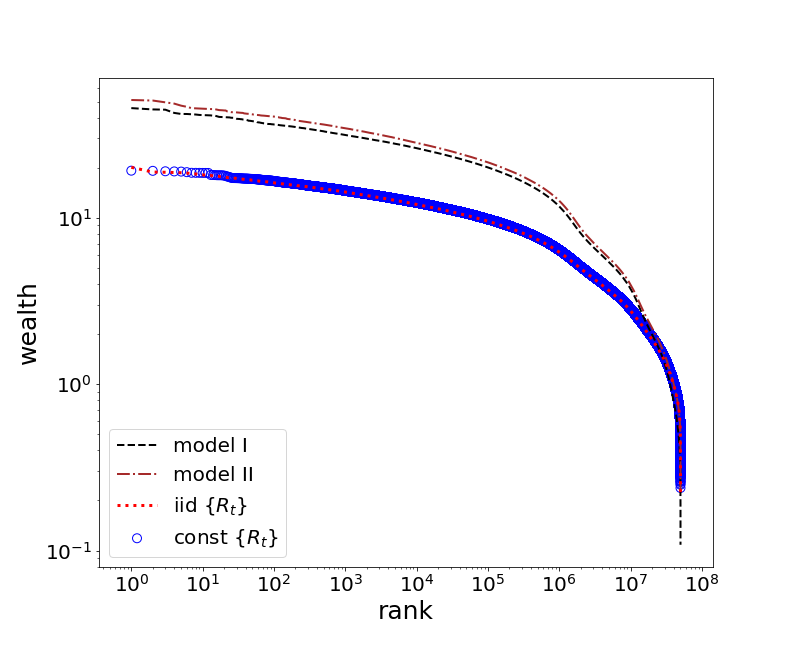

Since the dot points (calibrated parameter values) lie in the stable range in all cases, both the two calibrated models are globally stable, and stationary wealth distributions can be computed by the established ergodic theorems (theorem 4.4 and theorem 4.5). Moreover, the broad stability range indicates that our theory can handle a wide range of parameter setups, including highly persistent and volatile processes.

Our next goal is to explore the quantitative impact of capital income risk on wealth inequality. As a first step, we compute the optimal policy. This can be realized by iterating the Coleman opeartor and evaluating the distance between loops via the designed metric . The algorithm is guaranteed to converge based on theorem 3.2. Specifically, we assign 100 grid points to wealth equally spaced in . Expectations with respect to the iid innovations are evaluated via Monte Carlo with draws. Moreover, in all cases, we use piecewise linear interpolation to approximate policies. Policy function evaluation outside of the grid range is via linear extrapolation, as is justified by proposition 4.2.

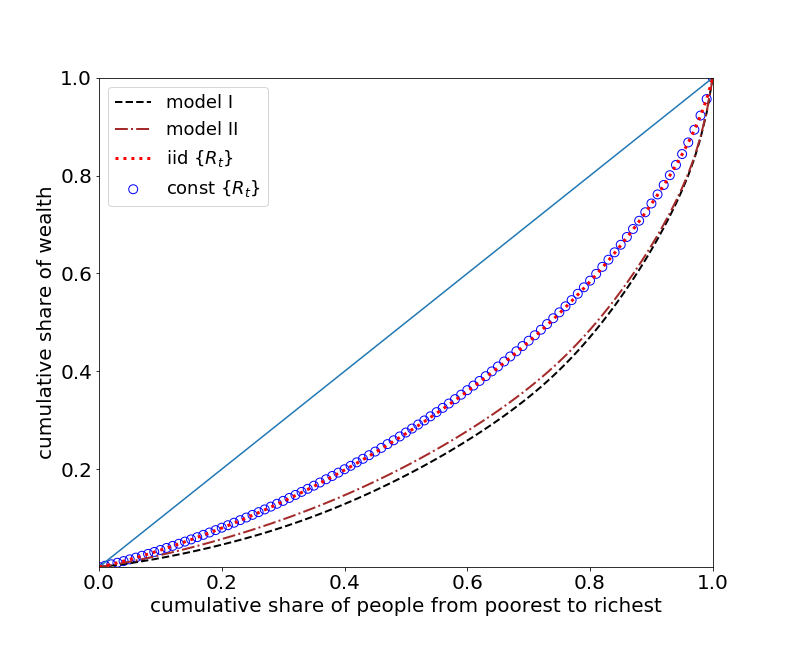

Once the optimal policy is obtained, we then simulate a single time series of agents in each case and compute the stationary distribution based on our ergodic theorems 4.4–4.5. As a final step, we compare the key properties of the stationary wealth distributions in different economies. In particular, we estimate the tail exponent based on the wealth level of the top and top of the simulated agents.171717Recall that a random variable is said to have a heavy upper tail if there exist constants such that for large enough , where is refered to as the tail exponent. The smaller the tail exponent is, the fatter the distribution tail is, and thus a higher level of inequality exists. It is common in the literature to estimate the tail exponent via linearly regressing the -ranks over the -wealth levels of the top and top most wealthy agents. Moreover, we estimate the Gini coefficient and provide a detailed analysis of the wealth share in each case.

