An Optimal Extraction Problem with Price Impact

Abstract.

A price-maker company extracts an exhaustible commodity from a reservoir, and sells it instantaneously in the spot market. In absence of any actions of the company, the commodity’s spot price evolves either as a drifted Brownian motion or as an Ornstein-Uhlenbeck process. While extracting, the company affects the market price of the commodity, and its actions have an impact on the dynamics of the commodity’s spot price. The company aims at maximizing the total expected profits from selling the commodity, net of the total expected proportional costs of extraction. We model this problem as a two-dimensional degenerate singular stochastic control problem with finite fuel. To determine its solution, we construct an explicit solution to the associated Hamilton-Jacobi-Bellman equation, and then verify its actual optimality through a verification theorem. On the one hand, when the (uncontrolled) price is a drifted Brownian motion, it is optimal to extract whenever the current price level is larger or equal than an endogenously determined constant threshold. On the other hand, when the (uncontrolled) price evolves as an Ornstein-Uhlenbeck process, we show that the optimal extraction rule is triggered by a curve depending on the current level of the reservoir. Such a curve is a strictly decreasing -function for which we are able to provide an explicit expression. Finally, our study is complemented by a theoretical and numerical analysis of the dependency of the optimal extraction strategy and value function on the model’s parameters.

Keywords: singular stochastic finite-fuel control problem; free boundary; variational inequality; optimal extraction; market impact; exhaustible commodity.

MSC2010 subject classification: 93E20; 49L20; 91B70; 91B76; 60G40.

OR/MS subject classification: Dynamic programming/optimal control: applications, Markov; Probability: stochastic models applications, diffusion.

JEL subject classification: C61; Q32.

1. Introduction

The problem of a company that aims at determining the extraction rule of an exhaustible commodity, while maximizing net profits, has been widely studied in the literature. To the best of our knowledge, the first model on this topic is the seminal paper [16], in which a deterministic model of optimal extraction has been proposed. Since then, many authors have generalized the setting of [16] by allowing for stochastic commodity prices and for different specifications of the admissible extraction rules (see, e.g., [1], [7], [13], [14], [25], [26] and [27] among a huge literature in Economics and applied Mathematics).

In this paper, we consider an optimal extraction problem for an infinitely-lived profit maximizing company. The company extracts an exhaustible commodity from a reservoir with a finite capacity incurring constant proportional costs, and then immediately sells the commodity in the spot market. The admissible extraction rules must not be rates, also lump sum extractions are allowed. Moreover, we assume that the company is a large player in the market, and therefore its extraction strategies affect the market price of the commodity. This happens in such a way that whenever the company extracts the commodity and sells it in the market, the commodity’s price is instantaneously decreased proportionally to the extracted amount.

Our mathematical formulation of the previous problem leads to a two-dimensional degene-rate finite-fuel singular stochastic control problem (see [8], [20], [21] and [23] as early contributions, and [4] and [15] for recent applications to optimal liquidation problems). The underlying state variable is a two-dimensional process whose components are the commodity’s price and the level of the reservoir (i.e. the amount of commodity still available). The price process is a linearly controlled Itô-diffusion, while the dynamics of the level of the reservoir are purely controlled and do not have any diffusive component. In particular, we assume that, in absence of any interventions, the commodity’s price evolves either as a drifted Brownian motion or as an Ornstein-Uhlenbeck process, and we solve explicitly the optimal extraction problem by following a guess-and-verify approach. This relies on the construction of a classical solution to the associated Hamilton-Jacobi-Bellman (HJB) equation, which, in our problem, takes the form of a variational inequality with state-dependent gradient constraint. To the best of our knowledge, this is the first paper that provides the explicit solution to an optimal extraction problem under uncertainty for a price-maker company facing a diffusive commodity’s spot price with additive and mean-reverting dynamics.

In the simpler case of a drifted Brownian dynamics for the commodity’s price, we find that the optimal extraction rule prescribes at any time to extract just the minimal amount needed to keep the commodity’s price below an endogenously determined constant critical level , the so-called free boundary. A lump sum extraction (and therefore a jump in the optimal control) may be observed only at initial time if the initial commodity’s price exceeds the level . In such a case, depending on the initial level of the reservoir, it might be optimal either to deplete the reservoir or to extract a block of commodity so that the price is reduced to the desired level .

If the commodity’s price has additionally a mean-reverting behavior and evolves as an Ornstein-Uhlenbeck process, the analysis is much more involved and technical than in the Brownian case. This is due to the unhandy and not explicit form of the fundamental solutions to the second-order ordinary differential equation involving the infinitesimal generator of the Ornstein-Uhlenbeck process. The properties of the increasing fundamental solution are indeed needed when constructing an explicit solution to the HJB equation. The optimal extraction rule is triggered by a critical price level that - differently to the Brownian case - is not anymore constant, but it is depending on the current level of the reservoir . This critical price level - that we call in Section 4.2 - is the inverse of a positive, strictly decreasing, -function that we determine explicitly. It is optimal to extract in such a way that the joint process is kept within the region , and a suitable lump sum extraction should be made only if the initial data lie outside the previous region. The free boundary has an asymptote at a point and it is zero at the point . These two points have a clear interpretation, as they correspond to the critical price levels triggering the optimal extraction rule in a model with infinite fuel and with no market impact, respectively.

In both the Brownian and the Ornstein-Uhlenbeck case, the optimal extraction rule is mathematically given through the solution to a Skorokhod reflection problem with oblique reflection at the free boundary in the direction . Here is the marginal market impact of the company’s actions on the commodity’s price. Indeed, if the company extracts an amount, say , at time , then the price is linearly reduced by and the level of the reservoir by . Moreover, we prove that the value function is a classical -solution to the associated HJB equation.

When the price follows an Ornstein-Uhlenbeck dynamics, our proof of the optimality of the constructed candidate value function partly employs arguments developed in the study of an optimal liquidation problem tackled in the recent [4], which shares mathematical similarities with our problem. Indeed, in the case of a “small” marginal cost of extraction, due to the unhandy and implicit form of the increasing eigenfunction of the infinitesimal generator of the Ornstein-Uhlenbeck process, we have not been able to prove via direct means an inequality that the candidate value function needed to satisfy in order to solve the HJB equation. For this reason, in such a case, we adopted ideas from [4] where an interesting reformulation of the original singular control problem as a calculus of variations approach has been developed. However, it is also worth noticing that when the marginal cost of extraction is “large enough”, the approach of [4] is not directly applicable since a fundamental assumption in [4] (cf. Assumption 2.2-(C5) therein) is not satisfied. Instead, a direct study of the variational inequality leads to the desired result. This fact suggests that a combined use of the calculus of variations method and of the standard guess-and-verify approach could be successful in intricate problems where neither of the two methods leads to prove optimality of a candidate value function for any choice of the model’s parameters. We refer to the proof of Proposition 4.11 and to Remark 4.12 for details.

As a byproduct of our results, we find that the directional derivative (in the direction ) of the optimal extraction problem’s value function coincides with the value function of an optimal stopping problem (see Section 4.2.1 and Remark 4.16 below). This fact, which is consistent with the findings of [20] and [21], also allows us to explain quantitatively why, in the case of a drifted Brownian dynamics for the commodity’s price, the level triggering the optimal extraction rule is independent of the current level of the reservoir . Indeed, in such a case, the value function of the optimal stopping problem is independent of and, therefore, so is also its free boundary .

