MSP: A Multi-step Screening Procedure

for Sparse Recovery

Abstract

We propose a Multi-step Screening Procedure (MSP) for the recovery of sparse linear models in high-dimensional data. This method is based on a repeated small penalty strategy that quickly converges to an estimate within a few iterations. Specifically, in each iteration, an adaptive lasso regression with a small penalty is fit within the reduced feature space obtained from the previous step, rendering its computational complexity roughly comparable with the Lasso. MSP is shown to select the true model under complex correlation structures among the predictors and response, even when the irrepresentable condition fails. Further, under suitable regularity conditions, MSP achieves the optimal minimax rate for the upper bound of -norm error. Numerical comparisons show that the method works effectively both in model selection and estimation, and the MSP fitted model is stable over a range of small tuning parameter values, eliminating the need to choose the tuning parameter by cross-validation. We also apply MSP to financial data and show that MSP is successful in asset allocation selection.

Keywords: High-dimensional data; Iterative algorithm; Lasso; Multi-step method.

1 Introduction

Sparse recovery is of paramount interest in high-dimensional statistical problems where many predictors are available yet the regression function is well approximated by a few relevant covariates. A seminal contribution to this endeavor, the Lasso (Tibshirani,, 1996) simultaneously performs model selection and parameter estimation through regularization with a convex penalty. Now widely used for sparse recovery in practice, further extensions of the Lasso have enhanced its applicability and offered some theoretical guarantees, for example, see Efron et al., (2004); Friedman et al., (2010); Meinshausen and Bühlmann, (2006); Zhao and Yu, (2006); Zou, (2006); Fan and Lv, (2010); Hastie et al., (2015); Bühlmann and Van De Geer, (2011).

Although convex regularization methods such as the Lasso are computationally attractive and enjoy great performance in prediction, they also lead to biased estimates and require rather restrictive conditions on the design matrix to obtain model selection consistency. Nonconvex penalization procedures such as SCAD (Fan and Li,, 2001), MCP (Zhang, 2010a, ) and the Spike-and-Slab Lasso (SSL) (Ročková and George,, 2018) have been proposed to lessen the bias. Multi-step methods do this too, including Zhang, 2010b who proposed the Capped regularization, leading to a multi-step convex relaxation scheme which is shown to obtain the correct feature set after a certain number of iterations. Zou and Li, (2008) proposed a unified algorithm based on the local linear approximation (LLA) for maximizing the penalized likelihood, presenting a one-step low-dimensional asymptotic analysis for justification. Fan et al., (2014) provided a unified theory to show how to obtain the oracle solution via LLA. The theoretical properties of LLA highly rely on the initial estimates. Bühlmann and Meier, (2008) proposed a method called multi-step adaptive lasso (MSA-Lasso), which updates the adaptive weights and re-estimates the entire set of regression coefficients at each iteration until convergence. Huang and Zhang, (2012) showed that, under certain conditions, the multi-step framework can improve the solution quality. Further work focusing on multi-step methods includes Liu et al., (2016); Wang et al., (2013); Zhang and Zhang, (2012).

In spite of the fact that most nonconvex penalties do not require the irrepresentable condition to achieve model selection consistency (Fan and Li,, 2001; Zhang, 2010a, ), identifying the relevant predictors in the presence of highly collinear predictors may still present numerical challenges, as shown in Sections 4 and 5. Indeed, nonconvex penalties can introduce numerical difficulties in fitting models, becoming less computationally efficient than convex optimization problems.

The main thrust of this paper, is to propose a Multi-step Screening Procedure (MSP), a simple multi-step method with the following characteristics:

-

(1)

MSP applies a single small penalty parameter, which remains fixed throughout, to minimize bias at each iteration. At each step, the active set is shrunk by deleting the “useless” variables whose coefficients have been thresholded to 0. When dealing with high dimensional data, this strategy will start off with a large model with many possibly incorrect variables and iteratively distinguish the nonzeros from zeros.

-

(2)

This backward deletion strategy of MSP significantly reduces the execution time of the multi-step method. As will be seen in simulations, the computational complexity of MSP is roughly comparable to the solution path of Lasso.

-

(3)

With an inherently small estimation error bound, MSP successfully recovers the true underlying sparse model even when the irrepresentable condition is relaxed. Indeed, MSP remains effective even when the irrelevant variables are strongly correlated with the relevant variables. Note that although many nonconvex methods do not require restrictive conditions on the design matrix in theory, they may still have difficulty in selecting the right model with finite samples. MSP is much better able to deal with such data.

-

(4)

It is seen in simulations that the MSP fitted model is stable over a range of small tuning parameter values, eliminating the need to choose the tuning parameter by cross-validation. The solution of this method is both sparse and stable.

This paper is organized as follows. Section 2 presents the method and discusses its relationship to other methods. Section 3 shows its theoretical properties. The simulations in Section 4 and application in Section 5 assess the performance of the proposed method and compare it with several existing methods. Technical details are provided in the Supplementary Material.

2 Method

In this section, we present the details of the MSP algorithm and compare it with existing methods. We consider the linear regression problem:

where is an response vector, is an matrix, is a vector of regression coefficients and is the error vector. We are particularly interested in the case where the number of parameters greatly exceeds the number of observations (). We consider the -sparse model, where has at most nonzero elements. Components of the error vector are independently distributed from . The data and coefficients are allowed to change as grows; meanwhile, and are allowed to grow with . For notational simplicity, we do not index them with .