All simulations are processed in a standard Julia environment on a laptop with a 2.9 GHz Intel Core i7 and 32GB RAM.

| Model Economy | Model I | Model II | IID | Constant | |

|---|---|---|---|---|---|

| Tail Exponent | Top 5% | 3.0 | 2.9 | 4.4 | 4.4 |

| Top 10% | 2.6 | 2.5 | 3.7 | 3.7 | |

| Gini Coefficient | 0.47 | 0.45 | 0.34 | 0.33 | |

-

•

Parameters: , , , , , , and .

| Poorest agents (%) | 5% | 10% | 15% | 20% | 25% | 30% | 35% | 40% | 45% | 50% |

|---|---|---|---|---|---|---|---|---|---|---|

| Model I | 0.8 | 1.8 | 3.1 | 4.6 | 6.2 | 8.2 | 10.4 | 12.9 | 15.7 | 18.7 |

| Model II | 1.1 | 2.4 | 3.9 | 5.7 | 7.6 | 9.7 | 12.1 | 14.7 | 17.5 | 20.6 |

| IID | 1.5 | 3.4 | 5.6 | 8.0 | 10.6 | 13.4 | 16.5 | 19.8 | 23.4 | 27.3 |

| Constant | 1.6 | 3.5 | 5.6 | 8.0 | 10.7 | 13.5 | 16.6 | 20.0 | 23.6 | 27.5 |

| Poorest agents (%) | 55% | 60% | 65% | 70% | 75% | 80% | 85% | 90% | 95% | 100% |

| Model I | 22.1 | 25.9 | 30.0 | 34.7 | 40.3 | 47.0 | 55.1 | 64.8 | 77.0 | 100 |

| Model II | 24.1 | 27.8 | 31.9 | 36.6 | 42.0 | 48.5 | 56.3 | 65.7 | 77.5 | 100 |

| IID | 31.4 | 35.9 | 40.7 | 46.0 | 51.8 | 58.4 | 65.7 | 74.2 | 84.3 | 100 |

| Constant | 31.6 | 36.1 | 41.0 | 46.3 | 52.0 | 58.5 | 65.9 | 74.3 | 84.4 | 100 |

-

•

Parameters: same as table 1. In the first and sixth rows, denotes the of agents with lowest levels of wealth.

We compare our models with two other models, in which is respectively an iid process and a constant.181818In the former case, we set in model \@slowromancapi@ (so that reduces to its stationary mean) or in model \@slowromancapii@ (so that reduces to its stationary mean). In the latter case, we reduce to its stationary mean. The difference between the results of model \@slowromancapi@ and model \@slowromancapii@ and the results of the other two models reflects the role of stochastic volatility and mean persistence of the wealth return process. Parameter setups and results are reported in tables 1–2.191919Since the standard Bewley-Ayagari-Hugget model does not generate fat-tailed wealth distribution (see, e.g., Stachurski and Toda (2018)), calculating the tail exponent of the stationary wealth distribution when is a constant is relatively less standard. However, doing this allows us to reveal the effect of capital income risk on the tail thickness of the stationary wealth distribution.

As can be seen in table 1, the tail exponents of model \@slowromancapi@ and model \@slowromancapii@ are smaller than the tail exponents when is iid or constant. In other words, both stochastic volatility and mean persistence in wealth returns lead to a higher degree of wealth inequality. Moreover, mean persistence results in slightly lower tail exponents than stochastic volatility does.

Similarly, the Gini coefficients generated by model \@slowromancapi@ and model \@slowromancapii@ are much higher than those generated by the other two models, illustrating from another perspective that stochastic volatility and mean persistence of wealth returns cause more inequality in wealth. However, different from the previous case, compared with mean persistence, which generates a Gini index 0.45, stochastic volatility has a higher impact on wealth inequality, creating a Gini index 0.47.

Moreover, at least in the current models, iid wealth returns do not have obvious effect on wealth inequality, both in terms of their impact on the tail exponent and in terms of their impact on the Gini coefficient.