Thanks to the explicit nature of our results, we can provide in Section 5 a detailed comparative statics analysis. We obtain theoretical results on the dependency of the value function and of the critical price levels , , and with respect to some of the model’s parameters. In the case of an Ornstein-Uhlenbeck commodity’s price, numerical results are also derived to show the dependency of the free boundary curve with respect to the volatility, the mean reversion level, and the mean-reversion speed.

The rest of the paper is organized as follows. In Section 2 we introduce the setting and formulate the problem. In Section 3 we provide preliminary results and a Verification Theorem. The explicit solution to the optimal extraction problem is then constructed in Sections 4.1 and 4.2 when the commodity’s price is a drifted Brownian motion and an Ornstein-Uhlenbeck process, respectively. A connection to an optimal stopping problem is derived in Section 4.2.1. A sensitivity analysis is presented in Section 5. The appendices contain the proofs of some results needed in Sections 4.2 and 5.2, and an auxiliary lemma.

2. Setting and Problem Formulation

Let be a filtered probability space, with filtration generated by a standard one-dimensional Brownian motion , and as usual augmented by -null sets.

We consider a company extracting a commodity from a reservoir with a finite capacity , and selling it instantaneously in the spot market. We assume that, in absence of any interventions of the company, the (fundamental) commodity’s price evolves stochastically according to the dynamics

| (2.1) |

for some constants , and . In the following, we identify the fundamental price when with a drifted Brownian motion with drift . On the other hand, when the price is of Ornstein-Uhlenbeck type, thus having a mean-reverting behavior typically observed in the commodity market (see, e.g., Chapter 2 of [24]). In this latter case, the parameter represents the mean-reversion level, and is the mean-reversion speed. In our model we do not restrict our attention to positive fundamental prices, since certain commodities have been traded also at negative prices. For example, that happened in Alberta (Canada) in October 2017 and May 2018 where the producers of natural gas faced the tradeoff between paying customers to take gas, or shutting down the wells111See, e.g., the article on the Financial Post or the news on the website of the U.S. Energy Information Administration.

The reserve level can be decreased at a constant proportional cost . The extraction does not need to be performed at a rate, and we identify the cumulative amount of commodity that has been extracted up to time , , as the company’s control variable. It is an -adapted, nonnegative, and increasing càdlàg (right-continuous with left-limits) process such that a.s. for all and a.s. The constraint for all has the clear interpretation that at any time it cannot be extracted more than the initial amount of commodity available in the reservoir. For any given , the set of admissible extraction strategies is therefore defined as

Clearly, .

The level of the reservoir at time , , then evolves as

where we have written in order to stress the dependency of the reservoir’s level on the initial amount of commodity and on the extraction strategy .

While extracting, the company affects the market price of the commodity. In particular, when following an extraction strategy , the market price at time , , is instantaneously reduced by , for some , and the spot price thus evolves as

| (2.2) |

We notice that for any there exists a unique strong solution to (2.2) by Theorem 6 in Chapter V of [28], and we denote it by in order to keep track of its initial value , and of the adopted extraction strategy .

Remark 2.1.

Notice that when , the impact of the company’s extraction on the price is permanent. On the other hand, it is transient (or temporary) in the mean-reverting case because, in the absence of any interventions from the company, the impact decreases since reverts back to its mean-reversion level.

The company aims at maximizing the total expected profits, net of the total expected costs of extraction. That is, for any initial price and any initial value of the reserve , the company aims at determining that attains

| (2.3) |

where

| (2.4) |

for any , and for a given discount factor . Here, and also in the following, , , and denotes the continuous part of .

Remark 2.2.

In (2.4) the integral term in the expectation is intended as a standard Lebesgue-Stieltjes integral with respect to the continuous part of . The sum takes instead care of the lump sum extractions, and its form might be informally justified by interpreting any lump sum extraction of size at a given time as a sequence of infinitely many infinitesimal extractions made at the same time . In this way, setting , the net profit accrued at time by extracting a large amount of the commodity is

This heuristic argument - also discussed at pp. 329–330 of [2] in the context of one-dimensional monotone follower problems - can be rigorously justified, and technical details on the convergence can be found in the recent [5]. We also refer to [17] and [29] as other papers on singular stochastic control problems employing such a definition for the integral with respect to the control process.

3. Preliminary Results and a Verification Theorem

In this section we derive the HJB equation associated to and we provide a verification theorem. We start by proving the following preliminary properties of the value function .

Proposition 3.1.

There exists a constant such that for all one has

| (3.1) |

In particular, . Moreover, is increasing with respect to and .

Proof.

The proof is organized in two steps. We first prove that (3.1) holds true, and then we show the monotonicity properties of .

Step 1. The nonnegativity of follows by taking the admissible (no-)extraction rule such that for all . The fact that clearly follows by noticing that and .

To determine the upper bound in (3.1), let be given and fixed, and for any we have

| (3.2) | ||||

where we have used that to obtain the term in right-hand side above.

We now aim at estimating the two expectations appearing in right-hand side of . To accomplish that, denote by the solution to (2.2) associated to (i.e. the solution to (2.1)). Then, if one easily finds a.s., since a.s. If , because a.s. for all and a.s., one has

Moreover, one clearly has for . Hence, in any case,

| (3.3) |

By an application of Itô’s formula we find for that

and for that

The previous two equations imply that, in both cases and , there exists such that

| (3.4) |

Then, the Burkholder-Davis-Gundy’s inequality (see, e.g., Theorem 3.28 in Chapter 3 of [22]) yields

| (3.5) |

for a constant , and therefore

| (3.6) |

for some constant , since it follows from standard considerations that there exists such that .

Now, exploiting (3.3) and (3.6), in both cases and we have the following:

- (i)

- (ii)

Thus, using (i) and (ii) in (3.2), we conclude that there exists a constant such that for any , and therefore (3.1) holds.

Step 2. To prove that is increasing for any , let , and observe that one clearly has a.s. for any and . Therefore which implies . Finally, letting , we have , and thus for any . ∎

We now move on by deriving the dynamic programming equation that we expect that should satisfy. In the rest of this paper, we will often denote by etc. the partial derivatives with respect to its arguments and of a given smooth function of several variables. Moreover, we will denote (unless otherwise stated) by , etc. the derivatives with respect to its argument of a smooth function of a single variable.

At initial time the company is faced with two possible actions: extract or wait. On the one hand, suppose that at time zero the company does not extract for a short time period , and then it continues by following the optimal extraction rule (if one exists). Since this action is not necessarily optimal, it is associated to the inequality

Then supposing is , we can apply Itô’s formula, divide by , invoke the mean value theorem, let , and obtain

Here is given by the second order differential operator

| (3.9) |

On the other hand, suppose that the company immediately extracts an amount of the commodity, sells it in the market, and then follows the optimal extraction rule (provided that one exists). With reference to (2.4), this action is associated to the inequality

which, adding and substracting , dividing by , and letting , yields

Since only one of those two actions can be optimal, and given the Markovian nature of our setting, the previous inequalities suggest that should identify with an appropriate solution to the Hamilton-Jacobi-Bellman (HJB) equation

| (3.10) |

with boundary condition (cf. Proposition 3.1), and satisfying the growth condition in (3.1). Equation (3.10) takes the form of a variational inequality with state-dependent gradient constraint.