Recall that the Lasso estimator (Tibshirani,, 1996) minimizes squared error loss regularized with the -penalty. Compared to least squares, Lasso shrinks a particular set of coefficients to zero while shrinking the others towards zero. These two effects, model selection and shrinkage estimation, are controlled only by a single tuning parameter, leading to its well-known estimation bias. Although Zhao and Yu, (2006) and Meinshausen and Bühlmann, (2006) proved that the Lasso is model selection consistent under an irrepresentable condition, the condition is, however, quite restrictive. To mitigate these drawbacks, we propose MSP with two goals in mind: 1) recovery of the true sparse model when the irrepresentable condition fails; and 2) “almost unbiased estimation” by lowering the influence of the shrinkage penalty.

The essential idea behind MSP is to provide more precise estimation through iterated penalization with a smaller tuning parameter that is less influential at each step. More precisely, the MSP Algorithm proceeds as follows.

-

•

Initialize . Obtain a lasso solution :

and let be the nonzero index set of , i.e. .

-

•

Repeat the following steps until convergence:

where the active set is updated in every step, i.e. .

At convergence, denote the active set by and the solution by . Note that the active sets obtained during the iterations are nested, i.e.

as in each iteration an adaptive lasso is fit using only the features selected by the previous step. This is key to control the computational time of the algorithm as well as to maintain a rather small tuning parameter . We will provide more details on the choice of this small tuning parameter in the theoretical results.

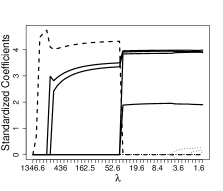

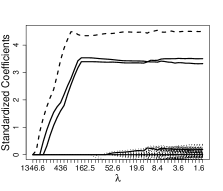

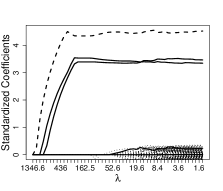

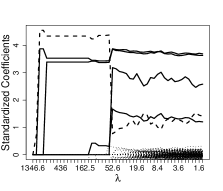

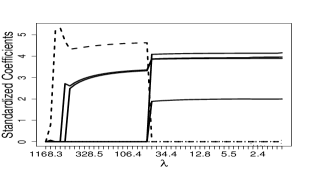

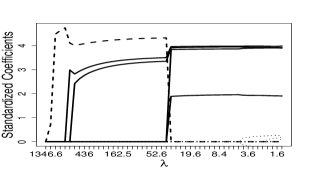

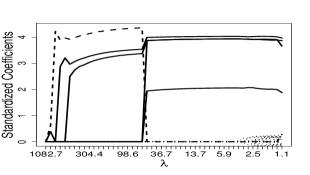

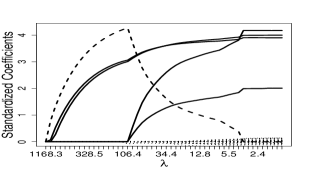

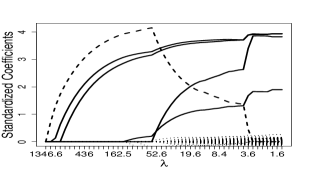

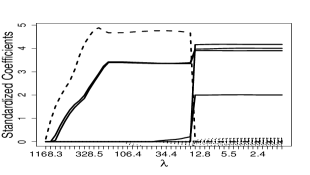

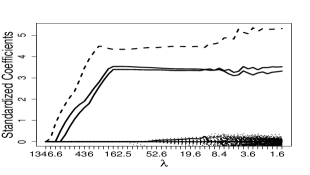

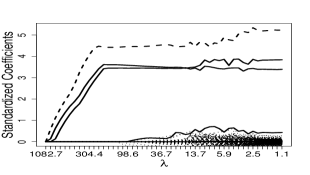

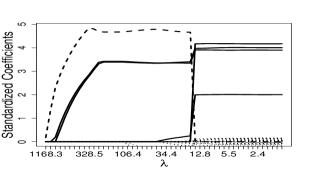

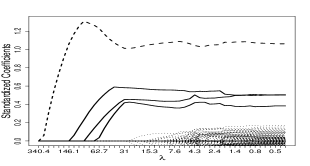

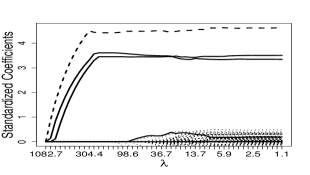

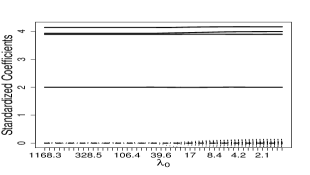

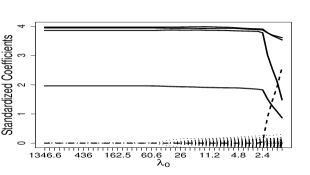

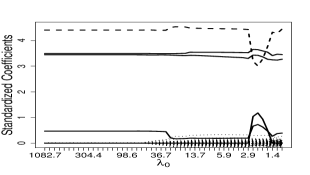

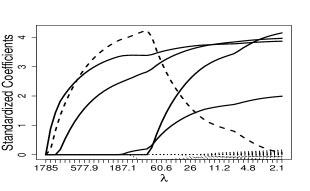

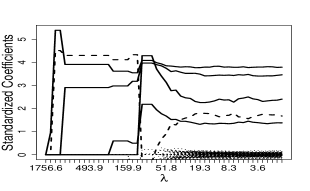

We use a simple example to demonstrate that many existing methods may not work as well as MSP when irrelevant variables are highly correlated with the relevant variables. Set and with 4 nonzero entries. In this example there exists a variable which is irrelevant but highly correlated with the relevant variables, hence the irrepresentable condition fails. Figure 1 shows eight methods’ (in)consistency in model selection: MSP, Lasso (Tibshirani,, 1996), LLA (Zou and Li,, 2008; Fan et al.,, 2014), MCP (Zhang, 2010a, ), SCAD (Fan and Li,, 2001), Adaptive Lasso (Zou,, 2006), OLS post Lasso (Belloni and Chernozhukov,, 2013) and Capped (Zhang, 2010b, ). As shown in Figure 1, except for MSP, all other methods pick up this irrelevant variable first and never shrink it back to zero. MSP performs similarly when is large, but when is small, MSP obtains a stable, accurate estimates and selects the right model. More details of this data example with further comparisons can be found in the simulation studies in Section 4.