The above descriptions are further illustrated in table 2 and figures 3–4. In particular, in table 2 we calculate the wealth share of a given fraction of poorest agents. Notably, the top richest agents hold respectively , , and of the total wealth, while the poorest agents hold respectively , , , of the total wealth in the four model economies. In figure 3 we create the Zipf plot (i.e., plotting wealth v.s. rank). It is clearly indicated that model \@slowromancapi@ and model \@slowromancapii@ generate stationary wealth distributions with fatter upper tails than the other models do, and that the stationary wealth distribution of model \@slowromancapii@ has the fattest upper tail. In figure 4 we plot the Lorenz curve, which can be viewed as a generalized graphical representation of table 2.

Finally, sensitivity analysis with respect to model parameters and a more detailed quantitative analysis can be found in the online appendix of this paper.

6. Appendix A: Proof of Section 3 Results

In proofs we let be the natural filtration, where with for all . We start by proving the results of section 3.

Proof of example 3.1.

For the rest of this section, we let and be defined as in assumption 3.1.

Proof of lemma 3.1.

Iterating backward on the maximal path (6), we can show that

Taking discounted expectation yields

Let . Then the monotone convergence theorem and the Markov property imply that

By the Markov property and assumption 3.1, for all and , we have

Taking supremum on both sides yields

| (24) |

Moreover, assumption 3.3 implies that . Hence,

for all . Taking supremum on both sides yields

| (25) |

Based on (24) and (25), we have

for all . Hence,

Finally, assumption 3.2 implies that

for all . This concludes the proof. ∎

Proof of theorem 3.1.

In the next, we aim to prove proposition 3.1. To that end, we define to be the set of functions that satisfies

-

(1)

is continuous,

-

(2)

is decreasing in the first argument, and

-

(3)

such that for all .

On we impose the distance

| (26) |

While the elements of are not bounded, the function is a valid metric. Moreover, standard argument shows that is a complete metric space.

Proof of proposition 3.1.

Standard argument shows that is a valid metric. To show completeness of , it suffices to show that and are isometrically isomorphic.

To see that this is so, let be the map on defined by . It is easy to show that and that it is a bijection. Moreover, for all ,

Hence, is an isometry. The space is then complete, as claimed. ∎

Proof of proposition 3.2.

Let be a policy in satisfying (11). That satisfies the first order optimality conditions is immediate by definition. It remains to show that any asset path generated by satisfies the transversality condition (8). To see that this is so, observe that, by (10),

| (27) |

Regarding the first term on the right hand side of (27), fix and observe that

where is the maximal path defined in (6). We then have

| (28) |

Since by assumption 3.3, the Markov property then implies that for all and ,

Hence, . Since in addition by lemma 3.1, (28) then implies that .

Proof of proposition 3.3.

Fix and . Because , the map is increasing. Since is strictly decreasing, the equation (12) can have at most one solution. Hence uniqueness holds.

Existence follows from the intermediate value theorem provided we can show that

-

(a)

is a continuous function,

-

(b)

such that , and

-

(c)

such that .

For part (a), it suffices to show that is continuous on . To this end, fix and . By (10) we have

| (29) |

The last term is integrable by assumption 3.3. Hence the dominated convergence theorem applies. From this fact and the continuity of , we obtain . Hence, is continuous.

Part (b) clearly holds, since as and is increasing and always finite (since it is continuous as shown in the previous paragraph). Part (c) is also trivial (just set ). ∎

Proof of proposition 3.4.

Fix . With slight abuse of notation, we denote

Step 1. We show that is continuous. To apply a standard fixed point parametric continuity result such as theorem B.1.4 of Stachurski (2009), we first show that is jointly continuous on the set defined in (13). This will be true if is jointly continuous on . For any and in with , we need to show that . To that end, we define

where and as defined in (2.2). Then and are continuous in by the continuity of and assumption 3.4, and they are nonnegative since (29) implies that .

Moreover, since the stochastic kernel is Feller, the product measure satisfies202020Here denotes weak convergence, i.e., for all bounded continuous function , we have The formal definition of weak convergence is provided in section 4.3.1.

Based on the generalized Fatou’s lemma of Feinberg et al. (2014) (theorem 1.1),

Since is continuous by assumption 3.4, this implies that

The function is then continuous since the above inequality is equivalent to

Hence, is continuous on , as was to be shown. Moreover, since takes values in the closed interval

the correspondence is nonempty, compact-valued and continuous. By theorem B.1.4 of Stachurski (2009), is continuous. is then continuous on since is continuous.

Step 2. We show that is increasing in . Suppose that for some and with , we have . Since is increasing in by assumption, is increasing in and decreasing in . Then . This is a contradiction.

Step 3. We have shown in proposition 3.3 that for all .

Step 4. We show that . Since , we have

for all . Assumption 3.3 then implies that

This concludes the proof. ∎

In the rest of this section, we aim to prove theorem 3.2. Recall defined above. Given , let be the function mapping into the that solves

| (30) |

The next lemma implies that is a well-defined self-map on , as well as topologically conjugate to under the bijection defined by .