With reference to (3.10) we introduce the waiting region

| (3.11) |

in which we expect that it is not optimal to extract the commodity, and the selling region

| (3.12) |

where it should be profitable to extract and sell the commodity. In the following, we will denote by the topological closure of .

The next theorem shows that a suitable solution to HJB equation (3.10) identifies with the value function, whenever there exists an admissible extraction rule that keeps (with minimal effort) the state process inside .

Theorem 3.2 (Verification Theorem).

Suppose there exists a function such that , solves HJB equation (3.10) with boundary condition , is increasing in , and satisfies the growth condition

| (3.13) |

for some constant . Then on .

Moreover, suppose that for all initial values , there exists a process such that

| (3.14) | |||

| (3.15) |

Then we have on and is optimal; that is, for all .

Proof.

The proof is organized in two steps. Since by assumption , , in the following argument we can assume that .

Step 1. Let be given and fixed. Here, we show that . Let , and for set By Itô-Tanaka-Meyer’s formula, we find

| (3.16) | ||||

Now,

which used into (3.16) gives the equivalence

Since satisfies (3.10) and , by taking expectations on both sides of the latter equation, and using that , we have

| (3.17) |

We now want to take limits as and on the right-hand side of the equation above. To this end notice that one has a.s.

| (3.18) | ||||

and the right-hand side of (3.18) is integrable by (3.7) and (3.8). Hence, we can invoke the dominated convergence theorem in order to take limits as and then as , so as to get

| (3.19) |

Since is arbitrary, we have

| (3.20) |

which yields by arbitrariness of in .

Step 2. Here, we prove that for any . Let satisfying (3.14) and (3.15), and let , for . Then, by employing the same arguments as in Step 1, all the inequalities become equalities and we obtain

where denotes the continuous part of . If now

| (3.21) |

then we can take limits as and , and by (3.18) (with ) together with (3.7) and (3.8) we find . Since clearly , then for all . Hence, using (3.20), on , and therefore on because for all .

To complete the proof it thus only remains to prove (3.21), and we accomplish that in the following. Since is increasing by assumption, we have by (3.13) and (3.3) that

Taking expectations and employing Hölder’s inequality

| (3.22) | ||||

To take care of the third expectation on right hand side of (3.22), observe that by Itô’s formula we have (in both cases and )

| (3.23) | ||||

Notice that , for some constant , and therefore an application of the Burkholder-Davis-Gundy’s inequality (see, e.g., Theorem 3.28 in [22]) gives

| (3.24) |

for a suitable . Then taking expectations in (3.23), employing (3.24), we easily obtain that there exists a constant such that

Hence, when taking limits as and in (3.22), the right-hand side of (3.22) converges to zero, thus proving (3.21) and completing the proof. ∎

4. Constructing the Optimal Solution

We make the guess that the company extracts and sells the commodity only when the current price is sufficiently large. We therefore expect that for any there exists a critical price level (to be endogenously determined) separating the waiting region and the selling region (cf. (3.11) and (3.12)). In particular, we suppose that

| (4.1) | ||||

| (4.2) |

According to such a guess, and with reference to (3.10), the candidate value function should satisfy

| (4.3) |

It is well known that (4.3) admits two fundamental strictly positive solutions and , with the former one being strictly decreasing and the latter one being strictly increasing. Therefore, any solution to (4.3) can be written as

for some functions and to be found. In both cases and (cf. (2.2)), the function increases exponentially to as (see, e.g., Appendix 1 in [6]). In light of the growth conditions of proved in Proposition 3.1, we therefore guess so that

| (4.4) |

for any .

For all , should instead satisfy

| (4.5) |

implying

| (4.6) |

To find and , , we impose that , and therefore by (4.4), (4.5), and (4.6) we obtain for all , i.e. , that

| (4.7) | ||||

| (4.8) |

From (4.7) and (4.8) one can easily derive that and , , satisfy

| (4.9) |

In the following we continue our analysis by studying separately the cases and , corresponding to a fundamental price of the commodity that is a drifted Brownian motion and an Ornstein-Uhlenbeck process, respectively. We will see that the form of the optimal extraction rule substantially differs among these two cases, and we will also provide a quantitative explanation of this by identifying an optimal stopping problem related to our optimal extraction problem (see Section 4.2.1 and Remark 4.16 below).

4.1. : The Case of a Drifted Brownian Motion Fundamental Price

We start with the simpler case , and we therefore study the company’s extraction problem (2.3) when the fundamental commodity’s price is a drifted Brownian motion. Dynamics (2.1) with yield

for any , and consequently (4.3) reads as

| (4.10) |

The increasing fundamental solution to the latter equation is given by

| (4.11) |

For future use, we notice that solves with

| (4.12) |

Upon observing that for all , we see that any explicit dependency on disappears in (4.9), and we therefore obtain that the critical price identifies for any with the constant value

| (4.13) |

Moreover, by using either (4.7) or (4.8), and by imposing (since we must have for all ; cf. Theorem 3.2), the function in (4.4) is given by

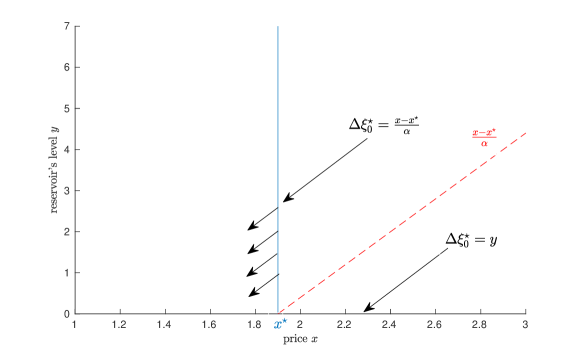

In light of the previous findings, the candidate waiting region is given by

and we expect that the selling region is such that where

In , we believe that it is optimal to deplete immediately the reservoir. In the company should make a lump sum extraction of size , and then sell the commodity continuously and in such a way that the joint process is kept inside , until there is nothing left in the reservoir. These considerations suggest to introduce the candidate value function

| (4.14) |

Notice that the first term in the second line of (4.14) is the continuation value starting from the new state , and that above is continuous by construction. From now on, we will refer to the critical price level as to the free boundary.

The next proposition shows that actually identifies with the value function .

Proposition 4.1.

Proof.

The proof is organized in steps.

Step 1. We start proving that . One can easily check that for any , and that is continuous on (recall also the comment after (4.14)). For all we derive from (4.14)

| (4.17) |

and

| (4.18) |

Also, for all we find from (4.14) by direct calculations that

| (4.19) |

and

| (4.20) |

Finally, for we have

| (4.21) |

From the previous expressions it is now straightforward to check that upon recalling (cf. (4.13)).

Step 2. Here we prove that solves HJB equation (3.10). By construction we have for , and for . Hence it remains to prove that for and for . This is accomplished in the following.

