Robust consumption-investment problem Under CRRA and CARA utilities with time-varying confidence sets

Abstract.

We consider a robust consumption-investment problem under CRRA and CARA utilities. The time-varying confidence sets are specified by , a correspondence from to the space of Lévy triplets, and describe priori information about drift, volatility and jump. Under each possible measure, the log-price processes of stocks are semimartingales and the triplet of their differential characteristics is a measurable selector from the correspondence almost surely. By proposing and studying the global kernel, an optimal policy and a worst-case measure are generated from a saddle point of the global kernel, and they also constitute a saddle point of the objective function. AMS 2000 Subject Classification: 91B28; 93E20; 49K35. JEL Classifications: G11; C61. Keywords: Robust Merton problem; Knightian uncertainty; Minimax problem; Time-varying confidence sets; Measurable saddle point; Deterministic-to-stochastic paradigm.

1. Introduction

We consider a robust Merton (consumption-investment) problem of the form

in a continuous-time market with jumps. Given the investment period , the objective function is the expectation of the sum of cumulative and terminal utilities, which is a function of consumption process and terminal wealth . The policy uniquely determines and , that is, there is a mapping from policy to consumption process and terminal wealth. The utility function is strictly concave and increasing due to the risk aversion, such as CRRA and CARA utilities. The supremum is taken over all admissible policies, and the infimum is over all possible measures for the log-price processes of the stocks. Rigorously, a policy is admissible if and only if it is predictable and the values of and are in the domain of . The model uncertainty is parameterized by , a correspondence from to the space of Lévy triplets . A measure is possible if and only if the log-price processes are semimartingales under , and the triplet of their differential characteristics is a measurable selector from almost surely.

The consumption-investment problem is firstly studied by Merton (1969, 1971) with the Black-Scholes model. The Black-Scholes model assumes the log-price processes of stocks are described by a drifted Brownian motion, which facilities an explicit expression of optimal strategy. As the research progresses, people try to weaken the assumptions for the dynamic of stocks and still hope to get an explicit or semi-explicit solution. Kallsen (2000) and Nutz (2012) both use Lévy processes to characterize the log-price, so that the wealth process is an exponential Lévy process. Stoikov and Zariphopoulou (2005), Kallsen and Muhle-Karbe (2010) and Benth et al. (2010) propose specific models for the volatility of log-price, such as Heston model, Carr model, and Barndorff-Nielsen-Shephard model. Usually, a complex model can characterize the reality more accurately with fewer assumptions, but more parameters will be needed. Especially when the market is nonstationary, the parameters could be time-varying and hardly estimated. Therefore, it is reasonable to adopt a robust model to describe the market. In practice, people only need to estimate the confidence set of each parameter to establish a robust model. We herewith consider a robust model to weaken the assumption and fortunately obtain the optimal value function and policy in semi-explicit form.

In the field of robust optimization, many papers focus on the investment (consumption-investment) problem. Talay and Zheng (2002) suppose all admissible measures have a same equivalent martingale measure, which is a dominated robust model. Schied (2008) adds a stochastic factor into the model of volatility, which makes the market incomplete but is still a dominated model. For nondominated robust models, Denis and Kervarec (2013) consider an investment problem under a bounded utility function, and Lin and Riedel (2014) solve a consumption-investment problem with the issue of non-equivalent multiple priors. Furthermore, Nutz (2016) and Neufeld and Nutz (2018) extend the model of stocks to the jump diffusion, for discrete-time and continuous-time investment problems, respectively. In this paper, we are interested in the robust consumption-investment problem with jump diffusions, which has not been studied yet. For each possible measure , the differential characteristics of log-price processes constitute a triplet , which is a measurable selector from the correspondence almost surely. Thus is a subset of all Lévy triplets and contains a priori information of drift, volatility and jump at time . Nontrivially, contains time-varying confidence sets, which does not appear in previous studies and causes difficulties in demonstrating the measurability of worst-case differential characteristics.

It is well known there are two commonly used methods to solve a stochastic optimization problem, namely the dynamic programming and the martingale method. The dynamic programming is firstly proposed by Merton (1971), which is from the idea of local optimization and describes the value function as a solution of a nonlinear PDE called Hamilton-Jacobi-Bellman (HJB) equation. The martingale method is developed by Cox and Huang (1989), which comes from the idea of global optimization by solving a dual problem. For a robust optimization, the ideas of these two methods still work. By the concept of G-Brownian motion (cf. Peng (2007, 2010)), the dynamic programming is still available for a robust problem, whose value function satisfies a Hamilton-Jacobi-Bellman-Isaacs (HJBI) equation. This method has been used in the fields of robust hedging problem, robust investment problem and robust investment-consumption problem, such as Tevzadze et al. (2013), Lin and Riedel (2014), Fouque et al. (2016) and Biagini and Pınar (2017). By introducing the conditional risk mapping as a dynamic analogues of coherent risk, the dynamic programming still can be established for this convex risk measure (cf. Artzner et al.(1999), Shapiro and Uğurlu (2016), Uğurlu (2017a)). Under a general uncertainty set with a reference probability measure, Uğurlu (2018) regards a robust optimal investment problem as a maximization problem with respect to the conditional risk mapping and then solves this problem explicitly by the robust dynamic programming equation. However, these two approaches derived from the dynamic programming are not adequate to solve the robust problem with jumps. Based on the idea of global optimization, a robust problem can be solved by finding its saddle point. Neufeld and Nutz (2018) characterize an optimal strategy by a saddle point of a deterministic function and accomplish the martingale argument under both logarithmic and power utilities. Uğurlu (2017b) directly analyzes the objective function and then obtains a saddle point by Sion’s minimax theorem.

This paper is devoted to solving the robust investment-consumption problem by the martingale method, under both CRRA and CARA utilities. We would like to name the method of Neufeld and Nutz (2018) as the martingale method of robust optimization because it is the martingale property that establishes the equivalence between a deterministic optimization and a stochastic optimization. Following this deterministic-to-stochastic paradigm, we introduce a deterministic functional (global kernel, cf. Definitions 3.4 and 4.2 below), then an optimal policy and a worst-case measure can be generated from its saddle point. There are three contributions in this paper: solving the robust investment-consumption problem with jump diffusions; treating exponential utilities; considering time-varying confidence sets. Because of these novelties, the deterministic optimization problem, which is finding a saddle point of global kernel over a product space of functionals, becomes an infinite-dimensional problem. The difficulty is inherent and cannot be avoided by any techniques because it is derived from the appearance of intertemporal consumption and time-varying confidence sets.