Lemma 6.1.

The operator and satisfies on .

Proof of lemma 6.1.

Pick any and . Let , then solves

| (31) |

We need to show that and evaluate to the same number at . In other words, we need to show that is the solution to

But this is immediate from (31). Hence, we have shown that on . Since is a bijection, we have . Since in addition by proposition 3.4, we have . This concludes the proof. ∎

Lemma 6.2.

is order preserving on . That is, for all with .

Proof of lemma 6.2.

Let be functions in with . Suppose to the contrary that there exists such that . Since functions in are decreasing in the first argument, we have

This is a contradiction. Hence, is order preserving. ∎

Lemma 6.3.

is a contraction mapping on with modulus .

Proof of lemma 6.3.

Since is order preserving and is closed under the addition of nonnegative constants, based on Blackwell (1965), it remains to verify: for and given by assumption 3.1,

To that end, by assumption 3.1, it suffices to show that for all and ,

| (32) |

Fix , , and let . By the definition of , we have

Here, the first inequality is elementary and the second is due to the fact that and is order preserving. Hence, and (32) holds for . Suppose that (32) holds for arbitrary . It remains to show that (32) holds for . Define

By the induction hypothesis, the monotonicity of and the Markov property,

Hence, (32) is verified by induction. This concludes the proof. ∎

With the results established above, we are now ready to prove theorem 3.2.

Proof of theorem 3.2.

In view of propositions 3.1 and 3.2, to establish all the claims in theorem 3.2, we need only show that

To this end, pick any . Note that the topological conjugacy result established in lemma 6.1 implies that . Hence,

By the definition of and the contraction property established in lemma 6.3,

The right hand side is just , which completes the proof. ∎

7. Appendix B: Proof of Section 4 Results

Before working into the results of each subsection, we prove a general lemma that is frequently used in later sections. Recall that, for all , the value solves

| (33) |

Let denote the optimal policy. For each and , define

| (34) |

The next result implies that the borrowing constraint binds if and only if wealth is below a certain threshold level.

Lemma 7.1.

For all , if and only if . In particular, if and only if .

Proof of lemma 7.1.

Let . We claim that . Suppose to the contrary that . Then . In view of (33), we have

From this we get , which is a contradiction. Hence, .

On the other hand, if , then . By (33), we have

Hence, . The first claim is verified. The second claim follows immediately from the first claim and the fact that is the unique fixed point of in . ∎

Given , lemma 7.1 implies that for , and that for , solves

7.1. Proof of section 4.1 results

Our first goal is to prove proposition 4.1. To that end, recall given by assumption 4.1, and define the subspace as

| (35) |

Lemma 7.2.

is a closed subset of , and for all .

Proof of lemma 7.2.

To see that is closed, for a given sequence in and with , we need to verify that . This obviously holds since for all and , and, on the other hand, implies that for all .

We next show that is a self-map on . Fix . We have since is a self-map on . It remains to show that satisfies for all . Suppose to the contrary that for some . Then

Since and , this implies that

This is a contradicted with condition (1) of assumption 4.1 since . Hence, for all and we conclude that . ∎

With this result, we are now ready to prove proposition 4.1.

Proof of proposition 4.1.

Since the claim obviously holds when , it remains to verify that this claim holds on . We have shown in theorem 3.2 that is a contraction mapping on the complete metric space , with unique fixed point . Since in addition is a closed subset of and by lemma 7.2, we know that . In summary, we have for all . ∎

Our next goal is to prove theorem 4.1. To that end, recall the integer given by the second condition of assumption 4.1.

Lemma 7.3.

for all .

Proof of lemma 7.3.

Since , proposition 4.1 implies that for all . For all , we have in general, where and . Using these facts and (2.2), we have:

with probability one. Hence,

for all . Define

Note that by assumption 4.1-(2) and by assumption 3.3 and the Markov property. Moreover, by assumption 4.2. The Markov property then implies that for all and ,

Hence, for all , as was claimed. ∎

A function is called norm-like if all its sublevel sets (i.e., sets of the form ) are precompact in (i.e., any sequence in a given sublevel set has a subsequence that converges to a point of ).

Proof of theorem 4.1.

Based on lemma D.5.3 of Meyn and Tweedie (2009), a stochastic kernel is bounded in probability if and only if for all , there exists a norm-like function such that the -Markov process satisfies .