On the one hand, letting we obtain from the first equation in (4.17) and (4.18) that

where the last inequality is due to , which derives from the well-known property of the exponential function for all .

On the other hand, for we find from the third line of (4.14) and (4.21) that

We now want to prove that for all . Because with , we find

In order to study the sign of , we need to distinguish two cases. If , then it follows immediately . If , then recall from (4.12) and notice that because is increasing on , , and , one has . Hence again . Since now for any , then we have just proved that for all , and for any . Hence, in .

Also, for , we find

To obtain the first equality in the equation above we have used the second line of (4.14), (4.19), and that solves with as in (4.12). Notice that and . If , we clearly have that , since . If , then if and only if , but the latter inequality holds for any since we have proved above that for we have , and therefore, . Hence, in any case, for all , and then in .

Combining all the previous findings we have that is a solution to the HJB equation (3.10).

Step 3. Here we verify that satisfies all the requirements needed to apply Theorem 3.2.

The fact that is increasing in and easily follows from (4.18) and (4.20), respectively. The monotonicity of in is instead due to (4.21) and to the fact that in and .

In order to show the upper bound in (4.15), notice that

| (4.22) |

since . Further, we find for all that

| (4.23) | ||||

where we have used that for all . Finally, for all it is clear that

| (4.24) |

Hence, from (4.22)-(4.24) we see that satisfies the required growth condition.

We now show the nonnegativity of . For all one clearly has , and one also finds that for all

where the last inequality is due to and . Moreover, for , one obtains

where we have used in the first inequality, and in the last inequality. Thus, is nonnegative on .

Remark 4.2.

Notice that, as , the optimal extraction rule of (4.16) converges to the extraction rule that prescribes to instantaneously deplete the reservoir as soon as the price reaches ; i.e., defining, for any given and fixed , , one has for all and for all . The latter control can be easily checked to be optimal for the extraction problem in which the company does not have market impact (i.e. ).

4.2. : The Case of a Mean-Reverting Fundamental Price

In this section we assume , and we study the optimal extraction problem (2.3) when the commodity’s price evolves as a linearly controlled Ornstein-Uhlenbeck process

for any . Before proceeding with the construction of a candidate optimal solution for (2.3), in the next lemma we recall some important properties of the (uncontrolled) Ornstein-Uhlenbeck process that will be needed in our subsequent analysis. Their proof can be found in Appendix A.

Lemma 4.3.

Let denote the infinitesimal generator of the uncontrolled Ornstein-Uhlenbeck process (cf. (3.9)). Then the following hold true.

-

(1)

The strictly increasing fundamental solution to the ordinary differential equation is given by

(4.25) where

(4.26) is the Cylinder function of order and is the Euler’s Gamma function (see, e.g., Chapter VIII in [3]). Moreover, is strictly convex.

-

(2)

Denoting by the k-th derivative of , , one has that is strictly convex and it is (up to a constant) the positive strictly increasing fundamental solution to .

-

(3)

For any , for all .

For any , from (4.9) we find a representation of in terms of ; that is,

| (4.27) |

Notice that the denominator of is nonzero due to Lemma 4.3-(3).

For our subsequent analysis it is convenient to look at as a function of the state variable , and, in particular, we conjecture that it is the inverse of an injective nonnegative function to be endogenously determined together with its domain and its behavior. This is what we are going to do in the following. From now on we set .

Since we have (cf. Theorem 3.2) for any , we impose . Then, from (4.27) we obtain the boundary condition

| (4.28) |

In fact, existence and uniqueness of such is given by the following (more general) result. Its proof can be found in Appendix A.

Lemma 4.4.

Recall that denotes the derivative of order , , of . Then, for any , there exists a unique solution on to the equation . In particular, there exists uniquely solving and uniquely solving .

Now, we define the functions and such that for any

| (4.30) |

and, by differentiating and rearranging terms, we obtain

Recall that by Lemma 4.4 there exists a unique solving ; that is, solving . Due to (4.31), this point is a vertical asymptote of , and the next result shows that is located to the left of . The proof can be found in Appendix A.

Lemma 4.5.

Recall Lemma 4.4 and let and be the unique solutions to (i.e. ) and (i.e. ), respectively. We have .

The following useful corollary immediately follows from the proof of Lemma 4.4.

Corollary 4.6.

One has

and

By integrating (4.31) in the interval , for , and using the fact that (cf. (4.28)), we obtain

| (4.32) |

which is well defined, but possibly infinite for . In the following we will refer to as to the free boundary. We now prove properties of that have been only conjectured so far.

Proposition 4.7.

The free boundary defined in (4.32) is strictly decreasing for all and belongs to . Moreover,

| (4.33) |

Proof.

Step 1. We start by proving the claimed monotonicity. Notice that by (4.32) one has , where the function is given by

By Lemma 4.3 one has for any . Moreover, for all by Corollary 4.6. Therefore the denominator of is strictly negative for any . Again, an application of Corollary 4.6 implies that the numerator of is strictly negative for any , and therefore and . Thus, we conclude that is strictly decreasing.

Step 2. To prove (4.33), recall that from Step 1 we have set for all , and define

which is continuous and nonnegative by Step 1. Notice that , with as in Step 1.

By de l’Hopital’s rule,

so that, for any , there exists such that if , then . Thus, for any , we let be as above, and we take . Then, recalling (4.32), we see that there exists a constant (possibly depending on and , but not on ) such that

as .

Finally, since the integrand in (4.32) is a -function on , it follows that is so as well. ∎

Remark 4.8.

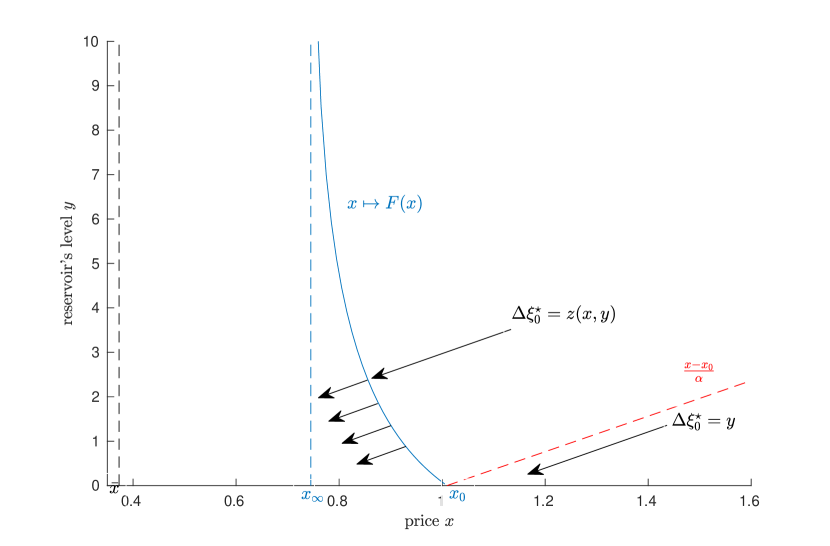

The critical price levels and have a clear interpretation. is the free boundary arising in the optimal extraction problem when we set , so that the company’s actions have no market impact. is the free boundary of the optimal extraction problem when there is an infinite amount of commodity available in the reservoir, i.e. .