2.1 Relationship to other methods

There are many widely used methods that estimate regression coefficients for sparse linear models well. In this section, we analyze the MSP solution and describe how our approach differs from these methods, more specifically, how MSP can select the right model when there exist strong correlations between the irrelevant and relevant variables.

Normally, is the key to control the amount of regularization, but the proposed method intends to use the iterations to do the controlling rather than using . Note for any , and , the solution of the th iteration of MSP is given by

where is the vector of signs of , and the equation on the right may be expressed as

| (1) |

where is the OLS estimator on the set . For , we make the following notes on the relevant and the irrelevant predictors respectively:

-

•

Assume and the first step of the MSP algorithm (i.e. Lasso) did not shrink its estimate to zero. Reviewing the estimation properties of the Lasso (Meinshausen and Yu,, 2009; Negahban et al.,, 2012), under the restricted eigenvalue condition and the proper choice of , this first iteration estimate is bounded by

with high probability. At the same time, it is not difficult to verify that has the same bound. According to (1), given , the penalty term for the th variable increases at the rate while is bounded by with some positive constant . Thus, the associated variable will be deleted from the active set in a finite number of steps, which we have found is typically few.

-

•

Assume satisfying the Beta-min condition for the nonzero coefficients (see (C.1) in the next section). Following the above argument, there will be a gap between its estimate and 0. Since is bounded away from zero and the penalty term will change little after several iterations, the algorithm will stabilize when all the irrelevant variables have been deleted.

To explain the difference between our method and others, we consider two examples, MCP (Zhang, 2010a, ) and LLA (Zou and Li,, 2008; Fan et al.,, 2014) for illustration. For the MCP, the method essentially uses a large penalty for variables whose estimated coefficients are close to zero and no penalty when the estimated coefficients are large. In the high-dimensional setting, however, by chance there often exist a few irrelevant variables whose estimated coefficients are not close to zero, and this is especially the case when the irrelevant variables are strongly correlated with the relevant variables. In practice, under such situations, a one-step procedure is often not sufficient to remove all irrelevant variables while keeping all relevant variables. See Figure 1. LLA, on the other hand, is an iterative method, but in each iteration, the method deals with the entire set of predictors, and since the number of irrelevant variables is always much larger than that of relevant variables, the iteration doesn’t really help in terms of choosing an appropriate value of the tuning parameter in comparison with one-step methods, especially when irrelevant variables are strongly correlated with relevant variables.

3 Theoretical results

We first define some notation. Without loss of generality, we assume the columns of are standardized: and for . Let , ; let , and . To state our theoretical results, we need the following assumptions.

-

(C.1) Beta-min condition: assume and there exists a positive constant that

-

(C.2) Restricted Eigenvalue (RE) condition: there exists a positive constant that

for all where .

(C.1) requires a small gap between and . It allows when but at a rate that can be distinguished. (C.1) has appeared frequently in the literature for proving model selection consistency, e.g. Zhao and Yu, (2006) and Zhang, 2010a . (C.2) is usually used to bound the -error between coefficients and estimates (Meinshausen and Yu,, 2009; Negahban et al.,, 2012), and is also the least restrictive condition of similar types, e.g. the restricted isometry property (Candes and Tao,, 2007) and the partial Riesz condition (Zhang and Huang,, 2008). It has been proved that (C.2) holds with high probability for quite general classes of Gaussian matrices for which the predictors may be highly correlated, in which case the irrepresentable condition or the restricted isometry condition may be violated with high probability (Raskutti et al.,, 2010).

We consider the following dimensions, in particular and where and . As a preparatory result, the following proposition shows that the first step of MSP selects an active set containing the true set with high probability.

Proposition 1

Suppose (C.1) and (C.2) hold. Set . Considering the first step of MSP, and the corresponding set , we have

| (2) |

REMARK 1. Since the first step estimator of MSP is the Lasso, Proposition 1 can be seen as proving a property for the Lasso estimator. We obtain this result by using the bound of -norm error between and , which is known from past work, e.g. Meinshausen and Yu, (2009) and Negahban et al., (2012). Proposition 1 supports the backward deletion strategy of MSP, which removes the variables that do not belong to as they are irrelevant with high probability.

REMARK 2. We set , which is the same as that for Lasso in order to achieve the error bound, while Lasso’s model selection consistency requires a larger tuning parameter, i.e. where . Hence when is large, the estimation accuracy and selection consistency cannot hold at the same time for Lasso. We solve this problem using an iterative strategy.

Now we show results on the error bound and the sign consistency of MSP.

Theorem 1

Suppose (C.1) and (C.2) hold. Set . For , with probability at least , the following error bounds for the estimate hold,

|

(3) |

where , and are defined in (C.1) and (C.2) respectively. Further, we have:

REMARK 3. Note that and have different orders under the assumption that

. If we consider another high dimensional setting, where , by setting , we would have the same result as in Theorem 1.