Fix . Since is bounded in probability by assumption 4.3, there exists a norm-like function such that . Then defined by is a norm-like function on . The stochastic kernel is then bounded in probability since lemma 7.3 implies that

Regarding existence of stationary distribution, since is continuous and assumption 3.4 holds, and we have shown in the proof of proposition 3.4 that

whenever , a simple application of the generalized Fatou’s lemma of Feinberg et al. (2014) (theorem 1.1) as in the proof of proposition 3.4 shows that the stochastic kernel is Feller. Since in addition is bounded in probability, based on the Krylov-Bogolubov theorem (see, e.g., Meyn and Tweedie (2009), proposition 12.1.3 and lemma D.5.3), admits at least one stationary distribution. ∎

7.2. Proof of section 4.2 results

We start by proving example 4.4.

Proof of example 4.4.

Next, we aim to prove proposition 4.2. Recall given by (35). Consider a further subspace defined by

| (36) |

Lemma 7.4.

is a closed subset of the metric space , and for all .

Proof of lemma 7.4.

The proof of the first claim is straightforward and thus omitted. We now prove the second claim. Fix . By lemma 7.2 we have . It remains to show that is concave for all . Given , lemma 7.1 implies that for and that for . Since in addition is continuous and increasing, to show the concavity of with respect to , it suffices to show that is concave on .

Suppose to the contrary that there exist some , , and such that

| (37) |

Let , where . Then by lemma 7.1 (and the analysis that follows immediately after that lemma), we have

Using assumption 4.4 then yields

This contradicts our assumption in (37). Hence, is concave for all . This concludes the proof. ∎

Now we are ready to prove proposition 4.2.

Proof of proposition 4.2.

By theorem 3.2, we know that is a contraction mapping with unique fixed point . Since is a closed subset of and by lemma 7.4, we know that . The first claim is verified.

Regarding the second claim, note that implies that is increasing and concave for all . Hence, is a decreasing function for all . Since in addition for all by proposition 4.1, we know that is well-defined and . Finally, by lemma 7.1 and the fact that (see footnote 6). Hence, the second claim holds. ∎

7.3. Proof of section 4.3 results.

We first prove the general result that the borrowing constraint binds in finite time with positive probability.

Lemma 7.5.

For all , we have .

Proof of lemma 7.5.

The claim holds trivially when . Suppose the claim does not hold on (recall that ), then for some , i.e., the borrowing constraint never binds with probability one. Hence,

for all , where with . Then we have

| (38) |

for all . Let , where is the integer defined by assumption 3.1. Based on assumption 3.3 and the Markov property,

as , where is given by assumption 3.1. Similarly,

as . Letting . (7.3) implies that , contradicted with the fact that . Thus, we must have for all . ∎

7.3.1. Proof of section 4.3.1 results

The next few results establish global stability and the law of large numbers for the case of iid process.

We say that a stochastic kernel increasing if is bounded and increasing whenever is.

Proof of theorem 4.2.

Obviously, assumptions 2.1, 3.1–3.4 and 4.1–4.4 hold under the stated assumptions of theorem 4.2. Based on proposition 4.2, we have . In particular, is continuous, and is decreasing on . Hence, is continuous and increasing in (see equation (17)). The stochastic kernel is then Feller and increasing. Moreover, is bounded in probability by lemma 7.3.

Fix and in with . Let and be two independent Markov processes generated by (17), starting at and respectively. Let and be the corresponding optimal consumption paths. By lemma 7.5, , i.e., the borrowing constraint binds in finite time with positive probability. Hence, with positive probability, . In other words, and is order reversing.

Since is increasing, Feller, order reversing, and bounded in probability, based on theorem 3.2 of Kamihigashi and Stachurski (2014), is globally stable. ∎

Proof of theorem 4.3.

We have shown in the proof of theorem 4.2 that the stochastic kernel is increasing, bounded in probability, and order reversing. Hence, is monotone ergodic by proposition 4.1 of Kamihigashi and Stachurski (2016). The two claims of theorem 4.3 then follow from theorem 4.2 (of this paper), and corollary 3.1 and theorem 3.2 of Kamihigashi and Stachurski (2016). In particular, if we pair with its usual pointwise order , then assumption 3.1 of Kamihigashi and Stachurski (2016) obviously holds. ∎

7.3.2. Proof of Section 4.3.2 Results

Our next goal is to prove theorems 4.4–4.5. In proofs we apply the theory of Meyn and Tweedie (2009). Important definitions (their locations in Meyn and Tweedie (2009)) include: -irreducibility (section 4.2), small set (page 102), strong aperiodicity (page 114), petite set (page 117), Harris chain (page 199), and positivity (page 230).

Note that since paired with its Euclidean topology is a second countable topological space (i.e., its topology has a countable base), while and are respectively Borel subsets of and paired with the relative topologies, and are also second countable. As a result, for , it always holds that (see, e.g., page 149, theorem 4.44 of Aliprantis and Border (2006))

Recall the Lebesgue measure on and the measure on defined in section 4.3.2. Let be the product measure on .