Given as above, we now introduce the sets and that partition the (candidate) selling region :

and the (candidate) waiting region

We now make a guess on the structure of the optimal strategy in terms of the sets and and . If the current price is sufficiently low, and in particular it is such that (i.e. ), we conjecture that the company does not extract, and the payoff accrued is just the continuation value . Whenever the price attempts to cross the critical level , then the company makes infinitesimal extractions that keep the state process inside the region . If the current price is sufficiently high (i.e. ) and the current level of the reservoir is sufficiently large (i.e. lies in ), then the company makes an instantaneous lump sum extraction of suitable amplitude , and pushes the joint process to the locus of points , and then continues extracting as before. The associated payoff is then the sum of the continuation value starting from the new state , and the profits accrued from selling units of the commodity, that is . If the current capacity level is not large enough (i.e. , so that ), then the company immediately depletes the reservoir. This action is associated to the net profit .

In light of the previous conjecture we therefore define our candidate value function as

| (4.34) |

where, for any , we denote by the unique solution to

| (4.35) |

In fact, its existence and uniqueness is guaranteed by the next lemma, whose proof is in Appendix A.

Lemma 4.9.

Next, we verify that is a classical solution to the HJB equation (3.10). This is accomplished in the next two results.

Lemma 4.10.

The function is .

Proof.

Continuity is clear by construction. We therefore need to eveluate the derivatives of .

Denoting by the interior of a set, we have by (4.34) that for all

| (4.38) |

and that for all

| (4.39) |

The previous equations easily give the continuity of the derivatives in , and in .

To evaluate , and for , we need some more work. From (4.35), we calculate the derivatives of with respect to and by the help of the implicit function theorem, and we obtain

| (4.40) |

and

| (4.41) |

for any . Moreover, recalling that we have set , and taking , we find from (4.7)

| (4.42) |

and from (4.8)

| (4.43) |

By differentiating with respect to strictly inside (cf. the second line of (4.34)), and using (4.40) and (4.42), we obtain

| (4.44) |

| (4.45) |

Moreover, differentiating with respect to the second line of (4.34), and using (4.41) and (4.42), yields

| (4.46) |

Now, let be any sequence converging to , . Since by continuity of , and because , , and are also continuous, we conclude from (4.38) and (4.44)–(4.46) that , where and denote the closures of and .

In order to prove that , consider a sequence converging to , . Again by the continuity of and exploiting that we get . Therefore, we have by (4.39) and (4.44)–(4.46), and upon employing and by (4.43).

Collecting all the previous results, the claim follows. ∎

Proposition 4.11.

Proof.

The claimed regularity follows from Lemma 4.10, whereas we see from (4.34) that since . Hence, we assume in the following that . Moreover, it is important to recall that in (4.7) and (4.8) we have set .

By construction for all . Moreover, for all . Also, for all by employing (4.44) and (4.46), and observing that from (4.7) one has

Hence, it is left to show that

| (4.47) | ||||

| (4.48) |

In Step 1 below we prove that (4.47) holds, whereas the proof of (4.48) is separately performed for and in Step 2 and Step 3 respectively.

Step 1. Here we prove that (4.47) holds for any . Notice that (4.7) gives

| (4.49) |

Then, by using the first and the third equation of (4.38), and (4.49), we rewrite the left-hand side of (4.47) (after rearranging terms) as

| (4.50) |

for any . Here, we have defined

for any . Since , in order to have (4.47) it suffices to show that one has (recall that is the domain of )

We prove this in the following.

Differentiating with respect to , and using (4.27), gives

| (4.51) |

Take and , and recall that solves . Then, after some simple algebra, we have

where the last inequality is due to the fact that is strictly increasing.

Moreover, we find

| (4.52) |

due to the fact that uniquely solves and is strictly decreasing.

By differentiating of (4.51) with respect to one obtains

| (4.53) |

where we have introduced the function

| (4.54) |

that is such that

| (4.55) |

since is decreasing due to Lemma 4.3 with .

By Corollary 4.6 we have that

| (4.56) |

for all . Hence, the term multiplying in the right-hand side of (4.53) is negative.

In light of (4.55), we know that is increasing in for . We now have three possible cases.

(a) If is such that for all , then by (4.56) (and noticing that the function in (4.56) in fact appears in the numerator of ) we must have for all , so that

| (4.57) |

(b) If is such that for all , then by (4.56) we must have for all , so that

| (4.58) |

(c) If is such that for all , where , and for all , then by (4.56) we must have for all , and for all , so that

| (4.59) |

From (4.57)-(4.59), we then conclude that (4.47) holds for any such that .

Now, take and let . For we find from (4.51) that

| (4.60) |

Then, proceeding as above, from (4.52) and (4.60), we obtain that for all with .

Hence, in conclusion, for all and , and (4.47) is then established.

Step 2. Here, we show that (4.48) holds in . Setting

by Lemma B.1 in Appendix B we have , with solving (cf. Lemma 4.4).

Now, let be given and fixed. Thanks to the first and second equation in (4.39) we have

Clearly . Also, since is such that and , we have

where the last inequality is due to . Hence on .

Step 3. Here we provide the proof of (4.48) in , separately for the two cases: (i) and (ii) , and different approaches are followed in these two cases (see also Remark 4.12 below).

(i) Assume . Let be given and fixed, and recall that and for all . By employing (4.44) and (4.45), and observing that from (4.3) one has

| (4.61) | ||||

we get

| (4.62) |

Since , , and , one has that , where we have set

Observe that since (cf. (4.36)). Hence, it suffices to show that for all . Differentiating with respect to gives

Since and (cf. (4.40) and recall that ), and , we find

| (4.63) | ||||

and clearly if , since the latter implies .

This shows that on , and therefore that solves (4.48) in if .

(ii) Assume that . In this case, as discussed in Remark 4.12, we did not succeed proving (4.48) by studying the sign of as done in (i) above. Therefore, we follow a different approach which is based on that developed in the proof of Lemma 6.7 in [4]. Here we just provide the main ideas, since most of the arguments follow from [4].

Let be given and fixed, and consider an arbitrary . From (4.35) we find , and employing the latter we have from (4.34), (4.44) and (4.45) that

Notice that , hence to show negativity of it suffices to prove that for all . We find

| (4.64) | ||||

after rearranging terms, and adding and substracting the term to obtain the second equality above. Now, define the function

| (4.65) |

and notice that

where we have used that solves for the first equality, and Lemma 4.3-(2) with for the second equality. Moreover,

since , which then yields for all . From the monotonicity and the negativity of , and the fact that is positive and increasing as , one obtains that is decreasing. Therefore, one has for all if .

To prove that the right-derivative is negative, we now explain how to employ in our setting the arguments of the proof of Lemma 6.7 in [4]. First of all, we discuss the standing Assumption 2.2 in [4]. Conditions C2 and C3 are satisfied for . If , then Condition C5 in Assumption 2.2 of [4] is satisfied for , , , , and . Moreover, all the other requirements in Assumption 2.2 of [4] are not needed in our case. Indeed, Condition C6 guarantees the existence and uniqueness of (in our terminology) and , that we already have by Lemma 4.4; Condition C4 only ensures a growth condition on the value function that we have from Proposition 3.1, whereas, in our setting, Condition C1 of [4] just means that the discount factor must be strictly positive.