For simplicity, we use the same value for and in simulation studies and empirical analysis.

REMARK 4. The error bound of MSP in (3) is influenced by the adaptive penalty. We allow to converge to 0 in (C.1), i.e., the lower bound of is for . As a consequence, dominates the denominator of the error bound of MSP rather than . When is close to , the -norm error bound is close to the rate .

Now suppose (C.1) is replaced by the following condition:

-

(C.1)* For the nonzero coefficients, let and assume .

Note (C.1)* sets a lower bound for where is allowed to be any positive constant. This condition has also appeared frequently in the literature, e.g. Huang et al., (2008). Replacing (C.1) by (C.1)* and considering the following dimensions: and where and , Corollary 1 shows that the -error and the -error of the MSP estimator achieve the rate and , respectively.

Corollary 1

Suppose (C.1)* and (C.2) hold. Set . With probability , the following error bounds hold for :

|

(4) |

Further, we have:

REMARK 5. Note the Gaussian assumption on the error term in the linear regression model can be relaxed by a subgaussian assumption. Specifically, there exist constants , such that for ,

4 Simulation studies

In this section, we use simulation studies to demonstrate the performance of the proposed method: 1) the first part illustrates MSP’s consistency in model selection; 2) the second part compares the performance of the proposed method with those of several existing methods, and also analyzes the stability of MSP with respect to the tuning parameter ; and 3) the third part evaluates the computational time of different methods.

Of the existing methods that are compared with the proposed method, we choose three one-step methods, Lasso (Tibshirani,, 1996), SCAD (Fan and Peng,, 2004) and MCP (Zhang, 2010a, ), and four multi(two)-step methods, Adaptive Lasso (Zou,, 2006) (denoted as Alasso), OLS post Lasso (denoted as Plasso) (Belloni and Chernozhukov,, 2013), Capped (Zhang, 2010b, ) and LLA (Zou and Li,, 2008; Fan et al.,, 2014). In addition, we also compare with a Bayesian method, SSL (Ročková and George,, 2018). We use the R package SSLASSO to run SSL; results of MCP, SCAD and LLA are obtained using the R ncvreg package (Breheny and Huang,, 2011), and results of other methods are based on the R glmnet package (Friedman et al.,, 2010).

We consider the following linear regression model for simulation studies

where are generated from a multivariate normal distribution and is generated from . Four regression coefficients are set as nonzero, specifically , and others are set to zero. We consider the case where some irrelevant variable is highly correlated with the relevant variables. Specifically, we set

where is generated from . Denote the covariance matrix of the last variables as . We consider two scenarios: (1) , and (2) , where .

In both scenarios, the RE condition (C.2) holds while the irrepresentable condition fails. Recall the irrepresentable condition states that: there exists a positive constant such that

With and , it is not difficult to check that the irrepresentable condition does not hold. Figure 1 in Section 2 shows the results from one typical simulation repetition when under scenario 1.

We compare both the estimation and selection performances of the nine methods mentioned above. The -norm () and the -norm errors () are computed. We also report the estimated number of nonzero coefficients (NZ), as well as the false positive rate (FPR) and the true positive rate (TPR), which are respectively defined as

| FPR | ||||

| TPR |

4.1 Model selection

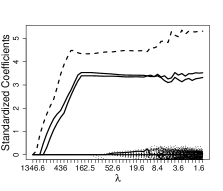

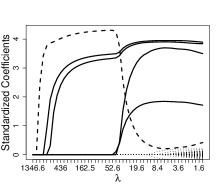

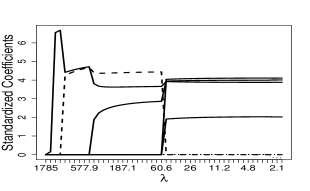

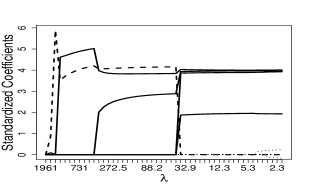

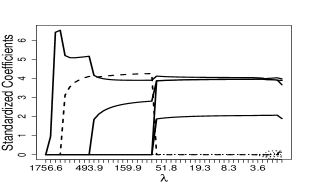

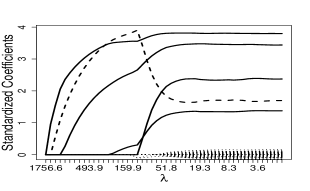

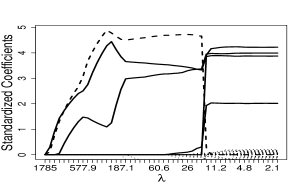

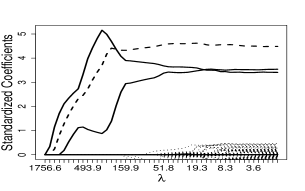

We consider three different dimensions, =40, 400 and 4000, and is fixed to be 200. Due to lack of space, we only show representative results in the main manuscript and delay other results in the supplementary material. Specifically, Figure 2 shows the comparison between the proposed MSP, Capped-, LLA, MCP and SSL under Scenario 1, while Figure 3 shows the comparison between MSP and Lasso, PLasso and SCAD under Scenario 2. As we can see in Figure 2, when is large, the first 4 methods select the irrelevant variable (as it is highly correlated with the relevant variables and the response). When decreases, in the case of relatively low dimension (left column), LLA and MCP are able to shrink the estimated coefficient for to zero but at the same time select many other irrelevant variables; while in the case of relatively high dimension (middle and right columns), LLA and MCP are not even able to shrink the estimated coefficient for to zero. Capped- performs slightly better as it is able to shrink the estimated coefficient for to zero in both low and high dimensional settings when is very small but at the same time also selects many irrelevant variables. SSL chooses the correct model when =40 and 400, however, when becomes larger, SSL always selects as an important variable. As a comparison, MSP chooses the exact correct model over a wide range of small values of in all settings.