Lemma 7.6.

Let the function be defined as in (34). Then .

Proof of lemma 7.6.

Since , there exists a constant such that

Assumption 3.3 then implies that

Then, by the definition of and the properties of ,

as claimed. ∎

Recall the compact subset and given by assumption 4.5. Let

| (39) |

Lemma 7.7.

The Markov process is -irreducible.

Proof of lemma 7.7.

We define the measure on by

Then is a nontrivial measure. In particular, since by lemma 7.6 and by assumption 4.5.

For fixed and with , by lemma 7.1,

| (40) |

Note that for all , by assumption 4.5, whenever . Since in addition , we have

Let and . Notice that by lemma 7.1 and lemma 7.5, there exists such that

Hence, (7.3.2) implies that

Therefore, we have shown that any measurable subset with positive measure can be reached in finite time with positive probability, i.e., is -irreducible. Based on proposition 4.2.2 of Meyn and Tweedie (2009), there exists a maximal (in the sense of absolute continuity) probability measure on such that is -irreducible. ∎

Lemma 7.8.

The Markov process is strongly aperiodic.

Proof of lemma 7.8.

By the definition of strong aperiodicity, we need to show that there exists a -small set with , i.e., there exists a nontrivial measure on and a subset such that and

| (41) |

Let be defined as in (39). We show that satisfies the above conditions. Let

Since by assumption 4.5, is strictly positive on and continuous in , and is strictly positive on , the definition of implies that is strictly positive whenever . Define the measure on by

Since as shown in the proof of lemma 7.7 and on , we have , which also implies that is a nontrivial measure.

Proof of theorem 4.4.

We first show that is a positive Harris chain. Positivity has been established in theorem 4.1. To show Harris recurrence, by lemma 6.1.4, theorem 6.2.9 and theorem 18.3.2 of Meyn and Tweedie (2009), it suffices to verify

-

(a)

is Feller and bounded in probability, and

-

(b)

is -irreducible, and the support of has non-empty interior.

Claim (a) is already proved in theorem 4.1. Regarding claim (b), in lemma 7.7 we have shown that is -irreducible and thus -irreducible, where is maximal in the sense that implies for all . This also implies that whenever . Recall that , where is defined by (39). Since by assumption 4.5, the support of contains that has nonempty interior and the support of (the Lebesgue measure) contains the interval (of positive measure), the support of contains that has nonempty interior. As a result, the support of contains and thus has nonempty interior. Claim (b) is verified. Therefore, is a positive Harris chain.

Our next goal is to prove theorem 4.5. We start by proving several lemmas.

Lemma 7.9.

The set is a petite set for all and .

Proof of lemma 7.9.

Since any small set is petite, it suffices to show that is a -small set, i.e., there exists a nontrivial measure on such that

| (42) |

Without loss of generality, we assume that is large enough. For , let

| (43) |

while for . Let be the density corresponding to the stochastic kernel . Since and are mutually independent by assumption 4.6, satisfies

Recall that we have shown in the proof of proposition 4.2 that is decreasing for all . This implies that, for the dynamical system (4), is increasing in with probability one. Since in addition if and only if by lemma 7.1, we have

for all , where the last inequality follows from the fact that is increasing in (shown above), which indicates that for all fixed and ,

We now show that defined this way is a nontrivial measure on . Obviously, is a measure. Moreover, for fixed , is decreasing in , strictly less than one as gets large, and bounded below by . Hence, there exists such that as gets large. Hence, , which implies that as . Using lemma 7.1 again shows that satisfies (43) as gets large. Let . Then by lemma 7.6. Recall , and the compact subset defined by assumption 4.5. Then

Since in addition is strictly positive on and is strictly positive on by assumptions 4.5–4.6, for that is large enough, is defined by (43) and it is strictly positive for all . Moreover, since is strictly positive on and by assumption 4.5,

Hence, is a nontrivial measure on . Since in addition is the only element of that appears in the analytical form of , (42) holds and thus is petite. ∎

In the following, we let and be defined as in assumption 4.1.

Lemma 7.10.

There exist a petite set , constants , and a measurable map such that, for all ,

Proof of lemma 7.10.

By assumption 4.6, there exists such that

Since for all by proposition 4.1, by assumption 3.3, and by assumption 4.1, we have

Define and . Then and the above inequality implies that

Choose such that (such an is available since by assumption 4.6). Let be defined as in (18), i.e., .

Then the above results imply that

Let . Then by assumption 4.1 and the construction of . Thus,

| (44) |

Choose and such that . Fix and let . Lemma 7.9 implies that is a petite set. Notice that

Hence, (7.3.2) implies that for all , we have

| (45) |

Let . Then by (7.3.2)–(7.3.2), we have

for all . This concludes the proof. ∎

References

- Aiyagari (1994) Aiyagari, S. R. (1994): “Uninsured idiosyncratic risk and aggregate saving,” The Quarterly Journal of Economics, 109, 659–684.