The rest of this paper is organized as follows. Section 2 presents the general model of the consumption-investment problem as well as the uncertainty set of semimartingale measures. Section 3 and Section 4 solve the robust consumption-investment problem for CRRA and CARA utilities, respectively, by martingale method. In Section 5, saddle points of global kernels for CRRA and CARA utilities are found without using Sion’s minimax theorem. Section 6 concludes. All proofs are in Appendixes A, B, C and D.

2. Robust Optimization

2.1. General Formulation

A general robust problem can be formulated as

| (2.1) |

where is the objective function, is the admissible policy set and is the uncertainty set. Below, we will introduce the definitions of , , and successively.

The objective function is the expectation of the sum of cumulative utilities and terminal utility.

| (2.2) |

where the expectation is taken under the measure . is the initial wealth, which is fixed and can be omitted for convenience. is the amount of consumption at time , and is the terminal wealth. They are all determined by the policy as well as . Here, we do not explain the rule that how determines consumption process and wealth process in detail, because the rule is different between the cases of CRRA and CARA utilities, respectively, in Sections 3 and 4. The utility function reflects the investor’s preference, which is usually concave and strictly increasing due to the risk aversion. For a given , we denote the value of (2.1) as

| (2.3) |

thus is the value function. We call optimal if it attains the supremum in (2.3) and worst-case if attaining the infimum.

Definition 2.1.

A policy is admissible if and only if

-

(i)

is predictable,

-

(ii)

, , -q.s,

where -q.s. is an abbreviation for quasi surely, which means a property holds -a.s. for all . The admissible policy set is the set of all admissible policies.

There are two essential conditions for admissible policy. The first one means the policy is established on the information from the past. The second one requires the consumption process and the terminal wealth both take values in the domain of the utility. Otherwise, the objective function would be negative infinity. For investors with CRRA utilities, the second condition prohibits the bankruptcy of terminal wealth and an injection of cash as a negative consumption.

2.2. Model uncertainty

We choose a Skorokhod space as the collection of all càdlàg path starting at origin and then there exists a natural -field by the Skorokhod topology. The canonical process can generate the natural filtration on . Same as Foldes (1990), we use to describe the log-price processes of stocks in the market and the model of the market is formulated by the measure on . Denote as the Polish space of all measures on and as the uncertainty set of all possible measures, then is much smaller than due to a priori information about drift, volatility and jump. Referring to the model of Chen and Epstein (2010) and Epstein and Ji (2014), we firstly introduce a correspondence for defining .

Let be the set of all -dimensional vectors with Euclidean metric and be the set of all symmetric positive definite matrices with metric induced from 2-norm. For any , denote

as a subset of all Lévy measures and let be the set of all Lévy measures. For any , we can define a metric on by

where is the measure defined by

and is the metric induced by -Hölder continuous functions, i.e., for any measure and ,

The subscript BH and superscript stand for boundedness and Hölder continuity with exponent . When , the metric space is exactly the space studied by Neufeld and Nutz (2014). For any positive , is a generalized metric space whose metric can be infinity on the set , while is a traditional metric space. Specifically, when , is the Kantorovich-Rubinshtein metric with (cf. theorem 8.3.2, Bogachev (2007)) and thus the customized metric induces the weak convergence on .

Therefore, the product space contains all Lévy triplets. Let be a compact subset of under the maximum metric:

for some . Thus is a separable metrizable space and has finite elements in . Generally speaking, the condition guarantees the existence of a measurable saddle point of global kernel, which will be thoroughly explained in Section 5 again.

Let be a weakly measurable correspondence from to , describing the range of all possible differential characteristics. The definition of weakly measurable correspondence is given by Aliprantis and Border (2006), definition 18.1, which is recall here for convenience.

Definition 2.2 (Aliprantis and Border (2006), 18.1 Definition).

Let be a measurable space and a topological space. We say that a correspondence is weakly measurable, if for each open subset of , where is the lower inverse (also called the weak inverse) of the correspondences and is defined by

Any measurable selector from correspondence is called the possible PII triplet because it has three components and corresponds to a possible PII measure introduced below. For convenience in notation, we give a convention that also represents the set of all possible PII triplets, i.e.,

This convention about would not cause any misunderstanding because one is a set and the other is a set-valued function. In previous studies of robust optimization, the confidence set is usually independent of the time , therefore, is a constant correspondence. The problem with constant correspondence is trivial because it can be easily solved by proposing the local kernel without considering the measurability of the optimal policy and the worst-case PII triplet.

Definition 2.3.

is a possible measure if and only if and under ,

-

(i)

is a semimartingale with predicable characteristics ;

-

(ii)

there exists a such that and

almost surely.

The triplet is called the DC (differential characteristics) triplet of under and is the set of all possible measures.

Definition 2.3 describes how to parameterize the model uncertainty by a correspondence . The uncertainty set contains all the semimartingale measures, under which the DC triplet of is a PII triplet almost surely. For a possible measure whose associated is independent of the probability space, we call it a possible PII measure because the log-price processes are processes with independent increments under this measure (cf. theorem II.4.15, Jacod and Shiryaev (2013)). The set of all possible PII measures is

| (2.4) |

which has a one-to-one relationship with , the set of all possible PII triplets. Finally, to make the uncertainty set have better properties, we give assumptions on as the end of this section.

Assumption 2.1.

For each , denote

as the union of all supports of Lévy measures in . Suppose is closed, bounded, and non-degenerate, i.e., there is a positive number such that

where represents the convex hull of a set.

Assumption 2.1 formulates the set of all possible jump sizes and demands is a closed set, which is also bounded and non-degenerate by a number . Though the support of any Lévy measure is closed, it is not trivial to assume is closed because it can be an infinite union. The closeness of actually contributes to the existence of an optimal policy over a nonclosed admissible policy set. In the definition of non-degeneracy, we require the convex hull of contains a neighborhood of origin, because the set may not be convex in general. Moreover, in the case of CRRA utility (see (3.3) below), it is enough to deduce the boundedness of admissible investment policy through the constraint on . The boundedness of jumps simplifies the differential notation for by omitting the truncation function (cf. definition I.2.6, Jacod and Shiryaev (2013)). For each ,

| (2.5) |

where is the DC triplet of under and is the compensated random measure with compensator . is a lower triangular matrix with positive diagonal entries and satisfies , which is unique by Cholesky decomposition (cf. Golub and Van Loan (2012)). is the corresponding -Brownian motion with respect to .