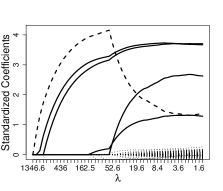

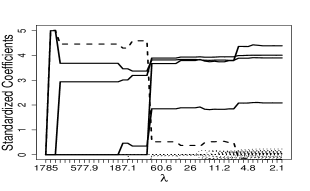

The results in Figure 3 are similar as in Scenario 1: Lasso, PLasso and SCAD are able to shrink the estimated coefficient for to zero when is small and the dimension is relatively low, but at the same time select many other irrelevant variables, and completely fail to shrink the estimated coefficient for to zero when the dimension is relatively high. The proposed MSP is again able to identify the correct model when is relatively small in all three considered dimensional settings.

We also want to note that, as one can see in both Figures 2 and 3, the MSP solution is quite stable over a wide range of small values of . This implies that MSP requires little tuning, which is a convenient and useful property in practice and different from many other regularization methods that require careful selection of the tuning parameter.

s

4.2 Performance comparison

We consider two settings, and . While cross-validation is not needed for SSL, the tuning parameter for all other methods is selected using 10-fold cross-validation. Each simulation is repeated 100 times. The results are summarized in Tables 1 and 2. It can be seen that MSP uniformly outperforms other methods in both estimation accuracy and model selection.

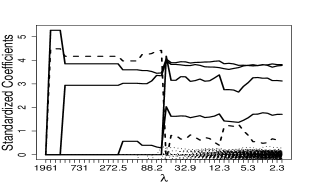

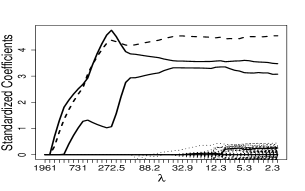

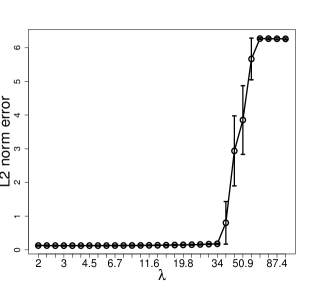

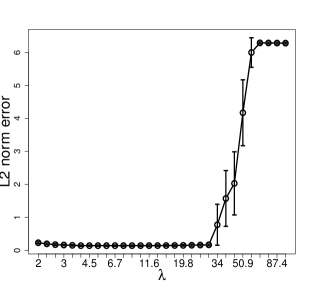

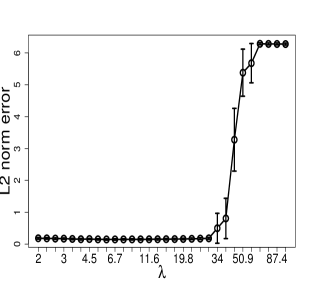

Figure 4 shows the estimation error of MSP when varies under the same simulation setting of Table 2, i.e. Scenario 1 with , and respectively. As one can see, the estimation error of MSP is low and stable over a range of small values. The results under Scenario 2 are similar and thus omitted. This implies that cross-validation may not be necessary for MSP in practice; setting at an appropriately small value often works well, for example, we found is a reasonable choice after standardizing the design matrix and the response variable.

| Method | -error | -error | NZ | FPR | TPR |

|---|---|---|---|---|---|

| = | (100, 50) | ||||

| MSP | 0.19 ( 0.07 ) | 0.33 ( 0.12 ) | 4.00 ( 0.00 ) | 0.00 ( 0.00 ) | 1.00 ( 0.00 ) |

| Lasso | 2.05 ( 0.81 ) | 2.16 ( 0.40 ) | 19.47 ( 2.98 ) | 0.34 ( 0.06 ) | 1.00 ( 0.00 ) |

| MCP | 6.44 ( 0.12 ) | 3.61 ( 0.06 ) | 7.74 ( 1.22 ) | 0.11 ( 0.02 ) | 0.63 ( 0.13 ) |

| SCAD | 6.40 ( 0.11 ) | 3.56 ( 0.06 ) | 8.14 ( 1.29 ) | 0.12 ( 0.03 ) | 0.65 ( 0.12 ) |

| SSL | 0.31 ( 0.61 ) | 0.73 ( 1.26 ) | 9.94 ( 3.53 ) | 0.13 ( 0.08 ) | 1.00 ( 0.05 ) |

| ALasso | 0.38 ( 0.35 ) | 0.79 ( 0.33 ) | 5.56 ( 1.06 ) | 0.03 ( 0.02 ) | 1.00 ( 0.00 ) |

| PLasso | 1.13 ( 1.29 ) | 1.46 ( 0.63 ) | 8.46 ( 1.45 ) | 0.10 ( 0.03 ) | 0.99 ( 0.05 ) |

| Capped- | 2.05 ( 0.81 ) | 2.16 ( 0.40 ) | 19.47 ( 2.98 ) | 0.34 ( 0.06 ) | 1.00 ( 0.00 ) |