- Aliprantis and Border (2006) Aliprantis, C. D. and K. C. Border (2006): Infinite dimensional analysis: A hitchhiker’s guide, Springer.

- Angeletos (2007) Angeletos, G.-M. (2007): “Uninsured idiosyncratic investment risk and aggregate saving,” Review of Economic Dynamics, 10, 1–30.

- Angeletos and Calvet (2005) Angeletos, G.-M. and L.-E. Calvet (2005): “Incomplete-market dynamics in a neoclassical production economy,” Journal of Mathematical Economics, 41, 407–438.

- Benhabib et al. (2011) Benhabib, J., A. Bisin, and S. Zhu (2011): “The distribution of wealth and fiscal policy in economies with finitely lived agents,” Econometrica, 79, 123–157.

- Benhabib et al. (2015) ——— (2015): “The wealth distribution in Bewley economies with capital income risk,” Journal of Economic Theory, 159, 489–515.

- Benhabib et al. (2016) ——— (2016): “The distribution of wealth in the Blanchard–Yaari model,” Macroeconomic Dynamics, 20, 466–481.

- Blackwell (1965) Blackwell, D. (1965): “Discounted dynamic programming,” The Annals of Mathematical Statistics, 36, 226–235.

- Blundell et al. (2008) Blundell, R., L. Pistaferri, and I. Preston (2008): “Consumption inequality and partial insurance,” American Economic Review, 98, 1887–1921.

- Borovička and Stachurski (2017) Borovička, J. and J. Stachurski (2017): “Necessary and Sufficient Conditions for Existence and Uniqueness of Recursive Utilities,” Tech. rep., National Bureau of Economic Research.

- Browning et al. (2010) Browning, M., M. Ejrnaes, and J. Alvarez (2010): “Modelling income processes with lots of heterogeneity,” The Review of Economic Studies, 77, 1353–1381.

- Cagetti and De Nardi (2006) Cagetti, M. and M. De Nardi (2006): “Entrepreneurship, frictions, and wealth,” Journal of Political Economy, 114, 835–870.

- Cagetti and De Nardi (2008) ——— (2008): “Wealth inequality: Data and models,” Macroeconomic Dynamics, 12, 285–313.

- Carroll (2004) Carroll, C. (2004): “Theoretical foundations of buffer stock saving,” Tech. rep., National Bureau of Economic Research.

- Carroll et al. (2017) Carroll, C., J. Slacalek, K. Tokuoka, and M. N. White (2017): “The distribution of wealth and the marginal propensity to consume,” Quantitative Economics, 8, 977–1020.

- Carroll (1997) Carroll, C. D. (1997): “Buffer-stock saving and the life cycle/permanent income hypothesis,” The Quarterly Journal of Economics, 112, 1–55.

- Chamberlain and Wilson (2000) Chamberlain, G. and C. A. Wilson (2000): “Optimal intertemporal consumption under uncertainty,” Review of Economic Dynamics, 3, 365–395.

- De Nardi et al. (2010) De Nardi, M., E. French, and J. B. Jones (2010): “Why do the elderly save? The role of medical expenses,” Journal of Political Economy, 118, 39–75.

- Deaton and Laroque (1992) Deaton, A. and G. Laroque (1992): “On the behaviour of commodity prices,” The Review of Economic Studies, 59, 1–23.

- DeBacker et al. (2013) DeBacker, J., B. Heim, V. Panousi, S. Ramnath, and I. Vidangos (2013): “Rising inequality: transitory or persistent? New evidence from a panel of US tax returns,” Brookings Papers on Economic Activity, 2013, 67–142.

- Fagereng et al. (2016a) Fagereng, A., L. Guiso, D. Malacrino, and L. Pistaferri (2016a): “Heterogeneity in returns to wealth and the measurement of wealth inequality,” American Economic Review: Papers and Proceedings, 106, 651–655.

- Fagereng et al. (2016b) ——— (2016b): “Heterogeneity and persistence in returns to wealth,” Tech. rep., National Bureau of Economic Research.

- Feinberg et al. (2014) Feinberg, E. A., P. O. Kasyanov, and N. V. Zadoianchuk (2014): “Fatou’s lemma for weakly converging probabilities,” Theory of Probability & Its Applications, 58, 683–689.

- Gabaix et al. (2016) Gabaix, X., J.-M. Lasry, P.-L. Lions, and B. Moll (2016): “The dynamics of inequality,” Econometrica, 84, 2071–2111.