Assumption 2.2.

is closed-valued and convex-valued, i.e., is a closed and convex set for every .

Assumption 2.2 requires each confidence set is convex and closed, which is common in an optimization problem. If is not a singleton, must be contained in , otherwise has infinitely many elements in and is not compact. Furthermore, since is compact, is bounded convex and compact, which contributes to the existence of a worst-case PII triplet. In the range of , there are two significant values. When , the log-price processes have jumps of finite variation under each possible measure by theorem 21.9 of Sato (1999). When , under each possible measure, the log-price processes are compound non-homogeneous Poisson processes with finite activity by theorem 21.3 of Sato (1999). Finally, for avoiding redundant notations, we further assume the in Assumption 2.1 is the bound of each , i.e.,

3. CRRA Utilities

We consider a family of CRRA utilities

| (3.1) |

with coefficient and domain . has significance as the coefficient of relative risk aversion (cf. Pratt (1964)). This section consists of three parts. The first one specifies the rule of policy, that is, how to determine the consumption process and terminal wealth by an admissible policy. Then we introduce a deterministic function called global kernel and show its relationship with the objective function. Finally, a saddle point of global kernel generates an optimal policy and a worst-case measure of the robust consumption-investment problem.

3.1. Admissible Policy

Under CRRA utility, it is usual to choose the percentage of the wealth invested in stocks and the amount of consumption per time unit to maximize the objective function, such as Merton (1969) and Foldes (1990). However, based on the remark 2.1 of Nutz (2010), we set the policy , where is the investment amount to wealth ratio and is the consumption amount to wealth ratio at time . Under this rule, the wealth process is the solution of

| (3.2) |

and the amount of consumption at time is . From the second condition in Definition 2.1, the consumption ratio must be non-negative and the investment ratio must satisfy

The latter is a direct conclusion from the theorem I.6.61 of Jacod and Shiryaev (2013) and the discussion of Karatzas and Kardaras (2007). Hence the admissible policy set can be expressed elegantly by restricting the policies.

where . Recalling the condition of non-degeneracy in Assumption 2.1, we have

| (3.3) | ||||

thus is bounded by . Moreover, it can be verified that is a bounded convex set and contains the origin.

3.2. Global kernel for CRRA utilities

The global kernel is a functional defined on and is closely related to the objective function (see Lemma 3.1 below). Firstly, we introduce the deterministic policy set as a domain of the global kernel.

Definition 3.1.

is the set of all deterministic admissible policies.

Definition 3.2.

is called the generated policy from , if and

We say a deterministic admissible policy is optimal, if its generated policy attains the supremum in (2.3).

and have a close connection while is independent of the probability space. Retrospecting the expression of , we notice quasi surely for any . Meanwhile, any deterministic admissible policy in can generate an admissible policy in by Definition 3.2. Due to their close relationship, we can regard the elements in as in if there is no misunderstanding.

Definition 3.3.

The local kernel (at time ) is a function defined on :

where and .

Definition 3.4.

The global kernel (over period ) is a two-variable function defined on . For every and ,

Observing the expression of in Definition 3.3, we notice that the domain depends on time , but the function is independent. So we omit the subscript of as in Definition 3.4. The global kernel can be expressed by the policy and PII triplet directly, not through any intermediate variables, such as the consumption process and the terminal wealth. This is the advantage of the global kernel in contrast to the objective function. The motivation of proposing global kernel comes from the martingale equality in the following lemma.

Lemma 3.1.

For any and any , the objective function (2.2) can be expressed by , and directly.

For , is the equivalent measure whose Radon-Nikodym derivative is

Proof.

See Appendix A. ∎

We primarily use the property of exponential martingales to rewrite the objective function in Lemma 3.1. In Equation (2.2), the objective function depends on the policy through the intermediate variables and . While in Lemma 3.1, it is expressed as a function of , , and without any intermediate variables by using global kernel. Above equality of objective function and global kernel is very important in establishing the relationship between saddle points of and .

3.3. Optimal policy and worst-case measure

We present an assumption for the confidence sets and then demonstrate the existence of an optimal policy and a worst-case measure of the robust consumption-investment problem. For concentrating on the robust problem, we postpone the study about global kernel in Section 5 and acquiesce to the existence of its saddle point.

Assumption 3.1.

For any and ,

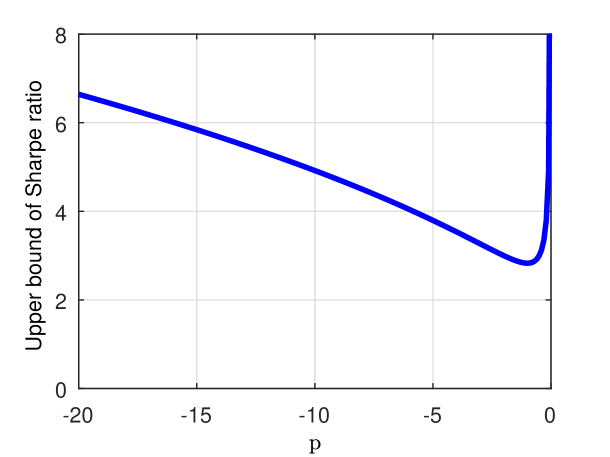

The condition in Assumption 3.1 is relaxed enough in the real market. Since is the Sharpe ratio of the diffusion process under measure , Assumption 3.1 indeed gives the upper bounds of Sharpe ratio under all possible measure for every . The upper bound is drawn in Figure 1 and attains the minimum as at . For a market with Sharpe ratio , the probability of a negative yield is after a year of investment. According to the annual returns of S&P 500 (^GSPC) Index from Jan 01, 1950 to Jan 01, 2018, there are 17 years that have negative returns, thus the probability of a negative yield is , which is much greater than . Referring to the Table C1 of Frazzini et al. (2013), we notice that the Sharpe ratio of overall US stocks is 0.39, and the Sharpe ratio of Buffett performance is about 0.7, which are both less than . Hence, Assumption 3.1 is undemanding and realistic. It plays an important role in finding a saddle point of the global kernel (see Section 5 below). Conceptually, it precludes the good market in which over-consumption occurs and thus simplifies the matters considered in kernel analyses.

As the end of this section, we present the main result of CRRA utilities that a saddle point of global kernel can generate an optimal policy and a worst-case measure.

Theorem 3.1.