Then, after reformulating our singular stochastic control problem as a calculus of variations problem where one seeks for a decreasing function triggering a strategy of reflecting type (see Section 4 in [4]), proceeding as in Section 5 of [4] (see in particular Theorem 5.6 therein), one can prove that our free boundary is a (one-sided) local maximizer of our performance criterion (2.4). Hence, a contradiction argument as that in the proof of Lemma 6.7 in [4] also applies in our case and yields that . This completes the proof. ∎

Remark 4.12.

-

(1)

As we have seen, the proof of (4.48) in when requires a different analysis, and here we try to explain why a more direct approach seems not to lead to the desired result. Assuming , if one aims at proving (4.48) by studying the sign of in , given that for all , one could try to prove that (cf. (4.62))

is negative for any . Calculations, employing (4.7) and the definition of (cf. (4.29)), reveal that for any one has , where, for any , we have set

with . By noticing that in (cf. (4.44)), one has that rewrites as , and because by (4.40) and by (4.45), it is easy to see that on .

Hence, to prove that on it would suffice to show that on . However, we have not been able to prove this property due to the unhandy implicit expression of the function , even if a numerical investigation seems to confirm negativity of . For this technical reason in Step 3-(ii) of the proof of Theorem 4.11 we have hinged on arguments as those originally developed in [4] to address the case .

-

(2)

It is also worth noticing that the calculus of variations approach of [4] would have not been directly applicable for any choice of the parameters. Indeed, when , the function of (4.65) is increasing and therefore has not the monotonicity required in Condition C5 of Assumption 2.2 of [4]. However, under such a parameters’ restriction, direct calculations as those developed in Step 3-(i) of the proof of Proposition 4.11 lead to the desired result. This fact suggests that a combined use of the calculus of variations method and of the more standard direct study of the HJB equation could be successful in complex situations where neither of the two methods seem to leed to the proof of optimality of a candidate value function for any choice of the model’s parameters.

We conclude by showing that of (4.34) identifies with the value function . As a byproduct we also provide an optimal extraction rule. We first need the following technical result. Its proof follows by suitably adopting the classical result in [10], upon considering the following joint process as a (degenerate) diffusion in with oblique reflection in the direction at the -free boundary (see also [4], Remark 4.2).

Lemma 4.13.

Theorem 4.14.

Proof.

We aim at applying Theorem 3.2. We already know that is a solution to the HJB equation (3.10) by Lemma 4.10 and Proposition 4.11, and that satisfies for all . Moreover, the function is increasing with respect to . To see that, notice that one has from (4.29) that , for (since the denominator of (4.29) is positive by Lemma 4.3-(3) and the numerator is positive as well due to ), and this gives on and on (cf. (4.38) and (4.46)). Also, one can easily check from (4.39) that on because and .

To prove the upper bound in (3.13), recall that (cf. (4.27))

Since for any , by using that and are continuous we have that there exists a constant such that for all . Hence, by (4.34) we have for all . Moreover, for all and thus . Since the upper bound in (3.13) is clearly satisfied in , we conclude that there exists a constant such that

As for the nonnegativity of , notice that for all we have

since , and . Moreover, the nonnegativity of and imply

and also, given , we have

since and . Therefore on .

4.2.1. A Related Optimal Stopping Problem

In this section we show that the directional derivative identifies with the value function of an optimal stopping problem. Such a result is consistent with that obtained - for a different model with Brownian dynamics - in [21], where connections between finite-fuel singular stochastic control problems and questions of optimal stopping have been studied.

Proposition 4.15.

Proof.

For the rest of this proof, will be given and fixed. Notice that by construction (cf. (4.7) and (4.8)). Moreover, direct calculations on (4.34) show that . We now show that solves the HJB equation

| (4.68) |

Recall the selling region and the waiting region . Let be such that , and notice that by (4.34) we have

Then, since ,

upon using that satisfies Lemma 4.3-(2) with .

Now, let be such that , so that (recall (4.5)). If then , and using that we obtain

On the other hand, let be such that , set , and notice that

due to the positivity of and . Thus, in order to prove that for all , it is enough to prove that . Set ; then, upon employing the definition of (cf. (4.27)), we obtain

where we have applied Lemma 4.3-(2) with and for the last equality, and the last inequality follows from Corollary 4.6 since . Hence, on .

Finally, from Proposition 4.11 we have for any .

Remark 4.16.

A few comments are worth being done.

-

1.

With regard to the connection between problems of singular stochastic control and questions of optimal stopping (see, e.g., [11], [12], [19], and [21] as early contributions, and the introduction of the recent [9] for a richer literature review), we can interpret the stopping time as the optimal time at which an additional unit of the commodity should be extracted. Indeed, the underlying process at that time is such that, in economic terms, equality between the marginal expected optimal profit (i.e. ) and the marginal instantaneous net profit from extraction (i.e. ) holds.

-

2.

If we do not consider price impact in our model (i.e. we take ), it can be easily seen that the value function of the resulting optimal extraction problem is such that

a result that is clearly consistent with (4.67). The integral term

appearing in (4.67) can then be seen as a running cost/penalty whose effect increases with increasing price impact .

-

3.

It can be checked that the arguments of the proof of Proposition 4.15 carry over also to the case of a fundamental price given by a drifted Brownian motion, i.e. when (cf. Section 4.1). As one would expect by setting in the right-hand side of (4.67), in such a case it holds

so that the stopping problem related to the optimal extraction problem does not depend on the current level of the reservoir . This explains why, in in the drifted Brownian motion case studied in Section 4.1, the free boundary triggering the optimal extraction rule is -independent.

5. Comparative Statics Analysis

In this section, we study the sensitivity of the solution to the extraction problem separately for the case of a fundamental price given by a drifted Brownian motion (Section 5.1) and by an Ornstein-Uhlenbeck process (Section 5.2). In particular, in Section 5.1 we analytically determine the dependency of the free boundary of (4.13) and of the value function (4.14) on the parameters and . In Section 5.2 we study analytically how the value function (4.34) and the critical price levels and from Lemma 4.5 depend on and , and, numerically, the sensitivity of the free boundary with respect to , and .

5.1. Sensitivity Analysis in the Case of a Drifted Brownian Motion Fundamental Price

Here we assume in (2.2). Thanks to the explicit formula (4.13), studying the sensitivity of the free boundary with respect to the parameters and is a simple exercise of differentiation.

Proposition 5.1.

The free boundary of (4.13) is increasing with respect to both and .

Proof.

We look at the parameter of (4.11) as a function of and ; that is, we set

Then, it is not hard to find by direct calculations that

| (5.1) |

and

| (5.2) |

Clearly, if one has and . Then, suppose and notice that

| (5.3) |

where the second inequality above follows by an application of the binomial formula. By using the first inequality of (5.3) in (5.1), and the second inequality of (5.3) in (5.2), one easily finds that , as well as .

Finally, the claim follows since is decreasing with respect to (cf. (4.11)). ∎

Proposition 5.2.

The value function defined in (2.3) is increasing with respect to and .

Proof.

Let and . We show the monotonicity with respect to and separately in two steps.