- Guner et al. (2011) Guner, N., R. Kaygusuz, and G. Ventura (2011): “Taxation and household labour supply,” The Review of Economic Studies, 79, 1113–1149.

- Guvenen (2011) Guvenen, F. (2011): “Macroeconomics with heterogeneity: A practical guide,” Tech. rep., National Bureau of Economic Research.

- Guvenen and Smith (2010) Guvenen, F. and A. Smith (2010): “Inferring labor income risk from economic choices: An indirect inference approach,” Tech. rep., National Bureau of Economic Research.

- Guvenen and Smith (2014) Guvenen, F. and A. A. Smith (2014): “Inferring labor income risk and partial insurance from economic choices,” Econometrica, 82, 2085–2129.

- Hansen and Scheinkman (2009) Hansen, L. P. and J. A. Scheinkman (2009): “Long-term risk: An operator approach,” Econometrica, 77, 177–234.

- Hansen and Scheinkman (2012) ——— (2012): “Recursive utility in a Markov environment with stochastic growth,” Proceedings of the National Academy of Sciences, 109, 11967–11972.

- Hardy et al. (1952) Hardy, G. H., J. E. Littlewood, and G. Pólya (1952): Inequalities, Cambridge university press.

- Heathcote et al. (2010) Heathcote, J., K. Storesletten, and G. L. Violante (2010): “The macroeconomic implications of rising wage inequality in the United States,” Journal of Political Economy, 118, 681–722.

- Heathcote et al. (2014) ——— (2014): “Consumption and labor supply with partial insurance: An analytical framework,” American Economic Review, 104, 2075–2126.

- Huggett (1993) Huggett, M. (1993): “The risk-free rate in heterogeneous-agent incomplete-insurance economies,” Journal of Economic Dynamics and Control, 17, 953–969.

- Huggett et al. (2011) Huggett, M., G. Ventura, and A. Yaron (2011): “Sources of lifetime inequality,” American Economic Review, 101, 2923–54.

- Kamihigashi and Stachurski (2014) Kamihigashi, T. and J. Stachurski (2014): “Stochastic stability in monotone economies,” Theoretical Economics, 9, 383–407.

- Kamihigashi and Stachurski (2016) ——— (2016): “Seeking ergodicity in dynamic economies,” Journal of Economic Theory, 163, 900–924.

- Kaplan (2012) Kaplan, G. (2012): “Inequality and the life cycle,” Quantitative Economics, 3, 471–525.

- Kaplan and Violante (2010) Kaplan, G. and G. L. Violante (2010): “How much consumption insurance beyond self-insurance?” American Economic Journal: Macroeconomics, 2, 53–87.

- Kuhn (2013) Kuhn, M. (2013): “Recursive Equilibria In An Aiyagari-Style Economy With Permanent Income Shocks,” International Economic Review, 54, 807–835.

- Li and Stachurski (2014) Li, H. and J. Stachurski (2014): “Solving the income fluctuation problem with unbounded rewards,” Journal of Economic Dynamics and Control, 45, 353–365.

- Meghir and Pistaferri (2011) Meghir, C. and L. Pistaferri (2011): “Earnings, consumption and life cycle choices,” in Handbook of Labor Economics, Elsevier, vol. 4, 773–854.

- Meyer and Sullivan (2013) Meyer, B. D. and J. X. Sullivan (2013): “Consumption and income inequality and the great recession,” American Economic Review, 103, 178–83.

- Meyn and Tweedie (2009) Meyn, S. P. and R. L. Tweedie (2009): Markov Chains and Stochastic Stability, Springer Science & Business Media.

- Quadrini (2000) Quadrini, V. (2000): “Entrepreneurship, saving, and social mobility,” Review of Economic Dynamics, 3, 1–40.

- Rabault (2002) Rabault, G. (2002): “When do borrowing constraints bind? Some new results on the income fluctuation problem,” Journal of Economic Dynamics and Control, 26, 217–245.

- Schechtman (1976) Schechtman, J. (1976): “An income fluctuation problem,” Journal of Economic Theory, 12, 218–241.

- Stachurski (2009) Stachurski, J. (2009): Economic Dynamics: Theory and Computation, MIT Press.

- Stachurski and Toda (2018) Stachurski, J. and A. A. Toda (2018): “An Impossibility Theorem for Wealth in Heterogeneous-agent Models without Financial Risk,” arXiv preprint arXiv:1807.08404.

- Tauchen and Hussey (1991) Tauchen, G. and R. Hussey (1991): “Quadrature-based methods for obtaining approximate solutions to nonlinear asset pricing models,” Econometrica, 371–396.

- Toda (2018) Toda, A. A. (2018): “Wealth distribution with random discount factors,” Journal of Monetary Economics.