| LLA | 6.40 ( 0.11 ) | 3.56 ( 0.06 ) | 8.14 ( 1.29 ) | 0.12 ( 0.03 ) | 0.65 ( 0.12 ) |

| = | (100, 200) | ||||

| MSP | 0.25 ( 0.64 ) | 0.44 ( 1.32 ) | 4.02 ( 0.20 ) | 0.00 ( 0.00 ) | 1.00 ( 0.05 ) |

| Lasso | 3.50 ( 0.88 ) | 7.66 ( 1.83 ) | 21.53 ( 3.48 ) | 0.09 ( 0.02 ) | 1.00 ( 0.00 ) |

| MCP | 6.51 ( 0.70 ) | 14.33 ( 1.65 ) | 18.00 ( 2.66 ) | 0.08 ( 0.01 ) | 0.64 ( 0.13 ) |

| SCAD | 6.50 ( 0.22 ) | 13.88 ( 0.74 ) | 21.55 ( 3.73 ) | 0.10 ( 0.02 ) | 0.66 ( 0.12 ) |

| SSL | 2.77 ( 3.01 ) | 6.41 ( 6.51 ) | 24.88 ( 8.08 ) | 0.11 ( 0.04 ) | 0.88 ( 0.17 ) |

| ALasso | 1.19 ( 1.36 ) | 2.23 ( 2.58 ) | 5.11 ( 0.96 ) | 0.01 ( 0.01 ) | 1.00 ( 0.03 ) |

| PLasso | 4.89 ( 2.27 ) | 9.66 ( 4.49 ) | 6.01 ( 1.23 ) | 0.02 ( 0.01 ) | 0.76 ( 0.15 ) |

| Capped- | 3.50 ( 0.88 ) | 7.66 ( 1.83 ) | 21.53 ( 3.48 ) | 0.09 ( 0.02 ) | 1.00 ( 0.00 ) |

| LLA | 6.50 ( 0.22 ) | 13.88 ( 0.74 ) | 21.55 ( 3.73 ) | 0.10 ( 0.02 ) | 0.66 ( 0.12 ) |

| Method | -error | -error | NZ | FPR | TPR |

|---|---|---|---|---|---|

| = | (100, 50) | ||||

| MSP | 0.22 ( 0.09 ) | 0.37 ( 0.17 ) | 4.00 ( 0.00 ) | 0.00 ( 0.00 ) | 1.00 ( 0.00 ) |

| Lasso | 1.82 ( 0.78 ) | 4.91 ( 1.74 ) | 25.87 ( 3.14 ) | 0.48 ( 0.07 ) | 1.00 ( 0.00 ) |

| MCP | 6.46 ( 0.19 ) | 13.14 ( 0.50 ) | 7.89 ( 1.52 ) | 0.12 ( 0.03 ) | 0.63 ( 0.13 ) |

| SCAD | 6.43 ( 0.17 ) | 13.44 ( 0.50 ) | 13.60 ( 2.35 ) | 0.24 ( 0.05 ) | 0.69 ( 0.11 ) |

| SSL | 0.23 ( 0.09 ) | 0.43 ( 0.19 ) | 5.67 ( 1.84 ) | 0.04 ( 0.04 ) | 1.00 ( 0.00 ) |

| ALasso | 0.61 ( 0.55 ) | 1.15 ( 1.06 ) | 4.88 ( 0.90 ) | 0.02 ( 0.02 ) | 1.00 ( 0.00 ) |

| PLasso | 1.14 ( 1.08 ) | 2.63 ( 2.24 ) | 9.18 ( 1.79 ) | 0.11 ( 0.04 ) | 0.99 ( 0.04 ) |

| Capped- | 1.82 ( 0.78 ) | 4.91 ( 1.74 ) | 25.87 ( 3.14 ) | 0.48 ( 0.07 ) | 1.00 ( 0.00 ) |

| LLA | 6.43 ( 0.17 ) | 13.44 ( 0.50 ) | 13.60 ( 2.35 ) | 0.24 ( 0.05 ) | 0.69 ( 0.11 ) |

| = | (100, 200) | ||||

| MSP | 0.28 ( 0.63 ) | 0.49 ( 1.28 ) | 4.01 ( 0.10 ) | 0.00 ( 0.00 ) | 1.00 ( 0.05 ) |

| Lasso | 2.96 ( 1.11 ) | 2.67 ( 0.43 ) | 33.50 ( 4.38 ) | 0.15 ( 0.02 ) | 1.00 ( 0.03 ) |

| MCP | 6.48 ( 0.12 ) | 3.62 ( 0.05 ) | 7.67 ( 1.74 ) | 0.03 ( 0.01 ) | 0.55 ( 0.10 ) |

| SCAD | 6.45 ( 0.12 ) | 3.59 ( 0.05 ) | 8.66 ( 2.24 ) | 0.03 ( 0.01 ) | 0.56 ( 0.10 ) |

| SSL | 1.55 ( 2.53 ) | 3.24 ( 5.25 ) | 9.73 ( 4.32 ) | 0.03 ( 0.02 ) | 0.93 ( 0.16 ) |

| ALasso | 0.89 ( 1.28 ) | 1.14 ( 0.71 ) | 6.57 ( 1.77 ) | 0.01 ( 0.01 ) | 1.00 ( 0.04 ) |

| PLasso | 2.01 ( 2.15 ) | 1.95 ( 0.93 ) | 10.43 ( 2.29 ) | 0.03 ( 0.01 ) | 0.95 ( 0.11 ) |

| Capped- | 2.96 ( 1.11 ) | 2.67 ( 0.43 ) | 33.50 ( 4.38 ) | 0.15 ( 0.02 ) | 1.00 ( 0.03 ) |

| LLA | 6.45 ( 0.12 ) | 3.59 ( 0.05 ) | 8.66 ( 2.24 ) | 0.03 ( 0.01 ) | 0.56 ( 0.10 ) |

4.3 Computational cost

To compare the computational cost of different methods, we considering the following settings: and under Scenario 1. Each running time involves 100 different values covering a wide range. For MSP, Lasso, ALasso, LLA, Cappled- and MSA, we used the R glmnet package (Friedman et al.,, 2010); for SSL, we used the SSLASSO package (Ročková and George,, 2018), and for SCAD and MCP, we used the R ncvreg package (Breheny and Huang,, 2011).