There exist an optimal policy and a worst-case measure of the robust consumption-investment problem, denoted by and . Moreover,

-

(i)

is a saddle point of objective function ;

-

(ii)

is the generated policy from a ;

-

(iii)

is the possible PII measure whose DC triplet equals ;

-

(iv)

is a saddle point of global kernel ;

-

(v)

the value function is

Proof.

Theorem 3.1 shows that a saddle point of the global kernel can generate a saddle point of objective function, that is, a solution of the robust consumption-investment problem. Also, the value function is expressed by the value of at saddle point. In general, a robust stochastic control can be solved by an auxiliary deterministic minimax problem, which follows the deterministic-to-stochastic paradigm and can be named as the martingale method of robust optimization.

4. CARA Utilities

In this section, we consider a family of CARA utilities:

whose domain is and parameter is positive. Because the coefficient of absolute risk aversion of (cf. Pratt (1964)) is constant, people usually regard the policy as a two-tuples , where is the amount of investment in stocks and is the amount of consumption at time , e.g., Karatzas et al. (1987), Vila and Zariphopoulou (1994), Liu (2004) and Chen et al. (2012).

Noticing CARA and CRRA utilities are both special cases of Hyperbolic absolute risk aversion (HARA) utilities, we want to use the martingale method as for CRRA utilities to solve the case of CARA utilities. For this purpose, we define a new kind of policy . Under this policy, the consumption amount per time unit is

and the dynamic of wealth process is

| (4.1) |

where is a scale coefficient about time . According to Theorem 3.1, the quantity is the optimal ratio of consumption at time for an investor with logarithmic utility so that is the excess amount of consumption compared to an investor with logarithmic utility (hereinafter referred to as the excess consumption). Proposing excess consumption contributes to a direct expression of objective function by using the policy and measure, just like Lemma 3.1. An analogous martingale equality will be established in Lemma 4.1 below.

Before this, we introduce the admissible policy set , the deterministic admissible policy set , the local kernels , and the global kernel for CARA utilities successively. The notations are same as the ones in CRRA case if there is no essential difference between them. The admissible policy set is

| (4.2) |

which has less constraints than CRRA case because the domain of CARA utility is . Indeed, the defined in Section 3 corresponds to the in (4.2). Similarly as Definitions 3.1 and 3.2, the deterministic admissible policy set is

and the way of generating an admissible policy from a deterministic admissible policy does not change.

Definition 4.1.

The local kernel (at time ) is defined by

for any and .

Definition 4.2.

The global kernel (over period ) is a two-variable function on . For any and ,

We adopt new notations for the local kernels and global kernel here because they have great differences from the CRRA case. Precisely, is a function of , that is, a function of remaining duration . It can been seen that and have similar expressions, where the , , and correspond to the , , and , respectively. Therefore, the relationship between the global kernel and the objective function for CARA utilities can be obtained by imitating the procedure in CRRA case with negative .

Lemma 4.1.

For any , ,

where is an equivalent measure whose Radon-Nikodym derivative is

Proof.

See Appendix A. ∎

Assumption 4.1.

For any ,

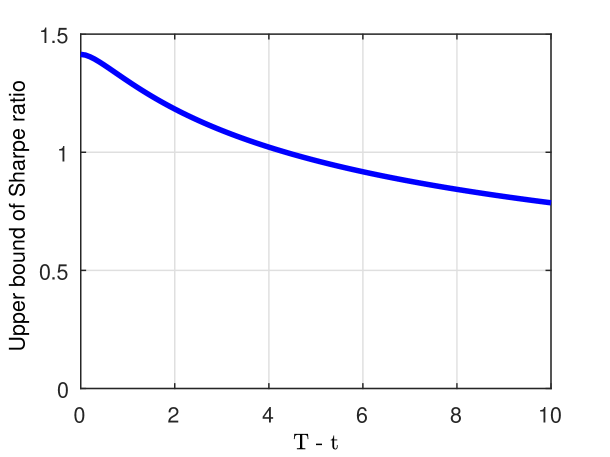

Just as Assumption 3.1 in the CRRA case, we demand Assumption 4.1 to support the main result – Theorem 4.1 for CARA utilities. Assumptions 3.1 and 4.1 both give restrictions on the Sharpe ratio but still have difference. The constraints in Assumption 3.1 vary in parameter but the constraints in Assumption 4.1 are diverse in time instead of parameter .

In Figure 2, the upper bounds for every remaining durations are depicted. It is obvious that the upper bound is decreasing with the increasing of . When , the upper bound of Sharpe ratio is about and thus the probability of a negative yield is about after a year of investment. This constraint is stricter than the condition in CRRA case but still tolerable enough for the vast majority of investment periods. Finally, we conclude this section by giving an optimal policy and a worst-case measure in the following theorem.

Theorem 4.1.

There exist an optimal policy and a worst-case model of the robust consumption-investment problem, denoted by and . Moreover,

-

(i)

is a saddle point of objective function ;

-

(ii)

is the generated policy from ;

-

(iii)

is the possible PII measure whose DC triplet equals ;

-

(iv)

is a saddle point of global kernel ;

-

(v)

the value function is

Proof.

An optimal excess consumption is given in Theorem 4.1, so an optimal amount of consumption for a CARA investor at time is

In kernel analyses, we will know is a non-negative function thus a CARA investor will consume more than a logarithmic investor if they have the same amount of wealth. Meanwhile, more consumption amount may make the wealth negative, which is acceptable for a CARA investor but intolerable for a CRRA investor.

5. Kernel Analyses

In this section, we divide the policy into two components, an investment policy and a consumption policy, for studying the relationship between global kernel and local kernels. Therefore, the global kernel can be regarded as a function with three arguments: an investment policy, a consumption policy, and a PII triplet. Meanwhile, we substitute the expressions and for and , respectively, to show and have three arguments.

The main contribution of this section is finding a saddle point of the global kernel, which can generate a saddle point of the objective function, i.e., an optimal policy and a worst-case measure of the robust consumption-investment problem (see Theorems 3.1 and 4.1). In Definitions 3.4 and 4.2, the global kernels and have similar expressions, so the procedures of finding their saddle points are similar. The difficulty comes from the fact that the global kernel is a functional defined on infinite dimensional spaces, and this difficulty is inherent and cannot be avoided because it is caused by time-varying confidence sets and intertemporal consumption. There are three steps in finding a saddle point. By proving the measurable saddle point theorem, we firstly find a deterministic admissible investment policy and a PII triplet, whose values at each time constitute a saddle point of the local kernel (cf. Theorems 5.2 and 5.6). Then we obtain the candidate policy and PII triple by defining an appropriate consumption policy. Finally, we demonstrate that the chosen policy and PII triple constitute a saddle point of the global kernel (cf. Theorems 5.4 and 5.8).