Step 1. Let be given and fixed. For any , we denote by the solution to (2.2) when and the drift is . One clearly has -a.s. for any . Therefore for any , where is given by (2.4) with underlying state . Hence, we conclude

where .

Step 2. To prove the monotonicity of with respect to we adapt to our setting ideas from Theorem 4 in [2]. Let be the value function when the volatility coefficient in (2.2) is . Recall as in (3.9), and let be as in (3.9) but with volatility coefficient . Then, for all we have

| (5.4) | ||||

since is convex by the second equations in (4.17) and (4.19), and the second equation of (4.21). Furthermore, since is the value function of the optimal extraction problem when in (2.2) the volatility is , must satisfy

| (5.5) |

for all , and for all . Now, arguing as in the first step of the proof of Theorem 3.2, by using (5.4) and (5.5), we obtain , and thus the claimed monotonicity. ∎

Propositions 5.1 and 5.2 show that the higher the level of the drift is, and hence the higher the expected prices are, the later the company starts extracting in order to obtain larger profits. Moreover, higher uncertainty, and hence larger price’s fluctuations, are exploited by the company that then sells the commodity at higher prices and increases the resulting profits.

5.2. Sensitivity Analysis in the Case of an Ornstein-Uhlenbeck Fundamental Price

We start by studying the sensitivity of and (cf. Lemma 4.5) on the model parameters and . In the following, when needed, we write in order to emphasize the dependency of a given real-valued function with respect to and .

Recall that the fundamental increasing solution to the equation is given by (4.25) (see also (4.26)). In the following, when needed, we denote by the th derivative with respect to of . By an application of the dominated convergence theorem one obtains the relation

| (5.6) |

Analogously, one finds

| (5.7) |

for all

Lemma 5.3.

One has that

| (5.8) |

Lemma 5.4.

One has that

| (5.9) | ||||

The previous results on the dependency of with respect to and (i.e. (5.8) and (5.9)) allow us to determine the dependency of and on and as well. One may intuitively expect that the company exploits a higher mean reversion level, and thus sells the commodity at higher prices. As an indication of this, we indeed find that , , and the value function increase as increases.

In the following we denote by , the unique solutions on to and , respectively. Also, denotes the value function when in (2.2) the mean-reversion level is and the volatility is .

Proposition 5.5.

Let , and denote by and the unique solutions on to and , respectively. Furthermore, we denote by , , the value function when in (2.2) the mean-reversion level is and the volatility is . We have

and

| (5.10) |

Proof.

The next proposition shows that the critical price levels and increase as the price’s fluctuations become larger.

Proposition 5.6.

Let , and denote by and the unique solutions on to and , respectively. Furthermore, denote by the value function when in (2.2) the mean-reversion level is and the volatility is . We have

and

| (5.11) |

Proof.

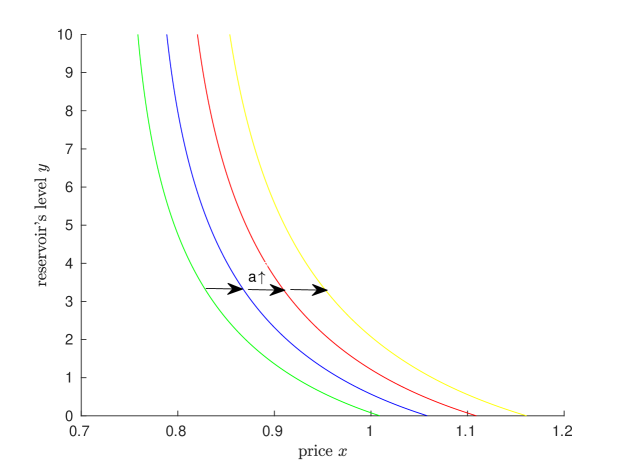

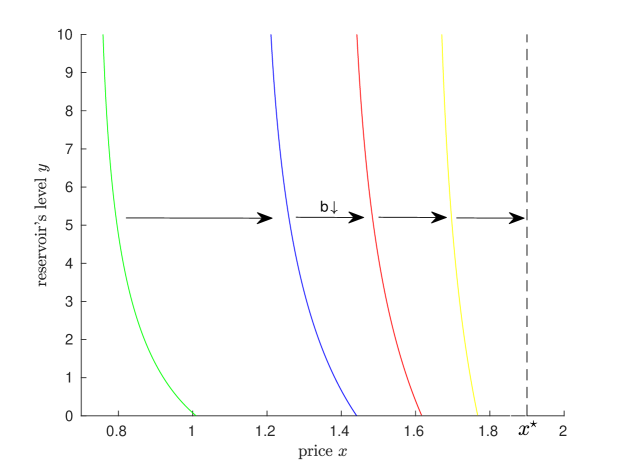

The semi-explicit nature of our results allows us to easily study numerically the dependency of the free boundary with respect to . This is shown in Figure 3. We see that increases as increases: the higher the level of mean reversion is, the later the company starts extracting in order to obtain larger profits.

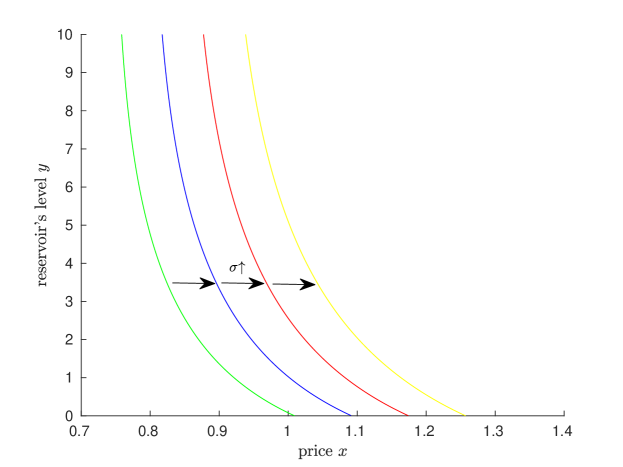

Figure 4 shows the dependency of the curve with respect to . We see that the whole curve increases as increases. We thus conclude that higher uncertainty, and hence higher fluctuations around the mean-reversion level, are exploited by the company which then sells the commodity at higher prices and increases its profits.

In Figure 5, we can observe the sensitivity of the free boundary with respect to . Differently to what it is happening when increasing and , now the whole curve increases as decreases, and in fact, as , it converges to , which is the free boundary in the case (i.e. related to the drifted Brownian motion case). This fact might be interpreted by saying that, if , a lower value of leads the company to wait more since it expects to be able to sell the commodity at higher prices in the future.

Appendix A Proofs of Results from Sections 4.2 and 5.2

Proof of Lemma 4.3.

- (1)

-

(2)

Define the function by

that, once differentiated with respect to , yields

Notice that is the integrand appearing in (4.26) for . Then, differentiating (4.25) with respect to , and invoking the dominated convergence theorem, we obtain

upon noticing that is the integrand of (cf. (4.26)).

Hence, can be identified (modulo a constant) as the positive strictly increasing fundamental solution to , and by direct calculations it can be checked that it is strictly convex. By iterating the previous argument, we see that, for any , the function is strictly convex and identifies with the positive strictly increasing fundamental solution to .