Table 3 summarizes the results. As one can see, the computational cost of MSP is in general larger than that of Lasso, but becomes more comparable as both and increase. In comparison with non-convex one-step methods, including MCP and SCAD, MSP is slower when and are small, but faster when and are large. Further, the computational cost of MSP is much lower than that of SSL and those of other multi(two)-step methods, including the Adaptive Lasso, LLA, Capped- and MSA; this is because the MSP only deals with the high-dimensional data in the first step, while other methods deal with the entire data set in every step.

| Lasso | MCP | SCAD | MSP | ALasso | SSL | LLA | Capped- | MSA | ||

|---|---|---|---|---|---|---|---|---|---|---|

| (, ) | mean | 0.01 | 0.05 | 0.04 | 0.71 | 0.28 | 0.78 | 1.02 | 1.46 | 1.48 |

| sd | 0.01 | 0.01 | 0.01 | 0.02 | 0.03 | 0.09 | 0.41 | 0.26 | 0.24 | |

| (, ) | mean | 0.02 | 0.04 | 0.07 | 0.58 | 0.89 | 0.77 | 2.01 | 4.64 | 4.04 |

| sd | 0.01 | 0.01 | 0.01 | 0.02 | 0.07 | 0.42 | 0.14 | 0.75 | 0.87 | |

| (, ) | mean | 0.25 | 0.52 | 0.38 | 0.59 | 7.67 | 4.10 | 16.47 | 21.04 | 18.02 |

| sd | 0.02 | 0.04 | 0.03 | 0.04 | 0.42 | 1.58 | 1.44 | 2.65 | 3.76 | |

| (, ) | mean | 0.33 | 4.08 | 4.83 | 2.03 | 7.31 | 76.15 | 95.76 | 216.24 | 24.16 |

| sd | 0.02 | 0.60 | 0.58 | 0.09 | 0.51 | 3.57 | 6.13 | 53.04 | 4.84 | |

| (, ) | mean | 1.21 | 7.79 | 4.28 | 3.77 | 43.87 | 81.75 | 282.58 | 388.00 | 148.18 |

| sd | 0.17 | 0.70 | 0.29 | 0.17 | 1.67 | 17.72 | 36.03 | 46.56 | 6.15 | |

| (, ) | mean | 10.96 | 33.22 | 32.30 | 14.48 | 644.87 | 302.12 | 1387 | 1508 | 1535 |

| sd | 0.08 | 3.30 | 0.22 | 0.23 | 29.73 | 86.47 | 126 | 196 | 224 |

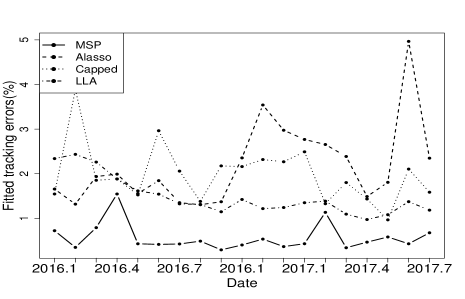

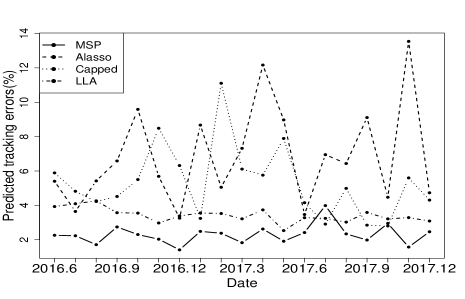

5 Empirical analysis: index tracking

In this section, we apply the proposed method to the important and useful index tracking problem in financial modeling. Roughly speaking, index tracking aims to replicate the movement of a financial index using a small set of financial assets, e.g. stocks, and is the core of the index fund. This is a high dimensional data modeling problem as the number of stocks that one can choose from is often on the order of hundreds or thousands, while the number of observations (days) is on the order of tens or hundreds. Further, due to transactional cost, one only wishes to select a few rather than many stocks (i.e. a sparse model) to mimic the behavior of the index.

We consider the S&P500 index and the following model: where denotes the return of the S&P500 index on day , denotes the return of stock on day and is the weight of stock . We consider 19 rolling periods from January 2016 till December 2017 and divide each period into training (=100 days) and testing (=20 days) parts. The training period is used to select stocks and estimate the corresponding ’s and then the testing part is used to evaluate the performance.

We compare 4 methods, including MSP, LLA, Capped- and ALasso, as these four methods had better performances in simulation studies. To measure the performance of different methods, we use the tracking error (Meade and Salkin,, 1989), which is a standard measure used in the financial industry to assess the performance of tracking. It is defined as

where , with and being the daily return of the index and the daily return of the constructed index on day respectively.

We did not use the validation or cross-validation approach to select the tuning parameter; instead, we chose the tuning parameter for each method such that the number of selected stocks is 20, which is often the way done in practice. Figure 5 shows the 19 tracking errors for both training and testing sets over time. As can be seen, MSP always produces lower and more stable errors than other methods, except for one rolling period.