5.1. Kernel of CRRA

We implement the steps described above for CRRA utilities under Assumptions 2.2, 2.1, and 3.1. In order to regard the global kernel as a function with three variables, we rewrite its domain as

where

and

Actually, in Definition 3.1 is the Cartesian product of and .

Definition 5.1.

For any , we say if and only if

We call is greater than in the kernel order.

Theorem 5.1.

For any and ,

-

(i)

for ;

-

(ii)

for , if

Proof.

See Appendix B. ∎

A partial order called kernel order is presented in Definition 5.1, under which we can compare elements in . Based on the kernel order, Theorem 5.1 reveals the monotonicity of over . It is worth mentioning that the conditions in Theorem 5.1 for and are different because we use different techniques to overcome the difficulties encountered in the proof. Generally speaking, Assumption 3.1 overcomes the difficulty of non-positive , so we do not need to add more assumptions for the case of . For , we overcome the difficulty by verifying the monotonicity with a stronger condition, that is, in a small domain of (see Eq. (B.3) in Appendix B). Fortunately, this small domain is large enough since we can verify that any optimal policy is in this domain, that is, the optimal policy satisfies the condition for in Theorem 5.1 (cf. the proof of Theorem 5.4).

Thanks to the monotonicity of global kernel, an immediate idea of constituting a saddle point of is to piece together the saddle points of local kernels from time to . The existence of saddle points of local kernels has been studied by Neufeld and Nutz (2018), however, it is not sure whether the joint combination of saddle points of local kernels is measurable with respect to time. Following theorem answers this question mainly by using Kuratowski-Ryll-Nardzewski measurable selection theorem and measurable maximum theorem repeatedly (cf. Appendix C). Theorem 5.2 is actually a measurable saddle point theorem.

Theorem 5.2.

There exist a and a such that is a saddle point of on for every .

Proof.

For using the Kuratowski-Ryll-Nardzewski measurable selection theorem to find a measurable saddle point, it is crucial to prove and are continuous, which is provided by Lemmas C.1 and C.2 in Appendix C. In more detail, Lemma C.1 holds thanks to the assumption that is compact under with a positive . Actually, is a sufficient and necessary condition in the proof of Lemma C.1. When , defined in Lemma C.1 is not Hölder continuous for any exponent because

where is the unit vector in the direction of , is a unit vector that is orthogonal to , and is the angle between two vectors. After finding the candidates for the components of saddle point on in Theorem 5.2, we are going to find the maximizer of on , which is a deterministic optimization and can be solved by dynamic programming.

Theorem 5.3.

For any and , the maximizer of over is

| (5.1) |

The maximum value is

| (5.2) |

The range of maximizer is

| (5.3) |

where

Proof.

Theorem 5.3 shows the maximum of on is attainable for any given . In the case of logarithmic utility, is a function increasing to one and dose not depend on other arguments. For power utilities, the monotony of is unknown because the arguments and affect through the values of local kernels. Indeed, the only sure thing is attains one at the terminal time, but it can be non-monotonic. This phenomenon appears in this robust problem because the confidence sets are time-varying. In the degenerated case that is a constant correspondence, in (5.1) must be monotonically increasing or decreasing. For now, we are ready to constitute a saddle point of based on above three theorems.

Theorem 5.4.

There exist and constituting a saddle point of global kernel with following properties.

-

(i)

For any , is a saddle point of local kernel on .

-

(ii)

For any ,

-

(iii)

The range of is

(5.4) -

(iv)

The value of global kernel at saddle point is

Proof.

Recalling the range (5.3) in Theorem 5.3, we notice that the maximizer of over can be greater than one, which means people may consume more than the total wealth instantaneously (over-consumption occurs). However, the optimal consumption ratio provided by Theorem 5.4 is not more than one according to (5.4). The over-consumption will not happen under the worst-case model because

for and given by Theorem 5.4. Actually, the first condition holds thanks to the optimality of saddle point, that is, for any and

The second one is tenable because Assumption 3.1 limits the Sharpe ratio of the market while the over-consumption only occurs in a good enough market.

5.2. Kernel of CARA

We try to find a saddle point of under Assumptions 2.2, 2.1, and 4.1 by analogous procedures as above. We denote

then and can be regarded as a function with three arguments. According to the comparison between global kernels of CARA and CRRA utilities in Section 4, the procedures of analyzing should be similar to with negative . So we omit the proofs in the following theorems and simply state the main ideas. Besides, it will be easier to understand them while comparing them with the conclusions about .

Definition 5.2.

For any , we say if and only if

We call is greater than in the kernel order.

Theorem 5.5.

For any , and ,

Proof.

Theorem 5.6.

There exist a and a such that is a saddle point of over for every .

Proof.

The main tools are Kuratowski-Ryll-Nardzewski measurable selection theorem and measurable maximum theorem as in the proof of Theorem 5.2. A subset of should be proposed as to avoid the singularity of local kernel for any . ∎

Thanks to the monotonicity of described in Theorem 5.5, the and selected in Theorem 5.6 are the candidates for the components of ’s saddle point. Then we study the maximizer of over for any given and .

Theorem 5.7.

For any and , the maximizer of over is

| (5.5) |

The maximum value is

| (5.6) |

Proof.

It not difficult to realize the procedure of proving Theorem 5.7 is analogous to Theorem 5.3, but we still show the details in Appendix D because the associated HJB equations have different forms.

Theorem 5.8.

There exist and constituting a saddle point of global kernel with following properties.

-

(i)

For any , is a saddle point of local kernel over .

-

(ii)

For any ,

-

(iii)

The value of global kernel at saddle point is

Proof.

In Definition 4.1, the function depends on the time , thus is time-dependent even though the confidence set keeps constant. This is an explanation of why CARA investors are not myopic from a mathematical point of view. By the optimality of saddle point, we have

which means is a non-negative function.

6. Conclusion

The main contribution of this paper is solving the robust consumption-investment problem in the market with jumps by martingale method. Conceptually, the uncertainty set consists of all the semimartingale measures, under which the DC triplet of the log-price processes is a PII triplet (measurable selector from the correspondence ) almost surely. Under this framework, the instantaneous confidence sets of all possible Lévy triplets are time-varying, which causes mensurability problems.