-

(3)

We define the function by

By direct calculations, we find

that, by the help of Hölder’s inequality (which is strict as is not a multiple of ), gives

The latter is in fact equivalent to

Proof of Lemma 4.4.

Let be given and fixed, and define , . We then have the following.

-

(i)

For , it is readily seen that .

-

(ii)

One has for all . To see this, rewrite , and notice that by Lemma 4.3

Hence, for all one has that , which implies

for all . The latter clearly gives for all .

Since for all , we conclude from (i) and (ii) that there exists a unique solution on to the equation by continuity of .

Proof of Lemma 4.5.

We argue by contradiction, and we suppose . Then by definition of and we have

| (A-1) |

Since by Lemma 4.3

we have by (A-1) that

again due to Lemma 4.3. But this contradicts .

Proof of Lemma 4.9.

First of all notice that for the existence of a solution to (4.35) it is necessary that since , and that since the domain of is . Hence, if a solution to (4.35) exists, it must be such that , for all .

Let with be given and fixed, and define , for . Then, one has and . Since is strictly decreasing (by strict monotonicity of ) it follows that there exists a unique solution to (4.35).

Finally, (4.36) follows by noticing that solves (4.35) when and by uniqueness of the solution. Analogously, (4.37) follows by noticing that uniquely solves (4.35), since .

Proof of Lemma 5.4.

The first equality in (5.9) follows from (5.7). In order to prove the last inequality in (5.9), we find by Lemma 4.3-(2) that

| (A-2) |

From (A-2), recalling that , we obtain

and we thus have

We now aim at establishing that the last term on the right-hand side of the latter equation is positive. With regard to (5.9), this would clearly imply that . From (A-2) we have

which then yields

where the last equality follows again by an application of (A-2), and the last inequality by Lemma 4.3. Hence and the proof is completed.

Appendix B An Auxiliary Result

Lemma B.1.

Proof.

Define . Since satisfies

and , we find Thus, we have

by the definition of . Since , for all and for all , it must necessarily be . ∎

Acknowledgments.. Financial support by the German Research Foundation (DFG) through the Collaborative Research Centre 1283 “Taming uncertainty and profiting from randomness and low regularity in analysis, stochastics and their applications” is gratefully acknowledged by the authors. We thank Stefan Ankirchner, Dirk Becherer, Todor Bilarev, Ralf Korn, Frank Riedel, Wolfgang J. Runggaldier, and Thorsten Upmann for valuable discussions and comments. In particular, we are thankful to Peter Frentrup for pointing out a mistake in a previous version of this manuscript.

References

- [1] Almansour, A., Insley, M. (2016). The Impact of Stochastic Extraction Cost on the Value of an Exhaustible Resource: An Application to the Alberta Oil Sands. Energy J. 37(2).

- [2] Alvarez, L.H.R. (2000). Singular Stochastic Control in the Presence of a State-dependent Yield Structure. Stoch. Processes Appl. 86 323–343.

- [3] Bateman, H. (1981). Higher Transcendental Functions, Volume II. McGraw-Hill Book Company.

- [4] Becherer, D., Bilarev, T., Frentrup, P. (2017). Optimal Liquidation under Stochastic Liquidity. Finance Stoch. 22(1) 39–68.

- [5] Becherer, D., Bilarev, T., Frentrup, P. (2018). Stability for Large Investors Strategies in M1/J1 Topologies. To appear on Bernoulli. ArXiv:1701.02167.

- [6] Borodin, W.H., Salminen, P. (2002). Handbook of Brownian motion-Facts and Formulae. 2nd Edition. Birkhäuser.

- [7] Brekke, K.A., Øksendal, B. (1994). Optimal Switching in an Economic Activity under Uncertainty. SIAM J. Control Optim. 32(4) 1021–1036.

- [8] Bridge, D.S., Shreve, S.E. (1992). Multi-dimensional Finite-Fuel Singular Stochastic Control. Lecture Notes Control Inform. Sci. 177 38–58.

- [9] De Angelis, T., Ferrari, G. (2018). Stochastic Nonzero-sum Games: a New Connection between Singular Control and Optimal Stopping. Adv. Appl. Probab. 50(2) 347–372.

- [10] Dupuis, P., Ishii, H. (1993). SDEs with Oblique Reflection on Nonsmooth Domains. Ann. Probab. 21(1) 554–580.

- [11] El Karoui, N., Karatzas, I. (1988). Probabilistic Aspects of Finite-Fuel, Reflected Follower Problems. Acta Appl. Math. 11 223–258.

- [12] El Karoui, N., Karatzas, I. (1991). A New Approach to the Skorohod Problem and its Applications. Stoch. Stoch. Rep. 34 57–82.

- [13] Feliz, R.A. (1993). The Optimal Extraction Rate of a Natural Resource under Uncertainty. Econ. Lett. 43 231–234.

- [14] Ferrari, G., Yang, S. (2018). On an Optimal Extraction Problem with Regime Switching. Adv. Appl. Probab. 50(3) 671–705.

- [15] Guo, X., Zervos, M. (2015). Optimal Execution with Multiplicative Price Impact. Siam J. Finance Math. 6(1) 281–306.

- [16] Hotelling H. (1931). The Economics of Exhaustible Resources. J. Political Econ. 39(2) 137–175.

- [17] Jack, A., Jonhnson, T.C., Zervos M. (2008). A Singular Control Problem with Application to the Goodwill Problem. Stoch. Processes Appl. 118 2098–2124.

- [18] Jeanblanc, M., Yor, M., Chesney, M. (2006). Mathematical Methods for Financial Markets. Springer.

- [19] Karatzas, I., Shreve, S.E. (1984). Connections between Optimal Stopping and Singular Stochastic Control I. Monotone Follower Problems. SIAM J. Control Optim. 22 856–877.

- [20] Karatzas, I. (1985). Probabilistic Aspects of Finite-Fuel Stochastic Control. Proc. Natl. Acad. Sci. U.S.A. 82 5579–5581.

- [21] Karatzas, I., Shreve, S.E. (1986). Equivalent Models for Finite-Fuel Stochastic Control. Stochastics 18(3-4) 245–276.

- [22] Karatzas, I., Shreve, S.E. (1991). Brownian Motion and Stochastic Calculus. Second edition. Springer.

- [23] Karatzas, I., Ocone, D., Wang, H., Zervos, M. (2000). Finite-Fuel Singular Control with Discretionary Stopping. Stochastics 71(1-2) 1–50.

- [24] Lutz, B. (2010). Pricing of Derivatives on Mean-Reverting Assets. Springer.

- [25] Pemy, M. (2018). Explicit Solutions for Optimal Resource Extraction Problems under Regime Switching Lévy Models. Preprint, ArXiv: :1806.06105v1.

- [26] Pindyck R.S. (1978). The Optimal Exploration and Production of Nonrenewable Resources. J. Political Econ. 86(5) 841-861.

- [27] Pindyck R.S. (1980). Uncertainty and Exhaustible Resource Markets. J. Political Econ. 88(6) 1203–1225.

- [28] Protter, P.E. (1990). Stochastic Integration and Differential Equations. Springer.

- [29] Zhu H. (1992). Generalized Solution in Singular Stochastic Control: the Nondegenerate Problem. Appl. Math. Optim. 25 225–245.