SUPPLEMENTARY MATERIAL

- Title:

-

Supplementary material for “MSP: A Multi-step Screening Procedure for Sparse Recovery’. (pdf)

References

- Belloni and Chernozhukov, (2013) Belloni, A. and Chernozhukov, V. (2013). Least squares after model selection in high-dimensional sparse models. Bernoulli, 19:521–547.

- Breheny and Huang, (2011) Breheny, P. and Huang, J. (2011). Coordinate descent algorithms for nonconvex penalized regression, with applications to biological feature selection. Annals of Applied Statistics, 5:232–253.

- Bühlmann and Meier, (2008) Bühlmann, P. and Meier, L. (2008). Discussion: “one-step sparse estimates in nonconcave penalized likelihood models,” by Zou, H. and Li, R. Annals of Statistics, 36:1534–1541.

- Bühlmann and Van De Geer, (2011) Bühlmann, P. and Van De Geer, S. (2011). Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media.

- Candes and Tao, (2007) Candes, E. and Tao, T. (2007). The dantzig selector: statistical estimation when p is much larger than n. Annals of Statistics, 35(6):2313–2351.

- Efron et al., (2004) Efron, B., Hastie, T., Johnstone, L., and Tibshirani, R. (2004). Least angle regression. Annals of Statistics, 32(2):407–451.

- Fan and Li, (2001) Fan, J. and Li, R. (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association, 96(456):1348–1360.

- Fan and Lv, (2010) Fan, J. and Lv, J. C. (2010). A selective overview of variable selection in high dimensional feature space. Statistica Sinica, 20(1):101.

- Fan and Peng, (2004) Fan, J. and Peng, H. (2004). Nonconcave penalized likelihood with a diverging number of parameters. Annals of Statistics, 32(3):928–961.

- Fan et al., (2014) Fan, J., Xue, L., and Zou, H. (2014). Strong oracle optimality of folded concave penalized estimation. Annals of Statistics, 42(3):819–849.

- Friedman et al., (2010) Friedman, J., Hastie, T., and Tibshirani, R. J. (2010). Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software, 33(1):1–22.

- Hastie et al., (2015) Hastie, T., Tibshirani, R., and Wainwright, M. (2015). Statistical learning with sparsity: the lasso and generalizations. Chapman and Hall/CRC.

- Huang et al., (2008) Huang, J., Ma, S., and Zhang, C.-H. (2008). Adaptive lasso for sparse high-dimensional regression models. Statistica Sinica, 18(4):1603–1618.

- Huang and Zhang, (2012) Huang, J. and Zhang, C.-H. (2012). Estimation and selection via absolute penalized convex minimization and its multistage adaptive applications. Journal of Machine Learning Research, 13(1):1839–1864.

- Liu et al., (2016) Liu, H., Yao, T., and Li, R. (2016). Global solutions to folded concave penalized nonconvex learning. Annals of statistics, 44(2):629.

- Meade and Salkin, (1989) Meade, N. and Salkin, G. R. (1989). Index funds—construction and performance measurement. Journal of the Operational Research Society, 40(10):871–879.

- Meinshausen and Bühlmann, (2006) Meinshausen, N. and Bühlmann, P. (2006). High-dimensional graphs and variable selection with the lasso. Annals of Statistics, 34(3):1436–1462.

- Meinshausen and Yu, (2009) Meinshausen, N. and Yu, B. (2009). Lasso-type recovery of sparse representations for high-dimensional data. Annals of Statistics, 37(1):246–270.

- Negahban et al., (2012) Negahban, S., Ravikumar, P., Wainwright, M. J., and Yu, B. (2012). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical Science, 27(4):1348–1356.

- Raskutti et al., (2010) Raskutti, G., Wainwright, M. J., and Yu, B. (2010). Restricted eigenvalue properties for correlated gaussian designs. Journal of Machine Learning Research, 11:2241–2259.

- Ročková and George, (2018) Ročková, V. and George, E. I. (2018). The spike-and-slab lasso. Journal of the American Statistical Association, 113(521):431–444.

- Tibshirani, (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B, 58(1):267–288.

- Wang et al., (2013) Wang, L., Kim, Y., and Li, R. (2013). Calibrating non-convex penalized regression in ultra-high dimension. Annals of statistics, 41(5):2505.

- (24) Zhang, C.-H. (2010a). Nearly unbiased variable selection under minimax concave penalty. Annals of Statistics, 38(2):894–942.

- Zhang and Huang, (2008) Zhang, C.-H. and Huang, J. (2008). The sparsity and bias of the lasso selection in high-dimensional linear regression. Annals of Statistics, 36(4):1567–1594.

- Zhang and Zhang, (2012) Zhang, C.-H. and Zhang, T. (2012). A general theory of concave regularization for high-dimensional sparse estimation problems. Statistical Science, 27(4):576–593.

- (27) Zhang, T. (2010b). Analysis of multi-stage convex relaxation for sparse regularization. Journal of Machine Learning Research, 11:1081–1107.

- Zhao and Yu, (2006) Zhao, P. and Yu, B. (2006). On model selection consistency of lasso. Journal of Machine Learning Research, 7:2541–2563.

- Zou, (2006) Zou, H. (2006). The adaptive lasso and its oracle properties. Journal of the American Statistical Association, 101(476):1418–1429.

- Zou and Li, (2008) Zou, H. and Li, R. (2008). One-step sparse estimates in nonconcave penalized likelihood models. Annals of Statistics, 36(4):1509–1533.