Thanks to the well-defined policy for each utility, the martingale equality describes the relationship between the objective function and global kernel, which is the core in the deterministic-to-stochastic paradigm. Thus the robust consumption-investment problem can be solved by finding a saddle point of the global kernel. However, it is difficult to find a measurable saddle point of the global kernel, because the confidence set is time-varying and the global kernel is a functional. Fortunately, while regarding the global kernel as a function with three arguments — an investment policy, a consumption policy, and a DC triplet, we obtain two essential conclusions . For fixed consumption policy, the global kernel is an increasing functional under the kernel order; for fixed investment policy and DC triplet, an optimal consumption policy can be explicitly expressed. Synthesizing these two conclusions, a saddle point of the global kernel can be found by the measurable saddle point theorem.

For a CRRA investor, the choices of optimal investment policy and worst-case differential characteristics are both myopic, uniquely determined by the instantaneous local kernel, i.e., the instantaneous model of the market. Thus, the optimal portfolio is changeless if the confidence set is constant. However, the time effect appears for CARA investors. The optimal investment policy and the worst-case differential characteristics are influenced by the remaining duration as well as the instantaneous model. Besides, the optimal consumption policy is non-myopic for any utilities and is affected by both local kernels and remaining duration.

Appendix A Proofs of Lemma 3.1, Theorem 3.1, and Lemma 4.1

Proof of Lemma 3.1. By (2.5), (3.2), and Itô’s formula for jump processes (cf. Øksendal and Sulem (2005)), we have

| (A.1) | ||||

for any . Take expectation on both sides of (A.1), then

and

This is the result for logarithmic utility (). Next we use the expansion of in (A.1) to expand as a product. For any ,

Proof of Theorem 3.1. is a saddle point of by Theorem 5.4, so we mainly verify the defined by conditions and is a saddle point of . We only show the details for power utility here, because the proof for power utility is more general than the logarithmic utility.

For any , using Lemma 3.1, we have

| (A.3) | ||||

where the second equality holds because is independent of the probability space for a possible PII measure in . Because is constant and Lemma 3.1 holds,

| (A.4) | ||||

where is the generated policy from according to Definition 3.2. By (A.3), (A.4), noting is arbitrary and is ’s saddle point, we conclude that

On the other hand,

| (A.5) | ||||

The second equality holds because there is a bijection between and . The third holds because is independent of the probability space for any possible PII measure . The last equality comes from Lemma 3.1. The first inequality holds because almost surely. The second inequality holds since contains . By (A.4), (A.5), and the property of saddle point, we obtain

Appendix B Proofs of Theorems 5.1 and 5.4

Proof of Theorem 5.1. The proof is divided into three cases: , and . Case 1: . For logarithmic utility, and are separate in the expression of , i.e.,

thus,

Case 2: . For any , let , thus according to . We use variational method here. For any , let

The derivative of is

Using Assumption 3.1 and noticing , we know for any and ,

| (B.1) |

Above estimation still holds for as well as . By , we get

which leads to directly. Thus , i.e., . Case 3: . We use the same notations as in case 2, while more constraints are given as follows:

Because and for any , we have

Proof of Theorem 5.4. It is sufficient to prove

where and are selected in Theorem 5.2 and is defined by condition in Theorem 5.4. To do this, we calculate

respectively. We firstly give two notations. For any , is a PII triplet that satisfies

For any , is an investment policy that satisfies

They both exist according to Lemmas C.3 and C.4. By the property of saddle point,

| (B.2) |

Step 1: Calculating .

It is easy to verify that the in Eq. (5.2) is increasing in the kernel order. Thus, following equalities hold by using Theorem 5.3 and Eq. (B.2).

and

Step 2: Calculating .

The calculation for is straightforward as in Step 1, while the case of is complicated. Case 1: . By Theorem 5.1, Eq. (B.2), and Theorem 5.3,

Case 2: . Firstly, we assert the value of does not change if we restrict the sets as

| (B.3) |

For any and satisfying

define

then and . By Theorem 5.3,

because is increasing in the kernel order. Therefore, we can restrict as

According to , Theorem 5.3, and (B.1) for negative , the optimal must take value in , thus we can further restrict the control set as (B.3). Finally, we calculate on the restricted control set (B.3).

Appendix C Proof of Theorem 5.2

Recalling the integral in the expression of the local kernel (cf. Definition 3.3), we notice its integrand contains , whose value or derivative approaches infinite when approaches . Thus, to avoid the singularity of local kernel near the boundary of , we consider the following closed subsets of for any and :

thus . Since is bounded by , is bounded too. We only write the proof for here because it is similar and easier for .

Lemma C.1.

For any and , define

then is continuous and there exists a constant such that

| (C.1) |

| (C.2) |

and

| (C.3) |

Proof.

We assume is a closed and convex set containing the origin, because we can substitute for without changing . The continuity on is obvious, so we only need to verify

which is ensured by the following two results:

Thus, is continuous and bounded by the compactness of , which is equivalent to (C.3). Moreover, we can show is continuous and bounded too. For convenience, we assume they are bounded by a common constant depending on and .

For verifying the -Hölder continuity of with respect to , we firstly study its property on a neighborhood of origin:

for . By Taylor’s theorem with Lagrange remainder, for any , we have

where is the cosine of the angle between and , and is a real number between and . Since , the first term is -Hölder continuous with respect to . Since

the second term is Lipschitz continuous with respect to . Thus, (C.1) holds for some over .

Secondly, we study the property on and . Because

and

is differentiable with bounded derivative on above tow domains. Thus is Lipschitz continuous with respect to over these two compact domains. Recalling the result on domain , we conclude that is -Hölder continuous with respect to over and the Hölder constant is independent of , which is equivalent to (C.1) for a large enough . Similarly, the Lipschitz continuity of with respect to can be proved, which is omitted here. ∎

Lemma C.2.

For any and , the map

is continuous on .

Proof.

For any and ,

By Lemma C.1, we have

Therefore, for fixed and , the family of functions

is equicontinuous and uniformly Lipschitz continuous with Lipschitz constant

under the maximum metric . Thus is continuous on . ∎

The proofs of the following two lemmas use Kuratowski-Ryll-Nardzewski measurable selection theorem and measurable maximum theorem many times, so we state them here for convenience. The details can be found in Chapter 18, Aliprantis and Border (2006).

Definition C.1 (Carathéodory function).

Let be a measurable space, and let and be topological spaces. A function is a Carathéodory function if:

-

(1)

for each , the function is -measurable; and

-

(2)

for each , the function is continuous.

Theorem C.1 (Kuratowski-Ryll-Nardzewski measurable selection theorem).

A weakly measurable correspondence with nonempty closed values from a measurable space into a Polish space admits a measurable selector.

Theorem C.2 (Measurable maximum theorem).

Let be a separable metrizable space and a measurable space. Let be a weakly measurable correspondence with nonempty compact values, and suppose is a Carathéodory function. Define the value function by , and the correspondence of maximizers by

Then:

-

(1)

The value function is measurable.

-

(2)

The argmax correspondence has nonempty and compact values.

-

(3)

The argmax correspondence is measurable and admits a measurable selector.

Lemma C.3.

There exists a such that attains the minimum of on for every .

Proof.

By Lemma C.2, the map is a Carathéodory function. Thus, for any , is measurable by the measurable maximum theorem. Referring to lemma 3.2 of Neufeld and Nutz (2018), we know

Therefore, the map

is a Carathéodory function and the correspondence

is measurable (cf. corollary 18.8, Aliprantis and Border (2006)). Since

increasingly converges to , we have

thus the correspondence

is measurable (cf. lemma 18.4, Aliprantis and Border (2006)). Finally, by Kuratowski-Ryll-Nardzewski measurable selection theorem, there exists a measurable function such that and

∎

Lemma C.4.

There exists a such that attains the maximum of on for every .

Proof.

Using (C.2) in Lemma C.1 and imitating the proof of Lemma C.2, we can prove that the map

is continuous on for any and . Similarly to the proof of Lemma C.3, the correspondence

is measurable for any , thus

is measurable as an union correspondence. It can be verified that this correspondence is nonempty by the assumption that is closed. Indeed, for any , there exists a such that

Thus, as approaches , decreases at infinite rate so that the supremum of over can be attained. Finally, by Kuratowski-Ryll-Nardzewski measurable selection theorem, a measurable exists satisfying

∎

Appendix D Proofs of Theorems 5.3 and 5.7

We firstly introduce the Lemma D.1, which is the so-called verification theorem in dynamic programming.

Lemma D.1.

For any , , and , there exists an unique function satisfying the following HJB equation:

| (D.1) |

The range of is , where

and

| (D.2) |

and

| (D.3) |

Especially, is the upper bound of over , i.e.,

Proof.

There are three parts in this proof. The first part proves that any solution of HJB equation (D.1) takes value in . The second part shows the existence and uniqueness by Picard-Lindelöf theorem. The third part verifies that is the upper bound.

Boundary. If is a solution of HJB equation in , we assert

If not, there exists such that , thus . This contradicts to the continuity of on . Therefore, attains the supremum of and the HJB equation (D.1) becomes

where . By the knowledge of dynamical system, it is sufficient to verify the following two inequalities for demonstrating that is the range of :

They can be easily verified when and are defined by (D.2) and (D.3) respectively.

Existence and uniqueness. By the Picard-Lindelöf theorem, we only need to show is Lipschitz continuous on . Noticing is Lipschitz continuous in the domain that avoids the singular point , we can conclude is Lipschitz continuous because the interval , which is defined by (D.2) and (D.3), strictly avoids .

Upper bound. For any , by Newton-Leibniz formula and ,

| (D.4) | ||||

Due to the arbitrariness of , we conclude . ∎

In above lemma, we do not prove a corresponding conclusion for the logarithmic utility (), because the variational method is enough for logarithmic utility. See the following proof.

Proof of Theorem 5.3. This proof has two steps. The first step is demonstrating the optimality of , and the second step is estimating the range of .

Step 1: Optimality. We use different approaches to demonstrate the optimality for logarithmic utility and power utility. The variational method solves the case of , while the dynamic programming works for .

Case 1: . For any , let be the variation. For any ,

For any positive or negative , notice

thus .

Case 2: . Lemma D.1 shows that is a upper bound of over . So it is sufficient to verify , where is defined by (5.1). Because attains the supremum in HJB equation (D.1), we substitute into (D.1) and get

This is a Riccati equation and is the unique solution. Since satisfies , the inequality in (D.4) becomes an equality, i.e.,

Step 2: Boundary. The range (5.3) of could be immediately obtained by (D.2) and (D.3), once noticing is decreasing with respect to for and increasing for .

Lemma D.2.

For any and , there exists an unique satisfying the following HJB equation:

| (D.5) |

The range of is , where

and

| (D.6) |

and

| (D.7) |

Especially, is the upper bound of global kernel over , i.e.,

Proof.

Same as Lemma D.1, this proof also has three parts.

Boundary. If is the solution of HJB equation in , we assert for any . If not, there exists satisfying , thus . This contradicts to the continuity of on . Therefore, is well-defined and attains the supremum of . The HJB equation (D.5) becomes

where . By the knowledge of dynamical system, it is sufficient to verify the following two inequalities for demonstrating that is the range of :

Existence and uniqueness. By the Picard-Lindelöf theorem, the conclusion holds because is Lipschitz continuous on .

Upper bound. For any , by Newton-Leibniz formula and ,

| (D.8) | ||||

By the arbitrariness of , we conclude ∎

Proof of Theorem 5.7. Lemma D.2 gives an upper bound of over . Thus we only need to verify where is defined by (5.5). Recalling attains the supremum in HJB equation (D.5) and substituting into (D.5), we obtain

defined in (5.5) is exactly the unique solution. Because satisfies

we conclude that by (D.8).

Acknowledgements. The authors acknowledge the support from the National Natural Science Foundation of China (Grant No.11471183, No.11871036). The authors also thank the members of the group of Insurance Economics and Mathematical Finance at the Department of Mathematical Sciences, Tsinghua University for their feedbacks and useful conversations.

References

- [1] Aliprantis, C. D., and Border, K. C. (2006). Infinite Dimensional Analysis: A Hitchhiker’s Guide. Springer.

- [2] Artzner, P., Delbaen, F., Eber, J. M., and Heath, D. (1999). Coherent measures of risk. Mathematical finance, 9(3), 203–228.

- [3] Benth, F. E., Karlsen, K. H., and Reikvam, K. (2010). Merton’s portfolio optimization problem in a black and scholes market with non-gaussian stochastic volatility of ornstein-uhlenbeck type. Mathematical Finance, 13(2), 215–244.

- [4] Biagini, S., and Pınar, M. Ç. (2017). The robust Merton problem of an ambiguity averse investor. Mathematics and Financial Economics, 11(1), 1–24.

- [5] Bogachev, V. I. (2007). Measure theory, vol II. Springer Science & Business Media.

- [6] Cox, J. C., Huang, C. F. (1989). Optimal consumption and portfolio policies when asset prices follow a diffusion process. Journal of Economic Theory. 49(1), 33–83 .

- [7] Chen, Y., Dai, M., and Zhao, K. (2012). Finite horizon optimal investment and consumption with CARA Utility and proportional transaction costs, Stochastic Analysis and its Applications to Mathematical Finance, Essays in Honour of Jia-an Yan, Eds. T. Zhang and X. Y. Zhou, World Scientific, 39–54.

- [8] Chen, Z., and Epstein, L. (2010). Ambiguity, risk, and asset returns in continuous time. Econometrica, 70(4), 1403–1443.

- [9] Denis, L., and Kervarec, M. (2013). Optimal investment under model uncertainty in nondominated models. SIAM Journal on Control and Optimization, 51(3), 1803–1822.

- [10] Epstein, L. G., and Ji, S. (2014). Ambiguous volatility, possibility and utility in continuous time. Journal of Mathematical Economics, 50(1), 269–282.

- [11] Foldes, L. (1990). Conditions for optimality in the infinite-horizon portfolio-cum-saving problem with semimartingale investments. Stochastics & Stochastics Reports, 29(1), 133–170.

- [12] Frazzini, A., Kabiller, D., and Pedersen, L. H. (2013). Buffett’s alpha. National Bureau of Economic Research.

- [13] Fouque, J. P., Pun, C. S., and Wong, H. Y. (2016). Portfolio optimization with ambiguous correlation and stochastic volatilities. SIAM Journal on Control and Optimization, 54(5), 2309–2338.

- [14] Golub, G. H., and Van Loan, C. F. (2012). Matrix computations (Vol. 3). JHU Press.

- [15] Jacod, J., and Shiryaev, A. N. (2013). Limit theorems for stochastic processes. Springer Science & Business Media.

- [16] Kallsen, J. (2000). Optimal portfolios for exponential Lévy processes. Mathematical Methods of Operations Research, 51(3), 357–374.

- [17] Kallsen, J., and Muhle-Karbe, J. (2010). Utility maximization in affine stochastic volatility models. International Journal of Theoretical and Applied Finance, 13(03), 459–477.

- [18] Karatzas, I., and Kardaras, C. (2007). The numéraire portfolio in semimartingale financial models. Finance and Stochastics, 11(4), 447–493.

- [19] Karatzas, I., Lehoczky, J. P., and Shreve, S. E. (1987). Optimal portfolio and consumption decisions for a ”small investor” on a finite horizon. SIAM Journal on Control and Optimization, 25(6), 1557–1586.

- [20] Liu, H. (2004). Optimal consumption and investment with transaction costs and multiple risky assets. The Journal of Finance, 59(1), 289–338.

- [21] Lin, Q., and Riedel, F. (2014). Optimal consumption and portfolio choice with ambiguity. Institute of Mathematical Economics Working Paper No. 497. Available at SSRN: https://ssrn.com/abstract=2377452 or http://dx.doi.org/10.2139/ssrn.2377452

- [22] Merton, R. C. (1969). Lifetime portfolio selection under uncertainty: the continuous-time case. Review of Economics & Statistics, 51(3), 247–257.

- [23] Merton, R. C. (1971). Optimum consumption and portfolio rules in a continuous-time model. Journal of Economic Theory, 3(4), 373–413.

- [24] Neufeld, A., Nutz, M. (2014). Measurability of semimartingale characteristics with respect to the probability law. Stochastic Processes & Their Applications. 124(11), 3819–3845.

- [25] Neufeld, A., and Nutz, M. (2018). Robust utility maximization with Lévy processes. Mathematical Finance, 28(1), 82-105.

- [26] Nutz, M. (2010). The opportunity process for optimal consumption and investment with power utility. Mathematics and Financial Economics, 3(3), 139–159.

- [27] Nutz, M. (2012). Power utility maximization in constrained exponential Lévy models. Mathematical Finance, 22(4), 690–709.

- [28] Nutz, M. (2016). Utility maximization under model uncertainty in discrete time. Mathematical Finance, 26(2), 252–268.

- [29] Øksendal, B. K., Sulem, A. (2005). Applied stochastic control of jump diffusions. Springer.

- [30] Peng, S. (2007). G-expectation, G-Brownian motion and related stochastic calculus of Itô type. In Stochastic analysis and applications. Springer, Berlin, Heidelberg, 541–567.

- [31] Peng, S. (2010). Nonlinear expectations and stochastic calculus under uncertainty. arXiv preprint arXiv:1002.4546.

- [32] Pratt, J. W. (1964). Risk aversion in the small and in the large. Econometrica, 32(2), 122–136.

- [33] Sato, K. (1999). Lévy processes and infinitely divisible distributions. Cambridge University Press.

- [34] Schied, A. (2008). Robust optimal control for a consumption-investment problem. Mathematical Methods of Operations Research, 67(1), 1–20.

- [35] Shapiro, A., and Uğurlu, K. (2016). Decomposability and time consistency of risk averse multistage programs. Operations Research Letters, 44(5), 663–665.

- [36] Sion, M. (1958). On general minimax theorems. Pacific Journal of Mathematics, 8(1), 171–176.

- [37] Stoikov, S. F., and Zariphopoulou, T. (2005). Dynamic asset allocation and consumption choice in incomplete markets. Australian Economic Papers, 44(4), 414–454.

- [38] Talay, D., and Zheng, Z. (2002). Worst case model risk management. Finance and Stochastics, 6(4), 517–537.

- [39] Tevzadze, R., Toronjadze, T., and Uzunashvili, T. (2013). Robust utility maximization for a diffusion market model with misspecified coefficients. Finance and Stochastics, 17(3), 535–563.

- [40] Uğurlu , K. (2017a). Controlled markov chains with AVaR criteria for unbounded costs. Journal of Computational and Applied Mathematics, 319, 24–37.

- [41] Uğurlu , K. (2017b). Robust Merton problem with time varying nondominated priors. Available at www.optimization-online.org/DB_HTML/2017/06/6059.html

- [42] Uğurlu, K. (2018). Robust optimal control using conditional risk mappings in infinite horizon. Journal of Computational and Applied Mathematics, 344, 275–287.

- [43] Vila, J. L., and Zariphopoulou, T. (1994). Optimal consumption and portfolio choice with borrowing constraints. Journal of Economic Theory, 77(2), 402–431.